Embed Size (px)

Citation preview

Homeowners Insurance Guide – Florida 2018/19

HOMEOWNERS

INSURANCE GUIDEFLORIDA - 2018/19

Martyn Belben

HOMEOWNERS INSURANCECLAIMS HANDLING PRACTICES TODAY

How Florida Homeowner policyholdersare fleeced by their insurance companies

with absolute and total impunitywith the tacit approval of the

Florida Department of Insurance

i

Homeowners Insurance Guide B Florida 2018/19

Copyright 8 2018 byMartyn G. D. Belben Fort Lauderdale, Florida, USA.March 2018All rights reserved, including the right to reproduce this book, or portions thereof, in any form, except for the inclusion of brief quotations in a review.

ii

Homeowners Insurance Guide B Florida 2018/19

iii

Homeowners Insurance Guide B Florida 2018/19

LEGAL ISSUES

Where it seems to me to be appropriate, I have made comments which may be considered to have a legal flavor.However, nothing written in this book should be construed as legal opinion or legal advice. The language used in this guide reflect my own thoughts and opinions and are based on knowledge and experience gained in this and other jurisdictions during my career spanning over sixty four years of investigating and adjusting property and marine claims in over seventy countries, worldwide.In some of those jurisdictions qualified loss adjusters routinely handle claims which they are prohibited from handling to a conclusion and settlement in the United States. Inevitably, some of that knowledge and experience has lodged in my subconscious, which I sometime call upon to make my point.If you need legal advice call any of the fine and able attorneys, specialists in Florida property insurance law, who practice at the Florida Plaintiffs= Bar. Go to www.FAPIA.net and research their website for attorneys advertising there.

Any of them, or all of them can give you advice upon which you may rely

iv

Homeowners Insurance Guide B Florida 2018/19

PROLOGUEEvery effort has been made to ensure that the information contained in this guide is accurate and may be relied upon as such by the reader.Statistics contained in the insurance carrier section, Chapter 30, at the end of this guide, were provided by the Florida Department of Insurance and other reliable research sites, and therefore are expected to be correct.The comments made in this guide relating to unethical conduct by those engaged in the claims business, on the carrier side of the equation, are based on facts, extracted from analysis of actual claim files over a period of two years preceding the dates of research.During the past 25 years, Plaintiff’s= attorneys and others have attempted to curb the carriers escalating unfair, and illegal claims handling practices using language which has taken the Ahigh road.@

Those efforts have fallen on deaf ears, and the carriers= lust for greater profits and surpluses have now become nothing short of a machine that openly defrauds its policyholders, in the manner of a disguised, variation of a Ponzi scheme, masquerading as an insurance company.Moreover, the Florida Department of Insurance, whose job includes protecting Florida=s policyholders from predatory insurance companies, have taken no action whatsoever to address this activity.

v

Homeowners Insurance Guide B Florida 2018/19

CHAPTER 1TRADITIONAL CLAIMS HANDLING

The global insurance industry has changed dramatically over the last twenty-five years, and the industry today is not the same as it was in our parents= days.In those days, when a homeowner filed a claim, the circumstances of loss and the merits of the claim were investigated by a trained, knowledgeable, experienced and licensed loss adjuster representing the insurance company. That adjuster, after a thorough inquiry into the reported loss (how, what, when, where and why), made determinations as to the cause of the loss, confirmed the coverage provided by the policy, the extent of damage to the property, and the repair value of the loss.

The adjuster then wrote an Estimate, a copy of which was provided to the policyholder, which included all the hidden damage. It also included all the items required to be included by Florida Statute Law and Florida Case Law. Settlement recommendations were then made to management. A payment in settlement was made promptly, usually within two to four weeks, depending upon the severity of the loss, and the amount of paperwork required by management and their reinsurers. Both the insurance carrier and the policyholder were satisfied.

The insurance company had made good on its promises in its policy, and had treated its policyholder fairly, reasonably and promptly. This system had stood the test of time for over four hundred years.Also, at that time, the property insurance industry was a quasi-service industry which managed to combine

1

Homeowners Insurance Guide B Florida 2018/19

on the one hand, the principle that they were providing a vital service to the insurance homeowner/consumer, while on the other hand, running their businesses with utmost integrity, fairness and good faith, and the absolute trust each had in the other (the insurance company and the policyholder), and a reasonable and satisfactory profit was made.The result was that the insurance industry, globally, over time, came to enjoy the envy and unimpeachable respect of every other business community, in every conceivable endeavor, profession and calling, worldwide.The whole system changed in 1992.

2

Homeowner=s Insurance Guide B Florida 2018/19

CHAPTER 2THE NEW CONCEPT OF CLAIMS HANDLING In 1992, the then President of Allstate Insurance hired McKInsey & Company., a New York firm of Management Consultants, to investigate all aspects of their business, and make recommendations for changes to improve their bottom line. Essentially, he wanted to convert Allstate from a quasi-service business to primarily an ultra-aggressive, profit motivated business.In due time, the resultant recommendations made by McKinsey were accepted enthusiastically by Allstate=s Board of Directors, and so was spawned what has been called a Plague, which quickly spread from its initiator, Allstate, to State Farm, Nationwide, and eventually to almost every property insurance carrier throughout the World, with a few, exceptions.Most states, including Florida, have made the McKinsey doctrine, the essence of which is using unfair claims handling practices, illegal. These unfair claims handling practices have become known as ADENY, DELAY AND DEFEND.@ DENY, DELAY AND DEFEND are the tools used by insurers massively to increase their profits by denying legitimate claims without a valid reason; delaying claims for months or years, without justifiable cause in the hope of bullying their policyholders into accepting an arbitrary settlement at a mere pittance of their actual policy entitlement. Finally, if their policyholder elects not to settle for the pittance offered but instead, consults an attorney who files suit for breach of contract, their tactic is to defend that (legitimate and justifiable) law suit using spurious and largely fictional reasons for denying, and/or delaying and/or defending the claim.

3

Homeowner=s Insurance Guide B Florida 2018/19

In addition, excessive and escalating use is made again, of delaying tactics as an additional tool as an inducement to force the insured policyholder into accepting a low- balled settlement.This is achieved by using one firm of attorneys to start the Defend, and delay the progress of the law suit by unethical, but legal means, for example: demanding that the policyholder sit for an Examination Under Oath (a Condition in the policy), three or four months in the future. The defense attorney then delays and reschedules the actual examination three or four times, each appointment three, four or six months ahead; as if that harassment were not enough, insurers= defense counsel then employ the same tactics for the legal process connected with the law suit, by making the policyholder sit for a deposition, again cancelling appointments three or four times, each appointment again, three, four or six months ahead. And finally, to add further insult to injury, when it seems that the defense attorneys are going to be forced into finalizing the claim, the defense attorneys are instructed to close their file, and then the claim is reassigned to another defense firm and this unethical game of musical chairs starts all over again, from scratch, with new attorneys.This, now, is AThe Plague,@ known as DENY, DELAY AND DEFEND, which is an abomination to most career insurance professionals, of the old school.Another way to put it that these tactics are used solely as a means of fleecing the policyholder out of his/her/their rightful, justifiable and legal recovery under the policy. Of course, their illegal tactics cost the insurers’ money which additional costs they blame on public insurance adjusters, contractors, and/or Plaintiff’s counsel.Insurance company regulators in Florida have taken little or no action to induce insurers to curb its use of any and all of these tactics, which they have deemed to be Aunfair claims handling practices@, leaving it up to the insured and plaintiff’s counsel to settle disputes using Florida=s legal system.

4

1166

CHAPTER 3 THE PLAGUE IN PRACTICE

This plague has come to be known as:

DENY, DELAY & DEFEND

To summarize: The McKinsey doctrine became an exceptionally successful strategy for handling claims and the system paid off for the insurance industry, in spades. How was this achieved? By radically changing the way they do business, which included, but was not limited to denying legitimate claims without stating a reason; using illegal tactics to delay a covered and compensable claim for months, and sometimes, years; and deliberately under paying their policyholders if and when they paid a claim; or, in the alternative by aggressively defending a law suit, which included but was not limited to using unethical and unfair delaying tactics,; and if suit were to be filed; changing defense attorneys, to delay the process further, and sometimes twice or three times, hoping the claim will go away. Sometimes, the claimant gets tired of the whole process and just lets the claim die. Deny, Delay and Defend has now become the norm, and there are virtually no insurance companies who handle claims the way they were handled before McKinsey.

2

Homeowner=s Insurance Guide B Florida 2018/19

The overriding goal over all other practices, in the handling of claims is now, and will remain for the foreseeable future, to ensure the upward escalation of Profits, Profits and still more Profits.Insurance companies don=t care what their policies promise, or how long a customer has been a customer, who perhaps had never made a claim. It=s always and only about the money!State Farm is notorious for this practice. Indeed, the Florida insurance commissioner allowed State Farm to Anon- renew@ the majority of its Aproperty@ risks, and Acherry pick@ those risks which State Farm considered would expose them to least risk. Most of the Anational@ companies followed suit, leading Florida government officials to resort to creating an AInsurer of Last Resort@ (Citizens), and a mishmash of new Astart up@ Florida companies, most of whom will disappear overnight if Florida has another AAndrew@ to deal with. But, executives in the insurance industry will tell you nothing has changed.they still have the same infrastructure, the same concern for their policyholders (SIC), the same insurance policies (with some modifications), and claims will still be paid. True, claims will be paid, without a fight, only if the claimant homeowner is willing to accept a settlement at a very small fraction of the amount of their actual policy entitlement.

They achieve this by telling the policyholder AThis is all you can get for this damage.@

Insurance company adjusters are now trained to Asee@ only minimal damage, and they write low balled, algorithm, computer based estimates, and they exclude from those estimates all of the items required to be included by Florida Laws, which the insurance industry characterizes as Ainflating an estimate.@ by licensed public adjusters. Insurance Commissioners, and the Florida Legislature have allowed this conduct to develop and continue unabated for over twenty five

Homeowner=s Insurance Guide B Florida 2018/19

years, to the point where every claimant believes they are being short changed. They are right. They are!

Homeowner=s Insurance Guide B Florida 2018/19

Florida Statutes call this conduct AUnfair Claims Handling Practices,@ sometimes called ABad Faith@ practices. The Florida legislature passed laws which allow victims of Bad Faith to sue for damages, but that process is time consuming, and costly.However, when the policyholder prevails in Court (or out of Court if suit has been filed), the defendant insurance company pays the policyholder=s legal fees and costs, for both the underlying suit for Breach of Contract, and the subsequent Bad Faith suit.A few insurance companies, including the largest insurance company in Florida, by the number of policies in force as of December 2017, Universal Property & Casualty Insurance Company, of Fort Lauderdale, Florida has been fined by the Florida Department of Insurance for their unfair and unlawful, claims handling practices.These fines have been in the millions of dollars. To insurers, these fines are only a slap on the wrist. They make (empty) promises to the Florida Insurance Commissioner to henceforth, change their unfair and illegal claims handling practices.The reality is that they then continue to do exactly what they have been fined for doing, and metaphorically thumb their noses at the Insurance Commissioner, who takes no further action, by turning his blind eye!One of the duties of the Florida Insurance Commissioner is to protect consumer policyholders from predator insurers, using unfair and illegal claims handling

practices. Sadly, consumers might just as well shout at a wall, for the shouting falls on deaf ears.The Insurance Commissioner, for once, should do the job to which he was appointed, and do something constructive to ensure that Florida laws are obeyed.

Homeowner=s Insurance Guide B Florida 2018/19

Maybe the Commissioner should suspend an insurance company=s license to do business in Florida until such time as a substantive Claims Manual for handling claims fairly and in a timely manner, in accordance with Florida Law(s) is submitted to The Department, and approved by the Commissioner would the suspension be lifted. That would be a start towards resporing some degree of respectability to the insurance industry.Some years ago, the Commissioner suspended Allstate=s license to do business in Florida after Allstate refused to provide the Department with thousands of documents demanded by the Commissioner, comprised of communications between McKinsey & Co and Allstate relating to the practice of Deny, Delay and Defend.Allstate=s License to do business in Florida was reinstated after Allstate complied with the Commissioner=s demand. Maybe the job should be done by an elected official?

So, where does the Florida Homeowner turn for help to get a claim paid property and fairly, and within the time frame required by the policy and applicable Florida law.Policyholders have one effective profession to turn to in the first instance.This is the profession known as APublic Insurance Adjusters,@ who represent, exclusively, the policyholder. Sometimes, these adjusters are called APrivate Adjusters.Because of the current claims handling practices of the insurance industry, every property claim made in Florida should be handled by a trained and experienced Florida, Licensed and Bonded Public Adjuster retained by the homeowner. Every single one. A Florida licensed and bonded Public Adjuster is the homeowner=s professional advocate, and property claims expert, who establishes the full extent of any damage, caused by an insured event, and he shall also determine the dollar value

Homeowner=s Insurance Guide B Florida 2018/19

of the repairs and claim demanded by your insurance policy, and as required by Florida law.A public adjuster shall also assist and guide the policyholder through all the complicated and perhaps time consuming duties imposed upon the policyholder by the policy after a loss has occurred. He/she shall prepare , also, all the documentation required to support a claim. Finally, the public adjuster shall use all his/her knowledge and skills to negotiate a settlement of the claim.

A policyholder usually has one or two claims in a lifetime. A public adjuster handles, adjusts and negotiates claims all day, every day, and always protects his client=s best interests.There are no Aup front@ fees payable to a public adjuster, and fees are capped by Florida statutes, and can only be billed to the policyholder when the homeowner claimant receives a payment from his insurers.The consumer policyholder who has been underpaid by his/her insurance company, has another option: he/she can hire a knowledgeable, and experienced plaintiff=s attorney/lawyer, on a contingency basis, who will sue for breach of contract.However, an attorney will still need information from a licensed, knowledgeable and experienced public adjuster who would provide him/her with a detailed, line by line, estimate, which will (a) include all hidden damage; and (b) include all additional items required by Florida law, and finally, would provide that attorney with all additional documentation required to prove the client=s claim. A policyholder may say to himself: AI can hire a contractor who will provide me with an estimate free of charge.@ However, it is unlikely that a contractor would be familiar with Florida law, and the way a Ascope of loss@ (the extent of the damage), and all the additional factors which are required to be included in an estimate, by Florida law, whether they are damaged or not.

Homeowner=s Insurance Guide B Florida 2018/19

Homeowner=s Insurance Guide B Florida 2018/19

CHAPTER 4 FLORIDA GOVERNMENTOFFICE OF PROGRAM POLICY ANALYSIS& GOVERNMENT ACCOUNTABILITYReport 10-06 - January 10, 2010

An independent office set up by the Florida Legislature was tasked eight years ago to investigate whether Florida=s Licensed Public Insurance Adjusters actually provide a valuable, and necessary, service to homeowner consumers. That office reported, inter alia, thus:

Public Adjuster retained: Non-Catastrophe Claims:Percentage of Settlement Achieved in excess of settlement offer +574 %

Catastrophe Claims: (Hurricanes)Percentage of Settlement Achievedin excess of settlement offer +747 %

Typical Public Adjuster=s Fees (Capped by Statute):

Catastrophe Claims 10 %Non-Catastrophe Claims 20 %

Homeowner=s Insurance Guide B Florida 2018/19

This independent Report, demonstrates the prudence, and benefit to a homeowner who hires a licensed public adjuster to handle their claim on their behalf, and assist in the settlement of their claims.

Homeowner=s Insurance Guide B Florida 2018/19

CHAPTER 5INFORMATION

NOTE: In 2004, I changed my Florida, Independent Adjuster=s License, to a Florida, Public Adjuster=s License, allowing me to represent policyholders exclusively. I made this change because of the escalating unfair and illegal claims handling practices required by my insurance company instructing principals. To me, their conduct was at best, dishonest.One afternoon, I received a telephone call from a State Farm Regional Claims Manager, based I believe in Georgia, who asked me, AWhen are you going to stop writing these nasty letters to my adjusters?@I replied, AWhen your adjusters resume paying claims as promised by your insurance policies, and the way State Farm used to do before McKinsey.@He said, AI haven=t seen letters like this in twenty five years in the claims business.@I responded, AI haven=t had to write them in fifty years in the claims business.@There was a silence of perhaps five seconds and he said, AWell, we=ll just have to disagree.@I said, AYes, we shall!@ and we hung up.Fifteen minutes later he called me back, and asked, AHow long have you been in the claims business?@I replied, "Fifty years!" "How OLD are you?" he asked, and I said, "71."

Homeowner=s Insurance Guide B Florida 2018/19

There was another long silence, and then he said, AWell, good luck to you, Sir.@ AThank you, Sir,@ I said, and we hung up. I never heard from him again.

CHAPTER 6MISCONCEPTION BYFORMER FLORIDA CABINET MEMBER

Homeowner=s Insurance Guide B Florida 2018/19

A former Florida Cabinet Member, then head honcho at the Florida Department of Financial Services, Tom Gallagher, stated to his audience of perhaps three hundred people, at a public meeting at a school in Port St. Lucie, Florida, after the hurricanes of 2004 struck Florida, words to the effect that: ANo one needs a public adjuster. They just take money out of your pocket.Let your insurance company handle your claim and you will be paid fairly by your insurance company.@After this assurance by the then Secretary of the Florida Department of Financial Services, and effectively, the Insurance Commissioner=s boss, I challenged Secretary Gallagher with a letter, published in the Sun Sentinel newspaper, which I now paraphrase:AA Homeowner submitted a claim for hurricane damage to his home. He received a payment from his insurer, after Deductible, of $4,000. The policyholder hired a public adjuster who wrote an estimate for the claim in the amount of $40,000 after Deductible.

Homeowner=s Insurance Guide B Florida 2018/19

The public adjuster negotiated a settlement with the insurance company at $40,000 after Deductible, an effective additional payment of $36.000.00.The public adjuster charged no fees on the first payment of $4,000.00.The claimant homeowner received an additional and final payment, after public adjuster fees (10%) or $32,400, a total of $36,400.00 against $4,000 initially paid by the insurance company, or an increase over the original offer of 810.0%.Tell me, Mr. Secretary, how has the public adjuster taken money out of his client=s pocket?@Secretary Gallagher did not respond to this question. Obviously, his opinion was flawed, and self- serving, and moreover, demonstrated his profound ignorance of property insurance claims.Former Secretary Gallagher is now Chief Operations Officer at People=s Trust Insurance!Nothing further needs to be said.

Homeowner=s Insurance Guide B Florida 2018/19

CHAPTER 7PRESS PUBLICATIONThe Huffington PostBy Molly Reilly & Max J. RosenthallDecember 13, 2011

AInsurance Claim Delays Deliver Massive Profits to Industry by Shorting Customers.@

AWashington - Unlike many other businesses, the insurance industry is bound by law to act in good faith with its customers. Because of their protective role in the lives of ordinary citizens, insurers have long operated as semi-public trusts. But since the mid-1990s, a new profit-hungry model, combined with weak regulation, has upended that ancient social contract.Claims have been converted into a money-making process, says Russ Roberts, a New Mexico-based management consultant and former business professor at Northwestern University who has studied the insurance industry=s evolution from a service industry to a profit driven machine.The change started when consulting giant, McKinsey & Co. sold Allstate and other leading insurance companies on a new system to boost the bottom line

Homeowner=s Insurance Guide B Florida 2018/19

Rather than adjusting claims the traditional way, which gave claims managers wide latitude to serve customers, insurers embraced a computer-driven method that produced purposely low offers to claimants.Those who took the low ball offers received prompt service, while those who didn=t had their claims delayed and potentially were reduced to bringing expensive lawsuits to fight for their benefits.@In Florida, if you have to sue your insurers to get a valid claim paid, and you prevail in your lawsuit, the insurer pays your legal fees and costs.

Homeowner=s Insurance Guide B Florida 2018/19

CHAPTER 8FLORIDA LICENSED ADJUSTERS

There are several classes of Licenses issued to insurance claims adjusters practicing in Florida: Resident=s Licenses and Non-Resident=s Licenses. But, there are three (3) main Resident=s Licenses issued to Florida resident adjusters by the Florida Department of Insurance. These are:

License 6-20 Insurance Company, Staff, AAll Lines@ Adjuster.

This license is issued to a supposedly qualified staff adjuster, employed by an insurance company, who may have duties as a field adjuster and/or an inside Adesk adjuster.@

License 5-20 Independent AAll Lines@ Adjuster.

This license is issued to a supposedly qualified adjuster who is either self-employed or employed by a firm of Aindependent adjusters@ either as a field adjuster and/or an inside, desk adjuster.

Homeowner=s Insurance Guide B Florida 2018/19

NOTE: In Florida, the term AIndependent Adjuster@ is a misnomer. By definition, he/she is NOT @Independent@ in the customary use of that term.During discussions with any insurance claims official they make a point that, if they assign a claim to an independent adjuster, his estimate carries more weight, because he is AIndependent. This is grossly misleading. By Florida statute, an Aindependent adjuster@ may handle claims only for (a) an insurance company as a self-employed adjuster (who is always subject to their directions and claims handling practices,), as directed by his Aad hoc@ insurance company employer; or he may work for a firm of Aindependent@ adjusters, as an employee of that firm, but he still takes Aarms-length@ directions from the insurance company employing the firm by which he is employed, and again, he is subject to the same claims handling practices as directed by the insurance company.Notwithstanding the title, there is no such person as an AIndependent Adjuster@ in Florida.

3-20 "All Lines" Public Adjuster.

A Florida licensed Public Adjuster may be self- employed, or be employed by a firm of public insurance adjusters. He works, exclusively, for the insured policyholder, whose interests he is duty bound to protect.

Homeowner=s Insurance Guide B Florida 2018/19

CHAPTER 9 FLORIDA PUBLIC ADJUSTERSGeneral Information About Public Adjusters.

A very large percentage of the Licensed and Bonded Public Adjusters now practicing in Florida were formerly senior or management adjusters who worked at some time for the insurance company side of the industry, but became disenchanted with the new claims handling practices under the McKinsey doctrine,. Essentially, they refused to be a party to deliberately short-changing policyholders which they considered a dishonest practice.

FLORIDA ASSOCIATION OF PUBLIC INSURANCE ADJUSTERS

In general, Members of F.A.P.I.A. are vastly more knowledgeable, much better trained and, by attending continuing education conferences arranged by F.A.P.I.A., at least twice each year, they are fully aware of all the changes in Florida Statute Law, Florida Case Law, as those laws that affect the investigation and adjustment of claims; and changes in the Rules and Regulations of the Department of Insurance, as they affect claims handling practices and procedures.

Homeowner=s Insurance Guide B Florida 2018/19

Licensed Public Adjusters are the advocates available to the Florida Homeowners Policyholder (except, of course, attorneys), who abide by Florida law in the investigation and adjustment of property claims, and who protect their homeowner clients= interests.

Homeowner=s Insurance Guide B Florida 2018/19

CHAPTER 10DUTIES PERFORMED BY YOUR LICENSEDAND BONDED PUBLIC ADJUSTER

$ Explain to the policyholder the terms and conditions of his/her Contract, which is required by Florida Statute Law.

$ Provide the homeowner/client with a copy of the signed Contract.

$ Write a Letter of Representation to the insurance company, providing them with a copy of the Contract.

$ Obtains a Certified Copy of the Policy issued to the Insured by the insurance company.

$ Explains the terms and condition of the policy to the policyholder(s) Claimant(s).

$ Attend on site and inspect the insured property and make a note (called writing a scope), of all the damage found, including all the hidden damage, if any.

Homeowner=s Insurance Guide B Florida 2018/19

$ Generate a detailed, line by line computerized Estimate (which is updated quarterly to reflect changes in the prices of materials and labor), of the costs of making good all the damage and restoring the insured property to its pre-loss condition.

$ Provide the insurance company, and the policyholder with a copy of his/her Estimate, with necessary supporting information.

$ Contact the field adjuster and, in liaison with the policyholder, set up a joint inspection with the field adjuster.

$ Meet the field adjuster on site at the agreed date and time, and will show him/her all the damage to the insured property; and he will provide that field adjust with a copy of his estimate.

$ Assists the policyholder(s) in preparing a Sworn Statement in Proof of Loss, which when signed by the policyholder(s) becomes the policyholders= formal Statement of Claim, and supporting documentation.

Homeowner=s Insurance Guide B Florida 2018/19

$ Submits the Proof of Loss and supporting documentation to the insurance company. $ Explains any partial payment made by the insurance company.

$ Explains any omissions from the insurance company=s Estimate submitted to the Claimant(s) or Policyholders, and discusses those omissions.

$ Makes recommendations to the policyholder(s) as to further action to obtain a full and complete recovery from the insurance company.

$ Attempts to negotiate an acceptable settlement with the insurance company representatives.

$ Explains the pros and cons of the Appraisal process, if necessary.

$ Explains the pros and cons of DFS sponsored Mediation.

$ Discusses options with the policyholder(s).

$ Establishes contact with the Policyholder(s) attorney, and briefs that attorney on the items at issue in the claim.

Homeowner=s Insurance Guide B Florida 2018/19

$ Provides the Attorney with a complete copy of his file.

$ If requested to do so, assists the attorney with additional work needed, if any, to enable the attorney to move forward with the claim.

$ Performs other duties, as directed by the attorney.

Homeowner=s Insurance Guide B Florida 2018/19

CHAPTER 11PUBLIC ADJUSTER=S FEES

Public Adjusters Fees are chargeable and payable only after the claimant/client has received the insurance company=s check(s). A public adjuster is prohibited from charging Aout of pocket@ costs, such as telephone, postage, etc. unless those charges have been fully explained and scheduled in his/her Contract with his/her Client. Florida Statutes prohibit any Aup front@ charges by a public adjuster.Fees may not be charged on partial settlements paid to the claimant/client, prior to the date of the Public Adjuster=s Contract.Public Adjusters Fees are capped by Florida Statutes, as follows:

Based on payments made to thepolicyholder by the insurer:

Catastrophe Claims, Hurricanes etc. 10%

Non-Catastrophe Claims 20%

Homeowner=s Insurance Guide B Florida 2018/19

Homeowner=s Insurance Guide B Florida 2018/19

CHAPTER 12INSURANCE INDUSTRY CLAIMS HANDLING PRACTICES

The insurance industry no longer trains its adjusters to adjust a claim, that task is in the hands of their estimating computer software.Nor do they inform, or train its adjusters in either existing Florida Statute Law or Florida Case Law, or changes in those laws, because to do so would increase the bottom line of estimates, which would be counter productive to the claims handling practices as espoused by the McKinsey plan.Moreover, what is more important, they are required to take those laws into account, but they ignore that duty, again, with impunity.In insurance company practice, as a claims handling strategy often results in a valid claim being denied outright, usually quoting a policy exclusion. For example: If a policyholder filed a claim for a broken pipe under the slab foundation of the dwelling, the Field Adjuster may state that the damage is not covered by the policy, because the damage was caused by Awear and tear@ which is one of the exclusions in every policy. The company will then deny that claim.However, what he will not tell the homeowner, is that, although the damage caused to the pipe was wear

Aand tear,@ and thus excluded from coverage, the costs of jack-hammering through the slab, and any damage caused to the concrete slab, floor coverings, cabinets, walls etc. etc. is damage caused by obtaining access to the damaged pipe; and restoring

Homeowner=s Insurance Guide B Florida 2018/19

the dwelling to it=s pre-loss condition, which is a recoverable expense under the policy.The insurance company will delay the progress of your claim for months, perhaps years, using a multitude of excuses well known to plaintiffs= attorneys. Failing to answer correspondence or other paperwork, for months. And then, when time is running out, they will pull that claim file from that attorney and then give the file to another firm, where the entire process is re-started from scratch.The new firm of attorneys needs to make money too by re-starting from scratch.Defend means that the defense attorneys will cite a myriad of spurious reasons why your claim should be denied, from suggesting that your roof, for example, had already lived it=s useful like prior to the alleged loss - to suggesting that your water damage claim should be denied because you child left the bath water faucet running. Defense attorneys can get quite creative.But, public adjusters have heard it all before.

Homeowner=s Insurance Guide B Florida 2018/19

INDUSTRY CLAIMED INFLATION OF ESTIMATES

It is common practice by insurance industry spokesmen or spokeswomen, and also the CEOs of the insurance companies using the McKinsey doctrine to a very extreme level, like the CEO of Citizens, for example, to try to convince the insuring consumer, at every opportunity, particularly when speaking to Athe media,@ to assert that public insurance adjusters habitually inflate their estimates, because they are paid a percentage of the amount paid on a claim. The truth is that public adjusters are only allowed by Florida law to chaarge a fee based upon the amount paid by the insurer to their policyholder. The further truth is the duty imposed upon them also by Florida law, as a duty to his/her Client, public adjusters are required to include in their estimates EVERY MANDATORY ITEM, demanded by every Statute Law, and every Florida COURT DECISION in Florida Case Law, which affect the SCOPE of a loss upon which an estimate is written.

Insurance companies, as an every day/every claim practice, actively and without exception ignore those laws which may increase their claim payment(s) and allege instead that public adjusters are inflating their estimates.

It bears repeating that, today, the primary purpose above all other considerations, is to increase profits or the surplus, and therefore, avoid, ignore and escape from compliance with any laws that might increase their obligation to pay for those parts of a claim which are outside their self serving practices, in a

Homeowner=s Insurance Guide B Florida 2018/19

deliberate attempt to defraud their policyholders of their right to a proper settlement. Public adjusters and plaintiffs= attorneys believe that Florida laws relating to what MUST be included in a claim exist for a reason: To provide a proper payment to the policyholder, so the he/she may repair his/her home to its pre-loss condition. Florida law, sets the standard for how claims are to be adjusted, but they are always ignored by the insurance companies as if they did not exist. This conduct of fleecing the policyholder by the insurance companies, is tacitly approved (by their total inaction on the issue), by the Florida Department of Insurance. Thus, the Florida Government Department, overseen by on of three members of the Florida Cabinet effectively, is a co-conspirator, with the insurance companies, in defrauding insured policyholders out of their proper indemnity under their policies.The insurance industry, following the McKinsey doctrine, doesn=t care about their policyholder=s losses, or what their policies promise to pay in the event of a covered loss.

Their only interest is to underpay every claim payment to improve profits/surplus at every opportunity, thus retaining as much money as they can from being spent on claims, using illegal or prohibited means to do so.

Homeowner=s Insurance Guide B Florida 2018/19

Homeowner=s Insurance Guide B Florida 2018/19

CHAPTER 13 CITIZENS PROPERTY INSURANCE CORP. PROTECTED BY FLORIDA STATUTES

Citizens Property Insurance Corporation, the second largest homeowners= insurer in Florida, based on the number of policies in force as of December, 2017, is one of the primary, and most aggressive, practitioners of the McKinsey doctrine of Deny, Delay and Defend.The history of Citizens conduct in claims handling practices, every day and on almost every claim, are illegal and in violation of all the Florida statutes relating to unfair claims handling practices to which, in theory, all insurance companies in business in Florida are required to conform, by Florida statutes.The most egregious conduct in the handling of property claims, is that standard of conduct which is referred to in Florida statutes as ABad Faith.@The Florida Legislature passed laws which provided for insured policyholders to sue their insurance company for handling a claim in Bad Faith if their claims handling practices crossed the line. The bar is set high, and although some insurance companies have been sued for bad faith for handling a claim, or claims plural, the incidence of reaching that standard in not great.

Homeowner=s Insurance Guide B Florida 2018/19

Under the Florida statutes, a policyholder must prevail in a breach of contract lawsuit, against his /her insurance company, before the policyholder can sue his insurer for Bad Faith in handling the breach of contract matter. Usually, damages for Bad Faith handling of claims are punitive, sometimes in the extreme, and many of those types of claim involve many plaintiffs , who have formed themselves into a Aclass.@Citizens Property Insurance Corporation is protected from a bad faith suit by a policy holder, by the Florida statute 627.361 (6) which created Citizens PIC in 2002.Under the Statute which created Citizens PIC., Citizens is absolutely protected, and are exempted from any and all law suits for conducting the handling of claim in ABad [email protected] the hysterical flight of the private sector=s major national insurance companies after the hurricanes of 2004 and 2005, which made inroads into their lust for short term profits, Citizens stepped up as Aan insurer of last resort@ to address the resulting very real shortage of capacity in the Florida homeowners= insurance market. However, notwithstanding that they are publicly owned by the Florida Government, Citizens, by its unfair and otherwise illegal claims handling practices, intentionally inflict harm and distress upon its policyholders.

Homeowner=s Insurance Guide B Florida 2018/19

This conduct, by Citizens, which was very same set up to protect and to serve, Florida citizens and residents, is patently unconscionable, and a clear abuse of its protected position.You may ask, since Citizens is a ANot for Profit@ corporation, why does it handle its claims using the McKinsey doctrine? The answer is because they can, with impunityCitizens hides behind its statutory protection, and many time has Acrossed the line@ between outrageous and illegal claims handling practices and encourages employees to short-change it=s policyholders. Perhaps, he Florida Legislature will wake up and correct the disservice they did to the Floridian homeowner. With the widespread daily practice of Citizens acting illegally towards its policyholders (because of the rampant abuse it encourages), this protective language in it=s creating statute law should be repealed as being against the public interest. If this were to occur, Citizens would then be held accountable, just like all it=s competitors in the insurance marketplace.Moreover, although Citizens is a not-for-profit corporation, it=s CEO is responsible for ensuring that the corporation makes a profit, although they don=t call it a profit.

In spite of It=s non-profit status, Citizens uses the practice which was used by Communist businesses behind the Iron and Bamboo Curtains.In all those businesses , which were wholly owned and managed by the state, the managers of those businesses were required to

Homeowner=s Insurance Guide B Florida 2018/19

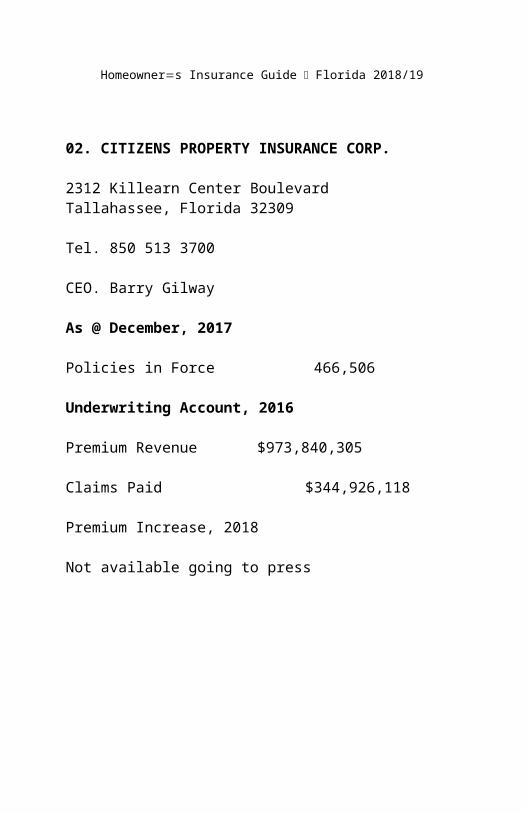

make a SURPLUS. The CEO of Citizens is required to make not a profit, but a surplus.Citizens makes a handsome surplus almost every year, at the cost of its victim policyholders. This is why it=s cash reserves are reportedly, well in excess of their PML (Probable Maximum Loss), for any one year of account, bearing in mind its reinsurance arrangements, and it=s claims handling practicesFor example, for it=s 2016 year of account, Citizens Underwriting Account enjoyed a premium income of $973,840,305 with total claim payments of $344,926,118 resulting in an underwriting surplus of $628,914,187 to run the total administration costs of the business.Yet, this massive surplus does not stop Citizens CEO from asking for almost annual rate (premium) increases.Frankly, while I am not an accountant, I have to record that I have a strong feeling that Aall is not well in the State of Denmark!@

A highly respected firm of Plaintiffs= attorneys in Florida and other states, attempted to sue Citizens, not for Bad Faith but its failure to act in Good Faith in its claims handling practices, which has been a fundamental concept of the theory of insurance for hundreds of years.This legitimate action should have succeeded, but the case was dismissed by the Court.

Homeowner=s Insurance Guide B Florida 2018/19

Someone once said that ACommon sense is not always Acommon!@ Charles Dickins, Mr. Bumble, in Oliver Twist said, AThe Law is a Ass.@ @ Sometimes, how true!

Homeowner=s Insurance Guide B Florida 2018/19

Homeowner=s Insurance Guide B Florida 2018/19

CHAPTER 14ASSIGNMENT OF BENEFITS

This handbook would not be complete without discussion of this issue which has caused a great deal of comment in the press and other media, in the recent past, most notably by the CEO of Citizens Property Insurance Corporation, Barry Gilway, and others at executive levels of other insurance companies.Some of these comments have merit, under their (most usually), particular circumstances.The Assignment of Benefits issue arises often after an insured claimant suffers a serious water damage loss. The policyholder seeks assistance from a water extraction company, and is then persuaded to sign a contract with that contractor, which contract includes an Assignment of Benefits Clause (AOB).This includes most of the nationally franchised business, such as Stanley Steemer, and other of equal status. The contractor tells the claimant policyholder that he will take care of everything with the insurance company, and that he will get paid directly by the insurance company.The policyholder signs the contractor=s Contract, and the contractor does what he needs to do, and submits his bill directly to the insurance company.

Homeowner=s Insurance Guide B Florida 2018/19

Often, or so it is claimed, the first the insurance company knows about the loss is when it is presented with the contractor=s bill. According to the contractor=s contract, the contractor is not required to notify the insurer of the loss. His duty is to his customer, that is to do the work stipulated in the contract. Which he completes to his customer= satisfaction.The insurance company, refuses to pay the contractor=s bill, alleging inflated charges, and the dispute rapidly escalates into a law suit, initiated by the contractor, but using his Customer=s name as the Plaintiff in the law suit, as is his right under the AOB clause of his contract.There are several issues at play here, which bear discussion:The first problem to understand is that there are two conflicting ACONDITIONS@ in a Homeowner=s Policy which lie at the root of this problematic issue. What is a ACONDITION@ in a policy of insurance?A ACONDITION@ in a policy of insurance is a MANDATORY DUTY imposed upon the policyholder by the language of the policy with which he is obliged to comply, to the letter. A study of the policy will reveal that there are a number of CONDITIONS listed in the policy under the title: "YOUR DUTIES AFTER LOSS."

These are therefore duties imposed upon the policyholder to protect the insurance company=s interests.

Homeowner=s Insurance Guide B Florida 2018/19

These duties include:

1. Give us prompt notice of claim to us or our Agent.

2. Protect the property from further damage. If repairs to the property are necessary, you must: a. Make reasonable and necessary repairs to Protect the property, and b. Keep an accurate recorxd of repair expenses

3. As often as we reasonably require: a. Show us the damaged property

Typically, there is a list of definitions at the beginning of a Homeowner=s Policy. Again, typically, the expressions: Aprompt,@ A further damage,@ Areasonable and necessary@ are not defined in the policy definitions. However, the Courts have ruled that, absent any definition of particular wording(s) or expressions in the policy language, the insurer and the insured shall be expected to interpret those wording(s) or expressions

using the ordinary meaning of those phrases as Aunderstood by the ordinary man in the street.@

Homeowner=s Insurance Guide B Florida 2018/19

If the policyholder refuses to comply with a ACONDITION,@ or simply ignores a ACONDITION@ or refuses or omits to comply is ABSOLUTE GROUNDS FOR DENIAL OF COVERAGE FOR THE CLAIM.This right of denial of claim from breach of a Condition has been upheld in the insurance industry=s favor for hundreds of years, and rightly so.However, different cultures have different understanding of these words and phrases, particularly when the written language is printed in a language other that the policyholders= first language.The conflicting duties imposed upon a policyholder are:1. APrompt notice@ effectively means Awithout delay.@What, you ask does Awithout delay@ mean?

If you are Jamaican, for example, without delay could mean within four weeks (Ha Ha). No offence!Jamaica Time!If you are from Brazil, perhaps that language and those expressions mean, AWhen I get around to it!.@

Florida is a state with a very diverse population, and there needs to be some machinery available to the policyholder so that unintentional mistakes can be avoided.

Homeowner=s Insurance Guide B Florida 2018/19

Perhaps policies should be worded differently, so that there is no mistake or misunderstanding, either actual or claimed, or indeed taken advantage of by an unscrupulous individual policyholder ot his/her contractor.Specific time frames are the obvious remedy. For example, the Notification of Loss Condition could be worded: AYou must report an event giving rise to a claim within 48 hours of the discovery of the loss, or your claim may be denied.@

2. Protect the property from further damage. This expression is self-explanatory.

3. Make reasonable and necessary repairs to protect the property. This means that you can do temporary repairs 4. Show us the damaged property.

The insurance company must be given the opportunity to inspect the damaged property before any permanent repairs are carried out.

To put it another way and putting to boot on the other foot: If you have medical insurance coverage and you break a leg, you would object to a surgeon amputating your leg before X-rays were taken, to determine what procedures might be considered before

Homeowner=s Insurance Guide B Florida 2018/19

your leg was amputated. You were not given the opportunity to make a full investigation to determine if you had any other options to amputation. So, in such a case, your rights were not considered, and the insurance companies feel the same way about their rights to see any damage for which they are being asked to pay to restore damaged property to it=s pre-loss condition. To put it another way, a ACondition@ is used as a tool used to force the policyholder to do some things which are reasonably demanded by the insurer. These include:(1) that the insurer be placed on notice of a loss within a reasonable time following the loss; and (2) that the insurer has by right created by a Condition in the policy to investigate and inspect the damaged property, and the extent of that damage, prior to any permanent repairs being carried out.Obviously, if the insurer is denied these rights, it's interests have been prejudiced, and because of this prejudice, the insurer has the right to deny the claim.

Without an investigation and an inspection of the damaged property, the insurer is denied the right to discover, how, when, where, why the loss occurred, the extent of the loss and whether

Homeowner=s Insurance Guide B Florida 2018/19

the loss is covered by the policy, and the value of that loss, and to discover other vital information concerning the lossNo insurer should tolerate a Adone deal@ without an opportunity to investigate the loss.For example: the policyholder would not buy a house sight unseen, and it would be unreasonable to expect him or her to do so.But, this situation presents another problem.There is another CONDITION in the policy which, with respect to the claim described, creates an AMBIGUITY in the language of the policy.Another of the ADUTIES AFTER LOSS@ includes another CONDITION, which requires the policyholder to take necessary steps to arrest and/or stop any further progress of the damage. This is called Amitigating the loss.@ The intention of imposing this duty upon the Insured is to require the policyholder to make temporary repairs to prevent further damage. But the policy does not use the expression Atemporary repairs.@ The contractor argues that in the context of the event giving rise to the claim, the expression "temporary repairs" and "permanent repairs" are often one and the same.

The contractor, in the scenario described above, states that he had to do all the repairs as a permanent repair to comply with this AMITIGATION CONDITION.This entire situation creates a Acan of worms,@, not the least of which is the ambiguity in the policy language and its

Homeowner=s Insurance Guide B Florida 2018/19

interpretation. Florida law states that ambiguities in insurance policy language are always found in favor of the person that did not write the contract. In this case, the policyholder.

FLORIDA SUPREME COURT DECISION

Recently, the Florida Supreme Court addressed the Assignment of Benefits issue. In short, the Court held that the right to assign policy benefits (as distinct from the assignment of the entire policy), to whomever the assignor wishes, has become an established custom and practice, and that the Court was not going to disturb that situation. However, the Supremes said also, that the more appropriate forum to resolve this issue was in the Florida Legislature, and not the Florida Court system.FLORIDA LEGISLATORS - TAKE NOTE!

STOP PRESS

The Florida legislators have just finished another of their annual trips to Tallahassee for the purpose of doing only God knows what, apart from collecting those bulging little brown envelopes

Homeowner=s Insurance Guide B Florida 2018/19

from their favorite lobbyists, containing what are euphemistically described as Acontributions to their re-election campaign fund.@Yet, again, it seems that very little was achieved by our legislators this year. The status quo never seems to change, and 2018 will go down in history as yet another waste of time and money. Status Quo, indeed!

Homeowner=s Insurance Guide B Florida 2018/19

Homeowner=s Insurance Guide B Florida 2018/19

CHAPTER 15 - COMMENT

Addressing the Assignment of Benefits (AOB) is long overdue, and the Florida legislature should do its job and enter into serious discussions to settle the issue. There is merit in the belief that an AAssignment of Benefits,@ clause in a contractor=s contract, per se, albeit an implied right created by custom and practice, is unfair to the insurer.There is a plethora of possible solutions, all of which will require not a small degree of leadership, negotiation and compromise from all sides of the issue.That is where the leaders in the Florida legislature, will show their negotiating skills, their mettle and backbone. To date, we have seen neither leadership, nor any of those skills.The 2018 Legislative cession produced more of the same, lack of leadership and backbones of wool from the legislators, with no real effort made to addresses any meaningful issues. Too busy counting those little brown envelopes to do anything constructive. Another issue relating to the AAssignment of Benefits Clause@ should be mentioned. This clause gives total control of the policyholder=s claim to a person or entity (the contractor), who has only a very limited interest in the outcome.

Homeowner=s Insurance Guide B Florida 2018/19

There may be other issues over which the contractor should not have full control under any circumstances, but strictly according to the language of the AOB, total control means total control.

Homeowner=s Insurance Guide B Florida 2018/19

CHAPTER 16THE OPTION TO REPAIR

The AOption to Repair@ is now appearing in Florida Homeowners policies, more and more, most notably in policies issued by People=s Trust Insurance Company of Deerfield Beach, Florida who are now suing some of their policyholders.These policyholders are fighting the language of their policies, because they object to handing over to their insurance company complete and total control of their claim for whatever repairs are necessary following a covered loss.People=s Trust is suing it=s policyholders because the Option to Repair is written into their policies as a CONDITION with which the policyholder is obliged to comply, under the threat of a denial of coverage.However, there is an AOpt Out@ provision in the Application for Insurance with People=s Trust. But how many prospective policyholders understand this option?It must be understood that the Option to Repair Condition in People=s Trust=s policy is already part of the language of their standard policy.

Homeowner=s Insurance Guide B Florida 2018/19

It is not an option per se. It is a Condition which the policyholder must be pro-active in AOpting Out@ at the time of application for the insurance.As stated earlier, Florida courts have held, and reaffirmed, that a violation of a CONDITION in a policy is valid grounds for a denial of coverage for that claim.This issue is also one that the Florida Legislature must address with urgency.However. There is another vital issue which is of paramount importance.And, it should be understood that this issue is very similar to the position which exists in the Assignment of Benefits practice, but in reverse. In the Assignment of Benefits issue, the contractor has total control over the insured policyholder=s claim.In the Right to Repair issue, the Insurer has total control over the insured policyholder=s claim: the repairs to be carried out, the materials to be used, and by labor of their choice, not the homeowner=s choice. Also, in the Right to Repair issue, the insurer has not only the sole rights to the policyholder's claim, but also has total control over the scope of repairs.People's Trust's quasi-ownership and control over its Rapid Response Team (affiliated contractors) will most assuredly be reduced to minimal repairs, and in monetary value, probably not more than the cost of the policy

Homeowner=s Insurance Guide B Florida 2018/19

Deductible, which People's Trust demands be paid to them, by the Insured, up front.There have already been rumors of very shoddy materials and workmanship by People's Trust's Rapid Response Team, including painting over mold with KIlz, after treatment with bleach. Shoddy in spades!!However, this is what I believe to be of utmost and paramount importance:Ownership and control of their Rapid Response Team is demonstrated by the familial relationship between the owners of People's Trust and the owners of the Rapid Response Team. The Right to Repair Condition in any insurance policy, is a clear MASSIVE, CONFLICT OF INTEREST, as between the parties to the contract of insurance (the policyholder and the insurer). This conflict, equally clearly, is not in the public interest. People's Trust has an additional contributing conflict of interest by its claimed "arms length" ownership and control of it's RAPID RESPONSE TEAM, Rapid Response Team has the same registered address in public records, and directorships are intertwined between the family members and/or owners of both companies.Because any conflict of interest is clearly not in the public interest, and most particularly in circumstances in

Homeowner=s Insurance Guide B Florida 2018/19

which an unscrupulous person or entity can take advantage of an individual, especially when that person or entity has made a clear promise to protect and indemnify that other party in the event of stated circumstances, such a conflicting Condition in the policy should be declared null and void by the Florida Legislature, and/or Florida Courts, and should be expunged from the policy language.It is hoped that the law suits filed by People's Trust, against its policyholders, will be dismissed by the Courts, on the grounds that the Condition creates Conflict of Interest and is thus, an illegal and unenforceable CONDITION. In its position of insurer and adjuster, under the Right to Repair Condition, acting in their position as Aadjuster,@ either Peoples Trust ot Rapid Response Team may be in violation Florida Statute, FS 626.878 which prohibits adjusters acting in a Conflict of Interest position.Moreover, this conflict of interest is clearly unconstitutional, as being a clear violation of the Equal Protection Clause, or language of the Constitutions of both Florida and the United States.Recently, a spokesman for People's Trust stated that the company was not interested in providing insurance to any person or entity that wished to opt out of the "Right to Repair" Condition in their policy.The answer is obvious, in the light and reality of this statement.

If you don=t like the idea that in the event of a loss, you have to turn over all your rights to repair your property as you see fit,

Homeowner=s Insurance Guide B Florida 2018/19

using contractors materials and workmanship of your choice, not the insurance company=s choice. Cancel your application, and if you already have a policy, cancel it and go somewhere else where you are not surrendering all you rights to a claim to the likes of People=s Trust.If enough policies are canceled, they will soon be on the way out of town voluntarily.

Homeowner=s Insurance Guide B Florida 2018/19

Homeowner=s Insurance Guide B Florida 2018/19

CHAPTER 17SUMMARY OF DENY, DELAY & DEFEND

The mind set of executives managing insurance companies today has changed since our parents= day.Today, those individuals are quite simply opportunists, and by their own actions, demonstrably are persons without either ethics or integrity. Their only purpose is to use their insurance companies as a tool by which to separate their policyholders from their hard earned money, and to keep as much of it as they can by obfuscating on claims by extreme means, by massively under paying its customers without any fear of retribution from official regulators.Many of the major players in the rookie homeowners insurance companies are unscrupulous carpetbaggers who had never been in the insurance business until the wholesale flight of the established insurance companies from Florida, after the hurricanes of 2004 and 2005, opened up an opportunity for them to join the bandwagon.Essentially, they realized that the insurance laws in Florida were weak, and its legislators not only weak but easily manipulated.

Homeowner=s Insurance Guide B Florida 2018/19

They took advantage of that situation and ran hot foot to Tallahassee to form their cardboard insurance companies. Quickly, they realized that they were sitting on a gold mine. They took to McKinsey=s doctrine of Deny, Delay and Defend like ducks to water, and the Florida authorities and Legislators drank their version of Kool Aid like drunken sailors.The result is a plethora of unscrupulous insurance companies, most of which will probably disappear after the next really destructive hurricane that comes Florida=s way, having perhaps far exceeded by far their PML (Probable Maximum Loss).Many of these rookie insurance companies are reminiscent of a flaky, but highly successful institutions running a poorly disguised PONZI SCHEME in a clown=s costume.It=s never about the policy. They are interested only in the amount of money they can avoid paying on every claim.This is chicanery at its worst!

Homeowner=s Insurance Guide B Florida 2018/19

Because insurers= attitude to claims has changed, so also must policyholders= attitudes change, to level the playing field.That is why there are more public adjusters in the claims business in Florida today. Most of them used to work for insurance companies, when those companies were managed by managers from the old school. But, when DENY, DELAY AND DEFEND was born, they found that they could not be employed by and owe allegiance to any part of any organization that pays its employees to misrepresent their coverage to policyholders, and to deny the policyholder his/her promised recovery of claim proceeds, by underpaying claims, which conduct they considered to be not only distasteful but also dishonest.While celebrating the growth of profits beyond their wildest dreams, insurance company CEOs, when talking to the media, usually whine about the higher costs of handling claims, alleging inflated invoices and attorneys= fees connected with some losses caused by the less attractive perils which they insure.The unspoken truth is that the escalation of some claims= costs and legal fees are being incurred, necessarily to collect accurate and legitimate payments due to an insured, and are the DELIBERATE, INTENTIONAL AND DIRECT CONSEQUENCES OF THEIR ADOPTION OF THE McKINSEY CLAIMS HANDLING DOCTRINE AND PRACTICES.

Homeowner=s Insurance Guide B Florida 2018/19

Those CEOs and Boards of Directors, made a conscious decision to adopt the McKinsey doctrine, but when following those practices, they whine, ad infinitum, about the costs of using that system, when their profits are diluted.However, their policyholders have no duty or obligation to Abail them out@ through increased premiums, after carrier managements have made unwise, dishonest and perhaps illegal business decisions, resulting in allegedly increased claims costs.Perhaps there should be, in American citizens= interests, a Federal, Congressional Inquiry into insurance companies= claims handling practices, nationwide. The insurance industry is the only industry, certainly in the United States, where the it=s customers can be openly and flagrantly fleeced with impunity, without any fear of accountability to official regulators or any meaningful consequences whatsoever. If stockbrokers, for example, ignored the regulations and laws governing the conduct of their professional practices, their regulators at the Securities and Exchange Commission would take swift action, with fines and criminal charges, often resulting in prison sentences; and moreover, banishment for life from practicing their profession ever again.

The major concept behind the use of the McKinsey doctrine is that the vast majority of claimants will accept the pittance

Homeowner=s Insurance Guide B Florida 2018/19

offerings of their insurance companies, because they believe that they have no alternative than to accept what they are offered, or file a law suit. In the recent past, the majority of policyholders who file a claim had no knowledge of the options open to them to fight their insurance company, for a proper recovery.They don=t realize that there are alternatives. This Guide seeks to address that misconception.Now, perhaps homeowners will realize that they have another alternative to being the victims of shorted settlements, and another way than to just give up and accept what they are offered.Florida=s homeowners, and not the insurance companies, are now holding the ball.Make good use of this opportunity.

Homeowner=s Insurance Guide B Florida 2018/19

Homeowner=s Insurance Guide B Florida 2018/19

CHAPTER 18TEN REASONS TO CALL A PUBLIC ADJUSTER BEFORE YOU CALL YOUR INSURANCE COMPANY

1. Your public adjuster should attend at the damaged property before he files a claim on your behalf with the insurance company.

2. This is important, because the public adjuster will findall the damage to the property, but just the damage visible to the naked eye.

3. Having inspected the damaged property, your public adjuster will file the claim on your behalf with the insurance company so that he is in control of your claim from the beginning.

4. Your public adjuster will contact the insurance company=s field adjuster, and in liaison with you, the polictholder, he or she will make an appointment for a joint inspection at the damaged property.

5. At that joint inspection, your public adjuster will point out all the damage, including all the hidden damage, which needs to be included in the field adjuster=s estimate of repair costs.

Homeowner=s Insurance Guide B Florida 2018/19

6. You may be asked by the field adjuster to give a recorded statement during that first visit.

7. FAPIA attorneys advise against being pressured into give a recorded statement without attorney representation, either in person, or present electronically by telephone.

Insurance company=s field adjusters are trained toask loaded questions and an attorney can protect

you against those types of questions.

8, FAPIA attorneys recommend that the policyholder should inform the field adjuster that you are will to give a recorded statement, but only if you are represented by counsel to safguard your position.

9. Your public adjuster will protect your interests throughout the claims process, and he will make sure that you do not innocently and unknowingly place you claim in jeopardy.

10. Your public adjuster will answer all your questions and will make the progress of the claim settlement as rapid as possible.

The policyholder should bear in mind the following:Insurance company adjusters are not your friends.

Homeowner=s Insurance Guide B Florida 2018/19

Their job is to make your experience throughout the progress of your claim as difficult as possible. Your public adjuster can take much of this Aflack@ off your back.The Good Hands people are not your friends.Insurance company adjusters are not your friendly neighbors, in spite of what they profess.Remember this. They don=t want to pay you any money at all. If they can close your claim file without making a payment, that=s a bonus day for them.Your FAPIA member public adjuster is on your side, exclusively.He will do everything in his power to see that you receive a settlement which is fair, reasonable and in accordance with the language of your insurance policy, and in compliance with Florida Statute Law, Case Law of the DOI Regulations.

Homeowner=s Insurance Guide B Florida 2018/19

Homeowner=s Insurance Guide B Florida 2018/19

CHAPTER 19 PUBLIC ADJUSTER=S COMMENT

After the conclusion of a Deposition by a deservedly respected defense attorney, retained by Citizens on a very small water damage loss, now in its seventh year of litigation, (the policyholder has now passed away), and with the third defense firm of attorneys representing Citizens, we were talking about claims and the current claims handling practices now endemic throughout the insurance industry.I mentioned, with my tongue firmly in my cheek, that I did not understand Citizens= business plan. I said to him that we always win on the claims we handle, which Citizens fight very aggressively. But in the end we still win, and achieve the settlement we are looking for, and Citizens pays enormous legal bills, about which they complain, ad infinitum.My friend, the opposing counsel said AIt=s a very good business plan, because only one claim in six or seven hundred goes to a public adjuster. The rest,@ he said, Asettle for the amount their insurance company offers, or just walk away from their claim, because they don=t know what else to do.@

Homeowner=s Insurance Guide B Florida 2018/19

The Florida Department of Insurance obviously needs to employ better actuaries and/or forensic accountants, because the present crew are obviously being taken for a ride by the insurance companies.Florida is fast getting to the stage when homeowners= insurance premiums are more than a mortgage payment.Moreover, the Insurance Department needs to be much more aggressive in its actions against the extreme companies it is supposed to oversee and regulate, and start protecting the public. To level the playing field, when you have a claim, call a public adjuster first. Get him/her involved from the beginning. The policyholder has nothing to lose by so doing, but has everything to gain.

Visit out Blog atwww.FLHOGuide.com

CHAPTER 20

Homeowner=s Insurance Guide B Florida 2018/19

THE TEN BEST INSURANCE COMPANIESWHEN YOU HAVE A CLAIM

1. FLORIDA FAMILY INSURANCE CO.

2. ST. JOHN'S INSURANCE COMPANY

3. UNITED SERVICES INSURANCE (USAA)

4. UNITED PROPERTY & CASUALTY INSURANCE

5. TOWER HILL COMPANIES

6. CYPRESS P & C INSURANCE CO.

7. GEO VERA SPECIALTY INSURANCE CO

8. ANCHOR P & C INSURANCE CO.

9. AMICA INSURANCE

10. SAWGRASS MUTUAL INSURANCE CO.

Homeowner=s Insurance Guide B Florida 2018/19

Homeowner=s Insurance Guide B Florida 2018/19

CHAPTER 21THE TEN WORST INSURANCE COMPANIESWHEN YOU HAVE A CLAIM

1. PEOPLE'S TRUST INSURANCE

2. UNIVERSAL P & C INSURANCE CO.

3. QBE INSURANCE

4. CITIZENS PROPERTY INSURANCE CORP.

5. NATIONWIDE INSURANCE

6. STATE FARM COMPANIES

7. ALLSTATE Companies

8. LIBERTY MUTUAL INSURANCE

9. HERITAGE P & C INSURANCE CO.

10. FIRST PROTECTIVE INSURANCE CO.

Homeowner=s Insurance Guide B Florida 2018/19

Homeowner=s Insurance Guide B Florida 2018/19

CHAPTER 22FLORIDA HOMEOWNERSBILL OF RIGHTS

Florida Homeowners have the right to:

1. Receive from your insurance company an acknowledgment of your reported claim within fourteen days from the date the loss was reported to them.

2. Upon written request, receive from your insurance company within 30 days after you have submitted a complete Sworn Statement in Proof of Loss to your insurance company, confirmation that your claim is covered in full, partially covered or denied, or receive a written statement that your claim is being investigated.

3. Within ninety (90) days, subject to any dual interest noted in the policy, receive full settlement payment for your claim or payment of the undisputed portion of your claim, or your insurance company's denial of your claim.

Homeowner=s Insurance Guide B Florida 2018/19

4. Free mediation of your disputed claim by the Florida Department of Financial Services Division of Consumer Services, under most circumstances and subject to certain restrictions.

5. Neutral evaluation of your disputed claim, if your claim is for damage caused by a sinkhole and is covered by your policy.

6 Contact the Florida Department of Financial Services' toll free help line for assistance with any insurance claim or questions pertaining to the handling of your claim.

You can contact the FLDFS Consumer Services Help line by phone at 1 877 693 5236, or you can seek assistance on line at the Florida Department of Financial Services Division of Consumer Services website at:

http://apps.fldfs.com/SERVICE/Default.aspx

Homeowner=s Insurance Guide B Florida 2018/19

CHAPTER 23FLORIDA HOMEOWNERSBILL OF RIGHTSFlorida Homeowners are advised to:

1. Contact your retained Licensed and Bonded Public Adjuster, or your insurance company, before entering into any contract for repairs to confirm any managed repair policy provisions, or optional preferred vendors or contractors.

2. Make and document all emergency repairs that are necessary to prevent further damage. Keep the damaged property, if feasible; keep all receipts for emergency work done, and take photographs both before and after any repairs are done. Your Public Adjuster and/or your insurance company will need this documentation to support your claim.

3. Read any and every contract you are asked to sign very carefully to see if you are required to pay any out-of-pocket expenses, or a fee that is based on a percentage of the insurance proceeds that you will receive for repairing or replacing your damaged property.

4. Confirm that every contractor, or sub-contractor, you may choose to hire, is licensed in the state of Florida. You can verify

Homeowner=s Insurance Guide B Florida 2018/19

contractors licenses and check to see if there are any complaints filed against him, or her, by calling the Florida Department of Business and Professional Regulation at: 1 850 487 1395 or online at www.myfloridalicnese.com

5 Require all contractors to provide proof of Insurance before starting any repairs.

6. Take precautions if the damage requires you to leave your home, including securing your property and turning off your gas, water, electricity, and contacting your insurance company and provide a phone number where you can be contacted.

Homeowner=s Insurance Guide B Florida 2018/19

Chapter 24HURRICANE PREPAREDNESSAND CHECKLIST

Whether or not you are faced with having to evacuate from your home, it is important that you have the basics available to see you through seven days without power, or perhaps worse. The basic essentials are:

0 Non-Perishable food0 Bottled Water (3 cases per person) 0 First Aid - including prescription meds0 Personal hygiene items and sanitation items0 Flashlights - and extra batteries0 Battery operated radio/TV, plus extra batteries0 Waterproof container for cash and documents0 Manual can opener0 Lighter or matches0 Books, magazines & games for recreation0 Baby & pet supplies, food, medications etc.0 Cooler for ice0 Propane stove and spare cans of propane gas0 A plan for emergency evacuation0 Location of nearest emergency shelter forfamily, including pets0 Meeting place in case family is separated0 Cell phone - plus charging device/spare battery

Homeowner=s Insurance Guide B Florida 2018/19

0 iPad/Tablet - plus charging cable

Homeowner=s Insurance Guide B Florida 2018/19

Homeowner=s Insurance Guide B Florida 2018/19

CHAPTER 25ATLANTIC HURRICANE NAMES - 2018

NAME DATES CAT REMARKS

1 ALBERTO

2 BERYL

3 CHRIS

4 DEBBY

5 ERNESTO

6 GORDON

7 HELENE

8 ISAAC

9 JOYCE

10

KIRK

1 LESLIE

Homeowner=s Insurance Guide B Florida 2018/19

1

12

MICHAEL

13

NADINE

14

OSCAR

15

PATTY

16

RAFAEL

17

SARA

18

TROY

19

VALERIE

20

WILLIAM

Homeowner=s Insurance Guide B Florida 2018/19

Homeowner=s Insurance Guide B Florida 2018/19

ATLANTIC HURRICANE NAMES2018 - (Continued)

NAMEDATES CAT REMARKS

21

22

23

24

25

26

27

28

29

30

Homeowner=s Insurance Guide B Florida 2018/19

Homeowner=s Insurance Guide B Florida 2018/19

Homeowner=s Insurance Guide B Florida 2018/19

NOTES

Homeowner=s Insurance Guide B Florida 2018/19

Homeowner=s Insurance Guide B Florida 2018/19

CHAPTER 26UNDISPUTED FUNDS

When you file a property claim on your insured dwelling, during the process of adjusting your loss your insurance company may send you a check for the amount they are offering to you to settle your claim.However, you may believe that the amount of their offer is insufficient to enable you to do all the repairs that are necessary to restore your property to it's pre-loss condition.At this stage, you believe you may have a dilemma.If you cash the check, does this preclude you from pursuing your claim further, to try to get an additional payment so that you have sufficient funds to do all the repairs necessary?The simple answer to this question is: No. In simple terms this payment is called "undisputed funds" and cashing the check does not mean that you cannot pursue your claim further. It is true, in general terms, that the acceptance of and cashing a check sent to you, for example, on a "slip & fall" claim, then that payment will be regarded as a "confession of judgement," and after you deposit that check in your bank account, you will not be able to pursue your claim any further.

It is true, in general terms, that the acceptance of and cashing a check sent to you, for example, on a "slip & fall" claim, then that payment will be regarded as a "confession of judgement," and

Homeowner=s Insurance Guide B Florida 2018/19