Embed Size (px)

Citation preview

ExchangeBulletin

January 6, 2006 Volume 34, Number 1The Constitution and Rules of the Chicago Board Options Exchange, Incorporated (“Exchange”), in certain specific instances,require the Exchange to provide notice to the Exchange membership. To satisfy this requirement, a complimentary copy of theExchange Bulletin, including the Regulatory Bulletin, is delivered by hard copy or e-mail to all effective members on a weeklybasis.

CBOE members are encouraged to receive the Exchange and Regulatory Bulletin and Information Circulars via e-mail. E-mailsubscriptions may be obtained by submitting your name, firm if applicable, mailing address, e-mail address, and phone number, [email protected], or, by contacting the Membership Department by phone, at 312-786-7449. There is no charge for e-maildelivery of the Exchange and Regulatory Bulletin or for Information Circulars. If you do sign up for e-mail delivery, please remem-ber to inform the Membership Department of e-mail address changes.

Additional subscriptions for hard copy delivery after the first complimentary copy may be obtained by submitting your name, firmif any, mailing address, e-mail address and telephone number to: Chicago Board Options Exchange, Accounting Department, 400South LaSalle, Chicago, Illinois 60605, Attention: Bulletin Subscriptions. The cost of an annual subscription (January 1 throughDecember 31) is $200.00 ($100.00 after July 1), payable in advance. The Exchange reserves the right to limit subscriptions by non-members.

For up-to-date Seat Market Quotes, call 312-786-7456 or refer to CBOE.com and click “Seat Market Information” under the “AboutCBOE” tab. For access to the CBOE Member Web Site, please also notify the Membership Department by sending an e-mail [email protected] or by phone at 312-786-7449.

Copyright © 2005 Chicago Board Options Exchange, Incorporated

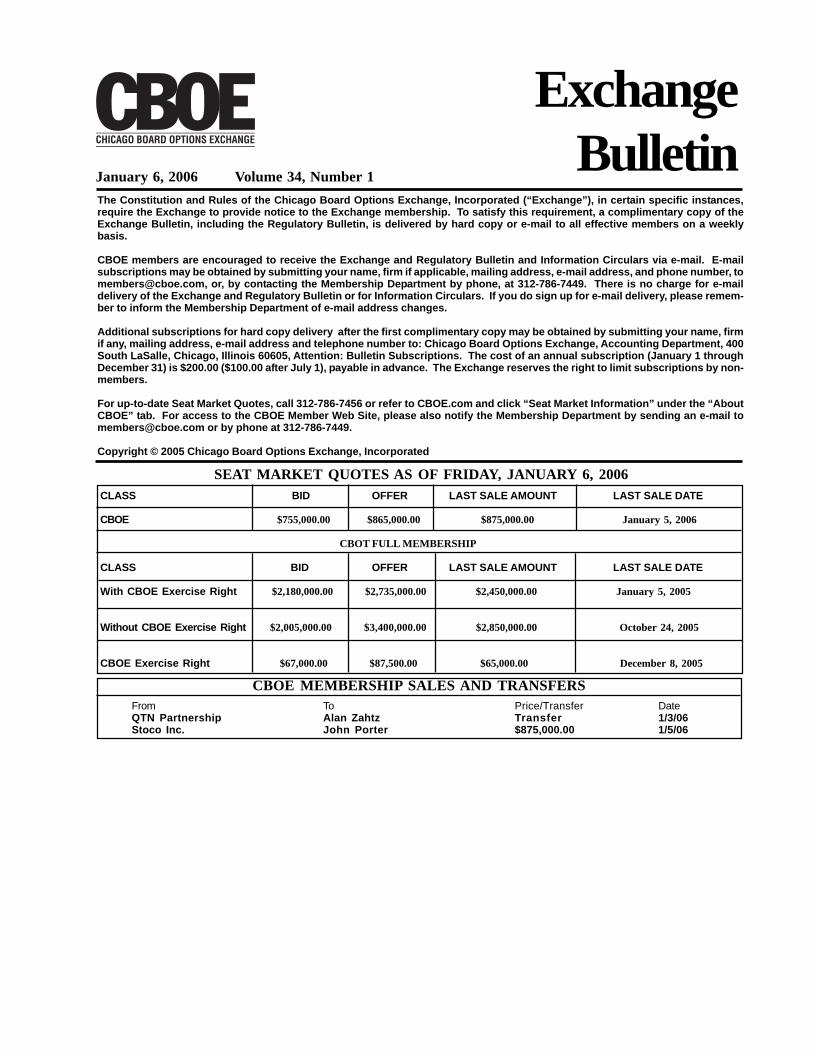

CLASS BID OFFER LAST SALE AMOUNT LAST SALE DATE

CBOE $755,000.00 $865,000.00 $875,000.00 January 5, 2006

CBOT FULL MEMBERSHIP

CLASS BID OFFER LAST SALE AMOUNT LAST SALE DATE

With CBOE Exercise Right $2,180,000.00 $2,735,000.00 $2,450,000.00 January 5, 2005

Without CBOE Exercise Right $2,005,000.00 $3,400,000.00 $2,850,000.00 October 24, 2005

CBOE Exercise Right $67,000.00 $87,500.00 $65,000.00 December 8, 2005

SEAT MARKET QUOTES AS OF FRIDAY, JANUARY 6, 2006

CBOE MEMBERSHIP SALES AND TRANSFERSFrom To Price/Transfer DateQTN Partnership Alan Zahtz Transfer 1/3/06Stoco Inc. John Porter $875,000.00 1/5/06

Page 2 January 6, 2006 Volume 34, Number 1 Chicago Board Options Exchange

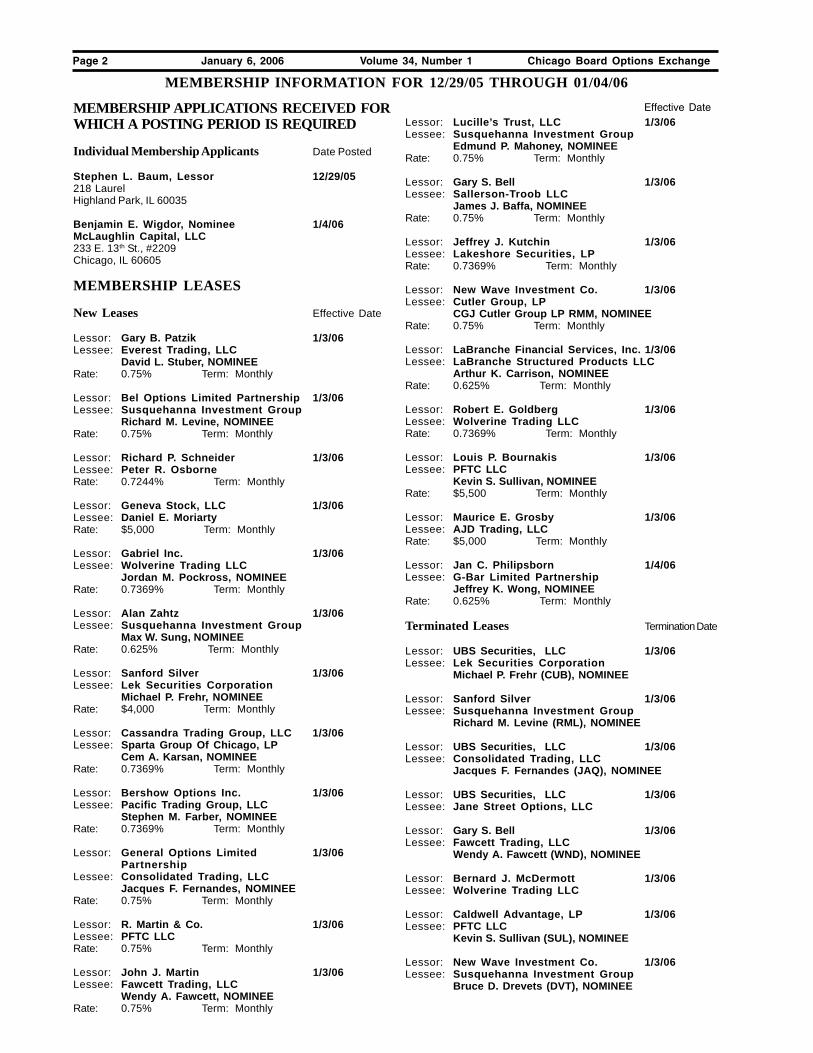

MEMBERSHIP INFORMATION FOR 12/29/05 THROUGH 01/04/06

MEMBERSHIP APPLICATIONS RECEIVED FORWHICH A POSTING PERIOD IS REQUIRED

Individual Membership Applicants Date Posted

Stephen L. Baum, Lessor 12/29/05218 LaurelHighland Park, IL 60035

Benjamin E. Wigdor, Nominee 1/4/06McLaughlin Capital, LLC233 E. 13th St., #2209Chicago, IL 60605

MEMBERSHIP LEASES

New Leases Effective Date

Lessor: Gary B. Patzik 1/3/06Lessee: Everest Trading, LLC

David L. Stuber, NOMINEERate: 0.75% Term: Monthly

Lessor: Bel Options Limited Partnership 1/3/06Lessee: Susquehanna Investment Group

Richard M. Levine, NOMINEERate: 0.75% Term: Monthly

Lessor: Richard P. Schneider 1/3/06Lessee: Peter R. OsborneRate: 0.7244% Term: Monthly

Lessor: Geneva Stock, LLC 1/3/06Lessee: Daniel E. MoriartyRate: $5,000 Term: Monthly

Lessor: Gabriel Inc. 1/3/06Lessee: Wolverine Trading LLC

Jordan M. Pockross, NOMINEERate: 0.7369% Term: Monthly

Lessor: Alan Zahtz 1/3/06Lessee: Susquehanna Investment Group

Max W. Sung, NOMINEERate: 0.625% Term: Monthly

Lessor: Sanford Silver 1/3/06Lessee: Lek Securities Corporation

Michael P. Frehr, NOMINEERate: $4,000 Term: Monthly

Lessor: Cassandra Trading Group, LLC 1/3/06Lessee: Sparta Group Of Chicago, LP

Cem A. Karsan, NOMINEERate: 0.7369% Term: Monthly

Lessor: Bershow Options Inc. 1/3/06Lessee: Pacific Trading Group, LLC

Stephen M. Farber, NOMINEERate: 0.7369% Term: Monthly

Lessor: General Options Limited 1/3/06Partnership

Lessee: Consolidated Trading, LLCJacques F. Fernandes, NOMINEE

Rate: 0.75% Term: Monthly

Lessor: R. Martin & Co. 1/3/06Lessee: PFTC LLCRate: 0.75% Term: Monthly

Lessor: John J. Martin 1/3/06Lessee: Fawcett Trading, LLC

Wendy A. Fawcett, NOMINEERate: 0.75% Term: Monthly

Lessor: Lucille’s Trust, LLC 1/3/06Lessee: Susquehanna Investment Group

Edmund P. Mahoney, NOMINEERate: 0.75% Term: Monthly

Lessor: Gary S. Bell 1/3/06Lessee: Sallerson-Troob LLC

James J. Baffa, NOMINEERate: 0.75% Term: Monthly

Lessor: Jeffrey J. Kutchin 1/3/06Lessee: Lakeshore Securities, LPRate: 0.7369% Term: Monthly

Lessor: New Wave Investment Co. 1/3/06Lessee: Cutler Group, LP

CGJ Cutler Group LP RMM, NOMINEERate: 0.75% Term: Monthly

Lessor: LaBranche Financial Services, Inc. 1/3/06Lessee: LaBranche Structured Products LLC

Arthur K. Carrison, NOMINEERate: 0.625% Term: Monthly

Lessor: Robert E. Goldberg 1/3/06Lessee: Wolverine Trading LLCRate: 0.7369% Term: Monthly

Lessor: Louis P. Bournakis 1/3/06Lessee: PFTC LLC

Kevin S. Sullivan, NOMINEERate: $5,500 Term: Monthly

Lessor: Maurice E. Grosby 1/3/06Lessee: AJD Trading, LLCRate: $5,000 Term: Monthly

Lessor: Jan C. Philipsborn 1/4/06Lessee: G-Bar Limited Partnership

Jeffrey K. Wong, NOMINEERate: 0.625% Term: Monthly

Terminated Leases Termination Date

Lessor: UBS Securities, LLC 1/3/06Lessee: Lek Securities Corporation

Michael P. Frehr (CUB), NOMINEE

Lessor: Sanford Silver 1/3/06Lessee: Susquehanna Investment Group

Richard M. Levine (RML), NOMINEE

Lessor: UBS Securities, LLC 1/3/06Lessee: Consolidated Trading, LLC

Jacques F. Fernandes (JAQ), NOMINEE

Lessor: UBS Securities, LLC 1/3/06Lessee: Jane Street Options, LLC

Lessor: Gary S. Bell 1/3/06Lessee: Fawcett Trading, LLC

Wendy A. Fawcett (WND), NOMINEE

Lessor: Bernard J. McDermott 1/3/06Lessee: Wolverine Trading LLC

Lessor: Caldwell Advantage, LP 1/3/06Lessee: PFTC LLC

Kevin S. Sullivan (SUL), NOMINEE

Lessor: New Wave Investment Co. 1/3/06Lessee: Susquehanna Investment Group

Bruce D. Drevets (DVT), NOMINEE

Effective Date

Page 3 January 6, 2006 Volume 34, Number 1 Chicago Board Options Exchange

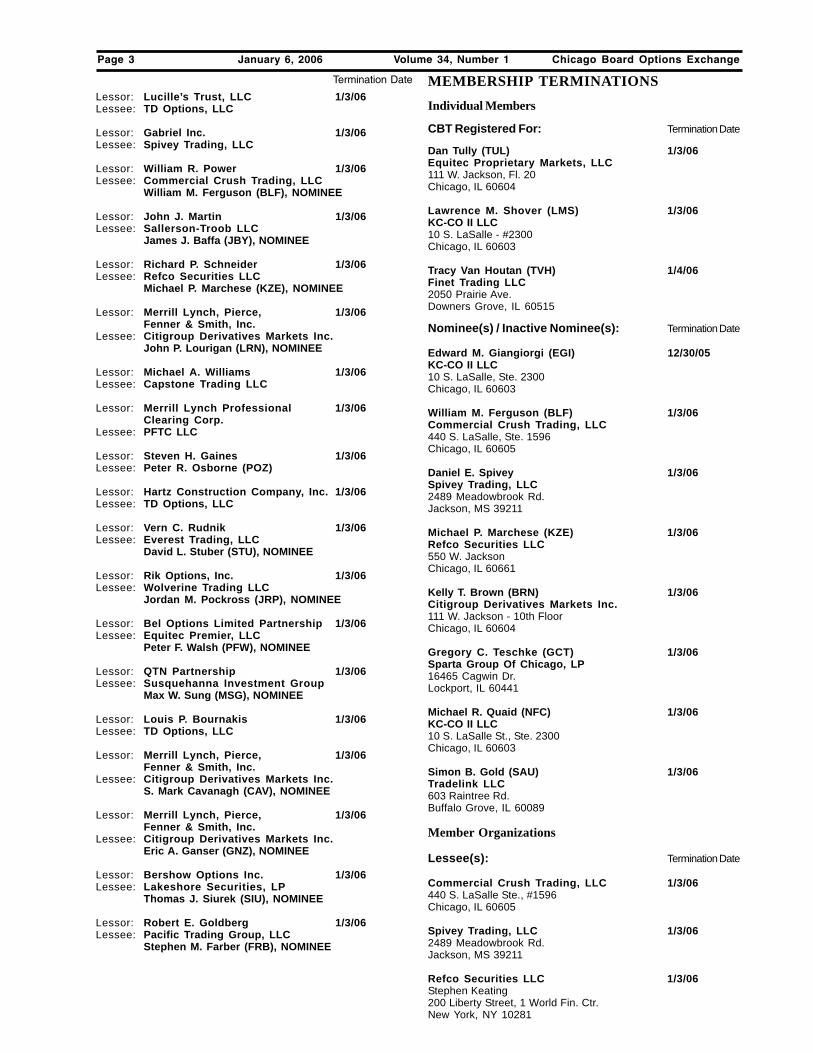

Lessor: Lucille’s Trust, LLC 1/3/06Lessee: TD Options, LLC

Lessor: Gabriel Inc. 1/3/06Lessee: Spivey Trading, LLC

Lessor: William R. Power 1/3/06Lessee: Commercial Crush Trading, LLC

William M. Ferguson (BLF), NOMINEE

Lessor: John J. Martin 1/3/06Lessee: Sallerson-Troob LLC

James J. Baffa (JBY), NOMINEE

Lessor: Richard P. Schneider 1/3/06Lessee: Refco Securities LLC

Michael P. Marchese (KZE), NOMINEE

Lessor: Merrill Lynch, Pierce, 1/3/06Fenner & Smith, Inc.

Lessee: Citigroup Derivatives Markets Inc.John P. Lourigan (LRN), NOMINEE

Lessor: Michael A. Williams 1/3/06Lessee: Capstone Trading LLC

Lessor: Merrill Lynch Professional 1/3/06Clearing Corp.

Lessee: PFTC LLC

Lessor: Steven H. Gaines 1/3/06Lessee: Peter R. Osborne (POZ)

Lessor: Hartz Construction Company, Inc. 1/3/06Lessee: TD Options, LLC

Lessor: Vern C. Rudnik 1/3/06Lessee: Everest Trading, LLC

David L. Stuber (STU), NOMINEE

Lessor: Rik Options, Inc. 1/3/06Lessee: Wolverine Trading LLC

Jordan M. Pockross (JRP), NOMINEE

Lessor: Bel Options Limited Partnership 1/3/06Lessee: Equitec Premier, LLC

Peter F. Walsh (PFW), NOMINEE

Lessor: QTN Partnership 1/3/06Lessee: Susquehanna Investment Group

Max W. Sung (MSG), NOMINEE

Lessor: Louis P. Bournakis 1/3/06Lessee: TD Options, LLC

Lessor: Merrill Lynch, Pierce, 1/3/06Fenner & Smith, Inc.

Lessee: Citigroup Derivatives Markets Inc.S. Mark Cavanagh (CAV), NOMINEE

Lessor: Merrill Lynch, Pierce, 1/3/06Fenner & Smith, Inc.

Lessee: Citigroup Derivatives Markets Inc.Eric A. Ganser (GNZ), NOMINEE

Lessor: Bershow Options Inc. 1/3/06Lessee: Lakeshore Securities, LP

Thomas J. Siurek (SIU), NOMINEE

Lessor: Robert E. Goldberg 1/3/06Lessee: Pacific Trading Group, LLC

Stephen M. Farber (FRB), NOMINEE

MEMBERSHIP TERMINATIONSIndividual Members

CBT Registered For: Termination Date

Dan Tully (TUL) 1/3/06Equitec Proprietary Markets, LLC111 W. Jackson, Fl. 20Chicago, IL 60604

Lawrence M. Shover (LMS) 1/3/06KC-CO II LLC10 S. LaSalle - #2300Chicago, IL 60603

Tracy Van Houtan (TVH) 1/4/06Finet Trading LLC2050 Prairie Ave.Downers Grove, IL 60515

Nominee(s) / Inactive Nominee(s): Termination Date

Edward M. Giangiorgi (EGI) 12/30/05KC-CO II LLC10 S. LaSalle, Ste. 2300Chicago, IL 60603

William M. Ferguson (BLF) 1/3/06Commercial Crush Trading, LLC440 S. LaSalle, Ste. 1596Chicago, IL 60605

Daniel E. Spivey 1/3/06Spivey Trading, LLC2489 Meadowbrook Rd.Jackson, MS 39211

Michael P. Marchese (KZE) 1/3/06Refco Securities LLC550 W. JacksonChicago, IL 60661

Kelly T. Brown (BRN) 1/3/06Citigroup Derivatives Markets Inc.111 W. Jackson - 10th FloorChicago, IL 60604

Gregory C. Teschke (GCT) 1/3/06Sparta Group Of Chicago, LP16465 Cagwin Dr.Lockport, IL 60441

Michael R. Quaid (NFC) 1/3/06KC-CO II LLC10 S. LaSalle St., Ste. 2300Chicago, IL 60603

Simon B. Gold (SAU) 1/3/06Tradelink LLC603 Raintree Rd.Buffalo Grove, IL 60089

Member Organizations

Lessee(s): Termination Date

Commercial Crush Trading, LLC 1/3/06440 S. LaSalle Ste., #1596Chicago, IL 60605

Spivey Trading, LLC 1/3/062489 Meadowbrook Rd.Jackson, MS 39211

Refco Securities LLC 1/3/06Stephen Keating200 Liberty Street, 1 World Fin. Ctr.New York, NY 10281

Termination Date

Page 4 January 6, 2006 Volume 34, Number 1 Chicago Board Options Exchange

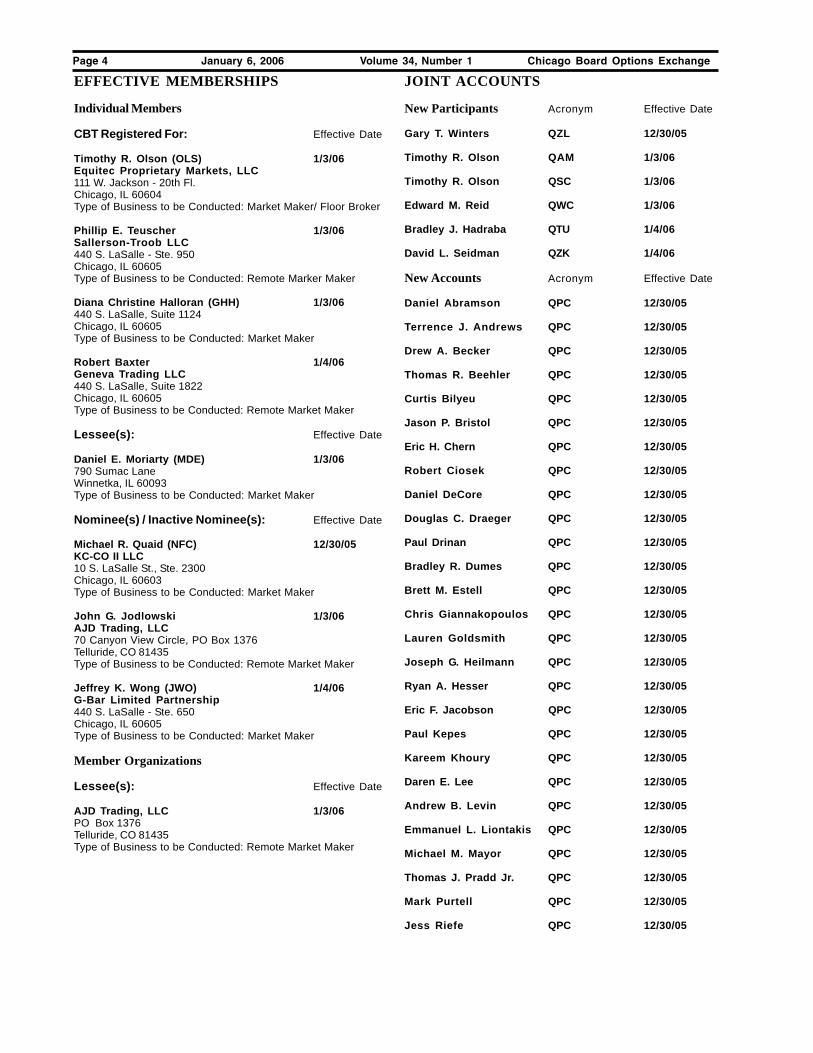

EFFECTIVE MEMBERSHIPS

Individual Members

CBT Registered For: Effective Date

Timothy R. Olson (OLS) 1/3/06Equitec Proprietary Markets, LLC111 W. Jackson - 20th Fl.Chicago, IL 60604Type of Business to be Conducted: Market Maker/ Floor Broker

Phillip E. Teuscher 1/3/06Sallerson-Troob LLC440 S. LaSalle - Ste. 950Chicago, IL 60605Type of Business to be Conducted: Remote Marker Maker

Diana Christine Halloran (GHH) 1/3/06440 S. LaSalle, Suite 1124Chicago, IL 60605Type of Business to be Conducted: Market Maker

Robert Baxter 1/4/06Geneva Trading LLC440 S. LaSalle, Suite 1822Chicago, IL 60605Type of Business to be Conducted: Remote Market Maker

Lessee(s): Effective Date

Daniel E. Moriarty (MDE) 1/3/06790 Sumac LaneWinnetka, IL 60093Type of Business to be Conducted: Market Maker

Nominee(s) / Inactive Nominee(s): Effective Date

Michael R. Quaid (NFC) 12/30/05KC-CO II LLC10 S. LaSalle St., Ste. 2300Chicago, IL 60603Type of Business to be Conducted: Market Maker

John G. Jodlowski 1/3/06AJD Trading, LLC70 Canyon View Circle, PO Box 1376Telluride, CO 81435Type of Business to be Conducted: Remote Market Maker

Jeffrey K. Wong (JWO) 1/4/06G-Bar Limited Partnership440 S. LaSalle - Ste. 650Chicago, IL 60605Type of Business to be Conducted: Market Maker

Member Organizations

Lessee(s): Effective Date

AJD Trading, LLC 1/3/06PO Box 1376Telluride, CO 81435Type of Business to be Conducted: Remote Market Maker

JOINT ACCOUNTS

New Participants Acronym Effective Date

Gary T. Winters QZL 12/30/05

Timothy R. Olson QAM 1/3/06

Timothy R. Olson QSC 1/3/06

Edward M. Reid QWC 1/3/06

Bradley J. Hadraba QTU 1/4/06

David L. Seidman QZK 1/4/06

New Accounts Acronym Effective Date

Daniel Abramson QPC 12/30/05

Terrence J. Andrews QPC 12/30/05

Drew A. Becker QPC 12/30/05

Thomas R. Beehler QPC 12/30/05

Curtis Bilyeu QPC 12/30/05

Jason P. Bristol QPC 12/30/05

Eric H. Chern QPC 12/30/05

Robert Ciosek QPC 12/30/05

Daniel DeCore QPC 12/30/05

Douglas C. Draeger QPC 12/30/05

Paul Drinan QPC 12/30/05

Bradley R. Dumes QPC 12/30/05

Brett M. Estell QPC 12/30/05

Chris Giannakopoulos QPC 12/30/05

Lauren Goldsmith QPC 12/30/05

Joseph G. Heilmann QPC 12/30/05

Ryan A. Hesser QPC 12/30/05

Eric F. Jacobson QPC 12/30/05

Paul Kepes QPC 12/30/05

Kareem Khoury QPC 12/30/05

Daren E. Lee QPC 12/30/05

Andrew B. Levin QPC 12/30/05

Emmanuel L. Liontakis QPC 12/30/05

Michael M. Mayor QPC 12/30/05

Thomas J. Pradd Jr. QPC 12/30/05

Mark Purtell QPC 12/30/05

Jess Riefe QPC 12/30/05

Page 5 January 6, 2006 Volume 34, Number 1 Chicago Board Options Exchange

Terminated Participants Acronym Termination Date

Dan Tully QAM 1/3/06

Dan Tully QSC 1/3/06

Kelly T. Brown QCM 1/3/06

Kelly T. Brown QKD 1/3/06

Kelly T. Brown QNT 1/3/06

Lawrence M. Shover QII 1/3/06

Lawrence M. Shover QQD 1/3/06

Lawrence M. Shover QVK 1/3/06

Gregory C. Teschke QTU 1/3/06

Simon B. Gold QGK 1/3/06

CHANGES IN MEMBERSHIP STATUS

Individual Members Effective Date

Daniel F. McHugh 1/3/06From: CBT Registered For KC-CO II LLC; Market MakerTo: Nominee For KC-CO II LLC; Market Maker

Carl M. Peller 1/3/06From: CBT Registered For Sparta Group Of Chicago, LP;

Market MakerTo: Nominee For Sparta Group Of Chicago, LP; Market

Maker

Bernard J. McDermott III 1/3/06From: LessorTo: Owner; Remote Market Maker

Cem A. Karsan 1/3/06From: CBT Registered For Sparta Group Of Chicago, LP;

Market MakerTo: Nominee For Sparta Group Of Chicago, LP; Market

Maker

Jeremy T. Nau 1/3/06From: CBT Registered For AB Financial LLC; Market MakerTo: Nominee For AB Financial LLC; Market Maker

David L. Seidman 1/4/06From: Nominee For BOTTA Capital Management LLC; Market

Maker/ Floor BrokerTo: Nominee For Zydeco Trading LLC; Market Maker

Member Organizations Effective Date

UBS Securities, LLC 1/4/06From: Lessor/ Owner/ Non-Member Customer Business/

Member Organization Affiliated with a CBT RegisteredFor; Associated with a Market Maker/ Floor Broker/Remote Market Maker

To: Owner/ Non-Member Customer Business/ MemberOrganization Affiliated with a CBT Registered For;Associated with a Market Maker/ Floor Broker/ RemoteMarket Maker

Sallerson-Troob LLC 1/3/06From: Lessee/ Member Organization Affiliated with a CBT

Registered For; Associated with a Market Maker/ FloorBroker

To: Lessee/ Member Organization Affiliated with a CBTRegistered For; Associated with a Market Maker/ FloorBroker/ Remote Market Maker

Capstone Trading LLC 1/4/06From: Lessee; Associated with a Market Maker/ Remote

Market MakerTo: Lessee; Associated with a Market Maker

.

Effective Date

RESEARCH CIRCULARSThe following Research Circulars were distributed between January 3 and January 5, 2006. If you wish to read the entire document, pleaserefer to the CBOE website at www.cboe.com and click on the “Trading Tools” Tab. New listings and series information is also available in theTrading Tools section of the website. For questions regarding information discussed in a Research Circular, please call The Options ClearingCorporation at 1-888-OPTIONS.Research Circular #RS06-002January 3, 2006Yellow Roadway Corporation (“YELL/YUX/VYX/YBQ”)Name and Underlying Symbol Change to:YRC Worldwide, Inc. (“YRCW”)Effective Date: January 4, 2006

Research Circular #R06-003January 3, 2006NDCHealth Corporation (“NDC”) Proposed Mergerwith Per-Se Technologies, Inc. (“PSTI”)

Research Circular #RS05-765January 4, 2006*****UPDATE*****UPDATE*****UPDATE*****IVAX Corporation (“IVX/OIV/YIV & adj. YXO/OYA”)Proposed Election Merger with Teva PharmaceuticalIndustries Limited (“TEVA/TVQ/OQV/WTX”)

Research Circular #RS06-005January 4, 2006Maxim Pharmaceuticals, Inc. (“MAXM/YQI”) MergerCOMPLETED with EpiCept Corporation (“EPCT”)

Research Circular #RS06-008January 5, 2006Psychiatric Solutions, Inc. (“PSYS/BYU”)2-for-1 Stock SplitEx-Distribution Date: January 10, 2006

POSITION LIMIT CIRCULARSPursuant to Exchange Rule 4.11, the Exchange issued the below listed Position Limit Circular on December 30, 2005. The complete circulars areavailable from the Department of Market Regulation, in the data information bins on the 2nd Floor of the Exchange, and on the CBOE website atcboe.com under the “Market Data” tab.

To receive regular updates of the position limit list via fax, contact Candice Nickrand at (312) 786-7730. Questions concerning position and exerciselimits may be directed to the Department of Market Regulation to Dan Earner at (312) 786-7059 or Tim Mac Donald at (312) 786-7706.Position Limit Circular PL05-58December 30, 2005MBNA Corporation (“KRB/VZK/WK”) merger completed withBank of America Corporation (“BAC/VBA/WBA”)Effective Date January 3, 2006

________________________________________________________________________________________________________ January 11, 2006 Volume RB17, Number 2

The Constitution and Rules of the Chicago Board Options Exchange, Incorporated (“Exchange”), in certain specific instances, require the Exchange to provide notice to the membership. The weekly Regulatory Bulletin is delivered to all effective members to satisfy this requirement. Copyright © 2006 Chicago Board Options Exchange, Incorporated.

_______________ Regulatory Circulars

_______________________________________________________ Regulatory Circular RG05-130 Circular RG05-130 (RG04-132 Revised) To: Members and Member Firms From: Research & Planning Date: December 29, 2005 Re: Monthly “Fair Value” Settlement of CME Stock Index Futures and

Options and Year End Closing Rotations. The Chicago Mercantile Exchange (CME) conducts a special “fair value” 1 settlement procedure for domestic stock index futures and options on the last business day of each month. On these days, the CME calculates the daily settlement price for its domestic stock index futures and options contracts on the basis of their fair value relative to the daily close of the underlying cash index as reflected at 3:15 p.m. (Chicago time). CBOE conducts special “closing rotations” on the days in which special settlement procedures are employed at the CME in order to allow the Exchange’s domestic broad-based index options to be valued on the same “fair value” basis as related index futures. Accordingly, on December 30, 2005, CBOE shall conduct special month end closing rotations in the following options contracts:

S&P 500 Index (SPX) S&P 100 Index (OEX) S&P 100 Index (XEO) Nasdaq-100 Index (NDX) Mini-NDX Index (MNX) Mini-S&P 500 Index (XSP)

1 “Fair value” of futures represents the price at which futures should theoretically trade in relation to cash index values in the absence of transaction costs. It is typically calculated as a function of the underlying index value plus the financing cost of owning the underlying stock portfolio, less dividends paid up to the futures expiration.

2

Special closing rotations are held for the sole purpose of determining theoretical fair values for these option contracts. No orders, including orders resting in the Exchange's limit order book, are allowed to trade during these special closing rotations. Please be advised that there will be no end of year trading closing rotation in the classes listed above. Also, please be aware that pursuant to Exchange Rule 11.1, as the close of trading for OEX options will be 3:15 p.m. (CT) on December 30, 2005, “exercise advices” must be submitted to the Exchange no later than 3:20 p.m. (CT). Please Note: No special closing rotation will be conducted in the following classes.

Nasdaq-100 Tracking Stock (QQQQ) Dow Jones Industrial Average Index (DJX) iShares S&P 100 Index Fund (OEF) DIAMONDS Trust (DIA) Russell 2000 Index (RUT) S&P SmallCap Index (SML) iShares Russell 2000 Index Fund (IWM)

Equity Year End Closing Rotation on December 30, 2005 Pursuant to Rule 6.2, Interpretation .05, a closing rotation will be held in all equity and narrow-based index option classes on Friday, December 30, 2005. The only orders that may participate in the closing rotation are those orders that are received prior to the normal close of the trading day, i.e. 3:02 p.m. CST for equity and narrow-based index options. However, for equity options, the rotation may commence at or after the 3:02 p.m. CST close once the closing price of the stock in its primary market has been established. Questions concerning the above may be directed to a member of the Floor Officials Committee, Kerry Winters (312) 786-7312 or Dan Earner (312) 786-7059. ____________________________________________________________

Regulatory Circular RG05-131 Date: December 30, 2005 To: The Membership From: Financial Planning Committee Subject: Fee Reductions for January 2006

3

CBOE has averaged approximately 1,704,000 contracts per day (CPD) during the period July 2004 through December 2005. Per the Prospective Fee Reduction Program, Market-Maker and DPM transaction fees and floor brokerage fees will be reduced by 30% per contract from standard rates during January 2006 (December 2005 discounts were 25%). Standard Jan. ‘06 Fee Rate Rate____ Equities Market-Maker Trans. Fee 22 cents 15.4 cents Equities DPM Trans. Fee 12 cents 8.4 cents QQQQ, SPY, DIA, DJX & Indexes Mrkt.-Maker/DPM Trans. Fee 24 cents (1) 16.8 cents (1) Mini-SPX (XSP) Market-Maker Trans. Fee 15 cents waived until 2/1/06 Floor Brokerage Fee 4 cents 2.8 cents Floor Brokerage Fee - Mini-SPX (XSP) 4 cents waived until 2/1/06 (1) Above rates exclude a 10 cents license fee surcharge for the following products:

• Dow Jones indexes, excluding DJX and DIA • Mini Nasdaq 100 (MNX) • Nasdaq 100 (NDX) • Russell 2000 cash-settled index (RUT)

Please call Ermer Love (312-786-7032) if you have any questions. ____________________________________________________________

Regulatory Circular RG05-132 To: Members and Member Organizations

From: Regulatory Services Division

Re: Prearranged Trades

Date: December 30, 2005

The Exchange wishes to restate its policy concerning prearranged trading. Members and Member Organizations are cautioned that any purchase or sale transaction or series of transactions, coupled with an agreement, arrangement or understanding, directly or indirectly to reverse such transaction which is not done for a legitimate economic purpose or without subjecting the transactions to market risk, violate Exchange Rules and may be inconsistent with various provisions of the Securities Exchange Act of 1934, as amended, and rules thereunder (the “Act”). All transactions must be effected in accordance with applicable trading rules, must be subject to risk of the market, and must be reported for dissemination over the tape.

4

Section 9(a)(1) of the Act prohibits any member of a national securities exchange, for the purpose of creating a false or misleading appearance of active trading in any security registered on a national securities exchange, or a false or misleading appearance with respect to the market for any such security, (A) from effecting any transaction in such security which involves no change in the beneficial ownership thereof, or (B) from entering an order or orders for the purchase of such security with the knowledge that an order or orders of substantially the same size, at substantially the same time, and at substantially the same price, for the sale of any such security, has been or will be entered by or for the same or different parties, or (C) from entering any order or orders for the sale of any such security with the knowledge that an order or orders of substantially the same size, at substantially the same time, and at substantially the same price, for the purchase of such security, has been or will be entered by or for the same or different parties. In order for transactions not to be viewed as prearranged trades, there should be two independent transactions, and the price of each should be independently established. At the time of the first transaction there should be no guarantee or assurance of the price of the second. The period of time between the two transactions may not of itself determine whether the subsequent entry of an order that reversed the buyer and seller in the first transaction into the seller and buyer on the second transaction had been effected at the risk of the market. The Exchange also believes that prearranged trading could result in a violation of CBOE Rule 4.1, which prohibits conduct inconsistent with just and equitable principles of trade, Rule 6.45 which addresses the priority of bids and offers, or Rule 10b-5 of the Act, which prohibits any act, practice, or course of business which operates or would operate as a fraud or deceit upon any person, in connection with the purchase or sale of any security, respectively. Any questions may be directed to Steve Slawinski (312) 786-7744. (Regulatory Circulars RG92-51, RG93-36, RG95-48, RG96-99 and RG97-166 Reissued, RG99-129 Revised, RG99-173 Reissued, RG00-91 Revised, 01-126 Revised) ____________________________________________________________

Regulatory Circular RG06-01

To: Members and Member Firms - Compliance Departments

From: Regulatory Services Division/Legal Division

Re: Extension of Rule 6.45A(b) and Applicability of Section 11(a)

(1)

Date: January 3, 2006

A proposed rule change to extend the duration of paragraph (b) of Rule 6.45A, Priority and Allocation of Equity Option Trades on the CBOE Hybrid System, through March 14, 2006 has become effective (see Release 34-52957; SR-CBOE-2005-102). Paragraph (b), which would have otherwise expired on December 14, 2005, relates to the allocation of orders represented in open outcry. This is merely an extension of the duration of the effectiveness of

5

paragraph (b), no other changes are being made at this time. In order to effect proprietary transactions on the floor of the Exchange, in addition to complying with the requirements of CBOE Rule 6.45A(b), members are also required to comply with the requirements of Section 11(a)(1) of the Securities Exchange Act of 1934 (the “Exchange Act”), 15 U.S.C. 78k(a)(1), or qualify for an exemption. Section 11(a)(1) of the Exchange Act restricts securities transactions of a member of any national securities exchange effected on that exchange for (i) the member’s own account, (ii) the account of a person associated with the member, or (iii) an account over which the member or a person associated with the member exercises discretion, unless a specific exemption is available.

Members seeking further information as to the previous extension of the duration of CBOE Rule 6.45A(b), and the application of Section 11(a)(1) of the Exchange Act or any of the exemptions from the prohibitions of that section, should refer to Regulatory Circulars RG05-102 and RG05-103 (both issued November 2, 2005), or contact Angelo Evangelou, Legal Division, at (312) 786-7464.

____________________________________________________________Regulatory Circular RG06-02

Date: January 3, 2006 From: Market Operations Department Re: Restrictions on Transactions in Mercury Interactive (MERQE) Mercury Interactive (RQB, VRD, YQR), will be delisted from the Nasdaq after the close today, January 3, 2006. Trading on the CBOE in existing series of RQB options will be subject to the following restrictions effective January 4, 2006. Only closing transactions may be affected in any series of RQB options except for (i) opening transactions by Market-Makers executed to accommodate closing transactions of other market participants and (ii) opening transactions by CBOE member organizations to facilitate the closing transactions of public customers executed as crosses pursuant to and in accordance with CBOE Rule 6.74(b) or (d). The execution of opening transactions in RQB options, except as permitted above, and/or the misrepresentation as to whether an order is opening or closing, will constitute a violation of CBOE rules, and may result in disciplinary action. Member organizations should ensure that they have appropriate procedures in place to prevent their customers from entering opening orders in this restricted option class. There are no restrictions in place with respect to the exercise of RQB options. The provisions of this circular apply to any options on RQB traded on CBOE. Any questions regarding this circular may directed to Kerry Winters at (312) 786-7312 or Joanne Heenan-Hustad at (312) 786-7786. ____________________________________________________________

6

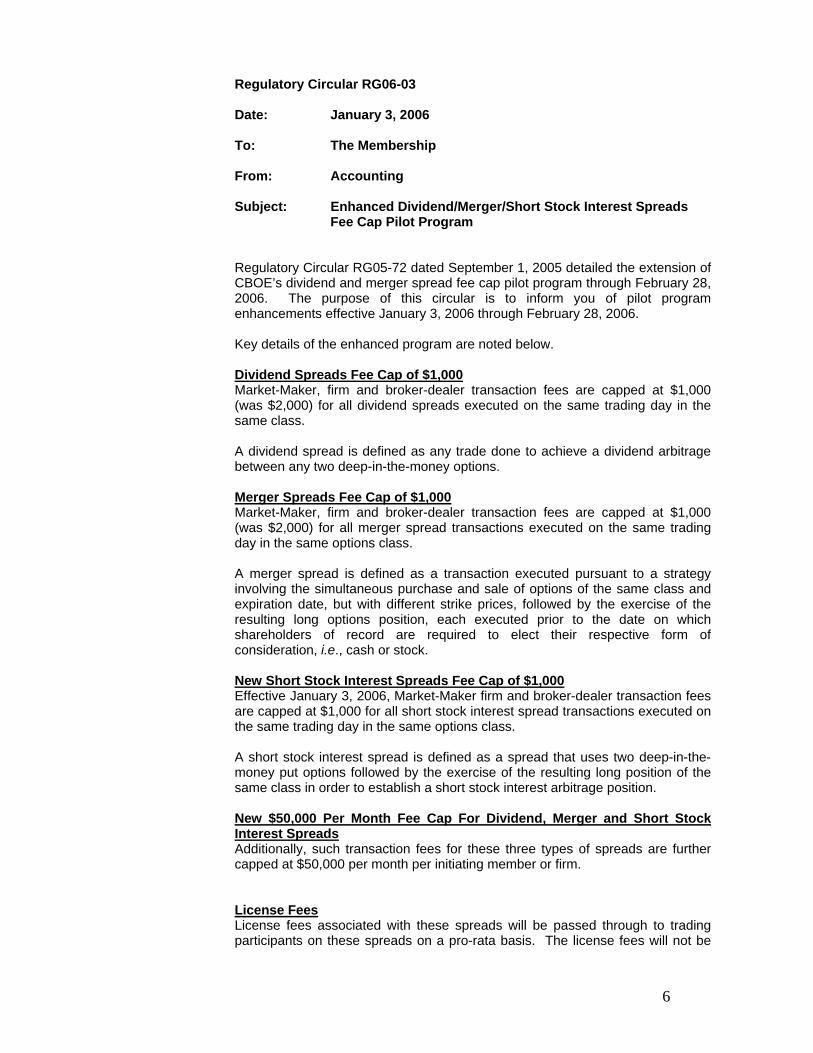

Regulatory Circular RG06-03

Date: January 3, 2006 To: The Membership From: Accounting Subject: Enhanced Dividend/Merger/Short Stock Interest Spreads

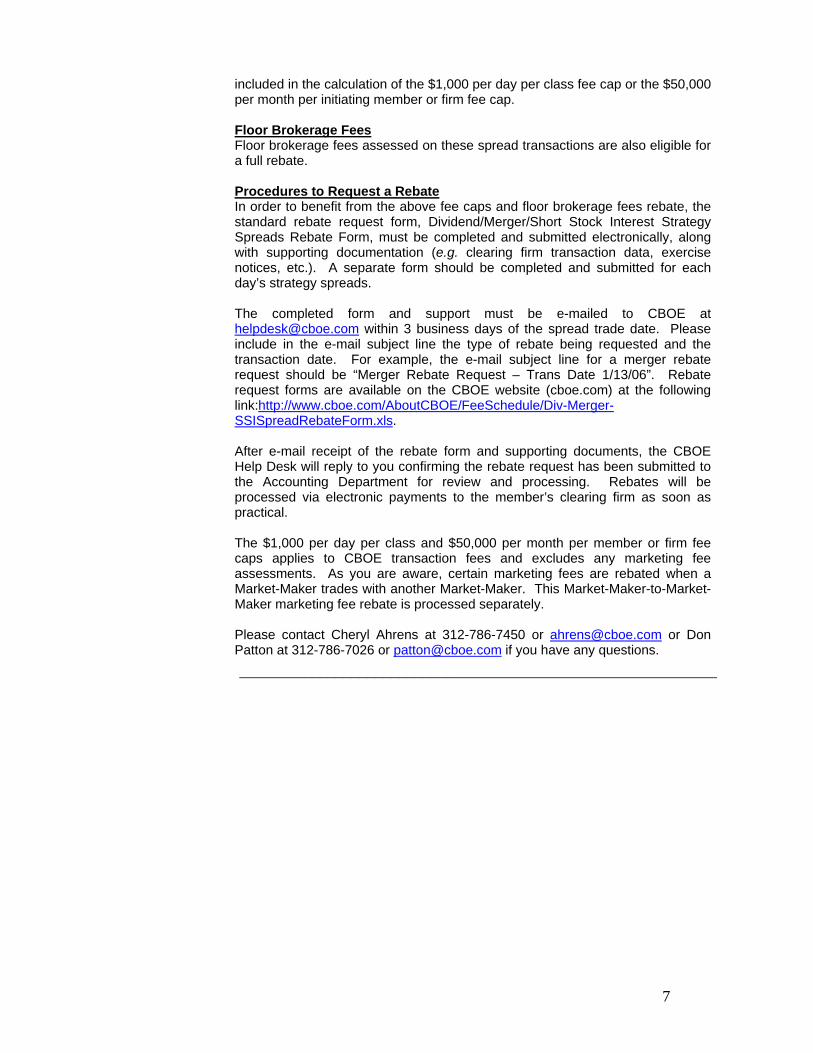

Fee Cap Pilot Program Regulatory Circular RG05-72 dated September 1, 2005 detailed the extension of CBOE’s dividend and merger spread fee cap pilot program through February 28, 2006. The purpose of this circular is to inform you of pilot program enhancements effective January 3, 2006 through February 28, 2006. Key details of the enhanced program are noted below. Dividend Spreads Fee Cap of $1,000 Market-Maker, firm and broker-dealer transaction fees are capped at $1,000 (was $2,000) for all dividend spreads executed on the same trading day in the same class. A dividend spread is defined as any trade done to achieve a dividend arbitrage between any two deep-in-the-money options. Merger Spreads Fee Cap of $1,000 Market-Maker, firm and broker-dealer transaction fees are capped at $1,000 (was $2,000) for all merger spread transactions executed on the same trading day in the same options class. A merger spread is defined as a transaction executed pursuant to a strategy involving the simultaneous purchase and sale of options of the same class and expiration date, but with different strike prices, followed by the exercise of the resulting long options position, each executed prior to the date on which shareholders of record are required to elect their respective form of consideration, i.e., cash or stock. New Short Stock Interest Spreads Fee Cap of $1,000 Effective January 3, 2006, Market-Maker firm and broker-dealer transaction fees are capped at $1,000 for all short stock interest spread transactions executed on the same trading day in the same options class. A short stock interest spread is defined as a spread that uses two deep-in-the-money put options followed by the exercise of the resulting long position of the same class in order to establish a short stock interest arbitrage position. New $50,000 Per Month Fee Cap For Dividend, Merger and Short Stock Interest Spreads Additionally, such transaction fees for these three types of spreads are further capped at $50,000 per month per initiating member or firm. License Fees License FeesLicense fees associated with these spreads will be passed through to trading participants on these spreads on a pro-rata basis. The license fees will not be

7

included in the calculation of the $1,000 per day per class fee cap or the $50,000 per month per initiating member or firm fee cap. or Brokerage Fees Floor Brokerage FeesFloor brokerage fees assessed on these spread transactions are also eligible for a full rebate. Procedures to Request a Rebate Procedures to Request a RebateIn order to benefit from the above fee caps and floor brokerage fees rebate, the standard rebate request form, Dividend/Merger/Short Stock Interest Strategy Spreads Rebate Form, must be completed and submitted electronically, along with supporting documentation (e.g. clearing firm transaction data, exercise notices, etc.). A separate form should be completed and submitted for each day’s strategy spreads. The completed form and support must be e-mailed to CBOE at [email protected] within 3 business days of the spread trade date. Please include in the e-mail subject line the type of rebate being requested and the transaction date. For example, the e-mail subject line for a merger rebate request should be “Merger Rebate Request – Trans Date 1/13/06”. Rebate request forms are available on the CBOE website (cboe.com) at the following link:http://www.cboe.com/AboutCBOE/FeeSchedule/Div-Merger-SSISpreadRebateForm.xls. After e-mail receipt of the rebate form and supporting documents, the CBOE Help Desk will reply to you confirming the rebate request has been submitted to the Accounting Department for review and processing. Rebates will be processed via electronic payments to the member’s clearing firm as soon as practical. The $1,000 per day per class and $50,000 per month per member or firm fee caps applies to CBOE transaction fees and excludes any marketing fee assessments. As you are aware, certain marketing fees are rebated when a Market-Maker trades with another Market-Maker. This Market-Maker-to-Market- Maker marketing fee rebate is processed separately. Please contact Cheryl Ahrens at 312-786-7450 or [email protected] or Don Patton at 312-786-7026 or [email protected] if you have any questions. ____________________________________________________________

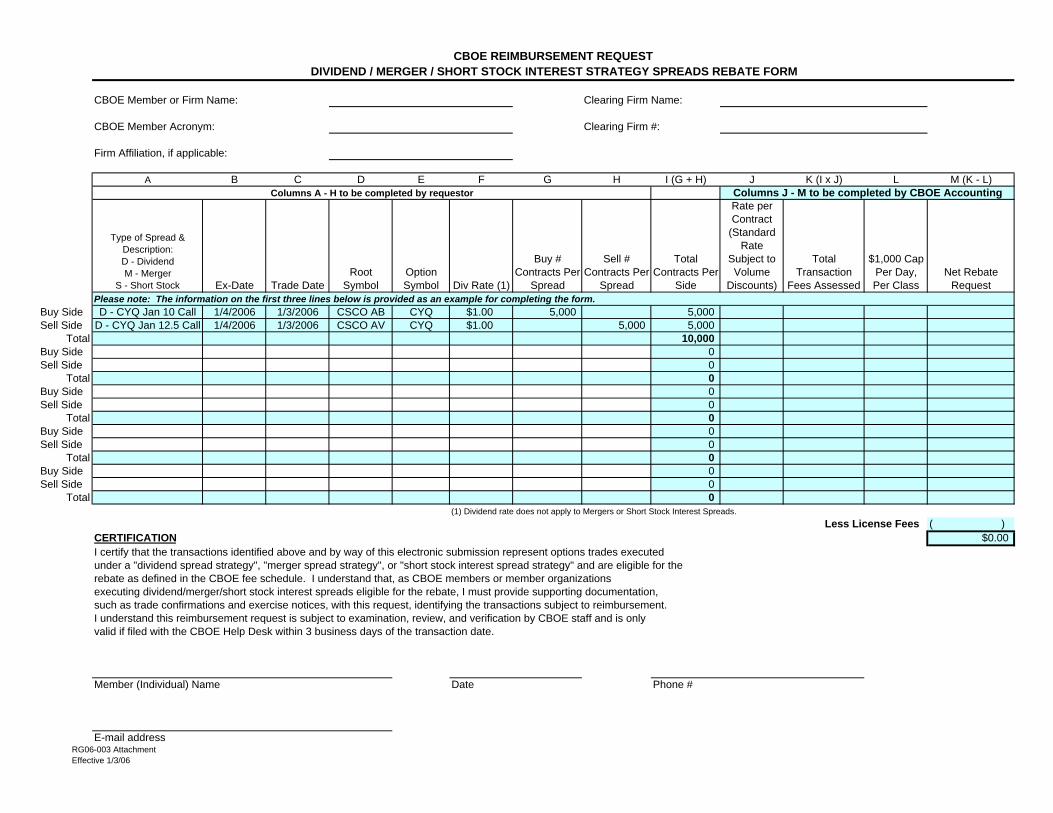

CBOE Member or Firm Name: Clearing Firm Name:

CBOE Member Acronym: Clearing Firm #:

Firm Affiliation, if applicable:

A B C D E F G H I (G + H) J K (I x J) L M (K - L)

Type of Spread & Description: D - Dividend M - Merger

S - Short Stock Ex-Date Trade DateRoot

SymbolOption Symbol Div Rate (1)

Buy # Contracts Per

Spread

Sell # Contracts Per

Spread

Total Contracts Per

Side

Rate per Contract

(Standard Rate

Subject to Volume

Discounts)

Total Transaction

Fees Assessed

$1,000 Cap Per Day, Per Class

Net Rebate Request

Please note: The information on the first three lines below is provided as an example for completing the form.Buy Side D - CYQ Jan 10 Call 1/4/2006 1/3/2006 CSCO AB CYQ $1.00 5,000 5,000Sell Side D - CYQ Jan 12.5 Call 1/4/2006 1/3/2006 CSCO AV CYQ $1.00 5,000 5,000

Total 10,000Buy Side 0Sell Side 0

Total 0Buy Side 0Sell Side 0

Total 0Buy Side 0Sell Side 0

Total 0Buy Side 0Sell Side 0

Total 0(1) Dividend rate does not apply to Mergers or Short Stock Interest Spreads.

Less License Fees ( )CERTIFICATION $0.00I certify that the transactions identified above and by way of this electronic submission represent options trades executedunder a "dividend spread strategy", "merger spread strategy", or "short stock interest spread strategy" and are eligible for therebate as defined in the CBOE fee schedule. I understand that, as CBOE members or member organizationsexecuting dividend/merger/short stock interest spreads eligible for the rebate, I must provide supporting documentation,such as trade confirmations and exercise notices, with this request, identifying the transactions subject to reimbursement.I understand this reimbursement request is subject to examination, review, and verification by CBOE staff and is onlyvalid if filed with the CBOE Help Desk within 3 business days of the transaction date.

Member (Individual) Name Date Phone #

E-mail address

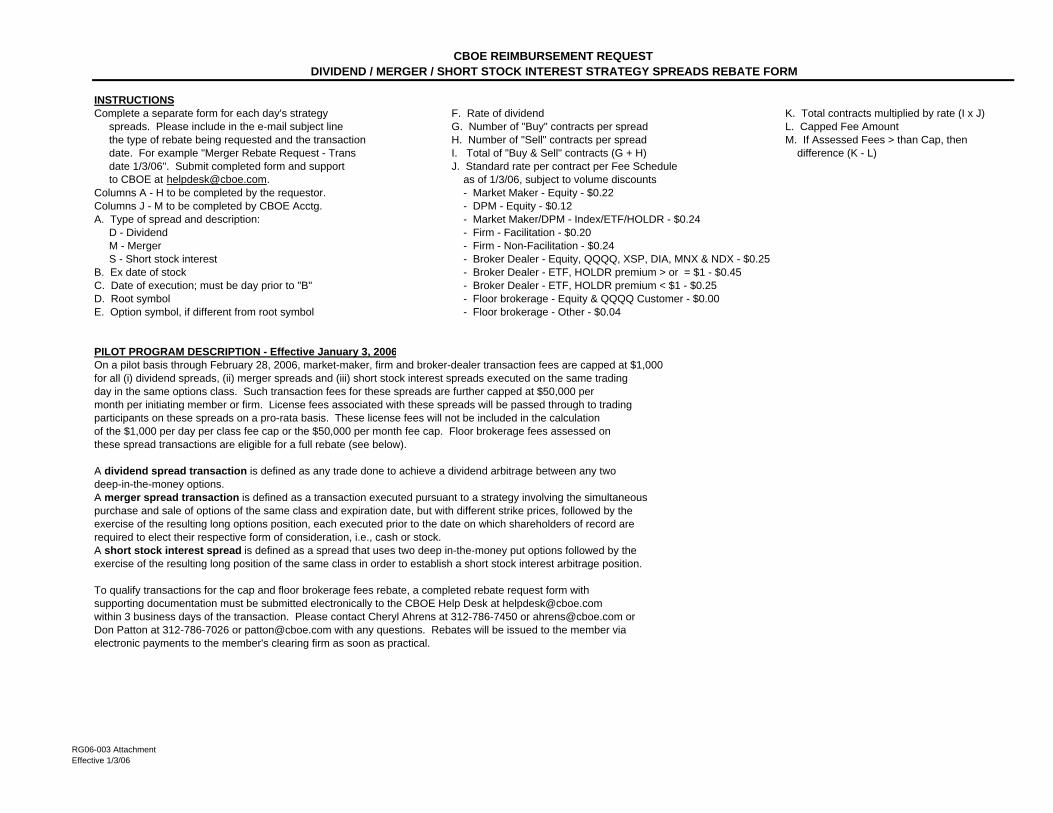

CBOE REIMBURSEMENT REQUESTDIVIDEND / MERGER / SHORT STOCK INTEREST STRATEGY SPREADS REBATE FORM

Columns A - H to be completed by requestor Columns J - M to be completed by CBOE Accounting

RG06-003 AttachmentEffective 1/3/06

CBOE REIMBURSEMENT REQUESTDIVIDEND / MERGER / SHORT STOCK INTEREST STRATEGY SPREADS REBATE FORM

INSTRUCTIONSComplete a separate form for each day's strategy F. Rate of dividend K. Total contracts multiplied by rate (I x J) spreads. Please include in the e-mail subject line G. Number of "Buy" contracts per spread L. Capped Fee Amount the type of rebate being requested and the transaction H. Number of "Sell" contracts per spread M. If Assessed Fees > than Cap, then date. For example "Merger Rebate Request - Trans I. Total of "Buy & Sell" contracts (G + H) difference (K - L) date 1/3/06". Submit completed form and support J. Standard rate per contract per Fee Schedule to CBOE at [email protected]. as of 1/3/06, subject to volume discountsColumns A - H to be completed by the requestor. - Market Maker - Equity - $0.22Columns J - M to be completed by CBOE Acctg. - DPM - Equity - $0.12A. Type of spread and description: - Market Maker/DPM - Index/ETF/HOLDR - $0.24 D - Dividend - Firm - Facilitation - $0.20 M - Merger - Firm - Non-Facilitation - $0.24 S - Short stock interest - Broker Dealer - Equity, QQQQ, XSP, DIA, MNX & NDX - $0.25B. Ex date of stock - Broker Dealer - ETF, HOLDR premium > or = $1 - $0.45C. Date of execution; must be day prior to "B" - Broker Dealer - ETF, HOLDR premium < $1 - $0.25D. Root symbol - Floor brokerage - Equity & QQQQ Customer - $0.00E. Option symbol, if different from root symbol - Floor brokerage - Other - $0.04

PILOT PROGRAM DESCRIPTION - Effective January 3, 2006On a pilot basis through February 28, 2006, market-maker, firm and broker-dealer transaction fees are capped at $1,000 for all (i) dividend spreads, (ii) merger spreads and (iii) short stock interest spreads executed on the same tradingday in the same options class. Such transaction fees for these spreads are further capped at $50,000 permonth per initiating member or firm. License fees associated with these spreads will be passed through to trading participants on these spreads on a pro-rata basis. These license fees will not be included in the calculation of the $1,000 per day per class fee cap or the $50,000 per month fee cap. Floor brokerage fees assessed onthese spread transactions are eligible for a full rebate (see below).

A dividend spread transaction is defined as any trade done to achieve a dividend arbitrage between any two deep-in-the-money options.A merger spread transaction is defined as a transaction executed pursuant to a strategy involving the simultaneous purchase and sale of options of the same class and expiration date, but with different strike prices, followed by the exercise of the resulting long options position, each executed prior to the date on which shareholders of record arerequired to elect their respective form of consideration, i.e., cash or stock. A short stock interest spread is defined as a spread that uses two deep in-the-money put options followed by theexercise of the resulting long position of the same class in order to establish a short stock interest arbitrage position.

To qualify transactions for the cap and floor brokerage fees rebate, a completed rebate request form withsupporting documentation must be submitted electronically to the CBOE Help Desk at [email protected] 3 business days of the transaction. Please contact Cheryl Ahrens at 312-786-7450 or [email protected] orDon Patton at 312-786-7026 or [email protected] with any questions. Rebates will be issued to the member viaelectronic payments to the member's clearing firm as soon as practical.

RG06-003 AttachmentEffective 1/3/06

10

Regulatory Circular RG06-04 To: CBOE Members and Member Firms From: Regulatory Services Division Legal Division

Date: January 4, 2006 Re: Market-Maker, RMM, e-DPM and DPM Quoting Obligations This circular summarizes the relevant quoting obligations in Hybrid. These obligations apply to Market-Makers (MMs), RMMs, e-DPMs and DPMs. For further information, please review Rule 8.7 relating to MMs and RMMs, Rule 8.93 relating to e-DPMs, and Rule 8.85 relating to DPMs which are available on CBOE’s website at www.cboe.org/Legal. A. MM Trades 20% or LESS of His/Her Contract Volume Electronically

When a MM is subject to these specific obligations (because he/she trades 20% or less of his/her volume electronically) ANY volume traded electronically by that MM will NOT count towards his/her in-person requirement. 1 The maximum permissible spread widths are as follows: $0.25 for options under $2, $0.40 for options above $2 but not over $5, $0.50 for options above $5 but not over $10; $0.80 for options above $10 but not over $20; and $1 for options above $20.

• Quote widths: Electronic quotes MUST be no wider than $5 • Opening Rotation: Quotes must be LEGAL WIDTH1 • Continuous Quoting: There is no continuous electronic quoting

obligation • Open Outcry RFQs: MUST respond to ALL verbal RFQs with a LEGAL-

WIDTH 10-up market for customers and 1-up for BDs • Quote Size: Initial quote size must be for at least 10-contracts. Once the

size decrements to zero, the MM must replenish to at least 10-contracts B. MM Trades MORE than 20% of His/Her Contract Volume Electronically2

Once a MM on Hybrid trades more than 20% of his/her contract volume electronically in a class, the following obligations will ALWAYS apply to him/her in that class:

• Quote Widths: Electronic quotes MUST be no wider than $5 • Opening Rotation: Quotes must be LEGAL WIDTH • Open Outcry RFQs: MUST respond to ALL verbal RFQs with a LEGAL-

WIDTH 10-up market for customers and 1-up for BDs • Quote Size: Initial quote size must be for at least 10-contracts. Once the

size decrements to zero, the MM must replenish to at least 10-contracts • Continuous Quoting Obligation: MM must continually quote 60% of

the series of his/her appointed classes

C. RMM Quoting Obligations

• Quote Widths: Electronic quotes MUST be no wider than $5 • Opening Rotation: Quotes must be LEGAL WIDTH • Quote Size: Initial quote size must be for at least 10-contracts. Once the

11

size decrements to zero, the RMM must replenish to at least 10-contracts

• Continuous Quoting Obligation: RMM must continually quote 60% of the series of his/her appointed classes

D. DPM Quoting Obligations

• Quote Widths: Electronic quotes MUST be no wider than $5 • Opening Rotation: Quotes must be LEGAL WIDTH • Quote Size: Initial quote size must be for at least 10-contracts. Once the

size decrements to zero, the DPM must replenish to at least 10-contracts

• Continuous Quoting Obligation: DPMs must quote a continuous, legal-width market in all series

• Opening Quotes: Must enter opening quotes in 100% of the series of each allocated class

E. e-DPM Quoting Obligations

• Quote Widths: Electronic quotes MUST be no wider than $5 • Opening Rotation: Quotes must be LEGAL WIDTH • Quote Size: Initial quote size must be for at least 10-contracts. Once the

size decrements to zero, the e-DPM must replenish to at least 10-contracts.

2The 20% Contract volume includes volume from all orders, including I orders and M orders.

• Continuous Quoting Obligation: e-DPM must continually quote 90%

of the series of his/her appointed classes, or alternatively respond to 98% of RFQs

• Opening Quotes: Must enter opening quotes in 100% of the series of each allocated class

F. Firm Quote Obligations

Each individual MM’s quotes are firm quotes and must be honored in accordance with CBOE’s Firm Quote Rule 8.51. This is different from non-Hybrid classes in which the crowd shares the responsibility for the quote. The firm quote size for customers is the disseminated size. G. Quote “Aping” and Anticompetitive Conduct In the Hybrid Approval Order, the SEC stated:

Although it is not unlawful for a Market-Maker to take the prices offered by its competitors into account when setting its own prices, or to follow or copy prices of its competitors, such a decision must be a unilateral business judgment not intended to harass or punish a competitor for improving prices or otherwise acting competitively and not the result of collusive agreement. Accordingly, the Commission expects that the CBOE will surveil its market to ensure that Market-Makers are not coordinating quotes in the Hybrid system or engaging in other anticompetitive conduct.

12

The Exchange’s Regulatory Division will surveil for such conduct. Violations may result in disciplinary or regulatory action by CBOE’s Business Conduct Committee. Any questions regarding this circular should be addressed to Tim MacDonald at (312) 786-7706 or Andrew Spiwak at (312) 786-7483. _________________________________________________________________ PROPOSED RULE CHANGE(S) Pursuant to Section 19(b)(1) of the Securities Exchange Act of 1934, as amended ("the Act"), and Rule 19b-4 thereunder, the Exchange has filed the following proposed rule change(s) with the Securities and Exchange Commission ("SEC"). Copies of the rule change filing(s) are available at www.cboe.com/legal/submittedsecfilings.aspx. Members may submit written comments to the Legal Division. The effective date of a proposed rule change will be the date of approval by the SEC, unless otherwise noted. ________________________________________________________________ SR-CBOE-2005-112 Pilot Relating to MM Orders in Hybrid On December 30, 2005, the Exchange filed Rule Change File No. SR-CBOE-2005-112, which filing seeks permanent approval of the Exchange's pilot program in CBOE Rule 6.13 relating to the frequency with which Market-Makers may submit orders for automatic execution through the Hybrid Trading System. Any questions regarding the rule change may be directed to Jennifer Lamie, Legal Division, at 312-786-7576. The text of the proposed rule change is provided below. Deletions are [bracketed and striken].

Rule 6.13 - CBOE Hybrid System’s Automatic Execution Feature (a) No change. (b) Automatic Execution

(i) No change.

(A) - (B) No change. (C) Access:

(i) No change. (ii) (A) Options Exchange Market-Makers: The appropriate FPC may also determine, on a class-by-class basis, to allow orders for the accounts of Market-Makers or specialists on an options exchange (collectively "options Market-Makers") who are exempt from the provisions of Regulation T of the Federal Reserve Board pursuant to Section 7(c)(2) of the Securities

13

Exchange Act of 1934 to be eligible for automatic execution. The appropriate FPC may establish the maximum order size eligibility for such options Market-Maker orders at a level lower than the maximum order size eligibility available to non-broker-dealer public customers and non-Market-Maker or non-specialist broker-dealers. Pronouncements pursuant to this provision regarding options Market-Maker access shall be made by the appropriate FPC and announced via Regulatory Circular.

(B) Stock Exchange Specialists: The appropriate FPC may determine, on a class-by-class basis, to allow orders for the account of a stock exchange specialist, with respect to a security in which it acts as a specialist, to be eligible for automatic execution in the overlying option class. The appropriate FPC may establish the maximum order size eligibility for such specialist orders at a level lower than the maximum order size eligibility available to options exchange Market-Makers. Stock exchange specialists, with respect to orders in securities in which they do not act as specialist, will be treated as broker-dealers that are not Market-Makers or specialists on an options exchange and will be eligible to submit orders for automatic execution in accordance with subparagraph (i) above.

(iii) 15-Second Limitation: With respect to orders eligible for submission pursuant to paragraph (b)(i)(C)(ii), members shall neither enter nor permit the entry of multiple orders on the same side of the market in an option class within any 15-second period for an account or accounts of the same beneficial owner. The appropriate FPC may shorten the duration of this 15-second period by providing notice to the membership via a Regulatory Circular that is issued at least one day prior to implementation. [The effectiveness of this rule shall terminate on October 12, 2006.]

* * * * * (ii) - (iv) No change.

(c) – (e) No change.

________________________________________________________________ SR-CBOE-2005-118 Portfolio Margining On December 28, 2005, the Exchange filed Rule Change File No. SR-CBOE-2005-118, which filing proposes to adopt rules that would allow portfolio margining of listed equity options, narrow-based index options, and security futures, as well as certain OTC instruments. Any questions regarding the rule change may be directed to Jaime Galvan, Legal Division, at 312-786-7058.

14

Additions are underlined; deletions are [bracketed and sticken].

Rule 12.4. Portfolio Margin for Index and Equity Options, and Cross-Margin for Index Options

As an alternative to the transaction / position specific margin requirements set forth in Rule 12.3 of this Chapter 12, members may require margin for listed[, broad-based U.S.] index and equity options (defined below as a “listed option”), options on exchange traded funds, security futures products, index warrants, [and ]underlying instruments and unlisted derivatives (as defined below) in accordance with the portfolio margin requirements contained in this Rule 12.4.

In addition, members, provided they are a Futures Commission Merchant ("FCM") and are either a clearing member of a futures clearing organization or have an affiliate that is a clearing member of a futures clearing organization, are permitted under this Rule 12.4 to combine a customer's related instruments (as defined below), listed index options, options on exchange traded funds[ and listed, broad-based U.S. index options], index warrants, [and ]underlying instruments and unlisted derivatives and compute a margin requirement ("cross-margin") on a portfolio margin basis. Members must confine cross-margin positions to a portfolio margin account dedicated exclusively to cross-margining.

Application of the portfolio margin and cross-margining provisions of this Rule 12.4 to IRA accounts is prohibited.

(a) Definitions.

(1) The term "listed option" shall mean any option traded on a registered national securities exchange or automated facility of a registered national securities association. (2) The term “security future” means a contract of sale for future delivery of a single security or of a narrow-based security index, including any interest therein or based on the value thereof, to the extent that that term is defined in Section 3(a)(55) of the Security Exchange Act of 1934. (3) The term “security futures product” means a security future, or an option on any security future. ([2]4) The term “unlisted derivative[option]” means any unlisted option, forward contract or swap that can be priced by a model approved by a “DEA” covering the same underlying instrument[ not included in the definition of listed option]. (5) The term “option series” means all option contracts of the same type (either a call or a put) and exercise style, covering the same underlying instrument with the same exercise price, expiration date, and number of underlying units. ([3]6) The term “options class” refers to all options contracts covering the same underlying instrument.

15

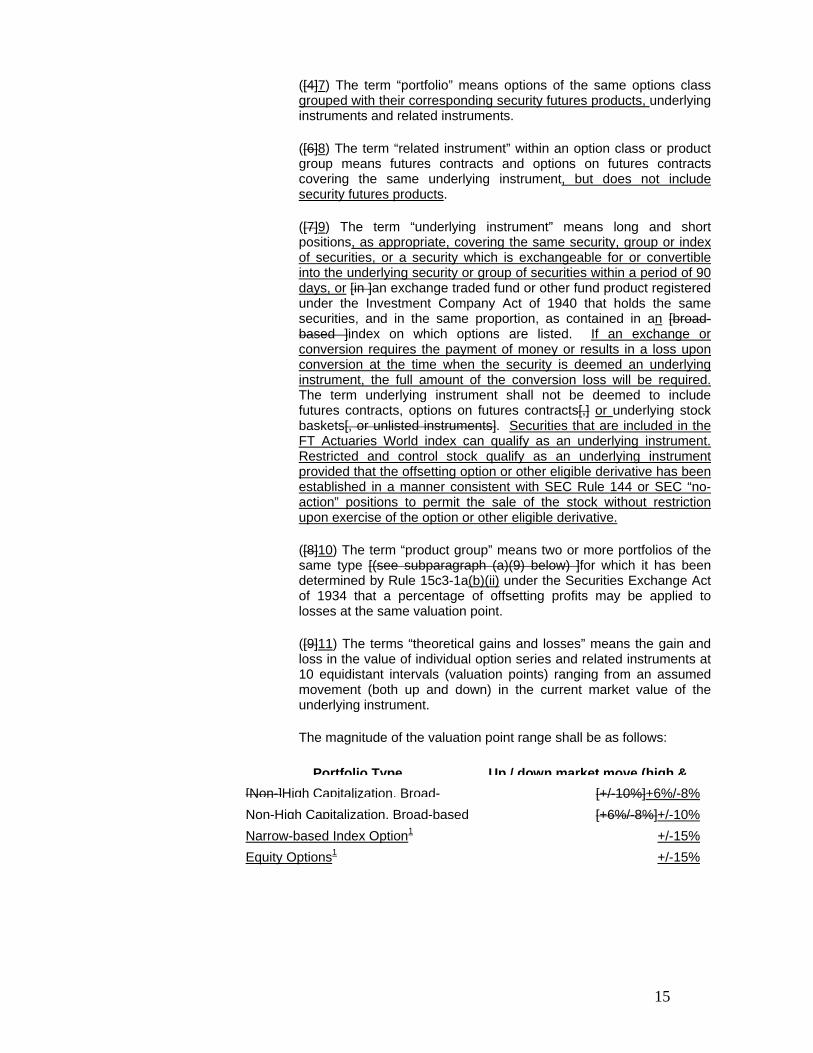

([4]7) The term “portfolio” means options of the same options class grouped with their corresponding security futures products, underlying instruments and related instruments. ([6]8) The term “related instrument” within an option class or product group means futures contracts and options on futures contracts covering the same underlying instrument, but does not include security futures products. ([7]9) The term “underlying instrument” means long and short positions, as appropriate, covering the same security, group or index of securities, or a security which is exchangeable for or convertible into the underlying security or group of securities within a period of 90 days, or [in ]an exchange traded fund or other fund product registered under the Investment Company Act of 1940 that holds the same securities, and in the same proportion, as contained in an [broad-based ]index on which options are listed. If an exchange or conversion requires the payment of money or results in a loss upon conversion at the time when the security is deemed an underlying instrument, the full amount of the conversion loss will be required. The term underlying instrument shall not be deemed to include futures contracts, options on futures contracts[,] or underlying stock baskets[, or unlisted instruments]. Securities that are included in the FT Actuaries World index can qualify as an underlying instrument. Restricted and control stock qualify as an underlying instrument provided that the offsetting option or other eligible derivative has been established in a manner consistent with SEC Rule 144 or SEC “no-action” positions to permit the sale of the stock without restriction upon exercise of the option or other eligible derivative. ([8]10) The term “product group” means two or more portfolios of the same type [(see subparagraph (a)(9) below) ]for which it has been determined by Rule 15c3-1a(b)(ii) under the Securities Exchange Act of 1934 that a percentage of offsetting profits may be applied to losses at the same valuation point. ([9]11) The terms “theoretical gains and losses” means the gain and loss in the value of individual option series and related instruments at 10 equidistant intervals (valuation points) ranging from an assumed movement (both up and down) in the current market value of the underlying instrument. The magnitude of the valuation point range shall be as follows:

Portfolio Type Up / down market move (high &[Non-]High Capitalization, Broad- [+/-10%]+6%/-8%Non-High Capitalization, Broad-based [+6%/-8%]+/-10%Narrow-based Index Option1 +/-15%Equity Options1 +/-15%

16

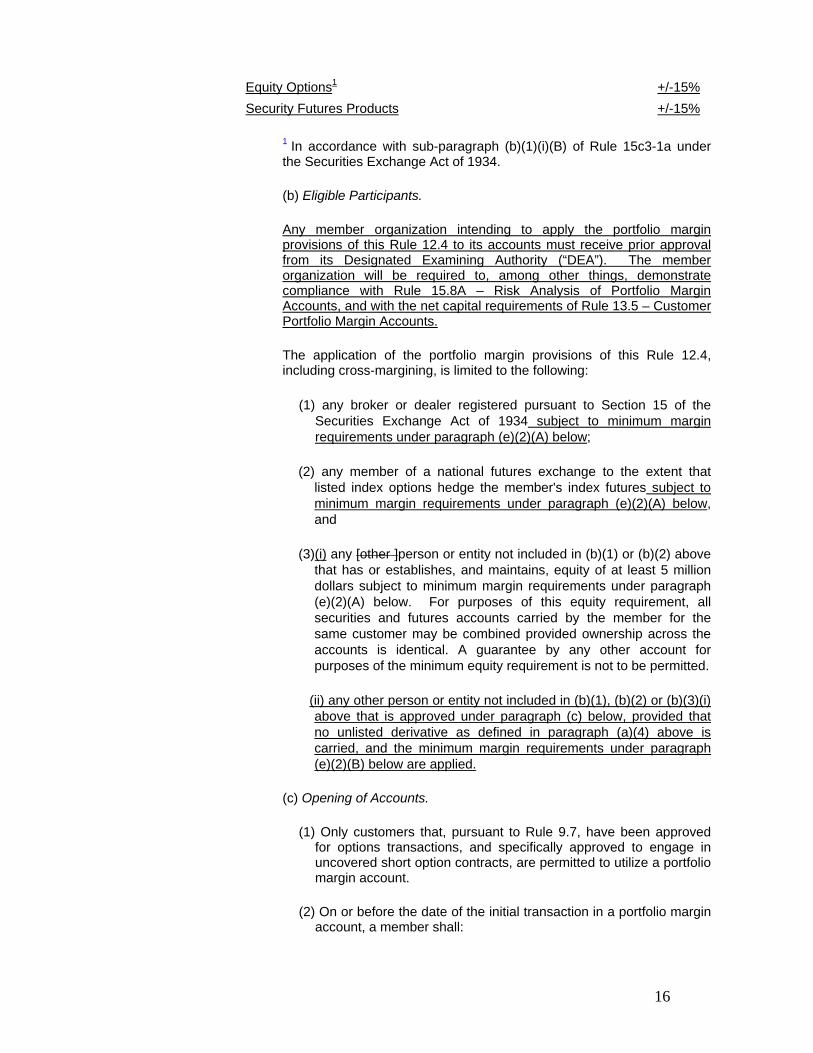

Equity Options1 +/-15%Security Futures Products +/-15%

1 In accordance with sub-paragraph (b)(1)(i)(B) of Rule 15c3-1a under the Securities Exchange Act of 1934.

(b) Eligible Participants.

Any member organization intending to apply the portfolio margin provisions of this Rule 12.4 to its accounts must receive prior approval from its Designated Examining Authority (“DEA”). The member organization will be required to, among other things, demonstrate compliance with Rule 15.8A – Risk Analysis of Portfolio Margin Accounts, and with the net capital requirements of Rule 13.5 – Customer Portfolio Margin Accounts.

The application of the portfolio margin provisions of this Rule 12.4, including cross-margining, is limited to the following:

(1) any broker or dealer registered pursuant to Section 15 of the Securities Exchange Act of 1934 subject to minimum margin requirements under paragraph (e)(2)(A) below;

(2) any member of a national futures exchange to the extent that listed index options hedge the member's index futures subject to minimum margin requirements under paragraph (e)(2)(A) below, and

(3)(i) any [other ]person or entity not included in (b)(1) or (b)(2) above that has or establishes, and maintains, equity of at least 5 million dollars subject to minimum margin requirements under paragraph (e)(2)(A) below. For purposes of this equity requirement, all securities and futures accounts carried by the member for the same customer may be combined provided ownership across the accounts is identical. A guarantee by any other account for purposes of the minimum equity requirement is not to be permitted.

(ii) any other person or entity not included in (b)(1), (b)(2) or (b)(3)(i) above that is approved under paragraph (c) below, provided that no unlisted derivative as defined in paragraph (a)(4) above is carried, and the minimum margin requirements under paragraph (e)(2)(B) below are applied.

(c) Opening of Accounts.

(1) Only customers that, pursuant to Rule 9.7, have been approved for options transactions, and specifically approved to engage in uncovered short option contracts, are permitted to utilize a portfolio margin account.

(2) On or before the date of the initial transaction in a portfolio margin account, a member shall:

17

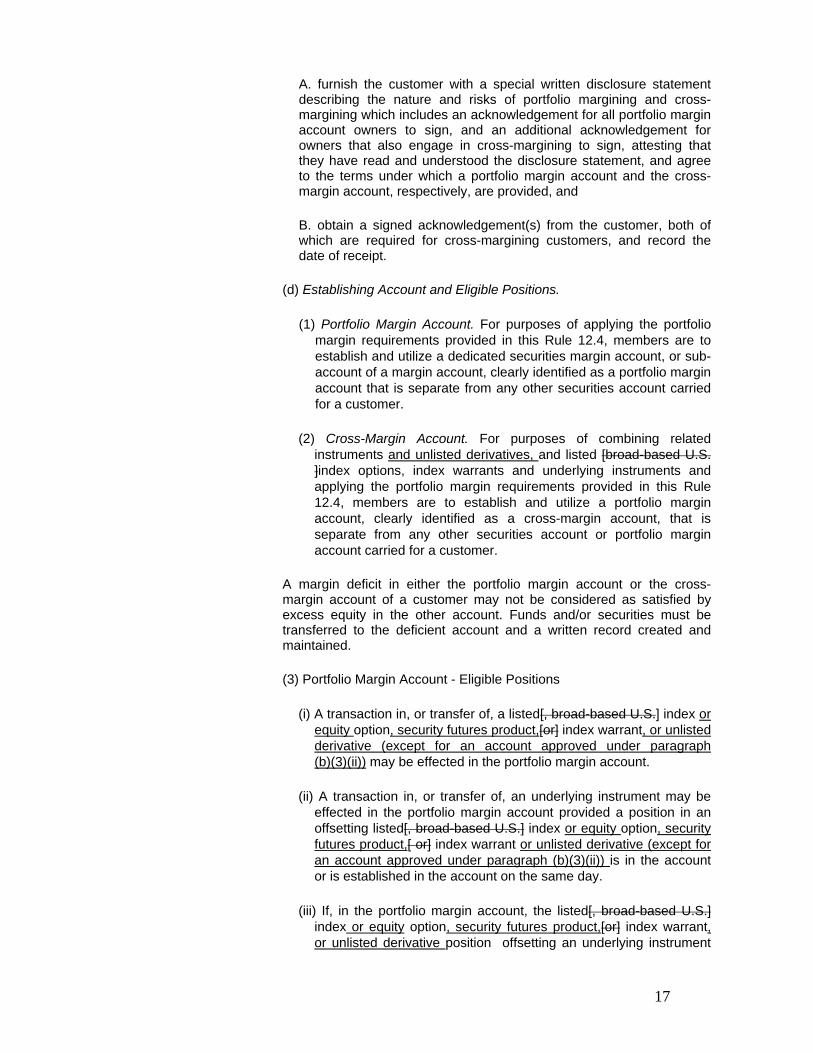

A. furnish the customer with a special written disclosure statement describing the nature and risks of portfolio margining and cross-margining which includes an acknowledgement for all portfolio margin account owners to sign, and an additional acknowledgement for owners that also engage in cross-margining to sign, attesting that they have read and understood the disclosure statement, and agree to the terms under which a portfolio margin account and the cross-margin account, respectively, are provided, and

B. obtain a signed acknowledgement(s) from the customer, both of which are required for cross-margining customers, and record the date of receipt.

(d) Establishing Account and Eligible Positions.

(1) Portfolio Margin Account. For purposes of applying the portfolio margin requirements provided in this Rule 12.4, members are to establish and utilize a dedicated securities margin account, or sub-account of a margin account, clearly identified as a portfolio margin account that is separate from any other securities account carried for a customer.

(2) Cross-Margin Account. For purposes of combining related instruments and unlisted derivatives, and listed [broad-based U.S. ]index options, index warrants and underlying instruments and applying the portfolio margin requirements provided in this Rule 12.4, members are to establish and utilize a portfolio margin account, clearly identified as a cross-margin account, that is separate from any other securities account or portfolio margin account carried for a customer.

A margin deficit in either the portfolio margin account or the cross-margin account of a customer may not be considered as satisfied by excess equity in the other account. Funds and/or securities must be transferred to the deficient account and a written record created and maintained.

(3) Portfolio Margin Account - Eligible Positions

(i) A transaction in, or transfer of, a listed[, broad-based U.S.] index or equity option, security futures product,[or] index warrant, or unlisted derivative (except for an account approved under paragraph (b)(3)(ii)) may be effected in the portfolio margin account.

(ii) A transaction in, or transfer of, an underlying instrument may be effected in the portfolio margin account provided a position in an offsetting listed[, broad-based U.S.] index or equity option, security futures product,[ or] index warrant or unlisted derivative (except for an account approved under paragraph (b)(3)(ii)) is in the account or is established in the account on the same day.

(iii) If, in the portfolio margin account, the listed[, broad-based U.S.] index or equity option, security futures product,[or] index warrant, or unlisted derivative position offsetting an underlying instrument

18

position ceases to exist and is not replaced within 10 business days, the underlying instrument position must be transferred to a regular margin account, subject to [Regulation T initial margin and ]the margin required pursuant to the other provisions of this chapter. Members will be expected to monitor portfolio margin accounts for possible abuse of this provision.

(iv) In the event that fully paid for long options and/or index warrants are the only positions contained within a portfolio margin account, such long positions must be transferred to a securities account other than a portfolio margin account or cross-margin account within 10 business days, subject to the margin required pursuant to the other provisions of this chapter, unless the status of the account changes such that it is no longer composed solely of fully paid for long options and/or index warrants.

(4) Cross-Margin Account - Eligible Positions

(i) A transaction in, or transfer of, a related instrument or unlisted derivative may be effected in the cross-margin account provided a position in an offsetting listed[, U.S. broad-based] index option, index warrant, [or ]underlying instrument or unlisted derivative is in the account or is established in the account on the same day.

(ii) If the listed[, U.S. broad-based] index option, index warrant,[ or] underlying instrument or unlisted derivative position offsetting a related instrument ceases to exist and is not replaced within 10 business days, the related instrument or unlisted derivative position must be transferred to a futures account. Members will be expected to monitor cross-margin accounts for possible abuse of this provision.

(iii) If the related instrument or unlisted derivative position offsetting an underlying instrument position ceases to exist and is not replaced within 10 business days, the underlying instrument position must be transferred to a regular margin account, subject to the margin required pursuant to the other provisions of this chapter. Members will be expected to monitor portfolio margin accounts for possible abuse of this provision.

(iv.) In the event that fully paid for long index options and/or index warrants (securities) are the only positions contained within a cross-margin account, such long positions must be transferred to a securities account other than a portfolio margin account or cross-margin account within 10 business days, subject to the margin required pursuant to the other provisions of this chapter, unless the status of the account changes such that it is no longer composed solely of fully paid for long options and/or index warrants.

(e) Initial and Maintenance Margin Required. The amount of margin required under this Rule 12.4 for each portfolio shall be the greater of:

(1) the amount for any of the 10 equidistant valuation points

19

representing the largest theoretical loss as calculated pursuant to paragraph (f) below or

(2)(A) In the case of an account operating under paragraph (b)(1), (b)(2) or (b)(3) of this Rule 12.4, $.375 for each listed [index ]option, security futures product,[ and] related instrument and unlisted derivative, multiplied by the contract or instrument's multiplier, not to exceed the market value in the case of long positions in listed options, including options on security futures, and options on futures contracts.

(B) In the case of an account operating under paragraph (b)(ii) of this Rule 12.4, $.75 for each listed option, security futures product and related instrument multiplied by the contract or instrument’s multiplier, not to exceed the market value in the case of long options, including options on security futures, and options on futures contracts in the case of a portfolio holding a position in the underlying instrument. In the case of a portfolio not holding a position in the underlying instrument, $.375 shall be applied instead of $.75.

(f) Method of Calculation.

(1) Long and short positions in listed options, security futures products, underlying instruments,[ and] related instruments and unlisted derivatives are to be grouped by option class; each option class group being a "portfolio". Each portfolio is categorized as one of the portfolio types specified in paragraph (a)([9]11) above.

(2) For each portfolio, theoretical gains and losses are calculated for each position as specified in paragraph (a)([9]11) above. For purposes of determining the theoretical gains and losses at each valuation point, members shall obtain and utilize the theoretical value of a listed [index ]option, security futures product, underlying instrument, [or ]related instrument and unlisted derivative, rendered by a theoretical pricing model that, in accordance with paragraph (b)(1)(i)(B) of Rule 15c3-1a under the Securities Exchange Act of 1934, qualifies for purposes of determining the amount to be deducted in computing net capital under a portfolio based methodology.

(3) Offsets. Within each portfolio, theoretical gains and losses may be netted fully at each valuation point.

Offsets between portfolios within the High Capitalization, Broad-Based Index Option, [product group and the ]Non-High Capitalization, Broad-Based Index Option [product group ]and Narrow-Based Index Option product groups may then be applied as permitted by Rule 15c3-1a under the Securities Exchange Act of 1934.

(4) After applying paragraph (3) above, the sum of the greatest loss from each portfolio is computed to arrive at the total margin required for the account (subject to the per contract minimum).

20

(g) Equity Deficiency. If, at any time, equity declines below the[ 5 million dollar] minimum required under Paragraph (b)[(4)] of this Rule 12.4 and is not brought back up to the required level[at least 5 million dollars] within three (3) business days (T+3) by a deposit of funds or securities, or through favorable market action; members are prohibited from accepting opening orders starting on T+4, except that opening orders entered for the purpose of hedging existing positions may be accepted if the result would be to lower margin requirements. This prohibition shall remain in effect until such time as the[an] required minimum account equity [of 5 million dollars] is re-established.

(h) Determination of Value for Margin Purposes. For the purposes of this Rule 12.4, all listed [index ]options, security futures products, underlying instruments,[ and] related instruments and unlisted derivative positions shall be valued at current market prices. Account equity for the purposes of this Rule 12.4 shall be calculated separately for each portfolio margin account by adding the current market value of all long positions, subtracting the current market value of all short positions, and adding the credit (or subtracting the debit) balance in the account.

(i) Additional Margin.

(1) If at any time, the equity in any portfolio margin account, including a cross-margin account, is less than the margin required, additional margin must be obtained within [one]three business days (T+[1]3). In the event a customer fails to deposit additional margin within [one]three business days, the member must liquidate positions in an amount sufficient to, at a minimum, lower the total margin required to an amount less than or equal to account equity. Exchange Rule 12.9 - Meeting Margin Calls by Liquidation shall not apply to portfolio margin accounts. However, members will be expected to monitor the risk of portfolio margin accounts pursuant to the risk monitoring procedures required by Rule 15.8A. Guarantees by any other account for purposes of margin requirements is not to be permitted.

(2) The day trading requirements of Exchange Rule 12.3(j) shall not apply to portfolio margin accounts, including cross-margin accounts.

(j) Cross-Margin Accounts - Requirement to Liquidate.

(1) A member is required immediately either to liquidate, or transfer to another broker-dealer eligible to carry cross-margin accounts, all customer cross-margin accounts that contain positions in futures and/or options on futures if the member is:

(i) insolvent as defined in section 101 of title 11 of the United States Code, or is unable to meet its obligations as they mature;

(ii) the subject of a proceeding pending in any court or before any agency of the United States or any State in which a receiver, trustee, or liquidator for such debtor has been appointed;

21

(iii) not in compliance with applicable requirements under the Securities Exchange Act of 1934 or rules of the Securities and Exchange Commission or any self-regulatory organization with respect to financial responsibility or hypothecation of customers' securities; or

(iv) unable to make such computations as may be necessary to establish compliance with such financial responsibility or hypothecation rules.

(2) Nothing in this paragraph (j) shall be construed as limiting or restricting in any way the exercise of any right of a registered clearing agency to liquidate or cause the liquidation of positions in accordance with its by-laws and rules.

*****

CHAPTER 9

Doing Business with the Public 9.15. Delivery of Current Options Disclosure Documents and Prospectus (a) No change. (b) No change.

(c) The special written disclosure statement describing the nature and risks of portfolio margining and cross-margining, and acknowledgement for customer signature, required by Rule 12.4(c)(2) shall be in a format prescribed by the Exchange or in a format developed by the member organization, provided it contains substantially similar information as the prescribed Exchange format and has received prior written approval of the Exchange.

Sample Risk Description for Use by Firms to Satisfy Requirements

of Exchange Rule 9.15(d) Portfolio Margining and Cross-Margining

Disclosure Statement and Acknowledgement For a Description of the Special Risks Applicable to a Portfolio

Margin Account and its Cross-Margining Features, See the

Material Under Those Headings Below.

OVERVIEW OF PORTFOLIO MARGINING

1. Portfolio margining is a margin methodology that sets margin requirements for an account based on the greatest projected net loss of all positions in a “portfolio[product class]” or "product group" as determined by an options pricing model using multiple pricing scenarios. These pricing scenarios are designed to measure the theoretical loss of the positions given changes in both the underlying price and implied volatility inputs to the model. Portfolio margining is currently limited to equity and equity index products[product classes and groups of index products relating to broad-based market indexes].

22

2. The goal of portfolio margining is to set levels of margin that more precisely reflect actual net risk. The customer benefits from portfolio margining in that margin requirements calculated on net risk are generally lower than alternative "position" or "strategy" based methodologies for determining margin requirements. Lower margin requirements allow the customer more leverage in an account.

CUSTOMERS ELIGIBLE FOR PORTFOLIO MARGINING

3. To be eligible for portfolio margining, customers [(other than broker-dealers)] must meet the basic standards for having an options account that is approved for uncovered writing. If a customer wishes to utilize unlisted derivatives, [and ]the customer must have and maintain at all times account net equity of not less than $5 million, aggregated across all accounts under identical ownership at the clearing broker. The identical ownership requirement excludes accounts held by the same customer in different capacities (e.g., as a trustee and as an individual) and accounts where ownership is overlapping but not identical ( e.g., individual accounts and joint accounts).

If a customer wishes to utilize only listed index and equity options, security futures products, underlying instruments and related instruments, no minimum equity is required by the exchanges. However, carrying broker-dealers will have their own minimum account equity requirement, and possibly other eligibility requirements. Also, pursuant to exchange rules, a higher per contract minimum margin requirement will apply to portfolios holding the underlying instrument.

Neither the $5 million minimum account equity requirement or the higher per contract minimum is applicable to portfolio margining of customers that are broker-dealers or futures locals.

POSITIONS ELIGIBLE FOR A PORTFOLIO MARGIN ACCOUNT

4. All positions in [broad-based U.S. market ]index and equity options, security futures products, and index warrants listed on a national securities exchange, underlying instruments including[and] exchange traded funds and other fund products registered under the Investment Company Act of 1940 that are managed to track the same index that underlies permitted index options, are eligible for a portfolio margin account. Additionally, an account that elects to operate with account equity of not less than $5 million may carry positions in unlisted derivatives (e.g., OTC swaps, options) that have the same underlying instrument as an index or equity option and can be priced by an approved vendor of theoretical values.

SPECIAL RULES FOR PORTFOLIO MARGIN ACCOUNTS

5. A portfolio margin account may be either a separate account or a subaccount of a customer's regular margin account. In the case of a subaccount, equity in the regular account will be available to satisfy any margin requirement in the portfolio margin subaccount without transfer to the subaccount.

6. A portfolio margin account or subaccount that elects to operate with

23

account equity of not less than $5 million will be subject to a minimum margin requirement of $.375 multiplied by the index multiplier for every options contract, security futures product, [or ]index warrant, unlisted derivative and related instrument carried long or short in the account. No minimum margin is required in the case of underlying instruments, eligible exchange traded funds or other eligible fund products. A portfolio margin account that elects to operate with account equity of less than $5 million will be subject to a minimum margin requirement of $.75 multiplied by the index multiplier for every options contract, security futures product, index warrant, unlisted derivative and related instrument carried long or short in any portfolio that contains a position in the underlying instrument. For portfolios that do not contain a position in the underlying security, a $.375 minimum will apply.

7. Margin calls in the portfolio margin account or subaccount, regardless of whether due to new commitments or the effect of adverse market moves on existing positions, must be met within [one]three business days. Any shortfall in aggregate net equity across accounts must be met within three business days. Failure to meet a margin call when due will result in immediate liquidation of positions to the extent necessary to reduce the margin requirement. Failure to meet an equity call prior to the end of the third business day will result in a prohibition on entering any new orders that would increase the margin requirement[opening orders, with the exception of opening orders that hedge existing positions], beginning on the fourth business day and continuing until such time as the minimum equity requirement is satisfied.

8. A position in an underlying instrument[exchange traded fund or other eligible fund product] may not be established in a portfolio margin account unless there exists, or there is established on the same day, an offsetting position in securities options or other eligible securities. Underlying instruments[Exchange traded index funds and/or other eligible funds] will be transferred out of the portfolio margin account and into a regular securities account subject to strategy based margin if, for more than 10 business days and for any reason, the offsetting securities options or other eligible securities no longer remain in the account.

9. When a broker-dealer carries a regular cash account or margin account for a customer, the broker-dealer is limited by rules of the Securities and Exchange Commission and of The Options Clearing Corporation ("OCC") in the extent to which the broker-dealer may permit OCC to have a lien against long option positions in those accounts. In contrast, OCC will have a lien against all long option positions that are carried by a broker-dealer in a portfolio margin account, and this could, under certain circumstances, result in greater losses to a customer having long option positions in such an account in the event of the insolvency of the customer's broker. Furthermore, the carrying broker-dealer has a lien on all long securities in a portfolio margin account, including underlying instruments, even if fully paid. Accordingly, to the extent that a customer does not borrow against long option and underlying instrument positions in a portfolio margin account or have margin requirements in the account against which the long option or underlying instruments can be credited, there is no advantage to carrying the long options and underlying instruments in a portfolio margin account and the customer should consider carrying them in an account other than a portfolio margin account.

24

SPECIAL RISKS OF PORTFOLIO MARGIN ACCOUNTS

10. Portfolio margining generally permits greater leverage in an account, and greater leverage creates greater losses in the event of adverse market movements.

11. Because the time limit for meeting margin calls is shorter than in a regular margin account, there is increased risk that a customer's portfolio margin account will be liquidated involuntarily, possibly causing losses to the customer.

12. Because portfolio margin requirements are determined using sophisticated mathematical calculations and theoretical values that must be calculated from market data, it may be more difficult for customers to predict the size of future margin calls in a portfolio margin account. This is particularly true in the case of customers who do not have access to specialized software necessary to make such calculations or who do not receive theoretical values calculated and distributed periodically by OCC.

13. For the reasons noted above, a customer that carries long options and underlying instrument positions in a portfolio margin account could, under certain circumstances, be less likely to recover the full value of those positions in the event of the insolvency of the carrying broker.

14. Trading of securities index and equity products in a portfolio margin account is generally subject to all the risks of trading those same products in a regular securities margin account. Customers should be thoroughly familiar with the risk disclosure materials applicable to those products, including the booklet entitled Characteristics and Risks of Standardized Options.

15. Customers should consult with their tax advisers to be certain that they are familiar with the tax treatment of transactions in securities index and equity products.

16. The descriptions in this disclosure statement relating to eligibility requirements for portfolio margin accounts, and minimum equity and margin requirements for those accounts, are minimums imposed under exchange rules. Time frames within which margin and equity calls must be met are maximums imposed under exchange rules. Broker-dealers may impose their own more stringent requirements.

OVERVIEW OF CROSS-MARGINING

17. With cross-margining, index futures and options on index futures and, for accounts that elect to maintain a minimum account equity of $5 million, unlisted derivatives, are combined with offsetting positions in securities index options and underlying instruments, for the purpose of computing a margin requirement based on the net risk. This generally produces lower margin requirements than if the futures products and securities products are viewed separately, thus providing more leverage in the account.

25

18. Cross-margining must be done in a portfolio margin account type. A separate portfolio margin account must be established exclusively for cross-margining.