Embed Size (px)

Citation preview

FARMER ENTREPRENEURSHIP IN UGANDA

AGRI-PROFOCUS SYNTHESIS PAPER October 2009

Prepared by

Nelson F. O. Ofwono Director / Principal Consultant

Africa Services Group Ltd.

1

TABLE OF CONTENTS

ACRONYMS .......................................................................................1

Executive Summary ...........................................................................5

1. Introduction ................................................................................6

2. Status of the Agriculture Sector .....................................................6

3. Policy Framework.........................................................................9

4. Institutional Framework .............................................................. 11

5. Constraints and Challenges ......................................................... 15

6. Existing Interventions by APF Members......................................... 18

7. Emerging Issues and Development Opportunities ........................... 21

Annex 1. Strategic Choices of APF Members........................................24

Annex 2. Further Analysis.................................................................29

Annex3. Persons and Resources Consulted..........................................32

2

ACRONYMS

APF Agri-ProFocus

ASPS Agricultural Sector Programme Support

ASWG Agriculture Sector Working Group

CAADP Comprehensive Africa Agriculture Development

Programme

CDO Cotton Development Organisation

COCTU Coordinating Office for the Control of Trypanosomiasis

in Uganda

CSO Civil Society Organisations

DANIDA Danish International Development Agency

DDA Dairy Development Authority

DPs Development Partners

DSIP Development Strategy and Investment Plan

FAO Food and Agriculture Organisation

FIA Financial Institutions Act

GDP Gross Domestic Product

GOU Government of Uganda

INGO International Non Governmental Organisation

LG Local Governments

MAAIF Ministry of Agriculture, Animal Industry and Fisheries

MAPS Marketing and Agro-Processing Strategy

MDI Microfinance Deposit-Taking Institutions

MOFPED Ministry of Finance, Planning and Economic

Development

MTEF Medium Term Expenditure Framework

NAADS National Agricultural Advisory Services

3

NAGRC & DB National Animal Genetic Resources Centre & Data Bank

NAP National Agriculture Policy

NARO National Agriculture Research Organisation

NCDP National Cooperatives Development Policy

NGO Non Governmental Organisation

NIP National Industrial Policy

NRM National Resistance Movement

NTP National Trade Policy

PEAP Poverty Eradication Action Plan

PFA Prosperity for All

PMA Plan for Modernisation of Agriculture

PO Producer Organisations

RDS Rural Development Strategy

RFSS Rural Financial Services Strategy

SACCO Saving and Credit Cooperative Organisations

SEP Strategic Exports Programme

SME Small and Medium Term Enterprises

TPM Top Policy Management

UCDA Uganda Coffee Development Authority

UNFFE Uganda National Farmers’ Federation

WHO World Health Organisation

4

5

Executive Summary

Agriculture is one of the key sectors of the Ugandan economy. Unfortunately, evidence

suggests that since 1997, the performance of the sector has not been impressive and

growth has been mixed; in some years growth in agriculture has been less than the

population growth. Key sector outcome indicators covering food and nutrition security

and market performance have also shown slow growth. While there were positive

increases in production of cereals, root crops recorded decreases. Growth in cash crops

was low as a result of negative growth in production of coffee; the most important cash

crop. In recent years, fisheries also witnessed a drop in production after significant

growth in early 2000s

The Government of Uganda has implemented various policies geared towards eradicating

poverty among the people of Uganda. The government’s development strategy was led

by the PEAP which was first prepared in 1997. To implement the PEAP, sector specific

policies and strategies were articulated. In the agriculture sector, although there was no

overall sector development policy (this is now rectified with the development of a

national agriculture policy), many other policies (PMA, NAADS, RDS, etc) were in place

to guide the development of the sector. Other policies that are important for farmer

entrepreneurship include those related to private and financial sector development and

to trade and commerce. These policies (RFSS, MDI, FIA, NTP, SEP, etc) are implemented

by the Ministry of Planning and Economic Development and that of Tourism, Trade and

Industry.

To implement sector policies and strategies, there are institutions covering both the

public and private sectors. In the public sector, these institutions include the Ministry of

Agriculture, Animal Industry and Fisheries and agencies, other ministries of the

government such as those responsible for finance, local government, higher education

and academia, etc. Private sector actors in agriculture include private companies,

farmers’ organisations, etc. The NGO participation is also strong as is participation by

development partners.

The implementation of the sector policies and strategies resulted in some achievements

as far as farmer entrepreneurship is concerned. However, many challenges including

poor access and adoption of new technologies, inadequate marketing capacity, limited

access to affordable finance, sub-optimal organisation framework for farmer

entrepreneurs, and inadequate infrastructure still remain. Many cross cutting issues such

as HIV/AIDS, gender and youth, environment and climate change also pose challenges

to the development of the sector.

Members of Agro-Profocus currently have a fair level of present on the development

scene in Uganda. They are involved in many activities in the key thematic areas of

financial services, food production, value chain and market access, knowledge and

research, organisational and institutional development and cross cutting issues. The level

of focus in each theme varies from member to member.

The challenges facing the development of farmer entrepreneurship present opportunities

for the APF members to review and, if found necessary, to reposition themselves to play

even more significant roles in farmer entrepreneurship in Uganda. This could be through

the promotion of partnerships between members. Such partnerships would be

appropriate vehicles for the consolidation of themes of operation, for each APF member,

in line with technical capacity, level of presence on the ground and the resources

available.

6

1. Introduction

Agri-ProFocus (APF), founded in 2005, is a partnership of 26 Dutch donor agencies,

credit institutions, training and knowledge institutions and companies. Their shared

mission is to provide coherent and demand driven support to enhance the capacity of

producer organizations (PO’s) in developing farmer entrepreneurship within the context

of poverty reduction.

One of the main goals of APF is to build solid, transparent and action-oriented support

programmes to promote farmer entrepreneurship. This synthesis paper is part of the

process of developing a country programme for Uganda. Strategically, the country

programme will aim to coordinate and harmonise existing efforts; identify and formulate

new joint activities; and link country programmes with learning and innovation. The

general objective of the country focus programme is to develop “an overall strategic

framework for collaboration between Uganda stakeholders and a support coalition from

the APF network”.

This synthesis paper identifies and analyses trends, cross-cutting issues and bottlenecks

for Uganda with regard to agriculture in general and farmer entrepreneurship in

particular; distinguishes scenarios / options for promoting farmer entrepreneurship

based on what important stakeholders are aiming for, while avoiding making

recommendations or prescribing solutions.

The methodology utilised in the development of this synthesis paper was mainly a desk

review of secondary data and interview with a few selected members of the APF, other

development partners such as DANIDA’s ASPS Programme, and the public sector. A

discussion workshop of a few APF members was help at SNV offices in Uganda.

The documents reviewed include the policies and strategies of the government of

Uganda such as: PEAP, the RDS, PFA, the draft National Development Plan, the draft

National Agriculture Policy, the Development Strategy and Investment Plan of MAAIF,

the National Trade Policy, the Marketing and Agro-Processing Strategy, the Strategic

Exports Programme, etc. Other documents include reports and programme documents of

APF members such as SNV Uganda, Heifer / Send a Cow1, and Oikocredit.

This report is divided into seven chapters. The first chapter presents an introduction, the

genesis of the assignment and the documents reviewed. The second chapter is a brief

summary of developments in the sector. Chapters three and four present the existing

policy and institutional frameworks, respectively, covering agriculture and farmer

entrepreneurship. Chapter five is a synopsis of the challenges affecting the development

of the sector, while chapter six presents a summary of the current themes and areas of

intervention for the APF members. Chapter seven attempts to link the challenges

identified in chapter five with the themes of involvement of APF members.

2. Status of the Agriculture Sector

Although agriculture is considered one of the key sectors of the Ugandan economy,

evidence suggests that since 1997, the performance of the sector has been less than

impressive as evidenced by the following:

Outcomes a. Growth: Over the years 1987-2005, agriculture in Uganda performed well, growing

at 3.8%, faster than population growth at that time; thus it was a major contributor to

the Uganda’s poverty reduction efforts. However, the evidence suggests that in recent

1 Send A Cow is not an APF member as such but a close collaborator, therefore their partner info has been included in annexes.

7

years, the performance of the sector has been less impressive as real growth in

agriculture output declined from 7.9 percent in 2000/01 to 1.3 and 2.6 percent

respectively in 2007/08 and 2008/09 (MOFPED, 2009)2. The latest growth is mainly due

to food crops (2.9%) as a result of a refocusing of NAADS and agricultural recovery in

Northern Uganda. Cash crops grew at a slower pace of 1.7%. However, this rate of

growth is well below the average national GDP growth rate of 6.5 percent attained

during the period and also below the population growth rate of 3.4 percent. It is also

short of the 6 percent target set by African Governments under the Comprehensive

Africa Agriculture Development Programme (CAADP)3.

b. Poverty reduction: Household surveys for the years 1992, 1999 and 2002 indicate

that national poverty fell from about 60% in 1992 to 34% in 1999, rising again to 38%

in 2002 and again dropping to 31% in 2008. Fiscal Year 1992/93 was a particularly bad

year for agricultural production and corresponds to the highest measured poverty rate.

The year 1999/00, which saw a large decline in the poverty rate, was the second in a

row of three very good years of agricultural production. 2002/03 was also a positive but

below average growth year and this corresponds to the small rise in the poverty rate in

that survey year. This suggests that positive agricultural performance is strongly related

poverty reduction.

c. Food Security: From 1992 to 2005, the country’s average caloric intake only

improved from 1,494 to 1,971 calories per person per day, much less than the WHO

recommended figure of 2,300. Moreover, the number of people deemed food insecure

has increased from 12 million in 1992 to 17.7 million in 2007. This is of course partly a

consequence of the high population growth rate. The population that was 6 million in

1968 is now 30 million and every year there are one million more mouths to feed.

d. Market Performance: There is increasing demand from regional and international

markets for both traditional and non-traditional agricultural products. As the only surplus

producer in the region, surrounded by countries facing a structural deficit in staple crops

(maize, beans and possibly bananas and other crops), Uganda is in a unique position to

exploit its comparative advantage in growing these crops. It is also in a good position to

exploit the high transportation cost barriers facing most countries in the region, and to

use its advantage to compete against imports from outside the region. Proximity to

countries that provide a market for its commodities gives Uganda the competitive

advantage over imports from outside the region.

e. Employment: Agriculture is easily the largest employer in Uganda; indeed the

sector increased its share of the working population from 66 percent in 2002/03 to 73

percent in 2005/064 (as against manufacturing at 4.2 percent and services at 23

percent). This is a challenge as, while structural change is taking place in the economy

labour seems to be stuck in agriculture with manufacturing and services absorbing less

and less of the labour force.

Outputs a. Crops: Over the years 1999/2000 to 2005/06, production of the major crops had a

mixed

record. While positive increases were recorded for cereals (maize, millet, rice and

sorghum), beans and simsim, significant and worrying decreases took place for root

2 MFPED, Background to the Budget, 2009/10. 3 CAADP is an initiative of the New Partnership for Africa’s Development under the African Union. It aims at accelerating growth and eliminating poverty and hunger among African countries by enhancing development in agriculture. The main goal is to help African countries reach a higher path of economic growth through agriculture led-development. The main principles being the pursuit of 6% average annual sector growth rate and the allocation of 10% of the public budget to agriculture. 4 Additionally, the fisheries sector directly employs over 300,000 people with up to 1.2 million more depending on fisheries as a source of income and livelihood (PEAP, 2004).

8

crops (cassava, Irish and sweet potatoes) and export crops. Growth in cash crops was

low at only 1.7% in FY2008/09 as compared to 9.0% in 2007/8. This was mainly due to

the negative growth -3% for coffee which contributes over 60% of the total cash crop

output. Tea also experienced negative (-11.3%) in 2008/09 as compared to 9.8% in the

previous year while cotton experienced positive 85.5% growth as compared to -54%

over the same period.

As for yields,5 it seems the record is even more disturbing. Between 1999 and 2006 nine

major crops showed substantial reductions in yield with only five showing increases.

Only simsim had a significant increase (Table 1).

Table 1: Change in productivity of major crops between 1999 and

2006.

Crop Av yield

(kg/ha)

Mean yield (kg/ha) Change

(%)

Simsim 114.06 277.80 144

Cassava 401.47 543.70 35

Sweet

potato 1,664.20 2,070.20 24

Millet 583.08 718.70 23

Groundnut 679.55 635.90 -6

Irish potato 1,457.20 1,002.70 -31

Sorghum 504.34 323.20 -36

Rice 1,385.12 733.60 -47

Cotton 627.70 292.20 -53

Maize 1,399.50 551.40 -61

Beans 988.36 358.30 -64

Coffee 1,215.03 368.70 -70

Matooke 8,593.96 1,872.10 -78

Source: EMU 2007.

b. Livestock: According to the FAO/IC6, over the last decade, meat production has

been increasing but has not kept pace with population growth. The report states that

between 1995 and 2006, total meat production grew at an annual rate of 1.8 percent but

average domestic meat consumption per capita declined from 10.3 kg per year in 2001

to 8.8 kg per year in 2006.

With regard to milk, FAO (2008) reports that, over the period 1995 to 2006, milk

production increased at an annual growth rate of 4.8 percent, resulting in an increase of

average domestic milk consumption from 20.1 kg per capita per year in 2001 to 25.4 kg

per capita per year in 2006. Specifically, over the 10 years to 2006, improved dairy

breeds have increased in number, reaching 10 percent of the total cattle population.

Consequently, imports of milk and milk products have declined from more than USh50

billion by value in 2001 to less than Us 10 billion in 2006.

c. Fisheries: Fisheries is one of Uganda’s key industries indeed fish exports were for a

while the second most important foreign exchange earner after coffee. Uganda has 20

percent of its surface areas as water. This comprises five major lakes (Victoria, Albert,

Kyoga, Edward and George and about 160 minor lakes, rivers and wetlands). These

water bodies, if well managed, have an estimated production potential of over 800,000

tonnes of fish although the current catch is estimated at 430,000 tonnes.

5 PMA Evaluating (2005) 6 FAO Investment Centre (2008) - End of Mission Report, ATAS Program

9

However, while exports increased dramatically after 1991, they have now witnessed a

serious decline, falling from a peak of 39,201 tons in 2005 to 23,000 tons in 20087 as a

consequence of declining catches, falling stocks and over-fishing.

3. Policy Framework

Over the last 20 years, the Government of Uganda implemented various policies geared

towards eradicating poverty among its people. The government’s development strategy

has been led by the PEAP which was first prepared in 1997, providing a model for the

poverty reduction strategy approach. The PEAP was revised in 2000 and again in 2004.

The last version of the PEAP expired in 2008 and is to be replaced by the National

Development Plan (currently under development).

The PEAP 2004 is presented in five ‘Pillars’; (i) economic management, (ii) production,

competitiveness and incomes, (iii) security, conflict resolution and disaster, (iv)

governance, and (v) human development. In this PEAP, agriculture falls under pillar II:

Enhancing production, competitiveness and incomes. The priorities of pillar II include,

among others, modernisation of agriculture, preservation of the natural resource base,

particularly soil and forests, infrastructure, and private sector skills and business

development. This and the first pillar would also cover entrepreneurship. Each sector of

Government is grouped as far as possible under one pillar. The PEAP recognises that

many sectors contribute to the objectives of other pillars and that there are cross cutting

issues that cut across the whole economy including: Gender, employment, population

growth, social protection, income distribution and regional equity.

Until now, there has been no specific National Agriculture Policy. However, this is being

rectified with the development of a National Agriculture Policy (NAP); currently a draft is

under discussion. The main policy instrument for the implementation of agriculture in the

PEAP has been the Plan for the Modernisation of Agriculture (PMA). The PMA has 11

areas of focus including the three areas of research, extension, rural finance and trade

which could be said to cover the needs of farmer entrepreneurship.

Since 2000, investments in agriculture have been guided by the Plan for Modernization

of Agriculture (PMA) whose main objective is poverty reduction through agricultural

commercialisation. The PMA was designed as a multi-sectoral approach to agricultural

development, based on the recognition that some of the investments needed to make a

difference in agriculture lie outside the mandate of Ministry of Agriculture, Animal

Industry and Fisheries (MAAIF).

In 2005, a Rural Development Strategy (RDS) was designed by the Ministry of Finance,

Planning and Economic Development (MFPED) with three main objectives: (i) increasing

farm productivity of selected commodities produced by agricultural households, (ii)

increasing household output of selected agricultural products, and (iii) adding value and

ensuring a stable market for agricultural products (MFOPED, 2005).

The current Government’s vision for the country is Prosperity for All (PFA), the

programme for which derives from the NRM manifesto of 2006. This emphasizes the

importance of continued liberalization and privatisation but also expresses views that are

more interventionist than have been common in recent times.

7 http://allafrica.com/stories/200909160722.html

10

The concurrent existence of the PMA, RDS and PFA frameworks and visions have raised

some concerns with regard to issues of policy consistency and the extent to which this

might affect the performance of the sector. To respond to these concerns, MAAIF is

developing an explicit comprehensive agricultural sector policy document for Uganda as

part of the implementation of this Development Strategy and Investment Plan (DSIP).

The trade sector is governed by the National Trade Policy (NTP) under the premise that

Uganda’s is a private sector led economy. The MTP spells out interventions covering

domestic and international trade and other cross cutting issues. Domestic trade aims to

promote specific policies, Laws and guidelines. Its implementation aims to develop

commercial offices at the district level, develop market information systems and to

ensure clear and functional linkages between investment, production and trade.

Other policies and strategies include the Strategic Exports Programme (SEP) aim at

promoting specific agriculture enterprises such as, the Marketing and Agro-Processing

Strategy (MAPS) which provides strategies for linking agricultural producers and

domestic and foreign consumers, and for processing to add value and ultimately increase

incomes of the small scale agricultural producers. Other relevant policies include the

National Industrial Policy (NIP) whose goal is to build Uganda’s industrial sector into a

modern, competitive and dynamic sector fully integrated into the domestic, regional and

global economies and the National Cooperatives Development Policy (NCDP), currently

under discussion, with the purpose to achieve a strong, vibrant and prosperous co-

operative movement in Uganda.

Table 2: Relevant PEAP pillars and priorities

Pillars (Priorities) Relevant Priorities for

Agriculture and Farmer

Entrepreneurship

I. Economic management

• The maintenance of macroeconomic stability

• Fiscal consolidation

• Boosting private investment

• Financial Deepening

• Microfinance institutions

• Private Investment

• Trade liberalisation

• Export Diversification

II. Enhancing production, competitiveness and

incomes

• The modernisation of agriculture

• Preservation of the natural resource base,

particularly soil and forests

• Infrastructure including roads, electricity and

railways; better maintenance, cost- reduction and

private sector participation will be key to

achieving improvements in the context of fiscal

consolidation.

• Enhancing private sector skills and business

development.

• Agriculture Research and

Extension

• Business development services

for MSEs

• Outreach of financial services

• Market information

• Other agricultural services

From tables 2 and 3 it can be seen that entrepreneurship is generally covered under

both pillar I and II in the PEAP. The specific issues such as boosting private investment

(pillar I) and enhancing private sector skills and business development (pillar II) are

related to entrepreneurship. Under both pillars, there are priorities that are relevant for

the promotion farmer entrepreneurship. Over the years, government has put in place

policies/ laws and strategies for the attainment of the priorities under the two pillars

relevant to this objective.

11

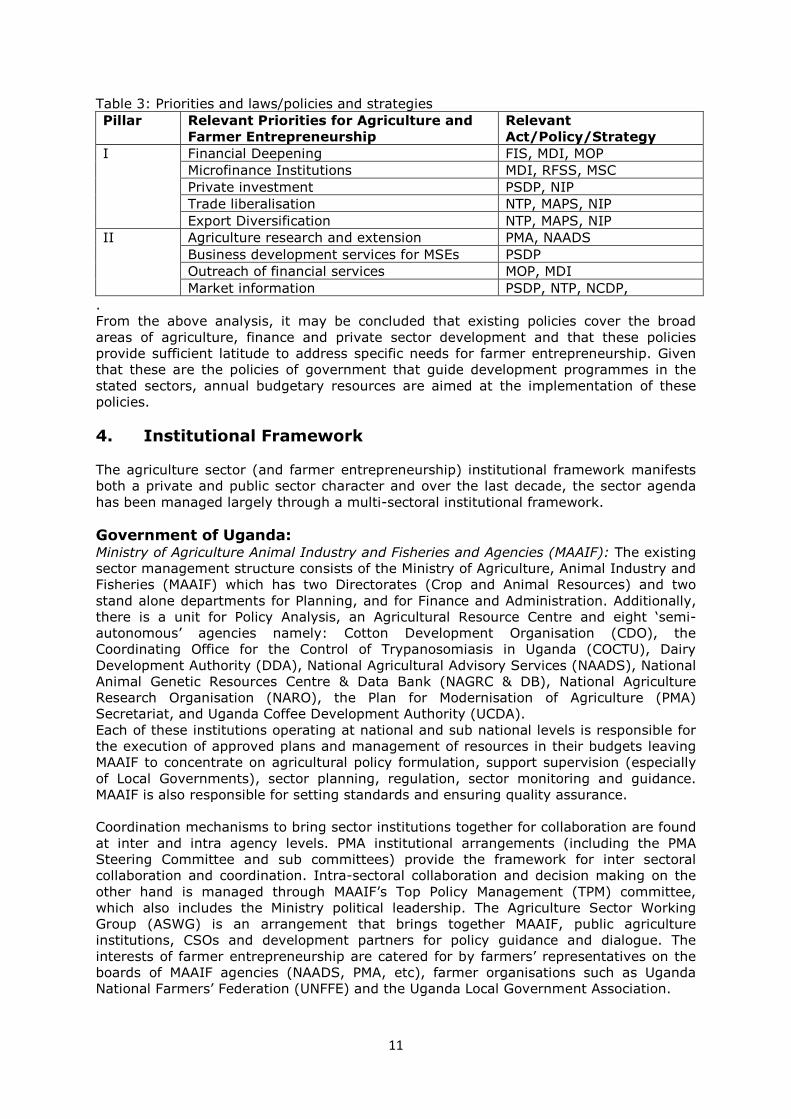

Table 3: Priorities and laws/policies and strategies

Pillar Relevant Priorities for Agriculture and

Farmer Entrepreneurship

Relevant

Act/Policy/Strategy

Financial Deepening FIS, MDI, MOP

Microfinance Institutions MDI, RFSS, MSC

Private investment PSDP, NIP

Trade liberalisation NTP, MAPS, NIP

I

Export Diversification NTP, MAPS, NIP

Agriculture research and extension PMA, NAADS

Business development services for MSEs PSDP

Outreach of financial services MOP, MDI

II

Market information PSDP, NTP, NCDP,

.

From the above analysis, it may be concluded that existing policies cover the broad

areas of agriculture, finance and private sector development and that these policies

provide sufficient latitude to address specific needs for farmer entrepreneurship. Given

that these are the policies of government that guide development programmes in the

stated sectors, annual budgetary resources are aimed at the implementation of these

policies.

4. Institutional Framework

The agriculture sector (and farmer entrepreneurship) institutional framework manifests

both a private and public sector character and over the last decade, the sector agenda

has been managed largely through a multi-sectoral institutional framework.

Government of Uganda: Ministry of Agriculture Animal Industry and Fisheries and Agencies (MAAIF): The existing

sector management structure consists of the Ministry of Agriculture, Animal Industry and

Fisheries (MAAIF) which has two Directorates (Crop and Animal Resources) and two

stand alone departments for Planning, and for Finance and Administration. Additionally,

there is a unit for Policy Analysis, an Agricultural Resource Centre and eight ‘semi-

autonomous’ agencies namely: Cotton Development Organisation (CDO), the

Coordinating Office for the Control of Trypanosomiasis in Uganda (COCTU), Dairy

Development Authority (DDA), National Agricultural Advisory Services (NAADS), National

Animal Genetic Resources Centre & Data Bank (NAGRC & DB), National Agriculture

Research Organisation (NARO), the Plan for Modernisation of Agriculture (PMA)

Secretariat, and Uganda Coffee Development Authority (UCDA).

Each of these institutions operating at national and sub national levels is responsible for

the execution of approved plans and management of resources in their budgets leaving

MAAIF to concentrate on agricultural policy formulation, support supervision (especially

of Local Governments), sector planning, regulation, sector monitoring and guidance.

MAAIF is also responsible for setting standards and ensuring quality assurance.

Coordination mechanisms to bring sector institutions together for collaboration are found

at inter and intra agency levels. PMA institutional arrangements (including the PMA

Steering Committee and sub committees) provide the framework for inter sectoral

collaboration and coordination. Intra-sectoral collaboration and decision making on the

other hand is managed through MAAIF’s Top Policy Management (TPM) committee,

which also includes the Ministry political leadership. The Agriculture Sector Working

Group (ASWG) is an arrangement that brings together MAAIF, public agriculture

institutions, CSOs and development partners for policy guidance and dialogue. The

interests of farmer entrepreneurship are catered for by farmers’ representatives on the

boards of MAAIF agencies (NAADS, PMA, etc), farmer organisations such as Uganda

National Farmers’ Federation (UNFFE) and the Uganda Local Government Association.

12

Local Governments: Since 1992, Decentralisation Policy has sought to strengthen local

governance structures by devolving service delivery, promoting participation and

empowering local people. MAAIF’s responsibility in this regard is to support Local

Governments (LGs) to deliver services relating to regulatory services, quality assurance

services, and agriculture statistics and information.

MAAIF also assists with capacity building in local government. MAAIF does this through

Agriculture Advisory Services and District Production Services. Under Agriculture

Advisory Services, MAAIF aims to (i) increase farmer access to improved technologies,

advisory service delivery, and “proactive participation in value chain development for

profitable agricultural production”; (ii) empower farmers to demand for advisory services

and technologies, and quality assurance services. Under District Production Services the

ministry aims to (i) to strengthen Local Government capacity in the delivery of services

relating to regulatory services, quality assurance services, agriculture statistics and

information; and capacity building for local governments; (ii) to strengthen disease, pest

and vector control and quality assurance services; improve the agriculture statistics and

information system; and build capacity in local government.

Although there is no formally established coordination framework for farmer

entrepreneurship for all (public, private, civil society, NGOs, etc) actors at the local

government level, there is substantial collaboration taking place and many CSOs, private

companies and NGOs are currently involved, through contacts, in the implementation,

capacity building and monitoring and evaluation of farmer entrepreneurship activities.

The Ministry of Finance, Planning and Economic Development: The Ministry of Finance,

Planning and Economic Development (MFPED) is responsible for ensuring that sectoral

developments are well co-ordinated and appropriately funded. The principal mechanism

is the Medium Term Expenditure Framework (MTEF) which is meant to provide a reliable,

rolling 3-year guide to overall, sector and sub-sector budget allocations. MFPED insists

that the substantive new budgeting procedures introduced for 2009/10, including the

requirement for signed Performance Contracts, will lead to more performance monitoring

and better budget discipline.

Funding8 for the agriculture sector from the GOU-financed budget showed a marked

decline through the 1980s from 9.6 percent in 1980/81, as the nature of the economy

changed under structural adjustment. Since 1991/92, agriculture has not received more

than 3 percent of the GOU-financed budget in any year and in some years the share has

been below 2 percent. Regular information on donor-financing of the budget is only

available since 2000/01. Information collected on public expenditure on agricultural

sector since 2001/02 at both the central- and local-government level by GOU and donors

raised the share of the GOU budget allocated to the sector to almost 8 percent in

2001/02 but there has been a continuous decline since to 5.7 percent in 2005/06. The

budget has decreased, in real terms, from approximately UGX 280 billion at the start of

the decade to UGX 210billion in 2005/06. Direct donor funding is also on the decline,

from approximately UGX 125 billion at the start of the decade to only UGX 76 billion in

2007/8. Decentralisation in sector financing is deepening, the share of the sector budget

channelled through local government rising from 7 percent of the total at the start of the

period, to 19 percent by 2005/06.

Other Sector Ministries and Agencies: Other ministries and agencies play critical and

complimentary roles to enable MAAIF deliver on its mandate. The roles of institutions

like the National Parliament and Ministries responsible for these sectors are important.

They include the Parliamentary committee on agriculture, which is responsible for

oversight as well as review and approval of proposed policies and strategies for the

sector. Other ministries and agencies include: Ministry of Tourism, Trade and Industry

8 Uganda: Agriculture Public Expenditure Review, 2007

13

(MTTI) responsible for trade; Ministry of Public Service responsible for personnel

management and development; Ministry of Water and Environment; Ministry of Gender

Labour and Social Development responsible for gender adult education and labour, the

Ministry of Education responsible for primary, secondary and tertiary education; Ministry

of Lands, and Urban Development responsible for land reforms including land use; and

Ministry of Energy and Mineral Development responsible for rural energy and

electrification.

The Ministries named above also have agencies that are critical for agriculture sector

activities like Uganda Bureau of Statistics (UBOS), Uganda National Bureau of Standards

(UNBS), Uganda National Council of Science and Technology (UNCST), National Forestry

Authority (NFA) and National Environmental Management Authority (NEMA), among

others.

Other agencies of the Government of Uganda that are involved in the promotion of

entrepreneurship include institutions of higher learning and research such as

universities, colleges of higher education (commerce, education and technical) and

cooperative development colleges. These institutions are involved in the generation and

propagation of knowledge

The Private Sector The private sector includes private companies, and farmer organisations, involved in

activities such as production, processing, marketing, knowledge generation, advisory

services, advocacy, provision of inputs, etc.

Private Companies: With the national policy of liberalisation of the economy, many

private companies are currently active in all segments of most value chains including

cotton, coffee, food commodities, etc, which were previously the preserve of state owned

marketing parastatal companies. It is therefore current practice for private companies to

engage in production, processing and marketing of all farm produce. The profile of the

private companies shows a full spectrum of firms from large international/multination

companies to MSEs.

Farmer Organisations: Over the years, Uganda’s agriculture sector was driven by

farmer’s organisations, mainly through the cooperative movement9. Under this

arrangement, many farmers produced and marketed crops such as cotton coffee,

tobacco, etc. They were also engaged in transport, dairy, shops, etc. At their peak, the

co-operatives were organized in a four tier vertical structure of primary societies (at the

village level) that consist of at least 30 persons aged above 12 years. A minimum of two

primary societies form a secondary (at the district level) while two or more secondary

societies form a tertiary (at the national level) which provides specialized services.

Secondary and tertiary societies form the apex at the national level.

This structure of the cooperative movement existed across the whole country. Under this

arrangement, primary cooperative societies sold their produce to the secondary, the

secondary to the tertiary which then sold to the national marketing boards. For example,

cotton was sold to the Lint marketing Board, Coffee to the Coffee Marketing Board, food

commodities to the Produce Marketing Board, and milk to the Dairy Corporation. These

marketing boards were parastatal companies of the government of Uganda.

Under economic liberalisation, at the national level, the marketing boards were

restructured to retain regulatory and standards roles; hence the birth of the Cotton

Development Authority, the Uganda Coffee Development Authority, the Dairy

Development Authority. At the lower levels, most of the cooperative societies (village

9 As the main marketing channels during this period, cooperative societies existed in nearly every village and district where relevant activities took place.

14

and district) were nearly completely wiped out as private sector companies ventured into

the lower segments of the value chains. In spite of this paradigm shift, some sub-sector

cooperative organisations such as the Uganda Cooperative Alliance, the Uganda

Cooperative Transport Union, the Uganda Cooperative Savings and Credit Union, and

some Savings and Credit Cooperative Societies (SACCOS) still exist though in

restructured and modified roles.

After two decades under the marketing structure described above, there is an emerging

opinion that the cooperative movement still has a significant role in a modern liberalised

economy. This is generating increased political support and farmer groups are

increasingly being promoted as credible vehicles for poverty reduction. To this effect, a

new National Cooperative Development Policy (NCDP) whose purpose to achieve a

strong, vibrant and prosperous co-operative movement in Uganda, has been developed

and is currently under discussion. The implementation of national strategies using the

cooperative movement such as seen in the roles of SACCOS in the Prosperity for All and

the Rural Financial Services Strategy (RFSS) is manifestation of political support for the

cooperative movement.

With the near demise of the cooperative movement, other farmer organisations and

associations emerged around sub-sector and or specific issues. Such organisations

include the Uganda National Farmers Federation (UNFFE) which was founded in 1992

with the objective to mobilize the farming community and voices under one independent

umbrella organisation, associations covering many commodities such as dairy, cotton,

honey, timber, etc and specific issues such as production, processing and marketing.

Non Governmental Organisations (NGOs) Another area of growth was in Non Governmental Organisations which were set up with

mandates such as the generation and dissemination of knowledge and implementation of

development projects. Accordingly many international and national NGOs are currently

key stakeholders in Uganda’s farmer entrepreneurship development. They collaborate in

research and the implementation of extension and advisory services and are actively

involved in activities such as farmer mobilization and farmer institutions’ capacity

development. Under such programmes NGOs are involved in the supervision of extension

service delivery.

Development Partners Since 2000, the PEAP framework shaped a new relationship between Government and

Development Partners (DPs) at the economy-wide level. There was a shift from project-

focused aid to sector programmes. The MTEF/BFP process provided the framework for

this, with DPs (and also NGOs) participating in the sector working groups through which

sector plans and budgets evolved. The funding modalities also changed with key DPs

providing either general or sector-earmarked budget support, based on dialogue with

GOU about policies and targets, rather than earmarking to specific projects.

The number of Development Partners supporting the agricultural sector has reduced in

recent years. This trend is evident in most sectors as donors refined their roles in

Uganda’s national economy Uganda and also as some Development Partners move to

general sector budget support as their preferred funding modality. Nonetheless there

are still major DPs who, as already indicated, are making a significant contribution in

financing and technical and policy advice (through the ASWG) to the sector, through

sector and general budget support. These DPs include: The World Bank, The African

Development Bank, The International Fund for Agriculture Development, The European

Union and DANIDA and JICA continue to be involved in support to public sector

agriculture. Under this financing arrangement, the government of Uganda determines its

own priorities based on its policies and development plans including those related to

farmer entrepreneurship.

15

5. Constraints and Challenges

Over the years, significant development and achievements have been made in the

agriculture sector to support farmer entrepreneurship. In spite of these achievements,

many challenges remain and they represent possible areas for further interventions by

all stakeholders (government, DPs, NGOs, CBOs, and the private sector) in the coming

planning periods.

Technology Many improved varieties, breeds and prototypes for increased yields, food security and

incomes have been developed since. At the same time, specific constraints have been

addressed including maize streak virus, groundnut rosette virus, cassava mosaic virus;

coffee wilt diseases.

In terms of sustainable land use, the National Agriculture Research Organisation (NARO)

has demonstrated an important set of results relating to natural resource management

adopted by households, including mulching and zero-tillage, as well as slash and burn

practices, have significant and positive impacts on farm productivity. In terms of

extension delivery, the National Agriculture Advisory Services (NAADS) has promoted

private delivery of extension services covering over seventy enterprises.

The challenge with adoption of new technologies is that there is no clearly defined

process for extension to access the new technologies being generated by research and

there are only limited mechanisms for feedback on the technologies released by research

and extension services are not enough and many farmers continue to demand for it.

Farmers do not get the opportunity to consider technology options for appropriateness to

their situation. Additionally, lack of a clearly defined feedback mechanism between

research and extension undermines efficient refinement of technologies.

As regards soil fertility, there remains room for improving soil fertility through better

management practices, but it also indicates that farmers who are not practicing these

methods, and who are also not using fertilizers, are likely depleting soil fertility quite

rapidly.

Marketing The elastic demand for commodities suggests that additional production could be

absorbed domestically while livestock products also have good market prospects.

Despite the recent fall in commodity prices brought on by the current global downturn,

the long-term prognosis is still one of a rising trend for global food prices especially for

key commodities. This should offer clear opportunities for a net food-producing country

like Uganda.

Nevertheless, a number of constraints threaten to undermine this potential:

Commodity volumes: The nature of agricultural production in Uganda is predominantly

subsistence. Farmers are unable to produce the quantities in line with national and

export demand orders. This leads to the loss of trust in export markets as well as share

since competitors step up their supplies. Notable cases where Uganda has failed to meet

export demand are in honey and fish.

Quality assurance standards: Standards are increasingly becoming important in the

international trade for food and agricultural products because they “stipulate what can or

cannot be exchanged and define the procedures that must be followed for exchange to

take place”. The export sector often fails to meet these standards and where attempts

towards compliance have been made, the associated costs have remained high and

prohibitive for the majority of the exporters. Apart from pockets of enhanced Sanitary,

Phyto-sanitary (SPS) and other Standards developed in response to export market

16

requirements (such as for fish) or acute problems (such as certain animal diseases),

Uganda lacks a broader strategy to utilize agro-food standards to protect human, plant

and animal health.

In the local market, standards are also important to ensure compliance with national

health standards but also to promote trade through storage of commodities in

warehouses licensed under the Warehouse Receipts Systems.

Market information and linkages: Market and production information is a resource

required in the making of all business decisions. Although there has been sporadic

attempts to collect market and production information, this information is not readily and

sufficiently available to agents involved in agribusiness and trading. The framework for

collection of data at the lower government level is not well established and data for

planning is mostly lacking. The result is usually poor production and market planning

decisions and losses for ill-informed agents and farmers.

Markets for agricultural products are now on the increase often as specialized niche

markets with specific (such as organic, traceability, etc) characteristics and

requirements. Such markets call for prior planning of production and value addition

infrastructure so as to match farmers’ supply with market demands. Unfortunately, in

Uganda today, these linkages are at best weak and in many cases not existent. Thus,

there is a growing need to link producers with those value chain players involved in

agro-processing and marketing.

Market infrastructure: In Uganda, agricultural production takes place in rural areas

where market infrastructure is inadequate or not available at all. For successful

marketing, the kind of infrastructure required includes good feeder roads,

communication facilities, electricity, pre-cooling and pack houses, cold and dry storage

facilities, refrigerated trucks, air freight facilities, and so forth. Unfortunately some of the

infrastructure is of public good nature and a framework for private sector financing of

such infrastructure is not defined. Even in the case of private good nature, farmer

entrepreneurs indicate that the current high cost of finance is a hindrance to the

acquisition of such infrastructure.

Export development competencies: Key competencies are needed for doing business in

other countries. Exporters should be able negotiate and execute export orders properly

as well as have reasonable knowledge in strategic export planning, management and

marketing. At the moment, there is no established institution in Uganda that is

responsible for training exporters on essential and basic export skills rendering the

export markets unachievable by most farmer entrepreneurs.

Finance The ability of agricultural enterprises and rural households to invest for the long term

and make calculated decisions for risky income flows is partly shaped by accessibility and

cost financial services. In spite of recent growth in the financial sector, a majority of

smallholders, especially in the rural areas, remain without access to the services they

need to compete in the market.

Lack of suitable development financing schemes for more affordable is still a big

challenge for small and medium enterprises (SMEs). Although the Bank of Uganda did

institute some credit finance schemes, they remained inaccessible to the majority of the

small and medium exporters not only on technical grounds but also because of high

interest rates. Other sources of finance such as micro-finance are too costly and

conventional commercial banks are reluctant to finance agriculture and agro-based

export business due to perceived high risk and unpredictability.

17

Infrastructure Infrastructure that supports agriculture cover certain categories including water for

production-related infrastructure (irrigation, livestock and aquaculture), disease control

infrastructure, research infrastructure, quality assurance infrastructure including

laboratories, market infrastructure, institutional infrastructure (e.g. offices). The state of

the infrastructure is generally inadequate and requires enhancement.

Farmer Organisation Arising from the general economic liberalization policy, competition for farm products

has increased in the market place with the involvement of large processors,

supermarkets and middlemen. These players exercise controlling powers in determining

market conditions and prices as well as stringent supply requirements and standards in

terms of quality, safety, consistency and traceability.

Unfortunately for the small scale farmer entrepreneurs who operate as individuals, they

have been reduced to weak players in the supply chain, with lower returns to their

farming activities. They do not have power to negotiate good prices as they, as

individuals, are not able to command large volumes of inputs and supply large volumes

of produce to the market.

The cooperative movement, when it existed, as strong in the mitigation of the adverse

market conditions affecting farmers. Unfortunately, this is no longer the case even where

some apex or farmer organisations exist. Many of these farmer organisations are

inhibited by inadequate technical, managerial and financial capacity to mitigate the

adverse conditions. The demand for strong and empowered farmer organisations is

therefore quite strong.

Cross-cutting Issues As well as the specific subject area issues, there are also a range of wider, cross-cutting

concerns that should be addressed: HIV/AIDS, gender, environment, Climate Change,

poverty, and food and nutrition security. These all have a critical impact on the

performance of the agricultural sector. An analysis of the impact and of any

opportunities available follows.

HIV/AIDS: The HIV/AIDS epidemic has had a multiplicity of negative impacts on

agricultural production in Uganda, including: forced selling by farmers of produce and

stock at inopportune times to meet costs; diverted expenditure towards medical bills;

reduced labour availability due to sickness and increased care obligations; reduced

household income due to falling productivity, leading to reduced school attendance,

reduced food security and nutrition, all tending towards the downward spiral; loss of the

most productive workforce (15-40 yrs); and dismantling of the family set up, resulting in

a decline in production and productivity, food insecurity, low incomes, increased health

care costs, greater job insecurity.

Gender and Youth: In Uganda, women constitute an estimated 70 per cent of

smallholder farmers and contribute about 70-75 per cent of agricultural GDP. According

to the Uganda 2002 Population Census, the agricultural sector employed a higher

proportion of women in employment (83 per cent) than men (71 per cent).

Division of labour between men and women in Uganda varies by region and farming

system. However some tasks are almost exclusively undertaken by men, and some by

women. Women usually undertake sowing, harvesting, head loading of produce, crop-

drying, winnowing, seed selection, pig and poultry-rearing and bartering sunflower seeds

for oil. Other tasks, such as weeding, bagging and crop storage, are almost equally

undertaken by both women and men.

18

It is estimated that women do 85% of the planting, 85% of the weeding, 55% of land

preparation and 98% of all food processing. At the same time, a substantial amount of

women’s time is taken up in providing care activities. In rural areas, it is estimated that

women’s workloads considerably exceed those of men. Given the foregoing, the role of

women in farmer organisations is becoming increasingly important and recognised.

Where cooperative societies used to be predominantly run by men, women are

increasingly recognised as dependable managers and owners of such organisations.

The low participation of the youth in agriculture is partly attributed to issues of access

and control over productive resources (land and capital), as well as limited knowledge

and skills in modern farming techniques. With the population growth rate so high,

however, it is unavoidable that the majority of the Ugandan population is made up of

young people and ways must be found to utilise this vast untapped labour force.

The Environment: Agricultural activities can have a major impact on land use, soil,

water, biodiversity and the landscape. Specifically, there are a number of environmental

issues (land degradation, agro-chemical pollution, etc) in agriculture with significant

implications on the performance of the sector. These will need to be addressed to

enhance sustainability of agriculture. Although at the national level, the National

Environment Management Agency is the main regulatory agency on environment

management, line ministries such as MAAIF have responsibility for agriculture related

issues. Important stakeholders in regard to the environment management include NGOs,

research institutions and the private sectors. Many farmers are yet to be educated about

their roles in sustainable natural resources management.

Climate Change: Given the Uganda’s heavy dependence on agriculture, the effects of

climate change could clearly put millions of people at greater risk of poverty and hunger.

Essentially climate change is just one of a number of stress factors (food insecurity,

conflict, malaria, energy deficit etc). Climate change aspects like heavy rainfall, floods,

drought and hailstorms are becoming common and frequent and have considerable

negative effects on agricultural activities and food security.

Vulnerability to climate shocks will influence the performance of the agriculture sector

and therefore there is a need to mainstream sustainable management of the

environment and natural resources in agricultural plans and programmes and to

strengthen capacity on an early warning system.

Currently, in Uganda, there is no strategy to manage climate change and, as a result,

there are no reliable predictions or early warning of the likely impacts of climate change

in Uganda. There is no weather and climate policy, there are low levels of awareness of

weather and climate issues, inadequate determination of adaptation and mitigation

options to control green house gas emissions. Although the Ministry of Water and

Environment indicates that it has prepared the National Adaptation Plan of Action (NAPA)

to address issues of climate change at national level it says it lacks funds to implement

it.

6. Existing Interventions by APF Members

The Affiliation matrix was summarised to bring out the salient features of the

participation of APF members in the various areas of strategic choices. For this purpose,

the strategic choices have been summarised as indicated in table 1 below. Details of the

strategic choices are given by the menu of products they contain as shown in the

ensuing strategic choice matrices.

The 13 APF members have made a total of 37 strategic choice areas, with two members

(CORDAID and Oxfam Novib) participating in the most number (5 out of 6) of thematic

areas, while two members (Oikocredit and Wageningen) with the highest level of

19

specialisation, show participation in only one of the areas of strategic choice; viz

Financial Services and Knowledge and Research respectively.

Participation in specific strategies choice areas also varies with the highest number of

members (9) choosing Value Chain and Market Access (VCMA) and the lowest number

(4) of members showing participation in Food production and Cross Cutting issues. Other

strategic choice options are chosen by between six and eight members.

Table 4: Matrix of Summary Activity Areas

Organisation CRCT FISS FOPR KWGE ODID VCMA

Total

Areas

1. Agriterra 4

2. Agro-Eco 2

3. CORDAID 5

4. Heifer Nederland 2

5. HIVOS 3

6. ICCO 3

7. KIT 2

8. Oikocredit 1

9. Oxfam Novib 5

10. Send a Cow 4

11. SNV 3

12. Solidaridad 2

13. WUR 1

Total 4 6 4 6 8 9 37

Key:

CCT-Cross Cutting Issues

FISS- Financial Services

FOPR-Food Production

KWGE-Knowledge and Research

ODID-Organisational and Institutional Development

VCMA-Value Chain and Market Access

This analysis might be useful for members wish to review the number of areas of

strategic choices in which to engage. For this purpose, internal SWOT analyses would

help to determine the strengths and weaknesses afflicting members as they attempt to

respond to the opportunities and threats that face them. In rationalising the size of areas

of intervention, development partners could be guided by factors such as: (i) the

intended depth of operation in the sectors they choose including the amount of resources

available to them, (ii) the internal technical expertise they bring to the sectors of choice.

Further analysis is undertaken, in the tables 2 to 7 in annex in annex, to bring out the

specific products that constitute the strategic choices of members. This is also reviewed

here in light of the constraints/opportunities existing relating to the products.

Financial Services (FISS): Members of the APF show engagement in four (loans, micro

credit, guarantees and micro-insurance) products (table 2, annex 2). This table also

shows that there are only 9 product choices made by 6 out of the 13 the members who

show participation in financial services. One member, Oikocredit, shows participation in 3

of the 4 products currently under offer and also demonstrating the highest (only one

strategic choice area) level of focus. Four members (Agriterra, CORDAID, Oxfam Novib

and Send a Cow) show participation in only one product. The most and least popular

products are micro credit and micro-insurance respectively with three and one members

respectively.

20

It is noteworthy that only a six members of APF are engaged in financial services and

that they offer a small number (4) of products under financial services although there

are so many products (grants, savings, accounts, leasing, warehouse receipts, etc) in

financial services. This is in spite of the fact that inadequate access to affordable

financial services especially in rural areas is cited as a significant hindrance development

and therefore poverty reduction by all including government, development partners,

NGOs and CSOs and the rural farmers.

Food Production (FOPR): Food Production was refined into four products as crops (staple

foods, maize, cassava, and pulses), poultry, dairy and livestock. Table 3, annex 2 shows

that there are only 7 product choices made by 4 of the 13 members who indicate

participation in Food Production. One member (Oxfam Novib) shows participation in only

one product while the remaining three members each participate in two products.

It is important to point out that the definition of products in this strategic choice area

was somewhat difficult given that some of the products are also covered under the Value

Chains and Market Access strategic choice. However, in the cases indicated here, the

APF member clearly demonstrated support for the product for the purposes of improving

food (and nutrition) supply. In the case of CORDAID, support for crops was specifically

for staple crops, Heifer Nederland was nutrition, Oxfam Novib was maize and Send a

Cow, Livestock development.

Knowledge and Research (KWGE): Knowledge and Research was refined into five

products of Impact Research, Scientific Research, Social Research, Economic Research

and Knowledge Sharing as indicated in table 4 of annex 2. The table shows 15 product

choices made by 5 out of 13 APF members who indicate participation in the strategic

choice area. The highest level of participation is by four members in social research and

the lowest by two members in scientific research. Agro-Eco and Oxfam Novib in Impact

and Social Research respectively demonstrate the lowest (1) product by a member.

Wageningen covers all the product areas; this being its only area of strategic choice

while KIT and SNV cover four of the five products.

It has been pointed out that technology and its adoption are important issues for farmer

entrepreneurship. It is also directly linked to the provision of advisory services to framer

entrepreneurs. Additionally, there is indication that there is insufficient data to support

planning for production and marketing.

Organisation and Institutional Development (ODID): Organisational and Institutional

Development is defined by five products (table 5, annex 2) of management information

systems, research and advocacy, governance, capacity building and technical assistance

and advisory services. This strategic choice area represents the highest level of

participation with 21 products by nine out of 13 APF members.

The most and least popular products are Capacity Building (7 members) and Technical

Assistance and Advisory Services (one member). The members with the most (5)

products in this strategic choice area is SNV and with the least (1 product) are Agro-Eco,

HIVOS and Solidaridad.

Value Chain and Market Access (VCMA)): Value Chains and Market Access is defined

using five products as indicated in table 6 of annex 2. The products include technical

services that are required in the support of value chain development, the segments of

the value chains and a grouping (crops or livestock) of the value chains themselves. This

strategic choice area represents the highest level of participation with 19 products by 7

members.

21

The most and least popular products are the Crops Value Chains (7 members) and

Livestock Value Chain (3 members). The value chains covered include coffee, cotton,

oilseed, horticulture, apiculture, dairy, etc. The members with the most (5) products in

this strategic choice area are CORDAID, SNV, and Send a Cow. Six members of the APF

do not participate in this strategic choice area.

Cross Cutting Issues: Cross cutting issues represent the category least shown by

members. Only three (out of 13) members indicate participation in a cross cutting issue.

Additionally, only three cross cutting issues (HIV/AIDS, Gender and Governance) are

covered leaving out such important cross cutting issues as environment, climate change,

human rights, etc. This is the case in spite of the fact that members are current involved

in activities that impact and or are impacted on by the cross cutting issues.

Areas of coverage: With the exception of ICCO and KIT which do not show data relating

to existing area coverage (annex 1b) in the country, all the other APF members indicated

that they have a national presence and outlook. In cases where a national presence has

not yet been achieved, the indication is that this is only a function of the current level of

operation which could change depending on resources and demand. Some of the

members indicated a regional (East Africa) and continental (Africa) presence.

Collaboration/Partnerships: Members such as SNV, HIVOS, CORDAID, Agriterra and

Oikocredit are shown to be in ongoing collaborations with other members. Reasons

leading to such collaborations and the lessons learned from them would be beneficial to

all. Again, with the exception of ICCO and KIT which do not show any data on

partnerships, there are existing partnerships with local organisations. The number of

partners exhibited by members ranges from one or two to over ten. In some cases,

organisations are partners of more than one APF members. Again, lessons on the

justification for and the experiences from such partnerships would be beneficial to all.

7. Emerging Issues and Development Opportunities

This study brings out six key issues as being of concern to Uganda. It also identifies

current areas of interest for the APF members. The purpose of this chapter is to attempt

a linkage between the most important existing challenges for farmer entrepreneurship in

Uganda and the strategic areas of the APF members. While there are many constraints,

only the most important ones are presented here for possible further discussion. The

task is up to the APF members to evaluate how their strategies can be tailored to

respond to the challenges facing Uganda

Technology It has been pointed out that technology and its adoption are important issues for the

sector. It is also directly linked to the provision of advisory services to farmer

entrepreneurs. There is a general acknowledgement that much of the basic technology is

available and that the challenge is really about making it accessible and available to

farmers. The existing agriculture advisory services under NAADs has been widely

criticised for not reaching all those who need it. Yet food nutrition and security is an

important national objective for Uganda. This is even more critical given the dreaded and

yet expected adverse impact of climate change and the increasing unsustainable

exploitation of land rendering it infertile.

The analysis of current activities of APF members shows that six out of thirteen are

currently involved in knowledge and research with only two members (KIT and WUR)

involved in scientific research and three (KIT, SNV and WUR) are involved in Knowledge

Sharing. Additionally, as technology is related to food production, it is noteworthy that

four (CORDAID, Heifer Nederland, Oxfam Novib and Send a Cow) of the thirteen

members are involved in this category and that they might be attracted to delivery of

technology going forward.

22

Marketing There are a number of issues that affect marketing generally and farmer

entrepreneurship in particular. Issues emerging from this study include the need to

enhance market power of farmers through production of larger volumes for the market,

ensuring acceptable standards of produce, provision of necessary market information

and infrastructure, and adequate capacity competences in export practices. These short

comings call for institutional development and capacity building of farmers and farmer

organisations

There are seven out of thirteen APF members that currently provide Value Chain

enhancing services generally. An equally high number (8 out 13) of APF members are

currently involved in institution and organisational development. As many members of

APF are already involved in capacity building including for marketing and yet these

issues continue to abound, it may be necessary to rethink and reposition for the delivery

of capacity development services for enhancing market management capacity.

Finance The ability of agricultural enterprises and rural households to invest for the long term

and make calculated decisions for risky income flows is partly shaped by accessibility and

cost of financial services. In spite of recent growth in the financial sector, a majority of

smallholders, especially in the rural areas, remain without access to the services they

need to compete in the market.

Lack of suitable development financing schemes for more affordable is still a big

challenge for small and medium enterprises (SMEs). Although the Bank of Uganda did

institute some credit finance schemes, they remained inaccessible to the majority of the

small and medium exporters not only on technical grounds but also because of high

interest rates. Other sources of finance such as micro-finance are too costly and

conventional commercial banks are reluctant to finance agriculture and agro-based

export business due to perceived high risk and unpredictability.

In spite of the importance of financial services to farmer entrepreneurship, only six

members of APF indicate engagement in these services and that they offer only a small

number (four) of products although there are many (grants, savings, accounts, leasing,

warehouse receipts, etc) of them in financial services. This is in spite of the fact that

inadequate access to affordable financial services especially in rural areas is cited by all

stakeholders as a significant hindrance to development and therefore poverty reduction.

Only one member, Oikocredit, shows participation in three of the four products cited.

Four members (Agriterra, CORDAID, Oxfam Novib and Send a Cow) show participation in

only one product. Given the stated high demand for financial services, it is not clear why

only a few members are involved in the provision of this service.

Farmer Organisation Organised as individuals, farmers do not have the power to demand for and deliver large

volumes of inputs and produce, respectively, to enable them negotiate good prices. Even

in the case of existing farmer organisations, it is recognised that they have weak

capacities in terms of institutional (systems and procedures) and legal framework and

technical and managerial capacity. This has impact on the effectiveness of farmer

activities across the value chain including the quantity and quality of production and the

processing and marketing efforts.

23

The affiliation matrix shows that many (eight out thirteen) APF members are involved in

institutional and organisations development activities. Members are engaged in Capacity

Building (seven members) and Technical Assistance and Advisory Services (one

member). Given that many APF members are already involved in capacity development

for farmer organisations, it may be necessary for members to carefully review the

impact of their involvement.

Cross-cutting Issues Many cross-cutting issues are important in the promotion of farmer entrepreneurship

and need to be addressed appropriately. The HIV/AIDS epidemic has had a multiplicity of

negative impacts on agricultural production in Uganda. Women who constitute an

estimated 70 per cent of smallholder farmers and contribute about 70-75 per cent of

agricultural GDP are too important to be positioned inappropriately in the sector and so

are the you whose current participation if too low. Given the Uganda’s heavy

dependence on agriculture, the effects of climate change and the impact of

unsustainable land utilisation practices could clearly put millions of people at greater risk

of poverty and hunger.

Cross cutting issues represent the category least cited by APF members. Only three (out

of 13) members indicate participation in a cross cutting issue. Additionally, only three

cross cutting issues (HIV/AIDS, Gender and Governance) are covered leaving out such

important cross cutting issues as environment, climate change, human rights, etc. It is

therefore clear that there is a need to critically review the handling of cross cutting

issues with a view to strengthening interventions to address them.

24

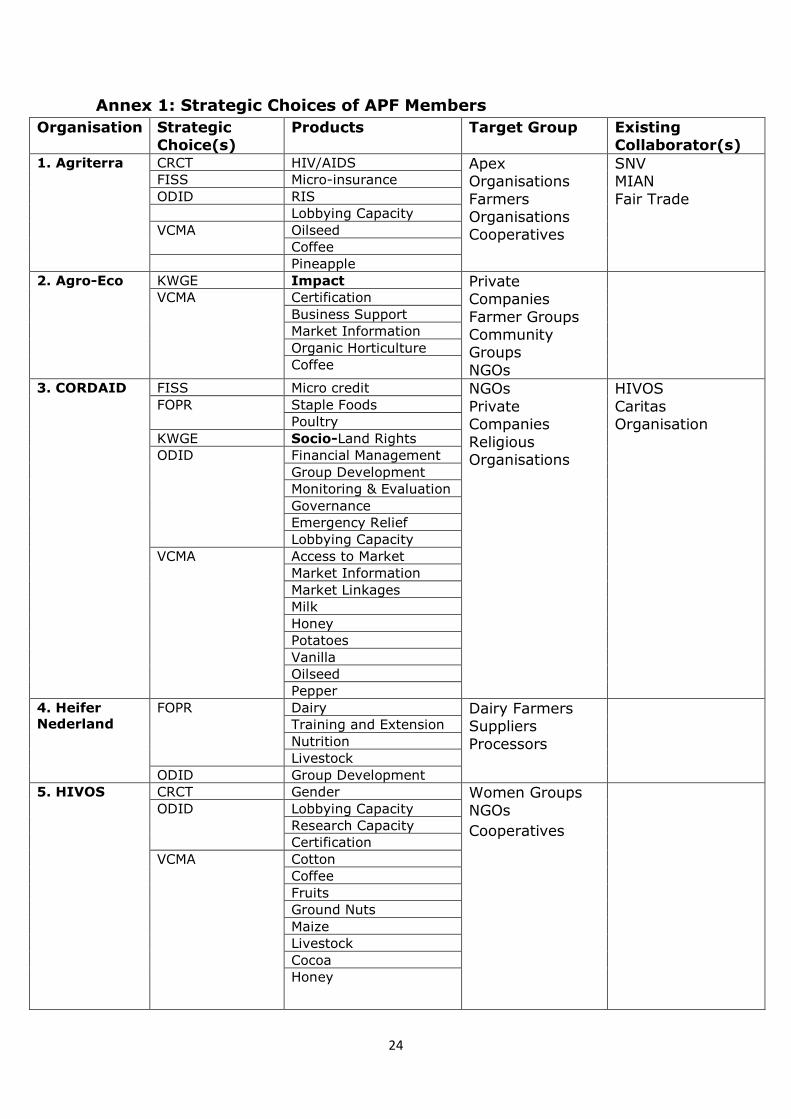

Annex 1: Strategic Choices of APF Members

Organisation Strategic Choice(s)

Products Target Group Existing Collaborator(s)

CRCT HIV/AIDS

FISS Micro-insurance

ODID RIS

Lobbying Capacity

Oilseed VCMA

Coffee

1. Agriterra

Pineapple

Apex Organisations

Farmers Organisations Cooperatives

SNV MIAN

Fair Trade

KWGE Impact

Certification

Business Support

Market Information

Organic Horticulture

2. Agro-Eco

VCMA

Coffee

Private Companies

Farmer Groups Community Groups

NGOs

FISS Micro credit

Staple Foods FOPR

Poultry

KWGE Socio-Land Rights

Financial Management

Group Development

Monitoring & Evaluation

Governance

Emergency Relief

ODID

Lobbying Capacity

Access to Market

Market Information

Market Linkages

Milk

Honey

Potatoes

Vanilla

Oilseed

3. CORDAID

VCMA

Pepper

NGOs

Private Companies

Religious Organisations

HIVOS

Caritas Organisation

Dairy

Training and Extension

Nutrition

FOPR

Livestock

4. Heifer

Nederland

ODID Group Development

Dairy Farmers Suppliers

Processors

CRCT Gender

Lobbying Capacity

Research Capacity

ODID

Certification

Cotton

Coffee

Fruits

Ground Nuts

Maize

Livestock

Cocoa

5. HIVOS

VCMA

Honey

Women Groups

NGOs

Cooperatives

25

Organisation Strategic Choice(s)

Products Target Group Existing Collaborator(s)

Governance

Security

Health Care

Education

CRCT

HIV/AIDS

Loans FISS

Guarantees

Access to Markets

6. ICCO

VCMA

Business Development

NGOs

CRCT Gender and Women

Scientific Research

Biomedical

Social Research

Health

Gender

Education

Culture

Economic Research

Business Development

7. KIT

KWGE

Training

NGOs Universities

Loans

Micro credit

8. Oikocredit FISS

Guarantees

Financial Institutions

Non-Bank F Institutions Cooperatives

NGOs

FISS Micro credit

FOPR Maize

Cassava

Pulses

Vegetables

FOPR

Nuts/Butter

Socio- Applied

Research

KWGE

Land Rights

Trade Lobbying

Group Development

Lobbying Capacity

Access to Markets

9. Oxfam

Novib

ODID

RIS

BDS Providers NGOs

Lobby Groups INGOs

Prolinova

FISS Micro credit

FOPR Livestock Development

Support Training

RIS

Livestock feeds

development

ODID

Group Strengthening

Business Management

Coffee

Livestock

10. Send A

Cow

VCMA

Marketing

INGOs NGOs

Farmers Cooperative

Societies Government Agencies

RRM-K

26

Organisation Strategic Choice(s)

Products Target Group Existing Collaborator(s)

Impact

Sharing-Publishing

KWGE

Sharing- Knowledge

Brokering

Group Development

Training

Technical Assistance

Stakeholder processes

RIS

BDS Provider

Strengthening

ODID

Advisory Services

Horticulture

Apiculture

Dairy

Oilseed

Access to Markets

Market Intelligence

Certification

11. SNV

VCMA

Financing

Apex Organisations

Farmer Groups Private Sector

BDS Providers Financial

Institutions

Government

Agencies

ASPS DANIDA

Agriterra

Capacity Building ODID

Certification

Coffee

Productivity

12.

Solidaridad

VCMA

Quality Enhancement

NGOs Small Farmers

Scientific Research

Biodiversity

Floriculture

Banana

Nature Conservation

Anti-ticks Vaccines

Forestry

Social Research

Hunger

Land use Systems

Nutrient Accounting

Urban Sanitation

Gender Dynamics

13. WUR KWGE

Capacity for Value

Chains

NGOs Small Farmers

Universities Research Institutes

KEY:

1. CRCT- Cross Cutting Issues

2. FISS- Financial Services

3. FOPR- Food Production

4. KWGE- Knowledge and Research

5. ODID- Organisation and Institutional Development

6. VCMA-Value Chain and Market Access

27

Annex 1b: Partners and Areas

Organisation Partner(s) Coverage Target Group Existing Collaborator(s)

1. Agriterra KIDFA, LUDFA, UCA

UNFFE, UOSPA, ACPCU

National Apex Organisations

Farmers

Organisations

Cooperatives

SNV, MIAN

Fair Trade

2. Agro-Eco Bio Uganda, CPNU

IBERO, LOPF (Shares),

Nile Trees Uganda,

Rwot Ber, and

Tree Shade Farming

All areas possible

(currently in

Central, East, Mid-

north)

Private Companies

Farmer Groups

Community Groups

NGOs