Embed Size (px)

Citation preview

2014 has been the busiest year for London IPOs since 2007, producing 93 listings, excluding investment vehicles, raising cumulative funds of £13bn.

Global IPO activity continues to strengthen with a 35% increase in volume and a 50% increase in value compared to 2013.

IPO EyeAn overview of 2014

2014 has been the busiest year for London IPOs since 2007, with 93 listings, excluding investment vehicles, raising cumulative funds of £13bn. This quarter saw increased market volatility which slowed the pace of activity seen in the first three quarters of the year. However the market didn’t close and there were a number of listings which have performed well in the aftermarket.

► Main market — two floats raised £453mn in Q4, taking the yearly tally to 34 IPOs raising cumulative funds of £10.9bn

► AIM — 11 admissions this quarter raised £302mn, taking the yearly tally to 59 admissions raising total funds of £2.1bn

Global IPO activity continues to strengthen with a 35% increase in volume and a 50% increase in value compared to 2013. The US hosted more cross-border IPOs than any other region this year and its stock exchanges led the world in terms of the number of deals and capital raised. Asia-Pacific had a strong year with proceeds raised jumping by 38% to US$81bn in comparison to last year. Greater China exchanges saw 233 IPOs raise capital of US$42bn, an increase of 118% by deal number and 89% by proceeds on 2013. In EMEIA exchanges ranked second by number of deals and third by proceeds, raising US$75bn from a total of 353 IPOs. This is the highest IPO activity by capital raised we have seen in this region since 2007.

A late flurry to cap off a bumper year

Note: all data in this report is as of 5 December 2014

2 | IPO Eye Q4 2014

Market listings — 2014

What constitutes an IPO? ► Not all new admissions, as listed by the London Stock Exchange, are defined as IPOs for the purposes of the commentary throughout

this report. Our definition excludes secondaries, re-admissions, investment funds, transfers from AIM to Main (and vice-versa) and introductions where no money is being raised, or shares placed with new investors.

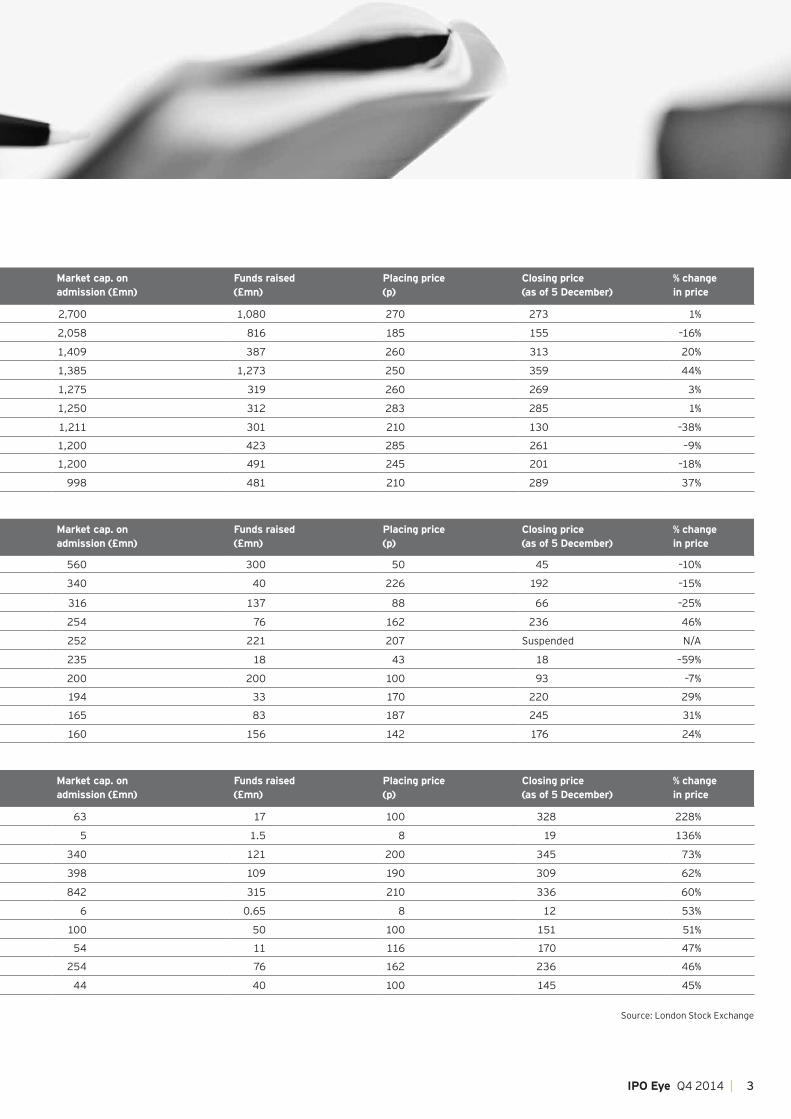

Top main market IPOs by market capitalisation as of 5 December 2014 (excluding GDRs)

Date of admission Company PE backed Country of incorporation

Region/s of domicile

Sector Market cap. on admission (£mn)

Funds raised (£mn)

Placing price (p)

Closing price (as of 5 December)

% change in price

12-Jun-14 B&M European Value Retail S.A. Y UK UK Retail 2,700 1,080 270 273 1%

23-May-14 Saga Plc Y UK UK Insurance/Leisure 2,058 816 185 155 –16%

03-Apr-14 Just Eat Plc Y UK Europe Technology 1,409 387 260 313 20%

23-Jun-14 AA Plc Y UK UK Motoring Services 1,385 1,273 250 359 44%

20-Jun-14 TSB Banking Group Plc N UK UK Financial Services 1,275 319 260 269 3%

13-Nov-14 Virgin Money Holdings (UK) Plc N UK UK Financial Services 1,250 312 283 285 1%

09-Apr-14 Seplat Petroleum Devt Co Plc N Nigeria Nigeria Oil & Gas 1,211 301 210 130 –38%

26-Feb-14 AO World Plc N UK UK Retail 1,200 423 285 261 –9%

12-Mar-14 Pets at Home Group Plc Y UK UK Retail 1,200 491 245 201 –18%

10-Jul-14 SSP Group Plc Y UK Global Leisure & Hospitality 998 481 210 289 37%

Top AIM admissions by market capitalisation as of 5 December 2014

Date of admission Company PE backed Country of incorporation

Region/s of domicile

Sector Market cap. on admission (£mn)

Funds raised (£mn)

Placing price (p)

Closing price (as of 5 December)

% change in price

14-Mar-14 Boohoo.com Plc N UK UK Retail 560 300 50 45 –10%

16-Jun-14 MySale Group Plc Y Australia Global Retail 340 40 226 192 –15%

06-Jan-14 RM2 International S.A. Y Luxembourg Europe & USA Manufacturing 316 137 88 66 –25%

02-Apr-14 SafeCharge International Group Limited N British Virgin Islands Global Financial Services 254 76 162 236 46%

19-Mar-14 Dalata Hotel Group Plc Y Ireland Ireland & UK Leisure & Hospitality 252 221 207 Suspended N/A

04-Feb-14 Hurricane Energy Plc N UK UK Oil & Gas 235 18 43 18 –59%

27-Feb-14 DX Plc N UK UK Logistics 200 200 100 93 –7%

14-May-14 Patisserie Holdings Plc Y UK UK Leisure & Hospitality 194 33 170 220 29%

10-Oct-14 Gamma Communications Plc N UK UK Telecommunications 165 83 187 245 31%

10-Feb-14 Manx Telecom Plc Y UK UK Telecommunications 160 156 142 176 24%

Top performing IPOs by closing market price as of 5 December 2014

Date of admission Company Market PE backed Region/s of domicile

Sector Market cap. on admission (£mn)

Funds raised (£mn)

Placing price (p)

Closing price (as of 5 December)

% change in price

18-Feb-14 4d Pharma plc AIM N UK Pharmaceutical 63 17 100 328 228%

20-Mar-14 Mosman Oil and Gas Limited AIM N Australia & New Zealand Oil & Gas 5 1.5 8 19 136%

06-Jun-14 Game Digital Plc MAIN Y Europe Retail 340 121 200 345 73%

20-Jun-14 Allied Minds Plc MAIN N USA Research 398 109 190 309 62%

18-Jul-14 Spire Healthcare Group Plc MAIN Y UK Healthcare 842 315 210 336 60%

17-Nov-14 Strat Aero Plc AIM N Global Aviation services 6 0.65 8 12 53%

30-May-14 Clipper Logistics Plc MAIN N UK Transport 100 50 100 151 51%

06-Nov-14 Quartix Holdings Plc AIM N Europe & North America Technology 54 11 116 170 47%

02-Apr-14 SafeCharge International Group Limited AIM N Global Financial Services 254 76 162 236 46%

21-May-14 Flowtech Fluidpower Plc AIM Y Benelux & UK Industrial Machinery 44 40 100 145 45%

3IPO Eye Q4 2014 |

Source: London Stock Exchange

Top main market IPOs by market capitalisation as of 5 December 2014 (excluding GDRs)

Date of admission Company PE backed Country of incorporation

Region/s of domicile

Sector Market cap. on admission (£mn)

Funds raised (£mn)

Placing price (p)

Closing price (as of 5 December)

% change in price

12-Jun-14 B&M European Value Retail S.A. Y UK UK Retail 2,700 1,080 270 273 1%

23-May-14 Saga Plc Y UK UK Insurance/Leisure 2,058 816 185 155 –16%

03-Apr-14 Just Eat Plc Y UK Europe Technology 1,409 387 260 313 20%

23-Jun-14 AA Plc Y UK UK Motoring Services 1,385 1,273 250 359 44%

20-Jun-14 TSB Banking Group Plc N UK UK Financial Services 1,275 319 260 269 3%

13-Nov-14 Virgin Money Holdings (UK) Plc N UK UK Financial Services 1,250 312 283 285 1%

09-Apr-14 Seplat Petroleum Devt Co Plc N Nigeria Nigeria Oil & Gas 1,211 301 210 130 –38%

26-Feb-14 AO World Plc N UK UK Retail 1,200 423 285 261 –9%

12-Mar-14 Pets at Home Group Plc Y UK UK Retail 1,200 491 245 201 –18%

10-Jul-14 SSP Group Plc Y UK Global Leisure & Hospitality 998 481 210 289 37%

Top AIM admissions by market capitalisation as of 5 December 2014

Date of admission Company PE backed Country of incorporation

Region/s of domicile

Sector Market cap. on admission (£mn)

Funds raised (£mn)

Placing price (p)

Closing price (as of 5 December)

% change in price

14-Mar-14 Boohoo.com Plc N UK UK Retail 560 300 50 45 –10%

16-Jun-14 MySale Group Plc Y Australia Global Retail 340 40 226 192 –15%

06-Jan-14 RM2 International S.A. Y Luxembourg Europe & USA Manufacturing 316 137 88 66 –25%

02-Apr-14 SafeCharge International Group Limited N British Virgin Islands Global Financial Services 254 76 162 236 46%

19-Mar-14 Dalata Hotel Group Plc Y Ireland Ireland & UK Leisure & Hospitality 252 221 207 Suspended N/A

04-Feb-14 Hurricane Energy Plc N UK UK Oil & Gas 235 18 43 18 –59%

27-Feb-14 DX Plc N UK UK Logistics 200 200 100 93 –7%

14-May-14 Patisserie Holdings Plc Y UK UK Leisure & Hospitality 194 33 170 220 29%

10-Oct-14 Gamma Communications Plc N UK UK Telecommunications 165 83 187 245 31%

10-Feb-14 Manx Telecom Plc Y UK UK Telecommunications 160 156 142 176 24%

Top performing IPOs by closing market price as of 5 December 2014

Date of admission Company Market PE backed Region/s of domicile

Sector Market cap. on admission (£mn)

Funds raised (£mn)

Placing price (p)

Closing price (as of 5 December)

% change in price

18-Feb-14 4d Pharma plc AIM N UK Pharmaceutical 63 17 100 328 228%

20-Mar-14 Mosman Oil and Gas Limited AIM N Australia & New Zealand Oil & Gas 5 1.5 8 19 136%

06-Jun-14 Game Digital Plc MAIN Y Europe Retail 340 121 200 345 73%

20-Jun-14 Allied Minds Plc MAIN N USA Research 398 109 190 309 62%

18-Jul-14 Spire Healthcare Group Plc MAIN Y UK Healthcare 842 315 210 336 60%

17-Nov-14 Strat Aero Plc AIM N Global Aviation services 6 0.65 8 12 53%

30-May-14 Clipper Logistics Plc MAIN N UK Transport 100 50 100 151 51%

06-Nov-14 Quartix Holdings Plc AIM N Europe & North America Technology 54 11 116 170 47%

02-Apr-14 SafeCharge International Group Limited AIM N Global Financial Services 254 76 162 236 46%

21-May-14 Flowtech Fluidpower Plc AIM Y Benelux & UK Industrial Machinery 44 40 100 145 45%

4 | IPO Eye Q4 2014

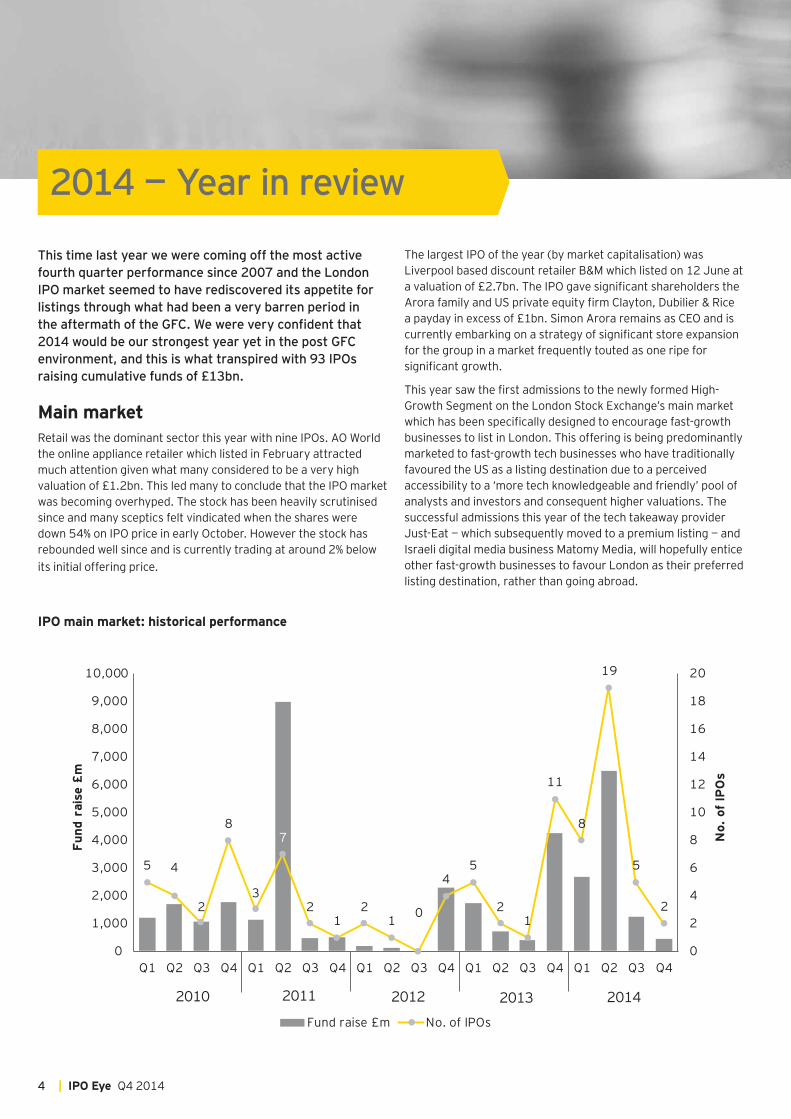

This time last year we were coming off the most active fourth quarter performance since 2007 and the London IPO market seemed to have rediscovered its appetite for listings through what had been a very barren period in the aftermath of the GFC. We were very confident that 2014 would be our strongest year yet in the post GFC environment, and this is what transpired with 93 IPOs raising cumulative funds of £13bn.

Main marketRetail was the dominant sector this year with nine IPOs. AO World the online appliance retailer which listed in February attracted much attention given what many considered to be a very high valuation of £1.2bn. This led many to conclude that the IPO market was becoming overhyped. The stock has been heavily scrutinised since and many sceptics felt vindicated when the shares were down 54% on IPO price in early October. However the stock has rebounded well since and is currently trading at around 2% below its initial offering price.

2014 — Year in review

The largest IPO of the year (by market capitalisation) was Liverpool based discount retailer B&M which listed on 12 June at a valuation of £2.7bn. The IPO gave significant shareholders the Arora family and US private equity firm Clayton, Dubilier & Rice a payday in excess of £1bn. Simon Arora remains as CEO and is currently embarking on a strategy of significant store expansion for the group in a market frequently touted as one ripe for significant growth.

This year saw the first admissions to the newly formed High-Growth Segment on the London Stock Exchange’s main market which has been specifically designed to encourage fast-growth businesses to list in London. This offering is being predominantly marketed to fast-growth tech businesses who have traditionally favoured the US as a listing destination due to a perceived accessibility to a ‘more tech knowledgeable and friendly’ pool of analysts and investors and consequent higher valuations. The successful admissions this year of the tech takeaway provider Just-Eat — which subsequently moved to a premium listing — and Israeli digital media business Matomy Media, will hopefully entice other fast-growth businesses to favour London as their preferred listing destination, rather than going abroad.

IPO main market: historical performance

5 4

2

8

3

7

21

21 0

45

21

11

8

19

5

2

0

1,000

2,000

3,000

4,000

5,000

6,000

7,000

8,000

9,000

10,000

Q1 Q2 Q3 Q4 Q1 Q2 Q3 Q4 Q1 Q2 Q3 Q4 Q1 Q2 Q3 Q4 Q1 Q2 Q30

2

4

6

8

10

12

14

16

18

20

No.

of I

PO

s

Fund

rai

se £

m

Fund raise £m No. of IPOs

2010 2011 2012 2013 2014

Q4

5IPO Eye Q4 2014 |

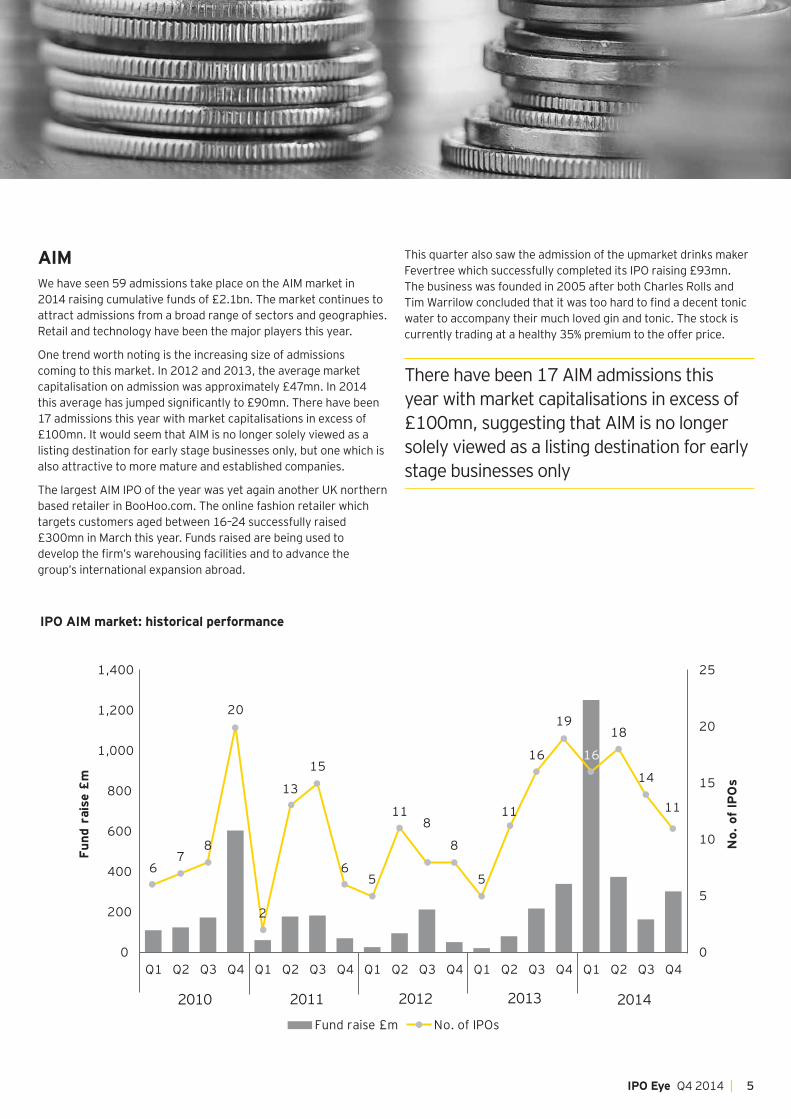

AIMWe have seen 59 admissions take place on the AIM market in 2014 raising cumulative funds of £2.1bn. The market continues to attract admissions from a broad range of sectors and geographies. Retail and technology have been the major players this year.

One trend worth noting is the increasing size of admissions coming to this market. In 2012 and 2013, the average market capitalisation on admission was approximately £47mn. In 2014 this average has jumped significantly to £90mn. There have been 17 admissions this year with market capitalisations in excess of £100mn. It would seem that AIM is no longer solely viewed as a listing destination for early stage businesses only, but one which is also attractive to more mature and established companies.

The largest AIM IPO of the year was yet again another UK northern based retailer in BooHoo.com. The online fashion retailer which targets customers aged between 16–24 successfully raised £300mn in March this year. Funds raised are being used to develop the firm’s warehousing facilities and to advance the group’s international expansion abroad.

This quarter also saw the admission of the upmarket drinks maker Fevertree which successfully completed its IPO raising £93mn. The business was founded in 2005 after both Charles Rolls and Tim Warrilow concluded that it was too hard to find a decent tonic water to accompany their much loved gin and tonic. The stock is currently trading at a healthy 35% premium to the offer price.

There have been 17 AIM admissions this year with market capitalisations in excess of £100mn, suggesting that AIM is no longer solely viewed as a listing destination for early stage businesses only

IPO AIM market: historical performance

67

8

20

2

13

15

65

118

8

5

11

16

19

16

18

14

0

200

400

600

800

1,000

1,200

1,400

Q1 Q2 Q3 Q4 Q1 Q2 Q3 Q4 Q1 Q2 Q3 Q4 Q1 Q2 Q3 Q4 Q1 Q2 Q3

Fund

rai

se £

m

Fund raise £m No. of IPOs

2010 2011 2012 2013 2014

0

5

10

15

20

25

No.

of

IPO

s

11

Q4

6 | IPO Eye Q4 2014

Volatility and aftermarket performance

FTSE Indices — 2014

Source: S&P Capital IQ

75

80

85

90

95

100

105

110

02-01-2

014

02-02-2

014

02-03-2

014

02-04-2

014

02-05-2

014

02-06-2

014

02-07-2

014

02-08-2

014

02-09-2

014

02-10-2

014

02-11-2

014

02-12-2

014

FTSE 100 FTSE 250 FTSE All-Share FTSE AIM All-Share

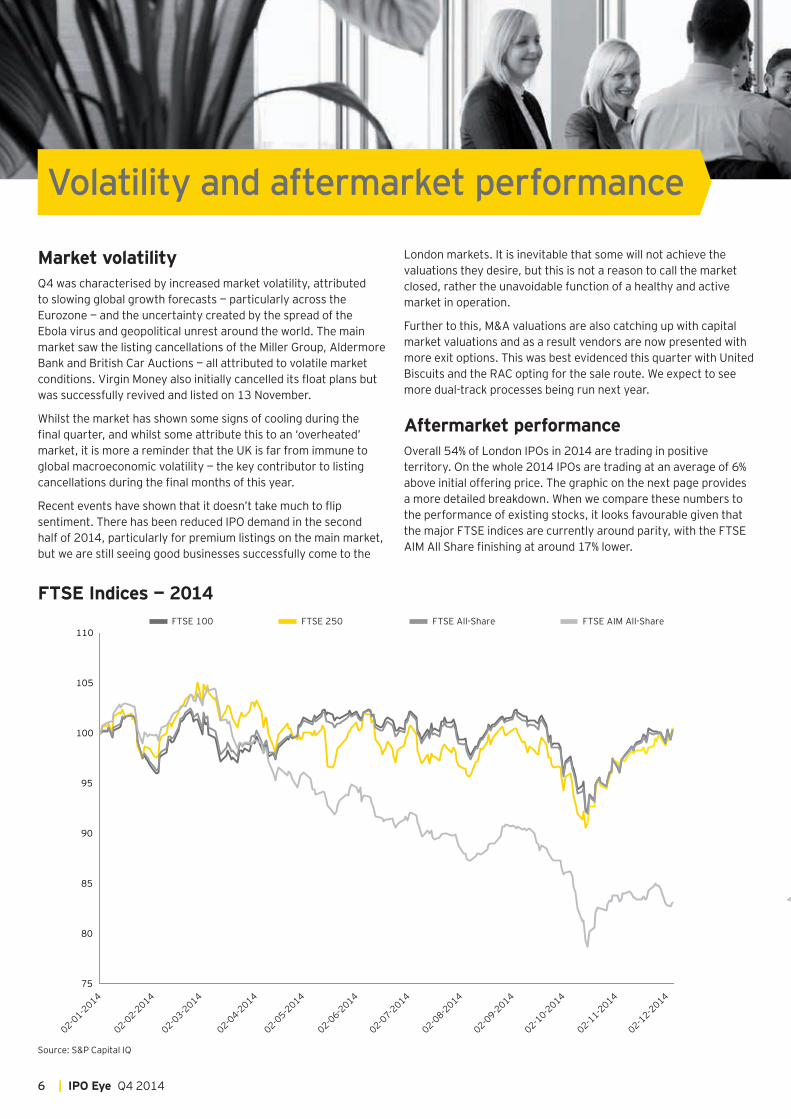

Market volatilityQ4 was characterised by increased market volatility, attributed to slowing global growth forecasts — particularly across the Eurozone — and the uncertainty created by the spread of the Ebola virus and geopolitical unrest around the world. The main market saw the listing cancellations of the Miller Group, Aldermore Bank and British Car Auctions — all attributed to volatile market conditions. Virgin Money also initially cancelled its float plans but was successfully revived and listed on 13 November.

Whilst the market has shown some signs of cooling during the final quarter, and whilst some attribute this to an ‘overheated’ market, it is more a reminder that the UK is far from immune to global macroeconomic volatility — the key contributor to listing cancellations during the final months of this year.

Recent events have shown that it doesn’t take much to flip sentiment. There has been reduced IPO demand in the second half of 2014, particularly for premium listings on the main market, but we are still seeing good businesses successfully come to the

London markets. It is inevitable that some will not achieve the valuations they desire, but this is not a reason to call the market closed, rather the unavoidable function of a healthy and active market in operation.

Further to this, M&A valuations are also catching up with capital market valuations and as a result vendors are now presented with more exit options. This was best evidenced this quarter with United Biscuits and the RAC opting for the sale route. We expect to see more dual-track processes being run next year.

Aftermarket performanceOverall 54% of London IPOs in 2014 are trading in positive territory. On the whole 2014 IPOs are trading at an average of 6% above initial offering price. The graphic on the next page provides a more detailed breakdown. When we compare these numbers to the performance of existing stocks, it looks favourable given that the major FTSE indices are currently around parity, with the FTSE AIM All Share finishing at around 17% lower.

7IPO Eye Q4 2014 |

Aftermarket share price growth/decline of 2014 IPOs

Of the main market listings 59% are trading in positive territory whereas AIM has 51% of its admissions trading above initial offer price. Main market listings in 2014 are trading at an average of 7% above their IPO price. The best performing main market IPO of 2014 has been video games retailer Game Digital which is currently trading at 73% above its initial offering price. New AIM admissions in 2014 are trading at an average of 5% above their IPO price with the best performing being 4d Pharma, which is currently trading at 228% above its initial offering price.

Aftermarket performance is definitely now more subdued than at the same time last year. Then we were reporting that main market IPOs in 2013 were trading at a 19% premium and AIM admissions at a lofty 37% premium. This more subdued performance, combined with cancelled IPOs and exits via M&A, has led many commentators to conclude that the London IPO market has effectively closed. However we have seen a late flurry of IPOs and, albeit over a relatively short timescale, they are trading at an average of 17% above their offering price.

This all shows the importance of pricing. Those businesses which seek to list in more challenging economic environments, have to price more competitively in order to get the IPO away. Subsequently they are less likely to suffer adverse price movements than those who have priced fully at the top of the market.

Our overall view is that the London market is neither overheated nor closed. It is rather starting to find an equilibrium following a period of intense activity which itself followed 5/6 years of significant inactivity.

Whilst the market has shown some signs of cooling during the final quarter, and whilst some attribute this to an ‘overheated’ market, it is more a reminder that the UK is far from immune to global macroeconomic volatility

–11% to –30%16

–30% andlower

8

0 to 10% 20

11% to 30% 14

30% and over 16

–1% to –10%18

Source: London Stock Exchange

8 | IPO Eye Q4 2014

In our view 2015 should be a reasonable year for IPO activity, although perhaps not at the level of 2014. We are anticipating reduced activity in Q2 and Q3 as a result of the uncertainty of the upcoming general election and the traditionally quiet summer period. However we are still aware of many businesses which are looking to list in Q1/2 and others who are hoping to get their deals away in the second half of next year.

As discussed earlier the M&A market is picking up we expect to see increasing numbers of businesses en route to IPO shift towards a trade or private equity sale. That said we still expect to see PE utilise IPO as an appropriate form of exit and also expect to see increasing numbers of cross-border transactions, originating predominantly from Europe and the Middle East.

Whilst we have experienced some significant market volatility this quarter we expect investor confidence to be OK over the next 12 months. The recent main market IPOs of Virgin Money and Jimmy Choo should go some way to restoring confidence in the aftermath of recent volatility, and if the currently planned IPOs for the rest of 2014 and early 2015 get away successfully, then we would expect to see a good post-election performance.

At the time of going to press it was expected that Indivior, the pharmaceutical arm of Reckitt Benckiser, would list on the main market on December 23 subject to shareholder approval.

Overall it has been a very busy 18 months for IPOs. Issuers, investors, and advisors alike will welcome a break over the Christmas period to reflect on what has been a very exciting return to activity for equity capital markets. It is perfectly possible to paint any number of scenarios for what 2015 will bring. As we have seen market sentiment can turn quickly. We however believe that we will see an effective, functioning IPO market in the absence of any new major macro-economic shocks.

The M&A market is picking up and we expect to see increasing numbers of businesses en route to IPO shift towards a trade or private equity sale

Looking forward

9IPO Eye Q4 2014 |

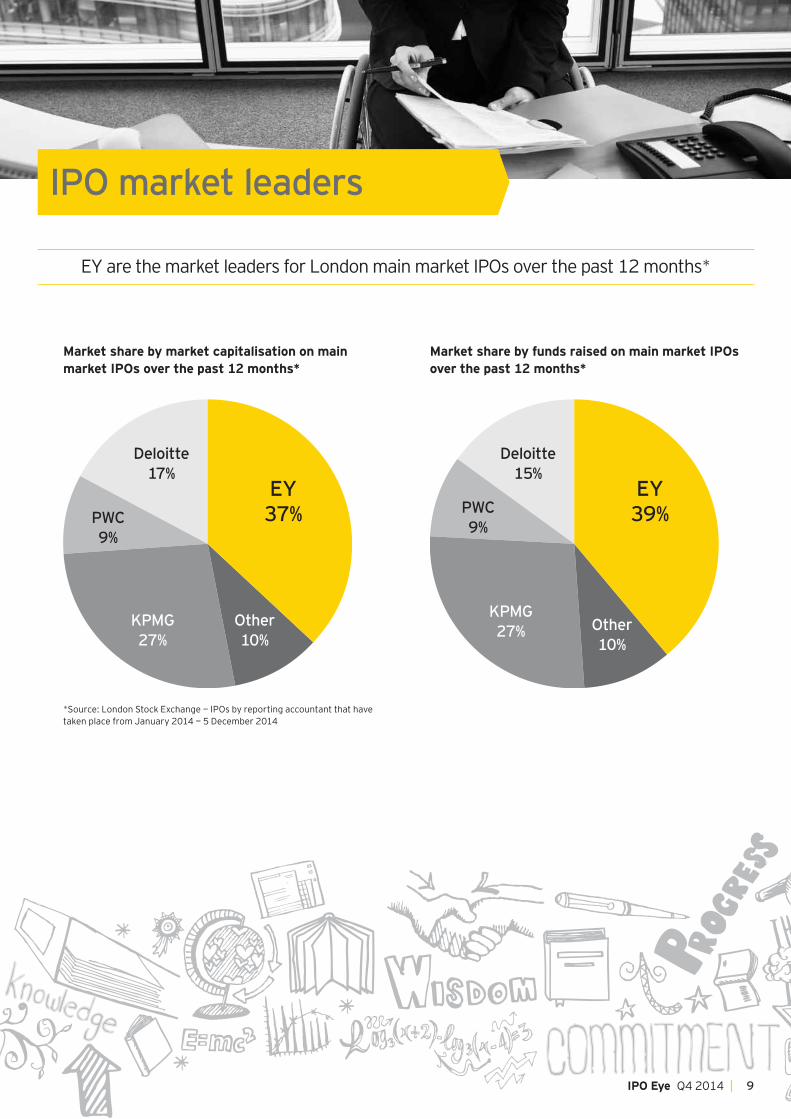

IPO market leaders

EY are the market leaders for London main market IPOs over the past 12 months*

Market share by funds raised on main market IPOs over the past 12 months*

Market share by market capitalisation on main market IPOs over the past 12 months*

EY 37%

EY 39%

KPMG 27%

KPMG 27%

Deloitte 17%

Deloitte 15%

PWC 9%

PWC 9%

Other 10%

Other 10%

*Source: London Stock Exchange — IPOs by reporting accountant that have taken place from January 2014 — 5 December 2014

10 | IPO Eye Q4 2014

For more information contact our international specialists or alternatively speak to your local EY adviser.

David VaughanIPO Leader

Tel: + 44 20 7951 3107Email: [email protected]

Scott McCubbinPartner, UK London

Tel: + 44 20 7951 3519Email: [email protected]

Richard HardingPartner, UK North

Tel: + 44 161 333 2626Email: [email protected]

Colm DevinePartner, Financial Position and Prospects

Tel: + 44 28 9044 3560Email: [email protected]

Dom McAraExecutive Director, UK Midlands

Tel: + 44 7770 571 175Email: [email protected]

Richard HallPartner, UK London

Tel: + 44 20 7951 6478Email: [email protected]

David WilkinsonPartner, UK South

Tel: + 44 20 7951 2335Email: [email protected]

Neil PateyPartner, Scotland

Tel: + 44 131 777 2064Email: [email protected]

Steve CollinsDirector, Americas

Tel: + 44 20 7951 8059Email: [email protected]

Nadeem KhanDirector, India

Tel: + 44 20 7951 0573Email: [email protected]

Marcus BaileyExecutive Director, Middle East and Africa

Tel: + 44 20 7951 1357Email: [email protected]

Timothy PinkstoneDirector, Russia and CIS

Tel: + 44 20 7951 2417Email: [email protected]

Cary WilsonPartner, Ireland

Tel: + 44 28 9044 3547Email: [email protected]

Ian KellyDirector, Ireland

Tel: + 44 28 9044 3640Email: [email protected]

Please visit www.ey.com/uk/IPO for more information on how we can help you or your business.

IPO specialist team

11IPO Eye Q4 2014 |

EY Global IPO Center of ExcellenceOur Global IPO Center of Excellence is a virtual hub which provides access to tools and knowledge for every step of the journey from finding out more about what going public means to considering capital raising options and addressing post-IPO risks. It provides access to all our IPO knowledge, tools, thought leadership and contacts from around the world in one easy-to-use source.

www.ey.com/ipocenter

IPO Retreat 11–12 May 2015Looking to float in the next 12–36 months?Our IPO Retreat helps CEOs and CFOs contemplating an IPO on one of the London markets.

It gives unparalleled advice from key advisors and guest speakers who have been through the process, and provides invaluable networking opportunities.

The IPO Retreat offers an invaluable opportunity to find out whether an IPO is the right growth option for your business.

To find out more, contact Drew Cordell [email protected], + 44 20 7951 1838

Relevant programmes

About EYEY is a global leader in assurance, tax, transaction and advisory services. The insights and quality services we deliver help build trust and confidence in the capital markets and in economies the world over. We develop outstanding leaders who team to deliver on our promises to all of our stakeholders. In so doing, we play a critical role in building a better working world for our people, for our clients and for our communities.

EY refers to the global organization and may refer to one or more of the member firms of Ernst & Young Global Limited, each of which is a separate legal entity. Ernst & Young Global Limited, a UK company limited by guarantee, does not provide services to clients. For more information about our organization, please visit ey.com.

About EY’s IPO services EY is a leader in helping to take companies public worldwide. With decades of experience, our global network is dedicated to serving market leaders and helping businesses evaluate the pros and cons of an IPO. We demystify the process by offering IPO readiness assessments, IPO preparation, project management and execution services, all of which help prepare you for life in the public spotlight. Our Global IPO Center of Excellence is a virtual hub which provides access to our IPO knowledge, tools, thought leadership and contacts from around the world in one easy-to-use source. www.ey.com/ipocenter

Ernst & Young LLPThe UK firm Ernst & Young LLP is a limited liability partnership registered in England and Wales with registered number OC300001 and is a member firm of Ernst & Young Global Limited.

Ernst & Young LLP, 1 More London Place, London, SE1 2AF.

© 2014 Ernst & Young LLP. Published in the UK. All Rights Reserved.

ED None

1491989.indd (UK) 12/14. Artwork by Creative Services Group Design.

In line with EY’s commitment to minimise its impact on the environment, this document has been printed on paper with a high recycled content.

Information in this publication is intended to provide only a general outline of the subjects covered. It should neither be regarded as comprehensive nor sufficient for making decisions, nor should it be used in place of professional advice. Ernst & Young LLP accepts no responsibility for any loss arising from any action taken or not taken by anyone using this material.

ey.com/uk

EY | Assurance | Tax | Transactions | Advisory