Embed Size (px)

Citation preview

m k.

>^^\ United States ' ° 'I Department of

■.f Agriculture

Foreign Agricultural Service

Forest Products Division

Agriculture Handbook No. 662

Revised §'^ July 199(1 4;..:

A Guide to Exporting Solid Wood Products

P if I

Jl

!llm IVE

: i: i.:

iiSrClStíSiE

,-*!,• r .4 "■tí ^-ï. -»^»Jdft.

.♦í.í'í i*.ïi_

Sîti !■:

■Ni?:'

Krft ; ■;■: !*

^% "—

■Hi.-^-i

.Ttr T:C loi^-'i' ■1,1 ■

Abstract

This handbook provides a guide for U.S. wood products producers to develop a successful export marketing strategy. It covers how to obtain accurate and up-to-date export marketing information so that the production, scheduling, and shipping of U.S. wood products can be done profitably.

Keywords: Wood products, export markets, exporting, marketing information, export financing, shipper's export declaration, shipping documentation, business organization, market development cooperators, trade servicing.

Acknowledgments

This is the first revision of the handbook originally published in 1986 by William G. Westman, who specifically acknowledged work done by David R. Schumann and Ralph T. Monahan, USDA Forest Service in The Lumberman's Guide to Exporting.

Portions of this revised publication draw on work done by the USDA's Office of Trans- portation and its publication, Export Handbook for U.S. Agricultural Products. Thanks also go to the state and federal agencies, cooperators, and others mentioned in this publication who provided information and assistance.

The material in this publication was prepared solely for the purpose of assisting U.S. firms interested in exporting U.S. solid wood products. References to private publica- tions and firms do not imply endorsement by the Foreign Agricultural Service or the U.S. Department of Agriculture.

:|^ United States })) Department of

Agriculture

Foreign Agricultural Service

Forest Products Division

Agriculture Handbook No. 662

Revised July 1990

A Guide to Exporting Soiid Wood Products By Cynthia Evans Agricultural Economist

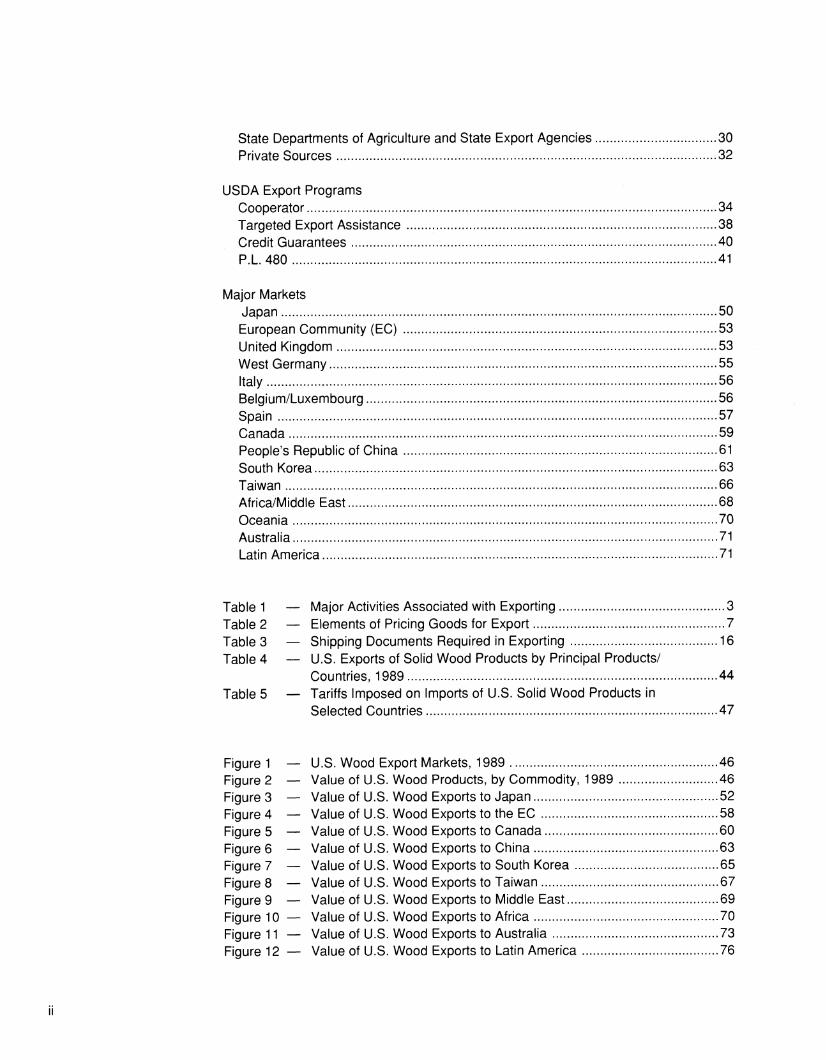

Contents

Page

Introduction

Exporting Wood Products ^ Trade Servicing 5

Supply Considerations 6

Pricing Products for Export 6

Financing Exports Payment Options for Export Shipments 8 Letters of Credit and Invoices 9 Foreign Credit Insurance Association (FCIA) 10 Export-Import Bank (Eximbank) of the United States 11 Overseas Private Investment Corporation (OPIC) 11 Small Business Administration (SBA) 11 U.S. Trade and Development Program (TDP) 12 Trade Finance Corporation/American International Group (TRAFCO) 12

Export Shipping Carriers 14 Terminals 15 Packaging and Shipping 15 Export Documentation 15 Shipper Export Declarations (SED's) 17 Exporting Checklist 20

Business Organization "In House" 22 Export Management Companies (EMC's or agents) 22 Export Trading Companies (ETC's) 22 Export Merchants (EM's) 22 Foreign Sales Corporation (FSC) 23

Export Market Information and Assistance United States Government

U.S. Department of Agriculture 25 Foreign Agricultural Service 25

Overseas Offices 25 Market Reports 25 Export Services 26

Office of Transportation 27 Animal and Plant Health Inspection Service 27 Forest Service 28

U.S. Agency for International Development 29 U.S. Department of Commerce 29 Office of the United States Trade Representative 30

State Departments of Agriculture and State Export Agencies 30 Private Sources 32

USDA Export Programs Cooperator 34 Targeted Export Assistance 38 Credit Guarantees 40 P.L 480 41

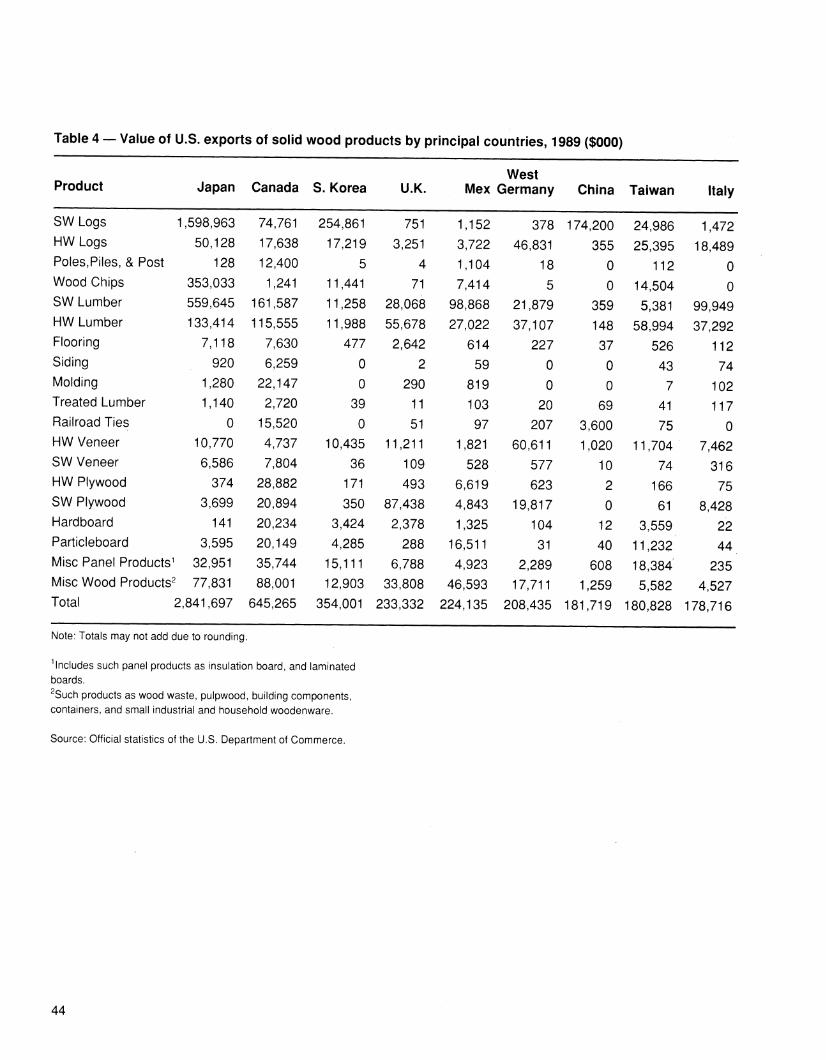

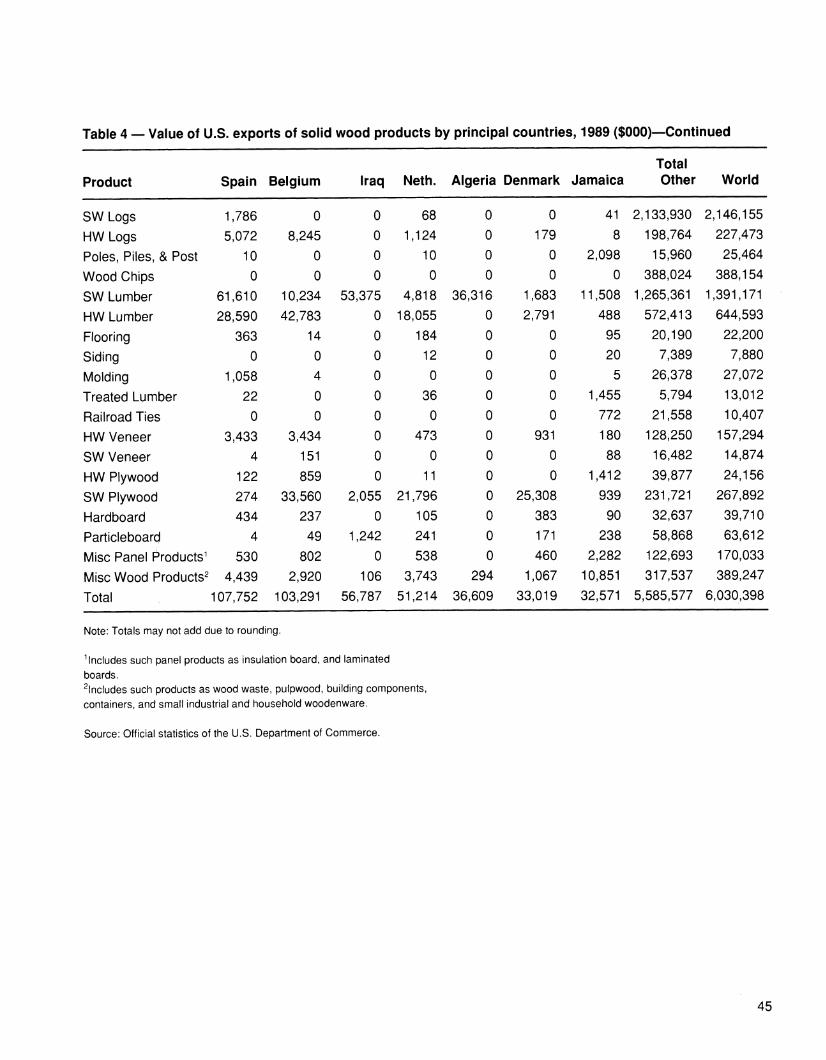

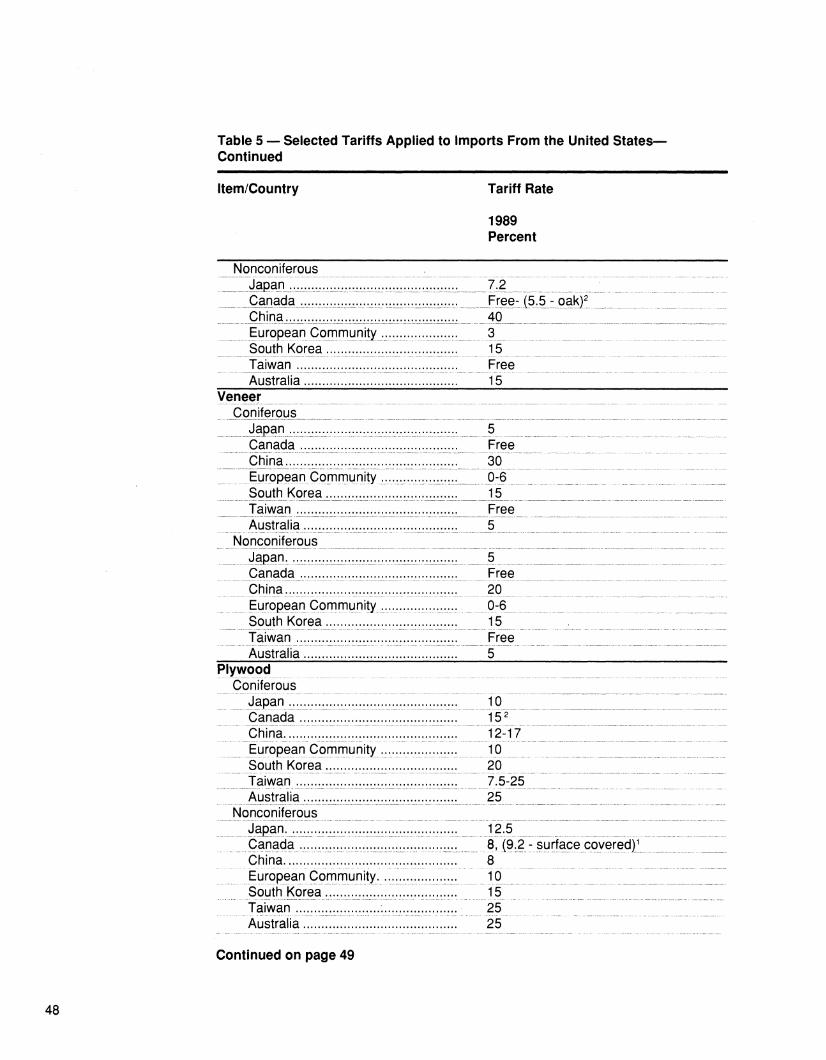

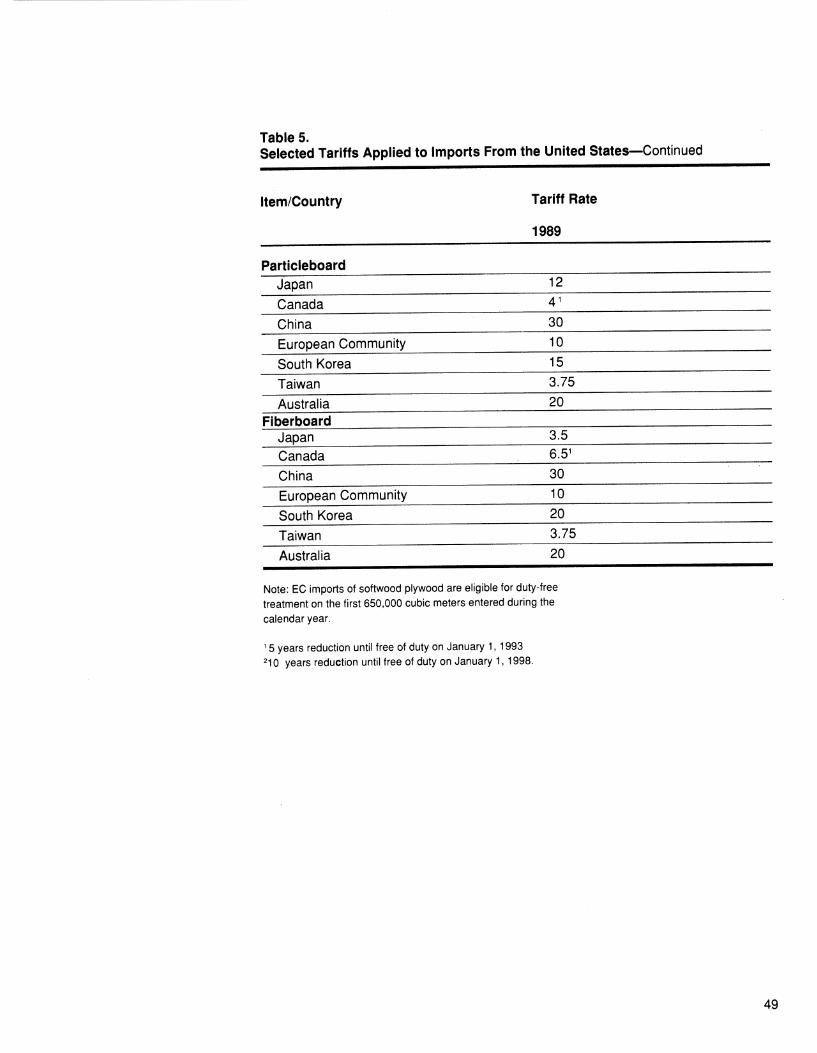

Major Markets Japan 50 European Community (EC) 53 United Kingdom 53 West Germany 55 Italy 56 Belgium/Luxembourg 56 Spain 57 Canada 59 People's Republic of China 61 South Korea 63 Taiwan 66 Africa/Middle East 68 Oceania 70 Australia 71 Latin America 71

Table 1 — Major Activities Associated with Exporting 3 Table 2 — Elements of Pricing Goods for Export 7 Table 3 — Shipping Documents Required in Exporting 16 Table 4 — U.S. Exports of Solid Wood Products by Principal Products/

Countries, 1989 44 Table 5 — Tariffs Imposed on Imports of U.S. Solid Wood Products in

Selected Countries 47

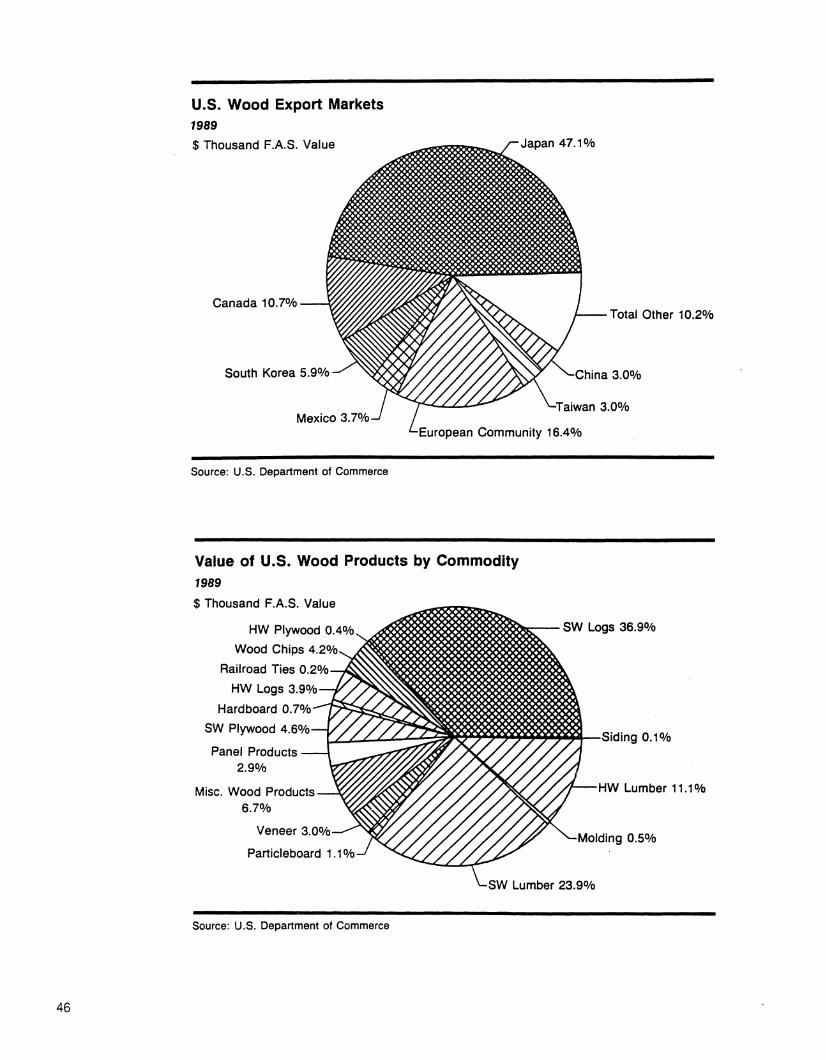

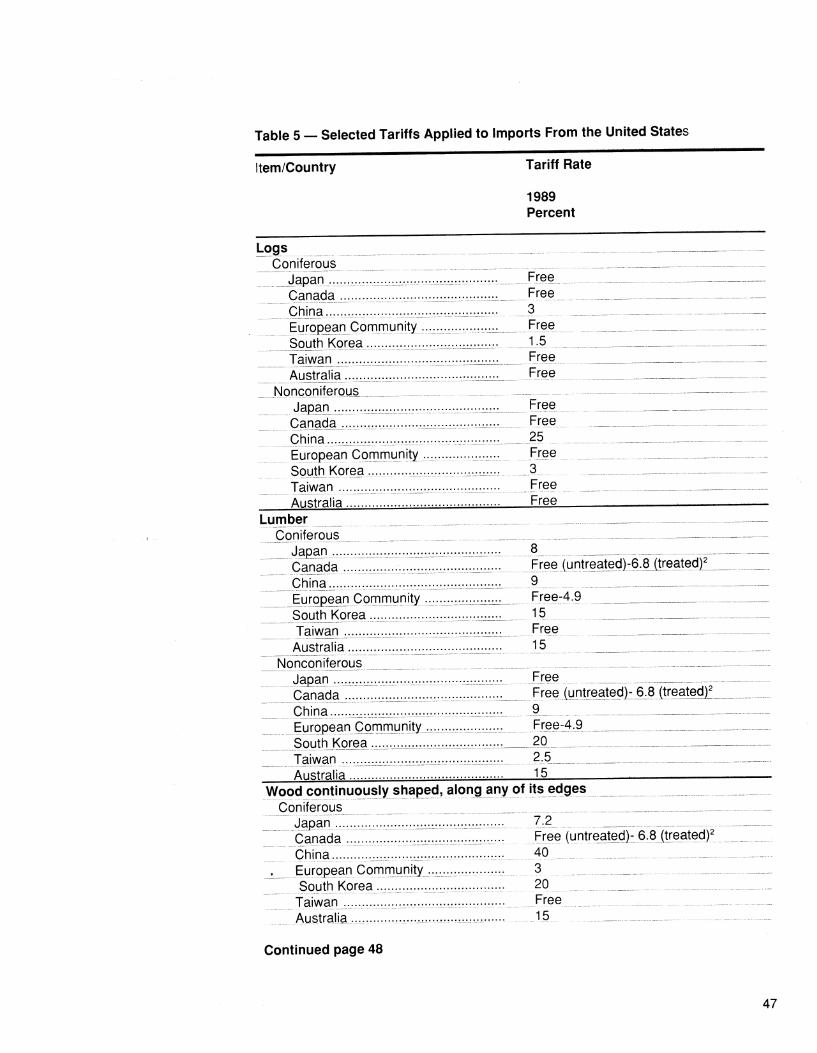

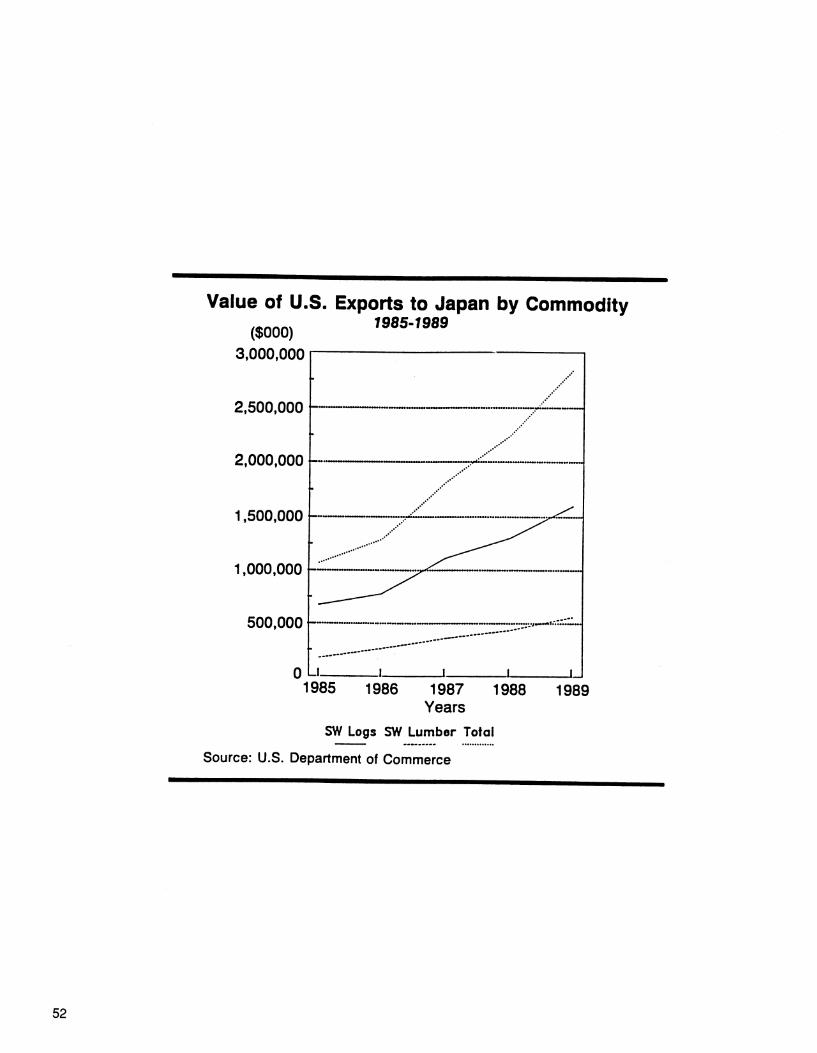

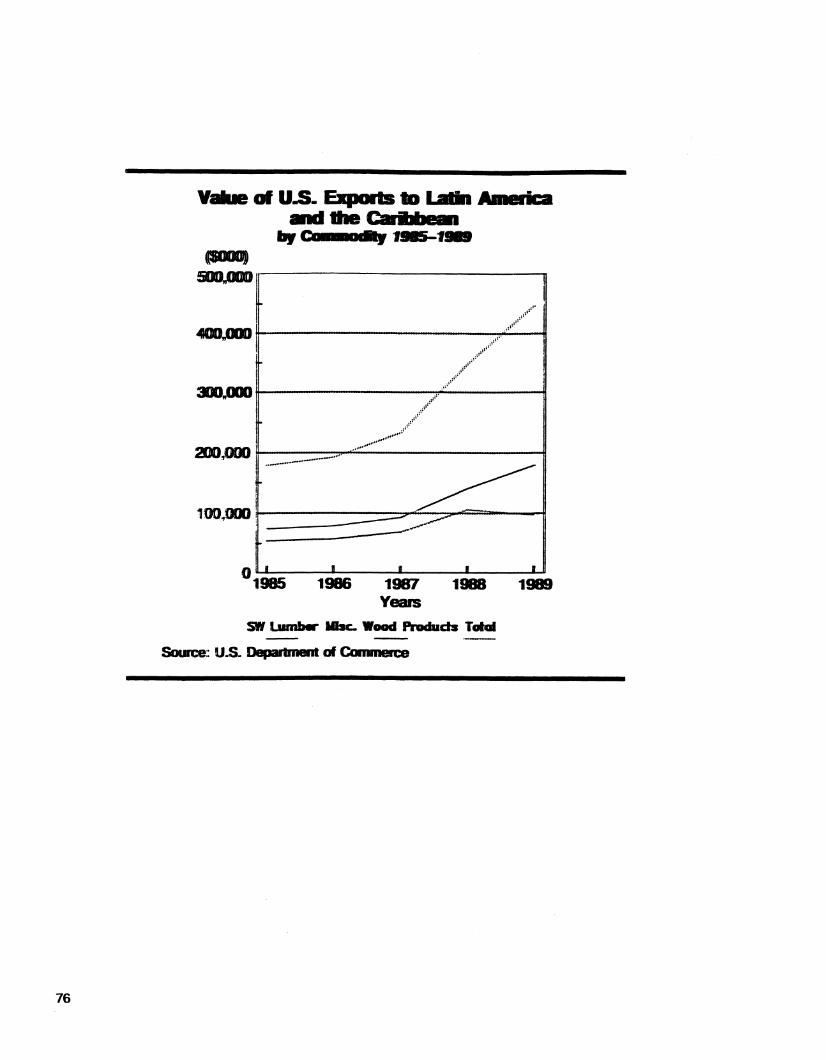

Figure 1 — U.S. Wood Export Markets, 1989 46 Figure 2 — Value of U.S. Wood Products, by Commodity, 1989 46 Figure 3 — Value of U.S. Wood Exports to Japan 52 Figure 4 — Value of U.S. Wood Exports to the EC 58 Figure 5 — Value of U.S. Wood Exports to Canada 60 Figure 6 — Value of U.S. Wood Exports to China 63 Figure 7 — Value of U.S. Wood Exports to South Korea 65 Figure 8 — Value of U.S. Wood Exports to Taiwan 67 Figure 9 — Value of U.S. Wood Exports to Middle East 69 Figure 10 — Value of U.S. Wood Exports to Africa 70 Figure 11 — Value of U.S. Wood Exports to Australia 73 Figure 12 — Value of U.S. Wood Exports to Latin America 76

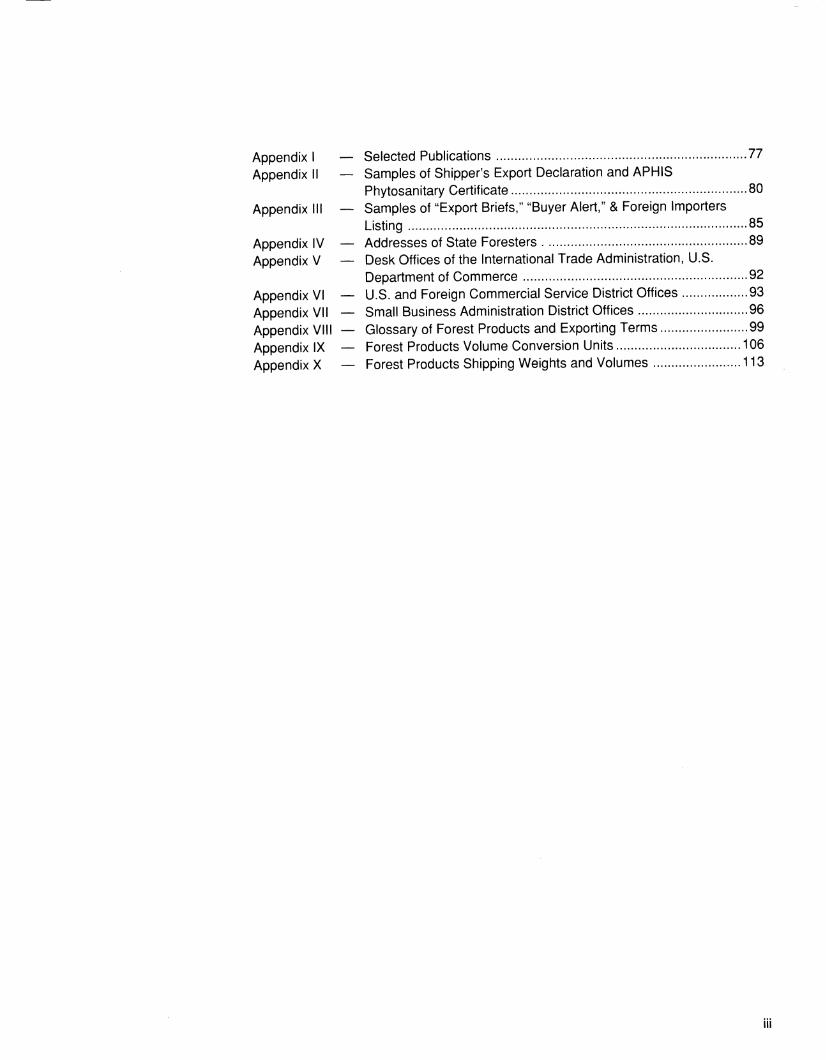

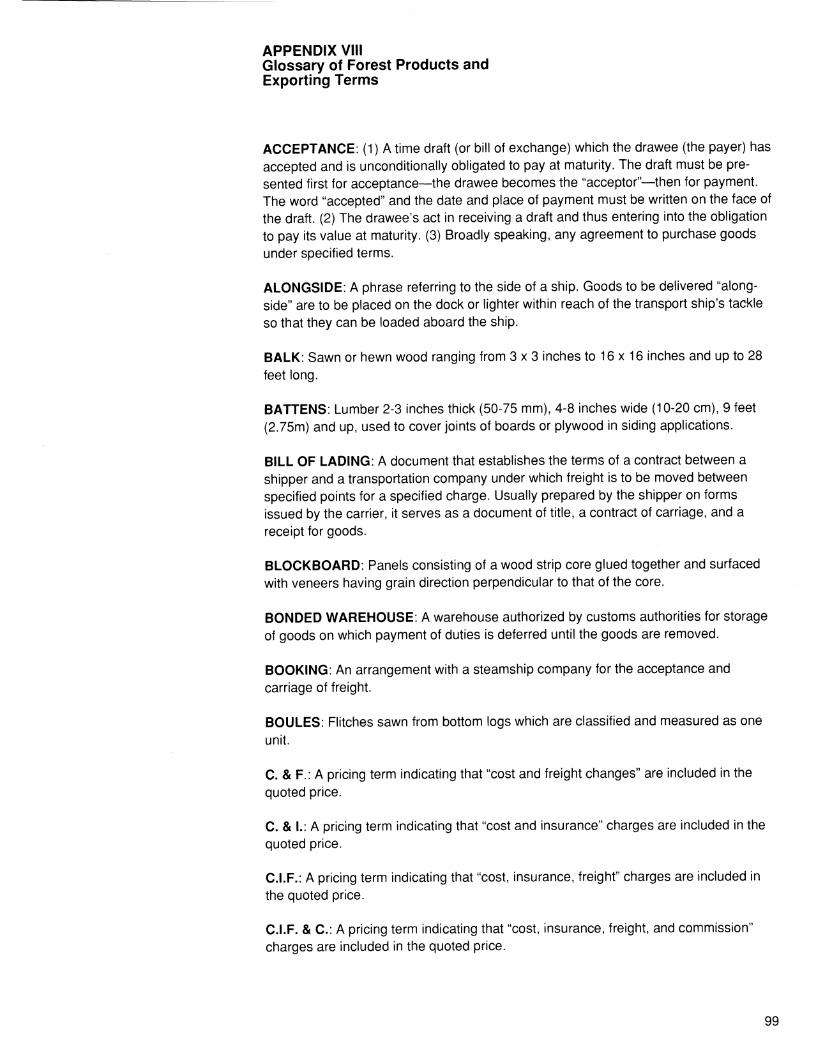

Selected Publications 77 Samples of Shipper's Export Declaration and APHIS Phytosanitary Certificate 80

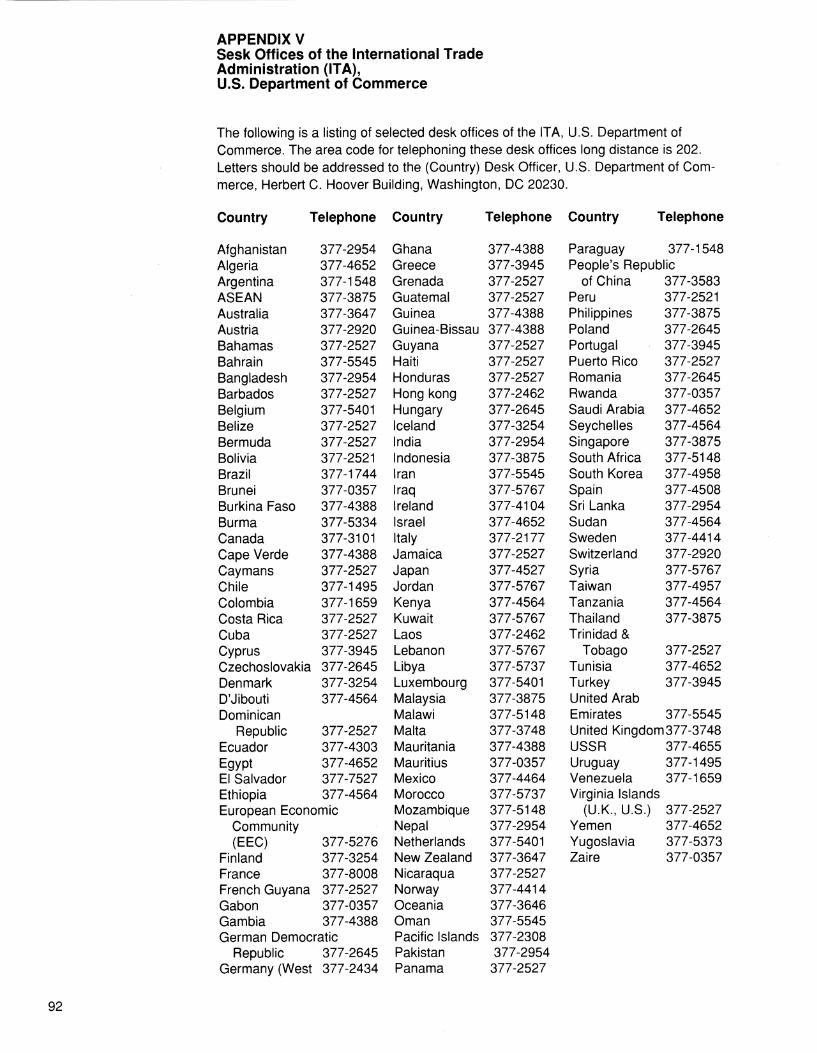

Appendix III — Samples of "Export Briefs," "Buyer Alert," & Foreign Importers Listing 85 Addresses of State Foresters 89 Desk Offices of the International Trade Administration, U.S. Department of Commerce 92

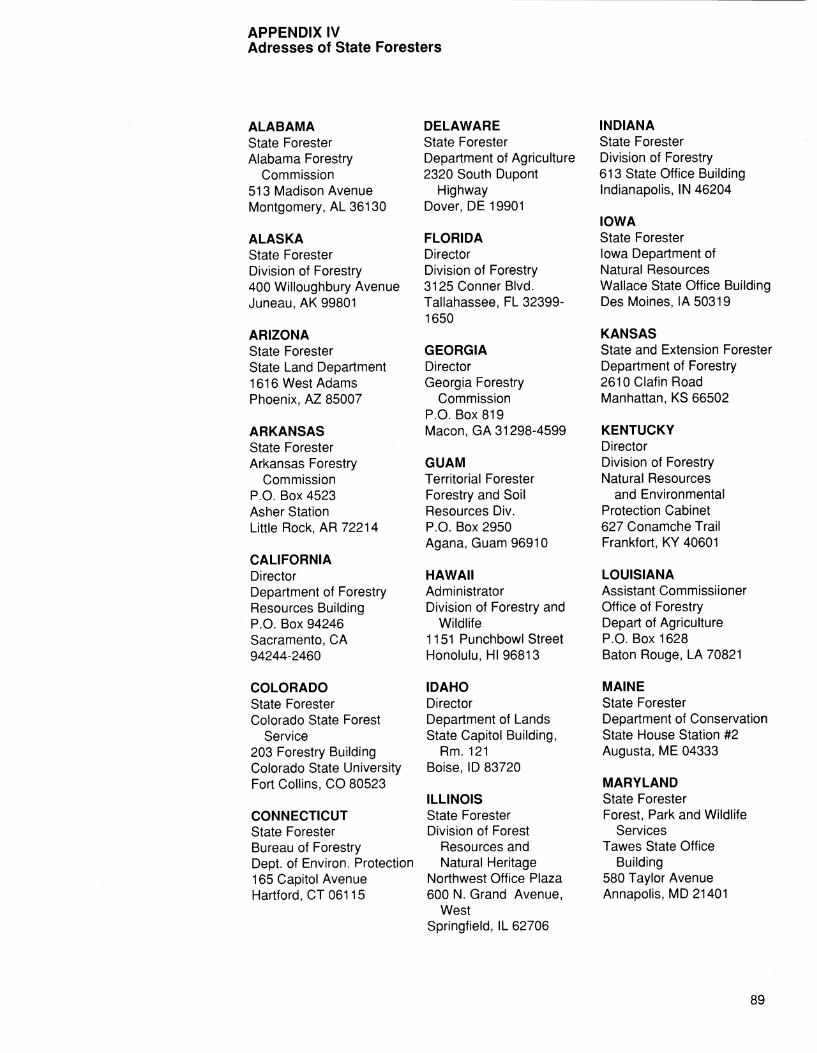

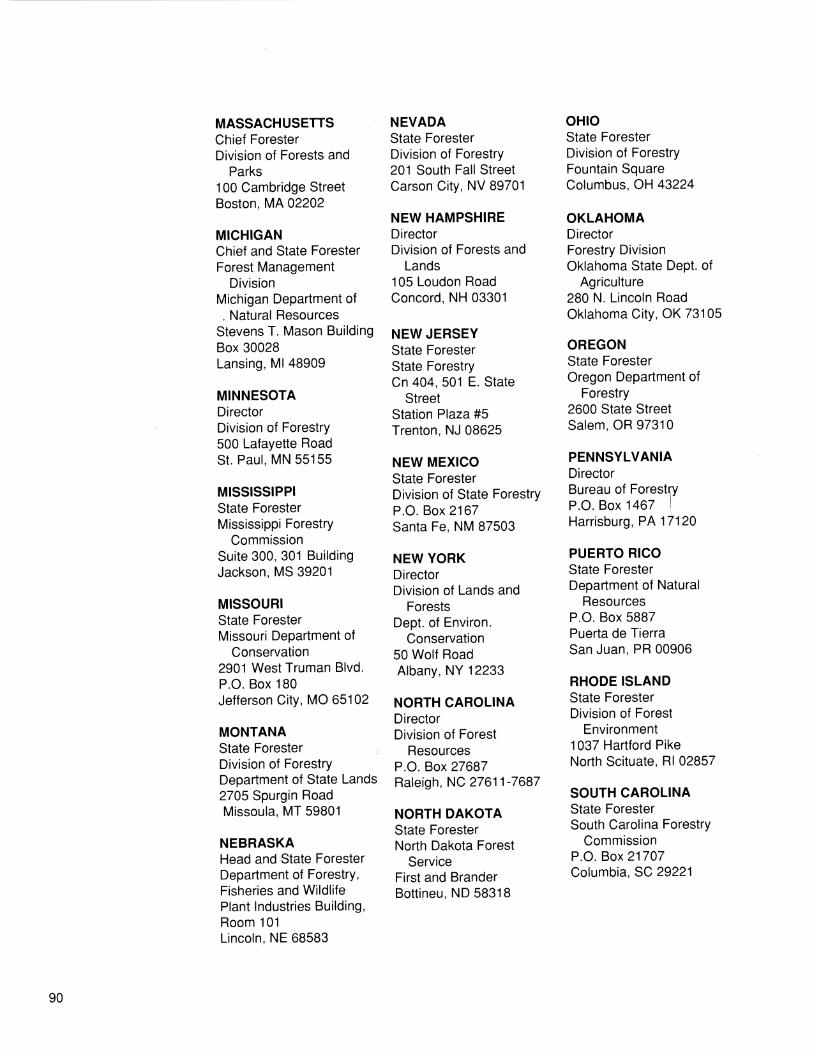

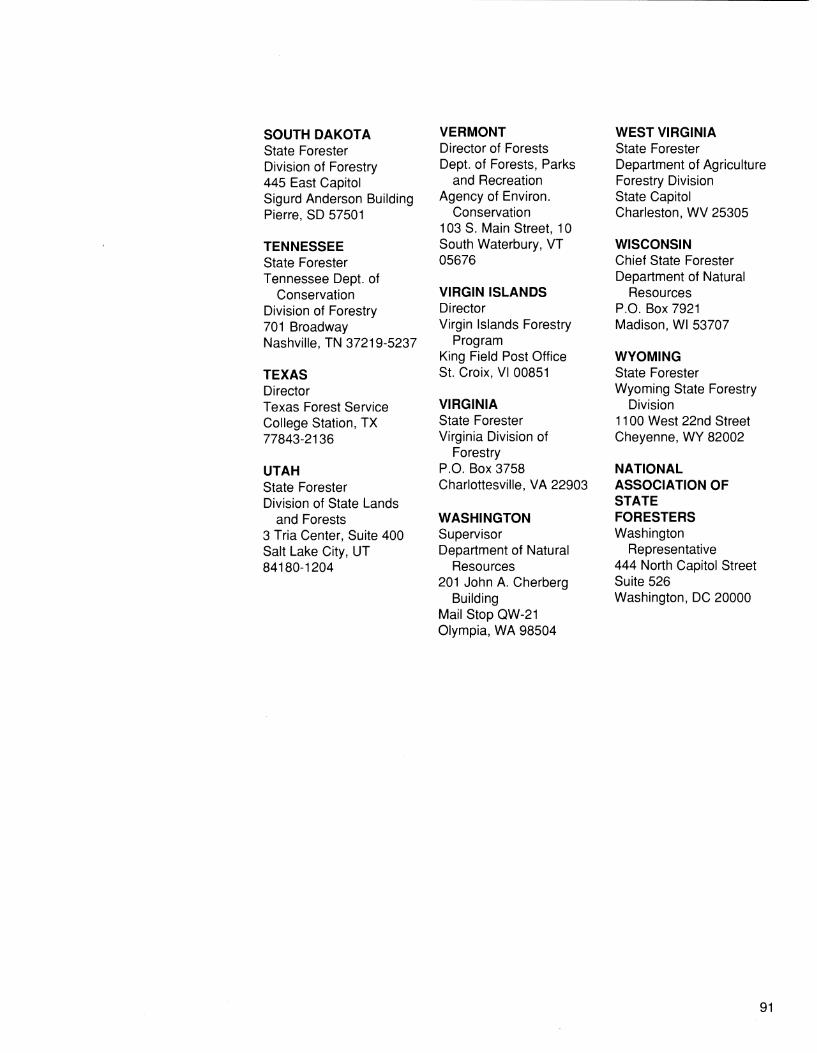

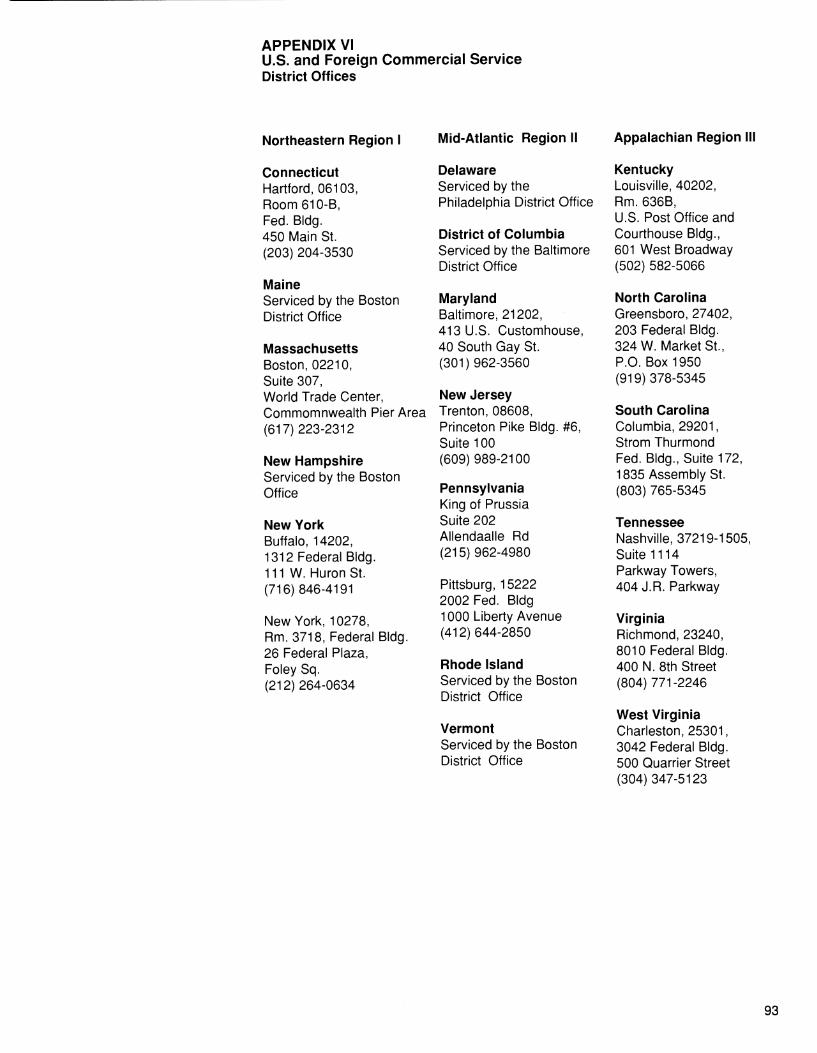

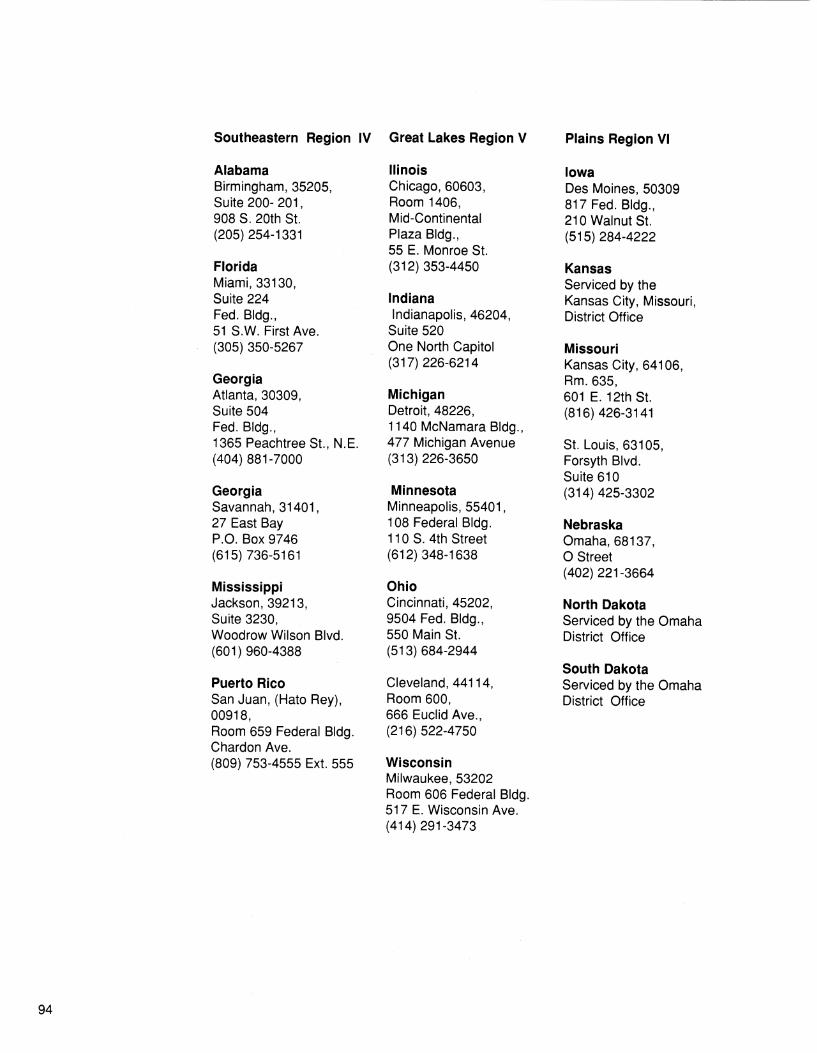

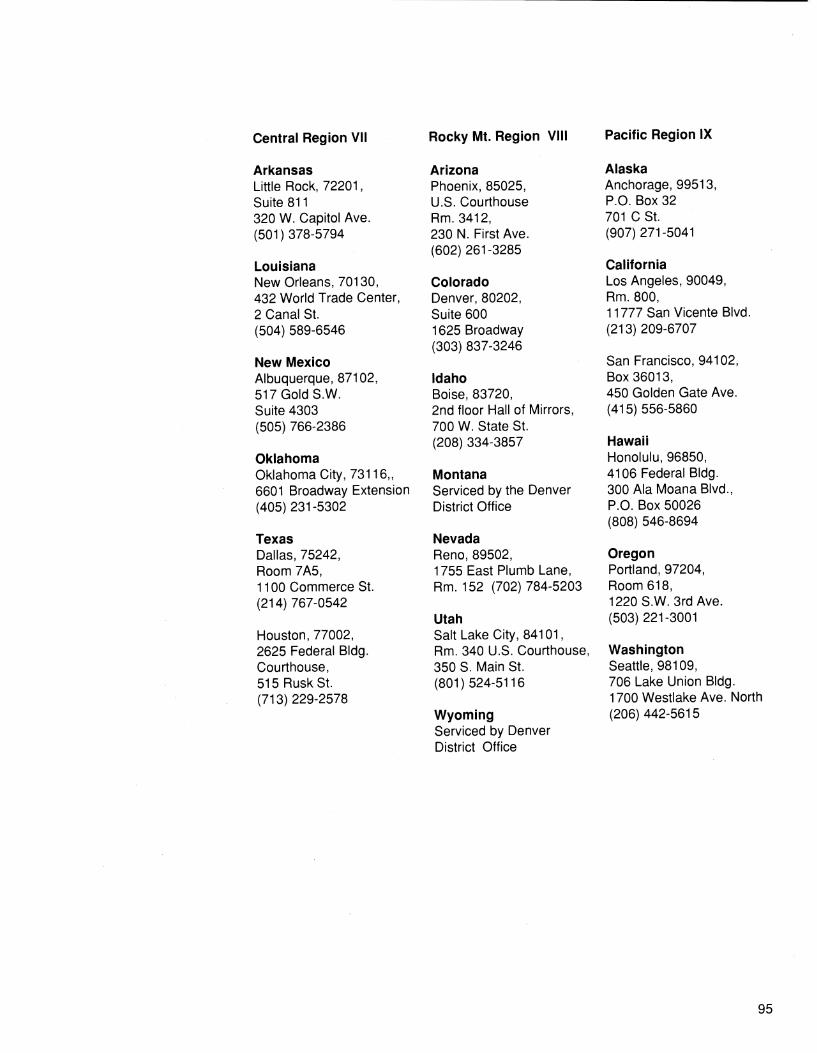

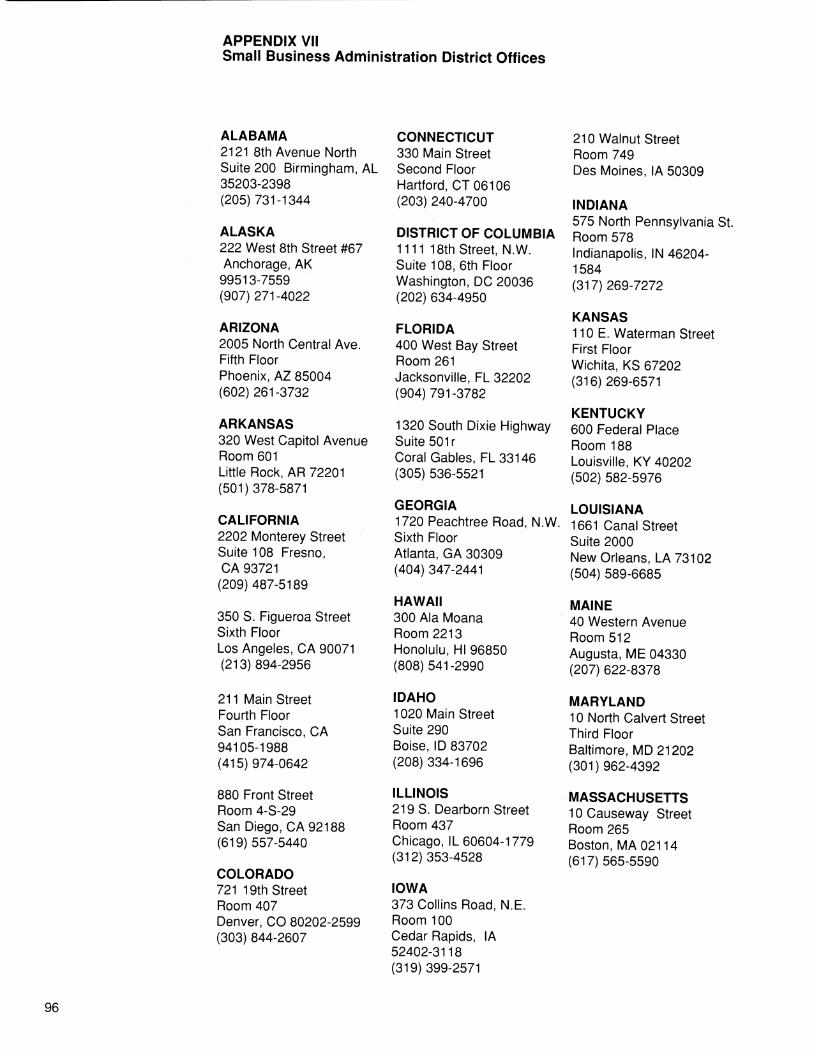

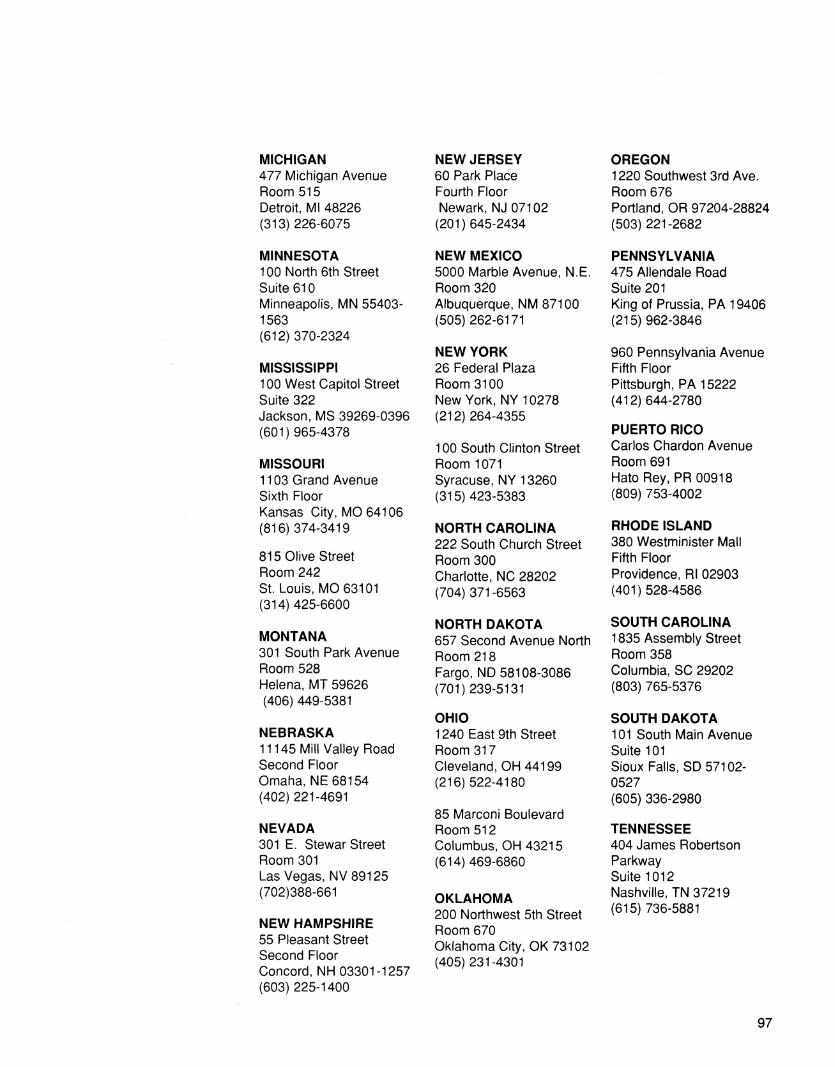

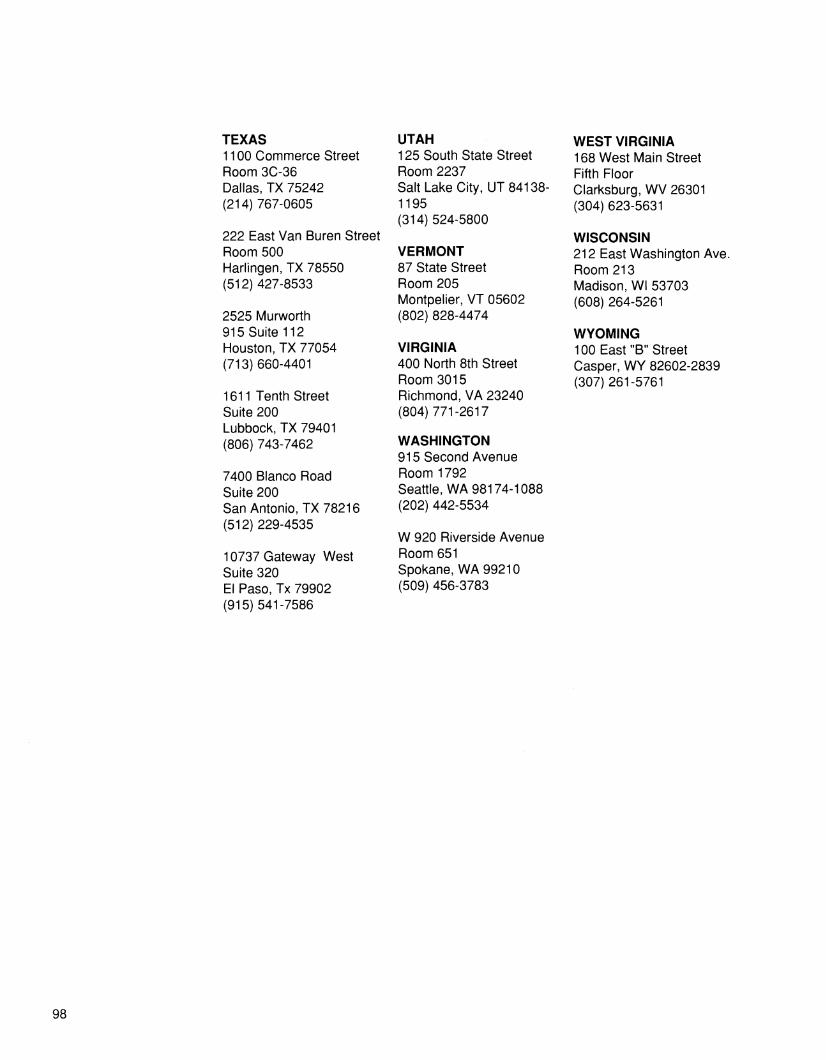

Appendix VI — U.S. and Foreign Commercial Service District Offices 93 Appendix VII — Small Business Administration District Offices 96 Appendix VIII — Glossary of Forest Products and Exporting Terms 99 Appendix IX — Forest Products Volume Conversion Units 106 Appendix X — Forest Products Shipping Weights and Volumes 113

Appendix I Appendix II

Appendix IV Appendix V

III

Introduction

This revision of the 1986 handbook provides a guide for U.S. wood product producers to develop a successful export marketing strategy. It covers how to obtain accurate and up-to-date export market information so that the production, scheduling, and shipping of U.S. wood products can be done profitably. The flow chart on page 3 provides an outline of the major activities associated with exporting and export market- ing. The outline includes many of the topics covered in this guide to exporting wood

products.

Major topics include trade servicing, supply considerations, a review of the major U.S. wood product markets, sources of export information, USDA export programs, export financing, shipping and documentation, product pricing, and the business organization of an export-oriented company.

By the turn of the century, U.S. exports of wood products are projected to be at least 50 percent larger on a value basis than the estimated 1989 level of $6.0 billion. Environmental concerns about dwindling tropical hardwood forests, coupled with export bans/restrictions on logs and rough lumber in tropical hardwood exporting countries, will increase demand for both U.S. hardwoods and softwoods. The Philip- pines, Indonesia, Cote d'Ivoire, and Thailand are recent examples of countries that have either banned or curtailed exports and/or commercial logging.

Traditionally, the U.S. forest products industry has not considered the international market to be an outlet for its products. Only during the 1980's did companies begin to seriously consider exports as a long-term market for wood products—partly in re- sponse to the U.S. recession in 1981-82. Yet, while export value has doubled since 1985, exports of wood products still represent a minor portion of U.S. annual wood production.

The decision to enter the export market is not for every company. Producers must have the flexibility or willingness to tailor a product line to meet specifications quite different from those used in the United States. Producers should be prepared to develop a long-term foreign market development strategy because commitment to foreign importers will include staying with sales when their market is weak.

Before getting involved, consider carefully your short- and long-term corporate objec- tives, the resources available, the level of international business expertise required, and the commitment your firm must make to servicing the export market. Servicing the export market will retain, expand, and diversify your outlets for U.S. forest products.

Strategic export planning in the world market can provide new jobs, greater income, and increased profitability for U.S. wood producers. A stronger forest products industry will lead to new investment in forest management, thus assuring a continuous supply of wood and fiber for the United States and its customers overseas.

A genuine commitment to exporting will include long-term sales to overseas markets regardless of domestic market conditions. "In and out" exporting will guarantee a company's failure in the overseas market and give U.S. producers a reputation for being unreliable.

Exporting clearly requires a long-term outlook as the following table illustrates. The decision to enter the export market requires the producer to commit sufficient managerial, economic, and financial resources to the task. Each company must weigh the advantages and disadvantages of exporting to determine if projected profits, possible losses, and inherent risks justify management's commitment to exporting.

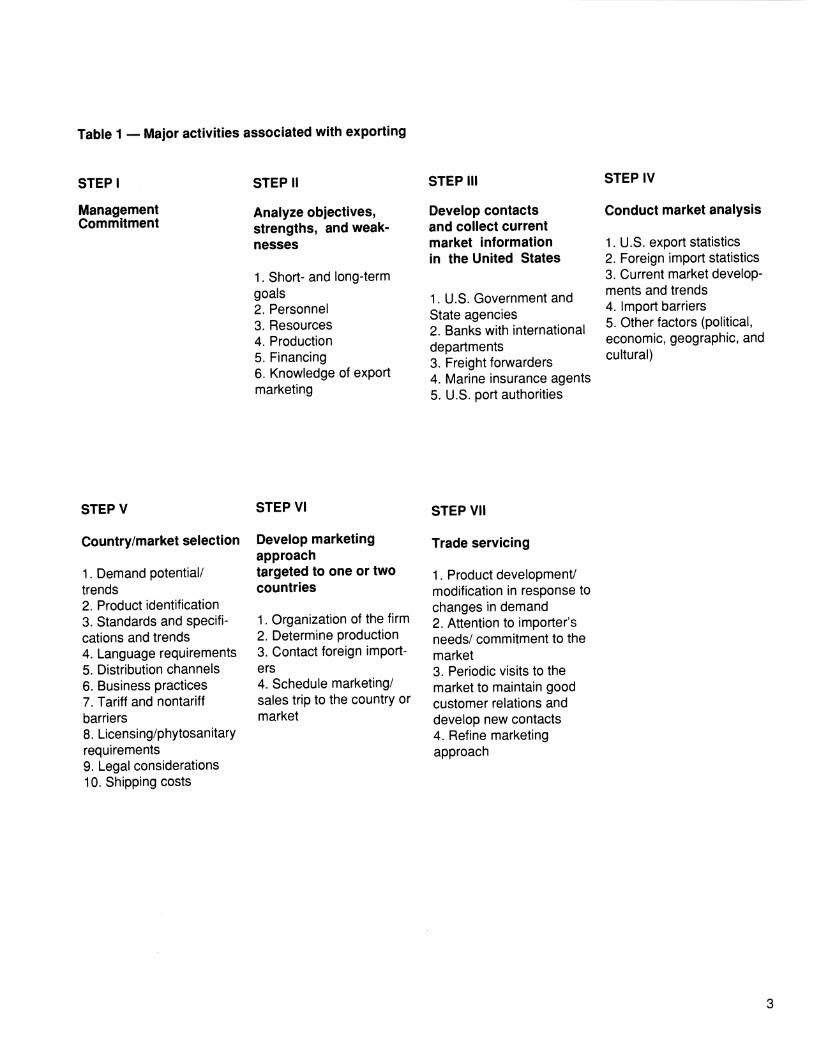

Table 1 — Major activities associated with exporting

STEP!

Management Commitment

STEP II

Analyze objectives, strengths, and weak- nesses

1. Short- and long-term goals 2. Personnel 3. Resources 4. Production 5. Financing 6. Knowledge of export marketing

STEP III

Develop contacts and collect current market information in the United States

1. U.S. Government and State agencies 2. Banks with international departments 3. Freight fon/varders 4. Marine insurance agents 5. U.S. port authorities

STEP IV

Conduct market analysis

1. U.S. export statistics 2. Foreign import statistics 3. Current market develop- ments and trends 4. Import barriers 5. Other factors (political, economic, geographic, and cultural)

STEPV

Country/market selection

1. Demand potential/ trends 2. Product identification 3. Standards and specifi- cations and trends 4. Language requirements 5. Distribution channels 6. Business practices 7. Tariff and nontariff barriers 8. Licensing/phytosanitary requirements 9. Legal considerations 10. Shipping costs

STEP VI

Develop marketing approach targeted to one or two countries

1. Organization of the firm 2. Determine production 3. Contact foreign import- ers 4. Schedule marketing/ sales trip to the country or market

STEP VII

Trade servicing

1. Product development/ modification in response to changes in demand 2. Attention to importer's needs/ commitment to the market 3. Periodic visits to the market to maintain good customer relations and develop new contacts 4. Refine marketing approach

Exporting Wood Products: Advantages, and Risks

The decision to enter the export market requires the producer to commit sufficient managerial, economic, and financial resources to the task. Each company must weigh the advantages and disadvantages of exporting to determine if projected profits, possible losses, and inherent risks justify management's commitment to exporting.

The advantages of exporting wood products include new marketing and financial opportunities, diversification of risk, and increased financial leverage and credit. In addition, revenue derived from export sales permits spreading fixed costs over a greater number of production units. Wider margins may be realized on higher valued products.

Producing for foreign markets can also have its downside. Tailoring wood products to foreign standards and specifications requires skilled personnel for procurement and milling operations.

Plans to produce according to foreign specifications may not match with existing high- speed, high-volume manufacturing practices. As a result, production costs per unit may be higher. If wood products designed and produced to foreign specifications need to be sold on the domestic U.S. market, they may require additional processing such as resawing, planing, or sanding.

Common mistakes made by companies entering the export market are:

• Failure to obtain qualified export counseling.

• Failure to develop an international market plan.

• Insufficient commitment by top management to overcome the initial difficulties and financial requirements of exporting.

• Insufficient care in selecting overseas agents or distributors.

• Pursuing orders from around the world, the shotgun approach, instead of establish- ing a basis for profitable operations and orderly growth.

• Neglecting export business when the U.S. market booms.

• Failure to treat international customers on an equal basis with domestic counter parts.

• Unwillingness to modify products to meet regulations or cultural preferences of other countries.

• Failure to print service, sales, and warranty messages in locally understood lan- guages.

• Failure to consider use of an export management company or other marketing intermediary.

• Failure to consider licensing or joint-venture agreements.

• Failure to realize that it takes patience and understanding to develop the ties necessary to obtain and retain export sales.

Success or failure in exporting hinges on an exporter's willingness to allocate sufficient resources to research foreign demand, develop contacts, and produce, market, ship, and sell wood products overseas. These activities are referred to as "trade servicing.

Trade Servicing: If employed conscientiously, trade servicing helps overcome many of the disadvan- The Key to Success ^^ges and pitfalls in export marketing and helps lessen the effect of economic forces

and other factors which an exporter cannot control.

There is no substitute for a good working relationship with the overseas buyer. This is particularly important given the U.S. wood exporter's reputation overseas as an "in-and-outer" in servicing the export market. The producers who have stayed in the export market, in good times as well as bad, have proved to be the most effective. Being reliable sometimes means sacrificing short-term gains for long-term market development opportunities.

Supply Consideration: What Do You Have To Sell Overseas?

Deciding what you can sell overseas depends on a host of variables. You will have to consider what you are producing now, your access to timber resources with respect to species, qualities, and quantities; access to processing facilities; transportation; proximity to ports; and how adaptable your current operation is to cutting special orders or scheduling the mill to cut or produce for export markets. Success in the export market may even involve adapting production facilities to produce for foreign grades and specifications.

Before taking on the world, you may do best by focusing first on one or two countries where U.S. wood products are familiar to importers. Become knowledgeable about the country and develop a consistent pattern of trade contacts with importers in that country. Nurturing a commitment to marketing in one or two countries before branch- ing out will pinpoint your strengths, weaknesses, and limitations in serving export markets. Once your expertise develops you may feel confident in testing new markets and new products, and in diversifying your export market portfolio.

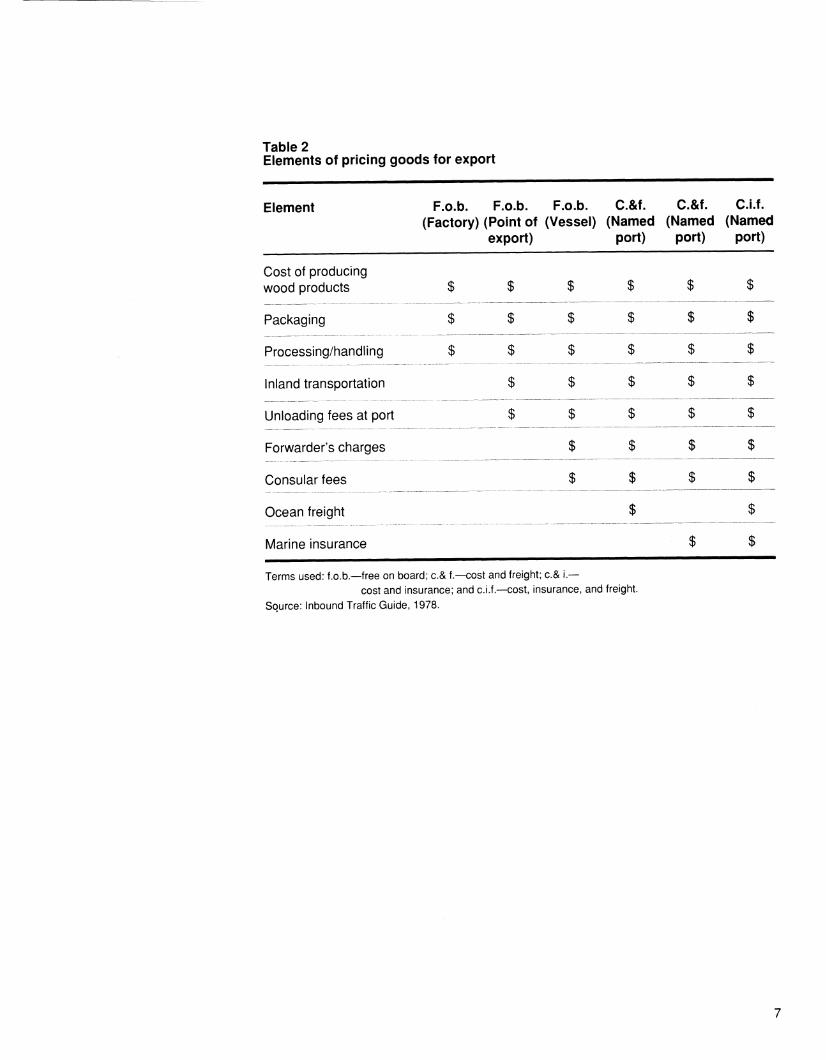

Pricing Products for Export

Table 2, on page 7, outlines the elements of a price quote for each stage through which products move as they pass from the mill to the port of destination overseas. The quote basis used, such as free-on-board (f.o.b.) vessel or cost, insurance, and freight (c.i.f.) named port overseas, will depend on the arrangement negotiated with the importer. A price quote that more closely reflects the cost of goods delivered to the importer's yard has a much better chance of being negotiated and accepted than a quote based on delivery to the U.S. port prior to export. Quotes should include infor- mation on shipping arrangements and dates, payment terms, weights, and total cubic volume. The actual price quote will include these elements but will be influenced by foreign import demand, freight rates, insurance costs, domestic supplies, and proximity to exporting facilities and ports.

Quotes based solely on domestic U.S. prices plus additional transportation, handling, and insurance costs may or may not be acceptable in international trade. This de- pends on the negotiations between the U.S. exporter and the foreign buyer. Current benchmark or average prices for specific species and grades of forest products in international trade may be obtained from the publications and newsletters outlined in this handbook.

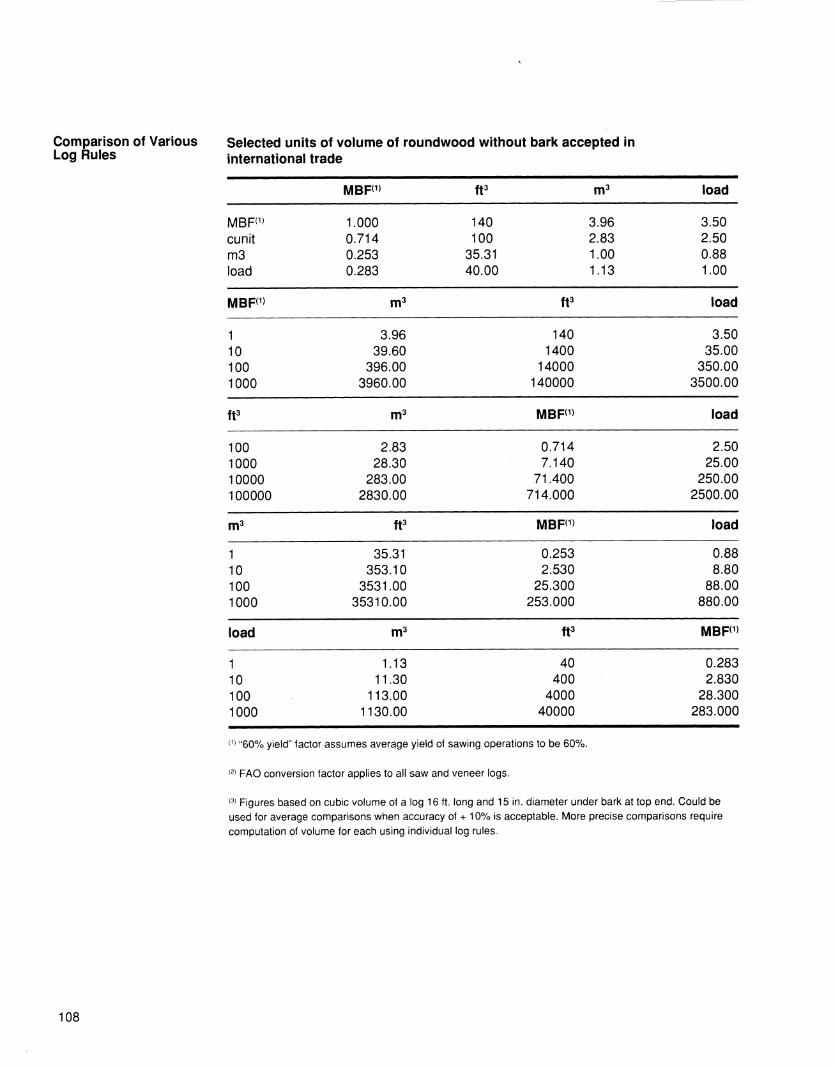

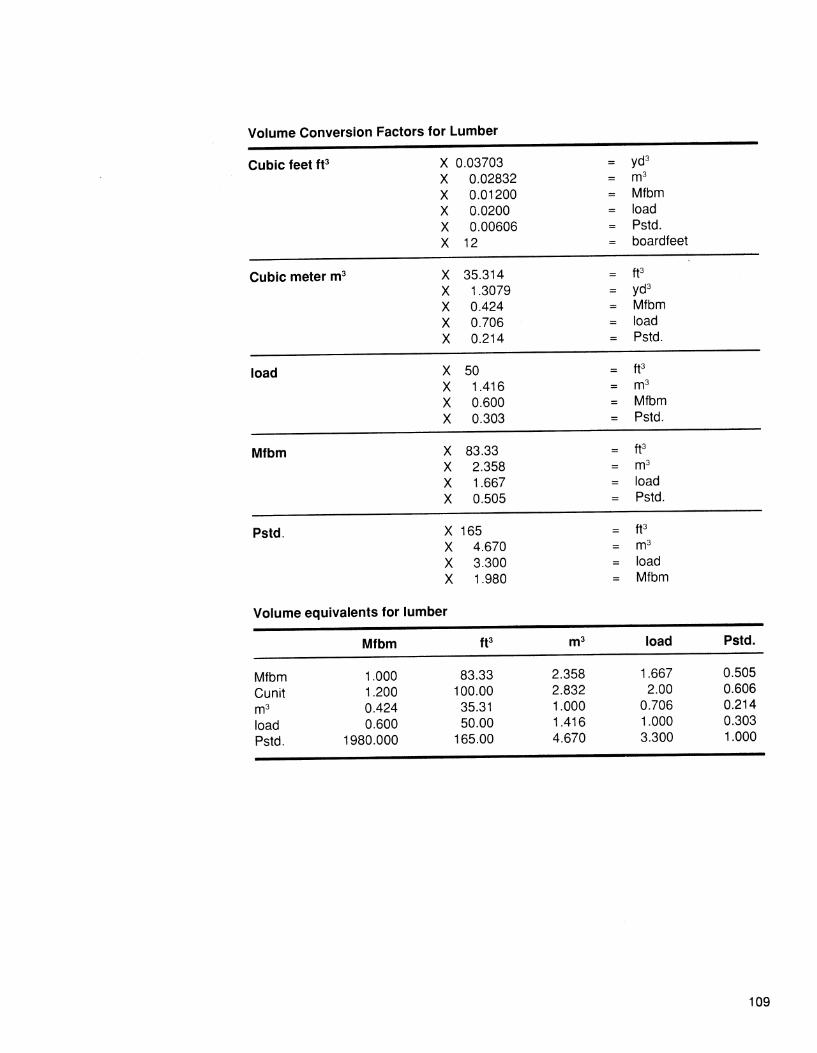

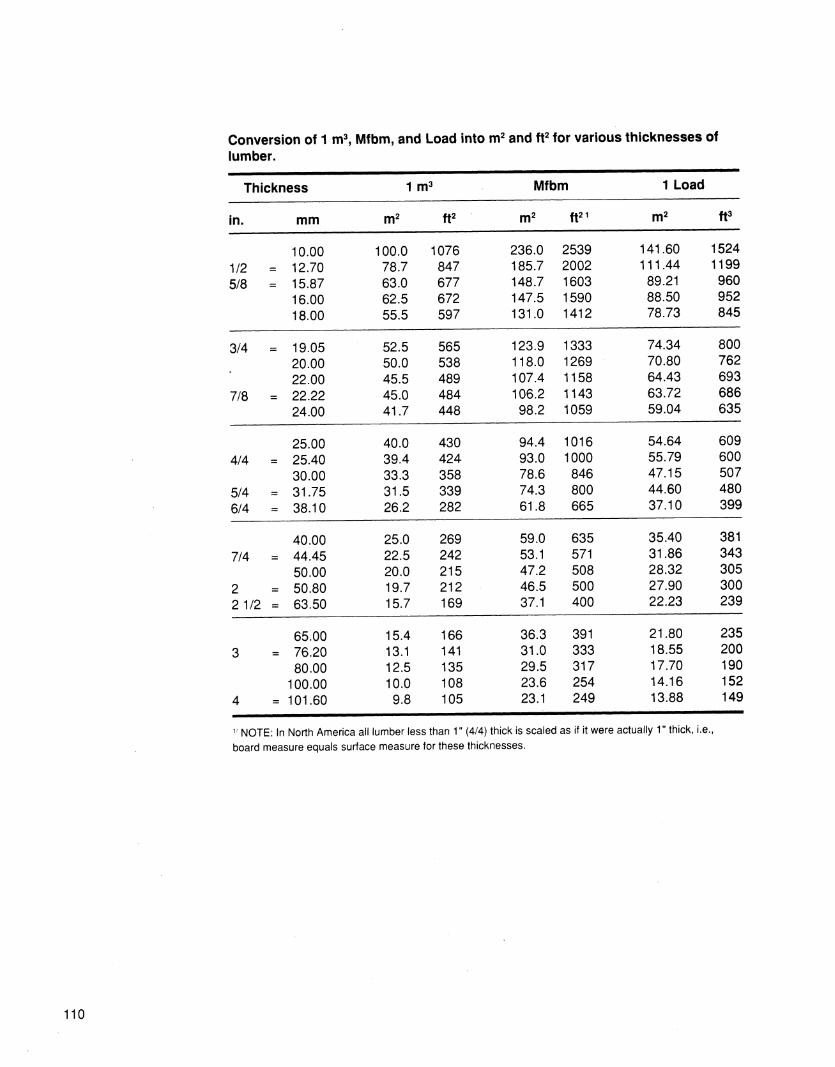

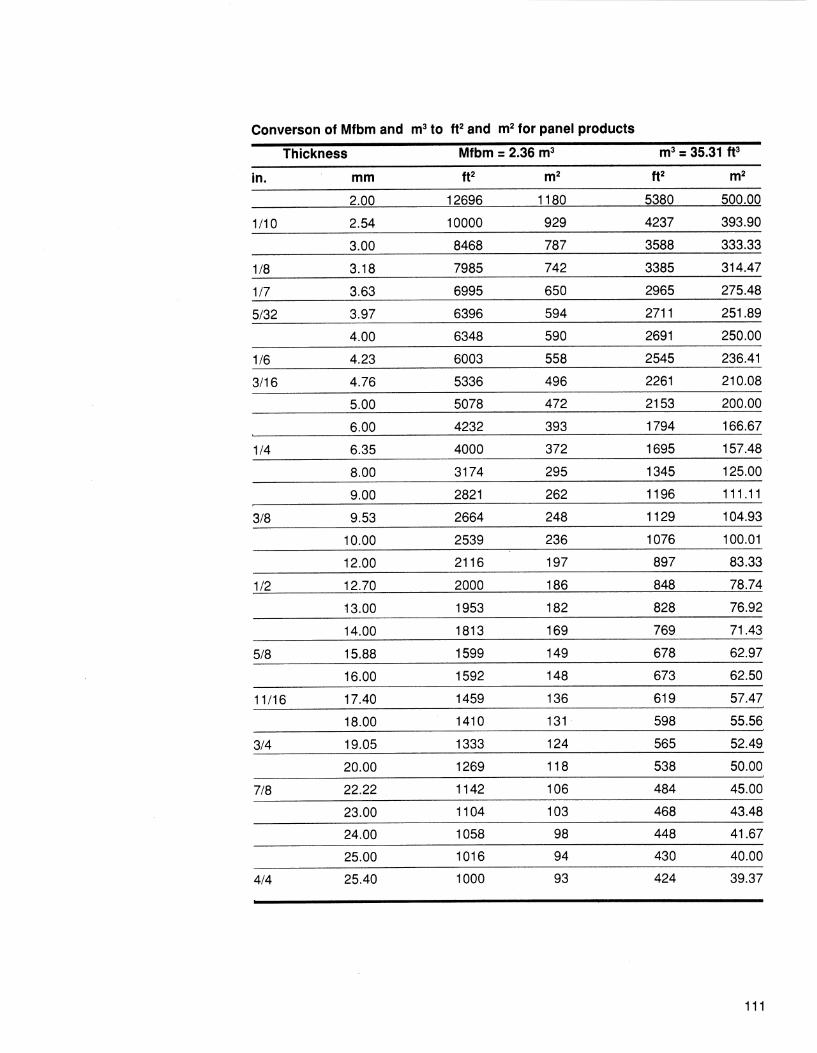

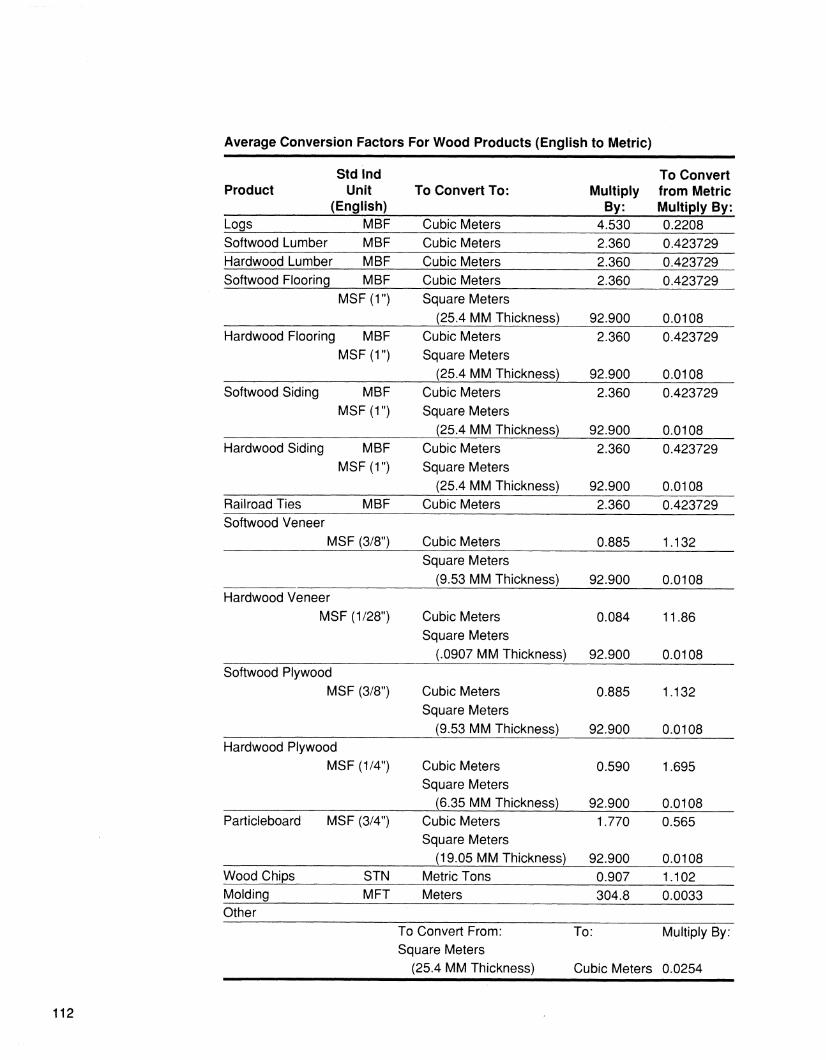

In the United States, forest products are bought and sold according to volume designa- tions such as 1,000 board feet, 1,000 square feet, or 1,000 linear feet. In foreign countries, common volume units in the wood trade are 1,000 cubic meters, 1,000 square meters, and metric tons.

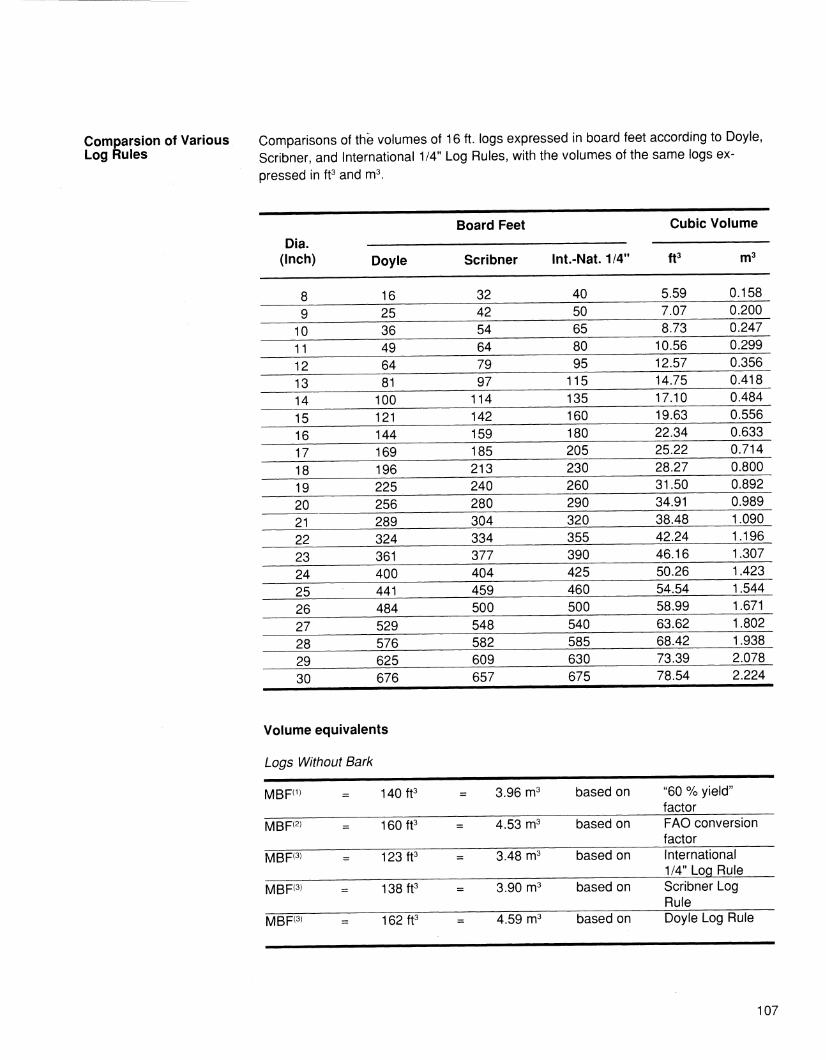

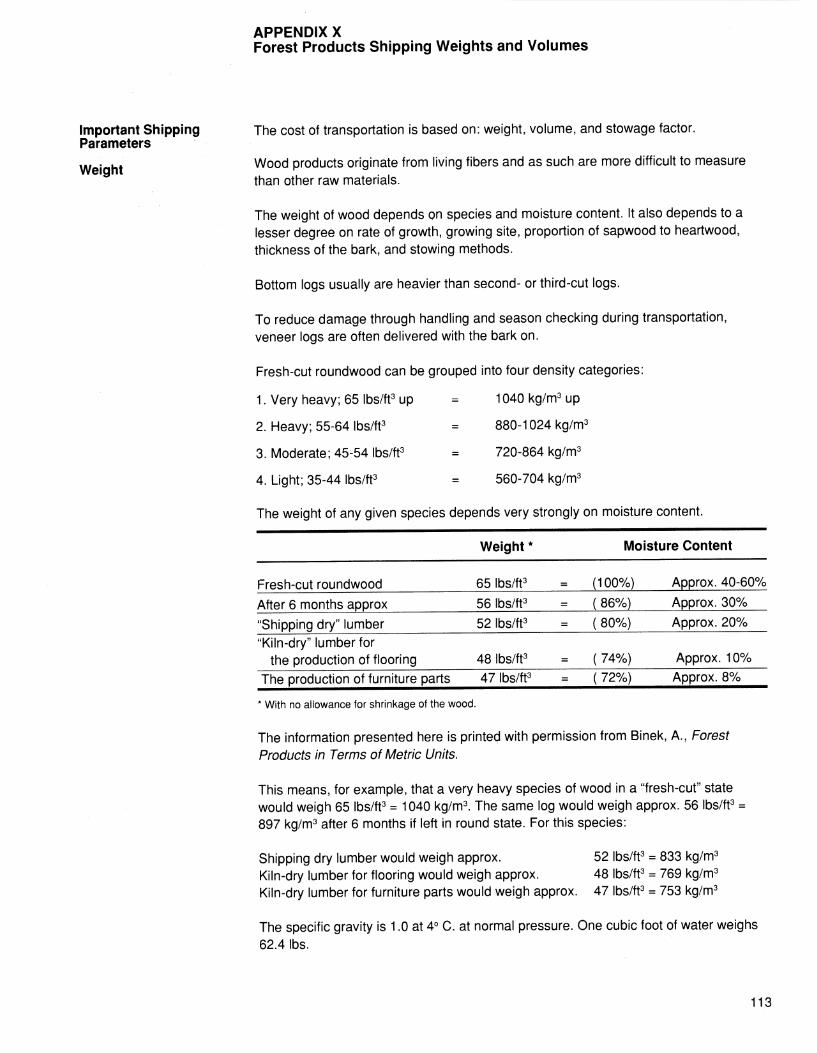

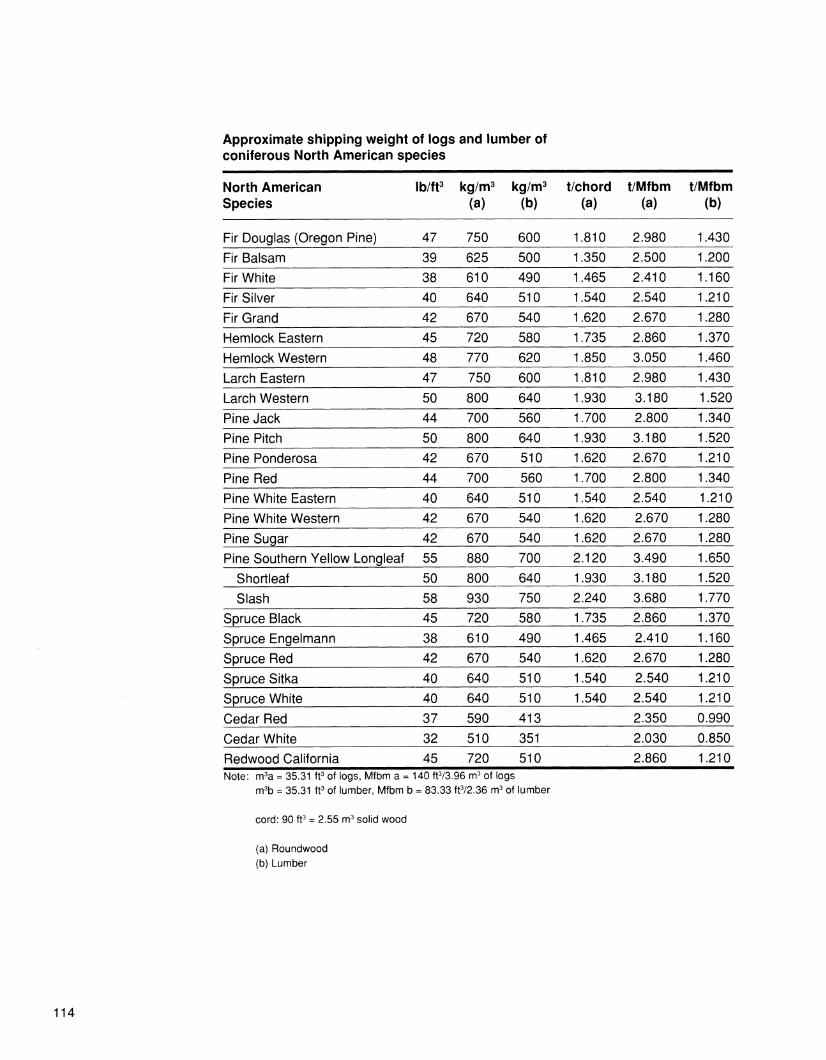

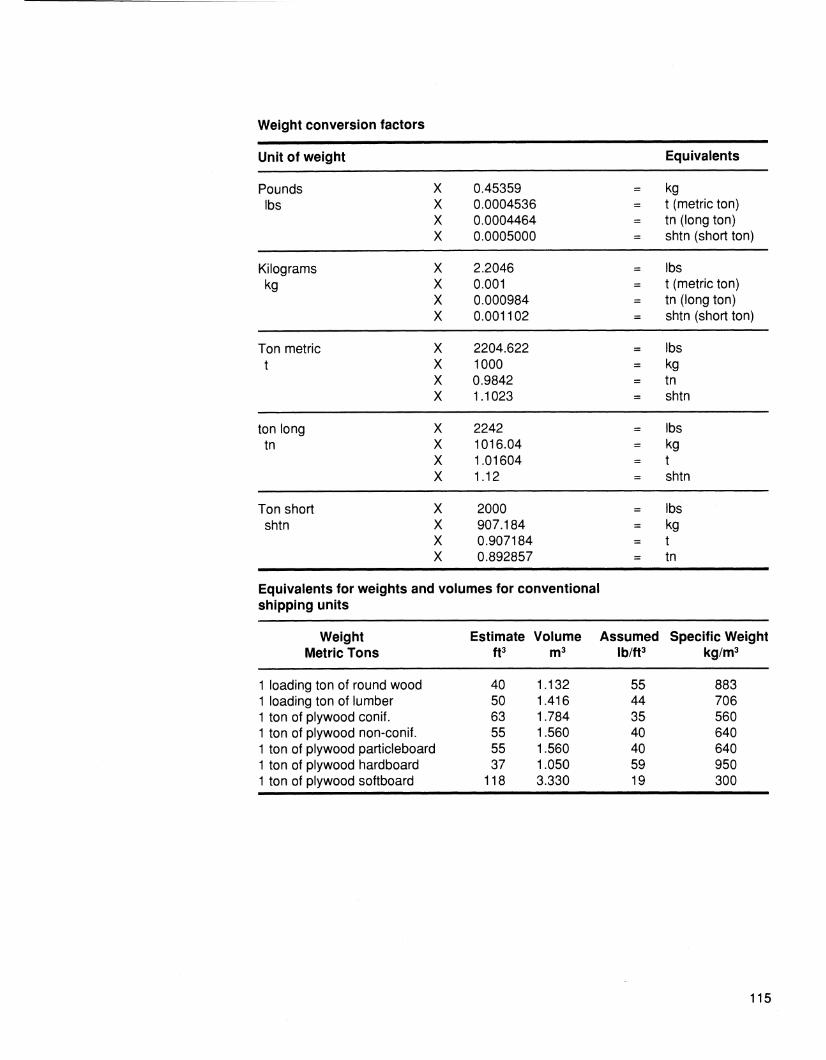

The exporter must be familiar with converting U.S.-based volume measurements to the metric system. Forest products volume conversion ratios and methods are shown in appendix IX. Shipping weights and volumes for a number of products and species are shown in appendix X.

Table 2 Elements of pricing goods for export

Element F.o.b. F.o.b. F.o.b. C.&f. C.&f. C.i.f. (Factory) (Point of (Vessel) (Named (Named (Named

export) port) port) port)

Cost of producing wood products

Packaging

Processing/handling

Inland transportation

Unloading fees at port

Forwarder's charges

Consular fees

$ $ $ $ $ $

$ $ $ $ $ $

$ $

$

$ $ $

$

$

$ $ $

$ $ $ $ $

$ $ $ $

$ $ $ $

Ocean freight

Marine insurance

Terms used: f.o.b.—free on board; c.& f.—cost and freight; c.& i.— cost and insurance; and c.i.f.—cost, insurance, and freight.

Source: Inbound Traffic Guide, 1978.

FINANCING EXPORTS

Payment Options for Listed below are nine options for receiving payment for exported goods. The best Export Shipments method to use depends on a number of factors including the credit rating of the foreign

customer, any foreign exchange restrictions imposed by the importing country, and competitive goods and credit facilities available to overseas buyers. Your bank or financial institution should be knowledgeable about most of these payment options.

Cash In advance—This is the most desirable and safest method of receiving payment since the exporter has immediate use of the money and is not concerned with repay- ment schedules. The percentage of trade conducted under this method is low.

Open account—This is the riskiest method because it is merely an arrangement between the buyer and seller for payment at a later date with no legal document or recourse available to the exporter. Also, the exporter's capital is usually tied up until time of payment. This method is used by exporters who deal with longstanding cus- tomers of unquestionable integrity.

Consignment sales—Under this method, the goods are available to the foreign firm on a deferred payment basis. The exporter usually secures political and commercial risk insurance for the goods until payment is received.

Sight draft—Money is payable at sight of the completed documents. This method is used when sellers wish to retain control of the shipment either for credit reasons or for the purpose of title retention. A bank acts as an intermediary and is presented with the original bill of lading endorsed by the shipper and other documents (such as packing lists, consular invoices, and insurance certificates) which are not released to the importer until payment of the draft. The advantage of this method is that the exporter retains title to the goods until payment is made. The disadvantage is that the importer can refuse to pay the draft, and the exporter is responsible for shipping the goods back to the United States at the seller's expense or reselling to a third party in the foreign country.

Time or acceptance draft—This method is similar to a sight draft except that the importer may defer payments of the draft for 30, 60, 90, or 180 days. Although the exporter does not have any legal recourse if the importer does not pay, a foreign or U.S. bank does act as an intermediary for collection purposes.

Date draft—The date draft requires payment by a specified date regardless of the date on which the goods and the draft are accepted by the importer. Date drafts prevent the importer from extending the period of credit as a result of postponing receipt of the goods.

Delivery orders—Some countries do not recognize or permit sight draft shipments, including negotiable bills of lading. Shippers may consign the merchandise to a third party, such as an import broker, in the foreign country on a straight bill of lading. The shipper will write a letter called a "delivery order" to the third party authorizing release of the shipment to the bearer of the original delivery order. The required documents will be sent to the importer's bank with instructions to the broker to release goods to the importer only after the draft is accepted. The importer's bank is usually the third party.

Letters of Credit and Invoices

Letters of Credit—The "letter of credit" is a document issued by a bank at the im- porter's request in favor of the exporter obligating the importer to pay for the shipment when the bank receives the required shipping documents. There are two types of letters of credit. The first is an irrevocable letter of credit confirmed by a U.S. bank. This guarantees the seller that payment terms and conditions of the letter credit have been met. The second type is an irrevocable letter of credit confirmed by the foreign bank but not the U.S. bank; payment is guaranteed by the foreign bank. The first type is preferred because the U.S. bank accepts the responsibility to pay and the exporter receives payment as soon as the documents are presented to the bank.

Barter and Countertrade—Countertrade is an arrangement for payment or financing by a means other than a cash-for-goods basis. Barter is the easiest form of counter- trade to understand: goods for goods. Bartering benefits Third World countries by offsetting the influence of other market forces that may work against their competitive position including high interest rates and a high relative strength of the U.S. dollar compared to other foreign currencies. Countertrade may be considered as an alterna- tive payment or financing scheme and is promoted by centrally planned economies. The method is not generally used by U.S. companies because it increases costs, requires additional management time and planning, and is characterized by detailed contract requirements. In the ideal countertrade arrangement, a company receives goods that it can use internally or sell to established customers.

Selling or distributing countertraded goods which are not traditionally handled by the firm will require new marketing practices and channels. Additional costs should be anticipated when handling new products obtained in countertrading. The company may consider employing a countertrade specialist or trading company to sell the goods.

Information required in the letter of credit (L/C) must match with other shipping docu- ments and invoices. Information from an American Express Company brochure lists some of the most common errors and oversights associated with shipping documenta-

tion:

Merchandise description not identical to that in the letter of credit (L/C). Buyer's name not identical to that shown in the L/C. Total amount not identical to that shown in the draft. Excess drawing or excess shipment. Net value in excess of L/C amount. Prices not as specified in the L/C. Incorrect extension of prices. Omission of the price basis, such as f.o.b., f.a.s., or c.i.f., specified in the L/C. Inclusion of charges not specifically permitted under the terms of the L/C, such as commission, storage, or messenger costs. Not marked "PAID" when specified in the L/C. Not certified, notarized, or visaed if required by the L/C. Absence of statements required by the L/C. Type of packing, weight, or marks omitted from invoice. Marks and numbers not consistent with other documents. Weights not consistent with those shown in other documents. Gross weight shown for net when not expressly permitted by L/C. Order and license numbers required by L/C omitted.

• Goods termed "used" or "second hand" when not allowed by L/C. • Absence of specified signature. • Insufficient number of copies.

Foreign Credit The Foreign Credit Insurance Association (FCIA) is an association of leading private /prMA^"^^ Association insurance companies which works in cooperation with the Export-Import Bank of the ^ ' United States (Eximbank). FCIA offers export credit insurance policies protecting U.S.

exporters against the risk of nonpayment by foreign debtors due to commercial (insol- vency, default) or specified political (war, revolution, currency inconvertibility) reasons.

FCIA offers a wide variety of policies for short-term sales (up to 180 days) and me- dium-term sales (generally, up to 5 years). Products must be of U.S. manufacture and contain no more than 49 percent foreign content (including labor, but exclusive of markup) for short-term sales, and generally no more than 15 percent foreign content is allowable for medium-term sales. Coverage is also available for services and for operating and financing lease transactions.

The widely used Multi-Buyer Export policy is generally written to cover shipments during a 1-year period and insures a reasonable spread of an exporter's eligible sales. It enables the exporter to make quick credit decisions, providing faster service to overseas buyers, and reduces paperwork. The exporter can obtain financing and can offer competitive credit terms to attract and retain buyers around the globe even in higher risk markets. The policy insures short-term sales with repayment terms gener- ally up to 180 days and, in an alternative version, covers medium-term sales, with repayment stretching out to 5 years, or longer under certain circumstances.

At the inception and at each annual renewal of the Short-Term Multi-Buyer policy, the exporter may choose to cover 90 percent of commercial risks and 100 percent of political risks, or choose equalized coverage at 95 percent for both commercial and political risk. Certain agricultural commodities may be insured under this policy, with terms extended to 1 year, if needed, and with commercial coverage increased to 98 percent. On short-term transactions coverage applies to the gross invoice amount and, in many cases, to interest at FCIA specified rates. Since medium-term sales require a minimum 15 percent cash payment by the buyer on or before due date of first install- ment, coverage here applies to the balance—the financed portion—of the transaction plus interest at FCIA specified rates.

The Multi-Buyer Export policy has a deductible feature similar to that of major medical and other forms of insurance.

The policy is subject to limits. The aggregate limit represents the insurers' maximum liability under the policy. Exporters make their own credit decisions for shipments up to the amount of a discretionary credit limit (DCL), after checking the country limitation schedule (CLS) and documenting the credit worthiness of the buyer as specified in the DCL endorsement to the policy. For larger amounts, a special buyer credit limit (SBCL) is available upon application to FCIA.

For additional information, contact FCIA at 40 Rector Street, 11th Floor, New York, NY 10006. Tel. (212)227-7020.

10

Export-Import Bank of the United States

Overseas Private Investment Corporation (OPIC)

Small Business Administration (SBA)

The Export-Import Bank (Eximbank) of the United States is the U.S. Government agency that facilitates the export financing of U.S. goods and services. Eximbank helps U.S. exporters compete against foreign governments subsidized financing in overseas markets. Eximbank offers four major export finance support programs: loans, guarantees, working capital guarantees, and insurance.

Lending Programs—Eximbank's loans provide competitive, fixed interest rate financing for U.S. export sales of capital equipment and services. Eximbank extends loans to foreign buyers of U.S. exports and intermediary loans to fund responsible parties that extend loans to foreign buyers. These loans are made at low, fixed interest rates according to the Organization for Economic Cooperation and Development arrange- ment. Special features are available for small businesses.

Guarantee Program—Guarantees provide repayment protection for private sector loans to creditworthy foreign buyers of U.S. goods and services. The guarantees provide coverage for both political and commercial risks.

Working Capital Guarantee Program—Eximbank also offers guarantees to lenders to support pre-export financial needs. The Working Capital Guarantee Program can help small- and medium-sized exporters obtain the financing they need to produce and market goods for sale abroad.

Insurance—The insurance program administered by the Foreign Credit Insurance Association, offers insurance policies to protect U.S. exporters and banks against the political and commercial risk of nonpayment by foreign debtors. Special policies exist for small or new-to-export businesses.

Inquiries should be directed to Eximbank Marketing Division, 811 Vermont Avenue, NW., Washington, DC 20571. Tel. (202) 566-4490; Small Business Hotline: (800) 424- 5201.

OPIC is a U.S. Government corporation that promotes U.S. investment in less devel- oped countries. OPIC's finance program is oriented towards medium- to long-term investments that involve significant developmental benefits. The program provides insurance coverage for U.S. investments against expropriation, inconvertibility of local currency, or losses resulting from war, revolution, or civil disorders. OPIC does not handle export financing directly but may assist in financing complementary projects, such as a distribution yard for U.S. wood products. Insurance on letters of credit may also be obtained in the absence of FCIA or other commercial insurance. The insurance covers 90 percent of the investment plus attributable earnings. For additional informa- tion, contact OPIC, 1615 M Street, NW., Washington, DC 20527. Tel. (202) 457-7010. Fax:(202)331-4234.

The mission of the Small Business Administration is to aid, counsel, assist, and protect the interests of small business; ensure that small businesses receive a fair portion of Government purchases, contracts, and subcontracts, as well as of the sales of Gov- ernment property; make loans to small business concerns, state and local develop- ment companies, and the victims of floods or other catastrophes or of certain types of economic injury. The SBA also licenses, regulates, and makes loans to small business investment companies.

11

Export Revolving Line of Credit Program (ERLCP)—The Small Business Administra- tion (SBA) can guarantee up to 90 percent of a bank line of credit to an eligible small business or Export Trading Company (ETC) to finance the acquisition of raw materials, inventory, or labor needed to produce, acquire, or market the product or service to be exported. The ERLCP may not exceed 18 months or $750,000. Funds may not be used to acquire fixed assets or retire existing debt.

The Export Trading Company must have been in business for 1 year (not necessarily in exporting) prior to applying for an ERLCP loan through its bank.

SBA Regular Business Loan Program—Under this program an eligible small business or Export Trading Company may obtain longer-term financing (depending on use of proceeds). Up to $750,000, or 90 percent of the loan, may be obtained on an SBA- guarantee basis. Up to $150,000 (depending on availability of funds) can be obtained as a direct loan under this program. Interest rates may be fixed or variable.

Regular Business Loan Program—Funds may be used to obtain plant or equipment and for working capital. However, export trading companies with any bank equity participation are not eligible for these SBA financing programs. SBA can assist only those eligible small businesses and export trading companies which have the majority of their assets in the United States. Funding through these programs cannot be used to establish joint ventures overseas.

Small Business Investment Companies (SBIC)—Equity capital or long-term financing may be obtained by eligible small businesses from SBIC's which are licensed by SBA, if these SBIC investment companies have an investment strategy that includes such activities. SBIC's may invest in export trading companies in which banks have equity participation, provided other SBIC requirements are met. For further information and a copy of a directory of SBICs, contact the Office of Investment, Small Business Admini- stration, 1441 L Street, NW., Washington, DC 20416. Tel. (202) 653-2806. Fax: (202) 254-6429.

U.S. Trade and Development Program (TDP)

The U.S. Trade and Development Program (TDP) of the U.S. International Develop- ment Cooperation Agency promotes U.S. exports to developing nations. The program provides financing for feasibility studies for public and private sector projects in devel- oping economies which would lead to the export of U.S. products and services. Helping U.S. businesses win construction contracts overseas is one of the main objectives of the TDP. For example, an export trading company of construction, architecture, and engineering firms might approach the TDP for financing a construc- tion, building, or housing project which could lead to an increase in U.S. wood products exports. Other studies include large-scale energy generation and conservation, infrastructure, mineral development, agribusiness, and basic industrial facilities all of which could use U.S. wood products. For additional information on country eligibility, developmental priorities, and U.S. goods procurement requirements, contact the U.S. International Development Cooperation Agency, Washington, DC 20523. Tel. (703) 875-4357.

Trade Finance Corporation (TRAFCO)

TRAFCO offers fixed and floating interest-rate financing for medium-term export loans insured by a major insurance companies. Export credit insurance covering commercial

12

and political risk is required in this financing program. TRAFCO "conduit" securities, representing a segment of a pool of export loans, are certificates that can be sold to institutional and private investors. The "pools" are held by a trustee who receives payments on behalf of the holders of the certificates. TRAFCO funds are generated through the U.S. capital market. Additionally, the program has effectively introduced export financing paper to the capital market. Principal buyers include insurance companies, fiduciaries, mutual funds, and public funds. For more information, contact TRAFCO, 2121 Ponce de Leon Blvd., Suite 920, Coral Gables, FL 33134. Tel. (305) 446-5607.

13

Export Shipping

Carriers

The development of a successful export strategy must encompass a thorough knowl- edge of shipping procedures, documents required, and methods. The mechanics of shipping include: (1) attention to packaging, including banding of bundles, grade stamping, labeling, and color coding; (2) proper documentation; (3) scheduling the best shipping routes and carriers; and (4) an understanding of U.S. and foreign customs, regulations, tariff rates, and plant health requirements.

Often, the details of export shipping may be handled by a "freight forwarder," who acts as an exporter agent shipping goods overseas. Freight forwarders are licensed by the Federal Maritime Administration to facilitate the movement of goods from U.S. ports. They may advise the exporter regarding freight costs, port charges, consular fees, documentation fees, insurance, and handling costs. In addition to assuring that the goods arrive overseas in good condition, they review the letter of credit and other necessary documentation and may prepare the ocean bill of lading. After shipment, the forwarder will send all documents to the paying bank to confirm the export of the commodity.

Additional information on freight forwarders may be obtained from port authorities, the International Trade Administration; the U.S. Department of Commerce; banks; or from the National Customs Brokers and Forwarders Association of America whose address is One World Trade Center, STE 1109, New York, NY 10048. Tel. (212) 432-0050.

USDA's Office of Transportation also helps exporters with problems concerning the transportation of U.S. agricultural products, including forest products. For further information, see page 27.

Three types of ocean carriers ship products overseas. The first are conference lines which consist of an association of ocean carriers providing common rates and serv- ices. Individual conference carriers may take independent action and offer shippers lower rates. Also shippers may form associations to negotiate lower rates with confer- ences.

The second type of carriers are the independents. Independent rates may be higher than other carriers, but they also may be lower when in direct competition with confer- ence carriers. Both conference and independent carriers operate on regular schedules and trade routes. Independent proprietary carriers include major forest products companies with their own transportation operations. These lines specialize in forest products and other bulk commodity shipping.

The third type of carrier is the tramp vessel. These carriers generally handle only bulk cargo and are not on regular schedules or trade routes. According to the Western Wood Products Association, tramps are the most common means of shipping wood products as they are relatively economical.

A booking contract is mandatory to reserve space for the cargo on a specified vessel. The contract is binding insofar as the carrier has the right to charge for reserved space that is not used or to charge for canceled reservations without adequate notice.

14

Terminals

Packaging and Shipping

Export Documentation

The use of specialized forest products handling facilities at the ports of export and destination prove to be the most cost effective. This will be reflected in lower freight rates and landed costs. Moving lumber and other forest products through general cargo terminals can be very expensive.

Packaging products is of vital importance particularly when shipments are bound for ports with inadequate handling and storage facilities. Lumber, plywood, and veneer bundles must be securely strapped and protected from damage because of rough handling, moisture, or weathering. This is essential in foreign ports where bundles may be stored uncovered while awaiting pickup or delivery. Bundles should be clearly marked according to foreign specifications and include the company logo or color

coding.

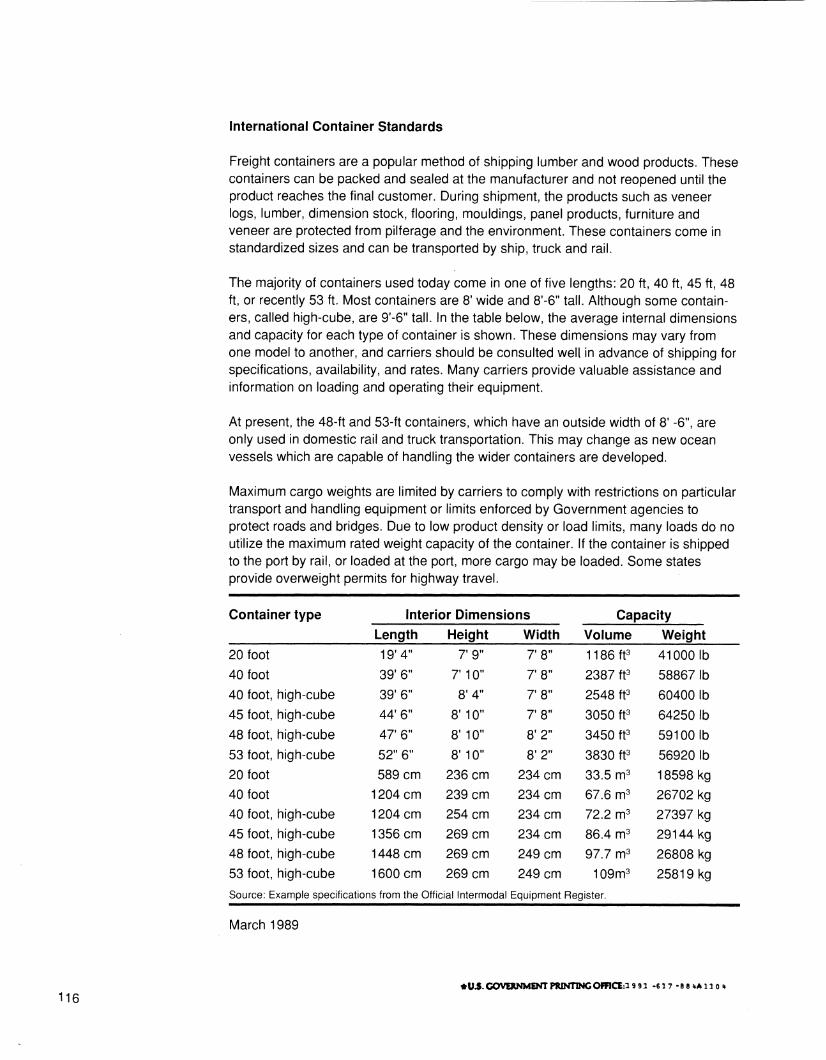

Wood products are shipped by a variety of methods including break bulk, containers, flat racks, and lash barge. The most common methods are break bulk for lumber and plywood shipments and containers for higher valued shipments such as kiln-dried dimension stock, lumber clears, and veneer.

In general, wood shipments from U.S. Atlantic ports are containerized, whereas those from the Gulf and West Coast ports tend to be break bulk. There are exceptions depending on the destination country and the type of wood product shipped.

Freight containers are capable of holding approximately 4,000 board feet of logs or 10,000-14,000 board feet of lumber depending on the product and moisture content. Maximum cargo weights are, however, limited by carriers to comply with laws estab- lished to protect roads and bridges. A 40-foot container, therefore, can only be loaded with about 46,000 pounds of forest products when traveling over U.S. highways. Containers loaded at the port may have higher cargo weights.

The documentation of exports is just as important as the goods you are exporting. Faulty information or incomplete documentation can lead to delays in transporting goods to their destination. Forty-six separate documents are the average for one shipment of goods being sold abroad. Many countries have laws that must be followed when completing export forms. A freight forwarder, a specialist in this area of export- ing, can often provide the necessary documentation for shipping your goods.

Every country varies as to the number and kind of documents that are necessary for importing different goods. The Department of Commerce's district office closest to you or your forwarder can provide you with up-to-date and specific information on export documentation.

15

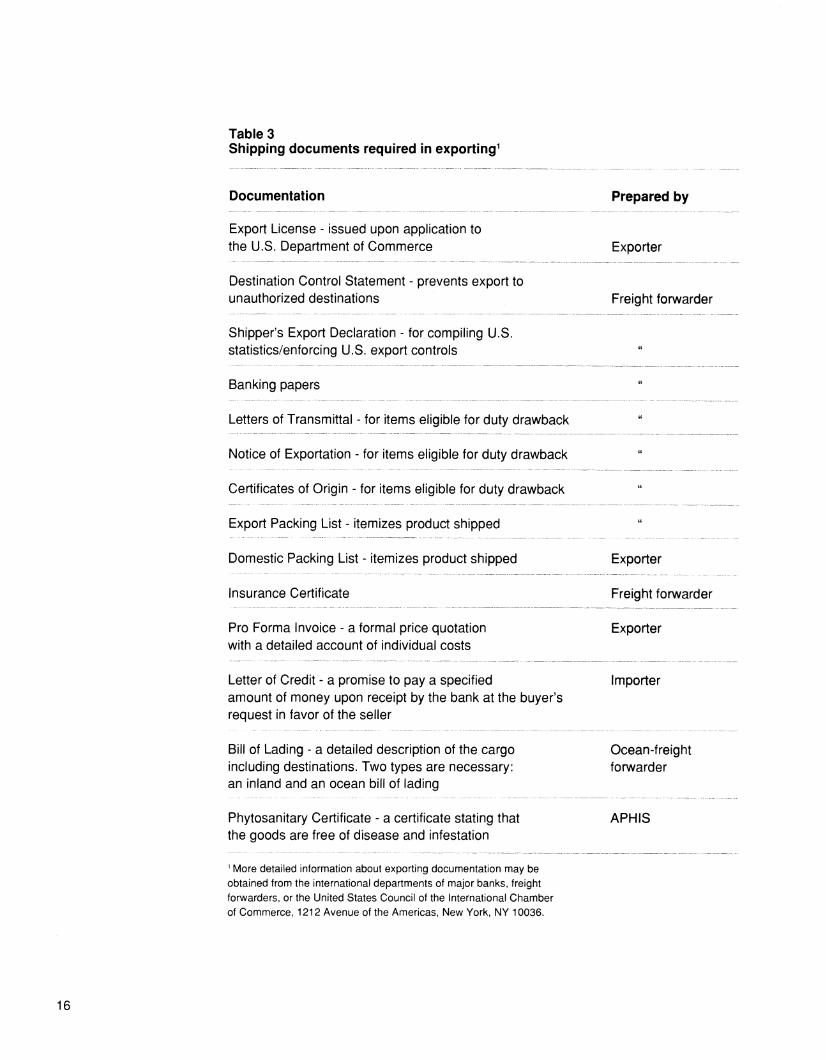

Table 3 Shipping documents required in exporting^

Documentation Prepared by

Export License - issued upon application to the U.S. Department of Commerce Exporter

Destination Control Statement - prevents export to unauthorized destinations Freight forwarder

Shipper's Export Declaration - for compiling U.S. statistics/enforcing U.S. export controls i(

Banking papers "

Letters of Transmittal - for items eligible for duty drawback »

Notice of Exportation - for items eligible for duty drawback

Certificates of Origin - for items eligible for duty drawback "

Export Packing List - itemizes product shipped t(

Domestic Packing List - itemizes product shipped

Insurance Certificate

Exporter

Freight forwarder

Pro Forma Invoice - a formal price quotation with a detailed account of individual costs

Letter of Credit - a promise to pay a specified amount of money upon receipt by the bank at the buyer's request in favor of the seller

Bill of Lading - a detailed description of the cargo including destinations. Two types are necessary:

Exporter

Importer

Ocean-freight forwarder

an inland and an ocean bill of lading

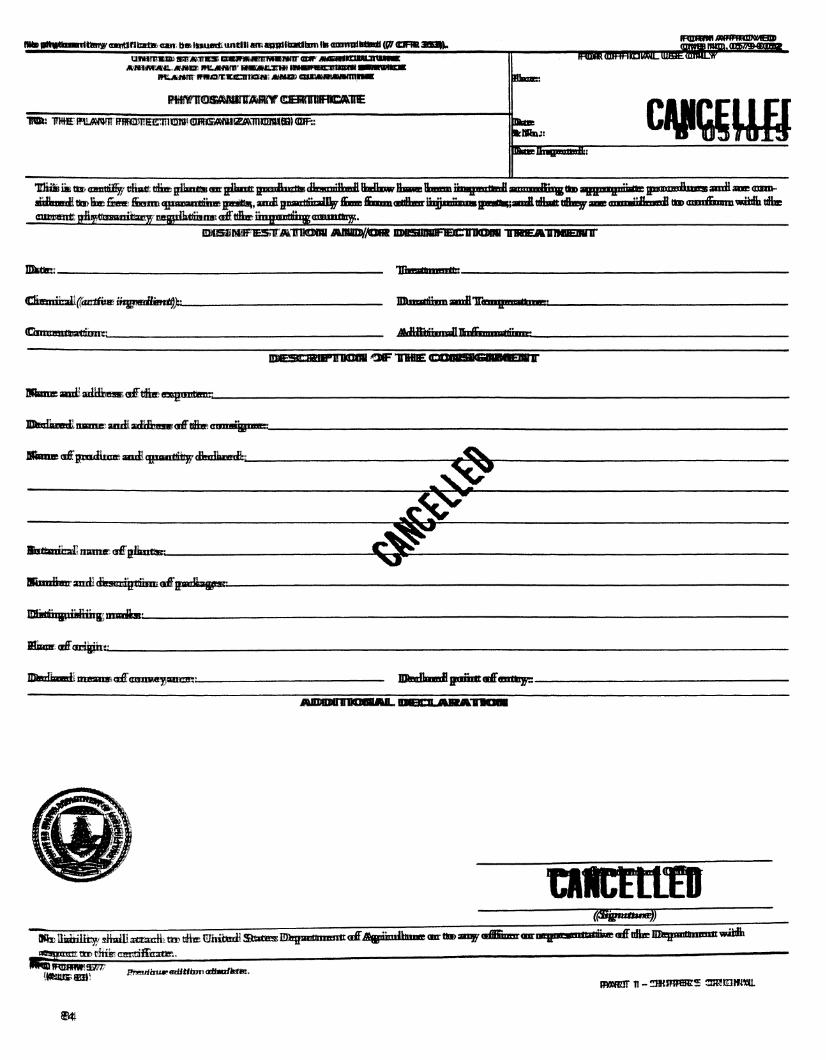

Phytosanitary Certificate - a certificate stating that the goods are free of disease and infestation

^ More detailed information about exporting documentation may be obtained from the international departments of major banks, freight forwarders, or the United States Council of the International Chamber of Commerce, 1212 Avenue of the Americas, New York, NY 10036.

APHIS

16

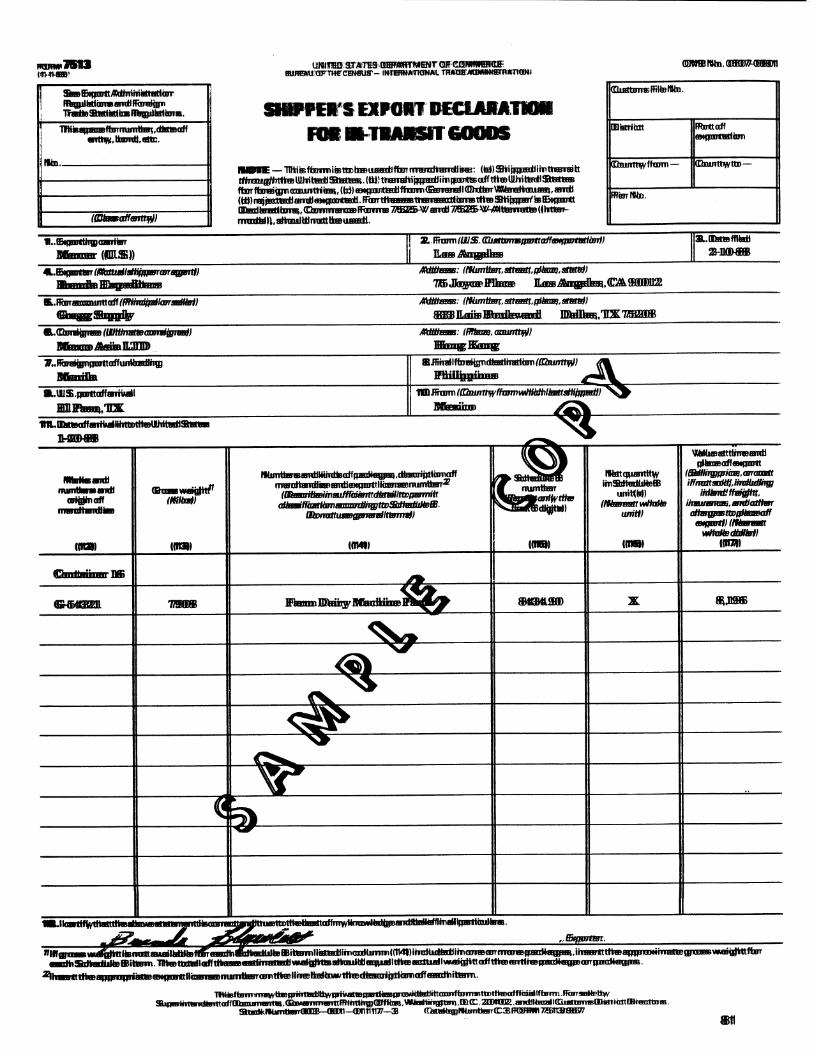

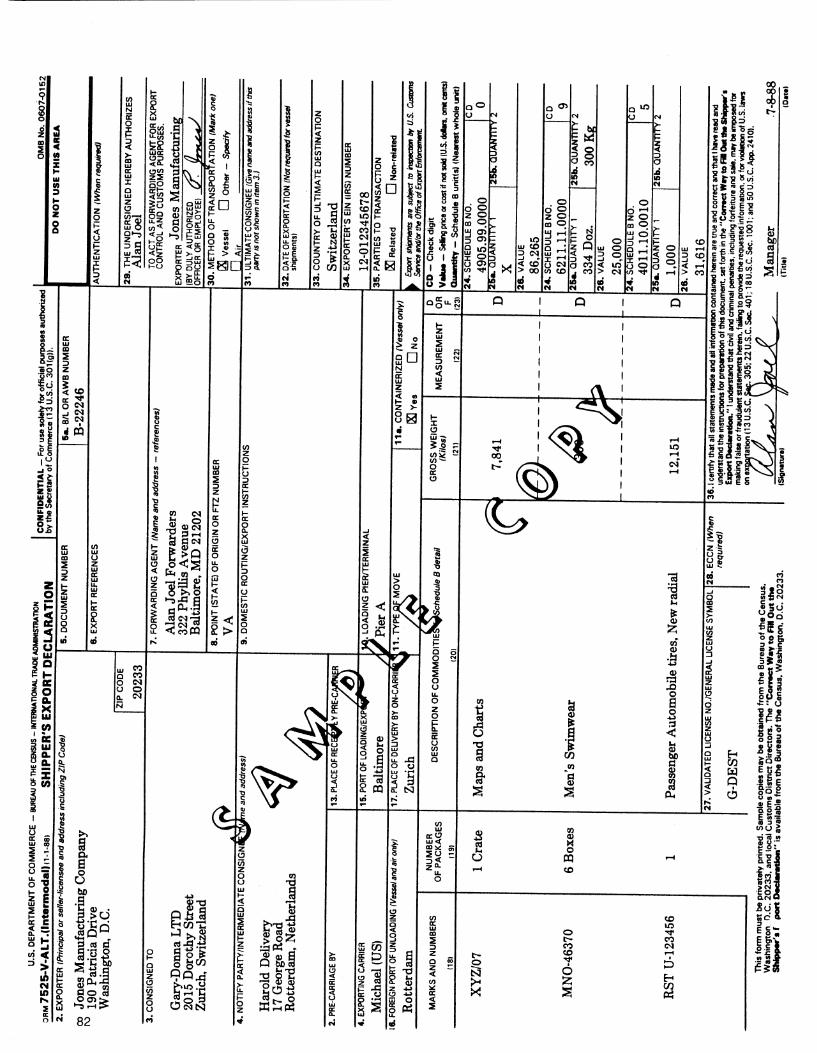

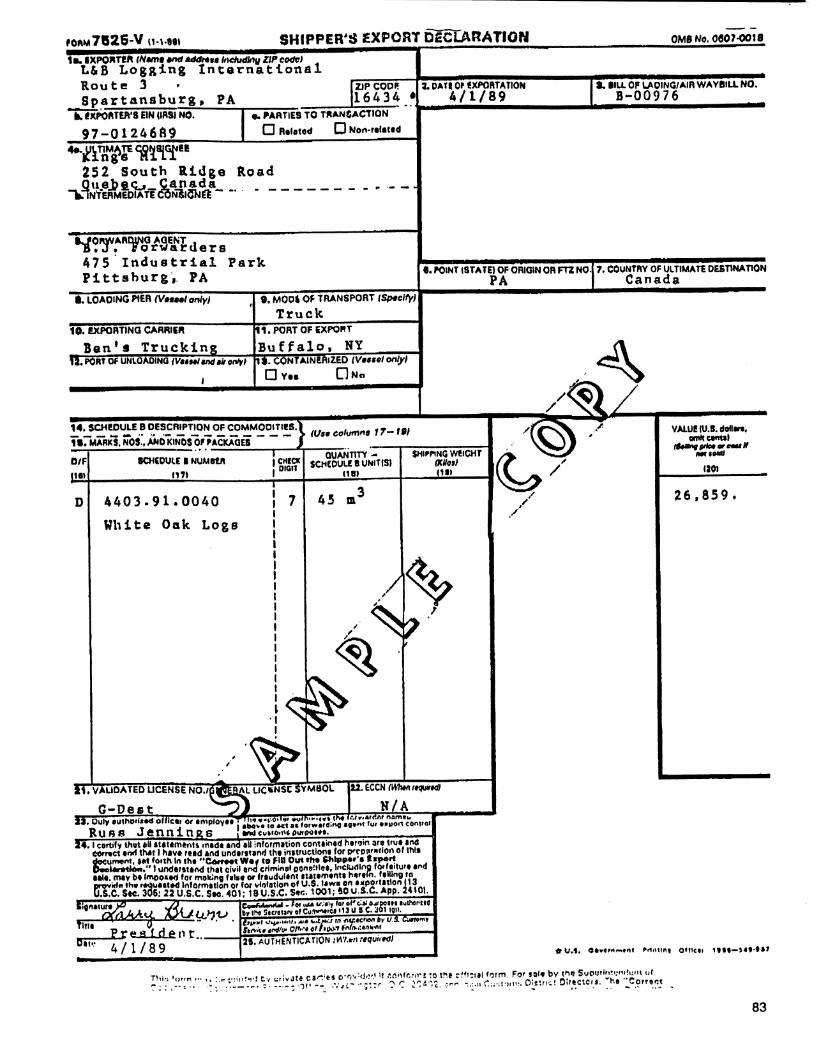

Shipper Export ^ The Shipper Export Declarations (SED's) are very important documents that are used Declarations (SED's) ^^^ ^^^ly ^^ ¡dentify cargo, but to determine the official U.S. export statistics as well.

These trade statistics are used throughout the Government and industry organizations and distributed to the industry. The importance of accurate information on the export declarations can not be understated.

Forms:

The forms used for export declarations are: SED Form 7525 or 7525-V-Alternate. These forms and continuation sheet must be copied. Sample copies may be obtained from the Bureau of the Census, Washington, DC 20233. When privately printing SED's, the forms must conform in every respect to the official forms in size, wording, color (black ink on buff paper for Form 7525-V), weight of paper stock (not less than 16 nor more than 20 pounds commercial substance), and arrangement, including printing the Office of Management and Budget Approval Number in the upper right-hand corner of the face of the form. The alignment of form 7525-V corresponds with air waybills and other vertically oriented documents while form 7525-V-Alternate corresponds with the ocean bill of lading and other horizontally oriented documents. (See sample documents in appendix II.) However, either form may be used regardless of the method of transportation or destination.

The Bureau of the Census has a program. Automated Reported Program, to which exporters, carriers, or freight forwarders may submit monthly reports by computer (tape, floppy disk, or direct transmission). For further information on this program, contact the Automated Data Reporting Branch, Department of Commerce, Suitland, MD 22222. Tel. (301) 763-7700.

When Required:

SED's are required for nearly all shipments (see section 9 for exemptions) from the United States, Puerto Rico, U.S. or Puerto Rican Foreign Trade Zones (FTZ), and the U.S. Virgin Islands. SED's are not required for shipments from the United States or Puerto Rico to U.S. possessions, except to the U.S. Virgin Islands or from a U.S. possession to the United States or Puerto Rico.

Number of Copies Required:

a) One copy for shipments to Canada, Puerto Rico, and the U.S. Virgin Islands;

b) One copy for exports through the U.S. Postal Service; and

c) Two copies for all other shipments.

Additional copies may be required for export control purposes by the International Trade Administration, other government agencies (when authorized), customs direc- tors, or the local postmaster.

Preparation:

The SED must be prepared in English in a permanent medium (ink, typewritten, etc.) with the original signed (a signature stamp is acceptable) by the exporter or an author- ized agent of the exporter. The agent must be authorized by a power-of-attorney or item #23 on form 725-V (an informal power-of-attorney) must be completed.

17

Requirement for Separate SED's:

Separate SED's are required for each shipment from one exporter to one importer on a single carrier (including each rail car, container, or other vehicle). However, customs directors may waive this requirement if multiple car shipments are made under a single loading document and cleared simultaneously. Also, merchandise requiring a validated export license shall not be reported on the same SED with goods moving under a general license.

Presentation:

a) Postal shipments—SED's must be delivered to the postmaster when the packages are mailed.

b) Pipeline shipments—SED's must be submitted to the customs director within 4 working days after the end of the calendar month.

c) All other shipments—SED's must be delivered to the exporting carrier before exporting.

d) Exporting carriers are required to file SED's and manifests with customs.

e) Shipments from an interior point—SED's may accompany the goods being transported to the exporting carrier or the port of exportation, or they may be delivered directly to the exporting carrier.

f) Shipments exempt from SED filing requirements—a reference to the exemption must be noted on the bill of lading, air waybill, or other loading document for verification that no SED is required.

Corrections:

Corrections, amendments, or cancellations of data may be made directly on the SED if it has not already been sent to the Bureau of the Census. If the SED has been sent to the Bureau, any corrections, cancellations, or amendments must be filed on a copy of the original SED but marked correction copy and filed with the customs director or the postmaster where the declaration was originally presented.

Retention of Siiipping Documents:

Three years is the usual length of time that the Bureau of the Census, U.S. Customs Service, and the International Trade Administration may require exporters or their agents to produce copies of shipping documents.

Exemptions:

a) Shipments (excluding postal shipments) where the value of the goods under each schedule B number or HS code is $1,500 or less and for which a validated export license is not required and when shipped to countries not prohibited by the Export Administration Regulations.

18

b) Shipments through the U.S. Postal Service that do not require a validated export license: (1) when the goods are valued $500 or less, (2) if either one of the parties is not a business concern, or (3) the shipment is not for commercial consideration.

c) In-transit shipments not requiring a validated export license and leaving for a foreign destination by means other than by ocean vessel.

d) Shipments from one point in the United States to another point by routes passing through Canada or Mexico, and shipments from one point in Canada or Mexico to another point by routes passing through the United States.

Administrative Provisions:

SED's and the information that is written on them are confidential and are exempted from the Freedom of Information Act. SED's are only for official purposes authorized by the Secretary of Commerce in accordance with 13 U.S.C Section 301. Neither Commerce nor the Census Bureau will give out the information to anyone except the

exporter or his or her agent.

Information from SED's (except common information—that is, information that is on both the SED and the manifest) may not be copied from manifests; other exporters may not give SED's or their information to anyone for unofficial purposes (for example, if the customer requests a copy of the SED).

Copies of the SED's may be supplied to exporters or their agents when they are needed to comply with official requirements; for instance, authorization for export, export control requirements, or USDA requirements for proof of export in connection with subsidy payments. These copies will be stamped certified and are not for any other use and may not be reproduced in any form.

When the Secretary of Commerce or a delegated person determines that withholding information on a particular SED is contrary to "national interest," the Secretary or delegate may make the information available while taking safeguards and precautions

as deemed appropriate.

A SED presented for export is a representation by the exporter that all statements and information follow the export control regulations. The product described on the SED must be described the same on all applicable licenses.

It is unlawful to knowingly make false or misleading representations for exportation. This is a violation of the Export Administration Act 50 U.S.C App 2410. It is also a violation of export control laws and regulations to be connected in any way with an

altered SED.

Goods that have been, are being, or for which there is probable cause to believe they are intended to be exported in violation of the Export Administration Act are subject to seizure, detention, condemnation, or sale under 22 U.S.C. section 401.

To knowingly make false or misleading statements relating to information on the SED is a criminal offense subject to penalties in 18 U.S.C. section 1001.

19

Violations of the Foreign Trade Statistics Regulations (FTSR) are subject to civil penalties as authorized by 13 U.S.C. section 305.

Regulations:

Detailed information about the SED and its preparation is contained in the FTSR (15 CFR Part 30). Also, the FTSR should be consulted for special provisions under particular circumstances. Copies may be purchased from the Bureau of the Census, Washington, DC 20233. Information concerning export laws and regulations of the International Trade Administration is contained in the Export Administration Regula- tions, which may be purchased from the Superintendent of Documents, Government Printing Office, Washington DC 20402.

Reference Schedules

Schedule B—Statistical Classification of Domestic and Foreign Commodities from the United States. For sale by the Superintendent of Documents, U.S. Government Printing Office, Washington, DC 20402 and local U.S. Customs District Directors.

Schedule C—Classification of Country and Territory Designations for U.S. Foreign Trade. Free from the Bureau of the Census, Washington, DC 20233. Also included as part of Schedule B and USTSA.

Schedule D—Classification of Customs Districts and Ports. Free from the Bureau of the Census. Also included as part of Schedule B and USTSA.

Schedule K—Classification of Foreign Ports by Geographic Trade Area and Country. Also free from the Bureau of the Census.

Foreign Trade Statistics Regulations—For sale by the Bureau of the Census.

Exporting Checklist The following checklist is a general guide outlining the steps involved in completing an export shipment under a confirmed letter of credit (L/C). The actual procedure will vary according to the bank's financing arrangements and the services provided by the freight forwarders and steamship companies. The price basis (f.o.b., f.a.s., c.i.f., etc.) and the terms of sale agreed upon between the exporter and importer also will affect the procedures to follow in exporting. Check first with the international department of your bank and the freight forwarder to determine all financing and documentation requirements and procedures.

• U.S. exporter and foreign importer agree on the terms of the sale. • Importer applies for a letter of credit (L/C) at the foreign bank. • Foreign bank issues the L/C to the exporter's bank. • Importer sends a purchase order accompanied by a copy of the L/C to the exporter. • Exporter prepares the order for shipment, arranges for inland transportation of the

shipment to the port, and issues shipping instructions to a freight forwarder. • Exporter's freight forwarder selects a suitable vessel, contacts the outbound

steamship line office, and books space on a particular vessel. The freight forwarder also collects or prepares the exporting documents, including the inland bill of lading, ocean bill of lading (B/L), insurance, and phytosanitary certificates. (The exporter may arrange for marine insurance through a private insurance company.)

20

Freight forwarder pays the due bills from the outbound steamship line and transmits to the exporter the original ocean bill of lading, together with the bill covering the inland freight, the stevedoring costs, and the freight forwarder's services. Exporter prepares a "commercial set"—a negotiable bill of lading, a copy of the L/C, an invoice, a bill for the freight forwarder's charges, insurance certificates, and, if necessary, a customs invoice. The exporter sends the commercial set to the exporter's bank. Upon receipt and acceptance of the commercial set, the bank pays the exporter covering the shipper's invoice in accordance with the L/C issued by the importer's bank. The bank transmits the commercial set and a debit notice to the importer's bank for payment. The exporter or freight forwarder sends a non-negotiable copy of the bill of lading to the importer notifying that the cargo has been shipped. After the vessel has sailed, the outbound steamship line's office sends the manifest to the inbound steamship office, together with non-negotiable copies of the bills of lading, arrival notice, delivery receipt, and container list. Outbound steamship office submits to the U.S. Customs one non-negotiable ocean bill of lading copy with the shipper's export declaration. This must be accomplished within 4 working days of the vessel's clearance from the U.S. port. Depending on the terms of the sale and financing arrangements, the exporter may be liable for the shipment after the vessel has sailed. Check with the bank, freight forwarder, and insurance company to determine your rights, responsibilities, and liabilities, as well as the proper procedures to follow in completing the export sale.

21

Business Organization of Firms Involved In Exporting

"In House" The organization of the firm and how your wood products are sold overseas are related and depend on several factors including the size of the company, productive capacity, types of wood products and degree of processing, previous exporting experi- ence, and business conditions overseas. "In-house" organization of the business involves direct selling of wood products by the U.S. producer to the foreign importer. The producer is usually responsible for shipping the product overseas.

Traditional and customary marketing and business practices in a foreign country will dictate how the products will be sold. Depending on the country, direct selling may involve working with foreign sales representatives, agents, or distributors. For ex- ample, agents are very active in the wood products trade in the United Kingdom and other European countries. In Japan, trading companies are the primary contacts.

"In-house" organization will provide the company greater control over the export marketing procedures for the firm's products. In general, there are higher start-up costs and fewer economies of scale under this organizational structure than with the others described below.

Export Management Companies (EMC's or agents)

Export Trading Companies (ETC's)

Export Merchants (EM'S)

EMC's are generally small, closely held companies which represent wood products manufacturers in export marketing. The EMC may represent a number of small, unrelated companies and provide benefits (economies of scale) relating to foreign sales, marketing missions, and scheduling or shipping products for export. The EMC often retains the identity of the manufacturer when dealing with foreign importers, whereas agents work under their own names.

The largest domestic barriers to exporting—lack of knowledge of foreign marketing, limited credit facilities, and legal restrictions in cooperating with other U.S. companies (antitrust violations)—may be hurdled by forming an export trading company (ETC). ETC's may assume the risks involved with international trade by taking title to the products and assuming responsibility for marketing and selling the products overseas.

One publication, the Export Trading Company Guidebook is available for sale from the Superintendent of Documents, U.S. Government Printing Office, Washington, DC 20402. Additional assistance may be obtained from the Office of Export Trading Company Affairs, International Trade Administration, U.S. Department of Commerce, Washington, DC 20230. Tel. (202) 377-5131.

Similar to an ETC, an export merchant (EM) may take title to a producer's goods and be responsible for selling to the foreign importer. The advantages of using an export merchant include:

1. Wood products are sold to an export merchant domestically. Producers do not need to be familiar with foreign business practices—this is the responsibility of the EM.

2. The EM may handle all intermediate processing and handling functions, such as pressure treatments or kiln-drying of lumber prior to export.

3. The EM may serve as a "sorter" or distribution yard for lumber and other products. This permits lumber to be regraded specifically for export and specialty markets. Lower volume, high-quality products may become more marketable as a result of using an EM.

22

Foreign Sales Corporation (FSC)

4. EM'S may become familiar with the operation of small lumber mills and wood producers and may provide valuable assistance in producing wood products for the export market.

Under the Foreign Sales Corporation (FSC) Act of 1984, an FSC is a corporation established in a foreign country or U.S. possession, excluding Puerto Rico, which may obtain a tax exemption on a portion of the earnings generated by the sale or lease of export property and the performance of some services. As a general rule, 15 percent of the profits from qualifying export transactions are treated as tax-free income.

An FSC program was intended to replace the Domestic International Sales Corpora- tion (DISC) program which has been interpreted by members of the councils of the General Agreement of Tariffs and Trade (GATT) as an illegal tax subsidy for exports.

FSC's cannot provide long-term tax deferrals and retention of profits to secure tax benefits. Rather, FSC's obtain tax exemptions on approximately 30 percent of the FSC foreign trade income if the FSC buys from independent suppliers—a smaller percent is given if parent corporations are the suppliers. Special administrative pricing rules apply if the FSC purchases from related suppliers.

An FSC must be incorporated and have its main office in a foreign country or U.S. possession, including the U.S. Virgin Islands, American Samoa, Guam, and the Northern Marianas. Additionally, an FSC must have at least one director who is not a U.S. resident and maintain a set of books at its main off-shore office. It cannot have more than 25 shareholders and cannot have any "preferred" stock. An "election" to become an FSC must be filed with the Internal Revenue Service (1RS).

An FSC may be incorporated in the following countries and U.S. possessions:

American Samoa France New Zealand Austria Germany Northern Marianas Islands Barbados Grenada Norway Belgium Guam Pakistaan Canada Iceland Philippines Cyprus Ireland South Korea Denmark Jamaica Sweden Dominica Malta Trinidad and Tobago Egypt Morocco U.S. Virgin Islands Finland Netherlands

When selecting a location for the FSC you should take into account that the 1RS will not allow foreign tax credits for foreign taxes imposed on the FSC's qualified income. Because of this, most FSC's are incorporated in the U.S. Virgin Islands.

Small exporters may establish either a "small" FSC or an "interest-charge" FSC depending on the level of export income. Small FSC's, «with gross export income of $5 million or less, have less stringent rules to meet.

23

FSC's can be formed by manufacturers, nonmanufacturers, and export groups. They can function as principals, buying and selling for their own account, or as commission agents. The FSC may be related to a manufacturing parent company or can be an independent merchant or broker. Commission agents are required to perform specific activities with respect to the export sale.

Other management activities must be performed at the offshore location. For further information about FSC's, jointly-owned FSC's, minimal foreign presence FSC's, small business FSC's, and export trading companies, contact: Office of Trade Finance, U.S. Department of Commerce, Room 4420, 14th and Constitution Avenue NW., Washing- ton, DC 20230. Tel. (202) 377-3277.

24

Export Market Information and Assistance

U.S. Department of Agriculture

United States Government

Foreign Agricultural Service

The Foreign Agricultural Service (FAS) of the U.S. Department of Agriculture is responsible for developing, maintaining, and expanding export markets for U.S. agricultural commodities—including solid wood products. FAS provides foreign market information, works to gain foreign market access for U.S. farm, food, and forest products, and cooperates with U.S. nonprofit trade associations in conducting market development activities in overseas markets.

Overseas Offices—FAS represents U.S. agriculture overseas through a network of agricultural counselors, attaches, and trade officers in 96 foreign posts covering 110 countries. The staff supervises market development activities, reports to FAS/Wash- ington, and alerts the U.S. trade to foreign market opportunities and competition.

The U.S. agricultural counselor/attache office is in frequent contact with foreign buyers and overseas representatives of U.S. firms and associations, and helps U.S. agricul- tural exporters, associations, and allied groups establish contacts with government officials and the foreign trade. In addition, 15 Agricultural Trade Offices (ATO's) have been opened in Algiers, Baghdad, Beijing, Caracas, Guangzhou (Canton), Hamburg, Istanbul, Jeddah, Lagos, London, Manama, Seoul, Singapore, Tunis, and Tokyo. These trade offices serve as a one-stop service center with facilities for trade repre- sentatives, nonresident private trade groups, and others engaged in exporting and importing U.S. agricultural commodities.

Annual reports on wood products production, marketing, and trade for 30 selected foreign markets are also available on an annual subscription basis. The markets are:

Australia Austria Belgium Brazil Burma Canada Chile China Cote d'Ivoire Denmark Egypt

Finland France Germany,

Federal Republic Indonesia Italy Japan Korea, South Malaysia Mexico Netherlands

New Zealand Philippines Spain South Africa Sweden Taiwan United Kingdom U.S.S.R. Venezuela

The annual reports are prepared by FAS agricultural counselors, attaches, and trade officers overseas. To order a subscription for the scheduled reports, voluntary reports, and report updates contact the Reports Officer/FAS, USDA, Room 6078-South Build- ing, Washington, DC 20250-1000. Tel. (202) 382-8924.

Market Reports—FAS issues quarterly circulars on the world supply and demand situation for wood products on an annual subscription basis. The reports include summaries of U.S. exports of logs, lumber, plywood, veneer, wood chips, and a variety

25

of other softwood and hardwood products. Foreign wood products production, supply, and distribution data are also provided.

The charge for four issues is $10.00 for domestic mailing and $15.00 for foreign mailing. For further information, contact FAS/lnformation Division, Room 4644-South Building, USDA, Washington, DC 20250-1000. Tel. (202) 382-9445.

Export Services—Through FAS services, agricultural exporters can keep abreast of foreign market development opportunities with marketing research reports, trade leads, product publicity, and listings of prospective foreign importers. FAS is working to expand its telecommunications link with its agricultural trade offices overseas in an effort to increase the volume and timeliness of trade leads available to U.S. agricultural exporters.

FAS serves as the liaison between U.S. companies and foreign importers seeking U.S. wood and other agricultural products. FAS works to help U.S. producers introduce products in new markets and further expand established markets.

FAS's agricultural counselors, attaches, and trade officers transmit market information, trade, and economic statistics electronically to FAS offices in Washington, DC. U.S. companies can subscribe to the following export services:

1. Trade Leads provide trade leads in overseas markets. They are distributed in three ways:

a) Electronic Dissemination. Electronic access to trade leads is available on a daily basis via computer information services that offer the leads on electronic bulletin boards. To access the trade inquiries you need a minicomputer with a modem and communications software. Listed below are the companies to contact directly to receive this service.

Agridata Resources, Inc. Dialcom, Inc. 330 East Kilbourn 600 Executive Blvd., Suite 150 Milwaukee, Wl 53203 Rockville, MD 20852 Tel. (800) 558-9044 Tel. (301 ) 770-4280

Master Productions Intellibanc Corporation 7300 Candletree Lane, Suite 21 2214 Torrance Blvd., Suite 101 Lincoln, NE 68506 Torrance, CA 90501 (402) 489-2183 (213) 618-9597

California Agricultural Technology Institute Maple and Shaw Avenues Fresno, CA 93470-0115 (209) 294-4872

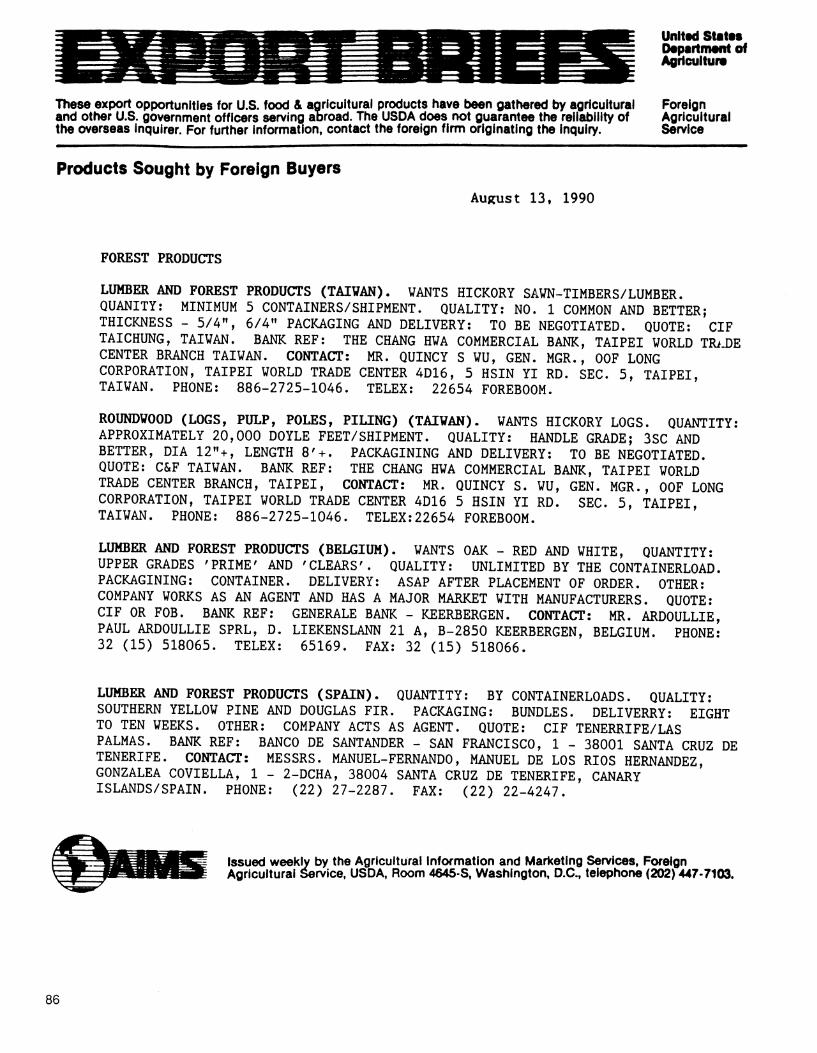

b) Export Briefs is a weekly bulletin of all trade leads received during the previous week. Export Briefs also includes highlights of upcoming trade shows, foreign trade developments, and changes in trade policy issues, product standards, and labeling

26

information. Information in each inquiry is identical to that in the electronic access. The subscription fee is $75 per year.

c) The Journal of Commerce, a daily paper, publishes export opportunities supplied by the U.S. Department of Agriculture regularly in its column "Agricultural Trade Leads." For information, contact The Journal of Commerce, 110 Wall Street, New York, NY 10005. Tel. (800) 221-3777; in New York: (212) 425-1616.

2. Foreign Buyer Listings are on a database that includes 15,000 foreign firms inter- ested in importing agricultural (including wood) products. Each listing may be format- ted (a) by specific commodity for the entire world; (b) by specific country for all com- modities; and (c) by specific commodity and country. These lists provide company and contact name, address, telephone, and telex number. The charge for each list is $15.

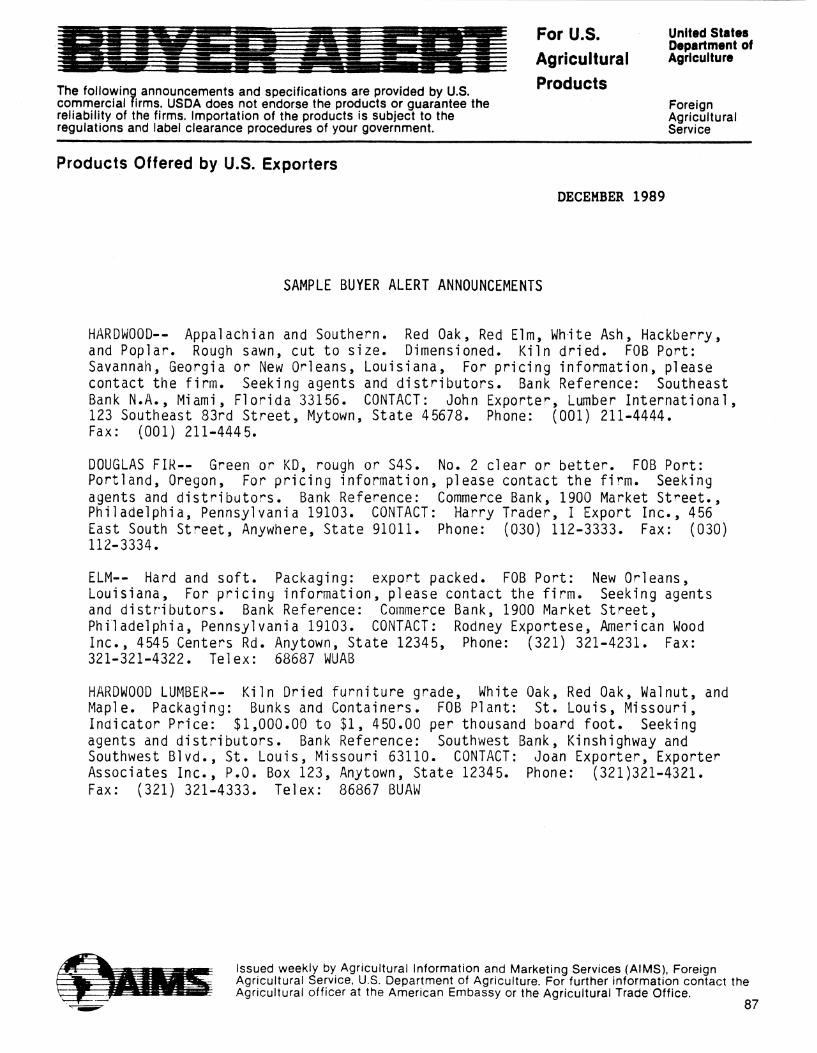

3. The Buyer Alert Notice uses high-speed telecommunications links, to forward specific information about the products you want to sell to foreign importers in 50 countries. This product publicity service is offered at no charge.

For further information on trade leads. Export Briefs, Foreign Buyer Lists, or the Buyer Alert contact: Foreign Agricultural Service, Room 4649-S, U.S. Department of Agricul- ture, Washington, DC 20250-1000. Tel. (202) 447-7103.

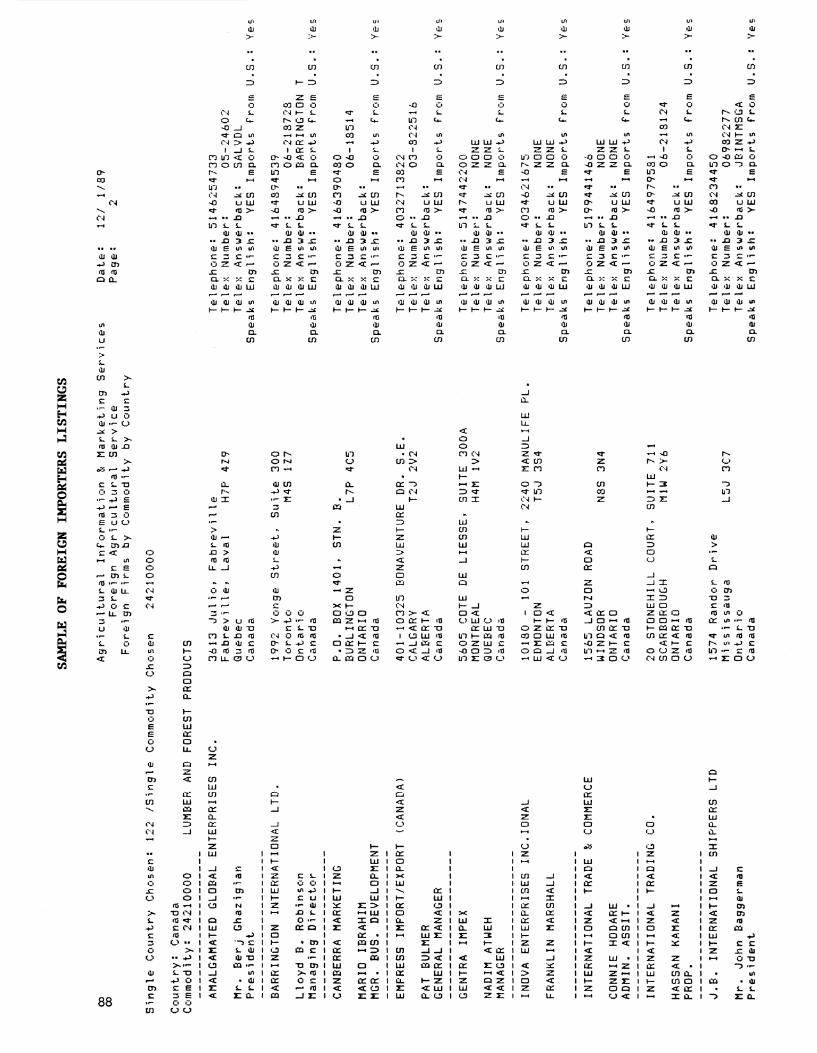

Refer to appendix III for examples of Export Briefs, Foreign Buyer Listings, and the Buyer Alert.

Office of Transportation

USDA's Office of Transportation (OT) provides the following services:

• Technical Assistance—OT publishes export handbooks, directories, and statistical news reports; sponsors export seminars; and participates in technical exchanges with other countries.

• Economic Studies—OT analyzes such topics as the future transportation needs of the U.S. agricultural export community, the impact of various cargo preference initiatives on agricultural shippers, and the feasibility of a transportation-oriented export trading company.

• Technological Research—OT works to develop better procedures for shipping agricultural commodities (including forest products), evaluates equipment needs, and analyzes and tests transportation packaging techniques.

For further information contact the USDA Office of Transportation, Washington, DC 20250-4500. Tel. (202) 653-6275.

Animal and Plant Health Inspection Service

USDA's Animal and Plant Health Inspection Service (APHIS) actively participates in international programs to protect against the spread of plant and animal pests and diseases. Many foreign countries require that shipments of wood products be accom- panied by phytosanitary certificates, issued by APHIS at the request of the shipper, certifying that the products conform to foreign quarantine import requirements.

27

For example, the European Community (EC) requires a phytosanitary certificate for U.S. shipments of veneer logs certifying that the logs have been fumigated with methyl bromide according to approved EC treatment schedules and procedures. (See appen- dix 2 for an example of a phytosanitary certificate.)

Inspection is handled by Federal and State government cooperators and the inspec- tions are normally not valid if conducted more than 14 days prior to the export of the commodity. The exporter must make written application for inspection and make the commodity available for physical inspection.

Certification is recognized by foreign plant protection services and by regional plant protection organizations.

Phytosanitary certificates are not issued to satisfy letter of credit or other commercial contract terms and are not certifications of grade or quality. Criteria on foreign country plant import requirements may be obtained by contacting: Protection and Quarantine (PPQ), APHIS, USDA, at ports of export, or by writing PPQ, APHIS, USDA, Port Operations, Room 633, Federal Building, Hyattsville, MD 20782. Tel. (301) 436-8537.

Forest Service

USDA's Forest Service conducts research and analysis of U.S. timber supply, de- mand, and wood products trade. The Forest Service experiment stations and the forest products laboratory can provide useful information and research on exporting.

The Southern Forest Experiment Station handles research involving exports of wood products from the southern United States and on the costs of exporting. Contact: Principal Economist, USFS/SFES, Room T-10034, 701 Loyola Avenue, New Orleans, LA 70114. Tel. (504) 589-6651 ; Fax: (504) 589-3961.

The Pacific Northwest Forest Experiment Station handles macroeconomic modeling of U.S. and international markets of wood products. Contact: Principal Economist, USES/ PNWFRES, P.O. Box 3890, Portland, OR 97208. Tel. (503) 231-2193; Fax: (503) 326- 2272 or (503) 326-3096.

The Northeastern Forest Experiment Station handles research on U.S. hardwood exports. Contact: William G. Luppold, Project Leader, Forestry Scientist Laboratory, Box 562-B, Princeton, WV 24740. Tel. (304) 425-8107.

The Northeastern Area State and Private Forestry office provides technical assistance on the exporting of forest products. Contact: Director, USFS/NA, Five Radnor Corpo- rate Center, Suite 200, 100 Madsen Ford Road, Radnor, PA 19087.

The Southern Region State and Private Forestry Office provides technical assistance on the exporting of forest products. Contact: R-8, S&PF, 1720 Peachtree Road, NW., Atlanta, GA 30367. Tel. (404) 347-7930; Fax: (404) 347-4488.

The Forest Products Laboratory conducts research and provides information on foreign and domestic woods and wood products. Contact: Information Office, Forest

28

Products Laboratory, One Gifford Pinchot Drive, Madison, Wl 53705-2398. Tel. (608) 231-9200; Telex: 7400032; Fax: (608) 231-9592.

U.S. Agency for International Development (AID)

The Agency for International Development (AID) publication, Export Opportunities With Agency for International Development, explains AID'S programs. The AID Docu- ments Kit for Export Suppliers is another useful publication. Both can be obtained by writing to the Office of Business Relations, AID, Washington, DC 20523. Additional AID publications are available on a subscription basis including: AID Financial Export Opportunities (SBC), AID Procurement Information Bulletins (PIB), or AID Small Business Memo (SBM).

U.S. Department of Commerce

The International Trade Administration (ITA) of the U.S. Department of Commerce provides a wide range of services and programs to assist U.S. firms in developing export markets. The best point of contact for U.S. firms is their local Department of Commerce district office, of which there are 48 across the United States. These offices are run by the division of ITA known as the U.S. and Foreign Commercial Service. For those companies operating from foreign locations, there are 66 commercial offices, which are part of this same network, located in embassies and consulates in countries comprising more than 95 percent of the world market for U.S. products.

For information about a specific country, contact the appropriate country desk officer at the ITA. A list of ITA desk offices is provided in appendix V. U.S. and Foreign Com- mercial Service District Offices are listed in appendix VI.

The services provided by the Office of Trade Information Services, ITA, are listed below:

• Agent Distributor Service is handled through the district offices. U.S. commercial officers overseas locate interested and qualified representatives on behalf of a U.S. firm. The commercial officer prepares a report identifying up to six foreign prospects that have examined the U.S. firm's product literature and have expressed interest in representing the company. There is a charge per market or specific area.

• The Trade Opportunities Program (TOP) Notice Service offers individual messages on current foreign trade leads detailing specifications, quantities, end-use, delivery, and bid deadlines for the products requested by the foreign buyer. TOP'S are available only electronically via the Economic Bulletin Board. To subscribe, contact the National Technical Information Service (NTIS) at (307) 487-4630, or write to the NTIS at 5285 Port Royal Road, Springfield, VA 22161. The registration fee now is $25 and gives the user 2 hours of connect time. After the initial 2 hours, the user is charged 10 cents per minute of connect time.

• Customized Export Mailing Lists (EML) provide profile information which allows the subscriber to identify only the most relevant potential contacts. Gummed labels for direct mailings are also available. The cost for this service is $10 for the basic fee and 25 cents for each name.

• International Market Research (IMR) Surveys are organized under foreign country/ product categories and contain statistics and analysis of trade, information on end- users, purchasing patterns, marketing practices, trade restrictions, and key contacts in Government purchasing agencies and other organizations. IMR's cost $50 to

29

Office of the United States Trade Representative

$200 and range up to 400 pages in length. These are available through the district offices via the Commercial Information Management System (CIMS).

• World Traders Data Reports (WTDR) provide background material on individual foreign firms, giving information about each firm's reputation, credit worthiness, and its overall reliability and suitability as a trade contact for U.S. exporters. WTDR's are designed to help U.S. firms locate and evaluate prospective customers overseas. Information includes: name, address, key contact, number of employees, type of business, general reputation in trade and financial circles, year established, sales territory, and products handled. The cost is $100 per report.

• Commercial News, USA (CNUSA) assists U.S. companies in advertising the availability of new U.S. products in foreign markets and provides one method for t esting new markets. Under CNUSA short descriptions of the products are published in the monthly publication Commercial News, USA. For further information on these publications contact the Information Management Division at (202) 377-4203.

• The Office of International Major Projects (OIMP) helps qualified U.S. firms develop exports by obtaining early information on upcoming engineering and construction projects valued at no less than $3 million. The office provides information to prospective U.S. bidders and special assistance to U.S. companies to enhance their ability to compete for contracts. A monthly listing of major projects is available. OIMP has a staff of project officers who will work individually with firms to assist them in competing for individual project contracts. Contact: OIMP, U.S. Department of Commerce, Room 2015B, Washington, DC 20230. Tel. (202) 377-5225.

• The Office of Forest Products and Domestic Construction offers various reports on foreign and domestic developments, and is active in export services. Contact: Director, Room 4045, ITA, U.S. Department of Commerce, Washington, DC 20230. Tel. (202) 377-0382

• The Office of Trade Finance (OTF) offers counseling and advice on countertrade only. Contact: OTF, ITA, U.S. Department of Commerce, Room 4004, Washington, DC 20230. Tel. (202) 377-3277.