Embed Size (px)

DESCRIPTION

Eye Care Benefits Center What we do and why it is critical to Optometrists’ success. Colorado Optometric Association Coding & Billing Seminar October 23, 2005. ECBC: What we do for you. Managed Care Marketing Initiative Coding education, initiatives and support - PowerPoint PPT Presentation

Citation preview

1

Eye Care Benefits CenterWhat we do and why it is critical to

Optometrists’ success

Colorado Optometric AssociationCoding & Billing Seminar

October 23, 2005

2

ECBC: What we do for youManaged Care Marketing InitiativeCoding education, initiatives and supportMonitoring trends in health care and

third party payment systemsImprove exchange of information with

statesPosition Optometry with healthcare

stakeholders

3

Managed Care Marketing Initiative: What it is.

Expanding the presence of Optometry in medical plans administered by managed care organizations (MCOs) and employers

Convert MCOs who exclude or underutilize Optometrists to full inclusion in their networks

Persuade ERISA plans managed by large employers to reimburse for medical services provided by Optometrists

4

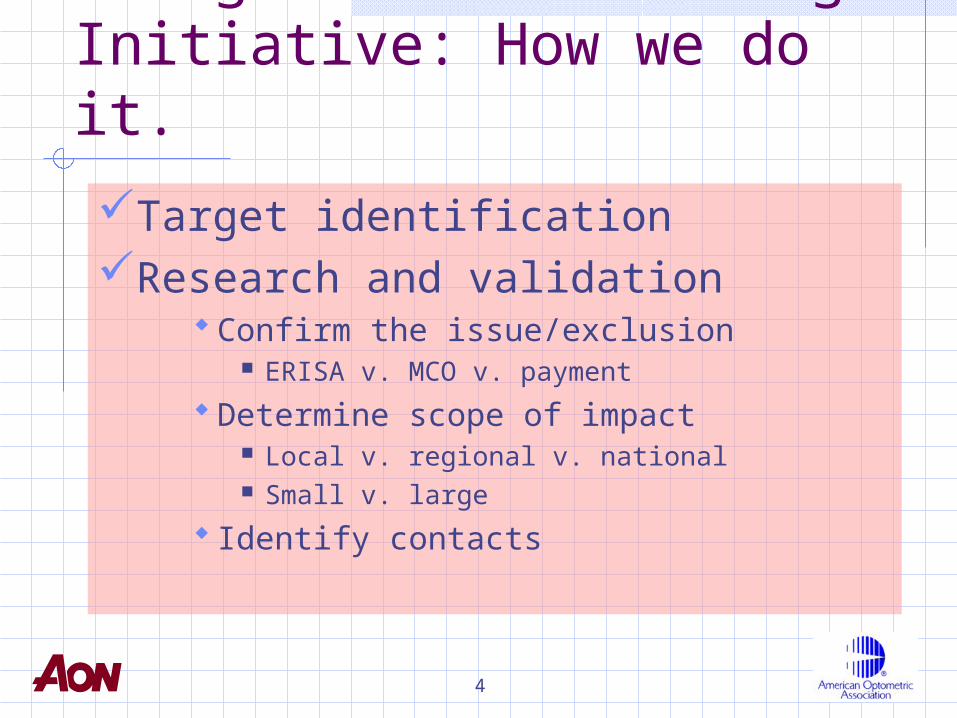

Managed Care Marketing Initiative: How we do it.

Target identificationResearch and validation

Confirm the issue/exclusion ERISA v. MCO v. payment

Determine scope of impact Local v. regional v. national Small v. large

Identify contacts

5

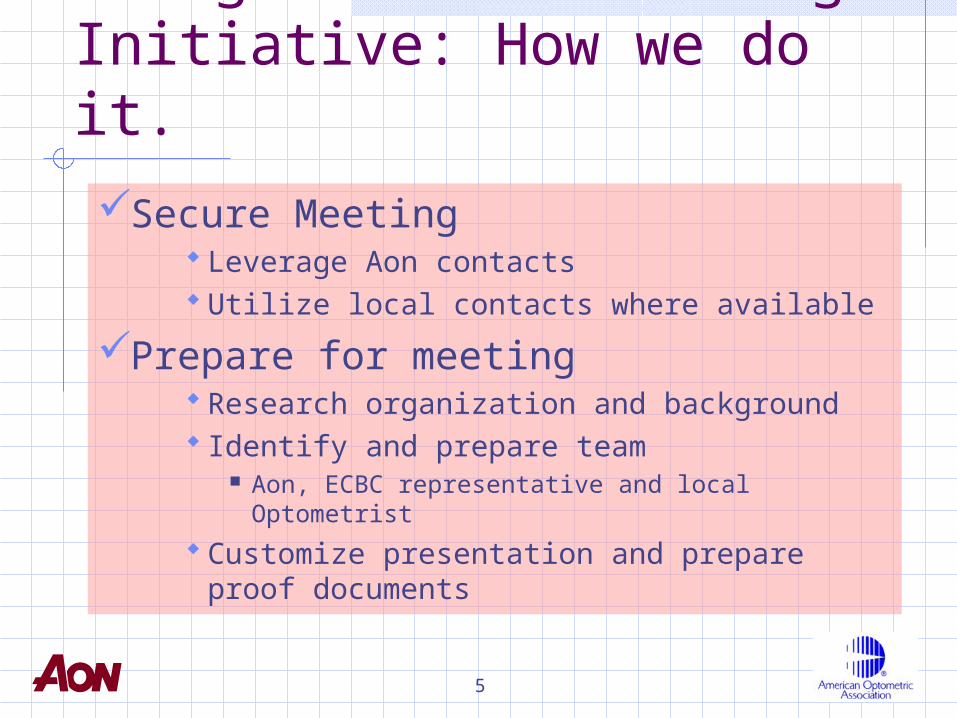

Managed Care Marketing Initiative: How we do it.

Secure Meeting Leverage Aon contacts Utilize local contacts where available

Prepare for meeting Research organization and background Identify and prepare team

Aon, ECBC representative and local Optometrist

Customize presentation and prepare proof documents

6

Well PreparedSeek to establish partnership

Understand MCO goals Demonstrate how Optometrists help meet

goalsThoroughly researchedVetted and proven documents

Power Point Presentation Emergency Room and cost studies Facts and relevant stories

Follow up

Managed Care Marketing Initiative: Style and Approach

7

Managed Care Marketing Initiative: Who does it

Eye Care Benefit Center volunteersTom Weaver DMD (AOA staff)Aon ConsultingLocal Optometrists from the

impacted State

8

Managed Care Marketing Initiative: Who does it

ECBC Dr. Mark Hennen, Chair Dr. Randy Fincher Dr. Kathleen Goff Dr. Greg Kraupa Dr. Mark Lee Dr. Doug Morrow Dr. Bill Rivard Dr. Joe Studebaker Dr. Mike Todd Dr. Rebecca Wartman

9

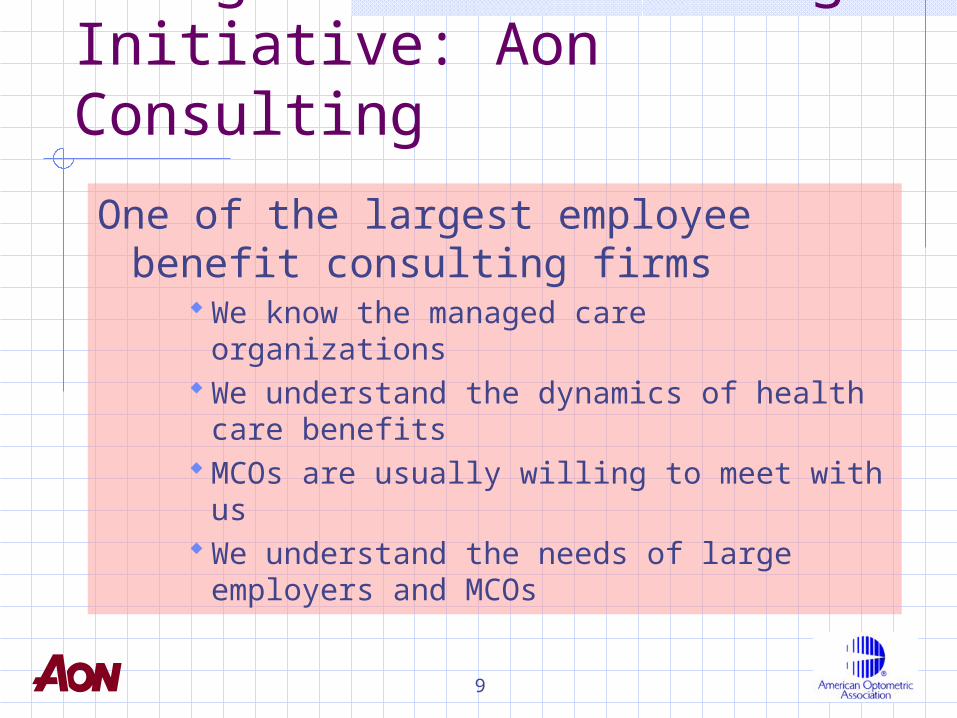

Managed Care Marketing Initiative: Aon Consulting

One of the largest employee benefit consulting firms

We know the managed care organizations

We understand the dynamics of health care benefits

MCOs are usually willing to meet with us We understand the needs of large

employers and MCOs

10

Managed Care Marketing Initiative: Targets

National, regional or large local PPOs

Large, multi-state employers (ERISA)

Medicare Advantage plans (newly added category)

Federal plans (cooperating with Federal Relations Committee-FRC)

11

Managed Care Marketing Initiative: SuccessesOptometrists now have access to reimbursed

medical care for 29.4 million additional patientsNotable Colorado Successes

12

Managed Care Marketing Initiative: Reasons for Exclusion

MCOs/Employers typically have excluded Optometrists due to: They do not understand what we do They think it will increase claims costs They do not want to spend resources

on credentialing “They always have done it this way”

13

Managed Care Marketing Initiative: Critical Success Factors

Liaison Program to identify targets ECBC representative maintains

contact with state appointed liaison Primary communication method

regarding managed care issues Ensures best effort by Optometry to

promote inclusion Liaison program needs full ED/state

leadership support and commitment

14

State Liaison Roles and Responsibilities

Knowledgeable of state managed care issues affecting all parts of the state

Familiar with coding issuesResponsive to/from ECBC and StateConnected to state leadershipWilling to attend national meetingsLongevity of service

15

Trends in Third Party PaymentContinued consolidation of payorsPay for performance

Driving quality to reduce cost increasesConsumer Directed Health Care

HSAs and HRAs Empowered consumer

Medicare Reform Prescription drug Advantage: HMOs and PPOs

16

What is driving change in health care?

COST!!!!

17

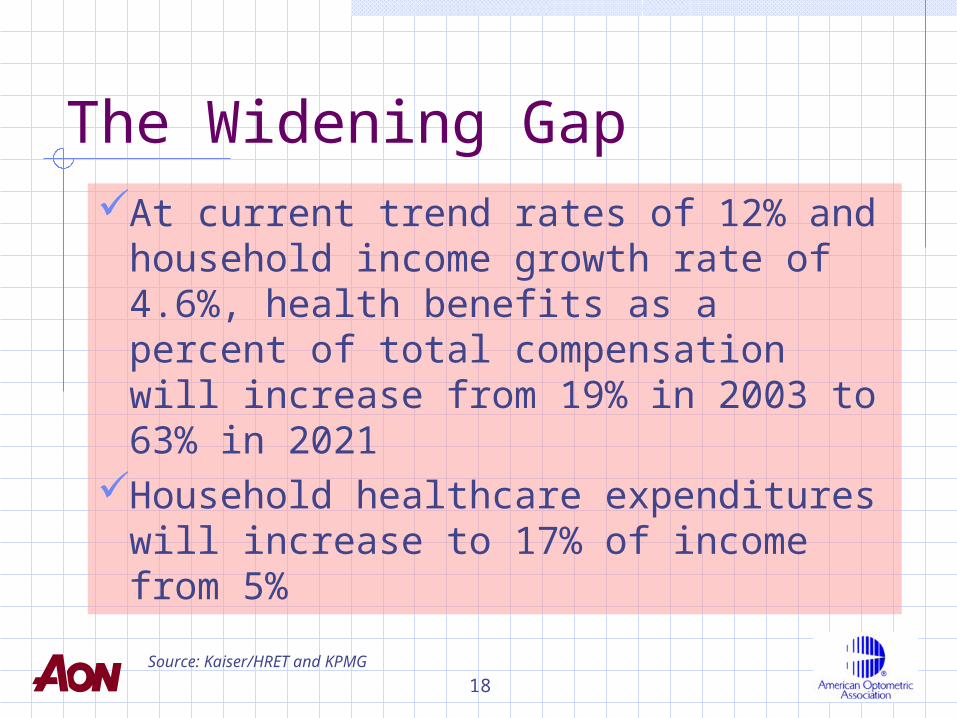

The Widening Gap

8.5%

5.3%

13.9%

12.0%

0.8%

10.9% 11.2%

0%

2%

4%

6%

8%

10%

12%

14%

16%

1988 1993 1996 1999 2001 2003 2004

Premiums Workers' Earnings Inflation

Increases in Premiums vs. Other Indicators

Source: Kaiser/HRET and KPMG

18

The Widening GapAt current trend rates of 12% and

household income growth rate of 4.6%, health benefits as a percent of total compensation will increase from 19% in 2003 to 63% in 2021

Household healthcare expenditures will increase to 17% of income from 5%

Source: Kaiser/HRET and KPMG

19

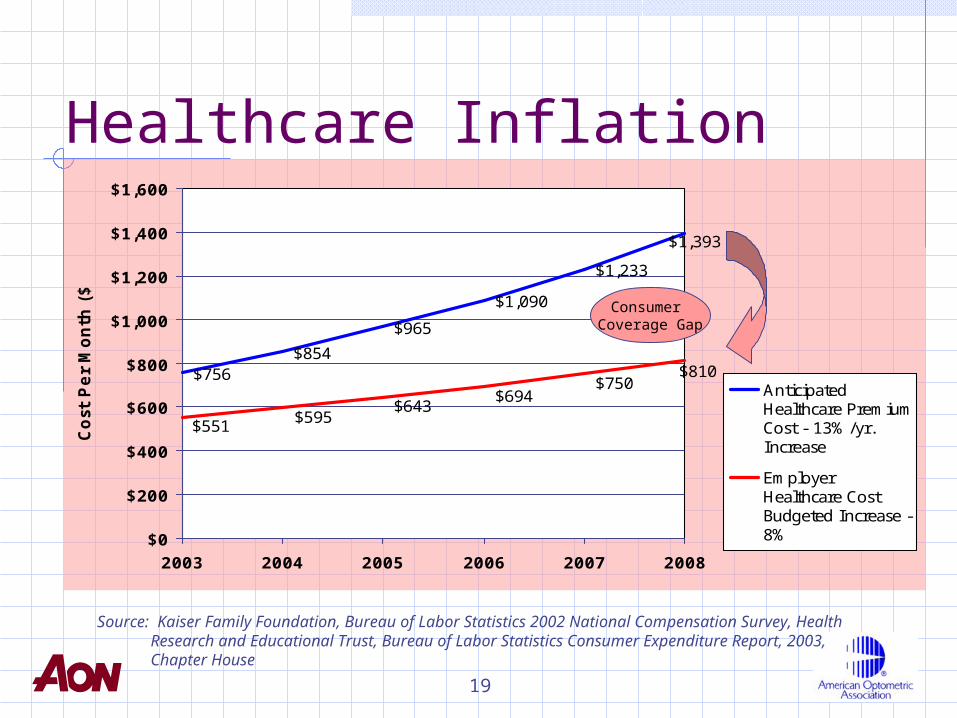

Healthcare Inflation

$756$854

$965

$1,090

$1,233

$1,393

$810$750

$694$643

$595$551

$0

$200

$400

$600

$800

$1,000

$1,200

$1,400

$1,600

2003 2004 2005 2006 2007 2008

Cost

Per

Month

($)

AnticipatedHealthcare PremiumCost - 13%/yr.Increase

EmployerHealthcare CostBudgeted Increase -8%

Consumer Coverage Gap

Source: Kaiser Family Foundation, Bureau of Labor Statistics 2002 National Compensation Survey, Health Research and Educational Trust, Bureau of Labor Statistics Consumer Expenditure Report, 2003, Chapter House

20

Driving Health Care QualityPay for performance

“Premier” physicians at UHC Network within a network More than 35 health plans utilizing

Electronic health records Implemented effectively at Veterans

Affairs Intended to eliminate errors VISTA is now available to any practice

21

Growth of HRAs and HSAsHSAs were legislated December 2003

Jan. 2005: over 600,000 participants Mid 2005: over 1 million participants

HRA available around 2001 Jan. 2005:2.6 million participants Mid 2005: over 3 million participants

Combined CDHP membership anticipated by January 2006: 6 million

Source: American Association of Health Plans, Inside Consumer Directed Healthcare

22

Expansion of Consumer Directed Health Care and HSAsMCOs now committed to marketplace

UHC purchased Definity UHC only offering HSA/CDHC to own staff Anthem purchased Lumenos

Federal Government offering HDHP/HSAs

Much of HSA growth coming from small employers

23

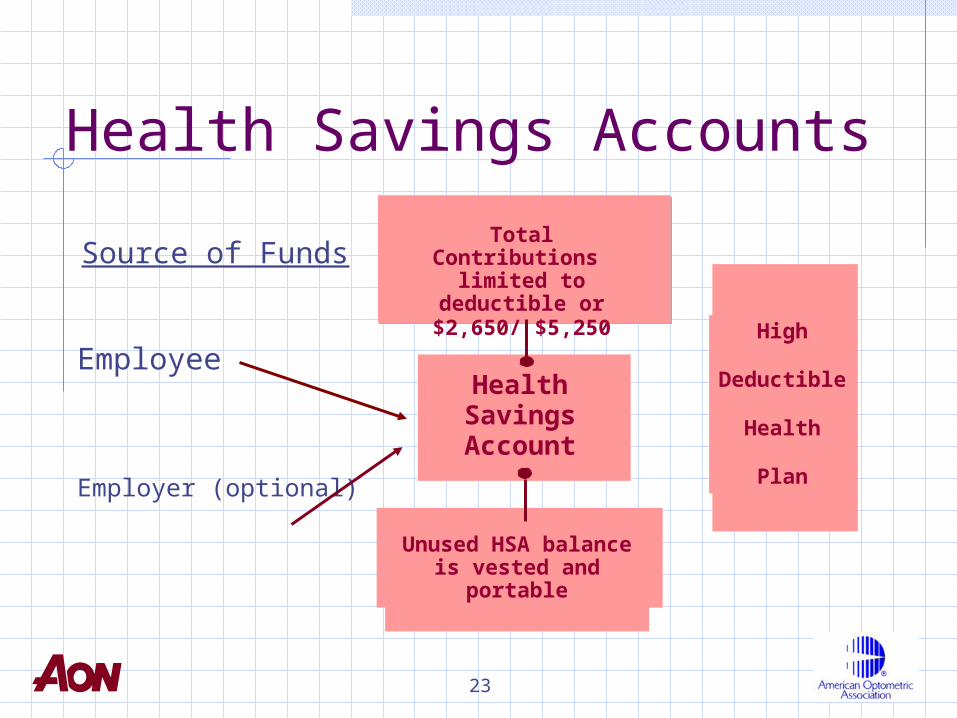

Health Savings Accounts

Source of Funds

HealthSavingsAccount

High

Deductible

Health

Plan

Employee

Employer (optional)

Total Contributions limited to deductible or

$2,650/ $5,250

Unused HSA balance is vested and portable

24

Empowered Consumer with Consumer Driven PlansAetna will provide actual allowed

office visit charge amountUHC is identifying “Premier”

physiciansParticipants have ready access to

peer reviewed health care informationMCOs and employers are driving

hospitals to measure outcomes and reduce errors

25

Impact on OptometryMore self-pay by patients. Patients may:

still use network doctors for discounts rely more on coupons for savings be willing to pay full cost for outstanding

value/service insist on negotiating fees

Direct-to-consumer marketing may become even more critical

More billing challenges

26

Impact on OptometryCompete on basis of cost, outcomes

and serviceCollect and monitor dataDevelop performance and quality

standards and strive to meet them

Source: Chapter House

27

Medicare Advantage

ECBC and FRC monitoring Medicare Advantage development

Aggressively pursuing plans that exclude ODs

Adopting successful Managed Care Marketing Initiative for discriminating Medicare Advantage plans

28

Impact on OptometryConsider joining Medicare Advantage

networks to provide medical and/or vision services Some networks may resist including

Optometrists

Fewer Traditional Medicare patientsDifferent rules than original MedicareBe aware, this may only be temporary

29

A Closer Look at Colorado

30

Trends in ColoradoHealthcare

Consolidation & ChangeUHC purchases PacifiCareWellPoint CA purchases AnthemGreat West HealthCare wins State of

CO contract and selects AvisisCigna drops Opticare for routine

vision in favor of VSP

31

Trends in ColoradoHealthcare – LegislativeHouse Bill 04-1354 - Uniform

Credentialing New 28 page credentialing application

Senate Bill 37 – 2nd Level Appeals Mandatory to Carriers –Voluntary to

Members

House Bill 05-1165 Insurance Benefit Assignment

Carriers are required to pay Claims directly to a Provider who holds assignment regardless of being In or Out-of-Network.

32

Trends in ColoradoVision Care

Voluntary Vision PlansColorado Vision Care Direct

Discount Plans are popping upeverywhere

Wal-Mart Vision InsurancePlans covering routine vision and

Safety Programs are being introduced

33