Embed Size (px)

Citation preview

EXECUTIVE TRAINING COMPANY(INTERNATIONAL) LTD

YOUR SITE HERE

LOGO

HKICPA Module B Seminar

Module Preparation Seminar onMajor or Difficult Syllabus Topics (Part I)

-Ethics, executive management and management reporting

YOUR SITE HERE

LOGO

About the Lecturer

www.etctraining.com.hk

More than 10 years working experience in managerial role

Currently working in an overseas bank

Notes writer, HKICPA speaker, QP marker and Mentor

A qualified Enhanced QP facilitator in the HKICPA

Regular speaker for HKICPA’s seminar

A mentor under a mentorship programme in a well-known professional accountancy body

Mr William Ng (MB, FE (MB))ACA (UK), FCCA and FCPA, Master of Accountancy,Master of Corporate Finance, BA (Business Studies)

YOUR SITE HERE

LOGO

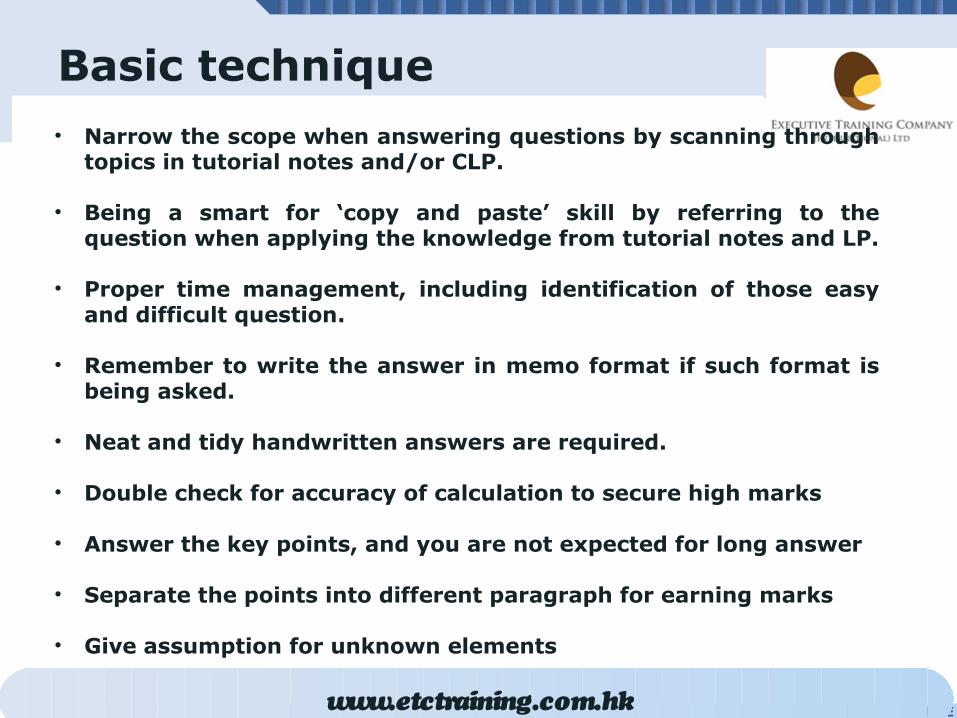

Basic technique• Narrow the scope when answering questions by scanning through

topics in tutorial notes and/or CLP.

• Being a smart for ‘copy and paste’ skill by referring to the question when applying the knowledge from tutorial notes and LP.

• Proper time management, including identification of those easy and difficult question.

• Remember to write the answer in memo format if such format is being asked.

• Neat and tidy handwritten answers are required.

• Double check for accuracy of calculation to secure high marks

• Answer the key points, and you are not expected for long answer

• Separate the points into different paragraph for earning marks

• Give assumption for unknown elements

www.etctraining.com.hk

YOUR SITE HERE

LOGO

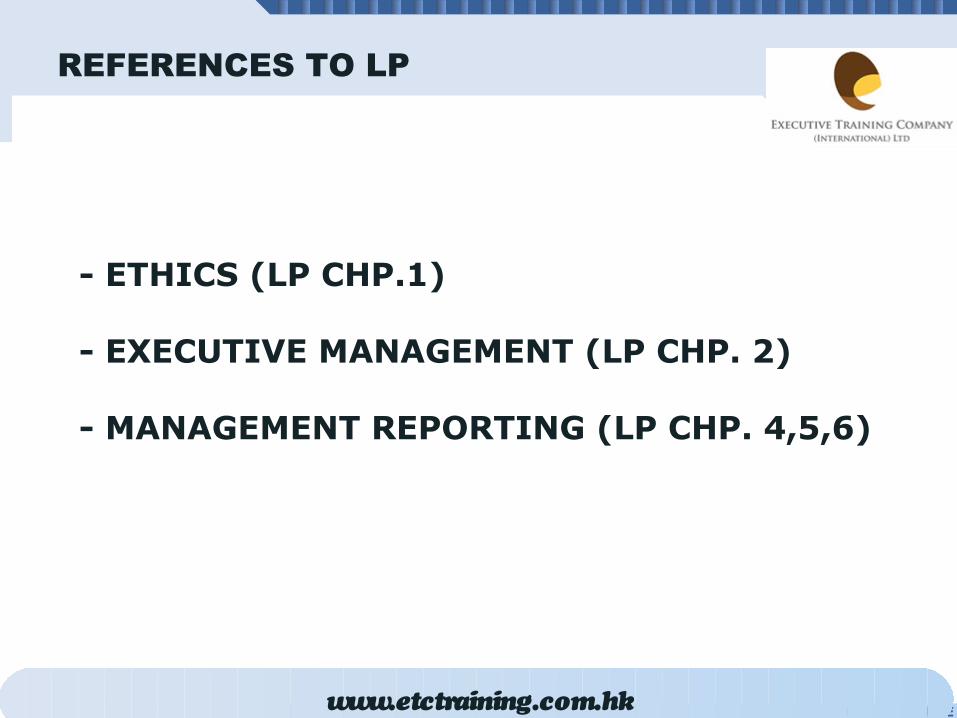

- ETHICS (LP CHP.1)

- EXECUTIVE MANAGEMENT (LP CHP. 2)

- MANAGEMENT REPORTING (LP CHP. 4,5,6)

www.etctraining.com.hk

REFERENCES TO LP

YOUR SITE HERE

LOGO

ETHICS (LP CHP.1)

www.etctraining.com.hk

FIRST TOPIC

YOUR SITE HERE

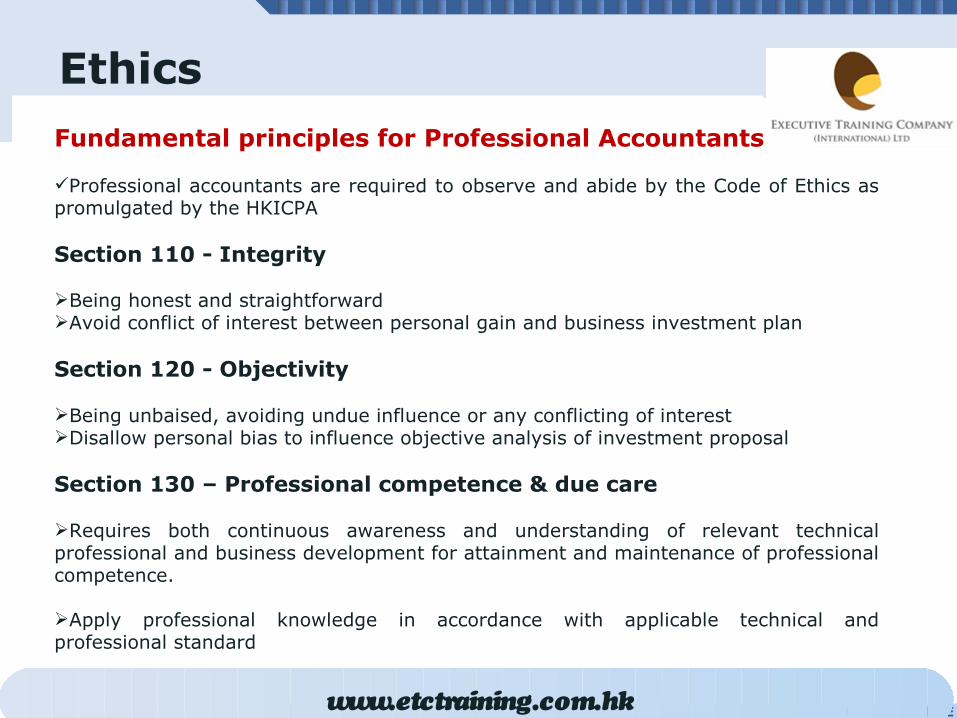

LOGOEthicsFundamental principles for Professional Accountants

Professional accountants are required to observe and abide by the Code of Ethics as promulgated by the HKICPA

Section 110 - Integrity

Being honest and straightforwardAvoid conflict of interest between personal gain and business investment plan

Section 120 - Objectivity

Being unbaised, avoiding undue influence or any conflicting of interestDisallow personal bias to influence objective analysis of investment proposal

Section 130 – Professional competence & due care

Requires both continuous awareness and understanding of relevant technical professional and business development for attainment and maintenance of professional competence.

Apply professional knowledge in accordance with applicable technical and professional standard

www.etctraining.com.hk

YOUR SITE HERE

LOGOEthics

Section 140 - Confidentiality

Respect confidentiality of information.Largely related to the case of insider dealing.

Section 150 – Professional behaviour

Abide by all laws, rules and regulationAvoid any actions that discredits the professional

www.etctraining.com.hk

YOUR SITE HERE

LOGOEthics

Ethical model – The American Accounting Association Model (7-steps)

Determine the facts

Define the ethical issues

Identify the major principles, rules and values

Specify the alternatives

Compare values and alternatives

Assess the consequences

Make your decision

www.etctraining.com.hk

YOUR SITE HERE

LOGOEthics

QP exam topic related to Ethics

Insider dealing

The trading of a corporation’s stocks or other securities (e.g. bonds or stock options) by individuals with potential access to non-public information about the company.

Relevant code of ethics to breach

Integrity

Objectivity

Confidentiality

Professional behaviour

P.S. Also consider violating the law

www.etctraining.com.hk

YOUR SITE HERE

LOGOEthicsQP exam topic related to Ethics

Fraud accounting

Overstate the profit in order to improve the profitability and liquidity of the company for ease to access of credit facility

Relevant code of ethics to breach

Integrity

Objectivity

Professional competence & due care

Professional behaviour

www.etctraining.com.hk

YOUR SITE HERE

LOGOEthics

Corporate social responsibility (CSR) and sustainable reporting

Definition : CSR is operating a business in a manner that meets or exceeds the ethical, legal, commercial and public expectations that society has of business. It is the way in which organizations achieve sustainable developments.

Benefits of pursuing CSR

Lower cost base from being energy efficient

Opportunities to attract ethical customers

Increase staff loyalty and morale

Protection or enhancement of reputation

Retention of licences to operate

Competitive advantage

Development in technology which improve the economies of alterative energy might generate opportunities to develop new business

www.etctraining.com.hk

YOUR SITE HERE

LOGOEthics

Corporate social responsibility (CSR) and substainability reporting

Also named as ‘social and environmental reporting’ and ‘sustainability reporting’

Linked in conjunction with triple bottom line reports (TBL)

TBL provides a quantitative summary of a corporation’s performance over a previous time period in terms of its economic or financial impact, environmental quality, and social performance

Companies report on three aspects of performance : economic, environmental and social aspects

This reporting is advocated by the Global Reporting Initiative

Adopted by a number of global companies

Corporation’s true performance must be measured in terms of a balance between economic (profits), environmental (planet) and social (people) factors, with no one factor growing at the expense of the others

Each aspect can be assessed by use of a number of proxies

www.etctraining.com.hk

YOUR SITE HERE

LOGOEthicsCorporate social responsibility (CSR) and substainability reporting

Each aspect can be assessed by use of a number of proxies

Economic aspects:

Operating profitGearing level Debtor collection period

Social aspect

Working conditionsFair payAppropriate labour force by employee numberSafety at work by number of accidents at workTraining days

www.etctraining.com.hk

YOUR SITE HERE

LOGOEthics

Corporate social responsibility (CSR) and substainability reporting

Each aspect can be assessed by use of a number of proxies

Environmental aspects:

Ecological footprintEmissions to airUse of energy and waterInvestment in renewable resources

With quantified target for CSR policies, it is useful for measuring actual performance and compare with the target level.

CSR reporting is more common in countries where institutional investors are major shareholders, such as the US, and lesson common where many large companies are family-owned or family-controlled, such as HK.

Energy company, CLP Group is one of few HK companies that produce CSR reports. These reports are mainly narrative in form, but contain some quantified performance that are independently verified by an external auditing agency

www.etctraining.com.hk

YOUR SITE HERE

LOGO

EXECUTIVE MANAGEMENT (LP CHP.2)

www.etctraining.com.hk

SECOND TOPIC

YOUR SITE HERE

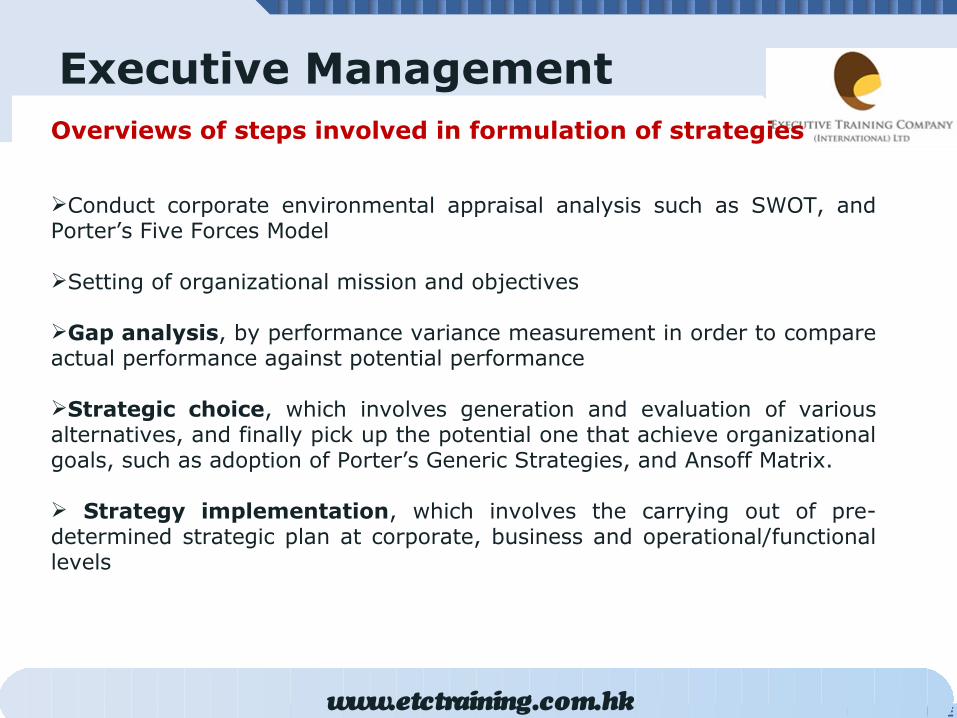

LOGOExecutive ManagementOverviews of steps involved in formulation of strategies

Conduct corporate environmental appraisal analysis such as SWOT, and Porter’s Five Forces Model

Setting of organizational mission and objectives

Gap analysis, by performance variance measurement in order to compare actual performance against potential performance

Strategic choice, which involves generation and evaluation of various alternatives, and finally pick up the potential one that achieve organizational goals, such as adoption of Porter’s Generic Strategies, and Ansoff Matrix.

Strategy implementation, which involves the carrying out of pre-determined strategic plan at corporate, business and operational/functional levels

www.etctraining.com.hk

YOUR SITE HERE

LOGOExecutive Management

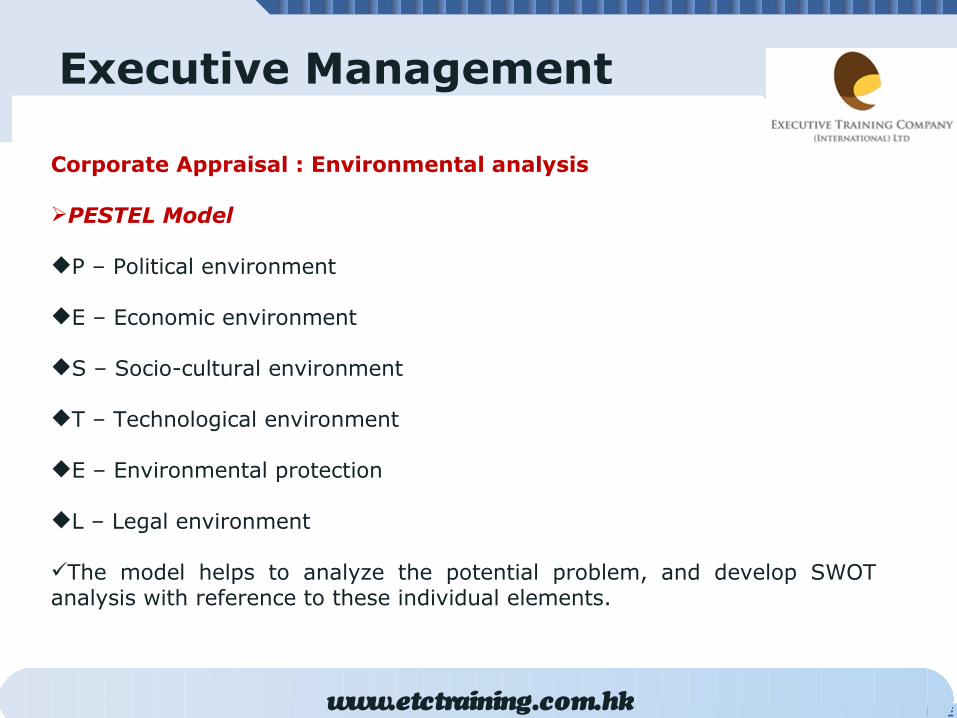

Corporate Appraisal : Environmental analysis

PESTEL Model

P – Political environment

E – Economic environment

S – Socio-cultural environment

T – Technological environment

E – Environmental protection

L – Legal environment

The model helps to analyze the potential problem, and develop SWOT analysis with reference to these individual elements.

www.etctraining.com.hk

YOUR SITE HERE

LOGOExecutive Management

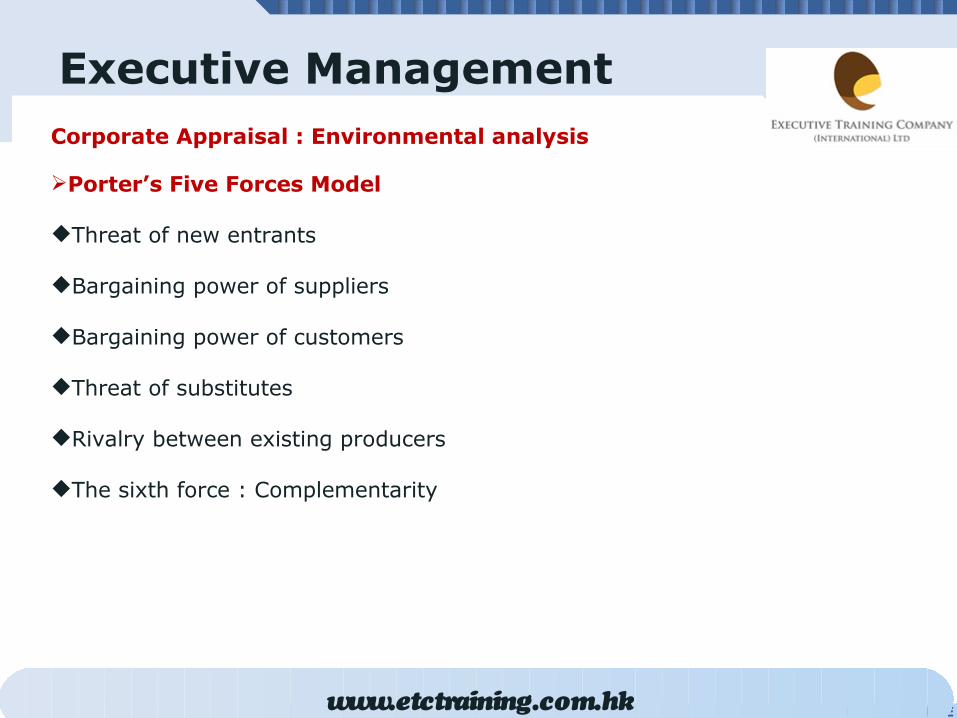

Corporate Appraisal : Environmental analysis

Porter’s Five Forces Model

Threat of new entrants

Bargaining power of suppliers

Bargaining power of customers

Threat of substitutes

Rivalry between existing producers

The sixth force : Complementarity

www.etctraining.com.hk

YOUR SITE HERE

LOGOExecutive Management

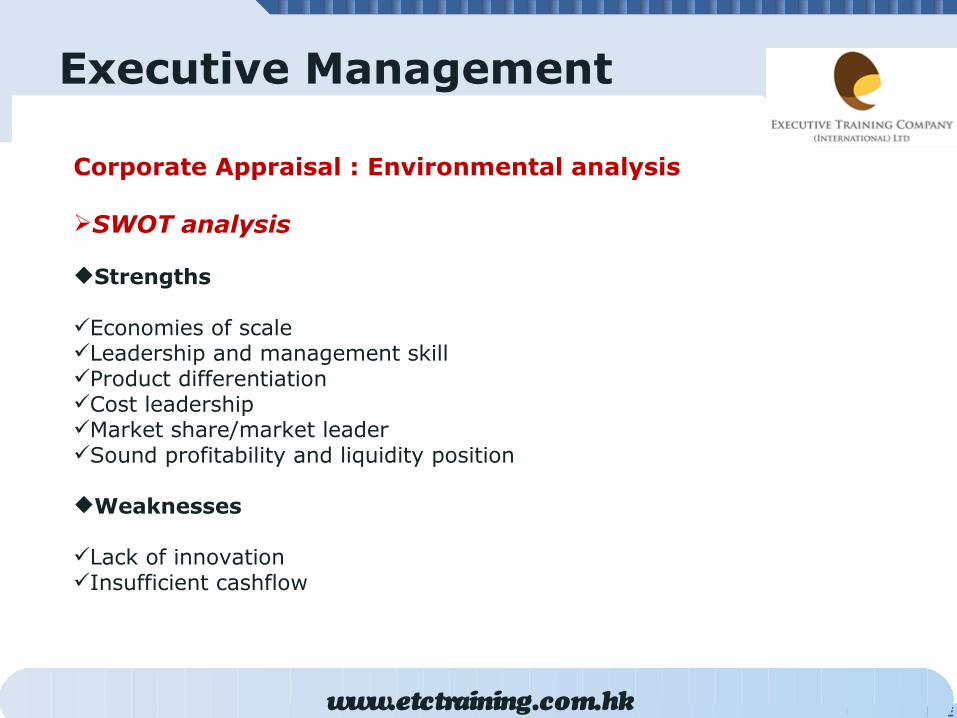

Corporate Appraisal : Environmental analysis

SWOT analysis

Strengths

Economies of scaleLeadership and management skillProduct differentiationCost leadershipMarket share/market leaderSound profitability and liquidity position

Weaknesses

Lack of innovationInsufficient cashflow

www.etctraining.com.hk

YOUR SITE HERE

LOGOExecutive ManagementCorporate Appraisal : Environmental analysis

SWOT analysis

Weaknesses

Lack of technical/expertise skillHigh gearing levelPoor quality product/services

Opportunities

New market segmentStable political environmentSound economic environmentLow interest rate environmentHigh threat for new entrants

www.etctraining.com.hk

YOUR SITE HERE

LOGOExecutive Management

Corporate Appraisal : Environmental analysis

SWOT analysis

Threats

Intense competitionBarrier to tradeEconomic downturnChange in political and legal environmentTechnological threat

www.etctraining.com.hk

YOUR SITE HERE

LOGOExecutive Management

Corporate Appraisal : Product/Service Portfolio Model

Product life cycle

Introduction

Launch of new productSlow growth in salesHeavy expenses on research and developmentHigh unit cost

Growth

New products gain market acceptanceHigh growth rate Product start to make profitLower unit cost

www.etctraining.com.hk

YOUR SITE HERE

LOGOExecutive ManagementCorporate Appraisal : Product/Service Portfolio Model

Product life cycle

Growth

Heavy expenses on promotionPossibility of overtrading issue

Maturity

Growth rate slow downThe longest period of product’s lifeProfit is stablePrice-based strategy is adopted in order to capture market share

www.etctraining.com.hk

YOUR SITE HERE

LOGOExecutive Management

Corporate Appraisal : Product/Service Portfolio Model

Product life cycle

Decline

Change in customer preference and lack of technical supportSales begin to declineProfits fallIntense competition leading to drop in priceProducers consider searching alternative market segments

www.etctraining.com.hk

YOUR SITE HERE

LOGOExecutive Management

Strategic choice : Ansoff Matrix

Current products or current markets : market penetration

Present products and new markets : market development

New products and present markets : product development

New products and new markets (diversification)

Horizontal integration

Vertical integration

Geographical integration

www.etctraining.com.hk

YOUR SITE HERE

LOGOExecutive ManagementStrategic choice : Porter’s generic strategies

Cost leadership or price-based strategies

Capture market shareCut cost in order to maintain profitabilityReduction in cost may sacrifice in product qualityProfit margin would be decreased

Product differentiation strategies

Tailor-made, and unique productFocus on providing high quality standard of product or servicesSeek to provide high perceived value justifying a substantial price premium

www.etctraining.com.hk

YOUR SITE HERE

LOGOExecutive ManagementStrategic choice : Porter’s generic strategies

Focus strategies

Concentrate on one or fewer market segmentsConcentrate on one or fewer product typeConcentrate on one or fewer geographical region

Hybrid strategies

Combination of price-based strategies and product differentiation strategies

www.etctraining.com.hk

YOUR SITE HERE

LOGOExecutive ManagementTechnique related to Executive Management

Scan through questions to determine whether the questions are related to environmental analysis, strategy determination, or focus on particular model

Underline key wordings in case study in order to capture point when answering question for application of case.

Read questions carefully in order to differentiate whether one strategy or multiple strategies being asked

Remember to weight the content with marks allocated in order to ensure proper time management

www.etctraining.com.hk

YOUR SITE HERE

LOGOExecutive Management

Common questions appearing in exam

Identify the strategies that company is currently adopted.

What are the strategic reasons for such acquisition?

What are the strengths (merit, advantages, contribution) for adoption of strategy?

What are the weaknesses (demerit, disadvantages, drawback) for adoption of strategy?

What are the potential business risks?

Suggest some managerial control to reduce the risk involved

www.etctraining.com.hk

YOUR SITE HERE

LOGO

Third Topic

www.etctraining.com.hk

Management Reporting (LP CHP. 4,5,6)

YOUR SITE HERE

LOGOManagement ReportingAbsorption Costing

Fixed and variable costs are allotted to cost unitsTotal overheads are absorbed according to activity level

Variable Costing (or marginal costing)

Only variable costs are allotted to cost unitsIt treats fixed overhead as period cost

Traditional Costing system

Use of one or fewer allocation bases to allocate individual production departments’ overhead costs to productOne or fewer indirect cost poolsIt has more indirect costsIt focuses on product/services as the cost object

www.etctraining.com.hk

YOUR SITE HERE

LOGOManagement Reporting

Activity Based Costing System (ABC)

It identifies various activities performed in an organization, collects costs on the basis of underlying nature and extent of those activities, and assigns costs to products and services based on those activities based on appropriate cost driver

Attempt to allocate overheads to product or services more accurately

ABC System has multiple indirect cost pools

It classifies many indirect costs as direct costs

ABC System focuses on activities as fundamental cost object

ABC System uses cost of activities as the basis for assigning cost, resulting in more accurate costing

www.etctraining.com.hk

YOUR SITE HERE

LOGOManagement Reporting

Stages to implement ABC System

Conduct interviews to determine appropriate activity centres and cost drivers

Establish the interrelationship between key activities and the resources consumed

Construct a process map to illustrate these relationships

Put costs under various costs pool and identify the cost of each activity and the related cost driver

Assign costs to products and services on the basis of the mix of activities needed to produce each product or service

Purchase of advanced software to carry out the mechanism of ABC.

www.etctraining.com.hk

YOUR SITE HERE

LOGOManagement Reporting

Benefits for ABC System

Better understanding of company activities

More accurate overhead cost allocation

Cost driver rates can be used as a measure of performance

Assist in setting the budget

More realistic product costs and better resource allocation decisions

Raised profile of overhead costs and improves control by linking costs to the activities that cause them

Enhanced the credibility of the costing system

www.etctraining.com.hk

YOUR SITE HERE

LOGOManagement ReportingDrawback for ABC System

Encounter difficulties in identifying cost pools, activities and subsequent cost driver rates for the range of products and services

Considerable time and effort are required

Adequate computer software may not be available to support the complexities of the ABC system

There may be inadequate human resources to undertake the research and analysis

The administration of the ABC system results in additional cost such that cost may be outweigh the benefit

The implementation of ABC system must be supported by senior management which might not be as smooth as one think.

www.etctraining.com.hk

YOUR SITE HERE

LOGOManagement Reporting

Pricing Decisions

Demand based pricing

Assumes that there exists a relationship between the selling price of the product and the demand.

Relationship can be described by an inverse, linear relationship Optimum price is set at marginal revenue equals to marginal cost

Cost plus pricing

Adding an amount to the cost of the item Simple to calculate Ignores the market Difficult to establish and decide actually which cost may be recovered Different absorption methods give rise to different costs and hence

different selling prices

www.etctraining.com.hk

YOUR SITE HERE

LOGOManagement Reporting

Pricing Decisions

Target cost pricing

Involve setting a target cost by subtracting a desired profit margin from a competitive price

Easy to justify the price change Encourage price stability, if all competitors have similar cost structure and

use a similar mark-up Staff may be demoralised if production costs cannot be reduced to meet

the target profit

www.etctraining.com.hk

YOUR SITE HERE

LOGOManagement Reporting

Pricing Decisions

Life cycle pricing

Tracks and accumulates costs and revenues attributable to each product over the entire product life cycle

A product life cycle can be divided into five phases: development, introduction, growth, maturity and decline The company can determine the price according to its stage in the product life cycle

Non-production costs are traced to individual products over complete life cycles, and hence more accurate feedback information is available

No simple formula for selling price can be set because it requires a lot of judgement from the management

www.etctraining.com.hk

YOUR SITE HERE

LOGOManagement Reporting

Customer Profitability Analysis

Total sales revenue from the customer group less than all costs incurred in servicing that customer group, ie., contribution margin

Customers are grouped according to behaviour

By understanding the cost implications of different customer types’ consumption of activities, measures can be put in place to modify their behaviour

The use of charges or increased services to modify behaviour can achieve this outcome

www.etctraining.com.hk

YOUR SITE HERE

LOGOManagement Reporting

Attempt Past Paper , please refer to the attached :

May 2010 Question 2

www.etctraining.com.hk

YOUR SITE HERE

LOGOManagement Reporting

Benefit of Customer Profitability Analysis

Improved profitability Efficient resources allocation Improve customer service Better negotiation with customers Retention of customers and highlight unprofitable

customers Comparative analysis between customers

www.etctraining.com.hk

YOUR SITE HERE

LOGOManagement ReportingFinancial performance indicator

Profitability Gross profit margin Net profit margin Return on equity

Gearing Gearing ratio Interest cover

Liquidity Current ratio Quick ratio Accounts receivable period Accounts payable period Inventory turnover period Use of average balance figures for calculation of ratio if the data is

available, say three-year data for two-year ratio comparison

www.etctraining.com.hk

YOUR SITE HERE

LOGOManagement Reporting

Non-Financial performance indicator

Reasons for increasing importance :

Monetary terms based on performance measurement system concentrates for a few variables

Lack of information on quality

Change in cost structure

Change in competitive environment

Change in manufacturing environment

www.etctraining.com.hk

YOUR SITE HERE

LOGOManagement Reporting

Non-Financial performance indicator

Samples for non-financial performance indicators

Occupancy rate in restaurant and hotel

Number of customers being served by one staff

Total units sold versus total units sold by competitors (indicating market share)

Warranty claims per month

Customer satisfaction rating by survey

Number of complaints over a certain period of time

www.etctraining.com.hk

YOUR SITE HERE

LOGOManagement Reporting

The Balance Scorecard (BSC)

Provides an organisation with a comprehensive framework that translates the organisation’s vision and strategy into a coherent set of performance measures

Both financial and non financial information is included

To implement the BSC, company must identify its vision, it then identifies all key and relevant performance measurement which lead to the achievement of the vision

The performance measures are grouped into 4 perspectives

Financial (eg., revenue growth, profitability) Customer (eg., market share, customer satisifaction) Internal business processes (eg., time to complete job, number of

pollution complaints) Innovation and learning (eg., skill levels of employees, hours of employee

training)

www.etctraining.com.hk

YOUR SITE HERE

LOGOManagement Reporting

The Balance Scorecard (BSC)

Each perspective has a short-term goal with one or more critical success factors identified with that goal

These factors are structured into a linked set of understandable and measurable operational targets and key performance indicators

The BSC can lead to consensus on organizational priorities, clear specification of goals, rigorous planning and improvement processes, alignment of strategy goals with shorter term actions, clearer communication, team working and knowledge sharing and clearer accountability for results

www.etctraining.com.hk

YOUR SITE HERE

LOGOManagement Reporting

Responsibility Accounting

A system if account that segregates revenues and costs into area of separate responsibility which are then assigned to managers, who are then evaluated on performance compared to budget.

Cost centre – focus on cost control

Revenue centre – focus for revenue generation

Profit centre – revenue generation and cost control

Investment centre – control over capital expenditure decision

www.etctraining.com.hk

YOUR SITE HERE

LOGOManagement Reporting

Responsibility Accounting

Measurement for investment centres

Return on Investment (ROI)

Profit/Capital Employed

where capital employed : Total assets – Current liabilities

Relative measurement as expressed in terms of percentage

Residual income

= Profit – an imputed interest charge on controllable investment

Absolute measurement

www.etctraining.com.hk

YOUR SITE HERE

LOGOManagement Reporting

Responsibility Accounting

Measurement for investment centres

Economic value added (EVA)

Net operating profit after tax – (Capital employed * WACC)

Make use of economic profit concept by adjustment from accounting profit:

Replacement cost of net assets included in EVA

Costs which would normally be treated as expenses be considering within EVA such as research and development cost

Adjustment for depreciation charge by means of amortisation cost

www.etctraining.com.hk

YOUR SITE HERE

LOGOManagement Reporting

Responsibility Accounting

Measurement for investment centres

Economic value added (EVA)

Advantages of EVA

Reflects the real wealth for shareholders Involves less distortion of accounting policies Generates absolute value which would be easily understandable by managers Treatment of certain costs as investments thereby encouraging expenditure

Disadvantages of EVA

Focus on short term performance Depend upon historical data, which might not be indicator for future use Involve efford for adjustments for deriving the EVA Comparison within industry is difficult as it involves absolute amount only

www.etctraining.com.hk

YOUR SITE HERE

LOGOManagement Reporting

Exam questions related to investment centre

Involves calculation of different division by EVA, ROI, and residual income

Analysis of divisional performance by means of numerical support

Discuss the strengths and weaknesses under different investment performance measurement

EVA is a better indicator for investment performance measurement

Qualitative factors should also be considered

www.etctraining.com.hk

YOUR SITE HERE

LOGOManagement Reporting

Transfer pricing

Definition

Price at which goods or services are sold by one division within an entity to another division in the same entity

Involve decision whether to buy/sell products to outsider or within the same group

The general rule is that price should equal the outgoing cost, ie variable cost (if no production constraint) plus the opportunity cost in the selling organisation (if with production constraint)

Objectives

Motivation of divisional managers Goal congruence Divisional autonomy

www.etctraining.com.hk

YOUR SITE HERE

LOGOManagement Reporting

Transfer pricing

Factors to be considered when setting of transfer price

Tax consideration

Fund positioning

Risk and uncertainty

Government policies

Management incentives and performance evaluation

www.etctraining.com.hk

YOUR SITE HERE

LOGOManagement Reporting

www.etctraining.com.hk

Attempt Past Paper , please refer to the attached :

Sept 2007 Question 2

YOUR SITE HERE

LOGOManagement Reporting

Exam questions related to transfer pricing

Optimal decisions for various scenario related as to whether production constraint or not

Concept of variable cost, opportunity cost, and fixed cost is critical for determination of transfer price

Link with the concept of residual income/ROI for calculation of bonus under different scenario for determination of transfer price

Staff morale problem should be considered when involved improper transfer price setting

www.etctraining.com.hk

YOUR SITE HERE

LOGOAt ETC Training, it is our aim to encourage

you.Thank you!!!

Website: www.etctraining.com.hk Email : [email protected]