Embed Size (px)

Citation preview

0

Evolution of the GCC(Gulf Cooperation Council)

Power Grid

by: Adnan Al-Mohaisen, GM, GCCIAS. Sud, V.P., SNC-Lavalin

ICF Congress, Chicago, October 2006

1

Evolution of the GCC Power Grid• Project background

• Evolution of power sectors in the GCC countries

• Characteristics of transmission in the GCC countries

• Demand growth

• The Interconnection Project

• Benefits of interconnection

• Components of the Interconnection Project

• Capital cost of the project (Phase I)

• Sharing of the costs and financing

• Implementation strategy and project schedule

• Future development of GCC power market

• Conclusions

GULF COOPERATION COUNCIL INTERCONNECTION AUTHORITY

2

Project Background

• Gulf Cooperation Council (GCC) between Kuwait, Saudi Arabia, Bahrain, Qatar, United Arab Emirates and Oman formed in 1981

• Recognized benefits of interconnection of electricity grids of the countries

• Initial study in mid-eighties

• Preliminary project definition study in 1990 confirmed technical, economic and financial feasibility, recommended formation of GCC Interconnection Authority

• GCCIA established in 1999

• Project technical, economic and financial feasibility updated in 2003/04

• Countries decided to self-finance project in 2004

• Project tendered and awarded in 2005

3

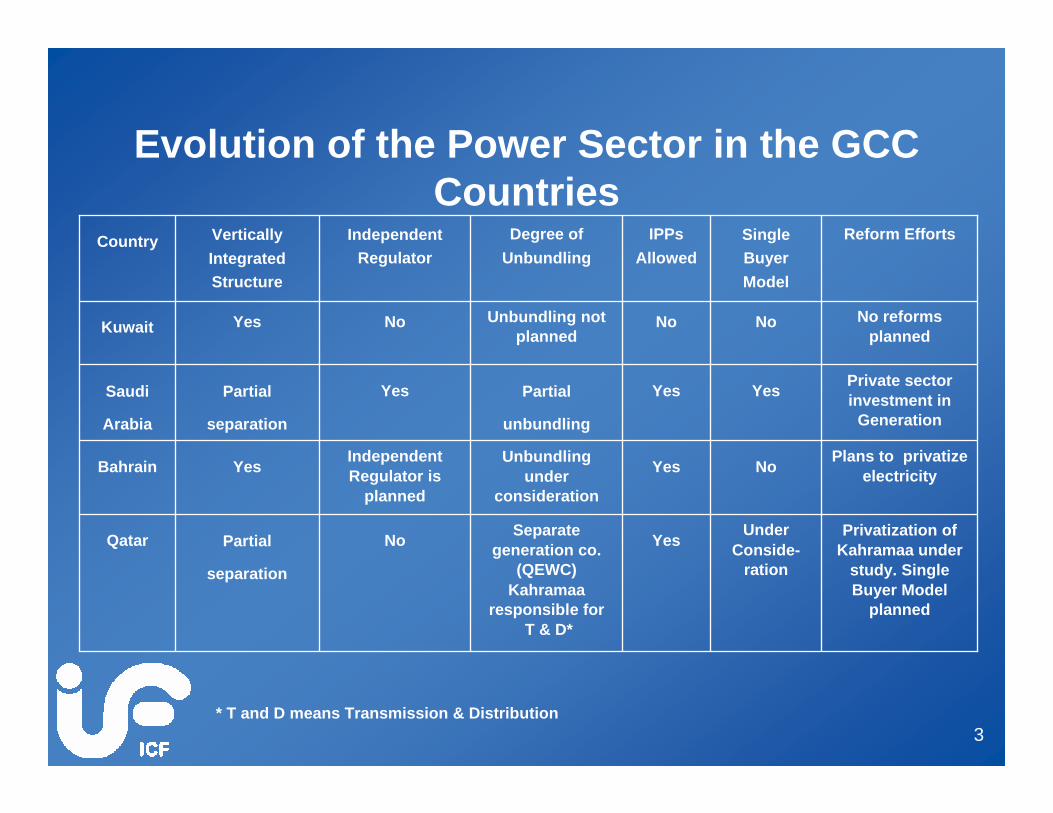

Evolution of the Power Sector in the GCC Countries

Privatization of Kahramaa under

study. Single Buyer Model

planned

UnderConside-

ration

YesSeparate generation co.

(QEWC)Kahramaa

responsible forT & D*

NoPartial

separation

Qatar

Yes

Yes

No

IPPsAllowed

Plans to privatizeelectricityNoUnbundling

under consideration

IndependentRegulator is

planned

YesBahrain

Private sector investment in

Generation

YesPartial

unbundling

YesPartial

separation

Saudi

Arabia

No reformsplanned

NoUnbundling not planned

NoYesKuwait

Reform EffortsSingle BuyerModel

Degree ofUnbundling

Independent Regulator

Vertically Integrated Structure

Country

* T and D means Transmission & Distribution

4

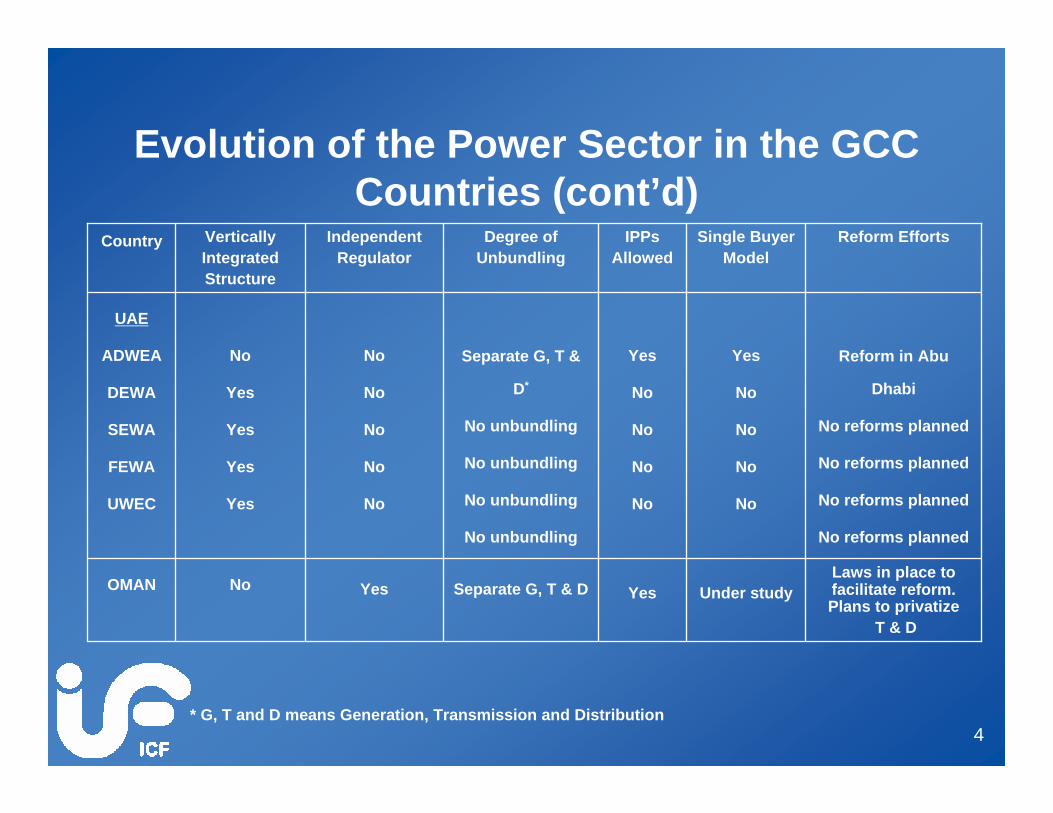

Evolution of the Power Sector in the GCC Countries (cont’d)

Laws in place to facilitate reform. Plans to privatize

T & D

Under studyYesSeparate G, T & DYesNoOMAN

Yes

No

No

No

No

IPPsAllowed

Reform in Abu

Dhabi

No reforms planned

No reforms planned

No reforms planned

No reforms planned

Yes

No

No

No

No

Separate G, T &

D*

No unbundling

No unbundling

No unbundling

No unbundling

No

No

No

No

No

No

Yes

Yes

Yes

Yes

UAE

ADWEA

DEWA

SEWA

FEWA

UWEC

Reform EffortsSingle BuyerModel

Degree ofUnbundling

IndependentRegulator

VerticallyIntegratedStructure

Country

* G, T and D means Generation, Transmission and Distribution

5

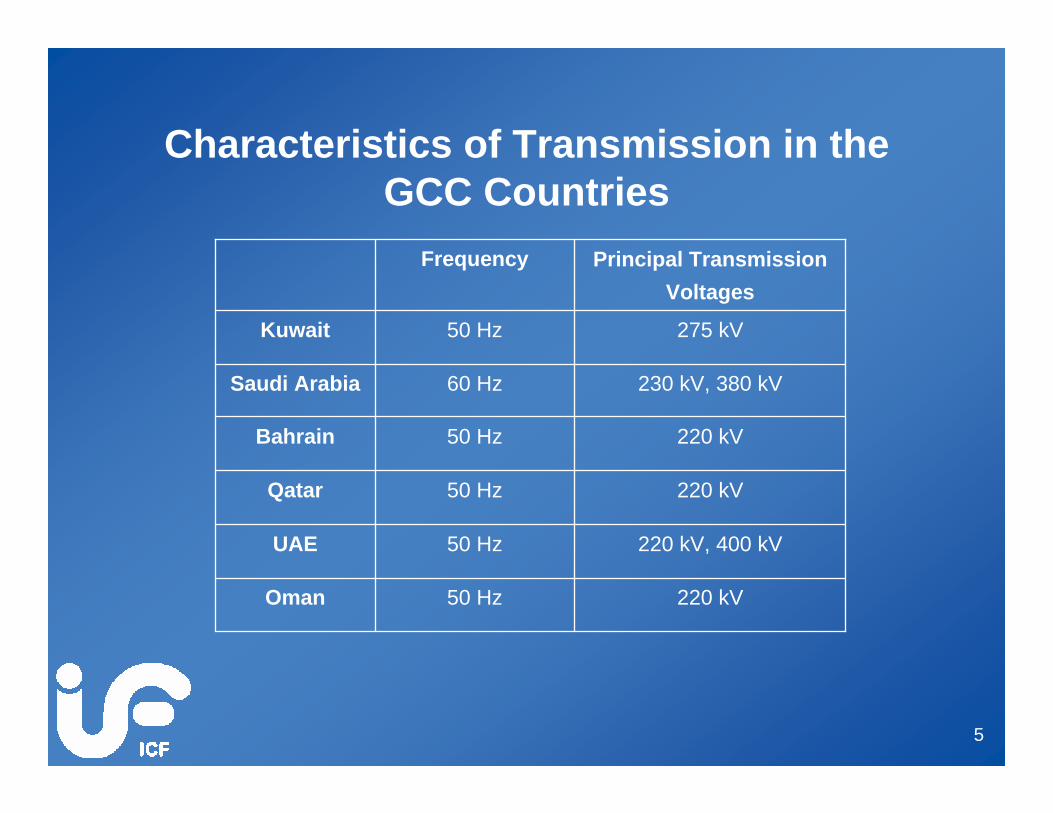

Characteristics of Transmission in theGCC Countries

220 kV50 HzOman

220 kV, 400 kV50 HzUAE

220 kV50 HzQatar

220 kV50 HzBahrain

230 kV, 380 kV60 HzSaudi Arabia

275 kV50 HzKuwait

Principal Transmission Voltages

Frequency

6

Demand Growth (MW)

93 7814 55829 3484 6494 98923 21027 0172028

71 7613 72322 3834 2123 64518 80018 9982020

49 2192 82414 3833 3872 32514 74511 5552010

44 9252 66212 7803 1842 07013 94510 2842008

32 7472 1609 1372 3081 5479 9107 6852003

TotalOmanUAEQatarBahrainSaudi Arabia*KuwaitYear

* Saudi Arabia demand supplied by SEC – ERB (represents about 38% of total load in Saudi Arabia)

7

Drivers of Demand Growth

• High oil and gas prices

• Fiscal surplus

• Increased public spending

• Attracting foreign investments

• Diversification

> Financial services

> Building industrial links

> Petrochemical industries

• Need for job creation

• Recent demand growth in region 7 to 14%

8

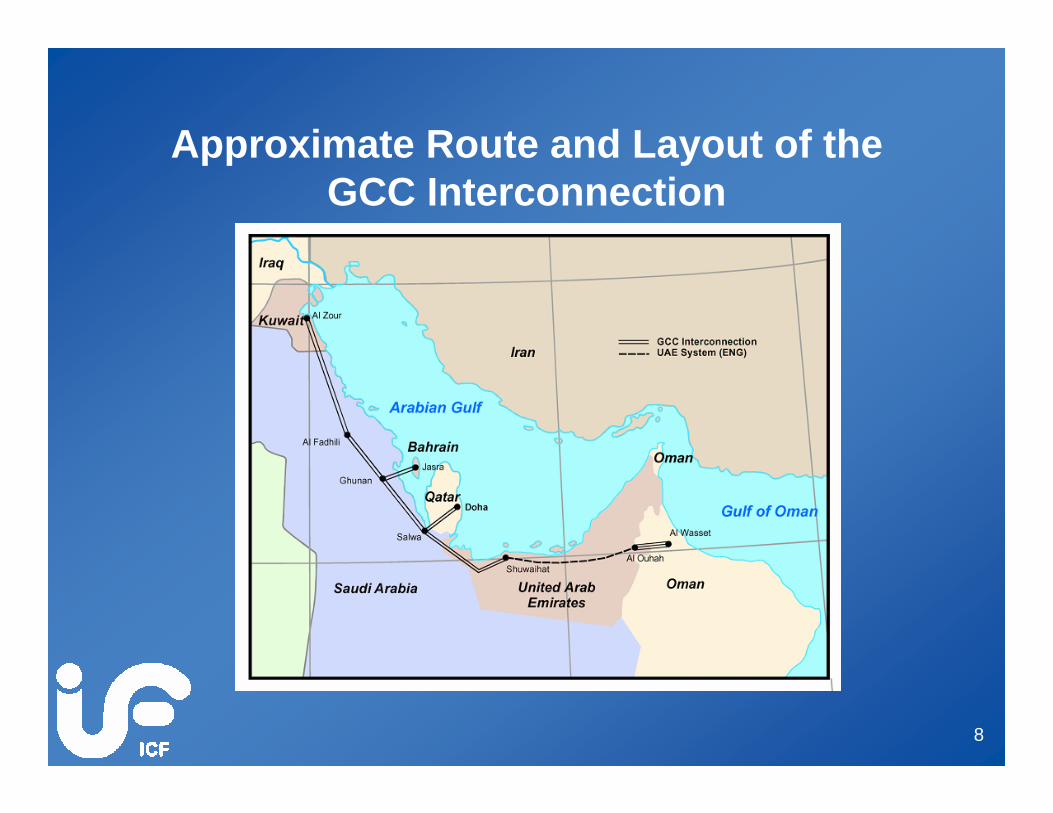

Approximate Route and Layout of theGCC Interconnection

9

Benefits of the Interconnection Project

• Result in the requirement for a lower installed capacity in each of the systems (due to reserve

sharing) while still supplying the load with the same (or better) level of reliability

• Permits larger and more efficient generating units to be installed on the individual systems

• Enables systems to share operating (spinning) reserves so that each system can carry less spinning

reserve

• Enables interchange of energy between systems resulting in a lowering of total operating costs

• Permits assistance from neighboring systems to cope with unforeseen construction delays and

unexpected load growth

• Permits emergency assistance between systems to mitigate the effects of unforeseen contingencies

such as catastrophic multiple outages

10

Principle Issues that had to be Resolved

• Agreement and participation by six GCC countries

• Demonstration of feasibility

• Creation of the GCC Interconnection Authority

• Agreement on cost sharing and financing

11

Phase I Development Plans• Kuwait

• Saudi Arabia-ERB

• Bahrain

• Qatar

• Year of Interconnection 2008

Phase II Development PlansPhase II Development Plans

• UAE – Formation of Emirates National Grid

• Oman – Formation of Oman Northern Grid

Phase III Development PlansPhase III Development Plans

• UAE

• Oman

• Year of Interconnection 2010

12

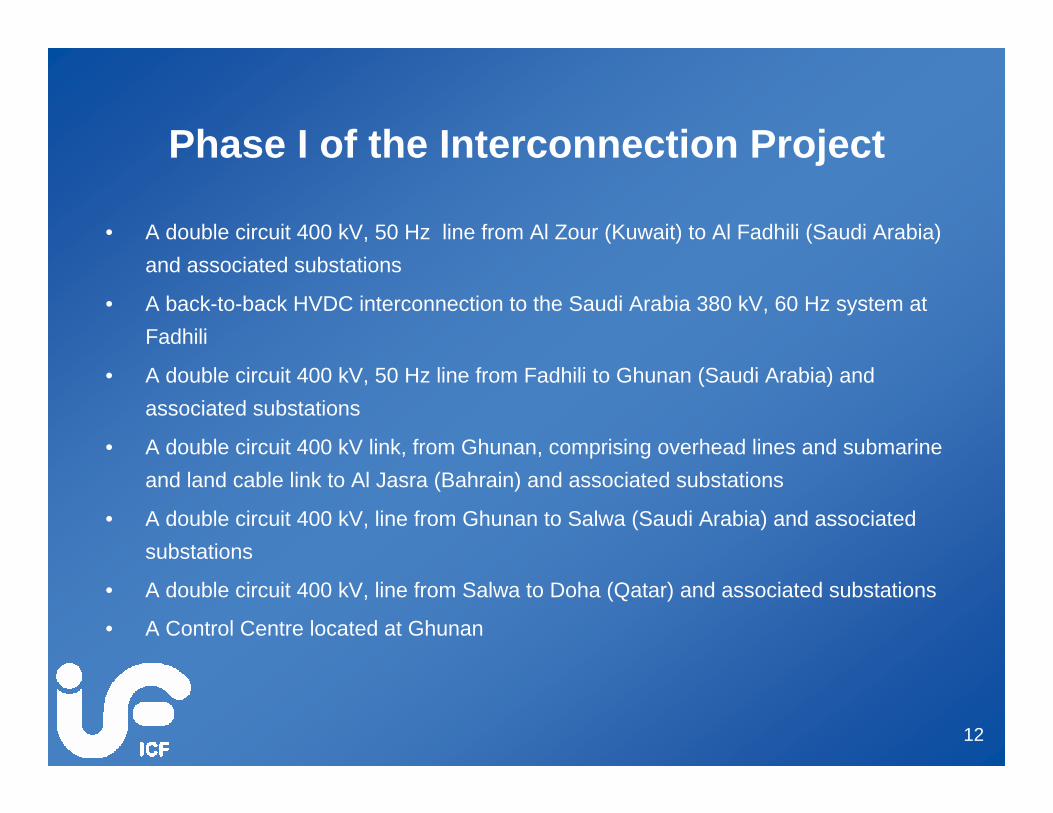

Phase I of the Interconnection Project

• A double circuit 400 kV, 50 Hz line from Al Zour (Kuwait) to Al Fadhili (Saudi Arabia) and associated substations

• A back-to-back HVDC interconnection to the Saudi Arabia 380 kV, 60 Hz system at Fadhili

• A double circuit 400 kV, 50 Hz line from Fadhili to Ghunan (Saudi Arabia) and associated substations

• A double circuit 400 kV link, from Ghunan, comprising overhead lines and submarine and land cable link to Al Jasra (Bahrain) and associated substations

• A double circuit 400 kV, line from Ghunan to Salwa (Saudi Arabia) and associated substations

• A double circuit 400 kV, line from Salwa to Doha (Qatar) and associated substations

• A Control Centre located at Ghunan

13

Phase III of the Interconnection Project

• A double circuit 400 kV, line from Salwa (Saudi Arabia) to Shuwaihat (UAE) and associated

substations

• A double circuit 220 kV, line from Al Ouhah (UAE) to Al Wasset (Oman) and associated substations

• A single circuit 220 kV, line from Al Ouhah to Al Wasset and associated substations

14

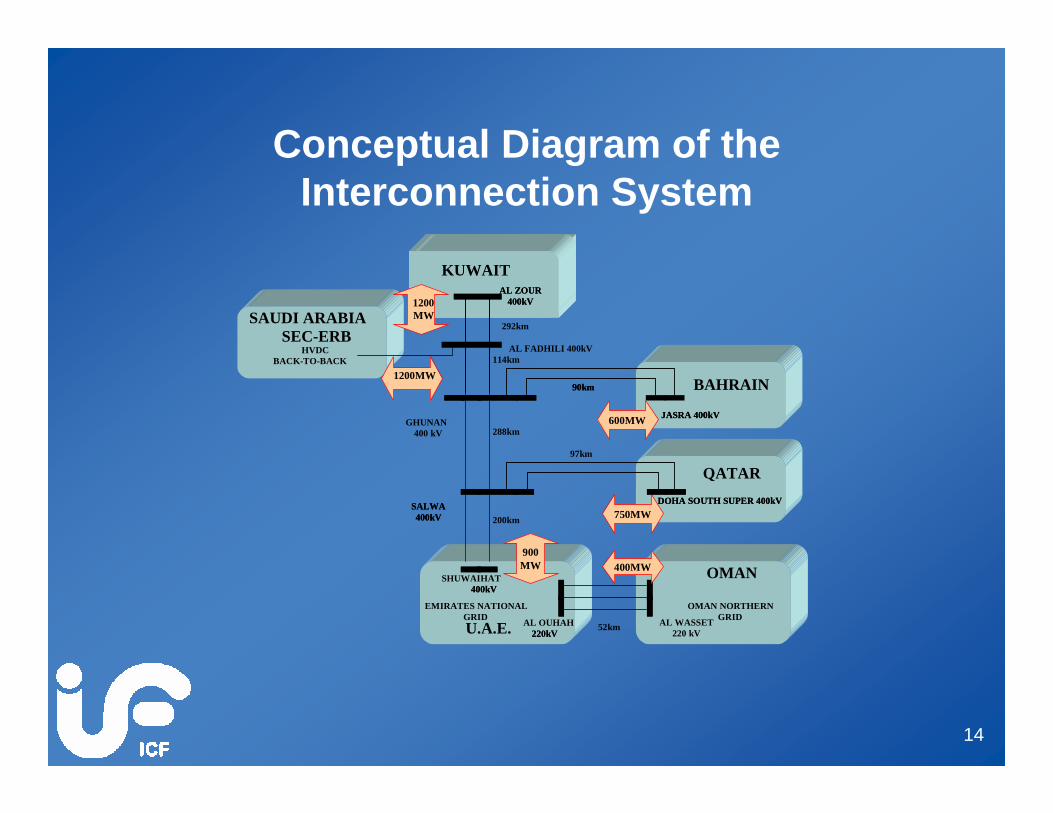

Conceptual Diagram of the Interconnection System

BAHRAIN

U.A.E. EMIRATES NATIONAL

GRID AL OUHAH220kV220kV

AL FADHILI 400kV

JASRA 400kVJASRA 400kVGHUNAN

400 kV 600MW

SALWA400kV

SALWA400kV

QATAR

750MW

90km90km

DOHA SOUTH SUPER 400kVDOHA SOUTH SUPER 400kV

288km

200km

SHUWAIHAT400kV400kV

900MW OMAN

OMAN NORTHERNGRIDAL WASSET

220 kV

400MW

52km

114km

97km

KUWAIT AL ZOUR

400kVAL ZOUR

400kV

292km

1200 MW SAUDI ARABIA

SEC-ERBHVDC

BACK-TO-BACK 1200MW

15

Simplified Single-Line Diagram of the Interconnection

G8

LEGEND

Note: All Substations are GIS, 1-1/2 Breaker Scheme

3 x 650 MVA

Umm An Na-S

an

Island

Ras Al-Q

urayya

h

Substati

on

Qatari 132 kVNetwork

Doha SouthSubstation

97 km

Projected Phase III(Shuwaihat UAE)

SalwaSubstation

Qatari 220 kVNetwork (4 circuits)

Doha south(Qatar)1 x 125 MVAR

3 x 400 MVA

400 kV

2 x 150 MVA

220 kV

4 x 125 MVAR

400 kV

AL-FADHILI SUBSTATION(KSA)

288 km

GhunanSubstation

GCCIAControl Centre

114 km

4 x 125 MVARAl Jasra

Substation3 x 325 MVA

42.5 km (Submarine Cable)40 km

400 kV

2 x 125 MVAR +2 x 300 MVAR

Bahraini 220 kVNetwork (2 circuits)

400 kV

SEC-ERB 380 kVNetwork (7 Circuits)

Al-FadhiliSubstation

292 km

Al-ZourSubstation

3 x 600 MW400 kV, 50 Hz

2 x 125 MVAR 2 x 125 MVAR

Back-to-BackConverter Facility

2 x 125 MVAR

400 kV

Al Jasra(Bahrain)

Bahraini66 kVNetwork

2 x 150 MVA

220 kV

SEC-ERB 220 kVNetwork

4 x 750 MVA

380 kV, 60 Hz

Shunt Reactor

Power Transformerwith OLTC

HVDC Converter

Overhead LineUnderground CableSubmarine Cable

AL-ZOUR POWER STATION(KUWAIT)

G1 G2

2500 MW

Kuwaiti 275 kVnetwork (6 Circuits)

275 kV

16

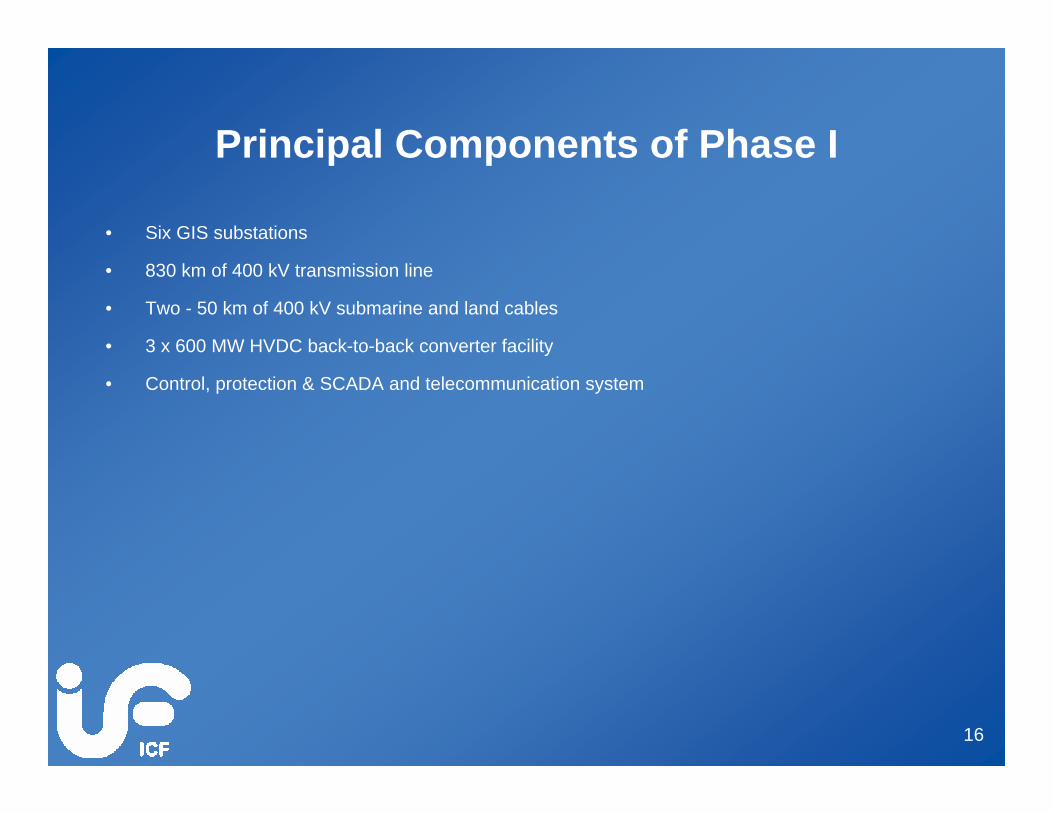

Principal Components of Phase I

• Six GIS substations

• 830 km of 400 kV transmission line

• Two - 50 km of 400 kV submarine and land cables

• 3 x 600 MW HVDC back-to-back converter facility

• Control, protection & SCADA and telecommunication system

17

400 kV Overhead Transmission Lines

Conductor: 740 MCM, AAAC, Flint

4 conductors / phase

Total length ≈ 19,500 km

Ground Wire: 2 OPGW

Total length ≈ 1,700 km

18

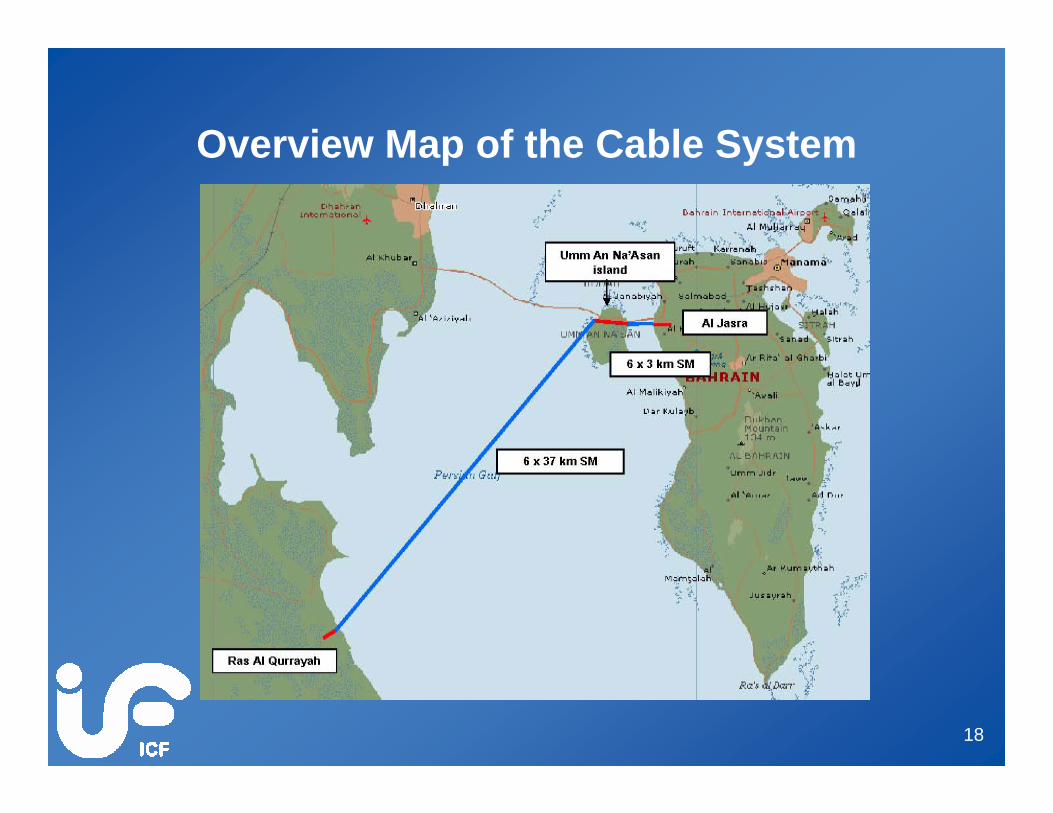

Overview Map of the Cable System

19

Submarine Cables - Description

Total Total LengthLength ≈≈ 6 x 40 km = 240 km6 x 40 km = 240 km

20

Land Cables - Description

Total Total LengthLength ≈≈ 6 x 9 km = 54 km6 x 9 km = 54 km

21

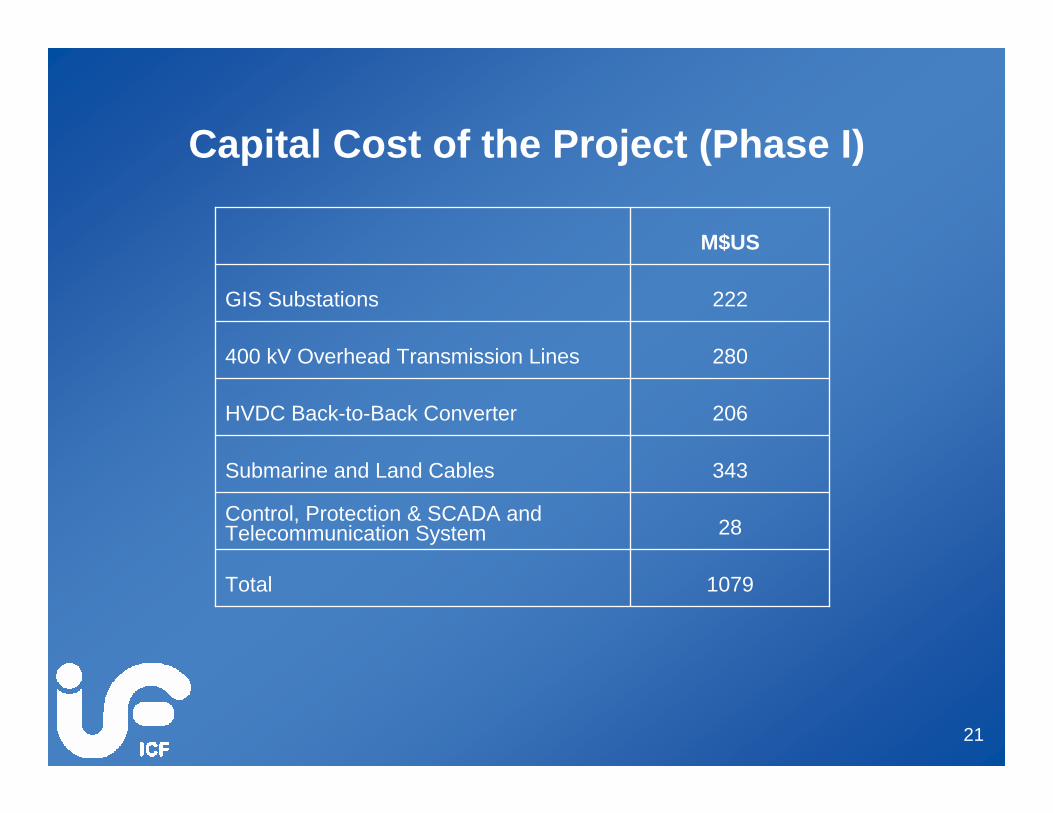

Capital Cost of the Project (Phase I)

1079Total

28Control, Protection & SCADA and Telecommunication System

343Submarine and Land Cables

206HVDC Back-to-Back Converter

280400 kV Overhead Transmission Lines

222GIS Substations

M$US

22

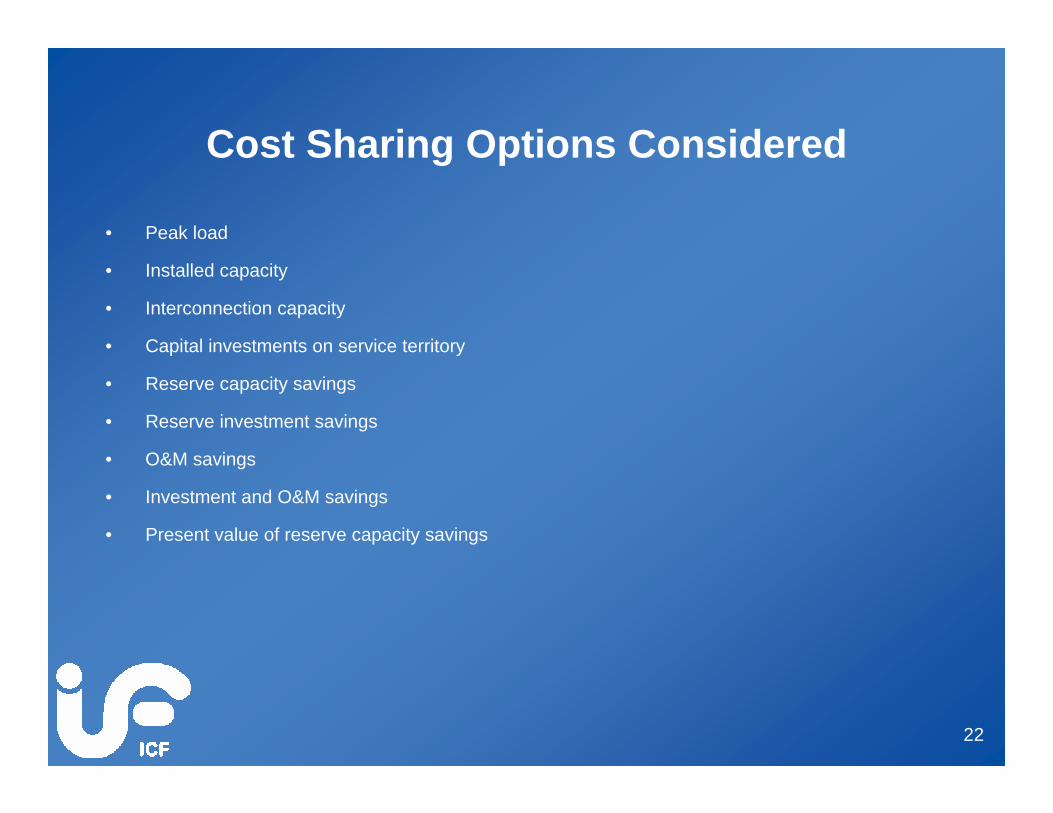

Cost Sharing Options Considered

• Peak load

• Installed capacity

• Interconnection capacity

• Capital investments on service territory

• Reserve capacity savings

• Reserve investment savings

• O&M savings

• Investment and O&M savings

• Present value of reserve capacity savings

23

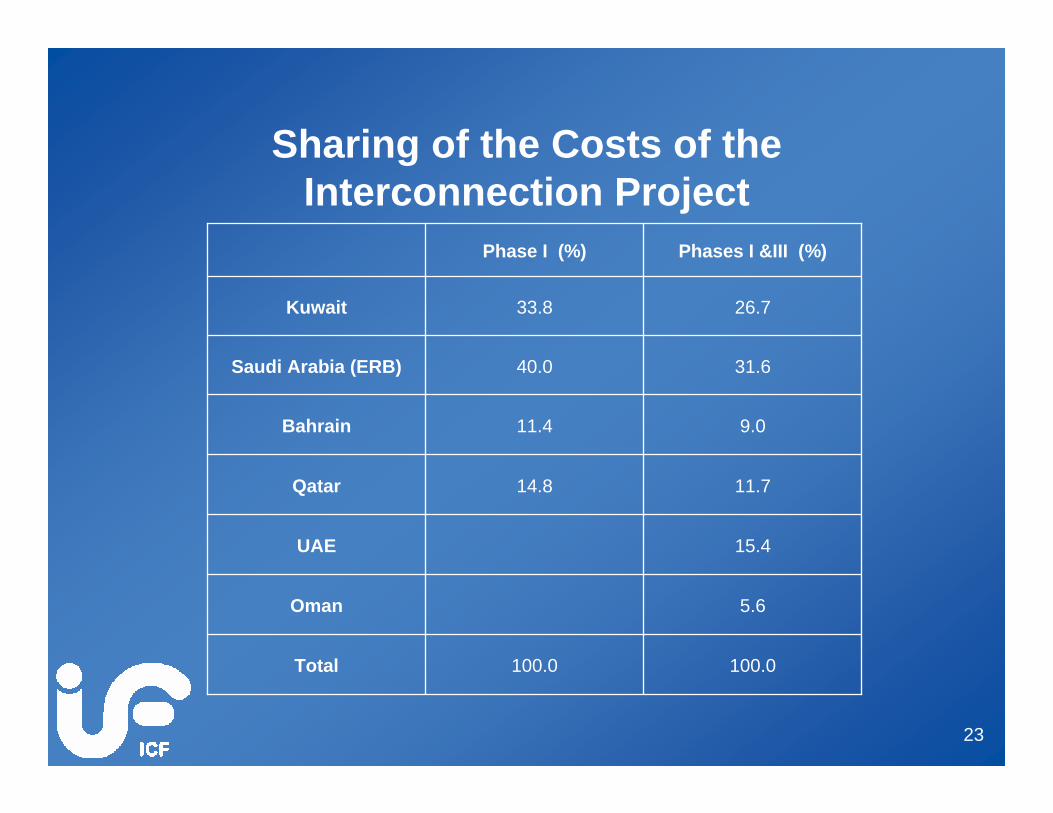

Sharing of the Costs of the Interconnection Project

100.0100.0Total

5.6Oman

15.4UAE

11.714.8Qatar

9.011.4Bahrain

31.640.0Saudi Arabia (ERB)

26.733.8Kuwait

Phases I &III (%)Phase I (%)

24

Financing Options Considered

50%25%25%50%50%5

65%17.5%17.5%50%50%4

65%35%--100%--3

65%--35%--100%2

----100%--100%1

Private SectorGovernment

LoansCapitalPrivate SectorGovernment

Sources of FinanceOwnershipFinance Options

25

Implementation Strategy

GCCIA

Contract Package 1 Contract Package 2 Contract Package ..n

Owner’s Engineer

Contract Administration Contract Supervision& Coordination

Functional Relationships

26

Contract Packages

• Six – 400 kV Substations

• One – HVDC Converter Station Package

• Four – Overhead Transmission Line Packages

• One – Submarine / Land Cable Package

• Control Centre Package

> GCC Control Centre

> Telecommunications, Control & Protection

27

Project Schedule

Early 2009Project Operation

November 2005Contracts Awarded

September 2005Tenders Evaluated and Recommendation for Award

June 2005Tenders Received

February 2005Issue of Tender Documents

May 2004Approval of Project Financing

2003 / 2004Update Technical and Economic Feasibility

28

Future Development of the GCC Power Market

• Once the GCC Grid is in place this will enable the GCC electricity market to develop in a step-by-

step manner:

> Allow competition in generation in the countries through IPPs and set up a single buyer

> Establish vertical separation to enhance competition

> Establish open access to transmission to allow generators to sell to other countries

> Form a national and ultimately regional power market

• Link to other regional grids

29

Evolution of the Market from Single Buyer to a Wholesale Market

Wholesale MarketMandatory Pool

Single Buyer

Single Buyer with

Generation Pool

Hybrid Market(Bilateral Trading)Central Purchaser

Wholesale MarketVoluntary Pool

30

Conclusions

• Project under-study since mid-eighties

• Agreement and participation required by six GCC countries

• Principal Issues that had to be resolved

> Demonstration of feasibility

> Agreement between countries

> Creation of the GCC Interconnection Authority

> Agreement on cost sharing and financing

• Project is now under implementation

• Once implemented the Project will enable development of a GCC Electricity Market