Embed Size (px)

Citation preview

Farmland Values and

Collateral Risk Guidance December 9 2010December 9, 2010

Robert Coleman, Director and Chief Examiner

Office of Examination

Dr. John Moore Chief Economist

Office of Regulatory Policy

Agendag

¾Farm real estate price and debt trends ¾Drivers and risks for farm real estate ¾FCA collateral risk guidance¾FCA collateral risk guidance ¾Future activities

2

t t

Long-Term National Trend in F R l E P iFarm Real Estate Prices 2,500

Nominal and Inflation Adjusted Values of US Farm Real Estate

2,000

3.1 % increase in USDA 2011 Forecast

1,500

er acre

1981‐82 Price Peak 71% Rise 1/03‐1/08

500

1,000

Dollars

p

0

1970 1975 1980 1985 1990 1995 2000 2005 2010

Values on January 1st

106% Rise 1976‐81

3

1970 1975 1980 1985 1990 1995 2000 2005 2010

Inflation Adjusted Values Nominal Values Source: FCA/ORP chart derived from USDA data. GDP Deflator 2005=100.

-

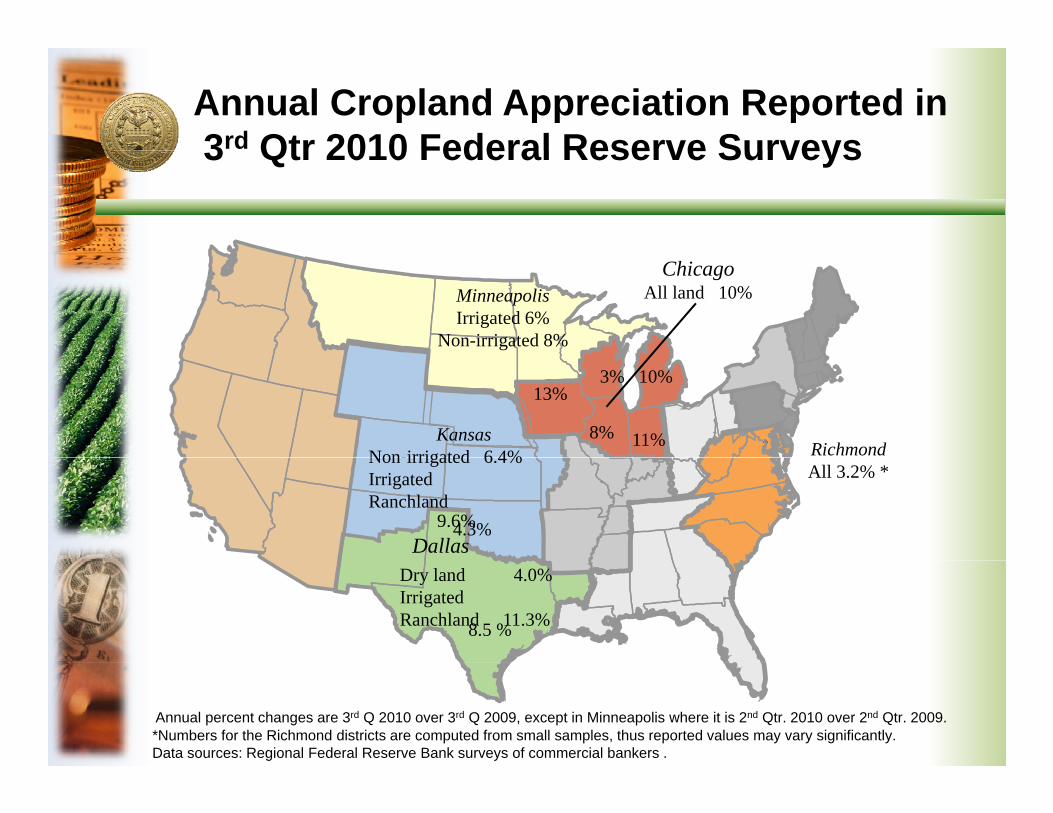

Annual Cropland Appreciation Reported in 3rd Qtr 2010 Federal Reserve Surveys 3 Qtr 2010 Federal Reserve Surveys

Chicago Minneapolis All land 10% Irrigated 6%

Non-irrigated 8%

3% 10% 13%

Kansas Non-irrigated 6 4% Non irrigated 6.4% Irrigated

9.6%

8% 11% Richmond All 3.2% *

Ranchland 4.3%

Dallas Dry land 4.0% Irrigated

8.5 % Ranchland 11.3%

Annual percent changes are 3rd Q 2010 over 3rd Q 2009, except in Minneapolis where it is 2nd Qtr. 2010 over 2nd Qtr. 2009. *Numbers for the Richmond districts are computed from small samples, thus reported values may vary significantly. Data sources: Regional Federal Reserve Bank surveys of commercial bankers .

Debt Owed on Farm Real Estate

18 0 Farm Real Estate Debt‐to‐Asset Ratio or Leverage Ratio

14.0

16.0

18.0 Total farm real estate debt / total value of farm real estate on sector balance sheet

12.9

9.610.0

12.0

7.4

6.0

8.0

0 0

2.0

4.0

Note: this measure includes all farm real estate, regardless of whether debt is owed. Source: FCA/ORP chart derived from USDA data. 5

0.0

1970 1975 1980 1985 1990 1995 2000 2005 2010F

Red = land price decline periods

December 31st of each year

Perccen

t

Concentration of System Real Estate Debt by State as of September 30 2010by State as of September 30, 2010

Total Outstanding System Real Estate Volume $73.1 billion

6

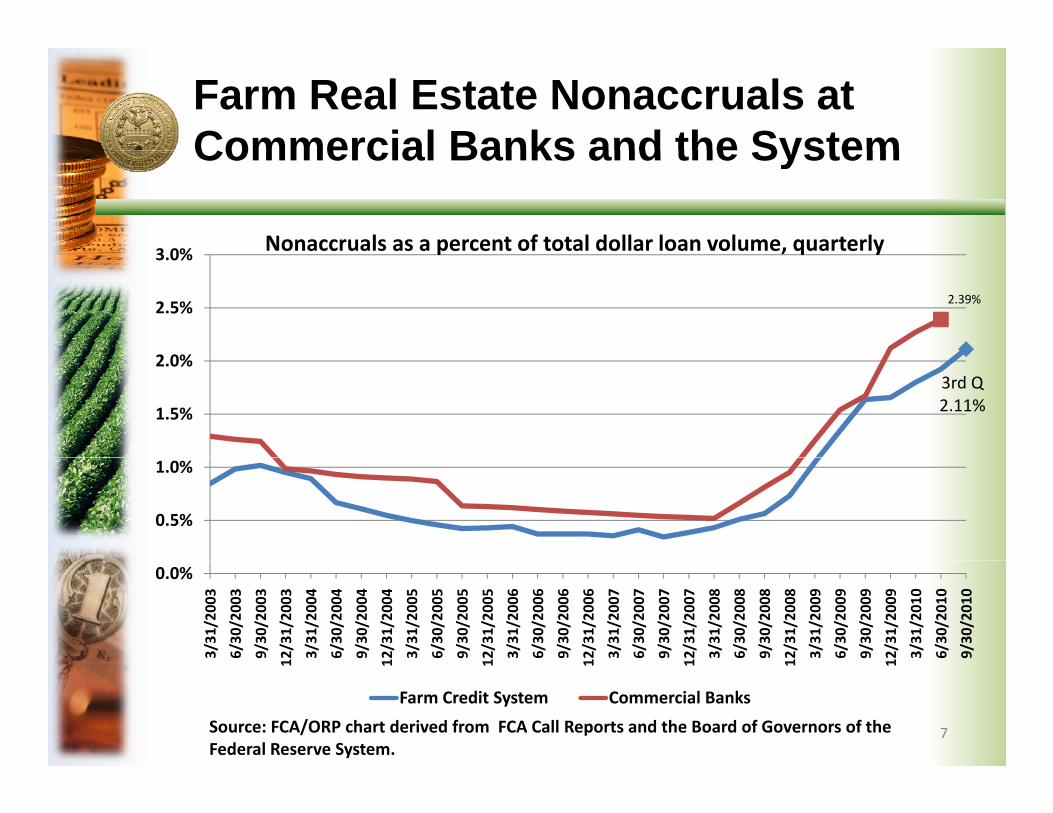

Farm Real Estate Nonaccruals at Commercial Banks and the SystemCommercial Banks and the System

3 0% Nonaccruals as a percent of total dollar loan volume, quarterly

2.39%

2 0%

2.5%

3.0% p , q y

3rd Q 2.11%1.5%

2.0%

0.5%

1.0%

0.0%

3/31/2003

6/30/2003

9/30/2003

12/31/2003

3/31/2004

6/30/2004

9/30/2004

12/31/2004

3/31/2005

6/30/2005

9/30/2005

12/31/2005

3/31/2006

6/30/2006

9/30/2006

12/31/2006

3/31/2007

6/30/2007

9/30/2007

12/31/2007

3/31/2008

6/30/2008

9/30/2008

12/31/2008

3/31/2009

6/30/2009

9/30/2009

12/31/2009

3/31/2010

6/30/2010

9/30/2010

7Source: FCA/ORP chart derived from FCA Call Reports and the Board of Governors of the Federal Reserve System.

1 1 1 1 1 1 1

Farm Credit System Commercial Banks

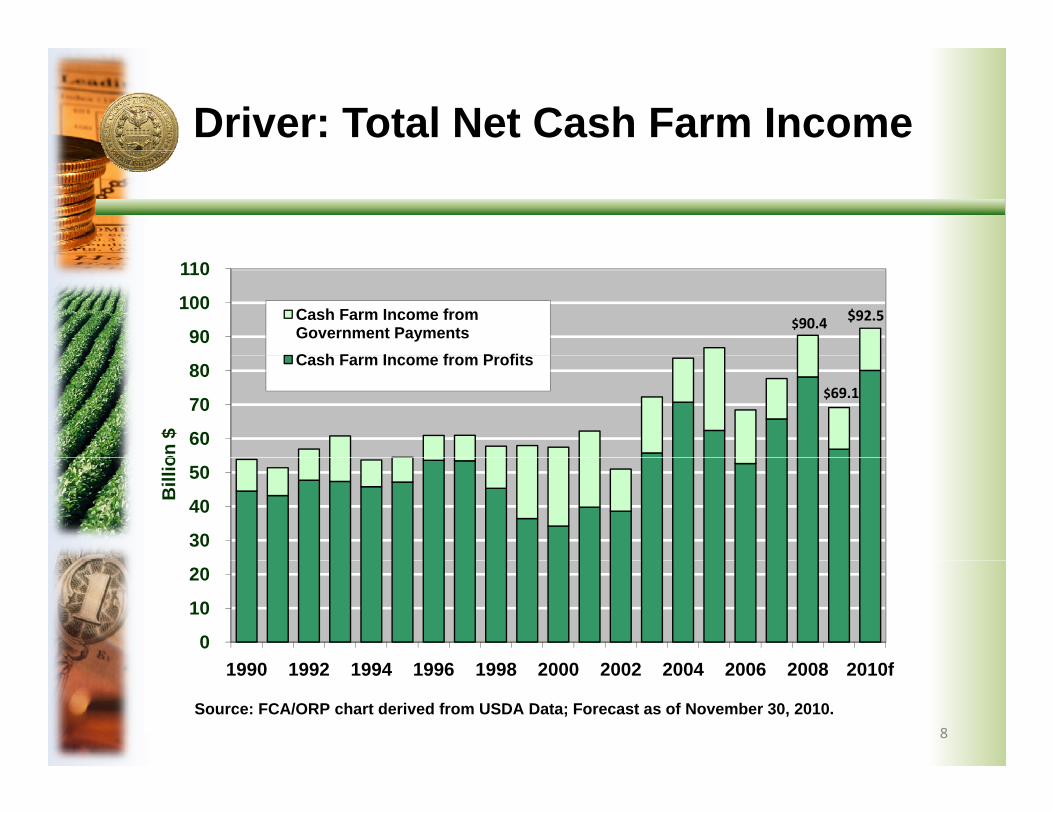

Driver: Total Net Cash Farm Income

90

100

110

Cash Farm Income from Government Payments C h F I f P fit

$90.4 $92.5

60

70

80

on $

Cash Farm Income from Profits

$69.1

30

40

50

Bill

io

0

10

20

1990 1992 1994 1996 1998 2000 2002 2004 2006 2008 2010f1990 1992 1994 1996 1998 2000 2002 2004 2006 2008 2010f

Source: FCA/ORP chart derived from USDA Data; Forecast as of November 30, 2010. 8

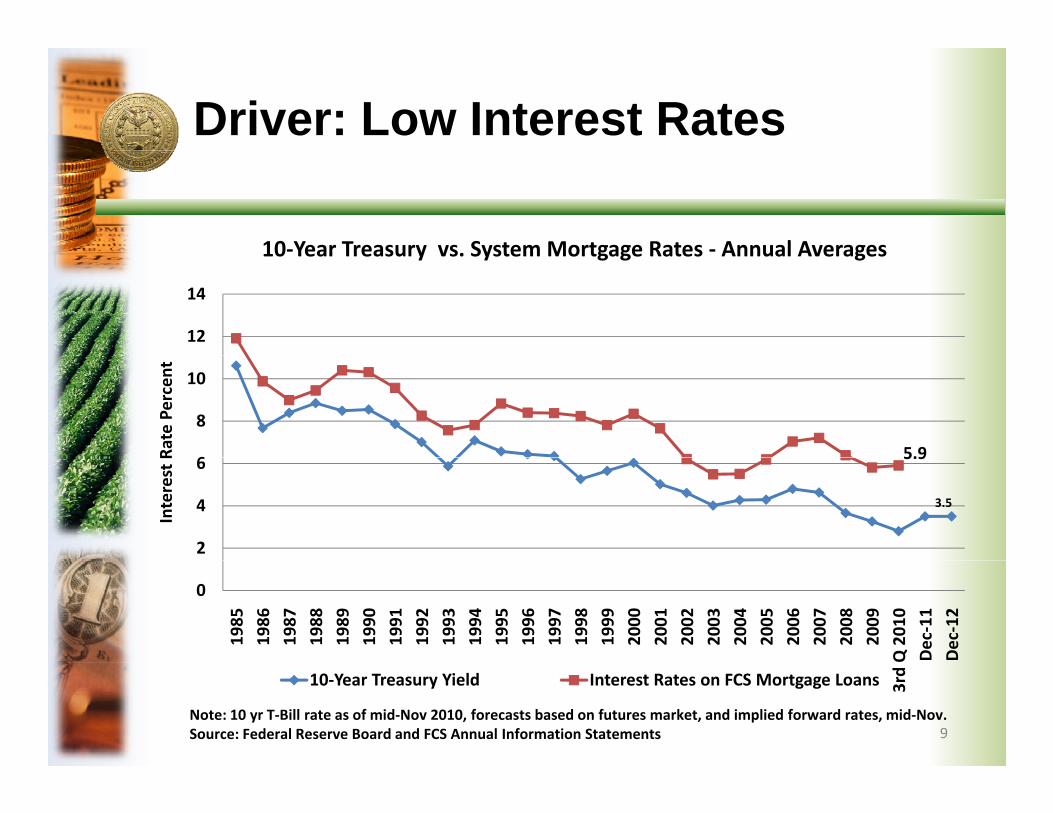

Driver: Low Interest Rates

10‐Year Treasury vs. System Mortgage Rates ‐ Annual Averages

5.9

3.5

5.9

10 Year Treasury vs. System Mortgage Rates Annual Averages

Interest

RRate Pe

rcen

t

14

12

10

8

66

4

2

0

1985

1986

1987

1988

1989

1990

1991

1992

1993

1994

1995

1996

1997

1998

1999

2000

2001

2002

2003

2004

2005

2006

2007

2008

2009

Q 2010

Dec‐11

Dec‐12

9

3rd 10‐Year Treasury Yield Interest Rates on FCS Mortgage Loans

Note: 10 yr T‐Bill rate as of mid‐Nov 2010, forecasts based on futures market, and implied forward rates, mid‐Nov. Source: Federal Reserve Board and FCS Annual Information Statements

This National Level Indicator does Not Sh E id f R t B bblShow Evidence of a Recent Bubble

Market Value of U.S. Farm Real Estate Divided by its Capitalized Value y p

3.5

4.0

4.5 1981 Peak in Land Values

A ratio significantly above 1.0 suggests that land prices may not be supported by returns

Ratio

2.5

3.0

may not be supported by returns.

Ratio = national average farmland price divided by Cap. value. Cap. value = 3‐year averages of net farm income plus

t t t l dl d di id d b th R

1.0

1.5

2.0 net rent to landlords divided by the annualized rate on 10‐year Treasury Notes.

0.0

0.5

1970 1975 1980 1985 1990 1995 2000 2005

10

1970 1975 1980 1985 1990 1995 2000 2005

Ratio of Market Value to Capitalized Value

Source: FCA/ORP chart derived from USDA and Federal Reserve System data.

2010F

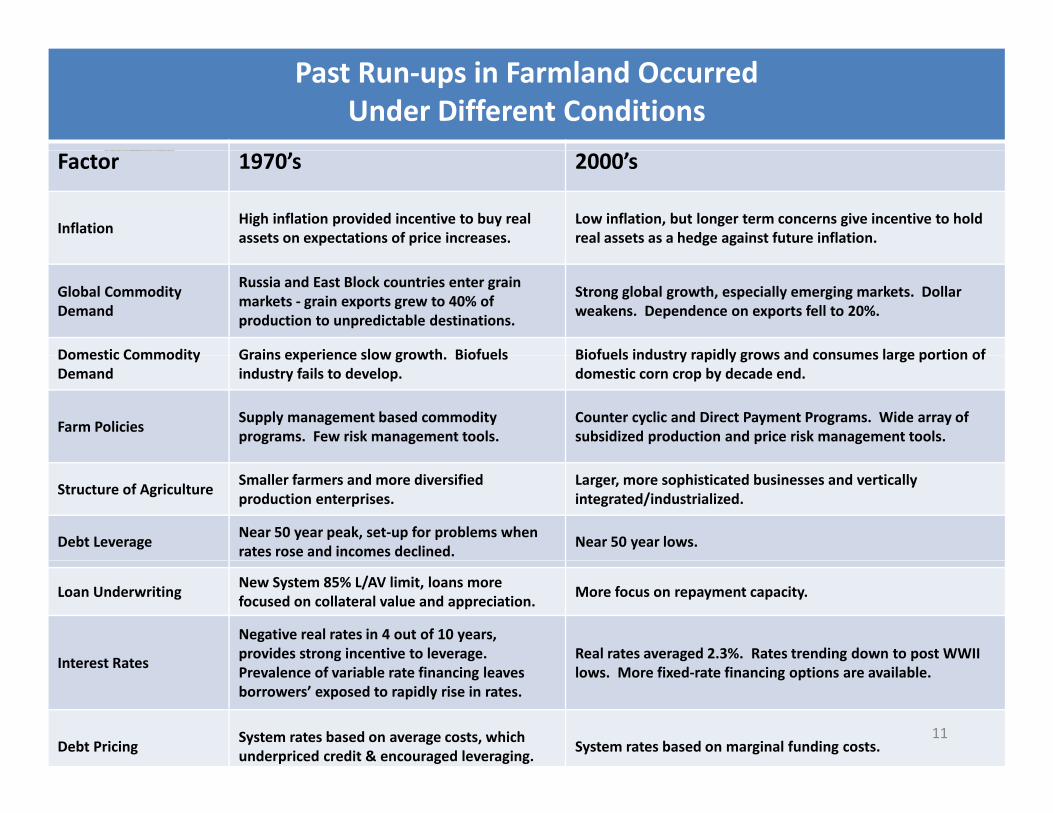

Past Run‐ups in Farmland Occurred Under Different Conditions

Factor 1970’s 2000’s

Inflation High inflation provided incentive to buy real assets on expectations of price increases.

Low inflation, but longer term concerns give incentive to hold real assets as a hedge against future inflation.

Global Commodity Demand

Russia and East Block countries enter grain markets ‐ grain exports grew to 40% of production to unpredictable destinations.

Strong global growth, especially emerging markets. Dollar weakens. Dependence on exports fell to 20%.

Domestic Commodity Grains experience slow growth Biofuels Biofuels industry rapidly grows and consumes large portion of Domestic Commodity Demand

Grains experience slow growth. Biofuels industry fails to develop.

Biofuels industry rapidly grows and consumes large portion of domestic corn crop by decade end.

Farm Policies Supply management based commodity programs. Few risk management tools.

Counter cyclic and Direct Payment Programs. Wide array of subsidized production and price risk management tools.

Structure of Agriculture Smaller farmers and more diversified production enterprises.

Larger, more sophisticated businesses and vertically integrated/industrialized.

Debt Leverage Near 50 year peak, set‐up for problems when rates rose and incomes declined.

Near 50 year lows.

Loan Underwriting New System 85% L/AV limit, loans more focused on collateral value and appreciation.

More focus on repayment capacity.

Interest Rates

Negative real rates in 4 out of 10 years, provides strong incentive to leverage. Real rates averaged 2.3%. Rates trending down to post WWII

Interest Rates Prevalence of variable rate financing leaves borrowers’ exposed to rapidly rise in rates.

lows. More fixed‐rate financing options are available.

Debt Pricing System rates based on average costs, which underpriced credit & encouraged leveraging.

System rates based on marginal funding costs. 11

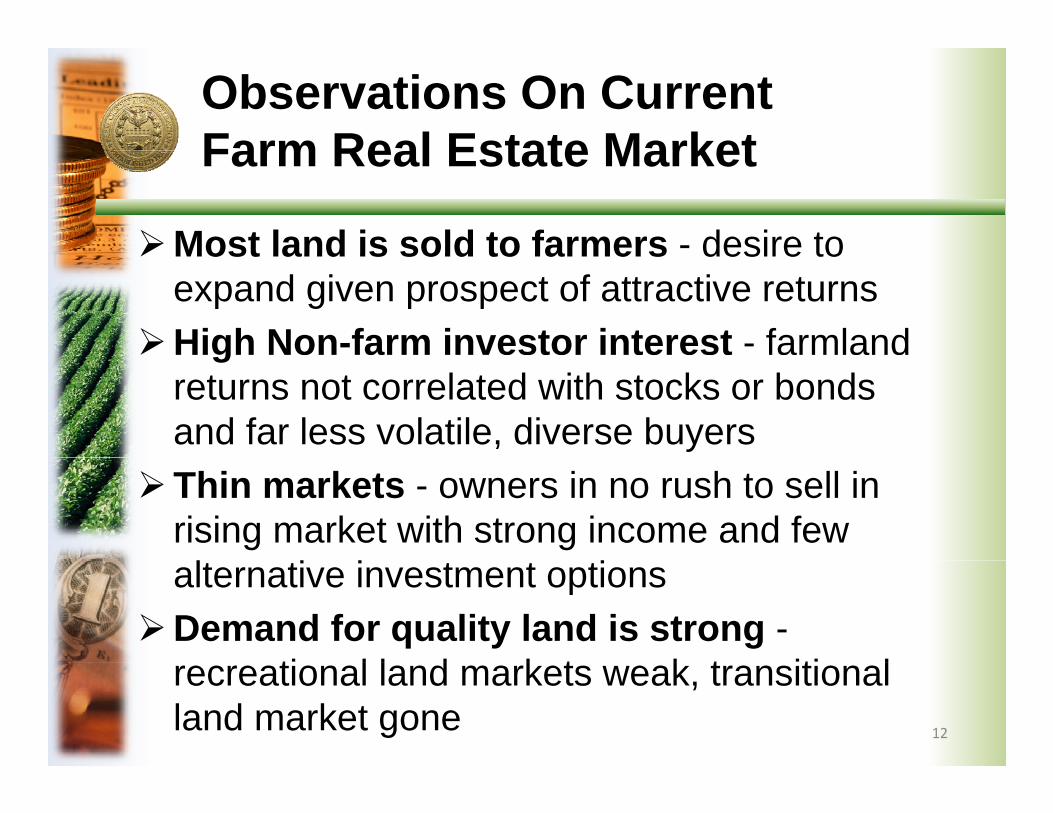

Observations On Current Farm Real Estate MarketFarm Real Estate Market

¾Most land is sold to farmers - desire to ¾Most land is sold to farmers desire to expand given prospect of attractive returns ¾High Non-farm investor interest - farmland g

returns not correlated with stocks or bonds and far less volatile, diverse buyers ¾Thin markets - owners in no rush to sell in

rising market with strong income and few l i i ialternative investment options

¾Demand for quality land is strong -ti l l d k t k t iti lrecreational land markets weak, transitional

land market gone 12

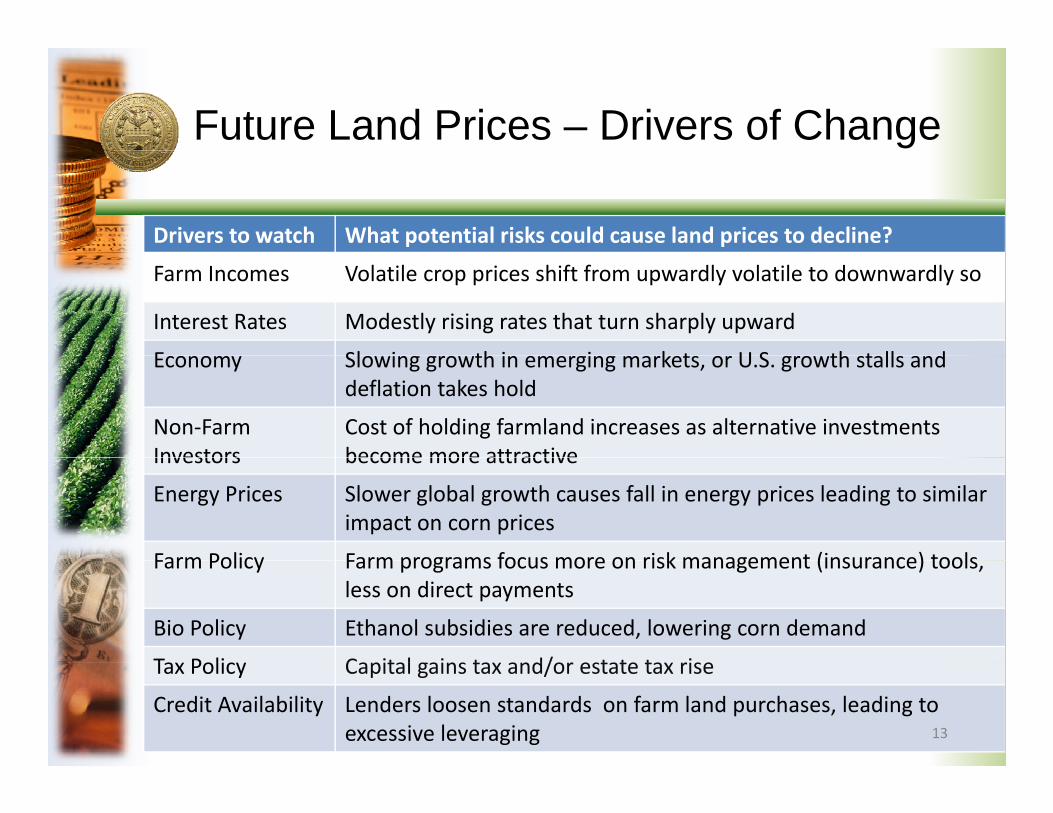

Future Land Prices – Drivers of Change

Drivers to watch What potential risks could cause land prices to decline?

Farm Incomes Volatile crop prices shift from upwardly volatile to downwardly so

Interest Rates Modestly rising rates that turn sharply upward

E Sl i th i i k t U S th t ll dEconomy Slowing growth in emerging markets, or U.S. growth stalls and deflation takes hold

Non‐Farm Investors

Cost of holding farmland increases as alternative investments become more attractive Investors become more attractive

Energy Prices Slower global growth causes fall in energy prices leading to similar impact on corn prices

Farm Policy Farm programs focus more on risk management (insurance) tools Farm Policy Farm programs focus more on risk management (insurance) tools, less on direct payments

Bio Policy Ethanol subsidies are reduced, lowering corn demand

Tax Policy Capital gains tax and/or estate tax rise Tax Policy Capital gains tax and/or estate tax rise

Credit Availability Lenders loosen standards on farm land purchases, leading to excessive leveraging 13

¾

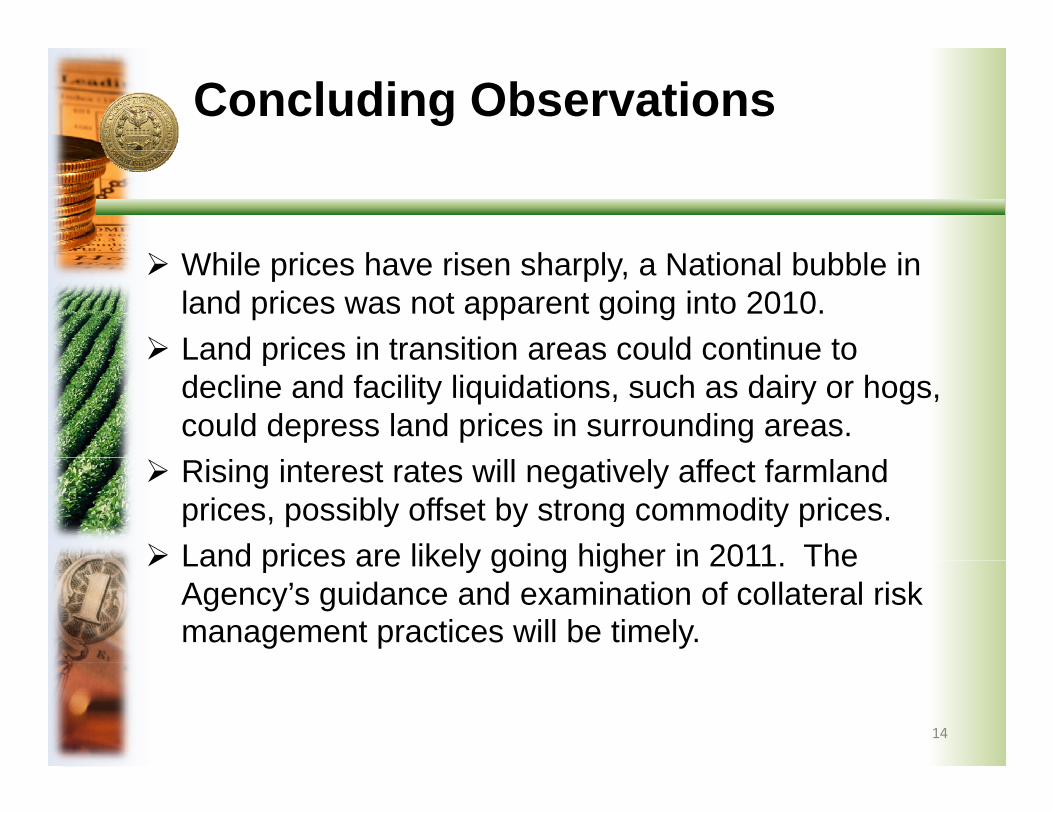

Concluding Observations

Whil i h i h l N i l b bbl i¾ While prices have risen sharply, a National bubble in land prices was not apparent going into 2010.

¾ Land prices in transition areas could continue to¾ Land prices in transition areas could continue to decline and facility liquidations, such as dairy or hogs, could depress land prices in surrounding areas.

¾ Rising interest rates will negatively affect farmland prices, possibly offset by strong commodity prices.

¾ Land prices are likely going higher in 2011 The ¾ Land prices are likely going higher in 2011. The Agency’s guidance and examination of collateral risk management practices will be timely.

14

FCA Guidance on Collateral Risk Management

Robert Coleman

Director and Chief ExaminerDirector and Chief Examiner

Office of Examination

t t

FCA Collateral Risk Management GuidanceGuidance

¾FCA’s collateral risk guidance history � FCA response to the 1980s crisis –

established our collateral evaluation regulations: Section 614 (September 1994) C i li i C ll l Ri k (M h 2005 IM) � Capitalizing Collateral Risk (March 2005 IM) � Significant Asset Growth and Its Implications

(F b 2007 IM) (February 2007 IM)

16

FCA Collateral Risk Management GuidanceGuidance

¾More recent FCA guidance includes:¾More recent FCA guidance includes: � Asset Growth, Market Volatility, and Best

Practices for Fast Growing InstitutionsPractices for Fast Growing Institutions (May 2008 IM) � FCA Bookletter – BL #58 in May 2009y� Guidance for Evaluating the Safety and

Soundness of Real Estate Lending(D b 2009 E B ll ti )(December 2009 Exam Bulletin) � FCA’s Stress Testing Expectations

(March 2010 IM)(March 2010 IM)

17

FCA Collateral Risk Management GuidanceGuidance

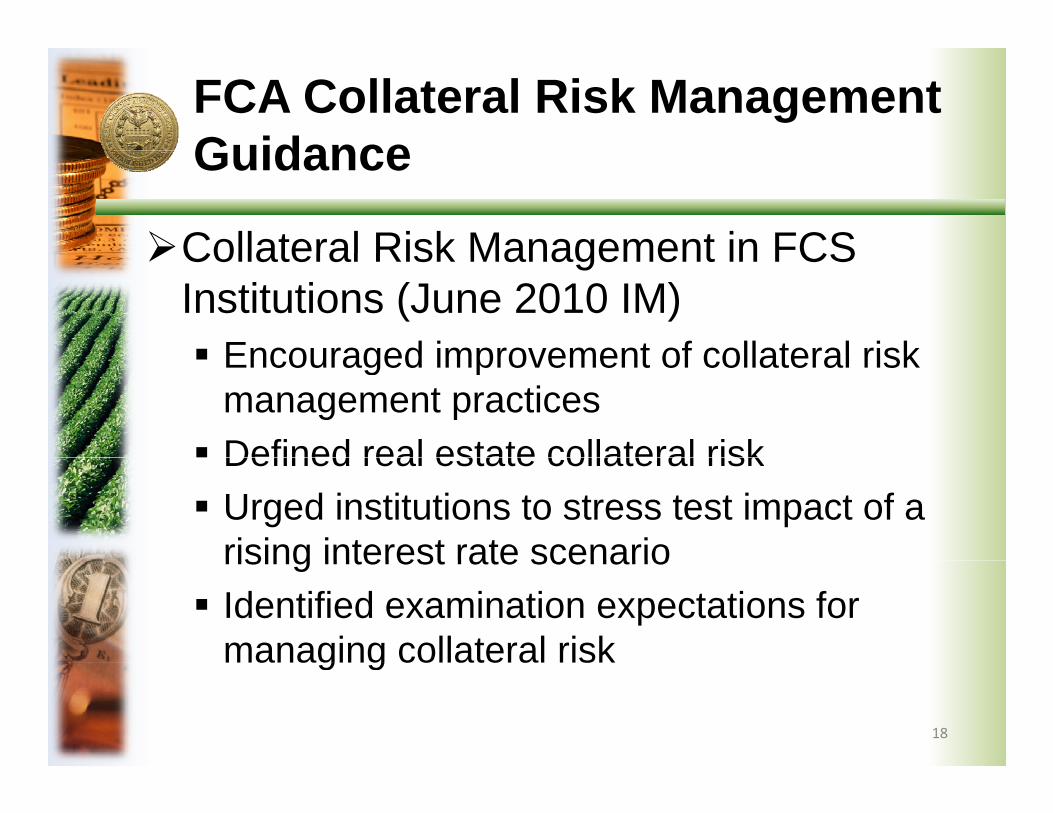

¾Collateral Risk Management in FCS¾Collateral Risk Management in FCS Institutions (June 2010 IM) � Encouraged improvement of collateral risk� Encouraged improvement of collateral risk

management practices � Defined real estate collateral riskDefined real estate collateral risk � Urged institutions to stress test impact of a

rising interest rate scenariorising interest rate scenario � Identified examination expectations for

managing collateral riskg g

18

FCA Collateral Risk Management GuidanceGuidance

¾National Oversight Plan for FY2010 and¾National Oversight Plan for FY2010 and FY2011

C ll t l Ri k M t� Collateral Risk Management 9Points to heightened collateral risk in several

stress sectors and regionsstress sectors and regions 9Need for collateral risk studies 9Monitoring and assessing collateral risk 9Adjustments made to better manage collateral

risk 9I fl l d iti d t9Influence on loan underwriting and stress

testing 19

t

Future Analyses and Monitoringy g

¾Evaluate farmland price changes ¾Continue to analyze potential impact ofy p p

changes in collateral values on the FCS ¾Examination activities to continue focus¾Examination activities to continue focus

on collateral risk management ¾More collaboration with other financial¾More collaboration with other financial

regulators ¾I lit f d ¾Improve quality of data

20