Embed Size (px)

Citation preview

1

Experience, Challenges and Opportunities under

HAM ❖ The Experience So Far

❖ Trends in Financial Closures and Key Issues

❖ Bidding Scenario and Competitive Intensity

❖ Key Players and Their Portfolios

❖ Stakeholder Perspective

❖ Key Upcoming Projects

❖ Opportunities at the State Level

❖ Issues and Challenges

❖ Government Initiatives in Light of COVID-19

❖ Future Outlook

© India Infrastructure Research | November 2020 www.indiainfrastructure.com

2

Experience, Challenges and Opportunities under HAM

The Experience So Far

• HAM was launched at a time when the project awards largely relied on the EPC mode and the privatesector’s interest had almost dried up BOT-based projects.

• As per projects tracked by India Infrastructure Research, for the NHAI, HAM constituted about 24% of theproject awards (in terms of length) in 2019-20. The share drastically increased from 8% in 2015-16 to 53%in 2016-17 due to euphoric sentiment regarding the new model. However, the share reduced to 45% in2017-18 with issues related to financial closures and land acquisition surfacing thus bringing prudency inbidding on the part of developers.

• During the 2020-21 (upto August 2020), HAM occupied a share of 28% in the total project awards.

• The lowest bids for HAM projects announced in 2020 are 25-35% higher than NHAI’s expectations vis-à-visaverage 15% premium that was seen two years ago. Also, the average number of bidders per project isoften limited to 3-5.

Acquisition by financial investors

• There is an emerging trend of acquisition of ongoing HAM projects. Private equity players are looking at these projects withthe idea of diversifying their portfolio of traffic-linked toll roads.

• Further, their in-house project management and engineering team will closely monitor all phases of construction to ensurethat the projects are completed on time and within budget.

• Recently, Cube Highways acquired two under-construction HAM road projects owned by KNR Constructions Limited and fiveHAM projects of Dilip Buildcon Limited.

• Meanwhile, Canadian pension fund Caisse de depot et placement du Quebec (CDPQ) and Sekura Roads are in talks with GRInfraprojects to acquire the latter’s seven ongoing HAM road projects.

• Reportedly, Welspun Enterprises is also in talks with Canadian Pension funds to invest in its road assets.

© India Infrastructure Research | November 2020 www.indiainfrastructure.com

3

Experience, Challenges and Opportunities under HAM

The Experience So Far

Year-wise HAM Projects Awarded

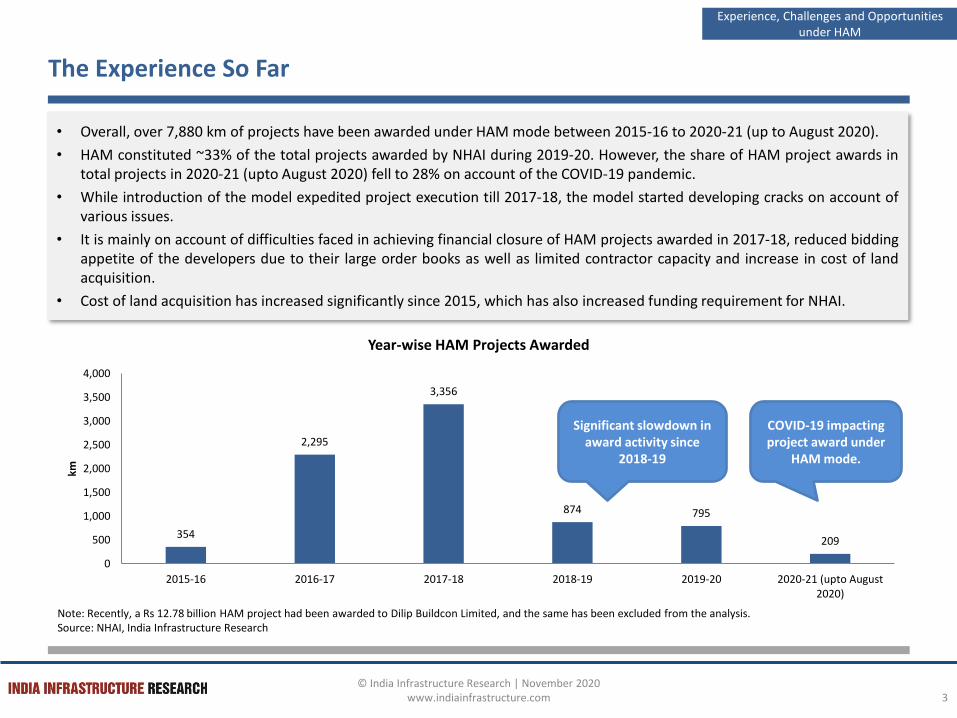

• Overall, over 7,880 km of projects have been awarded under HAM mode between 2015-16 to 2020-21 (up to August 2020).

• HAM constituted ~33% of the total projects awarded by NHAI during 2019-20. However, the share of HAM project awards intotal projects in 2020-21 (upto August 2020) fell to 28% on account of the COVID-19 pandemic.

• While introduction of the model expedited project execution till 2017-18, the model started developing cracks on account ofvarious issues.

• It is mainly on account of difficulties faced in achieving financial closure of HAM projects awarded in 2017-18, reduced biddingappetite of the developers due to their large order books as well as limited contractor capacity and increase in cost of landacquisition.

• Cost of land acquisition has increased significantly since 2015, which has also increased funding requirement for NHAI.

354

2,295

3,356

874 795

209

0

500

1,000

1,500

2,000

2,500

3,000

3,500

4,000

2015-16 2016-17 2017-18 2018-19 2019-20 2020-21 (upto August2020)

km

Note: Recently, a Rs 12.78 billion HAM project had been awarded to Dilip Buildcon Limited, and the same has been excluded from the analysis.Source: NHAI, India Infrastructure Research

Significant slowdown in award activity since

2018-19

COVID-19 impacting project award under

HAM mode.

© India Infrastructure Research | November 2020 www.indiainfrastructure.com

4

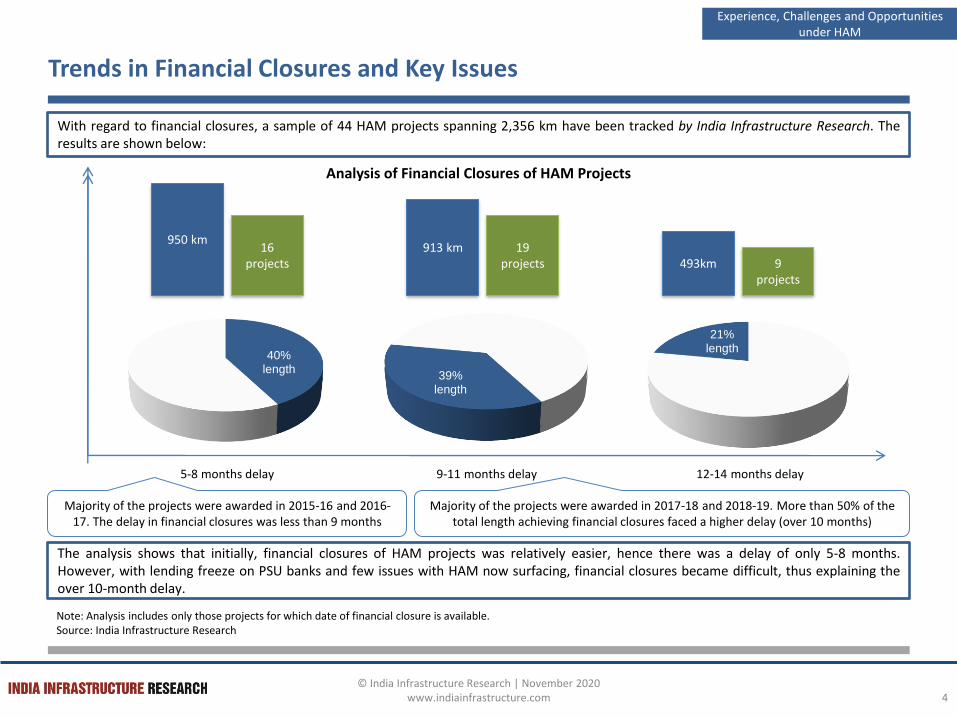

Trends in Financial Closures and Key Issues

Analysis of Financial Closures of HAM Projects

5-8 months delay 9-11 months delay 12-14 months delay

40% length

39% length

21% length

950 km16

projects913 km 19

projects 493km 9 projects

With regard to financial closures, a sample of 44 HAM projects spanning 2,356 km have been tracked by India Infrastructure Research. Theresults are shown below:

Majority of the projects were awarded in 2015-16 and 2016-17. The delay in financial closures was less than 9 months

Majority of the projects were awarded in 2017-18 and 2018-19. More than 50% of the total length achieving financial closures faced a higher delay (over 10 months)

The analysis shows that initially, financial closures of HAM projects was relatively easier, hence there was a delay of only 5-8 months.However, with lending freeze on PSU banks and few issues with HAM now surfacing, financial closures became difficult, thus explaining theover 10-month delay.

40% length

39% length

21% length

Note: Analysis includes only those projects for which date of financial closure is available. Source: India Infrastructure Research

Experience, Challenges and Opportunities under HAM

© India Infrastructure Research | November 2020 www.indiainfrastructure.com

5

Experience, Challenges and Opportunities under HAM

Trends in Financial Closures and Key Issues

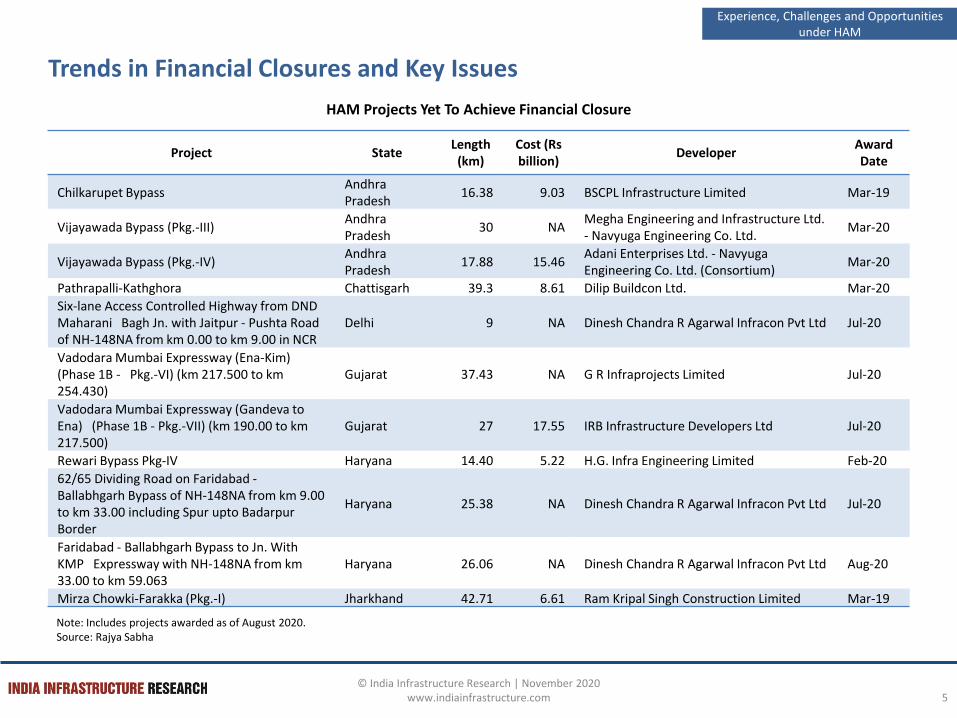

Note: Includes projects awarded as of August 2020.Source: Rajya Sabha

HAM Projects Yet To Achieve Financial Closure

Project StateLength

(km)Cost (Rs billion)

DeveloperAward Date

Chilkarupet BypassAndhra Pradesh

16.38 9.03 BSCPL Infrastructure Limited Mar-19

Vijayawada Bypass (Pkg.-III)Andhra Pradesh

30 NAMegha Engineering and Infrastructure Ltd. - Navyuga Engineering Co. Ltd.

Mar-20

Vijayawada Bypass (Pkg.-IV)Andhra Pradesh

17.88 15.46Adani Enterprises Ltd. - Navyuga Engineering Co. Ltd. (Consortium)

Mar-20

Pathrapalli-Kathghora Chattisgarh 39.3 8.61 Dilip Buildcon Ltd. Mar-20

Six-lane Access Controlled Highway from DND Maharani Bagh Jn. with Jaitpur - Pushta Road of NH-148NA from km 0.00 to km 9.00 in NCR

Delhi 9 NA Dinesh Chandra R Agarwal Infracon Pvt Ltd Jul-20

Vadodara Mumbai Expressway (Ena-Kim) (Phase 1B - Pkg.-VI) (km 217.500 to km 254.430)

Gujarat 37.43 NA G R Infraprojects Limited Jul-20

Vadodara Mumbai Expressway (Gandeva to Ena) (Phase 1B - Pkg.-VII) (km 190.00 to km 217.500)

Gujarat 27 17.55 IRB Infrastructure Developers Ltd Jul-20

Rewari Bypass Pkg-IV Haryana 14.40 5.22 H.G. Infra Engineering Limited Feb-20

62/65 Dividing Road on Faridabad -Ballabhgarh Bypass of NH-148NA from km 9.00 to km 33.00 including Spur upto Badarpur Border

Haryana 25.38 NA Dinesh Chandra R Agarwal Infracon Pvt Ltd Jul-20

Faridabad - Ballabhgarh Bypass to Jn. With KMP Expressway with NH-148NA from km 33.00 to km 59.063

Haryana 26.06 NA Dinesh Chandra R Agarwal Infracon Pvt Ltd Aug-20

Mirza Chowki-Farakka (Pkg.-I) Jharkhand 42.71 6.61 Ram Kripal Singh Construction Limited Mar-19

© India Infrastructure Research | November 2020 www.indiainfrastructure.com

6

Experience, Challenges and Opportunities under HAM

Trends in Financial Closures and Key Issues

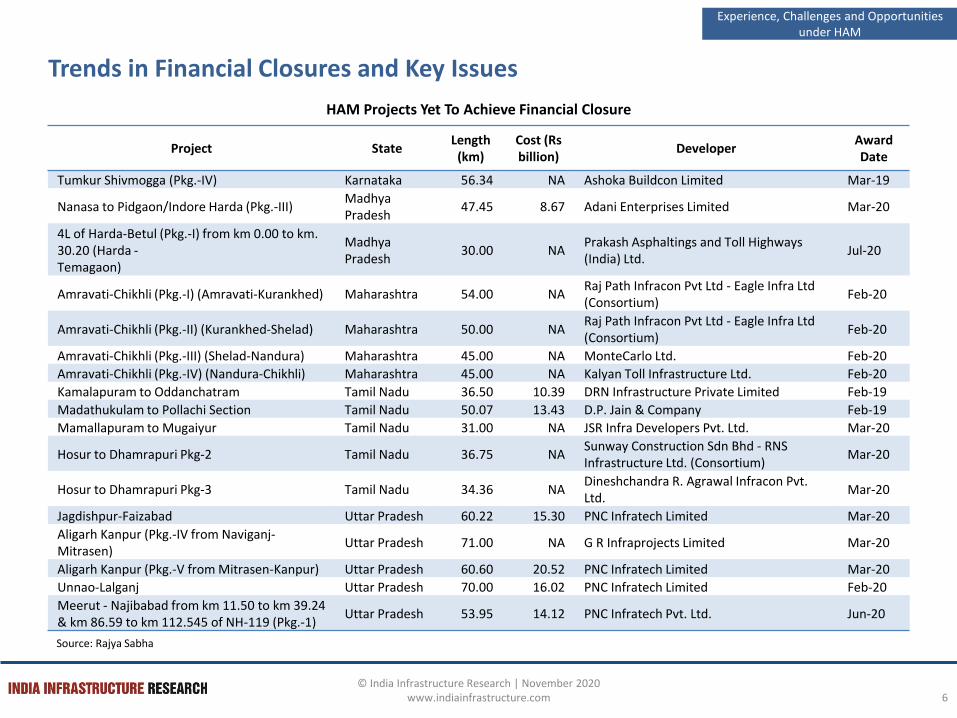

Source: Rajya Sabha

Project StateLength

(km)Cost (Rs billion)

DeveloperAward Date

Tumkur Shivmogga (Pkg.-IV) Karnataka 56.34 NA Ashoka Buildcon Limited Mar-19

Nanasa to Pidgaon/Indore Harda (Pkg.-III)Madhya Pradesh

47.45 8.67 Adani Enterprises Limited Mar-20

4L of Harda-Betul (Pkg.-I) from km 0.00 to km. 30.20 (Harda -Temagaon)

Madhya Pradesh

30.00 NAPrakash Asphaltings and Toll Highways (India) Ltd.

Jul-20

Amravati-Chikhli (Pkg.-I) (Amravati-Kurankhed) Maharashtra 54.00 NARaj Path Infracon Pvt Ltd - Eagle Infra Ltd (Consortium)

Feb-20

Amravati-Chikhli (Pkg.-II) (Kurankhed-Shelad) Maharashtra 50.00 NARaj Path Infracon Pvt Ltd - Eagle Infra Ltd (Consortium)

Feb-20

Amravati-Chikhli (Pkg.-III) (Shelad-Nandura) Maharashtra 45.00 NA MonteCarlo Ltd. Feb-20

Amravati-Chikhli (Pkg.-IV) (Nandura-Chikhli) Maharashtra 45.00 NA Kalyan Toll Infrastructure Ltd. Feb-20

Kamalapuram to Oddanchatram Tamil Nadu 36.50 10.39 DRN Infrastructure Private Limited Feb-19

Madathukulam to Pollachi Section Tamil Nadu 50.07 13.43 D.P. Jain & Company Feb-19

Mamallapuram to Mugaiyur Tamil Nadu 31.00 NA JSR Infra Developers Pvt. Ltd. Mar-20

Hosur to Dhamrapuri Pkg-2 Tamil Nadu 36.75 NASunway Construction Sdn Bhd - RNS Infrastructure Ltd. (Consortium)

Mar-20

Hosur to Dhamrapuri Pkg-3 Tamil Nadu 34.36 NADineshchandra R. Agrawal Infracon Pvt. Ltd.

Mar-20

Jagdishpur-Faizabad Uttar Pradesh 60.22 15.30 PNC Infratech Limited Mar-20

Aligarh Kanpur (Pkg.-IV from Naviganj-Mitrasen)

Uttar Pradesh 71.00 NA G R Infraprojects Limited Mar-20

Aligarh Kanpur (Pkg.-V from Mitrasen-Kanpur) Uttar Pradesh 60.60 20.52 PNC Infratech Limited Mar-20

Unnao-Lalganj Uttar Pradesh 70.00 16.02 PNC Infratech Limited Feb-20

Meerut - Najibabad from km 11.50 to km 39.24 & km 86.59 to km 112.545 of NH-119 (Pkg.-1)

Uttar Pradesh 53.95 14.12 PNC Infratech Pvt. Ltd. Jun-20

HAM Projects Yet To Achieve Financial Closure

© India Infrastructure Research | November 2020 www.indiainfrastructure.com

7

Experience, Challenges and Opportunities under HAM

Trends in Financial Closures and Key Issues

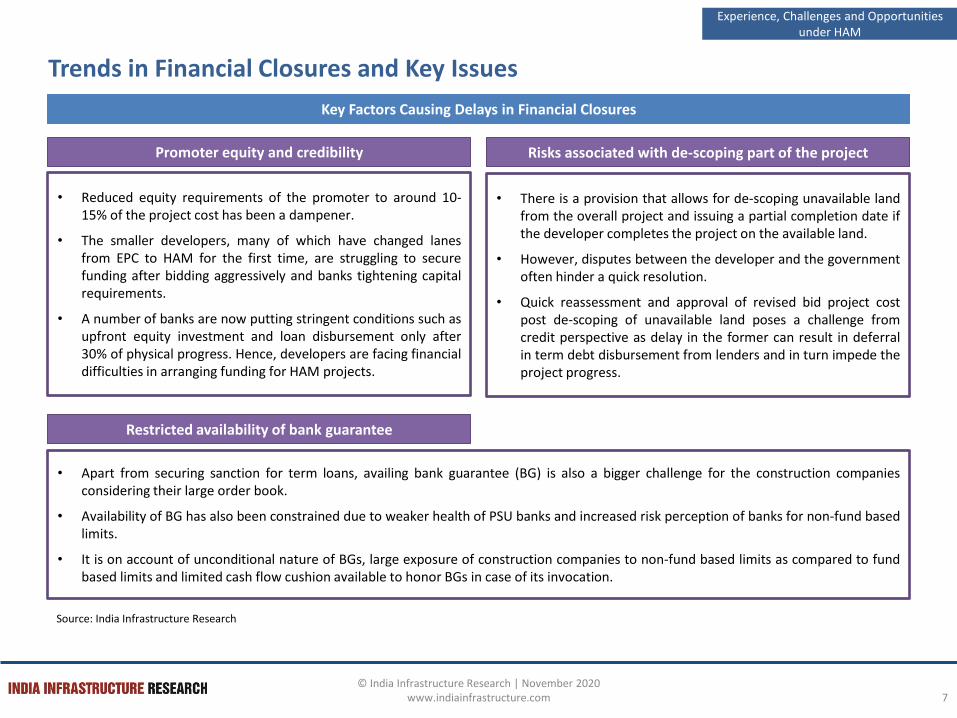

Source: India Infrastructure Research

Key Factors Causing Delays in Financial Closures

• Reduced equity requirements of the promoter to around 10-15% of the project cost has been a dampener.

• The smaller developers, many of which have changed lanesfrom EPC to HAM for the first time, are struggling to securefunding after bidding aggressively and banks tightening capitalrequirements.

• A number of banks are now putting stringent conditions such asupfront equity investment and loan disbursement only after30% of physical progress. Hence, developers are facing financialdifficulties in arranging funding for HAM projects.

Promoter equity and credibility

• There is a provision that allows for de-scoping unavailable landfrom the overall project and issuing a partial completion date ifthe developer completes the project on the available land.

• However, disputes between the developer and the governmentoften hinder a quick resolution.

• Quick reassessment and approval of revised bid project costpost de-scoping of unavailable land poses a challenge fromcredit perspective as delay in the former can result in deferralin term debt disbursement from lenders and in turn impede theproject progress.

Risks associated with de-scoping part of the project

• Apart from securing sanction for term loans, availing bank guarantee (BG) is also a bigger challenge for the construction companiesconsidering their large order book.

• Availability of BG has also been constrained due to weaker health of PSU banks and increased risk perception of banks for non-fund basedlimits.

• It is on account of unconditional nature of BGs, large exposure of construction companies to non-fund based limits as compared to fundbased limits and limited cash flow cushion available to honor BGs in case of its invocation.

Restricted availability of bank guarantee

© India Infrastructure Research | November 2020 www.indiainfrastructure.com

8

Experience, Challenges and Opportunities under HAM

Bidding Scenario and Competitive Intensity

Source: India Infrastructure Research

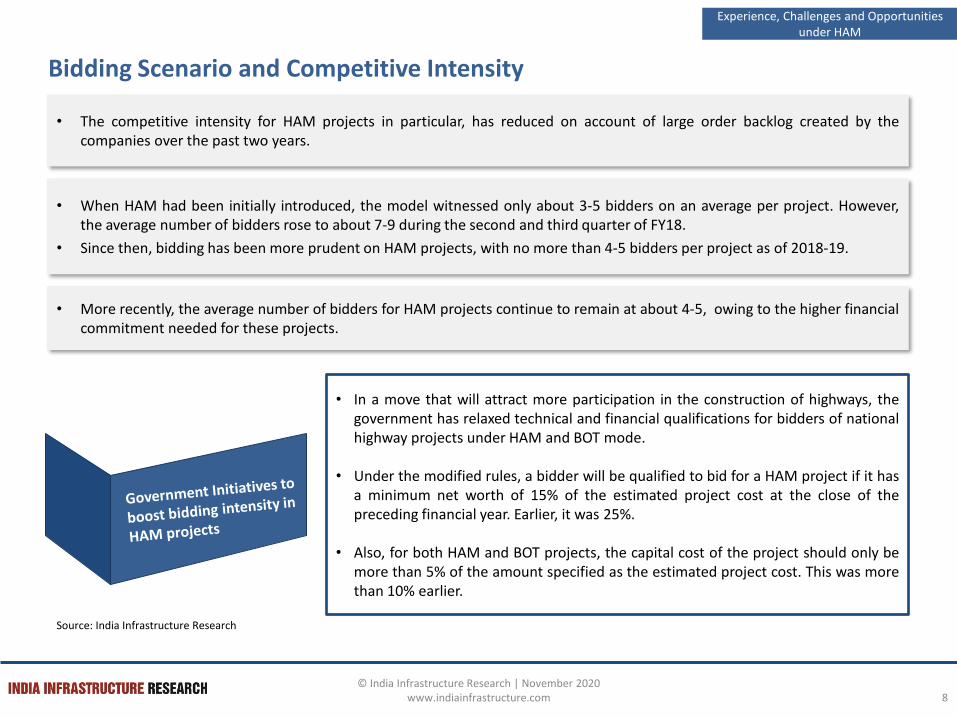

• When HAM had been initially introduced, the model witnessed only about 3-5 bidders on an average per project. However,the average number of bidders rose to about 7-9 during the second and third quarter of FY18.

• Since then, bidding has been more prudent on HAM projects, with no more than 4-5 bidders per project as of 2018-19.

• The competitive intensity for HAM projects in particular, has reduced on account of large order backlog created by thecompanies over the past two years.

• More recently, the average number of bidders for HAM projects continue to remain at about 4-5, owing to the higher financialcommitment needed for these projects.

• In a move that will attract more participation in the construction of highways, thegovernment has relaxed technical and financial qualifications for bidders of nationalhighway projects under HAM and BOT mode.

• Under the modified rules, a bidder will be qualified to bid for a HAM project if it hasa minimum net worth of 15% of the estimated project cost at the close of thepreceding financial year. Earlier, it was 25%.

• Also, for both HAM and BOT projects, the capital cost of the project should only bemore than 5% of the amount specified as the estimated project cost. This was morethan 10% earlier.

© India Infrastructure Research | November 2020 www.indiainfrastructure.com

9

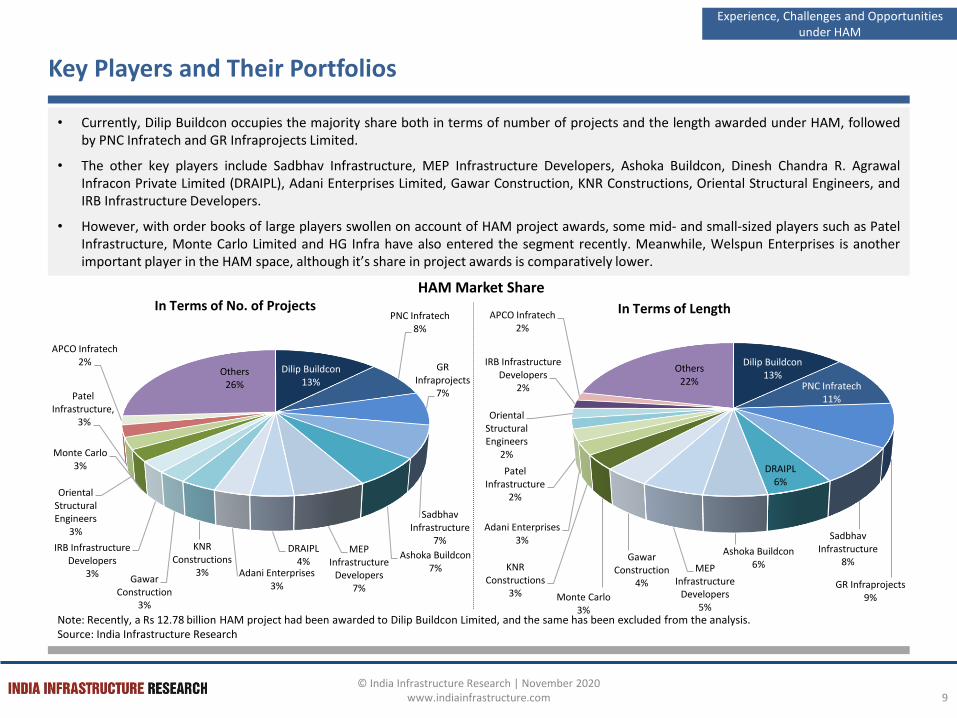

Key Players and Their Portfolios

• Currently, Dilip Buildcon occupies the majority share both in terms of number of projects and the length awarded under HAM, followedby PNC Infratech and GR Infraprojects Limited.

• The other key players include Sadbhav Infrastructure, MEP Infrastructure Developers, Ashoka Buildcon, Dinesh Chandra R. AgrawalInfracon Private Limited (DRAIPL), Adani Enterprises Limited, Gawar Construction, KNR Constructions, Oriental Structural Engineers, andIRB Infrastructure Developers.

• However, with order books of large players swollen on account of HAM project awards, some mid- and small-sized players such as PatelInfrastructure, Monte Carlo Limited and HG Infra have also entered the segment recently. Meanwhile, Welspun Enterprises is anotherimportant player in the HAM space, although it’s share in project awards is comparatively lower.

Note: Recently, a Rs 12.78 billion HAM project had been awarded to Dilip Buildcon Limited, and the same has been excluded from the analysis.Source: India Infrastructure Research

HAM Market ShareIn Terms of No. of Projects In Terms of Length

Experience, Challenges and Opportunities under HAM

Dilip Buildcon13%

PNC Infratech8%

GR Infraprojects

7%

Sadbhav Infrastructure

7%

Ashoka Buildcon7%

MEP Infrastructure

Developers7%

DRAIPL4%

Adani Enterprises3%

KNR Constructions

3%Gawar

Construction3%

IRB Infrastructure Developers

3%

Monte Carlo3%

Oriental Structural Engineers

3%

Patel Infrastructure,

3%

APCO Infratech2%

Others26%

Dilip Buildcon13%

PNC Infratech11%

GR Infraprojects9%

Sadbhav Infrastructure

8%

DRAIPL6%

Ashoka Buildcon6%MEP

Infrastructure Developers

5%

Gawar Construction

4%

Monte Carlo3%

KNR Constructions

3%

Adani Enterprises3%

Patel Infrastructure

2%

Oriental Structural Engineers

2%

IRB Infrastructure Developers

2%

APCO Infratech2%

Others22%

© India Infrastructure Research | November 2020 www.indiainfrastructure.com

10

Key Players and Their Portfolios

Dilip Buildcon

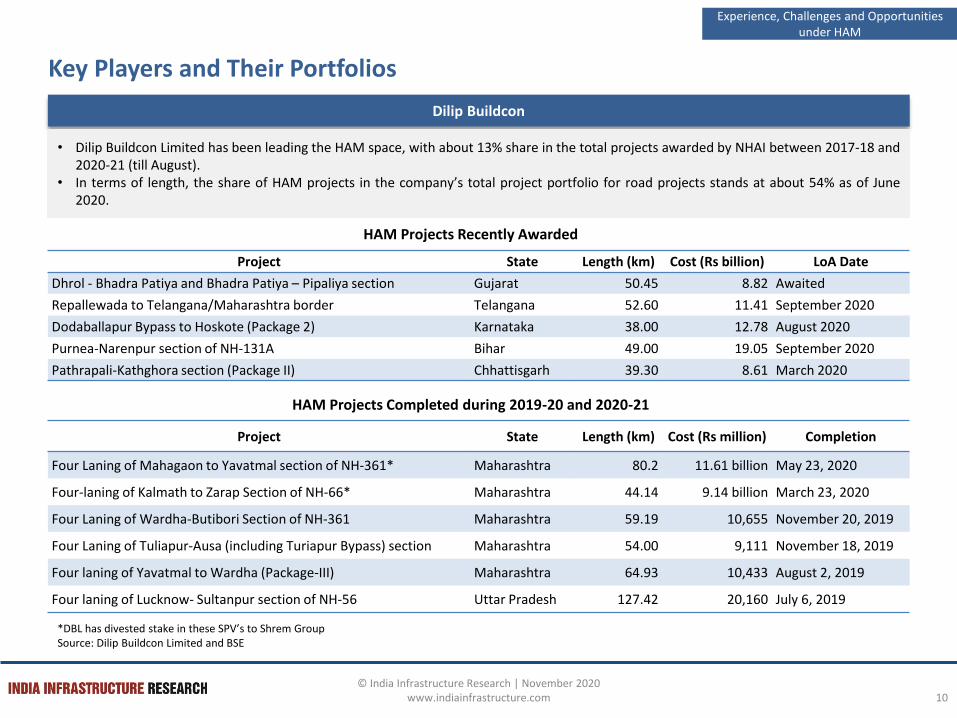

*DBL has divested stake in these SPV’s to Shrem GroupSource: Dilip Buildcon Limited and BSE

HAM Projects Completed during 2019-20 and 2020-21

Project State Length (km) Cost (Rs million) Completion

Four Laning of Mahagaon to Yavatmal section of NH-361* Maharashtra 80.2 11.61 billion May 23, 2020

Four-laning of Kalmath to Zarap Section of NH-66* Maharashtra 44.14 9.14 billion March 23, 2020

Four Laning of Wardha-Butibori Section of NH-361 Maharashtra 59.19 10,655 November 20, 2019

Four Laning of Tuliapur-Ausa (including Turiapur Bypass) section Maharashtra 54.00 9,111 November 18, 2019

Four laning of Yavatmal to Wardha (Package-III) Maharashtra 64.93 10,433 August 2, 2019

Four laning of Lucknow- Sultanpur section of NH-56 Uttar Pradesh 127.42 20,160 July 6, 2019

• Dilip Buildcon Limited has been leading the HAM space, with about 13% share in the total projects awarded by NHAI between 2017-18 and2020-21 (till August).

• In terms of length, the share of HAM projects in the company’s total project portfolio for road projects stands at about 54% as of June2020.

HAM Projects Recently Awarded

Project State Length (km) Cost (Rs billion) LoA Date

Dhrol - Bhadra Patiya and Bhadra Patiya – Pipaliya section Gujarat 50.45 8.82 Awaited

Repallewada to Telangana/Maharashtra border Telangana 52.60 11.41 September 2020

Dodaballapur Bypass to Hoskote (Package 2) Karnataka 38.00 12.78 August 2020

Purnea-Narenpur section of NH-131A Bihar 49.00 19.05 September 2020

Pathrapali-Kathghora section (Package II) Chhattisgarh 39.30 8.61 March 2020

Experience, Challenges and Opportunities under HAM

© India Infrastructure Research | November 2020 www.indiainfrastructure.com

11

Key Players and Their Portfolios

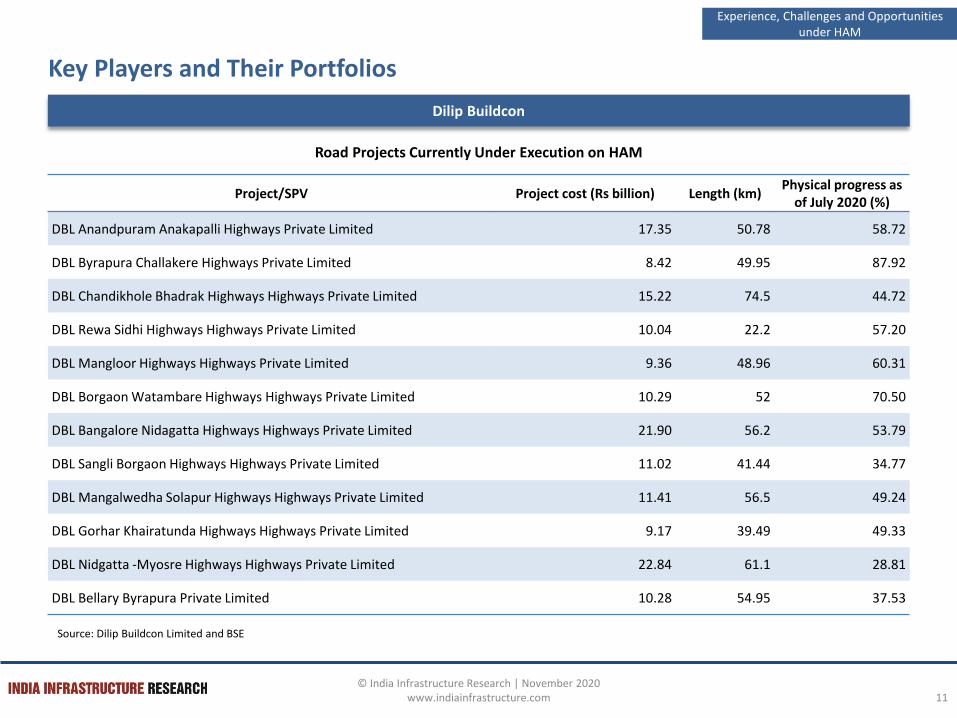

Dilip Buildcon

Project/SPV Project cost (Rs billion) Length (km)Physical progress as

of July 2020 (%)

DBL Anandpuram Anakapalli Highways Private Limited 17.35 50.78 58.72

DBL Byrapura Challakere Highways Private Limited 8.42 49.95 87.92

DBL Chandikhole Bhadrak Highways Highways Private Limited 15.22 74.5 44.72

DBL Rewa Sidhi Highways Highways Private Limited 10.04 22.2 57.20

DBL Mangloor Highways Highways Private Limited 9.36 48.96 60.31

DBL Borgaon Watambare Highways Highways Private Limited 10.29 52 70.50

DBL Bangalore Nidagatta Highways Highways Private Limited 21.90 56.2 53.79

DBL Sangli Borgaon Highways Highways Private Limited 11.02 41.44 34.77

DBL Mangalwedha Solapur Highways Highways Private Limited 11.41 56.5 49.24

DBL Gorhar Khairatunda Highways Highways Private Limited 9.17 39.49 49.33

DBL Nidgatta -Myosre Highways Highways Private Limited 22.84 61.1 28.81

DBL Bellary Byrapura Private Limited 10.28 54.95 37.53

Source: Dilip Buildcon Limited and BSE

Road Projects Currently Under Execution on HAM

Experience, Challenges and Opportunities under HAM

© India Infrastructure Research | November 2020 www.indiainfrastructure.com

12

Key Players and Their Portfolios

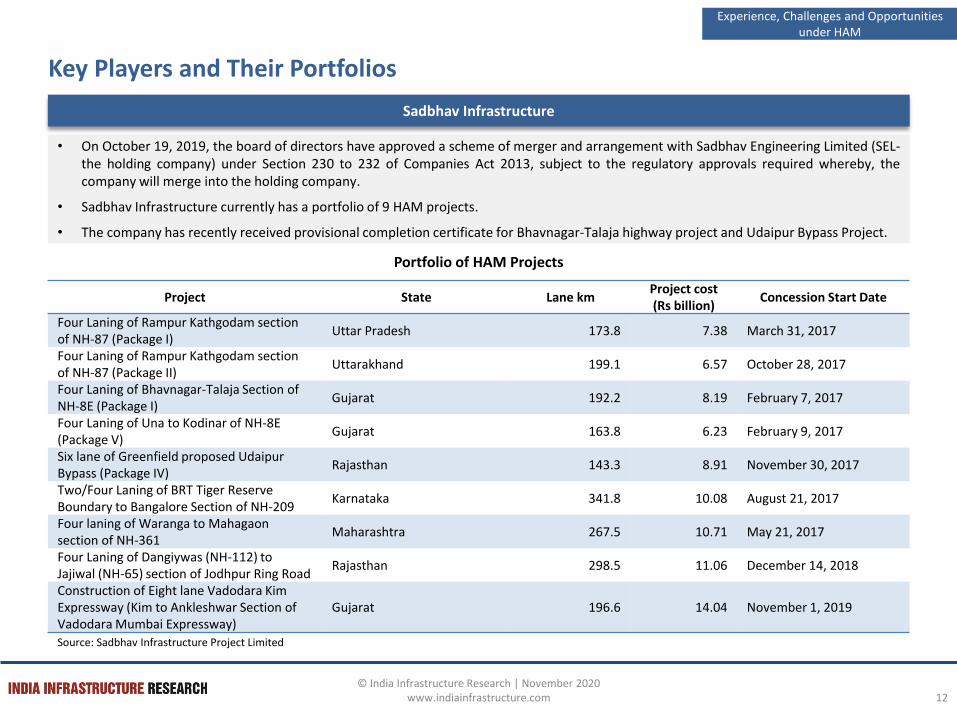

Sadbhav Infrastructure

• On October 19, 2019, the board of directors have approved a scheme of merger and arrangement with Sadbhav Engineering Limited (SEL-the holding company) under Section 230 to 232 of Companies Act 2013, subject to the regulatory approvals required whereby, thecompany will merge into the holding company.

• Sadbhav Infrastructure currently has a portfolio of 9 HAM projects.

• The company has recently received provisional completion certificate for Bhavnagar-Talaja highway project and Udaipur Bypass Project.

Portfolio of HAM Projects

Source: Sadbhav Infrastructure Project Limited

Project State Lane kmProject cost (Rs billion)

Concession Start Date

Four Laning of Rampur Kathgodam section of NH-87 (Package I)

Uttar Pradesh 173.8 7.38 March 31, 2017

Four Laning of Rampur Kathgodam section of NH-87 (Package II)

Uttarakhand 199.1 6.57 October 28, 2017

Four Laning of Bhavnagar-Talaja Section of NH-8E (Package I)

Gujarat 192.2 8.19 February 7, 2017

Four Laning of Una to Kodinar of NH-8E (Package V)

Gujarat 163.8 6.23 February 9, 2017

Six lane of Greenfield proposed Udaipur Bypass (Package IV)

Rajasthan 143.3 8.91 November 30, 2017

Two/Four Laning of BRT Tiger Reserve Boundary to Bangalore Section of NH-209

Karnataka 341.8 10.08 August 21, 2017

Four laning of Waranga to Mahagaonsection of NH-361

Maharashtra 267.5 10.71 May 21, 2017

Four Laning of Dangiywas (NH-112) to Jajiwal (NH-65) section of Jodhpur Ring Road

Rajasthan 298.5 11.06 December 14, 2018

Construction of Eight lane Vadodara Kim Expressway (Kim to Ankleshwar Section of Vadodara Mumbai Expressway)

Gujarat 196.6 14.04 November 1, 2019

Experience, Challenges and Opportunities under HAM

© India Infrastructure Research | November 2020 www.indiainfrastructure.com

13

Key Players and Their Portfolios

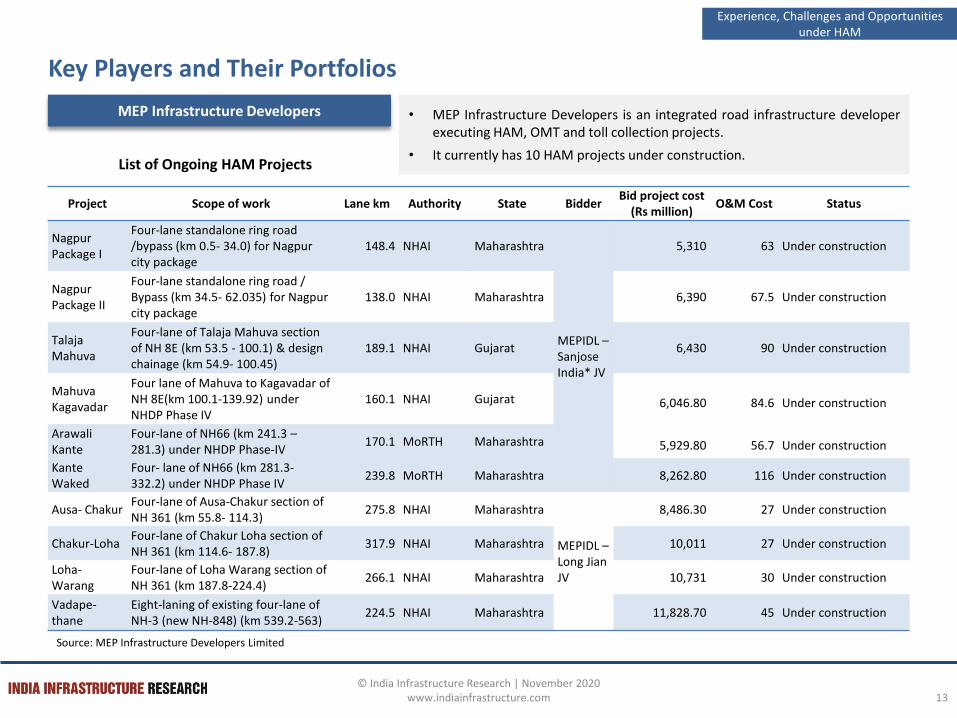

MEP Infrastructure Developers

List of Ongoing HAM Projects

Project Scope of work Lane km Authority State BidderBid project cost

(Rs million)O&M Cost Status

Nagpur Package I

Four-lane standalone ring road /bypass (km 0.5- 34.0) for Nagpur city package

148.4 NHAI Maharashtra

MEPIDL –SanjoseIndia* JV

5,310 63 Under construction

Nagpur Package II

Four-lane standalone ring road / Bypass (km 34.5- 62.035) for Nagpurcity package

138.0 NHAI Maharashtra 6,390 67.5 Under construction

Talaja Mahuva

Four-lane of Talaja Mahuva section of NH 8E (km 53.5 - 100.1) & designchainage (km 54.9- 100.45)

189.1 NHAI Gujarat 6,430 90 Under construction

Mahuva Kagavadar

Four lane of Mahuva to Kagavadar of NH 8E(km 100.1-139.92) underNHDP Phase IV

160.1 NHAI Gujarat 6,046.80 84.6 Under construction

ArawaliKante

Four-lane of NH66 (km 241.3 –281.3) under NHDP Phase-IV

170.1 MoRTH Maharashtra 5,929.80 56.7 Under construction

Kante Waked

Four- lane of NH66 (km 281.3-332.2) under NHDP Phase IV

239.8 MoRTH Maharashtra 8,262.80 116 Under construction

Ausa- ChakurFour-lane of Ausa-Chakur section of NH 361 (km 55.8- 114.3)

275.8 NHAI Maharashtra

MEPIDL –Long JianJV

8,486.30 27 Under construction

Chakur-LohaFour-lane of Chakur Loha section of NH 361 (km 114.6- 187.8)

317.9 NHAI Maharashtra 10,011 27 Under construction

Loha-Warang

Four-lane of Loha Warang section of NH 361 (km 187.8-224.4)

266.1 NHAI Maharashtra 10,731 30 Under construction

Vadape-thane

Eight-laning of existing four-lane ofNH-3 (new NH-848) (km 539.2-563)

224.5 NHAI Maharashtra 11,828.70 45 Under construction

Source: MEP Infrastructure Developers Limited

• MEP Infrastructure Developers is an integrated road infrastructure developerexecuting HAM, OMT and toll collection projects.

• It currently has 10 HAM projects under construction.

Experience, Challenges and Opportunities under HAM

© India Infrastructure Research | November 2020 www.indiainfrastructure.com

14

Key Players and Their Portfolios

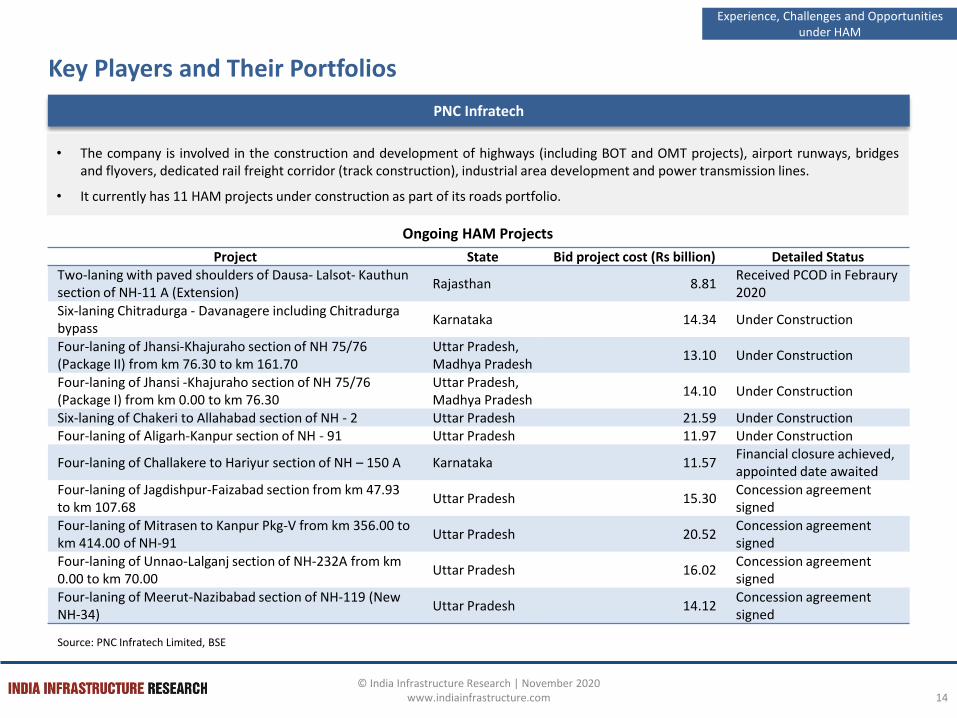

PNC Infratech

Source: PNC Infratech Limited, BSE

Ongoing HAM Projects

Project State Bid project cost (Rs billion) Detailed StatusTwo-laning with paved shoulders of Dausa- Lalsot- Kauthunsection of NH-11 A (Extension)

Rajasthan 8.81Received PCOD in Febraury2020

Six-laning Chitradurga - Davanagere including Chitradurgabypass

Karnataka 14.34 Under Construction

Four-laning of Jhansi-Khajuraho section of NH 75/76 (Package II) from km 76.30 to km 161.70

Uttar Pradesh, Madhya Pradesh

13.10 Under Construction

Four-laning of Jhansi -Khajuraho section of NH 75/76 (Package I) from km 0.00 to km 76.30

Uttar Pradesh, Madhya Pradesh

14.10 Under Construction

Six-laning of Chakeri to Allahabad section of NH - 2 Uttar Pradesh 21.59 Under ConstructionFour-laning of Aligarh-Kanpur section of NH - 91 Uttar Pradesh 11.97 Under Construction

Four-laning of Challakere to Hariyur section of NH – 150 A Karnataka 11.57Financial closure achieved, appointed date awaited

Four-laning of Jagdishpur-Faizabad section from km 47.93 to km 107.68

Uttar Pradesh 15.30Concession agreement signed

Four-laning of Mitrasen to Kanpur Pkg-V from km 356.00 to km 414.00 of NH-91

Uttar Pradesh 20.52Concession agreement signed

Four-laning of Unnao-Lalganj section of NH-232A from km 0.00 to km 70.00

Uttar Pradesh 16.02Concession agreement signed

Four-laning of Meerut-Nazibabad section of NH-119 (New NH-34)

Uttar Pradesh 14.12Concession agreement signed

• The company is involved in the construction and development of highways (including BOT and OMT projects), airport runways, bridgesand flyovers, dedicated rail freight corridor (track construction), industrial area development and power transmission lines.

• It currently has 11 HAM projects under construction as part of its roads portfolio.

Experience, Challenges and Opportunities under HAM

© India Infrastructure Research | November 2020 www.indiainfrastructure.com

15

Key Players and Their Portfolios

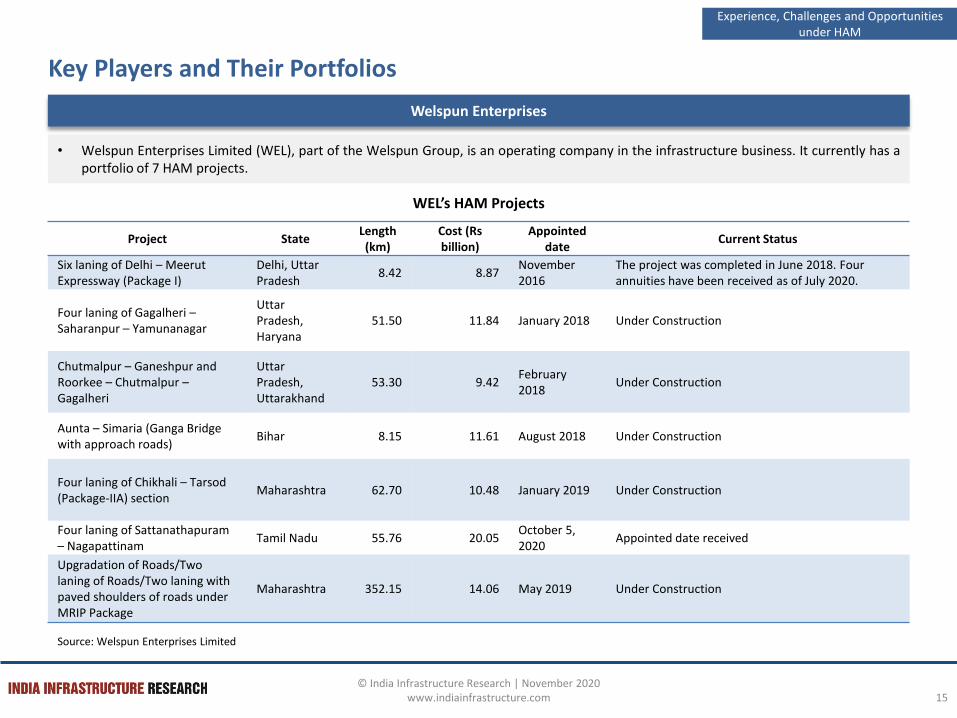

Welspun Enterprises

WEL’s HAM Projects

Project StateLength (km)

Cost (Rsbillion)

Appointed date

Current Status

Six laning of Delhi – Meerut Expressway (Package I)

Delhi, Uttar Pradesh

8.42 8.87November 2016

The project was completed in June 2018. Four annuities have been received as of July 2020.

Four laning of Gagalheri –Saharanpur – Yamunanagar

Uttar Pradesh, Haryana

51.50 11.84 January 2018 Under Construction

Chutmalpur – Ganeshpur and Roorkee – Chutmalpur –Gagalheri

Uttar Pradesh, Uttarakhand

53.30 9.42February 2018

Under Construction

Aunta – Simaria (Ganga Bridge with approach roads)

Bihar 8.15 11.61 August 2018 Under Construction

Four laning of Chikhali – Tarsod(Package-IIA) section

Maharashtra 62.70 10.48 January 2019 Under Construction

Four laning of Sattanathapuram– Nagapattinam

Tamil Nadu 55.76 20.05October 5, 2020

Appointed date received

Upgradation of Roads/Two laning of Roads/Two laning with paved shoulders of roads under MRIP Package

Maharashtra 352.15 14.06 May 2019 Under Construction

Source: Welspun Enterprises Limited

• Welspun Enterprises Limited (WEL), part of the Welspun Group, is an operating company in the infrastructure business. It currently has aportfolio of 7 HAM projects.

Experience, Challenges and Opportunities under HAM

© India Infrastructure Research | November 2020 www.indiainfrastructure.com

16

Key Players and Their Portfolios

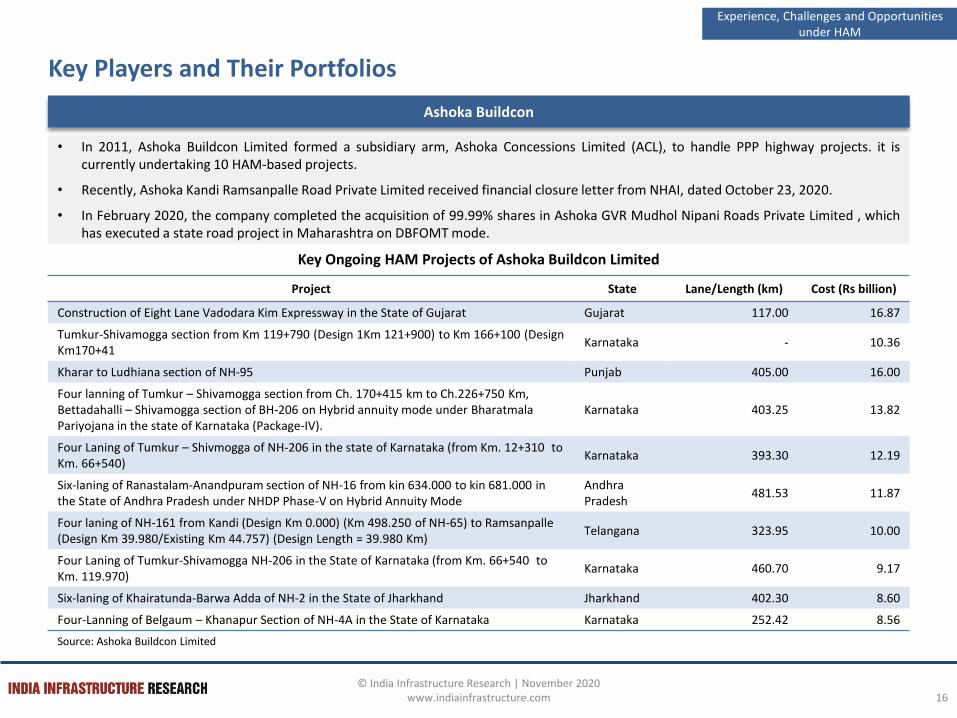

Ashoka Buildcon

Project State Lane/Length (km) Cost (Rs billion)

Construction of Eight Lane Vadodara Kim Expressway in the State of Gujarat Gujarat 117.00 16.87

Tumkur-Shivamogga section from Km 119+790 (Design 1Km 121+900) to Km 166+100 (Design Km170+41

Karnataka - 10.36

Kharar to Ludhiana section of NH-95 Punjab 405.00 16.00

Four lanning of Tumkur – Shivamogga section from Ch. 170+415 km to Ch.226+750 Km, Bettadahalli – Shivamogga section of BH-206 on Hybrid annuity mode under BharatmalaPariyojana in the state of Karnataka (Package-IV).

Karnataka 403.25 13.82

Four Laning of Tumkur – Shivmogga of NH-206 in the state of Karnataka (from Km. 12+310 to Km. 66+540)

Karnataka 393.30 12.19

Six-laning of Ranastalam-Anandpuram section of NH-16 from kin 634.000 to kin 681.000 in the State of Andhra Pradesh under NHDP Phase-V on Hybrid Annuity Mode

Andhra Pradesh

481.53 11.87

Four laning of NH-161 from Kandi (Design Km 0.000) (Km 498.250 of NH-65) to Ramsanpalle(Design Km 39.980/Existing Km 44.757) (Design Length = 39.980 Km)

Telangana 323.95 10.00

Four Laning of Tumkur-Shivamogga NH-206 in the State of Karnataka (from Km. 66+540 to Km. 119.970)

Karnataka 460.70 9.17

Six-laning of Khairatunda-Barwa Adda of NH-2 in the State of Jharkhand Jharkhand 402.30 8.60

Four-Lanning of Belgaum – Khanapur Section of NH-4A in the State of Karnataka Karnataka 252.42 8.56

Key Ongoing HAM Projects of Ashoka Buildcon Limited

Source: Ashoka Buildcon Limited

• In 2011, Ashoka Buildcon Limited formed a subsidiary arm, Ashoka Concessions Limited (ACL), to handle PPP highway projects. it iscurrently undertaking 10 HAM-based projects.

• Recently, Ashoka Kandi Ramsanpalle Road Private Limited received financial closure letter from NHAI, dated October 23, 2020.

• In February 2020, the company completed the acquisition of 99.99% shares in Ashoka GVR Mudhol Nipani Roads Private Limited , whichhas executed a state road project in Maharashtra on DBFOMT mode.

Experience, Challenges and Opportunities under HAM

© India Infrastructure Research | November 2020 www.indiainfrastructure.com

17

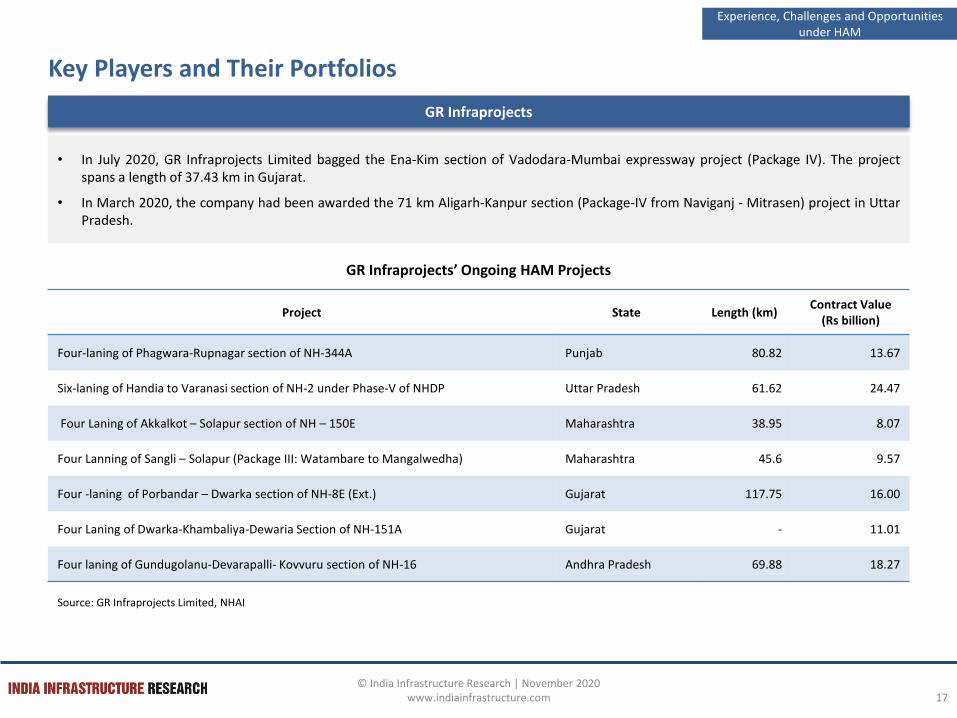

Key Players and Their Portfolios

GR Infraprojects

GR Infraprojects’ Ongoing HAM Projects

Project State Length (km) Contract Value

(Rs billion)

Four-laning of Phagwara-Rupnagar section of NH-344A Punjab 80.82 13.67

Six-laning of Handia to Varanasi section of NH-2 under Phase-V of NHDP Uttar Pradesh 61.62 24.47

Four Laning of Akkalkot – Solapur section of NH – 150E Maharashtra 38.95 8.07

Four Lanning of Sangli – Solapur (Package III: Watambare to Mangalwedha) Maharashtra 45.6 9.57

Four -laning of Porbandar – Dwarka section of NH-8E (Ext.) Gujarat 117.75 16.00

Four Laning of Dwarka-Khambaliya-Dewaria Section of NH-151A Gujarat - 11.01

Four laning of Gundugolanu-Devarapalli- Kovvuru section of NH-16 Andhra Pradesh 69.88 18.27

Source: GR Infraprojects Limited, NHAI

Experience, Challenges and Opportunities under HAM

• In July 2020, GR Infraprojects Limited bagged the Ena-Kim section of Vadodara-Mumbai expressway project (Package IV). The projectspans a length of 37.43 km in Gujarat.

• In March 2020, the company had been awarded the 71 km Aligarh-Kanpur section (Package-IV from Naviganj - Mitrasen) project in UttarPradesh.

© India Infrastructure Research | November 2020 www.indiainfrastructure.com

18

Experience, Challenges and Opportunities under HAM

Stakeholder Perspective

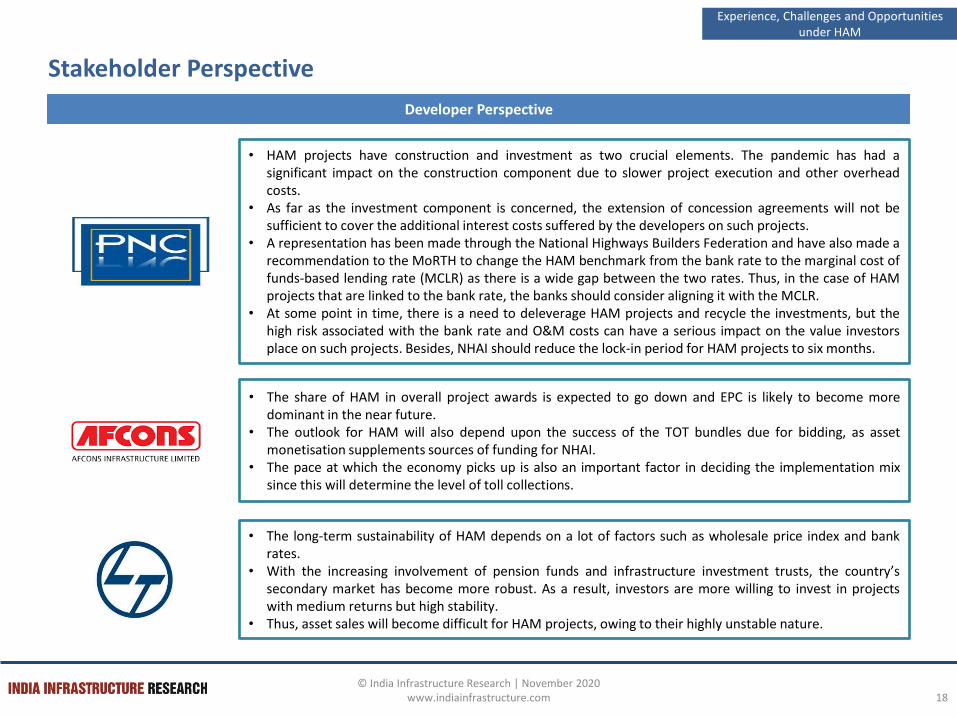

• HAM projects have construction and investment as two crucial elements. The pandemic has had asignificant impact on the construction component due to slower project execution and other overheadcosts.

• As far as the investment component is concerned, the extension of concession agreements will not besufficient to cover the additional interest costs suffered by the developers on such projects.

• A representation has been made through the National Highways Builders Federation and have also made arecommendation to the MoRTH to change the HAM benchmark from the bank rate to the marginal cost offunds-based lending rate (MCLR) as there is a wide gap between the two rates. Thus, in the case of HAMprojects that are linked to the bank rate, the banks should consider aligning it with the MCLR.

• At some point in time, there is a need to deleverage HAM projects and recycle the investments, but thehigh risk associated with the bank rate and O&M costs can have a serious impact on the value investorsplace on such projects. Besides, NHAI should reduce the lock-in period for HAM projects to six months.

• The share of HAM in overall project awards is expected to go down and EPC is likely to become moredominant in the near future.

• The outlook for HAM will also depend upon the success of the TOT bundles due for bidding, as assetmonetisation supplements sources of funding for NHAI.

• The pace at which the economy picks up is also an important factor in deciding the implementation mixsince this will determine the level of toll collections.

• The long-term sustainability of HAM depends on a lot of factors such as wholesale price index and bankrates.

• With the increasing involvement of pension funds and infrastructure investment trusts, the country’ssecondary market has become more robust. As a result, investors are more willing to invest in projectswith medium returns but high stability.

• Thus, asset sales will become difficult for HAM projects, owing to their highly unstable nature.

Developer Perspective

© India Infrastructure Research | November 2020 www.indiainfrastructure.com

19

Experience, Challenges and Opportunities under HAM

Stakeholder Perspective

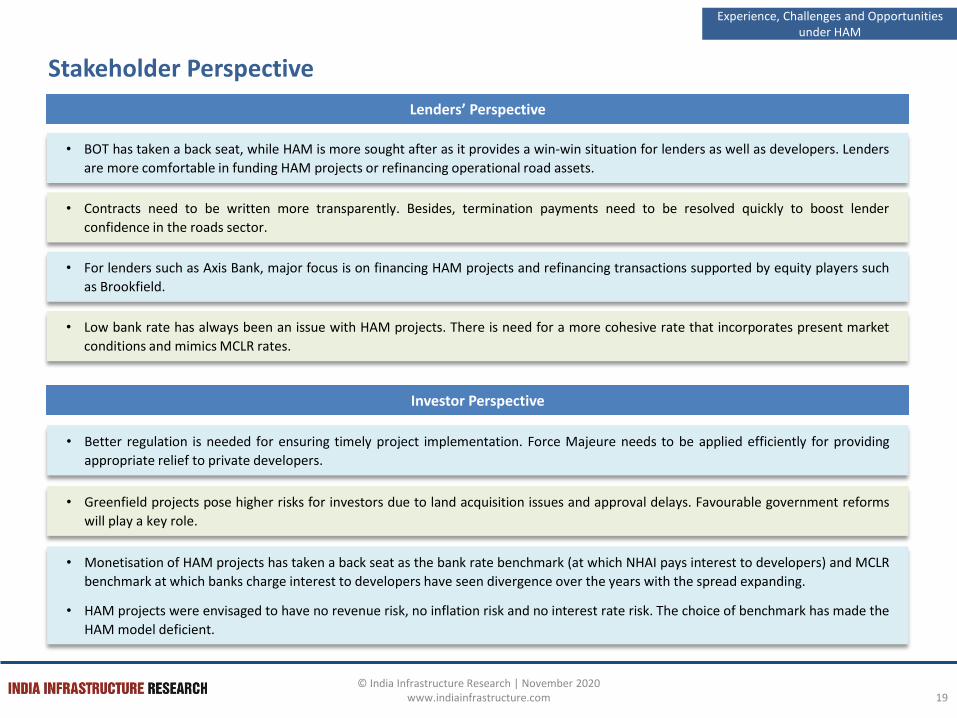

Lenders’ Perspective

• BOT has taken a back seat, while HAM is more sought after as it provides a win-win situation for lenders as well as developers. Lenders

are more comfortable in funding HAM projects or refinancing operational road assets.

• Contracts need to be written more transparently. Besides, termination payments need to be resolved quickly to boost lender

confidence in the roads sector.

• For lenders such as Axis Bank, major focus is on financing HAM projects and refinancing transactions supported by equity players such

as Brookfield.

• Low bank rate has always been an issue with HAM projects. There is need for a more cohesive rate that incorporates present market

conditions and mimics MCLR rates.

Investor Perspective

• Better regulation is needed for ensuring timely project implementation. Force Majeure needs to be applied efficiently for providing

appropriate relief to private developers.

• Greenfield projects pose higher risks for investors due to land acquisition issues and approval delays. Favourable government reforms

will play a key role.

• Monetisation of HAM projects has taken a back seat as the bank rate benchmark (at which NHAI pays interest to developers) and MCLR

benchmark at which banks charge interest to developers have seen divergence over the years with the spread expanding.

• HAM projects were envisaged to have no revenue risk, no inflation risk and no interest rate risk. The choice of benchmark has made the

HAM model deficient.

© India Infrastructure Research | November 2020 www.indiainfrastructure.com

20

Project Pipeline

Based on Length

Others include Mizoram, Nagaland and Sikkim.Note: Analysis Includes projects with length/cost not available.Source: India Infrastructure Research

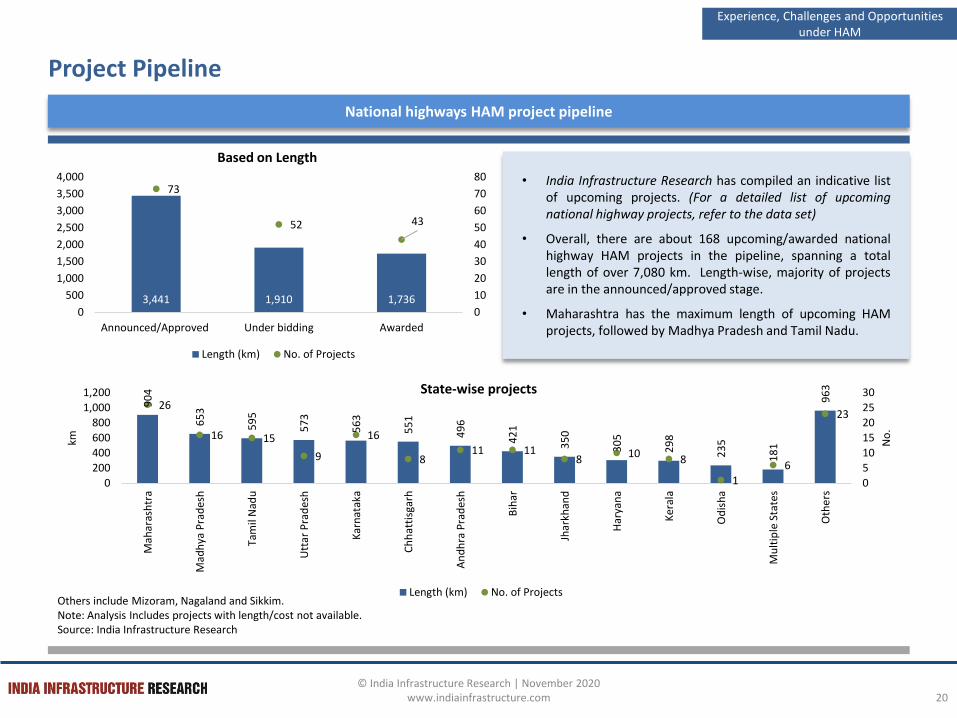

• India Infrastructure Research has compiled an indicative listof upcoming projects. (For a detailed list of upcomingnational highway projects, refer to the data set)

• Overall, there are about 168 upcoming/awarded nationalhighway HAM projects in the pipeline, spanning a totallength of over 7,080 km. Length-wise, majority of projectsare in the announced/approved stage.

• Maharashtra has the maximum length of upcoming HAMprojects, followed by Madhya Pradesh and Tamil Nadu.

National highways HAM project pipeline

State-wise projects

Experience, Challenges and Opportunities under HAM

90

4

65

3

59

5

57

3

56

3

55

1

49

6

42

1

35

0

30

5

29

8

23

5

18

1

96

3

26

16 15

9

16

811 11

810

8

1

6

23

0

5

10

15

20

25

30

0

200

400

600

800

1,000

1,200

Mah

aras

htr

a

Mad

hya

Pra

des

h

Tam

il N

adu

Utt

ar P

rad

esh

Kar

nat

aka

Ch

hat

tisg

arh

An

dh

ra P

rad

esh

Bih

ar

Jhar

khan

d

Har

yan

a

Ker

ala

Od

ish

a

Mu

ltip

le S

tate

s

Oth

ers

No

.

km

Length (km) No. of Projects

3,441 1,910 1,736

73

52 43

0

10

20

30

40

50

60

70

80

0

500

1,000

1,500

2,000

2,500

3,000

3,500

4,000

Announced/Approved Under bidding Awarded

Length (km) No. of Projects

© India Infrastructure Research | November 2020 www.indiainfrastructure.com

21

Project Pipeline

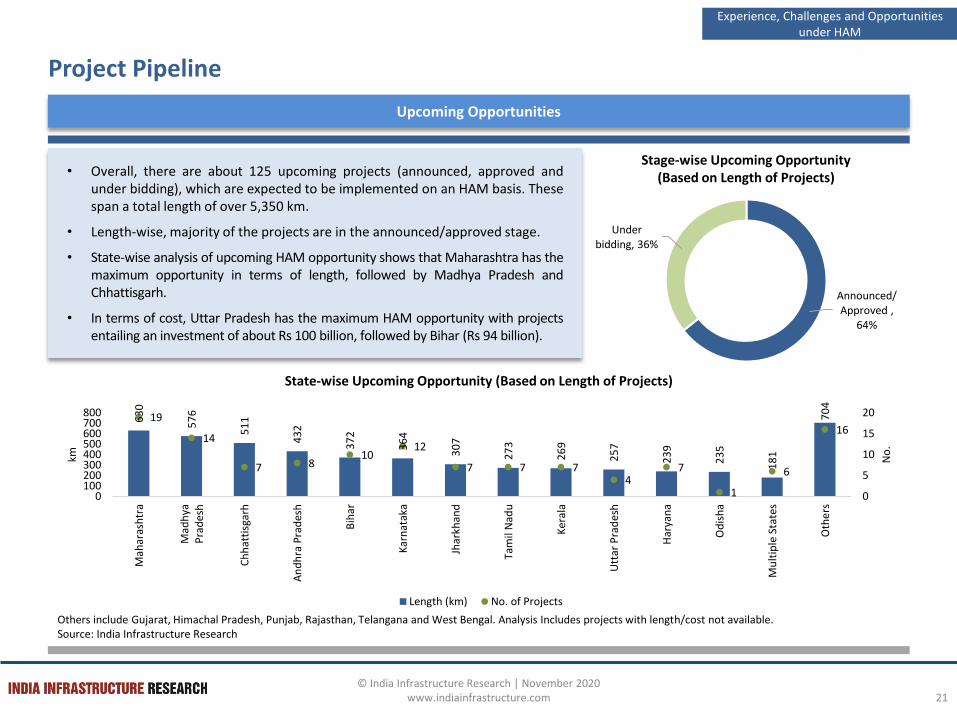

Stage-wise Upcoming Opportunity(Based on Length of Projects)• Overall, there are about 125 upcoming projects (announced, approved and

under bidding), which are expected to be implemented on an HAM basis. Thesespan a total length of over 5,350 km.

• Length-wise, majority of the projects are in the announced/approved stage.

• State-wise analysis of upcoming HAM opportunity shows that Maharashtra has themaximum opportunity in terms of length, followed by Madhya Pradesh andChhattisgarh.

• In terms of cost, Uttar Pradesh has the maximum HAM opportunity with projectsentailing an investment of about Rs 100 billion, followed by Bihar (Rs 94 billion).

Upcoming Opportunities

State-wise Upcoming Opportunity (Based on Length of Projects)

Others include Gujarat, Himachal Pradesh, Punjab, Rajasthan, Telangana and West Bengal. Analysis Includes projects with length/cost not available.Source: India Infrastructure Research

Announced/Approved ,

64%

Under bidding, 36%

63

0

57

6

51

1

43

2

37

2

36

4

30

7

27

3

26

9

25

7

23

9

23

5

18

1

70

4

19

14

7 810

12

7 7 74

7

1

6

16

0

5

10

15

20

0100200300400500600700800

Mah

aras

htr

a

Mad

hya

Pra

de

sh

Ch

hat

tisg

arh

An

dh

ra P

rad

esh

Bih

ar

Kar

nat

aka

Jhar

khan

d

Tam

il N

adu

Ker

ala

Utt

ar P

rad

esh

Har

yan

a

Od

ish

a

Mu

ltip

le S

tate

s

Oth

ers

No

.

km

Length (km) No. of Projects

Experience, Challenges and Opportunities under HAM

© India Infrastructure Research | November 2020 www.indiainfrastructure.com

22

Key Upcoming Projects

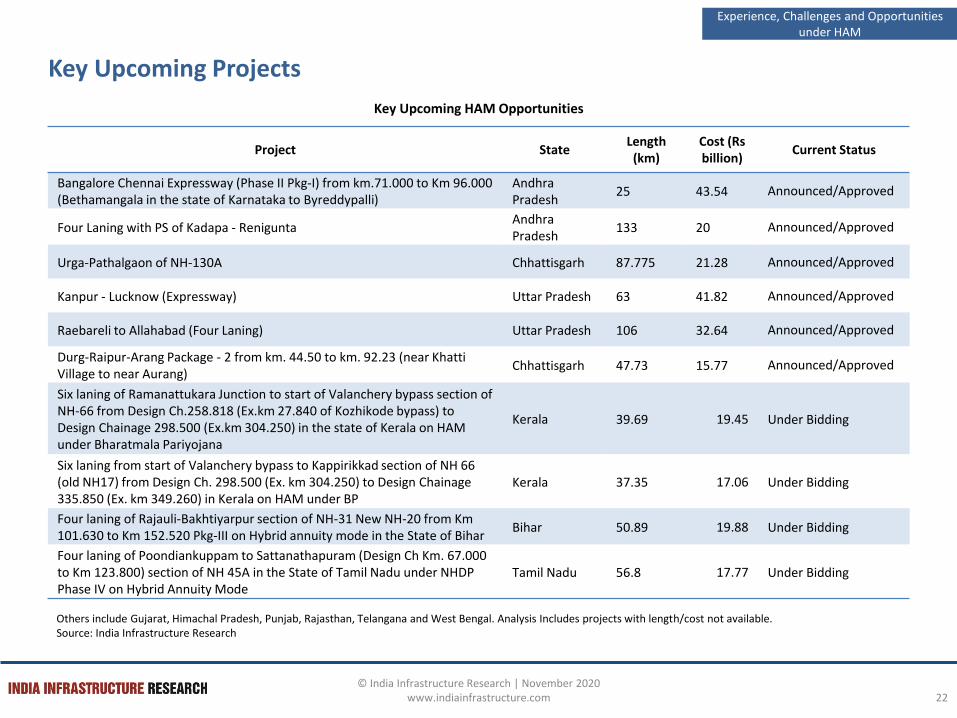

Key Upcoming HAM Opportunities

Others include Gujarat, Himachal Pradesh, Punjab, Rajasthan, Telangana and West Bengal. Analysis Includes projects with length/cost not available.Source: India Infrastructure Research

Experience, Challenges and Opportunities under HAM

Project StateLength

(km)Cost (Rs billion)

Current Status

Bangalore Chennai Expressway (Phase II Pkg-I) from km.71.000 to Km 96.000 (Bethamangala in the state of Karnataka to Byreddypalli)

Andhra Pradesh

25 43.54 Announced/Approved

Four Laning with PS of Kadapa - ReniguntaAndhra Pradesh

133 20 Announced/Approved

Urga-Pathalgaon of NH-130A Chhattisgarh 87.775 21.28 Announced/Approved

Kanpur - Lucknow (Expressway) Uttar Pradesh 63 41.82 Announced/Approved

Raebareli to Allahabad (Four Laning) Uttar Pradesh 106 32.64 Announced/Approved

Durg-Raipur-Arang Package - 2 from km. 44.50 to km. 92.23 (near Khatti Village to near Aurang)

Chhattisgarh 47.73 15.77 Announced/Approved

Six laning of Ramanattukara Junction to start of Valanchery bypass section of NH-66 from Design Ch.258.818 (Ex.km 27.840 of Kozhikode bypass) to Design Chainage 298.500 (Ex.km 304.250) in the state of Kerala on HAM under Bharatmala Pariyojana

Kerala 39.69 19.45 Under Bidding

Six laning from start of Valanchery bypass to Kappirikkad section of NH 66 (old NH17) from Design Ch. 298.500 (Ex. km 304.250) to Design Chainage 335.850 (Ex. km 349.260) in Kerala on HAM under BP

Kerala 37.35 17.06 Under Bidding

Four laning of Rajauli-Bakhtiyarpur section of NH-31 New NH-20 from Km 101.630 to Km 152.520 Pkg-III on Hybrid annuity mode in the State of Bihar

Bihar 50.89 19.88 Under Bidding

Four laning of Poondiankuppam to Sattanathapuram (Design Ch Km. 67.000 to Km 123.800) section of NH 45A in the State of Tamil Nadu under NHDP Phase IV on Hybrid Annuity Mode

Tamil Nadu 56.8 17.77 Under Bidding

© India Infrastructure Research | November 2020 www.indiainfrastructure.com

23

Experience, Challenges and Opportunities under HAM

Issues and Challenges

Funding IssuesCashflow Mismatch

Difficulty in Obtaining FC

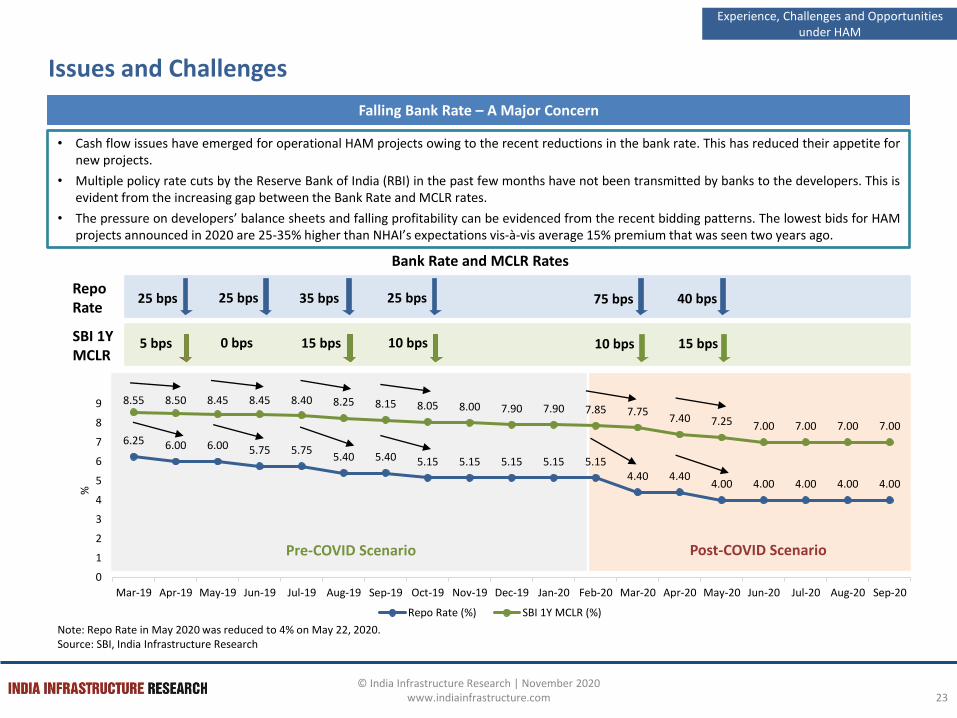

Falling Bank Rate – A Major Concern

Note: Repo Rate in May 2020 was reduced to 4% on May 22, 2020.Source: SBI, India Infrastructure Research

• Cash flow issues have emerged for operational HAM projects owing to the recent reductions in the bank rate. This has reduced their appetite fornew projects.

• Multiple policy rate cuts by the Reserve Bank of India (RBI) in the past few months have not been transmitted by banks to the developers. This isevident from the increasing gap between the Bank Rate and MCLR rates.

• The pressure on developers’ balance sheets and falling profitability can be evidenced from the recent bidding patterns. The lowest bids for HAMprojects announced in 2020 are 25-35% higher than NHAI’s expectations vis-à-vis average 15% premium that was seen two years ago.

Bank Rate and MCLR Rates

Repo Rate

SBI 1Y MCLR

25 bps

0 bps

35 bps

15 bps

25 bps

10 bps

75 bps

10 bps

40 bps

15 bps

25 bps

5 bps

6.25 6.00 6.00 5.75 5.755.40 5.40 5.15 5.15 5.15 5.15 5.15

4.40 4.404.00 4.00 4.00 4.00 4.00

8.55 8.50 8.45 8.45 8.40 8.25 8.15 8.05 8.00 7.90 7.90 7.85 7.757.40 7.25 7.00 7.00 7.00 7.00

0

1

2

3

4

5

6

7

8

9

Mar-19 Apr-19 May-19 Jun-19 Jul-19 Aug-19 Sep-19 Oct-19 Nov-19 Dec-19 Jan-20 Feb-20 Mar-20 Apr-20 May-20 Jun-20 Jul-20 Aug-20 Sep-20

%

Repo Rate (%) SBI 1Y MCLR (%)

Pre-COVID Scenario Post-COVID Scenario

© India Infrastructure Research | November 2020 www.indiainfrastructure.com

24

Experience, Challenges and Opportunities under HAM

Issues and Challenges

Falling Bank Rate – Implications

Source: ICRA, India Infrastructure Research

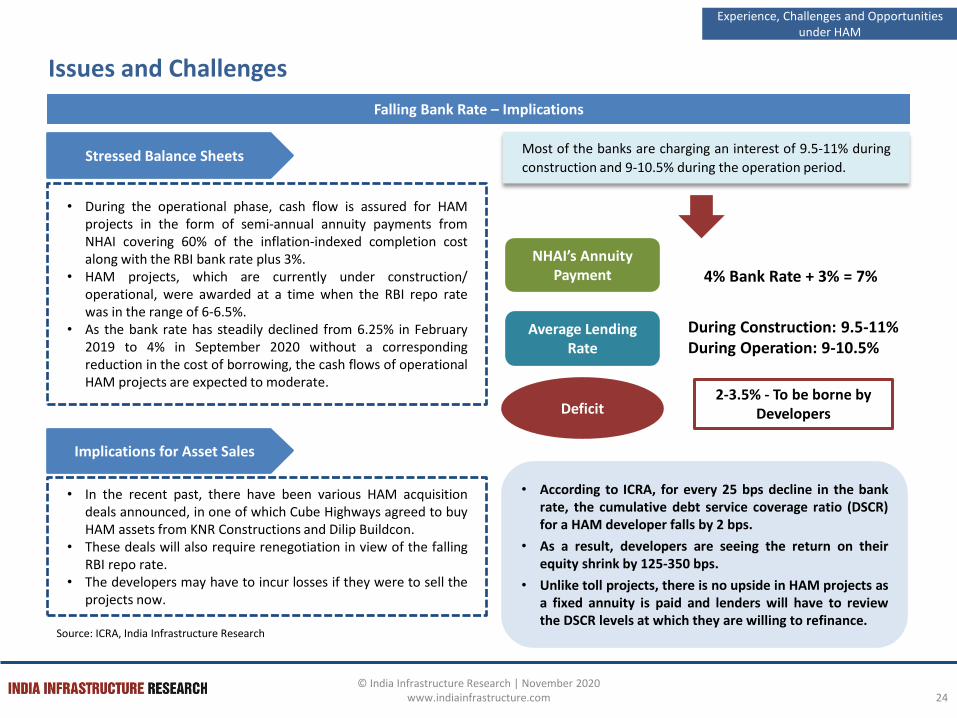

Stressed Balance Sheets

• During the operational phase, cash flow is assured for HAMprojects in the form of semi-annual annuity payments fromNHAI covering 60% of the inflation-indexed completion costalong with the RBI bank rate plus 3%.

• HAM projects, which are currently under construction/operational, were awarded at a time when the RBI repo ratewas in the range of 6-6.5%.

• As the bank rate has steadily declined from 6.25% in February2019 to 4% in September 2020 without a correspondingreduction in the cost of borrowing, the cash flows of operationalHAM projects are expected to moderate.

Implications for Asset Sales

• In the recent past, there have been various HAM acquisitiondeals announced, in one of which Cube Highways agreed to buyHAM assets from KNR Constructions and Dilip Buildcon.

• These deals will also require renegotiation in view of the fallingRBI repo rate.

• The developers may have to incur losses if they were to sell theprojects now.

Most of the banks are charging an interest of 9.5-11% during

construction and 9-10.5% during the operation period.

NHAI’s Annuity Payment 4% Bank Rate + 3% = 7%

Average Lending Rate

During Construction: 9.5-11%During Operation: 9-10.5%

Deficit 2-3.5% - To be borne by

Developers

• According to ICRA, for every 25 bps decline in the bankrate, the cumulative debt service coverage ratio (DSCR)for a HAM developer falls by 2 bps.

• As a result, developers are seeing the return on theirequity shrink by 125-350 bps.

• Unlike toll projects, there is no upside in HAM projects asa fixed annuity is paid and lenders will have to reviewthe DSCR levels at which they are willing to refinance.

© India Infrastructure Research | November 2020 www.indiainfrastructure.com

25

Experience, Challenges and Opportunities under HAM

Issues and Challenges

• Despite a number of HAM projects being able to tie up funds, many of them are still awaiting appointeddates on account of delays in land acquisition or regulatory clearances. These projects are stuck as themobilisation advance is not given by the government until the appointed date is fixed. The date isannounced only after the government secures 80% right of way for a project.

• Developers have already forfeited six projects citing similar issues. Although 80% land availability offersan edge for swifter completion of project, the delay in providing encumbrance-free land continues toweigh on the road sector.

• Developers are now cautiously accepting land only after the issuance of section 3G notification againstthe earlier practice of section 3D notification.

Land IssuesLand Issues

• The falling bank rate has started to impact the cash flow streams of HAM projects as the correspondingreduction in cost of borrowing has been slow. The annuity paid by the NHAI is linked to the bank rate(plus 3 per cent).

• In a falling interest rate scenario, the lag in rate transmission on loans creates a mismatch in annuityincome earned by the road developer and the interest paid by it to the bank. This can cause cash flowdisruptions for operational assets in the short term, till bank rates stabilise.

• Also, with frauds and scams surfacing in the banking industry, mid-sized construction companies arefinding it tougher to procure term loans and bank guarantees.

Funding IssuesCashflow Mismatch

• Some of the active lenders for HAM projects include State Bank of India, Axis Bank, HDFC Bank, PunjabNational Bank, Larsen and Toubro (L&T) Financial Services, and ICICI Bank, among others.

• Meanwhile, a few projects are facing difficulties in obtaining financial closure due to lending freeze onmany public sector banks and cherry-picking of projects by private banks.

• Further, the developer’s low equity share in the total project cost has also made the banks morecautious. As an offshoot, this has meant higher equity requirement for HAM developers.

• In addition, small and medium developers having an average or below average credit rating are nothelping them in raising funds from the capital market.

Difficulty in Obtaining FCDifficulty in

Obtaining FC

Cashflow Mismatch

© India Infrastructure Research | November 2020 www.indiainfrastructure.com

26

Experience, Challenges and Opportunities under HAM

Government Initiatives in Light of COVID-19

Source: India Infrastructure Research

• The government will now make the upfront construction payment to a highway projectconcessionaire under HAM in 10 tranches as against 5, subject to the overall ceiling of 40%of the project cost.

• The smaller instalments will ensure a comfortable liquidity situation for the company andalso a reduction in the developer’s working capital requirements.

• Besides, the release of upfront payments during the construction period will be linked tothe physical progress of the project.

• The annuity payment will be made on the reducing balance of completion cost at aninterest rate equal to average of one-year marginal cost of fund-based lending rate (MCLR)of top five scheduled commercial banks plus 1.25%.

• Linking annuity payments to MCLR, instead of bank rates, will ensure that the developers donot bear the consequences of the falling bank rate.

• Besides, the central government has unveiled a new set of norms for HAM contracts in order to promote fresh private investment inhighways through this route.

• NHAI has been taking various initiatives from time to time to support road developers.

• For HAM projects, NHAI has been releasing funds for working capital needs even before the milestones are completed. The funds areoffered at 200 bps above bank lending rates, and have offered low-cost working capital to developers.

© India Infrastructure Research | November 2020 www.indiainfrastructure.com

27

Experience, Challenges and Opportunities under HAM

Future Outlook

• Banks continue to be selective in funding infrastructure projects due to liquidity constraints and pile-up of sour loans. In addition, most of the developers have stretched balance sheets which will make financial closures difficult to come by.

• These factors, combined with prudent bidding, will reduce the share of HAM projects in the overall pie of project awards in the next few quarters.

• With the first round of HAM projects likely to achieve completion in the near term, these are best suited for acquisitions by investors.Though an opportunity area for global investors, the delay in transmission of rate cuts can disrupt cash flow streams, in turn, loweringequity returns to investors.

• Moreover, the delay in execution of some projects due to slow equity infusion from weak sponsors and land acquisition issues willfurther wane investor interest in the segment.

• The quality of independent engineers and authority engineers hasn't been up to the mark. To address this issue, the government has already appointed monitors and initiated third-party quality checks. In addition, there is a need to undertake skill development for enhancing quality of design and safety consultants.

• In the wake of the funding concerns, the government must take a pragmatic view of awarding projects on the HAM model and decideon a suitable portfolio based on a mix of EPC, BOT annuity and HAM mode. There is a need to evaluate projects on a case-to-case basis.

• Despite achieving financial closure, several HAM projects are still awaiting appointed dates on account of delays in land acquisition orregulatory clearances.

• This highlights the need for a more effective dispute resolution mechanism, proper project development and preparation, expeditedclearance approval and more balanced risk allocation to ensure the timely execution of projects.

• Although NHAI has plans to rely on private sector investment for the upcoming road projects, the outlook for HAM seems bleak in thenear future due to unhealthy balance sheets of project developers during the ongoing COVID-19 crisis.

• In these times, it has become harder for developers to achieve financial closures since banks are unwilling to lend in this uncertainmarket environment.

© India Infrastructure Research | November 2020 www.indiainfrastructure.com