Embed Size (px)

Citation preview

Family Business ServicesAre you ready to have your name in a

central EU shareholder's register?

Conference of 19th January, 2017

KPMG Luxembourg, Société Coopérative

© 2017 KPMG Luxembourg, Société coopérative, a Luxembourg entity and a member firm of the KPMG network of independent member firms affiliated with KPMG International Cooperative (“KPMG International”), a Swiss entity. All rights reserved

Document Classification: KPMG Confidential

Contents

2

• Introduction

• UBO register's current developments and most controversial discussions

* Luxembourg

* Netherlands

* United Kingdom

* Belgium

* Germany

• Panel discussion

• Q & A

• Networking cocktail

Introduction

© 2017 KPMG Luxembourg, Société coopérative, a Luxembourg entity and a member firm of the KPMG network of independent member firms affiliated with KPMG International Cooperative (“KPMG International”), a Swiss entity. All rights reserved

Document Classification: KPMG Confidential

KPMG Network

4

UBO register's current developments and most controversial discussions

Luxembourg

© 2017 KPMG Luxembourg, Société coopérative, a Luxembourg entity and a member firm of the KPMG network of independent member firms affiliated with KPMG International Cooperative (“KPMG International”), a Swiss entity. All rights reserved

Document Classification: KPMG Confidential

• Implementation not later than June 26, 2017

• Luxembourg :* no draft law yet available* no intention to make it public

4th Anti-Money Laundering Directive: implementation of UBO-register in

all EU Member States

7

© 2017 KPMG Luxembourg, Société coopérative, a Luxembourg entity and a member firm of the KPMG network of independent member firms affiliated with KPMG International Cooperative (“KPMG International”), a Swiss entity. All rights reserved

Document Classification: KPMG Confidential

Introduction of aggravated tax fraudType Definition Sanction

Simple tax fraud Intentional act that leads to evaded tax orundue tax reimbursements

Administrative(not a primary offence for AML purpose)

Aggravated tax fraud(art. 396 al. 5 LGI, art. 80§1 amended lawof 12/02/1979, art. 29 al. 1 amended lawof 28/01/1948)

Aggravated fraud qualified upon certain threshold: more than 25% of evaded taxes (if > €10k), or more than €200k

Criminal(Handled and sanctioned by the Criminal court)-> imprisonment (1 month to 3 years), and penalty (€25k to 6 times the amount of evaded taxes/undue tax reimbursements).

Tax swindle (art. 396 al.6 LGI, art. 80§1 amended lawof 12/02/1979, art. 29 al. 2 amended lawof 28/01/1948)

Systematic use of fraudulent maneuvers with the intent to conceal relevant facts from the authorities or to persuade them of inaccurate facts

Criminal(Handled and sanctioned by the Criminal court) -> imprisonment (1 month to 5 years), and penalty (€25k to 6 times the amount of evaded taxes/undue tax reimbursements).

Aggravated tax fraud and tax swindle will apply to acts committed after 1 January 2017.

Furthermore, the money laundering infraction has been extended to cases of “aggravated” tax fraud and tax evasion”. This means that perpetrators can face prison sentences of one to five years and/or fines of €1,250 to €1,250,000.

8

© 2017 KPMG Luxembourg, Société coopérative, a Luxembourg entity and a member firm of the KPMG network of independent member firms affiliated with KPMG International Cooperative (“KPMG International”), a Swiss entity. All rights reserved

Document Classification: KPMG Confidential

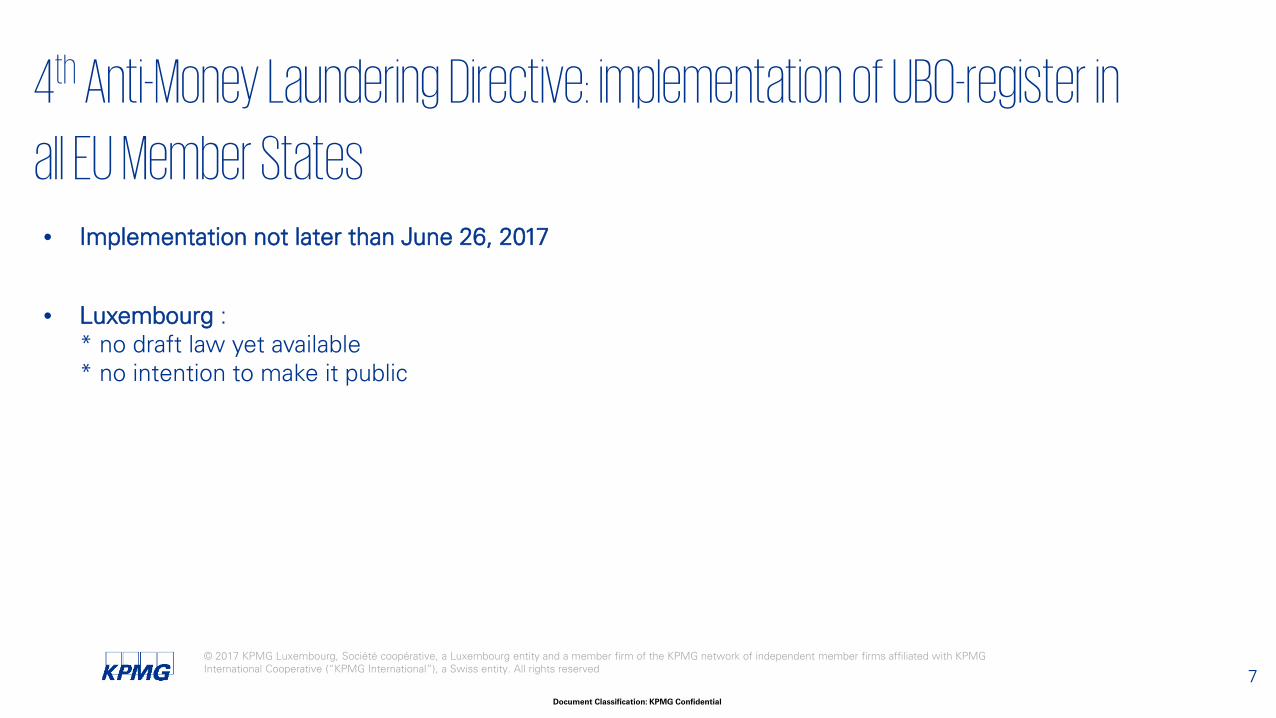

Luxembourg tax amnesty regime

9

Netherlands

AGENDA1. The Fourth EU Anti-Money Laundering Directive

2. Who is UBO?

3. Which entities must register?

4. What information needs to be included in the register?

6. Proposed additional measures concerning the register

5. Transparency versus Privacy

7. Implementation in legislation of various countries

© 2017 KPMG Luxembourg, Société coopérative, a Luxembourg entity and a member firm of the KPMG network of independent member firms affiliated with KPMG International Cooperative (“KPMG International”), a Swiss entity. All rights reserved

Document Classification: KPMG Confidential

• Adopted by the European Parliament on May 20, 2015

• The directive must be implemented in the legislation of the Member States on or before June 26, 2017

• Introduction of a central UBO register in every Member State

• Access for authorities and those with a legitimate interest

• Article 30: corporations / Article 31: trusts

1. The 4th EU ALMD

12

© 2017 KPMG Luxembourg, Société coopérative, a Luxembourg entity and a member firm of the KPMG network of independent member firms affiliated with KPMG International Cooperative (“KPMG International”), a Swiss entity. All rights reserved

Document Classification: KPMG Confidential

Objectives:

Prevention of the use of the financial system for the purpose of money laundering and terrorist financing

Organised criminal and terrorism financing can damage the stability and reputation of the financial sector andthreaten the internal markets

1. The 4th EU ALMD

13

© 2017 KPMG Luxembourg, Société coopérative, a Luxembourg entity and a member firm of the KPMG network of independent member firms affiliated with KPMG International Cooperative (“KPMG International”), a Swiss entity. All rights reserved

Document Classification: KPMG Confidential

• The following individuals qualify as a UBO under the Directive where it comes to legal entities:

i) An individual who directly or indirectly has a shareholding of more than 25%orii) who has the power (>25%) over such entity

iii) If no such person can be identified, then the individuals belonging to senior management staff are designated as UBO

• The identities of the following persons must be registered by trusts if the trust has tax consequences:

- the founder of the trust

- the trustee(s)

- the protector (where applicable)

- the beneficiaries (or class of beneficiaries) and

- any other individual exercising effective control over the trust

2. Who is UBO?

14

© 2017 KPMG Luxembourg, Société coopérative, a Luxembourg entity and a member firm of the KPMG network of independent member firms affiliated with KPMG International Cooperative (“KPMG International”), a Swiss entity. All rights reserved

Document Classification: KPMG Confidential

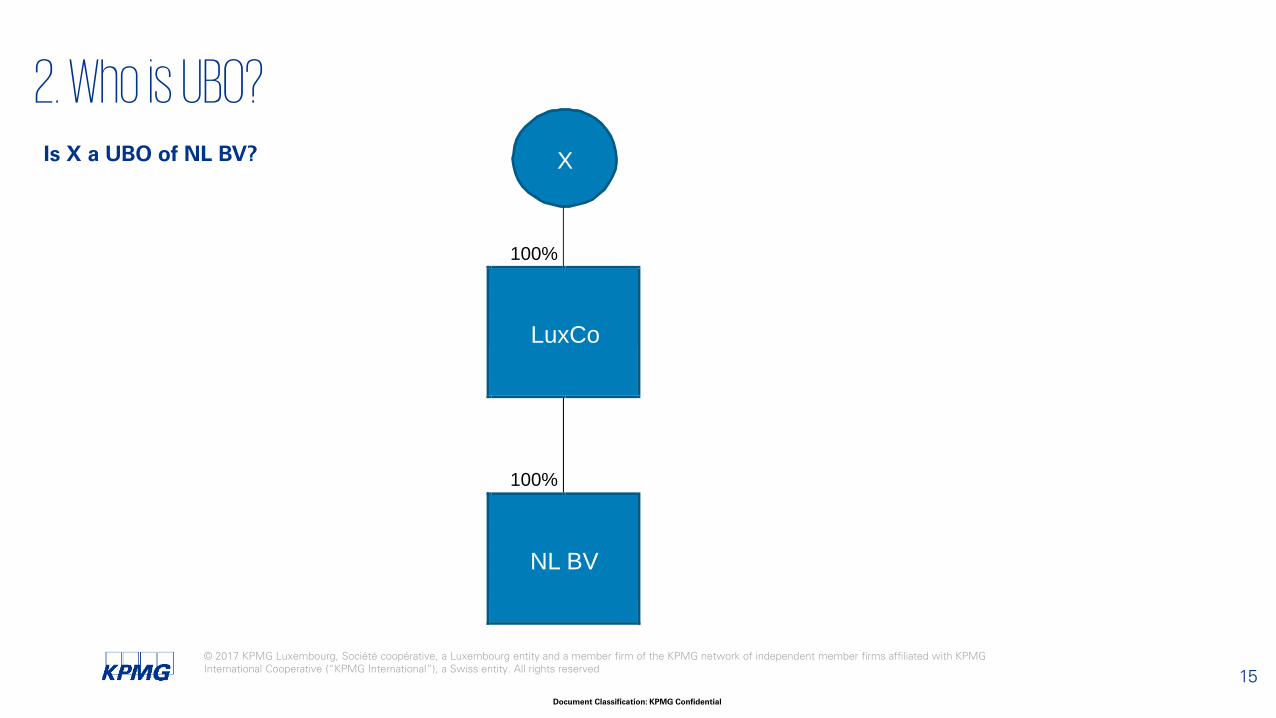

Is X a UBO of NL BV? X

100%

LuxCo

100%

NL BV

2. Who is UBO?

15

© 2017 KPMG Luxembourg, Société coopérative, a Luxembourg entity and a member firm of the KPMG network of independent member firms affiliated with KPMG International Cooperative (“KPMG International”), a Swiss entity. All rights reserved

Document Classification: KPMG Confidential

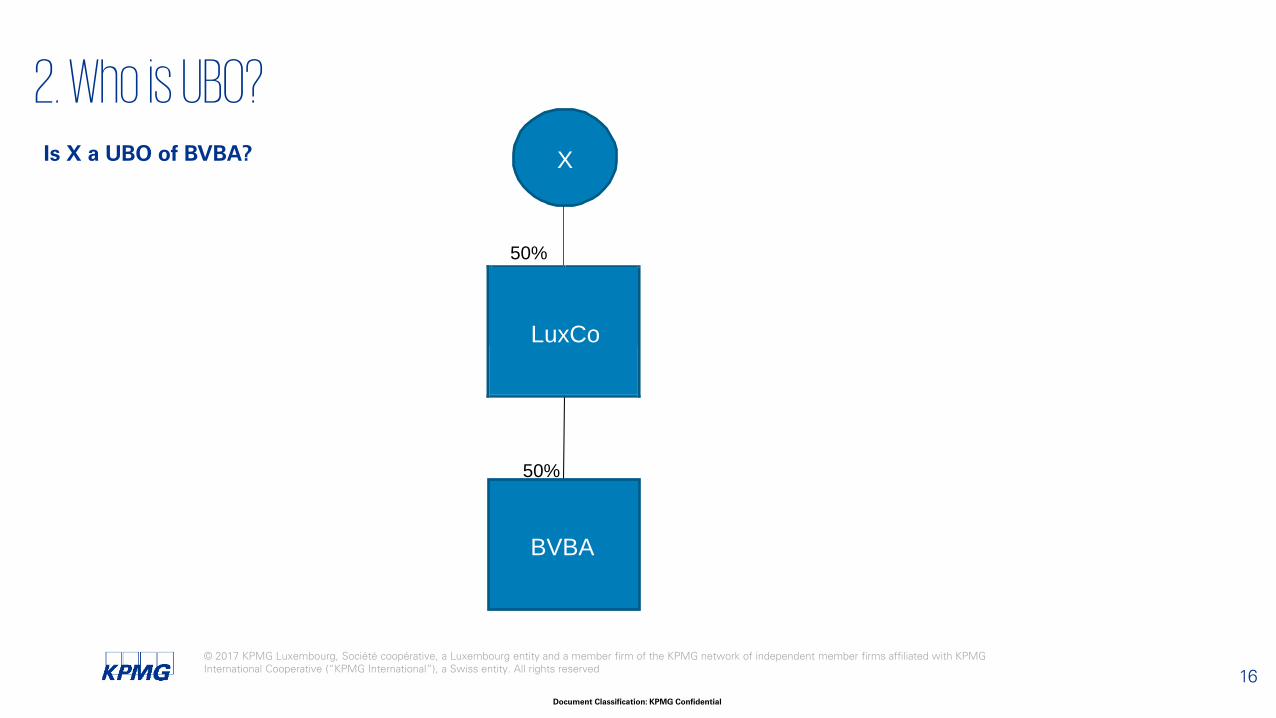

Is X a UBO of BVBA? X

50%

LuxCo

50%

BVBA

2. Who is UBO?

16

© 2017 KPMG Luxembourg, Société coopérative, a Luxembourg entity and a member firm of the KPMG network of independent member firms affiliated with KPMG International Cooperative (“KPMG International”), a Swiss entity. All rights reserved

Document Classification: KPMG Confidential

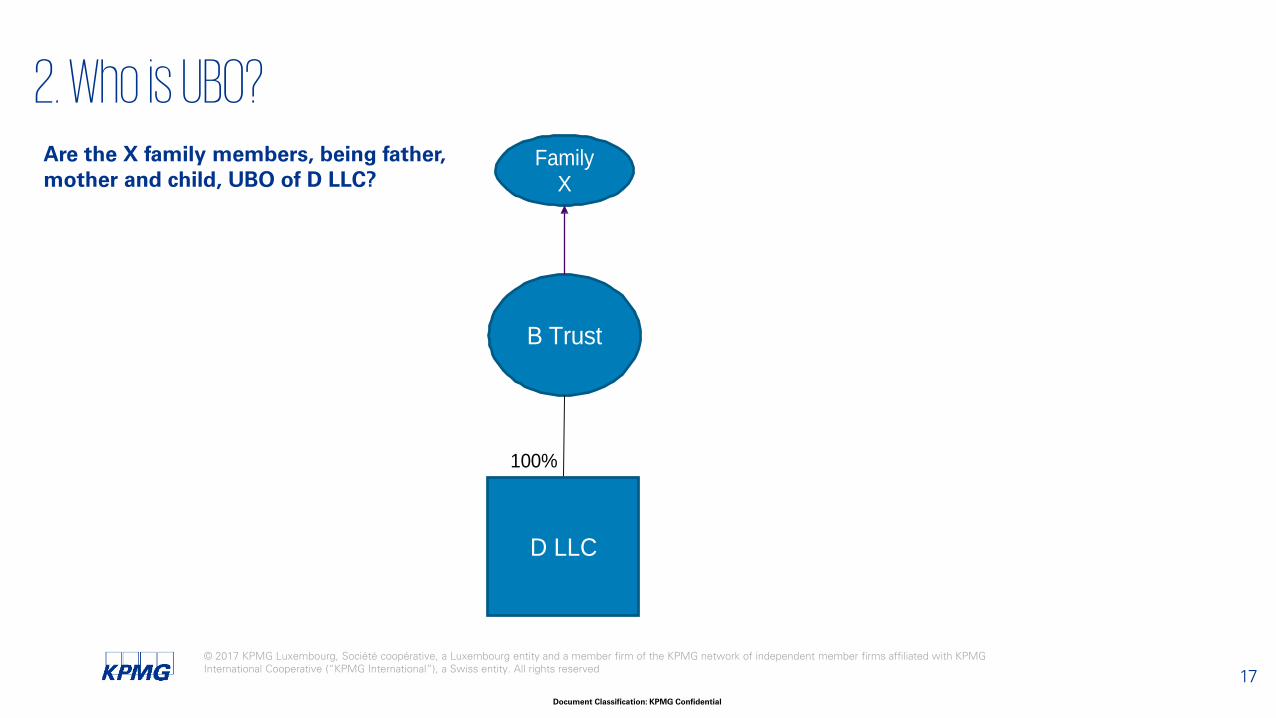

Are the X family members, being father, mother and child, UBO of D LLC?

D LLC

Family X

B Trust

100%

2. Who is UBO?

17

© 2017 KPMG Luxembourg, Société coopérative, a Luxembourg entity and a member firm of the KPMG network of independent member firms affiliated with KPMG International Cooperative (“KPMG International”), a Swiss entity. All rights reserved

Document Classification: KPMG Confidential

• All corporations and other legal entities incorporated within the territory of a Member State

• How about corporations and legal entities not incorporated within their territory?

• Trusts who fall under the laws of the Member State

• All those entities are required to obtain and hold adequate, accurate and up to date information on their beneficial owners. A UBO is obligated to cooperate.

• Intermediaries such as banks, financial institutions, trust offices, notaries, external accountants, auditors, tax advisors, have the duty to notify the register if they receive UBO-information which differsfrom the information as laid down in the register.

3. Entities that must register their UBO(s)

18

© 2017 KPMG Luxembourg, Société coopérative, a Luxembourg entity and a member firm of the KPMG network of independent member firms affiliated with KPMG International Cooperative (“KPMG International”), a Swiss entity. All rights reserved

Document Classification: KPMG Confidential

The following information on the UBO of legal entities must be included in the register:

• Name • Month of birth • Year of birth • Nationality • Country of residence • Nature and extent of the economic interest held by the UBO

the above is accessible to all including organisations and persons with a legitimate interest.

In all cases, in addition the following information is available to FIE’s and intermediaries:• Date of birth• Place of birth• Home address• Tax Identification Number

4. What UBO-information needs to be included in the register?

19

© 2017 KPMG Luxembourg, Société coopérative, a Luxembourg entity and a member firm of the KPMG network of independent member firms affiliated with KPMG International Cooperative (“KPMG International”), a Swiss entity. All rights reserved

Document Classification: KPMG Confidential

• UBO register for trusts is only accessible for authorities and FIE’s

• Without the UBO’s knowing

• Member States can require online registration of those with a legitimate interest

• Member States can ask a price for the information

• The price cannot exceed the administrative costs

4. What UBO-information needs to be included in the register?

20

© 2017 KPMG Luxembourg, Société coopérative, a Luxembourg entity and a member firm of the KPMG network of independent member firms affiliated with KPMG International Cooperative (“KPMG International”), a Swiss entity. All rights reserved

Document Classification: KPMG Confidential

5. Transparency versus Privacy

21

© 2017 KPMG Luxembourg, Société coopérative, a Luxembourg entity and a member firm of the KPMG network of independent member firms affiliated with KPMG International Cooperative (“KPMG International”), a Swiss entity. All rights reserved

Document Classification: KPMG Confidential

AMLD4 provides for exceptions when risk of:

• Fraud

• Kidnapping

• Blackmail

• Violence

• Intimidation

or where the beneficial owner is a minor or otherwise incapable

Proposal 25 Nov 2016: Member States may decide to opt for such wider access in their nationallegislation in case they choose to do so having regard to the utmost importance to retain balance andproportionality in the aim of transparancy and the aim of protection of fundamental rights of theindividuals especially the right to privacy.

5. Transparency versus Privacy

22

© 2017 KPMG Luxembourg, Société coopérative, a Luxembourg entity and a member firm of the KPMG network of independent member firms affiliated with KPMG International Cooperative (“KPMG International”), a Swiss entity. All rights reserved

Document Classification: KPMG Confidential

French Constitutional Court: public trust registry is in conflict with the French Constitution

• October 21, 2016 • The trust registry was introduced to counter tax evasion and money laundering using trusts.

Although the pursuit of this goal, according to the French Court, is in principle in line with the French Constitution and can justify the invasion of the privacy of citizens, the invasion of this right to privacy by the trust registry should not go beyond what is necessary to achieve this goal

• Disproportionate invasion of the right to privacy

The judgement by the French Constitutional Court does not relate to the UBO registry that all EU Member States must implement by virtue of the fourth European Anti-Money Laundering Directive

Nevertheless:• This judgement fosters the idea that a publicly accessible UBO registry is not necessarily consistent with National

law

5. Privacy in France

23

© 2017 KPMG Luxembourg, Société coopérative, a Luxembourg entity and a member firm of the KPMG network of independent member firms affiliated with KPMG International Cooperative (“KPMG International”), a Swiss entity. All rights reserved

Document Classification: KPMG Confidential

On July 5, 2016, the European Commission announced it wanted to take a number of additional measures:

• full public access to the UBO registers

• reduction of the percentage necessary to qualify as a UBO from 25% to 10% for “businesses that risk being used for money laundering or tax evasion”. The European Commission proposed using the definition ‘Passive Non-Financial Entity’, which is also used in other guidelines. Unlisted investment companies could fall under this definition.

• Direct interconnection of registers between Member States, to facilitate the cooperation between Member States

6.1. Proposed additional measures concerning the register

24

© 2017 KPMG Luxembourg, Société coopérative, a Luxembourg entity and a member firm of the KPMG network of independent member firms affiliated with KPMG International Cooperative (“KPMG International”), a Swiss entity. All rights reserved

Document Classification: KPMG Confidential

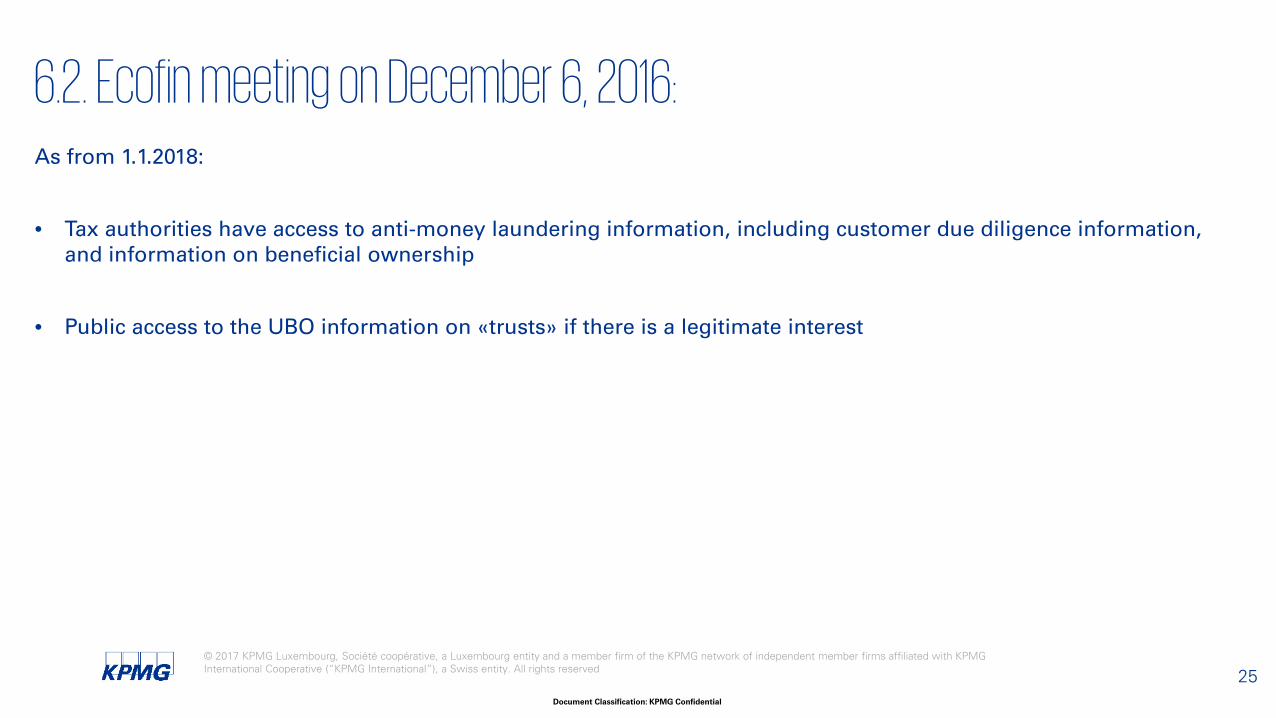

As from 1.1.2018:

• Tax authorities have access to anti-money laundering information, including customer due diligence information, and information on beneficial ownership

• Public access to the UBO information on «trusts» if there is a legitimate interest

6.2. Ecofin meeting on December 6, 2016:

25

© 2017 KPMG Luxembourg, Société coopérative, a Luxembourg entity and a member firm of the KPMG network of independent member firms affiliated with KPMG International Cooperative (“KPMG International”), a Swiss entity. All rights reserved

Document Classification: KPMG Confidential

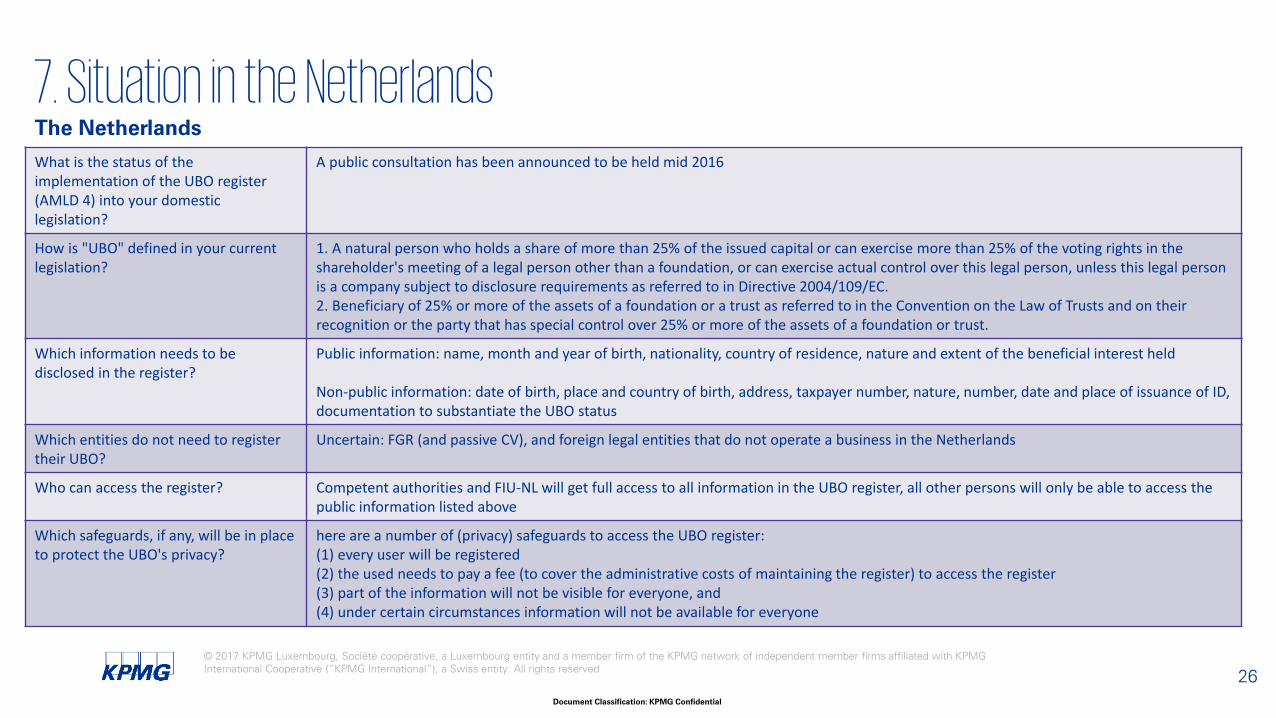

The Netherlands

What is the status of the implementation of the UBO register (AMLD 4) into your domestic legislation?

A public consultation has been announced to be held mid 2016

How is "UBO" defined in your current legislation?

1. A natural person who holds a share of more than 25% of the issued capital or can exercise more than 25% of the voting rights in the shareholder's meeting of a legal person other than a foundation, or can exercise actual control over this legal person, unless this legal person is a company subject to disclosure requirements as referred to in Directive 2004/109/EC.2. Beneficiary of 25% or more of the assets of a foundation or a trust as referred to in the Convention on the Law of Trusts and on their recognition or the party that has special control over 25% or more of the assets of a foundation or trust.

Which information needs to be disclosed in the register?

Public information: name, month and year of birth, nationality, country of residence, nature and extent of the beneficial interest held

Non-public information: date of birth, place and country of birth, address, taxpayer number, nature, number, date and place of issuance of ID, documentation to substantiate the UBO status

Which entities do not need to register their UBO?

Uncertain: FGR (and passive CV), and foreign legal entities that do not operate a business in the Netherlands

Who can access the register? Competent authorities and FIU-NL will get full access to all information in the UBO register, all other persons will only be able to access the public information listed above

Which safeguards, if any, will be in place to protect the UBO's privacy?

here are a number of (privacy) safeguards to access the UBO register: (1) every user will be registered (2) the used needs to pay a fee (to cover the administrative costs of maintaining the register) to access the register (3) part of the information will not be visible for everyone, and (4) under certain circumstances information will not be available for everyone

7. Situation in the Netherlands

26

© 2017 KPMG Luxembourg, Société coopérative, a Luxembourg entity and a member firm of the KPMG network of independent member firms affiliated with KPMG International Cooperative (“KPMG International”), a Swiss entity. All rights reserved

Document Classification: KPMG Confidential

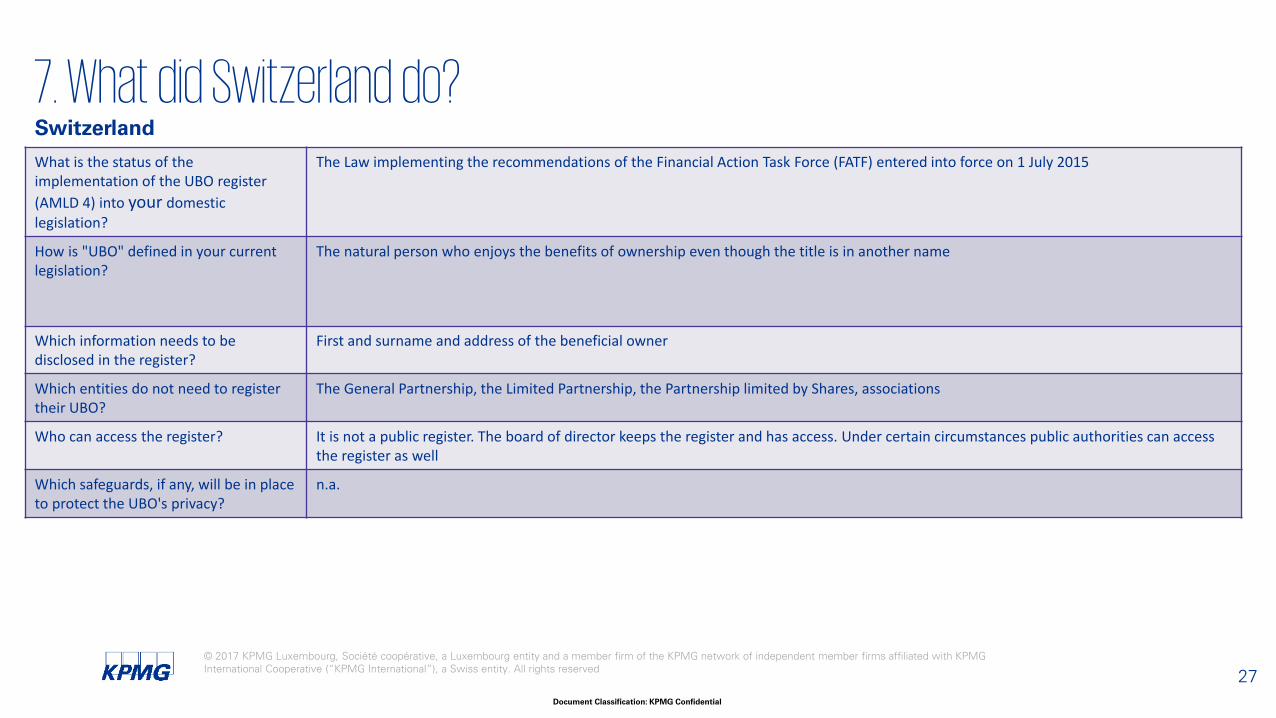

Switzerland

What is the status of the implementation of the UBO register (AMLD 4) into your domestic legislation?

The Law implementing the recommendations of the Financial Action Task Force (FATF) entered into force on 1 July 2015

How is "UBO" defined in your current legislation?

The natural person who enjoys the benefits of ownership even though the title is in another name

Which information needs to be disclosed in the register?

First and surname and address of the beneficial owner

Which entities do not need to register their UBO?

The General Partnership, the Limited Partnership, the Partnership limited by Shares, associations

Who can access the register? It is not a public register. The board of director keeps the register and has access. Under certain circumstances public authorities can access the register as well

Which safeguards, if any, will be in place to protect the UBO's privacy?

n.a.

7. What did Switzerland do?

27

© 2017 KPMG Luxembourg, Société coopérative, a Luxembourg entity and a member firm of the KPMG network of independent member firms affiliated with KPMG International Cooperative (“KPMG International”), a Swiss entity. All rights reserved

Document Classification: KPMG Confidential

Beyond the EU Global action on exchange of information on UBO

— 45 countries have committed to the project on automatic exchange of information on beneficial ownership

7. Beyond the EU

28

United Kingdom

© 2017 KPMG Luxembourg, Société coopérative, a Luxembourg entity and a member firm of the KPMG network of independent member firms affiliated with KPMG International Cooperative (“KPMG International”), a Swiss entity. All rights reserved

Document Classification: KPMG Confidential

Transparency –the UK perspective

Mike Walker

19 January 2017

© 2017 KPMG Luxembourg, Société coopérative, a Luxembourg entity and a member firm of the KPMG network of independent member firms affiliated with KPMG International Cooperative (“KPMG International”), a Swiss entity. All rights reserved

Document Classification: KPMG Confidential

The train is leaving the station – are you on it?

31

© 2017 KPMG Luxembourg, Société coopérative, a Luxembourg entity and a member firm of the KPMG network of independent member firms affiliated with KPMG International Cooperative (“KPMG International”), a Swiss entity. All rights reserved

Document Classification: KPMG Confidential

INFORMATION

What authorities and regulators want is…

32

© 2017 KPMG Luxembourg, Société coopérative, a Luxembourg entity and a member firm of the KPMG network of independent member firms affiliated with KPMG International Cooperative (“KPMG International”), a Swiss entity. All rights reserved

Document Classification: KPMG Confidential

Register of people exercising significant control of UK companies

© 2017 KPMG Luxembourg, Société coopérative, a Luxembourg entity and a member firm of the KPMG network of independent member firms affiliated with KPMG International Cooperative (“KPMG International”), a Swiss entity. All rights reserved

Document Classification: KPMG Confidential

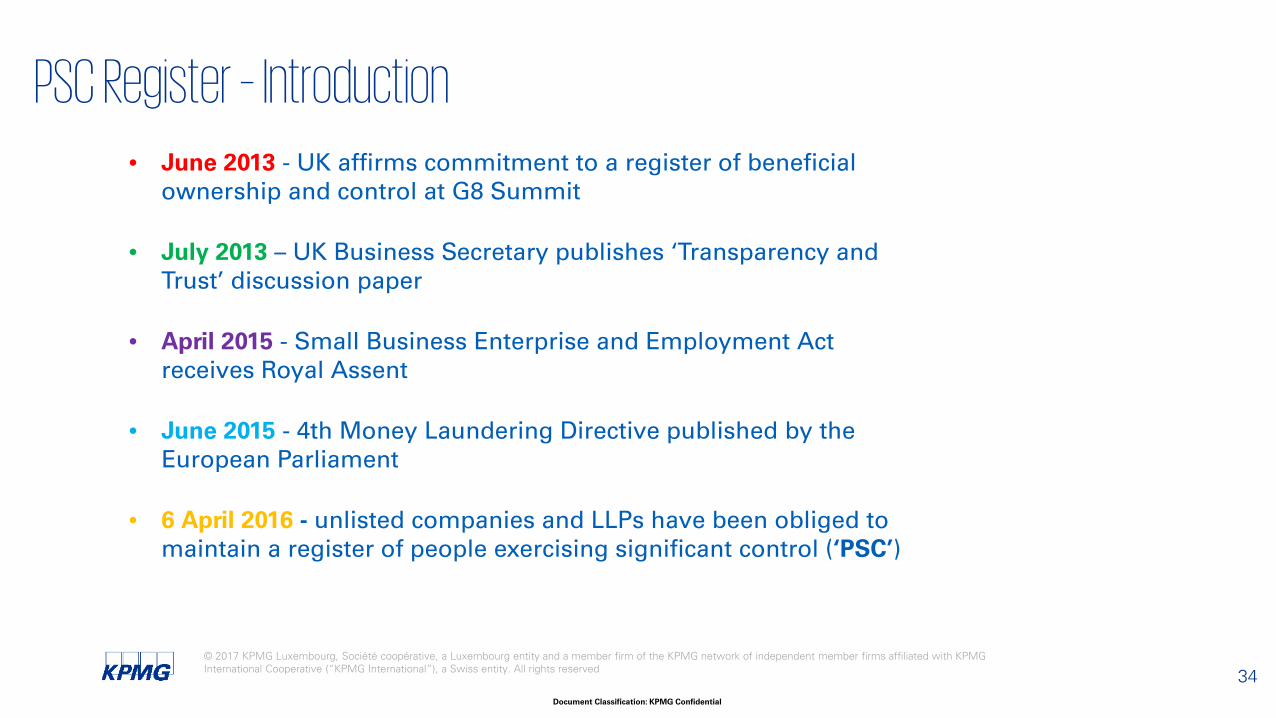

• June 2013 - UK affirms commitment to a register of beneficial ownership and control at G8 Summit

• July 2013 – UK Business Secretary publishes ‘Transparency and Trust’ discussion paper

• April 2015 - Small Business Enterprise and Employment Act receives Royal Assent

• June 2015 - 4th Money Laundering Directive published by the European Parliament

• 6 April 2016 - unlisted companies and LLPs have been obliged to maintain a register of people exercising significant control (‘PSC’)

PSC Register – Introduction

34

© 2017 KPMG Luxembourg, Société coopérative, a Luxembourg entity and a member firm of the KPMG network of independent member firms affiliated with KPMG International Cooperative (“KPMG International”), a Swiss entity. All rights reserved

Document Classification: KPMG Confidential

• The Register:

- contains details of all individuals who ultimately own or control 25% or more of the entity’s shares or voting rights or who otherwise exercise significant control over the entity or its management; and

- needs to be freely accessible at the registered address

• From 30 June 2016 this information has to filed with Companies House

• Companies House records freely available and searchable on-line

PSC Register – Introduction

35

© 2017 KPMG Luxembourg, Société coopérative, a Luxembourg entity and a member firm of the KPMG network of independent member firms affiliated with KPMG International Cooperative (“KPMG International”), a Swiss entity. All rights reserved

Document Classification: KPMG Confidential

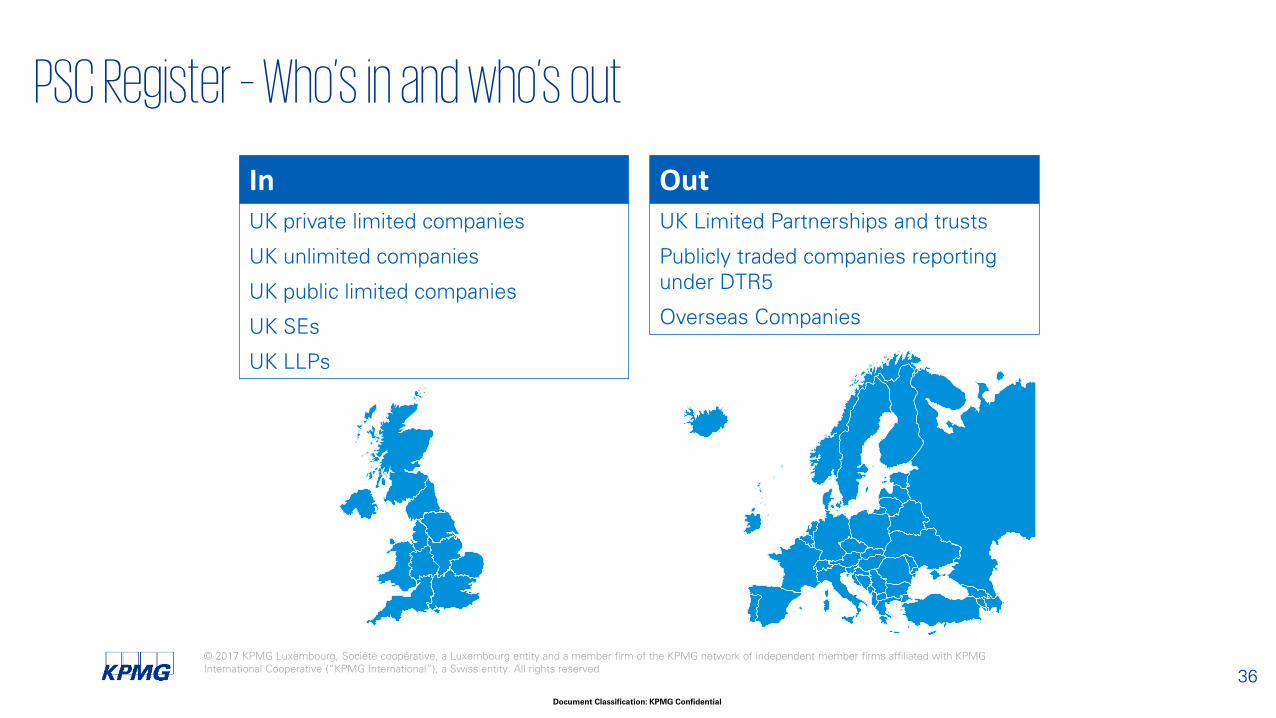

InUK private limited companies

UK unlimited companies

UK public limited companies

UK SEs

UK LLPs

OutUK Limited Partnerships and trusts

Publicly traded companies reporting under DTR5

Overseas Companies

PSC Register – Who’s in and who’s out

36

© 2017 KPMG Luxembourg, Société coopérative, a Luxembourg entity and a member firm of the KPMG network of independent member firms affiliated with KPMG International Cooperative (“KPMG International”), a Swiss entity. All rights reserved

Document Classification: KPMG Confidential

Individuals whose interest is to be recorded on a PSC Register

1. An individual holding, directly or indirectly:

- more than 25 per cent. of the shares in the company

- more than 25 per cent. of the voting rights in the company

- the right to appoint or remove a majority of the board of directors of the company

2. An individual who has the right to exercise, or actually exercises, significant influence or control over the company

3. Where the trustees of a trust or the members of a firm (other than a legal person) hold an interest in company in a way set out in the four bullets above any individual who has the right to exercise or actually exercises significant influence or control over the activities of that trust or firm

PSC Register – Interests to be recorded

37

© 2017 KPMG Luxembourg, Société coopérative, a Luxembourg entity and a member firm of the KPMG network of independent member firms affiliated with KPMG International Cooperative (“KPMG International”), a Swiss entity. All rights reserved

Document Classification: KPMG Confidential

Chains of entities

• Where the individual exercises relevant ownership rights or significant influence or control through an intermediate legal entity or chain of legal entities, the first legal entity in the chain which:

- keeps its own PSC register or

- which is subject to an equivalent disclosure regime in its jurisdiction

… must be registered instead of the individual.

PSC Register – Interests to be recorded

38

© 2017 KPMG Luxembourg, Société coopérative, a Luxembourg entity and a member firm of the KPMG network of independent member firms affiliated with KPMG International Cooperative (“KPMG International”), a Swiss entity. All rights reserved

Document Classification: KPMG Confidential

Significant influence or control are alternatives

• ‘Control’ – power to direct policies and activities

• ‘Significant influence’ – the ability to significantly influence the adoption of policies or activities

• NOT restricted to influence or control over financial and operating policies

• NOT restricted to influence or control deriving economic benefit

Right to exercise …

• constitution/LLP agreement, shareholders’ agreement

• interest or rights which IF exercised would give rise to significant influence or control

Actually exercises … : All relationships a person has with the entity or its managers taken into account – cumulative effect of all such interactions relevant

Excepted roles

• Advisors …

Meaning of ‘Significant Influence or Control’

39

© 2017 KPMG Luxembourg, Société coopérative, a Luxembourg entity and a member firm of the KPMG network of independent member firms affiliated with KPMG International Cooperative (“KPMG International”), a Swiss entity. All rights reserved

Document Classification: KPMG Confidential

I do not currently have a PSC Register

• Criminal offence: the PSC Register can never be empty

• Prescribed wording where PSCs not identified

I have not yet responded to notifications/requests for information sent to me

• Failure to respond is a criminal offence

• Shares subject to restrictions (comply or explain approach)

I have not provided the correct information or corrected my information

• Proactive obligation

• Criminal offence

Can I prevent my information being disclosed?

• Failure to respond is a criminal offence

• Exceptional circumstances

Common Questions

40

© 2017 KPMG Luxembourg, Société coopérative, a Luxembourg entity and a member firm of the KPMG network of independent member firms affiliated with KPMG International Cooperative (“KPMG International”), a Swiss entity. All rights reserved

Document Classification: KPMG Confidential

Trusts

© 2017 KPMG Luxembourg, Société coopérative, a Luxembourg entity and a member firm of the KPMG network of independent member firms affiliated with KPMG International Cooperative (“KPMG International”), a Swiss entity. All rights reserved

Document Classification: KPMG Confidential

• Feb 2014 – ‘MEPs vote to name trust beneficiaries in public registries’

• July 2014 –rejected by EU Council but under 4th Directive:

- trustees of express trusts must obtain and hold information identifying the settlor, the protector (if any) and the beneficiaries or class of beneficiaries of the trust, and of any other natural person exercising ultimate control over the trust;

- the information must be accessible by Member States' competent authorities;

- but the information does not have to be included in a publicly available register.

• June 2017 - Creation of non public register of trusts in UK

How are they affected?

42

© 2017 KPMG Luxembourg, Société coopérative, a Luxembourg entity and a member firm of the KPMG network of independent member firms affiliated with KPMG International Cooperative (“KPMG International”), a Swiss entity. All rights reserved

Document Classification: KPMG Confidential

UK residential property

© 2017 KPMG Luxembourg, Société coopérative, a Luxembourg entity and a member firm of the KPMG network of independent member firms affiliated with KPMG International Cooperative (“KPMG International”), a Swiss entity. All rights reserved

Document Classification: KPMG Confidential

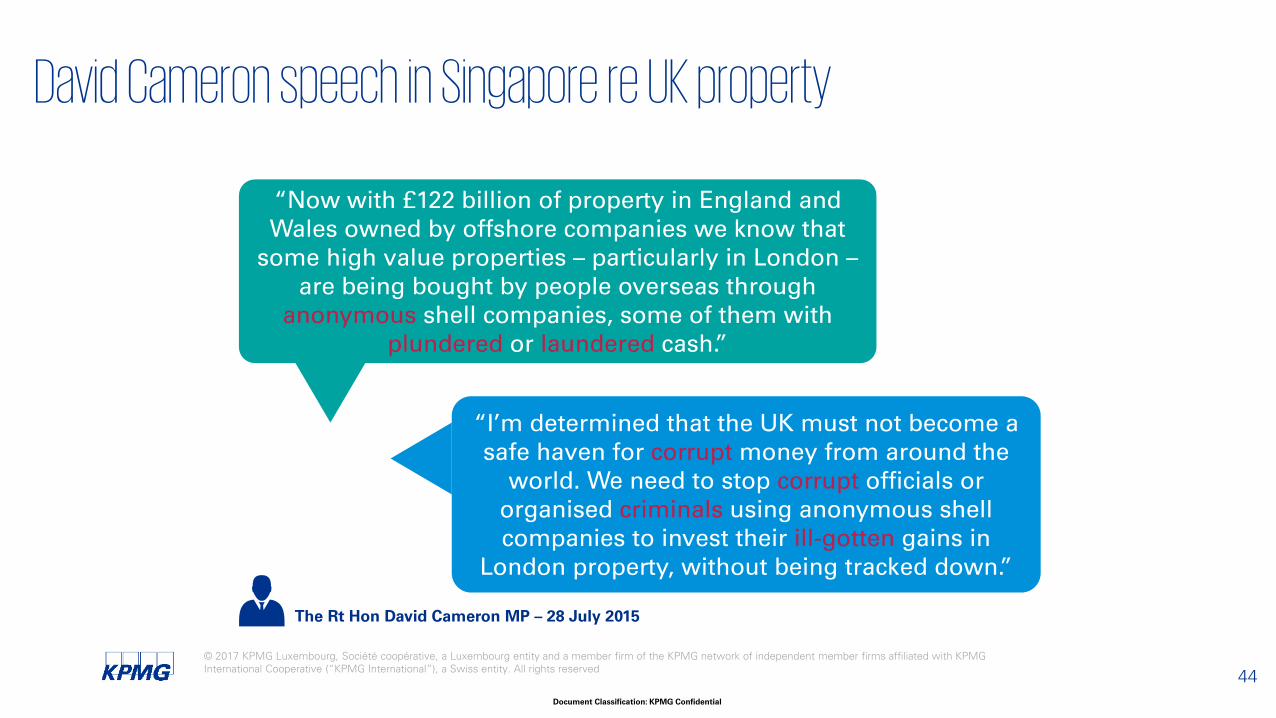

“Now with £122 billion of property in England and Wales owned by offshore companies we know that

some high value properties – particularly in London –are being bought by people overseas through

anonymous shell companies, some of them with plundered or laundered cash.”

“I’m determined that the UK must not become a safe haven for corrupt money from around the

world. We need to stop corrupt officials or organised criminals using anonymous shell companies to invest their ill-gotten gains in

London property, without being tracked down.”

The Rt Hon David Cameron MP – 28 July 2015

David Cameron speech in Singapore re UK property

44

© 2017 KPMG Luxembourg, Société coopérative, a Luxembourg entity and a member firm of the KPMG network of independent member firms affiliated with KPMG International Cooperative (“KPMG International”), a Swiss entity. All rights reserved

Document Classification: KPMG Confidential

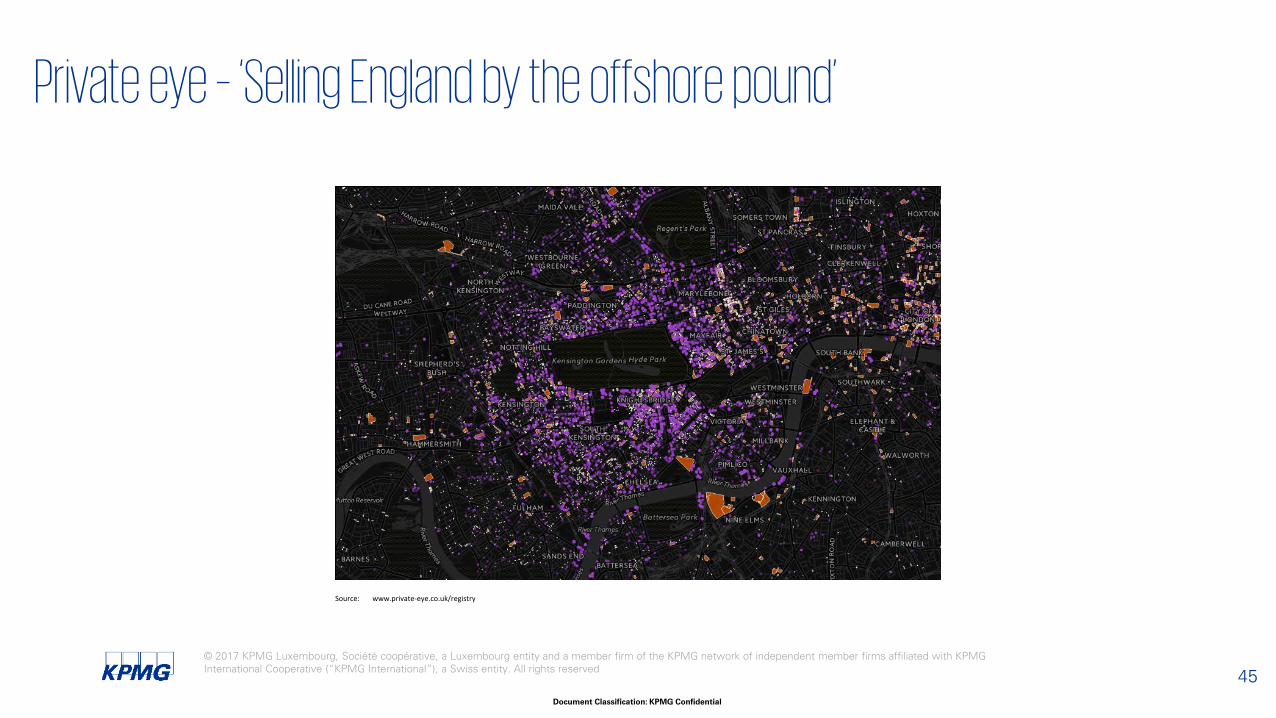

Source: www.private-eye.co.uk/registry

Private eye – ‘Selling England by the offshore pound’

45

© 2017 KPMG Luxembourg, Société coopérative, a Luxembourg entity and a member firm of the KPMG network of independent member firms affiliated with KPMG International Cooperative (“KPMG International”), a Swiss entity. All rights reserved

Document Classification: KPMG Confidential

Country Transactions

British Virgin Islands 22,155

Jersey 20,590

Isle of Man 12,061

Guernsey 11,536

Mauritius 2,782

Gibraltar 2,657

Luxembourg 2,513

Panama 1,963

Ireland 1,957

Singapore 1,782

Other (122 named jurisdictions) 21,001

• UK property acquired by offshore companies 1999-2014

• As a first step Land Registry to publish details of legal owners of UK property held by offshore company

Source: www.private-eye.co.uk/registry - March 2016

Private Eye (cont.)

46

© 2017 KPMG Luxembourg, Société coopérative, a Luxembourg entity and a member firm of the KPMG network of independent member firms affiliated with KPMG International Cooperative (“KPMG International”), a Swiss entity. All rights reserved

Document Classification: KPMG Confidential

• Discussion Paper – March 2016

• Beneficial Ownership details provided before acquisition of property

• What about existing 100,000?

• Sanctions for non provision of information

• Publicly available?

UK Property - UBO register?

47

© 2017 KPMG Luxembourg, Société coopérative, a Luxembourg entity and a member firm of the KPMG network of independent member firms affiliated with KPMG International Cooperative (“KPMG International”), a Swiss entity. All rights reserved

Document Classification: KPMG Confidential

The Common Reporting Standard

© 2017 KPMG Luxembourg, Société coopérative, a Luxembourg entity and a member firm of the KPMG network of independent member firms affiliated with KPMG International Cooperative (“KPMG International”), a Swiss entity. All rights reserved

Document Classification: KPMG Confidential

2017

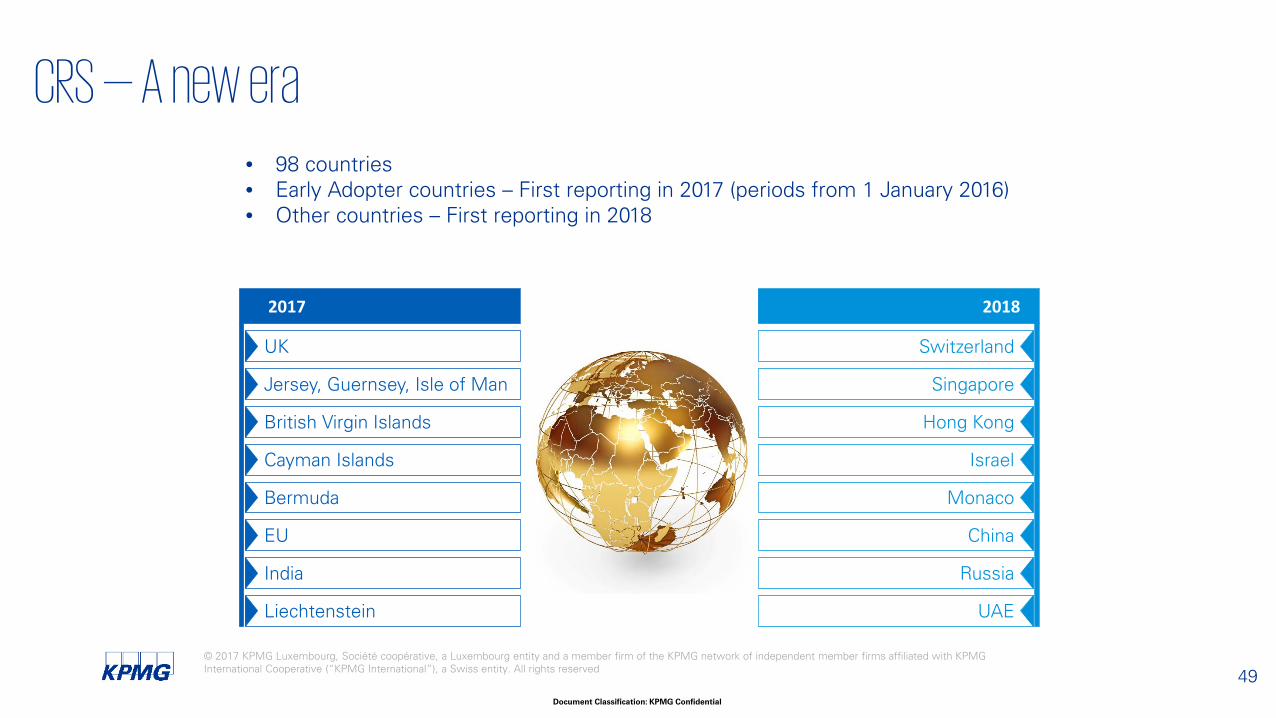

UK

Jersey, Guernsey, Isle of Man

British Virgin Islands

Bermuda

Cayman Islands

EU

India

Liechtenstein

2018

Switzerland

Singapore

Hong Kong

Monaco

Israel

China

Russia

UAE

• 98 countries• Early Adopter countries – First reporting in 2017 (periods from 1 January 2016)• Other countries – First reporting in 2018

CRS — A new era

49

© 2017 KPMG Luxembourg, Société coopérative, a Luxembourg entity and a member firm of the KPMG network of independent member firms affiliated with KPMG International Cooperative (“KPMG International”), a Swiss entity. All rights reserved

Document Classification: KPMG Confidential

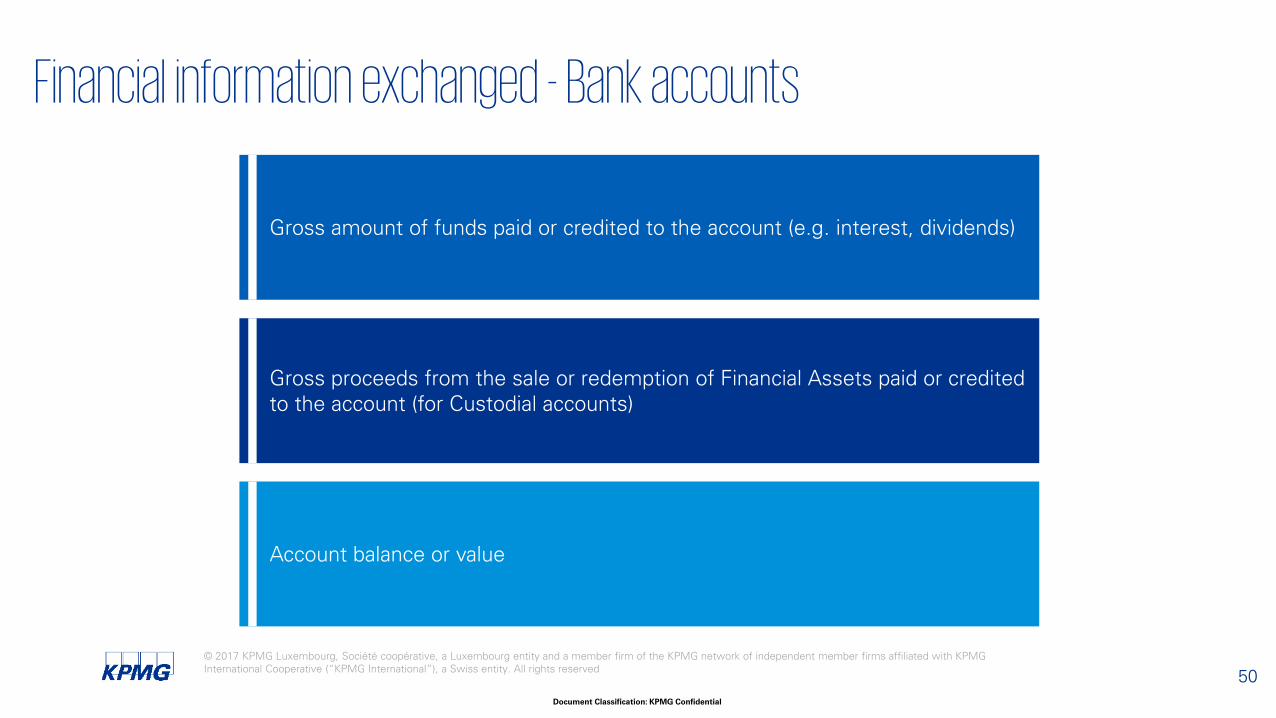

Gross amount of funds paid or credited to the account (e.g. interest, dividends)

Gross proceeds from the sale or redemption of Financial Assets paid or credited to the account (for Custodial accounts)

Account balance or value

Financial information exchanged - Bank accounts

50

© 2017 KPMG Luxembourg, Société coopérative, a Luxembourg entity and a member firm of the KPMG network of independent member firms affiliated with KPMG International Cooperative (“KPMG International”), a Swiss entity. All rights reserved

Document Classification: KPMG Confidential

Information and use

© 2017 KPMG Luxembourg, Société coopérative, a Luxembourg entity and a member firm of the KPMG network of independent member firms affiliated with KPMG International Cooperative (“KPMG International”), a Swiss entity. All rights reserved

Document Classification: KPMG Confidential

• AEOI data (CDOT, CRS)− Banking information− Interests in trusts and companies

• PSC Register for UK companies

• European 4th AML directive

• Proposed pilot to exchange beneficial ownership (companies and trusts) – 32 countries

• UK property owned by overseas companies

• ‘Panama papers’

• Other data leaks

Information at HMRC’s disposal

52

© 2017 KPMG Luxembourg, Société coopérative, a Luxembourg entity and a member firm of the KPMG network of independent member firms affiliated with KPMG International Cooperative (“KPMG International”), a Swiss entity. All rights reserved

Document Classification: KPMG Confidential

x 28

“CONNECT” - 22 billion lines of data

Size of data – can they cope?

53

© 2017 KPMG Luxembourg, Société coopérative, a Luxembourg entity and a member firm of the KPMG network of independent member firms affiliated with KPMG International Cooperative (“KPMG International”), a Swiss entity. All rights reserved

Document Classification: KPMG Confidential

• More enquiries

• Deeper enquiries

• Guilty until proven innocent – the Swiss account experience

• CDOT - allow UK competent authorities access to 'company beneficial ownership information without restriction, subject to relevant safeguards'

• Personal balance sheets for clients worth >£10m

What can we expect from HMRC?

54

© 2017 KPMG Luxembourg, Société coopérative, a Luxembourg entity and a member firm of the KPMG network of independent member firms affiliated with KPMG International Cooperative (“KPMG International”), a Swiss entity. All rights reserved

Document Classification: KPMG Confidential

The right to privacy?

© 2017 KPMG Luxembourg, Société coopérative, a Luxembourg entity and a member firm of the KPMG network of independent member firms affiliated with KPMG International Cooperative (“KPMG International”), a Swiss entity. All rights reserved

Document Classification: KPMG Confidential

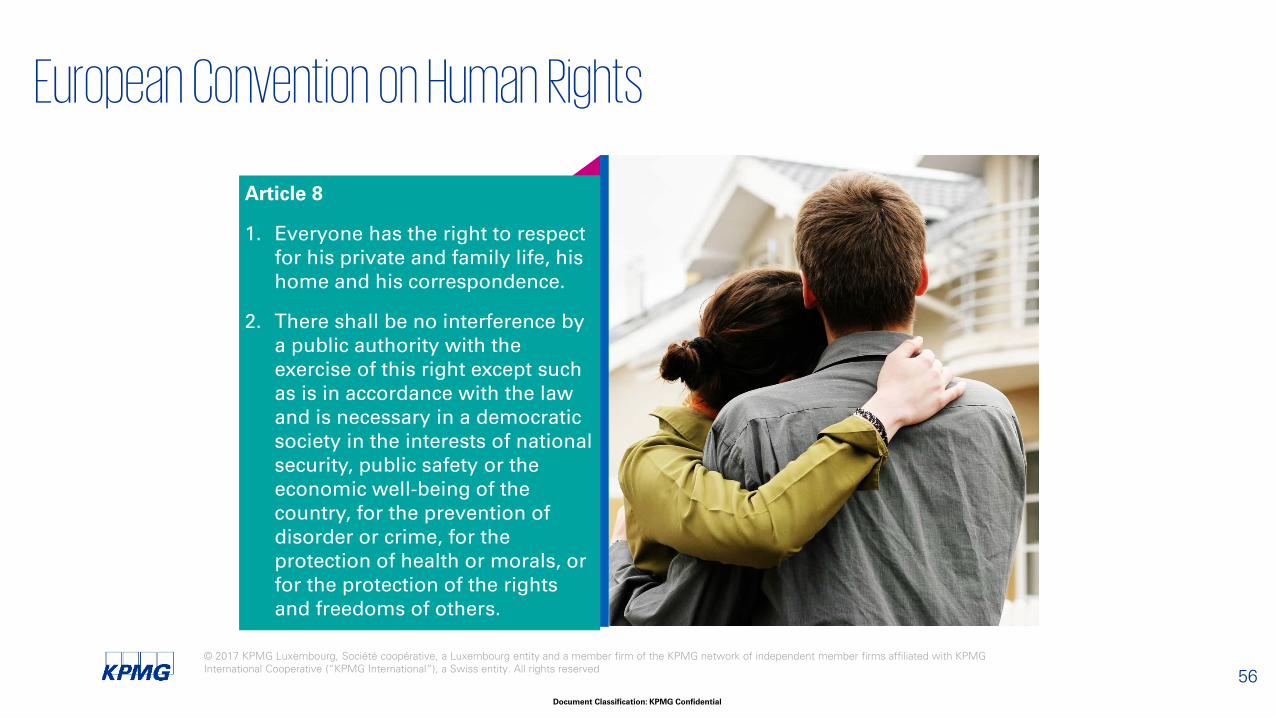

Article 8

1. Everyone has the right to respect for his private and family life, his home and his correspondence.

2. There shall be no interference by a public authority with the exercise of this right except such as is in accordance with the law and is necessary in a democratic society in the interests of national security, public safety or the economic well-being of the country, for the prevention of disorder or crime, for the protection of health or morals, or for the protection of the rights and freedoms of others.

European Convention on Human Rights

56

© 2017 KPMG Luxembourg, Société coopérative, a Luxembourg entity and a member firm of the KPMG network of independent member firms affiliated with KPMG International Cooperative (“KPMG International”), a Swiss entity. All rights reserved

Document Classification: KPMG Confidential

Clients’ reaction......so far

57

Belgium

© 2017 KPMG Luxembourg, Société coopérative, a Luxembourg entity and a member firm of the KPMG network of independent member firms affiliated with KPMG International Cooperative (“KPMG International”), a Swiss entity. All rights reserved

Document Classification: KPMG Confidential

Situation in Belgium

1. UBO – register…still a “non-event”

2. Cayman tax…a short update

3. Internal capital gains…“abolished” as from 2017

4. Withholding tax…increased as from 2017 up to 30%

5. Capital gains taxation…to be expected in 2017???

59

Germany

© 2017 KPMG Luxembourg, Société coopérative, a Luxembourg entity and a member firm of the KPMG network of independent member firms affiliated with KPMG International Cooperative (“KPMG International”), a Swiss entity. All rights reserved

Document Classification: KPMG Confidential

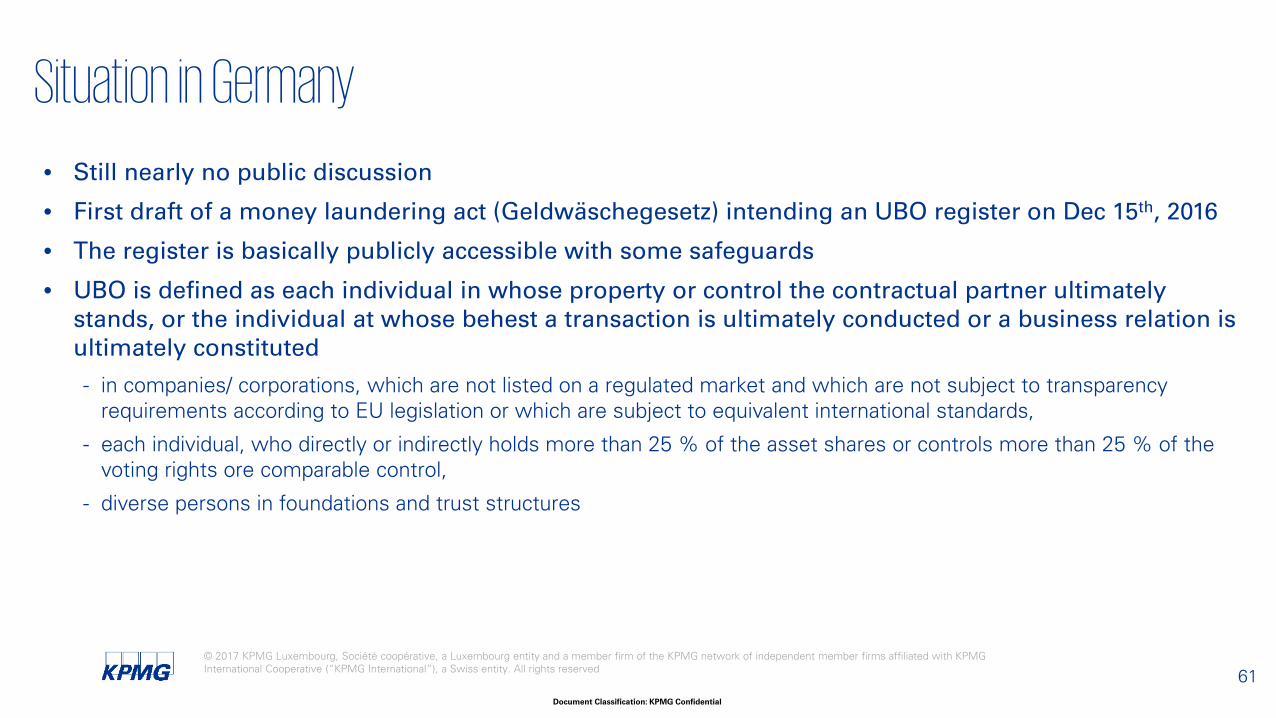

• Still nearly no public discussion

• First draft of a money laundering act (Geldwäschegesetz) intending an UBO register on Dec 15th, 2016

• The register is basically publicly accessible with some safeguards

• UBO is defined as each individual in whose property or control the contractual partner ultimately stands, or the individual at whose behest a transaction is ultimately conducted or a business relation is ultimately constituted

- in companies/ corporations, which are not listed on a regulated market and which are not subject to transparency requirements according to EU legislation or which are subject to equivalent international standards,

- each individual, who directly or indirectly holds more than 25 % of the asset shares or controls more than 25 % of the voting rights ore comparable control,

- diverse persons in foundations and trust structures

Situation in Germany

61

© 2017 KPMG Luxembourg, Société coopérative, a Luxembourg entity and a member firm of the KPMG network of independent member firms affiliated with KPMG International Cooperative (“KPMG International”), a Swiss entity. All rights reserved

Document Classification: KPMG Confidential

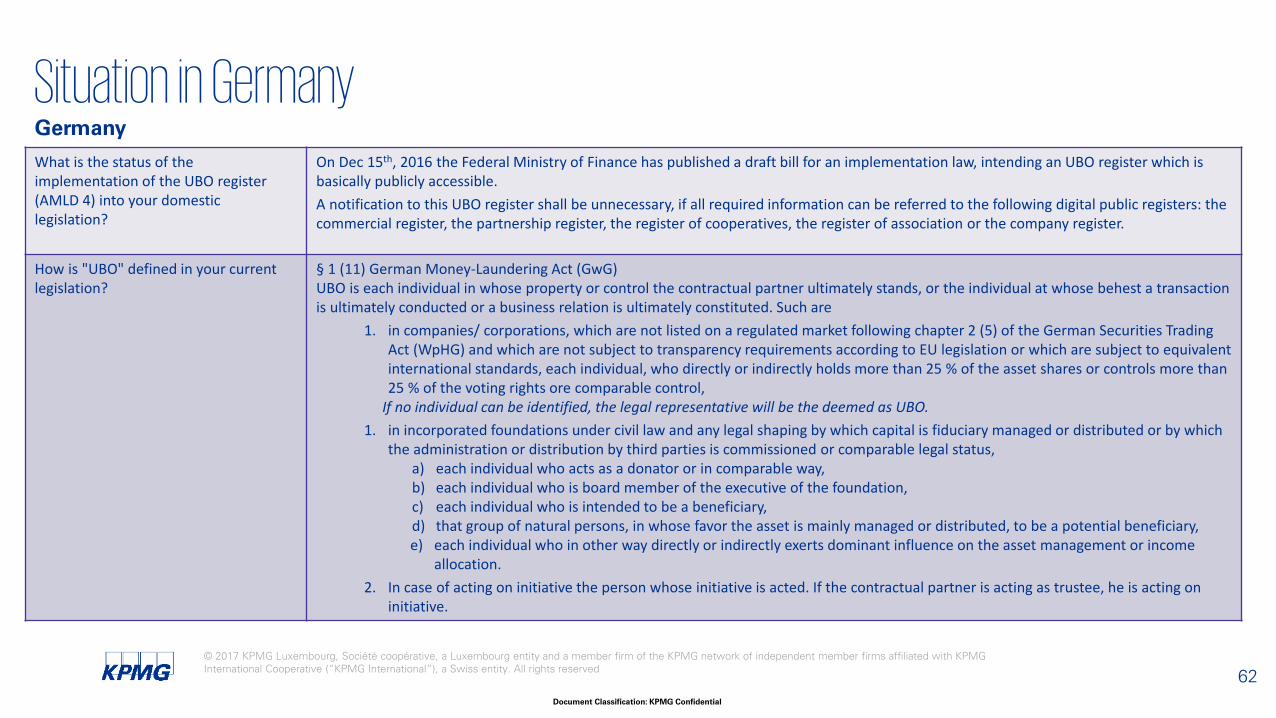

Germany

What is the status of the implementation of the UBO register (AMLD 4) into your domestic legislation?

On Dec 15th, 2016 the Federal Ministry of Finance has published a draft bill for an implementation law, intending an UBO register which is basically publicly accessible. A notification to this UBO register shall be unnecessary, if all required information can be referred to the following digital public registers: the commercial register, the partnership register, the register of cooperatives, the register of association or the company register.

How is "UBO" defined in your current legislation?

§ 1 (11) German Money-Laundering Act (GwG)UBO is each individual in whose property or control the contractual partner ultimately stands, or the individual at whose behest a transaction is ultimately conducted or a business relation is ultimately constituted. Such are

1. in companies/ corporations, which are not listed on a regulated market following chapter 2 (5) of the German Securities Trading Act (WpHG) and which are not subject to transparency requirements according to EU legislation or which are subject to equivalent international standards, each individual, who directly or indirectly holds more than 25 % of the asset shares or controls more than 25 % of the voting rights ore comparable control,

If no individual can be identified, the legal representative will be the deemed as UBO.1. in incorporated foundations under civil law and any legal shaping by which capital is fiduciary managed or distributed or by which

the administration or distribution by third parties is commissioned or comparable legal status,a) each individual who acts as a donator or in comparable way,b) each individual who is board member of the executive of the foundation,c) each individual who is intended to be a beneficiary,d) that group of natural persons, in whose favor the asset is mainly managed or distributed, to be a potential beneficiary,e) each individual who in other way directly or indirectly exerts dominant influence on the asset management or income

allocation.2. In case of acting on initiative the person whose initiative is acted. If the contractual partner is acting as trustee, he is acting on

initiative.

Situation in Germany

62

© 2017 KPMG Luxembourg, Société coopérative, a Luxembourg entity and a member firm of the KPMG network of independent member firms affiliated with KPMG International Cooperative (“KPMG International”), a Swiss entity. All rights reserved

Document Classification: KPMG Confidential

Germany

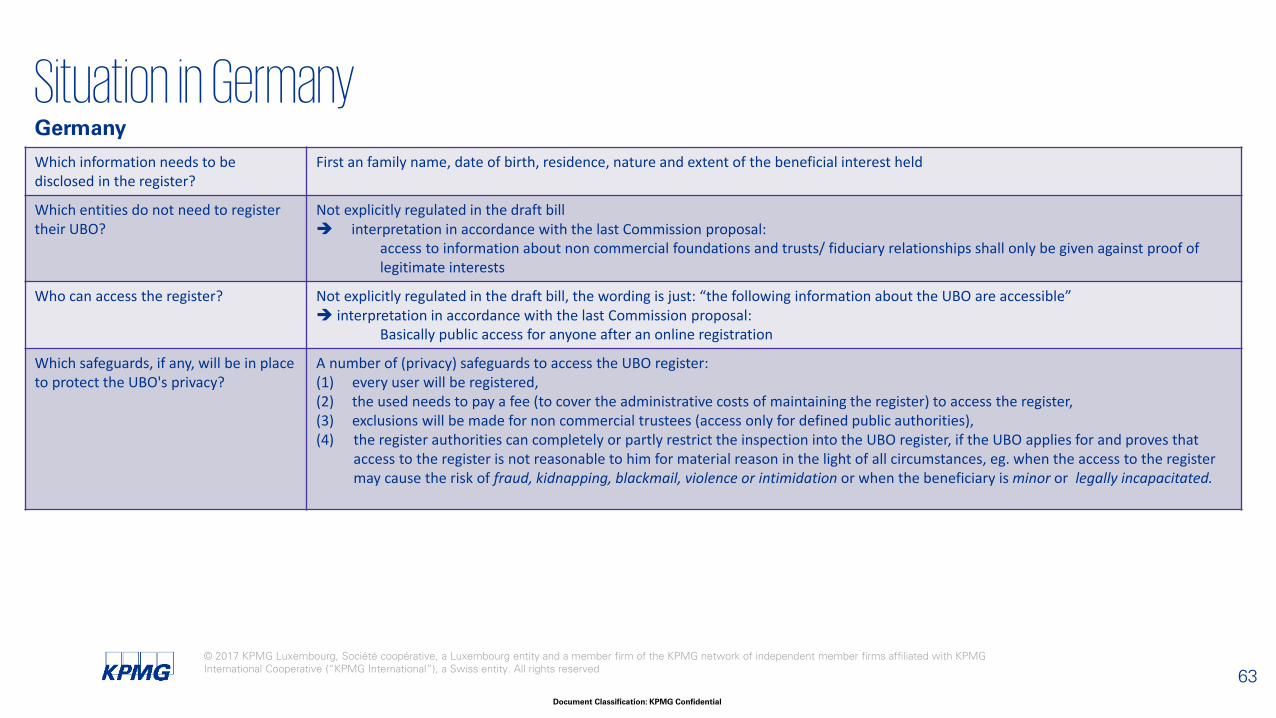

Which information needs to be disclosed in the register?

First an family name, date of birth, residence, nature and extent of the beneficial interest held

Which entities do not need to register their UBO?

Not explicitly regulated in the draft bill interpretation in accordance with the last Commission proposal:

access to information about non commercial foundations and trusts/ fiduciary relationships shall only be given against proof of legitimate interests

Who can access the register? Not explicitly regulated in the draft bill, the wording is just: “the following information about the UBO are accessible” interpretation in accordance with the last Commission proposal:

Basically public access for anyone after an online registration

Which safeguards, if any, will be in place to protect the UBO's privacy?

A number of (privacy) safeguards to access the UBO register: (1) every user will be registered,(2) the used needs to pay a fee (to cover the administrative costs of maintaining the register) to access the register,(3) exclusions will be made for non commercial trustees (access only for defined public authorities),(4) the register authorities can completely or partly restrict the inspection into the UBO register, if the UBO applies for and proves that

access to the register is not reasonable to him for material reason in the light of all circumstances, eg. when the access to the register may cause the risk of fraud, kidnapping, blackmail, violence or intimidation or when the beneficiary is minor or legally incapacitated.

Situation in Germany

63

Panel discussion

Q & A

Thank you

© 2017 KPMG Luxembourg, Société coopérative, a Luxembourg entity and a member firm of the KPMG network of independent member firms affiliated with KPMG International Cooperative (“KPMG International”), a Swiss entity. All rights reserved

Document Classification: KPMG Confidential

Contact us

67

The information contained herein is of a general nature and is not intended to address the circumstances of any particular individual or entity. Although we endeavour to provide accurate and timely information, there can be no guarantee that such information is accurate as of the date it is received or that it will continue to be accurate in the future. No one should act on such information without appropriate professional advice after a thorough examination of the particular situation.

© 2017 KPMG Luxembourg, Société coopérative, a Luxembourg entity and a member firm of the KPMG network of independent member firms affiliated with KPMG International Cooperative (“KPMG International”), a Swiss entity. All rights reserved

The KPMG name and logo are registered trademarks or trademarks of KPMG International.

kpmg.lu kpmg.lu/app