Embed Size (px)

Citation preview

Expense disallowed in

relation to

Exempt Income

(Section 14A)

by

CA. PRAMOD JAINFCA, FCS, FCMA, DISA, MIMA

LUNAWAT & CO.

Lunawat & Co

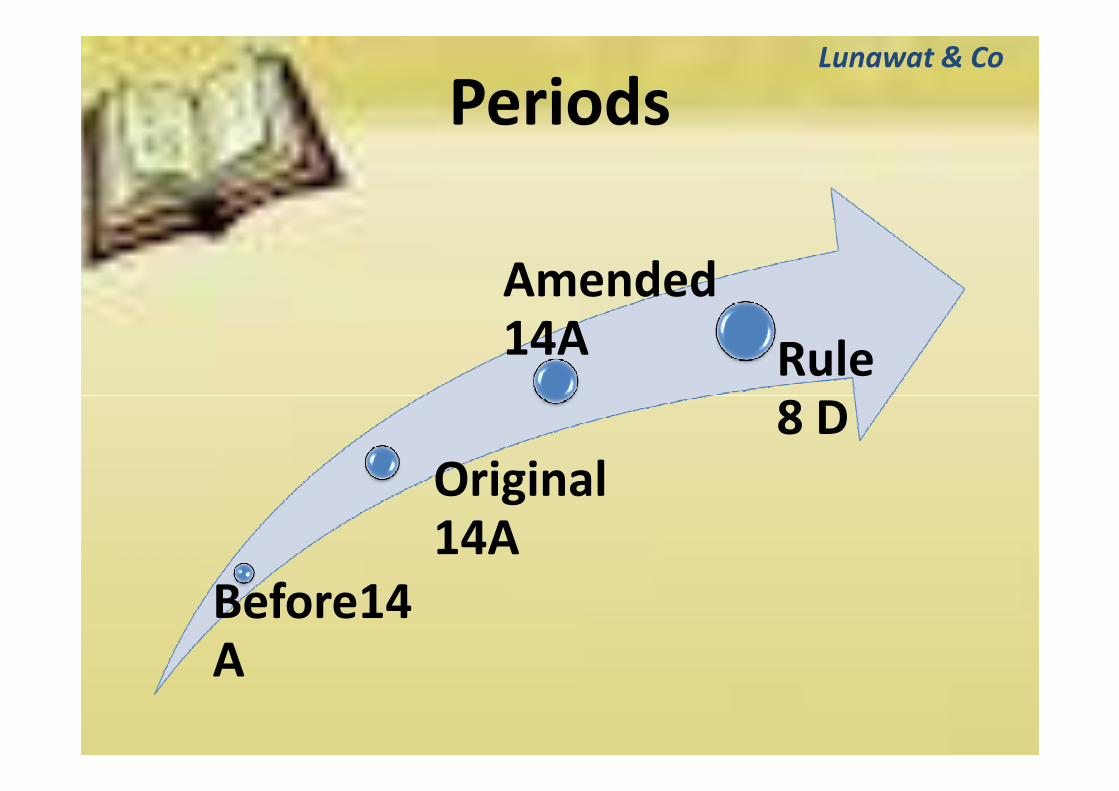

Periods

Amended 14A Rule

8 D

Lunawat & Co

Before14A

Original 14A

8 D

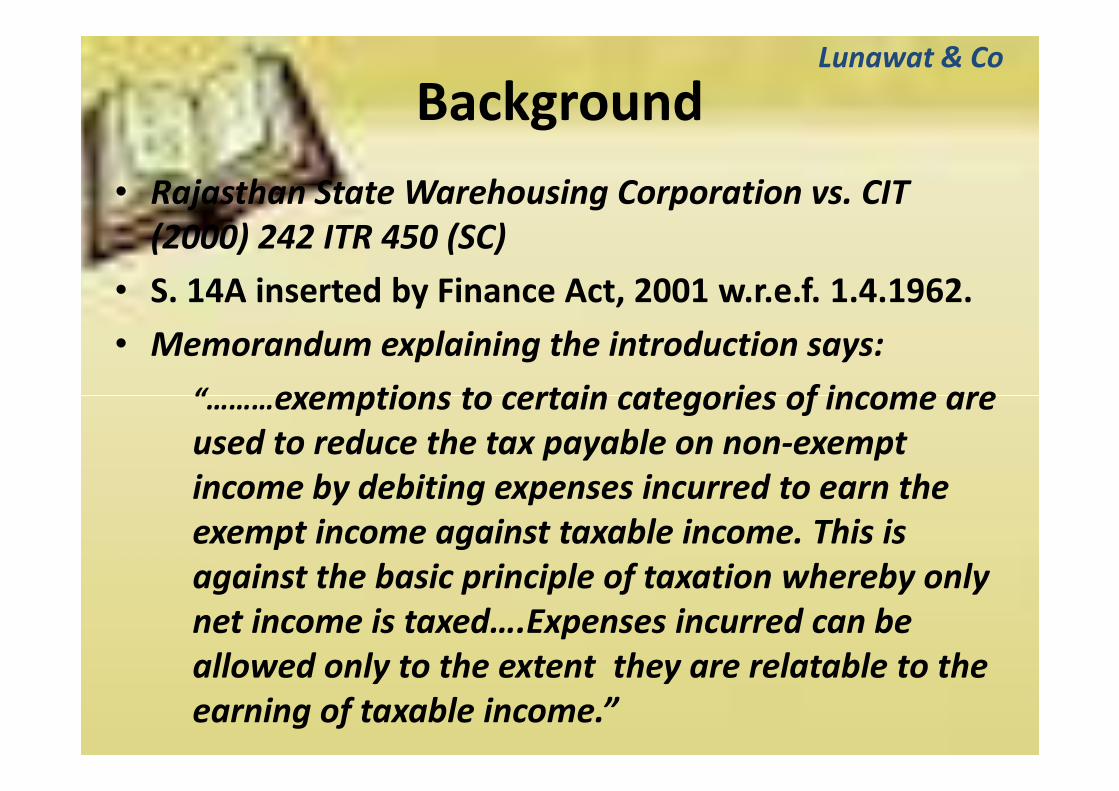

Background

• Rajasthan State Warehousing Corporation vs. CIT

(2000) 242 ITR 450 (SC)

• S. 14A inserted by Finance Act, 2001 w.r.e.f. 1.4.1962.

• Memorandum explaining the introduction says:

“………exemptions to certain categories of income are

Lunawat & Co

“………exemptions to certain categories of income are

used to reduce the tax payable on non‐exempt

income by debiting expenses incurred to earn the

exempt income against taxable income. This is

against the basic principle of taxation whereby only

net income is taxed….Expenses incurred can be

allowed only to the extent they are relatable to the

earning of taxable income.”

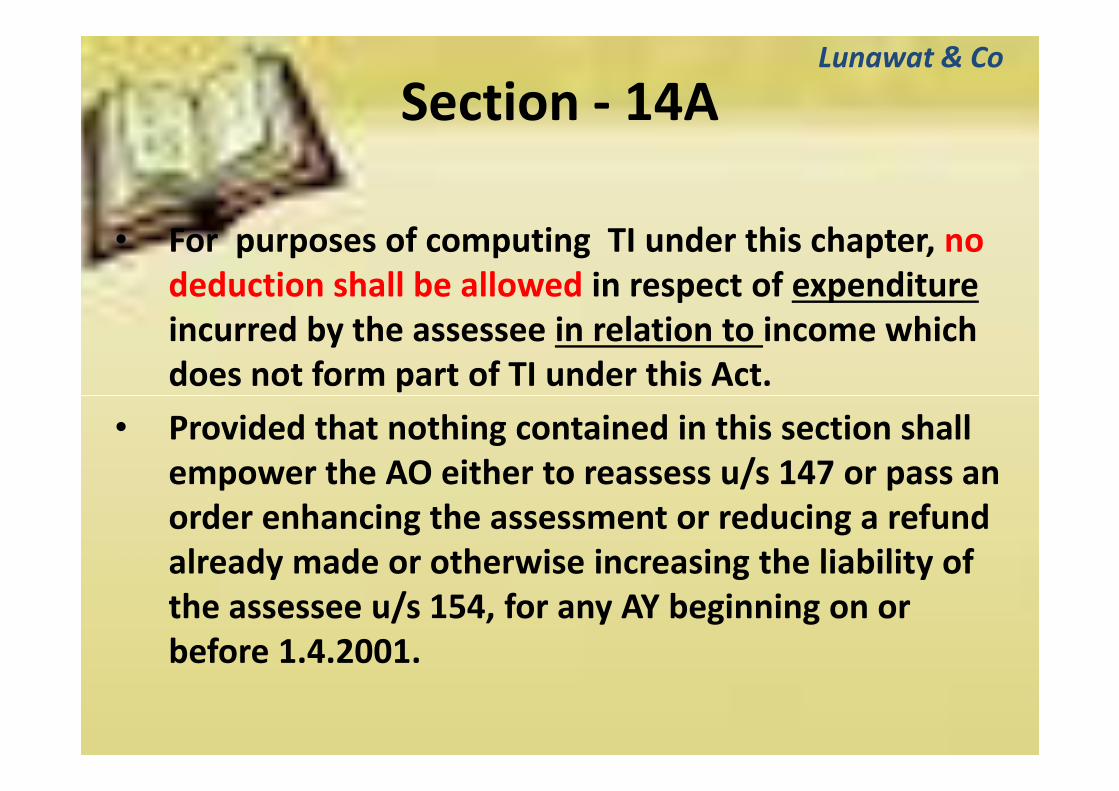

Section - 14A

• For purposes of computing TI under this chapter, no

deduction shall be allowed in respect of expenditure

incurred by the assessee in relation to income which

does not form part of TI under this Act.

Lunawat & Co

does not form part of TI under this Act.

• Provided that nothing contained in this section shall

empower the AO either to reassess u/s 147 or pass an

order enhancing the assessment or reducing a refund

already made or otherwise increasing the liability of

the assessee u/s 154, for any AY beginning on or

before 1.4.2001.

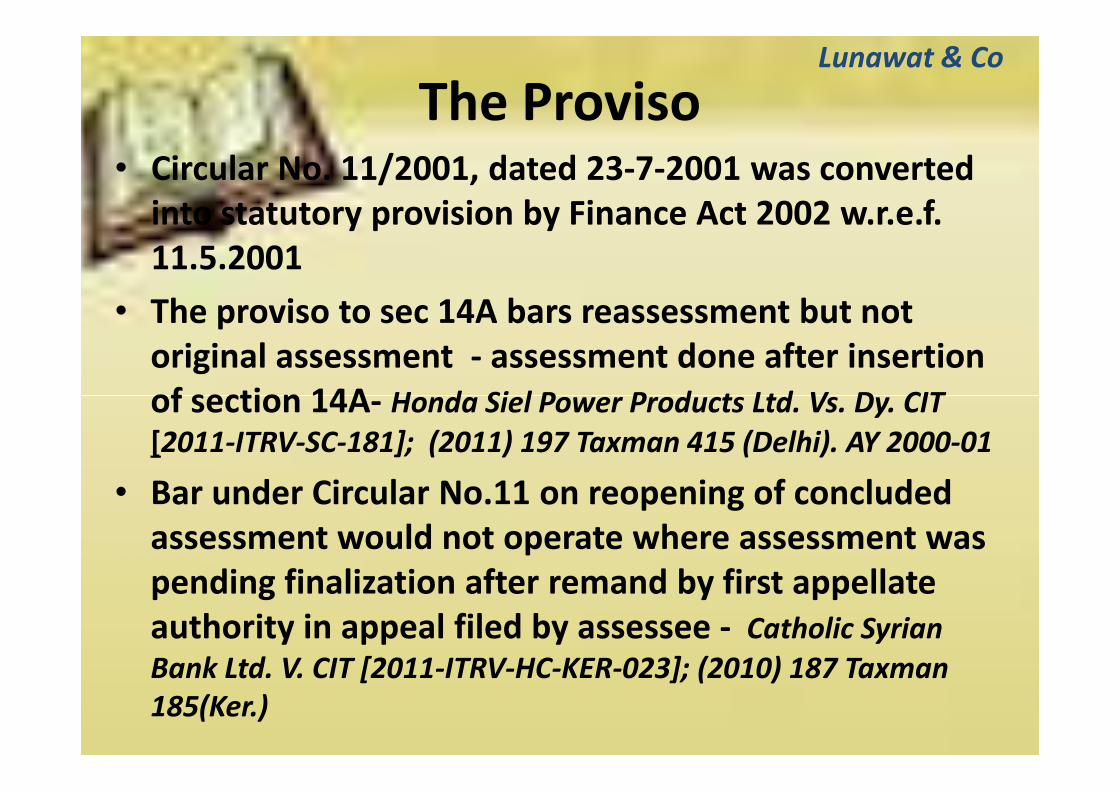

The Proviso• Circular No. 11/2001, dated 23-7-2001 was converted

into statutory provision by Finance Act 2002 w.r.e.f.

11.5.2001

• The proviso to sec 14A bars reassessment but not

original assessment - assessment done after insertion

of section 14A- Honda Siel Power Products Ltd. Vs. Dy. CIT

Lunawat & Co

of section 14A- Honda Siel Power Products Ltd. Vs. Dy. CIT

[2011‐ITRV‐SC‐181]; (2011) 197 Taxman 415 (Delhi). AY 2000‐01

• Bar under Circular No.11 on reopening of concluded

assessment would not operate where assessment was

pending finalization after remand by first appellate

authority in appeal filed by assessee - Catholic Syrian

Bank Ltd. V. CIT [2011‐ITRV‐HC‐KER‐023]; (2010) 187 Taxman

185(Ker.)

The Proviso

• Where order of CIT under section 263 was passed

earlier i.e. on 29/12/1999, the protection under the

proviso is not available ‐ Mahesh G. Shetty & Ors. V. CIT

Lunawat & Co

proviso is not available ‐ Mahesh G. Shetty & Ors. V. CIT

[2011-ITRV-HC-KAR-053]

• Issue to invoke section 14A cannot be raised before the

ITAT for the first time ‐ ACIT v. Delite Enterprises (P.) Ltd.

(2011)50 DTR 193 (MUM.) (Trib.)

Heads of Income

• The provisions of section 14A will apply to all

income which is exempt whether the income is

assessed under the head “Other sources’ or

Lunawat & Co

assessed under the head “Other sources’ or

under the head “Business” because there is

nothing in Section 14A which restricts the

operation of section to income of a particular

nature only - Insaallah Investments Ltd. V. ITO

(2008) 23 SOT 130 (DEL‐ Trib)

Expenditure Incurred

• Covers all forms of expenditure regardless of whether it is fixed, variable, direct, indirect, administrative, managerial or financial.

– Kalpataru Construction Overseas (P.) Ltd. v. Dy. CIT [2007] 13 SOT 194 (Mum. ‐ Trib.)

– Parry Agro Industries v. Asst. CIT 314 ITR (AT) 181(2009) (Cochin)

Lunawat & Co

(Cochin)

• Expenditure to be incurred actually and not notionally. AO should be in a position to pinpoint, with an acceptable degree of accuracy, the expenditure which was incurred by assessee to produce non-taxable income

– Asstt. CIT v. Eicher Ltd. [2006] 101 TTJ (Delhi ‐ Trib.) 369

– Wimco Seedlings Ltd. vDy. CIT[2007] 107 ITD 267 (Del)(TM)

Expenditure in relation to

• Only expenditure which has been proved to be

incurred in relation to earning of tax free income

can be disallowed and section cannot be extended

to disallow even expenditure which is assumed to

have been incurred for earning tax free income.

Lunawat & Co

• Common expenditure incurred cannot be broken

artificially to apportion a part thereof to earning of

tax‐free income on assumption that such part of

common expenditure was incurred in relation to

tax‐free income.

DLF Ltd. v. CIT [2009] 27 SOT 22 (DELHI)

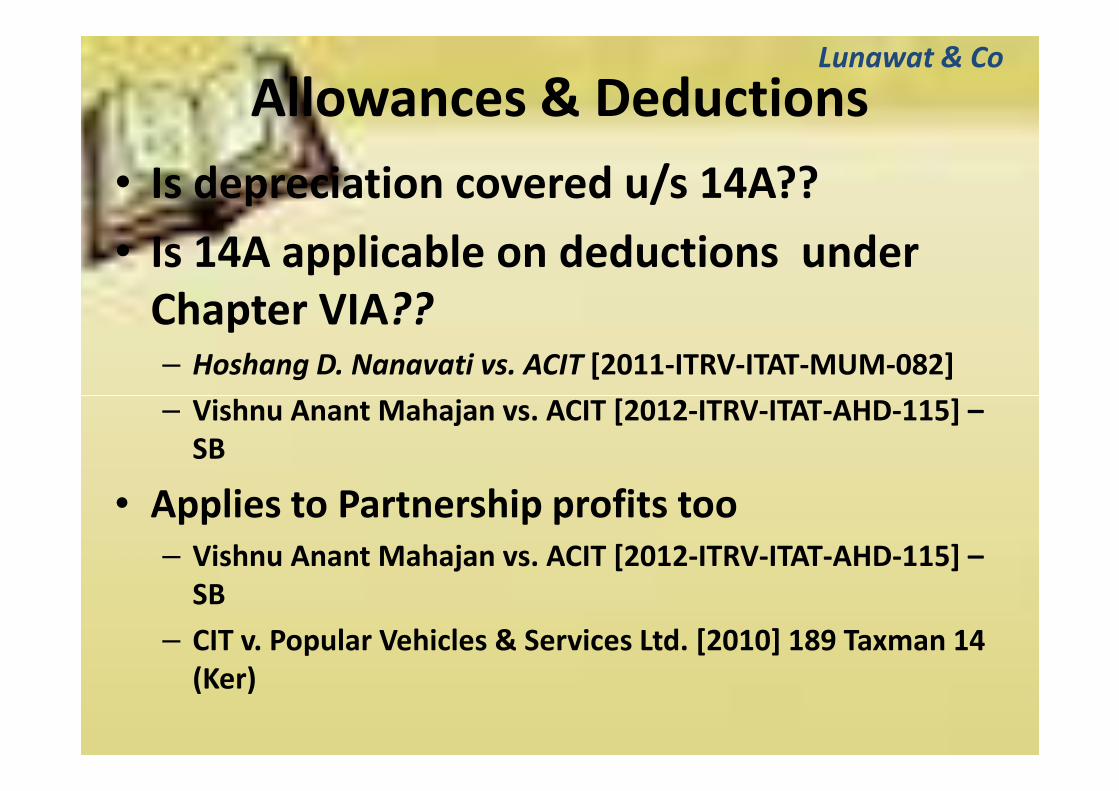

Allowances & Deductions

• Is depreciation covered u/s 14A??

• Is 14A applicable on deductions under

Chapter VIA??– Hoshang D. Nanavati vs. ACIT [2011-ITRV-ITAT-MUM-082]

– Vishnu Anant Mahajan vs. ACIT [2012-ITRV-ITAT-AHD-115] –

Lunawat & Co

– Vishnu Anant Mahajan vs. ACIT [2012-ITRV-ITAT-AHD-115] –

SB

• Applies to Partnership profits too

– Vishnu Anant Mahajan vs. ACIT [2012-ITRV-ITAT-AHD-115] –

SB

– CIT v. Popular Vehicles & Services Ltd. [2010] 189 Taxman 14

(Ker)

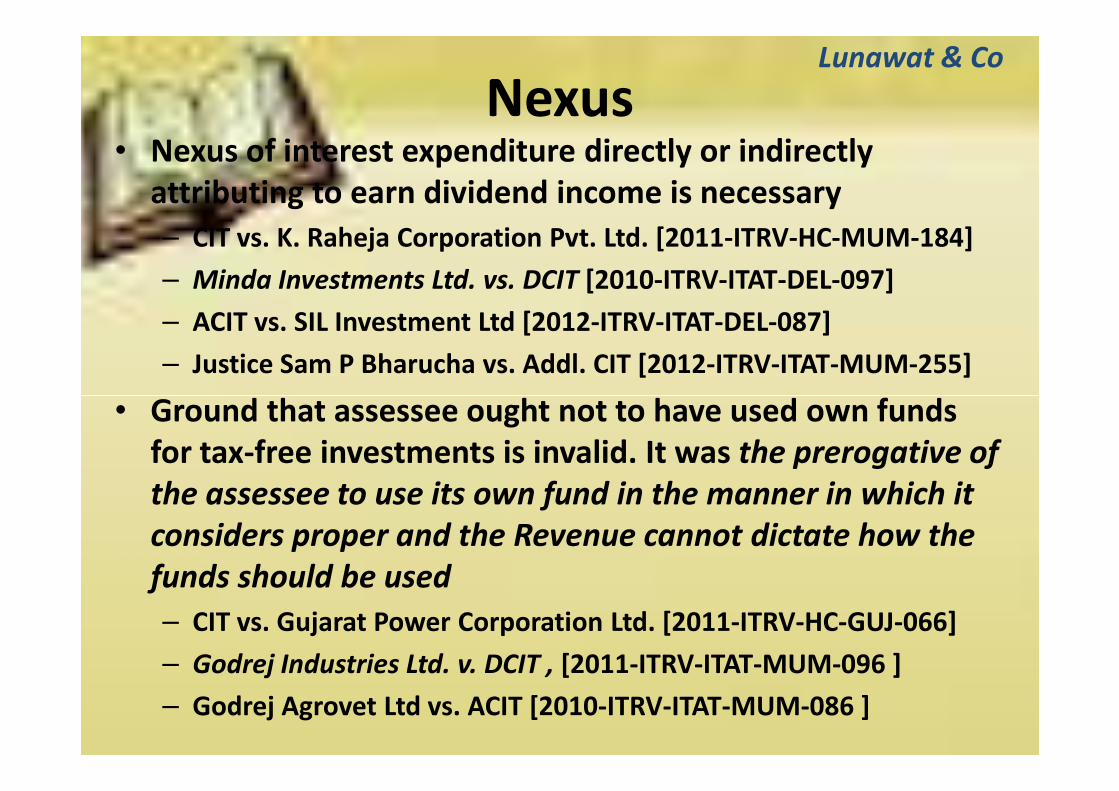

Nexus• Nexus of interest expenditure directly or indirectly

attributing to earn dividend income is necessary

– CIT vs. K. Raheja Corporation Pvt. Ltd. [2011-ITRV-HC-MUM-184]

– Minda Investments Ltd. vs. DCIT [2010-ITRV-ITAT-DEL-097]

– ACIT vs. SIL Investment Ltd [2012-ITRV-ITAT-DEL-087]

– Justice Sam P Bharucha vs. Addl. CIT [2012-ITRV-ITAT-MUM-255]

• Ground that assessee ought not to have used own funds

Lunawat & Co

• Ground that assessee ought not to have used own funds

for tax-free investments is invalid. It was the prerogative of

the assessee to use its own fund in the manner in which it

considers proper and the Revenue cannot dictate how the

funds should be used

– CIT vs. Gujarat Power Corporation Ltd. [2011-ITRV-HC-GUJ-066]

– Godrej Industries Ltd. v. DCIT , [2011-ITRV-ITAT-MUM-096 ]

– Godrej Agrovet Ltd vs. ACIT [2010-ITRV-ITAT-MUM-086 ]

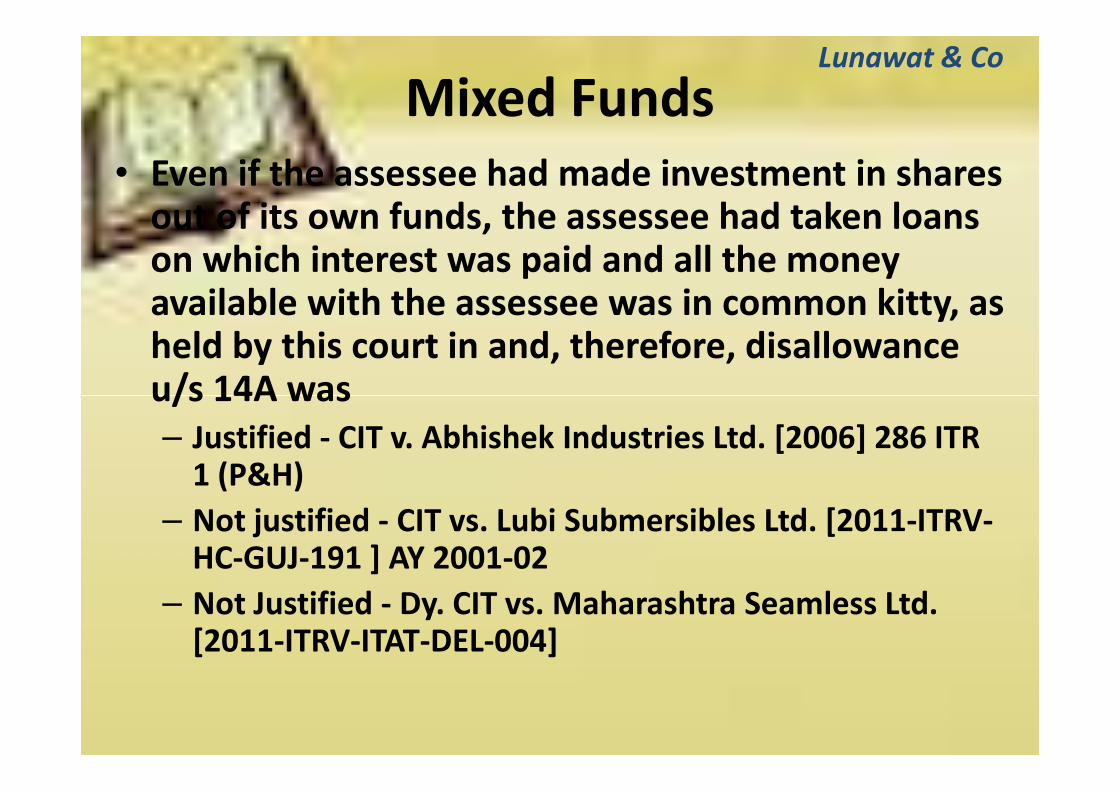

Mixed Funds

• Even if the assessee had made investment in shares out of its own funds, the assessee had taken loans on which interest was paid and all the money available with the assessee was in common kitty, as held by this court in and, therefore, disallowance u/s 14A was

Lunawat & Co

u/s 14A was

– Justified - CIT v. Abhishek Industries Ltd. [2006] 286 ITR 1 (P&H)

– Not justified - CIT vs. Lubi Submersibles Ltd. [2011-ITRV-HC-GUJ-191 ] AY 2001-02

– Not Justified - Dy. CIT vs. Maharashtra Seamless Ltd. [2011-ITRV-ITAT-DEL-004]

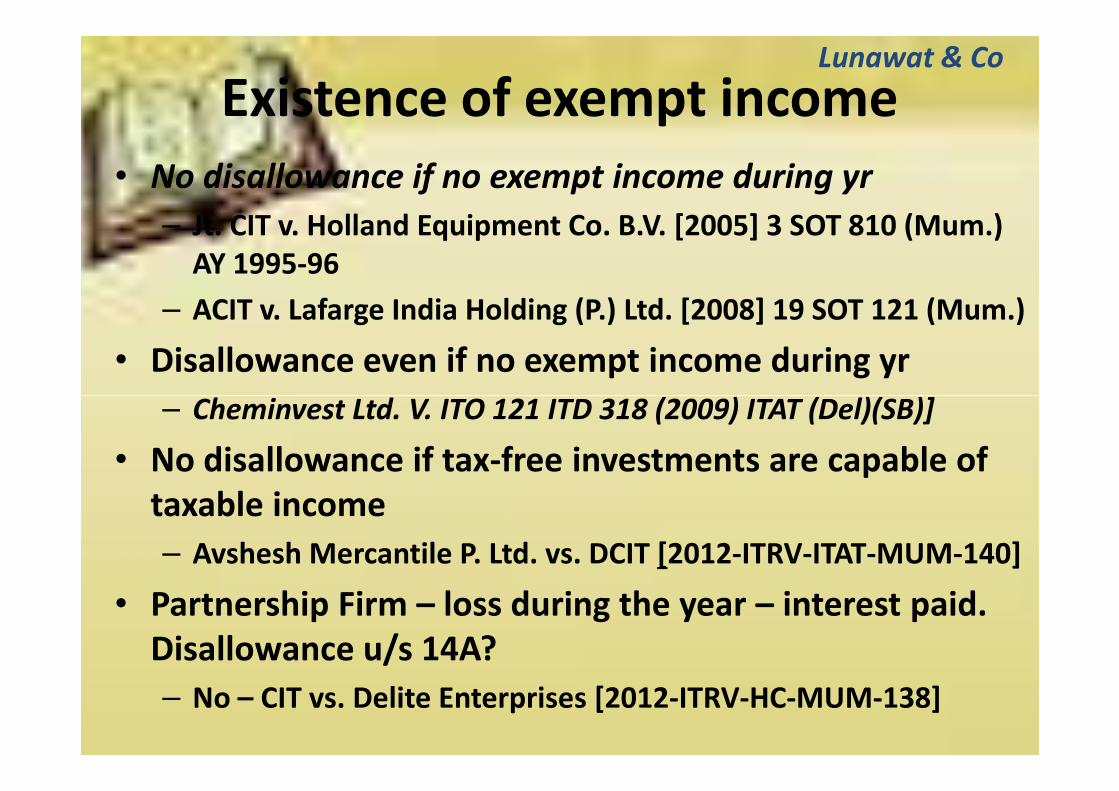

Existence of exempt income

• No disallowance if no exempt income during yr

– Jt. CIT v. Holland Equipment Co. B.V. [2005] 3 SOT 810 (Mum.)

AY 1995-96

– ACIT v. Lafarge India Holding (P.) Ltd. [2008] 19 SOT 121 (Mum.)

• Disallowance even if no exempt income during yr

– Cheminvest Ltd. V. ITO 121 ITD 318 (2009) ITAT (Del)(SB)]

Lunawat & Co

– Cheminvest Ltd. V. ITO 121 ITD 318 (2009) ITAT (Del)(SB)]

• No disallowance if tax-free investments are capable of

taxable income

– Avshesh Mercantile P. Ltd. vs. DCIT [2012-ITRV-ITAT-MUM-140]

• Partnership Firm – loss during the year – interest paid.

Disallowance u/s 14A?

– No – CIT vs. Delite Enterprises [2012-ITRV-HC-MUM-138]

Statutory Compliances

• The expenses, if at all were expenses, they were

incurred not for earning tax-free income but for

maintaining the required SLR.

• The tax-free interest is only an incidence on

Lunawat & Co

• The tax-free interest is only an incidence on

fulfillment of SLR requirements. Then, section

14A has no application in this case.

– State Bank of Travancore Vs. Assit. CIT [2009] 318

ITR (AT) 171- (ITAT-COCHIN )

Interest capitalized

• Where the interest on borrowings made for investment in shares is capitalised, since in such a case interest paid is not in relation to exempt income, but as part of cost of share, such interest could not be disallowed u/s 14A - S. Balan V. Dy. CIT 120 ITD 469 (2009) ITAT(Pune)

Lunawat & Co

CIT 120 ITD 469 (2009) ITAT(Pune)

• Interest paid on borrowed funds utilized for the purpose of investment in shares was not to be allowed as either an expenditure or as part of cost of acquisition of the shares, in view of the provisions of section 14A as the shares were not sold during the year-Harish Krishnakant Bhatt v. ITO [2004] 85 TTJ 872

Personal Tax Free Income• Would personal Tax Free income like PPF Interest,

dividend, etc come under 14A purview?

• The assessee is maintaining separate books of account for the purpose of business. The tax-free investments are in his personal capacity. As the Assessing Officer has not disallowed any expenditure of personal nature out of the business income, the expenditure claimed in the business of share dealings cannot be correlated to the

Lunawat & Co

business income, the expenditure claimed in the business of share dealings cannot be correlated to the incomes earned in personal capacity that too on dividend, PPF interest and tax free interest on RBI bonds

• Accordingly, the estimation of expenditure out of business expenditure as being incurred for earning tax free income is not acceptable.

Pawan Kumar Parmeshwarlal vs. ACIT

[2011-ITRV-ITAT-MUM-006]

Applicability in case of Chapter VIA

• Expenditure incurred for earning of export income which is

exempt u/s80HHC, cannot be held to be income which does not

form part of total income. Such expenses cannot be disallowed

u/s14A - CIT v. Kings exports 318 ITR 100 (2009) (Punj. & Har.)

• Section 14A could not be applied to provisions of Chapter VI-A

where deductions are to be made in computing the total income

and in no way that can be compared with the exempted income

Lunawat & Co

and in no way that can be compared with the exempted income

which does not form part of the total income- ACIT v. Tamil

Nadu Silk Producers Federation Ltd. [2006] 103 TTJ (Chennai)

716]; ACIT vs. Bank of Madura [2011] 007 ITR (Trib) 139 ITAT

[chen]

• Deduction of income derived by a co-operative society u/s 80P is

not a case of “exempt income” but of “deduction from income”.

Therefore provisions of sec.14A are not applicable in this case ‐

ACIT Vs. Kribhco 6 ITR 686 (2010) (ITAT‐Del)

Investment company

• In case of an investment company, where the business of the company is to invest its funds in the share of sister concerns and other companies and also deposit the money with group concerns on which interest is received, the infrastructure of the company is utilized for the purpose of carrying out its objects, i.e., investment in other concerns and

Lunawat & Co

its objects, i.e., investment in other concerns and also earning income on such investments. In such a case, assessee is required to furnish details of expenditure incurred on salary of staff utilized for the object of assessee‐company, which would be disallowed otherwise it would be disallowed under section14A on estimate basis – Dy. CIT V. Tata Investment Corporation Ltd. (2007) 295 ITR

330(Mum‐Trib)

Separate books?

• Section 14A authorises AO to make disallowance of expenditure incurred for earning tax free income, irrespective of whether assessee maintained separate accounts or not with regard to expenditure incurred for earning non-taxable income. CIT v. The Catholic Syrian Bank Ltd. [ 2011‐ITRV‐HC‐KER‐023 ]

Lunawat & Co

Catholic Syrian Bank Ltd. [ 2011‐ITRV‐HC‐KER‐023 ]

• Non maintenance of separate accounts by assesseewith regard to expenditure incurred for earning non‐taxable income was not justification to claim immunity from operation of section14A. CIT v. Dhanalakshmy Bank Ltd, [2011] 10 taxmann.com 213(Ker.)

Lunawat & Co

Section - 14AFinance Act 2006 inserted s.ss (2) & (3) w.e.f. AY 2007‐08:

1. For purposes of computing TI under this chapter, no

deduction shall be allowed in respect of expenditure

incurred by the assessee in relation to income which

does not form part of TI under this Act.

2. The AO shall determine the amount of expenditure

Lunawat & Co

2. The AO shall determine the amount of expenditure

incurred in relation to such income which does not

form part of the TI under this Act in accordance with

such method as may be prescribed, if the AO, having

regard to the accounts of the assessee, is not satisfied

with the correctness of the claim of the assessee in

respect of such expenditure in relation to income

which does not form part of TI under this Act

Section - 14A3. The provisions of sub‐section (2) shall also apply in

relation to a case where an assessee claims that no

expenditure has been incurred by him in relation to

income which does not form part of the total income

under this Act

4. Provided that nothing contained in this section shall

Lunawat & Co

4. Provided that nothing contained in this section shall

empower the AO either to reassess u/s 147 or pass an

order enhancing the assessment or reducing a refund

already made or otherwise increasing the liability of

the assessee u/s 154, for any AY beginning on or before

1.4.2001.

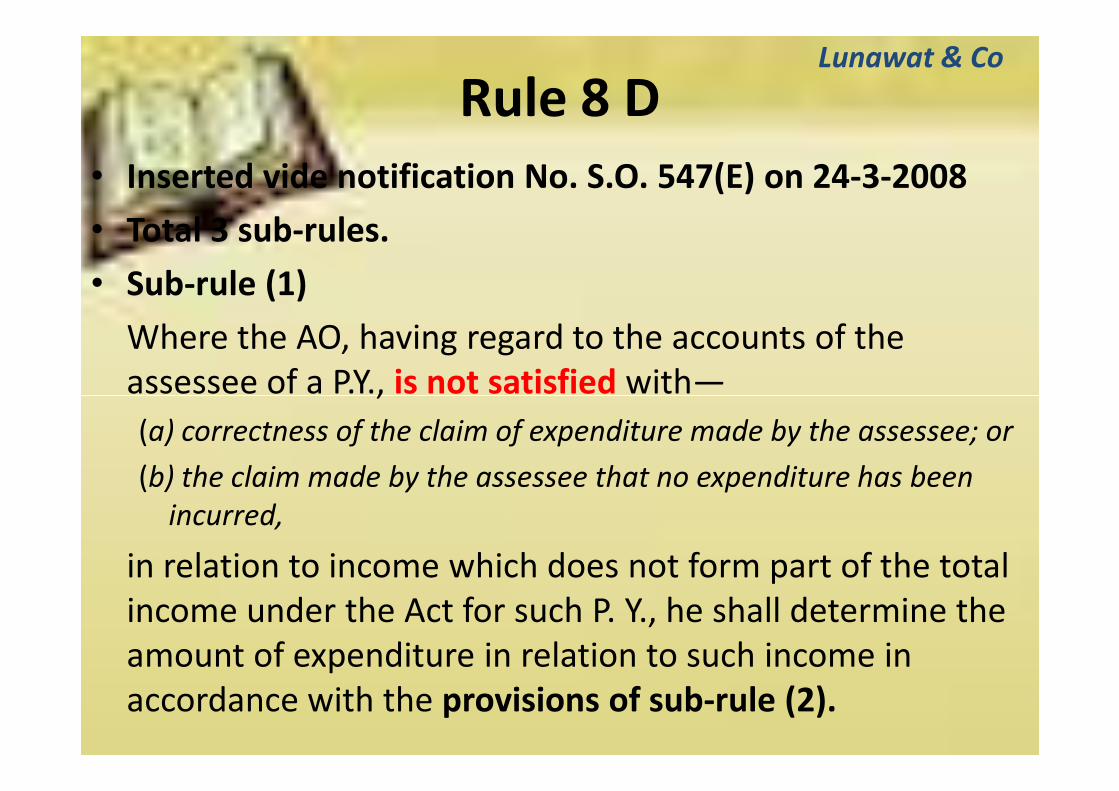

Rule 8 D

• Inserted vide notification No. S.O. 547(E) on 24-3-2008

• Total 3 sub-rules.

• Sub-rule (1)

Where the AO, having regard to the accounts of the

assessee of a P.Y., is not satisfied with—

Lunawat & Co

assessee of a P.Y., is not satisfied with—

(a) correctness of the claim of expenditure made by the assessee; or

(b) the claim made by the assessee that no expenditure has been

incurred,

in relation to income which does not form part of the total

income under the Act for such P. Y., he shall determine the

amount of expenditure in relation to such income in

accordance with the provisions of sub-rule (2).

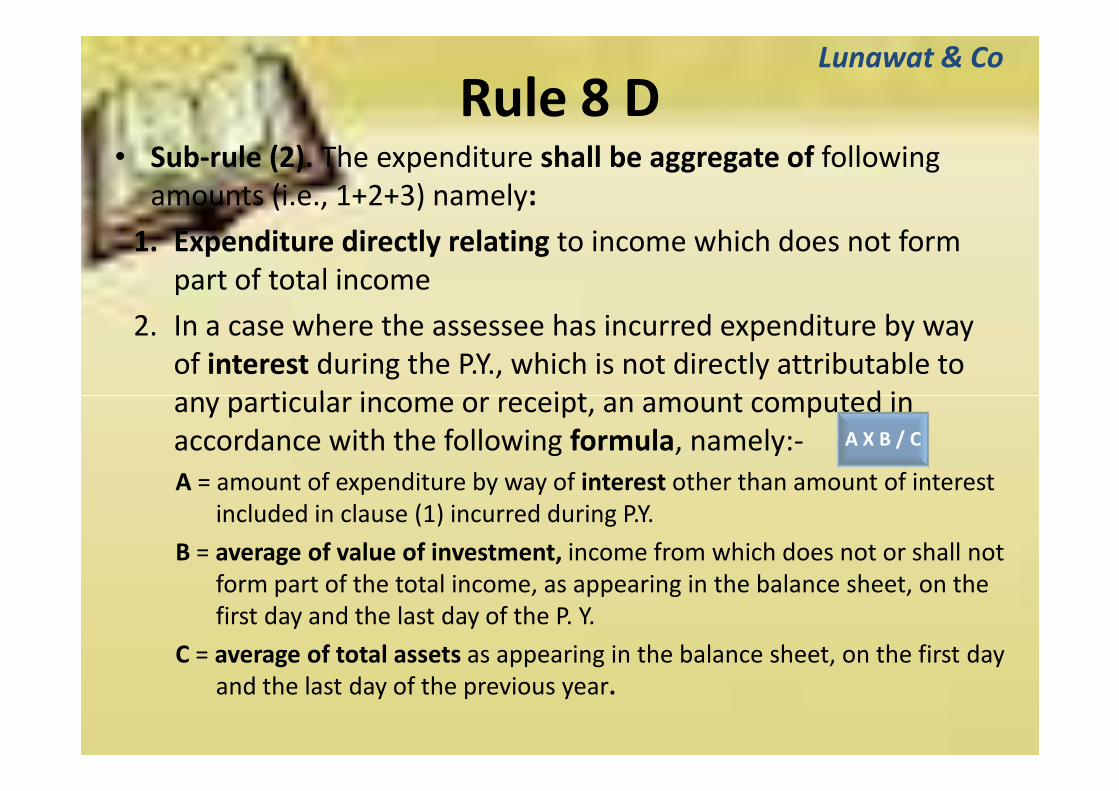

Rule 8 D• Sub-rule (2). The expenditure shall be aggregate of following

amounts (i.e., 1+2+3) namely:

1. Expenditure directly relating to income which does not form

part of total income

2. In a case where the assessee has incurred expenditure by way

of interest during the P.Y., which is not directly attributable to

any particular income or receipt, an amount computed in

Lunawat & Co

any particular income or receipt, an amount computed in

accordance with the following formula, namely:‐

A = amount of expenditure by way of interest other than amount of interest

included in clause (1) incurred during P.Y.

B = average of value of investment, income from which does not or shall not

form part of the total income, as appearing in the balance sheet, on the

first day and the last day of the P. Y.

C = average of total assets as appearing in the balance sheet, on the first day

and the last day of the previous year.

A X B / C

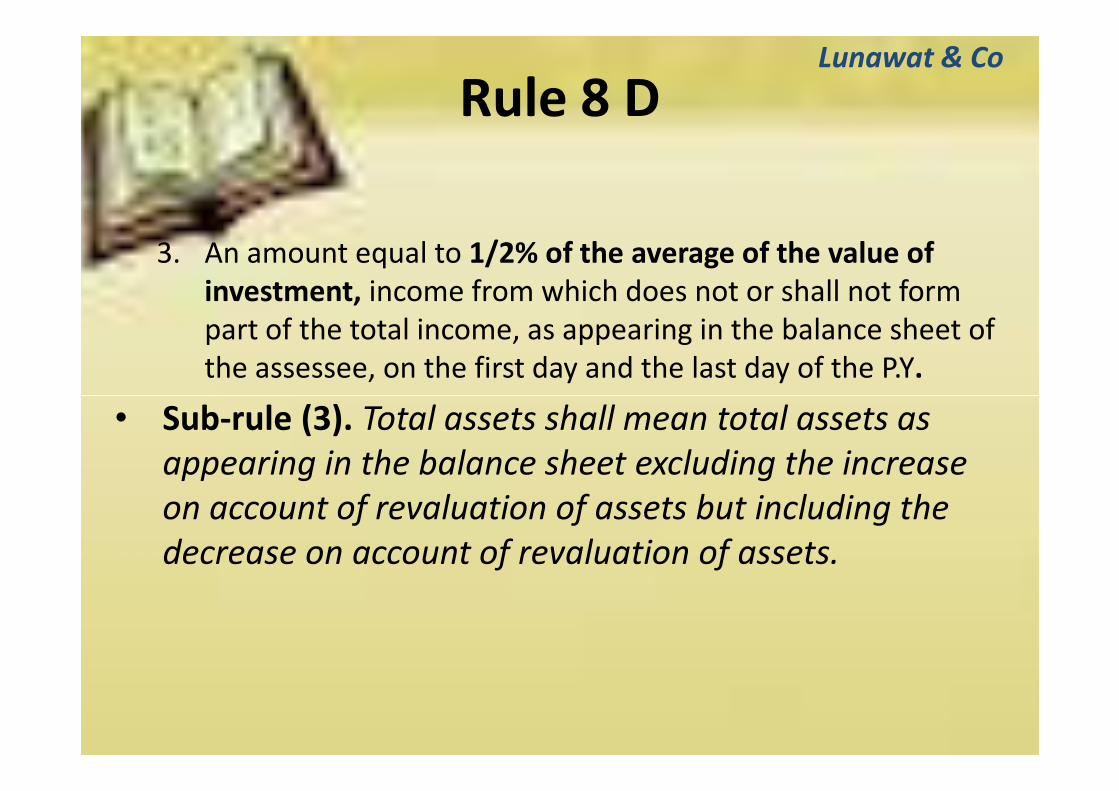

Rule 8 D

3. An amount equal to 1/2% of the average of the value of

investment, income from which does not or shall not form

part of the total income, as appearing in the balance sheet of

the assessee, on the first day and the last day of the P.Y.

Sub-rule (3). Total assets shall mean total assets as

Lunawat & Co

• Sub-rule (3). Total assets shall mean total assets as

appearing in the balance sheet excluding the increase

on account of revaluation of assets but including the

decrease on account of revaluation of assets.

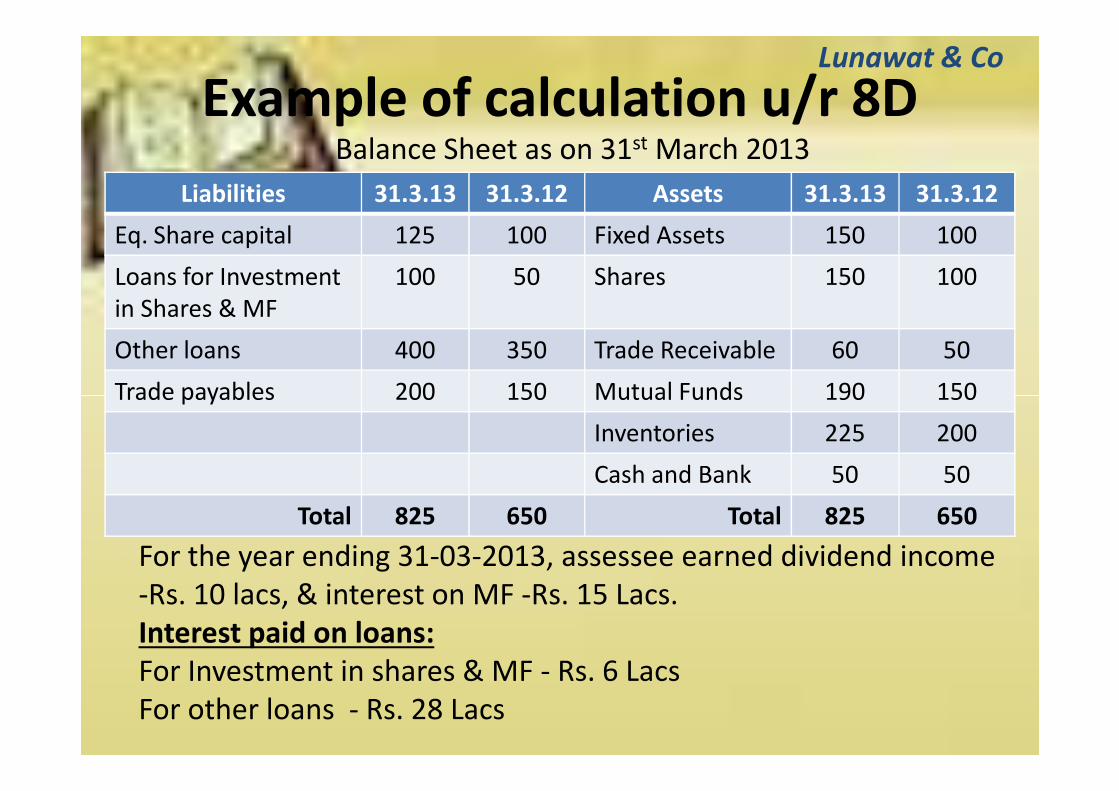

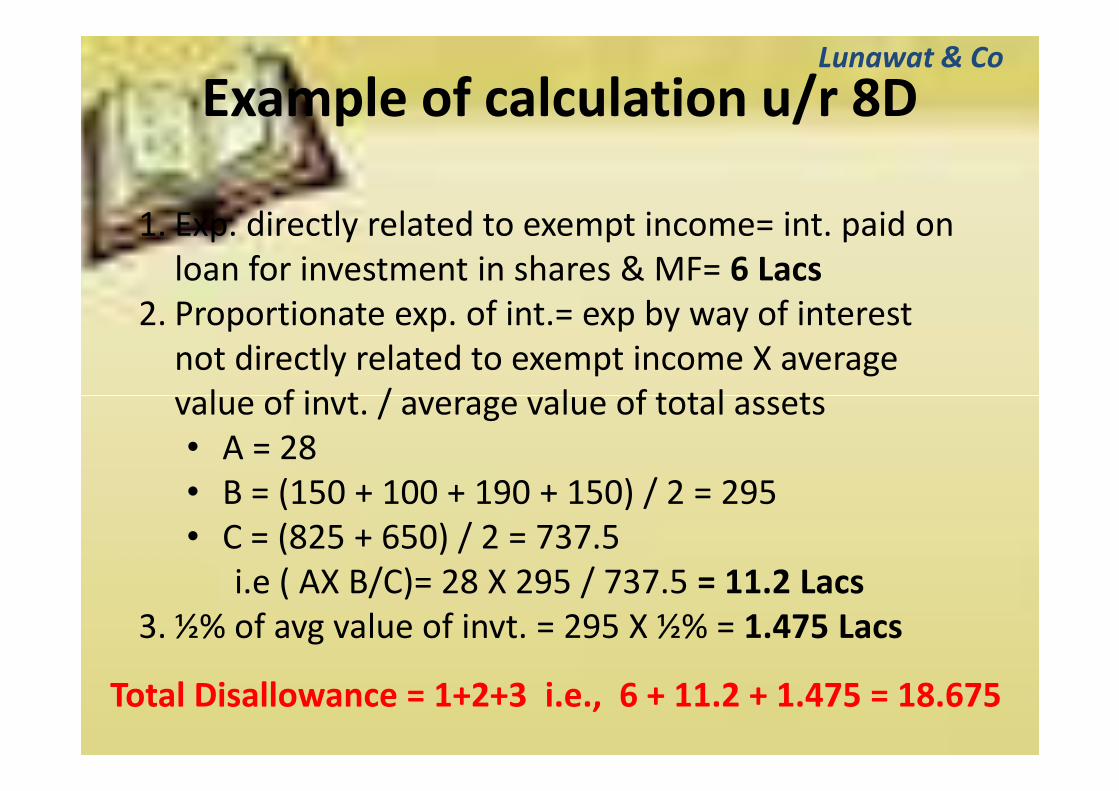

Example of calculation u/r 8D

Liabilities 31.3.13 31.3.12 Assets 31.3.13 31.3.12

Eq. Share capital 125 100 Fixed Assets 150 100

Loans for Investment

in Shares & MF

100 50 Shares 150 100

Other loans 400 350 Trade Receivable 60 50

Trade payables 200 150 Mutual Funds 190 150

Balance Sheet as on 31st March 2013

Lunawat & Co

Trade payables 200 150 Mutual Funds 190 150

Inventories 225 200

Cash and Bank 50 50

Total 825 650 Total 825 650

For the year ending 31‐03‐2013, assessee earned dividend income

‐Rs. 10 lacs, & interest on MF ‐Rs. 15 Lacs.

Interest paid on loans:

For Investment in shares & MF ‐ Rs. 6 Lacs

For other loans ‐ Rs. 28 Lacs

Example of calculation u/r 8D

1. Exp. directly related to exempt income= int. paid on

loan for investment in shares & MF= 6 Lacs

2. Proportionate exp. of int.= exp by way of interest

not directly related to exempt income X average

value of invt. / average value of total assets

Lunawat & Co

Total Disallowance = 1+2+3 i.e., 6 + 11.2 + 1.475 = 18.675

value of invt. / average value of total assets

• A = 28

• B = (150 + 100 + 190 + 150) / 2 = 295

• C = (825 + 650) / 2 = 737.5

i.e ( AX B/C)= 28 X 295 / 737.5 = 11.2 Lacs

3. ½% of avg value of invt. = 295 X ½% = 1.475 Lacs

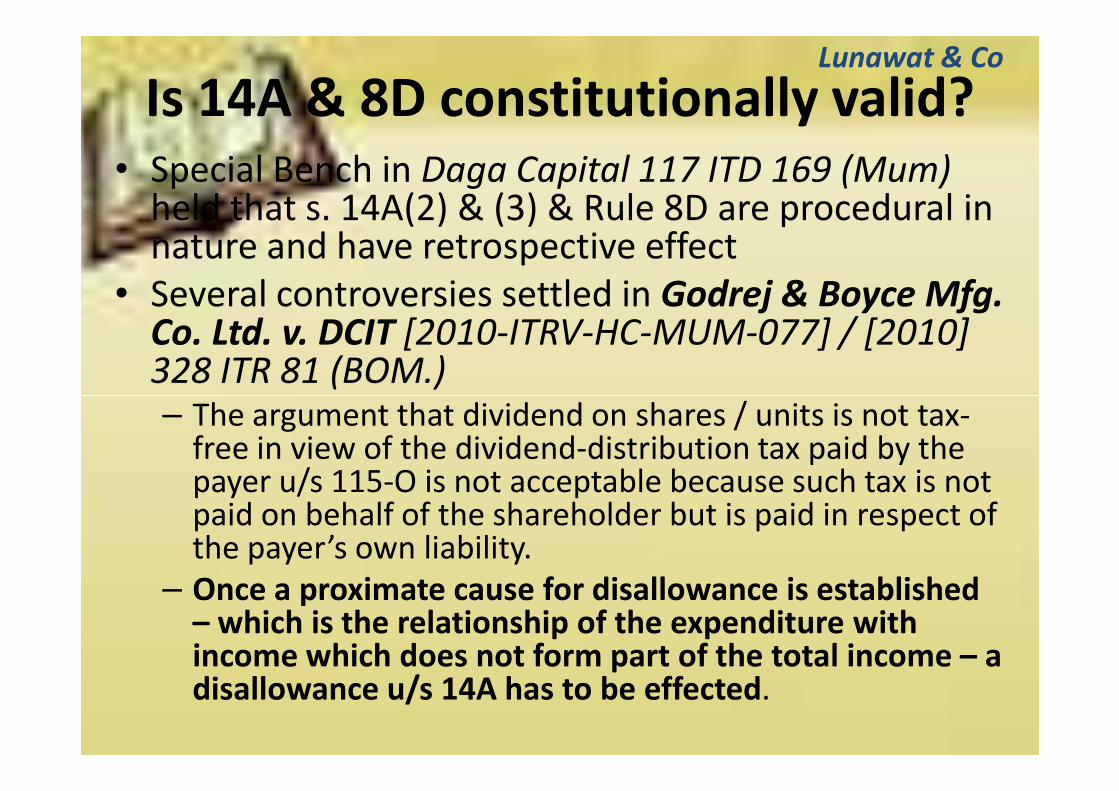

Is 14A & 8D constitutionally valid?• Special Bench in Daga Capital 117 ITD 169 (Mum)

held that s. 14A(2) & (3) & Rule 8D are procedural in nature and have retrospective effect

• Several controversies settled in Godrej & Boyce Mfg. Co. Ltd. v. DCIT [2010-ITRV-HC-MUM-077] / [2010] 328 ITR 81 (BOM.)– The argument that dividend on shares / units is not tax‐

Lunawat & Co

– The argument that dividend on shares / units is not tax‐free in view of the dividend‐distribution tax paid by the payer u/s 115‐O is not acceptable because such tax is not paid on behalf of the shareholder but is paid in respect of the payer’s own liability.

– Once a proximate cause for disallowance is established – which is the relationship of the expenditure with income which does not form part of the total income – a disallowance u/s 14A has to be effected.

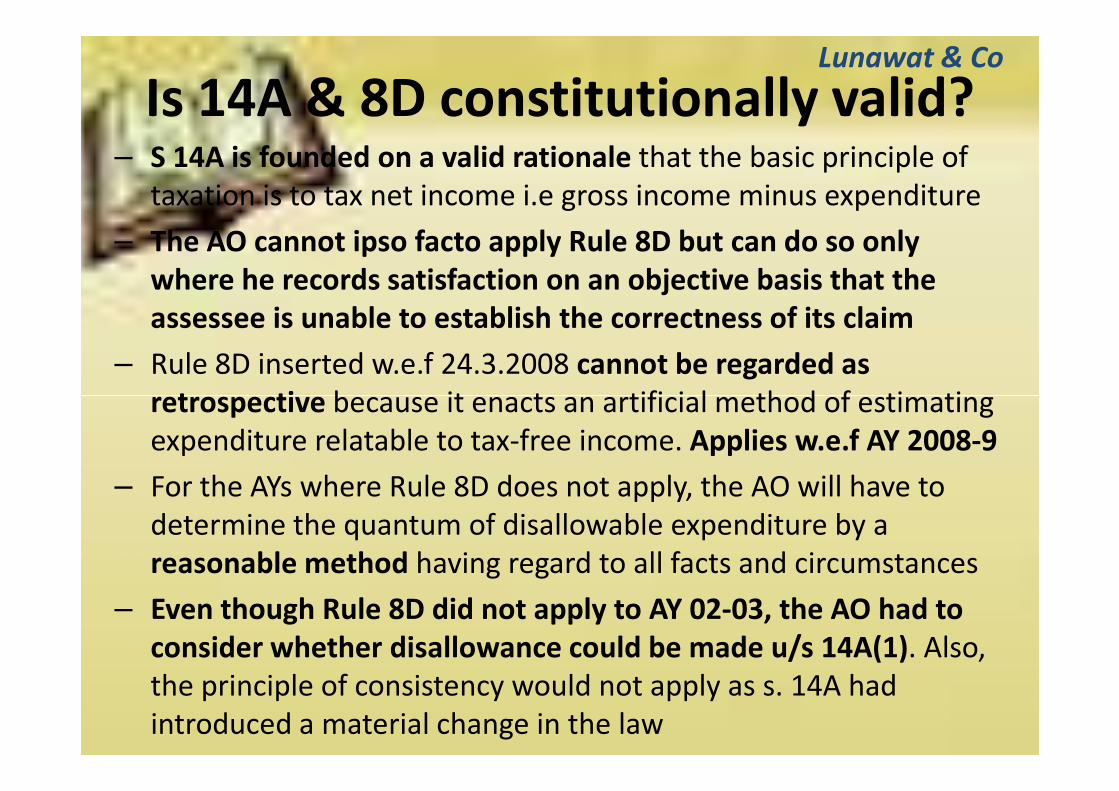

Is 14A & 8D constitutionally valid?– S 14A is founded on a valid rationale that the basic principle of

taxation is to tax net income i.e gross income minus expenditure

– The AO cannot ipso facto apply Rule 8D but can do so only

where he records satisfaction on an objective basis that the

assessee is unable to establish the correctness of its claim

– Rule 8D inserted w.e.f 24.3.2008 cannot be regarded as

retrospective because it enacts an artificial method of estimating

Lunawat & Co

retrospective because it enacts an artificial method of estimating

expenditure relatable to tax‐free income. Applies w.e.f AY 2008-9

– For the AYs where Rule 8D does not apply, the AO will have to

determine the quantum of disallowable expenditure by a

reasonable method having regard to all facts and circumstances

– Even though Rule 8D did not apply to AY 02-03, the AO had to

consider whether disallowance could be made u/s 14A(1). Also,

the principle of consistency would not apply as s. 14A had

introduced a material change in the law

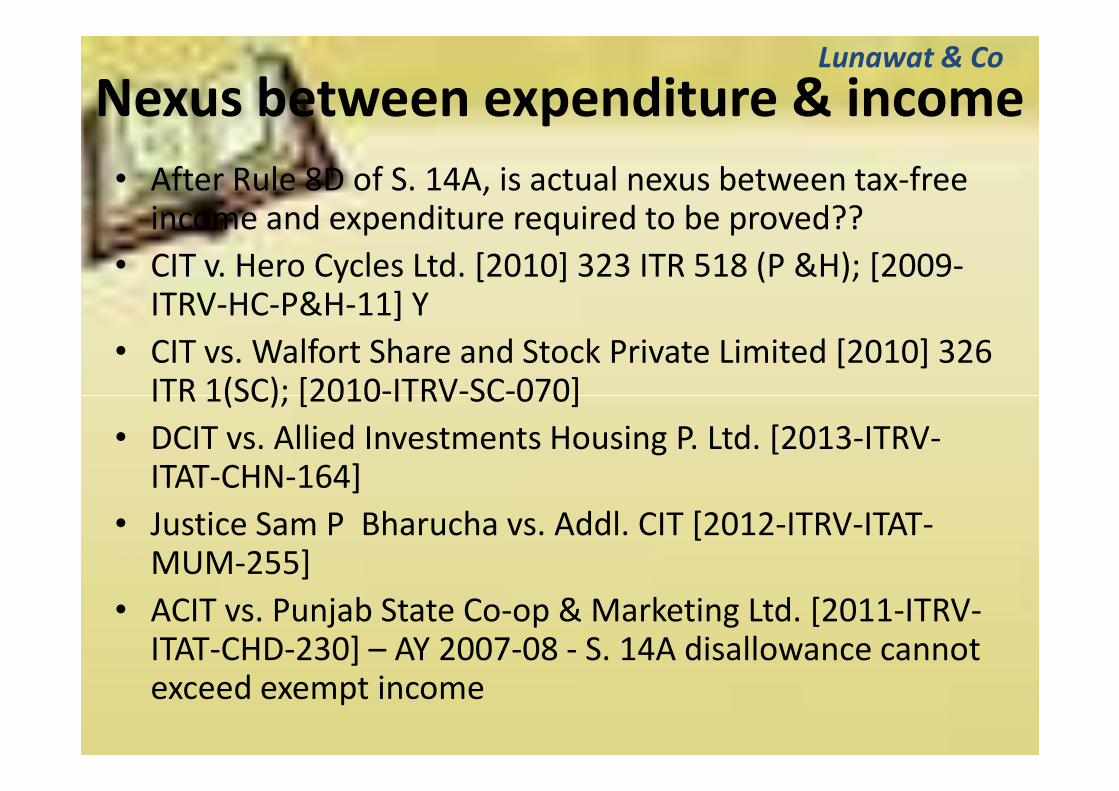

Nexus between expenditure & income

• After Rule 8D of S. 14A, is actual nexus between tax‐free income and expenditure required to be proved??

• CIT v. Hero Cycles Ltd. [2010] 323 ITR 518 (P &H); [2009‐ITRV‐HC‐P&H‐11] Y

• CIT vs. Walfort Share and Stock Private Limited [2010] 326 ITR 1(SC); [2010‐ITRV‐SC‐070]

Lunawat & Co

ITR 1(SC); [2010‐ITRV‐SC‐070]

• DCIT vs. Allied Investments Housing P. Ltd. [2013‐ITRV‐ITAT‐CHN‐164]

• Justice Sam P Bharucha vs. Addl. CIT [2012‐ITRV‐ITAT‐MUM‐255]

• ACIT vs. Punjab State Co‐op & Marketing Ltd. [2011‐ITRV‐ITAT‐CHD‐230] – AY 2007‐08 ‐ S. 14A disallowance cannot exceed exempt income

Satisfaction of AO• It is a pre‐requisite that before invoking Rule 8D, the AO

must record his satisfaction on how the assessee’s

calculation is incorrect. AO cannot apply Rule 8D

without pointing out any inaccuracy in method of

apportionment or allocation of expenses. Onus is on AO

to show that expenditure has been incurred by assessee

Lunawat & Co

to show that expenditure has been incurred by assessee

for earning tax‐free income. Without discharging the

onus, AO is not entitled to make an ad hoc disallowance

– DCIT vs. Jindal Photo Ltd. [2011‐ITRV‐ITAT‐DEL‐229] AY 2008-09

– AY 2007-08 followed

• AO has to show how assessee is wrong even if he claims

no expenditure was incurred

– DCIT vs. Ashish Jhunjhunwala [2013‐ITRV‐ITAT‐KOL‐071]

Maxxop Investment Ltd. vs. CIT• Batch of 21 appeals decided on 14A read with Rule 8D

[2011-ITRV-HC-DEL-253]

• The argument that if the dominant and main objective

of the expenditure was not the earning of ‘exempt’

income then, the expenditure cannot be disallowed

u/s 14A is not acceptable. The expression “in relation

Lunawat & Co

u/s 14A is not acceptable. The expression “in relation

to” cannot be given a narrow meaning and simply

means “in connection with” or “pertaining to”.

• The expression “expenditure incurred” in s. 14A refers

to actual expenditure and not to some imagined

expenditure. If no expenditure is incurred in relation to

exempt income, no disallowance can be made u/s 14A

Maxxop Investment• The AO cannot proceed to determine the amount of

expenditure incurred in relation to exempt income without

recording a finding that he is not satisfied with the

correctness of the claim of the assessee. This is a condition

precedent.

• Rule 8D comes into play only when the AO records a finding

that he is not satisfied with the assessee’s method. Though s.

Lunawat & Co

that he is not satisfied with the assessee’s method. Though s.

14A(2) & (3) were inserted w.e.f. 1.4.1962, Rule 8D was

inserted on 24.03.2008. Accordingly, Rule 8D would operate

prospectively.

• For periods prior to Rule 8D, the AO will have to adopt a

reasonable method on the basis of objective criteria to

determine the expenditure. However, here also, he will have

to show why he is not satisfied with the correctness of the

assessee’s claim

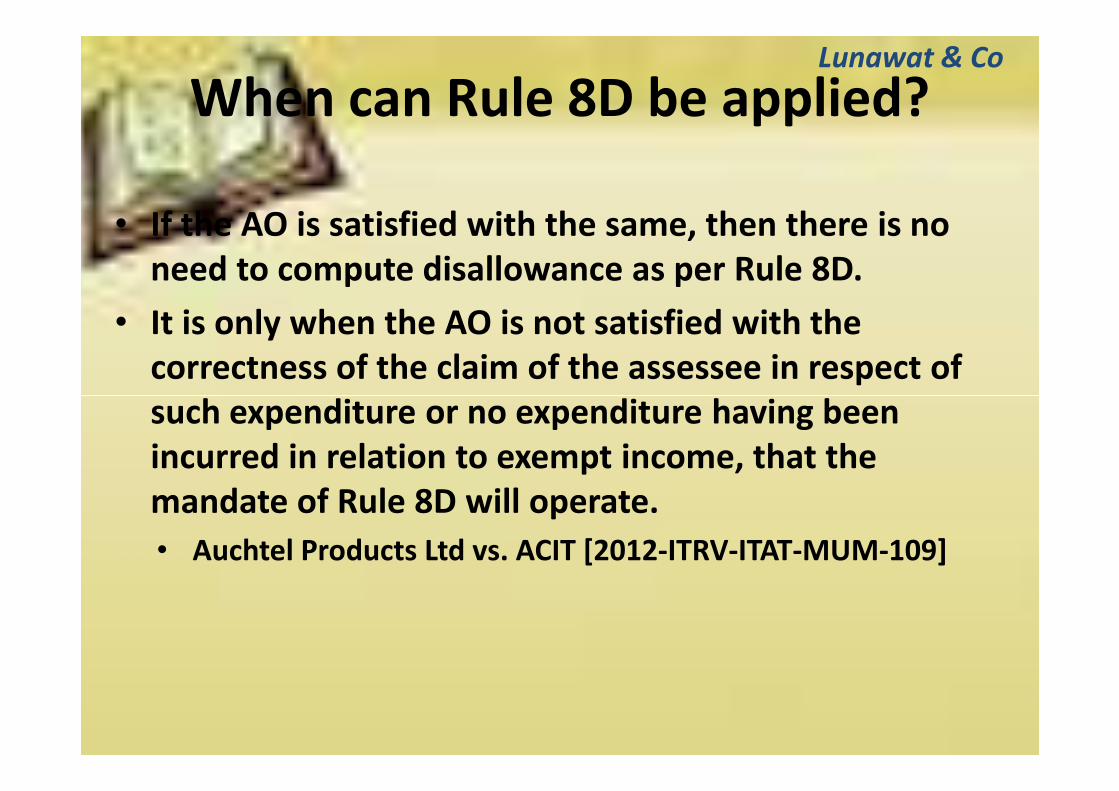

When can Rule 8D be applied?• The satisfaction of AO as to incorrect claim made by

the assessee is sine qua non for invoking the

applicability of Rule 8D. The satisfaction can be

reached only when claim of the assessee is verified.

• If the assessee proves before AO that it incurred a

particular expenditure in respect of earning the

Lunawat & Co

particular expenditure in respect of earning the

exempt income and the AO is satisfied, then there is no

requirement to proceed with the computation under

Rule 8D. Rule 8D is not automatic.

• The correct sequence for making any disallowance

u/s14A is to, firstly, examine the assessee’s claim of

having incurred some expenditure or no expenditure in

relation to exempt income.

When can Rule 8D be applied?

• If the AO is satisfied with the same, then there is no

need to compute disallowance as per Rule 8D.

• It is only when the AO is not satisfied with the

correctness of the claim of the assessee in respect of

such expenditure or no expenditure having been

Lunawat & Co

such expenditure or no expenditure having been

incurred in relation to exempt income, that the

mandate of Rule 8D will operate.

• Auchtel Products Ltd vs. ACIT [2012-ITRV-ITAT-MUM-109]

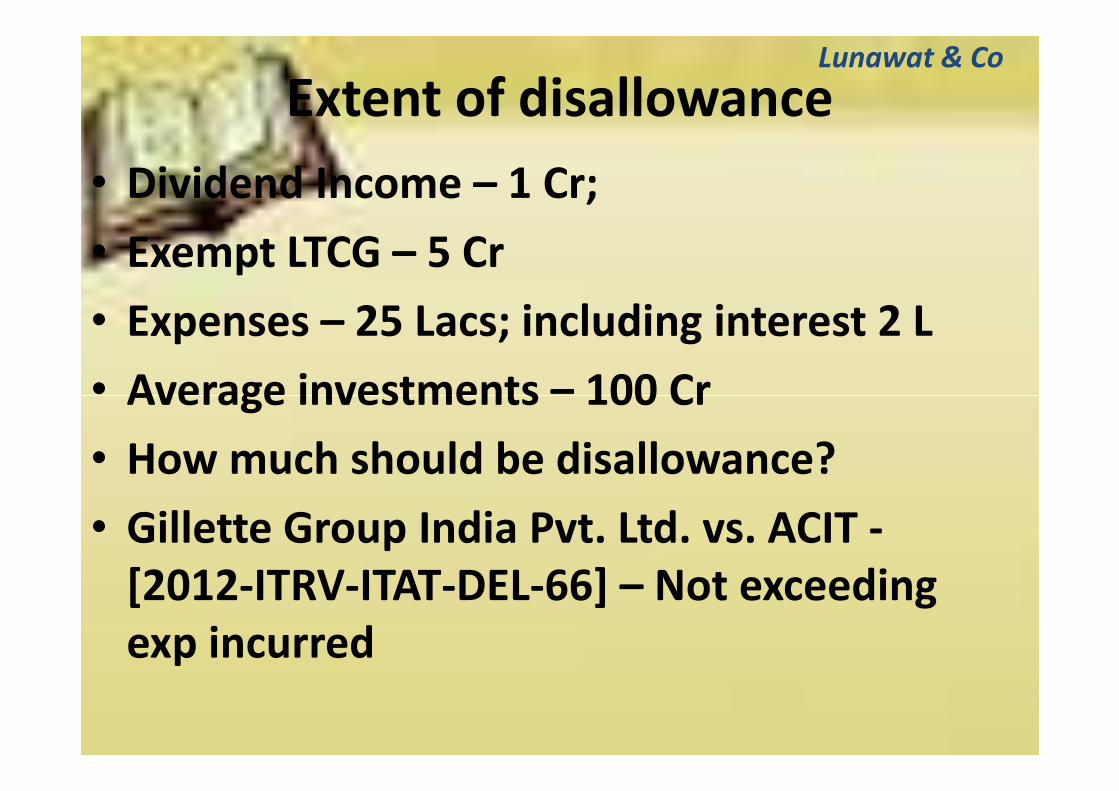

Extent of disallowance

• Dividend Income – 1 Cr;

• Exempt LTCG – 5 Cr

• Expenses – 25 Lacs; including interest 2 L

• Average investments – 100 Cr

Lunawat & Co

• Average investments – 100 Cr

• How much should be disallowance?

• Gillette Group India Pvt. Ltd. vs. ACIT -

[2012-ITRV-ITAT-DEL-66] – Not exceeding

exp incurred

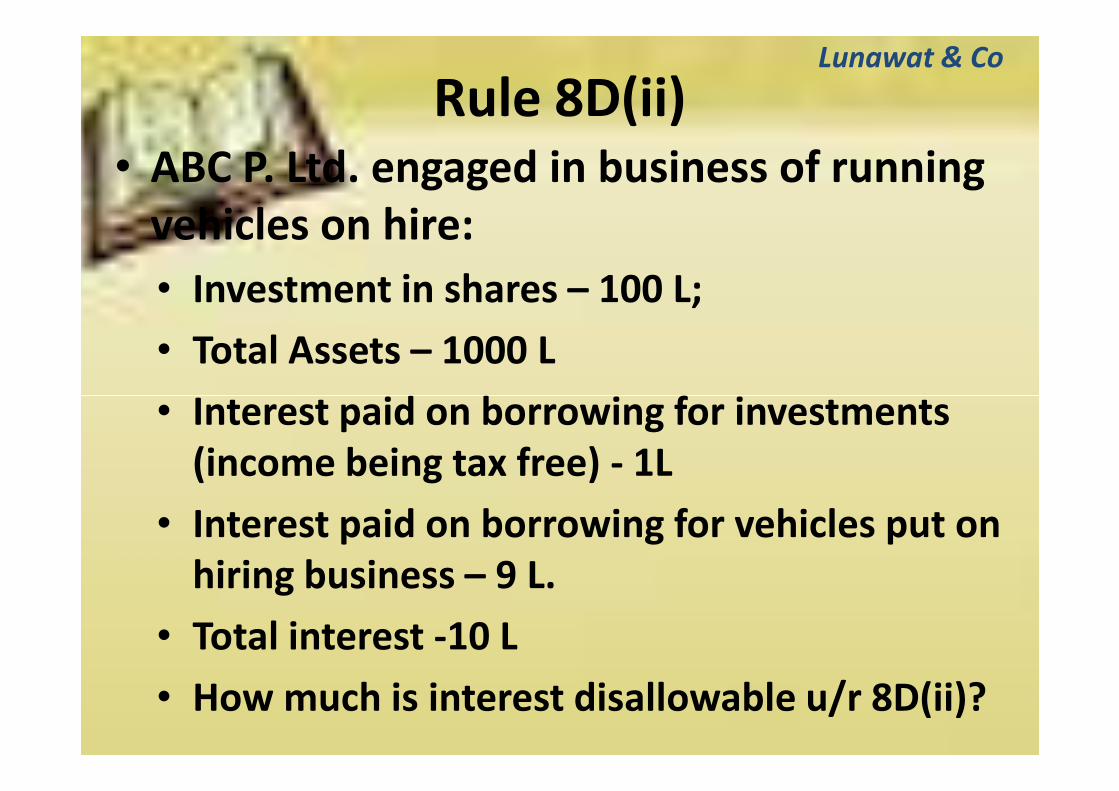

Rule 8D(ii)• ABC P. Ltd. engaged in business of running

vehicles on hire:

• Investment in shares – 100 L;

• Total Assets – 1000 L

• Interest paid on borrowing for investments

Lunawat & Co

• Interest paid on borrowing for investments

(income being tax free) - 1L

• Interest paid on borrowing for vehicles put on

hiring business – 9 L.

• Total interest -10 L

• How much is interest disallowable u/r 8D(ii)?

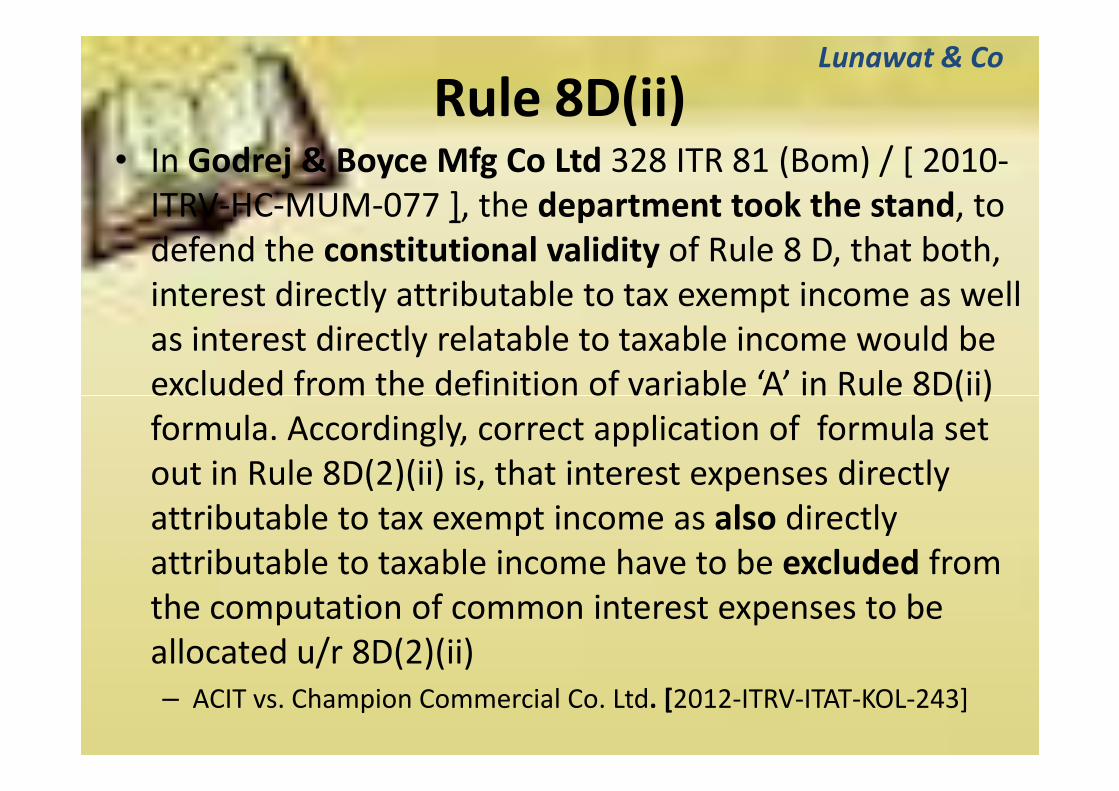

Rule 8D(ii)• In Godrej & Boyce Mfg Co Ltd 328 ITR 81 (Bom) / [ 2010‐

ITRV‐HC‐MUM‐077 ], the department took the stand, to

defend the constitutional validity of Rule 8 D, that both,

interest directly attributable to tax exempt income as well

as interest directly relatable to taxable income would be

excluded from the definition of variable ‘A’ in Rule 8D(ii)

Lunawat & Co

excluded from the definition of variable ‘A’ in Rule 8D(ii)

formula. Accordingly, correct application of formula set

out in Rule 8D(2)(ii) is, that interest expenses directly

attributable to tax exempt income as also directly

attributable to taxable income have to be excluded from

the computation of common interest expenses to be

allocated u/r 8D(2)(ii)

– ACIT vs. Champion Commercial Co. Ltd. [2012‐ITRV‐ITAT‐KOL‐243]

Specific Expenditure

• Can expenditure specifically incurred for taxable

income disallowed??

• JCIT (OSD) vs. Pilani Investment & Industries Corpn.

Lunawat & Co

• JCIT (OSD) vs. Pilani Investment & Industries Corpn.

Ltd. [2013-ITRV-ITAT-KOL-026] – N

• ACIT vs. Best & Crompton Engineering Ltd [2013-ITRV-

ITAT-CHN-100]

• REI Agro Ltd. vs. DCIT [2013-ITRV-ITAT-KOL-088]

No exempt income during year• Rule 8D(2)(ii), ‐numerator B ‐ average value of invest., income from

which does not form or shall not form part of TI as appearing in the

balance-sheet as on first day and in last day of the previous year“.

• It is not total investment at beginning and at end of year, which is to

be considered but it is average of the value of investments which

has given rise to income which does not form part of total income

which is to be considered.

Lunawat & Co

which is to be considered.

• Rule 8D(2)(iii), what is disallowable is an amount equal to ½

percentage of the average value of investment the income from

which does not or shall not form part of the total income

• The disallowance u/s 14A read with rule 8D is to be in relation to

the income which does not form part of total income and this can

be done only by taking into consideration invest. which has given

rise to this income which does not form part of the total income.

• REI Agro Ltd. vs. DCIT [2013‐ITRV‐ITAT‐KOL‐088]

Stock-in-trade• Is s. 14A / R 8D applicable on invest. held as stock in trade??

• Yes

• D. H. Securities P. Ltd. vs. DCIT [2013-ITRV-ITAT-MUM-160]

• Daga Capital 117 ITD 169 (Mum) (SB)

• Esquire Pvt. Ltd. vs. DCIT [2012-ITRV-ITAT-MUM-204]

• JCIT vs. American Express Bank Ltd. [2012-ITRV-ITAT-MUM-174]

Lunawat & Co

• JCIT vs. American Express Bank Ltd. [2012-ITRV-ITAT-MUM-174]

– No

• CCI Ltd 71 DTR (Kar) 141 [2012-ITRV-HC-KAR-075] ,

• Smt. Apporva Patni vs. Addl. CIT [2012- ITRV-ITAT-PUNE-282]

• Ethio Plastic Pvt. Ltd. vs. DCIT [2012-ITRV-ITAT-AHD-283]

• DCIT vs. Gulshan Investment Co. Ltd. [2013-ITRV-ITAT-KOL-032]

• Esquire Pvt. Ltd. vs. DCIT [2012-ITRVITAT-MUM-204]

• Yatish Trading vs. ACIT [2011-ITRV-ITAT-MUM-071]

Stock-in-trade• The argument that all expenditure has been incurred for share

trading business and that there is no additional expenditure

incurred for earning dividend is not acceptable because though

the expenditure is incurred for purpose of the business of share

trading, the said business yields taxable and non-taxable income

• If Rule 8D(2)(ii) which quantifies the interest on investments,

income from which is not taxable, on a proportionate basis, is

Lunawat & Co

income from which is not taxable, on a proportionate basis, is

applied literally, it will lead to absurd results.

• Rule 8D(2)(ii) needs to be scaled down by bifurcating the

expenditure so arrived at between the tax-free and the taxable

incomes. Given that the dominant objective of the share holding

is to earn share trading income, an ad hoc ratio of 20% toward

tax-exempt dividend income will be reasonable.

• DCIT vs. Damani Estates & Finance Pvt. Ltd [2013-ITRV-ITAT-

MUM-106]

Other points

• Can expenditure on acquiring shares out of commercial

expediency disallowed??

• CIT vs. Oriental Structural Engineers P. Ltd.[2013‐

ITRV‐HC‐DEL‐163] – N

• Does S. 14A/ Rule 8D apply to short-term investments?

Lunawat & Co

• Does S. 14A/ Rule 8D apply to short-term investments?

• Sundaram Asset Management Co. Ltd. vs. DCIT [2013‐

ITRV‐ITAT‐CHN‐099] ‐N

• Interest paid 5 L, interest received 2 L. How much to be

considered for Rule 8D?

• ITO vs. Karnavati Petrochmem Pvt. Ltd. [2013‐ITRV‐

ITAT‐AHD‐105] ‐ net

MAT

• Section 115 JB provides for increasing the book profit by the amount of expenditure relatable to any income to which section 10 [other than 10(38)] applies and reducing the book profit by the amount of income to which section 10 [other than sec. 10(38)] applies.

Lunawat & Co

[other than sec. 10(38)] applies.

• Now that the “method” is in place, the rigmarole of determining the amount of expenditure to be added and year of applicability of the “prescribed method” has to be undergone.

Tax Audit

• Para 17(l) of Form 3CD

• Amounts debited to the P & L A/c being ..

Amount of deduction inadmissible in terms of

Lunawat & Co

Amount of deduction inadmissible in terms of

section 14A in respect of the expenditure

incurred in relation to income which does not

form part of the total income

271 (1) (c) Penalty

• By applying the prescribed method under rule 8D, addition by way of disallowance of expenditure under section 14A is made, we have to ascertain whether or not the assessee has furnished inaccurate particulars in the course of assessment proceedings. If the assessee offers an explanation

Lunawat & Co

proceedings. If the assessee offers an explanation which is not found by the AO to be false there is no need to invoke this penal provision.

• No Penalty if no disallowance is made in tax audit report also as there is difference of opinion.

Dy. CIT vs. Nalwa Investments Ltd.

[2011-ITRV-ITAT-DEL-114]

CA. Pramod JainCA. Pramod [email protected]

+91 9811073867

© © 2014 2014 CA. Pramod Jain, Lunawat & CoCA. Pramod Jain, Lunawat & Co

![· Gift]Awards/MemoriaIs Expense Legal Services Food/Beverage Expense Polling Expense Printing Expense Salaries/Wages/Contract Labor Solicitation/Fundraising Expense](https://img.pdfslide.us/doc/110x75/5c5ef74209d3f2515c8cf3a9/-giftawardsmemoriais-expense-legal-services-foodbeverage-expense-polling-expense.jpg)