Embed Size (px)

Citation preview

Expansion of the Panama CanalPotential Impact on Asia – East Coast/Golf TradeExpansion of the Panama CanalPotential Impact on Asia – East Coast/Golf Trade

Rodolfo SabongeVice-President, Market Research and Analysis Office

Panama Canal Authority

Rodolfo SabongeVice-President, Market Research and Analysis Office

Panama Canal Authority

DISCLAIMER. The information, documents, reports, maps and photographs displayed in

this PowerPoint presentation is sole proprietary of the ACP or used with the

authors’ authorization; therefore its modification, reproduction, distribution or

publication for any purpose is prohibited. Its use requires previous authorization of the

ACP.

• Introduction

• World Trade and Canal Traffic

• Update on the Panama Canal Expansion Program

• Potential Changes in Trade Patterns

• Introduction

• World Trade and Canal Traffic

• Update on the Panama Canal Expansion Program

• Potential Changes in Trade Patterns

Gatun Lake

Atlantic Ocean

Pacific Ocean

MirafloresLake

Gatun Locks

Pedro Miguel Locks

Miraflores Locks

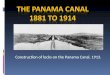

The Panama CanalThe Panama CanalApprox. 50 miles (80 km) long between the Atlantic and Pacific OceansGatun Lake is 85 feet (26 m) above sea levelThe water used to raise and lower vessels in each set of locks comes from Gatun Lake by gravity (approx. 52 million of gallons per transit)Transferred to the Republic of Panama at noon, Dec. 31, 1999.

Approx. 50 miles (80 km) long between the Atlantic and Pacific OceansGatun Lake is 85 feet (26 m) above sea levelThe water used to raise and lower vessels in each set of locks comes from Gatun Lake by gravity (approx. 52 million of gallons per transit)Transferred to the Republic of Panama at noon, Dec. 31, 1999.

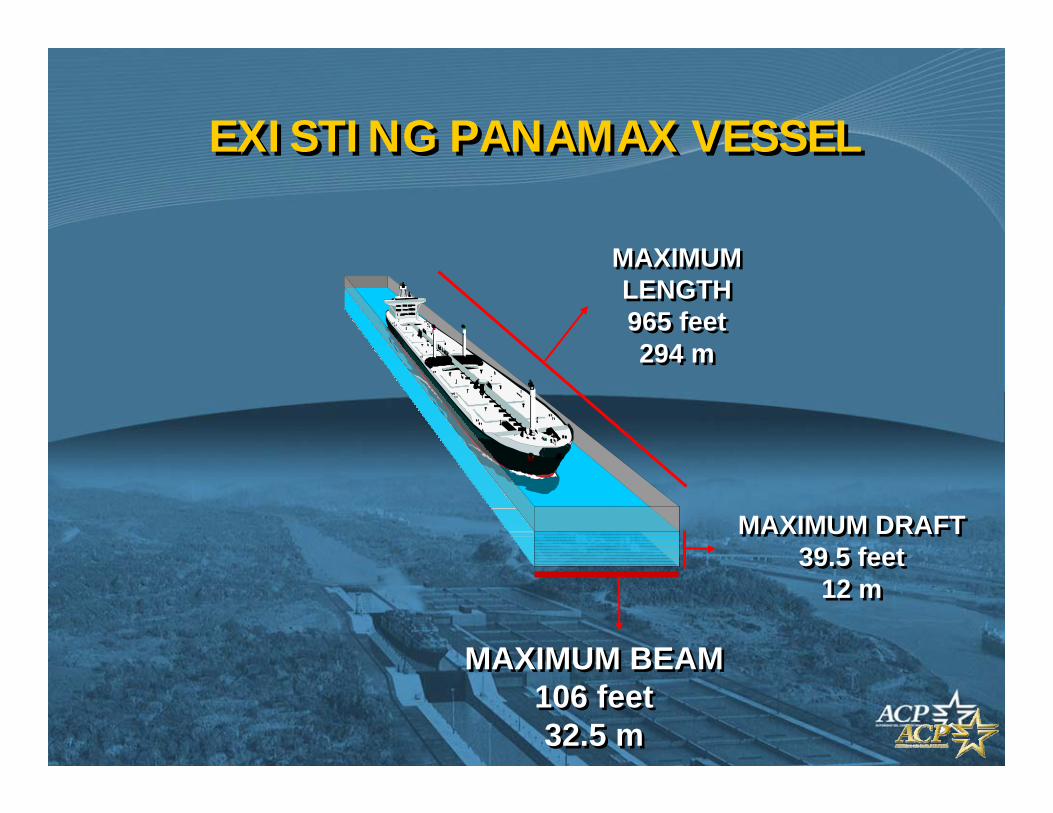

MAXIMUM DRAFT 39.5 feet

12 m

MAXIMUM DRAFT 39.5 feet

12 m

MAXIMUM BEAM 106 feet32.5 m

MAXIMUM BEAM 106 feet32.5 m

MAXIMUM LENGTH 965 feet294 m

MAXIMUM LENGTH 965 feet294 m

EXISTING PANAMAX VESSELEXISTING PANAMAX VESSEL

The Panama Canal in 1914The Panama Canal in 1914 The Panama Canal todayThe Panama Canal today

EVOLUTION OF SUPPLY CHAIN MANAGEMENT AND LOGISTICSEVOLUTION OF SUPPLY CHAIN MANAGEMENT AND LOGISTICS

In the relevant routes (Asia-east coast of the United States) the Panama Canal transported 43.0% of the Panama Canal trade cargo in 2008.

The Panama Canal Trade and Main UsersThe Panama Canal Trade and Main Users

* Measured in Million of Long TonsTotal Cargo Movement FY 2008

64% of Canal cargo traffic originates in or is destined to the United States

714.113.1Peru

817.317.3South Korea

1224.729.2Japan

1226.126.5European Union

1326.722.0Chile

2143.743.7China

64133.7136.8United States

2008 (%)

FY 2008*FY 2007*USERS

• World Trade and Canal Traffic

• Update on the Panama Canal Expansion Program

• Potential Changes in Trade Patterns

• World Trade and Canal Traffic

• Update on the Panama Canal Expansion Program

• Potential Changes in Trade Patterns

Tonnage growth 2006 2007 2008 2009 2010Airborne 7.9% 9.5% -4.6% -18.6% 6.6%Seaborne 5.1% 4.6% 3.4% -3.8% 3.9%Overland/other -1.3% 8.2% 3.0% -6.3% 4.0%

0

10002000

30004000

5000

60007000

80009000

1000020

00

2001

2002

2003

2004

2005

2006

2007

2008

2009

2010

2011

2012

2013

Airborne Seaborne Overland/other

(mill

ions

-m

etric

tons

)

Total World Trade by ModeTotal World Trade by Mode

Source: Global Navigator IHS Global Insight, June 09Source: Global Navigator IHS Global Insight, June 09

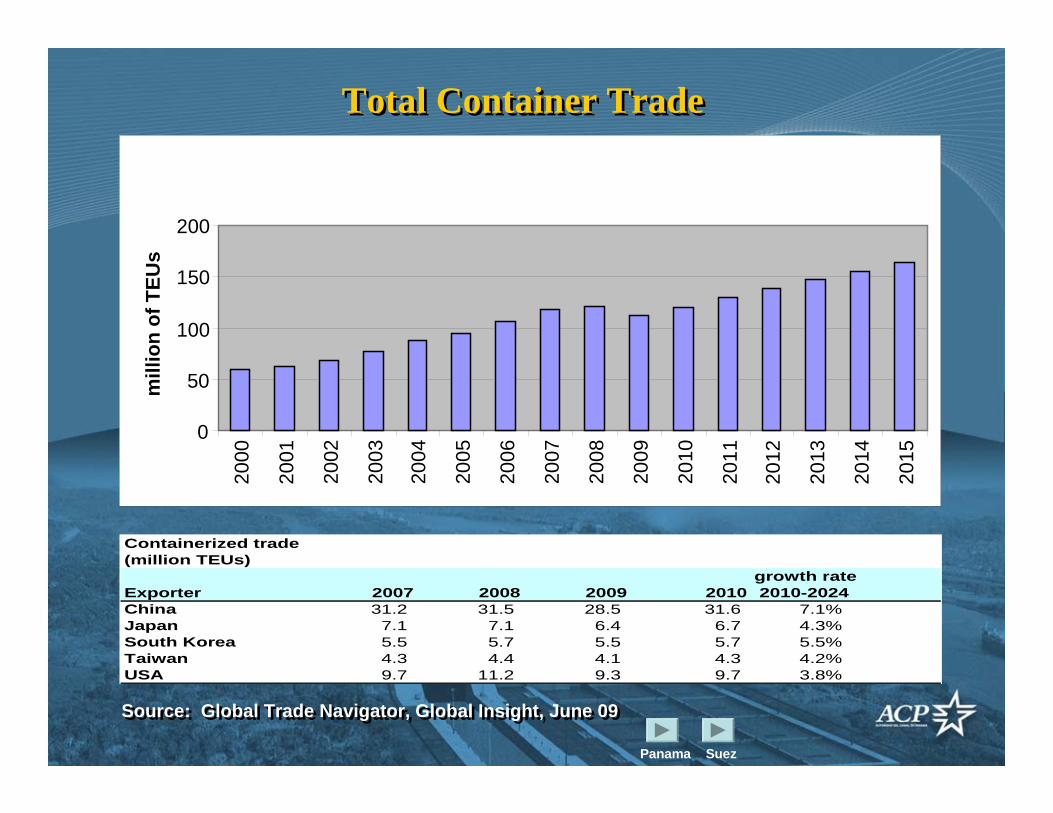

Containerized trade(million TEUs)

growth rateExporter 2007 2008 2009 2010 2010-2024China 31.2 31.5 28.5 31.6 7.1%Japan 7.1 7.1 6.4 6.7 4.3%South Korea 5.5 5.7 5.5 5.7 5.5%Taiwan 4.3 4.4 4.1 4.3 4.2%USA 9.7 11.2 9.3 9.7 3.8%

Total Container TradeTotal Container Trade

0

50

100

150

20020

00

2001

2002

2003

2004

2005

2006

2007

2008

2009

2010

2011

2012

2013

2014

2015

mill

ion

of T

EUs

Source: Global Trade Navigator, Global Insight, June 09Source: Global Trade Navigator, Global Insight, June 09

Panama Suez

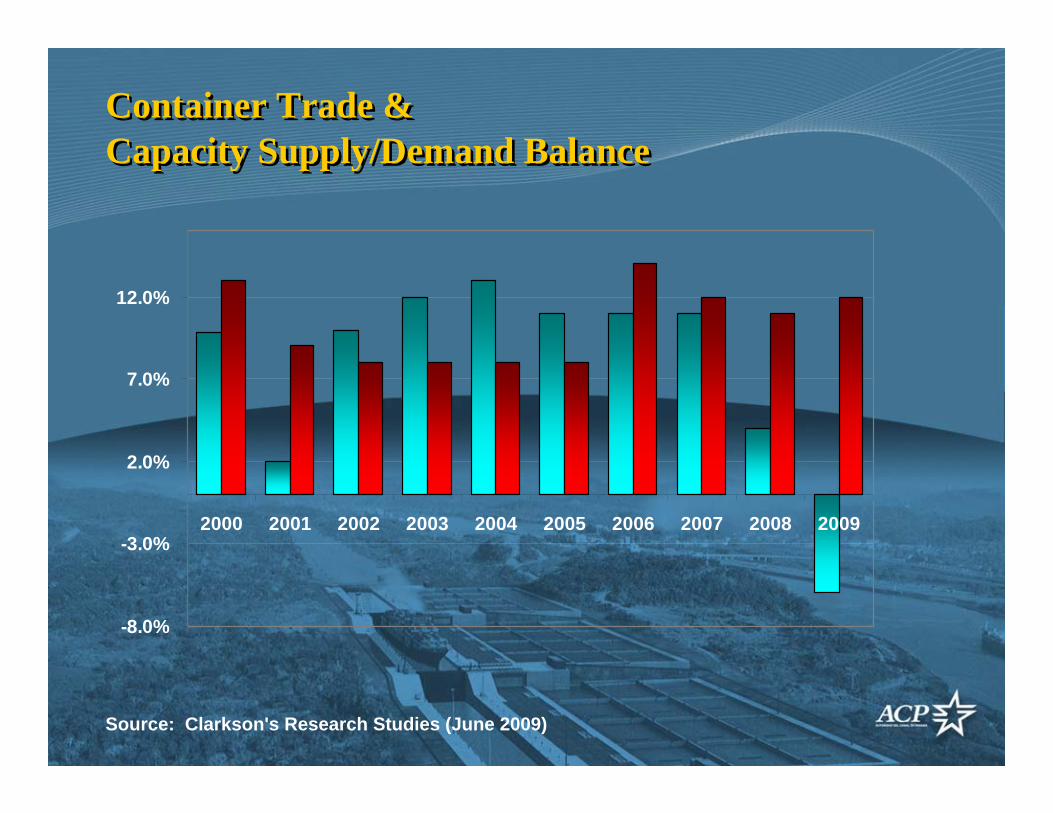

Container Trade & Capacity Supply/Demand BalanceContainer Trade & Capacity Supply/Demand Balance

Source: Clarkson's Research Studies (June 2009)

-8.0%

-3.0%

2.0%

7.0%

12.0%

2000 2001 2002 2003 2004 2005 2006 2007 2008 2009

0

50

100

150

200

250

300

350

400

25+ 20-24 15-19 10-14 5-9 0-4 OrderbookFeeder Handy Sub-Panamax Panamax Post-Panamax

Num

ber o

f Ves

sels

Age of Full Container Fleetby Size and Orderbook

Age of Full Container Fleetby Size and Orderbook

Source: Clarkson’s Reaserch Studies – August 2009

Post-Panamax FleetFull Container VesselsPost-Panamax Fleet

Full Container Vessels

Maersk Line 1/ 727,724 3,700-13,500 94 218,200 4,500-7,450 38 132 945,924Mediterranean Shipping (MSC) 404,308 4,469 - 13,800 47 133,400 12,400-13,800 10 57 537,708CMA-CMG 213,702 5,700 - 11,356 27 331,553 3,600-13,300 37 64 545,255Evergreen 200,478 5,364 - 7,024 33 N/A N/A N/A 33| 200,478Hapag Lloyd Cont. 97,613 7,719 - 8,750 12 122,500 8,750 14 26 220,113China Shipping 143,522 5,618 - 9,580 21 106,368 13,296 8 29 249,890Hanjin Shipping Co. 90,366 5,302 - 6,655 15 92,900 8,580-10,000 10 25 183,266Coscon 165,238 5250 - 10,050 24 108,000 13,500 8 32 273,238Nippon Yusen Kaisha (NYK) 171,348 6,148 - 9,012 24 46,500 9,300 5 29 217,848Mitsui O.S.K. 172,698 4,708 -9,100 26 53,600 6,700 8 34 226,298OOCL 152,467 4,583 -8,063 23 83,852 8,063-8,600 10 33 236,319K"Line" 157,632 5,500 -8,120 25 61,870 4,400-8,120 11 36 219,502Yang Ming 140,144 5,500 -8,236 21 90,700 4,500-8,200 15 36 230,844Hamburg Sud 84,712 5,550 - 5,905 15 37,405 5,905-6,300 6 21 122,117CSAV 32,705 6541 5 58,948 6,316 - 8,000 8 13 91,653Zim Integrated Shpg. 18270 8,200 - 10,070 2 198,420 8,200-12,600 18 20 210,440Otros 1,919,204 3700 -13,800 285 2,016,823 3,600 -14,000 203 488 3,936,027Total 4,892,131 699 3,761,039 409 1,108 8,653,170 Source: Shipping Intelligence Network, September 2009, Clarkson Research Services

Total Post-Panamax

Total TEU Capacity

Total Fleet - 2012

In order Post-Panamax Vessels

Shipping LineExisting

Post-Panamax TEU Range TEU Capacity

Post-Panamax Existing Fleet Full Container Vessels (Sept. 2009)

Orderbook - Post-Panamax Full Container Vessels

TEU Capacity in order TEU Range

4,892,131 3,761,039 8,653,170

• World Trade and Canal Traffic

• Update on the Panama Canal Expansion Program

• Potential Changes in Trade Patterns

• World Trade and Canal Traffic

• Update on the Panama Canal Expansion Program

• Potential Changes in Trade Patterns

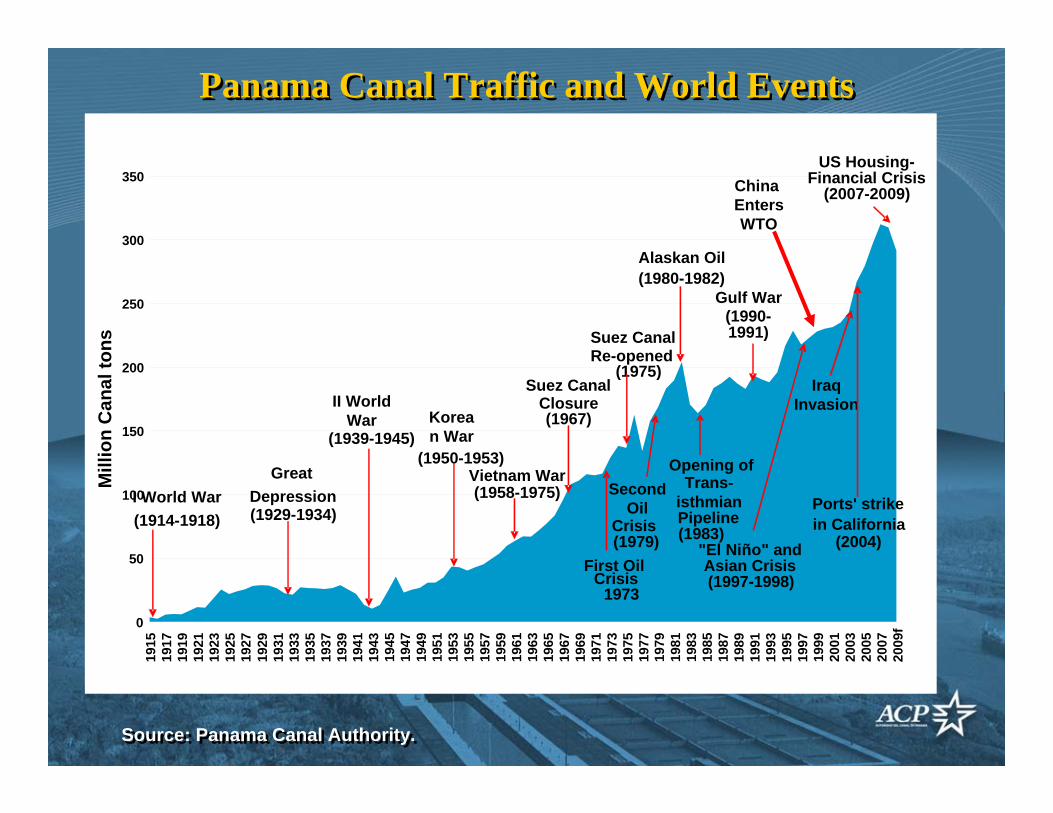

Source: Panama Canal Authority.Source: Panama Canal Authority.

Panama Canal Traffic and World EventsPanama Canal Traffic and World Events

0

50

100

150

200

250

300

350

1915

1917

1919

1921

1923

1925

1927

1929

1931

1933

1935

1937

1939

1941

1943

1945

1947

1949

1951

1953

1955

1957

1959

1961

1963

1965

1967

1969

1971

1973

1975

1977

1979

1981

1983

1985

1987

1989

1991

1993

1995

1997

1999

2001

2003

2005

2007

2009

f

Mill

ion

Can

al to

ns

I World War(1914-1918)

Great Depression(1929-1934)

Korean War

(1950-1953)Vietnam War(1958-1975)

Suez Canal Closure(1967)

"El Niño" and Asian Crisis (1997-1998)

Suez CanalRe-opened

(1975)

First Oil Crisis

1973

Trans-isthmian Pipeline (1983)

Gulf War(1990-1991)

Second Oil

Crisis(1979)

II World War

(1939-1945)

Iraq Invasion

Alaskan Oil(1980-1982)

Ports' strike in California

(2004)

US Housing-Financial Crisis

(2007-2009)

Opening of

China EntersWTO

Total PCUMS Vessel TonnageTotal PCUMS Vessel TonnageFiscal Years 2001-2009Fiscal Years 2001-2009

242.9

267.1

298.0313.2 309.9

231.8235.3

279.5299.1

0.0

50.0

100.0

150.0

200.0

250.0

300.0

350.0

2001 2002 2003 2004 2005 2006 2007 2008 2009

Mill

ion

Tons

Growth of container traffic throughthe Panama Canal (1998 – 2009 Est.)Growth of container traffic through

the Panama Canal (1998 – 2009 Est.)

Based on the capacity of transiting vessels – Source: ComPair Data - April 2009.

00

500500

10001000

15001500

20002000

25002500

30003000

35003500

40004000

FY98 FY99 FY00 FY01 FY02 FY03 FY04 FY05 FY06 FY07 FY08 FY09(Est)

Tran

sits

Tran

sits

00

22

44

66

88

1010

1212

1414

1616

Mill

ion

of T

EUs

Mill

ion

of T

EUs

Transits (1,644 - 3,485)

TEU Capacity (4.1M-12.6M)

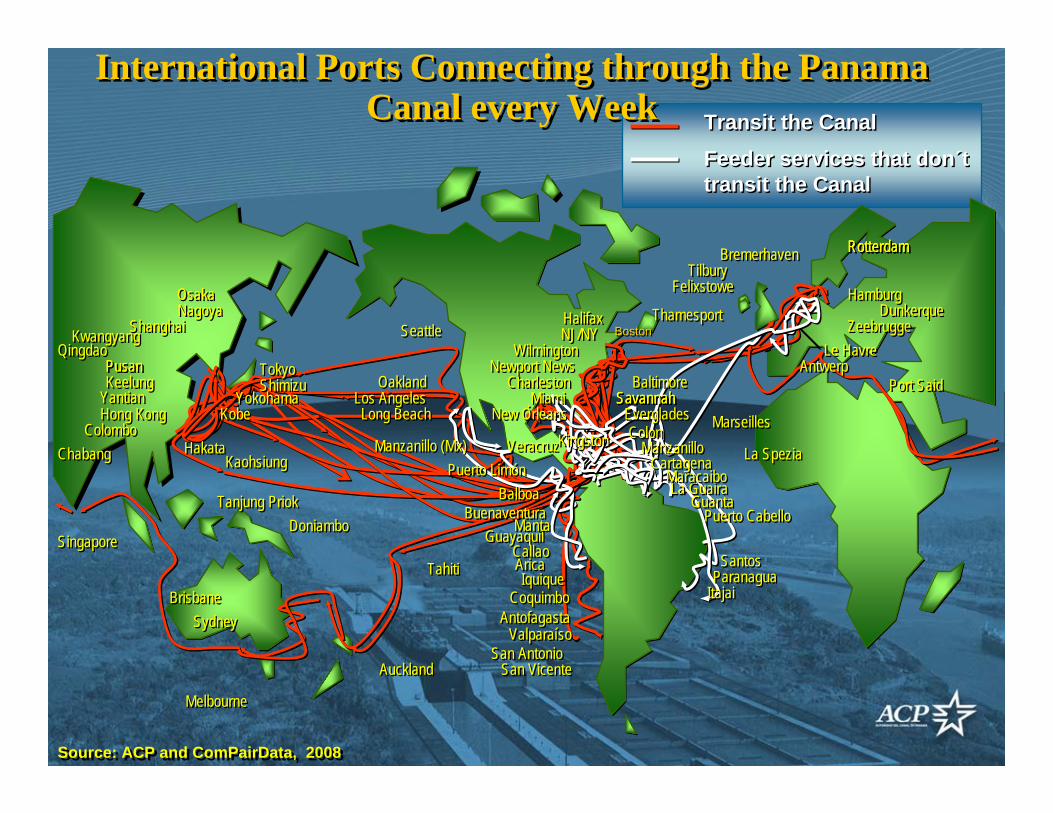

International Ports Connecting through the Panama Canal every Week

International Ports Connecting through the Panama Canal every Week

Source: ACP and ComPairData, 2008Source: ACP and ComPairData, 2008

SavannahSavannahYantianYantian

KwangyangKwangyang

Hong KongHong Kong

PusanPusan

SavannahSavannahKeelungKeelung

WilmingtonWilmingtonPusanPusan

NJ/NYNJ/NY

RotterdamRotterdam

Le HavreLe Havre

HalifaxHalifax

FelixstoweFelixstowe

Long BeachLong BeachLos AngelesLos Angeles

BremerhavenBremerhaven RotterdamRotterdam

KaohsiungKaohsiung

CharlestonCharleston

NagoyaNagoya ThamesportThamesport

OaklandOakland

SeattleSeattle

TokyoTokyo

ColomboColombo

ShanghaiShanghai

YokohamaYokohama

Newport NewsNewport News

HakataHakata Manzanillo (Mx)Manzanillo (Mx)

RotterdamRotterdam

KobeKobe

OsakaOsaka HamburgHamburg

ShimizuShimizu Port SaidPort Said

ZeebruggeZeebrugge

ChabangChabang

TahitiTahiti

AucklandAuckland

DoniamboDoniambo

BrisbaneBrisbaneSydneySydney

MelbourneMelbourne

Tanjung PriokTanjung Priok

SingaporeSingapore

MarseillesMarseilles

La SpeziaLa Spezia

TilburyTilbury

DunkerqueDunkerque

QingdaoQingdao

BuenaventuraBuenaventuraGuayaquilGuayaquil

CallaoCallaoAricaArica

CoquimboCoquimbo

San AntonioSan AntonioSan VicenteSan Vicente

Puerto LimónPuerto Limón

IquiqueIquique

MantaManta

AntofagastaAntofagastaValparaísoValparaíso

..

BalboaBalboa

AntwerpAntwerp

ItajaiItajai

SavannahSavannahBaltimoreBaltimore

New OrleansNew Orleans

ParanaguaParanaguaSantosSantos

Puerto CabelloPuerto Cabello

VeracruzVeracruz ManzanilloManzanilloColon Colon

CartagenaCartagenaLa GuairaLa Guaira

GuantaGuantaMaracaiboMaracaibo

EvergladesEverglades

KingstonKingston

MiamiMiami

Transit the CanalTransit the Canal

Feeder services that don´t transit the CanalFeeder services that don´t transit the Canal

BostonBoston

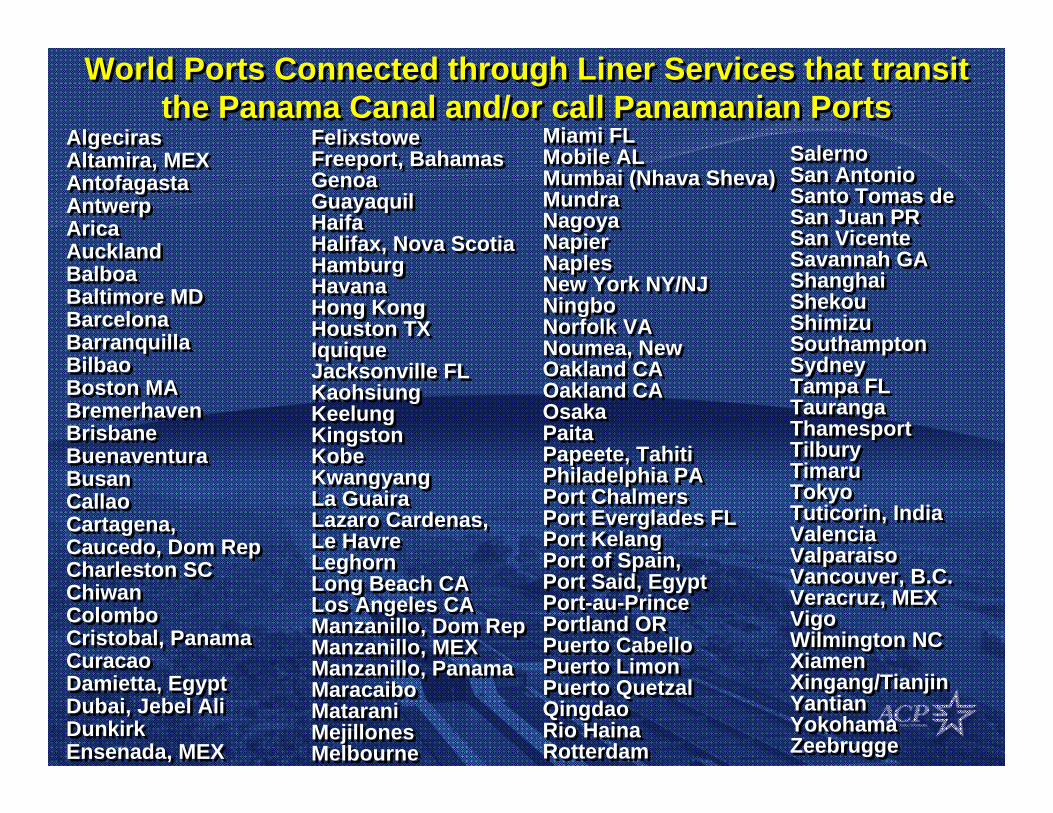

World Ports Connected through Liner Services that transit the Panama Canal and/or call Panamanian Ports

World Ports Connected through Liner Services that transit the Panama Canal and/or call Panamanian Ports

AlgecirasAlgecirasAltamira, MEXAltamira, MEXAntofagastaAntofagastaAntwerpAntwerpAricaAricaAucklandAucklandBalboaBalboaBaltimore MDBaltimore MDBarcelonaBarcelonaBarranquillaBarranquillaBilbaoBilbaoBoston MABoston MABremerhavenBremerhavenBrisbaneBrisbaneBuenaventuraBuenaventuraBusanBusanCallaoCallaoCartagena, Cartagena, Caucedo, Dom RepCaucedo, Dom RepCharleston SCCharleston SCChiwanChiwanColomboColomboCristobal, PanamaCristobal, PanamaCuracaoCuracaoDamietta, EgyptDamietta, EgyptDubai, Jebel AliDubai, Jebel AliDunkirkDunkirkEnsenada, MEXEnsenada, MEX

FelixstoweFelixstoweFreeport, BahamasFreeport, BahamasGenoaGenoaGuayaquilGuayaquilHaifaHaifaHalifax, Nova ScotiaHalifax, Nova ScotiaHamburgHamburgHavanaHavanaHong KongHong KongHouston TXHouston TXIquiqueIquiqueJacksonville FLJacksonville FLKaohsiungKaohsiungKeelungKeelungKingstonKingstonKobeKobeKwangyangKwangyangLa GuairaLa GuairaLazaro Cardenas, Lazaro Cardenas, Le HavreLe HavreLeghornLeghornLong Beach CALong Beach CALos Angeles CALos Angeles CAManzanillo, Dom RepManzanillo, Dom RepManzanillo, MEXManzanillo, MEXManzanillo, PanamaManzanillo, PanamaMaracaiboMaracaiboMataraniMataraniMejillonesMejillonesMelbourneMelbourne

Miami FLMiami FLMobile ALMobile ALMumbai (Nhava Sheva)Mumbai (Nhava Sheva)MundraMundraNagoyaNagoyaNapierNapierNaplesNaplesNew York NY/NJNew York NY/NJNingboNingboNorfolk VANorfolk VANoumea, New Noumea, New Oakland CAOakland CAOakland CAOakland CAOsakaOsakaPaitaPaitaPapeete, TahitiPapeete, TahitiPhiladelphia PAPhiladelphia PAPort ChalmersPort ChalmersPort Everglades FLPort Everglades FLPort KelangPort KelangPort of Spain, Port of Spain, Port Said, EgyptPort Said, EgyptPort-au-PrincePort-au-PrincePortland ORPortland ORPuerto CabelloPuerto CabelloPuerto LimonPuerto LimonPuerto QuetzalPuerto QuetzalQingdaoQingdaoRio HainaRio HainaRotterdamRotterdam

SalernoSalernoSan AntonioSan AntonioSanto Tomas de Santo Tomas de San Juan PRSan Juan PRSan VicenteSan VicenteSavannah GASavannah GAShanghaiShanghaiShekouShekouShimizuShimizuSouthamptonSouthamptonSydneySydneyTampa FLTampa FLTaurangaTaurangaThamesportThamesportTilburyTilburyTimaruTimaruTokyoTokyoTuticorin, IndiaTuticorin, IndiaValenciaValenciaValparaisoValparaisoVancouver, B.C.Vancouver, B.C.Veracruz, MEXVeracruz, MEXVigoVigoWilmington NCWilmington NCXiamenXiamenXingang/TianjinXingang/TianjinYantianYantianYokohamaYokohamaZeebruggeZeebrugge

1996: 235 Thousands TEUs2008: 4.6 Millions TEUs1996: 235 Thousands TEUs2008: 4.6 Millions TEUs

Source: Panama Maritime Authority (AMP).

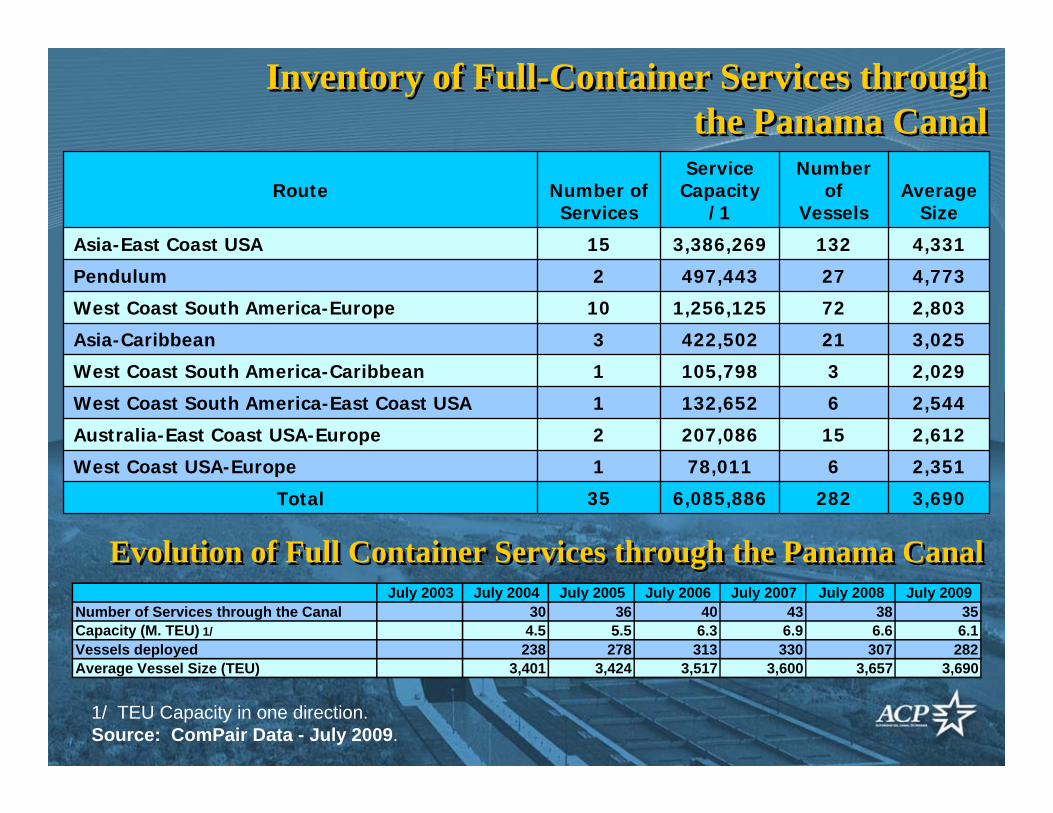

Inventory of Full-Container Services through the Panama Canal

Inventory of Full-Container Services through the Panama Canal

1/ TEU Capacity in one direction.Source: ComPair Data - July 2009.

Evolution of Full Container Services through the Panama CanalEvolution of Full Container Services through the Panama Canal

3,6902826,085,88635Total

2,351678,0111West Coast USA-Europe

2,61215207,0862Australia-East Coast USA-Europe

2,5446132,6521West Coast South America-East Coast USA

2,0293105,7981West Coast South America-Caribbean

3,02521422,5023Asia-Caribbean

2,803721,256,12510West Coast South America-Europe

4,77327497,4432Pendulum

4,3311323,386,26915Asia-East Coast USA

Average Size

Number of

Vessels

Service Capacity

/1Number of Services

Route

July 2003 July 2004 July 2005 July 2006 July 2007 July 2008 July 2009Number of Services through the Canal 30 36 40 43 38 35Capacity (M. TEU) 1/ 4.5 5.5 6.3 6.9 6.6 6.1Vessels deployed 238 278 313 330 307 282Average Vessel Size (TEU) 3,401 3,424 3,517 3,600 3,657 3,690

Source: PIERS, Global Container Report 1Q 2009 Source: PIERS, Global Container Report 1Q 2009

United States PortsImports from Northeast Asia (TEU)

United States PortsImports from Northeast Asia (TEU)

Source: ACP with information of IHS Global Insight, June 2009.Source: ACP with information of IHS Global Insight, June 2009.

2007 Q1 2008 Q1 2009 Q1 % 07-08 % 08-09East Coast 610,427 627,015 525,780 2.7% -16.1%Gulf 40,831 44,744 37,756 9.6% -15.6%West Coast 1,952,482 1,766,833 1,351,785 -9.5% -23.5%

• World Trade and Canal Traffic

• Update on the Panama Canal Expansion Program

• Potential Changes in Trade Patterns

• World Trade and Canal Traffic

• Update on the Panama Canal Expansion Program

• Potential Changes in Trade Patterns

Expansion Program ComponentsExpansion Program Components

Increase the Maximum Operating Level of Gatún Lake

Increase the Maximum Operating Level of Gatún Lake

26.7 m 26.7 m 27.1 m 27.1 m

Deepening & widening of the Gatun lake

navigational channels

Deepening & widening of the Gatun lake

navigational channels

Pacific Post PanamaxLocks

Pacific Post PanamaxLocksPost Panamax Locks Pacific Access Channel

46 M m3

Deepening & widening of the Pacific entrance

Deepening & widening of the Pacific entrance

9.1 M m39.1 M m3

3.7 M m3

4.1 M m3

Deepening of the Culebra Cut navigational channels

Deepening of the Culebra Cut navigational channels

14 M m314 M m3

Deepening & widening of the

Atlantic entrance

Deepening & widening of the

Atlantic entrance

Atlantic Post PanamaxLocks

Atlantic Post PanamaxLocks

The $2.3 billion financing package will cover a portion of the $5.25 billion total cost of the project and will be allocated as follows: The $2.3 billion financing package will cover a portion of the $5.25 billion total cost of the project and will be allocated as follows:

Secured Financing for Program – December 9, 2008Secured Financing for Program – December 9, 2008

FINANCING:FINANCING: European Investment Bank (EIB) European Investment Bank (EIB) $ 500 M$ 500 MJapan Bank for International Cooperation (JBIC)Japan Bank for International Cooperation (JBIC) $ 800 M$ 800 M

Inter‐American Development Bank (IDB)Inter‐American Development Bank (IDB) $ 400 M$ 400 MInternational Finance Corporation (IFC) International Finance Corporation (IFC) $ 300 M$ 300 MCorporación Andina de Fomento (CAF)Corporación Andina de Fomento (CAF) $ 300 M$ 300 M

Subtotal:Subtotal: $2,300 M$2,300 MACP:ACP: $ 2,950 M$ 2,950 M

Total:Total: $ 5,250 M$ 5,250 M

The negotiated financing structure includes favorable provisions for the ACP including a 20-year amortizing period with a 10-year grace period. The negotiated financing structure includes favorable provisions for the ACP including a 20-year amortizing period with a 10-year grace period.

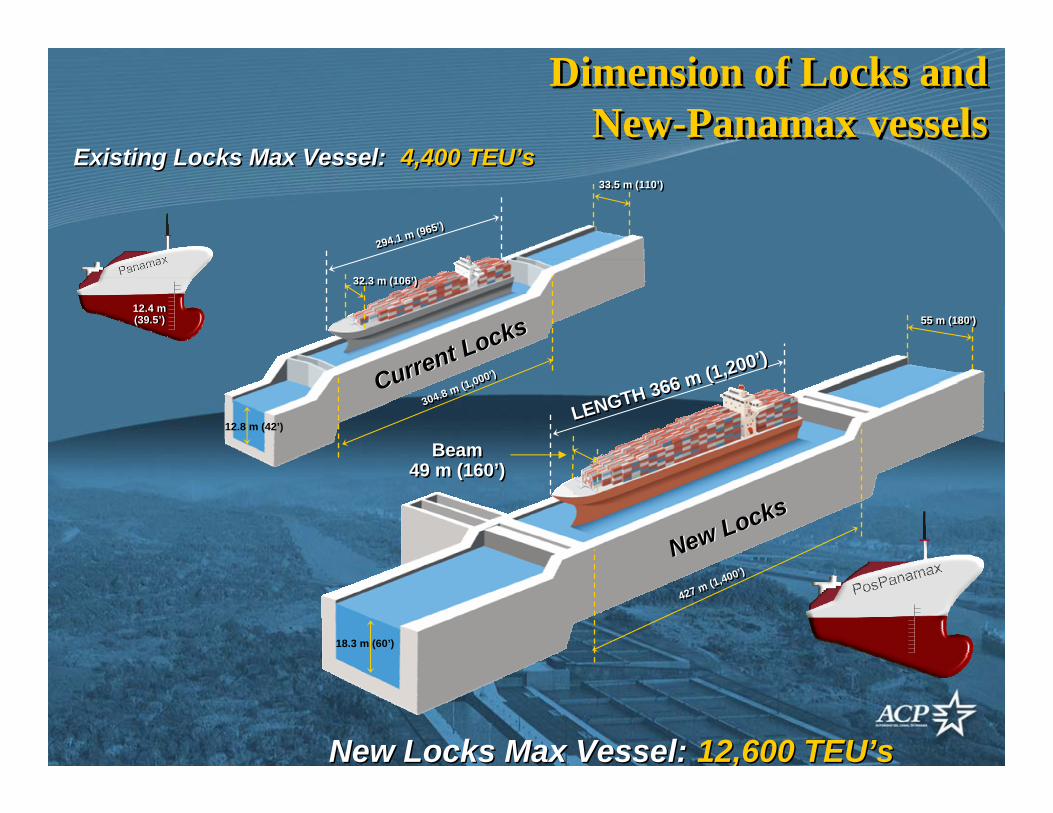

Dimension of Locks andNew-Panamax vessels

Dimension of Locks andNew-Panamax vessels

294.1 m (965’)294.1 m (965’)

33.5 m (110’)33.5 m (110’)

32.3 m (106’)32.3 m (106’)

304.8 m (1,000’)

304.8 m (1,000’)

12.8 m (42’)LENGTH 366 m (1,200’)

LENGTH 366 m (1,200’)

55 m (180’)55 m (180’)

Beam49 m (160’)

Beam49 m (160’)

427 m (1,400’)

427 m (1,400’)

18.3 m (60’)

12.4 m(39.5’)12.4 m(39.5’)

Existing Locks Max Vessel:Existing Locks Max Vessel: 4,400 TEU’s4,400 TEU’s

New Locks Max Vessel:New Locks Max Vessel: 12,600 TEU’s12,600 TEU’s

New LocksNew Locks

Current Locks

Current Locks

Post-Panamax Locks Operation

Post-Panamax Locks Operation

With the water saving basinsthe new locks will use 7% less water than the existing locks

With the water saving basinsthe new locks will use 7% less water than the existing locks

WSB 1 WSB 2 WSB 3

Existing LocksExisting LocksNew LocksNew Locks

Wat

er U

tiliz

atio

nW

ater

Uti

lizat

ion

Pacific Access Channel – Phase 1Pacific Access Channel – Phase 1Progress

Scheduled

97%97%97%

Relocation of 230 KV Transmission Towers and LinesRelocation of 230 KV Transmission Towers and Lines

0% 10% 20% 30% 40% 50% 60% 70% 80% 90% 100%

Progress

Scheduled

100%100%100%100%

89%94%94%Scheduled

ProgressPacific Access Channel – Phase 2Pacific Access Channel – Phase 2

Progress

Scheduled

48%48%

44%44%

Pacific Access Channel – Phase 3Pacific Access Channel – Phase 3

Pacific EntranceDredging and WideningPacific EntranceDredging and Widening

Progress

Scheduled

35%

26%26%

Gatun Lake and Culebra CutDredgingGatun Lake and Culebra CutDredging Progress

Scheduled

23%24%24%

Panama Canal Expansion ProgramPanama Canal Expansion Program

Recently Awarded Projects

Locks Design - BuildLocks Design - Build

0% 10% 20% 30% 40% 50% 60% 70% 80% 90% 100%

Pacific Access Channel – Phase 4Pacific Access Channel – Phase 4

Atlantic EntranceDeepening and WideningAtlantic EntranceDeepening and Widening

Major Contracts Under BidMajor Contracts Under Bid

Progress

Scheduled

1.2%

1.2%

0% 10% 20% 30% 40% 50% 60% 70% 80% 90% 100%

Progress

Scheduled

0.6%

0.6%

Progress

Scheduled

2%

2%

Panama Canal Expansion ProgramPanama Canal Expansion Program

149%

190%

102%

186%

108%

118%

219%

242%

273%

204%

186%

219%181%

133%

126%

146%

161%

151%

50% 100% 150% 200% 250% 300%

CAP1

CAP2

Dragado del Pacífico

CAP3

Esclusas

Dragado del Atlántico

Lowest Price Average Price Highest Price Budget

Prices for Canal Expansion ProgramMajor Projects

Lowest, Average and Highest Prices and Alloted Sums

Prices for Canal Expansion ProgramMajor Projects

Lowest, Average and Highest Prices and Alloted Sums

$177,500,677$258,851,577

$485,453,336Jan De Nul N.V/Van Oord Dredging and Marine Contractors BVBoskalis International BV Dredging Int.

$36,659,852

$46,049,339$74,654,322

Constructora Santa Fe, Ltd. Constructora MECO

$25,489,200$40,986,400

$61,745,339International Undergroup CorpConsorcio M&S MECO SANTA FÉCilsa Minera María

$41,094,000$61,930,269

$89,968,160Jay Cashman, Inc.ASTALDI – GHELLA SPAConstructura Urbana

$3,221,631,384$4,279,819,670

$5,981,020,333BTMGUPC

CANALBudget

Budget

Budget

Budget

Budget

$3,481,000,000

$61,208,966

$48,459,296

$181,096,000

$68,067,623

$89,617,317$162,182,828

$195,943,129Van Ord DredgingJan de Nul

Great Lakes Dredging and Dock Co.Budget $105,821,000

Cilsa Minera María

Atlantic Dredging

Locks

PAC-3

Pacific Dredging

PAC-1

PAC-2

• World Trade and Canal Traffic

• Update on the Panama Canal Expansion Program

• Potential Changes in Trade Patterns

• World Trade and Canal Traffic

• Update on the Panama Canal Expansion Program

• Potential Changes in Trade Patterns

+++ Container Trade Potential Game Changer

+ Dry Bulk Carriers

+ Liquid Bulks

+/- Vehicle Carriers

+/- Refrigerated Vessels

+ Cruise

+/- Others

+++ Container Trade Potential Game Changer

+ Dry Bulk Carriers

+ Liquid Bulks

+/- Vehicle Carriers

+/- Refrigerated Vessels

+ Cruise

+/- Others

Dimension of Locks andNew-Panamax vessels

Dimension of Locks andNew-Panamax vessels

294.1 m (965’)294.1 m (965’)

33.5 m (110’)33.5 m (110’)

32.3 m (106’)32.3 m (106’)

304.8 m (1,000’)

304.8 m (1,000’)

12.8 m (42’)LENGTH 366 m (1,200’)

LENGTH 366 m (1,200’)

55 m (180’)55 m (180’)

Beam49 m (160’)

Beam49 m (160’)

427 m (1,400’)

427 m (1,400’)

18.3 m (60’)

12.4 m(39.5’)12.4 m(39.5’)

Existing Locks Max Vessel:Existing Locks Max Vessel: 4,400 TEU’s4,400 TEU’s

New Locks Max Vessel:New Locks Max Vessel: 12,600 TEU’s12,600 TEU’s

New LocksNew Locks

Current Locks

Current Locks

U.S. Port DepthsU.S. Port Depths

39’39’MiamiMiami38’38’JacksonvilleJacksonville42’42’SavannahSavannah47’47’CharlestonCharleston42’42’WilmingtonWilmington48’48’NorfolkNorfolk40’40’BaltimoreBaltimore38’38’PhiladelphiaPhiladelphia43’43’New York / New JerseyNew York / New Jersey38’38’BostonBoston

MLWMLWU.S. East CoastU.S. East Coast

45’45’New OrleansNew Orleans

40’40’HoustonHoustonMLWMLWU.S. GulfU.S. Gulf

50’50’Seattle / TacomaSeattle / Tacoma

35’35’PortlandPortland

50’50’OaklandOakland

50’50’Los Angeles / Long BeachLos Angeles / Long Beach

MLWMLWU.S. West CoastU.S. West Coast

Depths at Mean Low Water (MLW)Depths at Mean Low Water (MLW)

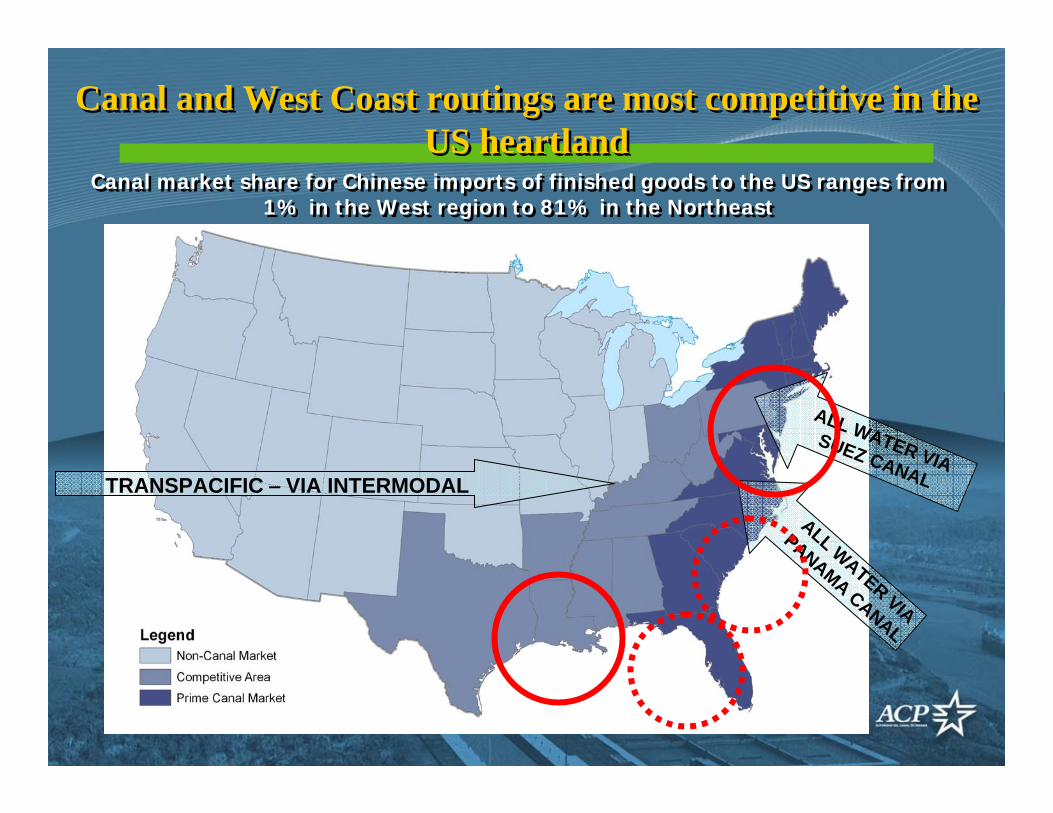

Canal market share for Chinese imports of finished goods to the US ranges from 1% in the West region to 81% in the Northeast

Canal market share for Chinese imports of finished goods to the US ranges from 1% in the West region to 81% in the Northeast

Canal and West Coast routings are most competitive in the US heartland

Canal and West Coast routings are most competitive in the US heartland

TRANSPACIFIC – VIA INTERMODALALL WATER VIA

PANAMA CANAL

ALL WATER VIA SUEZ CANAL

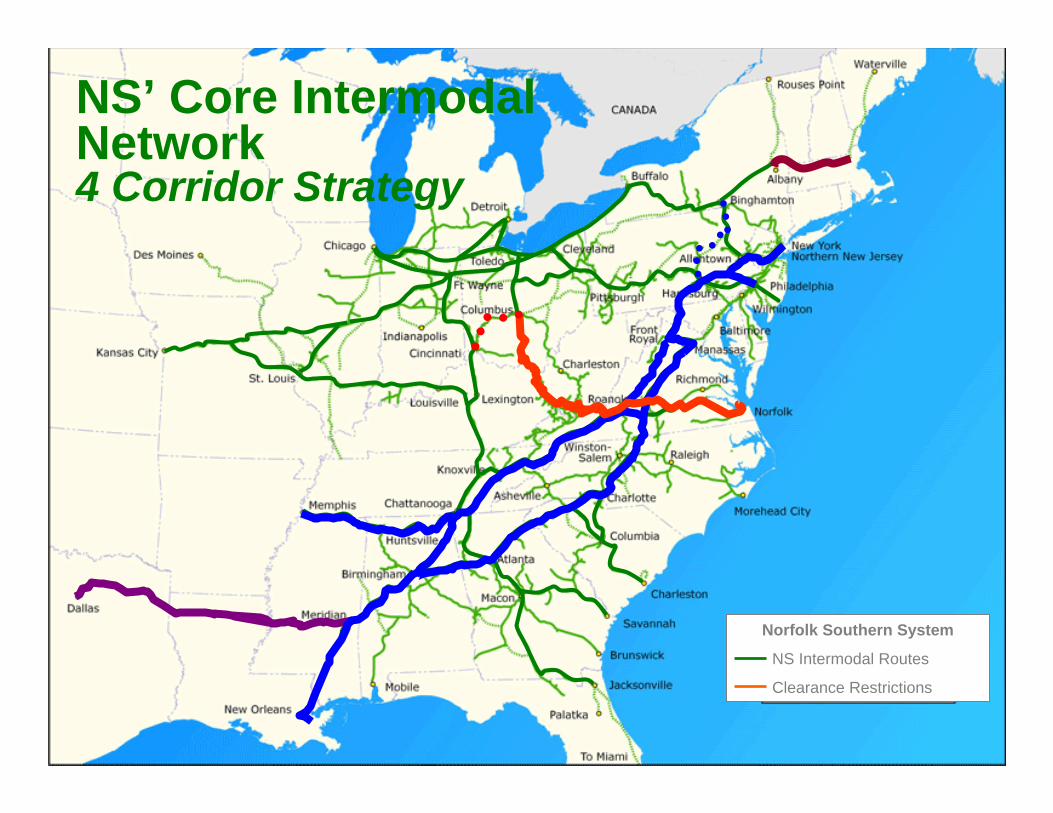

NS’ Intermodal Network

Norfolk Southern System

Intermodal Terminal

Market Expansions thru 2011

New Facilities/Markets

IM Port Terminal

TCS Terminals

NS Is Currently Engaged in Over $3 billion in Network improvements Targeting IntermodalNS Is Currently Engaged in Over $3 billion in Network improvements Targeting Intermodal

• Meridian Speedway: $300mm– Complete 2010

• Heartland Corridor: $250mm– Complete 2010

• Patriot Corridor: $140mm– Complete 2010*

• Crescent Corridor: $2.4bb– Completion tbd

• Meridian Speedway: $300mm– Complete 2010

• Heartland Corridor: $250mm– Complete 2010

• Patriot Corridor: $140mm– Complete 2010*

• Crescent Corridor: $2.4bb– Completion tbd

*Still under review by STB

Norfolk Southern System

NS Intermodal Routes

Clearance Restrictions

NS’ Core Intermodal Network4 Corridor Strategy

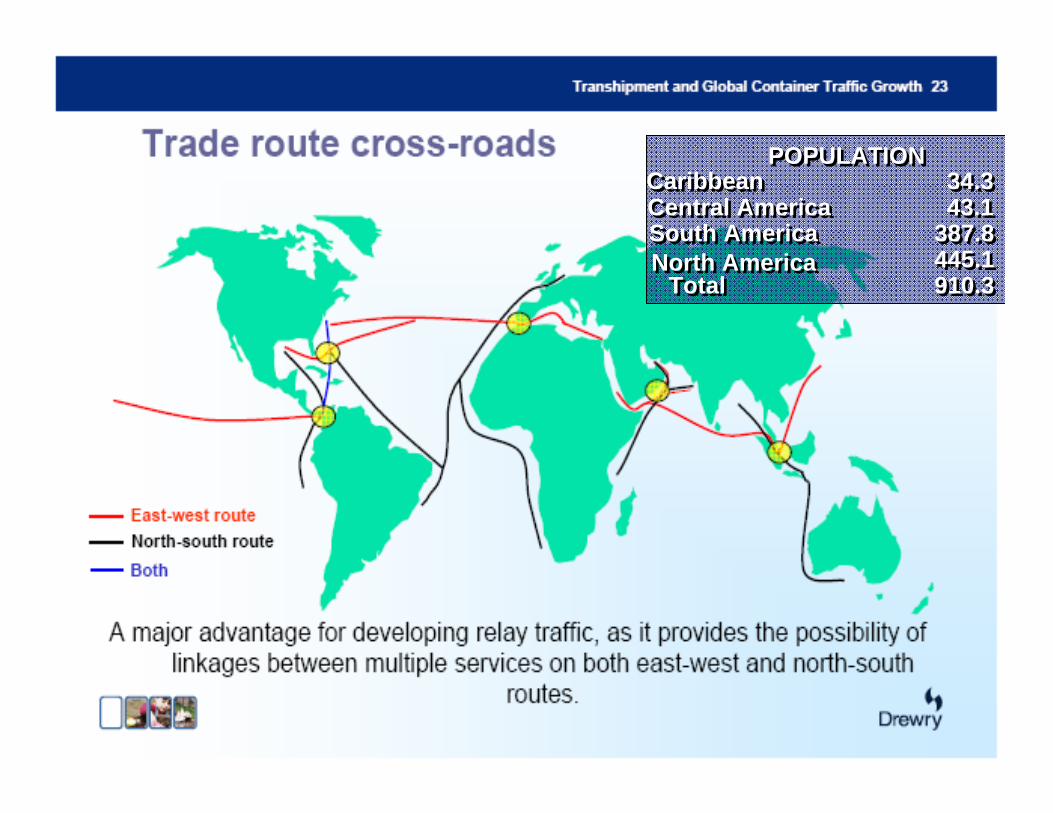

POPULATIONPOPULATIONCaribbeanCaribbeanCentral AmericaCentral AmericaSouth AmericaSouth AmericaNorth AmericaNorth America

TotalTotal

34.334.343.143.1

387.8387.8445.1445.1910.3910.3

EAST-WEST POST-PANAMAX MOVEMENT

CO

NN

ECTI

NG

PO

RTS

CO

NN

ECTI

NG

PO

RTS

MANZANILLOLAZARO CARDENAS

ACAPULCOSALINACRUZ

SAN JOSEPUERTO QUETZAL

ACAJUTLALA LIBERTAD

CORINTOPUERTO SANDINO

PUNTARENASCALDERAGOLFITO

PUERTO ARMUELLESBALBOA

BUENAVENTURATUMACO

ESMERALDASGUAYAQUIL

PAITACALLAO

ANTOFAGASTAVENTANAS

VALPARAISOSAN ANTONIOTALCAHUANO

TAMPICOVERACRUZCOATZACUALCOSBELICE CITYPUERTO CORTESPUERTO CASTILLAPUERTO CABEZASEL BLUFFPUERTO LIMONCHIRIQUI BRANDECRISTOBAL-MIT-EVERGREENCARTAGENABARRANQUILLAPUERTO BOLIVARPUERTO CABELLOLA GUAIRASUAP / PCEMRECIFEVITORIA TUBARAURIO DE JANEIROSEPETIBASANTOSPARANAGUAMONTEVIDEOBUENOS AIRESBAHIA BLANCA

Short Sea Shipping NetworkShort Sea Shipping Network

Forecast2010: 6.6 millions TEUs2015: 8.4 millions TEUs

Forecast2010: 6.6 millions TEUs2015: 8.4 millions TEUs

Source: Panama Maritime Authority (AMP).

PSA Panama International TerminalPSA Panama International Terminal• ½ million TEUs capacity

• USD$ 70 million investment

• 20 yr concession agreement

Dry Bulk Carriers Additional Cargo Capacity in the Expanded Panama Canal

Dry Bulk Carriers Additional Cargo Capacity in the Expanded Panama Canal

Existing Canal

Vessel data:

Cargo carrying Capacity ( tons) 80,238 100,000 -119,000

120,000 –150,000

151,000 –169,000

170,000 –200,000

Utilization rate via the Panama Canal 78% 98% 78% 76% 74%

Cargo (Metric Tons) 62,430 107,310 105,300 121,600 136,900Length (meters) 272.5 260.5 273 289 292Beam (meters) 32.3 43.9 43 43.1 48Salt Water Draft (meters) 14.1 13.8 17.5 17.4 18

Length (meters) 294.1 365.8 365.8 365.8 365.8Beam (meters) 32.3 48.8 48.8 48.8 48.8Tropical Fresh Water Draft (meters) 12 15.3 15.3 15.3 15.3

Utilization rate via the Panama Canal without restrictions 100% 100% 100% 100% 100%

Cargo without restrictions (Metric Tons) 80,238 107,310 132,300 156,800 181,300

Expanded Canal

Typical Panamaxvessel

Maximum size

ConceptSize Range for Dry Bulkers carrying Coal in the expanded canal

Panama Canal Restrictions:

Tankers Additional Cargo Capacity in the Expanded Panama Canal

Tankers Additional Cargo Capacity in the Expanded Panama Canal

Existing CanalTanker Vessel with Maximum

DimensionsVessel Data Aframax Suezmax VLCCTotal Cargo Capacity of vessel 88,170 100 - 119,999 120 - 199,999 > 200,000Utilization percentage of vessel through the Canal 70.0% 94.7% 89.6% 73.9%

Cargo in metric tons 64,257 107,520 146,316 226,205 LOA (m) 272.5 269 267 326Beam (m) 32.2 39.3 46.3 49Fresh water draft (m) 15.5 16.0 17.02 20.64Dimensions allowed by the Panama CanalLOA (m) 294.2 366 366 366Beam (m) 32.2 49 49 49Fresh water draft (m) 12 15.2 15.2 15.2Unrestricted vessel utilization percentage 100% 100% 100% 100%

Cargo carrying capacity with maximum draft of 15.2 m 88,170 101,818 131,107 167,064

Additional cargo allowed with expanded Canal (in MT) 23,913

Expanded CanalSize Range for Tanker Vessels in

Expanded Canal

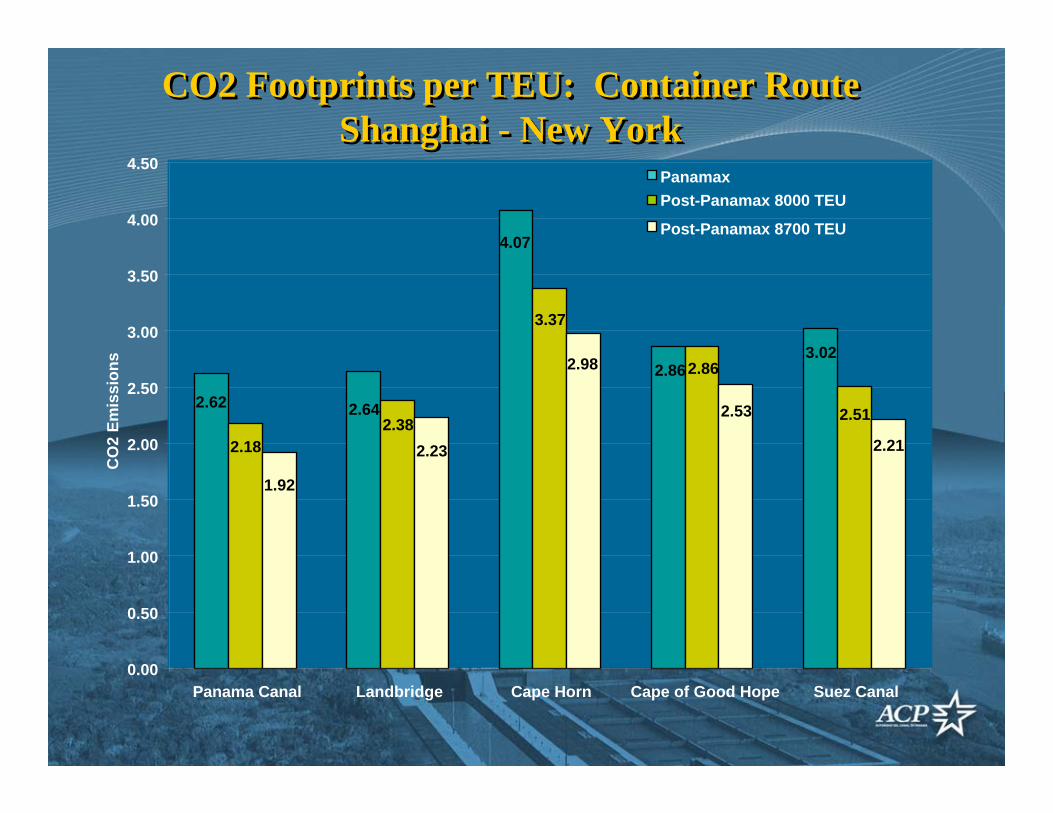

CO2 Footprints per TEU: Container Route Shanghai - New York

CO2 Footprints per TEU: Container Route Shanghai - New York

2.62 2.64

4.07

2.863.02

2.182.38

3.37

2.86

2.51

1.92

2.23

2.98

2.53

2.21

0.00

0.50

1.00

1.50

2.00

2.50

3.00

3.50

4.00

4.50

Panama Canal Landbridge Cape Horn Cape of Good Hope Suez Canal

CO

2 Em

issi

ons

PanamaxPost-Panamax 8000 TEU

Post-Panamax 8700 TEU

SINGAPORESINGAPORE

SHANGHAISHANGHAI BUSANBUSAN

ROTTERDAMROTTERDAM

HAMBURGHAMBURG

DUBAIDUBAI

LA/LBLA/LBNY/NJNY/NJ

SHENZHENSHENZHEN ALGECIRASALGECIRAS

PANAMAPANAMA

Main Logistics Hubs Main Logistics Hubs

SAVANNAHSAVANNAH

KINGSTONKINGSTONFREEPORTFREEPORT

HAMPTON RDS.

HAMPTON RDS.

HOUSTONHOUSTON

CHARLESTONCHARLESTON GENOAGENOA

HONG KONGHONG KONG

SANTOSSANTOS

SAN ANTONIO

SAN ANTONIO

Expansion of the Panama CanalPotential Impact on Asia – East Coast/Golf TradeExpansion of the Panama CanalPotential Impact on Asia – East Coast/Golf Trade

Rodolfo SabongeVice-President, Market Research and Analysis Office

Panama Canal Authority

Rodolfo SabongeVice-President, Market Research and Analysis Office

Panama Canal Authority