Embed Size (px)

Citation preview

Extending Credit to Bank Insiders (Reg O)

© 2020 American Bankers Association

ABA course content is not a substitute for professional legal advice.

Version 4

Extending Credit to Bank Insiders (Reg O)

© 2020 American Bankers Association

Menu

Introduction

Coverage

Lending Limits

Wrap Up

Extending Credit to Bank Insiders (Reg O)

© 2020 American Bankers Association

Introduction

Extending Credit to Bank Insiders (Reg O) defines the term bank “insider.” This course teaches the lending restrictions applied to bank insiders under Regulation O.

Version: 4.0

Review: November 2020. No significant changes. When the Federal Reserve was created in 1913, all national banks were required to become members, and state banks were allowed to become members.

While membership carried certain privileges and powers to borrow from the Federal Reserve, it also added restrictions. These included limits on lending to bank insiders to prevent conflicts of interest inside the bank. Regulation O governs such activities.

Banks are generally in business to take deposits from and loan money to their customers. Most banks have owners, usually in the form of shareholders, and are managed by boards of directors. (Mutual banks have trustees instead of boards, but the Reg O rules are the same.) Policy-making within the bank is handled by the bank's executive officers.

ABA course content is not a substitute for professional legal advice.

Page 1

Extending Credit to Bank Insiders (Reg O)

© 2020 American Bankers Association

Introduction

Executive officers, directors, or principal shareholders of a bank or of a bank holding company of which the member bank is a subsidiary, are called “insiders” and Regulation O applies to credit extended to these individuals.

When a bank makes an extension of credit to one of its insiders, it is important that the bank be just as careful as when it lends money to others in the community. In order to protect the bank, lending to insiders is regulated. Regulation O and related regulations govern lending to insiders. Additionally, prior approval by the Board may be required when certain aggregate lending limits are attained.

Objectives By the end of Extending Credit to Bank Insiders (Reg O), you will be able to

Describe who is covered by Regulation O and the rules and disclosures that must be followed Describe the lending limits and requirements when a bank makes a loan to an executive officer

Page 2

Extending Credit to Bank Insiders (Reg O)

© 2020 American Bankers Association

Introduction

Regulation O’s primary purpose is to protect the bank by making sure that all credit extended to insiders is made on a safe and sound basis and not made on a preferential basis.

Since insiders can potentially pressure the bank to make loans to them or to their businesses or family members, this regulation requires that loans to insiders be made on the same terms and conditions as those to regular customers. Loans with terms and conditions better than those offered the regular customer are “preferential” and are prohibited.

The regulation covers the following people and their related interests:

Principal shareholders Directors

Executive officers

Glossary terms:

Related interest

A company that is controlled by that person A political or campaign committee that is controlled by that person or the funds or services of which will benefit

that person

Principal shareholder A person that, directly or indirectly, owns, controls, or has power to vote more than 10 percent of any class of voting securities of the member bank. The term includes a person that controls a principal shareholder (e.g., a person that controls a bank holding company). Shares of a bank holding company, or other company owned or controlled by a member of an individual’s immediate family (spouse of an individual, the individual’s minor children, and any of the individual’s children—including adults—residing in the individual’s home) are presumed to be owned or controlled by the individual for the purposes of determining principal shareholder status.

Director A person who serves on the bank’s board of directors or the board of an affiliate not exempt from coverage. Directors are usually elected to serve by the shareholders. An advisory director is not considered to be a director for purposes of Regulation O. An advisory director is a person that: 1) is not elected by the shareholders; 2) is not authorized to vote on matters before the board of directors; and 3) provides solely general policy advice to the board of directors.

Extending Credit to Bank Insiders (Reg O)

© 2020 American Bankers Association

Executive officer A person who participates in or has the power to make major policies for the bank, including executive officers of affiliates not exempt from coverage. The chairman of the board, president, every vice president, cashier, secretary, and treasurer are presumed to be executive officer, unless an exemption applies.

Page 3

Extending Credit to Bank Insiders (Reg O)

© 2020 American Bankers Association

Coverage

When one of these insiders wants to borrow money from the bank, the bank must be careful to follow all of the rules in Regulation O, including making the necessary disclosures.

In addition, lenders must consider what is called the “tangible economic benefit rule” when making loans to insiders. This means that an extension of credit is considered made to an insider to the extent that the proceeds are transferred to the insider or are used for the tangible economic benefit of the insider.

Page 4

Extending Credit to Bank Insiders (Reg O)

© 2020 American Bankers Association

Coverage

A general lending rule in Regulation O is that a bank may not make a loan to an insider (principal shareholder, director, executive officer) on terms or conditions more favorable than the terms offered to those who are not insiders. This restriction also applies to loans made to any related interests of a bank insider.

This means the terms of the loan, such as the interest rate, the collateral required to secure the loan, and the repayment method must be substantially similar to those offered to other customers who are not bank insiders.

A loan to an insider may not pose a greater credit risk to the bank than loans made to customers who are not bank insiders.

Page 5

Extending Credit to Bank Insiders (Reg O)

© 2020 American Bankers Association

Coverage

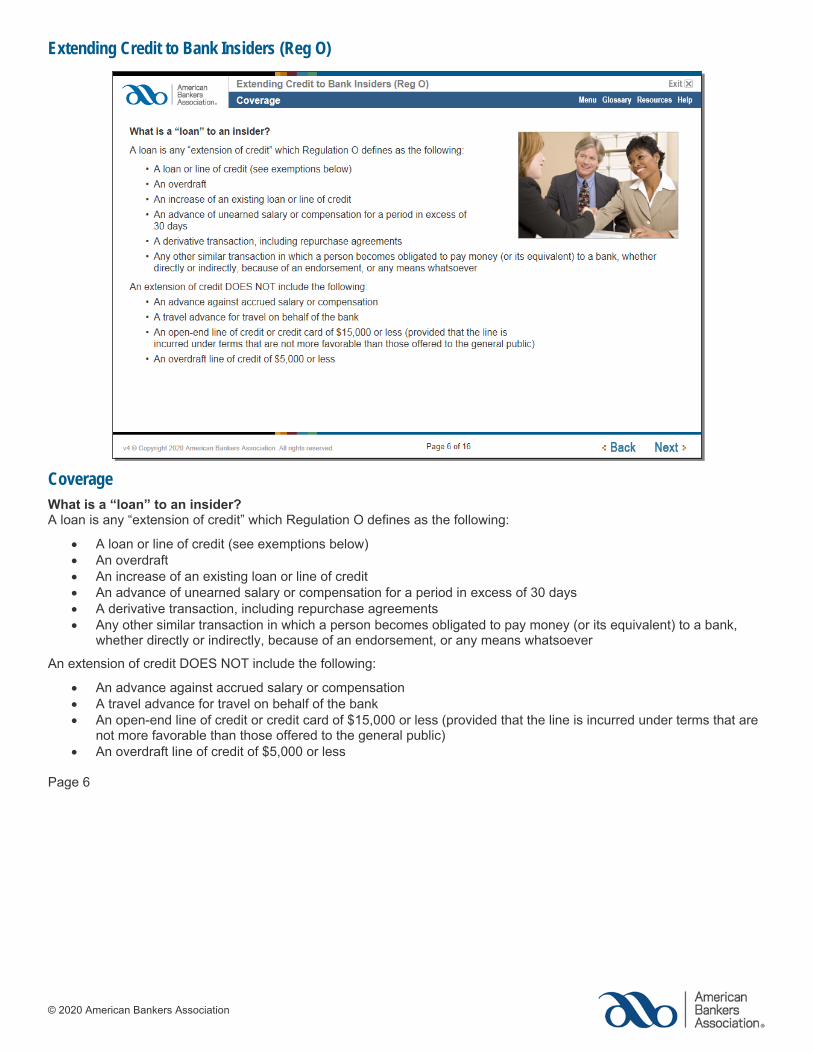

What is a “loan” to an insider? A loan is any “extension of credit” which Regulation O defines as the following:

A loan or line of credit (see exemptions below) An overdraft An increase of an existing loan or line of credit An advance of unearned salary or compensation for a period in excess of 30 days A derivative transaction, including repurchase agreements Any other similar transaction in which a person becomes obligated to pay money (or its equivalent) to a bank,

whether directly or indirectly, because of an endorsement, or any means whatsoever

An extension of credit DOES NOT include the following:

An advance against accrued salary or compensation A travel advance for travel on behalf of the bank An open-end line of credit or credit card of $15,000 or less (provided that the line is incurred under terms that are

not more favorable than those offered to the general public) An overdraft line of credit of $5,000 or less

Page 6

Extending Credit to Bank Insiders (Reg O)

© 2020 American Bankers Association

Coverage

» Roll over the images below to explore who is covered by Regulation O.

Ralph McGinty, one of the founders of the bank. He owns almost half of the bank’s stock. Yes, he is a principal shareholder, and thus an insider. Regulation O will apply to the loans the bank makes to him.

Georgia Miller, a loan processor in the note department. No, Regulation O does not apply to employees who are not executive officers.

Laura Lynn, a local business owner who sits on the bank’s board of directors. Yes, directors are insiders. Regulation O will apply to the loans the bank makes to her.

Julian Hinojosa, the bank’s president. Yes, he is an insider. Regulation O will apply to the loans the bank makes to him. The President, Chairman, Cashier, Secretary, every Vice President (unless otherwise excluded), and the Treasurer are typically considered executive officers and thus insiders.

William Hall, a retired businessman who is a long-time bank customer. He is an advisory director of the board. No, Regulation O does not apply to advisory directors, unless they act in the capacity of a regular insider.

Page 7

Extending Credit to Bank Insiders (Reg O)

© 2020 American Bankers Association

Coverage

Regulation O has additional restrictions on loans made to executive officers. Executive officers are officers with the ability to participate in major policy making functions within the bank, regardless of their titles.

A bank can define its own executive officers by a resolution of the board of directors that names them. If they are not excluded by a board resolution, the following persons will be considered executive officers:

Chairman of the Board of Directors President Each Vice President and higher (such as Senior Vice President, Executive Vice President, and so forth) Cashier Secretary Treasurer

However, even if any person is excluded by a board resolution, that person will still be considered an executive officer if he or she may make major bank policy.

Page 8

Extending Credit to Bank Insiders (Reg O)

© 2020 American Bankers Association

Coverage

In this example, ABC Bank has no board resolution designating executive officers. Of the following ABC Bank employees, which are considered an executive officer under Reg O?

» Roll over the images below to explore who is covered by Regulation O.

Harry Haywood, Executive Vice President of Information Technology Harry Haywood is an executive officer unless specifically excluded.

Merrin Salinas, New Accounts Officer Merrin Salinas is not an executive officer.

Martin Vincent, Operations Officer Martin Vincent is not an executive officer.

Patrick Jones, President Patrick Jones is an executive officer.

Steven Dungrey, Chairman of the Board Steven Dungrey is an executive officer unless specifically excluded; the Chairman of the Board is typically an executive officer.

Page 9

Extending Credit to Bank Insiders (Reg O)

© 2020 American Bankers Association

Coverage

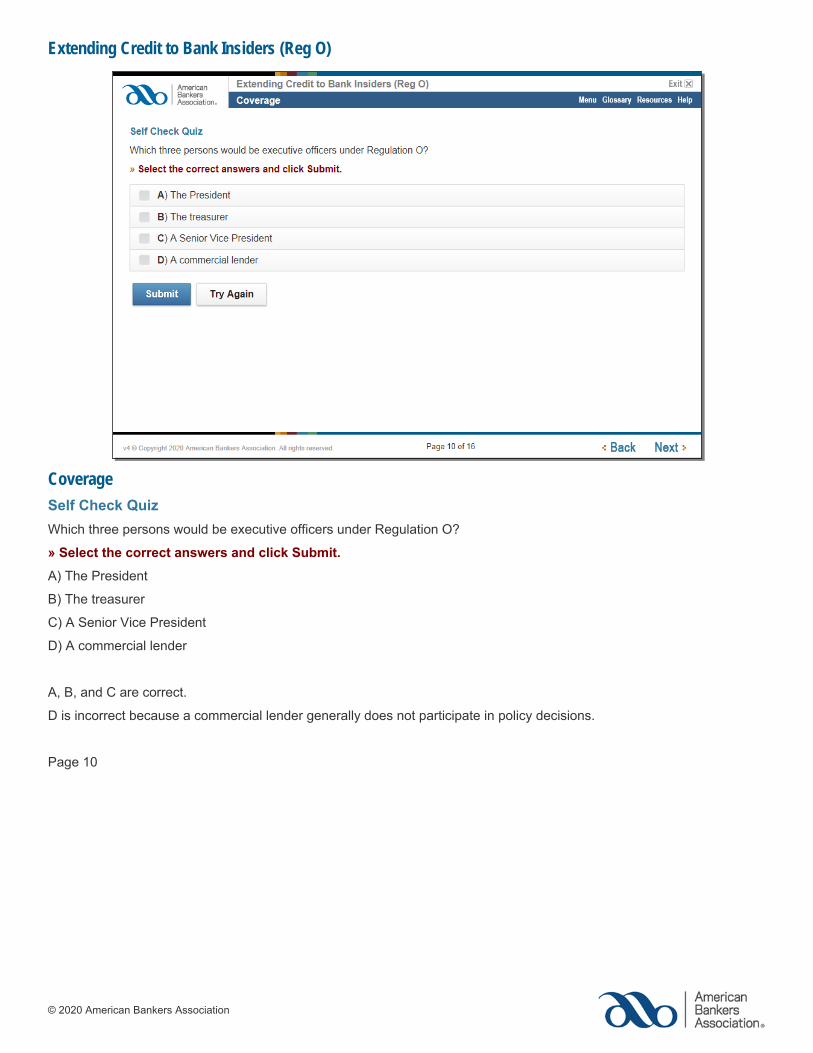

Self Check Quiz

Which three persons would be executive officers under Regulation O?

» Select the correct answers and click Submit.

A) The President

B) The treasurer

C) A Senior Vice President

D) A commercial lender

A, B, and C are correct.

D is incorrect because a commercial lender generally does not participate in policy decisions.

Page 10

Extending Credit to Bank Insiders (Reg O)

© 2020 American Bankers Association

Lending Limits

Regulation O has some additional lending limits on loans to executive officers. A bank may make a loan to an executive officer for any amount allowed to a single borrower (under the bank’s lending limit rules) if the following situations apply to the loan:

It is to finance the education of the officer’s children It is a first lien loan to finance or refinance the purchase, construction, maintenance or improvement of a

residence of the officer (only one such loan exception is allowed, yet is not limited to the primary residence) It is secured by an obligation of the U.S. Government (like a Treasury Bill) or by a segregated deposit in the bank

(such as a savings account or a CD) or by an unconditional guarantee of the U.S.

The bank can make loans to its executive officers for other purposes as long as the loan amounts, in aggregate, do not exceed the higher of either of the following:

2.5 percent of the bank’s unimpaired capital and unimpaired surplus $25,000

These are commonly called “other purpose loans” but in any event the credit extended under this section may not exceed $100,000.

Note: Check with your Reg O Officer or Chief Lending Officer for any lending limits applicable to your institution.

Page 11

Extending Credit to Bank Insiders (Reg O)

© 2020 American Bankers Association

Lending Limits

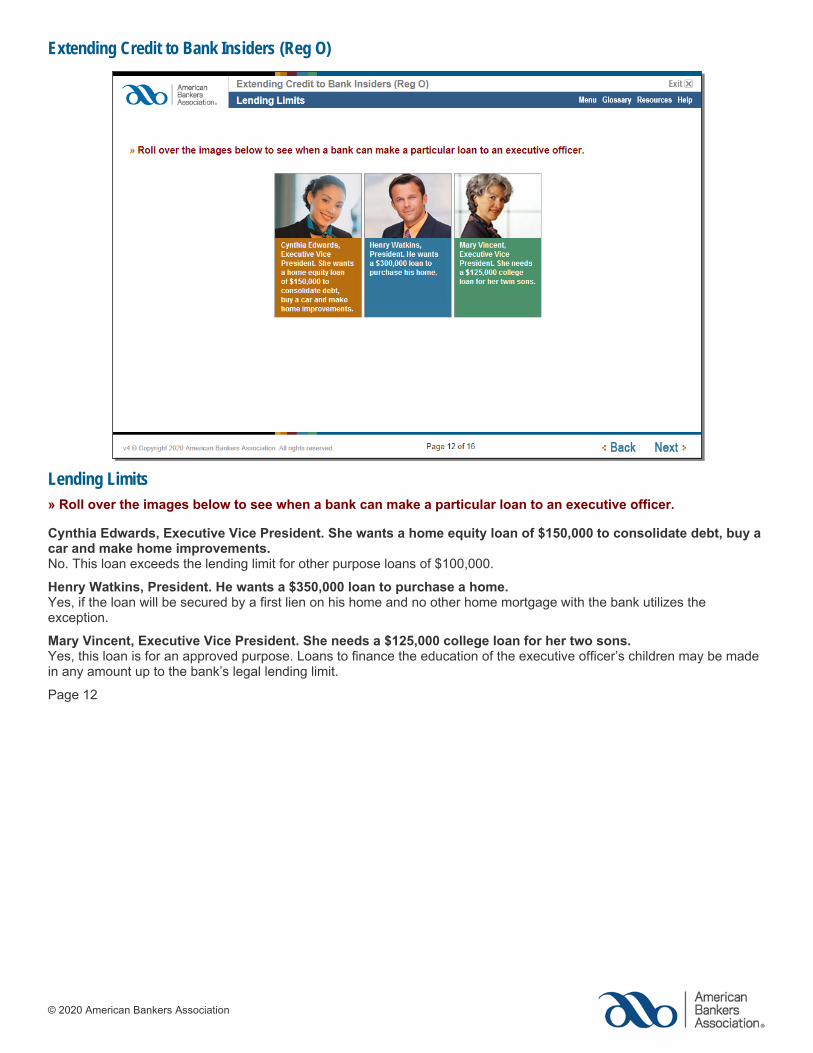

» Roll over the images below to see when a bank can make a particular loan to an executive officer.

Cynthia Edwards, Executive Vice President. She wants a home equity loan of $150,000 to consolidate debt, buy a car and make home improvements. No. This loan exceeds the lending limit for other purpose loans of $100,000.

Henry Watkins, President. He wants a $350,000 loan to purchase a home. Yes, if the loan will be secured by a first lien on his home and no other home mortgage with the bank utilizes the exception.

Mary Vincent, Executive Vice President. She needs a $125,000 college loan for her two sons. Yes, this loan is for an approved purpose. Loans to finance the education of the executive officer’s children may be made in any amount up to the bank’s legal lending limit.

Page 12

Extending Credit to Bank Insiders (Reg O)

© 2020 American Bankers Association

Lending Limits

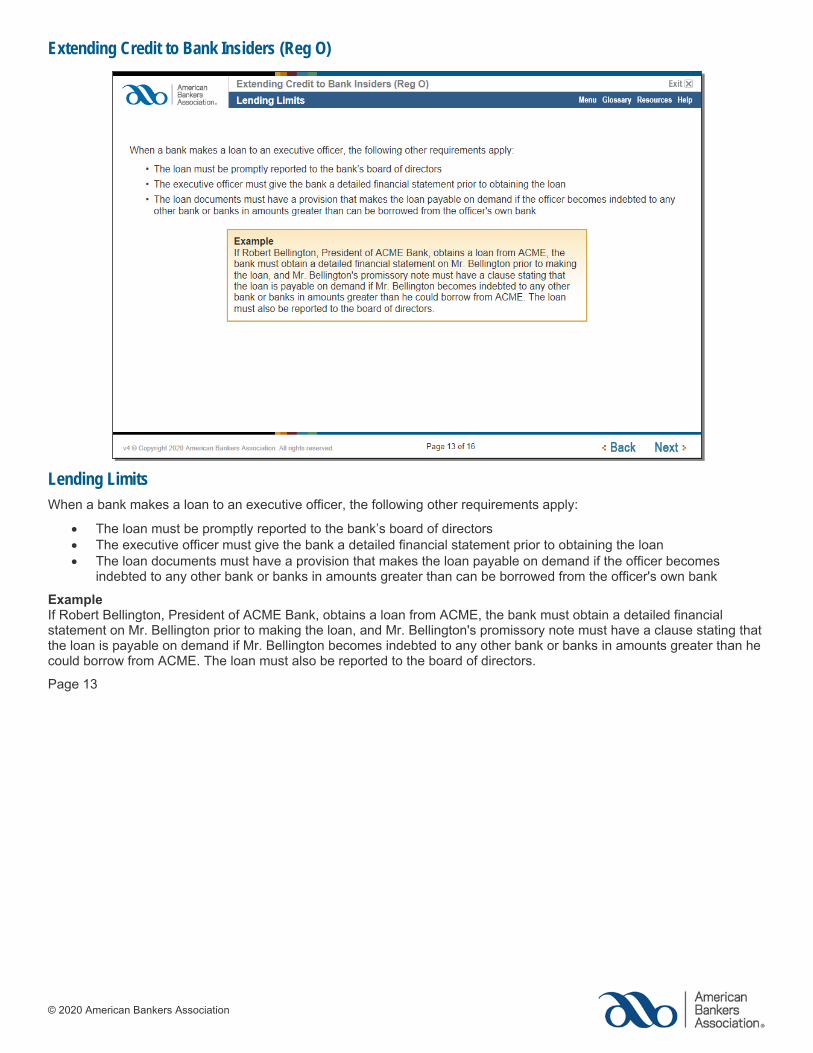

When a bank makes a loan to an executive officer, the following other requirements apply:

The loan must be promptly reported to the bank’s board of directors The executive officer must give the bank a detailed financial statement prior to obtaining the loan The loan documents must have a provision that makes the loan payable on demand if the officer becomes

indebted to any other bank or banks in amounts greater than can be borrowed from the officer's own bank

Example If Robert Bellington, President of ACME Bank, obtains a loan from ACME, the bank must obtain a detailed financial statement on Mr. Bellington prior to making the loan, and Mr. Bellington's promissory note must have a clause stating that the loan is payable on demand if Mr. Bellington becomes indebted to any other bank or banks in amounts greater than he could borrow from ACME. The loan must also be reported to the board of directors.

Page 13

Extending Credit to Bank Insiders (Reg O)

© 2020 American Bankers Association

Lending Limits

Prohibition on overdrafts Regulation O generally prohibits overdrafts on an executive officer’s or director’s own accounts. The regulation states that this prohibition does not apply to payment of inadvertent overdrafts on an account in an aggregate amount of $1,000 or less, provided the account is not overdrawn more than five business days and the executive officer or director is charged the same fee charged as any other customer of the bank in similar circumstances.

This prohibition does not apply to the payment by a member bank of an overdraft of a principal shareholder of the member bank, unless the principal shareholder is also an executive officer or director. This prohibition also does not apply to the payment by a member bank of an overdraft of a related interest of an insider.

This also does not apply if the overdraft is covered by written, preauthorized, interest-bearing overdraft protection plan or a written, preauthorized transfer of funds from another account of the insider at the bank.

Page 14

Extending Credit to Bank Insiders (Reg O)

© 2020 American Bankers Association

Lending Limits

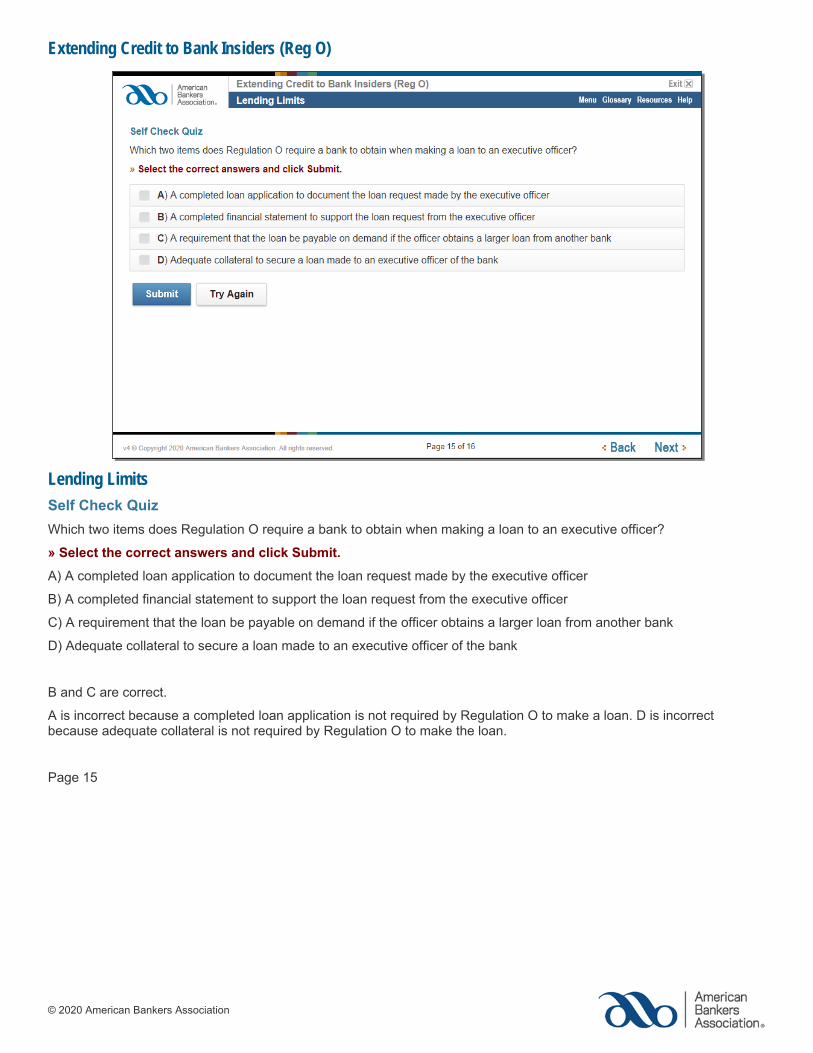

Self Check Quiz

Which two items does Regulation O require a bank to obtain when making a loan to an executive officer?

» Select the correct answers and click Submit.

A) A completed loan application to document the loan request made by the executive officer

B) A completed financial statement to support the loan request from the executive officer

C) A requirement that the loan be payable on demand if the officer obtains a larger loan from another bank

D) Adequate collateral to secure a loan made to an executive officer of the bank

B and C are correct.

A is incorrect because a completed loan application is not required by Regulation O to make a loan. D is incorrect because adequate collateral is not required by Regulation O to make the loan.

Page 15

Extending Credit to Bank Insiders (Reg O)

© 2020 American Bankers Association

Wrap Up

By completing Extending Credit to Bank Insiders (Reg O), you can describe who is covered by Regulation O and the rules and disclosures that must be followed. You can also describe the lending limits and requirements when a bank makes a loan to an executive officer.

» Click Exit to close this course.

Page 16