Embed Size (px)

Citation preview

The Impact of

Exogenous Shocks on the Egyptian Economy

And Policy Responses

Eman Selim1

January 03, 2008

Draft

Abstract

This paper attempts to estimate the impact of exogenous economic shocks on the

economic performance in the last three decades. The exogenous economic shocks

considered are terms of trade, the change in GDP in industrial countries and the cost

of foreign borrowing. An overview of the development of main macroeconomic

variables in Egypt in the last decades is presented. Two econometric methodologies

are used. First a reduced regression model of one equation for the ratio of current

account to exports of goods and services and then to GDP is estimated for the period

1983-2006. The results of the regression analysis show that exogenous economic

shocks are relatively less important in explaining variations in the ratio of current

account over the period of estimation. Second, unrestricted VAR is used to assess the

impact of exogenous economic shocks on three endogenous variables. The impulse

responses of the variables to one standard deviation and the variance decomposition

show that exogenous shocks are more important in explaining the variations in the

main macroeconomic variables.

Key Words, exogenous shocks, current account, foreign terms of trade, real exchange

rate, 1 Associate Professor of Economics [email protected] [email protected]

Topics in Middle Eastern and African Economies Vol. 10, Sept 2008

1-Introduction

The Egyptian economy has gone through tremendous changes and has been subject to

considerable exogenous economic and political shocks in the last three decades

starting from the mid of the 1970s. However, the Egyptian experience in economic

development is unique. The Egyptian economy has been affected by exogenous

economic shocks that have hit non-oil developing countries since the 1970s in

different ways to reflect the economic transition the Egyptian economy has gone

through and to reflect foreign grants flowed steadily to Egypt and to reflect debt relief

provided to Egypt. In the 1970s, Egypt was considered as non-oil developing country.

By the mid of the 1980s oil production and exports have taken place. However, Egypt

was not classified as one of the big producers of oil. Since the 1970s and throughout

the 1990s, non- developing countries faced unfavorable events that affected stable

growth and weakened their management of economic problems in general and balance

of payments in particular. The most important exogenous economic shocks to non-

developing countries were the considerable fluctuations in the world market prices of

primary commodities with increases in oil prices which were reflected in the

deterioration in the terms of trade; the slowdown in economic activities in the

industrial countries which was caused recession in world trade and decline in export

volume for non-oil developing countries; sharp changes in the cost and the availability

of foreign finance which were expressed in the rise in real interest rates in

international capital markets and the decline in availability of foreign finance even

with high cost resulted from the decline of developing countries credibility.

Developing countries also faced exogenous in the form of sudden decline or sudden

Topics in Middle Eastern and African Economies Vol. 10, Sept 2008

stop of foreign grants. Since these foreign grants are considered as one of the main

sources of foreign exchange especially small developing countries in Africa, these

countries were obliged to reduce their spending or search for costly sources.

The Egyptian economy did not impact with these exogenous shocks in the same way

as other developing countries for number of reasons. First, Egypt has been a

permanent foreign aid receiver in all stages of its development either from Arab

countries until the mid of the 1970s or from western countries before 1967 and after

the mid of the 1970s. Foreign grants provide Egypt an ability to absorb all negative

effects of exogenous shocks. Besides, Egypt is not classified as a net-oil importer at

any phase of its growth. The Egyptian economy has moved from producing oil for

domestic consumption to oil –export by the mid of the 1980s. Moreover, Egypt is not

considered as a primary-commodity importer any more. Egypt was shocked by

crashes of oil prices in 1982 and 1986-1987. The crash of oil prices did not only affect

Egypt s export proceeds but also it affected its revenues from the Suez Canal, tourism

and workers remittances. On the other hand, we can also add that the Egyptian

government applied conservative and rigid exchange rate and monetary policies that

helped to offset negative effects of exogenous shocks.

Finally, being in the middle of a very disturbing area, Egypt has been subject to

various political external shocks. However, political external shocks such as the Gulf

war and the Iraqi war were accompanied with positive economic effects to Egypt.

After the Gulf war, Egypt has been granted by the Paris Club a considerable relief of

its outstanding foreign debts that were a great burden on the Egyptian economy in the

1980s.

Topics in Middle Eastern and African Economies Vol. 10, Sept 2008

After the Iraqi war, Egypt has been compensated through the U.N. food for oil

program. The Egyptian authorities received the monetary compensations in dollars

and paid them to workers in installments with Egyptian pounds.

The rest of the paper is arranged as follows. Section II presents some studies on

exogenous shocks to developing countries. Section III briefly describes the

development of current account, real GDP and fiscal deficit in Egypt and the main

variables suggested by the literature as the factors determining current account

behavior in developing countries. Section IV examines the impact of different

variables on the current account with a sample of time series data over the period

1983-2006. The data were first applied on a regression model and then with a vector-

auto regression method. Section V briefly summarizes the results.

II-Literature Review

Literature of the impact of exogenous shocks on the economic performance of

developing countries concentrates on studying the impact of external variables such as

terms of trade, real GNP of industrial countries and real interest rates in international

capital markets on major macroeconomic variables as real exchange rate and current

account to exports ratio.

Macroeconomic fluctuations in developing countries have been presented by Agenor,

Mcdermott and Prasad (2000). They show that real fluctuations in developing

countries is caused by external shocks in developed countries business cycles and by

changes in foreign real interest rate.

Hoffmaister and Roldos (1997) use panel data. They find that domestic aggregate

supply shocks are the most important sources of output fluctuations in the Asian and

Latin American countries.

Topics in Middle Eastern and African Economies Vol. 10, Sept 2008

Fackler and Rogers (1995), Reinhart (1995), Edwards and Vegh 9 (1997) and Montiel

(1997) have used empirical studies to distinguish between external and domestic

shocks for developing.

Ahmed (1999) studies the sources of economic fluctuations and their implications for

exchange rate regime in key Latin American countries. He used a six variable vector

auto regression (VAR) model and annual data from Argentina, Brazil, Chile,

Colombia, and Mexico over the period 183- 1999. Terms of trade, foreign output and

U.S. real interest rat are considered as the external variables and are affected by

external factors. Real exchange rate, output and the price level are affected by both

the domestic factors and the external variables. He finds that external shocks has

small role in causing real GDP fluctuations in these countries.

Ahmed, Ara, Hyder 2006 examine the sources of economic fluctuations in Pakistan

They use a structural vector auto-regression ( VAR) model to show that external

shocks are the most important source of economic fluctuations in Pakistan.

Khan and Knight (1983) examined the impact of both internal shocks and external

shocks on the current account balances of 32 non-oil developing countries during the

1970s. They considered that the fiscal deficit, and the appreciation of real effective

exchange as the internal shocks. External shocks are the deterioration in terms of

trade, the slow down of economic growth in developed countries and the increase in

foreign real interest rates. They used regression analysis for across- section time-

series sample of 32 non-oil developing countries from 1973- 1980. They find that the

two types of shocks are important in affecting the current account balances of the

countries.

Dorooian (1983) examined the impact of terms of trade, growth differential, real

foreign interest rate, real effective exchange rate, fiscal position ratio, and ratio of

Topics in Middle Eastern and African Economies Vol. 10, Sept 2008

total reserves to nominal value of imports on the current account in analytical groups

of non-oil countries. The analytical groups are the net oil exporter, major exporters of

manufactures, low-income countries and other net oil importers. He used annual data

from 1973 to 1980 to each group.

Balassa (1986) researched on the policy responses of developing countries to external

shocks in two periods; 1973- 78 and 1978- 83. Balassa (1986) classified developing

countries as outward and inward countries depending on their incentive policy toward

exports and imports. Developing countries that provide more support to import

substitution are classified as inward countries. Developing countries that provide

similar incentives to exports and to imports are classified as outward countries. Both

groups of developing countries include newly industrialized countries and less

developed countries. Egypt was classified as a less developed countries pursued

inward – oriented policies.

External shocks in the first period are terms of trade affected by the increases in oil

prices, and the effects of changes in export volume as a result of the slowdown of

world trade and recession in developed countries. In the second period external shocks

include interest rate increase in world financial markets.

Balassa (1986) showed that policy responses to external shocks took the form of

additional external net borrowing, increasing export market shares, import substitution

by decreasing the income elasticity of import demand and deflationary

macroeconomic policies which led to the decline in the growth of demand for imports.

Balassa 1986 found that outward- oriented countries suffered greater terms of trade

losses than inward- oriented countries during both periods of external shocks.

Inward- oriented countries s policy response in the first period took entirely the form

of additional net external financing. In the second period, inward- oriented countries

Topics in Middle Eastern and African Economies Vol. 10, Sept 2008

depended less on additional net external financing because they faced their

accumulated foreign indebtedness and high debit – service ratios. Outward – oriented

countries initially applied deflationary policies and later on they applied export

promotion and import substitution policies which led to increase in economic growth.

J.Fry and M.Lilian ( 1986 ) have considered monetary policy response to external oil-

price shocks of 1973-74 and 1979-80 of oil-importing countries.

They tested the medium and long – run effects of discretionary monetary policy by

using pooled time series data across 55 developed and developing countries.

They find that the more monetary policy is used to contain the effects of external oil

price shocks the less effective it becomes.

Tanzi (1986) has discussed the factors associated with external shocks to developing

countries, the effects of these shocks on fiscal variables and the policy response to

shocks.

According to Tanzi, the exogenous shocks to developing countries include changes in

the export earnings, changes in major import prices, changes in the cost of foreign

borrowing, changes in the availability of foreign credit, changes in the level of foreign

grants, changes in foreign workers remittances, changes in direct foreign in the level

of capital outflows by nationals.

Tanzi 1986 argued that exogenous shocks to developing countries can directly and

automatically affect fiscal variables which require policy response.

He also argued that for developing countries it is very important to distinguish the

changes in fiscal variables that reflect genuine policy responses from that reflect

automatic effects.

Tanzi 1986 argued that developing countries have limited control over its fiscal policy

and may not be able to use it to face external shocks because there is a strong link

Topics in Middle Eastern and African Economies Vol. 10, Sept 2008

between the budget and the foreign sector from the revenue side and the expenditure

side.

Some other literature concentrates only on the shocks of endogenous variables

especially supply shocks.2

III. An Overview of the Egyptian Economy

The Egyptian economy has gone through different structural changes since 1952. In

1956, the government nationalized the Suez canal company and paid huge

compensations to foreigners. In 1962, the government introduced the social laws

which provided state ownership and control on all revenues generated from different

economic sectors. The state controlled the agriculture sector, especially the

distribution of cotton; the main agriculture product. The state owned and operated the

banking sector. Private enterprises were nationalized and managed by the state. The

import-substitution industrialization model was adopted. The government provided

subsidies to basic needs goods including food, utilities, electricity and water.

In 1973, Egypt started a new economic system which was called Infitah or open door

policy. The intention was to open the door for foreign investment and to encourage

the private sector to undertake a prominent role in economic development.

The Egyptian economy witnessed huge foreign capital inflows between 1974 and

19853 due to number of factors; the rise in oil price which had a positive impact on

Egypt because of the increase in oil production, the reopening of Suez Canal, the

surge in workers remittances and the inflow of foreign aid. However, the massive

expansion in the public budget caused the persistency of fiscal deficits. The open door

2 See Ball,L. and Mankiw.G. 1995.Gordon,R. 1984. 3 Alssia, 2007

Topics in Middle Eastern and African Economies Vol. 10, Sept 2008

policy took the form of liberalizing the import sector enhanced with the overvaluation

of the exchange rate. Before4 May 11, 1987 the Central Bank managed the proceeds

and disbursements of foreign exchange in Egypt. The Central Bank pool received the

receipts of foreign exchange from the exports of petroleum, cotton and rice; Suez

Canal dues and Sumed pipeline royalties. The commercial banks pool which received

foreign exchange from workers remittances, tourism, and exports not included in the

Central Bank pool. And provided them for public sector need not included in the

central bank pool. A parallel and unofficial foreign exchange market was established

outside the banks market. The exchange rate in the market reflected the supply,

demand and risk premium conditions. The main sources of this market were workers”

remittances and tourism and provided foreign exchange for the private sector.

The 1980s were characterized with heavy external debts burden, high rate of inflation

exceeding 20 percent, chronic current account deficit and huge government fiscal

deficit. On May 11, 1987 a new bank foreign exchange market was established. The

commercial banks and two travel agents were permitted to undertake foreign

exchange transactions. Egypt began an economic reform program in the 1990s

including the ten reforms in Washington consensus and IMF prescription. Egypt

started two reform programs under the supervision of international organizations. The

Egyptian government signed an economic stabilization program with the International

Monetary Fund in May 1991 and a structural adjustment program with the World

Bank in November 1991. The reform programs succeeded to help Egypt to achieve

some financial and fiscal improvements. Inflation rate declined from almost 20

percent to one digit percent, interest rates on Egyptian Pound were liberalized, and

budget deficit was declined. On February 27, 1991, foreign exchange transactions

4 International financial statistics, Country Notes 2007.

Topics in Middle Eastern and African Economies Vol. 10, Sept 2008

were carried out through two markets; the primary market and the free market. On

October 8, 1991 the primary market was eliminated and the exchange rates were

unified, devalued and begged to the dollar. Egypt enjoyed a period of capital inflows

which were sterilized to avoid their inflationary effect. However, the program stopped

three years after the mid of the 1990s. The Asian financial crisis 1997 and its

extension to some Latin American Countries and to Russia in 1998 and 1999 formed

unfavorable external economic conditions for the Egyptian economy. Egypt witnessed

massive foreign capital outflows.

As the assumed success of the economic reform did not reach the average person in

Egypt, the period 1998- 2004 witnessed a slowdown in economic reform measures.

The period was characterized with directing the attention to institutional and legal

reforms to provide a solid basis for economic reform5. It also witnessed the focus on

signing trade agreements with Arab Countries, Asian Countries, European Countries

and the United States. The foreign exchange market was subject to disturbances and

instability since the end of 1999 but the Government intervention maintained the fixed

exchange rate. By 2001, the authorities allowed limited depreciation in the exchange

rate. The unofficial market in foreign exchange and the official multiple rates

reemerged in 2001 and 2002. In 2003, the exchange rate was depreciated to fluctuate

between 6-7 pounds for one American dollar afterwards, with the stagnation of the

economy and the deterioration in the per capita income, exchange rate stabilized

around 5.7 and 5.5 pounds per American Dollar. Egyptian cabinet began a new reform

program in 2004. The new reform program puts great emphasis on tariff and tax

reductions, applying new procedures for national budget to avoid off budget

5 Such as the real estate Mortgage Law, Export Laws, intellectual Property Rights Law, Special Economic Zones Laws,

Topics in Middle Eastern and African Economies Vol. 10, Sept 2008

expenditures. Privatization of public enterprises was revived. New economic

legislations were implemented.

Egypt has been a recipient of foreign aid since the 1960s and since the mid of the

1970s. The donors- countries are the United States, Western Europe, Japan and the

Gulf countries. 6

The US has provided Egypt with $1.3 billion a year on military aid since 1979 and

$815 million a year in economic assistance. The USAID program gives $ 200 million

cash to the Egyptian government. This money is supposed to solve problems related

to deregulations, privatization and free trade.

U.S continues with large assistance program for Egypt .U.S. provides finance for

many programs. After the 2003 Iraq war, a portion of U.S. government assistances

took the form of bond guarantees conditioned on Egyptian compliance with series of

economic reforms. Upon fulfilling these conditions, U.S. government provides Egypt

with bond guarantees which enabled the Egyptian government to issue $ 1.5 billion

10-year bonds in September 2005. U.S. agrees to import products from Egypt without

tariffs if they have been produced in a qualified industries Zones and 11.7% of the

inputs of these products originate from Israel.

It has been argued that foreign aid has not helped Egypt to achieve the

characterization of newly industrialized countries. It has also been argued that foreign

aid helped Egypt to avoid real economic reform.7

6 Mustafa Kamal Al-Sayed, 2001 7 www.csmonitor.com

Topics in Middle Eastern and African Economies Vol. 10, Sept 2008

Foreign Aid to Egypt8

(Millions of Dollars)

Year Economic Military

Military Education and

Training (IMET)

Total

As a percentage of GDP

%

1948-1997 23,288.6 22,353.5 27.3 45,669.4 .------

1998 815.0 1,300.0 1.0 2,116.0 2.4891999 775.0 1,300.0 1.0 2,076.0 2.2412000 727.3 1,300.0 1.0 2,028.3 2.1462001 695.0 1,300.0 1.0 1,996.0 2.4982002 655.0 1,300.0 1.0 1,956.0 2.3232003 911.0 1,300.0 1.2 2,212.2 3.2312004 571.6 1,292.3 1.4 1865.3 2.2442005 530.7 1,289.6 1.2 1,821.5 1.9272006 495.0 1,300.0 1.2 1,796.2 1.657Total 29,464.2 34,035.4 37.3 63,536.9 -----

Source: Jewish Virtual Library 2007

Real GDP growth averaged around 3.8 in the 1990s and jumped to 6.1 by 1999. Real

GDP growth fluctuated during the following years until it rises to 6.8 in 2006.(table 1)

. Egypt fiscal position is improving with deficits improving.

Inflation reached 12.3 percent in the period 1989-1998. The inflation rate declined

afterwards and reached its lowest level in 2000 and 2001. However, inflation rate

witnessed another rise in 2004 and 2005 when it reached 8.8 percent. The inflation

showed a second decline in 2006.

8 www.jewishvirtuallibrary.org

Topics in Middle Eastern and African Economies Vol. 10, Sept 2008

Current account as a percentage of GDP improved from -1.9 percent to 4.3 in 2004 to

witness another decline in 2005 and 2006 when it reaches a very positive ratio 0.8.

Table 3

Macroeconomic Indicators for Egypt

Annual percent Change

Average

1989-98

1999 2000 2001 2002 2003 2004 2005 2006

Real GDP Growth 3.7 6.1 5.4 3.5 3.2 3.2 4.1 4.5 6.8

Inflation

Current account

% GDP

Consumer

prices

12.3

12.3

3.7

-1.9 3.7

2.8

-1.2 2.8

2.4

- 2.4

2.4

0.7 2.4

3.2

2.4 3.2

8.1

4.3 8.1

8.8 4.2

3.2 0.8

8.8 4.2

World Economic Outlook 2007

Debt to GNP was higher than 100 percent by the end of the 1980s and debt service

was higher than 30 percent of exports.9 Due to implementation of serious reform

program in the 1990s and debt relief provided to Egypt by Paris Club, Debt indicators

improved. Debt to GNP ratio declined to 39 percent in 1997 and debt service to

exports ratio declined to 8.9 percent.

9 Agenor,Diwan and Kibbi,2000.

Topics in Middle Eastern and African Economies Vol. 10, Sept 2008

Figure 1:The current Account to GDP Ratio

-2

0

2

4

6

8

10

75 80 85 90 95 00 05

CURRENTTACCEGPY The Consumer Price Index

0

50

100

150

200

75 80 85 90 95 00 05

CPI1995

80

120

160

200

240

75 80 85 90 95 00 05

INDIXTERMSDEVE Fiscal Position to GDP Ratio

-0.30

-0.25

-0.20

-0.15

-0.10

-0.05

0.00

0.05

75 80 85 90 95 00 05

GOVDY1

Topics in Middle Eastern and African Economies Vol. 10, Sept 2008

IV. Data and Methods Exogenous economic shocks are presented by changes in terms of trade, industrial

countries GDP and foreign interest rate. Economic performance is presented by

changes in major macroeconomic variables; current account, real GDP growth, the

inflation rate, the fiscal position and total reserves minus goods as a percentage of

imports of goods and services.

Data The data for terms of trade are not available for Egypt. The terms of trade are

presented by the percent of change in terms of trade for non-oil developing countries,

terms of trade index for developing countries and the ratio of the international price of

long cotton to the price of wheat. Foreign output is the annual change of GDP for

industrial countries. Real foreign interest rate is percent change in real U.S. deposit

rate. Real exchange rate for Egypt is the market exchange rate deflated by the

consumer price index. Domestic output is real GDP and is measured as the market

value of GDP deflated by the consumer price index. Non-gold official reserves as a

ratio of imports of goods and services are also measured.

The inflation rate is the natural logarithm of CPI. The fiscal position is the ratio of

fiscal deficit/surplus to GDP.

The sources of the data are International financial Statistics different issues, World

Economic Outlook and Balance of Payments Statistics, different issues, IMF.

The Augmented Dickey-Fuller Unit Root Test

To assess the stationary of the time series data, the Augmented Dicky-Fuller unit root

test is used. The first difference of the time series data are regressed against the one

year lag of the series, the lagged difference terms and a constant and a time trend.

Δ Xt = ß1 Xt-1 + ß2 ΔXt-1 + ß3 ΔXt-2 + ß4 + ß5t

If the coefficient of Xt-1 is significantly different than zero, then the hypothesis that X

contains a unit root is rejected and the stationary is accepted.

Since all the variables used in the estimation are either log-levels or percentage

changes, they are found to be stationary series.10

10 The results are provided in the appendix.

Topics in Middle Eastern and African Economies Vol. 10, Sept 2008

A Simple Reduced Form Model

First, a simple regression model is used where the current account ratio to GDP or to

exports of goods and services is measured to estimate the relative importance of

exogenous shocks as explanatory factors to current account development for the

period 1983-2006. Different versions of the current account model have been used.

The dependent variable in all these versions is the current account balance scaled by

exports of goods and services and then by GDP. This simple model depends on the

work of S.Khan and D.Knight (1983) and the extension of their model by Doroodian

(1985). The model can be considered as unrestricted reduced model and is derived

from a structural model of the components of current account which are the imports of

goods and services and the exports of goods and services11. Khan and Knight (1983).

The model is :

CA/X = f( TOT, DIFYY , RER, FIR, FB/Y, RES/M) (1)

Where

CA = current account balance

X = nominal exports of goods and services

TOT = terms of trade for non-oil developing countries taken first as rate of

change then the index is used.

DIFYY = difference between the rate of change of GDP in industrial and that of

Egypt.

RER = real exchange rate of Egypt where the consumer price index is used to

deflate the market exchange rate.

IR = the deposit interest rate of USA. position to GDP

RES/M= non-gold reserves to nominal imports

FB/Y = the ratio of fiscal budget of goods and services ratio.

In the light of the previous section discussion one would expect an improvement in

the terms of trade, or an increase in the difference between the growth rates of GDP

between industrial countries and Egypt or the improvement in the fiscal position

would improve the current account balance while the rise in the foreign interest, an

appreciation of real exchange rate or the increase in the ratio .

The specific form of equation (1) is given by equation (2).

11 See Khan and Knight.(1983)

Topics in Middle Eastern and African Economies Vol. 10, Sept 2008

CA/X = a + bΔTOT + cGDPVMIND + d RER + e FIR + f FPY + U (2)

CA/Y = a + b TOT + c GDPVMIND + d RER + e FIR + f FPY + g( RES/M)(-1)

(3)12

Different versions of equations (2) and (3) were estimated.

The Results The different versions of equation (2) were estimated with using time-

series data for Egypt for the period of 1983-2006.

The results for the different versions of equation (2) are shown in table (2 ).

An attempt13 has been done to estimate equation (2) containing only the three

exogenous variables, all the three variables yield insignificant coefficients and the

adjusted coefficient of determination was quite low. In equation 2.1 which includes

only the endogenous variables, all three variables have coefficients significantly

different from zero at the 5 percent level. However, the rate of growth of GDP and the

fiscal position as a ratio to GDP have unexpected signs. The negative effect of the

rate of growth of GDP on current account could be explained that economic

expansion would encourage imports. The positive effect of fiscal position on the

current account has one explanation is that the improvement in Egypt’s fiscal budget

and relying on domestic market to finance the fiscal deficit. Equation 2.2 includes

three exogenous variables; the terms of trade, the real foreign interest and the foreign

output and two endogenous variables; the real exchange rate and the fiscal position.

All exogenous variables are significantly different from zero at 5 percent level with

expected signs. The real exchange rate is insignificant and the fiscal position is

significant with a positive sign. This may indicate the positive impact of fiscal

improvement Egypt has witnessed after execution of economic reform program which

concentrates on financial adjustment. It may also indicate the government dependency

on internal finance of fiscal budget. Equation 2.3 used current account to GDP ratio

as a dependent variable instead of current account to exports of goods and services

ratio. This does not affect the significant of variables and their signs. Equation 2.4

contains the ratio of non-gold reserves as a dependent endogenous variable and it

excludes the rate of growth of GDP. The new variable is significantly different from

zero and with a negative sign. This is probably because the source of foreign reserves

is non-export earnings. Egypt’s ability to import depends on foreign reserves from

foreign grants. 12 Doroodian 1985 used this equation as an extended model of Khan and knight 1983 model. 13 This attempt is not included.

Topics in Middle Eastern and African Economies Vol. 10, Sept 2008

Table 2: Results For Current account Balance of Egypt :1983-12006

Equation

Number

Constant TOT DIFYY FIR GGDP RER RESM FBY R2 SEE

2.1 0.00053

(11.88)

-7.15

(-11.18)

0.00044

( 1.49)

0.00032

‘( 2.74)

0.87 1.58

2.2 0.00058

( 13.6)

2.54

( 2.92)

4.81

( 1.19)

-3.9

(-2.4)

0.0002

(0.74)

0.00029

(3.09)

0.934 1.15

2.3 23.37

(13.08)

0.0099

(2.7)

0.203

(1.2)

-

0.156

(-

2.34)

-3.18

(-15.12)

9.39

(0.822)

9.95

(2.48)

0.94 0.48

2.4 -0.19

(-6.8)

0.0002

(3.56)

0.0055

(2.7)

0.002

(1.05)

2.83

(7.9)

-0.03

(-1.4)

-0.38

(-1.4)

0.97 0.006

Dependent variable in equation 2.3 is the ratio of the current account to GDP of goods

and services. Dependent variable in equations 2.1,2.2 and 2.4 and is the ratio of

current account to exports. R2 is the adjusted coefficient of determination, T-values

are in the parentheses, and SEE is the standard error of the equation. Terms of trade in

equation 2.4 are the percentage changes in terms of trade for non-oil developing

countries.

Extended model (table3)

Constant F/y TOT GDPF FIR LogGDP RER Rese/M(-

1)

Adjusted

R2

SEE

3.1 25.6

(10.63)

14.5

(2.1)

-.015

(-

3.19)

0.26

(1.5)

-3.312

(-13.9)

17.6

(1.38)

-5.1

(-2.04)

0.90 0.55

3.2 27.2

(13.2)

14.7

(2.3)

-

0.013

(-2.5)

0.27

(1.6)

-

0.134

(-

1.58)

-3.3

(-14.18)

-5.24

(-2.19)

0.91 0.54

Topics in Middle Eastern and African Economies Vol. 10, Sept 2008

The dependent variable is current account as a percentage of nominal GDP. T

values are in parentheses. The adjusted are Square is provided.

The unexpected signs for log real GDP and for the percentage of total non-gold

reserves to imports of goods and services could be explained as the growth of

GDP and the availability of foreign reserves stimulate imports.

Vector Auto-Regression Model

Vector auto regression (VARs): A restricted VARs14 of three exogenous variables;

terms of trade, differences in growth between industrial countries and Egypt and

foreign interest rate and three endogenous variables; the ratio of current account to

exports of goods and services, real exchange rate and growth rate of real GDP. In a

restricted VARs exogenous are allowed to impact the endogenous variables only

directly and not indirectly through the other endogenous variables. The annual data

lags up to one year. The three equations of the model are constrained to be linear in

the lagged values of all endogenous variables and in lagged values of exogenous

variables. In the first VARs the endogenous variables are the ratio of current account

balance to GDP, the growth rate of GDP and the ratio of non-gold reserves to imports

of goods and services. The exogenous variables are the percentage change in

industrial countries GDP, the index of terms of trade for non-oil developing countries

and foreign interest rate.

The model can be estimated with OLS since there are no unlagged endogenous

variables on the right side of the equation and since the endogenous and exogenous

variables on the right side are the same in all equations. Due to data limitations, one

year lag was used for both the endogenous and exogenous variables.

The VAR model can be written as:

Yit =A (L) ∑Y(t-1) + Uit (3)

Where A(L) is a matrix polynomial in the lag operator L and Uit is the time t seriaaly

independent innovations to variable i. and var(Ut) =∑ is a diagonal variance matrix of

Uit. To recover the mutually uncorrelated structural shocks and the structural

parameters from the estimated reduced form parameters and the reduced form

residuals the reduced form residuals are orthogonalized by Cholesky decomposition.

14 The VAR model was introduced by Sims (1972,1980)

Topics in Middle Eastern and African Economies Vol. 10, Sept 2008

This method assumes that contemporaneous structural parameters have recursive

structures which take the form:

et =A (0)ut (4)

The specific model estimated is :

CX = A0 + A1 CX(-1) + A2 GGDP(-1) + A3 RER(-1) + A4 GDPVIND(-1) + A5

TOT (-1) + A6 FIR(-1) + U (5)

Annual data over the years 1983-2006 are used to estimate equation (5), with one year

lag because of data limitations.

Many attempts were undertaken to estimate the VAR model. Some of the results are

presented here. The first attempt introduced all variables as endogenous with one year

lag in the following order ; terms of trade , percentage change in GDP of industrial

countries, foreign interest rate, percent of current account to GDP , log real GDP, total

reserves minus gold to imports of goods and services ratio, fiscal position.

The Impulse responses

The impulse responses present the dynamic responses of the variables to major

economic shocks in relation with the time since the occurrence of the shock. It shows

the responses of the variables to a one-standard deviation of other variables shocks.

The impulse response is represented by the dark lines in figure 2. The dashed lines

represent 1.67 standard error bands or 90 percent confidence intervals. The first

column represents the impulse responses of terms of trade to itself and to other

variables in the VAR. The second column is for GDP of industrial countries impulse

responses, The third for foreign interest rate response. The fourth column for current

account to GDP ratio, the fifth for log GDP, the sixth one for total reserves to imports

ratio and the last column for the fiscal position impulse responses.

Topics in Middle Eastern and African Economies Vol. 10, Sept 2008

- 1 5

- 1 0

- 5

0

5

1 0

1 5

2 0

1 2 3 4 5 6 7 8 9 1 0

Re sp o ns e o f TO T3 t o TO T3

- 1 5

- 1 0

- 5

0

5

1 0

1 5

2 0

1 2 3 4 5 6 7 8 9 1 0

Response of TO T3 t o G DPVM I ND

- 1 5

- 1 0

- 5

0

5

1 0

1 5

2 0

1 2 3 4 5 6 7 8 9 1 0

Re sp o ns e o f TO T3 t o FI R

- 1 5

- 1 0

- 5

0

5

1 0

1 5

2 0

1 2 3 4 5 6 7 8 9 1 0

Re sp o ns e o f TO T3 t o CY

- 1 5

- 1 0

- 5

0

5

1 0

1 5

2 0

1 2 3 4 5 6 7 8 9 1 0

Response of TO T3 t o LO G REALG DP

- 1 5

- 1 0

- 5

0

5

1 0

1 5

2 0

1 2 3 4 5 6 7 8 9 1 0

Response of TO T3 t o TO TRESEI M P

- 1 5

- 1 0

- 5

0

5

1 0

1 5

2 0

1 2 3 4 5 6 7 8 9 1 0

Response of TO T3 t o G O VDY

- 0 . 4

- 0 . 2

0 . 0

0 . 2

0 . 4

0 . 6

0 . 8

1 . 0

1 2 3 4 5 6 7 8 9 1 0

Response of G DPVM I ND t o TO T3

- 0 . 4

- 0 . 2

0 . 0

0 . 2

0 . 4

0 . 6

0 . 8

1 . 0

1 2 3 4 5 6 7 8 9 1 0

Response of G DPVM I ND t o G DPVM I ND

- 0 . 4

- 0 . 2

0 . 0

0 . 2

0 . 4

0 . 6

0 . 8

1 . 0

1 2 3 4 5 6 7 8 9 1 0

Response of G DPVM I ND t o FI R

- 0 . 4

- 0 . 2

0 . 0

0 . 2

0 . 4

0 . 6

0 . 8

1 . 0

1 2 3 4 5 6 7 8 9 1 0

Response of G DPVM I ND t o CY

- 0 . 4

- 0 . 2

0 . 0

0 . 2

0 . 4

0 . 6

0 . 8

1 . 0

1 2 3 4 5 6 7 8 9 1 0

Response of G DPVM I ND t o LO G REALG DP

- 0 . 4

- 0 . 2

0 . 0

0 . 2

0 . 4

0 . 6

0 . 8

1 . 0

1 2 3 4 5 6 7 8 9 1 0

Response of G DPVM I ND t o TO TRESEI M P

- 0 . 4

- 0 . 2

0 . 0

0 . 2

0 . 4

0 . 6

0 . 8

1 . 0

1 2 3 4 5 6 7 8 9 1 0

Response of G DPVM I ND t o G O VDY

- 1 . 0

- 0 . 5

0 . 0

0 . 5

1 . 0

1 . 5

1 2 3 4 5 6 7 8 9 1 0

Re sp o ns e o f FI R t o TO T3

- 1 . 0

- 0 . 5

0 . 0

0 . 5

1 . 0

1 . 5

1 2 3 4 5 6 7 8 9 1 0

Response of FI R t o G DPVM I ND

- 1 . 0

- 0 . 5

0 . 0

0 . 5

1 . 0

1 . 5

1 2 3 4 5 6 7 8 9 1 0

Re sp o ns e o f FI R t o FI R

- 1 . 0

- 0 . 5

0 . 0

0 . 5

1 . 0

1 . 5

1 2 3 4 5 6 7 8 9 1 0

Re sp o ns e o f FI R t o CY

- 1 . 0

- 0 . 5

0 . 0

0 . 5

1 . 0

1 . 5

1 2 3 4 5 6 7 8 9 1 0

Response of FI R t o LO G REALG DP

- 1 . 0

- 0 . 5

0 . 0

0 . 5

1 . 0

1 . 5

1 2 3 4 5 6 7 8 9 1 0

Re sp o ns e o f FI R t o TO TRESEI M P

- 1 . 0

- 0 . 5

0 . 0

0 . 5

1 . 0

1 . 5

1 2 3 4 5 6 7 8 9 1 0

Response of FI R t o G O VDY

- 1 . 5

- 1 . 0

- 0 . 5

0 . 0

0 . 5

1 . 0

1 . 5

2 . 0

1 2 3 4 5 6 7 8 9 1 0

Re sp o ns e o f CY t o TO T3

- 1 . 5

- 1 . 0

- 0 . 5

0 . 0

0 . 5

1 . 0

1 . 5

2 . 0

1 2 3 4 5 6 7 8 9 1 0

Response of CY t o G DPVM I ND

- 1 . 5

- 1 . 0

- 0 . 5

0 . 0

0 . 5

1 . 0

1 . 5

2 . 0

1 2 3 4 5 6 7 8 9 1 0

Re sp o ns e o f CY t o FI R

- 1 . 5

- 1 . 0

- 0 . 5

0 . 0

0 . 5

1 . 0

1 . 5

2 . 0

1 2 3 4 5 6 7 8 9 1 0

Re sp o ns e o f CY t o CY

- 1 . 5

- 1 . 0

- 0 . 5

0 . 0

0 . 5

1 . 0

1 . 5

2 . 0

1 2 3 4 5 6 7 8 9 1 0

Response of CY t o LO G REALG DP

- 1 . 5

- 1 . 0

- 0 . 5

0 . 0

0 . 5

1 . 0

1 . 5

2 . 0

1 2 3 4 5 6 7 8 9 1 0

Response of CY t o TO TRESEI M P

- 1 . 5

- 1 . 0

- 0 . 5

0 . 0

0 . 5

1 . 0

1 . 5

2 . 0

1 2 3 4 5 6 7 8 9 1 0

Response of CY t o G O VDY

- 0 . 6

- 0 . 4

- 0 . 2

0 . 0

0 . 2

0 . 4

1 2 3 4 5 6 7 8 9 1 0

Response of LO G REALG DP t o TO T3

- 0 . 6

- 0 . 4

- 0 . 2

0 . 0

0 . 2

0 . 4

1 2 3 4 5 6 7 8 9 1 0

Response of LO G REALG DP t o G DPVM I ND

- 0 . 6

- 0 . 4

- 0 . 2

0 . 0

0 . 2

0 . 4

1 2 3 4 5 6 7 8 9 1 0

Response of LO G REALG DP t o FI R

- 0 . 6

- 0 . 4

- 0 . 2

0 . 0

0 . 2

0 . 4

1 2 3 4 5 6 7 8 9 1 0

Response of LO G REALG DP t o CY

- 0 . 6

- 0 . 4

- 0 . 2

0 . 0

0 . 2

0 . 4

1 2 3 4 5 6 7 8 9 1 0

Response of LO G REALG DP t o LO G REALG DP

- 0 . 6

- 0 . 4

- 0 . 2

0 . 0

0 . 2

0 . 4

1 2 3 4 5 6 7 8 9 1 0

Response of LO G REALG DP t o TO TRESEI M P

- 0 . 6

- 0 . 4

- 0 . 2

0 . 0

0 . 2

0 . 4

1 2 3 4 5 6 7 8 9 1 0

Response of LO G REALG DP t o G O VDY

- 0 . 0 4

- 0 . 0 2

0 . 0 0

0 . 0 2

0 . 0 4

1 2 3 4 5 6 7 8 9 1 0

Response of TO TRESEI M P t o TO T3

- 0 . 0 4

- 0 . 0 2

0 . 0 0

0 . 0 2

0 . 0 4

1 2 3 4 5 6 7 8 9 1 0

Response of TO TRESEI M P t o G DPVM I ND

- 0 . 0 4

- 0 . 0 2

0 . 0 0

0 . 0 2

0 . 0 4

1 2 3 4 5 6 7 8 9 1 0

Re sp o ns e o f TO TRESEI M P t o FI R

- 0 . 0 4

- 0 . 0 2

0 . 0 0

0 . 0 2

0 . 0 4

1 2 3 4 5 6 7 8 9 1 0

Response of TO TRESEI M P t o CY

- 0 . 0 4

- 0 . 0 2

0 . 0 0

0 . 0 2

0 . 0 4

1 2 3 4 5 6 7 8 9 1 0

Response of TO TRESEI M P t o LO G REALG DP

- 0 . 0 4

- 0 . 0 2

0 . 0 0

0 . 0 2

0 . 0 4

1 2 3 4 5 6 7 8 9 1 0

Response of TO TRESEI M P t o TO TRESEI M P

- 0 . 0 4

- 0 . 0 2

0 . 0 0

0 . 0 2

0 . 0 4

1 2 3 4 5 6 7 8 9 1 0

Response of TO TRESEI M P t o G O VDY

- 0 . 0 1 5

- 0 . 0 1 0

- 0 . 0 0 5

0 . 0 0 0

0 . 0 0 5

0 . 0 1 0

0 . 0 1 5

1 2 3 4 5 6 7 8 9 1 0

Response of G O VDY t o TO T3

- 0 . 0 1 5

- 0 . 0 1 0

- 0 . 0 0 5

0 . 0 0 0

0 . 0 0 5

0 . 0 1 0

0 . 0 1 5

1 2 3 4 5 6 7 8 9 1 0

Response of G O VDY t o G DPVM I ND

- 0 . 0 1 5

- 0 . 0 1 0

- 0 . 0 0 5

0 . 0 0 0

0 . 0 0 5

0 . 0 1 0

0 . 0 1 5

1 2 3 4 5 6 7 8 9 1 0

Response of G O VDY t o FI R

- 0 . 0 1 5

- 0 . 0 1 0

- 0 . 0 0 5

0 . 0 0 0

0 . 0 0 5

0 . 0 1 0

0 . 0 1 5

1 2 3 4 5 6 7 8 9 1 0

Response of G O VDY t o CY

- 0 . 0 1 5

- 0 . 0 1 0

- 0 . 0 0 5

0 . 0 0 0

0 . 0 0 5

0 . 0 1 0

0 . 0 1 5

1 2 3 4 5 6 7 8 9 1 0

Response of G O VDY t o LO G REALG DP

- 0 . 0 1 5

- 0 . 0 1 0

- 0 . 0 0 5

0 . 0 0 0

0 . 0 0 5

0 . 0 1 0

0 . 0 1 5

1 2 3 4 5 6 7 8 9 1 0

Response of G O VDY t o TO TRESEI M P

- 0 . 0 1 5

- 0 . 0 1 0

- 0 . 0 0 5

0 . 0 0 0

0 . 0 0 5

0 . 0 1 0

0 . 0 1 5

1 2 3 4 5 6 7 8 9 1 0

Response of G O VDY t o G O VDY

Response t o O ne S. D. I nnovat ions ± 2 S. E.

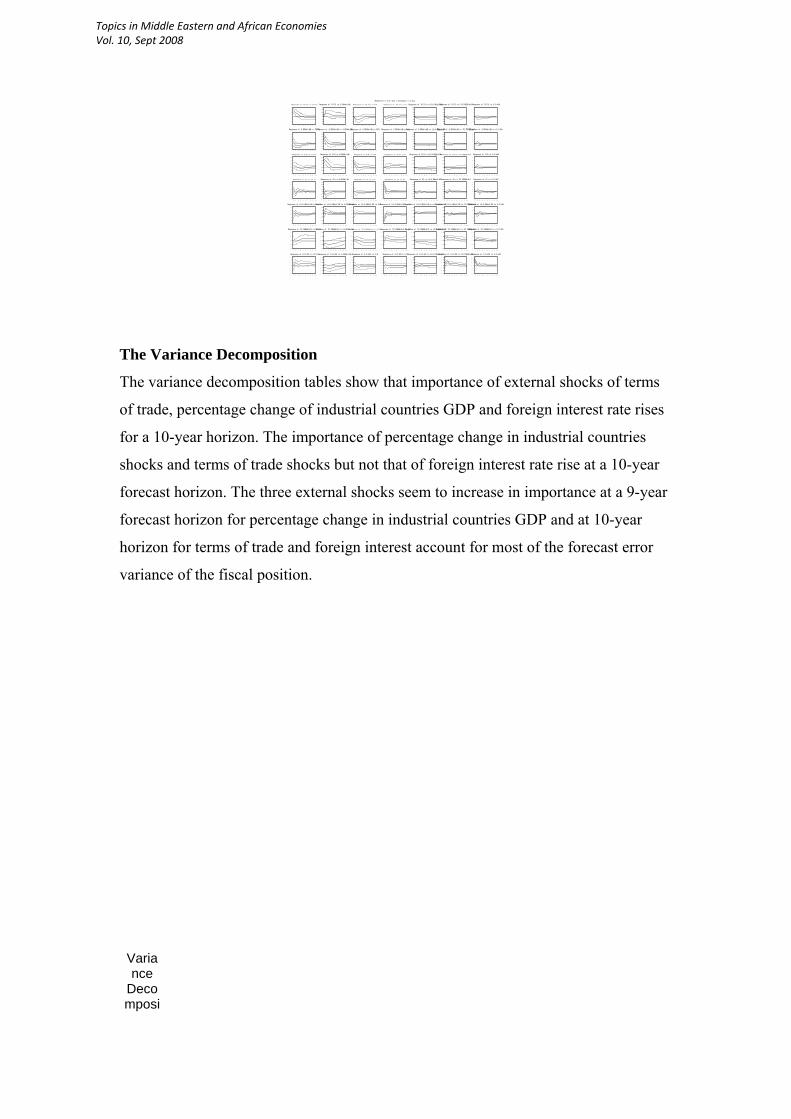

The Variance Decomposition

The variance decomposition tables show that importance of external shocks of terms

of trade, percentage change of industrial countries GDP and foreign interest rate rises

for a 10-year horizon. The importance of percentage change in industrial countries

shocks and terms of trade shocks but not that of foreign interest rate rise at a 10-year

forecast horizon. The three external shocks seem to increase in importance at a 9-year

forecast horizon for percentage change in industrial countries GDP and at 10-year

horizon for terms of trade and foreign interest account for most of the forecast error

variance of the fiscal position.

Variance

Decomposi

Topics in Middle Eastern and African Economies Vol. 10, Sept 2008

tion of CY:

Period

S.E. TOT3 GDPVMIND FIR CY

1 1.423742 6.541652 4.314920 4.749274 84.39415 2 1.647591 8.687021 16.69672 6.406716 63.08298 3 1.721135 10.07079 18.45694 6.093572 57.88638 4 1.740743 10.01045 19.41019 6.163971 56.58966 5 1.759277 11.10026 19.05284 6.356879 55.40363 6 1.768023 11.32437 18.87325 6.712654 54.85842 7 1.775920 11.53058 18.70794 6.957387 54.37497 8 1.780833 11.55076 18.60683 7.089470 54.09254 9 1.785082 11.54936 18.53043 7.131174 53.87966 10 1.789046 11.51556 18.47172 7.131059 53.70863

Variance

Decomposition of LOGREALGDP:

Period

S.E. TOT3 GDPVMIND FIR CY

1 0.388308 6.763725 4.399905 2.746551 85.31481 2 0.448497 7.938231 15.56943 5.658767 63.99438 3 0.470792 9.429078 16.98915 5.539897 58.60051 4 0.478930 9.386179 17.49349 5.685758 56.84443 5 0.487335 10.48855 16.90367 5.937499 55.12673 6 0.493650 10.64674 16.47845 6.320256 53.91868 7 0.500101 10.73837 16.10050 6.551897 52.82607 8 0.506056 10.60470 15.77113 6.631993 51.96778 9 0.512084 10.43229 15.48173 6.594025 51.23405 10 0.518254 10.21634 15.22071 6.497161 50.57607

Variance

Decomposition of

Topics in Middle Eastern and African Economies Vol. 10, Sept 2008

GOVDY:

Period

S.E. TOT3 GDPVMIND FIR CY

1 0.011765 6.768627 12.73053 1.219711 7.439568 2 0.015297 13.87435 15.62571 4.248845 4.444264 3 0.017472 11.26157 25.15624 7.011008 3.738740 4 0.019260 12.83210 27.76893 8.403091 3.258855 5 0.020384 13.37463 29.37527 9.735445 3.157469 6 0.021203 14.66702 29.21273 10.83072 3.115595 7 0.021714 15.43378 28.88642 11.81006 3.135018 8 0.022046 16.05933 28.44348 12.52904 3.138286 9 0.022238 16.41160 28.11622 13.02310 3.131947 10 0.022349 16.62590 27.87562 13.31800 3.115047

Topics in Middle Eastern and African Economies Vol. 10, Sept 2008

Conclusion

The paper purpose is to estimate the impact of exogenous shocks on the main

macroeconomic variables. The results show that all three exogenous shocks are

significant with the expected sign. Endogenous shocks are also important

interpretation of economic fluctuations. However, some endogenous shocks come

with unexpected sign. When exogenous shocks are examined separately, they were

not significant. An important exogenous variable was omitted because of lack of data.

The foreign grants Egypt has received during all its distinguished periods play the role

of a buffer against the impact of exogenous shocks. A reduced regression model of

current account ratio shows that changes in domestic variables are more important in

explaining the behavior of current account to GDP or to exports ratio. However, a

dynamic VAR model shows that shocks to exogenous variables are more important.

Attempts also should be done to take account of the different economic policies

applied. This could be presented by dummy variables that take zero in years before

implementing economic reform program in the 1991 and take one afterwards.

Topics in Middle Eastern and African Economies Vol. 10, Sept 2008

References

Ahmed, Shaghil,”” Sources of Economic Fluctuations in Latin America and

Implications for Choice of Exchange Rate Regimes” Board of Governors of the

Federal Reserve System, International Finance Division, No.656.December 1999.

Ahmed, Shaghil, Ara, Iffat and Hyder, Kalim”” How External Shocks and Exchange

Rate Depreciation Affect Pakistan? Implications for Choice of an Exchange Rate

Regime.” SBP-Research Bulletin Volume 2, No.1.2006.

Agenor ,P.,diwan.I,and Al-Kibbi,Jamal.”’ Non-Dent financing of Development in

MENA. 2000

Alissa, Sufyan. ”’The Political economy of reform in Egypt: Understanding the Role

of Institutions”” www.carnegieendowment.org

Balassa, Bela “” Policy Responses to Exogenous Shocks in Developing Countries””

The American Economic Review, Vol.76,No.2, Papers and Proceedings of the

Ninety-Eighth Annual Meeting of the American Association. May 1986, pp75-78

Doroodian, Khorow “” Determinants of Current Account Balances of Non-Oil

Developing Countries in the 1970: Comment on Khan and Knight”” Staff Papers-

International Monetary Fund, Vol.32, No.1.(Mar.,1985),pp160-164..

Ball,L.;Mankiw,G. “ Relative – Price Changes as Aggregate Supply Shocks”’

Vol.110,No.1. Feb.1996.pp 161-193 The quarterly journal Of Economics.

Gordon, Robert “’ Supply Shocks and Monetary Policy Revisited”’ The American

Economic Review,Vol.74,No.2,Ppers and proceedings of the Ninety-Sixth Annual

Meeting of the American Economic Association.(May,1984),pp.38-43.

Topics in Middle Eastern and African Economies Vol. 10, Sept 2008

J.Fry, Maxwell and M.Lilien, David “” Monetary Policy Responses to Exogenous

Shocks “The American Economic Review, Vol.76, No.2, Papers and Proceedings of

the Ninety-Eighth Annual Meeting of the American Association. May. 1986, pp79-83.

Khan, Mohsin, “ Developing Country Exchange Rate Policy Responses to Exogenous

Shocks “ The American Economic Review, Vol.76,No.2, Papers and Proceedings of

the Ninety-Eighth Annual Meeting of the American Association. May 1986, pp84-87.

“Determinants of Current account Balances of Non-Oil

Developing Countries in the 1970s: An Empirical Analysis “’ Staff papers-IMF

Vol.30,No 4 (Dec.1983) , pp.819-842.

Kamal, Mustafa. “” What Have We Done With U.S. Aid?””Al - Ahram Weekly On

line .21-27. June. 2001..Issue Number 539.

Tanzi, Vito, “Fiscal Policy Responses to Exogenous Shocks in Developing Countries”

The American Economic Review, Vol, 76, No.2 Papers and Proceedings of the

Ninety- Eighth Annual Meeting of the American Economic Association.(May, 1986),

pp. 88- 91.

Topics in Middle Eastern and African Economies Vol. 10, Sept 2008

Topics in Middle Eastern and African Economies Vol. 10, Sept 2008