Embed Size (px)

Citation preview

EurozoneEY Eurozone Forecast September 2014

AustriaBelgiumCyprusEstoniaFinlandFrance

GermanyGreeceIreland

ItalyLatvia

LuxembourgMalta

NetherlandsPortugalSlovakiaSlovenia

Spain

Spain

Portugal

France

Ireland

Finland

Estonia

Latvia

Belgium

Slovakia

Austria

Slovenia

Italy

Greece

Malta Cyprus

Netherlands

Luxembourg

Germany

Published in collaboration with

Outlook for Slovakia

Economy to grow by 2.3% this year and accelerate in 2015

Spain

Portugal

France

Ireland

Finland

Estonia

Latvia

Belgium

Slovakia

Austria

Slovenia

Italy

Greece

Malta Cyprus

Netherlands

Luxembourg

Germany

1EY Eurozone Forecast September 2014 | Slovakia

Highlights

• We expect GDP growth in Slovakia to accelerate to 2.3% this year, after sluggish expansion in 2013, as fiscal policy is relaxed and foreign demand picks up. Economic activity should accelerate even further in 2015.

• Government debt rose above 55% of GDP in 2013. As a result, the Government should freeze its spending in 2015. This will be a drag on growth next year, but the effect will be mitigated by lower real interest rates and strong demand for Slovakia’s exports.

• High unemployment will be a drag on domestic demand in 2014, as unemployment is unlikely to fall significantly until GDP grows at a sustained pace of above 3%, which will not be until 2015. Moreover, model changes at key car plants have prevented exporters from gaining market share this year.

• GDP growth should accelerate to 3.2% in 2015, as employment picks up and car production rises. We expect the unemployment rate to decline significantly to 12.9% in 2015 from 13.8% this year.

• Inflation remained very low in H1 2014, and was in negative territory most months. It should start to pick up from Q3 due to base effects (as prices fell in H2 2013) as well as rising inflation in the Czech Republic and in Slovakia’s other key Eurozone trading partners. We expect inflation to accelerate to 1.6% in 2015, as the effect of earlier electricity price cuts disappears and imported inflation rises.

• Risks to our forecast have become more balanced than in June. The European Central Bank (ECB) refinancing program might have a more significant effect on lending than expected, lifting growth in the Eurozone and driving up demand for Slovakia’s exports. However, any further escalation of the Ukraine conflict could restrict the supply of gas to the country and reduce demand in its trading partners.

GDP growth

2014

2.3% GDP growth

2015

3.2%

Unemployment

2014

13.8%

Consumer prices

2014

0.1%

2 EY Eurozone Forecast September 2014 | Slovakia

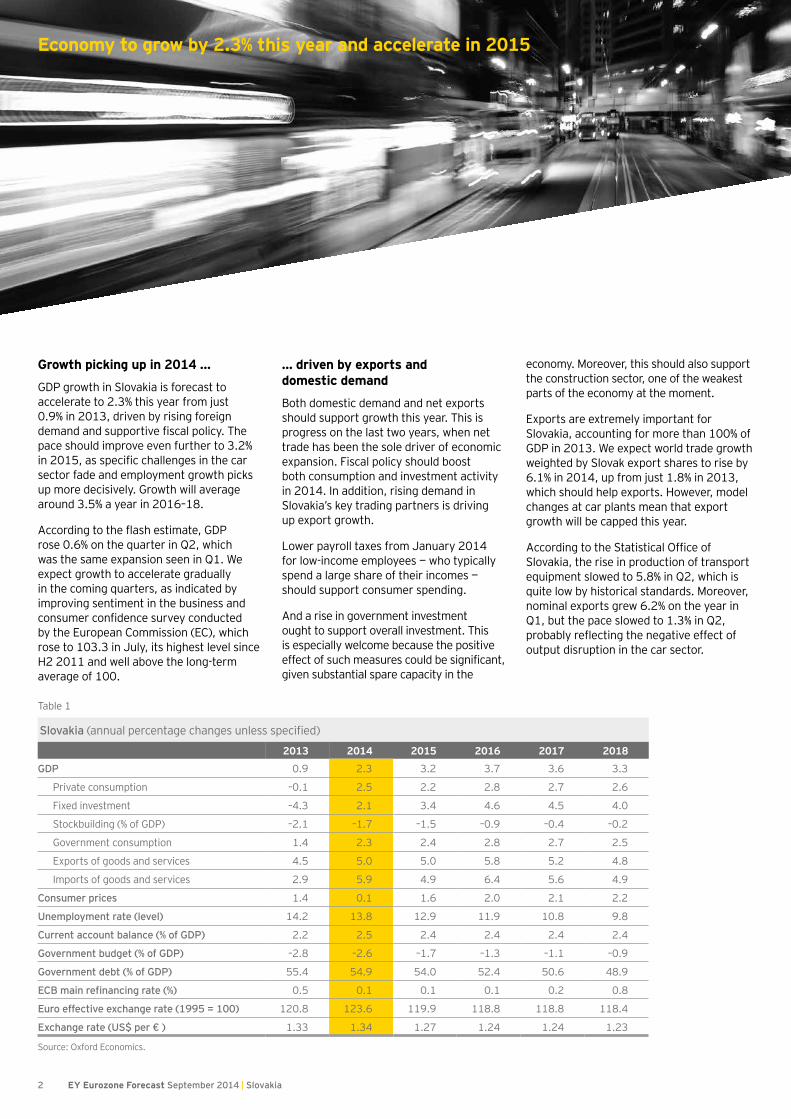

Economy to grow by 2.3% this year and accelerate in 2015

Growth picking up in 2014 …

GDP growth in Slovakia is forecast to accelerate to 2.3% this year from just 0.9% in 2013, driven by rising foreign demand and supportive fiscal policy. The pace should improve even further to 3.2% in 2015, as specific challenges in the car sector fade and employment growth picks up more decisively. Growth will average around 3.5% a year in 2016–18.

According to the flash estimate, GDP rose 0.6% on the quarter in Q2, which was the same expansion seen in Q1. We expect growth to accelerate gradually in the coming quarters, as indicated by improving sentiment in the business and consumer confidence survey conducted by the European Commission (EC), which rose to 103.3 in July, its highest level since H2 2011 and well above the long-term average of 100.

… driven by exports and domestic demand

Both domestic demand and net exports should support growth this year. This is progress on the last two years, when net trade has been the sole driver of economic expansion. Fiscal policy should boost both consumption and investment activity in 2014. In addition, rising demand in Slovakia’s key trading partners is driving up export growth.

Lower payroll taxes from January 2014 for low-income employees — who typically spend a large share of their incomes — should support consumer spending.

And a rise in government investment ought to support overall investment. This is especially welcome because the positive effect of such measures could be significant, given substantial spare capacity in the

economy. Moreover, this should also support the construction sector, one of the weakest parts of the economy at the moment.

Exports are extremely important for Slovakia, accounting for more than 100% of GDP in 2013. We expect world trade growth weighted by Slovak export shares to rise by 6.1% in 2014, up from just 1.8% in 2013, which should help exports. However, model changes at car plants mean that export growth will be capped this year.

According to the Statistical Office of Slovakia, the rise in production of transport equipment slowed to 5.8% in Q2, which is quite low by historical standards. Moreover, nominal exports grew 6.2% on the year in Q1, but the pace slowed to 1.3% in Q2, probably reflecting the negative effect of output disruption in the car sector.

Table 1

Slovakia (annual percentage changes unless specified)

2013 2014 2015 2016 2017 2018

GDP 0.9 2.3 3.2 3.7 3.6 3.3

Private consumption –0.1 2.5 2.2 2.8 2.7 2.6

Fixed investment –4.3 2.1 3.4 4.6 4.5 4.0

Stockbuilding (% of GDP) –2.1 –1.7 –1.5 –0.9 –0.4 –0.2

Government consumption 1.4 2.3 2.4 2.8 2.7 2.5

Exports of goods and services 4.5 5.0 5.0 5.8 5.2 4.8

Imports of goods and services 2.9 5.9 4.9 6.4 5.6 4.9

Consumer prices 1.4 0.1 1.6 2.0 2.1 2.2

Unemployment rate (level) 14.2 13.8 12.9 11.9 10.8 9.8

Current account balance (% of GDP) 2.2 2.5 2.4 2.4 2.4 2.4

Government budget (% of GDP) –2.8 –2.6 –1.7 –1.3 –1.1 –0.9

Government debt (% of GDP) 55.4 54.9 54.0 52.4 50.6 48.9

ECB main refinancing rate (%) 0.5 0.1 0.1 0.1 0.2 0.8

Euro effective exchange rate (1995 = 100) 120.8 123.6 119.9 118.8 118.8 118.4

Exchange rate (US$ per € ) 1.33 1.34 1.27 1.24 1.24 1.23

Source: Oxford Economics.

3EY Eurozone Forecast September 2014 | Slovakia

Table 2

Forecast for Slovakia by sector (annual percentage changes in gross added value) 2013 2014 2015 2016 2017 2018

GDP 0.9 2.3 3.2 3.7 3.6 3.3

Manufacturing 3.3 5.8 5.5 4.3 3.5 3.4

Agriculture 0.8 0.0 2.4 3.1 3.0 2.7

Construction –8.5 8.0 4.5 4.2 4.0 3.8

Utilities –10.4 –1.9 1.5 2.9 3.1 3.1

Trade 2.4 0.3 3.0 4.3 4.5 4.1

Financial and business services 3.3 1.3 2.4 3.1 3.1 2.7

Communications 2.6 1.8 2.4 4.0 3.7 3.3

Non-market services –1.8 –0.3 1.5 2.8 3.0 2.7

Source: Oxford Economics.

Car production and lower unemployment will support growth from 2015 …

Car production should pick up in 2015 when model changes are complete. Given the importance of the car sector to the country’s economy, Slovakia’s exports should grow by 5% next year. This is a roughly similar level to 2014, despite softer demand growth in key trading partners. However, capacity constraints at key car plants will prevent exporters from gaining significant market share in 2015–18.

In 2013, Slovakia’s 3 main car plants produced 987,718 cars, very close to their combined capacity limit of 1 million a year. Each plant exports almost all of its production, mainly to Eurozone countries. With no significant expansion projects in the pipeline, output in the car sector is likely to be capped throughout the forecasting period.

High unemployment will also be a drag on growth this year. We expect the unemployment rate (on the International Labour Organization definition) to decline significantly to 12.9% in 2015 from 13.8% in 2014, as GDP should grow at a level above 3% next year. This should support private consumption and households’ investment in dwellings, both of which were weak in 2013.

Hours of work are rising, approaching the level where hiring is likely to start improving more decisively. Moreover, the vacancy rate increased to 0.7 in Q1 this year, the highest rate since 2010. These two factors indicate that unemployment should start falling more decisively from 2015.

Finally, we expect credit conditions for corporate loans to improve in 2015 after the results of the ECB’s asset quality review are signaled this October. Moreover, the targeted longer-term refinancing operations (TLTROs) recently announced by the ECB should support the expansion of corporate loans in 2015.

… but fiscal austerity will drag on growth next year

Government debt (on the Maastricht definition) rose above 55% of GDP in 2013. As a result, under the budget-discipline law, the Government will have to cut its spending in 2015 by about 0.3% of GDP — more than we had originally expected. However, this is unlikely to derail the economy’s recovery, as long as demand in the rest of the Eurozone continues to strengthen. Moreover, the likely fiscal adjustment will be modest compared to that in 2013, when spending fell sharply and the Government raised taxes significantly.

Figure 1Real GDP growth

Source: Oxford Economics.

% year

–6

–4

–2

0

2

4

6

8

10

12

2000 2002 2004 2006 2008 2010 2012 2014 2016 2018

Slovakia

Eurozone

Forecast

Figure 2Export demand and goods export growth

Source: Oxford Economics

% year

–25

–20

–15

–10

–5

0

5

10

15

20

25

2000 2002 2004 2006 2008 2010 2012 2014 2016 2018

Export demand

Goods export growth

Forecast

4 EY Eurozone Forecast September 2014 | Slovakia

Economy to grow by 2.3% this year and accelerate in 2015

Figure 3Unemployment rate

Source: Oxford Economics.

% (seasonally adjusted rate, Eurostat)

7

9

11

13

15

17

19

21

2000 2002 2004 2006 2008 2010 2012 2014 2016 2018

Forecast

Figure 4Inflation

Source: Oxford Economics; World Bank.

% year

–2

0

2

4

6

8

10

12

14

16

18

2000 2002 2004 2006 2008 2010 2012 2014 2016 2018

Forecast

In addition, higher inflation in 2015 will reduce real interest rates, providing a further offset to the fiscal squeeze. As a result of these factors, we expect GDP to grow by 3.2% in 2015, down from our June forecast of 3.5%.

Inflation will remain very low …

Inflation has been negative so far in 2014, due to weak price pressures in key trading partners, substantial spare output capacity and cuts in regulated prices at the beginning of the year. Housing, electricity and other fuel costs account for almost 28% of the total consumer basket and are likely to affect other prices.

We expect inflation to pick up gradually in the coming months due to base effects (as prices fell in the second half of 2013) and rising prices in Slovakia’s key trading partners, the Czech Republic and the Eurozone.

As a result, consumer price inflation will average just 0.1% in 2014, before rising to 1.6% in 2015, when the effect of the electricity price cut disappears. Moreover, it is likely to remain low in 2016–18 as well, at just over 2% on average, given significant spare capacity in the economy that will take several years to use up.

… but it is more likely to support than undermine growth

Inflation expectations, as measured by EC surveys, are not in deflationary territory yet. Moreover, judging from data on retail sales, consumption of durable goods continued to improve in the first half of 2014.

As a result, we believe that a situation in which households postpone their consumption — mainly of durable goods — will be avoided in Slovakia this year as inflation expectations remain anchored. Low inflation should support the real incomes of households and hence private consumption this year.

Risks are more balanced

Risks to our forecast have become more balanced than in our June report. An escalation of the conflict between Russia and Ukraine could restrict the supply of gas to Slovakia and reduce demand in its key trading partners. This might significantly hurt economic growth. Moreover, Russia remains an important trade partner for Slovakia. Any Russian ban on car imports would affect activity at Slovakia’s car plants.

On a more positive note, an upside risk comes from the ECB’s TLTRO program, which might lift the Eurozone economy. Expansion in Germany — one of Slovakia’s key trading partners — could surprise on the upside, which would see Slovak exports grow more decisively. Given the export sector’s importance for the economy, this would have a positive spillover effect on domestic demand.

About EYEY is a global leader in assurance, tax, transaction and advisory services. The insights and quality services we deliver help build trust and confidence in the capital markets and in economies the world over. We develop outstanding leaders who team to deliver on our promises to all of our stakeholders. In so doing, we play a critical role in building a better working world for our people, for our clients and for our communities.

EY refers to the global organization, and may refer to one or more, of the member firms of Ernst & Young Global Limited, each of which is a separate legal entity. Ernst & Young Global Limited, a UK company limited by guarantee, does not provide services to clients. For more information about our organization, please visit ey.com.

© 2014 EYGM Limited. All Rights Reserved.

EYG no. AU2629

EMEIA Marketing Agency 1001401

ED None

In line with EY’s commitment to minimize its impact on the environment, this document has been printed on paper with a high recycled content.

This material has been prepared for general informational purposes only and is not intended to be relied upon as accounting, tax, or other professional advice. Please refer to your advisors for specific advice.

ey.com

About Oxford EconomicsOxford Economics was founded in 1981 to provide independent forecasting and analysis tailored to the needs of economists and planners in government and business. It is now one of the world’s leading providers of economic analysis, advice and models, with over 700 clients including international organizations, government departments and central banks around the world, and a large number of multinational blue-chip companies across the whole industrial spectrum.

Oxford Economics commands a high degree of professional and technical expertise, both in its own staff of over 80 professional economists based in Oxford, London, Belfast, Paris, the UAE, Singapore, New York and Philadelphia, and through its close links with Oxford University and a range of partner institutions in Europe and the US. Oxford Economics’ services include forecasting for 200 countries, 100 sectors, and 3,000 cities and sub-regions in Europe and Asia; economic impact assessments; policy analysis; and work on the economics of energy and sustainability.

The forecasts presented in this report are based on information obtained from public sources that we consider to be reliable but we assume no liability for their completeness or accuracy. The analysis presented in this report is for information purposes only and Oxford Economics does not warrant that its forecasts, projections, advice and/or recommendations will be accurate or achievable. Oxford Economics will not be liable for the contents of any of the foregoing or for the reliance by readers on any of the foregoing.

EY | Assurance | Tax | Transactions | Advisory