Embed Size (px)

Citation preview

EVALUATION AND SELECTION OF INNOVATION PROJECTS

Hugo Aléxis Alves Ribeiro

Thesis to obtain the Master of Science Degree in

Mechanical Engineering

Supervisor: Prof. Elsa Maria Pires Henriques

Examination Committee

Chairperson: Prof. Rui Manuel dos Santos Oliveira Baptista

Supervisor: Prof. Elsa Maria Pires Henriques

Member of the Committee: Prof. Paulo Miguel Nogueira Peças

November 2015

I

Abstract

Innovation plays a major role in the growth and economic competitiveness of companies, industries and

countries. Innovation projects are strong consumers of resources and their potential benefits occur in a long

time horizon, therefore, it is essential to develop the capacity to assess the potential performance and return

of the investment in innovation projects, which will allow companies to focus their efforts on the projects with

the highest expected return.

This thesis focused on the different approaches and methods used in the literature for evaluating and

prioritizing projects at the early stages of innovation in a context of limited resources. An exhaustive list of

different criteria and descriptors of performance was developed, establishing the foundation for the

methodology for project selection here proposed, which consists on the setting, structuring and execution of

the evaluation, risk analysis, resource allocation, decision and conclusions. This objective procedure involves

multicriteria decision-making, deals with the risk and uncertainty in innovation and supports the construction

of a portfolio of projects, therefore capturing the complexity of the problem while being simple to understand,

apply and adapt to specific company needs and constraints. It can thus constitute a valuable aid for companies

to build their own project selection process or to compare with the currently implemented one.

Keywords

Project selection; Innovation; Project portfolio management; Multicriteria decision-making.

II

Resumo

A inovação desempenha um papel importante no crescimento e competitividade económica de empresas,

indústrias e países. Os projetos de inovação são fortes consumidores de recursos e os seus potenciais

benefícios ocorrem num horizonte temporal futuro, como tal, é essencial desenvolver a capacidade de avaliar o

potencial desempenho e retorno do investimento em projetos de inovação, o que permitirá às empresas

centrarem os seus esforços nos projetos com maior retorno esperado.

Esta tese baseou-se nas diferentes abordagens e métodos utilizados na literatura para avaliar e prioritizar

projetos nas fases iniciais da inovação, num contexto de recursos limitados. Uma lista exaustiva de critérios e

descritores de desempenho foi criada, estabelecendo as bases para a metodologia de selecção de projectos

aqui proposta, composta pela definição, estruturação e execução da avaliação, análise de riscos, alocação de

recursos, decisões e conclusões. Este procedimento objetivo envolve a tomada de decisão multicritério, lida

com o risco e incerteza na inovação e apoia a construção de um portefólio de projetos, captando assim a

complexidade do problema e, simultaneamente, sendo simples de entender, aplicar e adaptar às necessidades

e limitações específicas das empresas. Esta tese pode, consequentemente, constituir uma ajuda valiosa para as

empresas que queiram construir o seu próprio processo de seleção de projetos ou comparar com o que têm

atualmente implementado.

Palavras chave

Seleção de projetos; Inovação; Gestão de portefólio de projetos; Decisão multicritério.

III

Index

Abstract .................................................................................................................................................................... I

Resumo ................................................................................................................................................................... II

List of figures .......................................................................................................................................................... IV

List of tables ............................................................................................................................................................ V

1. Introduction.................................................................................................................................................... 1

1.1. Innovation in Companies ....................................................................................................................... 1

1.2. An Overview of Project Selection .......................................................................................................... 2

1.3. Motivation and Objectives of the Thesis ............................................................................................... 3

1.4. Background of the Example of Application ........................................................................................... 3

1.5. Structure of the Thesis .......................................................................................................................... 4

2. State of the art ............................................................................................................................................... 5

2.1. Project Selection .................................................................................................................................... 5

2.2. Project Selection Models ....................................................................................................................... 7

2.3. Criteria used in Project Selection Models ............................................................................................ 16

2.4. Risk and Uncertainty ............................................................................................................................ 19

2.5. Common mistakes in Project Selection ............................................................................................... 22

2.6. Literature Research Conclusions ......................................................................................................... 23

3. Methodology for Project Selection .............................................................................................................. 24

3.1. Setting the Evaluation Process ............................................................................................................ 26

3.2. Structuring the Evaluation ................................................................................................................... 41

3.3. Project Evaluation ................................................................................................................................ 44

3.4. Risk Analysis ......................................................................................................................................... 46

3.5. Resource Allocation ............................................................................................................................. 49

3.6. Decision and Conclusions .................................................................................................................... 52

3.7. Computational tool: M-MACBETH ....................................................................................................... 53

3.8. Project Portfolio Management ............................................................................................................ 54

4. Example of application ................................................................................................................................. 55

4.1. Setting the Evaluation Process ............................................................................................................ 55

IV

4.2. Structuring the Evaluation ................................................................................................................... 60

4.3. Project Evaluation ................................................................................................................................ 63

4.4. Risk Analysis ......................................................................................................................................... 66

4.5. Resource Allocation ............................................................................................................................. 67

4.6. Decision and Conclusions .................................................................................................................... 69

5. Conclusion .................................................................................................................................................... 70

5.1. Summary .............................................................................................................................................. 70

5.2. Findings ................................................................................................................................................ 70

5.3. Contributions ....................................................................................................................................... 70

5.4. Challenges and Limitations .................................................................................................................. 71

5.5. Applications of this Thesis ................................................................................................................... 71

5.6. Recommendations for Future Development ....................................................................................... 71

6. References .................................................................................................................................................... 72

List of figures

Fig. 1: Innovation Value Chain [10] ......................................................................................................................... 2

Fig. 2: Popularity of methods employed [25] ........................................................................................................ 15

Fig. 3: Popularity of the criteria [25] ..................................................................................................................... 18

Fig. 4: Different risk methods [27] ........................................................................................................................ 21

Fig. 5: Diagram of the project selection methodology .......................................................................................... 25

Fig. 6: List of possible criteria ................................................................................................................................ 27

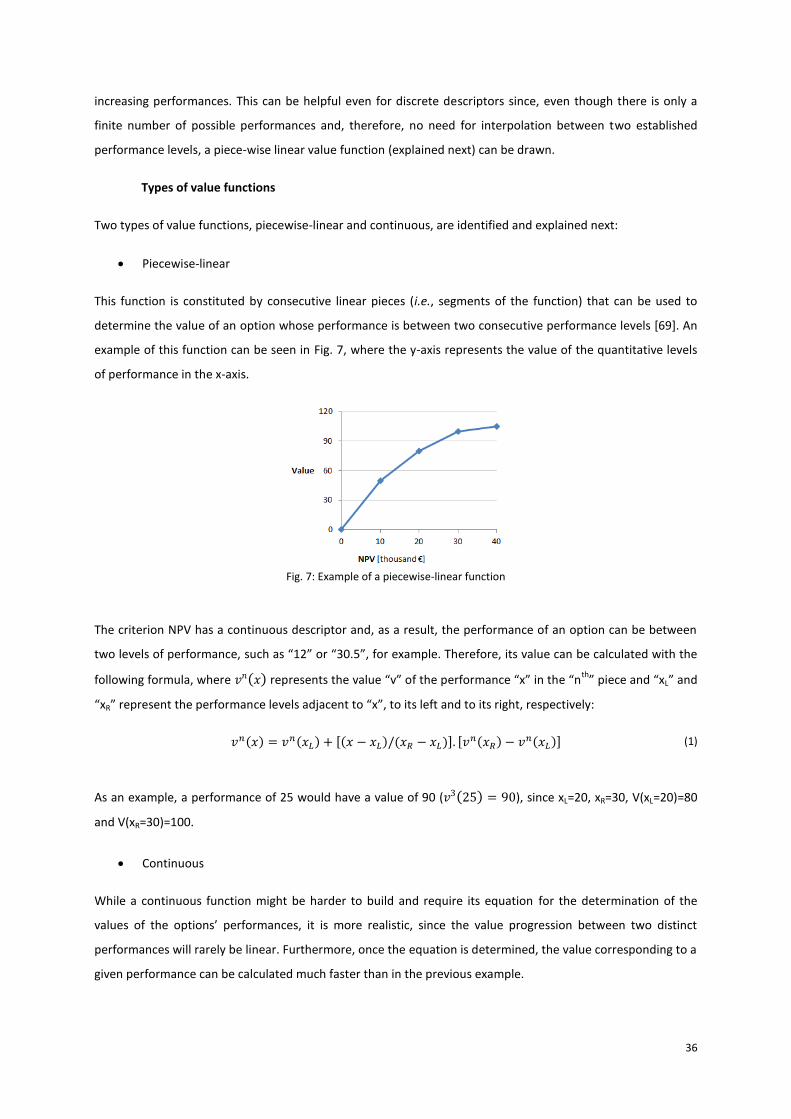

Fig. 7: Example of a piecewise-linear function ...................................................................................................... 36

Fig. 8: Example of a continuous value function [faculty evaluation] .................................................................... 37

Fig. 9: Example of the determination and use of a value function ....................................................................... 38

Fig. 10: Fictitious alternatives A and B (adapted from [73]) ................................................................................. 39

Fig. 11: Swings between the reference levels (adapted from [73]) ...................................................................... 40

Fig. 12: Project type filter (adapted from [22]) ..................................................................................................... 41

Fig. 13: Triage filter (adapted from [22]) ............................................................................................................... 44

Fig. 14: Graph of overall scores ............................................................................................................................. 46

Fig. 15: Probability of Success VS Overall Score (adapted from [ref5]) ................................................................ 47

Fig. 16: Efficient frontier [16] ................................................................................................................................ 47

Fig. 17: Prioritisation of projects by their benefit-to-cost ratio and by their benefits only [12] ........................... 49

V

Fig. 18: Innovation Effectiveness Curve [80] ......................................................................................................... 51

Fig. 19: Company criteria ...................................................................................................................................... 56

Fig. 20: Tree of identified criteria .......................................................................................................................... 56

Fig. 21: Performance levels of criterion "Durability" ............................................................................................ 58

Fig. 22: Judgements matrix and value function of criterion "Net present value” ................................................. 59

Fig. 23: Weighting matrix of judgements .............................................................................................................. 59

Fig. 24: Weights histograms (at the left, proposed by M-MACBETH, at the right, a possible adjustment) .......... 60

Fig. 25: Tree of selected criteria ............................................................................................................................ 61

Fig. 26: Options and table of performances.......................................................................................................... 62

Fig. 27: Table of overall scores .............................................................................................................................. 63

Fig. 28: Sensitivity analysis on criterion C4 ........................................................................................................... 64

Fig. 29: Robustness analysis (0% variation) ........................................................................................................... 65

Fig. 30: Robustness analysis (10% variation on the left, different variations on the right) .................................. 65

Fig. 31: Probability of success VS Overall score .................................................................................................... 67

Fig. 32: Portfolios of projects ................................................................................................................................ 68

List of tables

Tab. 1: Various kinds of project selection methods (adapted from [19]) ............................................................... 8

Tab. 2: Comparison of project selection methods (adapted from [19]) ................................................................. 9

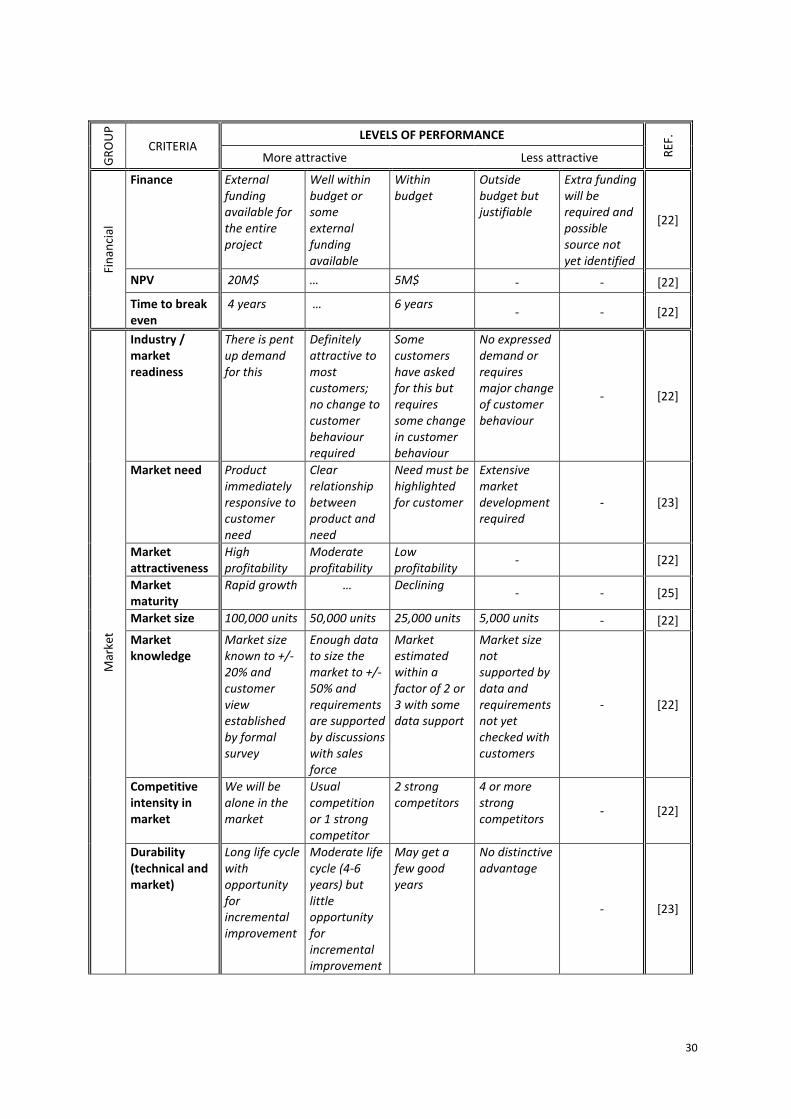

Tab. 3: Descriptor of performance of Market Attractiveness ............................................................................... 28

Tab. 4: List of possible descriptors of performance .............................................................................................. 29

Tab. 5: Example of reference levels (adapted from [64]) ..................................................................................... 34

Tab. 6: Table of performances .............................................................................................................................. 43

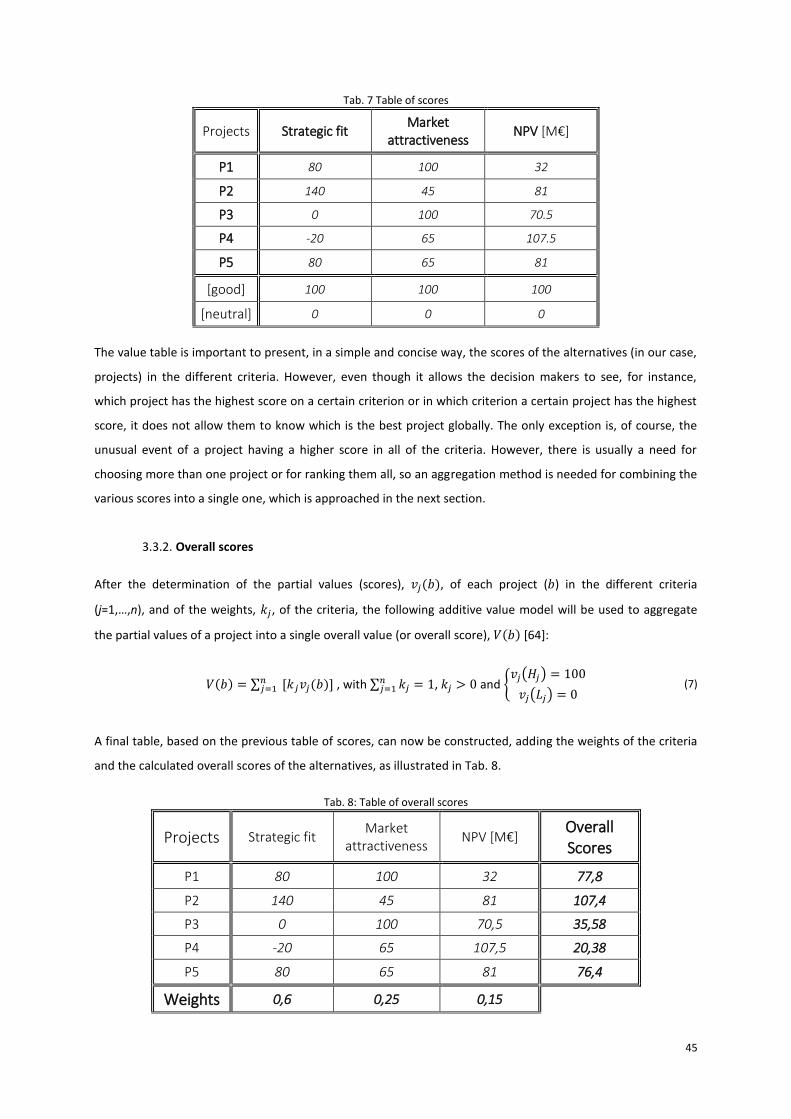

Tab. 7 Table of scores............................................................................................................................................ 45

Tab. 8: Table of overall scores ............................................................................................................................... 45

Tab. 9: Table of expected benefits ........................................................................................................................ 48

Tab. 10: Table of portfolios ................................................................................................................................... 50

Tab. 11: Descriptors of performance .................................................................................................................... 57

Tab. 12: Table of performances ............................................................................................................................ 62

Tab. 13: Table of expected value .......................................................................................................................... 66

Tab. 14: Possible portfolios of projects ................................................................................................................. 68

1

1. Introduction

This chapter provides an overview of project selection, its importance and the challenges in executing it, as well

as its role in the innovation value chain. The motivation and objectives of this work are then stated, followed by

the background of the example of application and the structure of this thesis.

1.1. Innovation in Companies

“Innovation, at the level of an individual firm, might be defined as the application of

new ideas to the firm, regardless of whether the new ideas are embodied in

products, processes, services, work organization, marketing or management

systems.”

Credited to Gibbons et al. [1] in [2]

Innovation strengthens the growth and dynamism of all economies and, while not a goal in itself, can play a

critical role in leading the world to a more sustainable growth path following the financial crisis, according to

OECD’s “Innovation Strategy 2015” [3]. In companies, it is also increasingly more imperative as consumer

demand becomes more sophisticated and competition more intense [4]. Consequently, companies invest in

innovation to increase competitive advantage, for instance, by gaining market share, reducing costs or

increasing productivity, spending on average 1-2% of turnover on various innovation-related activities [4]. In

turn, 5-7% of their turnover comes from products that are new to the market in most countries (6.24% in

Portugal) [4].

BCG’s 2010 global survey of senior executives on their innovation practices [5], responded by 1590 executives

representing all major markets and industries, reports that 72% of respondents say that innovation is one of

their company’s top-three priority. Furthermore, 61% of companies plan to increase their innovation spending,

most likely motivated by their rising satisfaction with their returns on innovation spending [5]. These

investments in innovation-related activities are also encourage by governments, who implement policies to

stimulate R&D, both directly (through grants or loans) and indirectly (through fiscal incentives) [3]. Hence,

public funding of innovation projects aims to produce more innovation by assisting companies to undertake

more development work, thus producing more innovation and ultimately resulting in increased financial

performance [6].

R&D projects are therefore a fundamental component of innovation and a crucial factor in developing new

competitive advantages [7]. For this reason, the Project Management Institute (PMI) calls project practitioners

“the engines of innovation” [8].

2

1.2. An Overview of Project Selection

Although there is a widespread belief that higher R&D spending translates into higher economic performance,

studies shows that there is no relationship between R&D spending and corporate success [9]. According to

Kandybin and Kihn [10], for companies to maximize their return on innovation investment (ROI2), a well-

organized innovation value chain (Fig. 1) is required, mastering four critical sets of capabilities: ideation, project

selection, development and commercialization.

Fig. 1: Innovation Value Chain [10]

At the start of this chain is the suggestion of several ideas and concepts that are conveyed through project

proposals. However, usually only a very small fraction can be selected since resources are limited, therefore,

there must be a professional method for prioritizing each potential project, just as there are systems to

manage the execution stages [11] (development and commercialization). This task is complex and difficult

because many options are present and resources have to be allocated considering costs, risks and benefits [12],

which are often uncertain and sometimes intangible.

A project is “a unique process, consisting of a set of coordinated and controlled

activities with start and finish dates, undertaken to achieve an objective conforming

to specific requirements.”

International Organization for Standardization [13]

Project selection is, therefore, a key part in this multifunctional capability that is innovation [10], which always

comes into play when the number of potential projects exceeds the number that can be effectively undertaken

within time and money constraints [14]. There are several different approaches to deal with project selection,

which should be part of an explicit formalized tool for portfolio management and applied consistently [15].

Regardless of the approach chosen by the company, choosing the right projects is a crucial step in ensuring

good project management [16], though it is not enough to guarantee innovation success [10].

The project selection problem has received plenty of attention in the literature at least since the 1960s [17],

[18], describing an abundant variety of approaches and models designed to support decision making in this

domain and taking into account different aspects and perspectives of the problem. They have evolved from

simple cost analysis to integer and linear programming to more flexible methods, such as fuzzy mathematical

3

programming [19]. However, more recent models have tried to consider more qualitative factors involved in

decision processes [20], which can easily be considered in scoring models.

The books on project management by Meredith and Mantle (2009) [21] and Pinto (2010) [16] have presented

various project selection models, criteria, examples and requisites for these models, among others. Regarding

criteria, there is an endless amount in the literature ([14], [16], [21], [22], [23], [24], [25]), which vary with the

type of projects and the models used for the selection. Sokmen [24] provides a list of the different methods

and criteria used until 2013.

In what concerns the analysis of risk, typical of innovation projects, most models developed and referred in the

literature rely on the determination or estimation of probability distributions to deal with uncertainty in some

parameters associated with the decision, as in [21] and [26], using them to estimate the risk profiles or

probability distributions of the outcomes of the decision [21]. However, risk is also sometimes treated as

criteria rather than as probabilities [12]. Ilevbare [27] presents a list of around 50 different methods and

techniques for addressing uncertainty and risk

1.3. Motivation and Objectives of the Thesis

Despite the importance of project selection and the existence of various approaches to deal with it, the

industrial use of these models is limited [17], [28], since models are not able to capture the complexity of the

problem [28] or, in contrast, they are excessively complex and mathematically elaborate themselves for

decision makers to systematically apply [17], [18], sometimes even requiring the assistance of an expert

decision analyst [17]. Bin et al. [18] recently pointed out that there is still the need for additional efforts in this

field, mostly to deal with complexity in a less complex way [18], which motivated the execution of this work.

In this context, an extensive research was conducted on the different criteria, descriptors of performance

(scaling statements) and methods used in the literature, as well as on the risk and uncertainty in innovation,

the construction of a portfolio of projects, the requisites of project selection tools and the most common

mistakes in these methods and in decision-making. As a result, a comprehensive methodology to assist

companies in selecting innovation projects is proposed, which intends to capture the complexity of the

problem and enable its application to different types of projects and companies. At the same time, it aims to be

simple to understand, apply and adapt to the specific needs of the company.

1.4. Background of the Example of Application

In order to exemplify how the developed methodology for project selection can be applied, a real case of

project selection was chosen. It was conducted in the context of a PhD Thesis [29] on the innovation in SMEs

(small and medium enterprises), where eco-design related ideas were evaluated for new product/process

development in Fapil, S.A., a manufacturer of domestic products. Innovation and sustainability are becoming

increasingly more critical in industrial companies, where mechanical/production engineers are often

4

responsible for the development of new products and processes that have to balance financial factors with

product/production characteristics, market and strategy, among others, consequently making a real example

like this more interesting and robust than a purely fictitious one.

1.5. Structure of the Thesis

The remainder of this thesis is organised into the following four chapters. Chapter II provides the foundation

for this work through the review of relevant literature. It introduces the project selection problem and

summarizes several methods to support it, as well as diverse criteria used in these models, including risk and

uncertainty. Finally, a discussion of common mistakes in project selection is made. Chapter III proposes a

comprehensive methodology to assist companies in selecting innovation projects, based on multicriteria

decision-making, which includes the evaluation of projects, risk analysis and resource allocation, resulting in a

final proposed portfolio of projects. Chapter IV presents an example of application of the methodology for

project selection. Chapter V concludes the thesis and indicates areas for further research.

5

2. State of the art

Since the beginning of the era of modern project management (around 60’s to early 00’s) project managers

focused on successfully completing projects (on time, within budget and with quality) and satisfying

stakeholders [14]. Project managers grew to be respected professionals that strived for project success, which

not always translated into business success, invoking the need for the postmodern era of project management

- Project Portfolio Management (PPM) [14]. Harvey A. Levine, former president of the board of directors of the

Project Management Institute, proposes the following definition for PPM:

PPM is a set of processes, supported by people and tools, to guide the enterprise in

selecting the right projects and the right number of projects and in maintaining a

portfolio of projects that will maximize the enterprise’s strategic goals, efficient use

of resources, stakeholder satisfaction and the bottom line.

Levine [14]

The primary components of the PPM process are the “prioritization and selection of candidate projects for the

portfolio” and “maintaining the pipeline: continuing, delaying or terminating approved projects” [14]. In this

chapter, the state of the art regarding the first component of PPM, project selection, is presented, as well as a

body of literature on this subject from the last 55 years. Different methods for prioritizing and selecting

projects are explained, followed by the criteria used, the risk in innovation and the most common mistakes in

project selection.

2.1. Project Selection

Prioritizing and selecting potential projects is one of the major challenges in PPM, which is one of the main axes

of management models of public and private organizations involved in research, development and innovation

activities [18]. For this reason, there is a large amount of literature dedicated to the project selection problem

at least since the 1960s [17], [18], describing an abundant variety of approaches and models designed to

support decision making in this domain and taking into account different aspects and perspectives of the

problem. In 1990, Harry M. Markowitz was awarded the Nobel Prize for having developed the theory of

portfolio choice, analysing investments in assets that differ in their expected return and risk (by performing

mean-variance analysis) [30], which led to the use of portfolio management in several other areas, particularly

in project management [31].

The first models for project prioritization and selection used return on investment (ROI) as the primary decision

criteria, to which more formal quantitative techniques followed, such as scoring and optimization models [32],

with developed mathematical tools becoming increasingly sophisticated but with no industry acceptance [20].

As a result, more recent models have tried to consider more qualitative factors involved in decision processes

[20].

6

Bretschneider [33] provides a complete list of project selection research from 1959 to 1990, were the

benefit/cost analysis is among the earliest references of prioritization methods. Henriksen and Traynor [17]

present an overview of the R&D project selection literature up to 1995. Graves and Ringuest [26] deliver the

latest work in this field, as of 2003, predominantly on mathematical programming. More recently, Meredith

and Mantle (2009) [21] and Pinto (2010) [16] presented various qualitative and quantitative project selection

models, as well as criteria, examples and requisites for this models, and, in 2014, Sokmen [24] organized a list

of the different methods and criteria used until 2013. There is also important work on the study of the “real

world” application of these models, such as [25] (2001), and on how to structure the scoring process for

prioritizing and selecting innovation projects [22] (2014), both of which, together with [23], include valuable

criteria that are present in the next chapter.

While literature about R&D is the most common, there is now also a great amount of work describing

Information Technology (IT) and New Product Development (NPD) portfolio selection (which is often

considered as R&D), however, it is usually assumed that the models apply equally well to R&D and IT project

selection [26], or to other capital spending projects, even though the specific criteria used for each type will

unsurprisingly differ. According to Levine [14], the process of project portfolio selection is comparable to the

one used in selecting items for an investment portfolio, which they actually are, since the company invests in

projects with the objective of maximizing the return.

“The Standard for Portfolio Management - Third Edition”, issued in 2013 by the PMI [34], identifies portfolio

management processes generally recognized as good practices, including the selection and prioritization of

projects. After the selection of the portfolio of projects, during the different stages of their life cycle, there are

two popular and proven techniques for the periodic evaluation of project status and performance [14]: earned

value analysis (EVA) and the Stage-Gate® process.

The EVA technique, which works best in conjunction with critical path scheduling techniques (CPM), compares

the value of the work scheduled with that of the work performed, at any point in time, enabling managers to

monitor schedule and cost variances in a consistent and structured manner [14]. Levine [14] describes in a

simple way the essentials of EVA and even presents a glossary of terms used in calculations.

The father of the Stage-Gate® process is Robert G. Cooper, widely recognized as a new product development

guru and a strong contributor to PPM, and though he developed the Stage-Gate® concept primarily for NPD

and technology development (which can be found in chapter 7.1 of [14]), it is frequently applied to PPM [14]. In

this process, each stage of the project life cycle is separated by a gate, which is a decision point where the

project is evaluated by a cross-functional team against pre-defined conditions for passing to the next stage.

7

2.2. Project Selection Models

Models are used to extract and deal with the relevant information about a problem, since reality is far too

complex to handle entirely [21]. Therefore, every model, however sophisticated it may be, will always

represent only a part of the reality it intends to reflect and may only yield an optimal result in its own particular

framework [21].

A project-screening model can thus be a valuable tool for an organization to help in choosing projects, mainly if

it can generate useful information in a timely and useful fashion at an acceptable cost [16]. There are various

concerns to consider when selecting a model, as well as several different types, which are approached next.

Requisites of the models 2.2.1.

According to [35], the following five aspects are the most important in a project selection model, which have

been adopted by Meredith & Mantel [21] (who added the sixth factor) and Pinto [16], who propose slightly

different definitions for the characteristics.

1. Realism: accuracy of representation of the real world [35] and in reflecting the firm’s decision

situation, objectives, limitations, risks, etc. [21].

2. Capability: ability to analyse different types of decision variables [35] and to deal with the several

factors (multiple time periods, interest rate changes, etc.) [21].

3. Flexibility: breadth of applicability to various types of projects and problems [36] and ease of

modification in response to changes in the firm’s environment [21].

4. Use: ease of comprehension and application of the model [36]. Clear, easily understood by all

organizational members and rapidly executed [16].

5. Cost: expense of setting up and using the model [35] should be inferior to the potential benefits of the

project and low relatively to the cost of the project [21].

6. Easy computerization: easily gather, store and manipulate the information with widely available

software (such as Excel®) [21].

Kerr et al. [37] published a paper on the “Key principles for developing industrially relevant strategic

technology management toolkits” (2013) that presents a vast list of “good practice” principles for technology

management tools observed by several authors, many of which apply to project selection tools in particular,

such as:

Robust (theoretically sound and reliable).

Economic, simple and practical to implement;

Integrated to other processes and tools of the business;

Flexible (adaptable to suit the particular context of the business and its environment).

8

Types of models 2.2.2.

There is an extensive amount of methods that have been used for project selection, from simple cost analysis

to integer and linear programming or more flexible methods, such as fuzzy mathematical programming [19].

Bretschneider [33] lists research on project selection dating as far as 1959, where multiple criteria and

mathematical programming methods were already used. Badri et al. [38] refer papers using the following

methods: scoring, ranking, decision trees, game-theoretic approach, Delphi technique, fuzzy logic, analytical

hierarchy process (AHP), goal programming, dynamic programming, linear 0–1 programming, quadratic

programming and non-linear programming. Dey [39] also refers goal and linear programming models, AHP and

fuzzy theory, adding the use of utility functions. Some methods can even be used together, as can be seen in

[19] and [38], which further increases the amount of possible techniques to be used for project selection.

Probably for this reason, authors usually present and discuss categories of project selection methods (such as

[16], [21] and [25]), rather than specific methods, as will also be done here later.

Tab. 1 shows several methods for project selection that have been used in different project selection decision

problems, such as construction, bid evaluation, information systems and R&D. The references to the

corresponding published papers can be found at [19].

Tab. 1: Various kinds of project selection methods (adapted from [19])

Decision method/model Decision problem

Net present value method Programming investment project selection

Cost analysis (e.g. NPV, DCF and payback) Construction project selection

Ranking and non-weighted model Project investment selection decision

Analytical hierarchy process (AHP) Industrial project selection

Multiattribute utility theory in conjunction with PRET Construction project selection

Linear and integer programming Construction project selection

Utility-theory model Bid markup decisions

Fuzzy outranking method Design evaluation

Competitive bidding strategy model Construction project selection

Multiattribute analysis in conjunction with regression models Public sector design-build project selection

Strategic classes IS project selection

Fuzzy multicriteria selection The aggregation of expert judgments

Fuzzy preference model Construction project selection

Fuzzy logic Software product selection

Mathematical programming Vendor selection decision

GREY Bid project selection

TOPSIS Bid decision making

Fuzzy stochastic Construction project selection

ELECTRE I Construction project selection

Mixed 0-1 goal programming IS project selection

Possibility theory Project investment decision

Mathematical programming R&D project selection

Analytic Network Process (ANP) R&D project selection

9

Decision method/model Decision problem

Fuzzy-logic New product development project selection

ANP Construction project selection

ANP in conjunction with Delphi and 0-1 goal programming IS project selection

Packing-multiple-boxes model R&D project selection

AHP and multiple-attribute decision-making technique Industrial project selection

Fuzzy mixed integer programming model R&D optimal portfolio selection

Chance-constrained zero-one integer programming models Random fuzzy project selection

As it can be observed, there are methods that are used for different decision problems, such as mathematical

programming, and there are decision problems that were carried out with different methods, such as

construction project selection. Therefore, it can be concluded that there is not a specific method for a certain

situation, but rather that there is a broad range of possibilities and applications. The advantages and

disadvantages of the methods should be weighted for the particular decision problem at hand in order to

choose the most appropriate one. Tab. 2 presents the explanation of some of the previous methods and

corresponding advantages and disadvantages.

Tab. 2: Comparison of project selection methods (adapted from [19])

Decision method

Method description Advantage Disadvantage

Cost analysis (e.g. NPV, DCF and payback)

It uses cost accounting and other relevant information to look for ways to cut costs and then to choose the project with the highest benefit

Controls costs and prevents waste and losses It only focuses on costs

and ignores the cost-benefit principle

Easy for the decision makers to select

Linear programming

Linear programming is a technique for optimization of a linear objective function, subject to linear equality and inequality constraints

Achieves the best outcome in a given mathematical model, given a list of requirements represented as linear equations

Perhaps no optimal solution can be found

Integer programming

A type of mathematical programming whose variables are (all or partially) integer in the problem

Greatly reduces the solution time and space

More difficult to solve than linear programming

Fuzzy logic

Fuzzy logic is a form of multi-valued logic derived from fuzzy set theory to deal with reasoning that is approximate rather than precise

It is a powerful tool to handle imprecise data

Fuzzy logic is difficult to scale to larger problems

AHP

A mathematical decision making technique that allows consideration of both qualitative and quantitative aspects of decisions

It reduces complex decisions to a series of one-on-one comparisons and then synthesizes the results

It depends on the expert's experience

The comparison and judgment process is rough, which cannot be used for high precision decision-making

10

Decision method

Method description Advantage Disadvantage

ANP It is a mathematical decision making technique similar to AHP

It can deal with the project evaluation problems

Requires large amounts of data and the decision depends on the expert's experience

Grey Target Decision

Grey Target Decision has a certain original effect on dealing with the pattern recognition problem with small samples, poor information, insufficient data and under uncertain conditions

Does not need a large number of samples and the samples do not need to have regular distribution

The optimal solution may not be the global optimization situation

It can more deeply describe the nature of things with small computational load

The results of quantitative and qualitative analysis will be consistent

It can be used for short-term or long-term predictions and is of high accuracy

Cooper et al. [25] divide the different methods into the following six categories:

1. Financial methods, such as NPV, ROI or payback period, can be used to rank-order projects against

each other or to make Go/Kill in comparison with determined acceptable levels.

2. Business strategy is used to allocate money across different types of projects. For instance, the

strategic buckets method divides the projects by buckets, that represent different dimensions (such as

type of market, type of development, product line, project magnitude, technology area, platform

types, strategic thrust or competitive needs) and distributes the money across the buckets. Then,

projects are rank-ordered within each bucket (through a financial, scoring or any other method) and

the money is spent progressively until the limit is reached for each bucket. With this method, the

spending is forced to mirror the business’s strategy [25].

3. Bubble diagrams (or portfolio maps) are used to plot projects on an X-Y plot or map (usually the

traditional risk-reward diagram [25]), categorizing them according to the quadrant they are in (e.g.:

pearls, oysters, white elephants and bread-and-butter projects).

4. Scoring models consist on scoring the projects on several criteria, for example, with {1, 2, 3, 4, 5}

scales, and then aggregating them to obtain a total score. This can be achieved by simply adding the

partial scores (unweighted scoring model) or by attributing weights to the criteria and doing a

weighted sum (weighted scoring model).

5. Check lists are a set of Yes/No questions that are answered for each project. The number of questions

answered positively can be used for prioritizing projects or to make Go/Kill decisions.

11

6. Others: all methods that do not fit in the above five categories, such as:

a. Multiple criteria without a formal scoring model;

b. Probabilities of commercial and technical success;

c. Methods that are variants or hybrids of methods comprised by the above categories;

d. Informal methods, such as decisions based on experience, top management

orders/preferences or simply intuition. Mitchell et al. [22] state that intuition can be

wonderfully effective if it derives from strong experience but surprisingly misleading in

unfamiliar situations – which is certainly the case in innovation projects – and so as much

logical structure as possible should be used to support the decision.

These categories are now further explained and some advantages and disadvantages are presented.

Financial methods 2.2.3.

According to Meredith & Mantel [21], the frequently mentioned ROI (Return On Investment), does not have a

specific method of calculation, but usually involves the NPV (Net Present Value) or the IRR (Internal Rate of

Return). Furthermore, they state that in project/investment evaluation the payback period is one of the most

commonly used, occasionally including discounted cash flows, since managers favour short payback periods in

order to minimize risk. The advantages and disadvantages of financial methods [21] are now presented:

Advantages:

1. Simple to use and understand.

2. Use readily available accounting data to determine cash flows.

3. Model output is familiar to decision makers and is usually on an “absolute” profit scale, allowing

“absolute” Go/Kill decisions.

4. Some profit models can be adjusted to account for project risk.

Disadvantages:

1. Ignore all non-monetary factors (except risk).

2. Models that do not include discounting ignore the timing of the cash flows and the time–value of

money.

3. Models that reduce cash flows to their present value are strongly biased toward the short run.

4. Payback-type models ignore cash flows beyond the payback period.

5. The internal rate of return model can result in multiple solutions.

6. Sensitive to errors in the input data for the early years of the project.

7. Non-linear, and the effects of changes/errors in the variables/ parameters are generally not

obvious to most decision makers.

8. Even though they depend on the determination of cash flows for the inputs, it is not clear exactly

how the concept of cash flow is properly defined for the purpose of evaluating projects.

12

Business strategy 2.2.4.

According to Cooper et al. [25], numerous businesses using the strategic buckets approach do not use a formal

ranking method to prioritize projects within a bucket, which indicates that strategy drives not only the

allocation by bucket but also within buckets. As a result, important indicators, such as risk or monetary factors,

might not be considered and, therefore, negatively influence the decision. Furthermore, the resulting portfolio

will possibly not have the maximum cumulative benefit for the available budget, since money can be left over

when allocating it across and within buckets.

Bubble diagrams 2.2.5.

Even though bubble diagrams appear to be more of a supporting tool than a dominant method for project

selection, their use is strongly recommended by managers, who believe that they are an effective decision tool,

yielding correct portfolio decisions [25]. Moreover, they enable managers to portray the entire portfolio in a

visual format and display portfolio balance.

Scoring models 2.2.6.

Scoring models, which differ extensively in their complexity and information requirements, have been

developed to use multiple criteria to evaluate projects, and they include the “Unweighted 0–1 Factor Scoring

Model”, equivalent to a checklist, the “Unweighted Factor Scoring Model” and the “Weighted Factor Scoring

Model” [21]. The advantages and disadvantages of scoring models [21] are now presented:

Advantages:

1. Multiple criteria can be used for evaluation and decision making, including profitability methods

and both tangible and intangible criteria.

2. Structurally simple and therefore easy to understand and use.

3. They are a direct reflection of managerial policy.

4. Easily modified according to changes in the environment or managerial policy.

5. Weighted scoring models allow to consider the relative “importance” of the criteria.

6. Allow easy sensitivity analysis, since the trade-offs between the several criteria are readily

noticeable.

Disadvantages:

1. The project score is strictly a relative measure, therefore, it does not represent its absolute value

and does not directly indicate whether or not the project should be supported.

2. Generally, scoring models are linear in form and the elements of such models are assumed to be

independent.

3. The ease of use of these models is conducive to the inclusion of a large number of criteria, most of

which have such small weights that they have little impact on the total project score.

13

4. Unweighted scoring models assume all criteria are of equal “importance”, which is almost certainly

contrary to the fact.

5. If profitability is included as criteria in the scoring model, this model will have the advantages and

disadvantages noted earlier for the profitability models themselves.

Pinto [16] states that most scoring models have important limitations, adding that they are influenced by the

relevance of the selected criteria and the accuracy of their weights, as well as by wrong interpretation and

usage of scales:

“If 3 means High and 2 means Medium, we know that 3 is better than 2, but we do

not know by how much. Furthermore, we cannot assume that the difference

between 3 and 2 is the same as the difference between 2 and 1.”

Pinto

In Chapter III a weighted scoring model is proposed, which took into account the above mentioned and

includes the construction of scales that do not fall into this mistake (i.e., the difference between two levels,

such as High and Medium, is well defined and readily noticeable through the use of value functions).

Check lists 2.2.7.

Check lists are usually employed as a Go/Kill decision tool for the individual project [25] due to the subjective

nature of the rating process [16] (using ratings such as high, medium, or low). If a check list is used to rank-

order projects, this is accomplished by simply counting the number of positive answers to obtain the final

score, which assumes that all criteria are equally “important”, almost certainly contrary to the fact [21].

Others 2.2.8.

Some examples of other methods for project selection are now presented.

Probabilistic financial models

They include decision trees and Monte Carlo simulation software or add-ons. Further explanation and

examples of these models can be found at [40].

Real options approach

The real options approach can be employed in parallel with project selection in order to reduce technological

and commercial risk [21]. According to Meredith and Mantel [21], it is based on the notion of “opportunity

cost” of an investment - the loss of potential gain from the other alternatives. If the investment in a project is

delayed, it may have a higher (or lower) value in the future, since uncertainty decreases with time. Therefore, a

project can be delayed if its NPV is expected to increase in the future and, if that prospect materializes, the

14

company will get a higher return, otherwise, the project’s value might even drop to a point that it fails the

selection process.

For a further understanding of this method, the authors propose readings on the full explanation and

applications of the real options method as a project selection tool [21], as can be found at [40].

Multicriteria decision-analysis

Multicriteria decision-analysis (MCDA) tools are used to support decision-making in problems with multiple

factors, with the purpose of helping people to make decisions according to their own understanding, through

descriptive and transparent methods [41]. They allow the incorporation of the preferences of the decision

makers and the analysis of multiple criteria, for which several aggregation methods (that provide an immediate

and simple interpretation of the project) exist, such as multiattribute value (and utility) theory and methods

that are based on it (e.g., weighted summation, analytic hierarchy process and MACBETH), outranking methods

such as ELECTRE and PROMETHEE and iterative approaches [42].

One of the most common MCDA models in the literature is the Analytical Hierarchy Process (AHP), which is

based on paired comparisons of projects and criteria [15]. This decision tool, similarly to other MCDA models,

originates more accurate alternatives and informed choices, as far as the correct criteria and weights are

developed honestly [16]. However, AHP has several reported flaws [43], such as discussed in a critical analysis

on its foundations made by Bana e Costa and Vansnick [44].

MACBETH (Measuring Attractiveness by a Category-Based Evaluation Technique) [45] differentiates itself from

other MCDA methods mainly because it requires only qualitative judgements of difference in attractiveness of

two elements at a time in order to generate value scores for the options in each criteria and weights for the

criteria [45]. This is done through a non-numerical pairwise comparison questioning mode, based on seven

semantic categories of difference in attractiveness: “no difference (indifference)”, “very weak”, “weak”,

“moderate”, “strong”, “very strong” and “extreme” [45].

There is a vast amount of literature of multicriteria methods used in project selection, including applications in

“real world” problems and organizations, such as:

Multi-Attribute Value Theory - Portuguese Public Administration [46]

MACBETH - “Rio Climate Challenge” environmental initiative [47]

PROMETHEE - Iran Telecommunication Research Centre [48]

Data Envelopment Analysis (DEA) - Bell Laboratories R&D projects [49]

Use of MCDA in transports projects [50]

For more detailed information about MCDA and its methods and applications, refer to Figueira et al. [51]

(2005), who present a collection of state-of-the-art surveys about MCDA (its foundations and techniques,

outranking methods and multiattribute utility and value theories, non-classical MCDA approaches,

multiobjective mathematical programming, applications and MCDM Software).

15

Behavioural approaches

According to Cooper et al. [15], these tools are intended to bring managers to a consensus in the project

selection decision and they are more useful at the early stage when only qualitative information is available.

Examples of these methods are the Delphi and Q-Sort techniques: Delphi is a technique for developing numeric

values that are equivalent to subjective, verbal measures of relative value [21]; the Q-Sort technique to

prioritize projects enables researchers to examine subjective perceptions of individuals on various topics and

measure the extent and nature of their agreements [31].

Popularity of the methods 2.2.9.

In 2001, Cooper et al. [25] developed a survey questionnaire answered by 205 member companies of

Washington’s Industrial Research Institute on the best practices of portfolio management. The results (in Fig. 2)

revealed that financial methods are the most popular for portfolio selection and also the most frequently used

as the dominant one, since many businesses use multiple methods.

Fig. 2: Popularity of methods employed [25]

As a result of this survey, Cooper et al. [25] noticed that the best performing companies do not give so much

emphasis to the financial models as the average and the worst performing companies do, being the business

strategy the main method applied. Furthermore, they recognise the limitations of the models and therefore

tend to use multiple methods, rather than a single one, in order to increase the information available to sustain

their decisions.

The study also identifies the scoring model as the third most used as the dominant method by the best

companies, after the business strategy and financial methods, which has the advantage of enabling the

combination of both strategic and financial criteria. Furthermore, they state that the 10.2% of the surveyed

16

companies that use the project’s financial value to rank-order projects and to make Go/Kill achieve slightly

higher performance than the businesses that use it for just one or none of these purposes.

2.3. Criteria used in Project Selection Models

According to Levine [14], even though the ROI (explained previously in Section 3.3.1 of this chapter) is one of

the primary factors for project prioritization, further aspects should be considered, such as alignment with

strategy, balance between maintenance projects and investment projects, effective allocation of resources,

probability of success and other non-financial benefits, all of which are handled throughout this work.

It is impossible to define a set of criteria suitable for all circumstances since they will strongly differ among

different companies and projects [22]. As a result, there is an endless amount of criteria referred in project

selection literature ([14], [16], [21], [22], [23], [24], [25]), which vary with the type of projects and the models

used for the selection, where the scoring models show the more extensive and vast set of criteria, usually

including more than just financial and strategic aspects. Likewise, there are different ways in which criteria can

be organized, such as by type of the criterion, which is the most common, but also by tangibility of the

criterion, as shown next.

Categories of criteria 2.3.1.

Some different ways of organizing criteria, different from the one proposed later in Chapter III Section 2.3, are

now presented. Further explanations or informations can be found in the respective author’s reference.

1. Eilat et al. [23]:

a. Financial (profitability, cash flow, cost vs. Budget, etc.).

b. Costumer (market value, stakeholder satisfaction, time to market, etc.).

c. Internal-business processes (contribution to the core competencies, mission and strategic

objectives of the organization).

d. Learning and growth (improvement on the capability of the human resources, systems and

organizational processes).

e. Uncertainty (probability of technical and commercial success, etc.).

2. Mitchell et al. [22]:

a. Volume (market size, sales potential, synergy opportunities, customer benefit, competitive

intensity in market).

b. Margin (increased margin, business cost reduction, industry / market readiness).

c. Platform for future growth (market growth, future potential).

d. Intangibles (learning potential, brand image, customer relations).

17

e. Characteristics of the product (product differentiation, sustainability of competitive, technical

challenge).

f. Skills and knowledge (market knowledge, technical capability).

g. Business processes (fit to sales and/or distribution, fit to manufacturing and/or supply chain,

finance).

h. Organisational backing (strategic fit, organisational backing).

3. Pinto [16]:

a. Risk (technical, financial, safety and quality risk, legal exposure).

b. Commercial (expected ROI, payback period, potential market share, etc.).

c. Internal operating issues (need to train employees, change in manufacturing or service

operations, etc.)

d. Additional factors (patent protection, impact on company’s image, strategic fit)

Another way of organizing the criteria can be done regarding the order of impact of the project’s cost and

benefits, similarly to what is done, for instance, in environmental disasters impact assessment. The difficulty in

the measurement/assessment of the costs and benefits increase when they change from direct to indirect and

from tangible to intangible. An example of how project criteria can be organized by their tangibility is proposed

next:

Direct and tangible (1st

order):

Direct (immediate) result of the project;

Easy measurement;

Example: net present value.

Indirect and tangible (2nd

order):

Indirect consequence of the project, which is more difficult to attribute to it;

Needs an additional tool for evaluation;

Example: complementary sales.

Intangible (3rd

order):

Intangible impacts resulting from the project that cannot be properly assessed monetarily;

Difficult to quantify;

Example: impact on brand image.

The advantage of this categorization is that it allows the company to choose different levels of complexity of

the procedure undertaken to determine the potential impacts of the projects. Naturally, if the categories are

not all considered the accuracy of the project’s benefit evaluation will be lower.

18

Intangible criteria 2.3.2.

The identification of intangible criteria related to the project should be done in order to understand the whole

scope of effects, both positive and negative, that derive from the project, not only after it is finished but also

while it is in progress. Furthermore, their impacts should be assessed whenever possible so as to determine

their impact on the company and its environment. However, this is usually difficult due to the intangible nature

of the criteria, which are difficult to quantify.

Meredith and Mantel [21] give a good example of the intangible impacts of a project: on the one hand, a

project for installing a kindergarten for the employees’ children can have substantial positive effects on their

morale and productivity; on the other hand, replacing a part of the workforce by new technology may make

sense financially but could hurt morale and productivity to a degree that it reduces profitability.

Other examples of intangible criteria are the potential for new products, new markets and learning

opportunities, brand image and customer relations [22] or regulatory, social and political impact [25].

More popular 2.3.3.

The survey questionnaire developed by Cooper et al. [25] also presented the most frequently used criteria (in

scoring models or check lists) to rank projects, as in Fig. 3. Similarly to the popularity of selection methods

presented previously (in Section 2.2.9 of this chapter), the strategic and financial aspects are the most

common.

Fig. 3: Popularity of the criteria [25]

19

Sokmen [24] presents a list of 47 different criteria used in project scoring and selection problems and several

authors using them, which can be helpful in choosing and understanding the criteria when developing the

project selection tool, in Section 3.1.1 of the next chapter.

2.4. Risk and Uncertainty

According to Mitchell et al. [22], decision theory makes a clear distinction between risk and uncertainty:

“The term risk is used when probabilities of the various possible outcomes are

known, either a priori (e.g. card games) or from objective data (e.g. health risks).

Uncertainty is used when no such objective probability data is available.”

Mitchell et al. [22]

Weber [52] places the use of “uncertainty” in strategic management into two categories: perceived

environmental uncertainty and decision-making under uncertainty, whose definitions are presented:

“Environmental uncertainty refers to the lack of complete knowledge and

unpredictability of the environment external to the organisation.”

Ilevbare [27]

“Decision-making under uncertainty, concerns choice-making circumstances where

information necessary for proper consideration of all the relevant factors associated

with a set of decision alternatives is incomplete. It is a result of insufficient

knowledge about the alternatives and their consequences, caused by limitations of

decision makers in information gathering and analysis.”

Simon [53] apud [27]

Nonetheless, the relationship between uncertainty and risk is rather ambiguous and open to different

interpretations, which is why this terms are frequently used interchangeably [27]. According to Keizer &

Halman [54], risk in innovation involves the outcome uncertainty, the level of control and the perceived impact

on the performance of the project. The outcome uncertainty of innovation activities is related to the gap

between what is available and necessary regarding knowledge, skills and experience, while the level of control

is the degree to which managers can anticipate risk factors and influence them towards the success of the

project. They conclude that an innovation issue will be perceived as “risky” if its uncertainty is high, its

controllability is low and its potential impact is high [54]. These authors [54] present the following list of 12

radical innovation risks categories, as one outcome of a case study in a company in the fast-moving consumer

sector, where 114 members of project teams where interviewed.

Product Family and Brand Positioning

Product Technology

Manufacturing Technology

20

Intellectual Property

Supply Chain and Sourcing

Consumer Acceptance and Marketing

Trade Customer

Competitors

Commercial Viability

Organization and Project Management

External

Screening and Appraisal

Risk analysis 2.4.1.

Many aspects of a project are uncertain, such as time, costs or benefits, and, even though this uncertainty may

sometimes be reduced, it usually cannot be eliminated [21]. In order to deal with this issue, risk analysis can be

applied, which provides managers with useful insight into the nature of the uncertainties that affect the project

[21]. Most models developed and referred in the literature about risk analysis rely on the determination or

estimation of probability distributions to deal with uncertainty in some parameters associated with the

decision, as in [21] and [26], using them to estimate the risk profiles or probability distributions of the

outcomes of the decision [21]. However, risk is also sometimes treated as criteria rather than as probabilities

[12].

Monte Carlo simulation is one of the most common methods used by risk analysis software, such as the

Microsoft Excel® add-ins @Risk® and Crystal Ball® of which examples of application can be found at [21] and

[40]. Despite its wide scientific use for decades, being even mentioned in the Project Management Institute’s

PMBOK (“A Guide to the Project Management Body of Knowledge”) [55], Monte Carlo simulation is not equally

established in the real practice of project management [56]. According to Kwak and Ingall [56], although this

tool is extremely powerful, it is only as good as the model it is simulating and the input information. The

authors state that in order to deal with the uncertainty associated with the information provide to the model,

detailed data and experience from previous similar projects can useful, however, these will rarely be available

in innovative projects. For further understanding the applications of Monte Carlo simulation for project

management, as well as its advantages and disadvantages, reading the article [56] is recommended.

A common tool to determine the “importance” of a risk is through a probability and impact matrix, which

combines the two dimensions of risk: probability of occurrence and impact on objectives if it occurs [55].

Ilevbare [27] presents a list of around 50 different methods and techniques for addressing uncertainty and risk,

which includes some of their characteristics (Fig. 4).

21

Fig. 4: Different risk methods [27]

Another frequent but simpler way to consider risks/uncertainty associated with projects in the selection phase

is through the probability (likelihood) of project success [26], which is more useful when probability

distributions are very hard to determine. Project success includes the probabilities of technical and commercial

success [23] explained next, which are commonly used in different methods as can be seen in [25].

Probability of technical success 2.4.2.

Cooper et al. [25] refer the following characteristics that influence the probability of technical success:

Technical gap;

Program complexity;

Existence of technological skill base;

Availability of people & facilities.

Probability of commercial success 2.4.3.

Cooper et al. [25] refer the following characteristics that influence the probability of commercial success:

Existence of a market need;

Market maturity;

Competitive intensity;

Existence of commercial applications development skills;

Commercial assumptions;

Regulatory/social/political impact.

22

Furthermore, Åstebro [57] concluded from a study of more than 500 R&D projects that the following

characteristics were excellent predictors of a project’s commercial success:

expected profitability;

technological opportunity;

development risk;

degree to which a project is appropriate for the organization.

Risk treatment 2.4.4.

Risk treatment deals with the identification and application of actions or measures that intend to mitigate risk,

which logically depend on the specific situation of the project, company and environment. ISO 31000:2009

“Risk management – Principles and guidelines” provides principles and generic guidelines on risk management

[58], as the following standard responses for risk treatment [27]:

Risk avoidance by not starting/continuing the activity that originates the risk;

Removing the risk source;

Changing the likelihood;

Changing the impact;

Sharing the risk with another party (e.g. insurance);

Retaining the risk by informed decision.

Risk mitigation strategies should thus be investigated and assessed by managers in order to fully understand

their effects and the effectiveness of the money spent, for example through cost/benefit analysis, because

even if its net effect (considering the cost of implementing the response) is an increased cost, that increase can

be justified by, for instance, the time it saves [59].

2.5. Common mistakes in Project Selection

According to Cooper et al. [25], the main reasons for ineffective portfolio management are the inexistence of

strategic criteria in project selection, resulting in efforts that do not support the company’s strategy, and of

consistent criteria for Go/Kill decisions, translating in the acceptance of low value projects and, consequently,

lack of focus in the ones with higher expected benefit. The criteria that is more used, in detriment of strategy,

is not surprisingly the financial, even though it alone does not capture the real richness of the projects [49] and

the over-reliance on financial models is commonly referred as one of the most critical mistakes made by

companies [16], [25], [42]. Cooper et al. [25] state that companies using financial methods as the dominant

portfolio selection method end up with the worst performing portfolios [25], for which they present three

reasons:

23

The sophistication of financial tools often far exceed the quality of the data inputs;

Important Go/Kill and prioritization decisions must be made at the early stages of the project,

precisely when financial data are less accurate;

Financial projections are fairly easy to manipulate, whether consciously or unconsciously.

Pinto [16] and Cooper et al. [25] also mention that the inexistence of a formal selection process means that the

selection of projects is based upon personal opinion of senior managers or politics rather than on objective

criteria, which sometimes drain financial resources until they yield satisfactory results. To avoid keep selecting

“losers”, Pinto [16] concludes, the key lies on the objectivity of the selection process, on a method that

incorporates both financial and nonfinancial criteria and on the acknowledgment that each method may only

be appropriate in certain situations, for a specific company and project circumstances.

Even considering the aforementioned, projects sometimes fail, i.e., exceed the timeline, overspend the budget

or underperform expectations [59]. According to Oracle’s White Paper on risk assessment [59], there are only

two reasons for this: overly optimistic plans and impact of external events (which should be considered during

risk analysis).

2.6. Literature Research Conclusions

The literature research allowed to understand the importance of project selection for the success of innovation

in companies but also the challenges they face in the application of project selection models. These challenges

arise because the available methods are usually too simple or excessively elaborate for most managers and

companies to understand and apply systematically [17], [18]. Furthermore, it allowed to notice that some

companies lack a formal selection process and, among the ones that do not, the most common mistakes that

lead to ineffective portfolio management are the over-reliance on financial models and the inexistence of

strategic criteria and criteria for Go/Kill decisions. It is therefore possible to conclude, as Bin et al. [18] recently

pointed out, that there is still the need for additional efforts in this field, which motivated the execution of this

work.

In this context, the following proposed methodology intends to deal with the complexity of the problem in a

less complex way, being simple to understand, apply and adapt to the specific needs of the company. At the

same time, it does not fall into the common mistakes mentioned above and approaches other areas related to

the project selection problem, such as risk analysis and resource allocation.

24

3. Methodology for Project Selection

Charvat [60] defines a methodology as a set of guidelines or steps that can be adapted and applied to a

particular situation, for example, a list of things to do in a project environment. Therefore, project managers

should not use methodologies they select just as they stand, but rather modify and tailor it in order to suit the

company’s needs [60]. Considering this, the objective of the proposed methodology is to assist companies in

selecting innovation projects to be pursued, among a set of projects proposals and in a context of limited

resources. It intends to be flexible in order to be adapted and customized to the specific needs of the company

and, at the same time, robust enough to enable its application to different types of projects and companies,

while considering the requisites for project selection tools referred in Section 2.2.1 of Chapter II. However, this

methodology is particularly helpful for companies that pursue projects with high uncertainty, such as projects

on technological innovation or new product development, due to the incorporation of risk and uncertainty in

the methodology.

The application of this methodology should be done by a team of decision makers, rather than a sole manager,

in order to eliminate the tendency to select projects by political means, power plays or emotion [14] but also to

gather a larger range of relevant knowledge and experience [22]. Even though this ensures the transparency of

the process, there can be conflicting opinions and preferences among different stakeholders and managers of

the company, since the individually optimal decision for each department is rarely collectively optimal [12]. In

some cases it might be worthwhile to execute a decision conference with the decision makers in order to

improve communication and understanding, ensuring their ownership of the model and their commitment to

the projects and company’s objectives [12]. Phillips & Bana e Costa [12] explain this social approach and its

combination with multicriteria decision analysis. The results obtained can therefore be influenced by the

number and experience of the decision makers, but also by the available data and the way it was obtained, the

choices regarding the selection of criteria, scoring the projects, among others, that is to say, the results will be

influenced by the overall effort allocated to this exercise. Nonetheless, it is a fairly simple method and does not

require complex mathematical models or formulations, for which software is sometimes recommended