Embed Size (px)

Citation preview

The European Commission’s Directorate–General for Economic and Financial Affairsmonitors activity in the field of mergers and acquisitions, with particular reference tooperations involving EU enterprises. The present issue of Supplement A is the sixth inthe series dealing with the subject.

Part A of this issue gives an overview of the evolution of mergers from 1991 to 1999,focusing on the period 1998–1999. Part B compares M&A activity in the EU and theU.S.A. and Part C summarises the largest deals carried out in 1998 and 1999. Lastly,Part D reports on Commission control of mergers. A box describes the sources of in-formation and presents the conventions used.

Previous editions have used data from the AMDATA data base, which has been discon-tinued. The statistical data required for this issue have therefore been drawn from theSDC M&A data base. SDC provides a somewhat more complete coverage than AMDA-TA, particularly in respect of national operations and transactions in the service sector.The average annual number of transactions involving EU firms is about 27% greaterin the SDC data base than in AMDATA and, in percentage terms, the year–to–yearfluctuations are less marked.

1. In 1998, the number of mergers and acquisitions involving an enterprise of theEuropean Union was over 10 000. This rose to nearly 12 800 in 1999, an increaseof 28%. The U.K. accounts for the largest share of M&A activity in the EU, followedby Germany, France and the Netherlands.

2. The distribution of aggregate M&A activity between Member States correlatesclosely with the stock market capitalisation of domestic firms. The latter variablereflects not only the size of the economy but also the extent to which companies makeuse of equity financing. Other factors do not seem to have a strong influence on therelative levels of M&A activity in different countries. Our analysis reveals no simpleexplanation of the evolution of the level of M&A activity over time during the 1990s.

Supplement AEconomic trendsNo 5/6 – 2000

In this number :Mergers and acquisitions

MERGERS AND ACQUISITIONS

SUMMARY AND MAIN POINTS

http://europa.eu.int/comm/economy_finance

– 2 –

3. Analysis suggests that the recent acceleration in thegrowth of M&A activity may be partly attributable tomonetary union. However, the evidence is far from con-clusive.

4. In 1998–99, National transactions accounted for 56%of all operations involving EU companies, Communityoperations for 15% and International transactions for29%. By comparison with the period 1996–1997, therehas been a fall in the shares of National transactionsand of International operations targeting EU firms,while the share of Community operations increasedslightly. There was a particularly sharp upward turn inInternational operations with a Community bidder (i.e.acquisitions of non–EU companies by EU enterprises).Over the 1990s, these operations have followed agrowth path which is very different from that of theother types of transaction.

5. There were 1455 Community operations in 1998 and1920 in 1999. The value of these operations reached90 billion in 1998 and climbed very steeply to 420

billion in 1999. A single transaction (Vodafone Air-Touch/Mannesmann) accounted for nearly half of the1999 value. In terms of geographical breakdown, prox-imity and traditional economic links are particularlyimportant for Community mergers and acquisitions,coupled with the size of the national economies.

6. The number of International operations in 1998 was3053. This rose to 3652 in 1999, the increase being en-tirely attributable to acquisitions made by EU firmsoutside the Community. The value of internationaloperations reached 313 billion in 1998 and rose to396 billion in the following year. 1999 was an excep-

tional year as far as International operations are con-cerned. The number of extra–EU acquisitions made byEU firms in that year vastly exceeded the number of ac-quisitions made by non–EU companies within theCommunity (2221, compared to 1431). Only once be-fore, in 1995, has the number of outward transactionsbeen greater than the number of inward transactionsand then the margin was very small (1119 against1113).

7. As in the period 1996–1997, the U.S.A. heads the listof both bidders and targets for International M&A in-volving Community firms, followed by Switzerland.Norway, Australia and Canada also figure prominentlyin the ranking of both bidders and targets. The Central

and Eastern European Countries, especially Poland,account for a large and increasing proportion of extra–EU acquisitions made by EU firms. Amongst EUcountries, the U.K. accounts for by far the largestnumber of international operations, as both target andbidder.

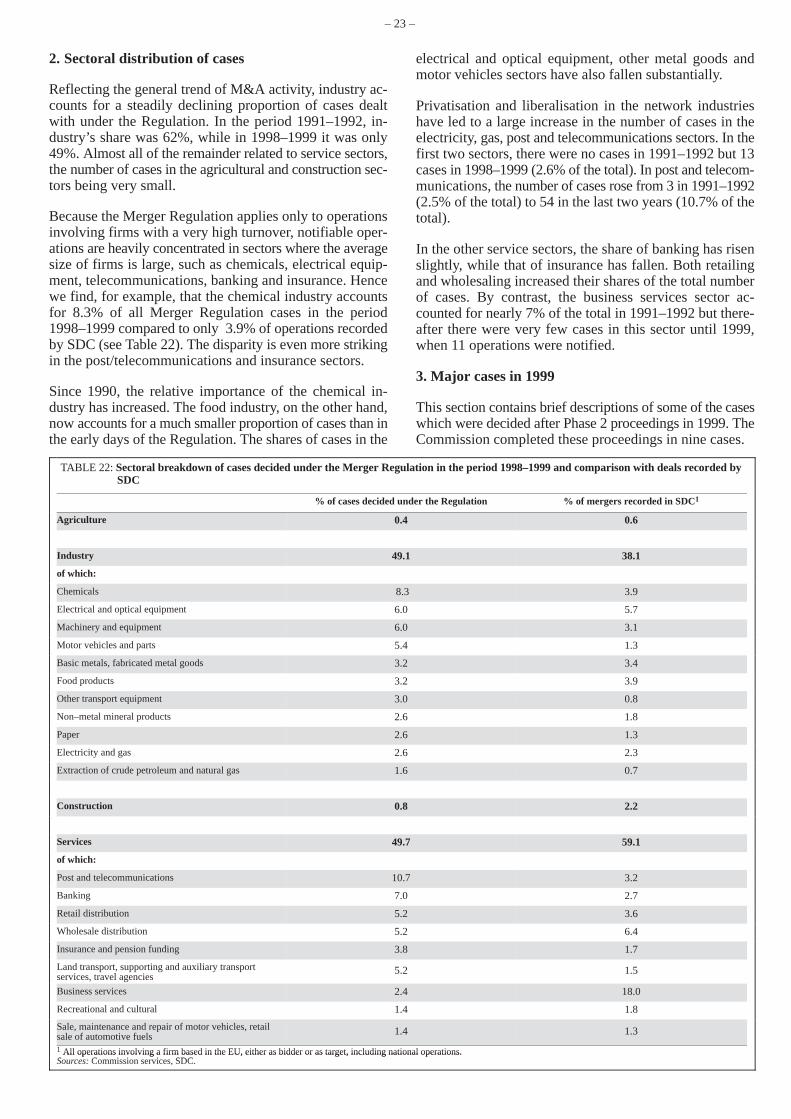

8. Over the 1990s, the number of operations (cross–bor-der and national) in industry has shown a slight down-ward trend, while the number of transactions in the ser-vices sectors has increased considerably, particularlyin 1998–1999. Amongst the individual two–digit SICsectors, the level of activity over the period 1998–1999was highest in the business services sector, followed byreal estate and wholesale distribution. M&A activity inbusiness services more than doubled in 1998–1999,compared to the previous two years.

9. A comparison with the U.S.A. shows remarkable simi-larities in the trends, sectoral structure and geographicorientation of M&A activity in the 1990s. These simila-rities can be attributed to a number of common un-derlying factors, such as the progressive lowering ofbarriers to international trade and rapid technologicalchange in the telecommunications and InformationTechnology sectors. In the financial services sector, thebreaking down of barriers between EU Member Stateshas been paralleled by the abolition of restrictions oninter–state banking in the U.S.A., while changes in theregulation of network industries have triggered re-structuring on both sides of the Atlantic. However, thegrowth of M&A activity in the 1990s has generally beenless strong and consistent in the EU than in the U.S.A.,although the growth rate was higher in the EU than inthe U.S.A. over the last two years.

10. 1228 operations have been notified to the Commissionunder the Merger regulation since its entry into forcein 1990. In 58 cases the Commission deemed that theoperation raised serious doubts as to its compatibilitywith the common market and undertook an in–depth(Phase 2) investigation. On completion of these inves-tigations, eleven mergers were authorised withoutconditions, eleven were forbidden and thirty–six wereauthorised subject to the fulfilment of undertakingsaimed at resolving competition problems identified bythe Commission. In 1998 and 1999, three mergers wereprohibited: two German operations in the field of digi-tal pay–TV and a merger between two U.K. tour oper-ating companies.

– 3 –

Box 1: Sources of statistical information and conventions

A variety of information sources are available to moni-tor mergers and acquisitions activity. The press plays akey role, together with other sources such as companyreports, announcements in official publications etc.Data base providers have established a network of ex-perts in several countries and devote considerable effortto collecting and cross–referencing information. Theseproviders include, for example, KPMG and SDC M&A.

There are certain differences between bases. Clearly,each provider endeavours to collect and present in-formation which is as full as possible, but the very natureof the information makes this somewhat arbitrary.Whereas major operations affecting publicly listedcompanies are often officially published and widely re-ported in the press, the large number of purchases ofsmaller or unlisted companies are more difficult to de-tect. In addition, subjective assessments are often inevi-table, e.g. as regards the date and sectoral classificationof a merger and acquisition operation. Providers mustalso make choices in defining the scope of their base:KPMG considers only cross–border operations butcovers the three main types of operation: outright ac-quisition, minority participation and joint ventures,whereas SDC M&A mainly considers acquisitions, butincludes purely domestic operations. Minimum thresh-olds are set for covering an operation. This can be a limiton turnover, transaction value, or percentage of sharestransferred.

Choices had to be made when drafting this SupplementA. Conventions were also established: they are listedbelow in italics, and apply throughout this issue unlessotherwise indicated.

We now use SDC M&A

In previous editions we used data from the AMDATAdata base of Acquisitions Monthly, which was takenover in 1998 by Thomson Financial Securities. SinceAMDATA was discontinued, we now use Thomson’sSDC data base. This base is very comprehensive. Itcovers all acquisitions of shareholdings of 5% or moreand with a value over US$1 million or an unknownvalue. The main differences between SDC and AMDA-TA are that the former has a more complete coverage ofdomestic transactions and operations in the service sec-tor. As a result, the average annual number of transac-tions involving EU companies is about 27% greater inthe SDC data base than in AMDATA and year–to–yearfluctuations are somewhat less marked in percentageterms, although they follow a similar pattern.

We take account of both completed and pending deals

Most pending deals are eventually completed but it issometimes difficult to obtain confirmation of comple-tion. The exclusion of pending deals would therefore

lead to some underestimation. In order to reduce themargin of error, we include pending deals in the data.

We consider only operations resulting in the change ofcontrol of an enterprise.

We equate change of control of an enterprise withmergers and acquisitions (M&A). Acquisitions of ma-jority holdings, which are clearly identified in SDCM&A, usually confer control. We include both mergersand acquisitions in this type of operation. Mergers arenot considered as a separate category, although theyconsist of two equal partners getting together and makethe distinction between purchaser and target enterprisedevoid of meaning.

We consider the target’s main activity.

Companies, and not only large conglomerates, are oftentoo diversified to be classified in a single sector. We usethe classification by main sector as proposed by the database. In general, as the target is smaller than the bidder,its main activity is usually better defined, and that activ-ity is probably the one which interests the bidder. That istherefore the sector in which the effects of an M&A willbe the greatest. The sectoral classification used by SDCM&A is an old version of the U.S. Standard IndustrialClassification (SIC). The numbering and, in some re-spects, the grouping of sectors differs from both theCommunity’s NACE classification and the U.N.’s ISICsystem.

– 4 –

PART A: TRENDS SINCE 1990

1. Total number of operations

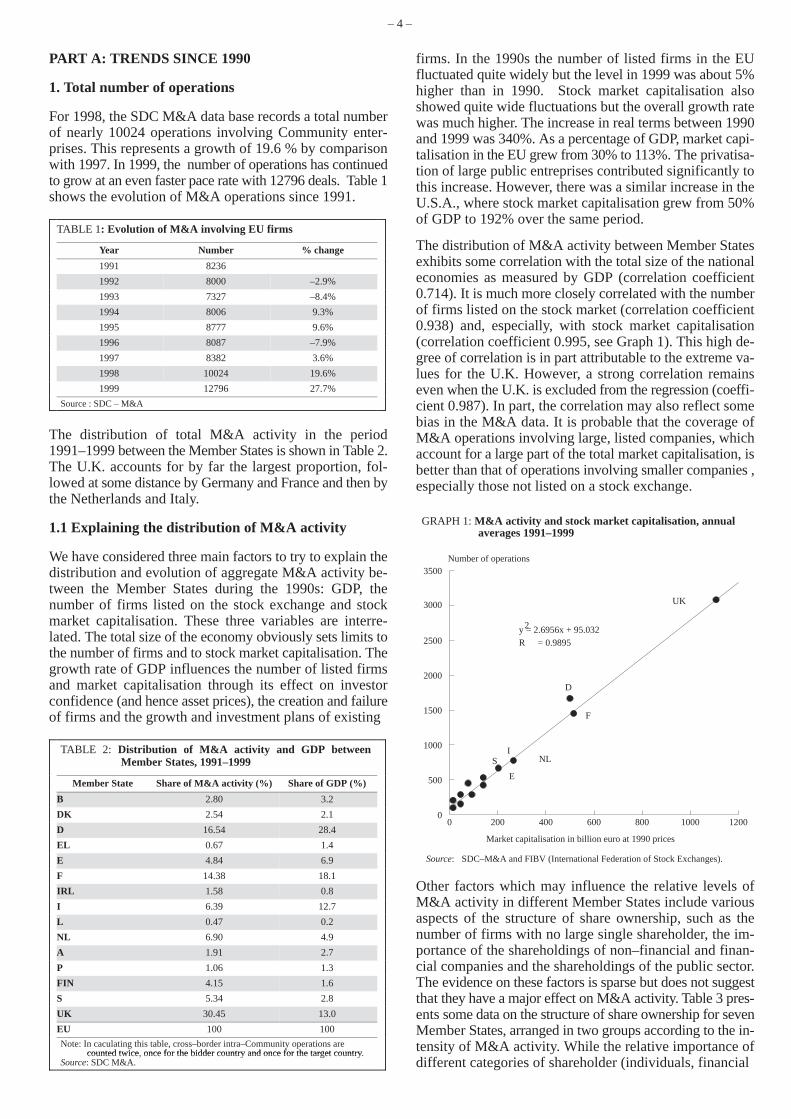

For 1998, the SDC M&A data base records a total numberof nearly 10024 operations involving Community enter-prises. This represents a growth of 19.6 % by comparisonwith 1997. In 1999, the number of operations has continuedto grow at an even faster pace rate with 12796 deals. Table 1shows the evolution of M&A operations since 1991.

TABLE 1: Evolution of M&A involving EU firms

Year Number % change

1991 8236

1992 8000 –2.9%

1993 7327 –8.4%

1994 8006 9.3%

1995 8777 9.6%

1996 8087 –7.9%

1997 8382 3.6%

1998 10024 19.6%

1999 12796 27.7%

Source : SDC – M&A

The distribution of total M&A activity in the period1991–1999 between the Member States is shown in Table 2.The U.K. accounts for by far the largest proportion, fol-lowed at some distance by Germany and France and then bythe Netherlands and Italy.

1.1 Explaining the distribution of M&A activity

We have considered three main factors to try to explain thedistribution and evolution of aggregate M&A activity be-tween the Member States during the 1990s: GDP, thenumber of firms listed on the stock exchange and stockmarket capitalisation. These three variables are interre-lated. The total size of the economy obviously sets limits tothe number of firms and to stock market capitalisation. Thegrowth rate of GDP influences the number of listed firmsand market capitalisation through its effect on investorconfidence (and hence asset prices), the creation and failureof firms and the growth and investment plans of existing

TABLE 2: Distribution of M&A activity and GDP betweenMember States, 1991–1999

Member State Share of M&A activity (%) Share of GDP (%)

B 2.80 3.2

DK 2.54 2.1

D 16.54 28.4

EL 0.67 1.4

E 4.84 6.9

F 14.38 18.1

IRL 1.58 0.8

I 6.39 12.7

L 0.47 0.2

NL 6.90 4.9

A 1.91 2.7

P 1.06 1.3

FIN 4.15 1.6

S 5.34 2.8

UK 30.45 13.0

EU 100 100

Note: In caculating this table, cross–border intra–Community operations arecounted twice once for the bidder country and once for the target countrycounted twice, once for the bidder country and once for the target country.

Source: SDC M&A.

firms. In the 1990s the number of listed firms in the EUfluctuated quite widely but the level in 1999 was about 5%higher than in 1990. Stock market capitalisation alsoshowed quite wide fluctuations but the overall growth ratewas much higher. The increase in real terms between 1990and 1999 was 340%. As a percentage of GDP, market capi-talisation in the EU grew from 30% to 113%. The privatisa-tion of large public entreprises contributed significantly tothis increase. However, there was a similar increase in theU.S.A., where stock market capitalisation grew from 50%of GDP to 192% over the same period.

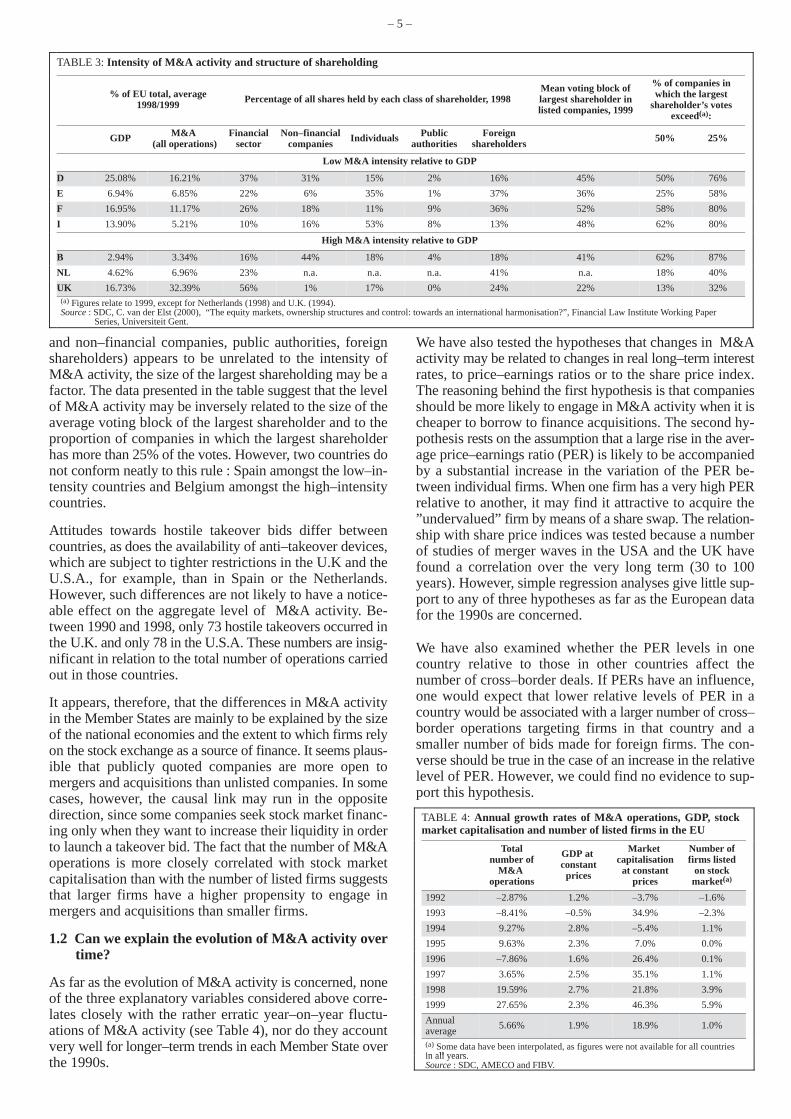

The distribution of M&A activity between Member Statesexhibits some correlation with the total size of the nationaleconomies as measured by GDP (correlation coefficient0.714). It is much more closely correlated with the numberof firms listed on the stock market (correlation coefficient0.938) and, especially, with stock market capitalisation(correlation coefficient 0.995, see Graph 1). This high de-gree of correlation is in part attributable to the extreme va-lues for the U.K. However, a strong correlation remainseven when the U.K. is excluded from the regression (coeffi-cient 0.987). In part, the correlation may also reflect somebias in the M&A data. It is probable that the coverage ofM&A operations involving large, listed companies, whichaccount for a large part of the total market capitalisation, isbetter than that of operations involving smaller companies ,especially those not listed on a stock exchange.

GRAPH 1: M&A activity and stock market capitalisation, annualaverages 1991–1999

Source: SDC–M&A and FIBV (International Federation of Stock Exchanges).

Number of operations

Market capitalisation in billion euro at 1990 prices

y = 2.6956x + 95.032R = 0.9895

0 200 400 600 800 1000 12000

500

1000

1500

2000

2500

3000

3500

UK

D

F

NLI

2

E

S

Other factors which may influence the relative levels ofM&A activity in different Member States include variousaspects of the structure of share ownership, such as thenumber of firms with no large single shareholder, the im-portance of the shareholdings of non–financial and finan-cial companies and the shareholdings of the public sector.The evidence on these factors is sparse but does not suggestthat they have a major effect on M&A activity. Table 3 pres-ents some data on the structure of share ownership for sevenMember States, arranged in two groups according to the in-tensity of M&A activity. While the relative importance ofdifferent categories of shareholder (individuals, financial

– 5 –

TABLE 3: Intensity of M&A activity and structure of shareholding

% of EU total, average1998/1999

Percentage of all shares held by each class of shareholder, 1998Mean voting block oflargest shareholder inlisted companies, 1999

% of companies inwhich the largest

shareholder’s votesexceed(a):

GDP M&A (all operations)

Financialsector

Non–financialcompanies

Individuals Publicauthorities

Foreignshareholders

50% 25%

Low M&A intensity relative to GDP

D 25.08% 16.21% 37% 31% 15% 2% 16% 45% 50% 76%

E 6.94% 6.85% 22% 6% 35% 1% 37% 36% 25% 58%

F 16.95% 11.17% 26% 18% 11% 9% 36% 52% 58% 80%

I 13.90% 5.21% 10% 16% 53% 8% 13% 48% 62% 80%

High M&A intensity relative to GDP

B 2.94% 3.34% 16% 44% 18% 4% 18% 41% 62% 87%

NL 4.62% 6.96% 23% n.a. n.a. n.a. 41% n.a. 18% 40%

UK 16.73% 32.39% 56% 1% 17% 0% 24% 22% 13% 32%(a) Figures relate to 1999, except for Netherlands (1998) and U.K. (1994).Source : SDC, C. van der Elst (2000), “The equity markets, ownership structures and control: towards an international harmonisation?”, Financial Law Institute Working Paper

Series, Universiteit Gent.

and non–financial companies, public authorities, foreignshareholders) appears to be unrelated to the intensity ofM&A activity, the size of the largest shareholding may be afactor. The data presented in the table suggest that the levelof M&A activity may be inversely related to the size of theaverage voting block of the largest shareholder and to theproportion of companies in which the largest shareholderhas more than 25% of the votes. However, two countries donot conform neatly to this rule : Spain amongst the low–in-tensity countries and Belgium amongst the high–intensitycountries.

Attitudes towards hostile takeover bids differ betweencountries, as does the availability of anti–takeover devices,which are subject to tighter restrictions in the U.K and theU.S.A., for example, than in Spain or the Netherlands.However, such differences are not likely to have a notice-able effect on the aggregate level of M&A activity. Be-tween 1990 and 1998, only 73 hostile takeovers occurred inthe U.K. and only 78 in the U.S.A. These numbers are insig-nificant in relation to the total number of operations carriedout in those countries.

It appears, therefore, that the differences in M&A activityin the Member States are mainly to be explained by the sizeof the national economies and the extent to which firms relyon the stock exchange as a source of finance. It seems plaus-ible that publicly quoted companies are more open tomergers and acquisitions than unlisted companies. In somecases, however, the causal link may run in the oppositedirection, since some companies seek stock market financ-ing only when they want to increase their liquidity in orderto launch a takeover bid. The fact that the number of M&Aoperations is more closely correlated with stock marketcapitalisation than with the number of listed firms suggeststhat larger firms have a higher propensity to engage inmergers and acquisitions than smaller firms.

1.2 Can we explain the evolution of M&A activity overtime?

As far as the evolution of M&A activity is concerned, noneof the three explanatory variables considered above corre-lates closely with the rather erratic year–on–year fluctu-ations of M&A activity (see Table 4), nor do they accountvery well for longer–term trends in each Member State overthe 1990s.

We have also tested the hypotheses that changes in M&Aactivity may be related to changes in real long–term interestrates, to price–earnings ratios or to the share price index.The reasoning behind the first hypothesis is that companiesshould be more likely to engage in M&A activity when it ischeaper to borrow to finance acquisitions. The second hy-pothesis rests on the assumption that a large rise in the aver-age price–earnings ratio (PER) is likely to be accompaniedby a substantial increase in the variation of the PER be-tween individual firms. When one firm has a very high PERrelative to another, it may find it attractive to acquire the”undervalued” firm by means of a share swap. The relation-ship with share price indices was tested because a numberof studies of merger waves in the USA and the UK havefound a correlation over the very long term (30 to 100years). However, simple regression analyses give little sup-port to any of three hypotheses as far as the European datafor the 1990s are concerned.

We have also examined whether the PER levels in onecountry relative to those in other countries affect thenumber of cross–border deals. If PERs have an influence,one would expect that lower relative levels of PER in acountry would be associated with a larger number of cross–border operations targeting firms in that country and asmaller number of bids made for foreign firms. The con-verse should be true in the case of an increase in the relativelevel of PER. However, we could find no evidence to sup-port this hypothesis.

TABLE 4: Annual growth rates of M&A operations, GDP, stockmarket capitalisation and number of listed firms in the EU

Totalnumber of

M&A operations

GDP at constantprices

Market capitalisationat constant

prices

Number offirms listed

on stockmarket(a)

1992 –2.87% 1.2% –3.7% –1.6%

1993 –8.41% –0.5% 34.9% –2.3%

1994 9.27% 2.8% –5.4% 1.1%

1995 9.63% 2.3% 7.0% 0.0%

1996 –7.86% 1.6% 26.4% 0.1%

1997 3.65% 2.5% 35.1% 1.1%

1998 19.59% 2.7% 21.8% 3.9%

1999 27.65% 2.3% 46.3% 5.9%

Annual average

5.66% 1.9% 18.9% 1.0%

(a) Some data have been interpolated, as figures were not available for all countriesin all years

p , gin all years.Source : SDC, AMECO and FIBV.

– 6 –

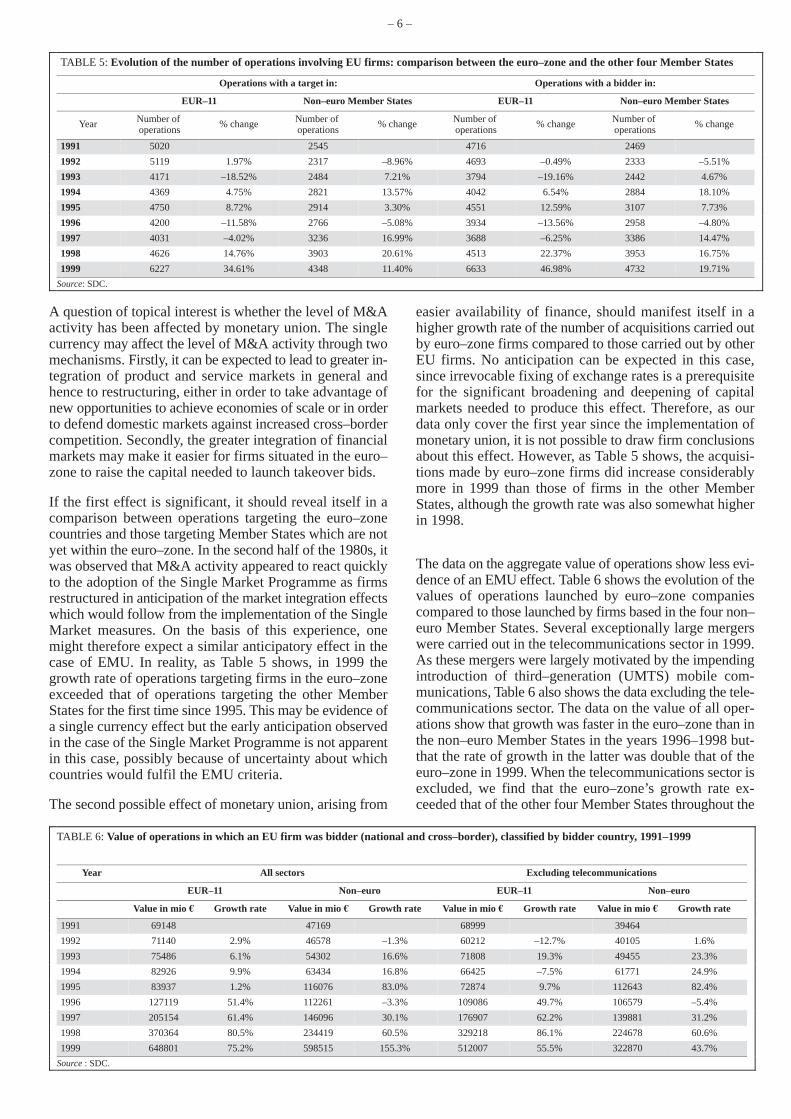

TABLE 5: Evolution of the number of operations involving EU firms: comparison between the euro–zone and the other four Member States

Operations with a target in: Operations with a bidder in:

EUR–11 Non–euro Member States EUR–11 Non–euro Member States

Year Number of operations

% change Number of operations

% change Number of operations

% change Number of operations

% change

1991 5020 2545 4716 2469

1992 5119 1.97% 2317 –8.96% 4693 –0.49% 2333 –5.51%

1993 4171 –18.52% 2484 7.21% 3794 –19.16% 2442 4.67%

1994 4369 4.75% 2821 13.57% 4042 6.54% 2884 18.10%

1995 4750 8.72% 2914 3.30% 4551 12.59% 3107 7.73%

1996 4200 –11.58% 2766 –5.08% 3934 –13.56% 2958 –4.80%

1997 4031 –4.02% 3236 16.99% 3688 –6.25% 3386 14.47%

1998 4626 14.76% 3903 20.61% 4513 22.37% 3953 16.75%

1999 6227 34.61% 4348 11.40% 6633 46.98% 4732 19.71%

Source: SDC.

A question of topical interest is whether the level of M&Aactivity has been affected by monetary union. The singlecurrency may affect the level of M&A activity through twomechanisms. Firstly, it can be expected to lead to greater in-tegration of product and service markets in general andhence to restructuring, either in order to take advantage ofnew opportunities to achieve economies of scale or in orderto defend domestic markets against increased cross–bordercompetition. Secondly, the greater integration of financialmarkets may make it easier for firms situated in the euro–zone to raise the capital needed to launch takeover bids.

If the first effect is significant, it should reveal itself in acomparison between operations targeting the euro–zonecountries and those targeting Member States which are notyet within the euro–zone. In the second half of the 1980s, itwas observed that M&A activity appeared to react quicklyto the adoption of the Single Market Programme as firmsrestructured in anticipation of the market integration effectswhich would follow from the implementation of the SingleMarket measures. On the basis of this experience, onemight therefore expect a similar anticipatory effect in thecase of EMU. In reality, as Table 5 shows, in 1999 thegrowth rate of operations targeting firms in the euro–zoneexceeded that of operations targeting the other MemberStates for the first time since 1995. This may be evidence ofa single currency effect but the early anticipation observedin the case of the Single Market Programme is not apparentin this case, possibly because of uncertainty about whichcountries would fulfil the EMU criteria.

The second possible effect of monetary union, arising from

easier availability of finance, should manifest itself in ahigher growth rate of the number of acquisitions carried outby euro–zone firms compared to those carried out by otherEU firms. No anticipation can be expected in this case,since irrevocable fixing of exchange rates is a prerequisitefor the significant broadening and deepening of capitalmarkets needed to produce this effect. Therefore, as ourdata only cover the first year since the implementation ofmonetary union, it is not possible to draw firm conclusionsabout this effect. However, as Table 5 shows, the acquisi-tions made by euro–zone firms did increase considerablymore in 1999 than those of firms in the other MemberStates, although the growth rate was also somewhat higherin 1998.

The data on the aggregate value of operations show less evi-dence of an EMU effect. Table 6 shows the evolution of thevalues of operations launched by euro–zone companiescompared to those launched by firms based in the four non–euro Member States. Several exceptionally large mergerswere carried out in the telecommunications sector in 1999.As these mergers were largely motivated by the impendingintroduction of third–generation (UMTS) mobile com-munications, Table 6 also shows the data excluding the tele-communications sector. The data on the value of all oper-ations show that growth was faster in the euro–zone than inthe non–euro Member States in the years 1996–1998 but-that the rate of growth in the latter was double that of theeuro–zone in 1999. When the telecommunications sector isexcluded, we find that the euro–zone’s growth rate ex-ceeded that of the other four Member States throughout the

TABLE 6: Value of operations in which an EU firm was bidder (national and cross–border), classified by bidder country, 1991–1999

Year All sectors Excluding telecommunications

EUR–11 Non–euro EUR–11 Non–euro

Value in mio Growth rate Value in mio Growth rate Value in mio Growth rate Value in mio Growth rate

1991 69148 47169 68999 39464

1992 71140 2.9% 46578 –1.3% 60212 –12.7% 40105 1.6%

1993 75486 6.1% 54302 16.6% 71808 19.3% 49455 23.3%

1994 82926 9.9% 63434 16.8% 66425 –7.5% 61771 24.9%

1995 83937 1.2% 116076 83.0% 72874 9.7% 112643 82.4%

1996 127119 51.4% 112261 –3.3% 109086 49.7% 106579 –5.4%

1997 205154 61.4% 146096 30.1% 176907 62.2% 139881 31.2%

1998 370364 80.5% 234419 60.5% 329218 86.1% 224678 60.6%

1999 648801 75.2% 598515 155.3% 512007 55.5% 322870 43.7%

Source : SDC.

– 7 –

GRAPH 2: Number of M&A within the EU: distribution, financialservices and total, 1992–1999

Source: SDC–M&A and FIBV (International Federation of Stock Exchanges).

Number of operations, 1991=100

Distribution Financial services Total–all sectors

92 93 94 95 96 97 98 9960

80

100

120

140

period 1996–1999. However, any influence of EMU ontransaction values is most likely to be exerted via the mech-anism of increased financial integration. As explainedabove, we would not expect this mechanism to give rise toany anticpatory effect on M&A activity. Consequently, thevalue data do not furnish any clear evidence of an EMU ef-fect.

For the first year of monetary union, therefore, the aggre-gate data do not provide any conclusive evidence of an ef-fect on M&A activity. We have therefore examined the sec-toral data to see if they can provide more insight.

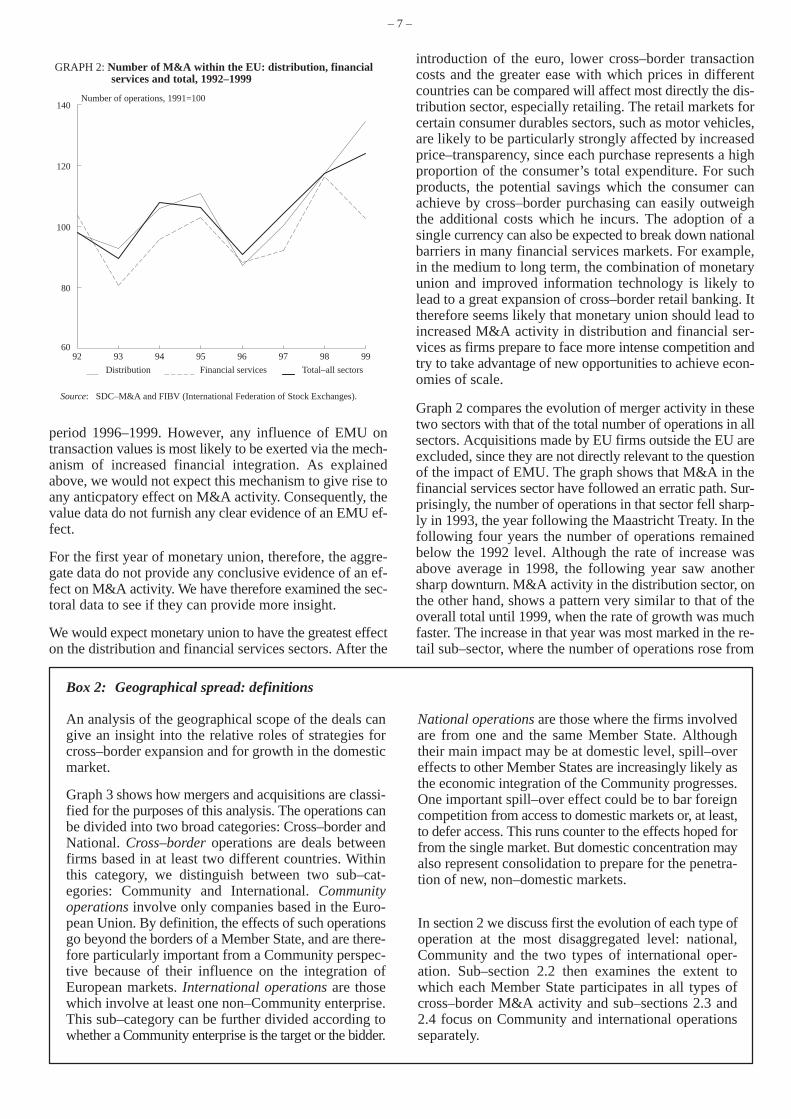

We would expect monetary union to have the greatest effecton the distribution and financial services sectors. After the

introduction of the euro, lower cross–border transactioncosts and the greater ease with which prices in differentcountries can be compared will affect most directly the dis-tribution sector, especially retailing. The retail markets forcertain consumer durables sectors, such as motor vehicles,are likely to be particularly strongly affected by increasedprice–transparency, since each purchase represents a highproportion of the consumer’s total expenditure. For suchproducts, the potential savings which the consumer canachieve by cross–border purchasing can easily outweighthe additional costs which he incurs. The adoption of asingle currency can also be expected to break down nationalbarriers in many financial services markets. For example,in the medium to long term, the combination of monetaryunion and improved information technology is likely tolead to a great expansion of cross–border retail banking. Ittherefore seems likely that monetary union should lead toincreased M&A activity in distribution and financial ser-vices as firms prepare to face more intense competition andtry to take advantage of new opportunities to achieve econ-omies of scale.

Graph 2 compares the evolution of merger activity in thesetwo sectors with that of the total number of operations in allsectors. Acquisitions made by EU firms outside the EU areexcluded, since they are not directly relevant to the questionof the impact of EMU. The graph shows that M&A in thefinancial services sector have followed an erratic path. Sur-prisingly, the number of operations in that sector fell sharp-ly in 1993, the year following the Maastricht Treaty. In thefollowing four years the number of operations remainedbelow the 1992 level. Although the rate of increase wasabove average in 1998, the following year saw anothersharp downturn. M&A activity in the distribution sector, onthe other hand, shows a pattern very similar to that of theoverall total until 1999, when the rate of growth was muchfaster. The increase in that year was most marked in the re-tail sub–sector, where the number of operations rose from

Box 2: Geographical spread: definitions

An analysis of the geographical scope of the deals cangive an insight into the relative roles of strategies forcross–border expansion and for growth in the domesticmarket.

Graph 3 shows how mergers and acquisitions are classi-fied for the purposes of this analysis. The operations canbe divided into two broad categories: Cross–border andNational. Cross–border operations are deals betweenfirms based in at least two different countries. Withinthis category, we distinguish between two sub–cat-egories: Community and International. Communityoperations involve only companies based in the Euro-pean Union. By definition, the effects of such operationsgo beyond the borders of a Member State, and are there-fore particularly important from a Community perspec-tive because of their influence on the integration ofEuropean markets. International operations are thosewhich involve at least one non–Community enterprise.This sub–category can be further divided according towhether a Community enterprise is the target or the bidder.

National operations are those where the firms involvedare from one and the same Member State. Althoughtheir main impact may be at domestic level, spill–overeffects to other Member States are increasingly likely asthe economic integration of the Community progresses.One important spill–over effect could be to bar foreigncompetition from access to domestic markets or, at least,to defer access. This runs counter to the effects hoped forfrom the single market. But domestic concentration mayalso represent consolidation to prepare for the penetra-tion of new, non–domestic markets.

In section 2 we discuss first the evolution of each type ofoperation at the most disaggregated level: national,Community and the two types of international oper-ation. Sub–section 2.2 then examines the extent towhich each Member State participates in all types ofcross–border M&A activity and sub–sections 2.3 and2.4 focus on Community and international operationsseparately.

– 8 –

GRAPH 3: Geographical classification

Source: Amdata.

ALL M&A INVOLVING

EU FIRMS

NATIONAL CROSS–BORDER

COMMUNITY INTERNATIONAL

EU TARGET EU BIDDER

360 to 551. In the wholesale sub–sector, the increase from612 to 757 was more in line with the overall growth rate. Itis possible, therefore, that EMU has had an effect on M&Aactivity in the distribution sector, especially retailing. How-ever, it should be noted that distribution contributed onlyabout 16% of the overall growth in the number of oper-ations in 1999.

In conclusion, we have not been able to explain the evol-ution of levels of M&A activity during the 1990s in terms ofoverall stock market developments or macroeconomic fac-tors, although there are some indications of a possible EMUeffect. It may be that short–run changes in M&A activitycan only be explained as the result of complex combina-tions of largely sector–specific and country–specific in-fluences.

2. Geographical spread

2.1 Breakdown of national, Community and interna-tional operations

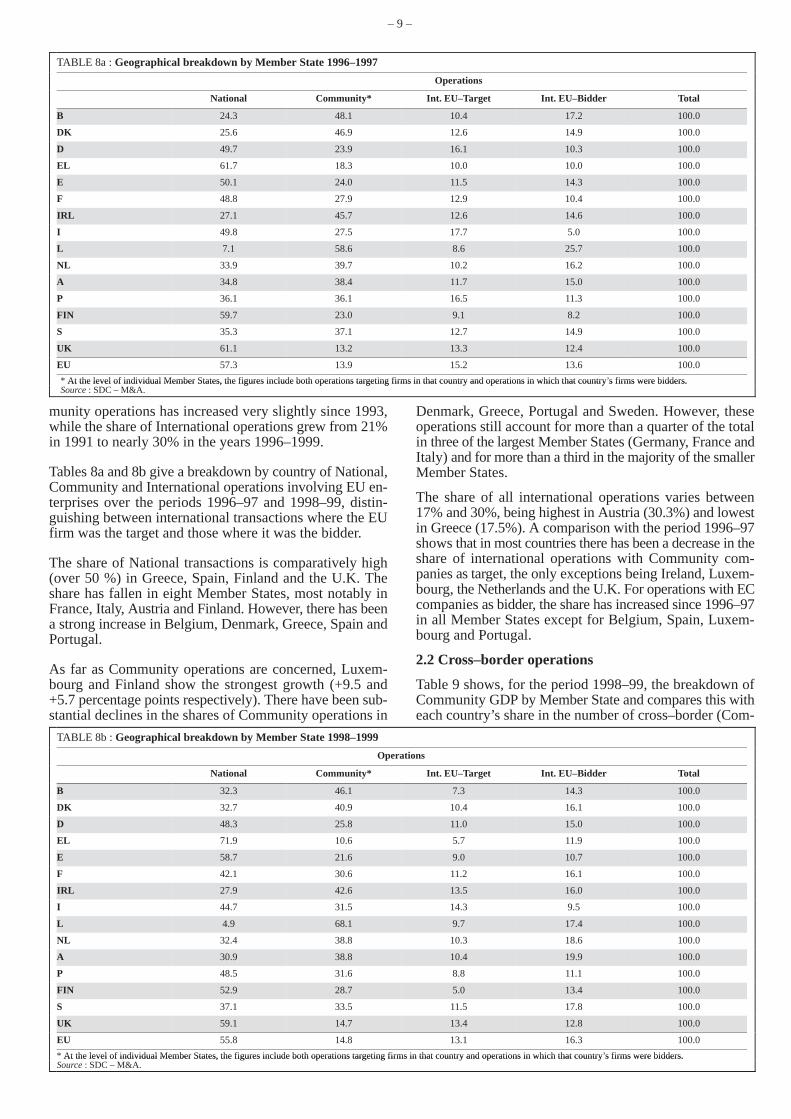

GRAPH 4: Number of National, Community and Internationaloperations

Source: SDC–M&A.

1991 = 100

91 92 93 94 95 96 97 98 99

0

50

100

150

200

250

300

350

National Community Int EC–target Int EC–bidder

Graph 4 tracks the evolution of the four types of operationat the most disaggregated level. The data are presented asindices, the base being the year 1991.

The graph shows that the numbers of National and Com-munity operations have followed quite similar paths. In-ternational operations with an EU target showed a moresteady growth trend until 1999, when there was a signifi-cant downturn (–8%). In contrast, the number of Interna-tional operations with an EU company as bidder has grownmuch more strongly than the other types of operationthroughout most of the 1990s, with a significant acceler-ation in the last two years. 1999 was an exceptional year asfar as International operations are concerned. The numberof extra–EU acquisitions made by EU firms in that yearvastly exceeded the number of acquisitions made by non–EU companies within the Community (2221, compared to1431). Only once before, in 1995, has the number of out-ward transactions been greater than the number of inwardtransactions and then the margin was very small (1119against 1113).

TABLE 7: Evolution of National, Community and InternationalM&A operations

Year National Community Int EU–target

Int EU–bidder

Total

1991 65.1% 14.0% 12.8% 8.1% 100.0%

1992 67.9% 12.9% 12.2% 7.1% 100.0%

1993 63.5% 12.5% 14.9% 9.1% 100.0%

1994 62.7% 13.6% 13.5% 10.2% 100.0%

1995 61.0% 13.5% 12.7% 12.7% 100.0%

1996 57.9% 13.5% 14.8% 13.8% 100.0%

1997 56.8% 14.3% 15.6% 13.3% 100.0%

1998 55.0% 14.5% 15.5% 14.9% 100.0%

1999 56.5% 15.0% 11.2% 17.4% 100.0%

Source : SDC – M&A.

Table 7 shows the evolution of the different types of oper-ations since 1991 in percentage of the total number of M&Aoperations involving an EU firm.

It can be observed that the share of National operations hasfluctuated around 56 % since 1996, after having fallensteeply from its 1992 level. National operations continue toconstitute the bulk of M&A operations. The share of Com-

– 9 –

TABLE 8a : Geographical breakdown by Member State 1996–1997

Operations

National Community* Int. EU–Target Int. EU–Bidder Total

B 24.3 48.1 10.4 17.2 100.0

DK 25.6 46.9 12.6 14.9 100.0

D 49.7 23.9 16.1 10.3 100.0

EL 61.7 18.3 10.0 10.0 100.0

E 50.1 24.0 11.5 14.3 100.0

F 48.8 27.9 12.9 10.4 100.0

IRL 27.1 45.7 12.6 14.6 100.0

I 49.8 27.5 17.7 5.0 100.0

L 7.1 58.6 8.6 25.7 100.0

NL 33.9 39.7 10.2 16.2 100.0

A 34.8 38.4 11.7 15.0 100.0

P 36.1 36.1 16.5 11.3 100.0

FIN 59.7 23.0 9.1 8.2 100.0

S 35.3 37.1 12.7 14.9 100.0

UK 61.1 13.2 13.3 12.4 100.0

EU 57.3 13.9 15.2 13.6 100.0

* At the level of individual Member States, the figures include both operations targeting firms in that country and operations in which that country’s firms were bidders.* At the level of individual Member States, the figures include both operations targeting firms in that country and operations in which that country s firms were bidders.Source : SDC – M&A.

munity operations has increased very slightly since 1993,while the share of International operations grew from 21%in 1991 to nearly 30% in the years 1996–1999.

Tables 8a and 8b give a breakdown by country of National,Community and International operations involving EU en-terprises over the periods 1996–97 and 1998–99, distin-guishing between international transactions where the EUfirm was the target and those where it was the bidder.

The share of National transactions is comparatively high(over 50 %) in Greece, Spain, Finland and the U.K. Theshare has fallen in eight Member States, most notably inFrance, Italy, Austria and Finland. However, there has beena strong increase in Belgium, Denmark, Greece, Spain andPortugal.

As far as Community operations are concerned, Luxem-bourg and Finland show the strongest growth (+9.5 and+5.7 percentage points respectively). There have been sub-stantial declines in the shares of Community operations in

Denmark, Greece, Portugal and Sweden. However, theseoperations still account for more than a quarter of the totalin three of the largest Member States (Germany, France andItaly) and for more than a third in the majority of the smallerMember States.

The share of all international operations varies between17% and 30%, being highest in Austria (30.3%) and lowestin Greece (17.5%). A comparison with the period 1996–97shows that in most countries there has been a decrease in theshare of international operations with Community com-panies as target, the only exceptions being Ireland, Luxem-bourg, the Netherlands and the U.K. For operations with ECcompanies as bidder, the share has increased since 1996–97in all Member States except for Belgium, Spain, Luxem-bourg and Portugal.

2.2 Cross–border operations

Table 9 shows, for the period 1998–99, the breakdown ofCommunity GDP by Member State and compares this witheach country’s share in the number of cross–border (Com-

TABLE 8b : Geographical breakdown by Member State 1998–1999

Operations

National Community* Int. EU–Target Int. EU–Bidder Total

B 32.3 46.1 7.3 14.3 100.0

DK 32.7 40.9 10.4 16.1 100.0

D 48.3 25.8 11.0 15.0 100.0

EL 71.9 10.6 5.7 11.9 100.0

E 58.7 21.6 9.0 10.7 100.0

F 42.1 30.6 11.2 16.1 100.0

IRL 27.9 42.6 13.5 16.0 100.0

I 44.7 31.5 14.3 9.5 100.0

L 4.9 68.1 9.7 17.4 100.0

NL 32.4 38.8 10.3 18.6 100.0

A 30.9 38.8 10.4 19.9 100.0

P 48.5 31.6 8.8 11.1 100.0

FIN 52.9 28.7 5.0 13.4 100.0

S 37.1 33.5 11.5 17.8 100.0

UK 59.1 14.7 13.4 12.8 100.0

EU 55.8 14.8 13.1 16.3 100.0

* At the level of individual Member States, the figures include both operations targeting firms in that country and operations in which that country’s firms were bidders.* At the level of individual Member States, the figures include both operations targeting firms in that country and operations in which that country s firms were bidders.Source : SDC – M&A.

– 10 –

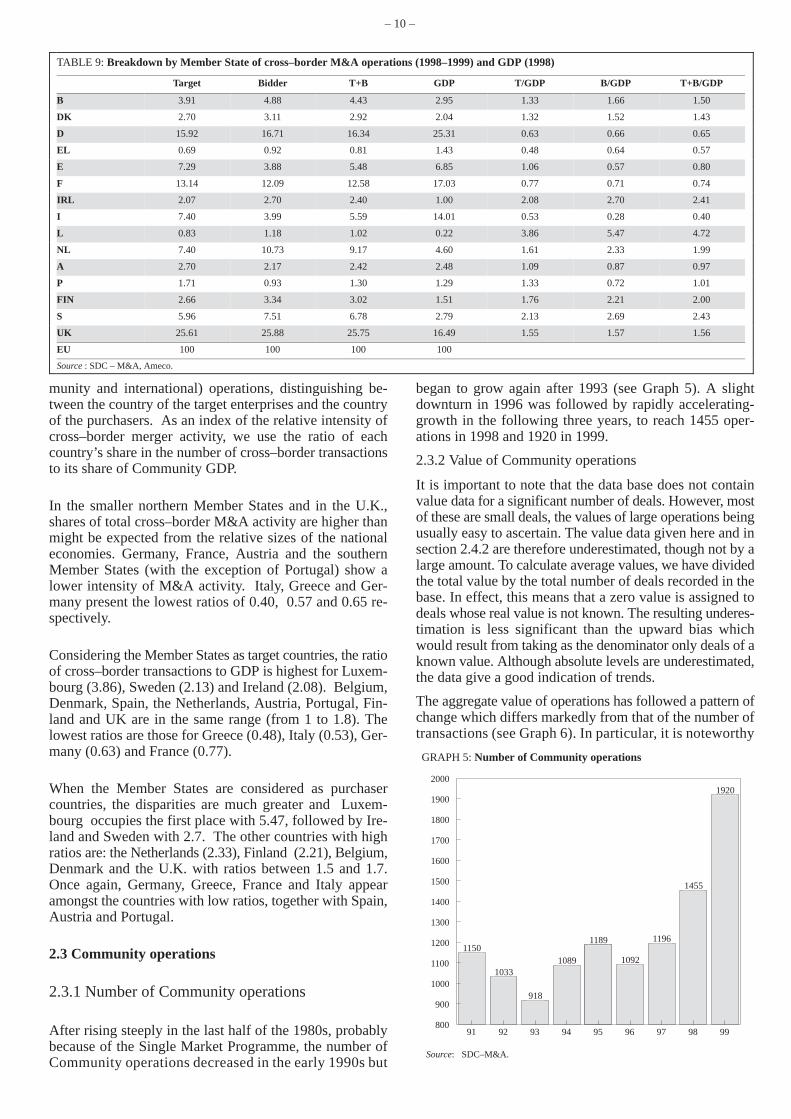

TABLE 9: Breakdown by Member State of cross–border M&A operations (1998–1999) and GDP (1998)

Target Bidder T+B GDP T/GDP B/GDP T+B/GDP

B 3.91 4.88 4.43 2.95 1.33 1.66 1.50

DK 2.70 3.11 2.92 2.04 1.32 1.52 1.43

D 15.92 16.71 16.34 25.31 0.63 0.66 0.65

EL 0.69 0.92 0.81 1.43 0.48 0.64 0.57

E 7.29 3.88 5.48 6.85 1.06 0.57 0.80

F 13.14 12.09 12.58 17.03 0.77 0.71 0.74

IRL 2.07 2.70 2.40 1.00 2.08 2.70 2.41

I 7.40 3.99 5.59 14.01 0.53 0.28 0.40

L 0.83 1.18 1.02 0.22 3.86 5.47 4.72

NL 7.40 10.73 9.17 4.60 1.61 2.33 1.99

A 2.70 2.17 2.42 2.48 1.09 0.87 0.97

P 1.71 0.93 1.30 1.29 1.33 0.72 1.01

FIN 2.66 3.34 3.02 1.51 1.76 2.21 2.00

S 5.96 7.51 6.78 2.79 2.13 2.69 2.43

UK 25.61 25.88 25.75 16.49 1.55 1.57 1.56

EU 100 100 100 100

Source : SDC – M&A, Ameco.

munity and international) operations, distinguishing be-tween the country of the target enterprises and the countryof the purchasers. As an index of the relative intensity ofcross–border merger activity, we use the ratio of eachcountry’s share in the number of cross–border transactionsto its share of Community GDP.

In the smaller northern Member States and in the U.K.,shares of total cross–border M&A activity are higher thanmight be expected from the relative sizes of the nationaleconomies. Germany, France, Austria and the southernMember States (with the exception of Portugal) show alower intensity of M&A activity. Italy, Greece and Ger-many present the lowest ratios of 0.40, 0.57 and 0.65 re-spectively.

Considering the Member States as target countries, the ratioof cross–border transactions to GDP is highest for Luxem-bourg (3.86), Sweden (2.13) and Ireland (2.08). Belgium,Denmark, Spain, the Netherlands, Austria, Portugal, Fin-land and UK are in the same range (from 1 to 1.8). Thelowest ratios are those for Greece (0.48), Italy (0.53), Ger-many (0.63) and France (0.77).

When the Member States are considered as purchasercountries, the disparities are much greater and Luxem-bourg occupies the first place with 5.47, followed by Ire-land and Sweden with 2.7. The other countries with highratios are: the Netherlands (2.33), Finland (2.21), Belgium,Denmark and the U.K. with ratios between 1.5 and 1.7.Once again, Germany, Greece, France and Italy appearamongst the countries with low ratios, together with Spain,Austria and Portugal.

2.3 Community operations

2.3.1 Number of Community operations

After rising steeply in the last half of the 1980s, probablybecause of the Single Market Programme, the number ofCommunity operations decreased in the early 1990s but

began to grow again after 1993 (see Graph 5). A slightdownturn in 1996 was followed by rapidly accelerating-growth in the following three years, to reach 1455 oper-ations in 1998 and 1920 in 1999.

2.3.2 Value of Community operations

It is important to note that the data base does not containvalue data for a significant number of deals. However, mostof these are small deals, the values of large operations beingusually easy to ascertain. The value data given here and insection 2.4.2 are therefore underestimated, though not by alarge amount. To calculate average values, we have dividedthe total value by the total number of deals recorded in thebase. In effect, this means that a zero value is assigned todeals whose real value is not known. The resulting underes-timation is less significant than the upward bias whichwould result from taking as the denominator only deals of aknown value. Although absolute levels are underestimated,the data give a good indication of trends.

The aggregate value of operations has followed a pattern ofchange which differs markedly from that of the number oftransactions (see Graph 6). In particular, it is noteworthy

GRAPH 5: Number of Community operations

Source: SDC–M&A.

1150

1033

918

1089

1189

1092

1196

1455

1920

91 92 93 94 95 96 97 98 99800

900

1000

1100

1200

1300

1400

1500

1600

1700

1800

1900

2000

– 11 –

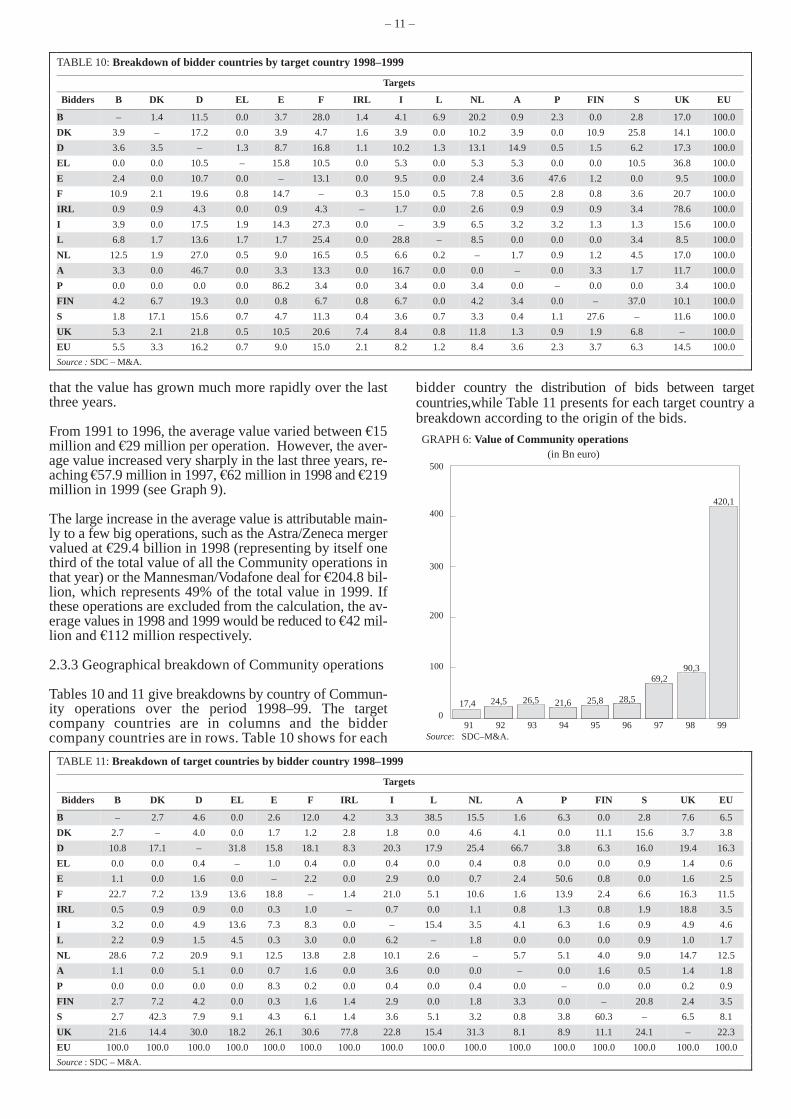

TABLE 10: Breakdown of bidder countries by target country 1998–1999

Targets

Bidders B DK D EL E F IRL I L NL A P FIN S UK EU

B – 1.4 11.5 0.0 3.7 28.0 1.4 4.1 6.9 20.2 0.9 2.3 0.0 2.8 17.0 100.0

DK 3.9 – 17.2 0.0 3.9 4.7 1.6 3.9 0.0 10.2 3.9 0.0 10.9 25.8 14.1 100.0

D 3.6 3.5 – 1.3 8.7 16.8 1.1 10.2 1.3 13.1 14.9 0.5 1.5 6.2 17.3 100.0

EL 0.0 0.0 10.5 – 15.8 10.5 0.0 5.3 0.0 5.3 5.3 0.0 0.0 10.5 36.8 100.0

E 2.4 0.0 10.7 0.0 – 13.1 0.0 9.5 0.0 2.4 3.6 47.6 1.2 0.0 9.5 100.0

F 10.9 2.1 19.6 0.8 14.7 – 0.3 15.0 0.5 7.8 0.5 2.8 0.8 3.6 20.7 100.0

IRL 0.9 0.9 4.3 0.0 0.9 4.3 – 1.7 0.0 2.6 0.9 0.9 0.9 3.4 78.6 100.0

I 3.9 0.0 17.5 1.9 14.3 27.3 0.0 – 3.9 6.5 3.2 3.2 1.3 1.3 15.6 100.0

L 6.8 1.7 13.6 1.7 1.7 25.4 0.0 28.8 – 8.5 0.0 0.0 0.0 3.4 8.5 100.0

NL 12.5 1.9 27.0 0.5 9.0 16.5 0.5 6.6 0.2 – 1.7 0.9 1.2 4.5 17.0 100.0

A 3.3 0.0 46.7 0.0 3.3 13.3 0.0 16.7 0.0 0.0 – 0.0 3.3 1.7 11.7 100.0

P 0.0 0.0 0.0 0.0 86.2 3.4 0.0 3.4 0.0 3.4 0.0 – 0.0 0.0 3.4 100.0

FIN 4.2 6.7 19.3 0.0 0.8 6.7 0.8 6.7 0.0 4.2 3.4 0.0 – 37.0 10.1 100.0

S 1.8 17.1 15.6 0.7 4.7 11.3 0.4 3.6 0.7 3.3 0.4 1.1 27.6 – 11.6 100.0

UK 5.3 2.1 21.8 0.5 10.5 20.6 7.4 8.4 0.8 11.8 1.3 0.9 1.9 6.8 – 100.0

EU 5.5 3.3 16.2 0.7 9.0 15.0 2.1 8.2 1.2 8.4 3.6 2.3 3.7 6.3 14.5 100.0

Source : SDC – M&A.

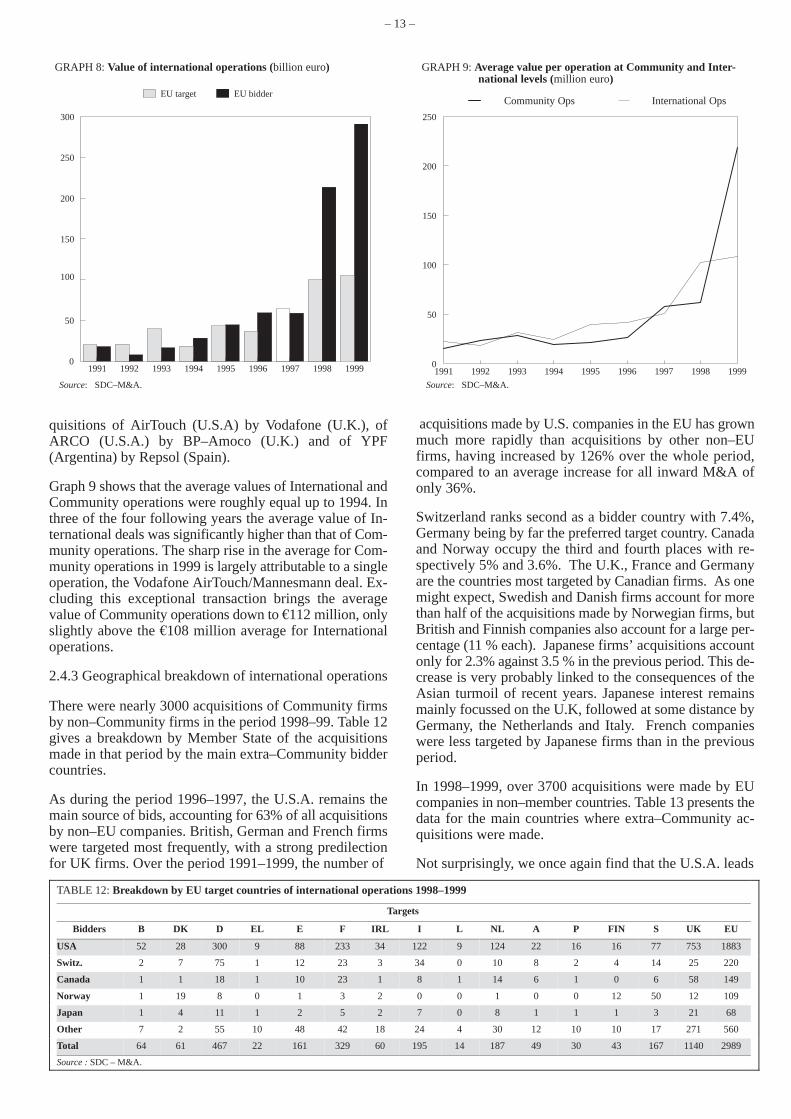

that the value has grown much more rapidly over the lastthree years.

From 1991 to 1996, the average value varied between 15million and 29 million per operation. However, the aver-age value increased very sharply in the last three years, re-aching 57.9 million in 1997, 62 million in 1998 and 219million in 1999 (see Graph 9).

The large increase in the average value is attributable main-ly to a few big operations, such as the Astra/Zeneca mergervalued at 29.4 billion in 1998 (representing by itself onethird of the total value of all the Community operations inthat year) or the Mannesman/Vodafone deal for 204.8 bil-lion, which represents 49% of the total value in 1999. Ifthese operations are excluded from the calculation, the av-erage values in 1998 and 1999 would be reduced to 42 mil-lion and 112 million respectively.

2.3.3 Geographical breakdown of Community operations

Tables 10 and 11 give breakdowns by country of Commun-ity operations over the period 1998–99. The targetcompany countries are in columns and the biddercompany countries are in rows. Table 10 shows for each

bidder country the distribution of bids between targetcountries,while Table 11 presents for each target country abreakdown according to the origin of the bids.GRAPH 6: Value of Community operations

Source: SDC–M&A.

(in Bn euro)

17,4 24,5 26,5 21,6 25,8 28,5

69,290,3

420,1

0

100

200

300

400

500

91 92 93 94 95 96 97 98 99

TABLE 11: Breakdown of target countries by bidder country 1998–1999

Targets

Bidders B DK D EL E F IRL I L NL A P FIN S UK EU

B – 2.7 4.6 0.0 2.6 12.0 4.2 3.3 38.5 15.5 1.6 6.3 0.0 2.8 7.6 6.5

DK 2.7 – 4.0 0.0 1.7 1.2 2.8 1.8 0.0 4.6 4.1 0.0 11.1 15.6 3.7 3.8

D 10.8 17.1 – 31.8 15.8 18.1 8.3 20.3 17.9 25.4 66.7 3.8 6.3 16.0 19.4 16.3

EL 0.0 0.0 0.4 – 1.0 0.4 0.0 0.4 0.0 0.4 0.8 0.0 0.0 0.9 1.4 0.6

E 1.1 0.0 1.6 0.0 – 2.2 0.0 2.9 0.0 0.7 2.4 50.6 0.8 0.0 1.6 2.5

F 22.7 7.2 13.9 13.6 18.8 – 1.4 21.0 5.1 10.6 1.6 13.9 2.4 6.6 16.3 11.5

IRL 0.5 0.9 0.9 0.0 0.3 1.0 – 0.7 0.0 1.1 0.8 1.3 0.8 1.9 18.8 3.5

I 3.2 0.0 4.9 13.6 7.3 8.3 0.0 – 15.4 3.5 4.1 6.3 1.6 0.9 4.9 4.6

L 2.2 0.9 1.5 4.5 0.3 3.0 0.0 6.2 – 1.8 0.0 0.0 0.0 0.9 1.0 1.7

NL 28.6 7.2 20.9 9.1 12.5 13.8 2.8 10.1 2.6 – 5.7 5.1 4.0 9.0 14.7 12.5

A 1.1 0.0 5.1 0.0 0.7 1.6 0.0 3.6 0.0 0.0 – 0.0 1.6 0.5 1.4 1.8

P 0.0 0.0 0.0 0.0 8.3 0.2 0.0 0.4 0.0 0.4 0.0 – 0.0 0.0 0.2 0.9

FIN 2.7 7.2 4.2 0.0 0.3 1.6 1.4 2.9 0.0 1.8 3.3 0.0 – 20.8 2.4 3.5

S 2.7 42.3 7.9 9.1 4.3 6.1 1.4 3.6 5.1 3.2 0.8 3.8 60.3 – 6.5 8.1

UK 21.6 14.4 30.0 18.2 26.1 30.6 77.8 22.8 15.4 31.3 8.1 8.9 11.1 24.1 – 22.3

EU 100.0 100.0 100.0 100.0 100.0 100.0 100.0 100.0 100.0 100.0 100.0 100.0 100.0 100.0 100.0 100.0

Source : SDC – M&A.

– 12 –

Together with the size of the economies of the countriesconcerned, proximity and traditional economic links re-main particularly important for cross–border mergers andacquisitions. For example, U.K. firms account for 79% ofcross–border acquisitions made in the Community by Irishcompanies. Conversely, 78% of Community operationstargeting Irish companies were carried out by U.K. firms.The latter percentage has increased sharply since 1996when U.K. firms accounted for less than 60% of all Com-munity operations in Ireland. A similar close relationshipexists between Sweden and Denmark. Acquisitions ofSwedish firms by Danish companies represent one quarterof Community operations launched by Danish companies,while 42 % of Community operations targeting Danishcompanies were carried out by Swedish firms. Finland andAustria are also more targeted by direct neighbours (i.e.Sweden and Germany respectively).

German companies were most often the target of Commun-ity operations (16% of the transactions). Given the size ofthe German economy this high number is unsurprising.Germany accounts for a high proportion of the acquisitionsmade by French, Italian, Dutch, Austrian and British firms.These countries also head the list of target countries foroperations launched by German companies.

France comes second as target country, with 15% of Com-munity operations. French firms were the main targets ofoperations undertaken by Belgian and Italian companiesand also accounted for a high proportion of bids made byGerman, Spanish and British firms. After the U.K., Ger-many, Italy, Spain and Belgium are the main countries of in-terest to French purchasers.

The U.K. occupies the third place amongst the targetcountries with 14.5% of the total. As noted above, Britishcompanies are particularly favoured by Irish purchasers,but they also feature in a prominent place amongst thetargets of Belgian, German, French and Dutch companies.Operations launched by U.K. firms concerned principallyGermany, France and the Netherlands.

Spain ranks fourth amongst the target countries, with 9% ofthe total, slightly ahead of the Netherlands and Italy, in spiteof the big differences in the size of the countries. Operationslaunched by Spanish firms concerned mainly Portugal,France and Germany. Operations launched by Dutch firmsconcerned mainly Germany, the UK, France and Belgium.

The four Member States whose companies make the mostcross–border bids within the Community are the U.K.(22.3%), Germany (16.3%), Netherlands (12.5%) andFrance (11.5%).

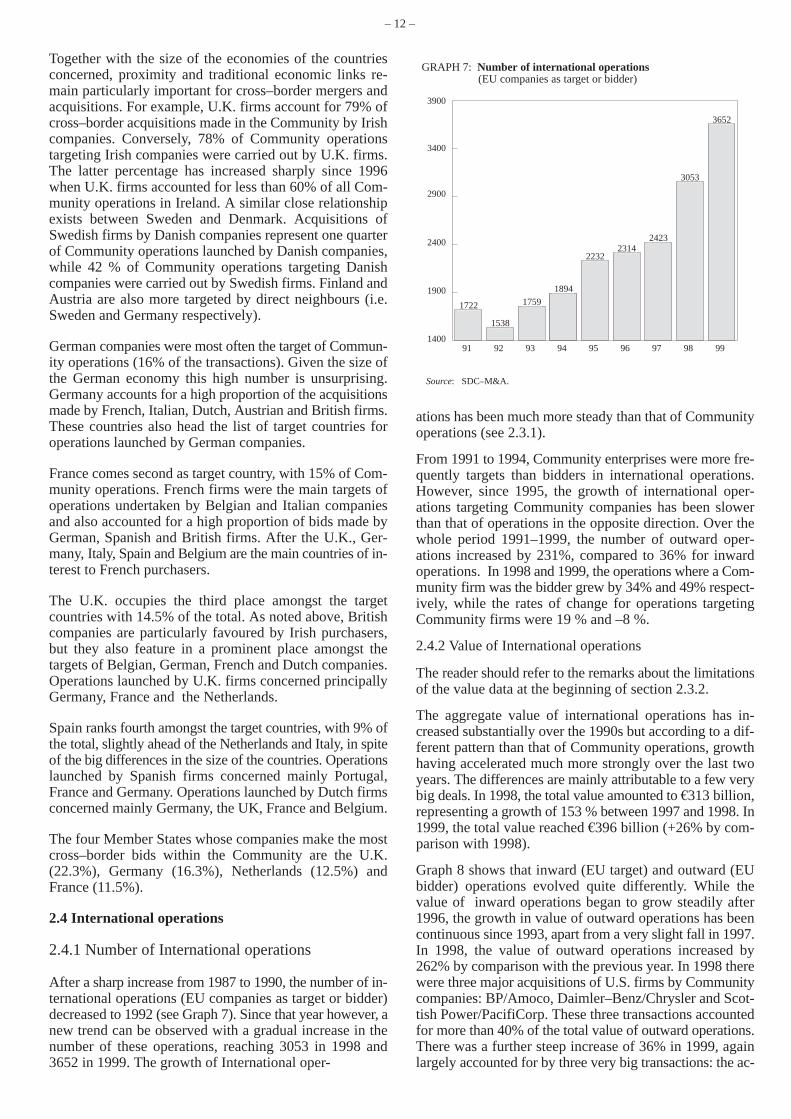

2.4 International operations

2.4.1 Number of International operations

After a sharp increase from 1987 to 1990, the number of in-ternational operations (EU companies as target or bidder)decreased to 1992 (see Graph 7). Since that year however, anew trend can be observed with a gradual increase in thenumber of these operations, reaching 3053 in 1998 and3652 in 1999. The growth of International oper-

GRAPH 7: Number of international operations (EU companies as target or bidder)

Source: SDC–M&A.

1722

1538

1759

1894

22322314

2423

3053

3652

91 92 93 94 95 96 97 98 991400

1900

2400

2900

3400

3900

ations has been much more steady than that of Communityoperations (see 2.3.1).

From 1991 to 1994, Community enterprises were more fre-quently targets than bidders in international operations.However, since 1995, the growth of international oper-ations targeting Community companies has been slowerthan that of operations in the opposite direction. Over thewhole period 1991–1999, the number of outward oper-ations increased by 231%, compared to 36% for inwardoperations. In 1998 and 1999, the operations where a Com-munity firm was the bidder grew by 34% and 49% respect-ively, while the rates of change for operations targetingCommunity firms were 19 % and –8 %.

2.4.2 Value of International operations

The reader should refer to the remarks about the limitationsof the value data at the beginning of section 2.3.2.

The aggregate value of international operations has in-creased substantially over the 1990s but according to a dif-ferent pattern than that of Community operations, growthhaving accelerated much more strongly over the last twoyears. The differences are mainly attributable to a few verybig deals. In 1998, the total value amounted to 313 billion,representing a growth of 153 % between 1997 and 1998. In1999, the total value reached 396 billion (+26% by com-parison with 1998).

Graph 8 shows that inward (EU target) and outward (EUbidder) operations evolved quite differently. While thevalue of inward operations began to grow steadily after1996, the growth in value of outward operations has beencontinuous since 1993, apart from a very slight fall in 1997.In 1998, the value of outward operations increased by262% by comparison with the previous year. In 1998 therewere three major acquisitions of U.S. firms by Communitycompanies: BP/Amoco, Daimler–Benz/Chrysler and Scot-tish Power/PacifiCorp. These three transactions accountedfor more than 40% of the total value of outward operations.There was a further steep increase of 36% in 1999, againlargely accounted for by three very big transactions: the ac-

– 13 –

GRAPH 8: Value of international operations (billion euro)

Source: SDC–M&A.

EU target EU bidder

1991 1992 1993 1994 1995 1996 1997 1998 19990

50

100

150

200

250

300

quisitions of AirTouch (U.S.A) by Vodafone (U.K.), ofARCO (U.S.A.) by BP–Amoco (U.K.) and of YPF(Argentina) by Repsol (Spain).

Graph 9 shows that the average values of International andCommunity operations were roughly equal up to 1994. Inthree of the four following years the average value of In-ternational deals was significantly higher than that of Com-munity operations. The sharp rise in the average for Com-munity operations in 1999 is largely attributable to a singleoperation, the Vodafone AirTouch/Mannesmann deal. Ex-cluding this exceptional transaction brings the averagevalue of Community operations down to 112 million, onlyslightly above the 108 million average for Internationaloperations.

2.4.3 Geographical breakdown of international operations

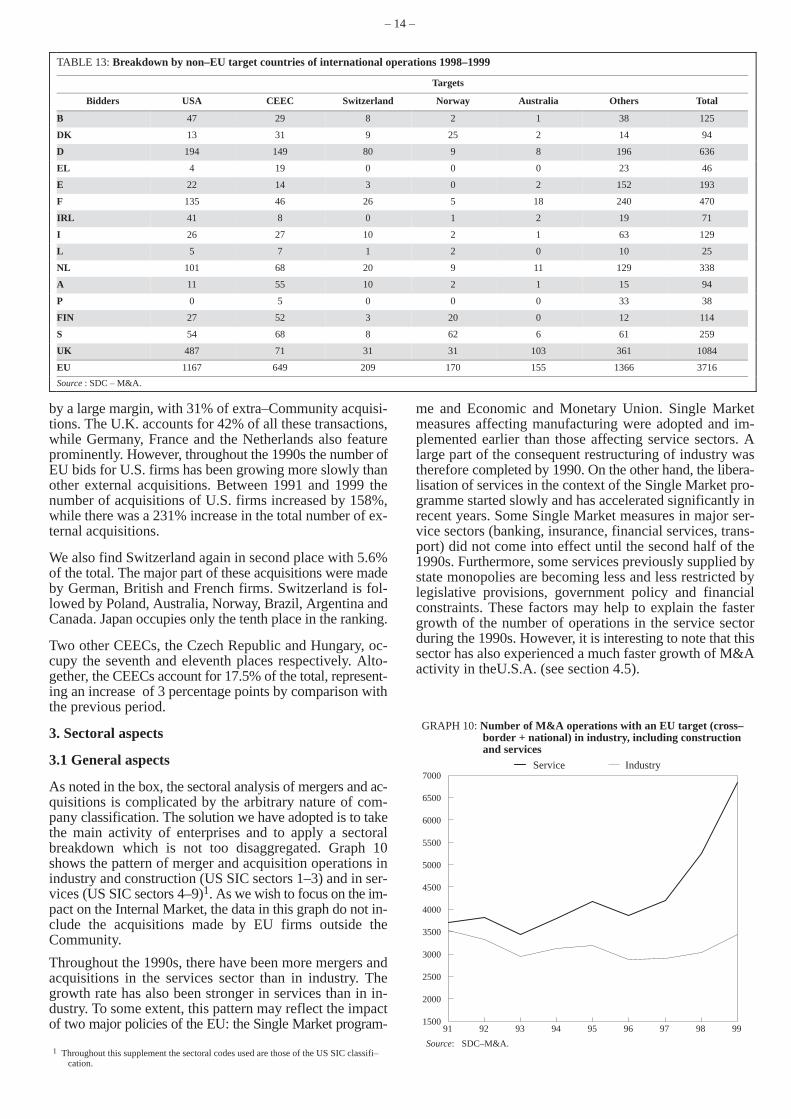

There were nearly 3000 acquisitions of Community firmsby non–Community firms in the period 1998–99. Table 12gives a breakdown by Member State of the acquisitionsmade in that period by the main extra–Community biddercountries.

As during the period 1996–1997, the U.S.A. remains themain source of bids, accounting for 63% of all acquisitionsby non–EU companies. British, German and French firmswere targeted most frequently, with a strong predilectionfor UK firms. Over the period 1991–1999, the number of

GRAPH 9: Average value per operation at Community and Inter-national levels (million euro)

Source: SDC–M&A.

Community Ops International Ops

1991 1992 1993 1994 1995 1996 1997 1998 19990

50

100

150

200

250

acquisitions made by U.S. companies in the EU has grownmuch more rapidly than acquisitions by other non–EUfirms, having increased by 126% over the whole period,compared to an average increase for all inward M&A ofonly 36%.

Switzerland ranks second as a bidder country with 7.4%,Germany being by far the preferred target country. Canadaand Norway occupy the third and fourth places with re-spectively 5% and 3.6%. The U.K., France and Germanyare the countries most targeted by Canadian firms. As onemight expect, Swedish and Danish firms account for morethan half of the acquisitions made by Norwegian firms, butBritish and Finnish companies also account for a large per-centage (11 % each). Japanese firms’ acquisitions accountonly for 2.3% against 3.5 % in the previous period. This de-crease is very probably linked to the consequences of theAsian turmoil of recent years. Japanese interest remainsmainly focussed on the U.K, followed at some distance byGermany, the Netherlands and Italy. French companieswere less targeted by Japanese firms than in the previousperiod.

In 1998–1999, over 3700 acquisitions were made by EUcompanies in non–member countries. Table 13 presents thedata for the main countries where extra–Community ac-quisitions were made.

Not surprisingly, we once again find that the U.S.A. leads

TABLE 12: Breakdown by EU target countries of international operations 1998–1999

Targets

Bidders B DK D EL E F IRL I L NL A P FIN S UK EU

USA 52 28 300 9 88 233 34 122 9 124 22 16 16 77 753 1883

Switz. 2 7 75 1 12 23 3 34 0 10 8 2 4 14 25 220

Canada 1 1 18 1 10 23 1 8 1 14 6 1 0 6 58 149

Norway 1 19 8 0 1 3 2 0 0 1 0 0 12 50 12 109

Japan 1 4 11 1 2 5 2 7 0 8 1 1 1 3 21 68

Other 7 2 55 10 48 42 18 24 4 30 12 10 10 17 271 560

Total 64 61 467 22 161 329 60 195 14 187 49 30 43 167 1140 2989

Source : SDC – M&A.

– 14 –

TABLE 13: Breakdown by non–EU target countries of international operations 1998–1999

Targets

Bidders USA CEEC Switzerland Norway Australia Others Total

B 47 29 8 2 1 38 125

DK 13 31 9 25 2 14 94

D 194 149 80 9 8 196 636

EL 4 19 0 0 0 23 46

E 22 14 3 0 2 152 193

F 135 46 26 5 18 240 470

IRL 41 8 0 1 2 19 71

I 26 27 10 2 1 63 129

L 5 7 1 2 0 10 25

NL 101 68 20 9 11 129 338

A 11 55 10 2 1 15 94

P 0 5 0 0 0 33 38

FIN 27 52 3 20 0 12 114

S 54 68 8 62 6 61 259

UK 487 71 31 31 103 361 1084

EU 1167 649 209 170 155 1366 3716

Source : SDC – M&A.

by a large margin, with 31% of extra–Community acquisi-tions. The U.K. accounts for 42% of all these transactions,while Germany, France and the Netherlands also featureprominently. However, throughout the 1990s the number ofEU bids for U.S. firms has been growing more slowly thanother external acquisitions. Between 1991 and 1999 thenumber of acquisitions of U.S. firms increased by 158%,while there was a 231% increase in the total number of ex-ternal acquisitions.

We also find Switzerland again in second place with 5.6%of the total. The major part of these acquisitions were madeby German, British and French firms. Switzerland is fol-lowed by Poland, Australia, Norway, Brazil, Argentina andCanada. Japan occupies only the tenth place in the ranking.

Two other CEECs, the Czech Republic and Hungary, oc-cupy the seventh and eleventh places respectively. Alto-gether, the CEECs account for 17.5% of the total, represent-ing an increase of 3 percentage points by comparison withthe previous period.

3. Sectoral aspects

3.1 General aspects

As noted in the box, the sectoral analysis of mergers and ac-quisitions is complicated by the arbitrary nature of com-pany classification. The solution we have adopted is to takethe main activity of enterprises and to apply a sectoralbreakdown which is not too disaggregated. Graph 10shows the pattern of merger and acquisition operations inindustry and construction (US SIC sectors 1–3) and in ser-vices (US SIC sectors 4–9)1. As we wish to focus on the im-pact on the Internal Market, the data in this graph do not in-clude the acquisitions made by EU firms outside theCommunity.

Throughout the 1990s, there have been more mergers andacquisitions in the services sector than in industry. Thegrowth rate has also been stronger in services than in in-dustry. To some extent, this pattern may reflect the impactof two major policies of the EU: the Single Market program-

1 Throughout this supplement the sectoral codes used are those of the US SIC classifi–cation.

me and Economic and Monetary Union. Single Marketmeasures affecting manufacturing were adopted and im-plemented earlier than those affecting service sectors. Alarge part of the consequent restructuring of industry wastherefore completed by 1990. On the other hand, the libera-lisation of services in the context of the Single Market pro-gramme started slowly and has accelerated significantly inrecent years. Some Single Market measures in major ser-vice sectors (banking, insurance, financial services, trans-port) did not come into effect until the second half of the1990s. Furthermore, some services previously supplied bystate monopolies are becoming less and less restricted bylegislative provisions, government policy and financialconstraints. These factors may help to explain the fastergrowth of the number of operations in the service sectorduring the 1990s. However, it is interesting to note that thissector has also experienced a much faster growth of M&Aactivity in theU.S.A. (see section 4.5).

GRAPH 10: Number of M&A operations with an EU target (cross–border + national) in industry, including constructionand services

Source: SDC–M&A.

Service Industry

91 92 93 94 95 96 97 98 991500

2000

2500

3000

3500

4000

4500

5000

5500

6000

6500

7000

– 15 –

GRAPH 11: Sectoral breakdown of cross–border M&A operations with an EU target, 1998–1999

0: Agric., forestry, fisheries1: Mining, construction2: Food, textiles, paper, chemicals etc.3: Glass, plastics, metals, machinery,

computers, transport equipment etc.4: Network industries5: Distribution6: Finance, insurance, real estate7: Hotels, personal, business services etc.8: Health, legal, social, engineering &

management services etc.9: Public administration

ÈÈÈÈÈÈÈÈÈÈÈÈÈÈÈÈÈÈÈÈÈÈÈÈÈÈÈÈÈÈÈÈÈÈÈÈÈÈÈÈÈÈÇÇÇÇÇÇÇÇÇÇÇÇÇÇÇÇÇÇÇÇÇÇÇÇÇÇÇÇ

ÉÉÉÉÉÉÉÉÉÉÉÉÉÉÉÉÉÉÉÉÉÉÉÉÉÉÉÉÉÉÉÉÉÉÉÉÉÉÉÉÉÉÉÉÉÉÉÉ

8+95%

720%

611%

511% 4

11%

3 24%

2 15%

0+1 3%

Economic and Monetary Union may have been anothercontributory factor, especially since the initiation of thesecond stage on 1 January 1994. However, the evolution ofM&A operations targeting EU companies in the sectormost affected by monetary union, banking and finance,shows no identifiable EMU effect (see section 1.2).

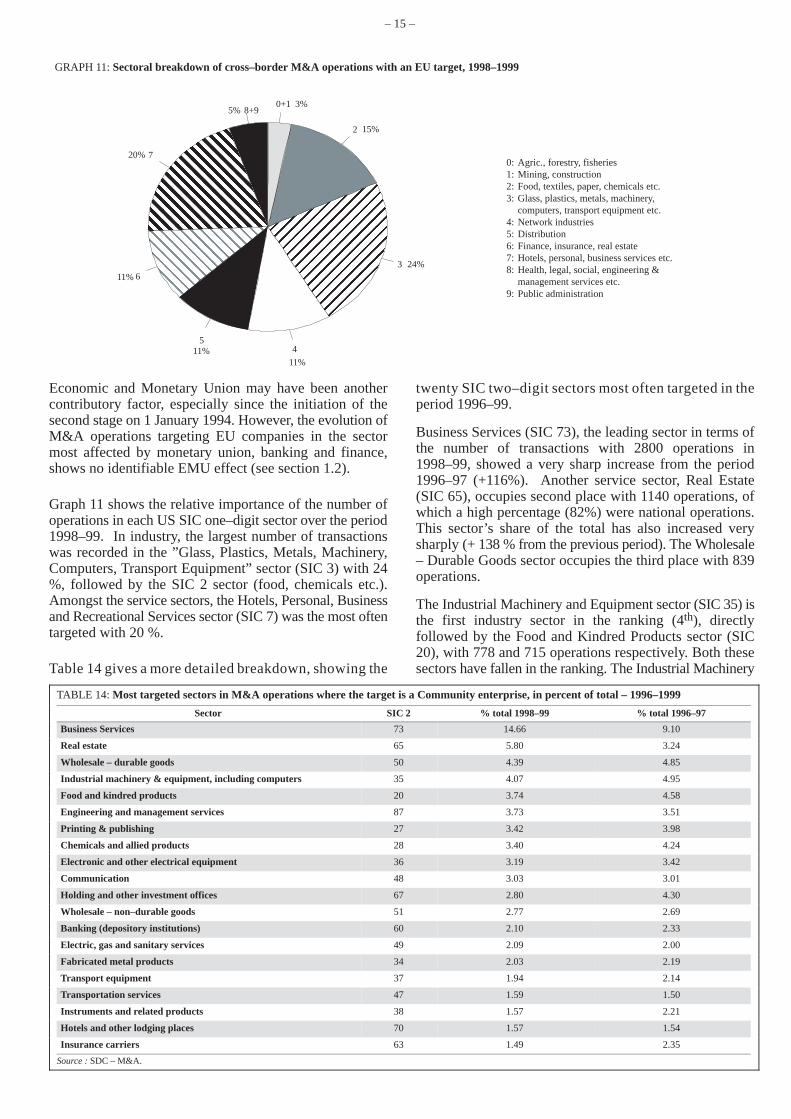

Graph 11 shows the relative importance of the number ofoperations in each US SIC one–digit sector over the period1998–99. In industry, the largest number of transactionswas recorded in the ”Glass, Plastics, Metals, Machinery,Computers, Transport Equipment” sector (SIC 3) with 24%, followed by the SIC 2 sector (food, chemicals etc.).Amongst the service sectors, the Hotels, Personal, Businessand Recreational Services sector (SIC 7) was the most oftentargeted with 20 %.

Table 14 gives a more detailed breakdown, showing the

twenty SIC two–digit sectors most often targeted in theperiod 1996–99.

Business Services (SIC 73), the leading sector in terms ofthe number of transactions with 2800 operations in1998–99, showed a very sharp increase from the period1996–97 (+116%). Another service sector, Real Estate(SIC 65), occupies second place with 1140 operations, ofwhich a high percentage (82%) were national operations.This sector’s share of the total has also increased verysharply (+ 138 % from the previous period). The Wholesale– Durable Goods sector occupies the third place with 839operations.

The Industrial Machinery and Equipment sector (SIC 35) isthe first industry sector in the ranking (4th), directlyfollowed by the Food and Kindred Products sector (SIC20), with 778 and 715 operations respectively. Both thesesectors have fallen in the ranking. The Industrial Machinery

TABLE 14: Most targeted sectors in M&A operations where the target is a Community enterprise, in percent of total – 1996–1999

Sector SIC 2 % total 1998–99 % total 1996–97

Business Services 73 14.66 9.10

Real estate 65 5.80 3.24

Wholesale – durable goods 50 4.39 4.85

Industrial machinery & equipment, including computers 35 4.07 4.95

Food and kindred products 20 3.74 4.58

Engineering and management services 87 3.73 3.51

Printing & publishing 27 3.42 3.98

Chemicals and allied products 28 3.40 4.24

Electronic and other electrical equipment 36 3.19 3.42

Communication 48 3.03 3.01

Holding and other investment offices 67 2.80 4.30

Wholesale – non–durable goods 51 2.77 2.69

Banking (depository institutions) 60 2.10 2.33

Electric, gas and sanitary services 49 2.09 2.00

Fabricated metal products 34 2.03 2.19

Transport equipment 37 1.94 2.14

Transportation services 47 1.59 1.50

Instruments and related products 38 1.57 2.21

Hotels and other lodging places 70 1.57 1.54

Insurance carriers 63 1.49 2.35

Source : SDC – M&A.

– 16 –

and Equipment sector occupied the second place in1996–97, while the Food sector was fourth.

3.2 Focus on the most targeted industry and servicessectors (SIC 73 and SIC 35)

As Table 14 shows, the Business Services sector (SIC 73)and the Industrial Machinery & Equipment sector (SIC 35)are by far the most targeted sectors in their branches. Wehave therefore chosen to examine these two sectors in moredetail.

3.2.1 Business services

Within this sector, the most targeted sub–sector has beenComputer Programming Services (SIC 7371) with 1804operations, followed by the Detective, Guard and Ar-moured Car sub–sector (SIC 7381) with 326 operations(see Table 15).

By comparison with the period 1996–1997, Computer Pro-gramming Services were the only sub–sector to have in-creased its share. The main reasons that could explain thissharp increase are the development of e–commerce and thedevelopment of new commercial products and platformsfor business systems.

3.2.2 Industrial Machinery & Equipment industry

In the Industrial Machinery & Equipment industry (SIC35), the main targeted sub–sector was Electronic Com-puters (SIC 3571). The other well–represented sub–sectorswere Pumps and Pumping Equipment (SIC 3561), Con-struction Machinery (SIC 3531) and Textile Machinery(SIC 3552) (see Table 16).

By comparison with the period 1996–97, the share of theElectronic Computers sub–sector increased slightly in theyears 1998–99, while that of Pumps and Pumping Equip-ment increased rather more sharply. The main reason forthese increases may lie in the fragmentation of the sub–sec-tors in terms of diversity of products. Through the purchaseof small specialised companies, mergers allow companiesto avoid R&D efforts in each ”niche” and to offer a broaderrange of products to their customers.

PART B: COMPARISON WITH THE USA

In this section, we distinguish between intra–EU and extra–EU operations. Intra–EU operations include National andCommunity operations while extra–EU refers to interna-tional operations of EU firms (as targets or as bidders). Forthe USA, we will use the terms intra–US for national oper-ations and extra–US for international operations by USfirms (as targets or as bidders).

1. Evolution of M&A operations

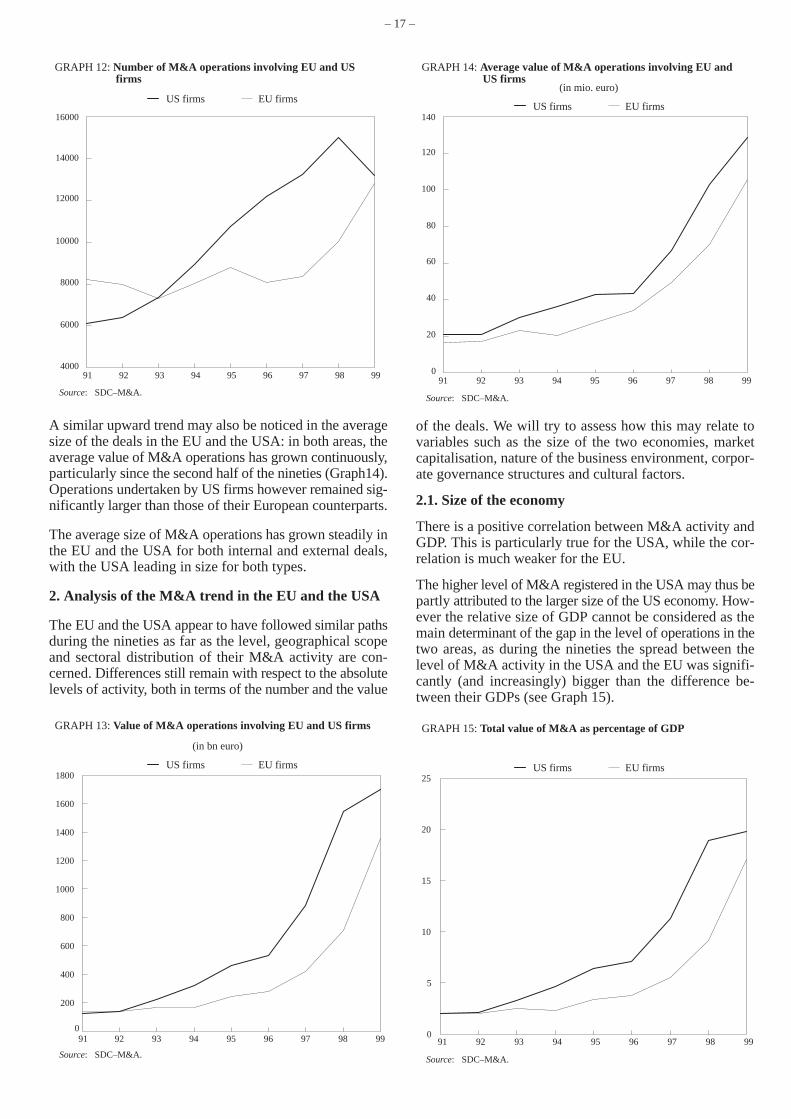

Over the nineties, M&A operations carried out by EU andUS firms displayed an overall similar and upward trend,particularly since 1993 (Graphs 12 and 13). US firmsnevertheless remained significantly more active than Euro-pean ones, in terms both of number and of value of M&Aoperations undertaken. The gap in the number and value ofoperations between the EU and the USA has been constant-ly increasing, with the exception of 1999, when M&A ac-tivity in the USA appears to have fallen suddenly2.

2 A more conclusive assessment of the trend will be possible when the data for 2000 are available, which will put the figures for 1999 in perspective.

TABLE 15: Targeted sector US SIC 73 – Business services (cross–border + national) 1998–99

Targeted sector SIC 4 Number 98–99 % total 98–99 % total 96–97

Computer programming services 7371 1804 64.43 53.47

Detective, guard and armoured car services 7381 326 11.64 17.21

Advertising agencies 7311 240 8.57 10.11

Employment agencies 7361 187 6.68 8.18

Medical equipment rental 7352 109 3.89 4.94

Disinfecting and pest control services 7342 80 2.86 2.78

Direct mail advertising services 7331 54 1.93 3.32

Total 2800 100.00 100.00

Source : SDC – M&A.

TABLE 16: Targeted sector US SIC 35 – machinery & computer equipment industry (cross–border + national) 1998–99

Targeted sector SIC 4 Number 98–99 % total 98–99 % total 96–97

Electronic computers 3571 138 17.74 17.60

Pumps and pumping equipment 3561 122 15.68 13.90

Construction machinery 3531 116 14.91 15.69

Textile machinery 3552 115 14.78 15.94

Automatic vending machines 3581 99 12.72 12.63

Machine tools, metal cutting types 3541 84 10.80 10.33

Others 3591 48 6.17 6.12

Turbines & turbine generator sets 3511 35 4.50 4.21

Farm machinery and equipment 3523 21 2.70 3.57

Total 778 100.00 100.00

Source : SDC – M&A.

– 17 –

GRAPH 12: Number of M&A operations involving EU and USfirms

Source: SDC–M&A.

US firms EU firms

91 92 93 94 95 96 97 98 994000

6000

8000

10000

12000

14000

16000

A similar upward trend may also be noticed in the averagesize of the deals in the EU and the USA: in both areas, theaverage value of M&A operations has grown continuously,particularly since the second half of the nineties (Graph14).Operations undertaken by US firms however remained sig-nificantly larger than those of their European counterparts.

The average size of M&A operations has grown steadily inthe EU and the USA for both internal and external deals,with the USA leading in size for both types.

2. Analysis of the M&A trend in the EU and the USA

The EU and the USA appear to have followed similar pathsduring the nineties as far as the level, geographical scopeand sectoral distribution of their M&A activity are con-cerned. Differences still remain with respect to the absolutelevels of activity, both in terms of the number and the value

GRAPH 13: Value of M&A operations involving EU and US firms

Source: SDC–M&A.

US firms EU firms

91 92 93 94 95 96 97 98 990

200

400

600

800

1000

1200

1400

1600

1800

(in bn euro)

GRAPH 14: Average value of M&A operations involving EU andUS firms

Source: SDC–M&A.

US firms EU firms

(in mio. euro)

91 92 93 94 95 96 97 98 990

20

40

60

80

100

120

140

of the deals. We will try to assess how this may relate tovariables such as the size of the two economies, marketcapitalisation, nature of the business environment, corpor-ate governance structures and cultural factors.

2.1. Size of the economy

There is a positive correlation between M&A activity andGDP. This is particularly true for the USA, while the cor-relation is much weaker for the EU.

The higher level of M&A registered in the USA may thus bepartly attributed to the larger size of the US economy. How-ever the relative size of GDP cannot be considered as themain determinant of the gap in the level of operations in thetwo areas, as during the nineties the spread between thelevel of M&A activity in the USA and the EU was signifi-cantly (and increasingly) bigger than the difference be-tween their GDPs (see Graph 15).

GRAPH 15: Total value of M&A as percentage of GDP

Source: SDC–M&A.

US firms EU firms

91 92 93 94 95 96 97 98 990

5

10

15

20

25

– 18 –

2.2 Market capitalisation

The degree of market capitalisation (i.e. the recourse offirms to equity) appears a more decisive factor in explain-ing the different level of M&A operations in the two areas.Market capitalisation has a positive influence on the abilityof firms to undertake M&A, both in terms of quicker accessto finance to fund the operation and of higher transparencyof the market for corporate control.

During the nineties, market capitalisation in the USA wason average 60% higher than in the EU, signalling a higherpropensity of US firms to make use of equity financing andto be involved in operations entailing the use of equity, suchas M&A. However, if we extrapolate from the regressionanalysis described in section 1.1, we would expect the levelof M&A activity in the USA to be considerably higher thanit is. This suggests that the elasticity of M&A activity withrespect to market capitalisation may be lower when thelatter reaches very high values.

2.3 Regulatory environment

Differences in the regulatory environment, particularly itsfriendliness to business activity and to market mechanismsgenerally, may also be a factor at the basis of the differentlevels of M&A activity in the two areas. A market–friendlyeconomic environment is expected to have a positive (al-though indirect) impact on M&A levels by virtue of its in-terrelations with the level of competition on the market, thedegree of economic efficiency and innovation, access toventure capital and freedom of firms to pursue their marketpositioning strategies.

Studies focusing on product markets3 show that, at the endof the nineties, the USA was among the countries with theleast restrictive regulatory environments. It is worth notingthat in the EU, the UK and Ireland were also characterisedby market–oriented economic and administrative environ-ments. On the other hand, the majority of continental Euro-pean countries displayed relatively restrictive regulatoryenvironments, with Italy being the most restrictive.

The efforts undertaken at the EU level, particularly sincethe second half of the nineties, to pursue market–friendlyregulatory strategies and which have generally led to theliberalisation of previously protected sectors and the reduc-tion of direct state control over the economy, prompted therestructuring of a number of industries leading to higher le-vels of M&A, with sectors such as telecoms and energybeing among the most dynamic. Coupled with quick tech-nological change, the evolution of the regulatory environ-ment may in part explain the strong rise in M&A activity inthe EU during the second half of the nineties.

2.4 Corporate governance

The level of M&A activity appears to be positively relatedto the dispersion of shareholdings. Generally speaking,companies owned by a single or large shareholders are like-ly to display less propensity to get involved in equity oper-ations and will also be less likely to be the object of a bid, atleast on the stock exchange. Clearly this does not rule outthe possibility of deals occurring as a result of private ne-gotiations.

3 “Cross–country patterns of product market regulation”, OECD 1999.

With the exception of the UK and Ireland, the EU marketfor corporate governance is still dominated by the presenceof large and powerful shareholders, mainly families, hold-ing companies and other non–financial companies. Thiscontrasts strongly with the USA, where the control of com-panies is more atomised and markets have a greater role indeciding the outcome of contests for control.

The analysis of the structure of voting rights provides someinteresting insights on the organisation of corporate con-trol. At the end of the nineties, in some of the largest conti-nental European countries (France, Germany and Italy),large shareholders whose vote exceeded 50% of the totalvotes owned the majority of companies listed on the stockexchange. The situation was quite different in the US,where shareholders with over 50% of voting rights con-trolled just 10% of all companies. In the USA, the averagevoting block of the largest shareholder was at least 50%lower than in the EU, with the notable exception of the UKwhich closely resembles the US structure of corporate gov-ernance.

2.5 Cultural factors

Cultural factors such as confidence in the capital markets,risk aversion and preference for national deals seem to playa role in determining the level of M&A activity. While inthe past EU firms have certainly behaved more conserva-tively than their US counterparts, the situation has started toevolve rapidly, with large and increasingly audacious dealsbecoming frequent events on the EU economic scene.

3. Geographical spread

Similarities between the M&A operations conducted in theEU and USA also emerge when looking at their geographi-cal scope: for both areas, internal operations representedthe great majority of the deals (Table 17). This is particular-ly true for the USA, where domestic deals accounted on av-erage for over 78% of the deals. The equivalent figure forthe EU was 74%.

Considering the development of the geographical spread ofthe activities, while EU operations became increasingly in-ternational over time, the proportion of international dealsby US companies was more stable. Within the category ofinternational operations, for both the EU and the USA,M&A operations where firms from the area were biddinggrew more rapidly than deals where firms from the areawere the targets of the operation. The EU and the USA seemtherefore to have shared the same dynamism in interna-tional M&A, pursuing an active strategy of internationalexpansion.

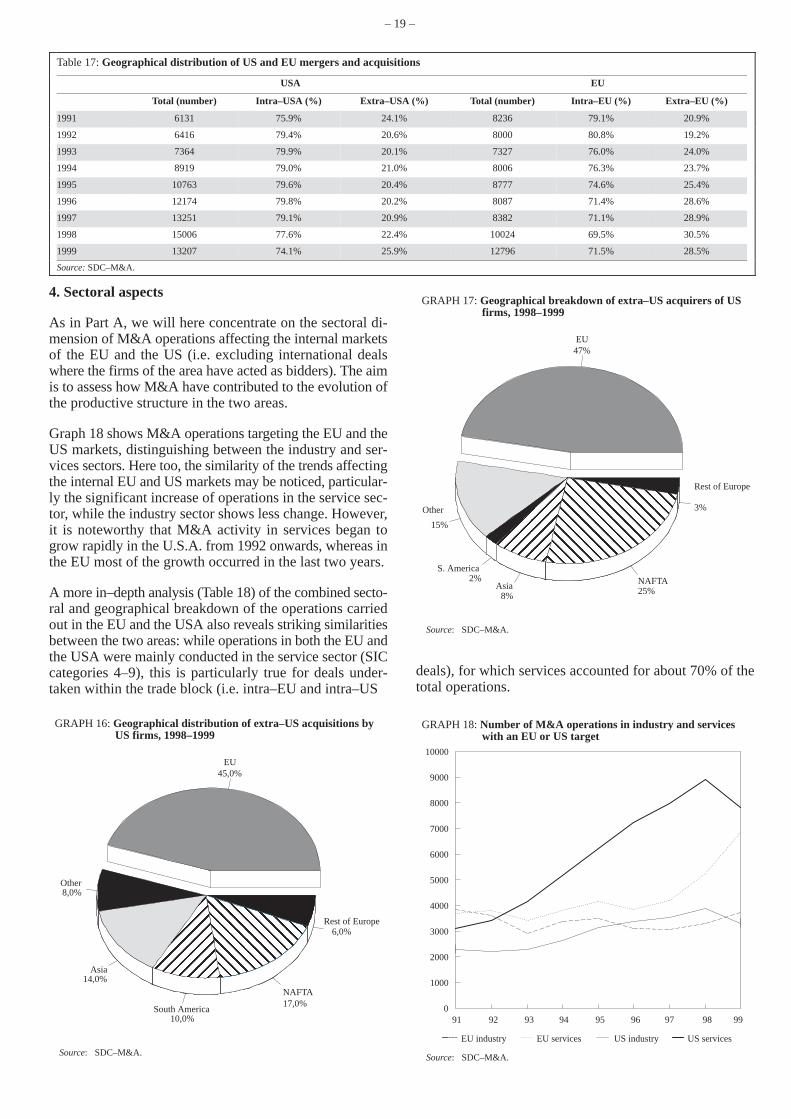

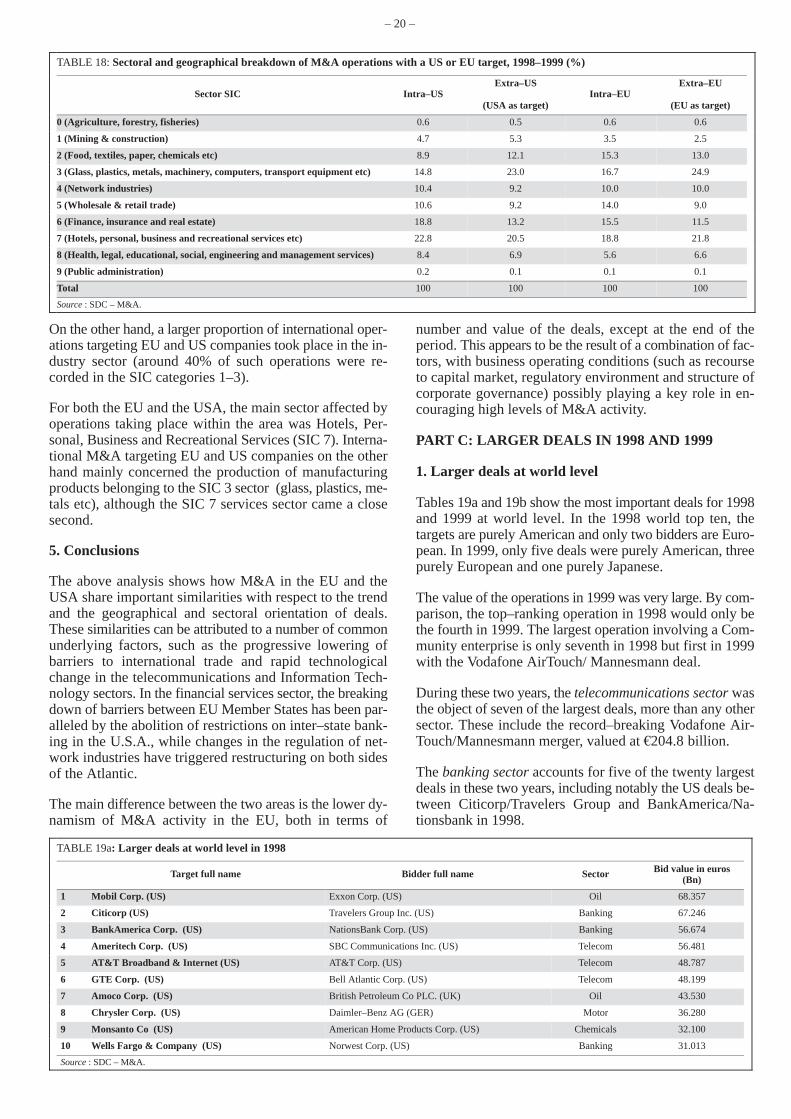

Looking more closely at the geographical distribution ofUS international operations, graphs 16 and 17 show that,both as bidder and target, the main partner of US firms wasthe EU, with over 45 % of operations. As in the case of theEU, factors such as geographic and cultural proximity andsimilarity of economic structures appear to play an import-ant role in determining the direction and intensity of M&Aoperations (in this respect, it is worth noting that the mainUS partner in the EU for M&A is the UK). The importanceof these factors seems also to be confirmed by the high per-centage of US international operations undertaken withinthe NAFTA trade block, particularly with Canada.

– 19 –

Table 17: Geographical distribution of US and EU mergers and acquisitions

USA EU

Total (number) Intra–USA (%) Extra–USA (%) Total (number) Intra–EU (%) Extra–EU (%)

1991 6131 75.9% 24.1% 8236 79.1% 20.9%

1992 6416 79.4% 20.6% 8000 80.8% 19.2%

1993 7364 79.9% 20.1% 7327 76.0% 24.0%

1994 8919 79.0% 21.0% 8006 76.3% 23.7%

1995 10763 79.6% 20.4% 8777 74.6% 25.4%

1996 12174 79.8% 20.2% 8087 71.4% 28.6%

1997 13251 79.1% 20.9% 8382 71.1% 28.9%

1998 15006 77.6% 22.4% 10024 69.5% 30.5%

1999 13207 74.1% 25.9% 12796 71.5% 28.5%

Source: SDC–M&A.

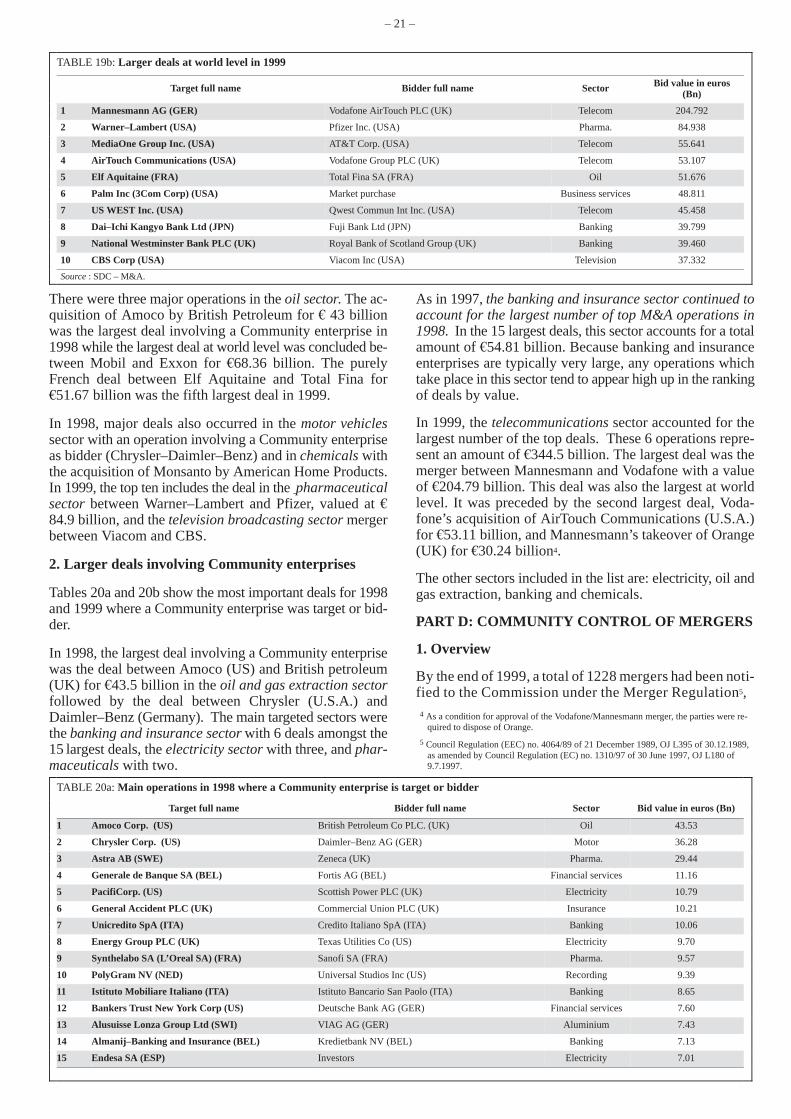

4. Sectoral aspects

As in Part A, we will here concentrate on the sectoral di-mension of M&A operations affecting the internal marketsof the EU and the US (i.e. excluding international dealswhere the firms of the area have acted as bidders). The aimis to assess how M&A have contributed to the evolution ofthe productive structure in the two areas.

Graph 18 shows M&A operations targeting the EU and theUS markets, distinguishing between the industry and ser-vices sectors. Here too, the similarity of the trends affectingthe internal EU and US markets may be noticed, particular-ly the significant increase of operations in the service sec-tor, while the industry sector shows less change. However,it is noteworthy that M&A activity in services began togrow rapidly in the U.S.A. from 1992 onwards, whereas inthe EU most of the growth occurred in the last two years.