Embed Size (px)

Citation preview

FAR Analysis

1

Presentation Compiled By

Akshay Kenkre Gaurav Garg Tejas Dharwadkar

3

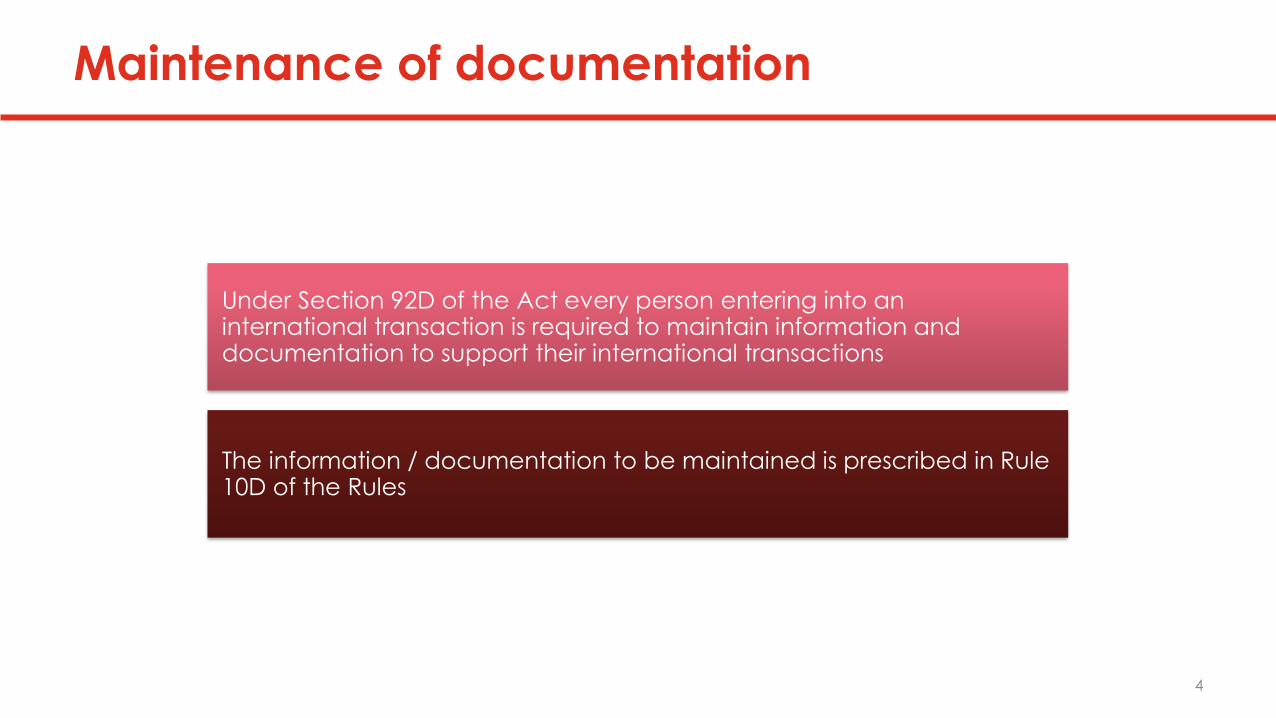

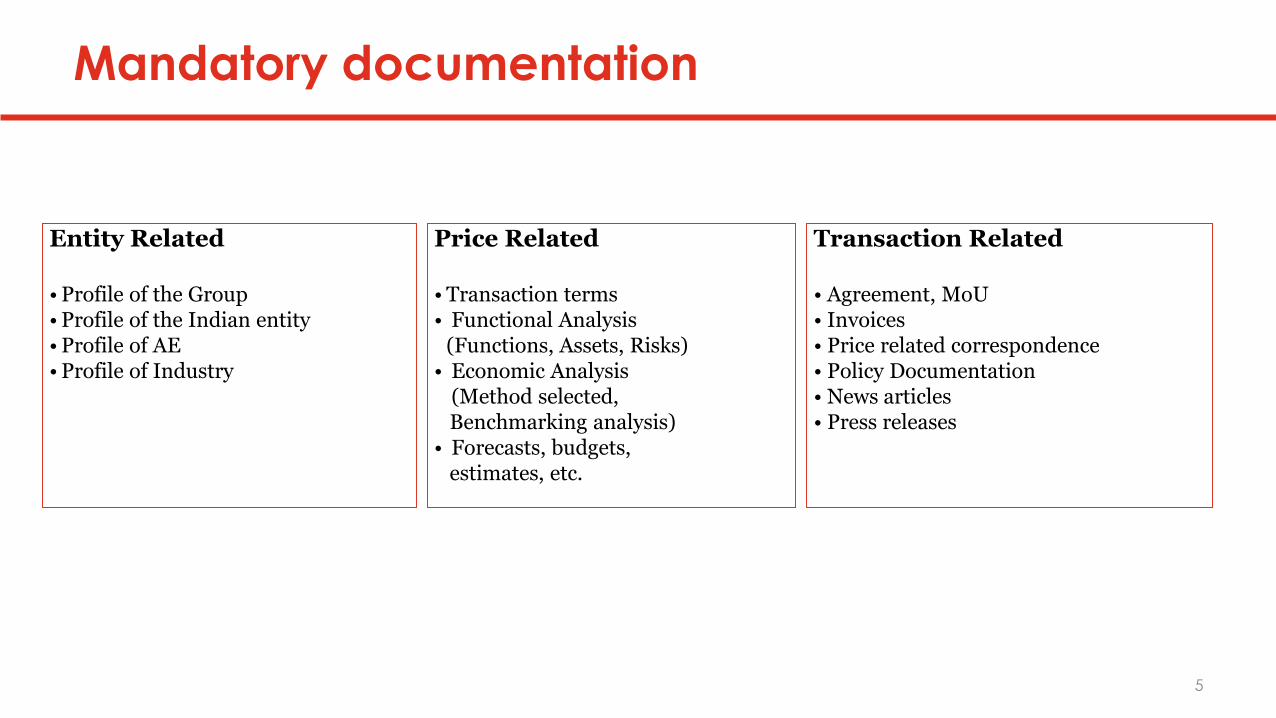

Maintenance of documentation

Under Section 92D of the Act every person entering into an international transaction is required to maintain information and documentation to support their international transactions

The information / documentation to be maintained is prescribed in Rule 10D of the Rules

4

Entity Related

•Profile of the Group•Profile of the Indian entity•Profile of AE •Profile of Industry

Price Related

•Transaction terms• Functional Analysis

(Functions, Assets, Risks)• Economic Analysis

(Method selected, Benchmarking analysis)

• Forecasts, budgets, estimates, etc.

Transaction Related

• Agreement, MoU• Invoices• Price related correspondence• Policy Documentation• News articles• Press releases

Mandatory documentation

5

6

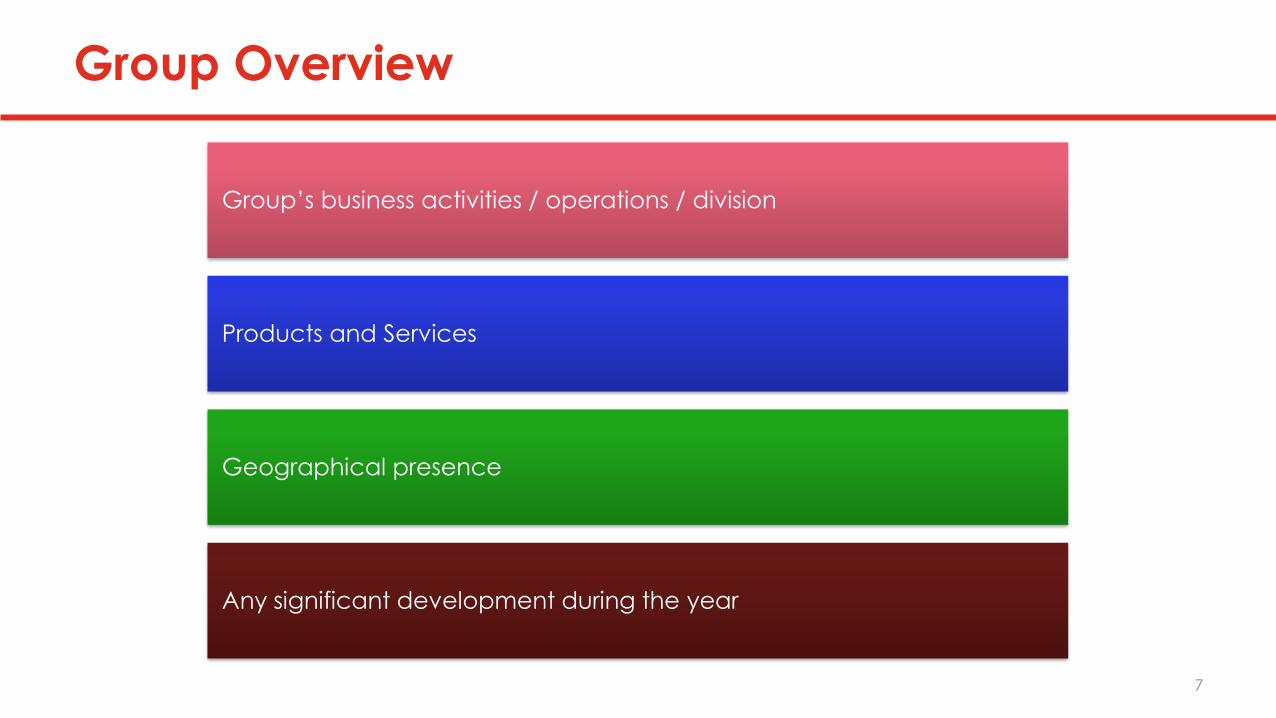

Group Overview

Group’s business activities / operations / division

Products and Services

Geographical presence

Any significant development during the year

7

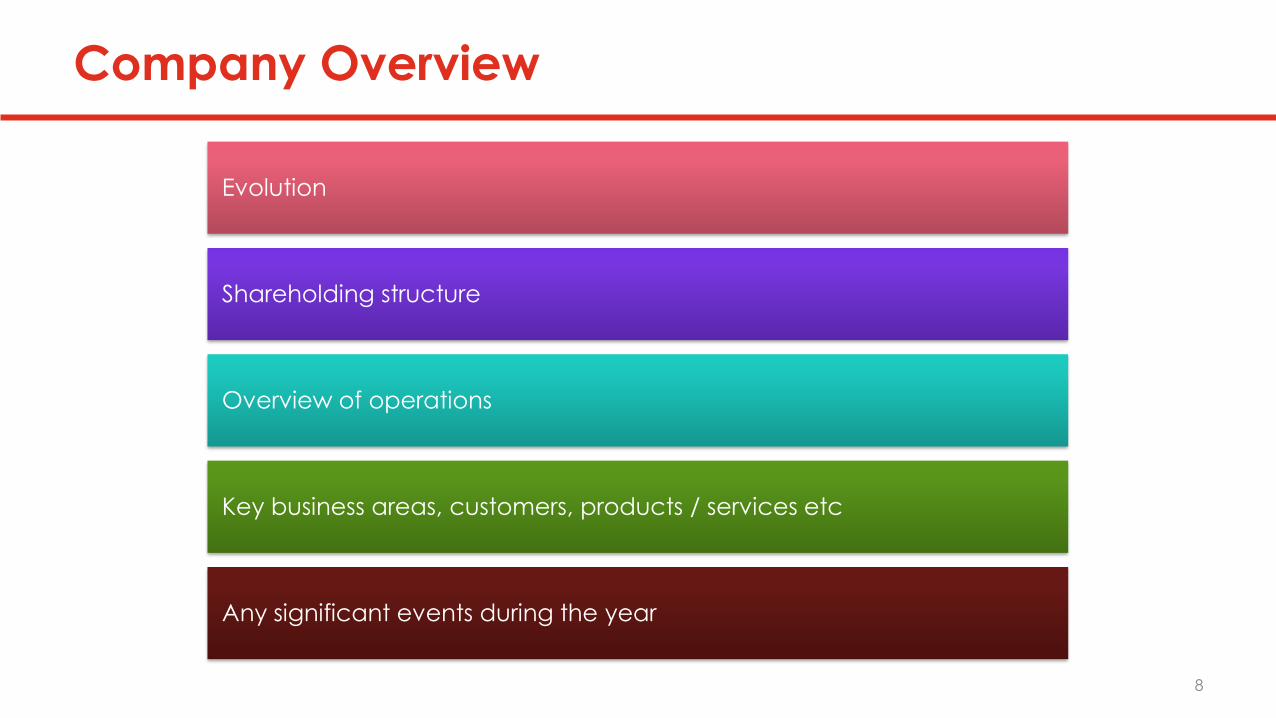

Company Overview

Evolution

Shareholding structure

Overview of operations

Key business areas, customers, products / services etc

Any significant events during the year

8

9

Why do we need Industry Overview (‘IO’)

Assists in understanding the clients relative positioning in the industry vis-à-vis other players

Helps in screening factors when undertaking a comparables search –qualitative analysis

Provides overall justification of clients financial results

10

10

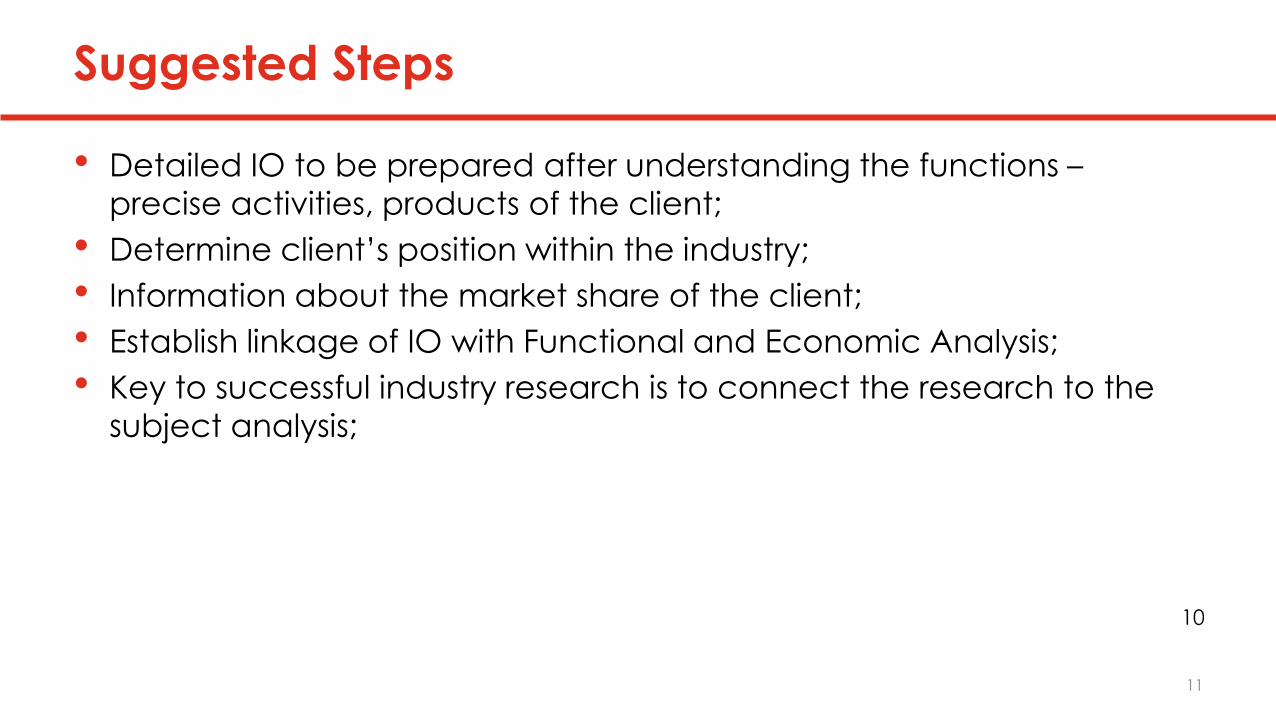

Suggested Steps

• Detailed IO to be prepared after understanding the functions –

precise activities, products of the client;

• Determine client’s position within the industry;

• Information about the market share of the client;

• Establish linkage of IO with Functional and Economic Analysis;

• Key to successful industry research is to connect the research to the

subject analysis;

11

12

• The source should be a publicly available and a reliable source;

• Assess the validity and reliability of the source;

• Few sources that one can consider in preparing an IO (not exhaustive):

−Annual report of client company – Management Discussion & Analysis (MD&A),

−Annual reports of clients competitors (names of competitors not to be

mentioned)

−Ask the client to provide industry information / presentations etc.

−Client website,

−Internet – Google,

−Material published in the trade journals and magazines etc.

−Newspaper articles,

−Specific subscriptions to magazines, trade journals, NASSCOM publications etc.

−Indian Brand Equity Foundation (IBEF) website

−www.business.gov.in

Sources of Research

12

12

Structure of IO

• About the industry (Introduction, Background)

• Size and Structure

• Industry drivers

• Competitive landscape

• Regulatory environment

• Key trends

• Key challenges

• Way forward or Outlook

• Summary

13

13

Do’s and Don’ts...

Do’s

• Understand the clients products, their nature i.e. if they are complimentary on

other products etc., and decide on the industry/industries that need to be

analyzed and documented;

• Always mention the source in the report such that we can easily locate the same in future;

• Customize the IO to your specific client in case of using the standard IO’s;

• Use of Pie charts / Diagrams / Bar charts will be helpful;

• Keep the IO as specific, crisp/short as possible;

• Take a look at last years IO to keep in line with long term statements, sources mentioned in last years IO etc.

14

14

...Do’s and Don’ts

Don’ts

• Copy-paste previous years IO as it is;

• Copy-paste standard IO’s blindly;

• Include statements in the IO which can be contradictory to our study;

• Leave the IO for the end of the assignment;

• Use too many technical jargons and figures;

• Document prices or price trends without being doubly sure of its

consequences.

15

16

Tested PartyIndustry

Overview

Comparability

Analysis

Functional

Analysis

Transfer

Pricing

Methods

Transfer Pricing Jigsaw

17

Functional Analysis

Introduction

• Critical part in establishing ALP

• Gathering information and analyzing controlled transactions to ensure

the parties and transactions are understood

• Understanding of ‘Economically Significant Factors’

• Helps appropriate assessment of comparability

• Important role in selection of TP Method and tested party

• Fixation of price by facilitating comparability

• Testing: One sided view; Functional Analysis: Two sided view

18

Functional Analysis

Economically Significant Factors

The profits a company makes are dependent on:

• The business environment it operates in

• The strategy it pursues in that environment

• The functions they engage in

• The assets they employ

• The risks they undertake

E (P) = ƒ (F,A,R)

19

20

Introduction

Focus on practical aspects of FAR

Aim is to build documentation highlighting key

functions, Assets and Risks

FAR is one of the most important aspects of TP as

it involves meetings with employees at all levels

We will understand practical background work

and front end work that goes in preparation of

FAR

Preparing for FAR

21

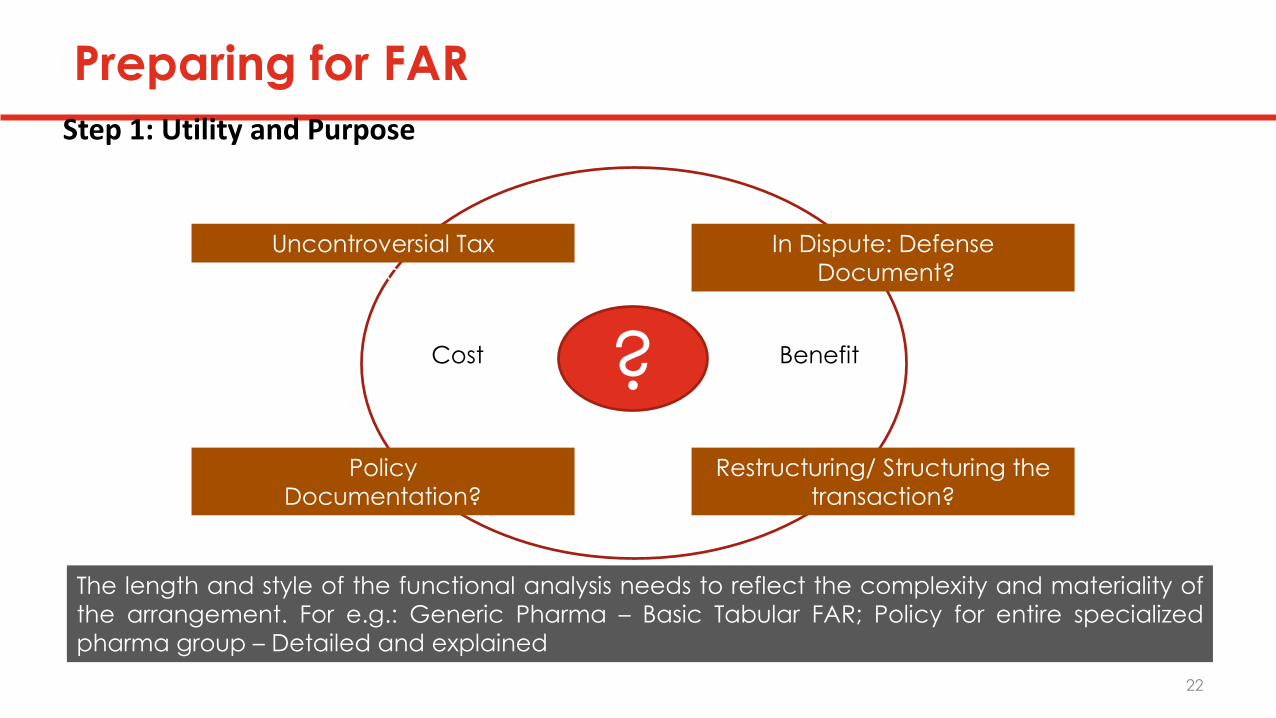

Step 1: Utility and Purpose

?

The length and style of the functional analysis needs to reflect the complexity and materiality of

the arrangement. For e.g.: Generic Pharma – Basic Tabular FAR; Policy for entire specialized

pharma group – Detailed and explained

Uncontroversial Tax

compliance?

In Dispute: Defense

Document?

Policy

Documentation?

Restructuring/ Structuring the

transaction?

Cost Benefit

Preparing for FAR

22

Step 2: Navigator

Navigator: One who arranges interviews and acts as a bridge between the interviewer and

interviewee

Traits of Navigator:

• Good understanding of overall business

• Understands Transfer Pricing and its importance

• Well connected in the organization

• Well Respected in the organization

• Knows internal processes

• Could also highlight business weakness and failures – Helps to identify risk

• Is responsible for Transfer Pricing

• E.g.: Tax Heads, Managers, CFOs, Business Controllers, Operational heads

Preparing for FAR

23

Step 3: Fact gathering Obtain relevant agreements and other documentation-

• Agreements with related

companies and third parties

• Business plans and Budgets

• Review and document the review

in a summary form

• Use organization charts to plan the

interviewing process

• Send questionnaires to people not

being interviewed

• Interview key personnel

• Financials and management accounts

Preparing for FAR

24

Step 4: Interview Team

Ideally 3 participants from Interview team

1. Interview Leader

2. Note Taker

3. Navigator

One can follow a ‘break up’ approach or a ‘big bang’ approach for an interview

• Introduction of the interview team

• Purpose of interview – Either by leader or Navigator

• Flexibility in questioning

• Bringing back on track

• Spot issues, guide note taker

• Clarify issues, give back ground

• Capturing of details by note taker

• Keep track of to-do

Preparing for FAR

25

Step 4: The Interview

• Taking interview is an art than science – Communication and Clarity

• Planning is the key

• Identify the persons to be interviewed prior hand

• Understand the basic business model from the Navigator

• Preparation and circulation of questionnaire / agenda

• Explain importance of documentation and confidentiality

• Ask open ended questions: “ what is the process involved in…..”

• Let the speaker share experiences and instances

• If technical jargons are not understood, ask for a simpler explanation

• Stick to timeliness

• Post interview- Summarize the understanding and ask for verbal confirmation

• Document the interview and ask for written confirmation

• In case of recording – INFORM and TAKE PERMISSION !!!

Preparing for FAR

26

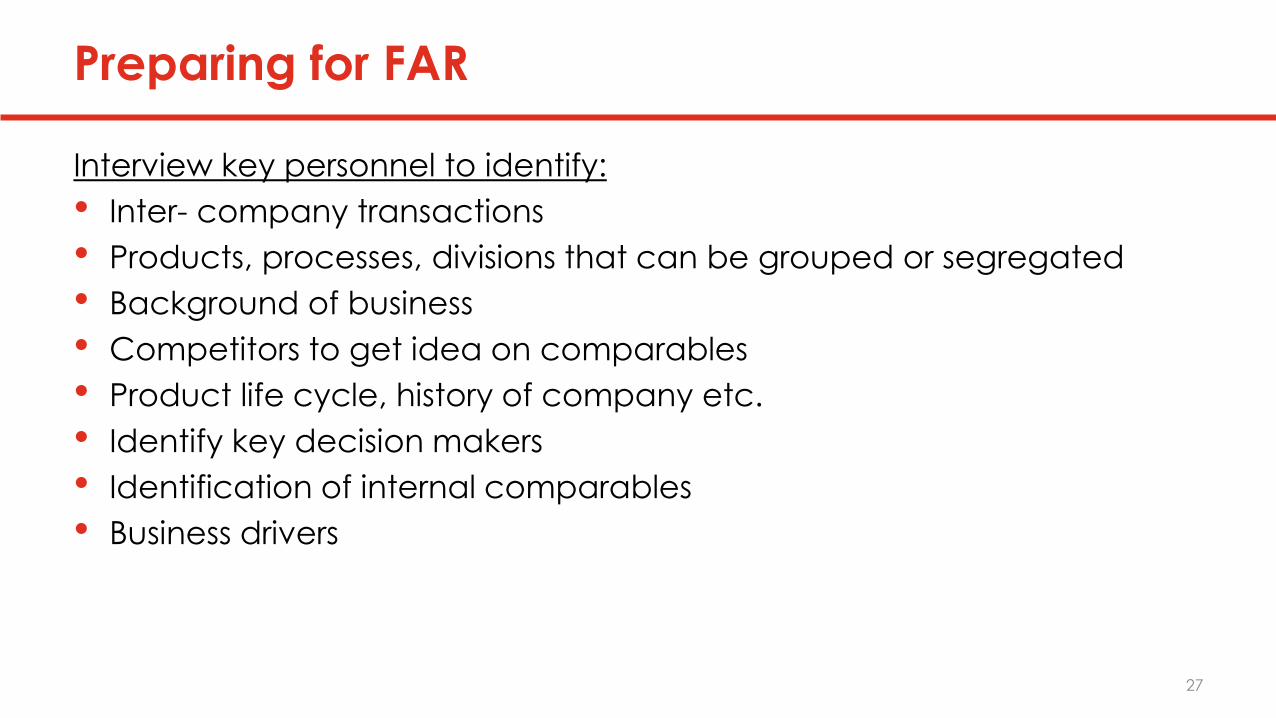

Preparing for FAR

Interview key personnel to identify:

• Inter- company transactions

• Products, processes, divisions that can be grouped or segregated

• Background of business

• Competitors to get idea on comparables

• Product life cycle, history of company etc.

• Identify key decision makers

• Identification of internal comparables

• Business drivers

27

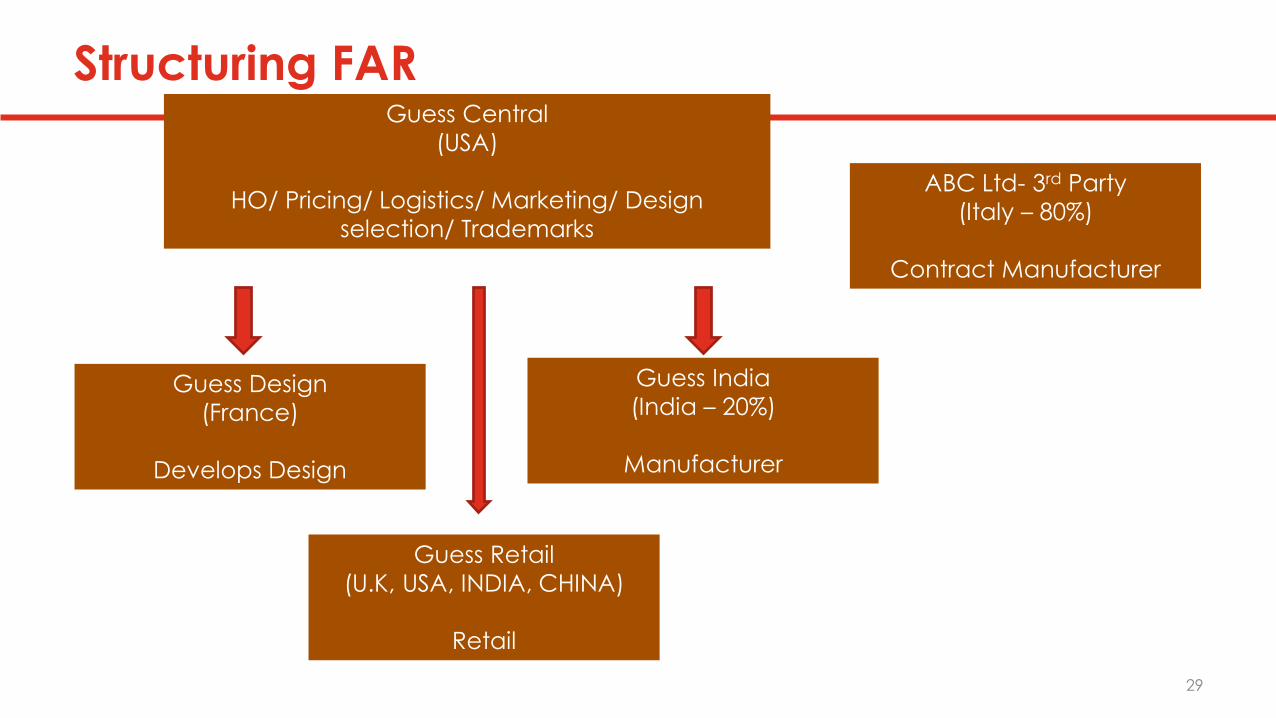

28

Guess Central

(USA)

HO/ Pricing/ Logistics/ Marketing/ Design

selection/ Trademarks

Guess Design

(France)

Develops Design

Guess India

(India – 20%)

Manufacturer

ABC Ltd- 3rd Party

(Italy – 80%)

Contract Manufacturer

Guess Retail

(U.K, USA, INDIA, CHINA)

Retail

Structuring FAR

29

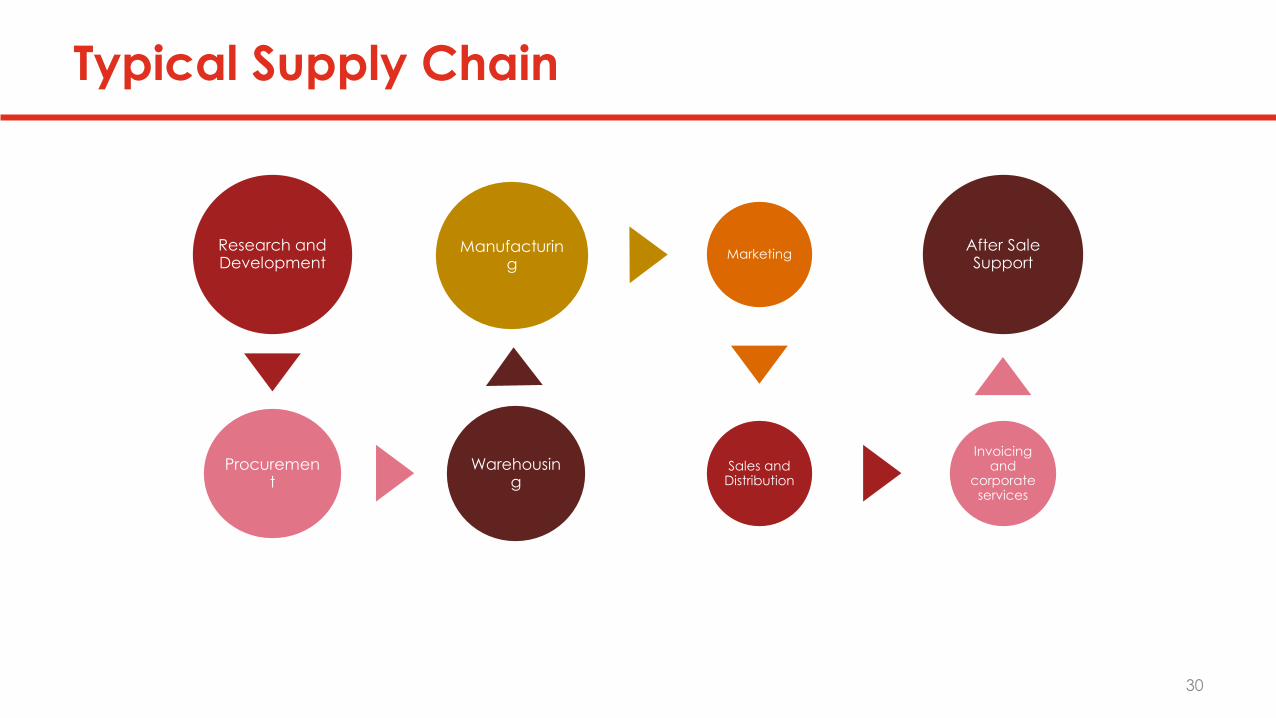

Typical Supply Chain

Research and Development

Procurement

Warehousing

Manufacturing

Marketing

Sales and Distribution

Invoicing and

corporate services

After Sale Support

30

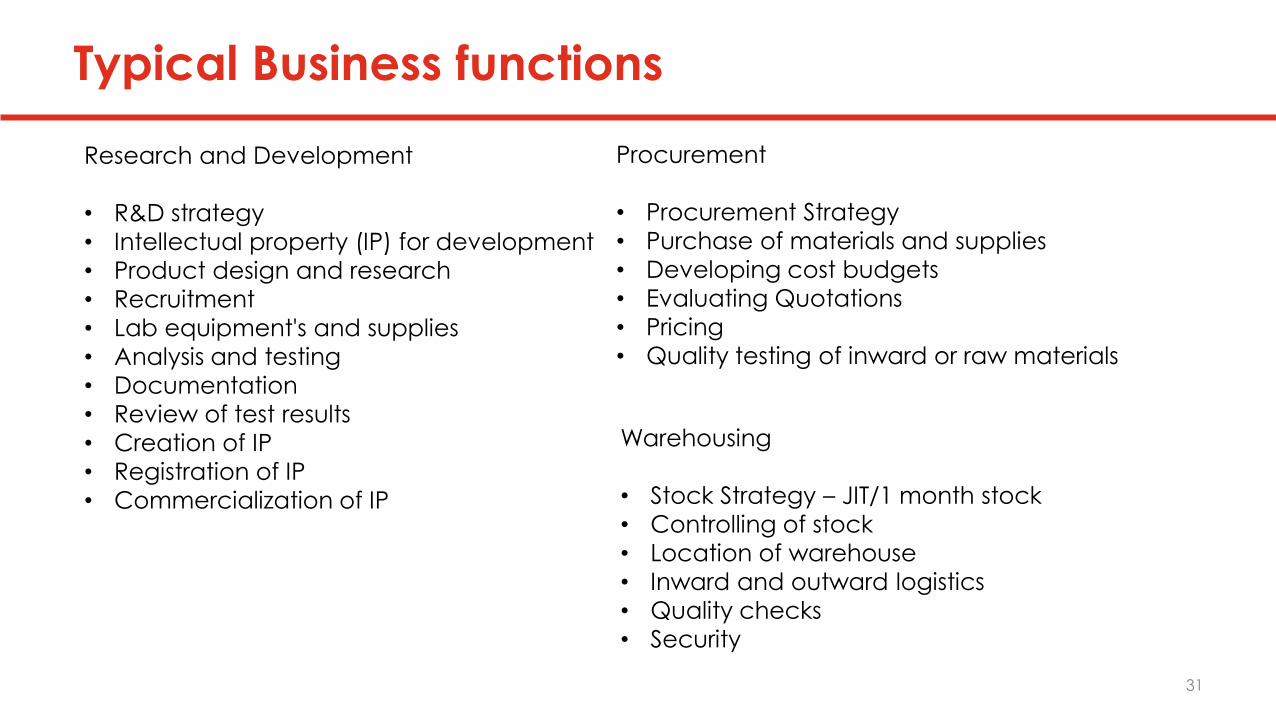

Research and Development

• R&D strategy

• Intellectual property (IP) for development

• Product design and research

• Recruitment

• Lab equipment's and supplies

• Analysis and testing

• Documentation

• Review of test results

• Creation of IP

• Registration of IP

• Commercialization of IP

Procurement

• Procurement Strategy

• Purchase of materials and supplies

• Developing cost budgets

• Evaluating Quotations

• Pricing

• Quality testing of inward or raw materials

Warehousing

• Stock Strategy – JIT/1 month stock

• Controlling of stock

• Location of warehouse

• Inward and outward logistics

• Quality checks

• Security

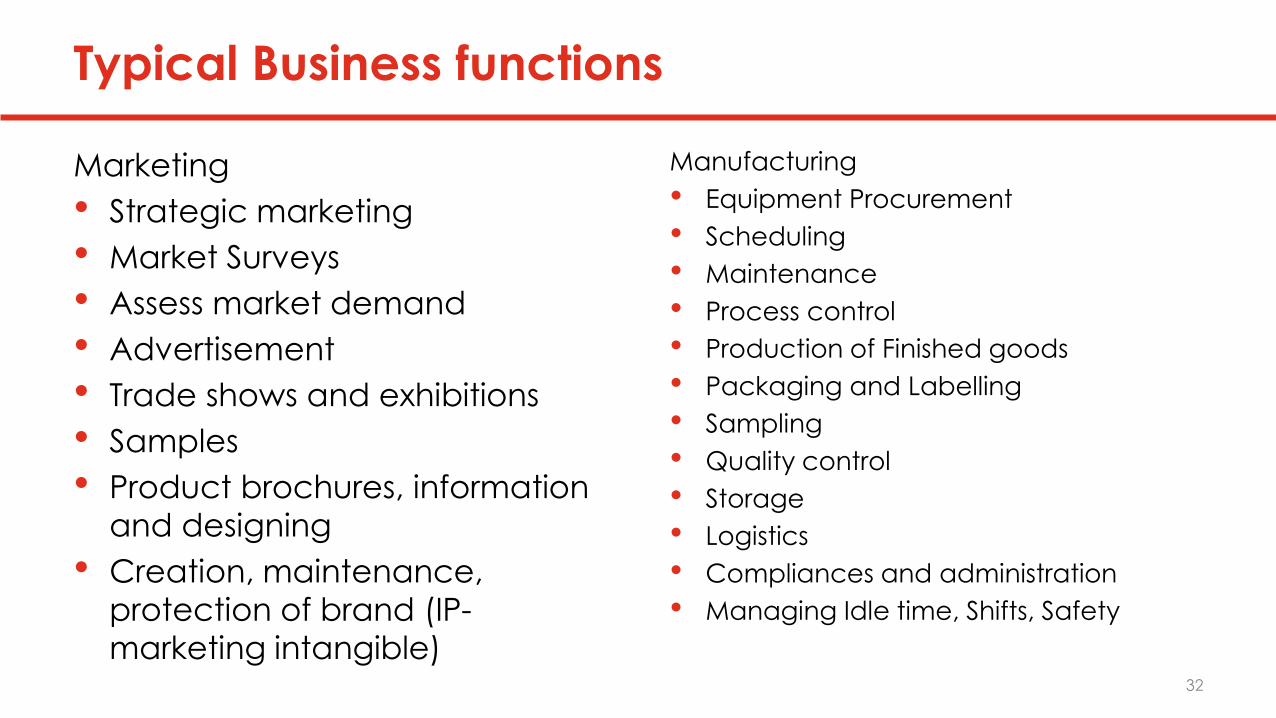

Typical Business functions

31

Marketing

• Strategic marketing

• Market Surveys

• Assess market demand

• Advertisement

• Trade shows and exhibitions

• Samples

• Product brochures, information

and designing

• Creation, maintenance,

protection of brand (IP-

marketing intangible)

Manufacturing

• Equipment Procurement

• Scheduling

• Maintenance

• Process control

• Production of Finished goods

• Packaging and Labelling

• Sampling

• Quality control

• Storage

• Logistics

• Compliances and administration

• Managing Idle time, Shifts, Safety

Typical Business functions

32

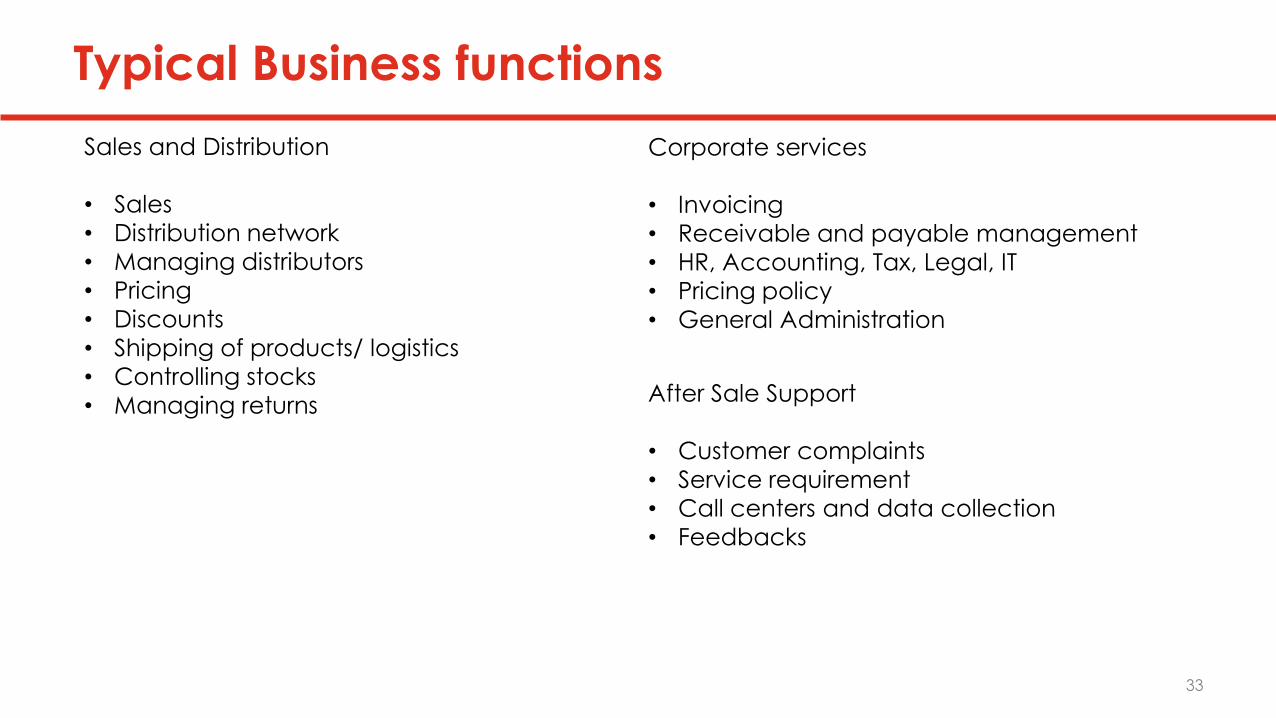

Corporate services

• Invoicing

• Receivable and payable management

• HR, Accounting, Tax, Legal, IT

• Pricing policy

• General Administration

Sales and Distribution

• Sales

• Distribution network

• Managing distributors

• Pricing

• Discounts

• Shipping of products/ logistics

• Controlling stocks

• Managing returnsAfter Sale Support

• Customer complaints

• Service requirement

• Call centers and data collection

• Feedbacks

Typical Business functions

33

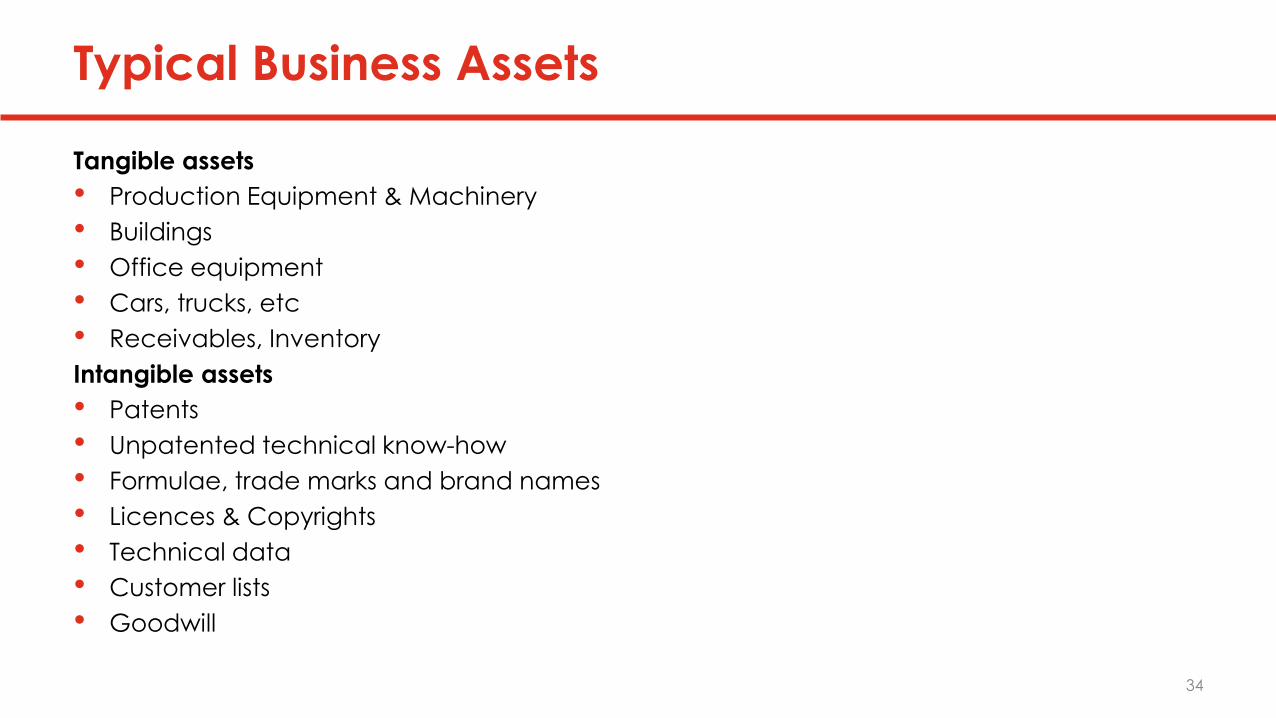

Typical Business Assets

Tangible assets

• Production Equipment & Machinery

• Buildings

• Office equipment

• Cars, trucks, etc

• Receivables, Inventory

Intangible assets

• Patents

• Unpatented technical know-how

• Formulae, trade marks and brand names

• Licences & Copyrights

• Technical data

• Customer lists

• Goodwill

34

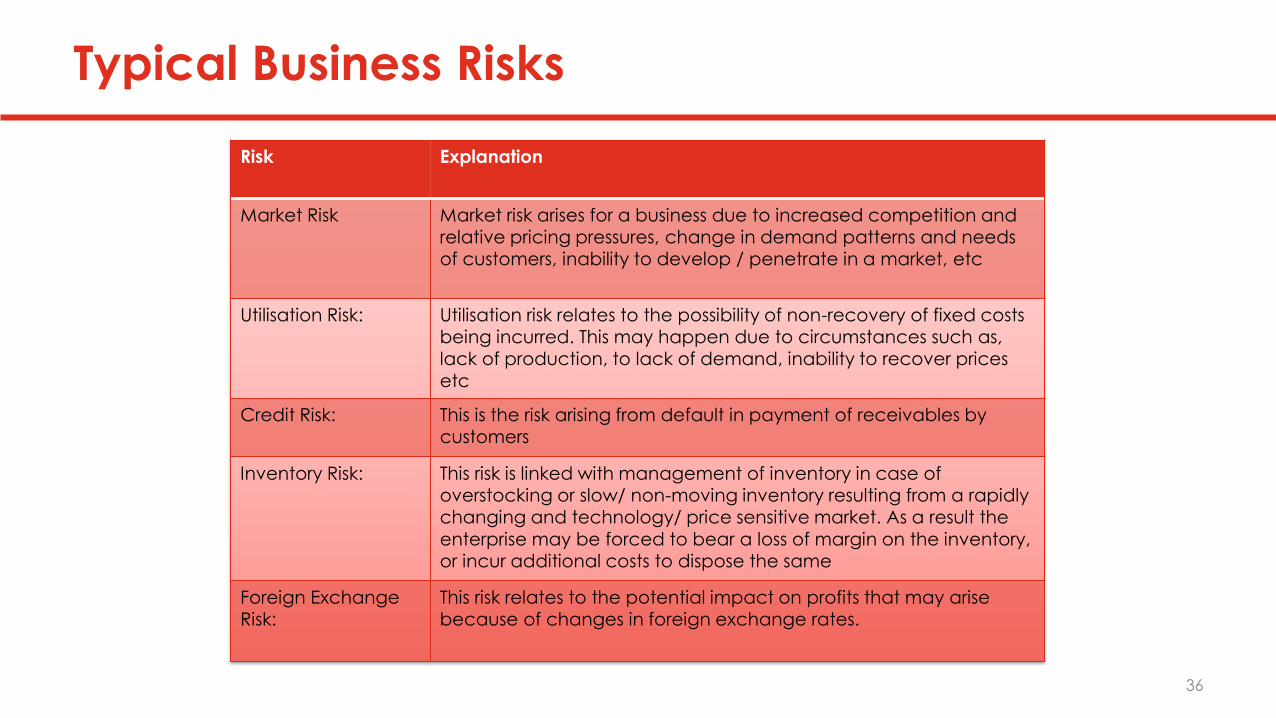

Typical Business Risks

• Market risk: volume, mix,

price

• Inventory risks: raw

materials, work in

progress and finished

goods

• Defective products and

warranty

• Credit risk

• Product liability risk

• Foreign exchange risk

• Environmental risk

35

Typical Business Risks

Risk Explanation

Market Risk Market risk arises for a business due to increased competition and

relative pricing pressures, change in demand patterns and needs

of customers, inability to develop / penetrate in a market, etc

Utilisation Risk: Utilisation risk relates to the possibility of non-recovery of fixed costs

being incurred. This may happen due to circumstances such as,

lack of production, to lack of demand, inability to recover prices

etc

Credit Risk: This is the risk arising from default in payment of receivables by

customers

Inventory Risk: This risk is linked with management of inventory in case of

overstocking or slow/ non-moving inventory resulting from a rapidly

changing and technology/ price sensitive market. As a result the

enterprise may be forced to bear a loss of margin on the inventory,

or incur additional costs to dispose the same

Foreign Exchange

Risk:

This risk relates to the potential impact on profits that may arise

because of changes in foreign exchange rates.

36

37

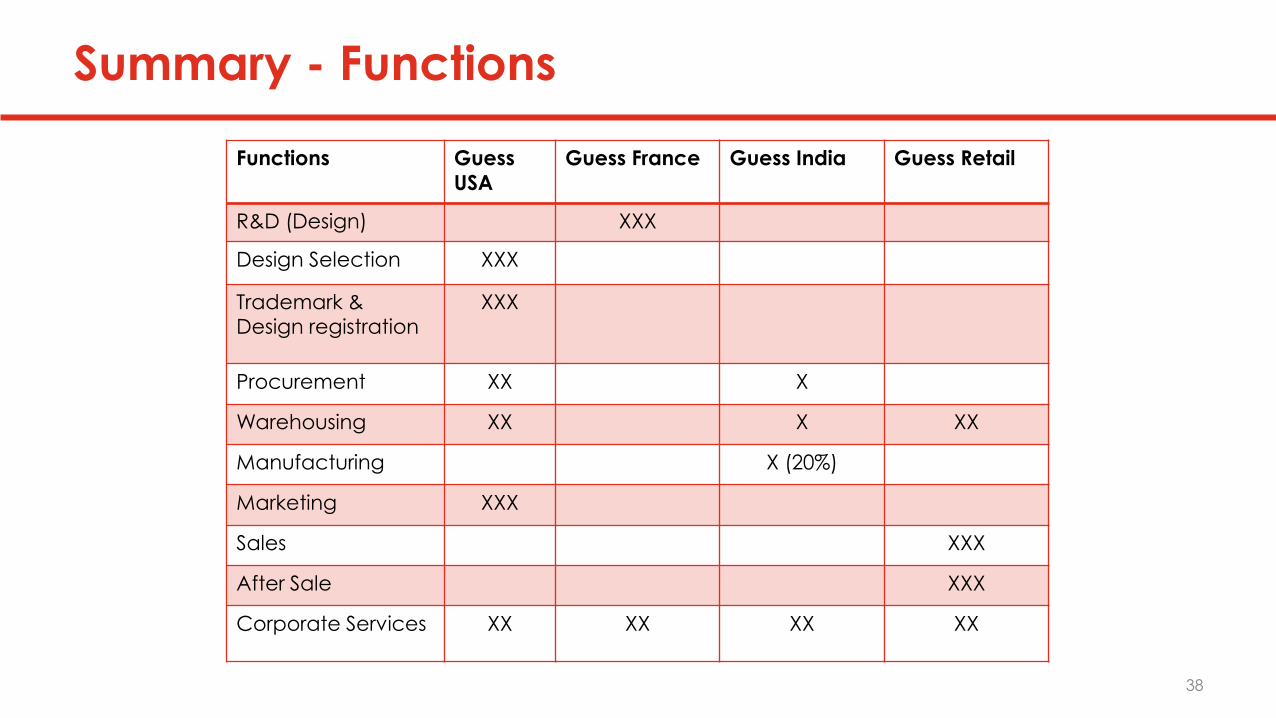

Summary - Functions

Functions Guess

USA

Guess France Guess India Guess Retail

R&D (Design) XXX

Design Selection XXX

Trademark & Design registration

XXX

Procurement XX X

Warehousing XX X XX

Manufacturing X (20%)

Marketing XXX

Sales XXX

After Sale XXX

Corporate Services XX XX XX XX

38

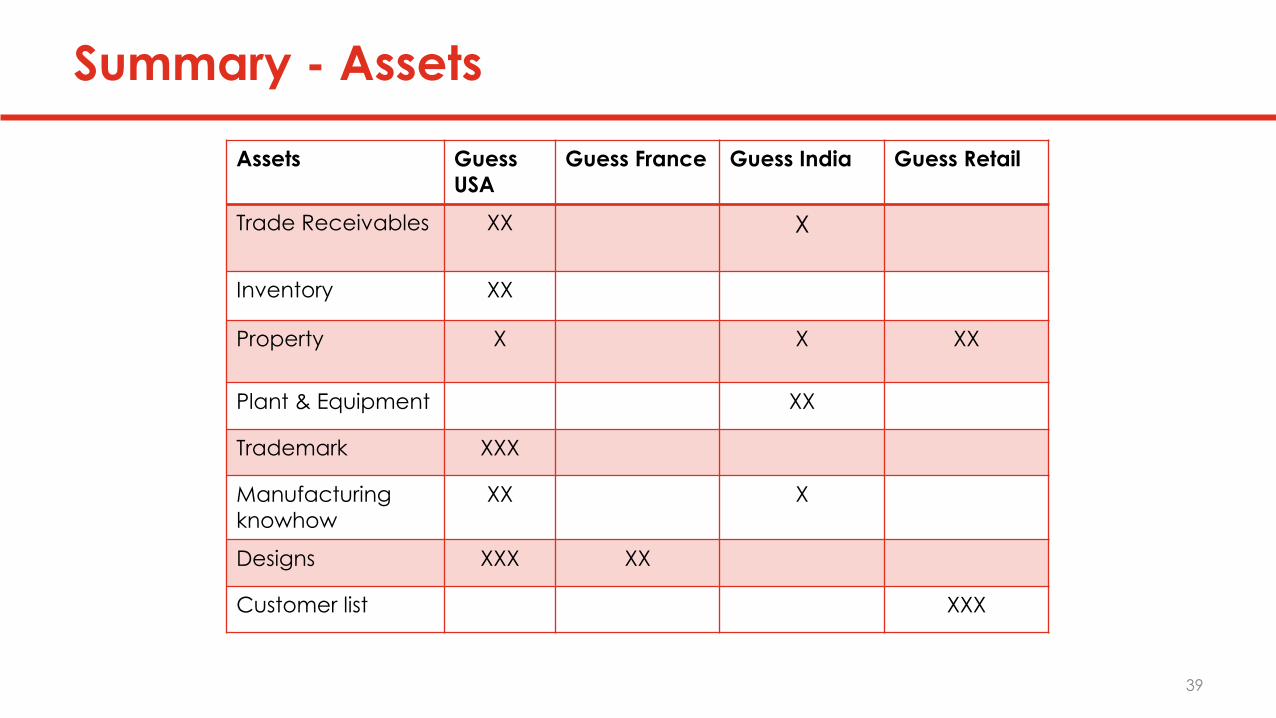

Summary - Assets

Assets Guess

USA

Guess France Guess India Guess Retail

Trade Receivables XX X

Inventory XX

Property X X XX

Plant & Equipment XX

Trademark XXX

Manufacturing

knowhow

XX X

Designs XXX XX

Customer list XXX

39

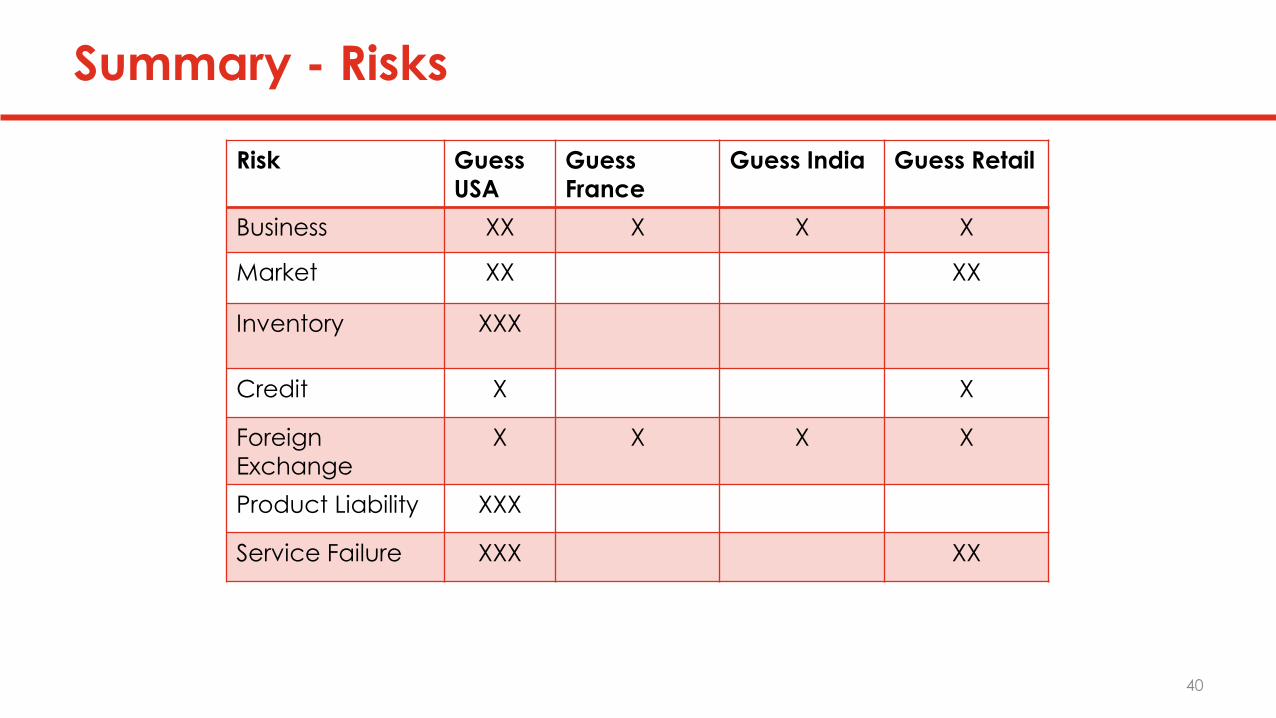

Summary - Risks

Risk Guess

USA

Guess

France

Guess India Guess Retail

Business XX X X X

Market XX XX

Inventory XXX

Credit X X

Foreign

Exchange

X X X X

Product Liability XXX

Service Failure XXX XX

40

41

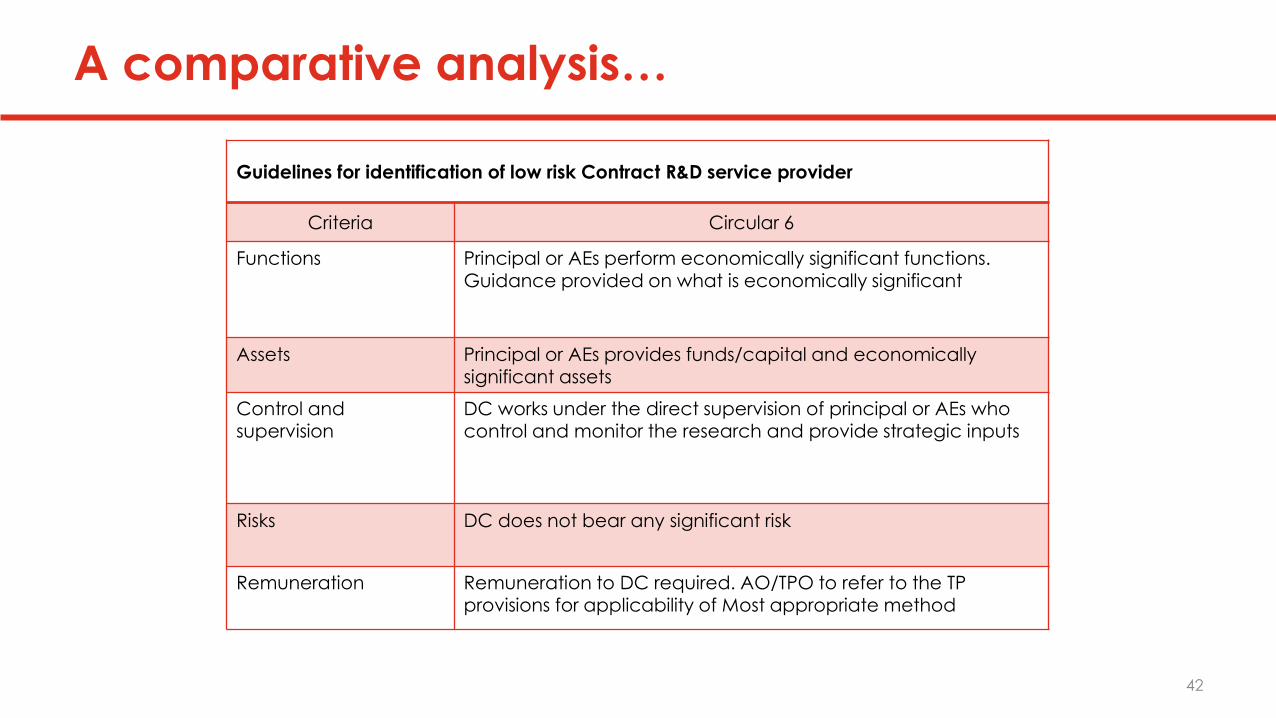

A comparative analysis…

Guidelines for identification of low risk Contract R&D service provider

Criteria Circular 6

Functions Principal or AEs perform economically significant functions. Guidance provided on what is economically significant

Assets Principal or AEs provides funds/capital and economically significant assets

Control and supervision

DC works under the direct supervision of principal or AEs who control and monitor the research and provide strategic inputs

Risks DC does not bear any significant risk

Remuneration Remuneration to DC required. AO/TPO to refer to the TP provisions for applicability of Most appropriate method

42

43

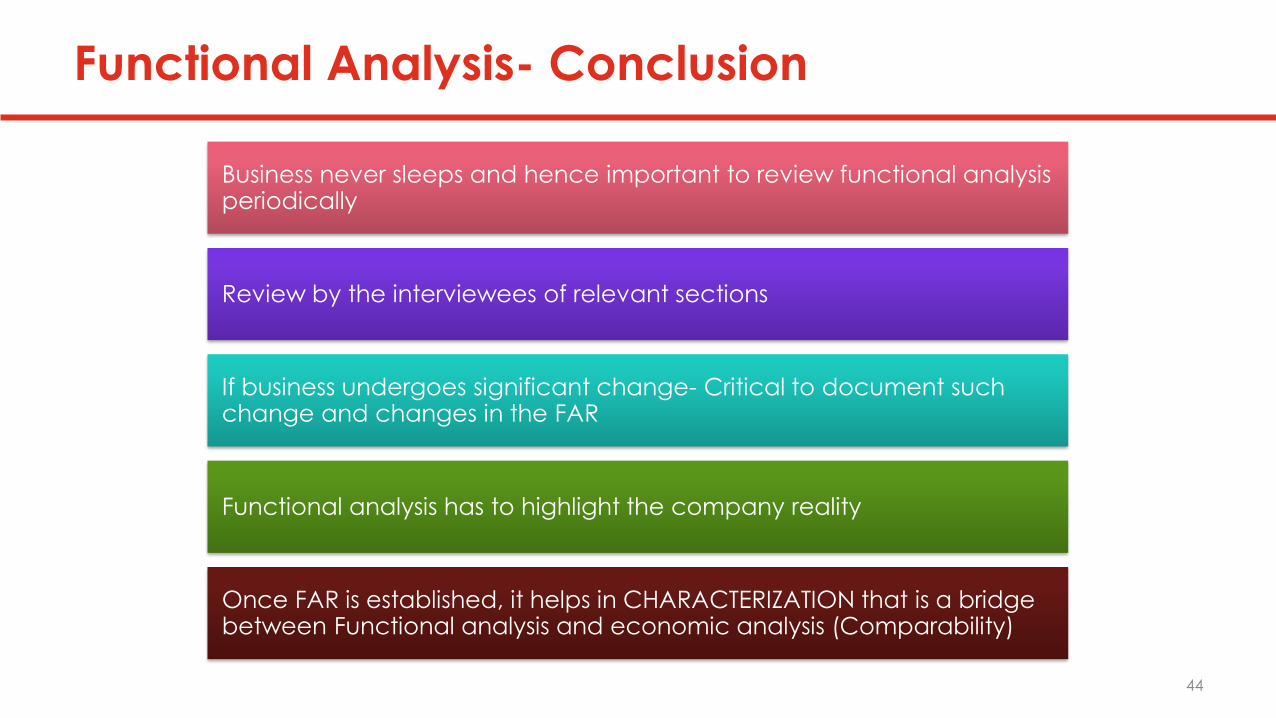

Functional Analysis- Conclusion

Business never sleeps and hence important to review functional analysis periodically

Review by the interviewees of relevant sections

If business undergoes significant change- Critical to document such change and changes in the FAR

Functional analysis has to highlight the company reality

Once FAR is established, it helps in CHARACTERIZATION that is a bridge between Functional analysis and economic analysis (Comparability)

44

45

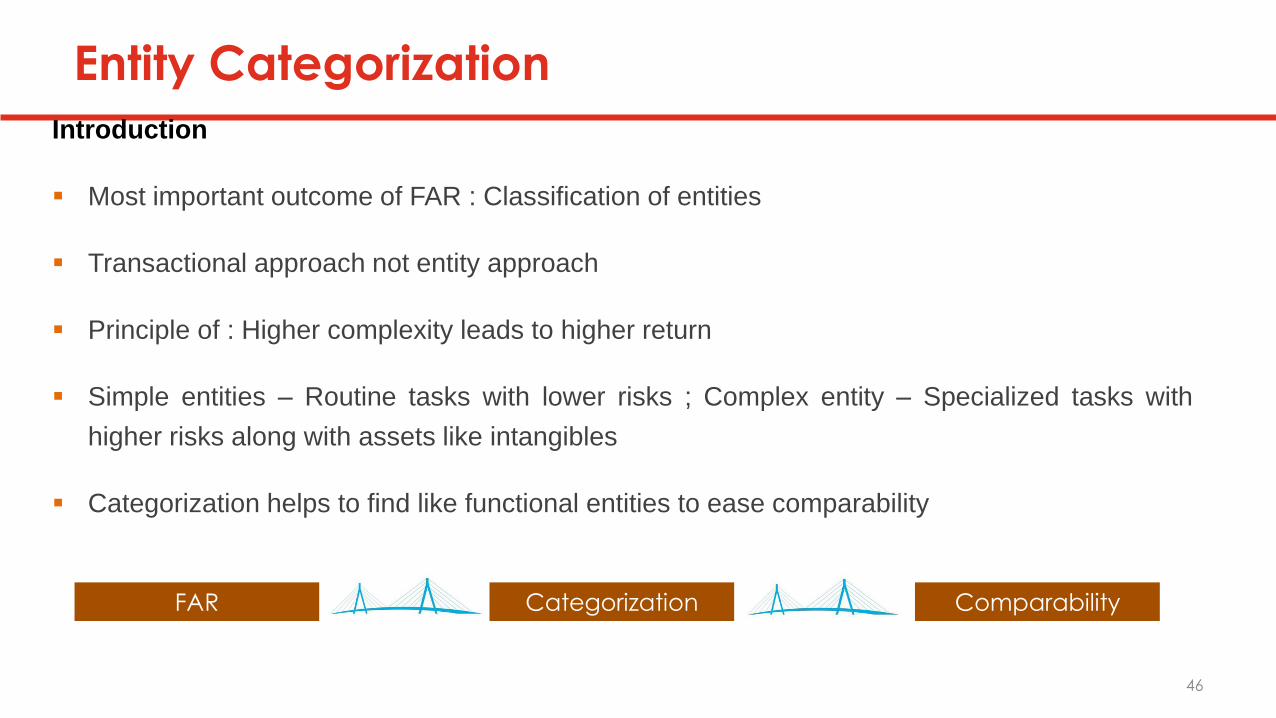

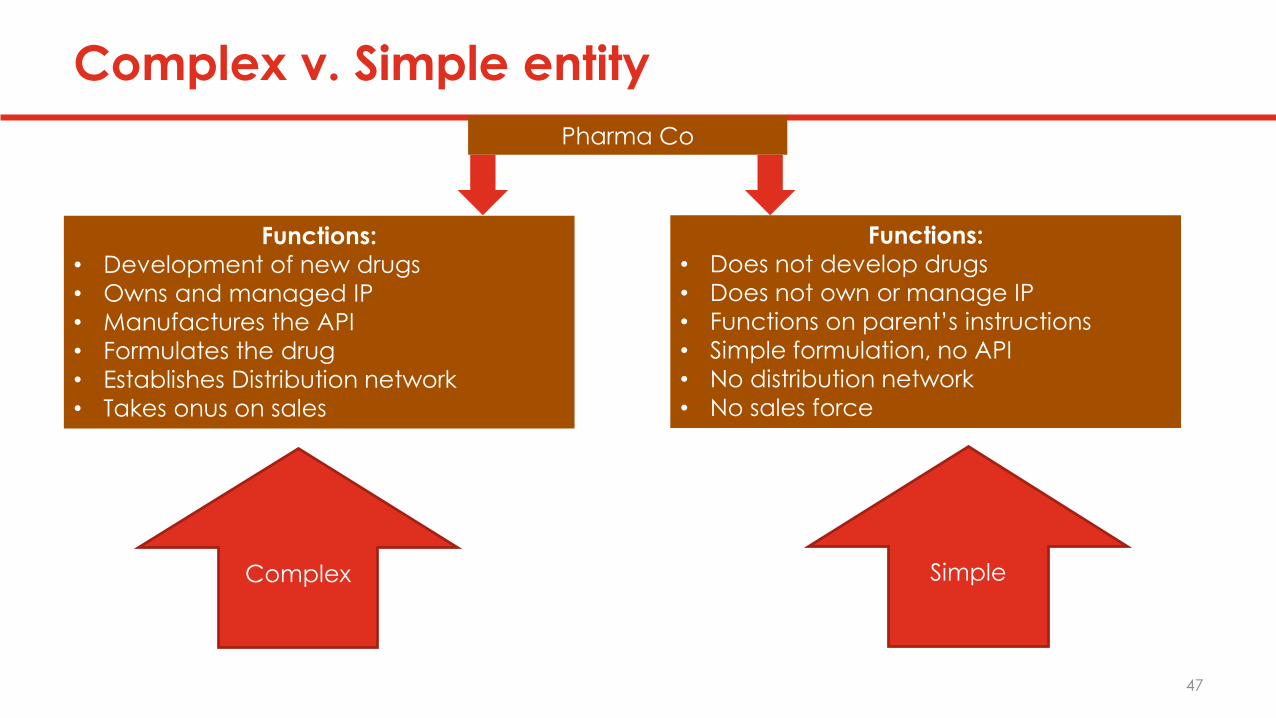

Introduction

▪ Most important outcome of FAR : Classification of entities

▪ Transactional approach not entity approach

▪ Principle of : Higher complexity leads to higher return

▪ Simple entities – Routine tasks with lower risks ; Complex entity – Specialized tasks with

higher risks along with assets like intangibles

▪ Categorization helps to find like functional entities to ease comparability

FAR Categorization Comparability

Entity Categorization

46

Functions:

• Development of new drugs

• Owns and managed IP

• Manufactures the API

• Formulates the drug

• Establishes Distribution network

• Takes onus on sales

Pharma Co

Functions:

• Does not develop drugs

• Does not own or manage IP

• Functions on parent’s instructions

• Simple formulation, no API

• No distribution network

• No sales force

Complex Simple

Complex v. Simple entity

47

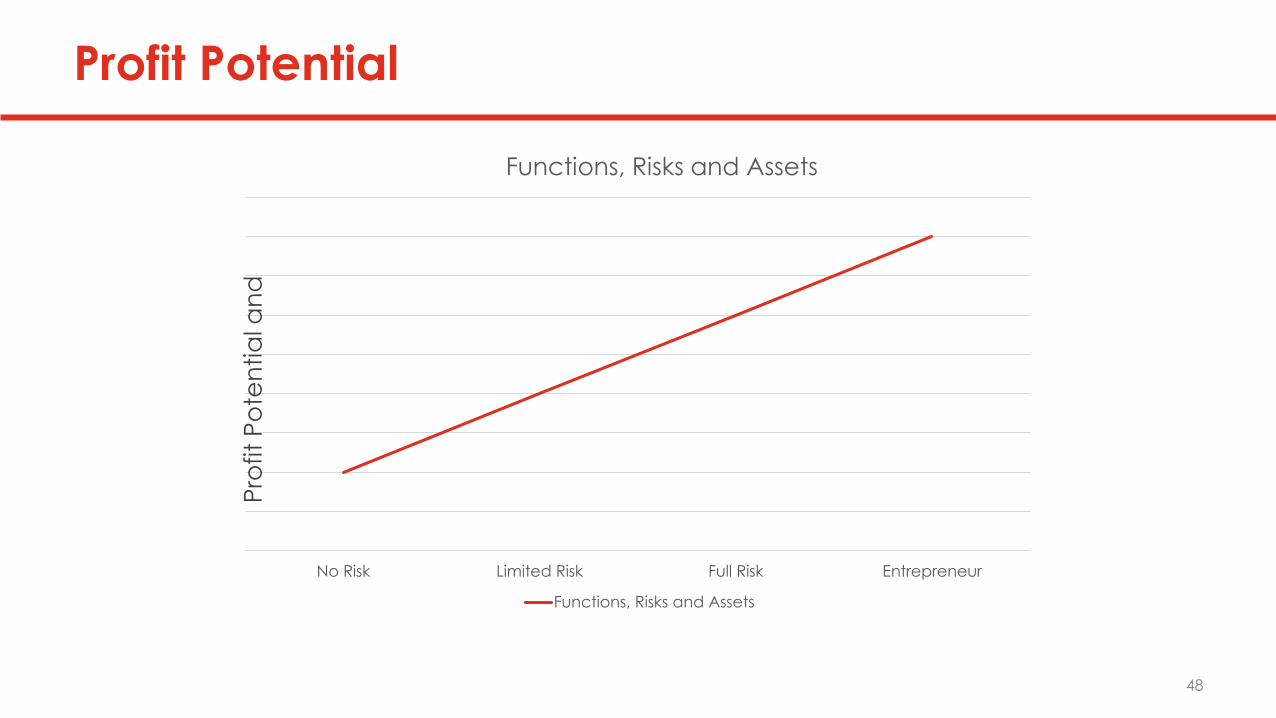

Profit Potential

No Risk Limited Risk Full Risk Entrepreneur

Functions, Risks and Assets

Functions, Risks and Assets

Pro

fit

Po

ten

tia

l an

d

48

Typical Distribution function

Sales Support Sales Agent LRD Licensed Distributor Full Risk

Functions, Risks and Assets

Functions, Risks and Assets

Pro

fit

Po

ten

tia

l an

d

49

Sales Support

• Provides market information

• Common link between principal and customer

• No title to product or stock

• No substantial risk

• Facilitation of distribution but has no control over distribution

• Value Driver is : Cost

50

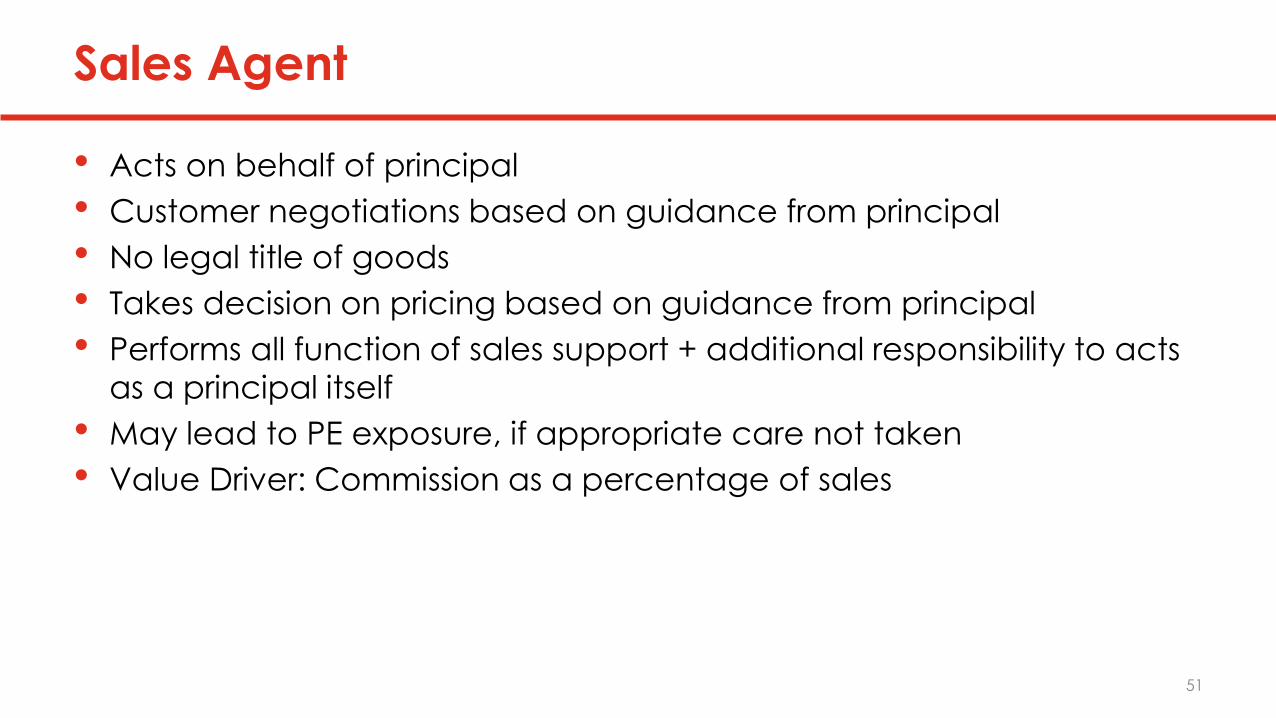

Sales Agent

• Acts on behalf of principal

• Customer negotiations based on guidance from principal

• No legal title of goods

• Takes decision on pricing based on guidance from principal

• Performs all function of sales support + additional responsibility to acts

as a principal itself

• May lead to PE exposure, if appropriate care not taken

• Value Driver: Commission as a percentage of sales

51

Limited Risk Distributor

Enters in contract on its own behalf

Makes sales inn its own name

Has a distribution network

Risk if inventory, losses, warranty, currency, bad debts would be restricted

Value Driver: Limited LRD profits

52

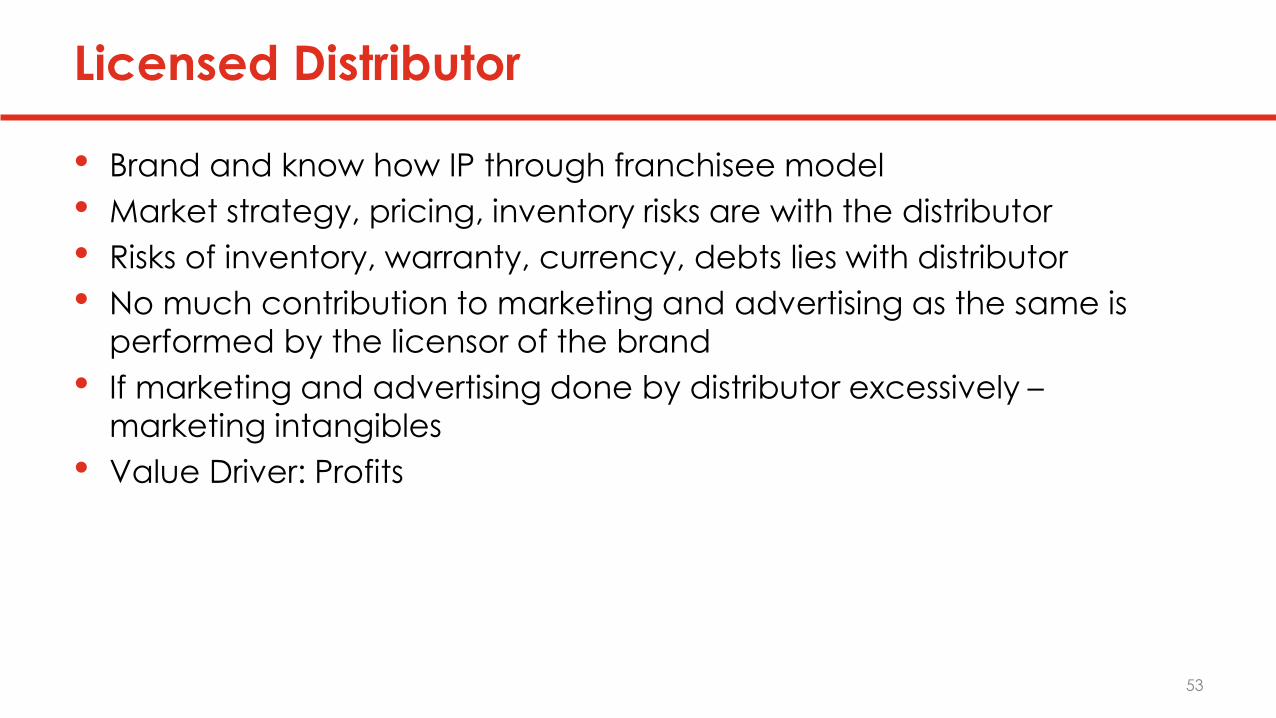

Licensed Distributor

• Brand and know how IP through franchisee model

• Market strategy, pricing, inventory risks are with the distributor

• Risks of inventory, warranty, currency, debts lies with distributor

• No much contribution to marketing and advertising as the same is

performed by the licensor of the brand

• If marketing and advertising done by distributor excessively –

marketing intangibles

• Value Driver: Profits

53

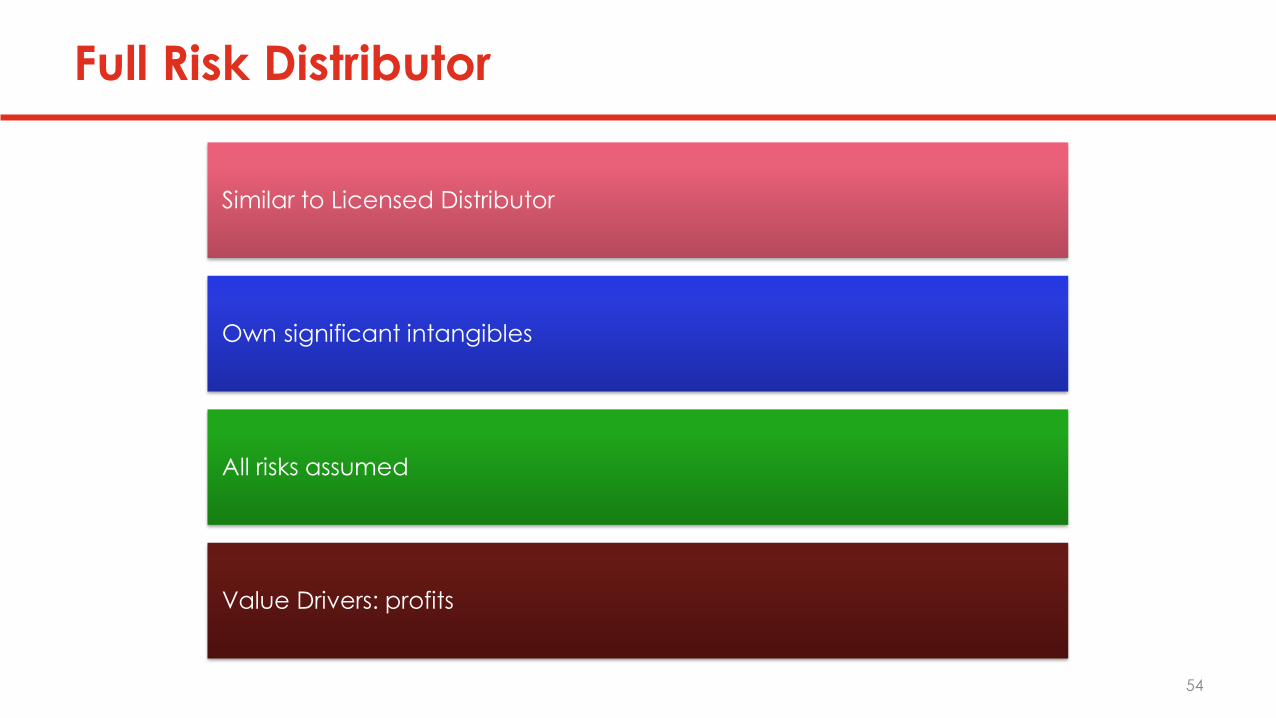

Full Risk Distributor

Similar to Licensed Distributor

Own significant intangibles

All risks assumed

Value Drivers: profits

54

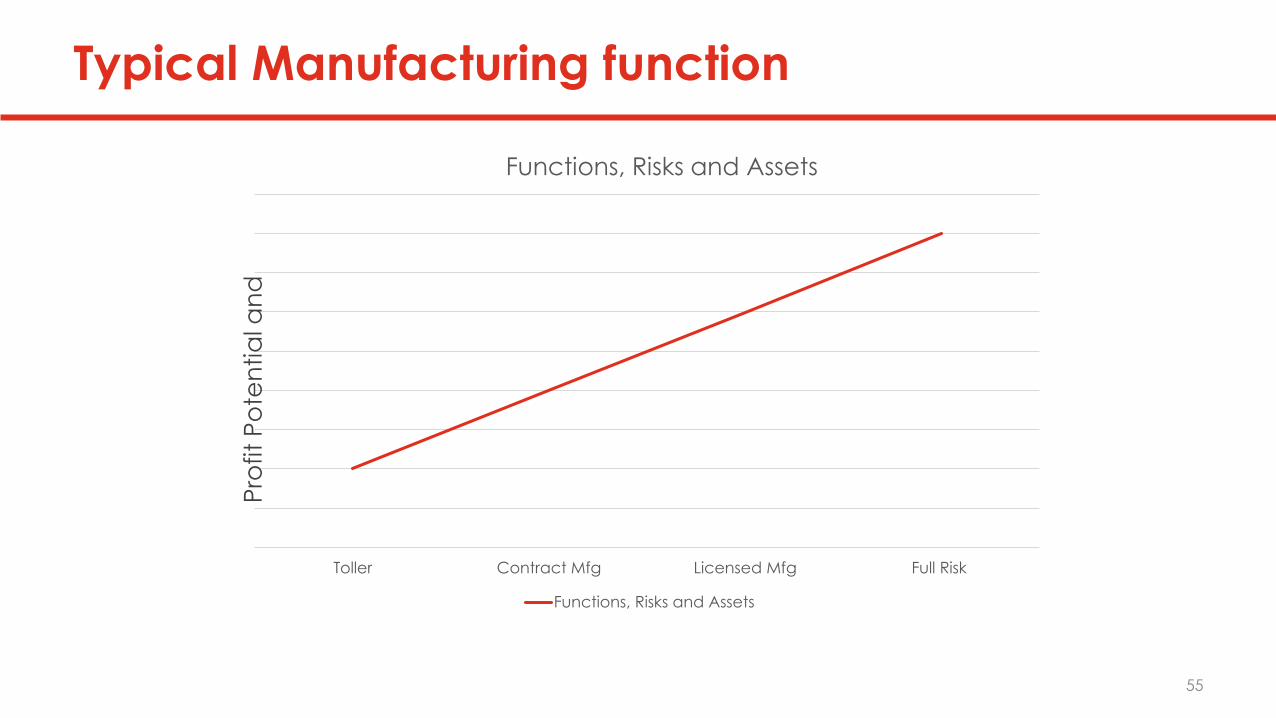

Typical Manufacturing function

Toller Contract Mfg Licensed Mfg Full Risk

Functions, Risks and Assets

Functions, Risks and Assets

Pro

fit

Po

ten

tia

l an

d

55

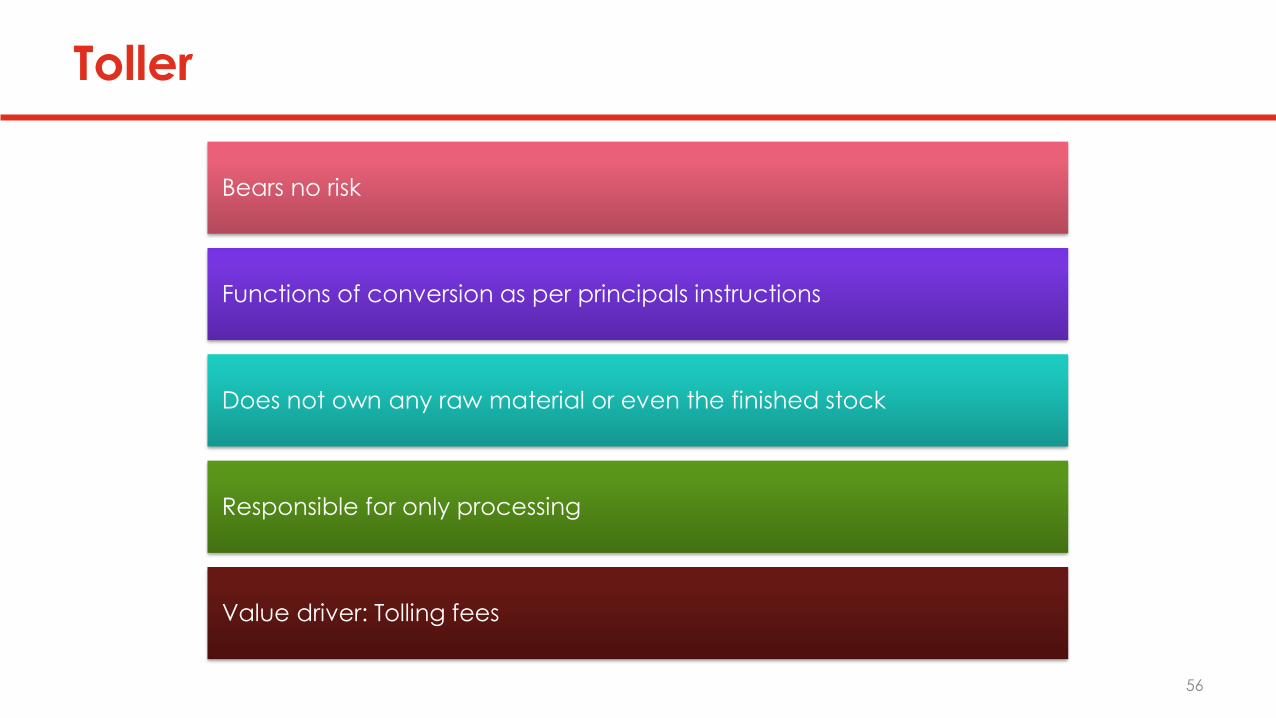

Toller

Bears no risk

Functions of conversion as per principals instructions

Does not own any raw material or even the finished stock

Responsible for only processing

Value driver: Tolling fees

56

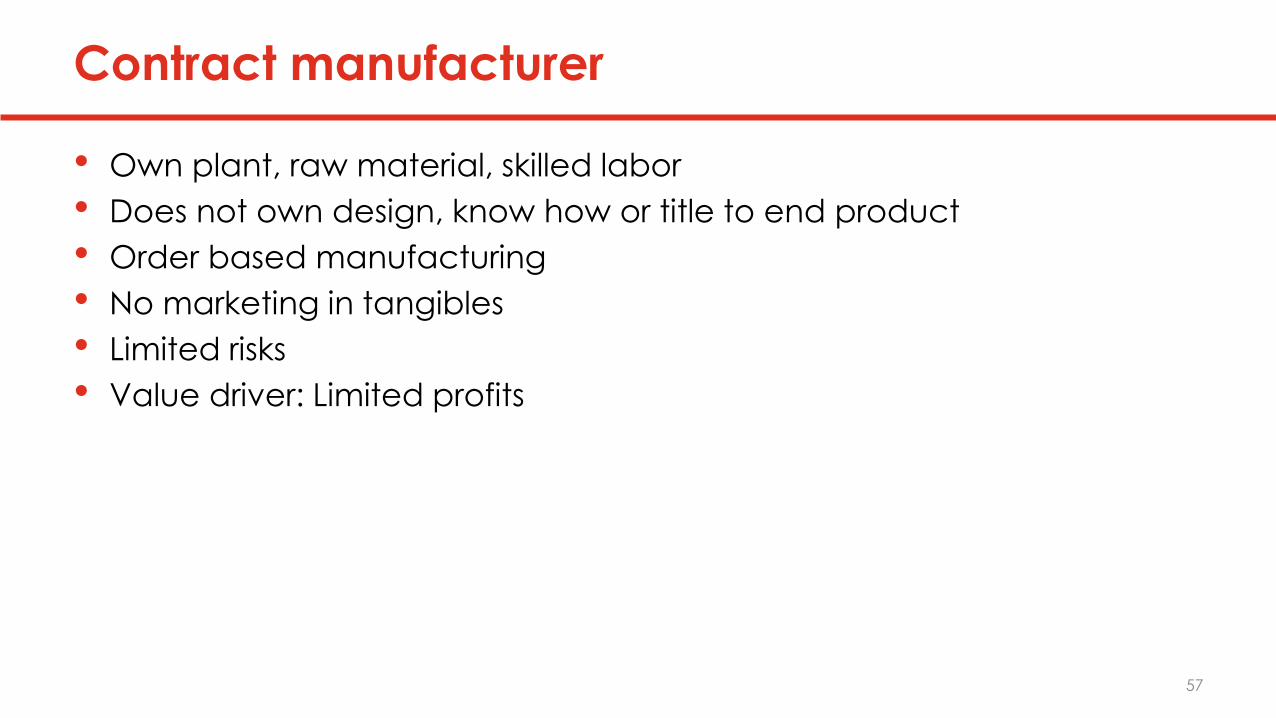

Contract manufacturer

• Own plant, raw material, skilled labor

• Does not own design, know how or title to end product

• Order based manufacturing

• No marketing in tangibles

• Limited risks

• Value driver: Limited profits

57

Licensed manufacturer

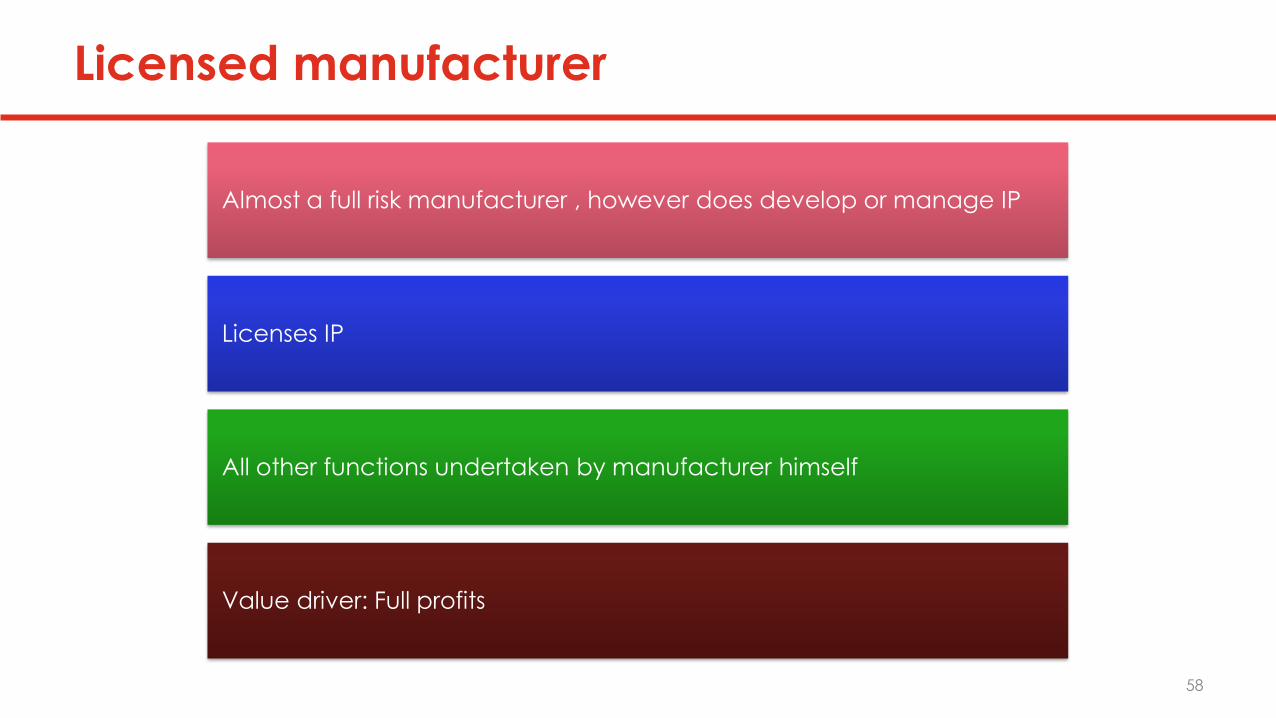

Almost a full risk manufacturer , however does develop or manage IP

Licenses IP

All other functions undertaken by manufacturer himself

Value driver: Full profits

58

Full risk manufacturer

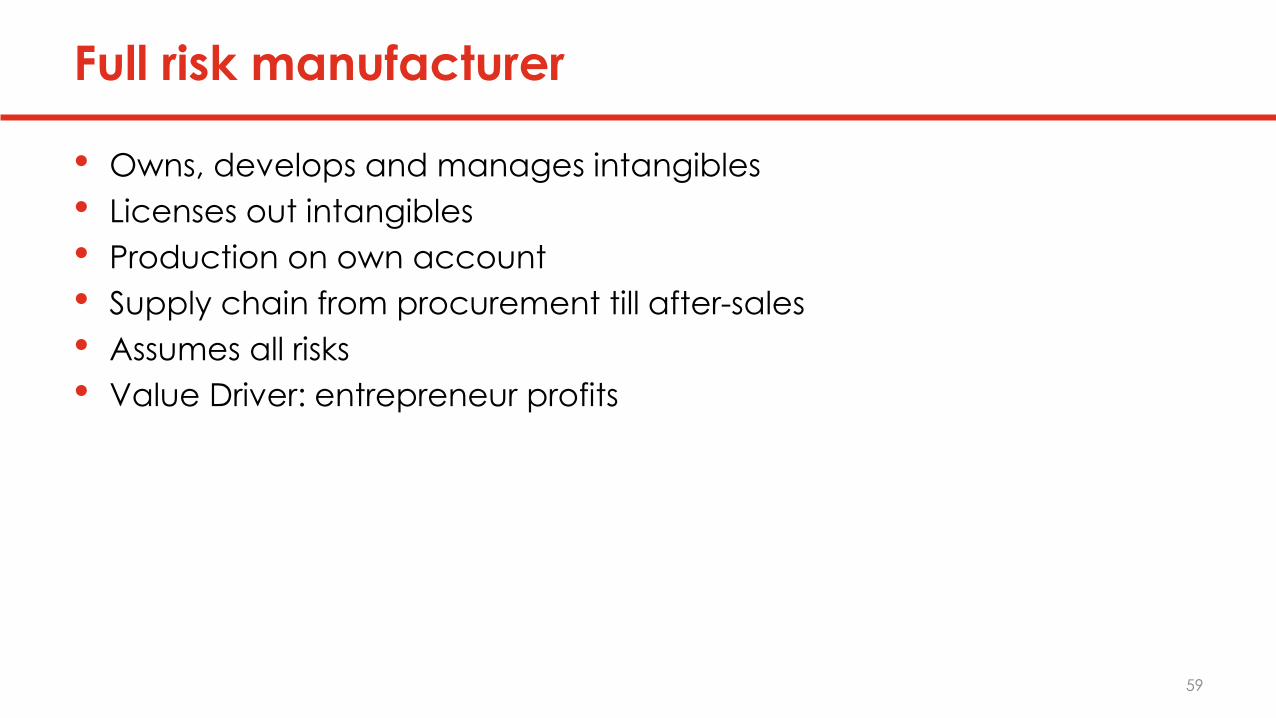

• Owns, develops and manages intangibles

• Licenses out intangibles

• Production on own account

• Supply chain from procurement till after-sales

• Assumes all risks

• Value Driver: entrepreneur profits

59

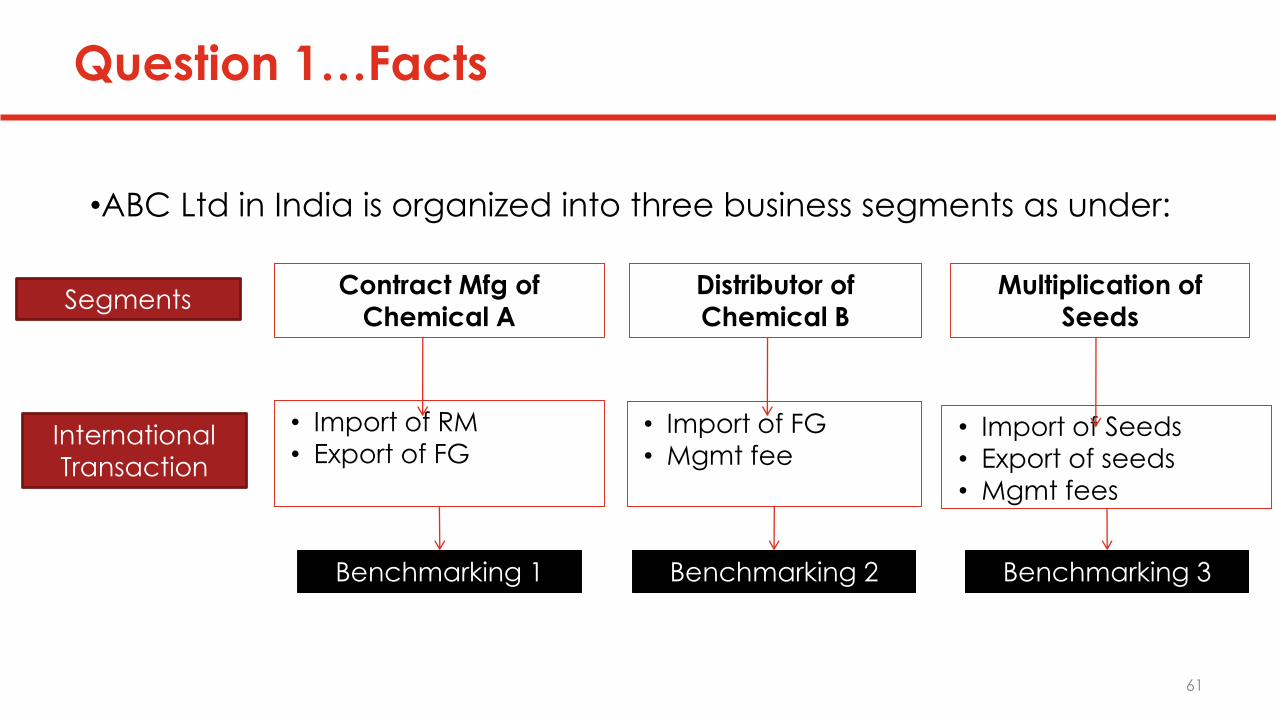

Case Studies

•ABC Ltd in India is organized into three business segments as under:

Contract Mfg of

Chemical A

Distributor of

Chemical B

Multiplication of

SeedsSegments

• Import of RM

• Export of FGInternational

Transaction

• Import of FG

• Mgmt fee• Import of Seeds

• Export of seeds

• Mgmt fees

Benchmarking 1 Benchmarking 2 Benchmarking 3

Question 1…Facts

61

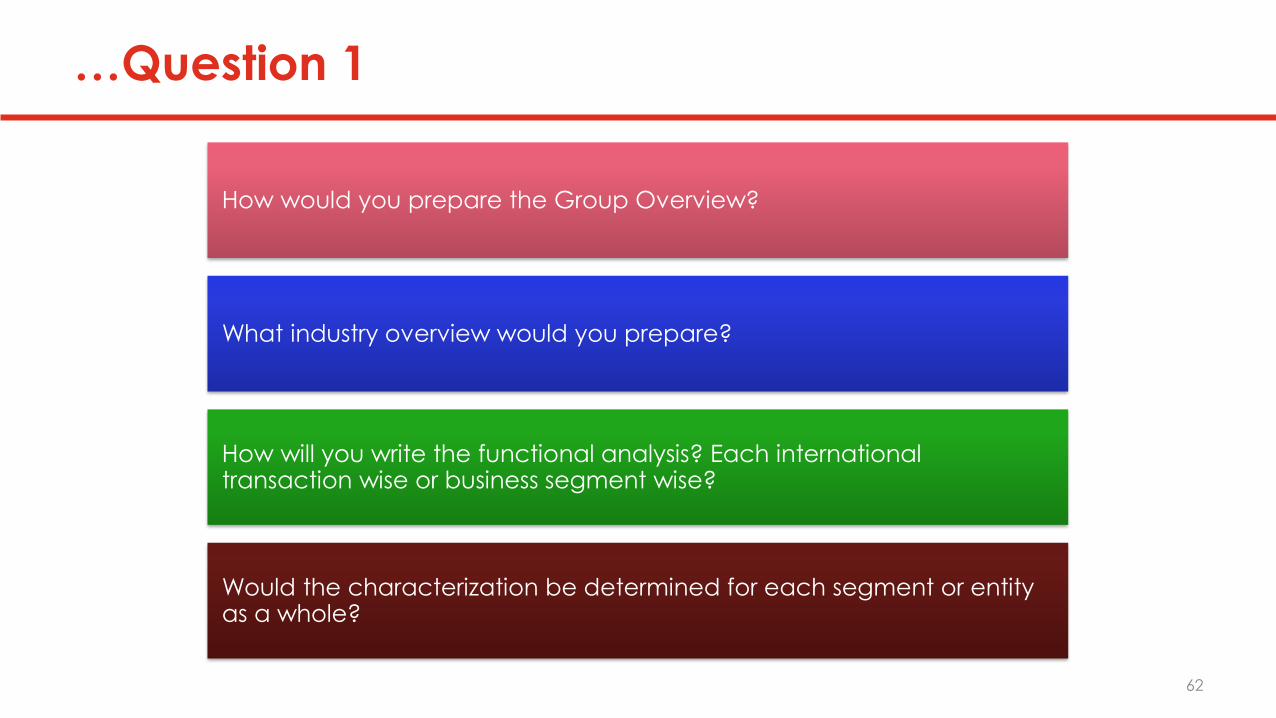

…Question 1

How would you prepare the Group Overview?

What industry overview would you prepare?

How will you write the functional analysis? Each international transaction wise or business segment wise?

Would the characterization be determined for each segment or entity as a whole?

62

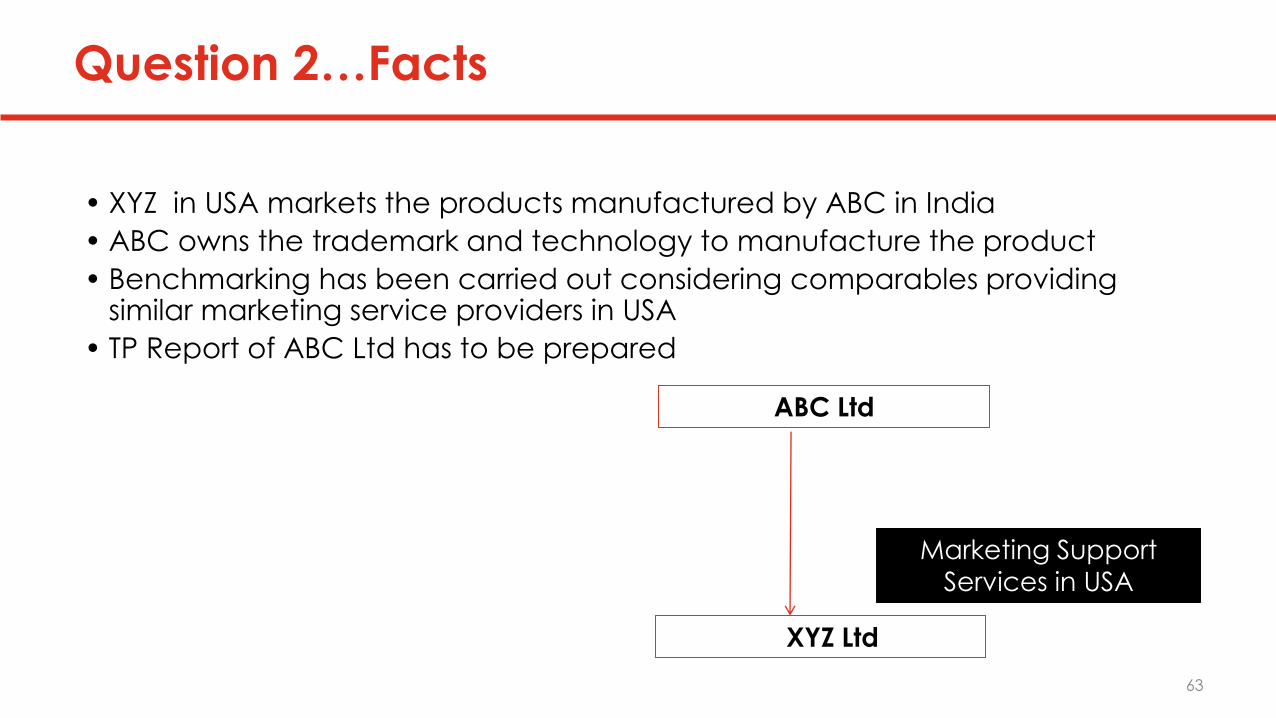

• XYZ in USA markets the products manufactured by ABC in India

• ABC owns the trademark and technology to manufacture the product

• Benchmarking has been carried out considering comparables providing similar marketing service providers in USA

• TP Report of ABC Ltd has to be prepared

ABC Ltd

Marketing Support

Services in USA

XYZ Ltd

Question 2…Facts

63

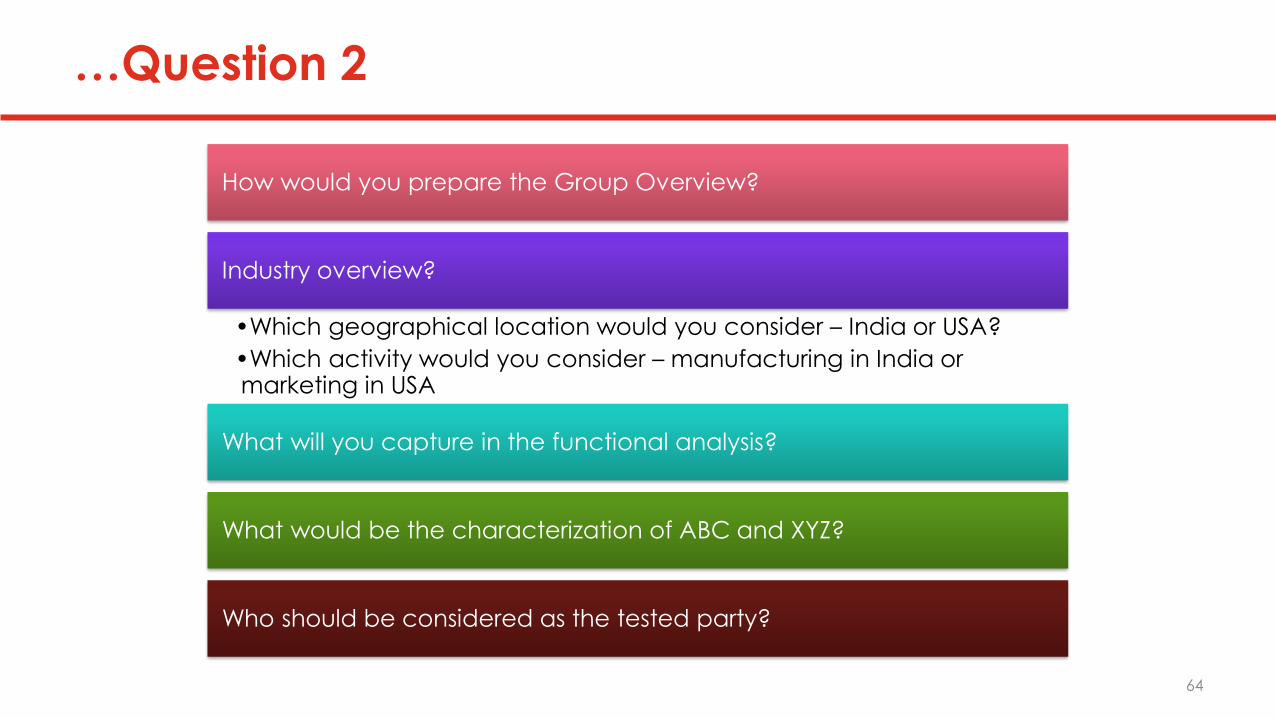

…Question 2

How would you prepare the Group Overview?

Industry overview?

•Which geographical location would you consider – India or USA?

•Which activity would you consider – manufacturing in India or marketing in USA

What will you capture in the functional analysis?

What would be the characterization of ABC and XYZ?

Who should be considered as the tested party?

64

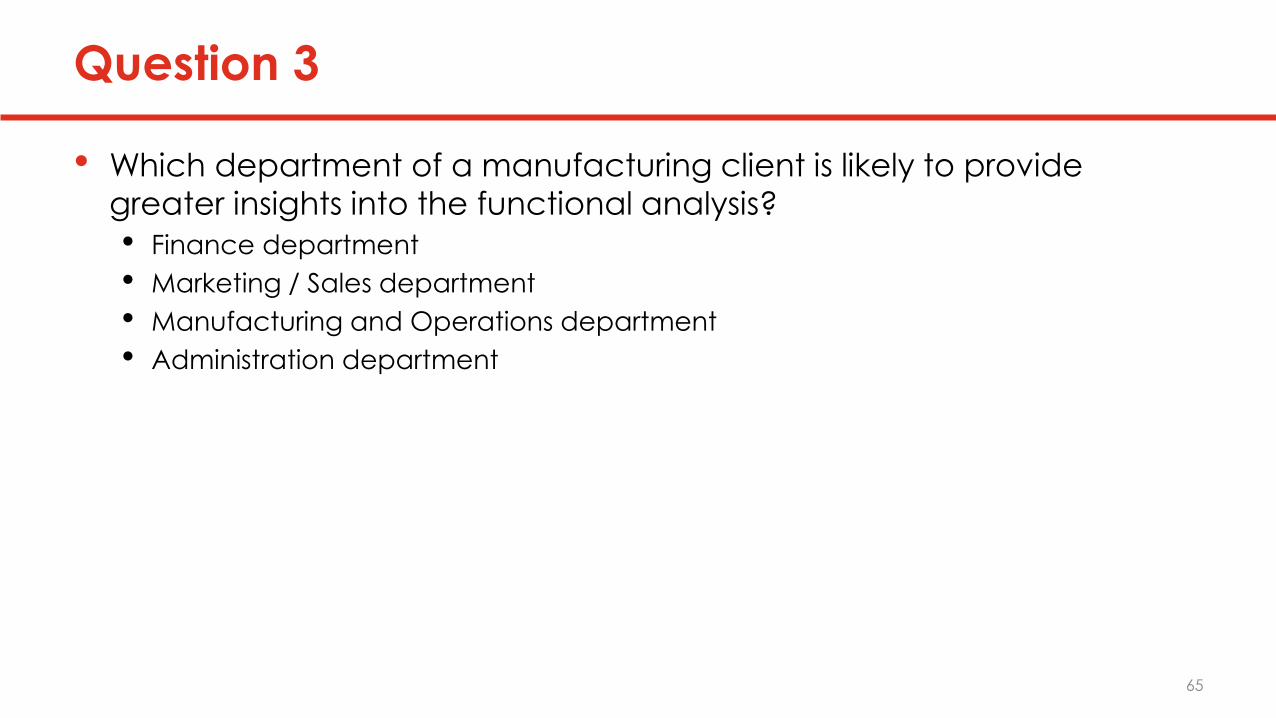

Question 3

• Which department of a manufacturing client is likely to provide

greater insights into the functional analysis?

• Finance department

• Marketing / Sales department

• Manufacturing and Operations department

• Administration department

65

Question 4

• Functional analysis has to be written for the Indian entity alone or for

both Indian entity and the Associated Enterprise?

66

67

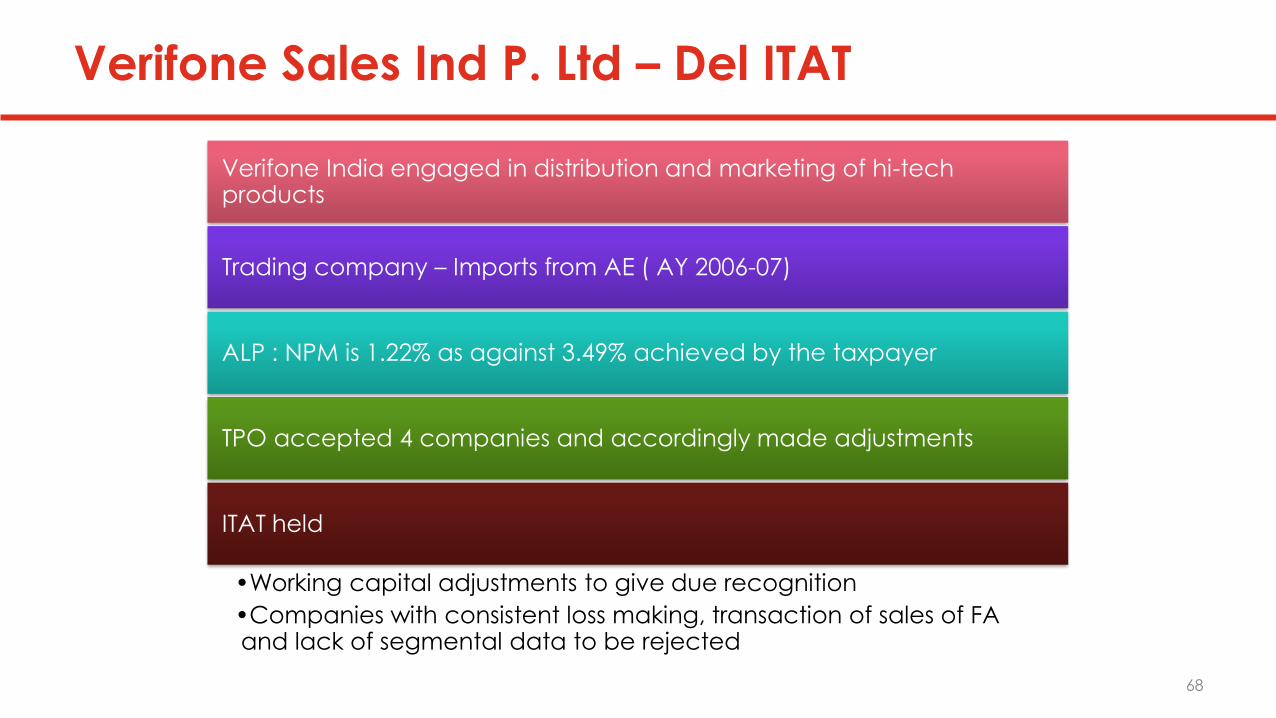

Verifone Sales Ind P. Ltd – Del ITAT

Verifone India engaged in distribution and marketing of hi-tech products

Trading company – Imports from AE ( AY 2006-07)

ALP : NPM is 1.22% as against 3.49% achieved by the taxpayer

TPO accepted 4 companies and accordingly made adjustments

ITAT held

•Working capital adjustments to give due recognition

•Companies with consistent loss making, transaction of sales of FA and lack of segmental data to be rejected

68

Symphony Services Pune P. Ltd.

Taxpayer engaged in business of software development for its AEs

Selling of Software products not comparable to the service provided by the taxpayer for software development; hence Kals Information as a comparable rejected

Companies in KPO business cannot be considered comparable to software development service. Hence functionally different. E-Zest Solutions Limited as a company rejected.

69

Thank

You