Embed Size (px)

Citation preview

Extensions to the Black-Scholes EquationMATH 472 Financial Mathematics

J. Robert Buchanan

2018

Objectives

In this lesson we will learn to:I model the value of a security paying dividends at a

continuous rate,I price European options on securities that pay dividends at

a continuous rate.

Dividends

I We have versions of the Put-Call Parity formula whichinclude the effects of dividends:

Pe + Se−δ T = Ce + K e−r T (continuous)

Pe + S(0)− δn∑

i=1

S(t−i )e−r ti = Ce + K e−r T (discrete)

I We do not have pricing formulas for the optionsthemselves. We explore modifications and extensions tothe Black-Scholes partial differential equation and itssolution in this lesson.

Basic Problem for the European Call

The non-dividend-paying stock is assumed to obey thestochastic process

dS = µS dt + σ S dW (t)

and the European call solves the initial boundary valueproblem:

r F = Ft + r S FS +12σ2S2FSS for (S, t) in [0,∞)× [0,T ],

F (S,T ) = (S(T )− K )+ for S > 0,F (0, t) = 0 for 0 ≤ t < T ,F (S, t) = S − K e−r(T−t) as S →∞.

Stock Pays Continuous DividendsAssumption: the stock pays dividends at a continuous rateproportional to the value of the stock

I What is a suitable expression for the dividend yield(dividend paid per unit time)?

dividend per unit time = δ S

I How much dividend is paid in a short time interval dt?

dividend paid = δ S dt

I What stochastic differential equation would the value of thestock paying a continuous proportional dividend obey?

dS = (µ− δ)S dt + σ S dW (t)

Stock Pays Continuous DividendsAssumption: the stock pays dividends at a continuous rateproportional to the value of the stock

I What is a suitable expression for the dividend yield(dividend paid per unit time)?

dividend per unit time = δ S

I How much dividend is paid in a short time interval dt?

dividend paid = δ S dt

I What stochastic differential equation would the value of thestock paying a continuous proportional dividend obey?

dS = (µ− δ)S dt + σ S dW (t)

Suppose F (S, t) is the value of a European call option on thestock paying a continuous dividend. F obeys the followingstochastic differential equation:

dF =

((µ− δ)S FS +

12σ2S2FSS + Ft

)dt + σ S FS dW (t).

As before, we wish to eliminate the random part of this equationby creating a portfolio of a long position in the call option and ashort position in ∆ shares of the stock.

Π = F − (∆)S

Suppose F (S, t) is the value of a European call option on thestock paying a continuous dividend. F obeys the followingstochastic differential equation:

dF =

((µ− δ)S FS +

12σ2S2FSS + Ft

)dt + σ S FS dW (t).

As before, we wish to eliminate the random part of this equationby creating a portfolio of a long position in the call option and ashort position in ∆ shares of the stock.

Π = F − (∆)S

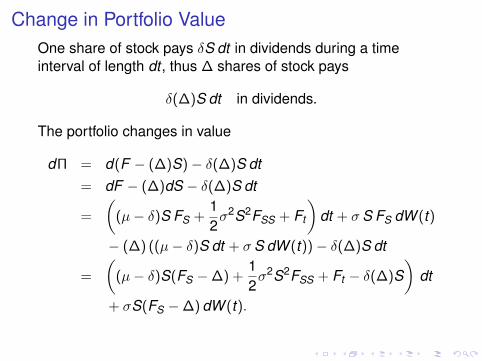

Change in Portfolio ValueOne share of stock pays δS dt in dividends during a timeinterval of length dt , thus ∆ shares of stock pays

δ(∆)S dt in dividends.

The portfolio changes in value

dΠ = d(F − (∆)S)− δ(∆)S dt= dF − (∆)dS − δ(∆)S dt

=

((µ− δ)S FS +

12σ2S2FSS + Ft

)dt + σ S FS dW (t)

− (∆) ((µ− δ)S dt + σ S dW (t))− δ(∆)S dt

=

((µ− δ)S(FS −∆) +

12σ2S2FSS + Ft − δ(∆)S

)dt

+ σS(FS −∆) dW (t).

Change in Portfolio ValueOne share of stock pays δS dt in dividends during a timeinterval of length dt , thus ∆ shares of stock pays

δ(∆)S dt in dividends.

The portfolio changes in value

dΠ = d(F − (∆)S)− δ(∆)S dt= dF − (∆)dS − δ(∆)S dt

=

((µ− δ)S FS +

12σ2S2FSS + Ft

)dt + σ S FS dW (t)

− (∆) ((µ− δ)S dt + σ S dW (t))− δ(∆)S dt

=

((µ− δ)S(FS −∆) +

12σ2S2FSS + Ft − δ(∆)S

)dt

+ σS(FS −∆) dW (t).

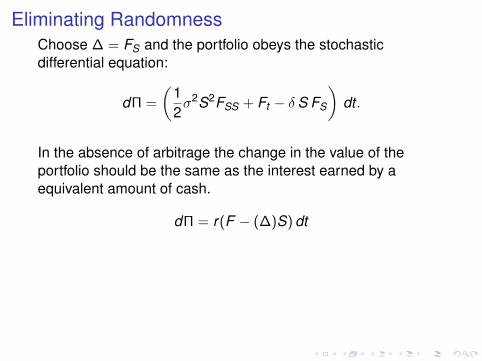

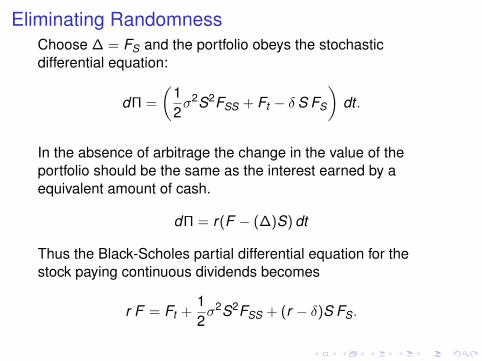

Eliminating RandomnessChoose ∆ = FS and the portfolio obeys the stochasticdifferential equation:

dΠ =

(12σ2S2FSS + Ft − δ S FS

)dt .

In the absence of arbitrage the change in the value of theportfolio should be the same as the interest earned by aequivalent amount of cash.

dΠ = r(F − (∆)S) dt

Thus the Black-Scholes partial differential equation for thestock paying continuous dividends becomes

r F = Ft +12σ2S2FSS + (r − δ)S FS.

Eliminating RandomnessChoose ∆ = FS and the portfolio obeys the stochasticdifferential equation:

dΠ =

(12σ2S2FSS + Ft − δ S FS

)dt .

In the absence of arbitrage the change in the value of theportfolio should be the same as the interest earned by aequivalent amount of cash.

dΠ = r(F − (∆)S) dt

Thus the Black-Scholes partial differential equation for thestock paying continuous dividends becomes

r F = Ft +12σ2S2FSS + (r − δ)S FS.

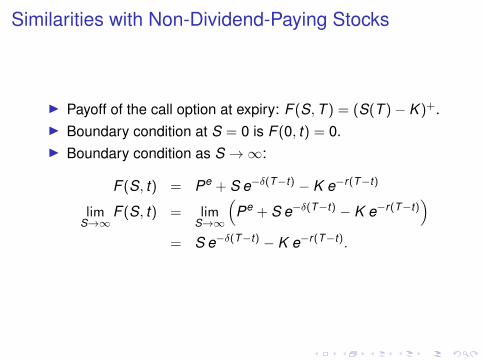

Similarities with Non-Dividend-Paying Stocks

I Payoff of the call option at expiry: F (S,T ) = (S(T )− K )+.I Boundary condition at S = 0 is F (0, t) = 0.I Boundary condition as S →∞:

F (S, t) = Pe + S e−δ(T−t) − K e−r(T−t)

limS→∞

F (S, t) = limS→∞

(Pe + S e−δ(T−t) − K e−r(T−t)

)= S e−δ(T−t) − K e−r(T−t).

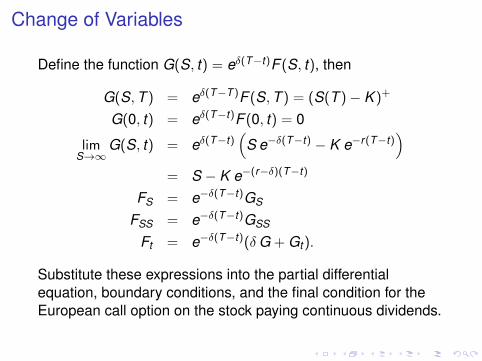

Change of Variables

Define the function G(S, t) = eδ(T−t)F (S, t), then

G(S,T ) = eδ(T−T )F (S,T ) = (S(T )− K )+

G(0, t) = eδ(T−t)F (0, t) = 0

limS→∞

G(S, t) = eδ(T−t)(

S e−δ(T−t) − K e−r(T−t))

= S − K e−(r−δ)(T−t)

FS = e−δ(T−t)GS

FSS = e−δ(T−t)GSS

Ft = e−δ(T−t)(δG + Gt ).

Substitute these expressions into the partial differentialequation, boundary conditions, and the final condition for theEuropean call option on the stock paying continuous dividends.

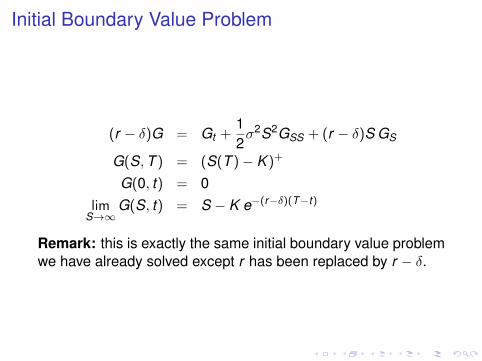

Initial Boundary Value Problem

(r − δ)G = Gt +12σ2S2GSS + (r − δ)S GS

G(S,T ) = (S(T )− K )+

G(0, t) = 0lim

S→∞G(S, t) = S − K e−(r−δ)(T−t)

Remark: this is exactly the same initial boundary value problemwe have already solved except r has been replaced by r − δ.

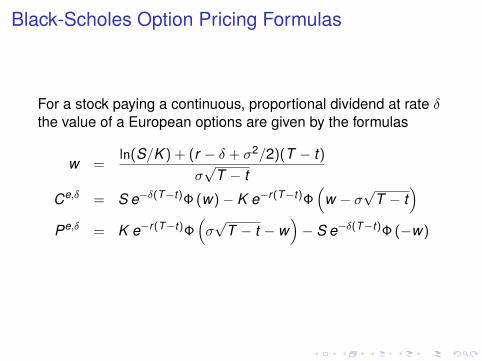

Black-Scholes Option Pricing Formulas

For a stock paying a continuous, proportional dividend at rate δthe value of a European options are given by the formulas

w =ln(S/K ) + (r − δ + σ2/2)(T − t)

σ√

T − t

Ce,δ = S e−δ(T−t)Φ (w)− K e−r(T−t)Φ(

w − σ√

T − t)

Pe,δ = K e−r(T−t)Φ(σ√

T − t − w)− S e−δ(T−t)Φ (−w)

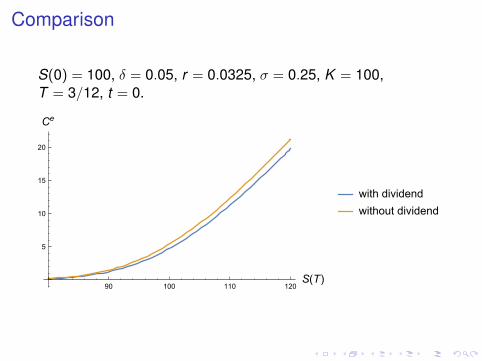

Comparison

S(0) = 100, δ = 0.05, r = 0.0325, σ = 0.25, K = 100,T = 3/12, t = 0.

90 100 110 120S(T)

5

10

15

20

Ce

with dividend

without dividend

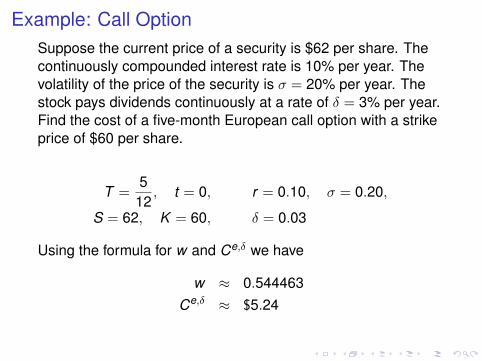

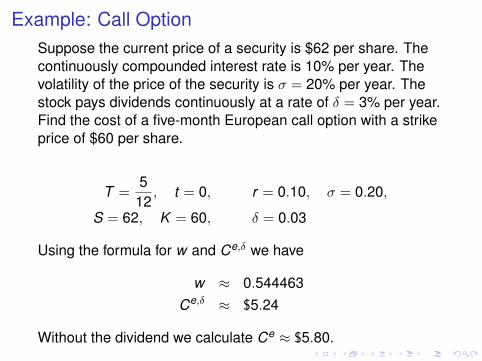

Example: Call OptionSuppose the current price of a security is $62 per share. Thecontinuously compounded interest rate is 10% per year. Thevolatility of the price of the security is σ = 20% per year. Thestock pays dividends continuously at a rate of δ = 3% per year.Find the cost of a five-month European call option with a strikeprice of $60 per share.

T =512, t = 0, r = 0.10, σ = 0.20,

S = 62, K = 60, δ = 0.03

Using the formula for w and Ce,δ we have

w ≈ 0.544463Ce,δ ≈ $5.24

Without the dividend we calculate Ce ≈ $5.80.

Example: Call OptionSuppose the current price of a security is $62 per share. Thecontinuously compounded interest rate is 10% per year. Thevolatility of the price of the security is σ = 20% per year. Thestock pays dividends continuously at a rate of δ = 3% per year.Find the cost of a five-month European call option with a strikeprice of $60 per share.

T =512, t = 0, r = 0.10, σ = 0.20,

S = 62, K = 60, δ = 0.03

Using the formula for w and Ce,δ we have

w ≈ 0.544463Ce,δ ≈ $5.24

Without the dividend we calculate Ce ≈ $5.80.

Example: Call OptionSuppose the current price of a security is $62 per share. Thecontinuously compounded interest rate is 10% per year. Thevolatility of the price of the security is σ = 20% per year. Thestock pays dividends continuously at a rate of δ = 3% per year.Find the cost of a five-month European call option with a strikeprice of $60 per share.

T =512, t = 0, r = 0.10, σ = 0.20,

S = 62, K = 60, δ = 0.03

Using the formula for w and Ce,δ we have

w ≈ 0.544463Ce,δ ≈ $5.24

Without the dividend we calculate Ce ≈ $5.80.

Example: Put Option

Suppose the current price of a security is $97 per share. Thestock pays a continuous dividend at a yield of 6.5% per year.The continuously compounded interest rate is 8% per year. Thevolatility of the price of the security is σ = 45% per year. Findthe cost of a three-month European put option with a strikeprice of $95 per share.

T = 1/4, t = 0, r = 0.08, σ = 0.45,δ = 0.065, S = 97, K = 95.

Using the formulas for w and Pe,δ we obtain

w ≈ 0.221763Pe,δ ≈ $7.34

Example: Put Option

Suppose the current price of a security is $97 per share. Thestock pays a continuous dividend at a yield of 6.5% per year.The continuously compounded interest rate is 8% per year. Thevolatility of the price of the security is σ = 45% per year. Findthe cost of a three-month European put option with a strikeprice of $95 per share.

T = 1/4, t = 0, r = 0.08, σ = 0.45,δ = 0.065, S = 97, K = 95.

Using the formulas for w and Pe,δ we obtain

w ≈ 0.221763Pe,δ ≈ $7.34

Useful Result

Lemma

S e−δ(T−t)φ (w) = K e−r(T−t)φ(

w − σ√

T − t)

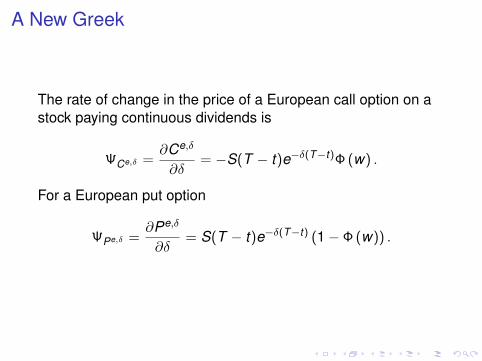

A New Greek

The rate of change in the price of a European call option on astock paying continuous dividends is

ΨCe,δ =∂Ce,δ

∂δ= −S(T − t)e−δ(T−t)Φ (w) .

For a European put option

ΨPe,δ =∂Pe,δ

∂δ= S(T − t)e−δ(T−t) (1− Φ (w)) .

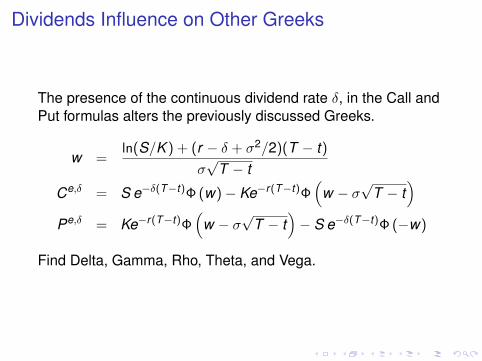

Dividends Influence on Other Greeks

The presence of the continuous dividend rate δ, in the Call andPut formulas alters the previously discussed Greeks.

w =ln(S/K ) + (r − δ + σ2/2)(T − t)

σ√

T − t

Ce,δ = S e−δ(T−t)Φ (w)− Ke−r(T−t)Φ(

w − σ√

T − t)

Pe,δ = Ke−r(T−t)Φ(

w − σ√

T − t)− S e−δ(T−t)Φ (−w)

Find Delta, Gamma, Rho, Theta, and Vega.

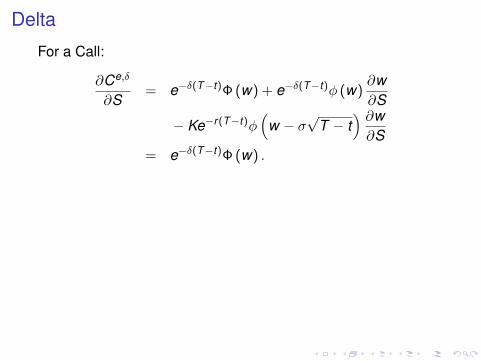

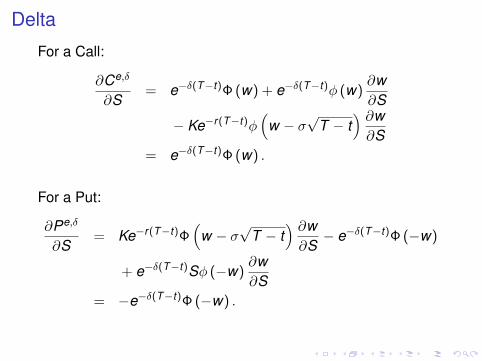

Delta

For a Call:

∂Ce,δ

∂S= e−δ(T−t)Φ (w) + e−δ(T−t)φ (w)

∂w∂S

− Ke−r(T−t)φ(

w − σ√

T − t) ∂w∂S

= e−δ(T−t)Φ (w) .

For a Put:

∂Pe,δ

∂S= Ke−r(T−t)Φ

(w − σ

√T − t

) ∂w∂S− e−δ(T−t)Φ (−w)

+ e−δ(T−t)Sφ (−w)∂w∂S

= −e−δ(T−t)Φ (−w) .

Delta

For a Call:

∂Ce,δ

∂S= e−δ(T−t)Φ (w) + e−δ(T−t)φ (w)

∂w∂S

− Ke−r(T−t)φ(

w − σ√

T − t) ∂w∂S

= e−δ(T−t)Φ (w) .

For a Put:

∂Pe,δ

∂S= Ke−r(T−t)Φ

(w − σ

√T − t

) ∂w∂S− e−δ(T−t)Φ (−w)

+ e−δ(T−t)Sφ (−w)∂w∂S

= −e−δ(T−t)Φ (−w) .

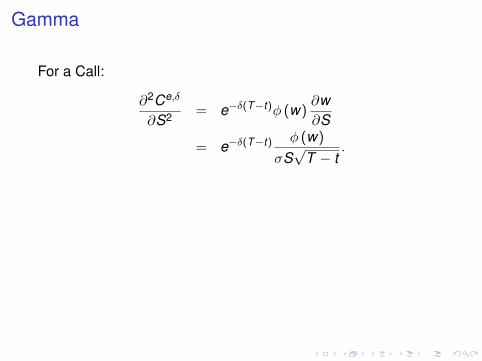

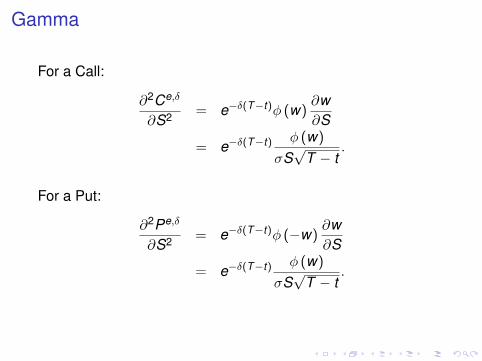

Gamma

For a Call:

∂2Ce,δ

∂S2 = e−δ(T−t)φ (w)∂w∂S

= e−δ(T−t) φ (w)

σS√

T − t.

For a Put:

∂2Pe,δ

∂S2 = e−δ(T−t)φ (−w)∂w∂S

= e−δ(T−t) φ (w)

σS√

T − t.

Gamma

For a Call:

∂2Ce,δ

∂S2 = e−δ(T−t)φ (w)∂w∂S

= e−δ(T−t) φ (w)

σS√

T − t.

For a Put:

∂2Pe,δ

∂S2 = e−δ(T−t)φ (−w)∂w∂S

= e−δ(T−t) φ (w)

σS√

T − t.

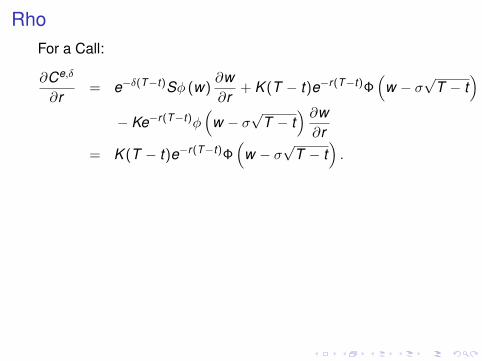

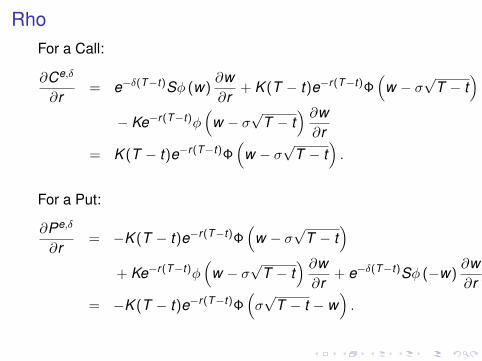

RhoFor a Call:

∂Ce,δ

∂r= e−δ(T−t)Sφ (w)

∂w∂r

+ K (T − t)e−r(T−t)Φ(

w − σ√

T − t)

− Ke−r(T−t)φ(

w − σ√

T − t) ∂w∂r

= K (T − t)e−r(T−t)Φ(

w − σ√

T − t).

For a Put:

∂Pe,δ

∂r= −K (T − t)e−r(T−t)Φ

(w − σ

√T − t

)+ Ke−r(T−t)φ

(w − σ

√T − t

) ∂w∂r

+ e−δ(T−t)Sφ (−w)∂w∂r

= −K (T − t)e−r(T−t)Φ(σ√

T − t − w).

RhoFor a Call:

∂Ce,δ

∂r= e−δ(T−t)Sφ (w)

∂w∂r

+ K (T − t)e−r(T−t)Φ(

w − σ√

T − t)

− Ke−r(T−t)φ(

w − σ√

T − t) ∂w∂r

= K (T − t)e−r(T−t)Φ(

w − σ√

T − t).

For a Put:

∂Pe,δ

∂r= −K (T − t)e−r(T−t)Φ

(w − σ

√T − t

)+ Ke−r(T−t)φ

(w − σ

√T − t

) ∂w∂r

+ e−δ(T−t)Sφ (−w)∂w∂r

= −K (T − t)e−r(T−t)Φ(σ√

T − t − w).

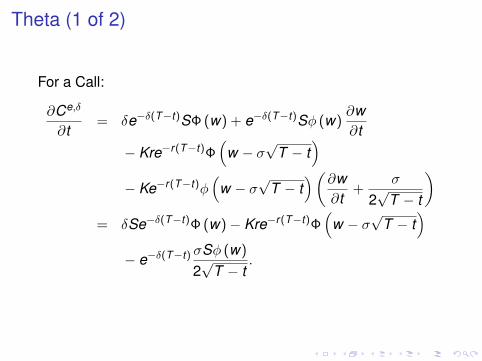

Theta (1 of 2)

For a Call:

∂Ce,δ

∂t= δe−δ(T−t)SΦ (w) + e−δ(T−t)Sφ (w)

∂w∂t

− Kre−r(T−t)Φ(

w − σ√

T − t)

− Ke−r(T−t)φ(

w − σ√

T − t)(∂w

∂t+

σ

2√

T − t

)= δSe−δ(T−t)Φ (w)− Kre−r(T−t)Φ

(w − σ

√T − t

)− e−δ(T−t) σSφ (w)

2√

T − t.

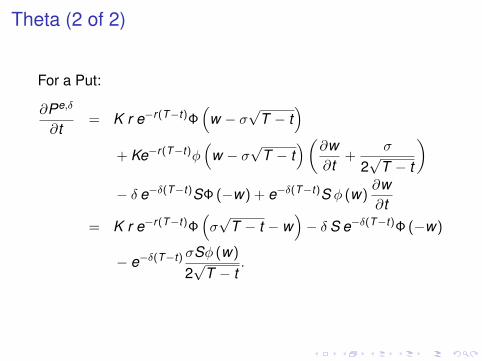

Theta (2 of 2)

For a Put:

∂Pe,δ

∂t= K r e−r(T−t)Φ

(w − σ

√T − t

)+ Ke−r(T−t)φ

(w − σ

√T − t

)(∂w∂t

+σ

2√

T − t

)− δ e−δ(T−t)SΦ (−w) + e−δ(T−t)S φ (w)

∂w∂t

= K r e−r(T−t)Φ(σ√

T − t − w)− δ S e−δ(T−t)Φ (−w)

− e−δ(T−t) σSφ (w)

2√

T − t.

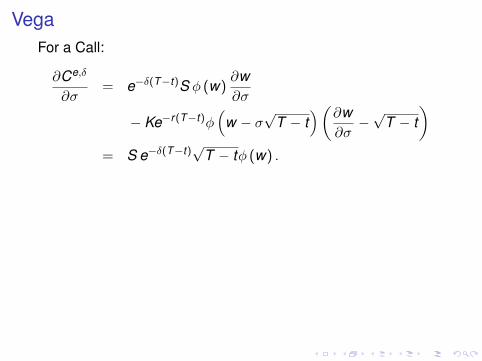

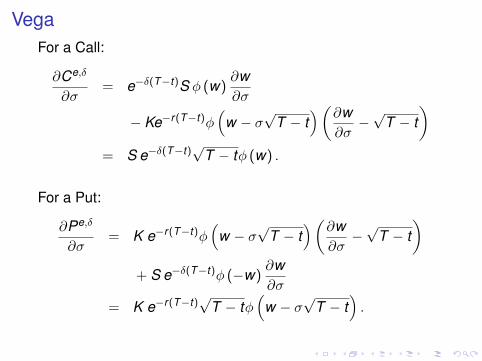

VegaFor a Call:

∂Ce,δ

∂σ= e−δ(T−t)S φ (w)

∂w∂σ

− Ke−r(T−t)φ(

w − σ√

T − t)(∂w

∂σ−√

T − t)

= S e−δ(T−t)√

T − tφ (w) .

For a Put:

∂Pe,δ

∂σ= K e−r(T−t)φ

(w − σ

√T − t

)(∂w∂σ−√

T − t)

+ S e−δ(T−t)φ (−w)∂w∂σ

= K e−r(T−t)√

T − tφ(

w − σ√

T − t).

VegaFor a Call:

∂Ce,δ

∂σ= e−δ(T−t)S φ (w)

∂w∂σ

− Ke−r(T−t)φ(

w − σ√

T − t)(∂w

∂σ−√

T − t)

= S e−δ(T−t)√

T − tφ (w) .

For a Put:

∂Pe,δ

∂σ= K e−r(T−t)φ

(w − σ

√T − t

)(∂w∂σ−√

T − t)

+ S e−δ(T−t)φ (−w)∂w∂σ

= K e−r(T−t)√

T − tφ(

w − σ√

T − t).

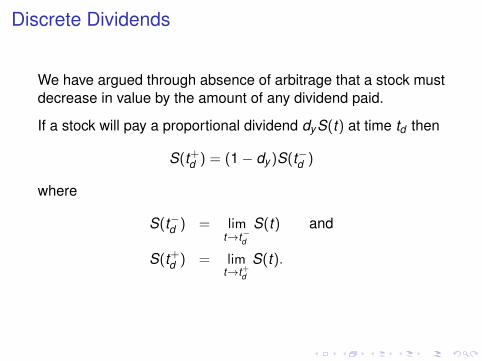

Discrete Dividends

We have argued through absence of arbitrage that a stock mustdecrease in value by the amount of any dividend paid.

If a stock will pay a proportional dividend dyS(t) at time td then

S(t+d ) = (1− dy )S(t−d )

where

S(t−d ) = limt→t−d

S(t) and

S(t+d ) = limt→t+d

S(t).

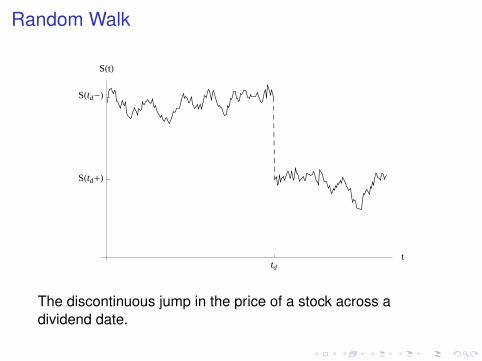

Random Walk

tdt

SHtd-L

SHtd+L

SHtL

The discontinuous jump in the price of a stock across adividend date.

Dirac Delta Function

The Dirac Delta function D (t), is a function with the followingproperties:I D(t) = 0 for all t 6= 0.

I∫ ∞−∞

D (t) dt = 1

I∫ ∞−∞

f (t)D (t) dt = f (0) for any continuous function f (t)

defined on the real numbers.

Thus if S(t) represents a stock which pays a single discretedividend at time td then S obeys the stochastic differentialequation:

dS = (µ− dy D (t − td ))S dt + σS dW (t).

Dirac Delta Function

The Dirac Delta function D (t), is a function with the followingproperties:I D(t) = 0 for all t 6= 0.

I∫ ∞−∞

D (t) dt = 1

I∫ ∞−∞

f (t)D (t) dt = f (0) for any continuous function f (t)

defined on the real numbers.Thus if S(t) represents a stock which pays a single discretedividend at time td then S obeys the stochastic differentialequation:

dS = (µ− dy D (t − td ))S dt + σS dW (t).

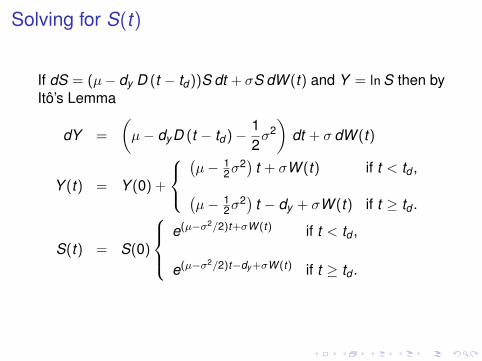

Solving for S(t)

If dS = (µ− dy D (t − td ))S dt + σS dW (t) and Y = ln S then byItô’s Lemma

dY =

(µ− dyD (t − td )− 1

2σ2)

dt + σ dW (t)

Y (t) = Y (0) +

(µ− 1

2σ2) t + σW (t) if t < td ,(

µ− 12σ

2) t − dy + σW (t) if t ≥ td .

S(t) = S(0)

e(µ−σ2/2)t+σW (t) if t < td ,

e(µ−σ2/2)t−dy+σW (t) if t ≥ td .

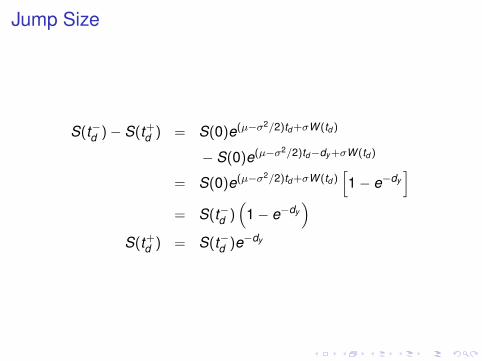

Jump Size

S(t−d )− S(t+d ) = S(0)e(µ−σ2/2)td+σW (td )

− S(0)e(µ−σ2/2)td−dy+σW (td )

= S(0)e(µ−σ2/2)td+σW (td )[1− e−dy

]= S(t−d )

(1− e−dy

)S(t+d ) = S(t−d )e−dy

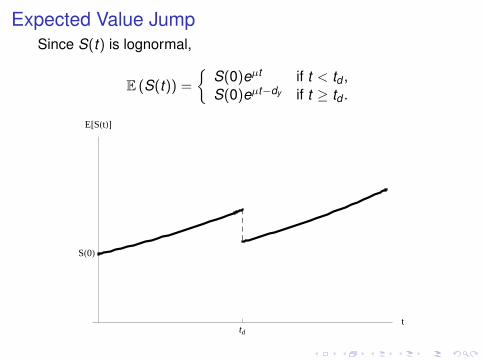

Expected Value JumpSince S(t) is lognormal,

E (S(t)) =

{S(0)eµt if t < td ,S(0)eµt−dy if t ≥ td .

tdt

SH0L

E@SHtLD

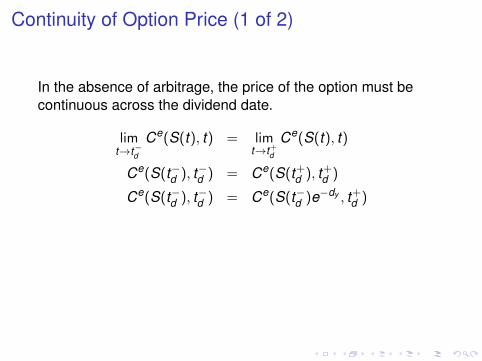

Continuity of Option Price (1 of 2)

In the absence of arbitrage, the price of the option must becontinuous across the dividend date.

limt→t−d

Ce(S(t), t) = limt→t+d

Ce(S(t), t)

Ce(S(t−d ), t−d ) = Ce(S(t+d ), t+d )

Ce(S(t−d ), t−d ) = Ce(S(t−d )e−dy , t+d )

Remark: the last equation says that the value of the call optionbefore the dividend payment is the same as the value of theoption after the dividend payment, but at stock price S(t−d )e−dy .

Continuity of Option Price (1 of 2)

In the absence of arbitrage, the price of the option must becontinuous across the dividend date.

limt→t−d

Ce(S(t), t) = limt→t+d

Ce(S(t), t)

Ce(S(t−d ), t−d ) = Ce(S(t+d ), t+d )

Ce(S(t−d ), t−d ) = Ce(S(t−d )e−dy , t+d )

Remark: the last equation says that the value of the call optionbefore the dividend payment is the same as the value of theoption after the dividend payment, but at stock price S(t−d )e−dy .

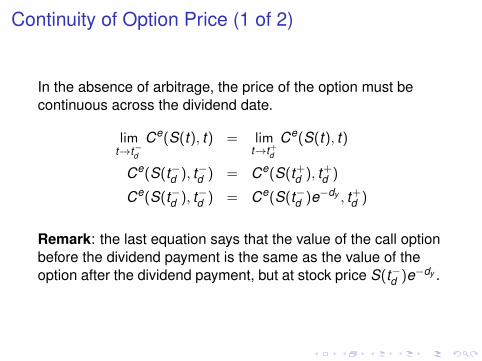

Continuity of Option Price (2 of 2)

Ce(S(t−d ), t−d ) = Ce(S(t−d )e−dy , t+d )

Remarks:I The value of the call option will change discontinuously

across the dividend date as a function of S.I However, the price of the option is made continuous by

equating the value of the option just before the dividend ispaid with the value of the option just after the dividend ispaid.

I The value of the stock underlying the option has beenadjusted to S(t+d ) = S(t−d )e−dy .

I Since the owner of the call option receives no benefit fromthe paid dividend, the option price is affected by thedividend payment.

Pricing the Option

Separate the life of the option into two intervals, [0, td ) and(td ,T ].

I On the interval (td ,T ] no dividends are paid and theoriginal formula for the price of a call option can be used.

I The post dividend value of the stock is Se−dy .I For td < t ≤ T ,

Ce,δ = e−dy SΦ (w)− Ke−r(T−t)Φ(

w − σ√

T − t)

Pre-dividend Pricing

At t = t+d the value of the call option is

Ce(S(t+d ), t+d ) = S(t+d )Φ (w)− Ke−r(T−t+d )Φ

(w − σ

√T − t+d

).

Immediately before the dividend date the value of the calloption is

Ce(S(t−d ), t−d ) = Ce(S(t−d )e−dy , t+d )

= S(t−d )e−dy Φ (w)

− Ke−r(T−t+d )Φ

(w − σ

√T − t+d

).

Note: the price of the stock underlying the option has beenscaled by the factor e−dy .

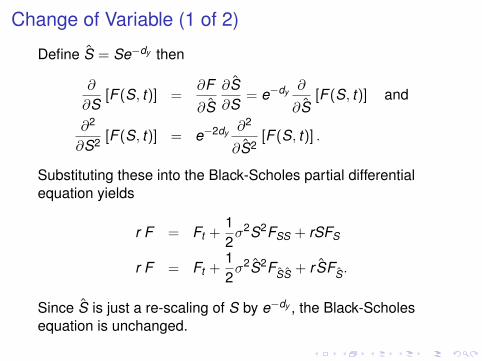

Change of Variable (1 of 2)

Define S = Se−dy then

∂

∂S[F (S, t)] =

∂F

∂S

∂S∂S

= e−dy∂

∂S[F (S, t)] and

∂2

∂S2 [F (S, t)] = e−2dy∂2

∂S2[F (S, t)] .

Substituting these into the Black-Scholes partial differentialequation yields

r F = Ft +12σ2S2FSS + rSFS

r F = Ft +12σ2S2FSS + r SFS.

Since S is just a re-scaling of S by e−dy , the Black-Scholesequation is unchanged.

Change of Variable (1 of 2)

Define S = Se−dy then

∂

∂S[F (S, t)] =

∂F

∂S

∂S∂S

= e−dy∂

∂S[F (S, t)] and

∂2

∂S2 [F (S, t)] = e−2dy∂2

∂S2[F (S, t)] .

Substituting these into the Black-Scholes partial differentialequation yields

r F = Ft +12σ2S2FSS + rSFS

r F = Ft +12σ2S2FSS + r SFS.

Since S is just a re-scaling of S by e−dy , the Black-Scholesequation is unchanged.

Change of Variable (2 of 2)

We have the PDE:

r F = Ft +12σ2S2FSS + r SFS.

What about the boundary and final conditions?

F (S,T ) = (S − K )+ = (Se−dy − K )+ = e−dy (S − Kedy )+

F (0, t) = F (0 · e−dy , t) = 0

limS→∞

F (S, t) = e−dy(

S − Kedy−r(T−t))

Change of Variable (2 of 2)

We have the PDE:

r F = Ft +12σ2S2FSS + r SFS.

What about the boundary and final conditions?

F (S,T ) = (S − K )+ = (Se−dy − K )+ = e−dy (S − Kedy )+

F (0, t) = F (0 · e−dy , t) = 0

limS→∞

F (S, t) = e−dy(

S − Kedy−r(T−t))

Pre-dividend Pricing

For 0 ≤ t < td use the established European call option pricingformula for e−dy call options with a strike price of Kedy .

Thus for t < td ,

Ce,δ = e−dy[SΦ (w)− Kedy−r(T−t)Φ

(w − σ

√T − t

)].

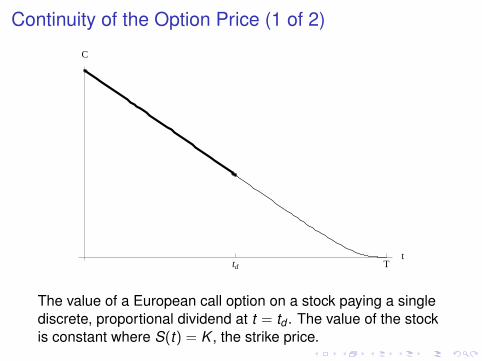

Continuity of the Option Price (1 of 2)

td Tt

C

The value of a European call option on a stock paying a singlediscrete, proportional dividend at t = td . The value of the stockis constant where S(t) = K , the strike price.

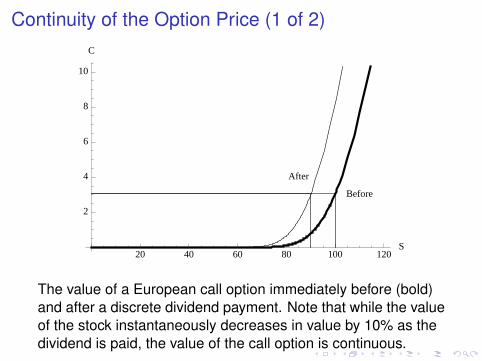

Continuity of the Option Price (1 of 2)

Before

After

20 40 60 80 100 120S

2

4

6

8

10

C

The value of a European call option immediately before (bold)and after a discrete dividend payment. Note that while the valueof the stock instantaneously decreases in value by 10% as thedividend is paid, the value of the call option is continuous.

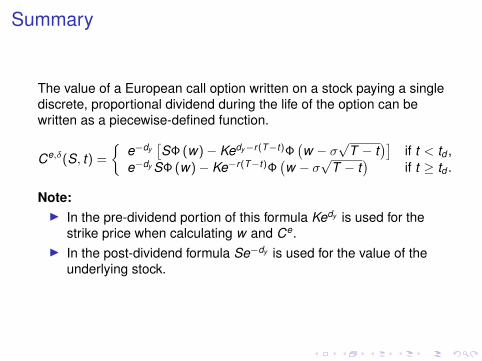

Summary

The value of a European call option written on a stock paying a singlediscrete, proportional dividend during the life of the option can bewritten as a piecewise-defined function.

Ce,δ(S, t) =

{e−dy

[SΦ (w)− Kedy−r(T−t)Φ

(w − σ

√T − t

)]if t < td ,

e−dy SΦ (w)− Ke−r(T−t)Φ(w − σ

√T − t

)if t ≥ td .

Note:I In the pre-dividend portion of this formula Kedy is used for the

strike price when calculating w and Ce.I In the post-dividend formula Se−dy is used for the value of the

underlying stock.

Credits

These slides are adapted from the textbook,An Undergraduate Introduction to Financial Mathematics,3rd edition, (2012).author: J. Robert Buchananpublisher: World Scientific Publishing Co. Pte. Ltd.address: 27 Warren St., Suite 401–402, Hackensack, NJ07601ISBN: 978-9814407441