Embed Size (px)

Citation preview

Executors' Duty to AccountLegal and Practical Perspectives

Gregg W. Knudsen Will and Estate Planning Officer

Scotiatrust Suite 900

1801 Hollis Street Halifax, NS, B3J 3N4

Telephone: (902) 420-2296 Fax: (902) 420-7119

I. Introduction

Recent changes to Regulation 47(1) of the Barristers and Solicitors Act expand the Trust Account reporting requirements of the membership of the Nova Scotia Barristers' Society. These changes were passed to respond to a number of transgressions widely reported in the local press and various Society publications. With this new pending responsibility, it is an appropriate time to review our current obligations as proctors and executors with respect to accounting. Accordingly, a review of the duty of an executor to account is in order.

Rather than dealing with the new regulation, this paper is a review of the current obligations. Firstly, I will provide a review of the relationship between anexecutor's duties at common law and the duty to account. I will then discuss the process of passing accounts under the current Probate Act. Finally, I will conclude with remarks that will assist you and your clients in tracking your efforts and, hopefully, keep risk management concerns to a minimum. Therefore, my comments apply equally to the proctor of an estate, a named sole or co-executor or a corporate executor.

II. Executors' Dutv to Account

Common Law

It is well established that an executor or administrator of an estate has duties akin to that of a trustee and, therefore, he/she is subject to the various common law duties applicable to a fiduciary.' The executor of an estate owes a fiduciary responsibility to the beneficiaries of an estate and to its lawful creditors (until the latter's claims are satisfied). There is considerable academic commentary and case law on the various duties, a meaningful review of which is beyond the scope of this paper. In summary, they include the obligation to protect the assets entrusted to him, to distribute the property according to law and the duty to act in the best interests of the beneficiaries and not to obtain secret profits from his office. Inherent in all of this is the duty to be accountable for these assets.

The authors of Widdifield - Law and Practice Relating to Executors Accounts quotes the old English case of Freeman v. Fairlie, 3. Mer. 43:

"It is the bounden duty of an executor, or other trustee, to keep clear and distinct accounts of the property which he is bound to administer."

Further, this duty includes a corresponding right of the beneficiaries to demand to review accounts of the executor at any time.

1 Re: Speight (1833), 22 Ch. D. 727 (C.A.); See also D.M. Waters' Law a/Trusts in Canada (2d ed.), pp. 31-42.

On a more concrete level, David A. Howlett provides a succinct commentary on executors' duties in his book, Estate Matters in Atlantic Canada2

• Ofthose principles, the following are the most relevant to our discussions:

"3. Within a reasonable time, convert (sell) assets which require conversion at the best possible price, and bring the assets into a proper state of investment ....

5. Refrain from misusing the estate property, or from commingling it with one's own funds. Otherwise, the personal representative's funds may be forfeited to the estate, except to the extent that the representative is able to prove they are his own separate assets ...

7. Distribute the assets properly ...

8. Maintain proper accounts and records ... "

Therefore, an executor's duty to account plays a crucial role in reinforcing the other fiduciary duties imposed by the common law as it, theoretically, provides an empirical illustration of how the executor has performed those duties.

Statutory Position

There are various statutory provisions which underscore the importance of a duty to account.

The Nova Scotia Probate Act requires an executor to file his accounts at least ten days before the time fixed for the Closing3

. Once the accounts are approved and the Estate is closed, this is conclusive evidence of the following:

(a) that the items in such account for money paid to creditors, to legatees, to the next of kin and for necessary expenses, are correct;

(b) that such executor or administrator has been charged all the interest for money received by him and embraced in his account for which he was legally accountable;

(c) that the money stated in such account as collected was all that was collectable on the debts mentioned in such account at the time of the allowance thereof. 4

Further, section 56 of the Trustee Act5 is also relevant:

2 See pp. 128-130 3 R.S.N.S. 1989. c. 359. s.73. 4 Probate Act, s. 79 5 R.S.N.S. 1989 c. 479

2

"Where an executor or administrator has given such or like notice as, in the opinion of the court in which such executor or administrator is sought to be charged, would be sufficient in the Supreme Court in an administration action, or in a court of probate, for creditors and others to send in to the executor or administrator their claims against the estate of the testator or intestate, such executor or administrator shall, at the expiration of the time named in the said notices, or the last of the said notices for sending such claims, be at liberty to distribute the assets of the testator or intestate, or any part thereof, having regard to the claims of which such executor or administrator has then notice, and shall not be liable for the assets or any part thereof so distributed to any person of whose claim such executor or administrator did not have notice at the time of distribution of the said assets or a part thereof, as the case may be, but nothing in this Section contained shall prejudice the right of any creditor or claimant to follow the assets or any part thereof into the hands of the person or persons who have received the same respectively. (emphasis mine)

While there has been considerable debate over the necessity to formally close every estate6

, it is clear that the act of doing so provides a measure of protection to the executor for the receipt and disbursement of funds up to the date of the Final Decree. At a minimum, these and other statutory provisions further reinforce the importance of an executor's duty to account. Furthermore, notwithstanding one's opinion on the requirement to close probate, it is well settled that an executor has a duty to account to those parties interested in an estate even if one chooses not to probate the estate at a1l7

.

III. Dealing with the Assets

An executor's account is merely a summary of all transactions involving the assets of an estate. Hence, it is useful to review some of the issues involved in preparing an inventory and their impact on the final accounting.

Asset Gathering

The executor is responsible for the administration of all assets to which the testator was entitled at the time of hislher death. Proof of title and ownership is, quite often, a question of fact readily ascertainable from the circumstances. That being said, it is not difficult to think of circumstances where entitlement is very much at issue. There are other types of assets whose "ownership" during the testator's lifetime may be undisputed but their status as estate assets is not as clear. Assets such as life insurance, RRSPs and RRIFs and

6 See article by LJ. Hayes, QC, "Estate Administration Overview", presentation given at CLE, October 1986; Vincent P. Allen, QC, Nova Scotia Probate Law and Procedure, pp. 44-45 also Law Reform Commission of Nova Scotia: Final Report Probate Reform in Nova Scotia, pp. 71-73; 7 For a general review, see MacDonald. Sheard and Hull- Probate Practice (4'h ed), pp. 335-336 and Waters, supra Note 1 at pp. 871-876. .

3

jointly held assets are becoming more common due, in part, to the growing popularity of probate fee avoidance as an estate planning strategy.

Beneficiary Designations

In life insurance policies, pension plans and registered investment plans, the annuitant/insured is, usually, the "owner" of the policy or plan. If a person makes a beneficiary designation, the assets pass to the named beneficiary as a consequence of the owner's death. So long as the estate is solvent and it is not the named beneficiary, the assets pass outside of the estate and no probate fees or executor's commission are payable on these assets8

. In that case, the executor is not responsible to the beneficiary for the proceeds unless, presumably, he has expressly or by his actions assumed responsibility for them. If the estate is the named beneficiary then the assets form part of the estate and must be taken into account and distributed according to the will (or to the deceased's heirs, in case of an intestacy). Therefore, it is important to check the latest will and/or beneficiary designation to determine the last named beneficiary.

In considering insolvent estates, there have been many cases dealing with the claims of a deceased's creditors when the deceased's assets include life insurance, RRSPs or annuities9

. In general, the rule seems to be that if an asset fits within the broad definition of "life insurance" as set out in the Insurance ActiO, then the proceeds pass to the named beneficiarr pursuant to the insurance contract and are not subject to the claims of hislher creditors I . Further, section 160.2 of the Income Tax Act provides that a named beneficiary of an RRSP/RRIF (other than a spouse, dependant child or grandchild) is jointly and severally liable with the deceased's estate for the tax payable. The deceased's estate is required to pay the income tax arising from the death ofthe annuitant l2

.

However, if the estate is unable to pay the income tax burden, the recipient is liable for the tax resulting from the RRSP/RRlF.

Therefore, in preparing an accounting, it is important to remember the impact of a beneficiary designation to determine if that asset forms part of the estate.

Joint Accounts

Many clients have cash or investments held injoint accounts. In some cases, it is intended to serve as a shared resource, such as a husband and wife, while at other times it is a matter of convenience, such as a parent and a child. Many people believe that joint accounts described as "joint with right of survivorship" always pass to the survivor and do not form part of the deceased's estate. However, as a general rule, there is a

8 Bruhm v. Feindel el al. (1999), 175 N.S.R. (2d.) 173 (SC). 9 Canadian Imperial Bank a/Commerce v. Besharah (1989),58 D.L.R. (4'h) 705 (Ont. H.C.); Pozniak Estate v. Pozniak et 01. (1993), 88 Man. R. (2d.) 36 (CA); Waugh Estate v. Waugh et al (1990), 63 Man. R. (2d) 155 (CAl. to R.S.N.S. 1989. c. 231. s. 3(0); "ibidss. 173-226 esp. ss. 193 and 198. 12 Slater v. Klassen Estate (2000), D.T.C. 6336 (Man.Q.B.) interpreting s. 146(8.8)(a) of the Income Tax Act;

4

presumption of advancement when assets are held jointly between two spouses. In that case, jointly held assets are deemed to pass to the survivor on death without flowing through the estate. In other cases, such as a parent and adult child, there is usually one contributor (the parent) with another ajoint account holder as a matter of convenience (e.g. to help write cheques to pay bills). On the death of the contributor, the noncontributor is said to hold the parent's interest in a resulting trust. The proceeds therefore, form part of the deceased's estate except for the amount the child has contributed on his/her own accord 13.

Capital versus Revenue - Not what we learned in Taxation I

The terms "capital" and "revenue" (or income) in an estate context are unique when compared with conventional accounting principles or those found in the Income Tax Act.

For example, if a person owns one share of the Bank of Nova Scotia - the share is the capital, while the dividend paid is the income.

In an Income Tax context, the impact is different. Using the above example, let us assume the share value rises resulting in a taxable capital gain of $20 on death. As a result, 2/3rds of the value of the gain is included in income and taxed at the taxpayer's marginal tax rate.

In an estate context, the capital includes all assets owned or due to the deceased at the time of his death except for those assets passing outside of the estate by operation of law. Thus, funds normally thought of as income receivable by the deceased prior to death would be capital for the purposes of the inventory or the accounting. For example, the person who owned the BNS share above and dies between the record date and the payment date of the dividend, the value of the dividend is part of the capital of the estate and should be shown as such on the inventory14.

As described later, where a will provides for an outright distribution of the estate without creating trusts, the capital/income distinction is not as significant.

InventorylWarrant of Appraisement

To adequately perform an executor's duties, accurate valuation of estate assets is critical. The surrounding circumstances and the terms of the will, dictate the best method for seeking valuation.

In preparing the accounts, an executor is required to account for the receipt and disbursement of all assets "flowing through" the estate. Two values are important for this

13 Re: Fenton Estate (1978) 26 N.S.R. (2d.) 662 (SCTD); MacInnes Estate v. MacDonald (1994), 138 N.S.R. (2d.) 321 affinned in an unreported decision S381/12 on May 31,1995. 14 Publicly traded companies pay dividends to all of those persons holding shares as ofa given date, the record date. The dividends are paid several days later on the payment date. Between these dates, the shares are referred to as e..t dividend.

5

process: the ascertained value (which is then verified by two independent appraisers appointed by the Court) and the final value appearing on the accounting. Before discussing the contents of the accounting, it is appropriate to review how to calculate the ascertained value of the assets as shown in the Inventory/Warrant of Appraisement.

a) Real Property -Any real property generally or specifically devised under a will passes directly to the devisee thereby not forming part of the deceased's assets available for probate (assuming the assets are sufficient to pay his creditors). Similarly, in the estate of an intestate, real property devolves upon the heirs at law removing the deceased's real property from the assets subject to administration15 (once again, assuming all of the deceased's creditor's are satisfied). Any real property originally conveyed or devised to two or more owners as joint tenants passes to the survivor(s) by operation of law on the death of one of the joint tenants and, consequently, should not appear on the inventory.

On the other hand, the interest of a tenant in common must appear on the inventory as the proportionate value of the property. It is important to keep in mind the provisions of the Real Property Act which provides that when the deed, will or other manner of conveyance coveys property to two or more joint owners, the real property is presumed held by the grantees as tenants in common 16 unless otherwise stated.

In valuing real property, there is considerable debate over the most appropriate method to be used. Some executors prefer to employ a private appraiser, while others, attempting to save costs, obtain an estimate from a real estate agent or use the property's most recent assessed value.

Each of these methods, while useful, have limitations. The cost of a private appraiser may be prohibitive in cases where the property in question is of little value. Real estate agents' estimates are sometimes unreliable, such as when their valuation techniques are driven by the motivation to obtain the listing and its commission. Finally, the assessed value may be oflimited utility as it is based on a historical base date 17

15 See Howlett. supra Note 3, pp. 64-66. 16 R.SN.S. 1989, c. 385, s.5. 17 R.SN.S 1989, c.23, s.42. An assessment is calculated using the market value of your property at an earlier date. However, this calculation takes into account the physical state of one's property as of January I of the current year (,state date"). Thus, if deceased's property has not changed during the year and the base date is only a few years prior, the assessment may be close to its fair market value. However, using a real life example, in 1995, residential assessments were calculated using a base date of January I, 1988 and a state date of January I, 1995. Therefore, if your deceased passed away in late 1995, his property assessment would have been based on its value in 1988 and its condition on New Year's Day of 1995. 1fhe experienced a fire, expropriation or other loss of value during the year, the assessment would not reflect it. Nor would itreflect any additional value if the deceased had renovated his house or added an outbuilding.

6

bi Personal Property - There are many types of personal property. I have summarized below some of the more common examples:

i. Personal Effects - One should seek the advice of an appraiser or auctioneer in valuing personal effects, furniture, etc. owned by the deceased. In some circumstances, it may be appropriate to use an unsupported estimate of value. For example, if the deceased resided in a room at a private care facility before his death, the contents may be fairly minimal. Most Registrars will accept a reasonable estimate of a nominal value in such cases.

ii. Shares of publicly traded companies - Valuation is readily available from the financial press or a brokerage. Dividends due should be included if the deceased died between the record date and the payment date.

iii. Debt securities, Gles and Government Bonds - The value of a debt security is either its market value or coupon value - depending on if it is publicly traded, plus accrued interest. In the case of publicly traded bonds (e.g. corporate and government bonds except CSBs and treasury bills), their market value can be obtained from the financial press or a brokerage. For all others, their capital value is, simply, the face value of the instrument. Accrued interest is calculated by determining the amount of interest earned between the last payment date and the date of death. This figure is the per diem rate times by the number of days or:

Amount of interest payment X # of days # of Days to the next payment (inc!. date of death)

*In the above fonnula. the previous payment date should be excluded.

For example, ifthe deceased owned a $1000 OlC paying 10% annual interest with payments semi annually, and the accrued interest was calculated as $12.50. The value of the OlC on the inventory will be $1012.50 while income collected will be shown as $37.50.

iv. Bank Accounts - This is simply the balance on the date of death plus accrued interest.

v. Interests in privately owned enterprises - Valuation in these matters is very tricky due to the variety of business arrangements. One should consult the corporate accountant (if there is one) to see if a formal valuation is required or if some other method is appropriate, such as the value of the shareholder's equity. Certain partnership agreements and "buy-sell" agreements mandate a method of va!uation on the death of a shareholder or partner.

Investment

Section 3 of the Trustee ActJ8 provides:

18 • R.SNS 1989 . . c.479. as amended, SNS 1994-95.c.19

7

" ... a trustee may, for the sound and efficient management of a trust, establish and adhere to investment policies, standards and procedures that a reasonable and prudent person would apply in respect of a portfolio of investments to avoid undue risk of loss and to obtain a reasonable return."

This principle, commonly known as the "prudent man rule" applies equally to executors of an estate.

There has been little judicial discussion on the definition of "a reasonable and prudent person" in this context. Where a will directs the executor to completely liquidate the estate and distribute the proceeds to a number of named beneficiaries, prudent investment requires liquidity, safety of principal and a suitable rate of return. In essence, treasury bills or a suitable deposit instrument subject to limits imposed by the Canadian Deposit Insurance Corporation should meet those requirements. If assets are to be distributed in kind or a trust created, more sophisticated investment approaches are required. One should seek appropriate investment advice to determine the needs ofthe particular trust or estate.

IV, Passing The Accounts

Once the assets are administered, the executor proceeds to close the estate. The following section discusses the process of passing the accounts in that context.

Following the issuance of the Citation to Close, the executors or administrators are obliged to file their accounts for approval at the Closingl9

. Though not specifically required, it is common for the executor to send copies of the accounts to all residual beneficiaries (along with those in priority where an abatement or insolvency occurs).

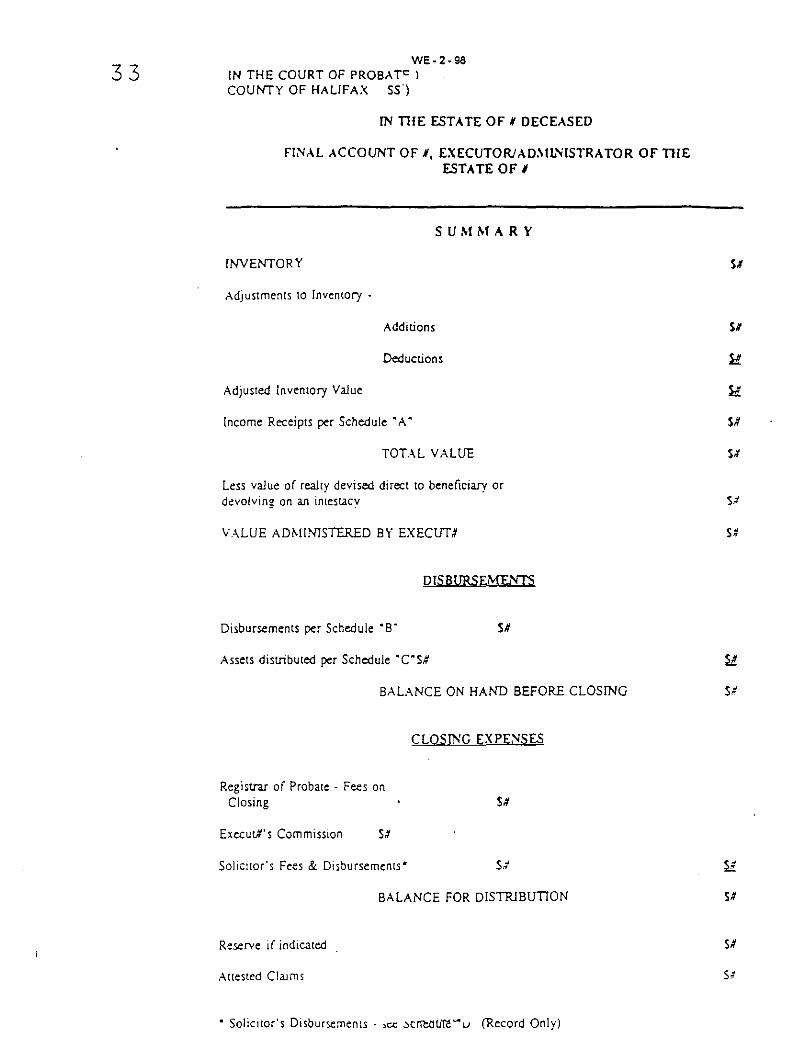

Form

Unlike other jurisdictions, the current Probate Act does not require an executor or administrator's accounts to adhere to a certain prescribed form. Vincent P. Allen, QC, alleviated this somewhat by providing the following guidelines:

"In its simplest form, this account will begin with the valuation shown on the inventory. Then add any additions to the inventory, subtract anything deleted, and this will give the final revised inventory. Add any income the estate earned and the total will be the total value of the estate. The next step is to deduct all the expenses of the estate, and then deduct the value of any paid gifts, including money. Basically, that's all there is to it. To complete the documentation, add a separate sheet itemizing each separate group so that the total can be checked. These sheets are called "schedules", and they are usually arranged alphabetically.

Your final accounts then may consist of (I) a summary sheet, which summarizes the

19 Probate Act. s. 73.

8

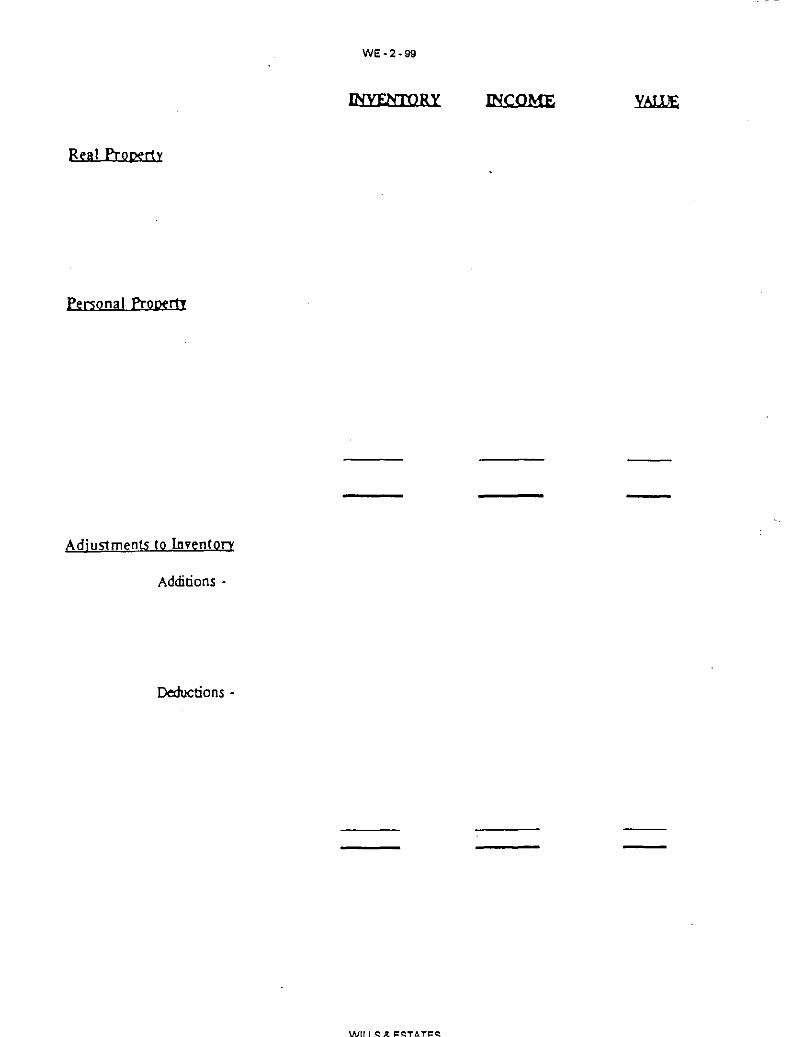

results of the administration by using totals only, leaving spaces at the bottom for the insertion of Probate fees, commission awarded to the executor, and fees of the solicitor, and (2) a series of Schedules, e.g. Schedule A may be a reproduction or summary of the inventory as shown in the original appraisal, with the additions or deletions, shown here or on a separate schedule; Schedule B might be a detailed statement of all income earned, (sometimes the income is shown on the same Schedule as the inventory information); Schedule C might be the itemized list of expenses (disbursements); Schedule D might be the list of assets or cash transferred to entitled persons. ,,20

From this he has developed a "standard" form of accounts which is attached as an appendix to this paper.

In my experience, there have been situations where these schedules are not adequate and, as Mr. Allen suggests, it is indeed necessary to expand upon the number of schedules. For example, if an estate has a large portfolio of securities, it will be necessary to show the gain or loss realized when the assets have been sold. Ifthere are many unique personal effects, a separate schedule may be appropriate as well.

Whatever format one uses, it is important to remember that an accounting is a statutory requirement once the Citation to Close has been issued. Therefore, it should be prepared in a way that will satisfy the Registrar that all statutory requirements have been met. In other words, it should show that all assets have been taken into account, distributions have been made and all funds paid are "actual and necessary disbursements which are just and reasonable". In doing so, the executor will be assured of the protections afforded by statute.

Contents

l. Summary - This cover page contains the final total for each schedule described below. Thus, it gives the Registrar and the residual heirs a "snap shot" 9fthe activity in the estate.

II. Capital Receipt Entries:

It may be possible to include these items in one schedule or, if necessary, several schedules could be used. For each schedule, the total amount is calculated at the bottom of the page and carried over to the cover page.The following items form part of the total capital value ofthe estate:

- Assets shown on the Inventory;

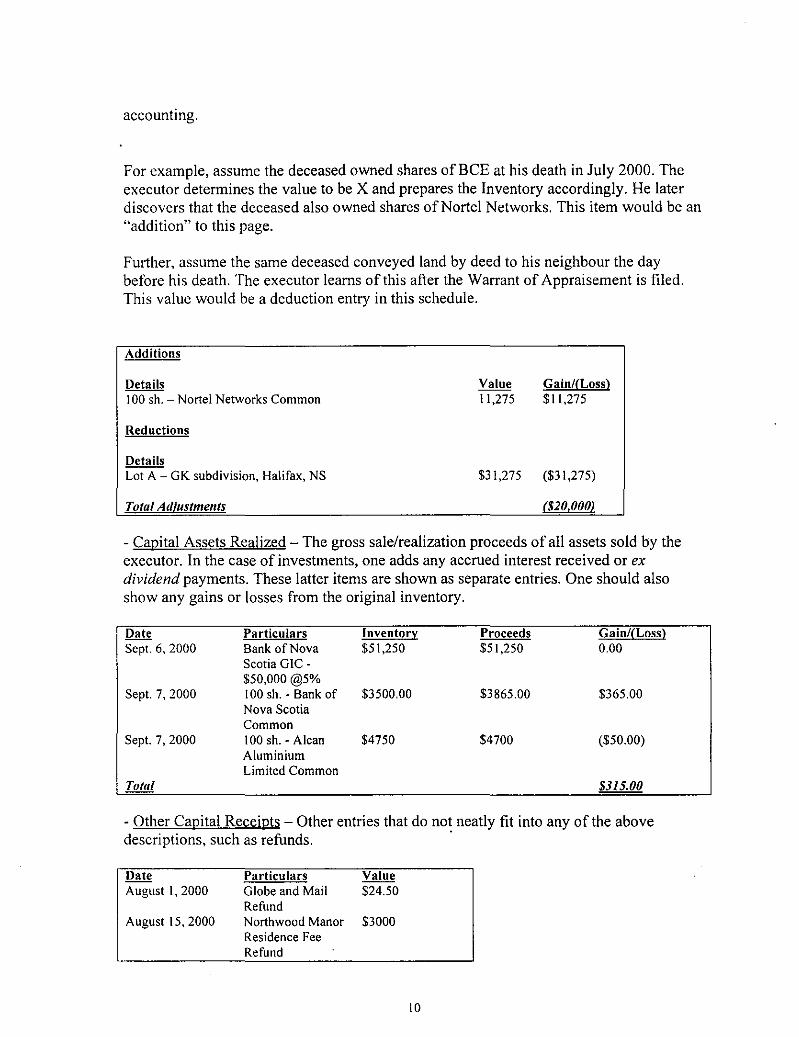

- Adjustments to Inventory - It is not uncommon for an executor to become aware of assets or subsequent owners of assets after the filing of the Inventory and Warrant of Appraisement. Further, estimated values may be found to be incorrect. This entry allows the executor to reconcile any differences between the original inventory and the final

20 supra note 6, p.4D.

9

accounting.

For example, assume the deceased owned shares ofBCE at his death in July 2000. The executor determines the value to be X and prepares the Inventory accordingly. He later discovers that the deceased also owned shares of Norte I Networks. This item would be an "addition" to this page.

Further, assume the same deceased conveyed land by deed to his neighbour the day before his death. The executor learns of this after the Warrant of Appraisement is filed. This value would be a deduction entry in this schedule.

Additions

Details 100 sh. - Nortel Networks Common

Reductions

Details Lot A - OK subdivision, Halifax, NS

Total Adjustments

Value 11,275

Gain/fLoss) $11,275

$31,275 ($31,275)

($20.000)

- Capital Assets Realized - The gross sale/realization proceeds of all assets sold by the executor. In the case of investments, one adds any accrued interest received or ex dividend payments. These latter items are shown as separate entries. One should also show any gains or losses from the original inventory.

Date Particulars Inventor~ Proceeds Gain/(Loss} Sept. 6, 2000 Bank of Nova $51,250 $51,250 0.00

Scotia OlC-$50,000@5%

Sept. 7. 2000 100 sh. - Bank of $3500.00 $3865.00 $365.00 Nova Scotia Common

Sept. 7, 2000 100 sh. - Alean $4750 $4700 ($50.00) Aluminium Limited Common

Totlll $315.00

- Other Capital Receipts - Other entries that do not neatly fit into any of the above descriptions, such as refunds. .

Date August 1.2000

August 15,2000

Particulars o lobe and Mail Refund Northwood Manor Residence Fee Refund

Value $24.50

$3000

10

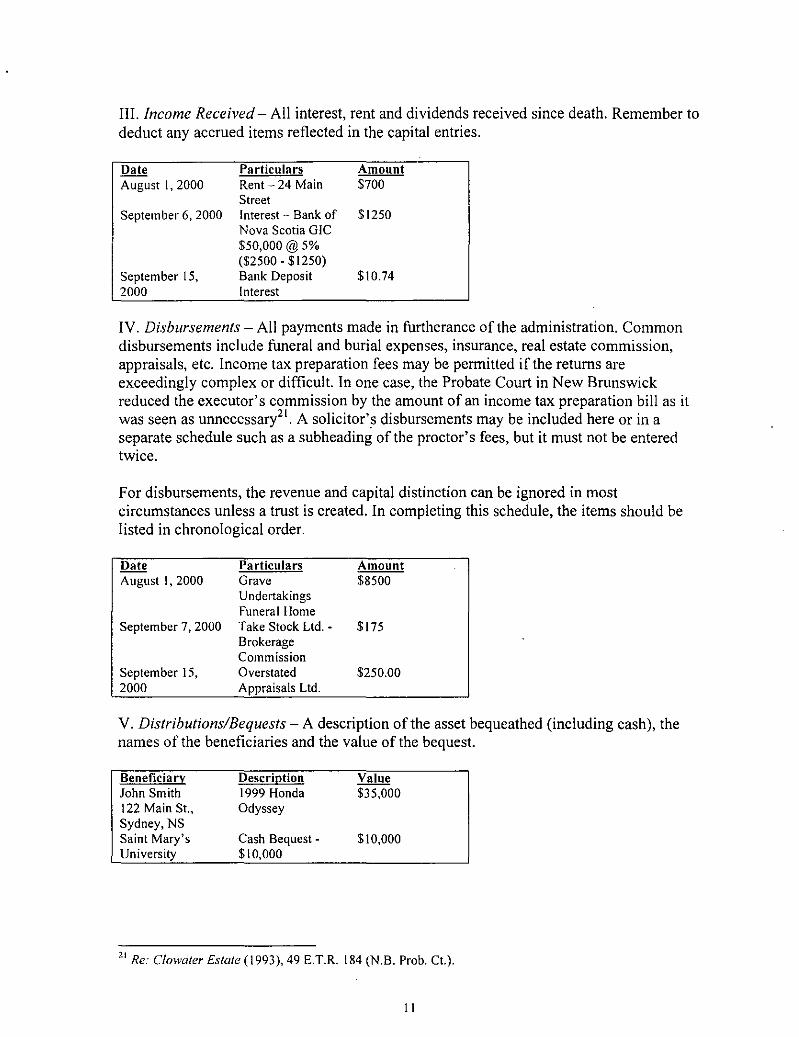

III. Income Received - All interest, rent and dividends received since death. Remember to deduct any accrued items reflected in the capital entries.

Date Particulars Amount August I, 2000 Rent - 24 Main $700

Street September 6, 2000 Interest - Bank of $1250

Nova Scotia OIC $50,000@5% ($2500 - $1250)

September 15, Bank Deposit $10.74 2000 Interest

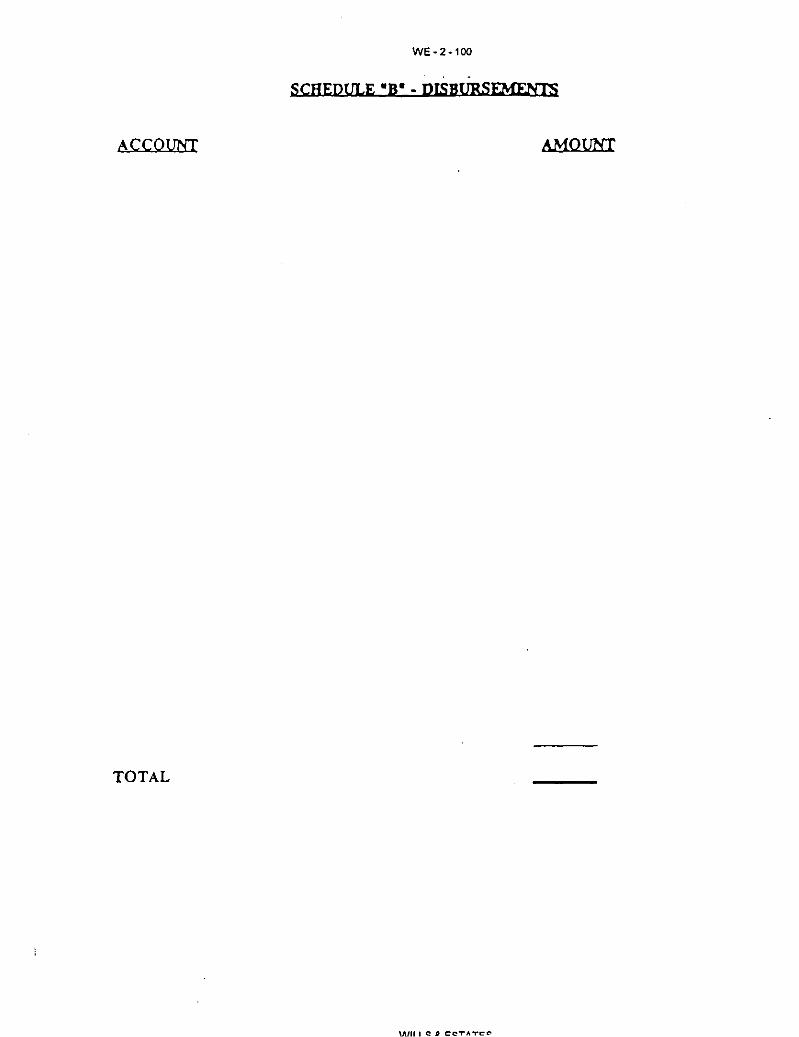

IV. Disbursements - All payments made in furtherance of the administration. Common disbursements include funeral and burial expenses, insurance, real estate commission, appraisals, etc. Income tax preparation fees may be permitted if the returns are exceedingly complex or difficult. In one case, the Probate Court in New Brunswick reduced the executor's commission by the amount of an income tax preparation bill as it was seen as unnecessarll. A solicitor's disbursements may be included here or in a separate schedule such as a subheading of the proctor's fees, but it must not be entered twice.

For disbursements, the revenue and capital distinction can be ignored in most circumstances unless a trust is created. In completing this schedule, the items should be listed in chronological order.

Date Particulars Amount August I, 2000 Grave $8500

Undertakings Funeral Home

September 7, 2000 Take Stock Ltd. - $175 Brokerage Commission

September 15, Overstated $250.00 2000 Appraisals Ltd.

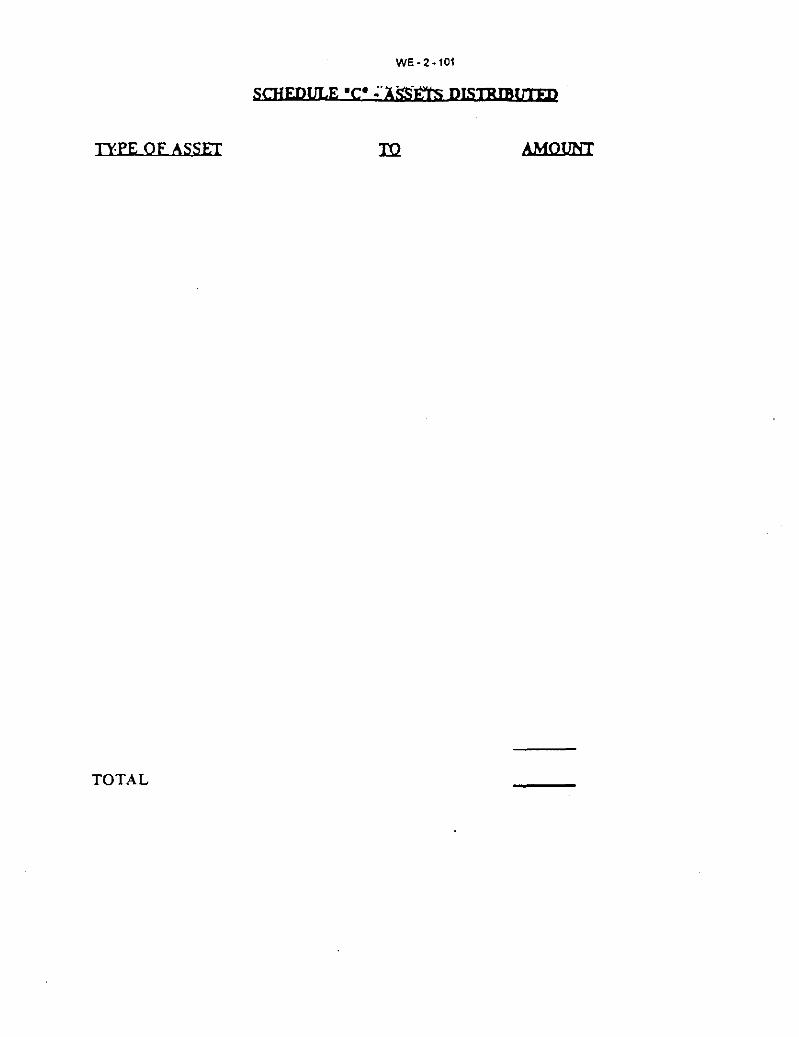

V. Distributions/Bequests - A description of the asset bequeathed (including cash), the names of the beneficiaries and the value of the bequest.

Beneficiary DescriQtion Value John Smith 1999 Honda $35,000 122 Main St., Odyssey Sydney, NS Saint Mary's Cash Bequest - $10,000 University $10,000

21 Re: Clowater Estate (1993),49 E.T.R. 184 (N.B. Prob. Ct.).

11

Supporting Documentation

Section 74(2) of the Probate Act requires an executor to produce vouchers and receipts for all debts, legacies and expenses. Subsection (3) provides that, in the absence of a voucher, any expenses may be proven by sworn evidence. Thus, it is common practice to file vouchers at the same time as the accounts are filed. Please note that local practice varies in each Probate District. For example, some Registrars insist on copies of all statements showing the assets in the hands of the deceased while others view them only when challenged as they have already appeared on the Inventory. However, the following suggestions may be helpful in assembling the vouchers:

1) Keep all vouchers and statements in order and separate from the ordinary correspondence of the estate - More than one lawyer has told a story of executor/clients appearing at their offices with a shoebox of receipts. Simple chronological filing of these items will help maintain order for easy preparation of accounts. If they are mixed in with correspondence, they become easy to miss.

2) Vouchers should be tabbed andfiled in the order in which they appear in the accounting.

3) Distributions made pursuant to an Order of another Court should be supported by a Certified Copy of that Order - For example, where relief is granted against the estate under the Testators' Family Maintenance Act or Matrimonial Property Act by the Supreme Court, the Civil Procedure Rules do not contain any provision that I am aware of requiring those orders to be filed with the Probate Court. At a minimum, a certified copy should accompany the accounting. In the appropriate schedule, one should show a breakdown of the amount paid inclusive of pre judgement and post judgement interest and costs. Obviously, a receipt from the other side (or ifregistered, a Certificate of Satisfaction) should also be obtained. In many instances, you may choose to file the certified copy before the estate is closed ..

12 Specific Legacies should be accompanied by Receipts and Releases.

~ Bring all quotes for services to the Closing - Sometimes, several quotes are obtained for various services during the administration. Since discretionary costs could be challenged, a prudent executor should bring all other quotes to the Closing to support hislher decision. Further, a voucher for services should provide sufficient detail of the service provided to address any questions of reasonableness.

Ql Clearance Certificate - It is common to close Probate before Final Clearance has been issued. The Final Decree is then issued, subject to any claims for income tax by the Canada Customs and Revenue Agency. While not specifically an item for the accounting, if Clearance has been issued, it is good practice to bring the Clearance Certificate with you to the closing.

12

V. Executor and Trustee Fees

Sections 76 and 77 of the Probate Act stipulate as follows:

76. In the settlement of any estate the executors may be allowed over and above all such actual and necessary expenses, as appear just and reasonable, a commission not exceeding five per cent on the amount received by them, and the court further may apportion such commission among the executors and administrators as appears just and proper, according to the labour bestowed or responsibility incurred by them respectively.

77. When any provision is made by any will for specific compensation to an executor, the same shall be deemed a full satisfaction for his services in lieu of any commission, or his share thereof, unless such executor, within twelve months from the date of probate, by declaration under his hand filed with the registrar, renounces all claim to such specific compensation.

These sections give the Registrar the discretion to award fees of up to 5% of the total value of the estate to be split among all of the executors. Section 77 authorizes the testatrix to provide specific compensation to her executor by will unless the beneficiary renounces any claim to it. When a trust company is appointed, the testatrix normally incorporates a compensation agreement in her will. In any case, there is no entitlement to payment of any remuneration until authorized by the court22

.

In exercising her discretion, the Registrar may refer to the test found in Re: Toronto General Trust and Central Ontario Railway (1905),6 O.W.R. 350 where the following factors were considered relevant:

the size of the trust;

the care and responsibility involved;

the time occupied in performing duties;

the skill and ability shown; and

the success resulting from administration.

2' - Adams Estate v. Keough (1993),119 N.S.R (2d) 235 (S.C.-T.D.).

13

Reference is made to the cases of Re: Forbes Estate23 and Re: Chappell Estat/' for a discussion on the Probate Courts' approach to setting executors' compensation.

Please note that an executor's fee is reduced when a loss occurs on realization of the assets, in that the lesser value is used to calculate the percentage in s. 76. For real property, executor's commission is reduced by any registered encumbrances25

.

VI. Proctors' Fees

As with executors' commission, Registrars have the duty to tax reasonable fees and disbursements charged by a proctor of an estate26

. Local practice may result in different fees being awarded. Some Registrars award compensation using a scale of fees while others prefer an hourly rate method similar to that used by a Taxing Master of the Supreme Court.

A solicitor can be compensated for acting as both a proctor and executor. 27

Further, a solicitor who is a co-executor may charge solicitors fees with the consent of the other co-executor(s) provided that no such charge is made for services where a solicitor is not ordinarily required28

. Justice Wright of the Nova Scotia Supreme Court recently reviewed the duties and standards to be applied in Bruhm v. Feindei et ai. 29

VII. Professional Responsibilitv Concerns

As in other matters, a solicitor should be aware of the provisions of the "Legal Ethics Handbook" most of which can reasonably apply to hirnlher in any estate. In addition to the statutory provisions previously cited, there are already rules in place specifically aimed at executors and proctors. 30

VIII. Trust Accountabilitv - A Few Observations

The following personal observations and suggestions apply to any executor, although the use of each will vary with the circumstances.

1) Adequate disclosure to beneficiaries is paramount - Dissatisfaction is minimized and decisions are more readily accepted when beneficiaries are kept up to date on the progress of the estate. For example, trust

23 (1992), 116 N.S.R. (2d.) 227. 24 (1991),110 N.S.R. (2d) 361. " Probate Act, s. 130(2). 26 Probate Act, s. 129. 27 Civil Procedure Rule 62.23 28 Trustee Act. s.63 29 supra Note 8. 30 See for example, Rule 7R(f), 7.3 and Rule 9 (Protecting Clients' Propenyl

14

companies typically provide financial statements on a monthly basis during its administration. Further, providing clients with regular progress reports is also useful.

2) Exercises of discretion should be documented - Any discretion empowered by the will or by statute should be carefully documented with memos and corroborating sources. For example, the sale of a parcel of land should be accompanied by the report of one or several appraisers and, if the property is to be listed, a listing opinion from a realtor.

3) Develop checklists and precedents.

4) Solicitors' and Executors' Disbursements should be tracked separately.

5) Estates should be maintained in separate accounts.

6) Be aware of deadlines prescribed under the various legislation.

7) Follow the will.

8) Consider using a trust company - Trust companies are objective and are not typically confronted with the same conflicts of interest as one may find in practice. Therefore, when taking instructions from clients for a Will, you may encounter situations where a trust company is a logical choice as an executor or co-executor. Further, if you or your client are named an executor and do not wish to contend with the "legwork" involved, it is possible to hire a trust company as your agent to assist in the administration.

IX. Conclusion

The law as it relates to passing accounts has evolved in Nova Scotia. It has always been the "bounden duty" of an executor to account to his beneficiaries although there is considerable debate over whether an executor is obliged to formally close Probate and pass accounts. Lawyers who have traditionally acted as executors for clients have been subject to a number of statutory and professional obligations. Regulation 47(1) has mandated more thorough disclosure by solicitors when acting as a proctor or fiduciary. Thus, members of the legal profession in Nova Scotia must scrutinize their estate practices carefully in order to comply with this new regulation.

Regardless of how the profession chooses to meet these standards, it is clear that a new expectation of this role has been imposed upon us. It is

15

critical that our responsibility to the public as a self-governing profession be evident through this accountability which brings with it greater expectations of a solicitor and his or her estate practice. While this paper is, by no means, an exhaustive commentary or remedy, I hope it has helped place the duty to account in its perspective and provided some guidance to help you meet this new responsibility.

16

33 WE·2·98

IN THE COURT OF PROBATe I COUNTY OF HALIFAX SS")

IN TIlE ESTATE OF 1 DECEASED

fiNAL ACCOUNT OF I, EXECUTORJAD,\IL'iISTRATOR OF TIlE ESTATE OF I

SUMMARY

fNVENTORY

Adjustments to Inventory •

Additions

Deductions

Adjusted Inventory Value

Income Receipts per Schedule" A"

TOTAL VALUE

Less value o( realty devised direct to beneficiary or devolvJng on an imesLlcy

VALUE ADMINISTERED BY EXEClIT#

DISBURSEMENTS

Disbursements per Schedule "B" 51

Assets distributed per Schedule "C"51

BALANCE ON HAND BEFORE CLOSING

Registrar o( Probate· Fees on Closing

ExecutA"s CommisstOn 51

Solicitor's Fees & Disbursemen[s·

CLOSING EX PE:'<SES

51

BALANCE FOR DISTRJBUTION

Reserve if indicated

Attested CiaJms

" Solicitor's Disbursements· ,cc ,c=8Te-u (Record Only)

$1

$#

$1

$#

51

51

S#

Real Property

Personal Property

Adjustments to Inventory

Additions -

Deductions -

WE-2-99

INYF.NTORY INCOME

WE·2·100

SCHEDULE "B" - pISBURSEMENTS

ACCOUNT AMOUNT

TOTAL

WE-2-101

SCHEDULE ·C· ~':\SS-m DISTBmurm

TYPE OF ASSET AMOUNT

TOTAL

WE·2·102

SCHEDULE ·D· - SOLICITOR'S DISBURSEMENTS

(Record Onl y)

Executors' Duty to Account (Presentation Notes)

Gregg W. Knudsen Will and Estate Planning Officer

Scotiatrust Suite 900

1801 Hollis Street Halifax; NS, B3J 3N4

Telephone: (902) 420-2296 Fax: (902) 420-7119

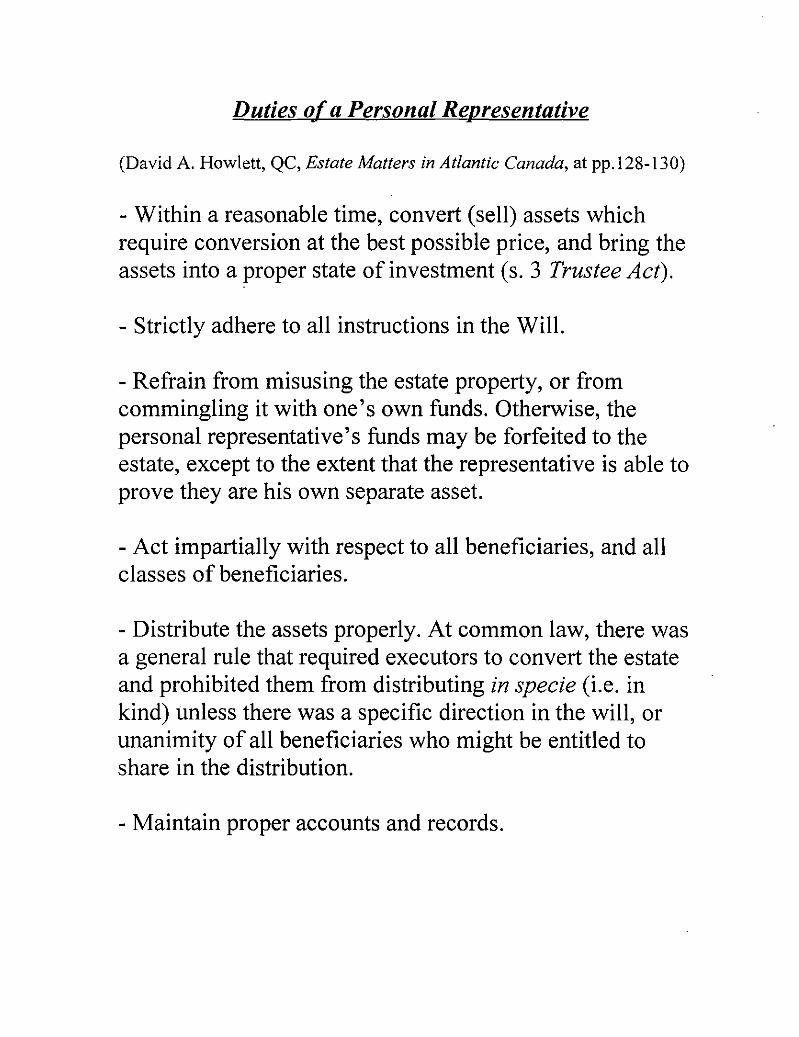

Duties of a Personal ReDresentative ~ ~

(David A. Howlett, QC, Estate Matters in Atlantic Canada, at pp.128-130)

- Within a reasonable time, convert (sell) assets which require conversion at the best possible price, and bring the assets into a proper state of investment (s. 3 Trustee Act).

- Strictly adhere to all instructions in the Will.

- Refrain from misusing the estate property, or from commingling it with one's own funds. Otherwise, the personal representative's funds may be forfeited to the estate, except to the extent that the representative is able to prove they are his own separate asset.

- Act impartially with respect to all beneficiaries, and all classes of beneficiaries.

- Distribute the assets properly. At common law, there was a general rule that required executors to convert the estate and prohibited them from distributing in specie (Le. in kind) unless there was a specific direction in the will, or unanimity of all beneficiaries who might be entitled to share in the distribution.

- Maintain proper accounts and records.

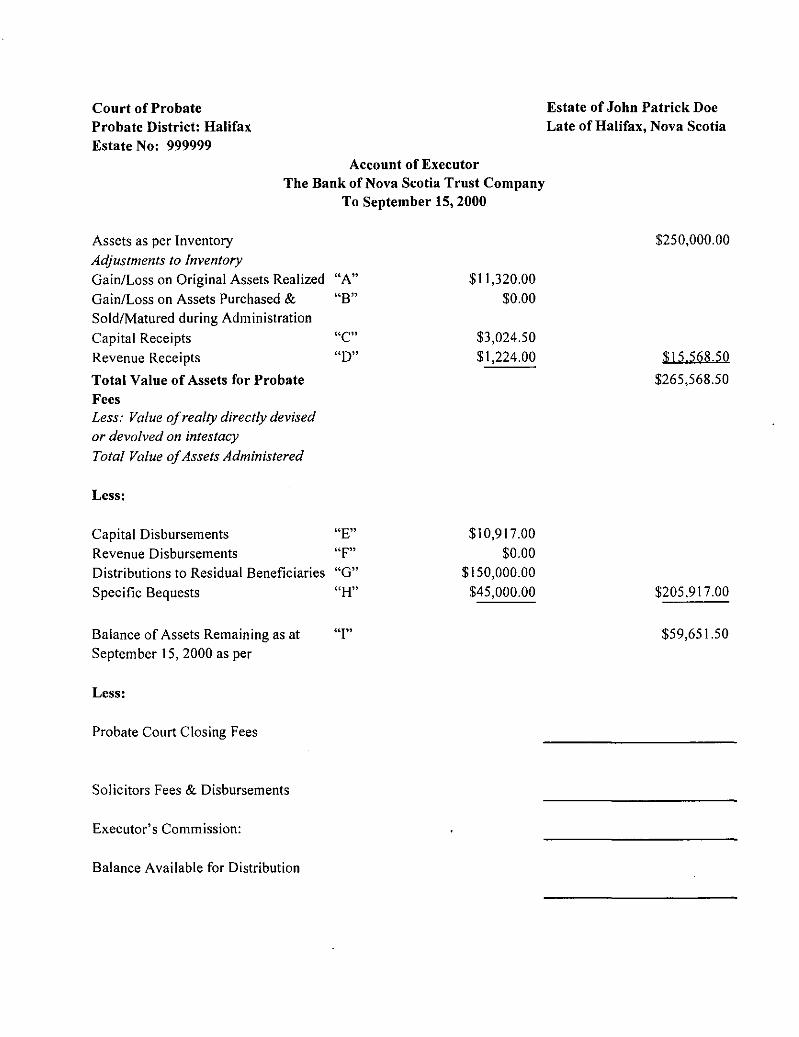

Court of Probate Probate District: Halifax Estate No: 999999

Account of Executor The Bank of Nova Scotia Trust Company

To September 15,2000

Assets as per Inventory Adjustments to Inventory Gain/Loss on Original Assets Realized "A" Gain/Loss on Assets Purchased & "B" Sold/Matured during Administration Capital Receipts Revenue Receipts

Total Value of Assets for Probate Fees Less: Value of realty directly devised or devolved on intestacy

Total Value of Assets Administered

Less:

"C" "D"

Capital Disbursements "E" Revenue Disbursements "F" Distributions to Residual Beneficiaries "G"

Specific Bequests "H"

Balance of Assets Remaining as at September 15,2000 as per

Less:

Probate Court Closing Fees

Solicitors Fees & Disbursements

Executor's Commission:

Balance Available for Distribution

"I"

$11,320.00 $0.00

$3,024.50 $1,224.00

$10,917.00 $0.00

$150,000.00 $45,000.00

Estate of John Patrick Doe Late of Halifax, Nova Scotia

$250,000.00

$15.568.50

$265,568.50

$205,917.00

$59,651.50

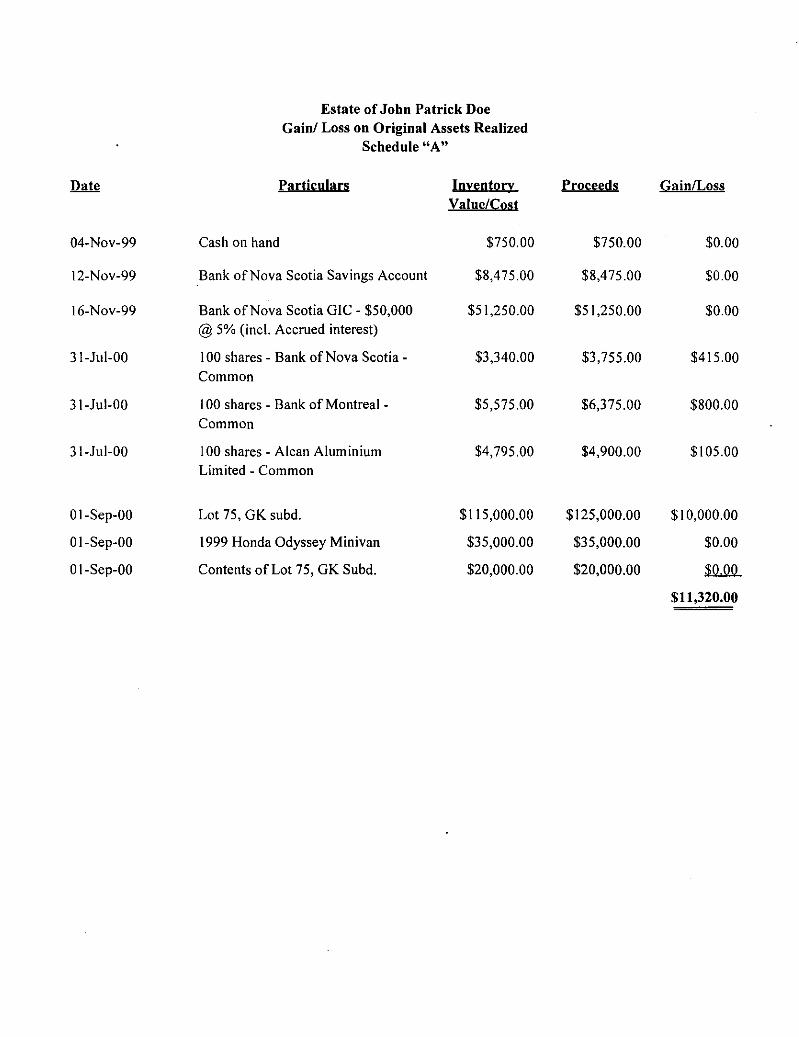

Estate of John Patrick Doe Gain/ Loss on Original Assets Realized

Schedule "A"

Date Particulars IDl:~DtIlO: Pro~~g!ls GainlLos~

ValUe/ellst

04-Nov-99 Cash on hand $750.00 $750.00 $0.00

12-Nov-99 Bank of Nova Scotia Savings Account $8,475.00 $8,475.00 $0.00

16-Nov-99 Bank of Nova Scotia GIC - $50,000 $51,250.00 $51,250.00 $0.00 @ 5% (incl. Accrued interest)

31-Jul-00 100 shares - Bank of Nova Scotia- $3,340.00 $3,755.00 $415.00 Common

31-Jul-00 100 shares - Bank of Montreal - $5,575.00 $6,375.00 $800.00 Common

31-Jul-00 100 shares - Alcan Aluminium $4,795.00 $4,900.00 $105.00 Limited - Common

Ol-Sep-OO Lot 75, GK subd. $115,000.00 $125,000.00 $10,000.00

Ol-Sep-OO 1999 Honda Odyssey Minivan $35,000.00 $35,000.00 $0.00

Ol-Sep-OO Contents of Lot 75, GK Subd. $20,000.00 $20,000.00 RQQ..

$11,320.00

Date Purchased

23-Dec-99

Ol-Aug-OO

Ol-Aug-OO

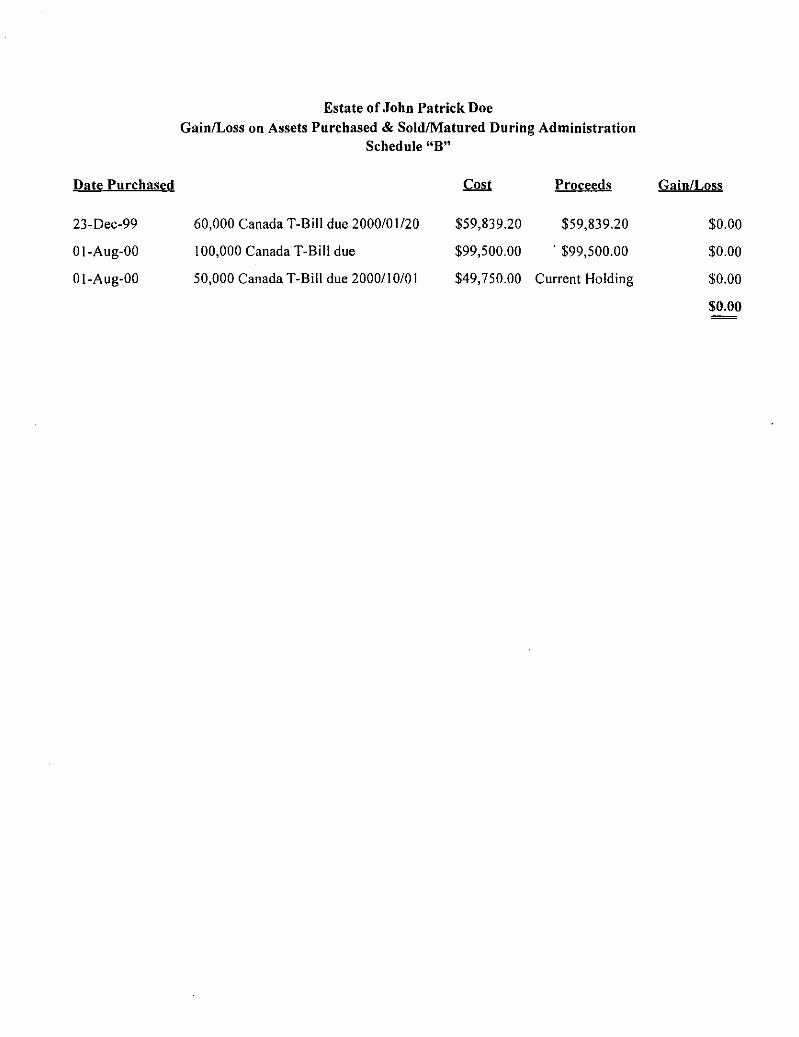

Estate of John Patrick Doe GainlLoss on Assets Purchased & SoldlMatured During Administration

Schedule "B"

60,000 Canada T-Bill due 2000101/20

100,000 Canada T-Bill due

50,000 Canada T-Bill due 2000110101

CQll

$59,839.20

$99,500.00

$49,750.00

Proceeds

$59,839.20

. $99,500.00

Current Holding

GainlLoss

$0.00

$0.00

$0.00

$0.00 =

Date

Ol-Aug-OO

15-Aug-00

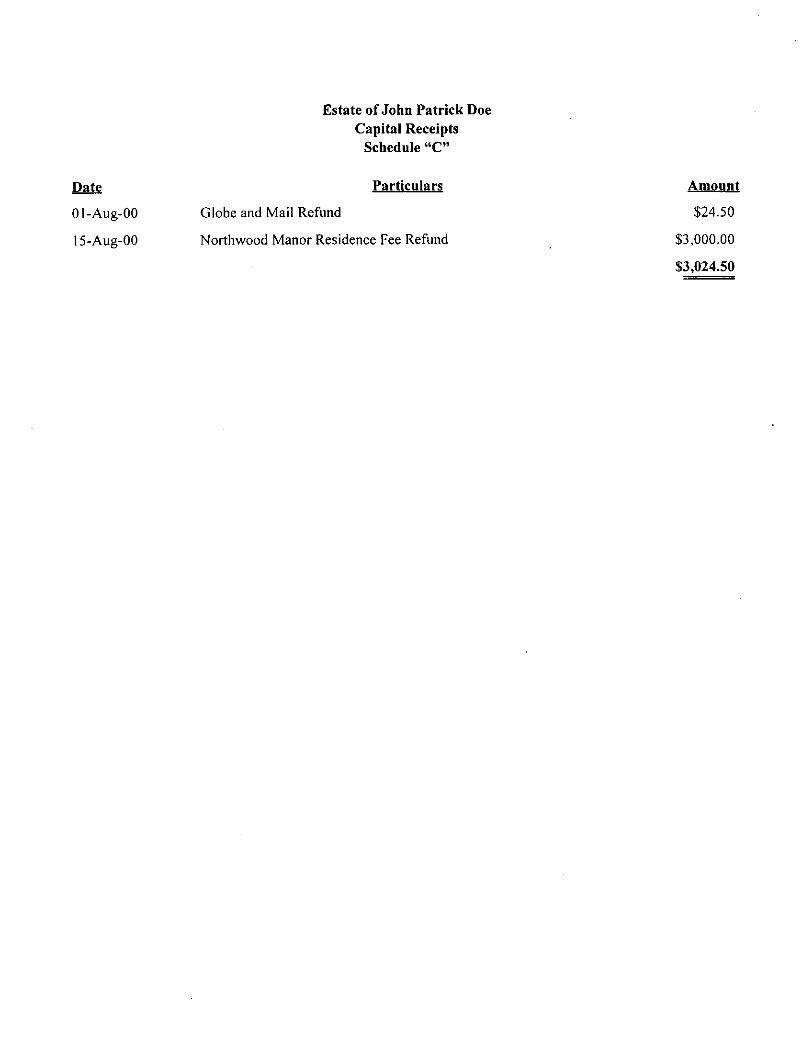

Estate of John Patrick Doe Capital Receipts

Schedule "C"

Particulars

G lobe and Mail Refund

Northwood Manor Residence Fee Refund

Amount

$24,50

$3,000,00

$3,024.50

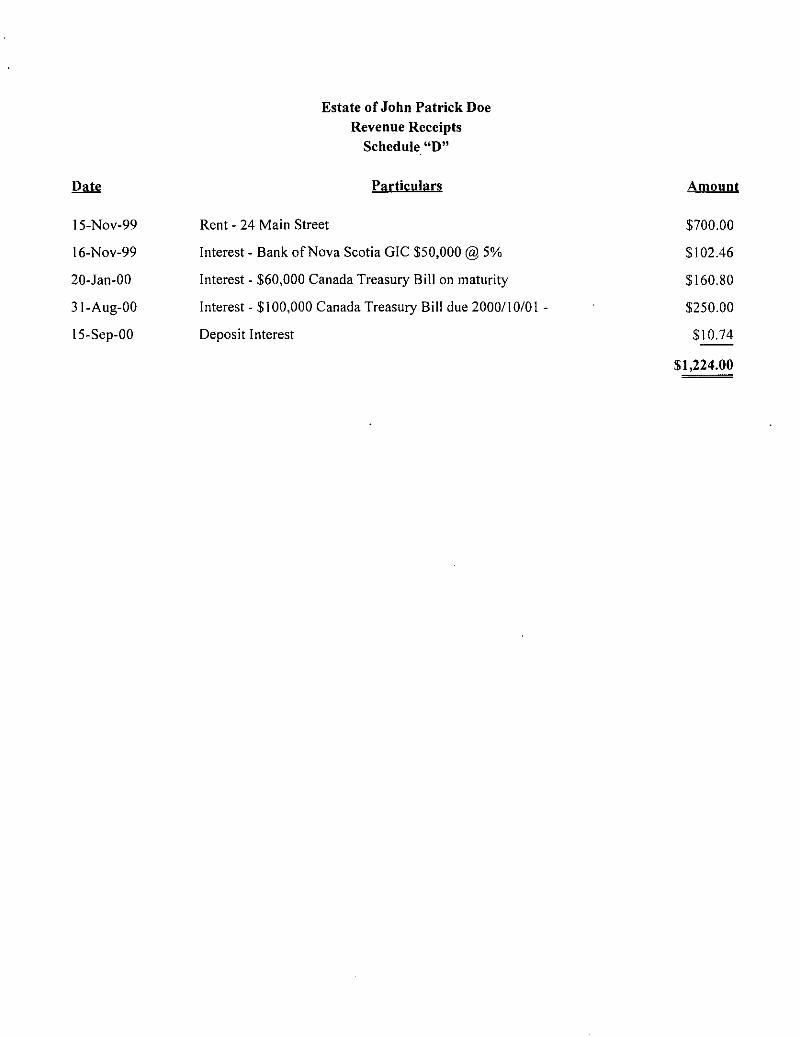

15-Nov-99

16-Nov-99

20-Jan-00

31-Aug-00

15-Sep-00

Estate of John Patrick Doe Revenue Receipts

Schedule "D"

Particulars

Rent - 24 Main Street

Interest - Bank of Nova Scotia OIC $50,000 @ 5%

Interest - $60,000 Canada Treasury Bill on maturity

Interest - $100,000 Canada Treasury Bill due 200011 010 I -

Deposit Interest

Amount

$700.00

$102.46

$160.80

$250.00

$10.74

$1,224.00

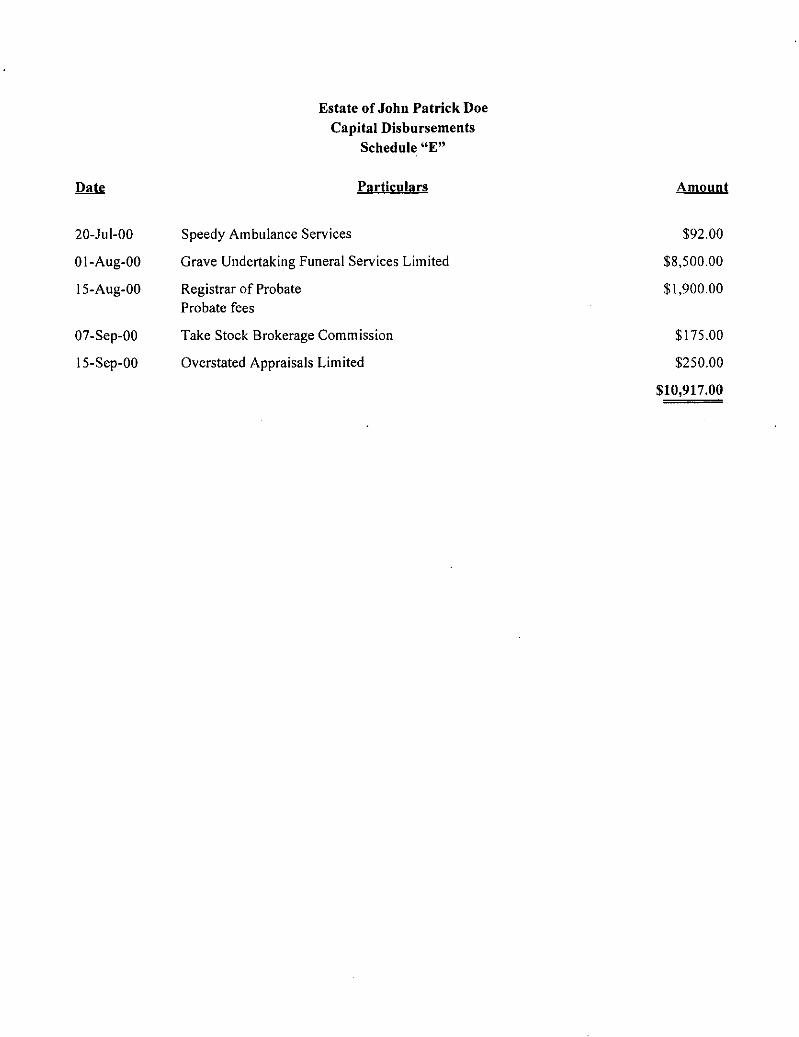

20-Jul-00

Ol-Aug-OO

15-Aug-00

07-Sep-00

15-Sep-00

Estate of John Patrick Doe Capital Disbursements

Schedule "E"

Particulars

Speedy Ambulance Services

Grave Undertaking Funeral Services Limited

Registrar of Probate Probate fees

Take Stock Brokerage Commission

Overstated Appraisals Limited

Amount

$92.00

$8,500.00

$1,900.00

$175.00

$250.00

$10,917.00

Date

Nil

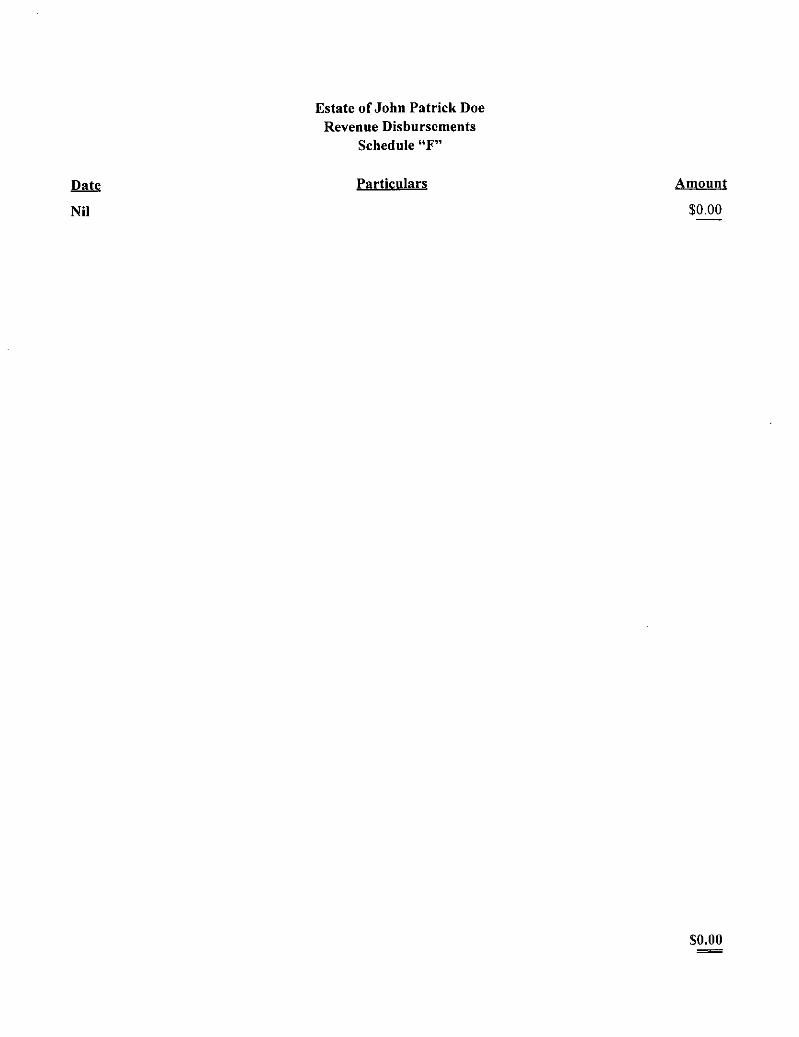

Estate of John Patrick Doe Revenue Disbursements

Schedule "F"

Particulars Amount

$0.00

so.oo =

Date

Ol-Sep-OO

Ol-Sep-OO

Ol-Sep-OO

20-Dec-99

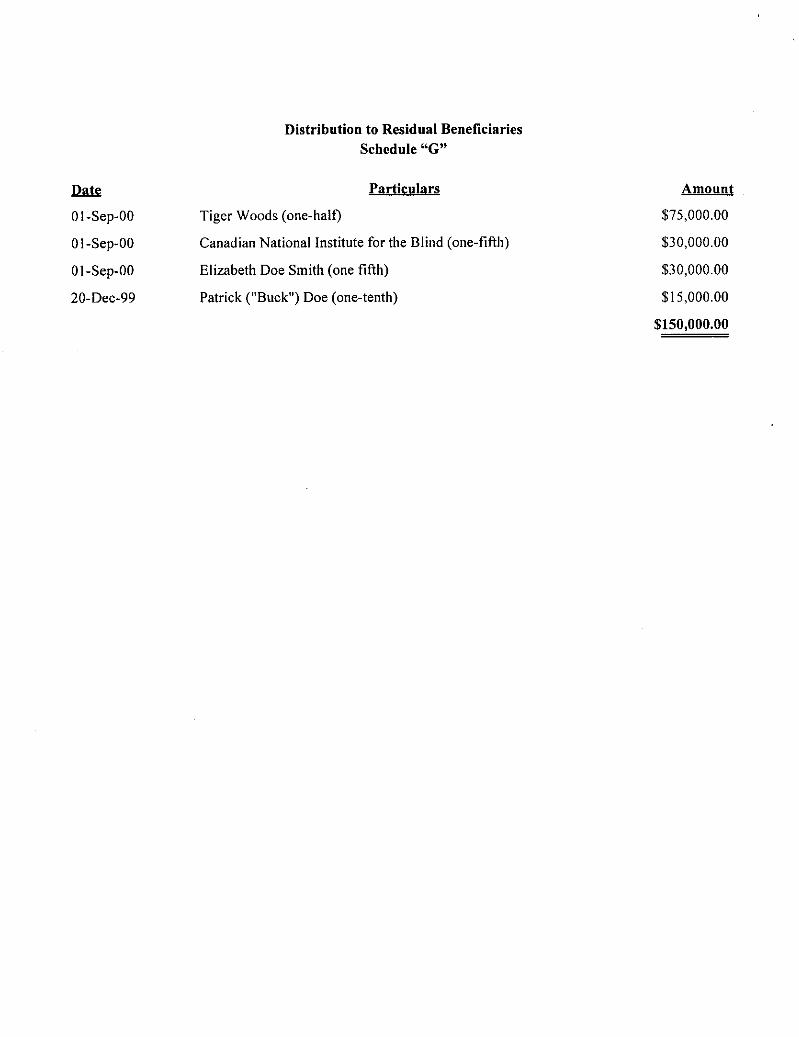

Distribution to Residual Beneficiaries Schedule "G"

Particulars

Tiger Woods (one-halt)

Canadian National Institute for the Blind (one-fifth)

Elizabeth Doe Smith (one fifth)

Patrick ("Buck") Doe (one-tenth)

Amount

$75,000.00

$30,000.00

$30,000.00

$15,000.00

$150,000.00

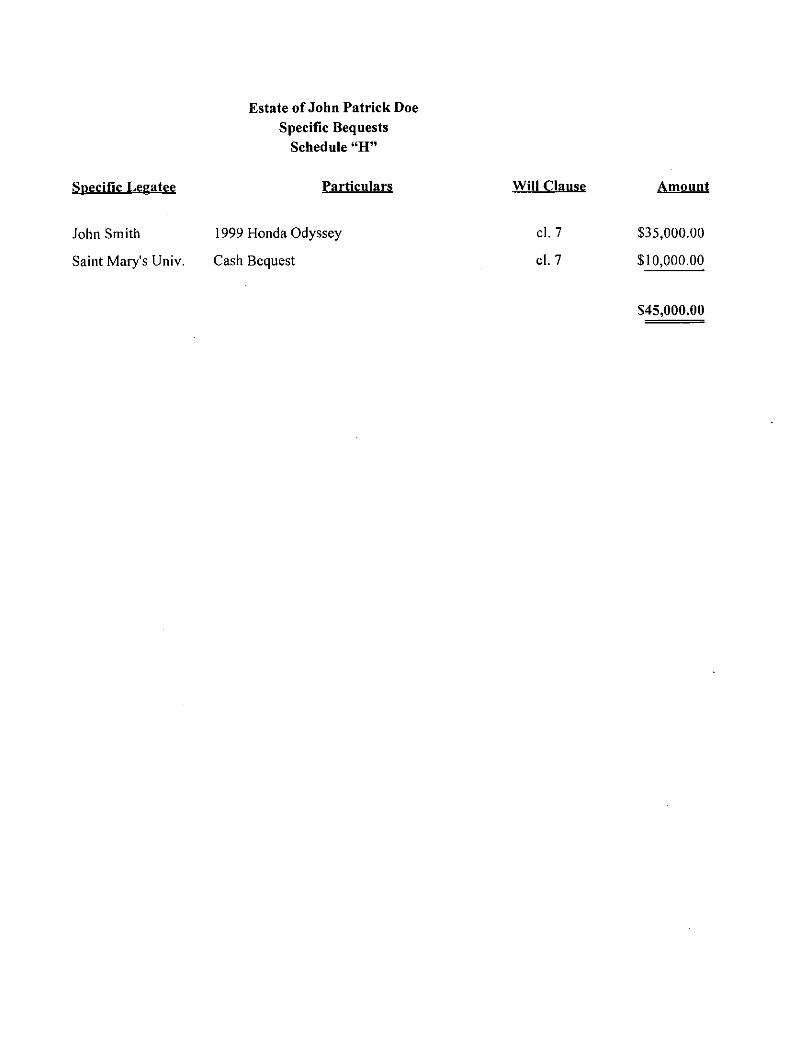

Specific Legatee

John Smith

Saint Mary's Univ.

Estate of John Patrick Doe Specific Bequests

Schedule "H"

Particulars

1999 Honda Odyssey

Cash Bequest

Will Clause

cl. 7

cl. 7

Amount

$35,000.00

$10,000.00

$45,000.00

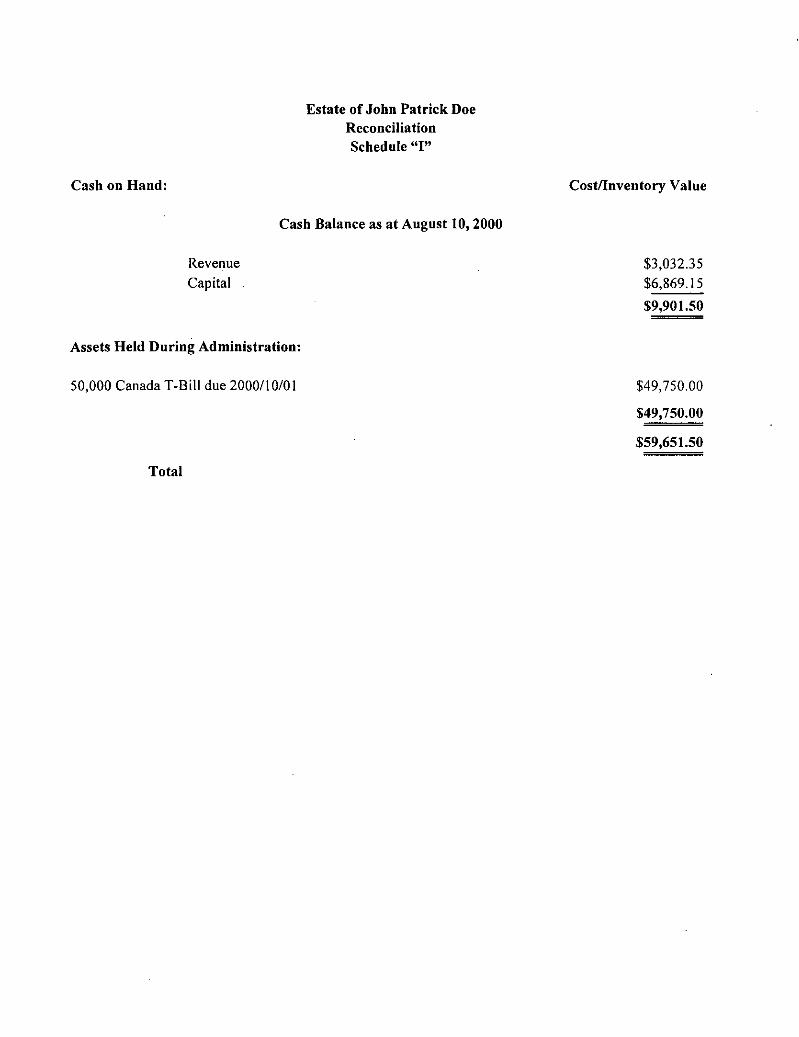

Cash on Hand:

Estate of John Patrick Doe Reconciliation Schedule "I"

Cash Balance as at August 10,2000

Revenue Capital

Assets Held During Administration:

50,000 Canada T-Bill due 2000/10/01

Total

Costllnventory Value

$3,032.35 $6,869.15

$9,901.50

$49,750.00

$49,750.00

$59,651.50