Embed Size (px)

Citation preview

EVALUATION OF THE COMMON MARKET ORGANISATION (CMO) IN THE CEREAL SECTOR

NATIONAL REPORT — UK

David Jackson

LMC International Ltd

Oxford, England

Contents (i)

Table of Contents

Case Study Monograph — UK..................................................................................... 1

1. Overview of National Report — UK ............................................................................ 1

1.1 Rationale ......................................................................................................... 1 1.2 Structure.......................................................................................................... 1

2. An Introduction to the Cereals Sector......................................................................... 2

2.1 UK ................................................................................................................... 2 2.2 England ........................................................................................................... 6 2.3 Scotland .......................................................................................................... 7

3. Producers’ Income Levels .......................................................................................... 9

3.1 Overview ......................................................................................................... 9 3.2 Net Farm Value Added per Annual Work Unit............................................... 10 3.3 National Farm Income Sources..................................................................... 10 3.4 Non-Farm Incomes........................................................................................ 12 3.5 Land Prices and Rentals ............................................................................... 13 3.6 General Conclusions ..................................................................................... 15

4. Dependence on Direct Payments ............................................................................. 15

4.1 Overview ....................................................................................................... 15 4.2 Direct Payments Relative to Farm Net Value Added Per Annual Work Unit . 16 4.3 Direct Payments Relative to Gross Margins.................................................. 16 4.4 General Conclusions ..................................................................................... 17

5. Production Structures on Holdings ........................................................................... 18

5.1 Overview ....................................................................................................... 18 5.2 Farm Size ...................................................................................................... 18 5.3 Farm Practices .............................................................................................. 20 5.4 Environmental Considerations ...................................................................... 24 5.5 Capital Inputs ................................................................................................ 24 5.6 Labour Inputs ................................................................................................ 25 5.7 General Conclusions ..................................................................................... 27

6. Adapting Supply to Demand — quantity and Quality................................................ 28

6.1 Overview ....................................................................................................... 28 6.2 Cereal Quantity ............................................................................................. 29 6.3 Cereal Quality................................................................................................ 29 6.4 On-Farm Feed — Barley and Wheat............................................................. 32 6.5 General Conclusions ..................................................................................... 32

7. Effects of the Drop in Institutional Prices .................................................................. 33

7.1 Overview ....................................................................................................... 33 7.2 Institutional Prices ......................................................................................... 33 7.3 Competitiveness on the Export Market.......................................................... 34

Contents (ii)

7.4 Competitiveness on the Domestic Market ..................................................... 34 7.5 General Conclusions ..................................................................................... 36

8. Effects Restricting Competition — UK...................................................................... 36

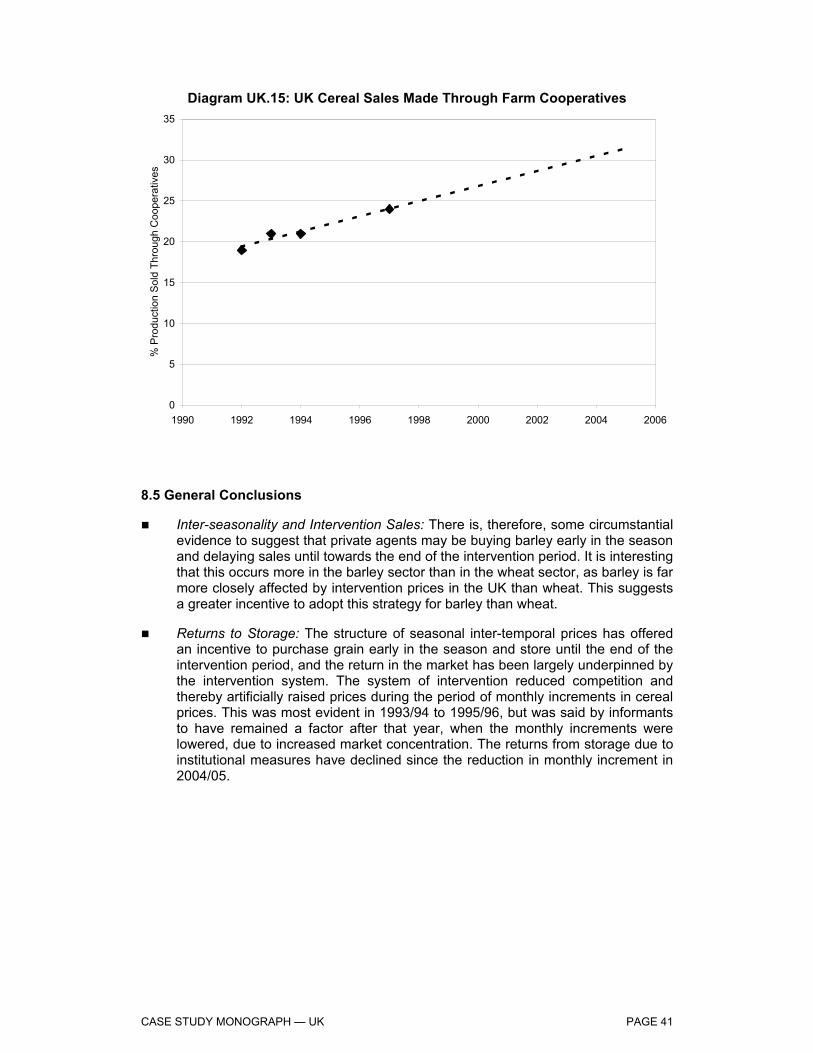

8.1 Overview ....................................................................................................... 36 8.2 Monthly Sales into Intervention ..................................................................... 37 8.3 Returns to Storage ........................................................................................ 38 8.4 Market Structure............................................................................................ 40 8.5 General Conclusions ..................................................................................... 41

Appendix to the Case Study Monograph — UK........................................................ I1

Part 1: Introduction to the Cereals Sector...................................................................... I2

Crop Production (Area & Yield), Consumption and Trade Balances — UK ......... I2 Crop Production (Area & Yield) — England ......................................................... I5 Agricultural Structure — Scotland ........................................................................ I6 Crop Production (Area & Yield) — Scotland......................................................... I7

Part 2.1: Producers’ Income level.................................................................................. I9

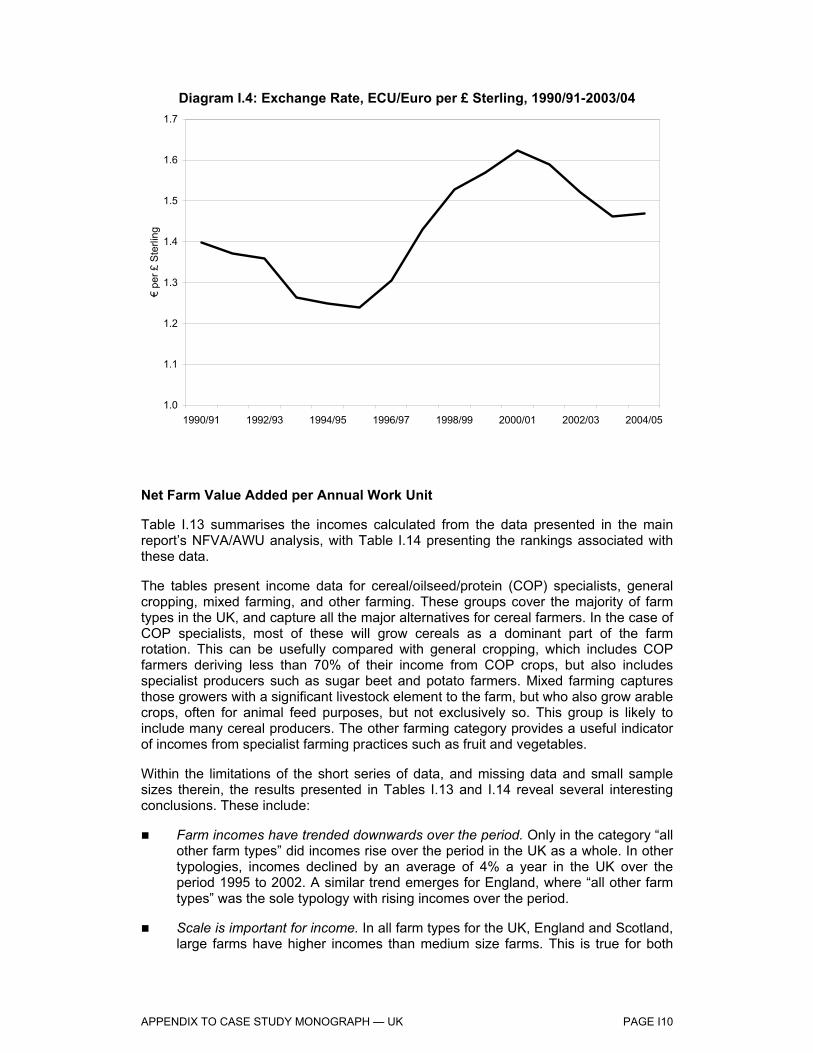

Prices, Exchange Rates ....................................................................................... I9 Net Farm Value Added per Annual Work Unit.................................................... I10 National Farm Income Sources.......................................................................... I14 Land Prices and Rents ....................................................................................... I19

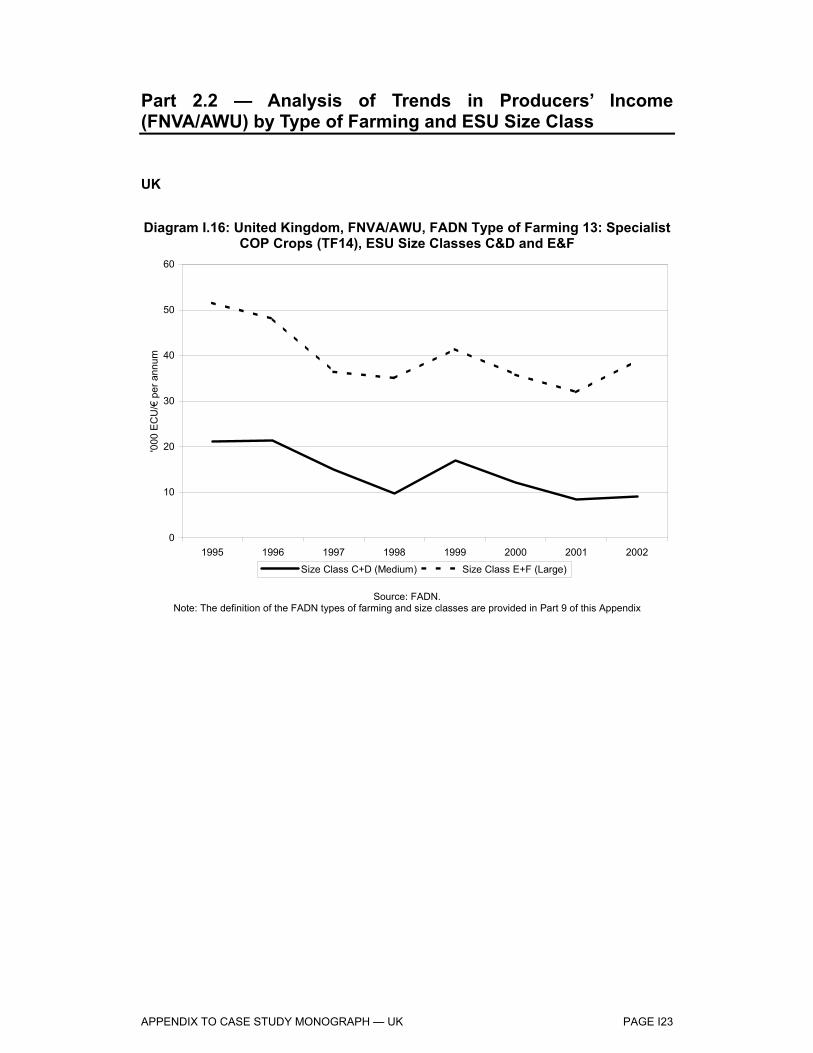

Part 2.2 — Analysis of Trends in Producers’ Income (FNVA/AWU) by Type of Farming and ESU Size Class ............................................................................. I23

UK ..................................................................................................................... I23 Scotland ............................................................................................................. I26 England .............................................................................................................. I27

Part 3: Dependence on Direct Payments .................................................................... I30

England Summary.............................................................................................. I30 Scotland Summary ............................................................................................. I32

Part 4: Production Structures on Holdings................................................................... I35

Farm Size ........................................................................................................... I35 Farm Practices ................................................................................................... I37 Chemical Plant Protection .................................................................................. I39 Environmental Considerations ........................................................................... I41 Capital Inputs ..................................................................................................... I44 Labour Inputs ..................................................................................................... I45

Part 5: Adapting Supply to Demand — Quantity and Quality ...................................... I46

Cereal Quantity .................................................................................................. I46 Wheat Quality..................................................................................................... I47 On-Farm Feed, Barley and Wheat ..................................................................... I48

Part 6: Effects of the Drop in Institutional Prices ......................................................... I51

Contents (iii)

Institutional Prices .............................................................................................. I51 Competitiveness on the Export Market .............................................................. I52 Competitiveness on the Domestic Market .......................................................... I53 Feed Usage........................................................................................................ I54

Part 7: Effects Restriction Competition ........................................................................ I57

Monthly Sales into Intervention .......................................................................... I57 Market Structure................................................................................................. I59

Part 8: Analysis of Questionnaire Submitted to Producers.......................................... I60

England .............................................................................................................. I61 Producers’ Income Levels .................................................................................. I61 Dependence on Direct Payments....................................................................... I61 Production Structures on Holdings..................................................................... I62 Adapting Supply to Demand: Quality and Quantity ............................................ I62 Land Use: Choice of Crop .................................................................................. I62 Effects of the Drop in Institutional Prices............................................................ I62 Effects Restricting Competition .......................................................................... I63 Scotland ............................................................................................................. I77 Background Information ..................................................................................... I77 Producers’ Income Levels .................................................................................. I77 Dependence on Direct Payments....................................................................... I77 Production Structures on Holdings..................................................................... I77 Adapting Supply to Demand: Quality and Quantity ............................................ I78 Land Use: Choice of Crop .................................................................................. I78 Effects of the Drop in Institutional Prices............................................................ I78 Effects Restricting Competition .......................................................................... I79

Part 9: Typology of Farms ........................................................................................... I96

Contents (iv)

List of Tables

Table UK.1: United Kingdom, Area Statistics, 2003 .................................................... 2 Table UK.2: United Kingdom, Employment Statistics, 2003........................................ 3 Table UK.3: Change in Number of Farm Holdings by Economic Size Unit

by Farm Type, 1992/93-2003/04 ........................................................... 19 Table UK.4: England/Eastern Counties, Impact on Fixed Costs of Contract

Farming, 2003/04 .................................................................................. 27 Table UK.5: Relationship of the Percentage Bread-making Wheat Premium with

Changes in Production of Feed Wheat and Bread-making Wheat, 1995/96-2003/04 ................................................................................... 31

Table I.1: UK, Production of Wheat, Barley and Oats, 1995/96-2003/04 ............... I2 Table I.2: UK, Wheat Supply Demand Balance, 1995/96-2003/04 ........................ I3 Table I.3: UK, Barley Supply Demand Balance, 1995/96-2003/04......................... I3 Table I.4: UK, Oats Supply Demand Balance, 1995/96-2003/04 ........................... I4 Table I.5: UK, Total Cereals Supply Demand Balance, 1995/96-2003/04 ............. I4 Table I.6: UK, Area and Yields for Wheat, Barley and Oats, 1995/96-2003/04...... I4 Table I.7: England, Production of Wheat and Barley, 1995/96-2003/04 ................ I5 Table I.8: England, Area of Wheat and Barley, 1995/96-2003/04 .......................... I5 Table I.9: England, Yields of Wheat and Barley, 1995/96-2003/04........................ I6 Table I.10: Scotland, Production of Barley and Oats, 1995/96-2003/04 .................. I7 Table I.11: Scotland, Area of Oats and Barley, 1995/96-2003/04 ............................ I7 Table I.12: Scotland, Yields of Oats and Barley, 1995/96-2003/04.......................... I8 Table I.13: Producer Incomes for UK, England and Scotland, 1995-2002............. I12 Table I.14: Rankings of Producer Incomes and Changes in Incomes for UK,

England and Scotland, 1995-2002 ....................................................... I13 Table I.15: UK, Non-Farming Incomes, All Farm Types, 2004............................... I18 Table I.16: England, Agricultural Land Sales, 1993-2003 ...................................... I19 Table I.17: UK, Calculation of Gross Margin for Winter Wheat, 2004/05 ............... I34 Table I.18: UK, Farm Practices Survey Results, 2004: “If you grow cereal

crops, do you limit the spraying of pesticides/fertilisers on headlands to encourage wildlife?” ........................................................ I43

Table I.19: Monthly Increments in Intervention Price, 1995/96-2004/05 ................ I57 Table I.20: Member State Agricultural Production Sold Through

Cooperatives, 1997 .............................................................................. I59 Table I.21: Number of Respondents in Each Farm Type ....................................... I61 Table I.22: Number of Respondents in Each Farm Type ....................................... I77 Table I.23. : Aggregation of FADN ESU Size Classes into New ESU Size

Classes................................................................................................. I96

Contents (v)

List of Diagrams

Diagram UK.1: UK Cereal Production, 1970/71-2003/04 ............................................ 4 Diagram UK.2: UK Area for Wheat, Barley and Oats, 1970/71-2003/04..................... 5 Diagram UK.3: UK Yields for Wheat, Barley and Oats, 1970/71-2003/04................... 5 Diagram UK.4: England, Cereal Production, 1995/96-2003/04................................... 7 Diagram UK.5: Scotland, Cereal Production, 1995/96-2003/04 .................................. 8 Diagram UK.6: Average Net Farm Incomes for Cereal Farms, 1994/95-2002/03..... 11 Diagram UK.7: Scotland, Comparison of Average Net Farm Income and Non-

Farming Incomes, 1998/99-2003/04 ................................................. 13 Diagram UK.8: Direct Payments as a Percentage of Gross Margins ........................ 17 Diagram UK.9: Arable Land Area Under Inversion and Minimum Tillage,

1997-2004......................................................................................... 21 Diagram UK.10: Fertiliser Application Rates for All Crops and Grassland,

1988-2002......................................................................................... 23 Diagram UK.11: UK Agricultural Labour Force, 1984-2004 ........................................ 25 Diagram UK.12: England/Eastern Counties, Real Expenditure on Contracting

by Farm Holdings, 1995/96-2003/04................................................. 26 Diagram UK.13: UK – Millers’ Wheat Usage by Source, 1984/85-2003/04................. 30 Diagram UK.14: UK, Monthly Increment in Intervention Price Compared

with Implied Monthly Market Rate of Interest for Feed Wheat ...................................................................................... 39

Diagram UK.15: UK Cereal Sales Made Through Farm Cooperatives ....................... 41

Diagram I.1: UK, Arable Crop Production, 1984/85-2003/04 ................................. I2 Diagram I.2: UK, Cereal Trade Balance, 1990/91-2003/04.................................... I3 Diagram I.3: UK, Cereal Prices, 1990/91-2004/05 ................................................. I9 Diagram I.4: Exchange Rate, ECU/Euro per £ Sterling, 1990/91-2003/04........... I10 Diagram I.5: Average Net Farm Incomes for Cereal Farms, 1994/95-2002/03.... I14 Diagram I.6: England, Average Net Farm Incomes for Cereal Specialists,

General Cropping and Mixed Farming, 1994/95-2002/03................ I16 Diagram I.7: Scotland, Average Net Farm Incomes for Cereal Specialists,

General Cropping and Mixed Farming, 1994/95-2002/03................ I16 Diagram I.8: Distribution of Net Farm Incomes, 2001/02 ..................................... I17 Diagram I.9: England/Eastern Counties, Real Net Farm Incomes per

Hectare by Farm Type, 1993/94-2003/04 ........................................ I17 Diagram I.10: Scotland, Non-Farming Incomes per Farm Household,

1998/99-2003/04.............................................................................. I18 Diagram I.11: England, Real and Nominal Agricultural Land Prices, 1990-2003 ... I19 Diagram I.12: Scotland, Value of Assets per Hectare (Land and Buildings),

1993/94-2003/04.............................................................................. I20 Diagram I.13: England, Agricultural Land Prices by Size of Land Area Sold,

1993-2003I........................................................................................ 21 Diagram I.14: England, Agricultural Land Sales by Size of Land Area Sold,

1993-2003........................................................................................ I21 Diagram I.15: England & Scotland, Rent of Cereal Specialist Agricultural

Land, 1993/94-2003/04.................................................................... I22 Diagram I.16: United Kingdom, FNVA/AWU, FADN Type of Farming 13:

Specialist COP Crops (TF14), ESU Size Classes C&D and E&F.... I23 Diagram I.17: United Kingdom, FNVA/AWU, FADN Type of Farming 14:

General Field Cropping (TF14), ESU Size Classes C&D and E&F . I24 Diagram I.18: United Kingdom, FNVA/AWU, FADN Type of Farming 8:

Mixed Crops – Livestock (TF8), ESU Size Classes C&D and E&F . I24

Contents (vi)

Diagram I.19: United Kingdom, FNVA/AWU, All FADN Types of Farming, Size Class C&D (Medium) ....................................................................... I25

Diagram I.20: United Kingdom, FNVA/AWU, All FADN Types of Farming, ESU Size Class E&F (Large) ........................................................... I25

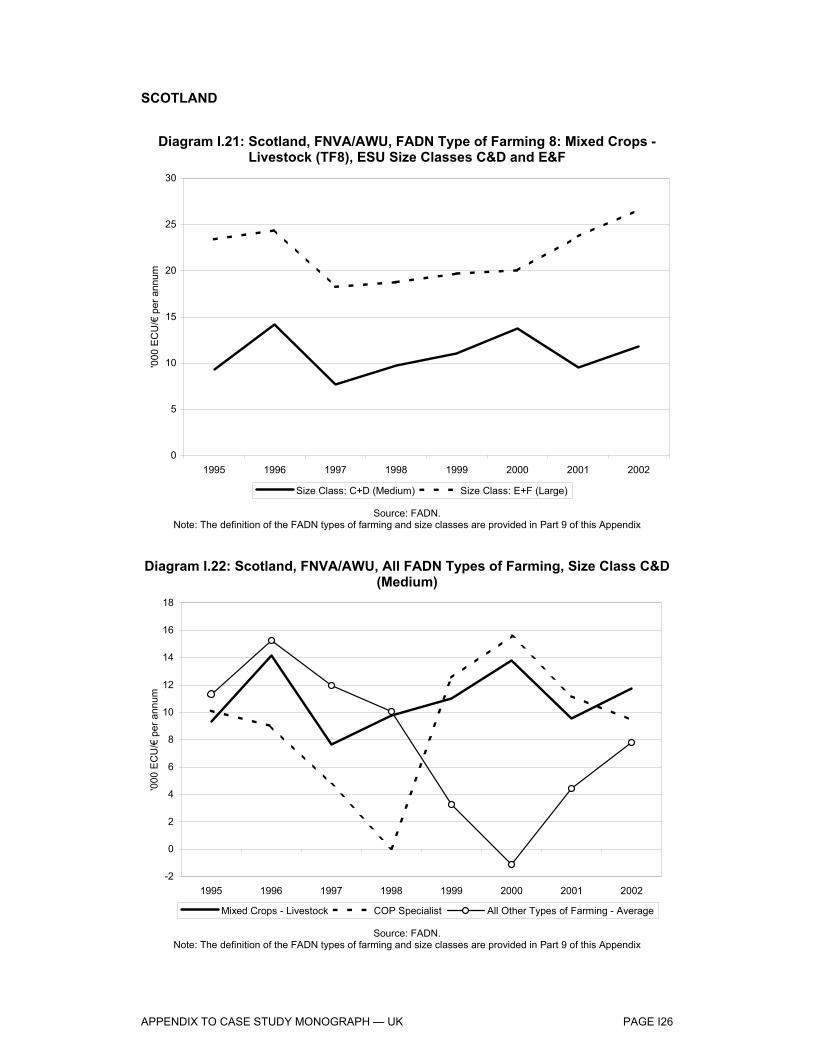

Diagram I.21: Scotland, FNVA/AWU, FADN Type of Farming 8: Mixed Crops – Livestock (TF8), ESU Size Classes C&D and E&F............................................................. I26

Diagram I.22: Scotland, FNVA/AWU, All FADN Types of Farming Size Class C&D (Medium) ............................................................... I26

Diagram I.23: Scotland, FNVA/AWU, All FADN Types of Farming Size Class E&F (Large) ................................................................... I27

Diagram I.24: England, FNVA/AWU, FADN Type of Farming 13: Specialist COP Crops (TF14), ESU Size Classes C&D and E&F .................... I27

Diagram I.25: England, FNVA/AWU, FADN Type of Farming 14: General Field Cropping (TF14), ESU Size Classes C&D and E&F .................................................................................. I28

Diagram I.26: England, FNVA/AWU, FADN Type of Farming 8: Mixed Crops – Livestock (TF8), ESU Size Classes C&D and E&F .................................................................................. I28

Diagram I.27: England, FNVA/AWU, FADN Type of Farming, Size Class C&D (Medium) ....................................................................... I29

Diagram I.28: England, FNVA/AWU, FADN Type of Farming, Size Class E&F (Large) ........................................................................... I29

Diagram I.29: England, The Proportions of FNVA/AWU Accounted for by Area and Set-Aside Payments by Farm Type, 1995-97 and 2000-02...... I31

Diagram I.30: England, Comparison of the Value of Area and Set-Aside Payments per AWU by Farm Typology, 1995-97 and 2000-02 ....... I31

Diagram I.31: Scotland, The Proportions of FNVA/AWU Accounted for by Area and Set-Aside Payments by Farm Type, 1995-97 and 2000-02...... I33

Diagram I.32: Scotland, Comparison of the Value of Area and Set-Aside Payments per AWU by Farm Typology, 1995-97 and 2000-02 ....... I33

Diagram I.33: UK, Number of Farm Holdings, 1992/93-2003/04............................ I35 Diagram I.34: UK, Number of Cereal Specialist Farm Holdings by Economic

Size Unit, 1992/93-2003/04 ............................................................. I36 Diagram I.35: Scotland, Average Farm Size, 1993/94-2003/04 ............................. I36 Diagram I.36: Scotland, Value of Seed per Hectare, 1993/94-2003/04 ................. I37 Diagram I.37: Scotland, Value of Fertiliser per Hectare, 1993/94-2003/04 ............ I37 Diagram I.38: UK, Organically Managed Land, 1993 –2003 .................................. I38 Diagram I.39: UK, Organically Managed Land by Sector, 2003............................. I39 Diagram I.40: Pesticide Use on Winter Wheat in Great Britain, 1992-2002 ........... I40 Diagram I.41: UK, Area in Environmentally Sensitive Areas and Countryside

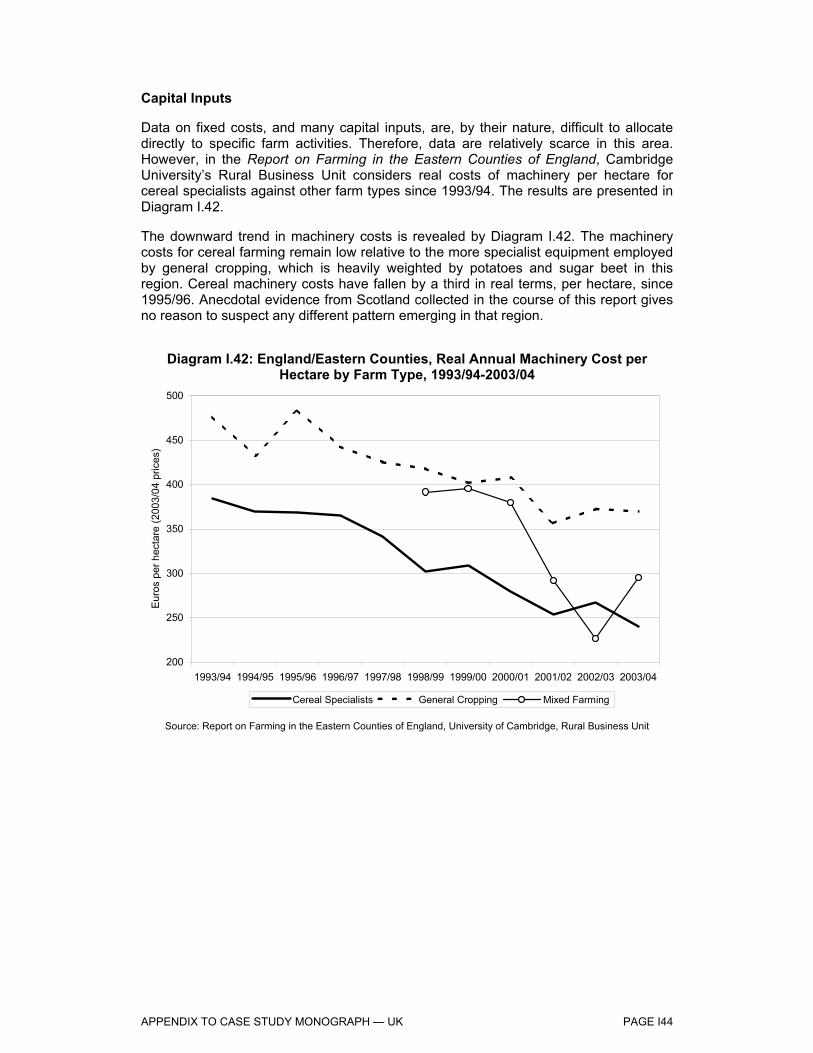

Stewardship Schemes, 1987-2002.................................................. I42 Diagram I.42: England/Eastern Counties, Real Annual Machinery Cost

per Hectare by Farm Type, 1993/94-2003/04.................................. I44 Diagram I.43: England/Eastern Counties, Real Labour Cost per Hectare

by Farm Type, 1993/94-2003/04...................................................... I45 Diagram I.44: Scotland, Real Labour Cost per Hectare by Farm Type,

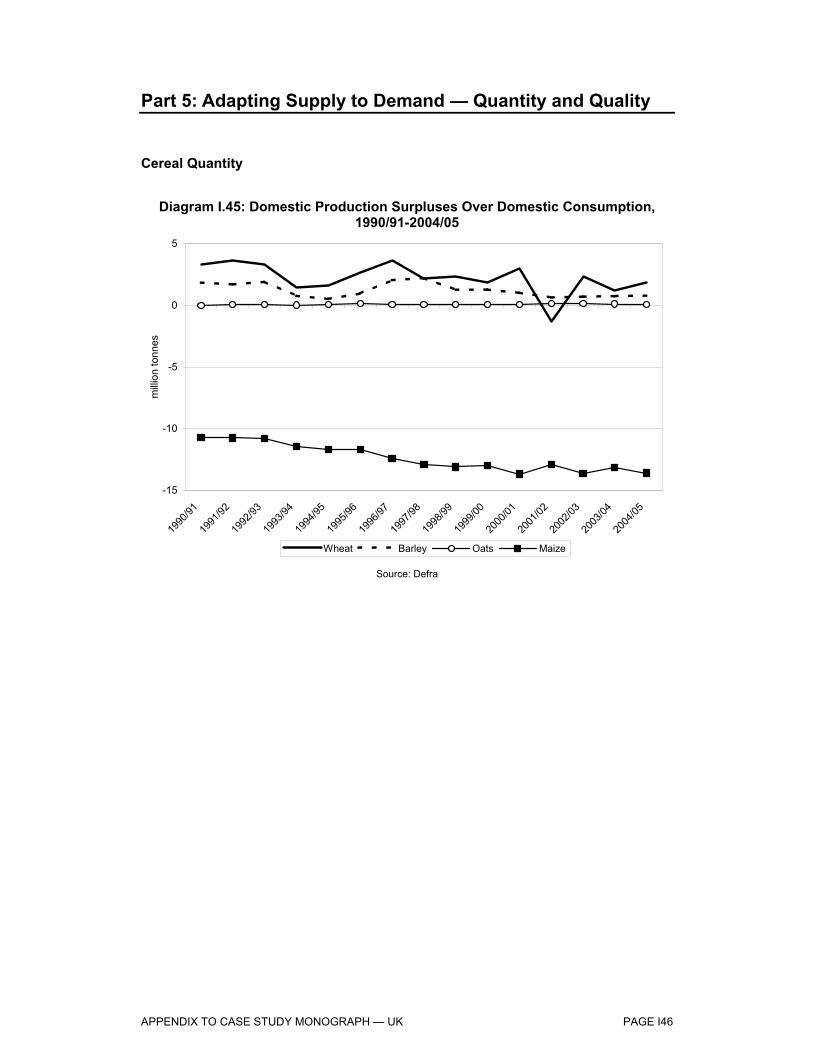

1993/94-2003/04 ............................................................................. I45 Diagram I.45: Domestic Production Surpluses Over Domestic Consumption,

1990/91-2004/05.............................................................................. I46 Diagram I.46: UK, End-of-Year Cereal Stocks, 1990/91-2004/05 .......................... I47 Diagram I.47: UK, Wheat Production by Quality Group, 1995/96-2004/05 ............ I48 Diagram I.48: UK, Compound Feed Production and Feed Wheat / Barley

Prices, 1992/93-2003/04.................................................................. I50

Contents (vii)

Diagram I.49: On-Farm Cereal Consumption as Percentage of Cereal Sales to Compound Feed Mills, 1995/96-2002/03........................... I50

Diagram: I.50: UK, Intervention Prices, 1990/91-2003/04 ....................................... I51 Diagram I.51: UK, Total Cereal Exports, 1990-2004 .............................................. I52 Diagram I.52: EU, Average Export Refunds, 1996/97-2003/04.............................. I52 Diagram I.53: UK, Intervention Year-End Stocks, 1995/96-2003/04 ...................... I53 Diagram I.54: UK, Total Cereal Imports, 1990-2004 .............................................. I53 Diagram I.55: UK, Horse Feed Consumption, 1992-2004...................................... I54 Diagram I.56: UK, Total Cereal and Oilseed Meal Usage in Compound

Animal Feed, 1992/93-2003/04........................................................ I55 Diagram I.57: UK, Maize Gluten Feed and Citrus Pulp Usage in Compound

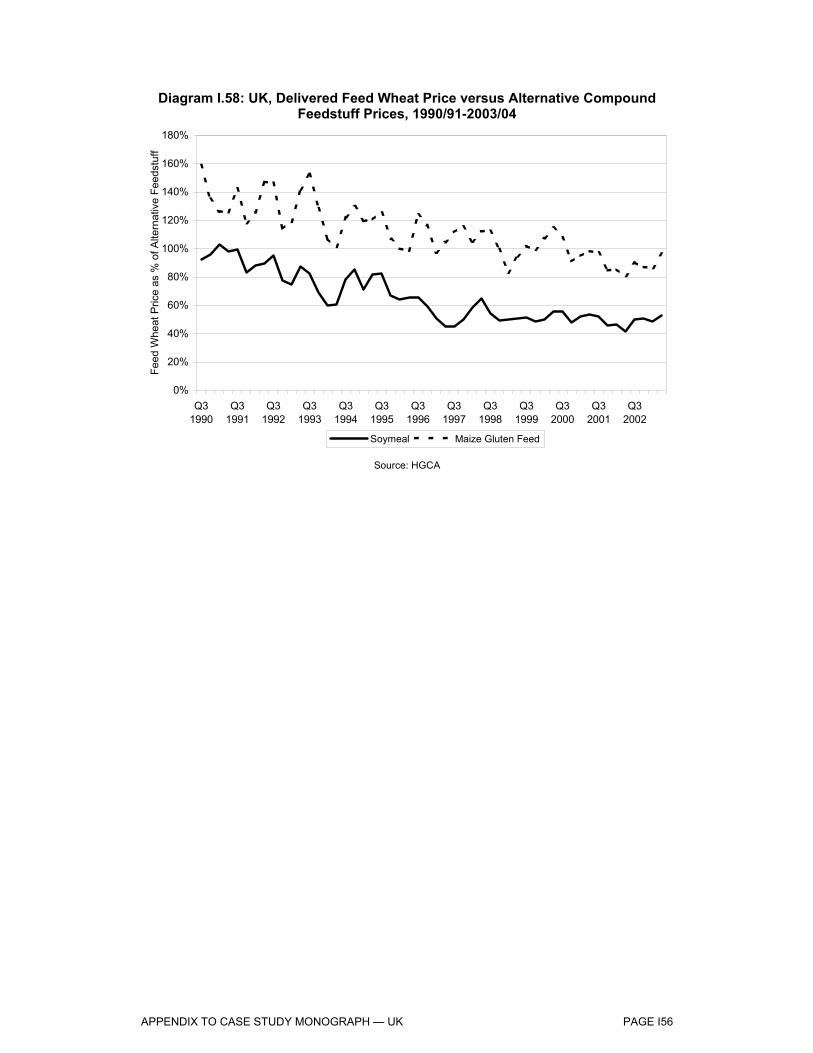

Animal Feed, 1992/93-2003/04........................................................ I55 Diagram I.58: UK, Delivered Feed Wheat Price versus Alternative Compound

Feedstuff Prices, 1990/91-2003/04.................................................. I56 Diagram I.59: UK, Average Total Monthly Cereal Sales into Intervention,

1997/98-2003/041............................................................................ I57 Diagram I.60: UK, Average Monthly Feed Barley Sales Off-Farm,

1997/98-2003/04.............................................................................. I58 Diagram I.61: UK, Average Monthly Feed Wheat Sales Off-Farm ......................... I58 Diagram I.62: Percentage of Farm Household Income Derived from

Farm Activities ................................................................................. I64 Diagram I.63: Percentage of Farm Income Derived from 1st Cereal

Production — Wheat........................................................................ I64 Diagram I.64: Percentage of Farm Income Derived from Total Cereal

Production 10 Years Ago................................................................. I64 Diagram I.65: Percentage of Farm Income Derived from Total

Cereal Production. ........................................................................... I64 Diagram I.66: Percentage of Farm Income Derived from 2nd Cereal

Production — Rapeseed.................................................................. I64 Diagram I.67: Percentage of Farm Income Derived from 1st Cereal

Production 10 Years Ago — Wheat ................................................. I64 Diagram I.68: Percentage of Farm Income Derived from 2nd Cereal

Production 10 Years Ago — Rapeseed ........................................... I65 Diagram I.69: Change in Asset Value of Farmland Over the Past 10 Years.......... I65 Diagram I.70: Reduction of Involvement in Farming, Without Direct Payments..... I65 Diagram I.71: Change in Rental Value of Farmland Over the Past 10 Years ........ I65 Diagram I.72: Farm Income From Direct Payments ............................................... I65 Diagram I.73: Changes in the Dependence on Direct Payments Over the

Past 10 Years .................................................................................. I65 Diagram I.74: Changes in Cereal Area Since 1995................................................ I66 Diagram I.75: Changes in the Amount and Type of Capital Investment in

Machinery Since 1995 ..................................................................... I66 Diagram I.76: Changes in the Amount and Type of Seed Use for

Cereal Production on Farms Since 1995 ......................................... I66 Diagram I.77: Influence of Price Support on Cereal Farming Practices

Since 1995....................................................................................... I66 Diagram I.78: Changes in the Use of Labour per Hectare in Cereal

Production Since 1995..................................................................... I66 Diagram I.79: Changes in the Amount and Type of Fertiliser Use for Cereal

Production on Farms Since 1995..................................................... I66 Diagram I.80: Changes in the Amount and Type of Irrigation Use for Cereal

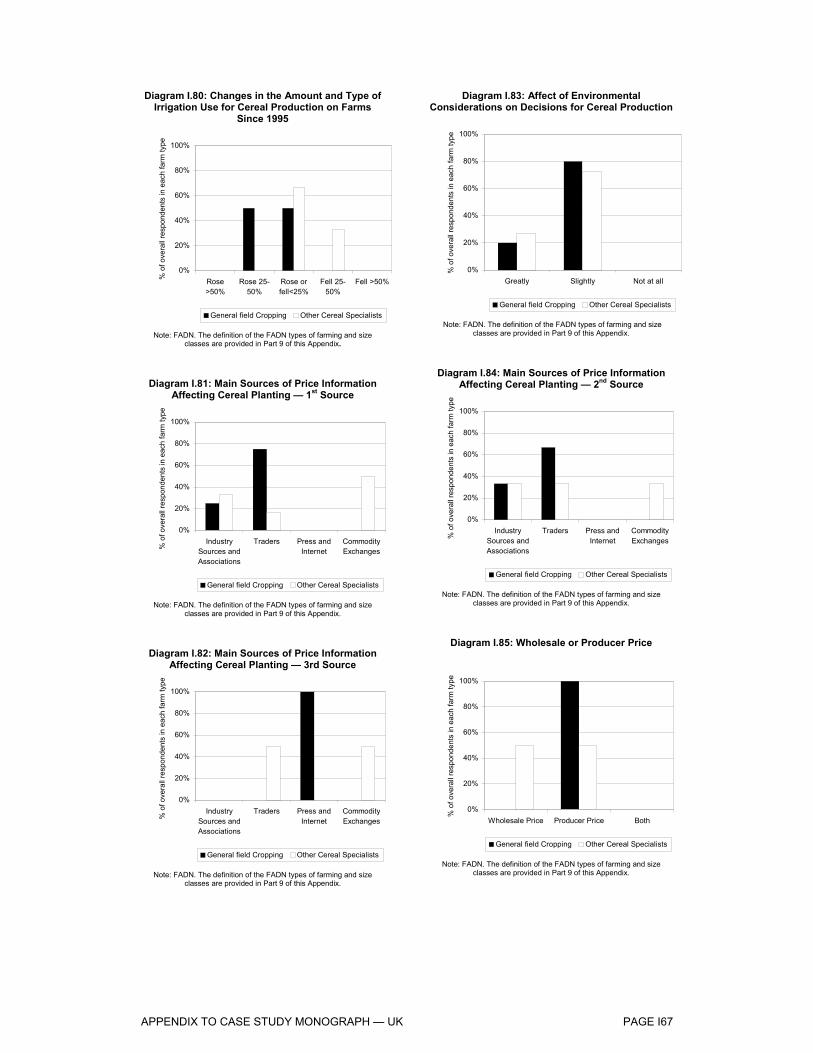

Production on Farms Since 1995..................................................... I67 Diagram I.81: Main Sources of Price Information Affecting Cereal

Planting — 1st Source ..................................................................... I67 Diagram I.82: Main Sources of Price Information 3rd Source ................................ I67

Contents (viii)

Diagram I.83: Affect of Environmental Considerations on Decisions for Cereal Production........................................................................................ I67

Diagram I.84: Main Sources of Price Information Affecting Cereal Planting — 2nd Source.................................................................... I67

Diagram I.85: Wholesale or Producer Price ........................................................... I67 Diagram I.86: Other Crops Affected by Expansions/Contractions in Cereal

Area — 1st Crop .............................................................................. I68 Diagram I.87: Effect of direct payments on cereal planting decisions — 1st Crop. I68 Diagram I.88: Influence of Quality Price Premium on Cereal Quality..................... I68 Diagram I.89: Other Crops Affected by Expansions/Contractions in Cereal

Area — 2nd Crop ............................................................................. I68 Diagram I.90: Influence of the Rules on Set Aside Since 1992 on Cereal

Planting Decisions ........................................................................... I68 Diagram I.91: Influence of Quality Needs of Customers on Cereal Quality............ I68 Diagram I.92: Change in Cereal Quality Since 1995 — 1st Cereal — Wheat........ I69 Diagram I.93: Change in the Volume of Feed Produced On-Farm, since 1995 ..... I69 Diagram I.94: Sequence of Crops Over the Rotational Cycle — Crop 2................ I69 Diagram I.95: Effects of Changed Minimum Quality Standards for Cereals

Sold to Intervention on Cereal Production ....................................... I69 Diagram I.96: Influence of the New Cereals Regime on the Volume of Feed

Produced On-Farm .......................................................................... I69 Diagram I.97: Sequence of Crops Over the Rotational Cycle — Crop 3................ I69 Diagram I.98: Sequence of Crops Over the Rotational Cycle — Crop 4................ I70 Diagram I.99: Main Sources of Price Information Affecting Cereal

Planting — 2nd Source.................................................................... I70 Diagram I.100: Change in the Relative Profitability of Cereals Since 1995

Against the Main Alternative Crops.................................................. I70 Diagram I.101: Main Sources of Price Information Affecting Cereal

Planting — 1st Source ..................................................................... I70 Diagram I.102: Main Sources of Price Information Affecting Cereal

Planting — 3rd Source..................................................................... I70 Diagram I.103: Change in the Relative Profitability of Cereals Since 1995

Against Voluntary Set Aside ............................................................ I70 Diagram I.104: Crop Affected by Changes in the Cereal Area 1.............................. I71 Diagram I.105: Crop Affected by Changes in the Cereal Area 3.............................. I71 Diagram I.106: Influence of the Rules on Set Aside on Cereal Planting Decisions.. I71 Diagram I.107: Crop Affected by Changes in the Cereal Area 2.............................. I71 Diagram I.108: Influence of the Introduction of Direct Payments on Cereal

Planting Decisions ........................................................................... I71 Diagram I.109: Extent of Agronomic Constraints on the Optimal Planting Decision I71 Diagram I.110: Extent of Environmental Constraints on the Optimal

Planting Decision ............................................................................. I72 Diagram I.111: Changes Labour Use per Hectare in Cereal Production

Since 1995....................................................................................... I72 Diagram I.112: Changes in the Amount and Type of Fertiliser Use Since 1995 ...... I72 Diagram I.113: Changes in the Amount and Type of Capital Investment In

Machinery Since 1995 ..................................................................... I72 Diagram I.114: Changes in the Amount and Type of Seed Use Since 1995............ I72 Diagram I.115: Changes in the Amount and Type of Irrigation Use Since 1995 ...... I72 Diagram I.116: Influence of the Cereal Regime Since 1995 .................................... I73 Diagram I.117: Effect of the Intervention Prices on the Area Planted to

Cereals — Cereal 1 — Wheat ......................................................... I73 Diagram I.118: Effect of the Intervention Prices on the Area Planted to

Cereals — Cereal 3 — Rapeseed ................................................... I73

Contents (ix)

Diagram I.119: Influence of Environmental Consideration on Decisions for Cereal Production ............................................................................ I73

Diagram I.120: Effect of the Intervention Prices on the Area Planted to Cereals — Cereal 2 — Barley.......................................................... I73

Diagram I.121: Change in On-Farm Feed Practice, in Relation to Purchases of Feed Off-Farm, since 1995.......................................................... I73

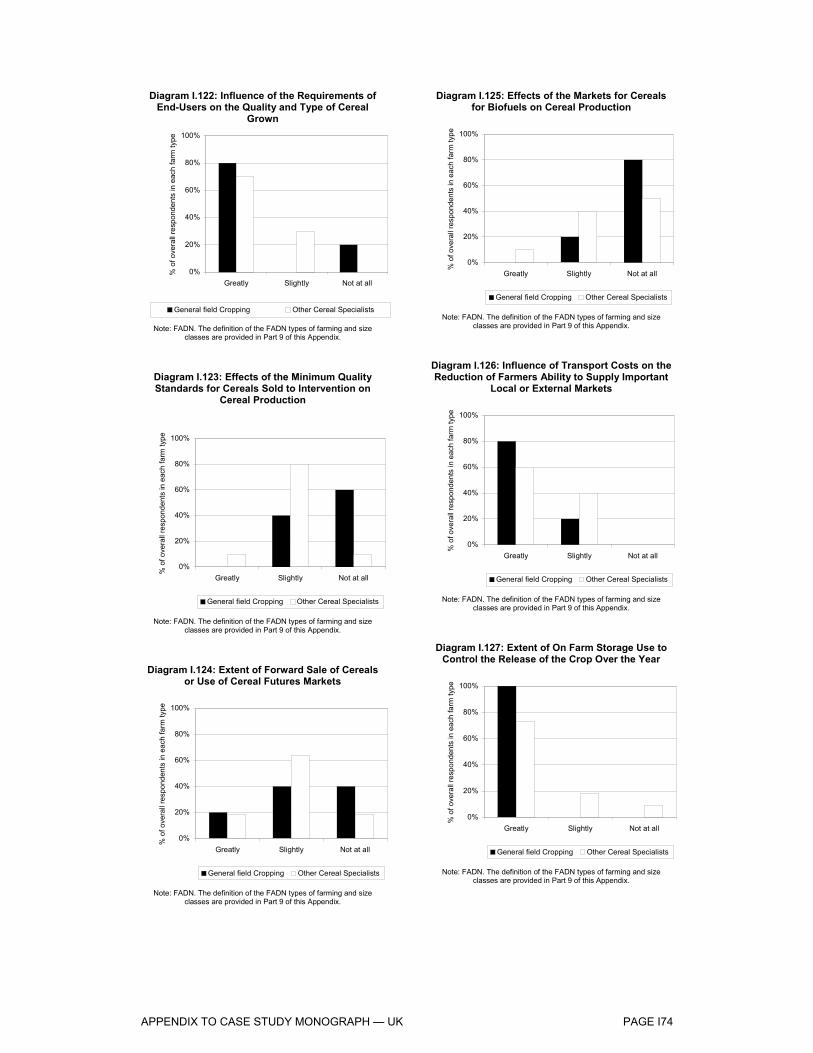

Diagram I.122: Influence of the Requirements of End-Users on the Quality and Type of Cereal Grown............................................................... I74

Diagram I.123: Effects of the Minimum Quality Standards for Cereals Sold to Intervention on Cereal Production ................................................... I74

Diagram I.124: Extent of Forward Sale of Cereals or Use of Cereal Futures Markets ............................................................................................ I74

Diagram I.125: Effects of the Markets for Cereals for Biofuels on Cereal Production ............................................................................ I74

Diagram I.126: Influence of Transport Costs on the Reduction of Farmers Ability to Supply Important Local or External Markets ..................... I74

Diagram I.127: Extent of On Farm Storage Use to Control the Release of the Crop Over the Year.......................................................................... I74

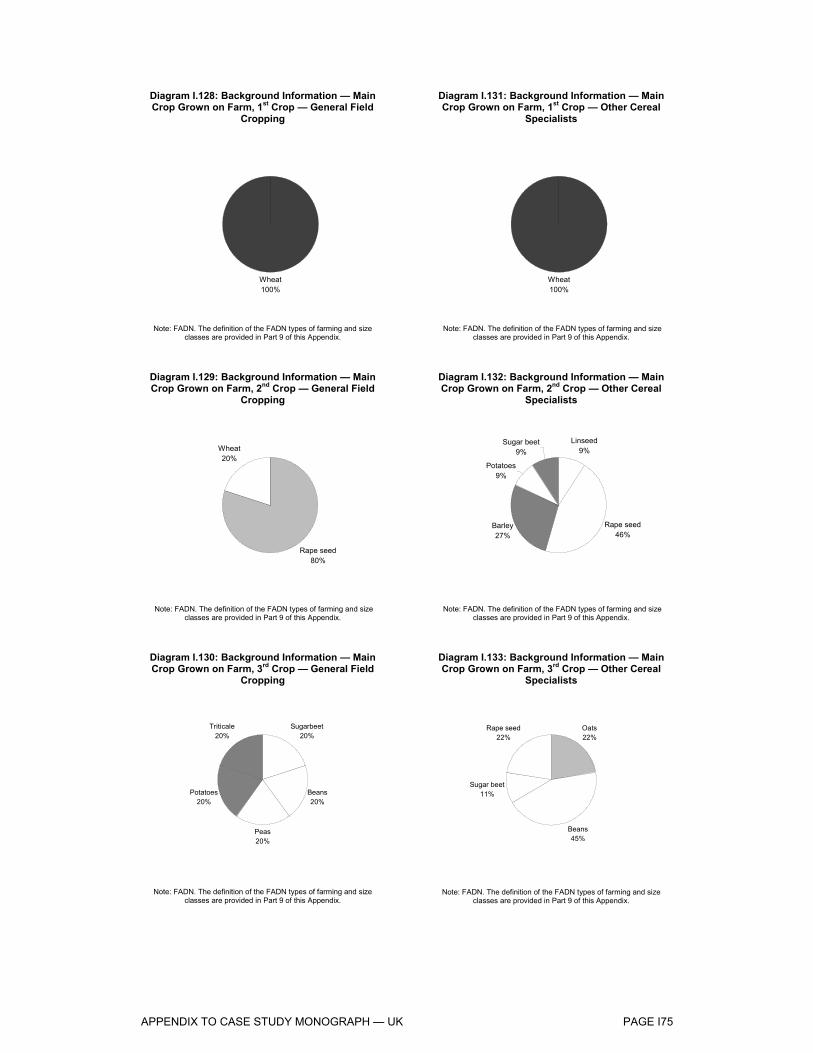

Diagram I.128: Background Information — Main Crop Grown on Farm, 1st Crop — General Field Cropping................................................. I75

Diagram I.129: Background Information — Main Crop Grown on Farm, 2nd Crop — General Field Cropping ............................................... I75

Diagram I.130: Background Information — Main Crop Grown on Farm, 3rd Crop — General Field Cropping ................................................ I75

Diagram I.131: Background Information — Main Crop Grown on Farm, 1st Crop — Other Cereal Specialists ............................................... I75

Diagram I.132: Background Information — Main Crop Grown on Farm, 2nd Crop — Other Cereal Specialists.............................................. I75

Diagram I.133: Background Information — Main Crop Grown on Farm, 3rd Crop — Other Cereal Specialists............................................... I75

Diagram I.134: Background Information — Main Crop Grown on Farm, 4th Crop — General Field Cropping ................................................ I76

Diagram I.135: Background Information — Main Crop Grown on Farm, 5th Crop — General Field Cropping ................................................ I76

Diagram I.136: Background Information — Main Crop Grown on Farm, 4th Crop — Other Cereal Specialists............................................... I76

Diagram I.137: Background Information — Main Crop Grown on Farm, 5th Crop — Other Cereal Specialists............................................... I76

Diagram I.138: Percentage of Farm Household Income Derived from Farm Activities ................................................................................. I80

Diagram I.139: Percentage of Farm Income Derived from 1st Cereal Production — Wheat........................................................................ I80

Diagram I.140: Percentage of Farm Income Derived from 2nd Cereal Production — Barley ........................................................................ I80

Diagram I.141: Percentage of Farm Income Derived from Total Cereal Production I80 Diagram I.142: Percentage of Farm Income Derived from 1st Cereal

Production — Barley ........................................................................ I80 Diagram I.143: Percentage of Farm Income Derived from 2nd Cereal

Production — Wheat........................................................................ I80 Diagram I.144: Percentage of Farm Income Derived from Total Cereal

Production 10 Years Ago................................................................. I81 Diagram I.145: Percentage of Farm Income Derived from 1st Cereal

Production 10 Years Ago — Barley ................................................. I81 Diagram I.146: Percentage of Farm Income Derived from 2nd Cereal

Production 10 Years Ago — Wheat ................................................. I81

Contents (x)

Diagram I.147: Percentage of Farm Income Derived from 1st Cereal Production 10 Years Ago — Wheat ................................................. I81

Diagram I.148: Percentage of Farm Income Derived from 2nd Cereal Production 10 Years Ago — Barley ................................................. I81

Diagram I.149: Change in Rental Value of Farmland Over the Past 10 Years. ....... I81 Diagram I.150: Change in Asset Value of Farmland Over the Past 10 Years.......... I82 Diagram I.151: Reduction of Involvement in Farming, Without Direct Payments..... I82 Diagram I.152: Changes in Cereal Area Since 1995................................................ I82 Diagram I.153: Farm Income From Direct Payments ............................................... I82 Diagram I.154: Changes in the Dependence on Direct Payments Over the

Past 10 Years .................................................................................. I82 Diagram I.155 Influence of Price Support on Cereal Farming Practices

Since 1995....................................................................................... I82 Diagram I.156: Changes in the Amount and Type of Capital Investment in

Machinery Since 1995 ..................................................................... I83 Diagram I.157: Changes in the Amount and Type of Seed Use for Cereal

Production on Farms Since 1995..................................................... I83 Diagram I.158: Changes in the Amount and Type of Irrigation Use for Cereal

Production on Farms Since 1995..................................................... I83 Diagram I.159: Changes in the Use of Labour per Hectare in Cereal

Production Since 1995..................................................................... I83 Diagram I.160: Changes in the Amount and Type of Fertiliser Use for Cereal

Production on Farms Since 1995..................................................... I83 Diagram I.161: Affect of Environmental Considerations on Decisions for Cereal

Production........................................................................................ I83 Diagram I.162: Main Sources of Price Information Affecting Cereal

Planting — 1st Source ..................................................................... I84 Diagram I.163: Main Sources of Price Information Affecting Cereal

Planting — 3rd Source..................................................................... I84 Diagram I.164: Other Crops Affected by Expansions/Contractions in Cereal

Area — 1st Crop .............................................................................. I84 Diagram I.165: Main Sources of Price Information Affecting Cereal

Planting — 2nd Source.................................................................... I84 Diagram I.166: Wholesale or Producer Price ........................................................... I84 Diagram I.167: Effect of Direct Payments on Cereal Planting

Decisions — 1st Crop ...................................................................... I84 Diagram I.168: Other Crops Affected by Expansions/Contractions in Cereal

Area — 2nd Crop ............................................................................. I85 Diagram I.169: Influence of the Rules on Set Aside Since 1992 on Cereal

Planting Decisions ........................................................................... I85 Diagram I.170: Change in Cereal Quality Since 1995 — 1st Cereal — Wheat........ I85 Diagram I.171: Influence of Quality Price Premium on Cereal Quality..................... I85 Diagram I.172: Influence of Quality Needs of Customers on Cereal Quality............ I85 Diagram I.173: Change in Cereal Quality Since 1995 — 1st Cereal — Barley ........ I85 Diagram I.174: Change in Cereal Quality Since 1995 — 2nd Cereal — Barley....... I86 Diagram I.175: Effects of Changed Minimum Quality Standards for Cereals

Sold to Intervention on Cereal Production ....................................... I86 Diagram I.176: Influence of the New Cereals Regime on the Volume of Feed

Produced On-Farm .......................................................................... I86 Diagram I.177: Change in Cereal Quality Since 1995 — 2nd Cereal — Wheat....... I86 Diagram I.178: Change in the Volume of Feed Produced On-Farm, since 1995 ..... I86 Diagram I.179: Sequence of Crops Over the Rotational Cycle — Crop 1................ I86 Diagram I.180: Sequence of Crops Over the Rotational Cycle — Crop 2................ I87 Diagram I.181: Sequence of Crops Over the Rotational Cycle — Crop 4................ I87

Contents (xi)

Diagram I.182: Main Sources of Price Information Affecting Cereal Planting — 2nd Source.................................................................... I87

Diagram I.183: Sequence of Crops Over the Rotational Cycle — Crop 3 Note: FADN. The definition of the FADN types of farming and size classes are provided in Part 9 of this Appendix........................ I87

Diagram I.184: Main Sources of Price Information Affecting Cereal Planting — 1st Source ..................................................................... I87

Diagram I.185: Main Sources of Price Information Affecting Cereal Planting — 3rd Source..................................................................... I87

Diagram I.186: Wholesale or Producer Price ........................................................... I88 Diagram I.187: Change in the Relative Profitability of Cereals Since 1995

Against Voluntary Set Aside ............................................................ I88 Diagram I.188: Crop Affected by Changes in the Cereal Area 2.............................. I88 Diagram I.189: Change in the Relative Profitability of Cereals Since 1995

Against the Main Alternative Crops.................................................. I88 Diagram I.190: Crop Affected by Changes in the Cereal Area 1.............................. I88 Diagram I.191: Crop Affected by Changes in the Cereal Area 3.............................. I88 Diagram I.192: Influence of the Introduction of Direct Payments on Cereal

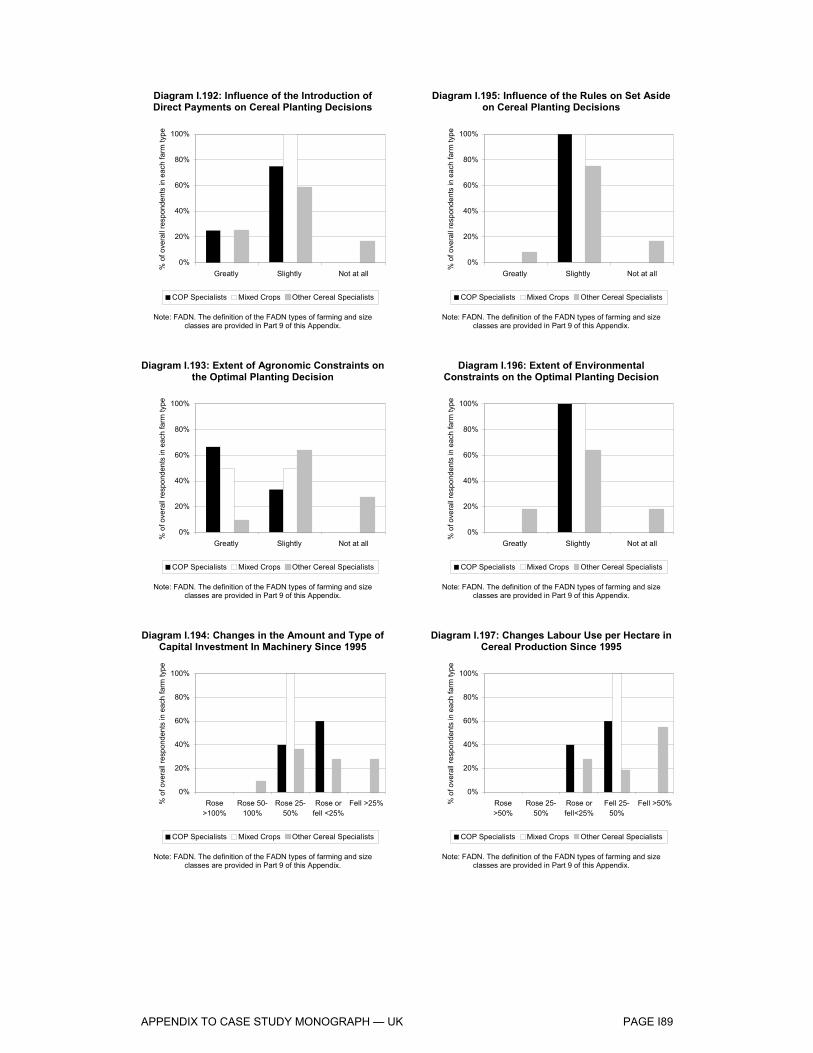

Planting Decisions ........................................................................... I89 Diagram I.193: Extent of Agronomic Constraints on the Optimal Planting Decision I89 Diagram I.194: Changes in the Amount and Type of Capital Investment In

Machinery Since 1995 ..................................................................... I89 Diagram I.195: Influence of the Rules on Set Aside on Cereal Planting Decisions.. I89 Diagram I.196: Extent of Environmental Constraints on the Optimal

Planting Decision ............................................................................. I89 Diagram I.197: Changes Labour Use per Hectare in Cereal Production

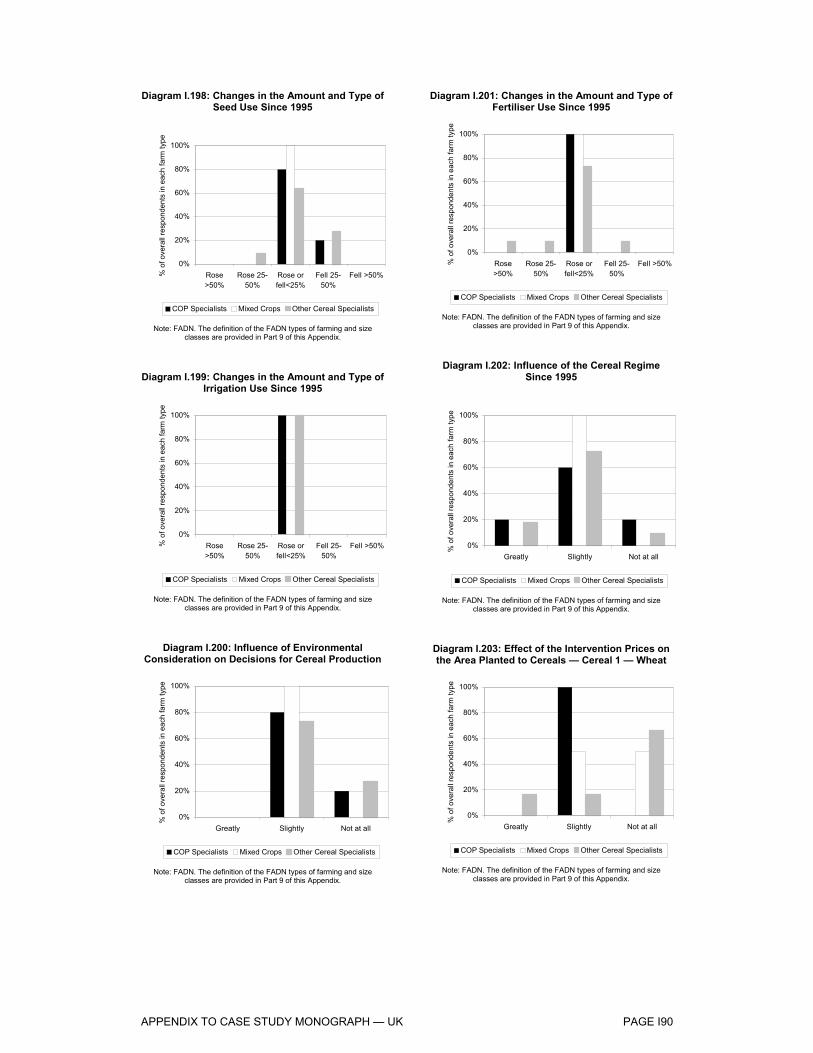

Since 1995....................................................................................... I89 Diagram I.198: Changes in the Amount and Type of Seed Use Since 1995............ I90 Diagram I.199: Changes in the Amount and Type of Irrigation Use Since 1995 ...... I90 Diagram I.200: Influence of Environmental Consideration on Decisions for

Cereal Production ............................................................................ I90 Diagram I.201: Changes in the Amount and Type of Fertiliser Use Since 1995 ...... I90 Diagram I.202: Influence of the Cereal Regime Since 1995 .................................... I90 Diagram I.203: Effect of the Intervention Prices on the Area Planted to

Cereals — Cereal 1 — Wheat ......................................................... I90 Diagram I.204: Effect of the Intervention Prices on the Area Planted to

Cereals — Cereal 1 — Barley.......................................................... I91 Diagram I.205: Effect of the Intervention Prices on the Area Planted to

Cereals — Cereal 2 — Wheat ......................................................... I91 Diagram I.206: Effect of the Intervention Prices on the Area Planted to

Cereals — Cereal 3 — Oats ............................................................ I91 Diagram I.207: Effect of the Intervention Prices on the Area Planted to

Cereals — Cereal 2 — Barley.......................................................... I91 Diagram I.208: Effect of the Intervention Prices on the Area Planted to

Cereals — Cereal 3 — Rapeseed ................................................... I91 Diagram I.209: Change in On-Farm Feed Practice, in Relation to Purchases

of Feed Off-Farm, since 1995.......................................................... I91 Diagram I.210: Influence of the Requirements of End-Users on the Quality

and Type of Cereal Grown............................................................... I92 Diagram I.211: Effects of the Minimum Quality Standards for Cereals Sold to

Intervention on Cereal Production ................................................... I92 Diagram I.212: Extent of Forward Sale of Cereals or Use of Cereal Futures

Markets ............................................................................................ I92 Diagram I.213: Effects of the Markets for Cereals for Biofuels on Cereal

Production........................................................................................ I92

Contents (xii)

Diagram I.214: Influence of Transport Costs on the Reduction of Farmers Ability to Supply Important Local or External Markets ..................... I92

Diagram I.215: Extent of On Farm Storage Use to Control the Release of the Crop Over the Year.................................................................... I92

Diagram I.216: Background Information — Main Crop Grown on Farm, 1st Crop — COP Specialists............................................................ I93

Diagram I.217: Background Information — Main Crop Grown on Farm, 2nd Crop — COP Specialists........................................................... I93

Diagram I.218: Background Information — Main Crop Grown on Farm, 2nd Crop — Other Cereal Specialists.............................................. I93

Diagram I.219: Background Information — Main Crop Grown on Farm, 1st Crop — Other Cereal Specialists ............................................... I93

Diagram I.220: Background Information — Main Crop Grown on Farm, 2nd Crop — Mixed Crops Livestock ................................................ I93

Diagram I.221: Background Information — Main Crop Grown on Farm, 3rd Crop — COP Specialists ........................................................... I93

Diagram I.222: Background Information — Main Crop Grown on Farm, 3rd Crop — Mixed Crops Livestock ................................................. I94

Diagram I.223: Background Information — Main Crop Grown on Farm, 4th Crop — COP Specialists............................................................ I94

Diagram I.224: Background Information — Main Crop Grown on Farm, 4thCrop — Other Cereal Specialists................................................ I94

Diagram I.225: Background Information — Main Crop Grown on Farm, 3rd Crop — Other Cereal Specialists............................................... I94

Diagram I.226: Background Information — Main Crop Grown on Farm, 4th Crop — Mixed Crops Livestock ................................................. I94

Diagram I.227: Background Information — Main Crop Grown on Farm, 5th Crop — Mixed Crops Livestock ................................................. I94

Diagram I.228: Background Information — Main Crop Grown on Farm, 5th Crop — Other Cereal Specialists............................................... I95

CASE STUDY MONOGRAPH — UK PAGE 1

Case Study Monograph — UK

As part of this Evaluation of the market regime for cereals, we have undertaken case studies to develop the basis for answering the Evaluation Questions. We have prepared case study monographs of six member states of the EU-15, and of regions within several of those members as relevant to particular Evaluation Questions, as well as case studies of two new member states.

1. OVERVIEW OF NATIONAL REPORT — UK

1.1 Rationale

This report covers the United Kingdom, which was selected because it is a leading cereal producer in the EU. The UK is used as a case study for discussions about adapting supply to demand and price formation and competitiveness of cereals on the internal and export markets, with particular emphasis on the effects of the drop in institutional prices and the effects restricting competition.

For specific discussions, this case study also covers two separate regions:

England, which is characterised by large farm sizes, greater than the EU average, with intensive agricultural practices, but with input use affected by environmental legislation. It has become a net cereals exporter since the reforms were introduced. England is used as a case study for the discussion on producers’ income levels and dependence on direct payments.

Scotland, which, like Denmark, is a representative of northerly European farming conditions, as reflected in its choice of cereal crops. There has been a major shift in the area of cereal production since the reforms. Scotland is ideal for use as a case study in the discussion about producers’ income levels and dependence on direct payments.

1.2 Structure

This national report on the UK is divided in two parts:

The Case Study Monograph — after this overview, we describe the cereal sector in the UK and in the two regions selected. We then proceed to summarise the national and regional case studies, presenting the key information obtained that serves as tools for addressing the specific, relevant evaluation themes.

Appendix to the Case Study Monograph — This part contains copious supporting material, mostly statistical in illustrative tables and diagrams but also more detailed text, that expands on key points in the Case Study Monograph. The Appendix to the Case Study Monograph for the UK is denoted as I. Please note: the tables and diagrams in the Appendix are denoted as Table I.x and Diagram I.x (“x” being an integer).

In the course of preparing this case study monograph, we have drawn heavily upon a series of interviews with participants from all the main cereal sectors, from production to processors and end-users, traders, government agencies, storage and transport companies. These are provided separately, but only in a confidential appendix, due to necessary terms and conditions for conducting the interviews.

CASE STUDY MONOGRAPH — UK PAGE 2

Interviews and Questionnaires conducted in the UK For the purpose of this case study, 42 stakeholders in the cereal sector were

interviewed by the regional consultant. In order to collect primary data for the study, a questionnaire survey was

undertaken of cereals producers in the UK regions of England and Scotland. Out of the 200 questionnaires sent out in each region, 17 were returned to the regional consultant by respondents in England and 19 by respondents in Scotland. The main findings of the analysis of the questionnaires, together with the relevant diagrams, are provided in the Appendix.

2. AN INTRODUCTION TO THE CEREALS SECTOR

2.1 UK

Agricultural Conditions — UK

Table UK.1: United Kingdom, Area Statistics, 2003 (‘000 hectares)

Total Country Area 24,410 Utilised Agricultural Area 16,352 Total Cereals Area (excl.rice) 3,059 Common Wheat Area 1,833 Barley Area 1,078 Oats & Mixed Cereals Area 126 Maize Area - Rye & Meslin Area 4 Durum Wheat Area 3 Total Set Aside Area 722 Industrial Set Aside Area 88

Source: EUROSTAT

Total UK land area is 24,410,000 hectares, of which 16,352,000 hectares (approximately 67%) were under cultivation in 2003.

In 2003, cereals were grown on 17% of the UK’s utilised agricultural land, common wheat accounted for roughly 60% of this area (see Table UK.1).

Table UK.1 also illustrates that 722,000 hectares of land were set aside under the different set-aside schemes for arable land, of which 88,000 hectares was industrial set-aside.

Farming accounts for more than 70% of the total land area of the UK, and produces nearly 65% of food products consumed nationally. UK farming contributes £6.6 billion (€9.7 billion) a year to the economy, and employs over half a million people. Agriculture’s share in the gross domestic product of the UK was 0.8% in 2003/04.

CASE STUDY MONOGRAPH — UK PAGE 3

The UK is a major producer of arable crops, and of cereal crops in particular. The main crops grown are wheat, oats, oilseed rape, sugar beet, barley and potatoes. Arable areas are concentrated in the eastern and southern portions of the UK, with large sheep, beef and dairy sectors providing significant outlets for feed grains.

Cereal production dominates the UK arable sector, dwarfing production of oilseeds and protein crops, with cereals accounting for 90% of total cereal, oilseed and protein crop (COP) production over the past three crop years. (See Diagram I.1 in the Appendix.)

Table UK.2: United Kingdom, Employment Statistics, 2003 (‘000 hectares)

Numbers of Holdings ('000) 61Civilian Employment in Agriculture ('000 persons) 344Employment in Agriculture (AWU) -Regularly Employed non-Family Members in Agriculture (%) (AWU) -Irregularly Employed non-Family Members in Agriculture (%) (AWU) -

Note: AWU = equivalent full-time workers.

Source: EUROSTAT

In 2003, 344 thousand civilians were employed in agriculture in the United Kingdom (see Table UK.2). The United Kingdom had 61 thousand holdings in 2003.

Cereals Production — UK

Within the cereals sector, wheat and barley are currently the most important crops grown in the UK, with oats comprising a minor, but significant, sector. However, the relative importance of wheat has increased substantially since the UK acceded to the EU in 1973. Diagram UK.1 presents UK cereal production since 1970/71, illustrating the growth of wheat to its current dominant position.

Total UK cereals production has declined since 1995/96, mostly accounted for by barley production, which has fallen by two million tonnes over the period. Meanwhile, wheat production has fallen very slightly and oats have remained largely static.

CASE STUDY MONOGRAPH — UK PAGE 4

Diagram UK.1: UK Cereal Production, 1970/71-2003/04

0

5

10

15

20

25

30

1970/71 1974/75 1978/79 1982/83 1986/87 1990/91 1994/95 1998/99 2002/03

Milli

on T

onne

s

Wheat Barley Oats

Source: HGCA

Cereals Area and Yields — UK

As Diagram UK.1 above reveals, since 1970/71 UK wheat production has grown by 220%. Meanwhile, area has grown only 80%, while barley area has declined 55% and oats area 70% (Diagram UK.2 below). The difference is explained by long term yield increases: over the period, wheat yields have progressed at a faster rate than barley and oats (Diagram UK.3 below). The emerging gap between wheat and barley yields has been important in driving gross margins from wheat above those of barley, thereby ensuring the place of wheat in the farm rotation. An interesting point to note, however, is that since 1995/96, yields of all three major cereals have been largely unchanged. (See Table I.1 in the Appendix.)

CASE STUDY MONOGRAPH — UK PAGE 5

Diagram UK.2: UK Area for Wheat, Barley and Oats, 1970/71-2003/04

0

500

1,000

1,500

2,000

2,500

1970/71 1974/75 1978/79 1982/83 1986/87 1990/91 1994/95 1998/99 2002/03

Hec

tare

s ('0

00)

Wheat Barley Oats

Source: HGCA

Diagram UK.3: UK Yields for Wheat, Barley and Oats, 1970/71-2003/04

3

4

5

6

7

8

9

1970/71 1974/75 1978/79 1982/83 1986/87 1990/91 1994/95 1998/99 2002/03

Tonn

es p

er H

ecta

re

Wheat Barley Oats

Source: HGCA

CASE STUDY MONOGRAPH — UK PAGE 6

Cereals Trade — UK

Before its accession to the EU in 1973, the UK was a net importer of cereals, notably in wheat. Since accession, the UK has evolved into a net exporter of cereals, including wheat, with a current production surplus for wheat, barley and oats, and a deficit in maize. Nonetheless, since 1995/96, exports of each crop have declined. In the case of barley, this has been due largely to decreasing production, while in the cases of wheat and oats, increased domestic consumption has eroded exportable surpluses. (See Diagram I.2 and Tables I.2 to I.5 in the Appendix for the UK cereals trade balance and supply/demand balances.)

Now that we have considered the aggregate position of the UK cereal sector, we turn to the regional positions of England and Scotland, considering barley and oats production in England, and barley and oats production in Scotland.

2.2 England

Cereals Production — England

In this report, we consider specifically the cases of barley and wheat production in England, as within the cereals sector, they are the most important crops, with oats comprising a minor sector. Diagram UK.4 presents English cereal production since 1995/96, revealing the dominance of wheat in the sector, though a slight downward trend is observable in wheat production. The severely weather-affected wheat crop is 2001/02 is clearly visible.

Barley production has declined since 1995/96, with the three-year average declining by 0.9 million tonnes over the period. Wheat has been broadly stable, although the most recent three-year average is distorted by the poor crop of 2001/02. Overall, these trends have led to an increased dominance of wheat production in the English cereal sector. (See Table I.7 for crop production between 1995/96 and 2003/04.)

CASE STUDY MONOGRAPH — UK PAGE 7

Diagram UK.4: England, Cereal Production, 1995/96-2003/04

0

5

10

15

20

25

1995/96 1996/97 1997/98 1998/99 1999/00 2000/01 2001/02 2002/03 2003/04

Milli

on T

onne

s

Wheat Barley Oats

Source: Defra Note: Oats production is presented where data available for comparison, 1998/99 to 2002/03 only.

Area and Yields — England

The decline in English cereal production is in large part a consequence of reduced acreage under cereals, sharper for barley than for wheat since 1995/96. However, barley area has not declined as fast as production of the crop over the same period, while wheat area has fallen faster than the decline in production.

The explanation lies with the trend in yields. The English cereal sector is characterised by high yields, though the maritime climate can limit production of the highest quality hard wheat varieties. Yields have declined, however, for English barley since 1995/96, while risen slightly for wheat. (See Tables I.8 and I.9 in the Appendix for English barley and wheat area and yields from 1995/96 to 2003/04.)

2.3 Scotland

Below we discuss the cereals sector in Scotland; for a discussion of the structure of agriculture, see the Appendix.

Cereals Production — Scotland

In this report, we consider specifically the cases of barley and oats production in Scotland, because within the cereals sector, wheat and barley are the most important crops, though oats is an important niche crop. Diagram UK.5 presents Scottish cereal production since 1995/96, illustrating the dominant position of barley, which represents around two-thirds of the cereal sector in Scotland.

Barley and oats production have increased since 1995/96, largely at the expense of the decline in wheat production highlighted in Diagram UK.5. The trend in barley production has increased by an annual average of 0.9% over the period, while the

CASE STUDY MONOGRAPH — UK PAGE 8

trend in oats production has increased by 1.0% per annum. (See Table I.10 in the Appendix for production of these crops between 1995/96 and 2003/04.)

Diagram UK.5: Scotland, Cereal Production, 1995/96-2003/04

0.0

0.5

1.0

1.5

2.0

2.5

3.0

3.5

1995/96 1996/97 1997/98 1998/99 1999/00 2000/01 2001/02 2002/03 2003/04

Milli

on T

onne

s

Wheat Barley Oats

Source: SEERAD/Defra

Area and Yields — Scotland

The increase in Scottish production of barley and oats over the last ten years has been driven by two separate phenomena. Barley area has increased over the period 1995/96 to 2003/04, while oats area has declined. Overall, Scottish cereal production is characterised by high yields but high moisture levels, which necessitate extensive drying. However, as both crops have increased their production over the period (see Table I.10), yields must have moved in opposite directions. This is confirmed by the data from the period, which show a small rise in oat yields, but a slight fall in barley yields. (See Tables I.11 and I.12 in the Appendix for Scottish barley and oats area and yields from 1995/96 to 2003/04.)

CASE STUDY MONOGRAPH — UK PAGE 9

3. PRODUCERS’ INCOME LEVELS

3.1 Overview

In this section, we examine incomes at the producer level between 1995/96 and 2003/04 for the UK, and for England and Scotland separately, considering whether the CMO measures for cereals, including market support, direct payments and set-aside, have helped producers obtain a fair and sufficiently stable income.

We also consider some of the unexpected effects within the sector, notably the impact on agricultural land prices and rents, and assess whether any observed effects have been due to cereal policy measures.

Indicators

In order to assess income levels, we adopt both EU and national level data. The EU measures use the Net Farm Value Added (NFVA) per Annual Working Unit (AWU) methodology presented in the main report accompanying this case study. For the national level, we draw upon the Farm Business Survey results from the annual survey carried out on behalf of the UK Department for Environment, Food and Rural Affairs (Defra). Off-farm incomes are also considered to assess the impact of policy measures.

Land prices and land rentals are utilised to consider the unexpected effects of cereal policy measures.

Judgement Criteria

Cereal incomes will be considered fair and sufficiently stable if they have moved in a broadly similar direction to those earned in other farm sectors, and do not display notably greater volatility.

Statistical Importance of Featured Period 1995/96-2003/04

Before exploring UK farm incomes, it is important to recognise at the outset that 1995 was a particularly good year for UK producers for several reasons, including importantly:

Cereal prices were at high levels.

The weakness of sterling against the euro meant that euro-denominated area payments converted to high payments when expressed in pounds sterling.

Because of these market circumstances in the early part of the featured period 1995/96 to 2003/04, there was a lag in the transmission of the MacSharry reforms of the CAP through to UK cereal producers. Reductions in intervention prices, denominated in euros, did not translate into falls when expressed in sterling until sterling began to rise after 1995/96. Moreover, compensatory area payments were denominated in euros, as explained above.

Have the measures, in particular the level of market support, direct payments and set-aside, helped the different types of producers obtain a fair and sufficiently stable income?

CASE STUDY MONOGRAPH — UK PAGE 10

In the opinion of most farmers interviewed in the course of this report, farm incomes in England and Scotland actually rose briefly around 1995/96 following the implementation of the MacSharry reforms.

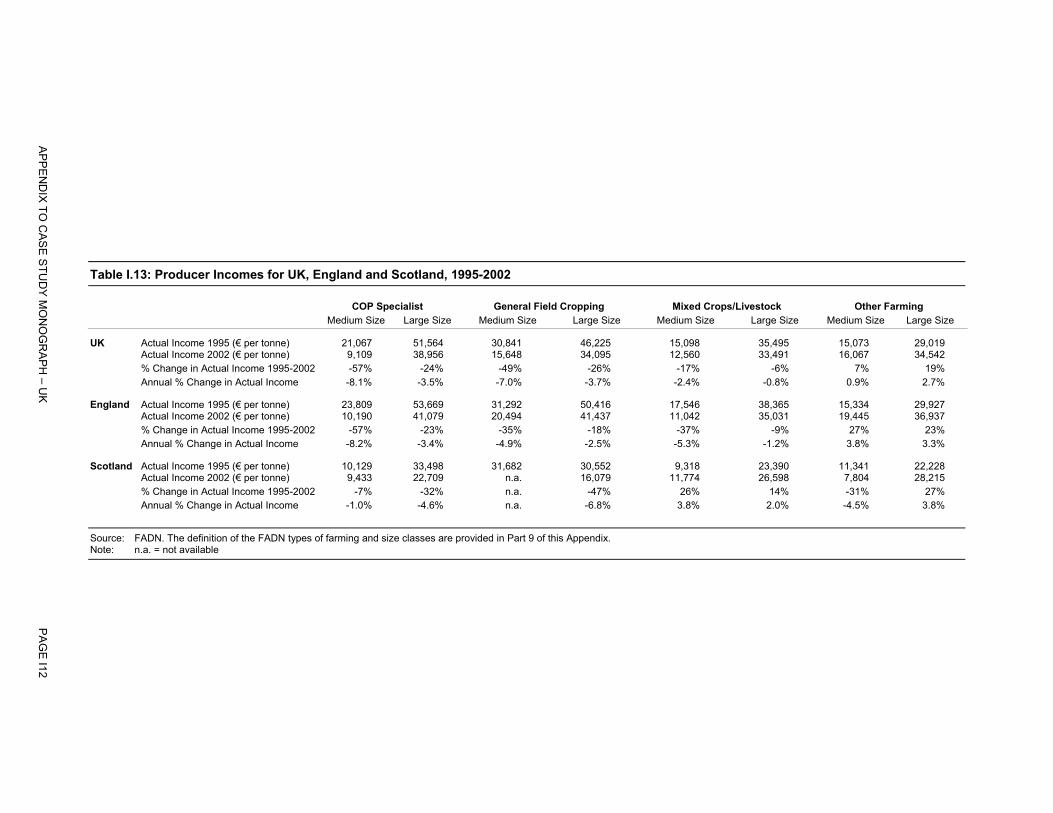

3.2 Net Farm Value Added per Annual Work Unit

In broad terms, farm incomes for all farm types considered in this report have for the most part declined since 1995. (See Appendix for fuller discussion and Tables I.15 and I.14 for analysis of income data.)

Within the limitations of the short series of data, and missing data and small sample sizes therein, analysis of income data reveals several interesting conclusions. These include:

Farm incomes have trended downwards over the period, in the UK as a whole and in England.

Scale is important for income. In all farm types for the UK, England and Scotland, large farms have higher incomes than medium size farms.

Scale is especially important for COP specialists, in the UK, England and Scotland. There is a large divergence between incomes for COP specialists on large and medium scale farms: on large farms, COP specialists were among the highest ranked incomes in both 1995 and 2002, while for medium farms, incomes were all toward the lower end of the income rankings in both years.

Incomes have fallen relatively steeply for both large and medium size COP specialists. For the UK as whole and for England, medium size COP specialists have experienced the greatest percentage falls over the period, from already low-income levels. In Scotland, the pattern is somewhat reversed, with large COP farms experiencing larger income reductions relative to other farm types.

3.3 National Farm Income Sources

In this section, we compare regional and national information sources of farm income data with the broad conclusions presented above from the NFVA/AWU data.

In Diagram UK.6, we present nominal net farm incomes for cereal specialists in the UK, England and Scotland according to Defra’s Farm Business Survey1.

The diagram reveals the peak in net farm incomes enjoyed in 1995/96, and the steep decline to 1997/98 as falling cereal prices and sterling’s appreciation meant that the MacSharry reforms belatedly affected incomes in the UK farm sector. Incomes stabilised somewhat between 1997/98 and 2002/03, and have enjoyed a recovery recently, due primarily to higher prices for cereals in 2003/04 (Diagram UK.6).

A considerable amount of volatility is depicted by cereal farm incomes, although the peaks in income are notably more pronounced than the flat-bottomed troughs. This observation is supported by farmers interviewed in the course of this report, who considered farm support measures, notably intervention prices and arable area payments, to provide a floor to incomes. Set-aside may also help in this regard, by

1 Estimates for 2004/05 are provisional.

CASE STUDY MONOGRAPH — UK PAGE 11

providing a positive remuneration for marginal fields that would derive negative margins if farmed with cereals.

Diagram UK.6: Average Net Farm Incomes for Cereal Farms2, 1994/95-2002/03

-20

0

20

40

60

80

100

1994/95 1995/96 1996/97 1997/98 1998/99 1999/00 2000/01 2001/02 2002/03 2003/04 2004/05

'000

Eur

os

UK England Scotland

Source: Defra

A further notable feature of Diagram UK.6 is how closely the England and UK figures are related, with England accounting for over 90% of the UK weighting in cereals. This should be borne in mind in the remainder of this case study, as data is sometimes available only for the UK as a whole and for Scotland separately (as a result of the devolution of some functions to a separate Scottish parliament from London). Where this is the case, the UK can be taken as a close proxy for the English situation.

Using Defra data to compare cereal specialists with general arable cropping and mixed farming reveals the convergence in incomes among farm types over the period in England, where cereal farm incomes are now similar to mixed farming, although general cropping incomes remain somewhat higher but more volatile. In this regard, support measures can be said to have affected incomes in a fair manner, as incomes across farming sectors have converged over time. (See Diagrams I.6 and I.7 in the appendix.)

In Scotland, cereal farm incomes plummeted from their mid 1990s peaks, and have become negative in 2004/05, as have other farming activities. Scottish cereal incomes have been more volatile than other sectors over the period, as measured by the coefficient of variation, although this is largely due to the high prices of the initial years in the period. By contrast, mixed farming incomes in Scotland rose gradually from the

2 Defra define cereal farms in this context to have more than two-thirds of farm gross margins derived from

cereal crops. General cropping farms have no more than two-thirds of farm gross margins from any single crop type. Mixed farms are defined as those farms where no more than two-thirds of the farm gross margin comes from either arable or livestock.

CASE STUDY MONOGRAPH — UK PAGE 12

late 1990s, until 2004/05, largely due to the successful product differentiation and premium branding of Scottish beef.

In this latter case, the phenomenon has not been a product of policy, although farmers felt that policy reforms in the form of declining support had stimulated various private initiatives.

Almost half of all cereal farms (defined as deriving 70% of gross margins from cereal crops) in England and Scotland earned net farm incomes of less than zero in 2001/02, while the most successful 5% of cereal farms in England earned over €80,000. (See Diagram I.8 in the appendix.)

Another way of considering net farm incomes is to compare incomes on a per hectare basis. Again the peaks in 1995/96 are apparent, and the downward trend in incomes per hectare since that time is notable for all sectors, with cereal specialists becoming the lowest remunerated sector in several years recently. The rather dramatic recovery for both arable sectors in 2003/04 is explained by the impact of high grain prices, and is thought to be anomalous and unsustainable by industry sources. Evidence for this supposition is provided by other income series contained here extending to 2004/05. (See Diagram I.9 in the appendix.)

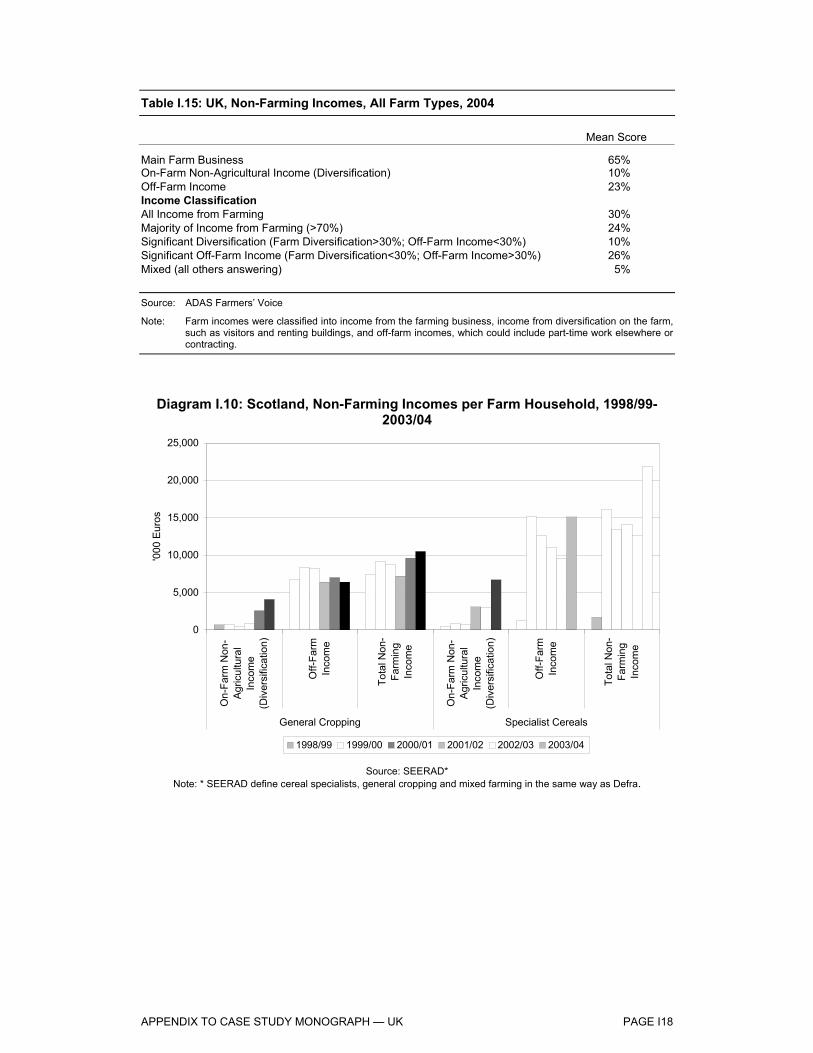

3.4 Non-Farm Incomes

Although accurate data on non-farm incomes for farm holdings is sparse, an ADAS Farmers’ Voice Survey in 2004 found that 70% of UK farm households have some income from non-farming sources. Only two-thirds of average farm income for respondents came directly from farming. Table I.15 in the appendix presents the results of the ADAS survey. (Unfortunately, there are no figures available prior to this date to assess how this source of income has altered over time.)

The Cambridge University Report on Farming in the Eastern Counties has also found increases in non-farm income in the eastern counties of England, which represent the English cereal heartland, predominantly from rental of farm buildings and contract work.

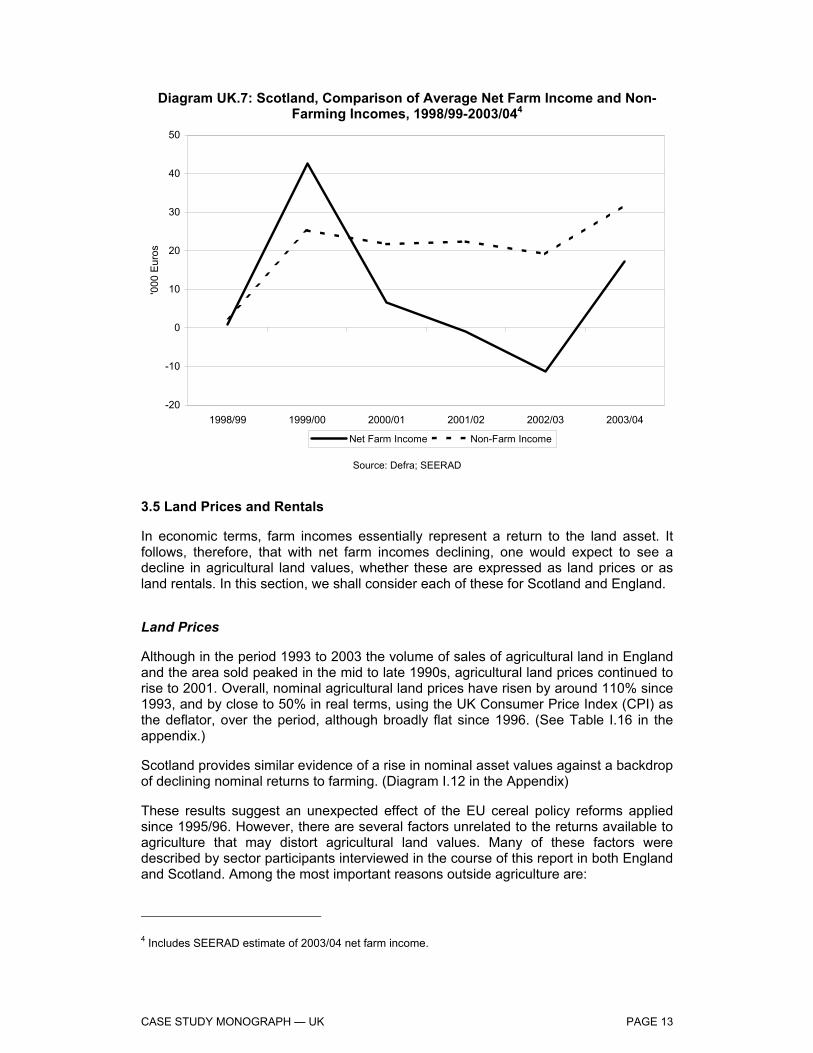

For Scotland, SEERAD data on non-farm incomes show that specialist cereal producers earn more income from non-farming activities than do general field cropping farmers, while for both types of producers3 off-farm income is considerably more important than on-farm diversification. (See Diagram UK.7)

Such is the importance of non-farm incomes to the farm household, non-farm incomes now typically contribute more to the total household income than incomes from farming activities, as Diagram UK.9 reveals. Moreover, non-farm incomes display notably greater stability than net farm incomes.

3 SEERAD define cereal specialists, general cropping and mixed farming in the same way as Defra.

CASE STUDY MONOGRAPH — UK PAGE 13

Diagram UK.7: Scotland, Comparison of Average Net Farm Income and Non-Farming Incomes, 1998/99-2003/044

-20

-10

0

10

20

30

40

50

1998/99 1999/00 2000/01 2001/02 2002/03 2003/04

'000

Eur

os

Net Farm Income Non-Farm Income

Source: Defra; SEERAD

3.5 Land Prices and Rentals

In economic terms, farm incomes essentially represent a return to the land asset. It follows, therefore, that with net farm incomes declining, one would expect to see a decline in agricultural land values, whether these are expressed as land prices or as land rentals. In this section, we shall consider each of these for Scotland and England.

Land Prices

Although in the period 1993 to 2003 the volume of sales of agricultural land in England and the area sold peaked in the mid to late 1990s, agricultural land prices continued to rise to 2001. Overall, nominal agricultural land prices have risen by around 110% since 1993, and by close to 50% in real terms, using the UK Consumer Price Index (CPI) as the deflator, over the period, although broadly flat since 1996. (See Table I.16 in the appendix.)

Scotland provides similar evidence of a rise in nominal asset values against a backdrop of declining nominal returns to farming. (Diagram I.12 in the Appendix)

These results suggest an unexpected effect of the EU cereal policy reforms applied since 1995/96. However, there are several factors unrelated to the returns available to agriculture that may distort agricultural land values. Many of these factors were described by sector participants interviewed in the course of this report in both England and Scotland. Among the most important reasons outside agriculture are:

4 Includes SEERAD estimate of 2003/04 net farm income.

CASE STUDY MONOGRAPH — UK PAGE 14

Amenity Value of Land: Agricultural smallholdings and farmland have become prized assets in the booming UK property market of the last decade. With improved transport networks and changes in work practices (including the increase in home working), the distances from employment centres that people can and will travel has increased, bringing more rural areas into the prospective property market.

Inheritance Tax: Agricultural land is exempt from inheritance tax in the UK, and is therefore retained by land-owning farmers more readily than would otherwise be the case. If the land were sold, the capital would be eligible for capital gains tax (however, see rollover tax allowance below) and inheritance tax. Given the age structure for UK farmers (average age 59), this is an important restraint on the volume of land entering the market for sale.

Rollover Tax: Liabilities for capital gains tax can be rolled over for three years, and any asset purchases made during this time become exempt from capital gains tax. For example, if a farmer sold land, he would normally be liable to pay capital gains tax at a rate of 40%; however, if this capital is spent on eligible assets over the next three years, the amount spent is exempt from capital gains tax. Many farmers acknowledged that they have sold agricultural land, and then purchased agricultural land elsewhere, to take advantage of this rollover allowance. This offers support to agricultural land prices by creating demand for the asset as a tax avoidance strategy.

Uncertainty: Many farmers and other cereal sector participants felt that reforms in EU agriculture had increased uncertainty in the sector, particularly with regard to prices. Because of this, many farmers felt that holding land assets, for the reasons described above, provide a hedge against agricultural commodity prices.

In addition to the above, interviewees also suggested several farm-related factors supporting the price of land:

Scale Economies: As the analysis above revealed, returns to agriculture improve with the scale of farm. Thus, at the margin, there is always an incentive to increase the scale of production by purchasing appropriate land when it becomes available. The prime reason for scale economies is that fixed costs are spread over a larger land area, so lowering costs per unit area. Thus, returns from additional units of land are offset against marginal, or variable, cost only, increasing the return from purchased land units and thereby supporting land prices.

Lack of Contiguous Fields: One drawback commonly cited as inhibiting farm expansion and operational efficiency is that farm holdings often comprise non-contiguous plots of land. For this reason, when favourably sited agricultural land becomes available contiguous to existing holdings, this land is highly prized, thereby supporting land prices.

Illiquid Market: For many of the reasons mentioned above, the volume of land entering the market is relatively low, and, therefore, demand often outstrips supply when suitable holdings are available.

(Some insight into the importance of some of these factors is provided by Diagrams I.13 and I.14, which present English agricultural land sales by the size of area sold.)

CASE STUDY MONOGRAPH — UK PAGE 15

Land Rentals

As with land prices, land rentals have risen over the period as a whole, although there has been a distinct drop since the late 1990s — slightly earlier than the recent declines in land prices. Nevertheless, the overall impression may again lend some credence to the support given to land prices by the farming factors mentioned above — namely, the desire for economies of scale and contiguous plots, and the problem of illiquid markets providing limited opportunities to pursue these strategies. (See Diagram I.15.)