Embed Size (px)

Citation preview

Examination Technique Seminar (Case)

for

Module D on Taxation

Speaker

Dr. Fiona Lam

22 November 2012

1

EXECUTIVE TRAINING COMPANY (INTERNATIONAL) LTD

Dr Fiona Lam

Managing Director and Principal Lecturer - MC & MD

PhD, ACA(UK), FCCA, FAIA,

CPA(Practising), BBA(Acc & Fin), ATIHK

Practising partner of a medium size firm

Practical experience in corporate governance, risk management,

auditing and tax

Passed QP exams and other exams ie ACCA, AIA, PC all in one go

Professional training 9 years ago and has been teaching MC & MD

since then

Taught over 5000 students

www.etctraining.com.hk

About the Lecturer

2

Examination Technique Seminar on Section A

(Case)

• December 2011

• June 2012

• Other Hot Topics in MD

www.etctraining.com.hk

MD Taxation

December 2011 CASE

www.etctraining.com.hk

MD Taxation

3

MD – December 2011 (Case)

Case Facts

A Ltd. has engaged in the property consultancy business in Hong

Kong with annual turnover of around HK$10 million. It has

sustained a loss and recorded an overall deficit in its balance sheet

for years. In February 2009, A Ltd. came across an offer for sale of a

new 10-storey industrial building (“the Building”) from a developer.

It decided to use a Hong Kong shelf company, B Ltd., to acquire the

Building. First, A Ltd. acquired the only issued share (par value of

HK$1) in B Ltd. in March 2009. Then, in April 2009, B Ltd. acquired

the Building for HK$200 million which included the land price of

HK$100 million and the estimated construction cost of HK$50

million. The Building was classified as a fixed asset in the accounts

of B Ltd. The purchase consideration was mainly financed by a

mortgage loan from Bank C. The mortgage loan led to installment

payments (including interest) of around HK$15 million per annum.

www.etctraining.com.hk

MD – December 2011 (Case)

As B Ltd. had yet to decide on the usage of the Building, it left the

Building vacant from April 2009 to October 2009. In August 2009,

Mr. Y approached A Ltd. and showed great interest in acquiring the

Building. A Ltd. sold the share in B Ltd. to Mr. Y in the same month

and made a substantial profit.

After acquiring the share in B Ltd., Mr. Y caused B Ltd. to solicit

tenant(s) for the Building. B Ltd. eventually let the Building to a

manufacturing company as a factory (7 floors), office (2 floors) and

showroom (1 floor) for three years in November 2009.

www.etctraining.com.hk

4

MD – December 2011 (Case)

A Ltd. applied the proceeds from the sale of the share in B Ltd. to

launch its property consultancy business in the Mainland of China

(“the Mainland”). It established a number of representative offices

in the Mainland. At each representative office, A Ltd. employed

certain staff to operate a computer server and perform the liaison

work. The offices obtained job orders from the Mainland clients

through the servers and passed the orders to the Hong Kong office

for the carrying out of the research work. The final reports would

then be delivered back to the clients through the Mainland servers.

www.etctraining.com.hk

MD – December 2011 (Case)

Being a director of A Ltd., Mr. X had a service agreement with A Ltd.

which merely provided him with base salary of HK$200,000 per

month. In June 2009, A Ltd. entered into an unstamped tenancy

agreement with Mr. X whereby Mr. X would let his solely-owned

property (“the Property”) to A Ltd. for one year retrospectively from

April 2009, whilst A Ltd. would provide the Property back to Mr. X as

a free place of residence. Notwithstanding that the market rent of

the property at that time was HK$50,000, the rent provided under

the tenancy was HK$100,000 payable in arrears at the end of each

month. The mortgage interest payable by Mr. X in respect of the

Property was around HK$40,000 per month.

www.etctraining.com.hk

5

MD – December 2011 (Case)

www.etctraining.com.hk

A Ltd Property Consultancy Business (Loss)

100%

B Ltd – Shelf Company

Building –

Purchase price

HK$200m

Construction

cost - $50m

Land Cost -

$100m

Financing by

mortgage loan –

Bank C - $15m

Mr Y

Let to Manufacturing Company (3yrs) 7 floors – factory 2 floors – office 1 – show room

PRC – Representative office

MD – December 2011 (Case)

Time Line:

www.etctraining.com.hk

Sold to Mr Y

Vacant Rental Income

Apr 09 Aug 09 Oct 09 Nov 09

6

• A Ltd. employed certain staff to operate a computer server and

perform the liaison work.

• Obtain PRC Clients

Pass the jobs to HK for

research work

Give the report back

to PRC clients

MD – December 2011 (Case)

www.etctraining.com.hk

Representative Office

A Ltd Property Consultancy Business (Loss)

Mr X

Director of A Ltd

Let Mr X’s Property to A Ltd

- $100k per month

Let back to Mr

X as free place

of residence

Mortgage interest -

$40k per month

MD – December 2011 (Case)

www.etctraining.com.hk

A Ltd Property Consultancy Business (Loss)

7

MD – December 2011 (Case)

Recently, D & Co. has been engaged to review the tax affairs of A

Ltd. and B Ltd. for the year of assessment 2009/10. D & Co. had the

following findings:

1. A Ltd. did not report its profits from selling the share in B Ltd.

and its consultancy income from the Mainland clients for profits

tax purposes. For the latter income, A Ltd. neither made a return

nor payment for business tax in the Mainland.

www.etctraining.com.hk

MD – December 2011 (Case)

2. In the employer’s return for the year ended 31 March 2010, A Ltd.

declared that Mr. X had received a salary of HK$1.2 million and

had been provided with a rent-free place of residence. The rent

paid by A Ltd. in respect of that residence was HK$1.2 million.

3. In computing its assessable profits, B Ltd. deducted various

expenses which included stamp duty for the acquisition of the

Building and mortgage interest payable to Bank C. It also

claimed deduction of Industrial Building Allowance (“IBA”) in

respect of the Building.

www.etctraining.com.hk

8

MD – December 2011 (Case)

Question 1 (17 marks – approximately 30 minutes)

Discuss the following tax issues in respect of A Ltd.:

a) whether the profits from selling the share in B Ltd. are revenue or

capital in nature. (7 marks)

(Trade S14(1) – Profits tax scope)

(b) whether its consultancy service income from the Mainland clients was

derived outside Hong Kong. (6 marks)

(Profits tax scope – services income)

(c) whether it should pay business tax in respect of the above consultancy

income in the Mainland and if so, the consequences for its non-payment

of such tax. (4 marks)

(China Tax)

www.etctraining.com.hk

MD – December 2011 (Case)

Question 2 (6 marks – approximately 11 minutes)

Evaluate whether B Ltd. has properly claimed deduction of the

following in respect of the Building for the year of assessment

2009/10:

a) stamp duty on purchase; and (3 marks)

b) mortgage interest payable to Bank C. (3 marks)

(Deduction – S16(1) ; S16(2))

Question 3 (7 marks – approximately 12 minutes)

Determine whether B Ltd. is entitled to claim IBA in respect of the

Building and if so, the amount of the allowance. (7 marks)

(Profits Tax allowances)

www.etctraining.com.hk

9

MD – December 2011 (Case)

Question 4 (15 marks – approximately 27 minutes)

In respect of the quarters arrangement between A Ltd. and Mr. X,

advise:

a) how Mr. X could benefit from the arrangement for tax purposes

(Note: No computation is required); (6 marks)

(Salaries Tax – housing allowances)

b) how Mr. X should be assessed to salaries tax in respect of the

arrangement (Note: Critically analyse the arrangement and

discuss whether section 61 of the Inland Revenue Ordinance

(“IRO”) is likely to be invoked by the Inland Revenue

Department (“IRD”)). (9 marks)

(General Anti-avoidance provisions)

www.etctraining.com.hk

MD – December 2011 (Case)

Question 5 (5 marks – approximately 9 minutes)

Discuss from the ethical perspective of a tax advisor, how D & Co.

should act in view of A Ltd.'s failure to report to the IRD its profits

from selling the share in B Ltd. and its consultancy income from

Mainland clients.

(5 marks)

(Ethics – Code of ethics)

www.etctraining.com.hk

10

December 2011 CASE

- Answer -

www.etctraining.com.hk

MD Taxation

MD – December 2011 (Case) – ANSWER

Question 1(a)

• Profits tax scope - The chargeability of the profits in question

depends on whether the share in B Ltd. is a trading stock or a

long-term investment.

• Consider the intention to trade at the time of acquisition of the

asset - In Simmons case

Applying to the case :

• B Ltd. started off as a shelf company with no business activity;

• it mainly relied on the mortgage loan from Bank C to finance the

purchase consideration of the Building;

www.etctraining.com.hk

11

MD – December 2011 (Case) – ANSWER

Question 1(a) (Cont’d)

• by the sale of the subject share in August 2009, the Building had

yet to generate any income for B Ltd. to meet the mortgage

repayment; and

• the financial position of A Ltd. was also not good enough to

assist B Ltd. in repaying the mortgage loan.

• For the above reasons, it is difficult to contend that A Ltd.

intended to acquire the share in B Ltd. as a long-term

investment.

• In addition, A Ltd. acquired and sold the subject share within a

short period (only five months).

• All these facts clearly show that the relevant share transactions

were a trading venture and the profits so derived should thus be

chargeable to profits tax.

www.etctraining.com.hk

MD – December 2011 (Case) – ANSWER

Question 1(a) (Cont’d)

Extra points:

• Consider “Badges of Trade”

• Give assumption – consider the length of ownership to be the

most important

www.etctraining.com.hk

12

MD – December 2011 (Case) – ANSWER

Question 1(b)

• The broad guiding principle for determining the source of profits

– operation test [Hang Seng Bank Case and TVBI case]

• “one looks to see what the taxpayer has done to earn the profit

in question and where he has done it”.

www.etctraining.com.hk

MD – December 2011 (Case) – ANSWER

Question 1(b) (Cont’d)

• DIPN 39 stated that “the operation test” would continue to apply

in determining the source of profits earned by different types of

business via electronic commerce.

• Conducted business using a server located outside Hong Kong,

the IRD took the view that it was generally the location of the

physical business operations, rather than the location of the

server alone, that determined the locality of the profits.

• It would give greater weight to the underlying physical

operations conducted by the taxpayer to earn the profits in

question than the location of the electronic processes.

www.etctraining.com.hk

13

MD – December 2011 (Case) – ANSWER

Question 1(b) (Cont’d)

Applying to the case :

• Although A Ltd. established certain representative offices in the

Mainland to carry on a consultancy business via the internet, the

staff members of those offices were only responsible for liaison

work, whilst the servers there merely acted as a gateway for

obtaining orders from and delivering the consultancy reports to

the Mainland clients.

• All these functions were antecedent or incidental matters which

did not determine the source of the consultancy income: see

Kwong Mile Services Case

• The effective cause of such income was the research work and it

was done in Hong Kong. As such, the income should not be

regarded as having a source outside Hong Kong.

www.etctraining.com.hk

MD – December 2011 (Case) – ANSWER

Question 1(b) (Cont’d)

Extra points:

• Kwong Mile case – Consider income generating activities

• Neutrality of transactions

• Physical presence of a server is not PE

www.etctraining.com.hk

14

MD – December 2011 (Case) – ANSWER

Question 1(c)

• Article 1 of the Provisional Regulation of Business Tax of the

People Republic of China provides that all units and individuals

providing prescribed taxable services within the territory of

People's Republic of China shall be subject to business tax.

• The prescribed taxable services include, inter alia, the business

of providing services by making use of equipment, tools, sites,

information or techniques. In considering whether a taxable

service is provided “within the territory of People's Republic of

China”, the State Administration of Taxation takes the view that

the determinant is the place where the service recipient or

service provider is located, not where the service is performed.

www.etctraining.com.hk

MD – December 2011 (Case) – ANSWER

Question 1(c) (Cont’d)

Applying to the case :

• A Ltd. provided consultancy services to the Mainland clients via

servers operated in various representative offices. The services

were taxable services by making use of information about the

property market, and the service recipients were located in the

Mainland. Therefore, the income from such a consultancy

business shall be subject to business tax.

• A Ltd. neither made a return nor payment for business tax in the

Mainland. It appears that the non-compliance was entirely caused

by the mistake of A Ltd. In the circumstances, the Mainland tax

authorities may seek recourse for the business tax payment plus

a surcharge.

www.etctraining.com.hk

15

MD – December 2011 (Case) – ANSWER

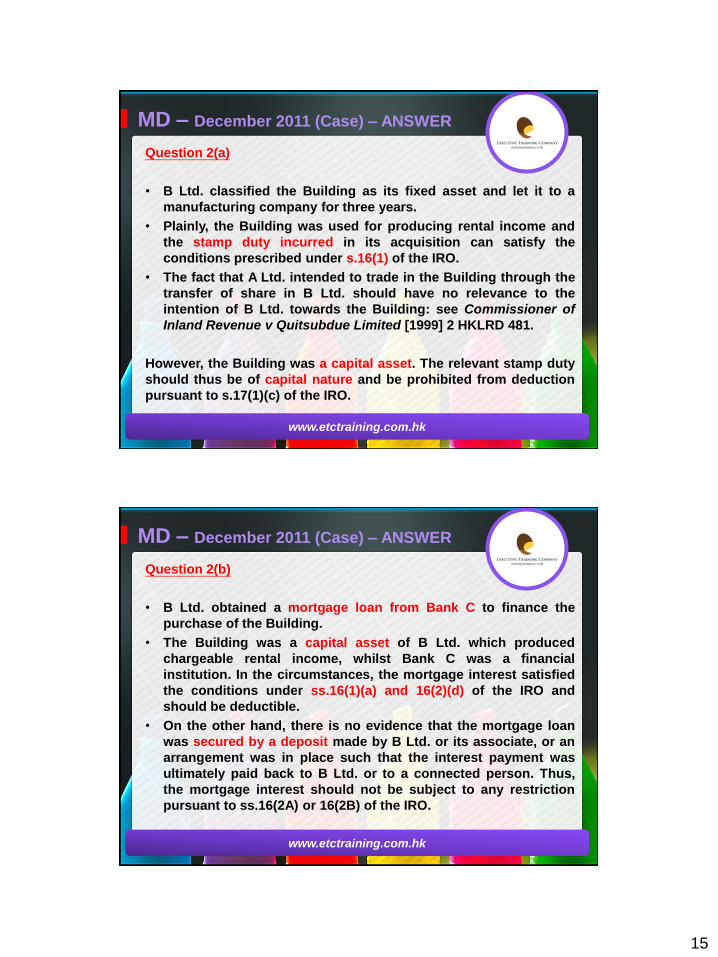

Question 2(a)

• B Ltd. classified the Building as its fixed asset and let it to a

manufacturing company for three years.

• Plainly, the Building was used for producing rental income and

the stamp duty incurred in its acquisition can satisfy the

conditions prescribed under s.16(1) of the IRO.

• The fact that A Ltd. intended to trade in the Building through the

transfer of share in B Ltd. should have no relevance to the

intention of B Ltd. towards the Building: see Commissioner of

Inland Revenue v Quitsubdue Limited [1999] 2 HKLRD 481.

However, the Building was a capital asset. The relevant stamp duty

should thus be of capital nature and be prohibited from deduction

pursuant to s.17(1)(c) of the IRO.

www.etctraining.com.hk

MD – December 2011 (Case) – ANSWER

Question 2(b)

• B Ltd. obtained a mortgage loan from Bank C to finance the

purchase of the Building.

• The Building was a capital asset of B Ltd. which produced

chargeable rental income, whilst Bank C was a financial

institution. In the circumstances, the mortgage interest satisfied

the conditions under ss.16(1)(a) and 16(2)(d) of the IRO and

should be deductible.

• On the other hand, there is no evidence that the mortgage loan

was secured by a deposit made by B Ltd. or its associate, or an

arrangement was in place such that the interest payment was

ultimately paid back to B Ltd. or to a connected person. Thus,

the mortgage interest should not be subject to any restriction

pursuant to ss.16(2A) or 16(2B) of the IRO.

www.etctraining.com.hk

16

MD – December 2011 (Case) – ANSWER

Question 3 (Cont’d)

• On the other hand, B Ltd. let the Building to a manufacturing

company which used 70% of the Building as a factory (a

qualified trade) and 30% as office and showroom (non-qualified

trade).

• As the non-qualified part exceeds one-tenth of the Building, by

virtue of s.40 of the IRO and its provisos, only 70% of the net

price should qualify for IBA.

• Of course B Ltd. may still claim Commercial Building Allowance

in respect of the remaining 30% of the net price pursuant to

s.33A of the IRO.

www.etctraining.com.hk

MD – December 2011 (Case) – ANSWER

Question 3 (Cont’d)

www.etctraining.com.hk

2 floors – offices and 1 floor show room

> 10% of the Industrial building

7 floors – Manufacturing

17

MD – December 2011 (Case) – ANSWER

Question 3 (Cont’d)

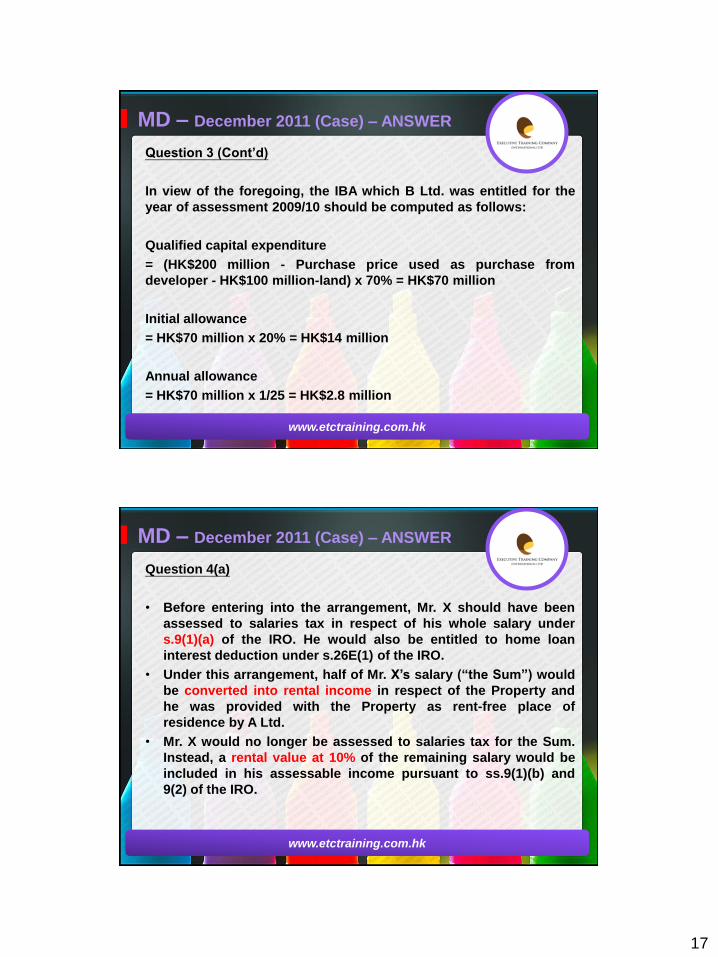

In view of the foregoing, the IBA which B Ltd. was entitled for the

year of assessment 2009/10 should be computed as follows:

Qualified capital expenditure

= (HK$200 million - Purchase price used as purchase from

developer - HK$100 million-land) x 70% = HK$70 million

Initial allowance

= HK$70 million x 20% = HK$14 million

Annual allowance

= HK$70 million x 1/25 = HK$2.8 million

www.etctraining.com.hk

MD – December 2011 (Case) – ANSWER

Question 4(a)

• Before entering into the arrangement, Mr. X should have been

assessed to salaries tax in respect of his whole salary under

s.9(1)(a) of the IRO. He would also be entitled to home loan

interest deduction under s.26E(1) of the IRO.

• Under this arrangement, half of Mr. X’s salary (“the Sum”) would

be converted into rental income in respect of the Property and

he was provided with the Property as rent-free place of

residence by A Ltd.

• Mr. X would no longer be assessed to salaries tax for the Sum.

Instead, a rental value at 10% of the remaining salary would be

included in his assessable income pursuant to ss.9(1)(b) and

9(2) of the IRO.

www.etctraining.com.hk

18

MD – December 2011 (Case) – ANSWER

Question 4(a) (Cont’d)

• On the other hand, the Sum would be assessed to property tax

by virtue of s.5(1) of the IRO after deduction of the rates paid by

Mr. X (s.5(1A) of the IRO) and 20% allowance for outgoings and

repairs (s.5(1B) of the IRO). Further, if Mr. X elected to be

assessed under personal assessment, he would also be entitled

to deduction of the mortgage interest paid in respect of the

Property under the proviso to s.42(1) of the IRO.

• The amount of such interest deduction would be greater than

that of the home loan interest deduction, which would have been

allowed to Mr. X if he had not entered into the arrangement.

• In short, the arrangement could cut down the taxable amount of

the Sum and provide a greater amount of interest deduction. Mr.

X’s overall tax liabilities could thus be reduced.

www.etctraining.com.hk

MD – December 2011 (Case) – ANSWER

Question 4(b)

• According to the terms of Mr. X’s service agreement, his

remuneration package only included a base salary. He was not

contractually entitled to any housing benefit. Although Mr. X

purported to have let the Property to A Ltd., the tenancy

agreement between the parties was unstamped which was not

admissible in evidence pursuant to ss.15(1) and (2) of the Stamp

Duty Ordinance (“SDO”).

• Apart from such agreement, there is simply no evidence that Mr.

X did let the Property to A Ltd. The Sum, which was allegedly

paid to Mr. X as rent, was no more than part of his base salary,

and it should be fully chargeable to salaries tax by virtue of

s.9(1)(a) of the IRO.

www.etctraining.com.hk

19

MD – December 2011 (Case) – ANSWER

Question 4(b) (Cont’d)

Even if it were accepted that Mr. X had let the Property to A Ltd.

which had in turn provided the Property back to Mr. X as free

quarters, the arrangement would be considered as artificial within

the ambit of s.61 of the IRO, having regard to the following:

a) The Property was at all material times owned by Mr. X. He had

every legal right to use the Property for residence. There is

neither need nor commercial sense for him to let the Property to

A Ltd. and then get it back as free quarters.

www.etctraining.com.hk

MD – December 2011 (Case) – ANSWER

Question 4(b) (Cont’d)

b) The tenancy agreement took retrospective effect for two

months before the date of execution. The rent provided

thereunder also doubled the then market rent. Unlike the

common requirement of paying rent in advance, A Ltd. was

required to pay rent to Mr. X in arrears at the end of each month.

All these terms are unusual for normal tenancy agreements

between unrelated parties dealing with each other at arm’s

length. They highlight the artificiality of the tenancy between Mr.

X and A Ltd.

www.etctraining.com.hk

20

MD – December 2011 (Case) – ANSWER

Question 4(b) (Cont’d)

As the arrangement, if left unchallenged, would reduce Mr. X’s

overall tax liabilities (see answer 4(a)), it should be disregarded

pursuant to s.61. It follows that the Sum was not rental payment to

Mr. X but part of his base salary and it should be fully chargeable to

salaries tax under s.9(1)(a).

www.etctraining.com.hk

MD – December 2011 (Case) – ANSWER

Question 5

Having noticed the failure of A Ltd. to return the profits on sale of

the share in B Ltd. and the consultancy service income from the

Mainland clients for profits tax purposes, D & Co. should take the

following actions in accordance with s.430 of the Code of Ethics for

Professional Accountants:

D & Co. should promptly advise A Ltd. of the above irregularities

and recommend that A Ltd. makes disclosure to the IRD. The firm is

not obligated to inform the IRD, nor may it do so without A Ltd’s

consent. [Confidentiality constraint]

www.etctraining.com.hk

21

MD – December 2011 (Case) – ANSWER

Question 5 (Cont’d)

As the arrangement, if left unchallenged, would reduce Mr. X’s

overall tax liabilities (see answer 4(a)), it should be disregarded

pursuant to s.61. It follows that the Sum was not rental payment to

Mr. X but part of his base salary and it should be fully chargeable to

salaries tax under s.9(1)(a).

www.etctraining.com.hk

MD – December 2011 (Case) – ANSWER

Question 5 (Cont’d)

If A Ltd. does not correct the irregularities, D & Co. should inform A

Ltd. that it cannot continue the representation in connection with

the relevant tax return and/or other related information submitted to

the authorities. The firm should also consider whether continued

association with A Ltd. in any capacity is consistent with its

professional responsibilities and if it decides to continue with its

professional relationships with A Ltd., it should take all reasonable

steps to assure that the irregularities are not repeated in

subsequent tax returns.

www.etctraining.com.hk

22

MD – December 2011 (Case) – ANSWER

Question 5 (Cont’d)

If because of the irregularities, D & Co. ceases to act for A Ltd., it

should advise A Ltd. of the position before informing the authorities

of it having ceased to act and should give no further information to

the authorities without the consent of A Ltd., unless required to do

so by law.

www.etctraining.com.hk

June 2012 CASE

www.etctraining.com.hk

MD Taxation

23

MD – June 2012 (Case)

Manchester Knitting Limited (“MKL”) is a company established in

Hong Kong carrying on a garment trading business.

The accounts and information for the year ended 31 March 2011

are provided below.

www.etctraining.com.hk

MD – June 2012 (Case)

www.etctraining.com.hk

24

MD – June 2012 (Case)

Notes:

1. The goods sold by MKL were mainly purchased from its PRC

wholly owned subsidiary and were manufactured in mainland

China. MKL reported all its trading profits as onshore in prior

years and will continue to maintain this filing basis for the year

2010/11.

2. Details of net exchange gain were as follows:

www.etctraining.com.hk

HK$

Exchange gain on trade debts [DIPN 42] 125,000

Exchange loss on foreign currency bank deposit (10,000)

115,000 Offshore

MD – June 2012 (Case)

3. Details of the gain on disposal of fixed assets

were as follows:

www.etctraining.com.hk

HK$ HK$

Sales proceeds of office furniture

(ranked into respective pool claiming for

depreciation allowance in prior years)

30,000

Original cost 150,000

Accumulated depreciation 134,000 (16,000)

Gain on disposal 14,000

25

MD – June 2012 (Case)

4. Details of interest income were as follows:

5. MKL paid a fee of HK$300,000 to an individual to provide

consultancy work regarding the company’s daily business

activities. (Expenses)

www.etctraining.com.hk

HK$

Interest from local bank deposit pledged as loan

security (per Note 7 below)

8,800

Interest from local bank deposit denominated in Euro

Dollar

5,500

Interest from overseas overdue trade debts 3,700

18,000

MD – June 2012 (Case)

6. Depreciation and additional information

on fixed assets:

Accounting depreciation of HK$84,000 was calculated on the straight-

line basis.

MKL acquired a motor vehicle on 1 August 2010 under a hire

purchase scheme with a local bank and used it for business

purposes. The cash price of the vehicle was HK$300,000. An initial

payment of HK$120,000 was made upon acquisition, and the balance

was repaid over 20 monthly installments of HK$10,000 each which

commenced on 1 September 2010. The hire purchase interest was

evenly allocated into each installment.

MKL did not have any tax written down value brought forward from

the prior year in any pool claiming depreciation allowances.

www.etctraining.com.hk

26

MD – June 2012 (Case)

7. Details of interest expenses were as follows:

www.etctraining.com.hk

HK$

Interest on bank loan secured by deposit (per Note 4

above) placed in the same bank, and on hire purchase

of the motor vehicle (per Note 6 above)

16,800

Interest to overseas unrelated suppliers on overdue

trade debts

66,000

Interest on loan from individual director 15,200

98,000 Non-Deductible

MD – June 2012 (Case)

8. The amount was a cash allowance paid to

a director of MKL.

During the year the director leased a residential flat with an

unrelated landlord and paid the rental of HK$240,000. MKL fully

subsidised the rental expenses of the director by paying a

rental allowance to him without setting any restriction on the

usage of the amount.

www.etctraining.com.hk

27

MD – June 2012 (Case)

Question 1 (19 marks – approximately 34 minutes)

a) Calculate the depreciation allowance that MKL was entitled to

claim for the year of assessment 2010/11. (3 marks)

(Consider the hire purchase)

b) Calculate the profits tax liabilities of MKL for the year of

assessment 2010/11 (ignore provisional tax). (8 marks)

(Profits Tax Computation)

c) Explain the tax treatment on the following items:

(i) interest income (4 marks)

(ii) interest expenses (4 marks)

www.etctraining.com.hk

MD – June 2012 (Case)

Question 2 (6 marks – approximately 11 minutes)

Evaluate the PRC Business Tax and Value Added Tax implications

on the sales income derived by MKL’s PRC subsidiary from goods

sold to MKL.

(6 marks)

(China Tax – PRC Business Tax and VAT)

www.etctraining.com.hk

28

MD – June 2012 (Case)

Question 3 (17 marks – approximately 31 minutes)

a) Suggest an efficient planning scheme from a salaries tax

perspective for the director of MKL to replace the cash

allowance in Note 8 of the Case, and analyse how the

proposed planning scheme for the director will be assessed

under salaries tax. (8 marks)

(Tax planning on Salaries Tax)

b) Under what circumstance would the proposed planning

scheme be tax efficient for the director from a salaries tax

perspective? (2 marks)

c) Explain how the proposed planning scheme should be

arranged in order to be accepted as a valid scheme by the

Inland Revenue Department ("IRD"). (7 marks)

www.etctraining.com.hk

MD – June 2012 (Case)

Question 4 (8 marks – approximately 14 minutes)

a) What is the basic principle to determine whether the income

derived by the consultant from MKL, as per Note 5 of the Case,

is subject to either profits tax or salaries tax? Cite a court case

to illustrate your answer.

(2 marks)

b) Outline the information that needs to be further obtained in

order to ascertain the nature of the income derived by the

consultant. Provide examples to illustrate your answer.

(6 marks)

www.etctraining.com.hk

29

June 2012 CASE

- Answer -

www.etctraining.com.hk

MD Taxation

MD – June 2012 (Case) – ANSWER

Question 1(a)

www.etctraining.com.hk

Principal

Depreciation allowances

30

MD – June 2012 (Case) – ANSWER

Question 1(b)

www.etctraining.com.hk

Capital gain

Interest income

exemption order

ND – S16(2)(c)

Offshore

MD – June 2012 (Case) – ANSWER

Question 1(c)(i)

Local bank interest income is exempt from profits tax under the

Exemption from Profits Tax (Interest Income) Order 1998 ("1998 Order").

However, the bank interest income of $8,800 derived from the deposit

utilised as security pledged to a loan incurring deductible interest

expenses (conditions under s.16(2)(d) of the Inland Revenue Ordinance

(“IRO”) are satisfied and ss.16(2A) and 16(2B) of the IRO do not apply)

would not be eligible for the exemption. Accordingly, the respective

interest income is taxable. On the other hand, the bank interest income of

$5,500 is exempt from tax under the 1998 Order regardless of the currency

denomination.

Interest income from overseas overdue trade debts is taxable as it is

derived from the normal course of business and is on-shore in nature.

www.etctraining.com.hk

31

MD – June 2012 (Case) – ANSWER

Question 1(c)(ii)

Interest to overseas unrelated suppliers on overdue trade debts is

deductible under ss.16(1)(a) and 16(2)(e) of the IRO.

As the interest derived by the individual director is not subject to

tax under the IRO, the respective interest expenses incurred by

MKL are non-deductible as the conditions under s.16(2)(c) or any

other provisions of s.16(2) of the IRO are not satisfied.

www.etctraining.com.hk

MD – June 2012 (Case) – ANSWER

Question 2

Under the Provisional Regulations of the People’s Republic of

China on Business Tax, income derived from (i) prescribed taxable

services (e.g. transportation industry, construction industry, etc.),

(ii) the transfer of intangible assets or (iii) the sale of immovable

properties in mainland China are subject to business tax. The

manufacture & sales of garment products are not prescribed

taxable services and therefore would not be subject to business

tax.

www.etctraining.com.hk

32

MD – June 2012 (Case) – ANSWER

Question 2 (Cont’d)

Under the Provisional Regulations of the People’s Republic of

China on Value Added Tax, the sale of goods, provision of

processing, repair and replacement services and the importation

of goods in mainland China are subject to Value Added Tax

(“VAT”). In this regard, the respective sales income derived by

MKL’s PRC subsidiary is subject to VAT.

The sale of garment products does not fall into any prescribed

category subject to the lower VAT rate of 13% on the sales amount,

it is therefore subject to the basic VAT tax rate of 17% on the sales

amount.

www.etctraining.com.hk

MD – June 2012 (Case) – ANSWER

Question 2 (Cont’d)

However, as the garment products manufactured by MKL’s PRC

subsidiary are sold and exported outside mainland China, the

"Exempt, Credit and Refund" method should be adopted to

calculate the VAT refund.

If the input VAT paid for the purchase of local raw materials used in

the manufacturing of export sales is larger than the output VAT,

there may be a VAT refund to MKL’s PRC subsidiary provided that

it is a general VAT taxpayer and input VAT has been paid relating to

the export sales.

www.etctraining.com.hk

33

MD – June 2012 (Case) – ANSWER

Question 3(a)

In the present situation, the rental allowance received by the

director is a cash allowance and would be subject to salaries tax in

full under s. 9(1)(a) of the IRO.

Under s.9(1A)(a)(ii) of the IRO, where an employer or an associated

corporation refunds all or part of the rent paid by the employee,

such a payment or refund is not treated as income. In this regard,

MKL can set up a rental refund scheme in order to replace the

current cash allowance with full discretion on the usage of the

money by the director.

www.etctraining.com.hk

MD – June 2012 (Case) – ANSWER

Question 3(a) (Cont’d)

Under the above mentioned rental refund scheme, MKL should

have proper controls to ensure that the director has a genuine

tenancy arrangement for residential purposes, and that the

respective amount paid to the director represents a refund of the

rental expenses.

Under s.9(1A)(b) of the IRO, a place of residence for which an

employer or associated corporation has refunded all of the rent is

regarded as being provided rent free by the employer or

associated corporation.

www.etctraining.com.hk

34

MD – June 2012 (Case) – ANSWER

Question 3(a) (Cont’d)

Under s.9(1)(b) of the IRO, if a place of residence is provided rent-

free by a taxpayer’s employer or an associated corporation, the

“rental value” of the residence is regarded as the taxpayer's

income which may be chargeable to salaries tax.

Under s.9(2) of the IRO, “rental value” is 10% (for residential flat) of

the assessable income as described in s.9(1)(a) of the IRO, after

deducting the outgoings, expenses, etc., under s.12(1)(a) and (b),

and any lump sum payment or gratuity upon the retirement or

termination of the employment of the employee. (Alternatively the

rateable value included in the valuation list prepared under s.12 of

the Rating Ordinance may be elected as the taxable “rental value”

under s.9(2)(b) of the IRO.)

www.etctraining.com.hk

MD – June 2012 (Case) – ANSWER

Question 3(b)

The scheme would be tax efficient for the director from a salaries

tax perspective if the amount of tax exempt rental refund under

s.9(1A)(a)(ii) is greater than the amount of “rental value” as laid

down under s.9(2) of the IRO.

The IRD requires that the employer has to establish clear

guidelines to control and exercise proper supervision over the

reimbursements of the rent paid by the employee as tenant to the

landlord. Only under these circumstances will the rent refund

scheme be accepted, so that the “rental value” will be included in

the employee’s assessable income while the reimbursement of

rent will not be treated as assessable income.

www.etctraining.com.hk

35

MD – June 2012 (Case) – ANSWER

Question 3(c) (Cont’d)

Proper control means that

• a clearly defined system is in place, including the ranks of those

officers entitled and the limit of the entitlements;

• there is a detailed specification of the rent refund in the contract

of employment; and

• the employer examines the tenancy agreement, rental receipts,

etc., and retains them for the record.

The IRD also requires that the tenancy agreement should be based

on the market rent, and that the normal letting formalities (e.g. duly

stamped tenancy agreement and periodic issue of rental receipts)

have been executed, and that the rights and obligations between

ordinary landlord and tenant have been observed.

www.etctraining.com.hk

MD – June 2012 (Case) – ANSWER

Question 4(a)

For an employment to exist, there must be an employer and

employee relationship or a “contract of service”. Under the

principle established in the case of Fall v Hitchen (1972) 49 TC 433

(or other relevant case), an employment relationship would not

exist if the person who has engaged himself to perform these

services performed them as a person in business on his own

account, i.e. under a “contract for service”.

www.etctraining.com.hk

36

MD – June 2012 (Case) – ANSWER

Question 4(b)

Four kinds of information should be obtained to evaluate whether

the consultancy income was derived under a contract of service or

a contract for service from a tax perspective (see Appendix B of

the Departmental Interpretation and Practice Notes (“DIPN”) No.25

(November 2011)).

1. Information regarding the degree of control exercised by MKL.

In this regard, the employer in an employment relationship will

exercise a higher degree of control over the employee as to

how the services are to be performed. Examples of information

include: Who decides the work to be done? Who prescribes the

work schedule? (or information sought in point 1 of Appendix B

of DIPN 25 (November 2011) or other relevant information)

www.etctraining.com.hk

MD – June 2012 (Case) – ANSWER

Question 4(b)(Cont’d)

2. Information regarding the capacity of the consultant of MKL to

provide the consultancy services i.e., whether the consultant

holds a position in MKL. Examples of information include: Does

the consultant represent to third parties that he/she is a staff

member of MKL? What are the chances of the consultant

getting promotion in MKL? (or information sought in point 2 of

Appendix B of DIPN 25 (November 2011) or other relevant

information)

www.etctraining.com.hk

37

MD – June 2012 (Case) – ANSWER

Question 4(b)(Cont’d)

3. Information to determine whether there is any financial risk

undertaken by the consultant in providing the services to MKL.

Examples of the information include: Are equipment, capital

assets or assistants provided by MKL to the consultant in

performing his/her duties? What is the basis of the computation

of the consultancy fee received by the consultant from MKL?

(or information sought in point 3 of Appendix B of DIPN 25

(November 2011) or other relevant information)

www.etctraining.com.hk

MD – June 2012 (Case) – ANSWER

Question 4(b)(Cont’d)

4. Information to determine whether there has been some form of

mutual obligation between the consultant and MKL. Examples

of the information include: Whether MKL is obliged to pay a

wage or remuneration? Whether the consultant is obliged to

provide his/her work? (or information sought in point 4 of

Appendix B of DIPN 25 (November 2011) or other relevant

information)

www.etctraining.com.hk

38

Other Hot Topics in MD

www.etctraining.com.hk

MD Taxation

Overall view of Hot Topics in MD

Profits Tax

• S14(1) - Profits tax scope of charge

• Source concept (- Locality of profits) DIPN 21 (Revised)

• Operation test – Hang Seng Bank Case, TVBI case

• Trade : Capital gain on disposal – Badges of trade [Marson Vs Morton]

• Capital/revenue items - S14(1)

• Doing business in Hong Kong – Permanent Establishment – Branch or

Agent - IRR 5(1)

• Deemed trading receipts – royalty S15(1)(a),(b)(ba), S21A, S20A, 20B,

Emerson case, Lam Soon Trademark Case

• Interest income – DIPN 13 and DIPN 34 – S15(1)(f) [Provision of credit

test] and Interest Income Exemption Order

• Deductible expenses - S16(1)

• Interest Expenses - S16(2), S16(2A) – (2C)

www.etctraining.com.hk

39

Overall view of Hot Topics in MD

Profits Tax

• Interest on Redevelopment Costs - Wharf Properties and Secan Case

• Interest to Non-financial institution and related to debentures -

S16(2)(c), S16(2)(f), S16(2C)

• IBA & CBA – S40(1), Balancing adjustments

• Deduction of R & D expenses – S16B

• Deduction of patent – S16E

• Building Refurbishment Expenses – S16F

• Prescribed Fixed Assets S16G

• Environment protection machinery / Installation S16H-J

• Leased assets – S39E

• Exchange differences and financial instruments DIPN 42 [Secan Case]

• Off-shore Funds - DIPN 43, S20AB, S20AC, S20 AE

• S20 Transfer Pricing , S61 and S61A General anti-avoidance

provisions

• Profits tax computation

• DTA DIPN 44 – Article 5 and 14

www.etctraining.com.hk

Overall view of Hot Topics in MD

Salaries Tax

• Salaries Tax – scope of charge – S8(1), DIPN 10, Goepfert case

• Exemption – S8(1A)(b), S8(1B), S8(1A)(c)

• Rental arrangements

• Share Options and Awards – S9(1)(d) DIPN 38

• Salaries Tax computation - allowances

• Personal assessment ie benefits

www.etctraining.com.hk

40

Overall view of Hot Topics in MD

Tax Administration

• Reporting obligations S51 and S52

• Holdover of provisional tax

• S70A Error and omission claim

• Basis Period

• DIPN 45 -47 (only briefly)

Stamp Duty

• Scope of Charge – Head 1 and 2

• Group Relief – S45

• S27(4) and S27(5)

www.etctraining.com.hk

Please refer to Handouts

www.etctraining.com.hk

Review of Profits tax scope and Royalties

41

Specific Techniques to pass MD

A. What kinds of taxes involved ?

www.etctraining.com.hk

Profits Tax 50%

Salaries Tax 30%

Others

(Property tax, Tax admin, Stamp Duty, China Tax) 20%

B. Income or expenses?

Profits Tax income

• S14(1) Charging section

• DIPN 21 (Revised)

• Operation test [Hang Seng Bank Case , TVBI case]

• S15 (Deeming Provisions) – Royalties

Profits tax expenses

• Always give General Deduction Rule S16(1) first +

Specific Deduction Rules if applicable

www.etctraining.com.hk

Specific Techniques to pass MD

42

C. Give whole set of answer

For example: Royalties income

• Scope of Charge – S15(1)(b) or S15(1)(ba)

• Tax adjustments – S21A – 30% or 100%

• Tax administration – S20A or S20B

• Emerson case

www.etctraining.com.hk

Specific Techniques to pass MD

D. Count marks

5 marks question: around 7 points

E. Tax computation

3 out of 10 for calculation

7 out of 10 for explanation

• Remember to use cross referencing

• Explanations are the most important

www.etctraining.com.hk

Specific Techniques to pass MD

43

A. Consideration of commencement of business

and termination of business

B. Always consider capital or revenue – capital gain S14(1)

not taxable Capital expenditure S17(1)(c)

C. Disposal of properties or shares – tax implication and

stamp duty implication – always consider profits tax and

stamp duty

• Profits tax: Badges of Trade

• Stamp Duty: Heads

D. Watch out for most updated cases (subject to 6-month rule)

www.etctraining.com.hk

Final Techniques to pass MD

A. Prepare your critical files

B. Only need 1 set of notes

C. Time yourself

D. Start practise writing

E. Don’t just copy – use key words for application

F. Demonstrate logical thinking – sometimes no right or

wrong

G. No need to highlight everything in the question booklet

H. Writing – legible to read

www.etctraining.com.hk

Common Techniques to pass MD

44

Knowledge Course: 10 Sessions

Boost your knowledge

Revision Course: 9 Sessions

Practice past papers and other ETC questions

Only got 1 month left – What shall you do?

• Do past papers with updated answers

• Practise writing out:

Progress test + Exam Pack (2 additional tests) + Final Mock

• Write as many questions out as possible

• Practise using your critical file

• Time yourself

www.etctraining.com.hk

MD Preparation with ETC

• The time to look-up the textbook is limited during

an open-book exam

• Students should:

have a good understanding of the topics before going into the exam

read the case and questions carefully

answer what is being asked, not what they wanted to be asked

identify the core issues of the question and allocate their time

accordingly

analyse the facts of the case and apply the tax rules or principles to

arrive at the conclusion

not copy large passages from the textbook

use logical thinking to understand and respond to the questions

www.etctraining.com.hk

Final Advice

45

At ETC, it is our aim to encourage you. Thank you!

Website: www.etctraining.com.hk Email: [email protected]