Embed Size (px)

Citation preview

The views expressed in this presentation are those of the presenter,

not necessarily those of the IASB or IFRS Foundation.

International Financial Reporting Standards

Accounting for Financial Instruments

(IFRS 9)

© 2013 IFRS Foundation. 30 Cannon Street | London EC4M 6XH | UK. www.ifrs.org

Executive IFRS workshop for Regulators

Diplomatic Academy of Vienna

Darrel Scott, IASB member

2

© 2013 IFRS Foundation. 30 Cannon Street | London EC4M 6XH | UK. www.ifrs.org

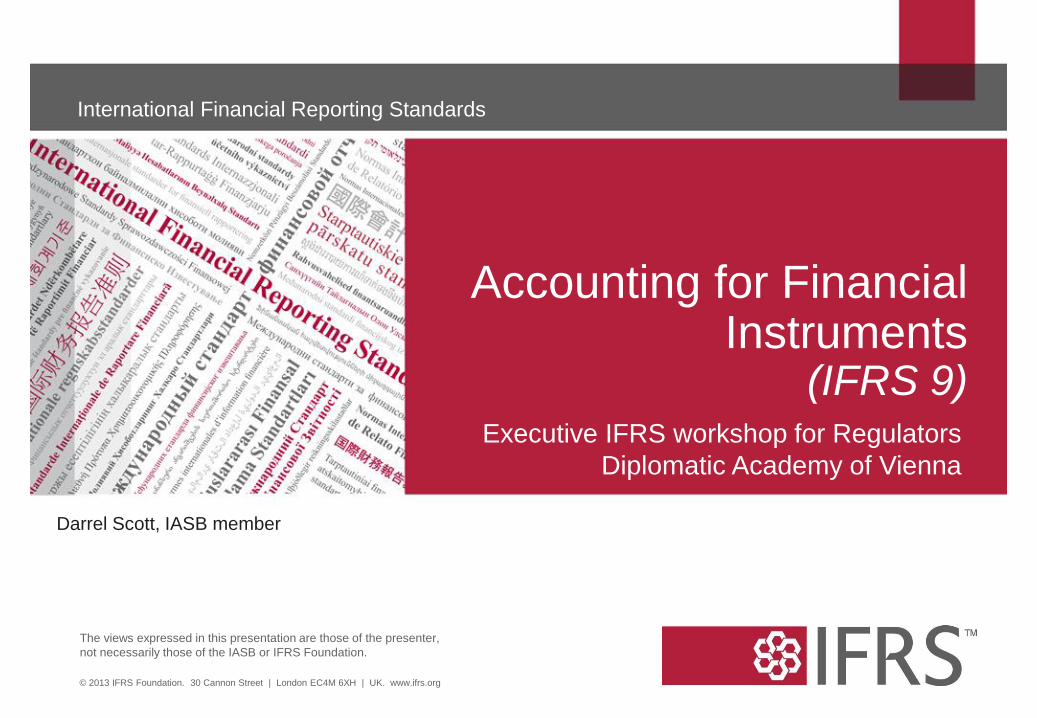

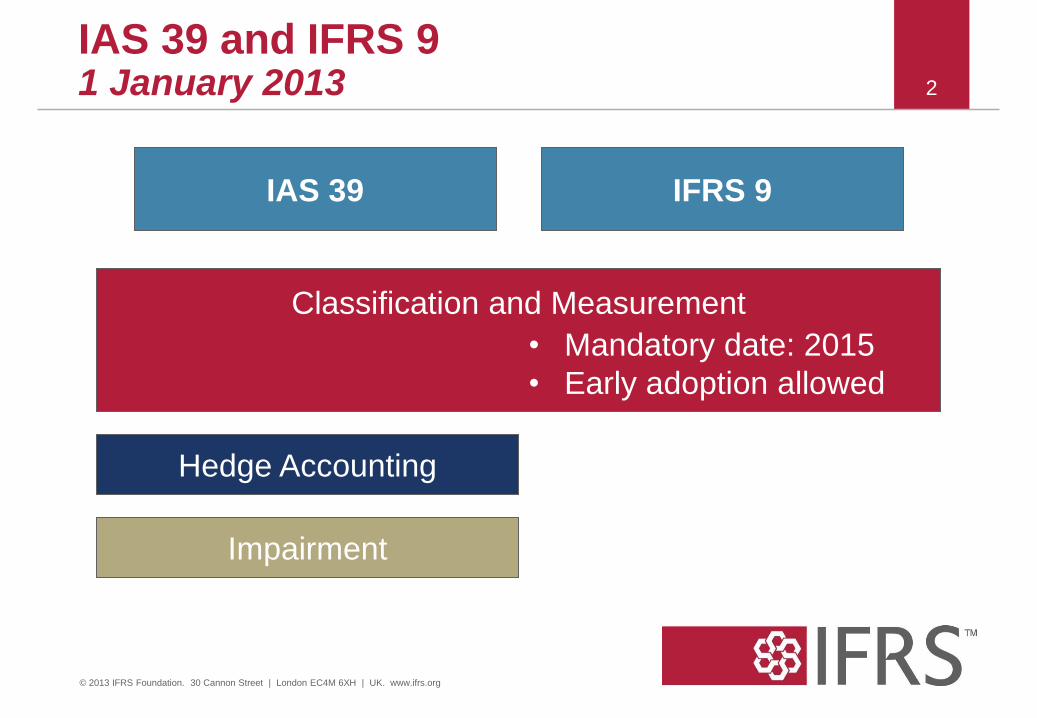

IAS 39 and IFRS 9 1 January 2013

IAS 39 IFRS 9

Classification and Measurement

• Mandatory date: 2015

• Early adoption allowed

Hedge Accounting

Impairment

3

© 2013 IFRS Foundation. 30 Cannon Street | London EC4M 6XH | UK. www.ifrs.org

IAS

39 IF

RS

9

Classification & Measurement IFRS 9 (2010) + ED of limited

amendments

Impairment Forthcoming ED

General Hedge accounting* Review draft

* Macro hedge accounting is separated from this project

IAS 39 and IFRS 9 1 January 2013 continued

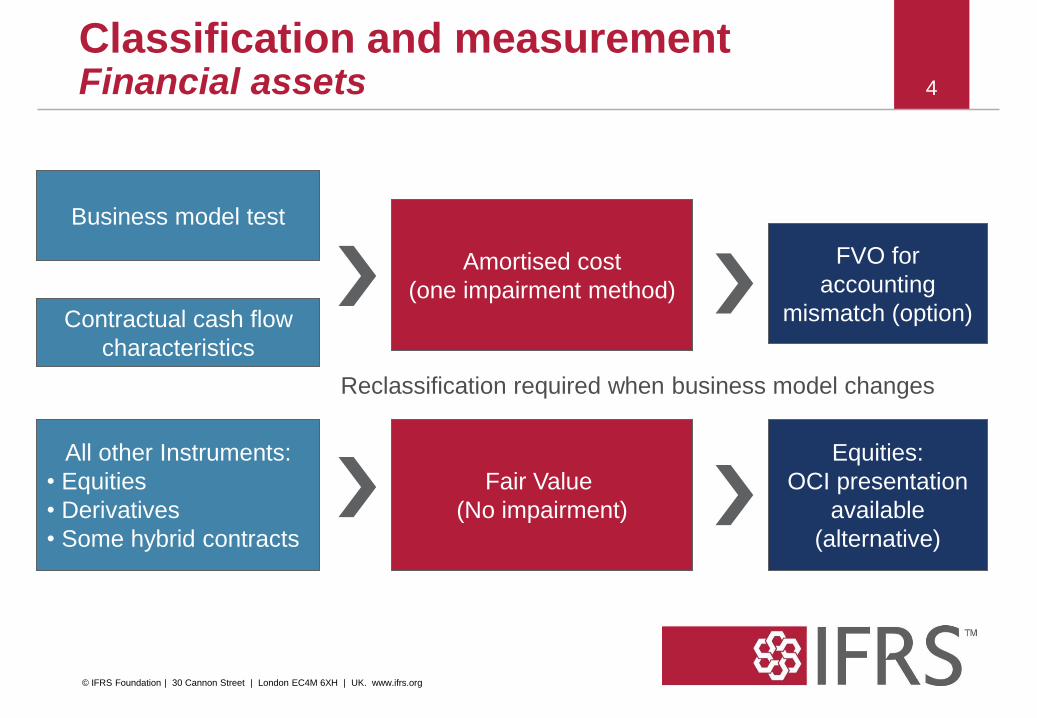

Classification and measurement Financial assets

Fair Value

(No impairment)

Amortised cost

(one impairment method)

Contractual cash flow

characteristics

Business model test

FVO for

accounting

mismatch (option)

All other Instruments:

• Equities

• Derivatives

• Some hybrid contracts

Equities:

OCI presentation

available

(alternative)

Reclassification required when business model changes

4

© IFRS Foundation | 30 Cannon Street | London EC4M 6XH | UK. www.ifrs.org

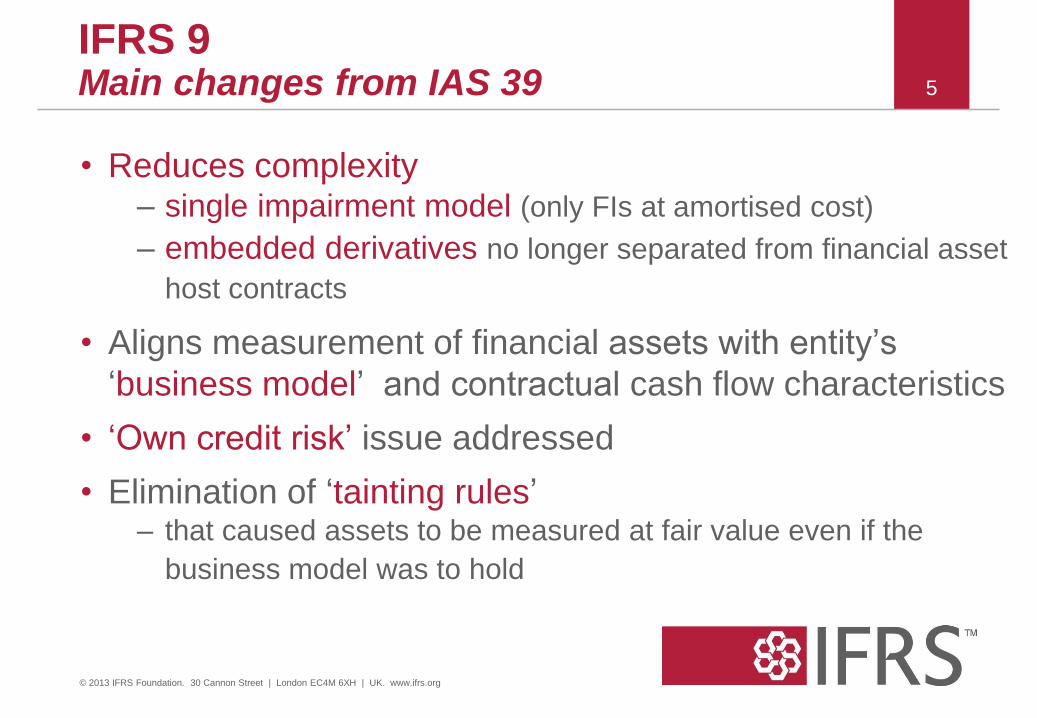

IFRS 9 Main changes from IAS 39

• Reduces complexity – single impairment model (only FIs at amortised cost)

– embedded derivatives no longer separated from financial asset

host contracts

• Aligns measurement of financial assets with entity’s

‘business model’ and contractual cash flow characteristics

• ‘Own credit risk’ issue addressed

• Elimination of ‘tainting rules’ – that caused assets to be measured at fair value even if the

business model was to hold

5

© 2013 IFRS Foundation. 30 Cannon Street | London EC4M 6XH | UK. www.ifrs.org

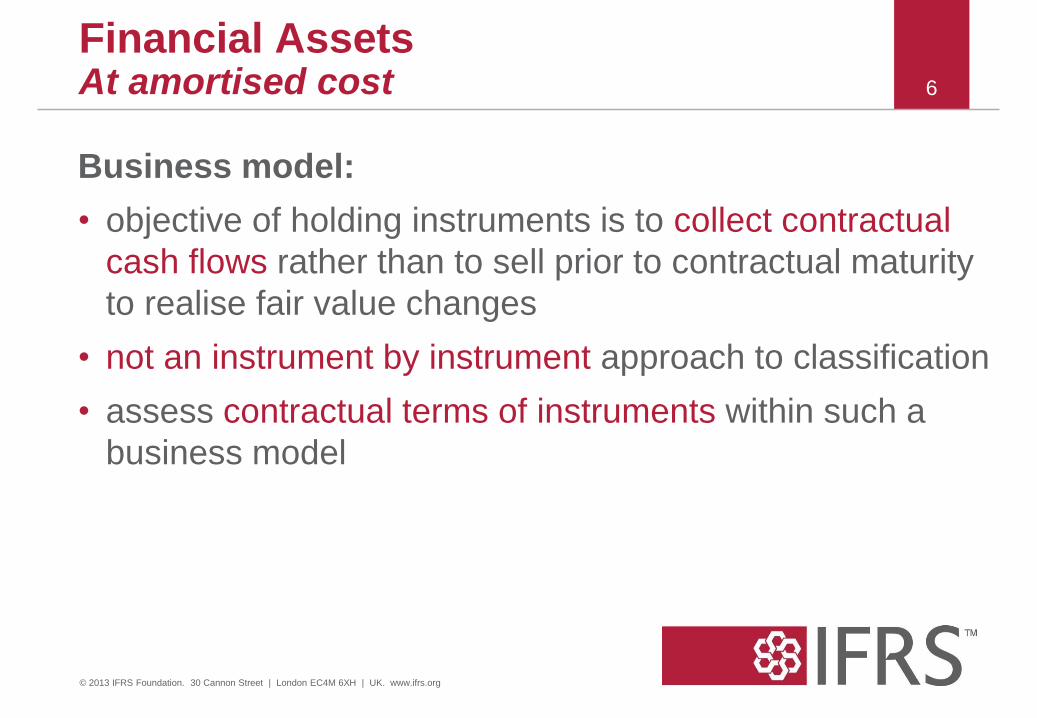

Business model:

• objective of holding instruments is to collect contractual

cash flows rather than to sell prior to contractual maturity

to realise fair value changes

• not an instrument by instrument approach to classification

• assess contractual terms of instruments within such a

business model

Financial Assets At amortised cost 6

© 2013 IFRS Foundation. 30 Cannon Street | London EC4M 6XH | UK. www.ifrs.org

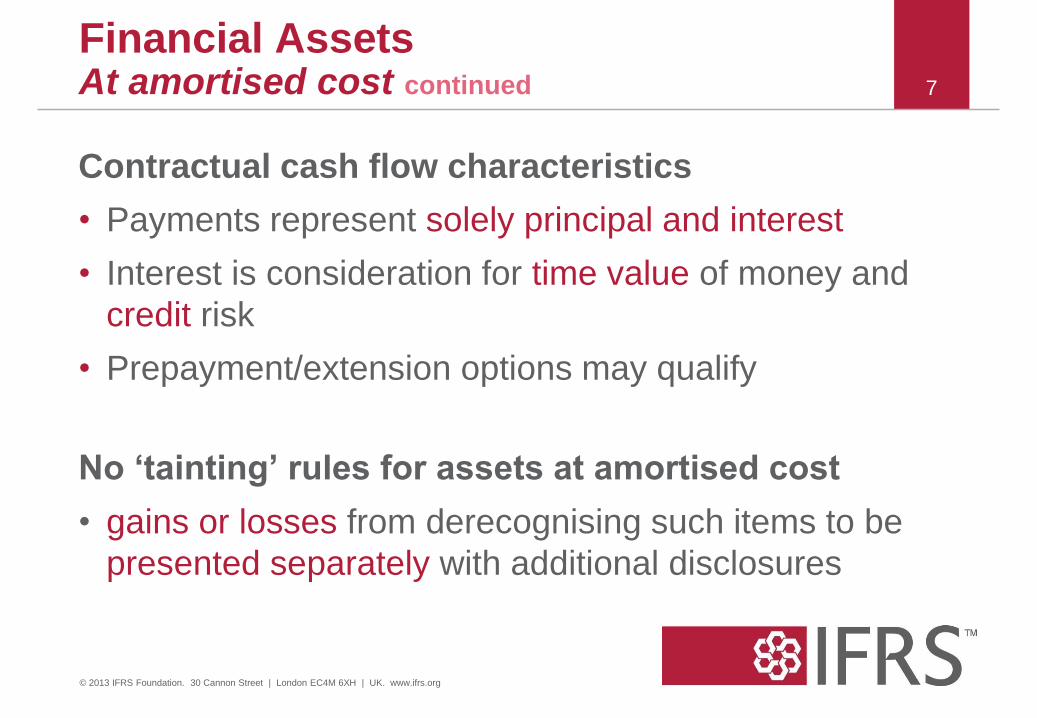

Contractual cash flow characteristics

• Payments represent solely principal and interest

• Interest is consideration for time value of money and

credit risk

• Prepayment/extension options may qualify

No ‘tainting’ rules for assets at amortised cost

• gains or losses from derecognising such items to be

presented separately with additional disclosures

Financial Assets At amortised cost continued 7

© 2013 IFRS Foundation. 30 Cannon Street | London EC4M 6XH | UK. www.ifrs.org

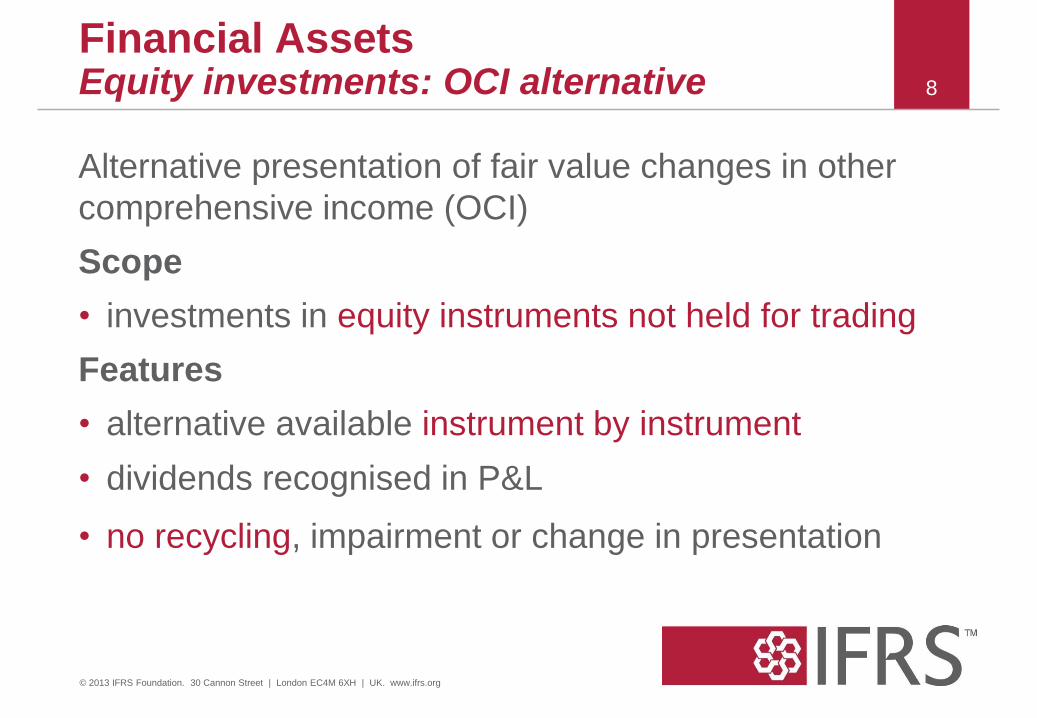

Alternative presentation of fair value changes in other

comprehensive income (OCI)

Scope

• investments in equity instruments not held for trading

Features

• alternative available instrument by instrument

• dividends recognised in P&L

• no recycling, impairment or change in presentation

Financial Assets Equity investments: OCI alternative 8

© 2013 IFRS Foundation. 30 Cannon Street | London EC4M 6XH | UK. www.ifrs.org

9

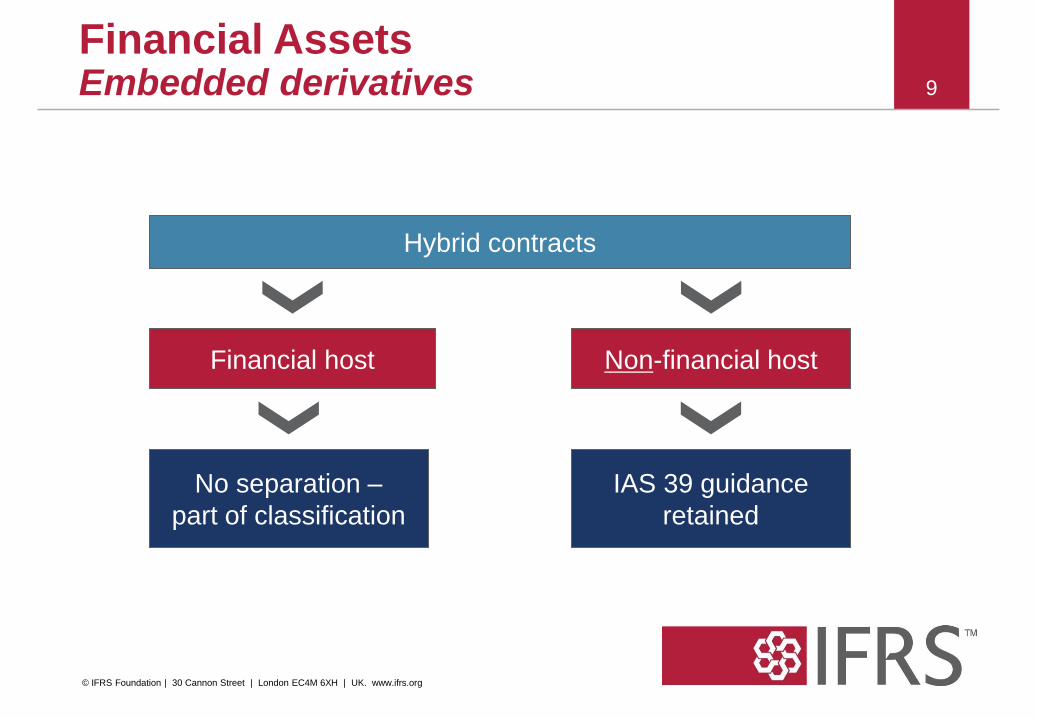

Hybrid contracts

Financial host Non-financial host

IAS 39 guidance

retained

No separation –

part of classification

Financial Assets Embedded derivatives

© IFRS Foundation | 30 Cannon Street | London EC4M 6XH | UK. www.ifrs.org

10

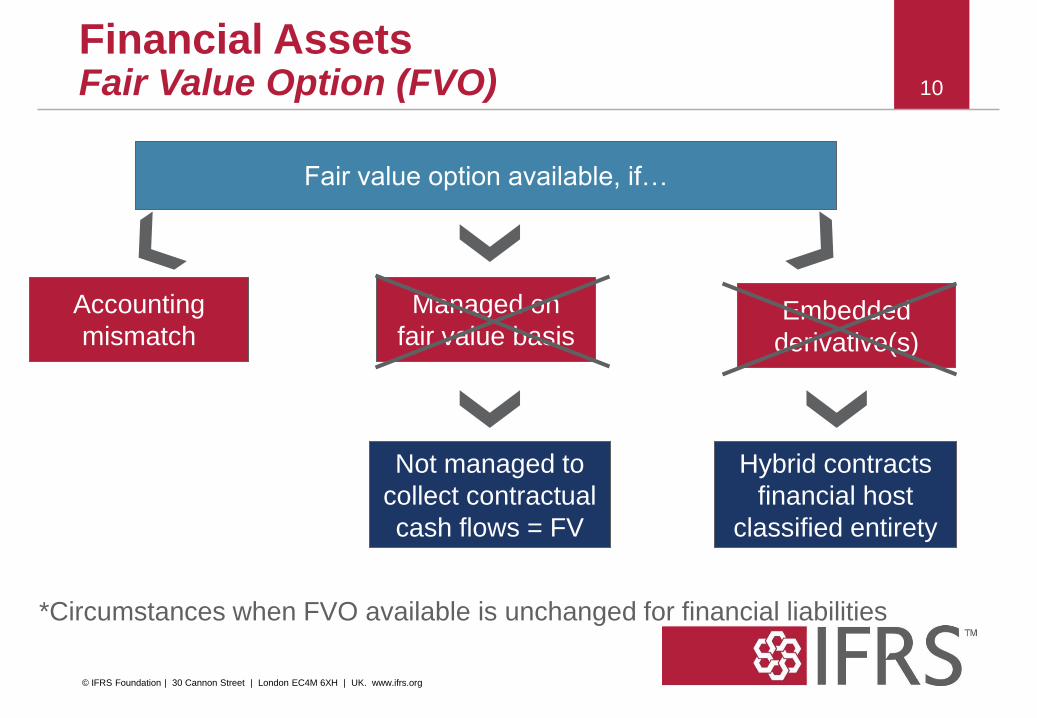

Fair value option available, if…

Accounting

mismatch

Managed on

fair value basis Embedded

derivative(s)

Not managed to

collect contractual

cash flows = FV

Hybrid contracts

financial host

classified entirety

*Circumstances when FVO available is unchanged for financial liabilities

Financial Assets Fair Value Option (FVO)

© IFRS Foundation | 30 Cannon Street | London EC4M 6XH | UK. www.ifrs.org

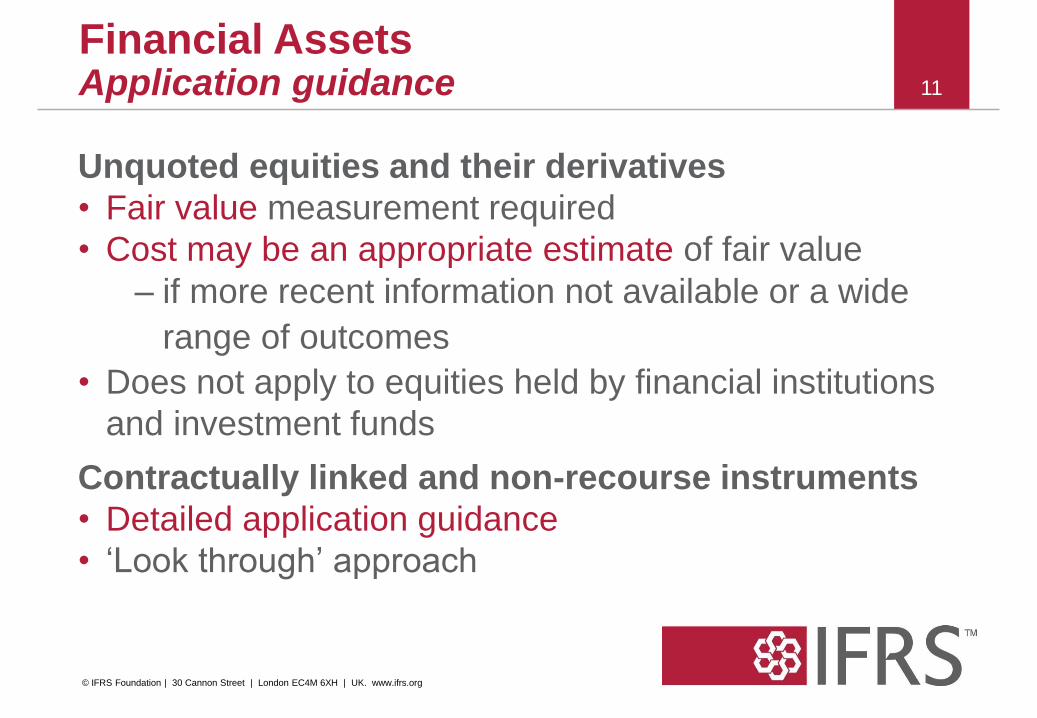

Unquoted equities and their derivatives

• Fair value measurement required

• Cost may be an appropriate estimate of fair value

– if more recent information not available or a wide

range of outcomes

• Does not apply to equities held by financial institutions

and investment funds

Contractually linked and non-recourse instruments

• Detailed application guidance

• ‘Look through’ approach

11

Financial Assets Application guidance

© IFRS Foundation | 30 Cannon Street | London EC4M 6XH | UK. www.ifrs.org

11

12

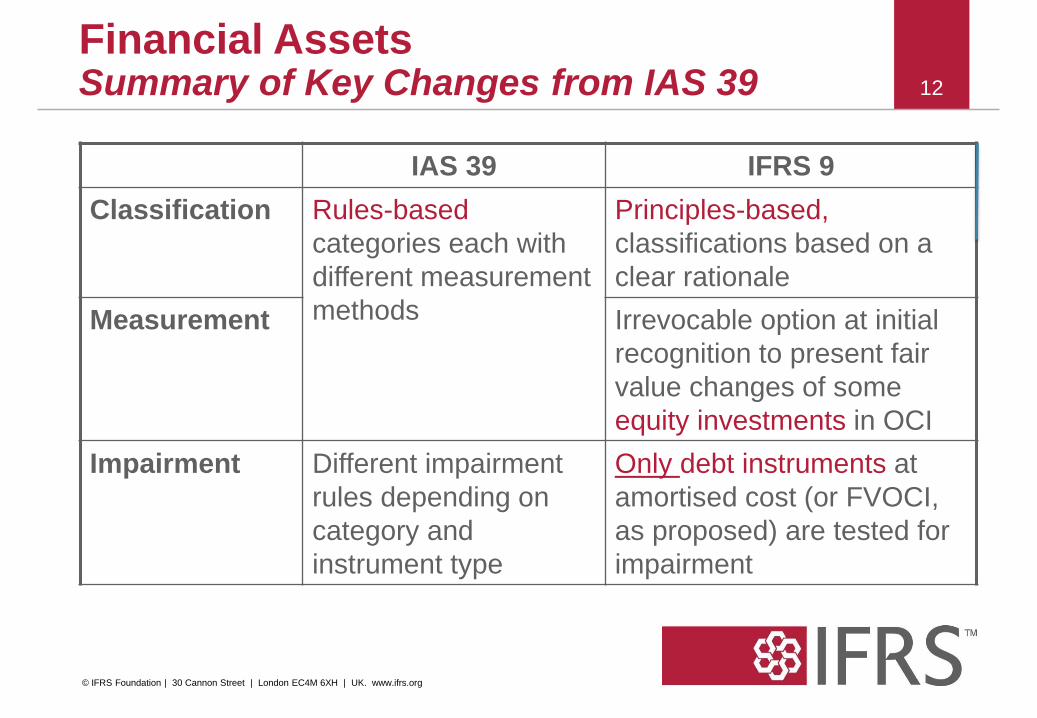

IAS 39 IFRS 9

Classification Rules-based

categories each with

different measurement

methods

Principles-based,

classifications based on a

clear rationale

Measurement Irrevocable option at initial

recognition to present fair

value changes of some

equity investments in OCI

Impairment Different impairment

rules depending on

category and

instrument type

Only debt instruments at

amortised cost (or FVOCI,

as proposed) are tested for

impairment

Financial Assets Summary of Key Changes from IAS 39

© IFRS Foundation | 30 Cannon Street | London EC4M 6XH | UK. www.ifrs.org

13

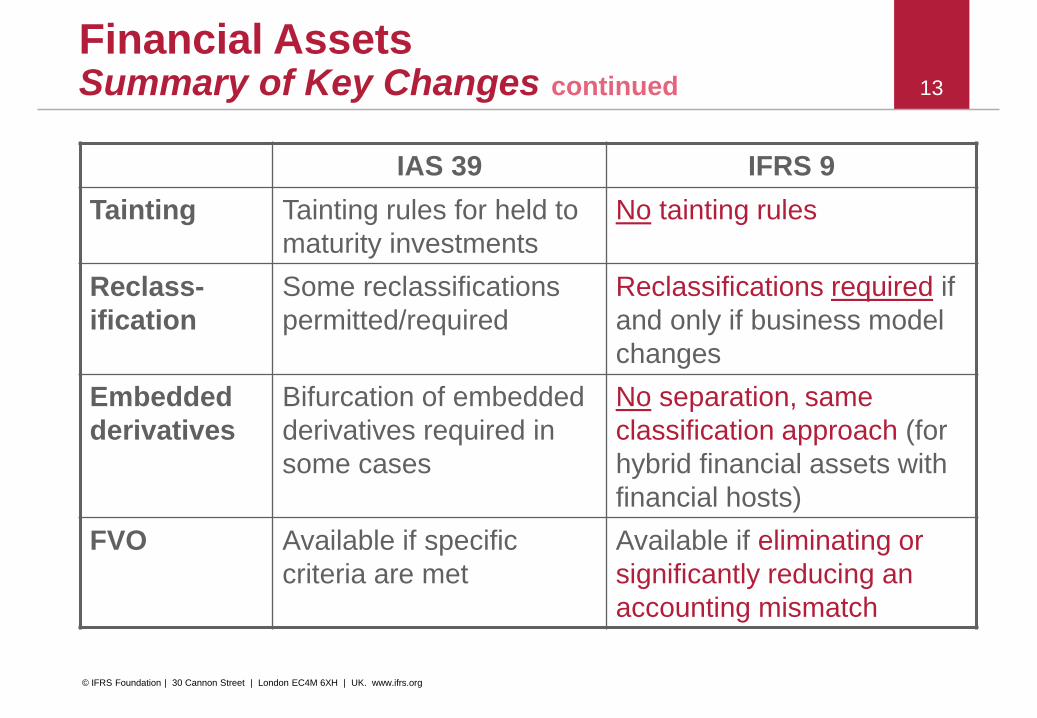

Financial Assets Summary of Key Changes continued

IAS 39 IFRS 9

Tainting Tainting rules for held to

maturity investments

No tainting rules

Reclass-

ification

Some reclassifications

permitted/required

Reclassifications required if

and only if business model

changes

Embedded

derivatives

Bifurcation of embedded

derivatives required in

some cases

No separation, same

classification approach (for

hybrid financial assets with

financial hosts)

FVO Available if specific

criteria are met

Available if eliminating or

significantly reducing an

accounting mismatch

© IFRS Foundation | 30 Cannon Street | London EC4M 6XH | UK. www.ifrs.org

14

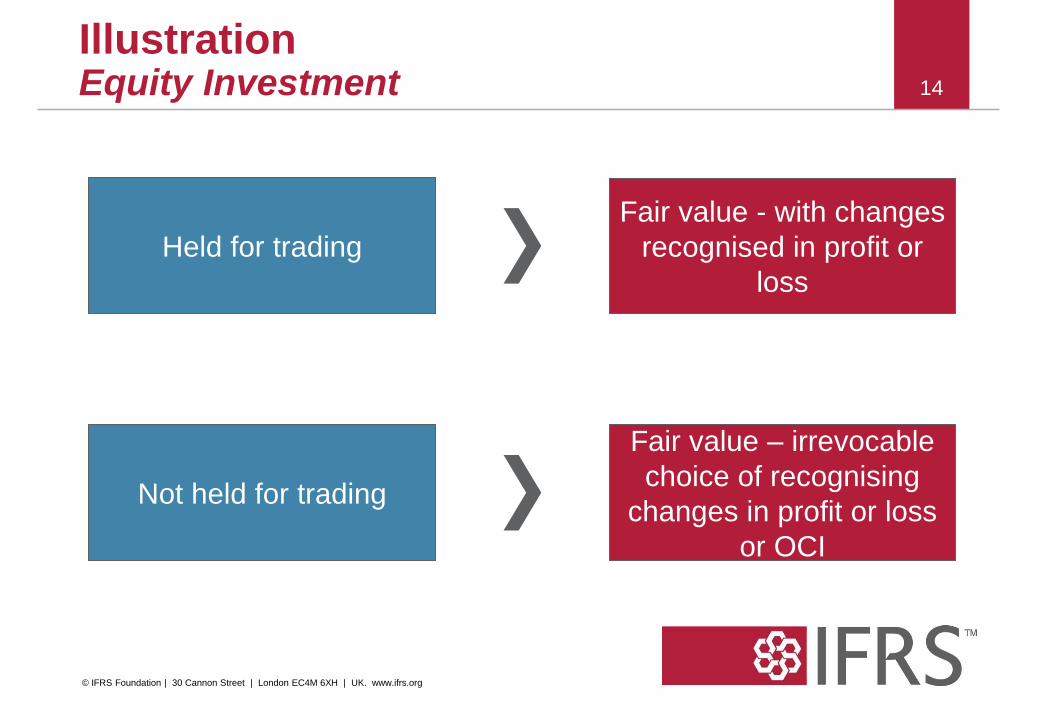

Held for trading

Fair value - with changes

recognised in profit or

loss

Not held for trading

Fair value – irrevocable

choice of recognising

changes in profit or loss

or OCI

© IFRS Foundation | 30 Cannon Street | London EC4M 6XH | UK. www.ifrs.org

Illustration Equity Investment

15

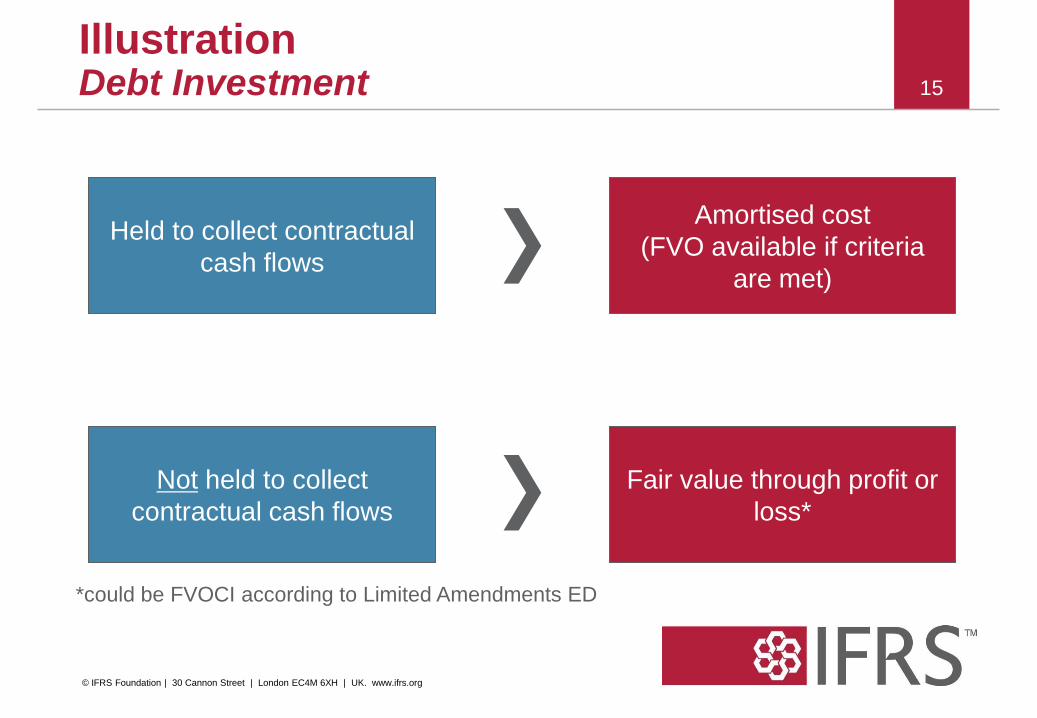

Held to collect contractual

cash flows

Amortised cost

(FVO available if criteria

are met)

Not held to collect

contractual cash flows

Fair value through profit or

loss*

© IFRS Foundation | 30 Cannon Street | London EC4M 6XH | UK. www.ifrs.org

*could be FVOCI according to Limited Amendments ED

Illustration Debt Investment

16

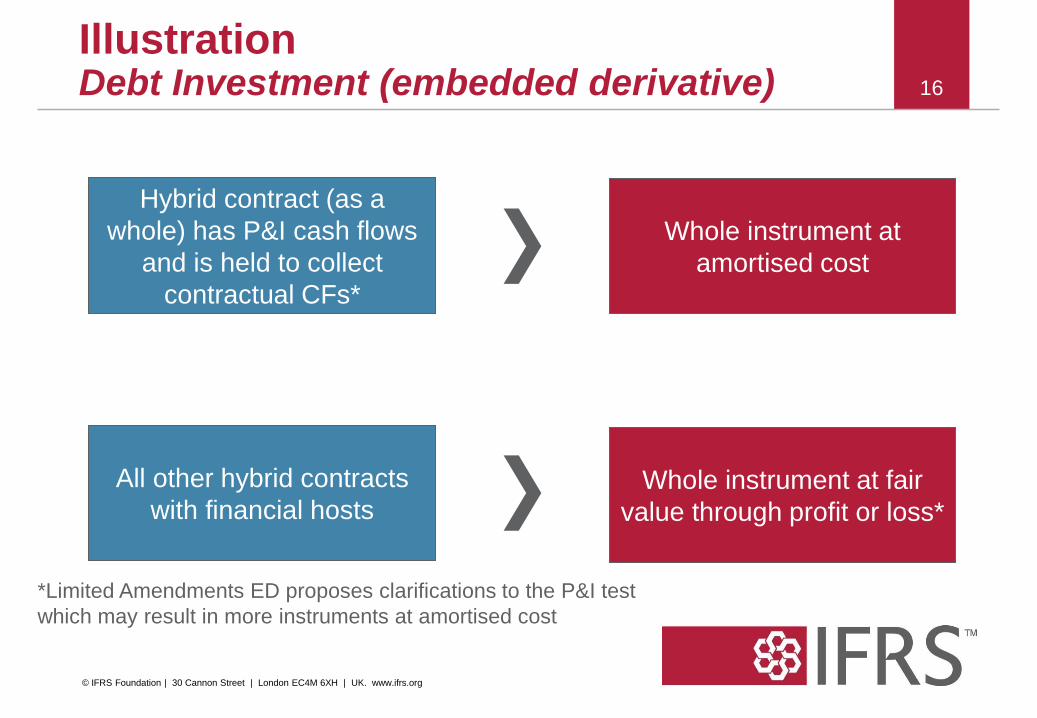

Hybrid contract (as a

whole) has P&I cash flows

and is held to collect

contractual CFs*

Whole instrument at

amortised cost

All other hybrid contracts

with financial hosts Whole instrument at fair

value through profit or loss*

© IFRS Foundation | 30 Cannon Street | London EC4M 6XH | UK. www.ifrs.org

*Limited Amendments ED proposes clarifications to the P&I test

which may result in more instruments at amortised cost

Illustration Debt Investment (embedded derivative)

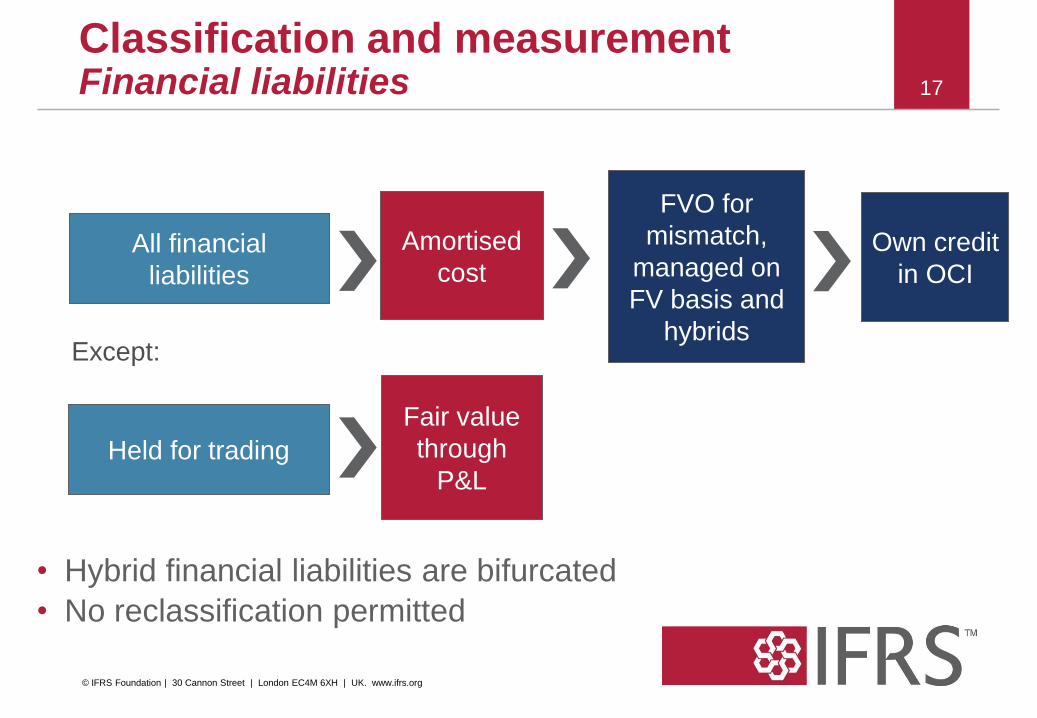

Classification and measurement Financial liabilities

All financial

liabilities

Amortised

cost

FVO for

mismatch,

managed on

FV basis and

hybrids Except:

Held for trading

Fair value

through

P&L

Own credit

in OCI

• Hybrid financial liabilities are bifurcated

• No reclassification permitted

17

© IFRS Foundation | 30 Cannon Street | London EC4M 6XH | UK. www.ifrs.org

18

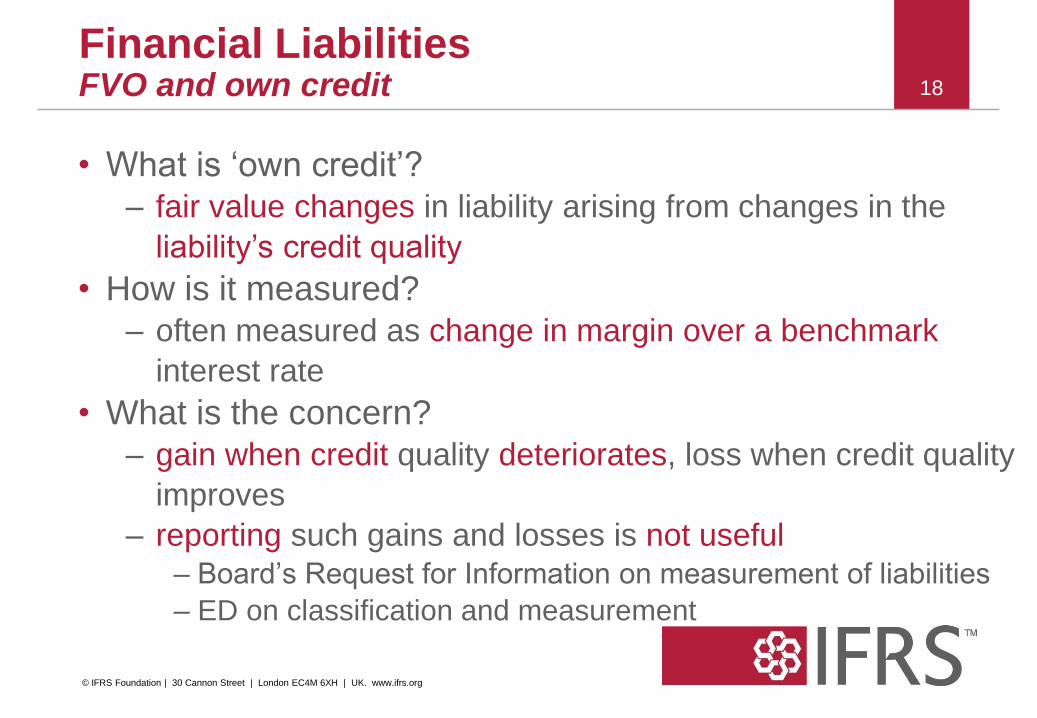

Financial Liabilities FVO and own credit

• What is ‘own credit’?

– fair value changes in liability arising from changes in the

liability’s credit quality

• How is it measured?

– often measured as change in margin over a benchmark

interest rate

• What is the concern?

– gain when credit quality deteriorates, loss when credit quality

improves

– reporting such gains and losses is not useful

– Board’s Request for Information on measurement of liabilities

– ED on classification and measurement

© IFRS Foundation | 30 Cannon Street | London EC4M 6XH | UK. www.ifrs.org

19

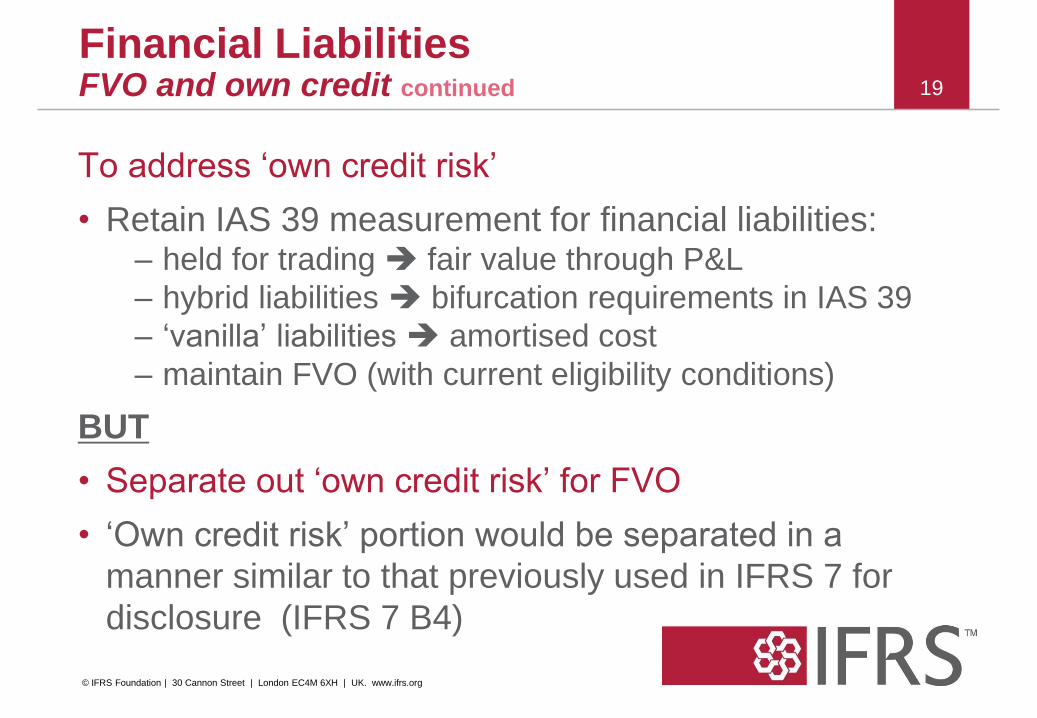

To address ‘own credit risk’

• Retain IAS 39 measurement for financial liabilities: – held for trading fair value through P&L

– hybrid liabilities bifurcation requirements in IAS 39

– ‘vanilla’ liabilities amortised cost

– maintain FVO (with current eligibility conditions)

BUT

• Separate out ‘own credit risk’ for FVO

• ‘Own credit risk’ portion would be separated in a

manner similar to that previously used in IFRS 7 for

disclosure (IFRS 7 B4)

Financial Liabilities FVO and own credit continued

© IFRS Foundation | 30 Cannon Street | London EC4M 6XH | UK. www.ifrs.org

19

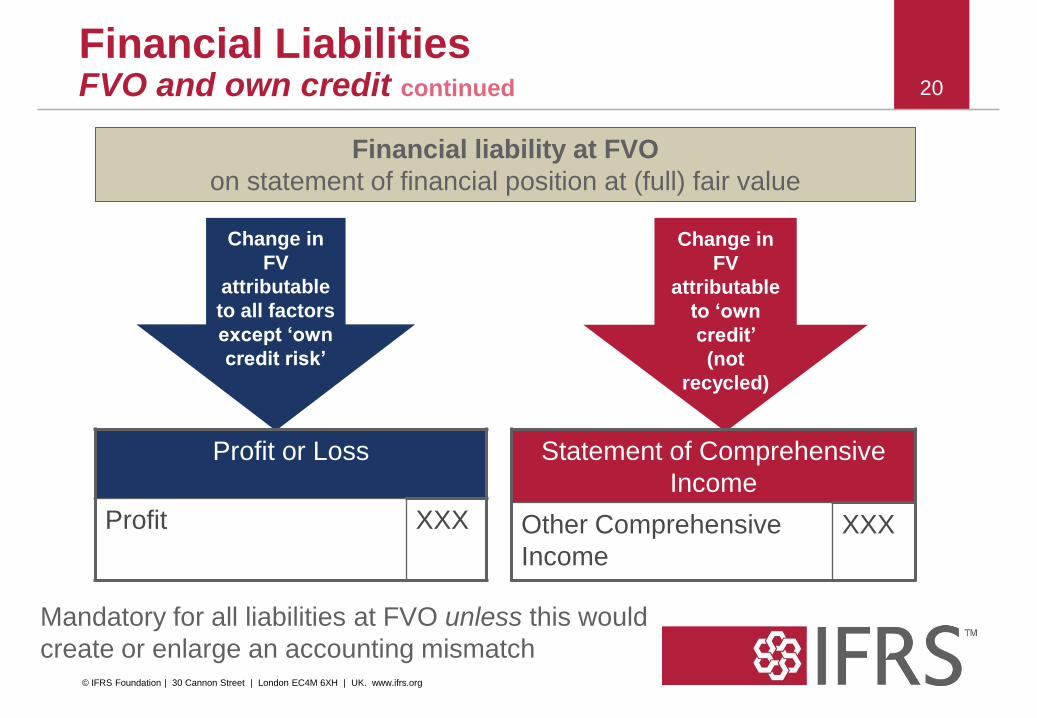

20

Change in

FV

attributable

to all factors

except ‘own

credit risk’

Change in

FV

attributable

to ‘own

credit’

(not

recycled)

Profit or Loss

Profit XXX

Financial liability at FVO

on statement of financial position at (full) fair value

Statement of Comprehensive

Income

Other Comprehensive

Income

XXX

© IFRS Foundation | 30 Cannon Street | London EC4M 6XH | UK. www.ifrs.org

Mandatory for all liabilities at FVO unless this would

create or enlarge an accounting mismatch

20

Financial Liabilities FVO and own credit continued

International Financial Reporting Standards

The views expressed in this presentation are those of the presenter,

not necessarily those of the IASB or IFRS Foundation

Reopening Phase I Classification and Measurement

© IFRS Foundation | 30 Cannon Street | London EC4M 6XH | UK. www.ifrs.org

22 Reopening Phase I

• Limited modifications

• IFRS 9 is sound and operational

• Address specific application issues

• Consider interaction of IFRS 9 and insurance project

• Seek to reduce key differences with the FASB’s

classification and measurement model – Both are mixed measurement models

– Both consider characteristics of the instrument and

business model

– Joint deliberations but separate exposure drafts

© IFRS Foundation | 30 Cannon Street | London EC4M 6XH | UK. www.ifrs.org

Scope of possible changes

• Clarify the contractual cash flow characteristics and

business model tests

• Reconsider the need for bifurcation of financial assets

• To address interaction with the insurance project and

align with the FASB’s model, consider: – Introducing a third business model

– Whether some debt instruments should be remeasured

through OCI

• Knock on effects, eg interrelated issues for financial

liabilities, transition and disclosure

23

© IFRS Foundation | 30 Cannon Street | London EC4M 6XH | UK. www.ifrs.org

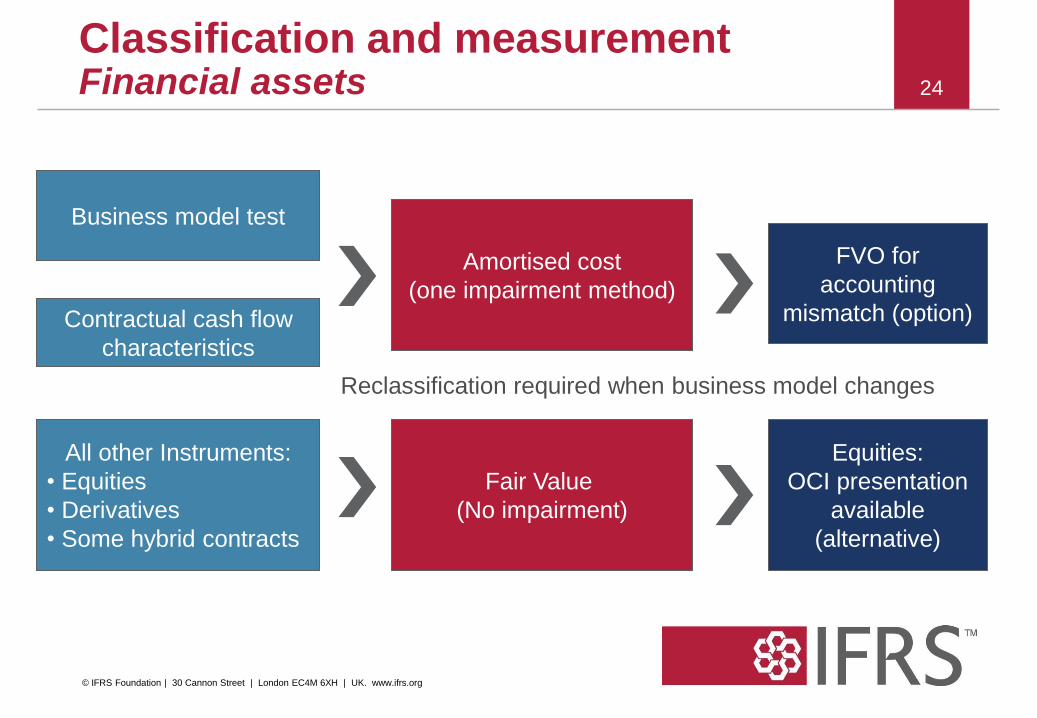

Classification and measurement Financial assets

Fair Value

(No impairment)

Amortised cost

(one impairment method)

Contractual cash flow

characteristics

Business model test

FVO for

accounting

mismatch (option)

All other Instruments:

• Equities

• Derivatives

• Some hybrid contracts

Equities:

OCI presentation

available

(alternative)

Reclassification required when business model changes

24

© IFRS Foundation | 30 Cannon Street | London EC4M 6XH | UK. www.ifrs.org

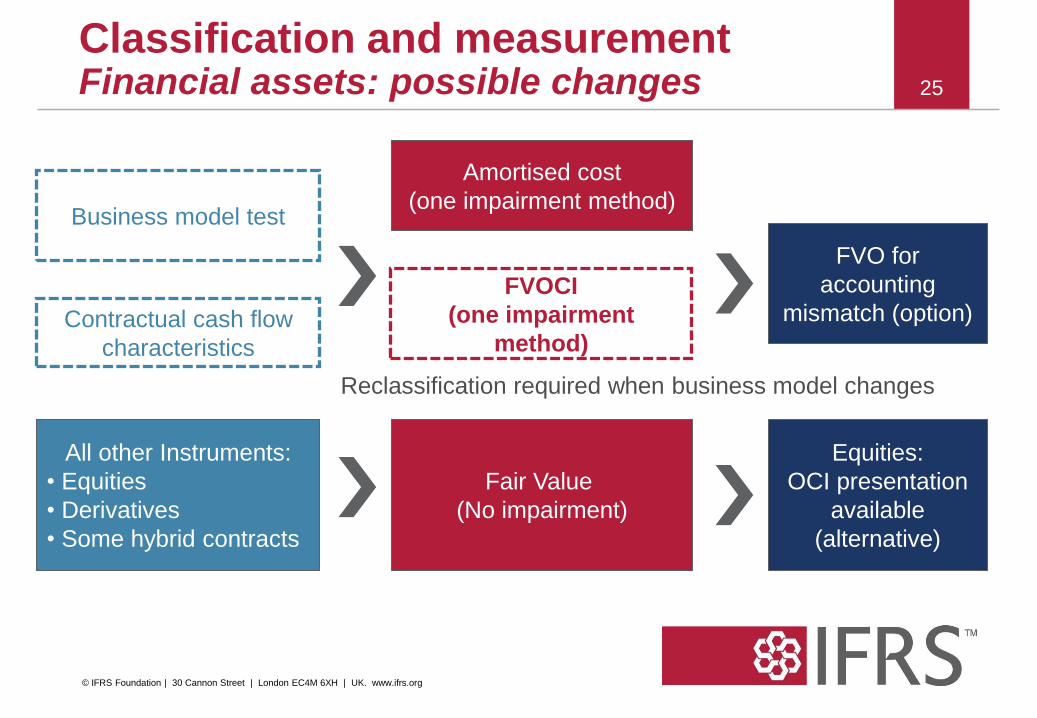

Classification and measurement Financial assets: possible changes

Fair Value

(No impairment)

Amortised cost

(one impairment method)

Contractual cash flow

characteristics

Business model test

FVO for

accounting

mismatch (option)

All other Instruments:

• Equities

• Derivatives

• Some hybrid contracts

Equities:

OCI presentation

available

(alternative)

Reclassification required when business model changes

25

© IFRS Foundation | 30 Cannon Street | London EC4M 6XH | UK. www.ifrs.org

FVOCI

(one impairment

method)

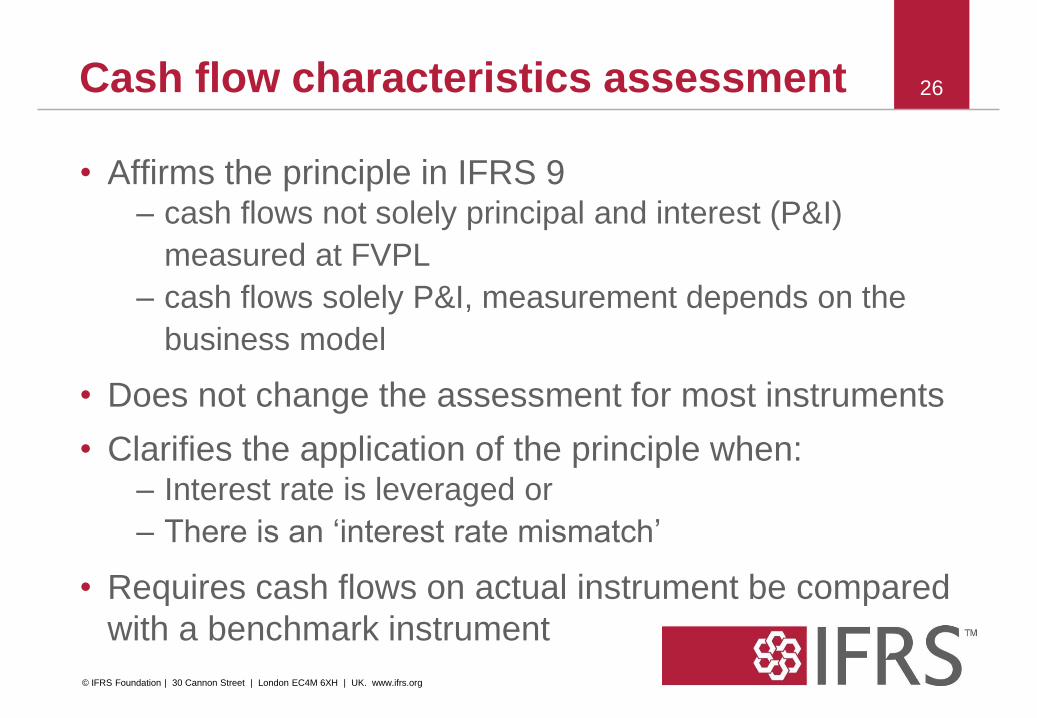

Cash flow characteristics assessment

• Affirms the principle in IFRS 9 – cash flows not solely principal and interest (P&I)

measured at FVPL

– cash flows solely P&I, measurement depends on the

business model

• Does not change the assessment for most instruments

• Clarifies the application of the principle when: – Interest rate is leveraged or

– There is an ‘interest rate mismatch’

• Requires cash flows on actual instrument be compared

with a benchmark instrument

26

© IFRS Foundation | 30 Cannon Street | London EC4M 6XH | UK. www.ifrs.org

27

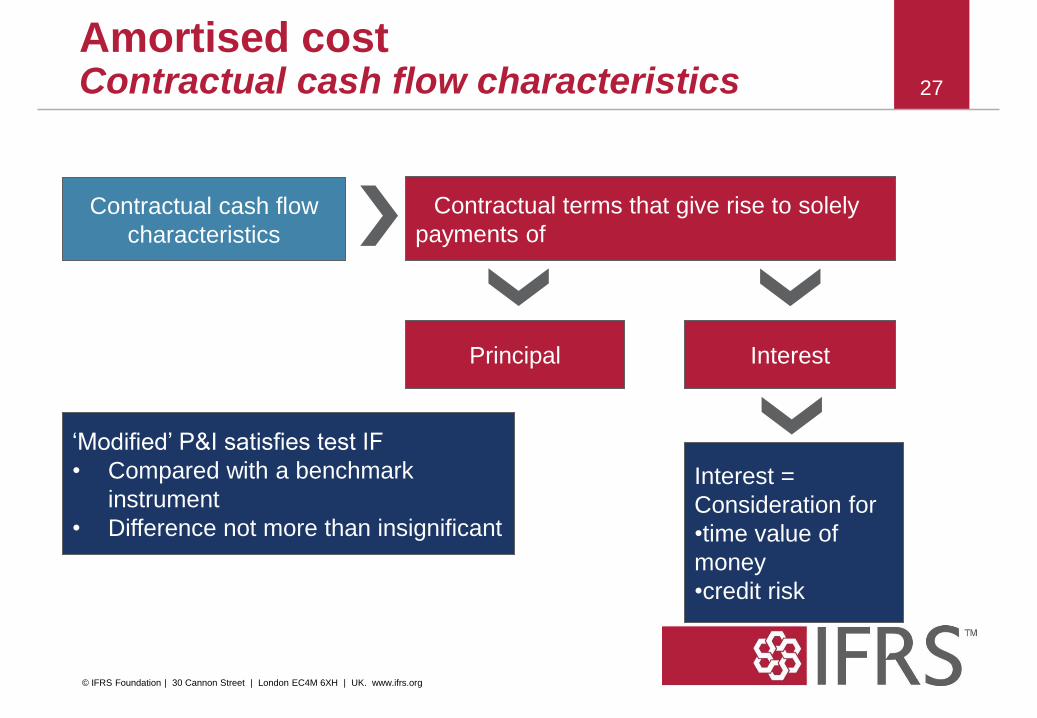

Amortised cost Contractual cash flow characteristics

Contractual terms that give rise to solely

payments of

Contractual cash flow

characteristics

Interest =

Consideration for

•time value of

money

•credit risk

Principal Interest

‘Modified’ P&I satisfies test IF

• Compared with a benchmark

instrument

• Difference not more than insignificant

© IFRS Foundation | 30 Cannon Street | London EC4M 6XH | UK. www.ifrs.org

Amortised cost Business model

• Financial assets qualify for amortised cost if: – Objective of business model is to collect contractual

cash flows

• Clarify the term ‘hold to collect’ by providing additional

application guidance on: – Type of business activities

– Frequency and nature of ‘acceptable’ sales

28

© IFRS Foundation | 30 Cannon Street | London EC4M 6XH | UK. www.ifrs.org

Bifurcation

• 3 primary options considered: – Current asymmetrical model in IFRS 9

– Bifurcation of both assets and liabilities

– No bifurcation

• Several bifurcation methods considered

• Decision to retain the current model

29

© IFRS Foundation | 30 Cannon Street | London EC4M 6XH | UK. www.ifrs.org

Business model/strategy

• IFRS 9 business models – Held to collect contractual cash flows (amortised cost)

– Other (FVTPL)

• Introduced FVOCI: – Interest revenue: effective interest method

– Impairment: same as amortised cost

– Other gain/loss in OCI: recycle to P/L on derecognition

– P/L same as for amortised cost

30

© IFRS Foundation | 30 Cannon Street | London EC4M 6XH | UK. www.ifrs.org

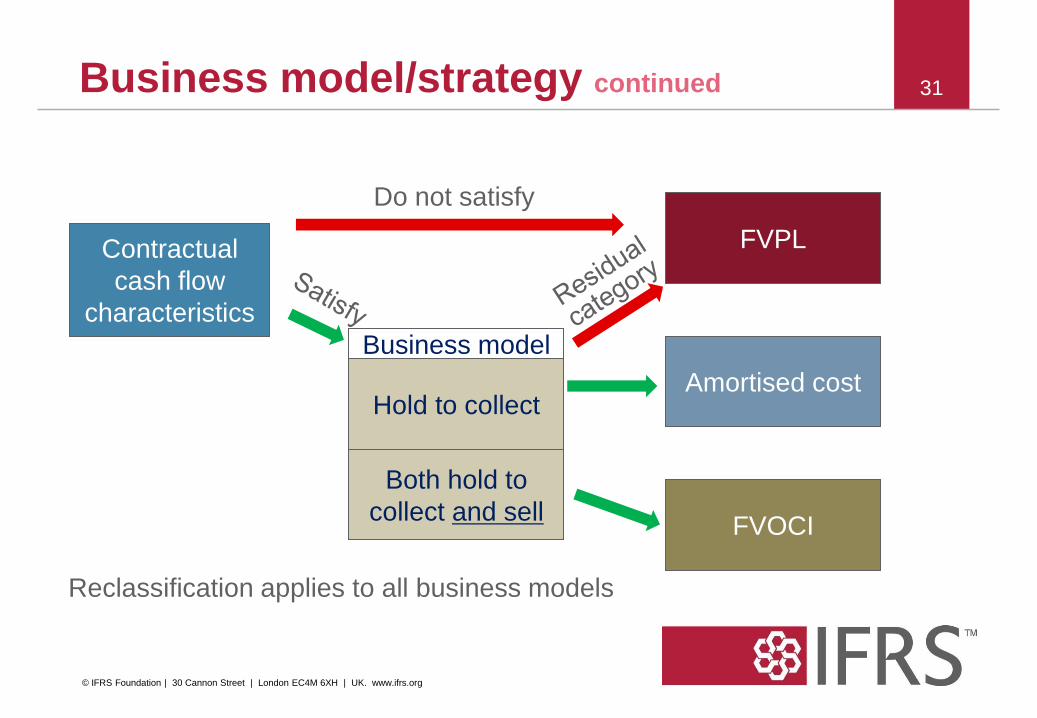

Business model/strategy continued 31

© IFRS Foundation | 30 Cannon Street | London EC4M 6XH | UK. www.ifrs.org

Contractual

cash flow

characteristics

FVPL

Business model

Hold to collect

Both hold to

collect and sell

Amortised cost

FVOCI

Reclassification applies to all business models

Do not satisfy

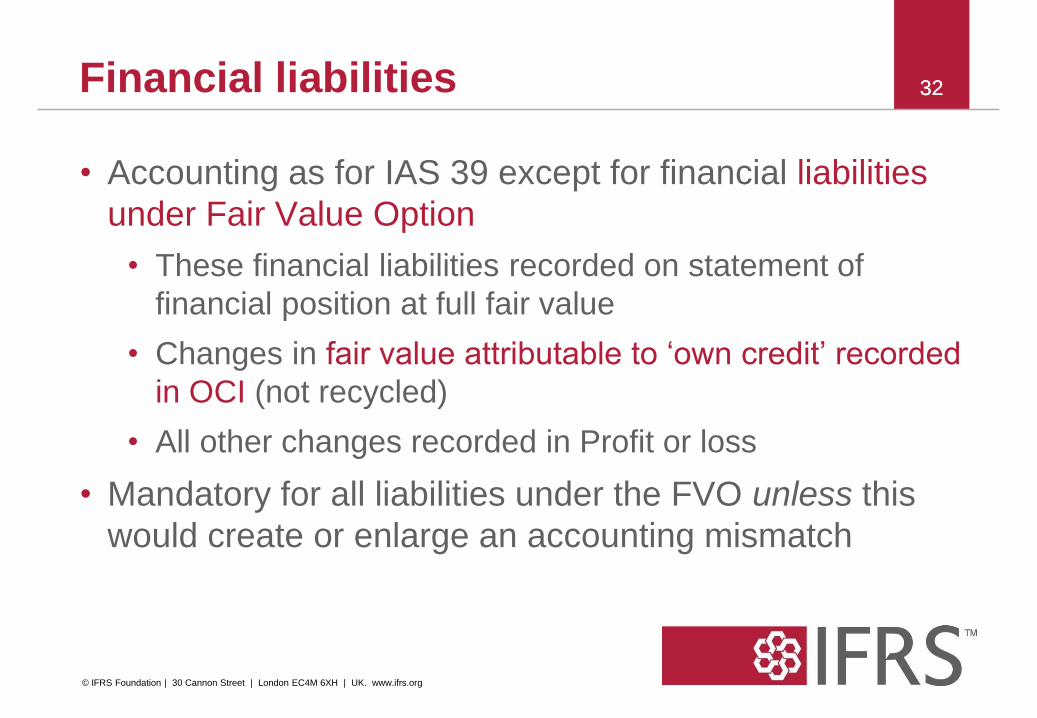

32 32 Financial liabilities

• Accounting as for IAS 39 except for financial liabilities

under Fair Value Option

• These financial liabilities recorded on statement of

financial position at full fair value

• Changes in fair value attributable to ‘own credit’ recorded

in OCI (not recycled)

• All other changes recorded in Profit or loss

• Mandatory for all liabilities under the FVO unless this

would create or enlarge an accounting mismatch

© IFRS Foundation | 30 Cannon Street | London EC4M 6XH | UK. www.ifrs.org

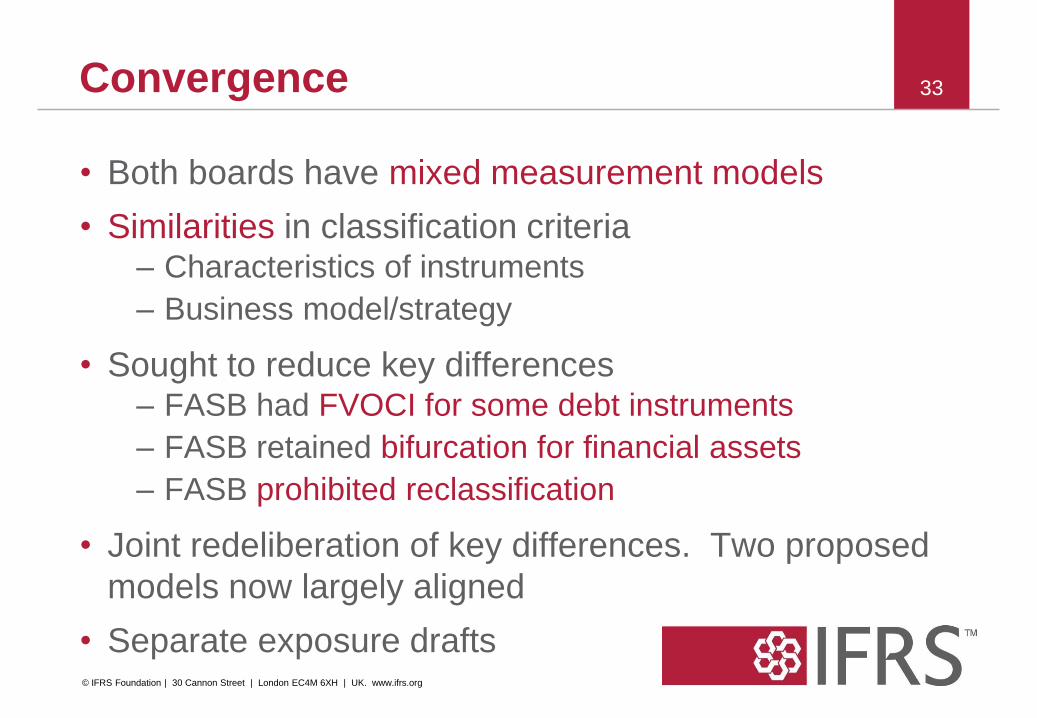

Convergence

• Both boards have mixed measurement models

• Similarities in classification criteria – Characteristics of instruments

– Business model/strategy

• Sought to reduce key differences – FASB had FVOCI for some debt instruments

– FASB retained bifurcation for financial assets

– FASB prohibited reclassification

• Joint redeliberation of key differences. Two proposed

models now largely aligned

• Separate exposure drafts

33

© IFRS Foundation | 30 Cannon Street | London EC4M 6XH | UK. www.ifrs.org

34

© 2012 IFRS Foundation. 30 Cannon Street | London EC4M 6XH | UK. www.ifrs.org

Thank You

35

The requirements are set out in International Financial Reporting Standards (IFRSs), as issued by the IASB at 1 January 2013 with an effective date after 1 January 2013 but not the IFRSs they will replace.

The IFRS Foundation, the authors, the presenters and the publishers do not accept responsibility for loss caused to any person who acts or refrains from acting in reliance on the material in this PowerPoint presentation, whether such loss is caused by negligence or otherwise.

35

© IFRS Foundation | 30 Cannon Street | London EC4M 6XH | UK. www.ifrs.org