Embed Size (px)

Citation preview

EXAMINE TRADE FINANCE METHODS USED BY

TRADING COMPANIES GLOBALLY AND EVALUATE

THEIR EFFECTIVENESS

TEOH TEIK TOE

(James Cook University Australia – Singapore Campus)

Werner R. Murhadi

(Universitas Surabaya, Indonesia)

NEETU KATARIA

(Anglia Ruskin University, UK)

ABSTRACT

This study is planned in the functional area of Trade Finance Methods used by trading

companies globally and in Singapore with focus to study on effectiveness in each

method. While arriving at the effectiveness of the trade finance method the effort has

been to include not just the cost or pricing dimension but also risk mitigation aspects

as well as the documentation intensity translating to the convenience factor of the

method. Research further attempted to explore importance accorded to country risk

element over the counterparty risk by banks while pricing the trade finance product

offered to the trading companies. Research aim is to quantify and validate the general

understanding on the effectiveness of trade finance techniques employed by the

trading companies. Researcher has explored and analysed the relationship or

interrelationships between variable – cost effectiveness, risk mitigation and

documentation aspects of commonly used trade finance products, so as to obtain

effects by causative factors (Creswell, 1994) to have a great insight into the overall

effectiveness of the trade finance products being used by the trading companies.

Researcher employed „Survey‟ methodology to articulate research questions and

hypothesis in the field. Researcher designed and administered the questionnaires to

specific set of banking professionals & representatives of trading companies active in

trade finance areas. Sample of trading Companies and Banks was carefully selected

using stratified random probabilistic sampling approach. Data collected was analysed

using non-parametric statistical packages to establish association like chi-square (χ²)

and the extent/ degree of association like spearman correlation coefficient( or rs).

Researcher concluded that documentation has been sighted as major reason for its

lower use as a source of trade finance. Based on the results it can be reasonably

deduced that documentation intensity might affect rationality significantly while

choosing between letter of credit vis-à-vis other source of finance such as Bill

discounting. It can be reasonably inferenced that increased documentation might have

resulted in a risky practice of going for clean invoice financing where use of letter of

credit would have been optimal from the risk management perspective of the trading

companies. Research concluded that country risk is more potent factor considered by

the banks where documentary credit like Letter of Credit is extended while

creditworthiness might influence pricing where trading company goes in for other

trade finance methods such as invoice financing.

Keywords: International Trade, Bill Discounting, Letter of Credit, Clean Invoice

Finance & Country Risk

1. Introduction

Trading companies from various parts of the globe have set up their offices in

Singapore for carrying out trading activities due to varied reasons like better access to

ports, good legal system, convenient time zoning etc. Schemes like Global Trading

Partners (GTP) etc. administered by International Enterprises, Singapore (IE website,

2012) provide congenial atmosphere for the trading companies. Further Singapore

provides strong judicial and legal system and has good presence of financial

institutions - 122 commercial banks and 49 merchant banks in Singapore as per

Monetary Authority of Singapore (Source: MAS website, 2012). Trading companies

deal in multiple commodities who facilitate import- export based on commercial and

financial documents. In the process trading companies facilitate to manage the

pressures on the working capital cycles of both importers and exporters by stepping in

to make payment to the exporters using the trade finance facilities available from the

banks based on the title documents. Bank facilities are used till importer pays off on

receiving the goods. Trading companies thus always look out for the financing

facilities to keep this fund cycle going and would ensure that bank facilities are

effective in terms of cost and risk effectiveness. Most effective bank facility would be

the one that would optimally balance the cost, convenience of use and the risk for

these trading companies. In contrast, the bankers who provide these trade finance

facilities would also base the pricing of the trade facilities on the inherent risk of the

facility besides considering factors such as creditworthiness of the companies, tenure

of the facility and the security offered. Thus it is always a tight rope walk for trading

companies to balance finance costs and their trading margins.

How efficiently these trading company rotate funds would determine how

profitable their operations would be. This would critically depend on trading company

using the most effective bank facility. Most effective bank facility is one which

optimally balances cost, ease of documentation and the risk mitigation for these

trading companies. From industry practice it is observed that trading companies

predominantly prefer use of bill discounting as a source of trade finance. Letter of

credit- a documentary credit, on the other hand is preferred where there is potential

counterparty risk is observed. However documentary credit documentation is really a

major hurdle. What are the chances that increased documentation would result in a

risky practice of going for bill discounting in such cases? On the Other hand, Banks

who are on the opposite end of the price risk spectrum, has to manage the risk arising

out of the trade finance facilities. Are they inclined to build risk premium by way of

higher rates while pricing their products. What is the consideration for pricing, is it

creditworthiness of buyer or the country risk? Researcher will study various trade

finance facilities and design a research methodology which would aim to arrive at the

most commonly used source of trade finance, most cost effective source of trade

finance and least documentation intensive source of trade finance.

Based on the explanation above, this research will study following research questions:

(1) Do Trading Companies prefer Bill Discounting over other sources of trade finance

like Letter of credit as most cost effective? (2) Is Letter of credit superior product

compared to Bill discounting from the perspective of risk mitigation for trading

companies? (3) Would excessive documentation influence choice of trade finance

method employed by the trading companies? (4) Do banks charge premium based on

creditworthiness while pricing the trade finance products to reflect the higher risk. Do

banks consider Country risk as more important factor for pricing decision than the

counterparty risk

2. Literature Review

2.1. International Trade

International trade is the buying and selling of goods and services across national

borders or Territories as a result of uneven distribution of natural resources in different

countries. Both when sourcing supplies and when selling the products, a company is

exposed to risk. Such risks cannot be avoided but can only be better managed.

Sources of Risk for the Parties involved in trade finance are:

Buyer’s Insolvency/Credit Risk refers to the inability of the buyer to honour full

payment for goods or services rendered on due date. This is a risk on seller

associated with selling or supplying a product or service without collecting full

payment or experienced late payment.

Buyer’s Acceptance Risk refers to the buyer‟s non-acceptance of goods delivered

or services rendered. Unaccepted goods or services may create difficulty for the

seller to dispose the goods to another buyer or encounter working capital problem.

Knowledge Inadequacy A buyer or seller who intends to expand his business into

another product/service/industry/country

may not have adequate knowledge on the risk of the new product/service, local

market situation or goods‟ fashion. The lack of knowledge increases the chances of

business failure.

Seller’s Performance Risk - A seller may fail to carry out his obligations in a

sales contract due to one or more reasons, and such non-performance by the seller

may have adverse consequential impacts on the buyer‟s business. It could be

expensive for the buyer to take legal actions against the seller in his country.

Documentation Risk is the risk of non-conformance to specific documentation

requirements under a sales contract or documentary credit. Failure in fulfilling

documentation requirements may result in seller‟s inability or delay in obtaining

payment for goods delivered or service rendered.

Economic Risk -Refers to unfavorable economic conditions in buyer or seller‟s

country which may affect both parties in fulfilling their obligations. On the buyer

side, economic risk may result in buyer‟s insolvency or inability to accept the

goods or services. On the other hand, the seller may experience difficulty in

producing or shipping the goods per se.

Cultural Risk - Different countries have their unique language and culture. The

inability to appreciate/accept cultural differences and/or language barrier may

result in conflicts and non-completion of the sales contract.

Legal Risk - Potential for financial loss arising from uncertainty of legal

proceeding or change in legislation, such as a foreign exchange control policy. A

sales contract could be frustrated due to changes in laws and regulations.

Foreign Exchange Risk -A buyer or seller may deal with foreign currencies in

their daily course of business. This implies that they are exposed to fluctuations in

foreign exchange market which may result in paying more (by the buyer) or

receiving less (from the buyer) in terms of the local currency.

Interest Rate Risk is the risk borne by an interest-bearing asset, such as a floating

rate loan. An increase in interest rate will result in buyer or seller paying more

interest for their floating rate loan.

Political/Sovereign Risk refers to the complications that buyer or seller may

expose due to unfavourable political decisions or political changes that may vary

the expected outcome of an outstanding contract. Examples of political/sovereign

risk are changes in fiscal/monetary policy, war, riots, terrorism, trade embargoes,

etc.

Transit Risk is the risk of goods being damaged during shipment from the place

of origin to the place of destination. Failure in addressing transit risk may result in

heavy replacement cost or performance risk.

Trading companies should be mindful of the risk involved. One such step to

manage such risk is to consider payment term which varies depending on the

negotiating power of the transacting companies. Four common payment terms in

international trade: Open Account, Advance Payment, Documentary Credit and

Documentary Collection. In this paper, we focus on a documentary credit. A

documentary credit, or letter of credit, offers greater security still to the exporter,

compared with both open account trading and documentary collections. Just as with a

documentary collection, both parties to a documentary credit use their banks as

intermediaries. However, in contrast to the documentary collection, under the terms of

a documentary credit the importer‟s bank guarantees payment to the exporter, as long

as the terms of the credit are met.

Trading Company face a reduced risk by using a documentary credit compared

with documentary collections because they effectively have a guarantee of payment

from a bank. This does rely on the trading company complying with the terms of letter

of credit, so care needs to be taken in the preparation of the documentation. As with a

documentary collection, it is important that the trading company has sufficient

resource to be able to prepare and present documents in accordance with the terms of

the letter of credit However, there is still a risk that the bank may not honor the terms

of the letter of credit. There is also a country risk in the sense that payment under the

letter of credit may be affected by any debt rescheduling for that particular country.

Local customs rules also apply, and the trading company will need to ensure the

shipment does not breach the terms of any local import rules or restrictions and, if

necessary, an appropriate import licence is obtained. Because of the central role of

banks in the process, creditworthiness of the counterparty bank is also an important

source of risk. This applies particularly when exporting to a new market where the

local banks are not well known to the exporter. One solution is for the company to ask

its bank to confirm the letter of credit issued by the importer‟s bank, although this will

be at additional cost. This further mitigation of risk effectively removes bank and

country risk in the importer‟s country.

Despite this focus on the LC, over the years the term trade finance has been

shifting away from this sometimes cumbersome method of conducting business. It is

now estimated that over 80% of global trade is conducted on an open account basis.

While volumes of LCs have remained flat in recent years, their value actually

increased and they remain an essential part of emerging market trade and trade in

countries where exchange controls are in force. This increase in value is also a

reflection of the commodity price boom of 2007/08. Led by large corporates, this form

of trade saves costs and time and so has been adopted by smaller corporates as they

become more comfortable with their buyer and supplier relationships. Open account

transactions can be described as „buy now, pay later‟ and are more like regular

payments for a continuing flow of goods rather than specific transactions. This is

much cheaper for corporates.

2.2. The future use of documentary credit trade finance technique

In the aftermath of the contraction of bank credit and the increased focus on

counterparty risk, there was an expectation that the use of import letters of credit, for

example, would increase. Because letters of credit provide the seller with more

certainty with respect to a purchaser‟s promise to pay, it appeared they would become

more popular as all entities refocused on managing the risks inherent in any trade

transaction. This would have represented a significant change, as the use of import

letters of credit has been declining in recent years. In practice no clear pattern

emerged. Initially, as global trade volumes dropped, the use of letters of credit also

dropped, although whether these were directly correlated is not clear. Looking into the

future it is not obvious that there will be a revival in the use of letters of credit and

other trade instruments. They remain relatively expensive to establish, so many

companies only seek to use them when the risk profile of the transaction justifies this

cost. In other words, they remain most common for transactions with new trading

partners. In this way the letters of credit perform their traditional role, which is to

reduce the risks inherent in trade. Yet letters of credit and other trade documents also

have a funding function, especially for small and medium-sized enterprises which may

not have access to the same range of funding tools as larger entities. Letters of credit

are important in providing access to pre-export and post-shipment finance, critical

elements in those companies‟ working capital cycles. More interestingly, the

difficulties in the bank and bond markets have also changed the perspective of many

larger companies towards letters of credit and other trade finance instruments. These

instruments benefit the larger companies in two ways. Firstly, the funding techniques

open funding streams larger companies have been able to ignore in recent years. With

more emphasis on managing funding risk, treasurers in even the largest companies are

reviewing their assessment of trade instruments. Secondly, the risk management

tools incorporated into trade instruments are of increased interest as companies focus

more on managing counterparty risk. These movements have come at a time when

bank technologies have made it possible for banks to offer a more coordinated cash

and trade proposition, integrating the two sides of traditional banking activity, which

historically had remained separate.

2.2.1. Bill Discounting

Collection/ Bill Discounting is one of the conventional methods of payment in

international trade whereby the seller forwards financial and/or commercial documents

to the buyer against cash payment or acceptance of a bill of exchange. In collection,

banks control the release of documents and payments based on the Uniform Rules for

Collection ICC Publication No. 522, but do not commit to pay the seller, unlike

documentary credit operations. Collection is suitable in circumstances where the

buyer‟s solvency is not in doubt and the seller wants additional security in payment.

2.2.2. Invoice or Trust Receipt (TR) discounting

Trust Receipt (TR) is a type of short-term import loan to provide the buyer with

financing to settle goods imported under Letter of Credit where title of goods is held

by the bank. Under a TR arrangement, the Bank retains title to the goods but allows

the buyer to take possession of the goods on trust for resale before paying the Bank on

TR due date. TR financing is applicable to goods imported under documentary credit.

For documentary collection, we offer import loans against Import Invoice Financing is

a short term loan applicable to buyer who trade on open account basis.

2.2.3. Banker’s Guarantee Issuance

A Banker‟s Guarantee (BG) is a definite undertaking by the bank (guarantor) to pay

the beneficiary a certain sum of money within a specified period if the applicant

(principal) fails to fulfill his contractual or other obligations of an underlying

transaction. It is normally used to secure either a financial or performance obligation

of the principal. BG can be issued to both local and overseas beneficiary either in the

form of hardcopy or transmitted via SWIFT message MT760 or MT799.

2.2.4. Overdrafts

Overdrafts can be an effective way to finance working capital. Where offered, they are

usually relatively flexible, although this will depend on any terms and conditions

applied by the bank offering the facility. An overdraft facility allows a company to run

its current or checking account with a debit balance. Overdraft facilities should be pre-

arranged and are sometimes offered by banks without the need for formal security.

Where available, overdrafts are usually renewable on an annual basis, although in

certain jurisdictions a bank may require funds to be repaid before a facility is renewed.

In some locations it is common practice to turn an informal overdraft into a committed

facility after a period, often a month. They are not available everywhere, through

either market practice or regulation. Some countries prohibit companies from

arranging any unsecured overdrafts. In Venezuela, for example, account holders are

prohibited from writing cheques with insufficient funds to support them. Their

availability may be restricted to short periods. In some countries, for example France,

companies may only be able to arrange overdrafts for periods up to about a month,

after which banks insist on converting the arrangement to secured borrowing. Banks in

Poland, on the other hand, usually require companies to clear their overdraft facilities

once a year. Banks can withdraw overdraft facilities on demand. A bank is most likely

to withdraw such facilities from a company which relies on them, simply because such

companies represent the greatest counterparty risk to the bank. In 2009 a number of

UK companies reported that their banks withdrew part of their overdraft facilities

when the UK government arranged a moratorium on the payment of VAT.

However it occurs, any withdrawal of overdraft facilities to a company which relies on

them (whether as a permanent source of funds or as the funding of last resort) will put

significant pressure on that company‟s cash flow. Because they are unsecured,

overdrafts are often a relatively expensive method of arranging finance. For example,

overdrafts in Mexico are usually charged at more than double the prevailing rate on

treasury bills. The Basel 2 treatment of overdrafts is less favorable than other

techniques, such as invoice discounting. Banks will now be looking more often for a

facility fee and a non-utilisation fee to cover the capital costs associated with such a

facility.

2.2.5. Bank lines of credit

As an alternative to an overdraft facility, companies can arrange lines of credit with

one or more of their banks. These are appropriate when the company requires greater

security of finance or in locations where overdraft facilities are prohibited or not

available.

The company can arrange a line of credit with a bank, which it can draw against as

necessary. This will require formal documentation to be drawn up between the

company and the bank, so a line of credit will take longer to arrange than an overdraft

facility. The bank will charge an arrangement fee (for establishing the facility), a

commitment fee (for putting funds aside for the company‟s use) and a margin on all

funds actually drawn down from the facility. Different credit lines are available. Some

will require all the committed lines to be drawn down at the start of the facility and

then repaid over the term (a „term loan‟). Others will allow committed funds to be

drawn down and repaid as often as necessary (a „revolving‟ facility), as long as the

maximum level of the commitment is never exceeded at any one time. Banks require

all committed funds to be repaid at the end of the facility, although it can be possible

to roll one facility into another without repayment.

Based on the brief explanation above, we make a hypothesis:

H1 Bill discounting is more cost effective way of trade finance than Letter of

Credit

H2 Letter of Credit is mitigates risk better than Bill Discounting.

H3 Documentation for Letter of Credit is more onerous compared to that for Bill

discounting.

H4 Pricing of Clean Invoice Finance does not vary with credit-worthiness of

Borrower.

H5 Country Risk is more important than counterparty risk while pricing letter of

credit.

3. Research Methodology

These research used „Survey‟ methodology to articulate research question or the

hypothesis in the field. Questionnaire designed to administer specific set of banks who

are active in providing trade finance to trading companies. Survey research

methodology is generally mapped to relativist epistemologies (Easter-Smith, 2008,

p.83) which assume that there are regular patterns in human and organisational

behaviour which are often difficult to detect and to explain. As a result cross-sectional

designs, which enable multiple factors to be measured simultaneously, are employed.

Researcher had used factual & inferential survey designs. Factual questions in

the questionnaire were used to collect and collate the factual data on the cost

effectiveness of Invoice financing as a trade finance tool. Inferential questions in the

questionnaire which is aim to establish relationship between use of trade facility vis-à-

vis documentation intensity. Cross Sectional survey was performed by the researcher.

Participants included banks incorporated in Singapore & branches of the global banks

and trading companies were included local trading companies as well as branches of

the global trading companies. Researcher included the trading companies from varying

sizes in term of their turnover and those dealing in different trading products.

Data collected would be quantitative and any qualitative data would be

quantified. Researcher used both qualitative (non-numerical form) and quantitative

(numerical form) data for the purpose of conducting research using various sources of

data. Questionnaire and Interviews were used as in Delphi Study, where the aim is to

gather opinions from carefully selected group of experts (Collis, 2009, p.192)

Researcher used primary and secondary sources of data. For Primary sources,

interviews were carefully scheduled with bank respondents due to confidentiality or

commercially sensitiveness perceived by interviewees (Easterby-Smith, 1991 cited in

Collis, 2009, p.144). Questionnaires using Likert scale were developed as a source of

primary data. Primary Sources included self-administered questionnaires,

Interviews- Face to face, email & telephonic with the representatives of 30 Banks &

50 Trading companies. Secondary sources of data included organisation‟s websites,

annual reports, Journals etc. Official websites of 10 major banks and 8 trading

companies were reviewed for trade finance practices. Discrete details of data collected

from the respondent category-wise as per under:

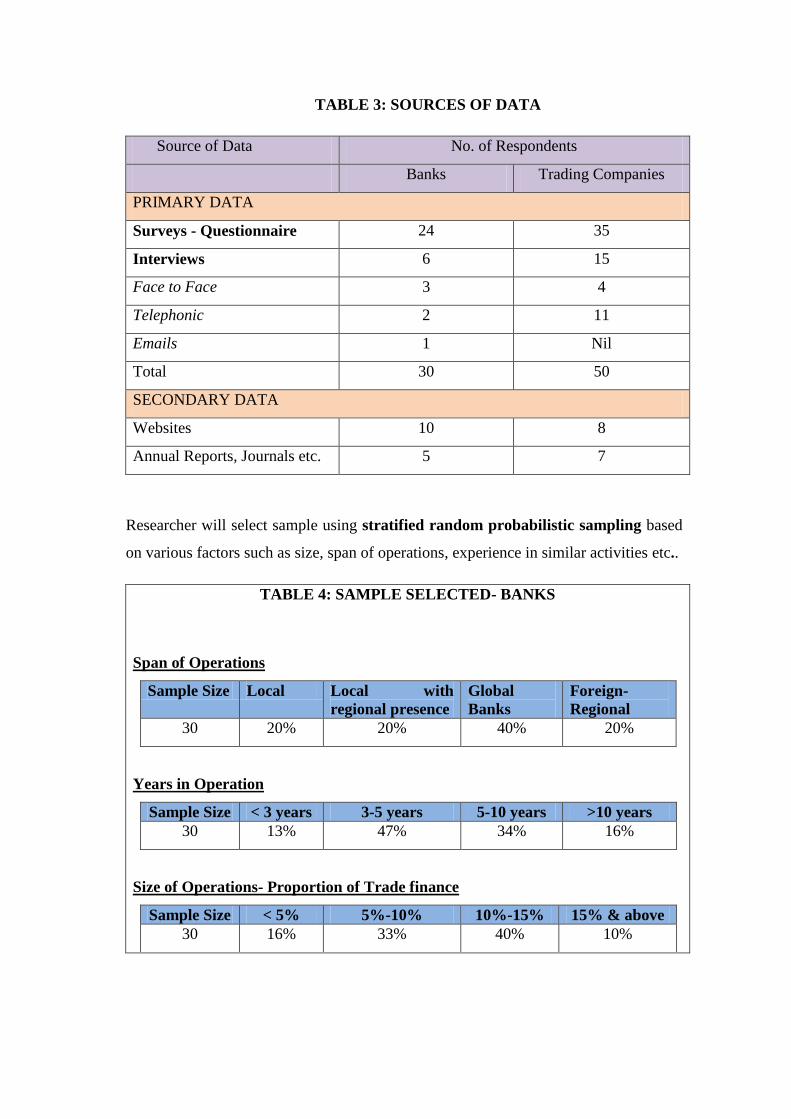

TABLE 3: SOURCES OF DATA

Source of Data No. of Respondents

Banks Trading Companies

PRIMARY DATA

Surveys - Questionnaire 24 35

Interviews 6 15

Face to Face 3 4

Telephonic 2 11

Emails 1 Nil

Total 30 50

SECONDARY DATA

Websites 10 8

Annual Reports, Journals etc. 5 7

Researcher will select sample using stratified random probabilistic sampling based

on various factors such as size, span of operations, experience in similar activities etc..

TABLE 4: SAMPLE SELECTED- BANKS

Span of Operations

Sample Size Local Local with

regional presence

Global

Banks

Foreign-

Regional

30 20% 20% 40% 20%

Years in Operation

Sample Size < 3 years 3-5 years 5-10 years >10 years

30 13% 47% 34% 16%

Size of Operations- Proportion of Trade finance

Sample Size < 5% 5%-10% 10%-15% 15% & above

30 16% 33% 40% 10%

TABLE 5: SAMPLE SELECTED- TRADING COMPANIES

Span of Operations

Sample

Size

Local Local with

regional presence

Global Foreign-

Regional

50 24% 20% 34% 22%

Business Segment

Sample

Size

Agri-

Commodities

Non-Agri (excl.

Energy)

Energy

Related

Others

50 28% 26% 28% 18%

Size of operations*

Sample

Size

< 40 40-100 100-200 200 and

above

50 30% 40% 20% 10%

* No of Trade Finance Transactions per month

Years of Operation

Sample

Size

< 3 years 3-5 years 5-10 years >10 years

50 20% 30% 30% 20%

Preferred Source of Trade Finance

Sample Size Bill

Discounting

Letter of Credit Invoice

Finance

Bankers

Guarantee

50 36% 12% 48% 4%

Researcher used Excel and SPSS (Statistical Package for Social Sciences) or

PASW (Predictive Analytics SoftWare) for analysing quantitative data. Researcher

analysed data using following statistical techniques: Researcher will use the

descriptive statistics to summarize data in a compact form so that it can be presented in

tables, charts or other graphical forms to help ascertain patterns which will aid

subsequent Hypothesis detection/ confirmation (Lovie, 1986 cited in Collis, 2009, p.

221). Researcher will analyse data by using the following descriptive statistics:

Distribution, Central Tendency Measures: Mean(μ), Mode & Median, Dispersion

Measure: Range & Standard Deviation, Normal Distribution – Skewness (extent of

asymmetry beyond +1 & -1 indicates Skewness) & Kurtosis ( extent to which

distribution is flat or peak) distribution where responses are heavily in the centre are

peaked (+3) or where scores are widely distributed (-3) are flat.

Researcher also used inferential statistics that helped to lead her to conclusions

about the target population based on the random sample (Kervin, 1992 cited in Collis,

2009, p.222). Following non parametric tests/ techniques were used since the data

collected was largely Ordinal/Nominal: Test of Association: Chi-Square test (χ²)

and Test of Correlation. Strength of association between the two variables is

measured by correlation coefficient. Pearson correlation measures linear

relationship, while Spearman correlation measures non-linear relationship. Number

varies between +1 and nearer the value to 1 more is the association either positive or

negative.

4. Results, Analysis & Discussion

4.1. Results

4.1.1. Bill Discounting was preferred by trading companies over Letter of Credit in

terms of cost effectiveness. Of the total 50 respondents from various industry segments

and varies level of operations and varied sizes, 37 of the respondents preferred Bill

discounting over Letter of credit.

4.1.2. Based on the sample data results were deduced for the total population using

chi- square test of „goodness of fit‟. Following conclusions were drawn :

We sampled 50 Trading companies and evaluated whether the Trading companies who

consider Bill Discounting was equal to the number of Traders who consider LC in

terms of cost effectiveness (expected outcome representing null Hypothesis H0). The

data was analyzed using chi square goodness of fit test. Observed frequencies for Bill

Discounting (f=37) compared with that observed for LC (f=13) was much higher. The

null hypothesis was rejected, χ² (1) = 11.520, p<0.001. Bill Discounting was

preferred by the traders over LC in terms of cost effectiveness.

4.1.3. Letter of credit was observed to be a superior product compared to Bill

discounting from the perspective of risk mitigation for trading companies. Of the total

50 respondents from various industry segments and varies level of operations and

varied sizes, 34 of the respondents preferred Letter of credit compared to 16 who

preferred Bill discounting.

4.1.4. Based on the sample data results were deduced for the total population using

chi- square test of „goodness of fit‟. Following conclusions were drawn :

We sampled 50 Trading companies and evaluated whether the Trading companies who

consider Bill Discounting was equal to the number of Traders who consider LC in

terms of risk mitigation features (expected outcome representing null Hypothesis H0).

The data was analyzed using chi square goodness of fit test. Observed frequencies for

Bill Discounting (f=34) compared with that observed for LC (f=16) was much higher.

The null hypothesis was rejected, χ² (1) = 6.480, p<0.011. Letter of Credit was

preferred by the Traders over Bill Discounting from risk mitigation perspective.

4.1.5. Documentation for Letter of Credit was observed to be more onerous

compared to that for Bill discounting. Of the total 50 respondents from various

industry segments and varies level of operations and varied sizes, 32 of the

respondents considered documentation for Letter of credit to be more onerous

compared to that for Bill discounting.

4.1.6. Based on the sample data results were deduced for the total population using

chi- square test of „goodness of fit‟. Following conclusions were drawn :

We sampled 50 Trading companies and evaluated whether the Trading companies who

consider Bill Discounting was equal to the number of Traders who consider LC in

terms of documentation intensity (expected outcome representing null Hypothesis H0).

The data was analyzed using chi square goodness of fit test. Observed frequencies for

Bill Discounting (f=32) compared with that observed for LC (f=18) was much higher.

The null hypothesis was rejected, χ² (1) = 3.920, p<0.048. Documentation is most

time consuming and greatest hurdle in in the use of Letter of Credit as a source of

finance by trading companies.

4.1.7. It was considered by respondents price premium should be based on

creditworthiness while pricing the trade finance products which are not supported by

commercial documents to reflect the risk of the borrowing trade company.

Accordingly spearman correlation coefficient ( or rs) was computed as 0.693. This

represent fairly strong positive correlation between the creditworthiness and pricing

representing better the creditworthiness (low risk) better the pricing (low price).

4.1.8. Besides Creditworthiness of the counterparty, other risk factors also have

bearing on the price premium charged by the bankers. Researcher observed that

country risk element was strongly viewed by the respondents as more potent risk

compared to counterparty risk for documentary credits.

4.2. Analysis & Discussion

4.2.1. Do Trading Companies prefer Bill Discounting over other sources of trade

finance like Letter of credit as most cost effective?

Descriptive statistical analysis: The responses received from 50 respondents of the

sample trading companies with varying size, span and business segment. Responses

were mapped on the on the Likert scale of 1 to 7, with 1 meaning „Strongly Agree‟ and

7 meaning „Strongly Disagree‟ and frequency distribution was prepared as per below:

Table 6: Frequency Distribution: Cost Effectiveness

Valid Frequency Percent Valid Percent Cumulative Percent

1 12 24.0 24.0 24.0

2 10 20.0 20.0 44.0

3 13 26.0 26.0 70.0

4 4 8.0 8.0 78.0

5 4 8.0 8.0 86.0

6 4 8.0 8.0 94.0

7 3 6.0 6.0 100.0

Total 50 100.0 100.0

It can be observed that 70% of the sample population, as represented by the right most

column in the table above, strongly agree that bill discounting is more cost effective

compared to the use of Letter of Credit. Since there are no missing numbers percent

and valid percent are the same. Histogram was plotted with normal curve

superimposed on histogram to present the visual representation of the frequency

distribution chart prepared as above.

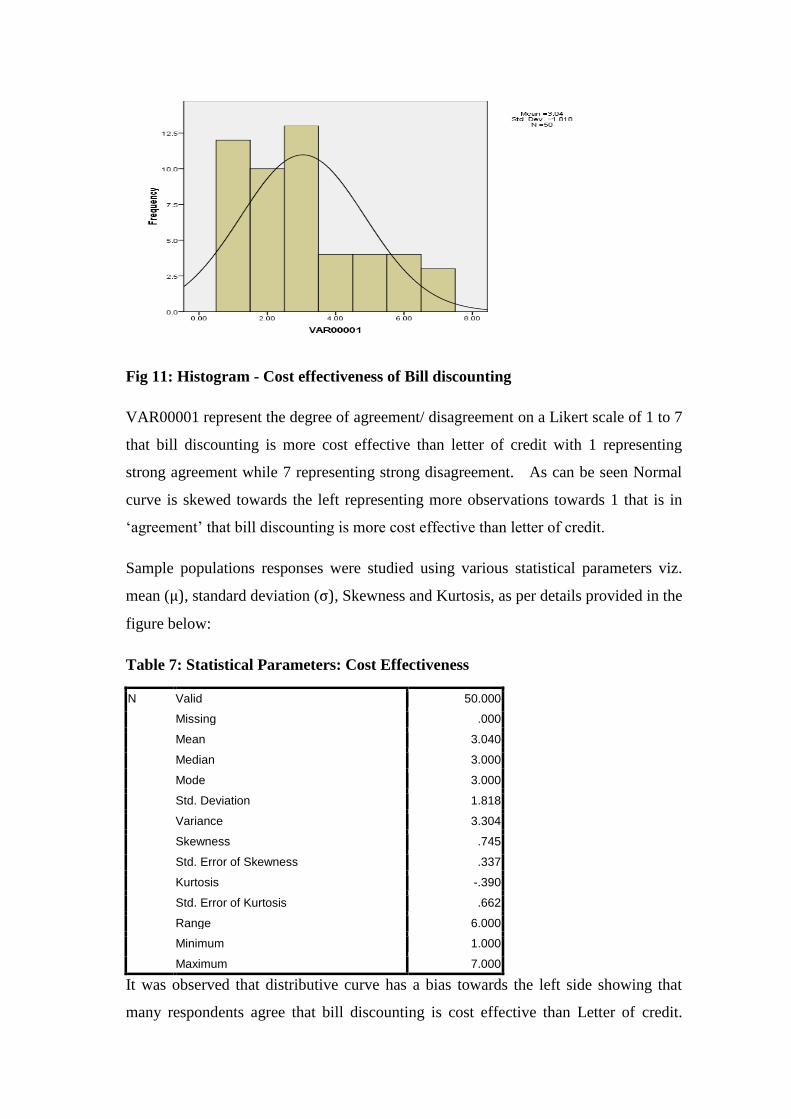

Fig 11: Histogram - Cost effectiveness of Bill discounting

VAR00001 represent the degree of agreement/ disagreement on a Likert scale of 1 to 7

that bill discounting is more cost effective than letter of credit with 1 representing

strong agreement while 7 representing strong disagreement. As can be seen Normal

curve is skewed towards the left representing more observations towards 1 that is in

„agreement‟ that bill discounting is more cost effective than letter of credit.

Sample populations responses were studied using various statistical parameters viz.

mean (μ), standard deviation (σ), Skewness and Kurtosis, as per details provided in the

figure below:

Table 7: Statistical Parameters: Cost Effectiveness

N Valid 50.000

Missing .000

Mean 3.040

Median 3.000

Mode 3.000

Std. Deviation 1.818

Variance 3.304

Skewness .745

Std. Error of Skewness .337

Kurtosis -.390

Std. Error of Kurtosis .662

Range 6.000

Minimum 1.000

Maximum 7.000

It was observed that distributive curve has a bias towards the left side showing that

many respondents agree that bill discounting is cost effective than Letter of credit.

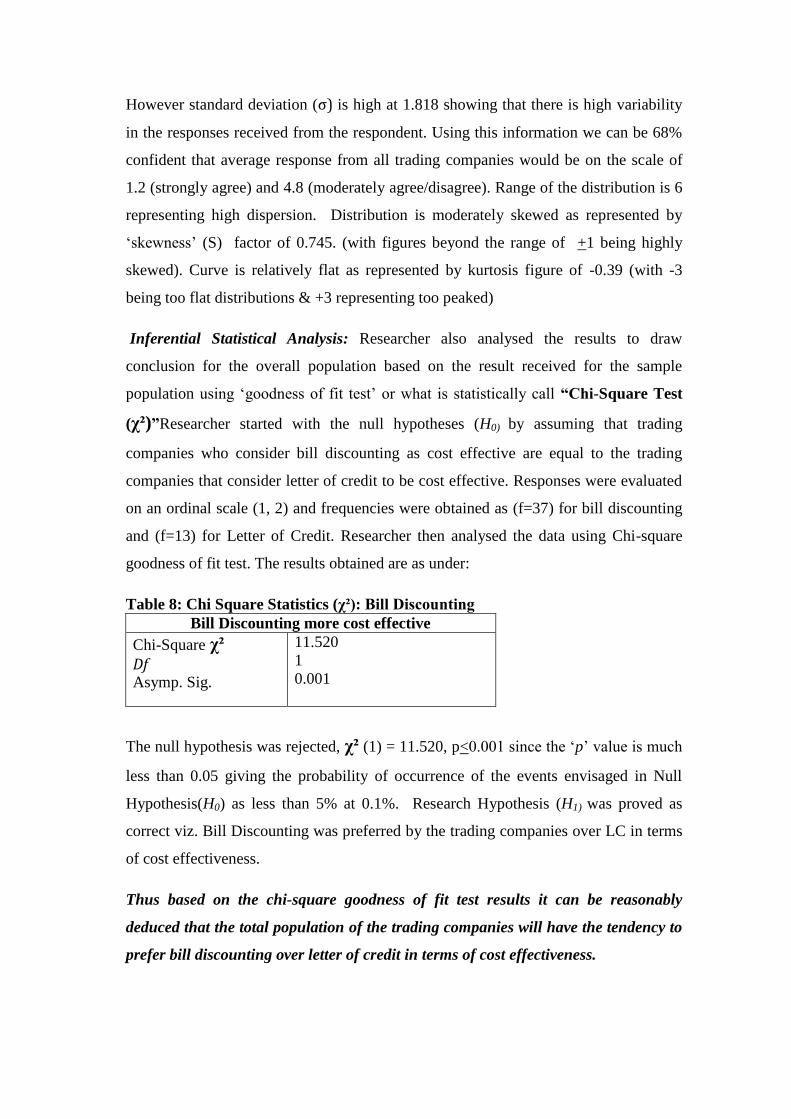

However standard deviation (σ) is high at 1.818 showing that there is high variability

in the responses received from the respondent. Using this information we can be 68%

confident that average response from all trading companies would be on the scale of

1.2 (strongly agree) and 4.8 (moderately agree/disagree). Range of the distribution is 6

representing high dispersion. Distribution is moderately skewed as represented by

„skewness‟ (S) factor of 0.745. (with figures beyond the range of +1 being highly

skewed). Curve is relatively flat as represented by kurtosis figure of -0.39 (with -3

being too flat distributions & +3 representing too peaked)

Inferential Statistical Analysis: Researcher also analysed the results to draw

conclusion for the overall population based on the result received for the sample

population using „goodness of fit test‟ or what is statistically call “Chi-Square Test

(χ²)”Researcher started with the null hypotheses (H0) by assuming that trading

companies who consider bill discounting as cost effective are equal to the trading

companies that consider letter of credit to be cost effective. Responses were evaluated

on an ordinal scale (1, 2) and frequencies were obtained as (f=37) for bill discounting

and (f=13) for Letter of Credit. Researcher then analysed the data using Chi-square

goodness of fit test. The results obtained are as under:

Table 8: Chi Square Statistics (χ²): Bill Discounting

Bill Discounting more cost effective

Chi-Square χ² Df Asymp. Sig.

11.520

1

0.001

The null hypothesis was rejected, χ² (1) = 11.520, p<0.001 since the „p‟ value is much

less than 0.05 giving the probability of occurrence of the events envisaged in Null

Hypothesis(H0) as less than 5% at 0.1%. Research Hypothesis (H1) was proved as

correct viz. Bill Discounting was preferred by the trading companies over LC in terms

of cost effectiveness.

Thus based on the chi-square goodness of fit test results it can be reasonably

deduced that the total population of the trading companies will have the tendency to

prefer bill discounting over letter of credit in terms of cost effectiveness.

4.2.2. Is Letter of credit superior product compared to Bill discounting from the

perspective of risk mitigation for trading companies?

Descriptive statistical analysis: The responses received from 50 respondents of the

sample trading companies with varying size, span and business segment. Responses

were mapped on the on the Likert scale of 1 to 7, with 1 meaning „Strongly Agree‟ and

7 meaning „Strongly Disagree‟ and frequency distribution was prepared as per below:

Table 9: Frequency Distribution: Risk Mitigation by use of LC

Frequency Percent Valid Percent

Cumulative Percent

Valid 1 28 56.0 56.0 56.0

2 18 36.0 36.0 92.0

3 4 8.0 8.0 100.0

Total 50 100.0 100.0

It can be observed that 92% of the sample population, as represented by the right most

column in the table above, strongly agree that Letter of Credit is more effective

compared to the use of bill discounting from the risk management perspective. Since

there are no missing numbers percent and valid percent are the same. Histogram was

plotted with normal curve superimposed on histogram to present the visual

representation of the frequency distribution chart prepared as above.

Fig 12: Histogram – Risk Mitigation by use of LC

“RISKLC” represent the degree of agreement/ disagreement on a Likert scale of 1 to 7

that letter of credit is more effective than bill discounting with 1 representing strong

agreement while 7 representing strong disagreement. As can be seen Normal curve is

skewed towards the left representing more observations towards 1 that is in

„agreement‟ that letter of credit is more cost effective than bill discounting from the

risk management perspective meaning trade finance availed by way of Letter of credit

proffered more safety to the trading companies compared to Bill discounting.

Sample populations responses were studied using various statistical parameters viz.

mean, standard deviation, Skewness and Kurtosis, as per details provided in the figure

below:

Table 10: Statistical Parameters: Risk Mitigation by use of LC

N Valid 50.000

Missing .000

Mean 1.520

Median 1.000

Mode 1.000

Std. Deviation .646

Variance .418

Skewness .867

Std. Error of Skewness .337

Kurtosis -.262

Std. Error of Kurtosis .662

Range 2.000

Minimum 1.000

Maximum 3.000

It was observed that distributive curve has a bias towards the left side showing that

many respondents agree that Letter of credit is effective than bill discounting from the

risk mitigation perspective meaning trade finance availed by way of Letter of credit

proffered more safety to the trading companies compared to Bill discounting. However

standard deviation is moderate at 0.646 showing that there is moderate variability in

the responses received from the respondent. Using this information we can be 68%

confident that average response from all trading companies would be on the scale of

0.874 (strongly agree) and 2.166 (moderately agree). Range of the distribution is 3

representing moderate dispersion. Distribution is near highly skewed as represented

by „Skewness‟(S) factor of 0.867. (with figures beyond the range of +1 being highly

skewed). Curve is relatively flat as represented by kurtosis(K) figure of -0.26 (with -3

being too flat distributions & +3 representing too peaked)

Inferential Statistical Analysis: Researcher also analysed the results to draw

conclusion for the overall population based on the result received for the sample

population using „goodness of fit test‟ or what is statistically call “Chi-Square Test

(χ²)”. Researcher started with the null hypotheses (H0) by assuming that trading

companies who consider bill discounting to be as effective from the risk mitigation

angle are equal to the trading companies that consider letter of credit to be cost

effective. Responses were evaluated on an ordinal scale (1, 2) and frequencies were

obtained as (f=34) for bill discounting and (f=16) for Letter of Credit. Researcher then

analysed the data using Chi-square goodness of fit test. The results obtained are as

under:

Table 11: Chi Square Statistics (χ²): Risk Mitigation by use of LC

LC mitigates risk better than Bill Discounting

Chi-Square (χ²) Df

Asymp. Sig.

6.480a

1

0.011

The null hypothesis was rejected, χ² (1) = 6.480, p<0.011 since the „p‟ value is much

less than 0.05 giving the probability of occurrence of the events envisaged in Null

Hypothesis(H0) as less than 5% at 1.1%. Research Hypothesis (H1) was proved as

correct viz. Letter of Credit was preferred by the trading companies over Bill

Discounting in terms of effectiveness from risk management perspective .

Thus based on the chi-square goodness of fit test results it can be reasonably

deduced that the total population of the trading companies will have the tendency to

prefer letter of credit over bill discounting in terms of effectiveness of LC from risk

mitigation perspective.

4.2.3. Would excessive documentation influence choice of trade finance method

employed by the trading companies?

Descriptive statistical analysis: The responses received from 50 respondents of the

sample trading companies with varying size, span and business segment. Responses

were mapped on the on the Likert scale of 1 to 7, with 1 meaning „Strongly Agree‟ and

7 meaning „Strongly Disagree‟ and frequency distribution was prepared as per below:

Table 12: Frequency Distribution – Documentation

Frequency Percent Valid Percent

Cumulative Percent

Valid 1 23 46.0 46.0 46.0

2 13 26.0 26.0 72.0

3 6 12.0 12.0 84.0

4 5 10.0 10.0 94.0

5 3 6.0 6.0 100.0

Total 50 100.0 100.0

It can be observed that 84% of the sample population, as represented by the right most

column in the table above, strongly agree that level of documentation would have

influence over the choice of the trade finance product employed by the trading

companies. Since there are no missing numbers percent and valid percent are the same.

Histogram was plotted with normal curve superimposed on histogram to present the

visual representation of the frequency distribution chart prepared as above.

FIG. 13 Histogram- Documentation Intensity of LC

LCDOC represent the degree of agreement/ disagreement on a Likert scale of 1 to 7

that Letter of credit is more document intensive than Bill discounting with 1

representing strong agreement while 7 representing strong disagreement on the Likert

scale. As can be seen Normal curve is skewed towards the left representing more

observations towards 1 that is in „agreement‟ that Letter of credit is more document

intensive than Bill discounting.

Sample populations responses were studied using various statistical parameters viz.

mean, standard deviation, Skewness and Kurtosis, as per details provided in the figure

below:

Table 13: Statistical Parameters: Documentation Intensity of LC

N Valid 50.000

Missing .000

Mean 2.040

Median 2.000

Mode 1.000

Std. Deviation 1.245

Variance 1.549

Skewness 1.046

Std. Error of Skewness .337

Kurtosis .037

Std. Error of Kurtosis .662

Range 4.000

Minimum 1.000

Maximum 5.000

It was observed that distributive curve has a bias towards the left side showing that

many respondents agree that Letter of credit is more document intensive than Bill

discounting. However standard deviation (σ) is high at 1.245 showing that there is

high variability in the responses received from the respondent. Using this information

we can be 68% confident that average response from all trading companies would be

on the scale of 0.795 (strongly agree) and 3.285(moderately agree). Range of the

distribution is 4 representing moderate dispersion. Distribution is highly skewed as

represented by „Skewness‟ (S) factor of 1.046. (with figures beyond the range of +1

being highly skewed). Curve is relatively flat as represented by kurtosis figure of -0.03

(with -3 being too flat distributions & +3 representing too peaked)

Inferential Statistical Analysis: Researcher also analysed the results to draw

conclusion for the overall population based on the result received for the sample

population using „goodness of fit test‟ or what is statistically call “Chi-Square Test”

(χ²). Researcher started with the null hypotheses (H0) by assuming that trading

companies who consider documentation requirements for bill discounting as extensive

as those for Letter of Credit to be equal to the trading companies that consider letter of

credit to be more extensive. Responses were evaluated on an ordinal scale (1, 2) and

frequencies were obtained as (f=32) for bill discounting and (f=18) for Letter of

Credit. Researcher then analysed the data using Chi-square goodness of fit test. The

results obtained are as under:

Table 14: Chi Square Statistics (χ²): Documentation Intensity of LC

LC documentation was most extensive

Chi-Square χ² Df

Asymp. Sig.

3.920a

1

0.048

The null hypothesis was rejected, χ² (1) = 3.920, p<0.048 since the „p‟ value is less

than 0.05 giving the probability of occurrence of the events envisaged in Null

Hypothesis(H0) as less than 5% at 4.8%. Research Hypothesis (H1) was proved as

correct confirming that documentation requirements for Letter of credit are more

extensive than Bill discounting.

Thus based on the chi-square goodness of fit test results it can be reasonably

deduced that the total population of the trading companies will have the tendency to

prefer bill discounting over letter of credit purely from the perspective of ease of

documentation

4.2.4. Do banks charge premium based on creditworthiness while pricing the

trade finance products to reflect the higher risk.

Descriptive statistical analysis: The responses received from 30 respondents of the

sample banks with varying size, span and level of trade finance operations were

analysed. Responses were mapped on the on the Likert scale of 1 to 7, with 1 meaning

„Strongly Agree‟ and 7 meaning „Strongly Disagree‟ and frequency distribution was

prepared as per below:

Table 15: Frequency Distribution Credit worthiness vs. Price

Valid Frequency Percent Valid Percent

Cumulative Percent

1 9 30.0 30.0 33.3

2 8 26.7 26.7 60.0

3 2 6.6 6.6 66.6

4 4 13.3 13.3 76.7

5 5 16.7 16.7 93.3

6 2 6.7 6.7 100.0

Total 30 100.0 100.0

It can be observed that 76.7% of the sample population, as represented by the right

most column in the table above, strongly agree that creditworthiness of the trading

company would have influence over the price premium charged by the bank

especially for trade finance products not supported by commercial documents viz.

Clean invoice finance. Histogram was plotted with normal curve superimposed on

histogram to present the visual representation of the frequency distribution chart

prepared as above.

FIG 14: Histogram – Creditworthiness vs. Price

PRICECREDIT represent the degree of agreement/ disagreement on a Likert scale of 1

to 7 that credit worthiness affects the price premium charged by the banks for the trade

finance facilities offered especially those not supported by the commercial documents

viz. Clean invoice finance with 1 representing strong agreement while 7 representing

strong disagreement on the Likert scale. As can be seen Normal curve moderately

Skewed towards the left representing more observations towards 1 that is in

„agreement‟ that Letter of credit is more document intensive than Bill discounting.

Sample populations responses were studied using various statistical parameters viz.

mean, standard deviation, Skewness and Kurtosis, as per details in the figure below:

Table 16: Statistical Parameters: Creditworthiness vs. Price

N Valid 30.000

Missing .000

Mean 2.700

Median 2.000

Mode 1.000

Std. Deviation 1.784

Variance 3.183

Skewness .487

Std. Error of Skewness .427

Kurtosis -1.165

Std. Error of Kurtosis .833

Range 6.000

Minimum .000

Maximum 6.000

It was observed that distributive curve has a slight bias towards the left side showing

that many respondents agree that creditworthiness somewhat determines price

premium charged by the banks for the trading companies especially where the

facilities requested for is not based on the commercial documents viz. Clean invoice

financing. However standard deviation (σ) is high at 1.784 showing that there is high

variability in the responses received from the respondent. Using this information we

can be 68% confident that average response from all trading companies would be on

the scale of 0.916 (strongly agree) and 4.484 (moderately disagree/ agree). Range of

the distribution is 4 representing moderate dispersion. Distribution is moderately

skewed as represented by „Skewness‟ (S) factor of 0.487 (with figures beyond the

range of +1 being highly skewed). Curve is relatively flat as represented by kurtosis

figure of -1.1653 (with -3 being too flat distributions & +3 representing too peaked)

Inferential Statistical Analysis: Researcher also analysed the results to draw

conclusion for the overall population based on the result received for the sample

population using correlation observed between the sample variables

“creditworthiness” and “price premium” charged by the bank. It was considered by

respondents price premium should be based on creditworthiness while pricing the

trade finance products which are not supported by commercial documents to reflect

the risk of the borrowing trade company. Accordingly spearman correlation coefficient

( or rs) was computed as 0.693. This represent fairly strong positive correlation

between the creditworthiness and pricing representing better the creditworthiness (low

risk) better the pricing (low price).

4.2.5. Do banks consider Country risk as more important factor for pricing

decision than the counterparty risk

Creditworthiness of the counterparty though does play role in price premium

determination by banks. However it was observed that Country risk element was also

strongly viewed by the respondents as more potent risk compared to counterparty risk

Descriptive statistical analysis: The responses received from 30 respondents of the

sample banks with varying size, span and level of trade finance operations were

analysed. Responses were mapped on the on the Likert scale of 1 to 7, with 1 meaning

„Strongly Agree‟ and 7 meaning „Strongly Disagree‟ and frequency distribution was

prepared as per below:

Table 17: Frequency Distribution – Country Risk Vs. Counterparty Risk

Frequency Percent Valid Percent

Cumulative Percent

Valid 1 13 43.3 43.3 43.3

2 10 33.3 33.3 76.7

3 5 16.7 16.7 93.3

4 2 6.7 6.7 100.0

Total 30 100.0 100.0

It can be observed that 93.3% of the sample population, as represented by the right

most column in the table above, strongly agree that country-risk as more potent risk

compared to the counterparty risk. Histogram was plotted with normal curve

superimposed on histogram to present the visual representation of the frequency

distribution chart prepared as above

FIG 15: Histogram- Country Risk vs. Counterparty Risk

“CountryRisk” represent the degree of agreement/ disagreement on a Likert scale of 1

to 7 that country risk is more important than the counterparty risk for trade finance

transaction. with 1 representing strong agreement while 7 representing strong

disagreement on the Likert scale. As can be seen Normal curve moderately Skewed

towards the left representing more observations towards 1 meaning thereby that

country risk is more important than the counterparty risk for trade finance products.

Sample populations responses were studied using various statistical parameters viz.

mean, standard deviation, Skewness and Kurtosis, as per details provided in the figure

below:

Table 18: Statistical Parameters- Country vs. Counterparty Risk

N Valid 30.000

Missing .000

Mean 1.867

Median 2.000

Mode 1.000

Std. Deviation .937

Variance .878

Skewness .820

Std. Error of Skewness .427

Kurtosis -.201

Std. Error of Kurtosis .833

Range 3.000

Minimum 1.000

Maximum 4.000

It was observed that distributive curve has a slight bias towards the left side showing

that many respondents agree that country risk is more important than the counterparty

risk for trade finance transaction. However standard deviation (σ) is high at 0.934,

showing that there is high variability in the responses received from the respondent.

Using this information we can be 68% confident that average response from all trading

companies would be on the scale of 0.930 (strongly agree) and 2.804 (moderately

agree). Range of the distribution is 3 representing moderate dispersion. Distribution is

moderately skewed as represented by „Skewness‟ (S) factor of 0.820 (with figures

beyond the range of +1 being highly skewed). Curve is relatively flat as represented

by kurtosis figure of -0.201 (with -3 being too flat distributions & +3 representing too

peaked)

Inferential Statistical Analysis: Researcher also analysed the results to draw

conclusion for the overall population based on the result received for the sample

population using „goodness of fit test‟ or what is statistically call “Chi-Square Test

(χ²)”. Researcher started with the null hypotheses (H0) by assuming that trading

companies who consider documentation requirements for bill discounting as extensive

as those for Letter of Credit to be equal to the trading companies that consider letter of

credit to be more extensive. Responses were evaluated on an ordinal scale (1, 2) and

frequencies were obtained as (f=22) for country risk and (f=8) for counterparty risk.

Researcher then analysed the data using Chi-square goodness of fit test. The results

obtained are as under:

Table 19: Chi -Square Statistics (χ²): Country vs. Counterparty Risk

LC documentation was most extensive

Chi-Square (χ²)

Df

Asymp. Sig.

6.533a

1

0.011

The null hypothesis was rejected, χ² (1) = 6.533, p<0.011 since the „p‟ value is less

than 0.05 giving the probability of occurrence of the events envisaged in Null

Hypothesis(H0) as less than 5% at 1.1%. Research Hypothesis (H1) was proved as

correct confirming that country risk is more important than the counterparty risk.

Thus based on the chi-square goodness of fit test results it can be reasonably

deduced that the total population of the trading companies will have the tendency to

rate country risk as a higher than the counterparty risk.

5. Conclusion & Recommendations

Research concluded that bill discounting is overall more effective than other

form of trade finance since it optimally balances the cost, documentation and risk

elements in favor of trading companies. Letter of credit on the other hand is preferred

where the risk element involved is on a higher side be it risk on account of counterpart

risk or country risk. However research concluded that despite robust risk management

features, lower use of letter of credit is on account of intensive documentation

involved. Research further concluded that country risk is more potent factor

considered by the banks where documentary credit like Letter of Credit is extended

while creditworthiness might influence pricing where trading company goes in for

other trade finance methods such as invoice financing.

Research concluded that bill discounting is overall more effective than other

form of trade finance since it optimally balances the cost, documentation and risk

elements in favor of trading companies. However it was observed that availability of

the bill discounting critically depend on the availability of existing credit lines with the

banks. Given that documentation is not extensive it can be reasonably argued that

bankers would have done due diligence while granting those credit lines to these

trading companies. Since the scope of the current result does not factor into account

the possible role of availability of the established line of credit from the banker, future

research in this area can review the role of established lines of credit in influencing the

overall choice of Trade finance methods employed by the trading companies.

Research has attempted to draw conclusions to the universe of trading

companies based on the observations made for the sample population selected with the

help of inferential statistical techniques such as “goodness of fit” test using Chi-Square

(χ²) method in respect of the findings viz. cost effectiveness of bill discounting,

effectiveness of LC in the risk mitigation and intensity of the documentation in the

Letter of credit. Conclusions of the inferential statistic confirm that the results of the

research are equally valid for the entire population since the p statistics of the Chi-

Square (χ²) test is less than 0.05.

While sample selected is representative of the industry and covered the cross

section of all significant participants in the industry in terms of size, span of operation,

business segment etc. in a fair manner so that the sample selected represents full proxy

to the Universe of trading companies i.e the entire population. However the research

included trading companies whose operations are global but the contacts have been

made to the representative based out of Singapore. For better global participation and

improve inferences at the global level future research may be done by including

representations from the Head office of the Global companies rather than their regional

offices.

Research focuses on areas where information sensitivity and confidentiality is

very high. Research has attempted to involve participant who have good

understanding, access and authority to reveal information on selective basis so that

research results are meaningful. However in view of the fact that information is

guarded and confidentiality is high in the research area, we feel that future research

would be more meaningful if conducted with the support of industry association or

self-regulatory body in terms of participation and willingness to share sensitive

information.

Researcher concluded that despite extensive documentation requirements for

Letter of credit, it remains the first choice where there is high risk perception of the

counterparty or where there is potentially strong country risk. However the possibility

of moral hazard cannot be completely ignored and there is a possibility that on account

of business exigencies, trading companies might be prone to choose riskier options

such as clean invoice finance for riskier counterparties or jurisdictions where letter of

credit would have been the ideal option. Given the criticality of this aspect future

research may focus on the moral hazard associated with various types of trade finance

sources.

REFERENCES

Berdies, D. & Anderson, J., 1974. Questionnaires: Design and Use. Metuchen, NJ:

Scarecrow Press.

Black, T. R., 1993, Evaluating Social Science Research, London: Sage.

British Chambers of Commerce, 1997. International Trade Manual, Oxford, UK:

Butterworth-Heinemann

Bryman, A., 2006. Integrating Quantitative and Qualitative Research: How it‟s done?,

Qualitative Research, Vol 6, pp.97-113.

Collis, Jill & Hussey, Roger, 2009. Business Research : A Practical Guide for

Graduate and Undergraduate Students, 3rd

ed. New York, NY: Palgrave

Macmillan

Coolican, H., 1992. Research Methods and Statistics in Psychology, London: Hodder

& Stoughton.

Creedy, J., 2001.Starting Research, The Australian Economic Review, 34(1), p.116.

Creswell, J. W., 2003. Research Design: Qualitative, Quantitative and Mixed Methods

Approaches, 2nd

ed., Thousand Oaks, CA: Sage.

Easterbay-Smith, M., Thorpe R. & Jackson Paul R., 2008, Management Research, 3rd

Ed. London: Sage Publications Ltd.

Easter-by Smith, M., Thorpe, R. & Lowe, A., 1991. Management Research: An

Introduction, London: Sage.

Edwards, P. et al, 2002. Increasing Response Rates to Postal Questionnaire:

Systematic Review, British Medical Journal, 324 May, pp.1183-91.

Fink, A., 1995. How to ask Survey Questions, Thousand Oaks, CA: Sage

Hair, Joseph F., Money Arthur H., Samouel, Phillip and Page, Mike, 2007. Research

Methods for business. England: John Wiley & Sons.

Hussey, R., 2007. The Application of personal construct theory in international

accounting research, Journal of Theoretical Accounting Research, 2(2), pp.34-

51.

Kerlinger, F. N., 1979, Behavioural Research: A Conceptual Approach, New York:

Holt, Rinehart & Winston.

Kuhn, T. S., 1962. The Structure of Scientific Revolutions, Chicago, IL: University of

Chicago Press.

Lovie, P., 1986. Identifying Outliers: New Developments in Statistics for Psychology

and Social Sciences 1, London: Methuen.

Morgan, G. & Smircich, L., 1980. The Case of Qualitative Research, Academy of

Management Review, 5, pp. 491-500.

Oppenheim, A.N., 2000. Questionnaire Design, Interviewing and Attitude

Measurement, London: Continuum International.

Patten, M., 1998. Questionnaire Research, Los Angeles, CA: Sage

Saunders, M., Lewis P. & Thornhill Adrian, 2009. Research Methods for Business

Students, 5th

ed. Harlow, England: Pearson Education Limited.

Vogt, W. P., 1993. Dictionary of Statistics and Methodology, Newbury Park, CA:

Sage.

Wallace, R.S.O. & Mellor, C. J., 1988. Non-response bias in mail accounting surveys:

A Pedagogical Note, British Accounting Review, 20, pp. 131-139.

Whiting, D. P., 1986. Finance of Foreign Trade. London: Pitman

Woodside, A.G. & Wilson, E. J. 1995., Applying Long Interview in Direct Marketing

Research, Journal of Direct Marketing Research, 9(1), 37-65