Embed Size (px)

Citation preview

eWaste

Collection and Recycling in Australia

AIIA ENVIRONMENTAL ACTIVITIES

WITSA Presentation May 2007

Agenda

• Overview eWaste

• AIIA Role

• Proposed Industry Scheme– Policy Framework– Product Flow – Financial Flow

• Questions

Overview

The new world order: an environmentally sustainable future

Gartner found global IT and communications industry produces as much carbon emissions as the global airline industry. Source: GreenerComputing.com

Corporate Responsibility:

According to Simon Mongay, Gartner’s Research Vice President, ‘with media coverage of climate change "making environmentalists out of millions of people worldwide," consumer demand for greener IT and communications is growing, and will soon force the global IT industry to take environmental concerns seriously.’

Producers must think holistically about their products’ lifecycles as the onus has shiftedfrom the consumer to the company to be more responsible for their products. Enforcement of EPR is an increasing issue.

Overview

What is eWaste?• Electronic products used for DP, T/com or entertainment in households and

businesses that are now obsolete, broken, or irreparable (Wikipedia)• Key issue is the disposal of e-waste in landfill• Three kinds of waste – Historical, Current and Future• eWaste is a source for secondary raw materials

Who’s Responsible:• Vendors think holistically about their product lifecycles • Governments try to shift responsibility from consumer to vendor • AIIA position is responsibility shared by all involved in product lifecycle. • Consumers, producers and governments have a role to play in the process. • Need to handle collection, recycling and disposal that is equitable for vendors,

consumers and environment.

AIIA “Go Green” dialogue - ICT is a green enabler to reduce carbon footprint and solve environmental issues.

Overview

• Market Trends– Consumers purchasing more laptops and smaller portable printers– EU standards (WEEE and ROHS) for environment becoming pervasive– Companies focusing on designing products for the environment– Convergence - integration of computers and other electronic devices– Approximately 40 million tonnes of eWaste generated worldwide each year– Greenpeace claim that it is more likely to be 50 million tonnes– 2006 the EU generated approximately 8.5 million tonnes of eWaste– 2006 EU collected only 0.5 tonnes of energy-intensive precious metals (Source:

Step - http://www.step-initiative.org/ – Increased competition: cheaper goods, tighter margins– Not just cost shift exercise

Overview

• Australia Specific

– Federated Model – 9 jurisdictions (Federal, States & Territories) constitutionally empowered jurisdiction over the environment

– 30 million PC’s since 1980’s – presume 80% in landfill (Meinhardt Report)• If this correct then $150m liability for industry to take back• If not correct impost much greater

– OEM Branded vs “White Box• 60/40 split

– Meets environmental objectives at lowest cost for industry and consumers

– Simple solution for consumers/end user

– Educate all stakeholders (consumers, industry and government)

AIIA Role

• Major OEMs are members– 40 to 45% of total market in sales for PCs and printers/MFPs

• Special Interest Group • Take the lead to collect EOL IT equipment* for environmentally responsible

disposal and recycling (offering the community an alternative to landfill) • Reinforce benefits of Governments adopting a streamlined national scheme

– Model underpinned by concept of ‘Shared Responsibility’ including: industry, consumers and government (all stakeholders are involved in the chain of responsibility).

– Generate solution-oriented dialogue between government and industry– Develop national ‘staged approach’– Co-regulatory approach, no “free riders”– Capitalise on existing public infrastructure (simple and lower cost)

• Recognition and reward for brand leadership

• Each manufacturer responsible for own products • User pays (included in cost) • Jointly address the issue of historic waste• Registration at point of import (narrowest point and addresses everybody)• Scaleable for national coverage, can co-exist with other take-back schemes• Establish PRO

Proposed Industry Scheme

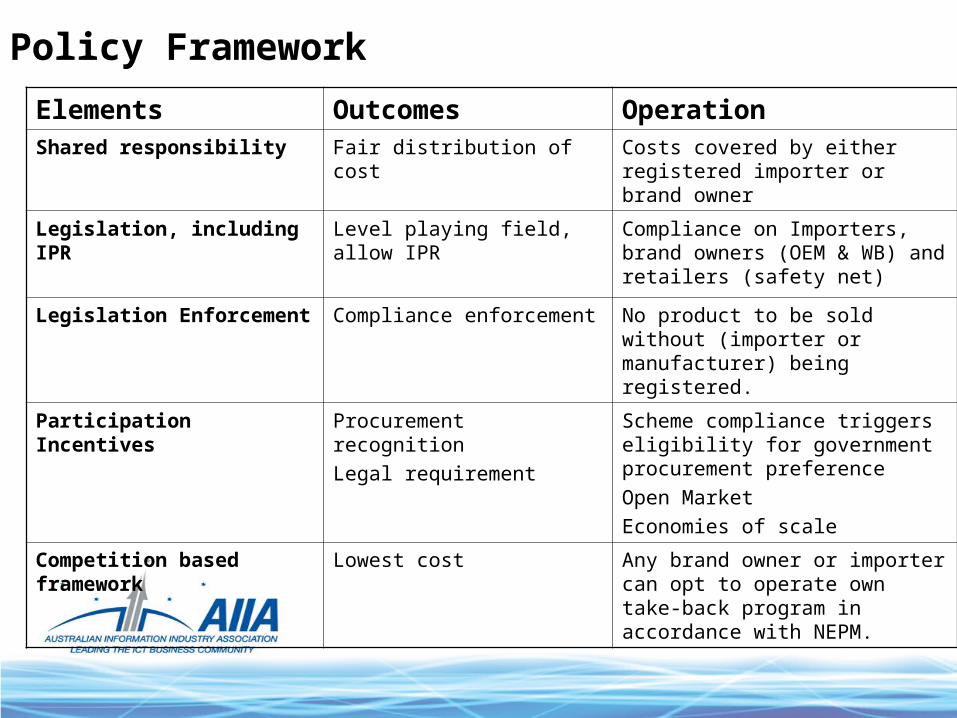

Policy Framework

Elements Outcomes OperationShared responsibility Fair distribution of cost Costs covered by either registered

importer or brand owner

Legislation, including IPR Level playing field, allow IPR Compliance on Importers, brand owners (OEM & WB) and retailers (safety net)

Legislation Enforcement Compliance enforcement No product to be sold without (importer or manufacturer) being registered.

Participation Incentives Procurement recognition

Legal requirement

Scheme compliance triggers eligibility for government procurement preference

Open Market

Economies of scale

Competition based framework

Lowest cost Any brand owner or importer can opt to operate own take-back program in accordance with NEPM.

Product imported to

Australia

Product 1) Collected and taken

to recycling / consolidation point

2) Allocated to the different schemes

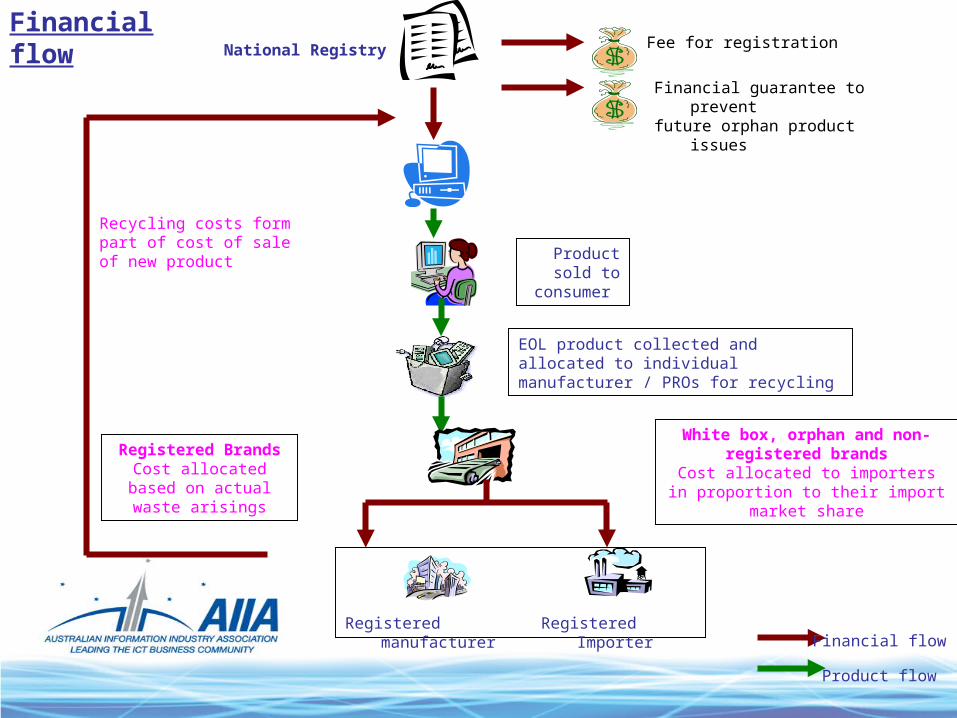

National registry• Importer and manufacturer register with the

national registry• Receive a registration number• Financial guarantee and take-back scheme are

prerequisite for the registration

Product flow

Product manufactured in

Australia

Importer / manufacturer registered Importer / manufacturer not registered

Product cannot be placed into the market until registration done

CollectionOnce EOL product returned to designated collection point by the consumer

Importer / manufacturer registered

Product can be placed into the market

Product sold to consumer

PRO 1Individual company PRO 2

Recycler 1) Recycles the products according to

agreed standard 2) Invoices the manufacturer / importer or

the PRO based on the waste arising

data

data

data

Product flow

Fee for registration

Recycling costs form part of cost of sale of new product

Financial flow

Registered BrandsCost allocated based on

actual waste arisings

White box, orphan and non-registered brands

Cost allocated to importers in proportion to their import market share

Financial guarantee to preventfuture orphan product issues

National Registry

Product sold to consumer

Registered manufacturer Registered Importer

EOL product collected and allocated to individual manufacturer / PROs for recycling

Financial flow

Product flow

Go Green - Questions

• Equitable participation for all industry

• Shared responsibility framework

• Trial to test model for participation

• Develop sustainable solution based on participants

• Find sustainable funding solution

• Show net environmental benefits