Embed Size (px)

Citation preview

Before printing this must be sent back to

CSG.

This template needs to be PDF’d with specific set-up which includes crop marks, bleeds and page layouts.

The total number of pages

needs to be divisible by four

Total pages must not exceed 48

Imp

ort

an

t

IMPORTANT

The colours in this template have been adjusted from the standard printed templates.

When bringing content from

any other file you must check the values of all EY greys are mapped to the palette in this

file.

EY Gray: 128, 128, 128 EY Gray tint 1: 153, 153, 153 EY Gray tint 2: 192, 192, 192 EY Gray tint 3: 240, 240, 240

Opening up the capital markets

July 2015

FCA investment and corporate banking market study

PLEASE DO NOT REMOVE FOR CSG PURPOSES ONLY Image ref no: 14H03375_RF

Before printing this must be sent back to

CSG.

This template needs to be PDF’d with specific set-up which includes crop marks, bleeds and page layouts.

The total number of pages

needs to be divisible by four

Total pages must not exceed 48

Imp

ort

an

t

IMPORTANT

The colours in this template have been adjusted from the standard printed templates.

When bringing content from

any other file you must check the values of all EY greys are mapped to the palette in this

file.

EY Gray: 128, 128, 128 EY Gray tint 1: 153, 153, 153 EY Gray tint 2: 192, 192, 192 EY Gray tint 3: 240, 240, 240

Opening up the capital markets 2

The UK Financial Conduct Authority (FCA) has hit the ground running in pursuing its new competition objective, with its last two business plans providing high-level indications of how it will engage in the competition agenda. Now, following the wholesale sector competition review, the FCA has published terms of reference for a formal market study into corporate and investment banking, presenting firms in these markets with specific regulatory challenges with respect to effective competition, for the first time.

The study will focus on primary market and related activities provided in the UK. Primary markets are defined by the FCA as being equity and debt capital markets, mergers and acquisitions and acquisition financing. Related activities such as corporate broking and ancillary services will be considered for how they impact competition in relation to the review topics. The three main themes of study, based on feedback from the initial wholesale sector competition review are:

► Choice of banks and advisers — this includes the competitive landscape, clients’ purchasing behaviour, including the impact of syndication, and entry and expansion, including the potential effects of regulation

► Limited transparency — this includes the adequacy of information, the transparency of the allocation process and the impact of established practices, processes or regulations on transparency in the IPO process

► Bundling and cross-subsidisation — this includes both whether bundling and/or cross-subsidisation occurs and also whether such activities, if they exist, have adverse effects on competition and clients

In this paper we outline these further and consider the likely impact for firms.

Stakeholder engagement with the FCA

► In February, the FCA announced that it would launch a market study into the wholesale sector in 2015. The FCA formally launched its study in May, with the publication of its Terms of Reference (ToR) and scope.

► The ToR states that the FCA is keen to engage with stakeholders of all sizes about their experiences.

► The FCA will approach market participants for information and data to enable assessment of the key themes. There will be a series of roundtables and bilateral meetings with stakeholders, and the FCA has stated it is keen to hear from stakeholders throughout. As the timetable is tight, stakeholders should actively seek to engage with the process to get their views heard.

► The FCA will publish a report setting out interim findings and proposed remedies at the end of 2015, with a final report expected in spring 2016.

Overview

Before printing this must be sent back to

CSG.

This template needs to be PDF’d with specific set-up which includes crop marks, bleeds and page layouts.

The total number of pages

needs to be divisible by four

Total pages must not exceed 48

Imp

ort

an

t

IMPORTANT

The colours in this template have been adjusted from the standard printed templates.

When bringing content from

any other file you must check the values of all EY greys are mapped to the palette in this

file.

EY Gray: 128, 128, 128 EY Gray tint 1: 153, 153, 153 EY Gray tint 2: 192, 192, 192 EY Gray tint 3: 240, 240, 240

Opening up the capital markets 3

PLEASE DO NOT REMOVE FOR CSG PURPOSES ONLY Image ref no: 14L02872_RF

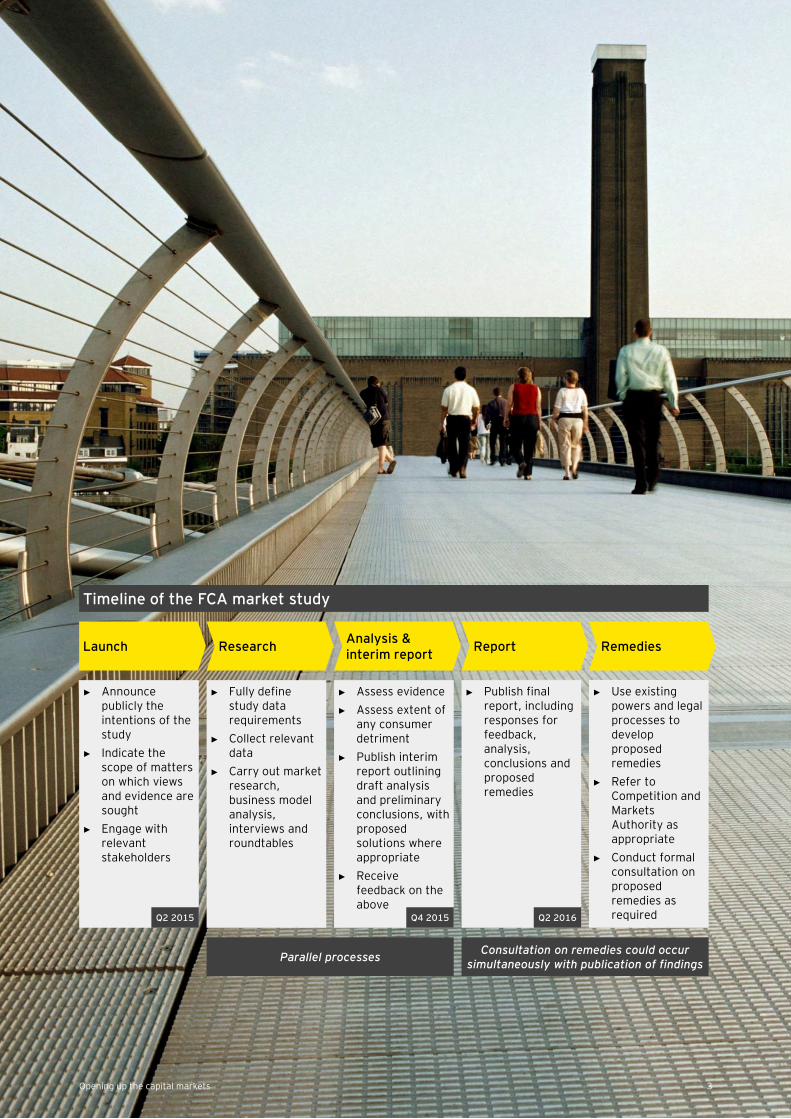

Report Remedies

► Use existing powers and legal processes to develop proposed remedies

► Refer to Competition and Markets Authority as appropriate

► Conduct formal consultation on proposed remedies as required

Consultation on remedies could occur simultaneously with publication of findings

Research Analysis & interim report

Launch

Parallel processes

► Fully define study data requirements

► Collect relevant data

► Carry out market research, business model analysis, interviews and roundtables

► Announce publicly the intentions of the study

► Indicate the scope of matters on which views and evidence are sought

► Engage with relevant stakeholders

Q2 2015

► Assess evidence

► Assess extent of any consumer detriment

► Publish interim report outlining draft analysis and preliminary conclusions, with proposed solutions where appropriate

► Receive feedback on the above

Q4 2015

► Publish final report, including responses for feedback, analysis, conclusions and proposed remedies

Q2 2016

Timeline of the FCA market study

Before printing this must be sent back to

CSG.

This template needs to be PDF’d with specific set-up which includes crop marks, bleeds and page layouts.

The total number of pages

needs to be divisible by four

Total pages must not exceed 48

Imp

ort

an

t

IMPORTANT

The colours in this template have been adjusted from the standard printed templates.

When bringing content from

any other file you must check the values of all EY greys are mapped to the palette in this

file.

EY Gray: 128, 128, 128 EY Gray tint 1: 153, 153, 153 EY Gray tint 2: 192, 192, 192 EY Gray tint 3: 240, 240, 240

Opening up the capital markets 4

The FCA’s focus

The market study will explore whether competition for investment banking and corporate banking services is working well, focusing especially on specific areas of the capital markets.

The FCA has particular concerns in the following areas:

Choice of banks and advisers

The FCA is keen to understand variation in service by client group, and the extent to which smaller clients in particular are less well served by the current competitive landscape. Firms will need to explain why they do not serve certain types of client or explain key differentials in service.

The FCA will also look at clients’ purchasing behaviour and the impact of syndication, seeking to understand if client preferences drive competition, and what factors may cause a client to choose syndication, affecting the competitive dynamics in the market.

Entry to and expansion of the market is under consideration. Banks will be challenged to explain how they establish and maintain their client base for these markets, to facilitate the regulator’s understanding of potential barriers faced by new entrants to the market. The FCA is particularly interested in practices or regulations that may inhibit the establishment of new ways of serving clients.

EY view

A key question for the regulator to decide is what size of client it expects to have access to the capital markets. This will have implications for client segmentation.

We expect the regulator to examine whether there are circumstances in which syndication restricts instructing or issuing clients’ ability to select banks and advisers to play them off against each other.

It will be important for firms to consider the continued regulatory emphasis on conduct and client detriment focus on disproving its occurrence.

However, this is also an opportunity to raise areas where ‘red tape’ is stifling competition, and we expect that challenger firms will be especially eager to take advantage of this.

Interaction with other regulatory initiatives

The FCA has highlighted specific regulatory initiatives that it will be looking at throughout the process of the market study. These are:

► The Fair and Effective Markets Review (FEMR) — conducted jointly by the FCA, Bank of England (BoE) and HM Treasury, this looked at the operation of fixed income, currencies and commodities markets (FICC) and has made a number of relevant recommendations.

► Capital Markets Union — the European Commission is currently exploring ways to establish a single capital market in the EU. The FCA has noted that while the precise areas where action will be taken have not been decided, this could have a significant impact on competition in the UK and European financial markets.

► MiFID II — this will apply from 3 January 2017 and has impact relating to transparency and bundling that may address some areas relating to the review. However, the FCA believes it is too early to decide how far the changes made in MiFID II will address the concerns identified in this sector.

The FCA has stated that it will take account of these other regulatory initiatives appropriately during the review. It may incorporate them into the market study or into remedies identified if this is appropriate.

“Authorities across Europe are looking to improve the way capital markets support the needs of the real economy, in particular, beyond the largest and most liquid investments. The FCA has recognised the need for consistency, and banks should see the potential strategic impact of these initiatives and respond proactively.”

John Liver, Partner EY UK, Global Regulatory Reform Leader

Before printing this must be sent back to

CSG.

This template needs to be PDF’d with specific set-up which includes crop marks, bleeds and page layouts.

The total number of pages

needs to be divisible by four

Total pages must not exceed 48

Imp

ort

an

t

IMPORTANT

The colours in this template have been adjusted from the standard printed templates.

When bringing content from

any other file you must check the values of all EY greys are mapped to the palette in this

file.

EY Gray: 128, 128, 128 EY Gray tint 1: 153, 153, 153 EY Gray tint 2: 192, 192, 192 EY Gray tint 3: 240, 240, 240

Opening up the capital markets 5

Limited transparency

Limited transparency over both price and quality may make it difficult for clients to assess value for money. Both quality and costs are often difficult to predict in advance. While corporate clients are generally considered to be more sophisticated than retail customers, a lack of transparency, both of expected quality and of the costs of service at the point of purchase, may prevent competition from working effectively in the market. The FCA will explore the extent to which clients have access to adequate information and feel well placed to assess value. As a result, firms should be prepared to handle large information requests and provide rationale for information disclosure in this respect.

The FCA also intends to investigate the transparency of the allocation process specifically. Concerns were raised during the wholesale competition review that when issuing debt or equity, issuing banks may favour certain investors. The FCA is seeking to consider circumstances that may make it difficult for issuing clients to influence and monitor allocations.

Another specific consideration for the FCA is whether existing rules and practices for disclosing information around IPOs allow information, such as prospectuses and unconnected research, to be released at the appropriate junctures, and whether the timing of publication gives publishing banks a privileged position.

EY view

The FCA’s drive for the market to become more transparent was shown through its Thematic Review on Best Execution. If best execution had been looked at through the prism of the overall impact of transparency on competition within the financial markets, the regulator’s reach could have widened beyond pure MiFID instruments.

It is important that banks understand their client base in order to meet the needs of their clients, which vary by age and experience. Products and services are typically offered to professional clients on the basis that those clients have sufficient knowledge and understanding to receive only minimal disclosure and explanation. This leads to assumptions about what clients know and whether they are capable of determining the risk associated with a transaction or strategy. The level of transparency and disclosure will vary depending on the complexity of the product or service and the relative sophistication of the clients, and firms may need to apply their experience of segmenting the professional client population against specific and demonstrable criteria in the markets under scrutiny in this study.

In the context of this market study, we expect transparency to create a need for clearer breakdowns of charges applied to a transaction so that the client can assess value. The regulator has already shown a clear focus on transparency in its standard approach to conduct; we expect also to see this under its competition objective.

“Transparency is a major part of this review, and this should be seen in the context of other key areas of FCA focus, such as conflicts of interest and information flows. Whatever the outcome of the review, increased transparency within capital markets is likely to be required by regulators.”

Stuart Crotaz, Partner EY UK, Corporate and Investment Banking

Before printing this must be sent back to

CSG.

This template needs to be PDF’d with specific set-up which includes crop marks, bleeds and page layouts.

The total number of pages

needs to be divisible by four

Total pages must not exceed 48

Imp

ort

an

t

IMPORTANT

The colours in this template have been adjusted from the standard printed templates.

When bringing content from

any other file you must check the values of all EY greys are mapped to the palette in this

file.

EY Gray: 128, 128, 128 EY Gray tint 1: 153, 153, 153 EY Gray tint 2: 192, 192, 192 EY Gray tint 3: 240, 240, 240

Opening up the capital markets 6

Bundling and cross-subsidisation

A long-standing concern in the market has surrounded the selling together of multiple investment and corporate banking services, and whether such bundling or cross-subsidisation may restrict either clients’ ability to switch or their ability to choose different services, as well as create barriers to entry and expansion.

The FCA will consider to what extent bundling and cross-subsidisation occurs in practice and secondly, the impact of such bundling and cross-subsidisation will be explored.

EY view

Investment and corporate banking services often operate with economies of scale; the cost of providing additional services for an existing client is likely to be lower than the stand-alone cost of providing these services, given the pre-existing understanding of the client’s business model and investment in the client relationship.

This can be beneficial for the client. However, where a bundling of the products and services occurs, it may be more difficult for clients to assess whether they are getting value for money when paying for a series of services over time, as the client may not understand the relative prices of the different services.

Firms that bundle or cross-subsidise will need to consider whether the way in which they do this creates an anti-competitive effect in the market or whether it has a beneficial effect for clients. Clearly showing any such benefits, as well as demonstrating evidence of transparency, to the regulator will be key to minimising the interventions made in this area.

We see it as highly likely firms will need to provide details of their stand-alone products when offering bundled services. This has been the case for competition regulators in other industries, and we would expect the same in capital markets.

Case study: dealing commissions ► We have previously seen the

FCA place particular focus on bundling and cross-subsidisation. In 2014, the FCA conducted a review on how firms use dealing commission.

► The review found that only a minority of firms give sufficient consideration to the value added and cost of research paid for by clients’ dealing commission. The negative impact on transparency and assessment of investor value was called out by the FCA, which, following the review, announced its support for reforms to prevent research being paid for by dealing commissions.

► As a direct result of this, some banks are beginning to charge their clients separately for research. Although it is still early days to know the long-term effects of this regulatory intervention, a number of questions have emerged, such as how the research is valued and how different clients will be charged for access to it.

► However, as a case study, this presents a useful precedent for firms to consider – both in terms of actions that the FCA has previously taken and also when considering whether in the future it might use its competition powers to take more rigorous action in this area.

“Given the FCA and CMA’s interest in the bundling of products across all financial services, firms will need to be able to explain in detail whether and how products are cross-subsidised. Firms should be looking at how to demonstrate where bundling and cross-subsidisation can create benefits for clients and the markets.”

Rute Aparicio, Partner EY UK, Valuation and Business Modelling

Before printing this must be sent back to

CSG.

This template needs to be PDF’d with specific set-up which includes crop marks, bleeds and page layouts.

The total number of pages

needs to be divisible by four

Total pages must not exceed 48

Imp

ort

an

t

IMPORTANT

The colours in this template have been adjusted from the standard printed templates.

When bringing content from

any other file you must check the values of all EY greys are mapped to the palette in this

file.

EY Gray: 128, 128, 128 EY Gray tint 1: 153, 153, 153 EY Gray tint 2: 192, 192, 192 EY Gray tint 3: 240, 240, 240

Overarching considerations for firms

Overall, clients should be able to make informed decisions as to which arrangements they enter into. They need to understand precisely what they are paying for, and be able to analyse and compare services from different institutions, especially as the client-institution relationship ages. We expect firms to be faced with increased requirements from the regulator to prove their commitment to allowing client choice and pricing transparency. Value for money is particularly pertinent for smaller corporate clients as they have less bargaining power than their larger counterparts.

Institutions should consider how they conduct business in the market and whether any of their actions could lead to anti-competitive outcomes. The FCA looks to identify potential risks to consumers or market integrity. Firms need to contemplate how they could respond to requests for data and information. We expect increased requirements for firms to demonstrate competitive outcomes for their clients, with controls in place to underpin this competitive framework. Firms should also show proactive consideration of any potential remediation requirements identified.

This is a key time for firms to seek to engage with the regulator on these topics. Firms should be proactively demonstrating where competition already provides benefits to clients as well as explaining any benefits they perceive of a one-stop shop.

Opening up the capital markets 7

PLEASE DO NOT REMOVE FOR CSG PURPOSES ONLY Image ref no: 14L02469_RF

Before printing this must be sent back to

CSG.

This template needs to be PDF’d with specific set-up which includes crop marks, bleeds and page layouts.

The total number of pages

needs to be divisible by four

Total pages must not exceed 48

Imp

ort

an

t

IMPORTANT

The colours in this template have been adjusted from the standard printed templates.

When bringing content from

any other file you must check the values of all EY greys are mapped to the palette in this

file.

EY Gray: 128, 128, 128 EY Gray tint 1: 153, 153, 153 EY Gray tint 2: 192, 192, 192 EY Gray tint 3: 240, 240, 240

Opening up the capital markets 8

PLEASE DO NOT REMOVE FOR CSG PURPOSES ONLY Image ref no: 14L02469_RF

Competition-related changes to Principle 11

► The FCA is introducing a new rule (SUP 15.3.32R(1)) to the FCA handbook related to Principle 11 of the Principles for Business. The current principle requires firms to disclose ‘appropriately anything relating to the firm of which that regulator would reasonably expect notice’.

► Following the publication of PS15-18, the FCA will now require a firm to ‘notify the FCA if it has, or may have, committed a significant infringement of any applicable competition law’. This is a change to the original proposed rule as it includes a materiality threshold.

► The policy statement remains clear that this should be done ‘as soon as it becomes aware, or has information which reasonably suggests, that a significant infringement has, or may have, occurred’ (SUP 15.3.2R(2)). This poses potential risks to firms as the lack of defined threshold means it will be hard to know at what point the disclosure must be made. On disclosing an infringement of one competition law, the firm may be subject to a wider investigation that could uncover further breaches.

Before printing this must be sent back to

CSG.

This template needs to be PDF’d with specific set-up which includes crop marks, bleeds and page layouts.

The total number of pages

needs to be divisible by four

Total pages must not exceed 48

Imp

ort

an

t

IMPORTANT

The colours in this template have been adjusted from the standard printed templates.

When bringing content from

any other file you must check the values of all EY greys are mapped to the palette in this

file.

EY Gray: 128, 128, 128 EY Gray tint 1: 153, 153, 153 EY Gray tint 2: 192, 192, 192 EY Gray tint 3: 240, 240, 240

The Capital Markets Union

A green paper on the proposed Capital Markets Union (CMU) was launched by Lord Hill in January 2015. This has clear implications for the stakeholders of this market study. The key objectives include:

► Bringing forward proposals for high-quality securitisation standards to free up bank balance sheets to lend

► Relaxing capital requirements for insurers and banks investing in infrastructure

► Streamlining the prospectus requirements on companies, especially small ones, to raise capital and reach investors across borders

► Improving SME credit information to facilitate loans to smaller companies

► Working with industry to develop a pan-EU private placement regime to encourage direct investment into businesses

► Removing obstacles to cross border investment by citizens and funding of SMEs

The proposals focus on improving the medium- to long-term investment environment in Europe and improve investor participation in capital markets.

PLEASE DO NOT REMOVE FOR CSG PURPOSES ONLY Image ref no: 14H04271_RF

Opening up the capital markets 9

The FCA’s use of its powers

The FCA has specifically stated that it is conducting this market study under its Financial Services and Markets Act (FSMA) remit. It acknowledges that some of the activities it intends to look at are outside its normal FSMA regulatory perimeter but believes that its information-gathering powers under FSMA are available in relation to ancillary activities and are therefore covered.

Using FSMA powers allows the FCA to be flexible in the actions it might take following the market study. The FCA states in both the ToR and its general guidance on market studies that the possible remedies include:

► Market-wide remedies such as rule-making, publishing general guidance or proposing enhanced industry self-regulation

► Firm-specific remedies (for example, variation of permissions, cancelling permissions, public censure, imposing financial penalties or filing for injunction orders or restitution orders)

► Making a formal market investigation reference to the Competition & Markets Authority

The FCA believes considerable benefits can be derived from improvements in the way competition works. As part of its recent work on competition, it has highlighted its own ability to intervene effectively at a UK level, and we would expect the outcomes of market studies to include a focused look at what remedies are appropriate and most likely to cause an effective intervention.

Before printing this must be sent back to

CSG.

This template needs to be PDF’d with specific set-up which includes crop marks, bleeds and page layouts.

The total number of pages

needs to be divisible by four

Total pages must not exceed 48

Imp

ort

an

t

IMPORTANT

The colours in this template have been adjusted from the standard printed templates.

When bringing content from

any other file you must check the values of all EY greys are mapped to the palette in this

file.

EY Gray: 128, 128, 128 EY Gray tint 1: 153, 153, 153 EY Gray tint 2: 192, 192, 192 EY Gray tint 3: 240, 240, 240

EY is well placed to help our clients given our experience of markets where competition regulation is mature. We can help to understand the likely outcomes of the market study and actions that clients may wish to take.

EY has a proven track record in helping our clients to:

► Shape the agenda in their communications with the FCA and design integrated response plans, covering financial, strategic, economic, risk and legal perspectives

► Consider the impact of competition for key regulatory initiatives

► Design governance processes that consider the impact of the FCA’s competition agenda and flag issues appropriately to senior managers

► Assess the transparency of processes and communications to clients and consider how they should be personalised to different segments of the client base

► Model the existence and impact of bundling and cross-subsidisation in terms of both positive and negative impacts on clients

► Leverage existing regulatory projects to deliver enhanced outcomes that consider the impact of competition regulation

► Respond to FCA data requests, proactively informing the regulator of areas they should consider and structuring submissions to the regulator

► Understanding information and data requirements

► Collection and coordination of the consolidation of material

► Market research and analysis of the outcomes

► Collating information on how a market functions and how competitive it is

► Respond to remedies, delivering tailored solutions that analyse and quantify the likely strategic impacts of potential business model changes, and deliver on implementing the operational solutions

Opening up the capital markets 10

How EY can help

PLEASE DO NOT REMOVE FOR CSG PURPOSES ONLY Image ref no: 14H01442_RF

Before printing this must be sent back to

CSG.

This template needs to be PDF’d with specific set-up which includes crop marks, bleeds and page layouts.

The total number of pages

needs to be divisible by four

Total pages must not exceed 48

Imp

ort

an

t

IMPORTANT

The colours in this template have been adjusted from the standard printed templates.

When bringing content from

any other file you must check the values of all EY greys are mapped to the palette in this

file.

EY Gray: 128, 128, 128 EY Gray tint 1: 153, 153, 153 EY Gray tint 2: 192, 192, 192 EY Gray tint 3: 240, 240, 240

For further information, please contact one of the following or your usual EY contact:

Opening up the capital markets 11

Next steps

Omar Ali

Banking & Capital Markets Leader

+ 44 20 7951 1789

John Liver

Global Regulatory Reform Leader

+ 44 20 7951 0843

Mark Gregory

Chief Economist

+ 44 20 7951 5890

Rute Aparicio

Valuation & Business Modelling

+ 44 20 7951 0957

PLEASE DO NOT REMOVE FOR CSG PURPOSES ONLY Image ref no: 14H02251_RF

Tim Rooke

Corporate & Investment Banking

+ 44 20 7951 1472

Stuart Crotaz

Corporate & Investment Banking

+ 44 20 7951 9714

Sam Carruthers

Corporate & Investment Banking

+ 44 20 7951 3804

Before printing this must be sent back to

CSG.

This template needs to be PDF’d with specific set-up which includes crop marks, bleeds and page layouts.

The total number of pages

needs to be divisible by four

Total pages must not exceed 48

Imp

ort

an

t

EY | Assurance | Tax | Transactions | Advisory

About EY EY is a global leader in assurance, tax, transaction and advisory services. The insights and quality services we deliver help build trust and confidence in the capital markets and in economies the world over. We develop outstanding leaders who team to deliver on our promises to all of our stakeholders. In so doing, we play a critical role in building a better working world for our people, for our clients and for our communities.

EY refers to the global organization, and may refer to one or more, of the member firms of Ernst & Young Global Limited, each of which is a separate legal entity. Ernst & Young Global Limited, a UK company limited by guarantee, does not provide services to clients. For more information about our organization, please visit ey.com.

© 2015 EYGM Limited. All Rights Reserved.

EYG No. CQ0241

11113_11115 (UK) 07/15. Creative Services Group.

ED None

In line with EY’s commitment to minimize its impact on the environment, this document has been printed on paper with a high recycled content.

This material has been prepared for general informational purposes only and is not intended to be relied upon as accounting, tax, or other professional advice. Please refer to your advisors for specific advice.

ey.com/ukbanking