Embed Size (px)

Citation preview

European Construction OutlookEuropean Construction Outlook

Laura Hanlon

Product Manager, Global Construction Outlook

June 23, 2009

Copyright © 2009 IHS Global Insight. All Rights Reserved.

What This Means for You

• Like most of the developed world, Europe will also be hit with the steepest decline in construction spend in at least 20 years

• The financial crisis has hit Western Europe hard, in part due tobanks’ high leverage and exposure to Eastern Europe

• Fiscal stimulus, together with financial rescue from the IMF, will gradually ease the credit crunch and improve the construction outlook

• Bottom Line: The European construction market is unlikely to recover before 2011, and recovery in the medium-term will lag the rest of the world

Copyright © 2009 IHS Global Insight. All Rights Reserved.

-6

-4

-2

0

2

Germany U.K. France Italy Spain

2008 2009 2010 2011

(Real GDP, percent change)

Recessions in Western Europe

Likely to Linger into 2010

Copyright © 2009 IHS Global Insight. All Rights Reserved.

Western European

Total Construction Outlook

• Western Europe will endure the second-worst market conditions this year and is expected to experience the worst recovery going forward

-8%

-6%

-4%

-2%

0%

2%

4%

6%

8%

10%

2000 2002 2004 2006 2008 2010 2012 2014 2016 2018

Ye

ar-

Ov

er-

Ye

ar

Gro

wth

World

WesternEurope

Copyright © 2009 IHS Global Insight. All Rights Reserved.

Western Europe Losing Share of

Global Construction Market

2018

Asia

43%

North America

18%

South America

4%

Western Europe

26%

MidEast and

Africa

4%

Eastern Europe

5%

2008

Asia

34%

Eastern Europe

5%

MidEast and

Africa

4%

North America

20%

South America

4%

Western Europe

33%

Copyright © 2009 IHS Global Insight. All Rights Reserved.

Dominant Western European

Construction Markets

Allocation of Western European Construction Spend, 2008

Note: Rest of Region includes Austria, Belgium, Denmark, Finland, Greece, Ireland, Norway, Portugal, Sweden, Switzerland, and Turkey — each which make up 2-3% of Western European total construction.

United

Kingdom

15%

Spain

16%

France

15%Italy

13%

Germany

13%

Rest of Region

23%

Netherlands

6%

Copyright © 2009 IHS Global Insight. All Rights Reserved.

Dominant Western European

Construction Market Outlooks

• The construction market lags that of the economic cycle

-16%

-14%

-12%

-10%

-8%

-6%

-4%

-2%

0%

2%

4%

6%

United

Kingdom

Spain France Netherlands Italy Germany

2009 2010 2011 2012

Copyright © 2009 IHS Global Insight. All Rights Reserved.

Total Construction Outlook

Regional Comparison

0.3%

-0.3%

-0.3%

-0.3%

-0.5%

-2.6%

-4.4%

-1.1%

2.1%

-5% -4% -3% -2% -1% 0% 1% 2% 3%

Rest of Region*

Netherlands

Germany

France

Italy

Spain

United Kingdom

Western Europe

World

Compound Annual Growth Rate 2008-13

• Deteriorating economic conditions, paired with the unrelenting high value of the euro, have created a meager and expensive environment for construction

Copyright © 2009 IHS Global Insight. All Rights Reserved.

-50 -25 0 25 50 75 100 125 150 175 200

Japan

Hong Kong

Canada

United States

Italy

Sweden

United Kingdom

France

Australia

Spain

Ireland

2007 Q4 - 2008 Q4 1997-2008

Housing Prices Soared

in Many Countries

Source: The Economist, December 6, 2008

• Some of the worst contractions are seen in Western Europe

Copyright © 2009 IHS Global Insight. All Rights Reserved.

Residential Construction Outlook

Regional Comparison

-1.7%

-0.7%

-1.4%

-1.7%

-3.0%

-10.8%

-8.0%

-3.9%

0.5%

-13% -12% -11% -10% -9% -8% -7% -6% -5% -4% -3% -2% -1% 0% 1% 2%

Rest of Region*

Netherlands

Italy

Germany

France

Spain

United Kingdom

Western Europe

World

Compound Annual Growth Rate 2008-13

• Housing bubble bursts are taking the heaviest tolls on the United Kingdom and Spain

Copyright © 2009 IHS Global Insight. All Rights Reserved.

Structures Construction Outlook

Regional Comparison

-0.1%

-0.1%

-0.4%

-0.5%

-4.4%

-4.2%

-4.8%

-2.1%

1.3%

-6% -5% -4% -3% -2% -1% 0% 1% 2%

Rest of Region*

Netherlands

France

Italy

Germany

Spain

United Kingdom

Western Europe

World

Compound Annual Growth Rate 2008-13

• While Germany avoided the real estate bubble, the collapse of exports hasreally affected the nonresidential construction market

Copyright © 2009 IHS Global Insight. All Rights Reserved.

Composition of Nonresidential

Structures Construction Markets

28%

24%23%

25%

UK

18%

28%

18%

36%

Spain

22%

17%

43%

18%

Germany

20%

38%

15%

27%

Italy

28%

21%20%

31%

Office

Commercial

Institutional

Industrial

France

Copyright © 2009 IHS Global Insight. All Rights Reserved.

Infrastructure Construction

Outlook Regional Comparison

3.9%

0.3%

1.6%

4.6%

6.1%

6.8%

7.1%

4.8%

5.1%

-1% 0% 1% 2% 3% 4% 5% 6% 7% 8%

Rest of Region*

Netherlands

Italy

France

United Kingdom

Spain

Germany

Western Europe

World

Compound Annual Growth Rate 2008-13

Copyright © 2009 IHS Global Insight. All Rights Reserved.

Sources of Infrastructure Growth

In Western Europe

•Country-specific stimulus packages

•Large transport programs co-funded by EC in the context of the development of the trans-European transport network (TEN-T)

•City traffic de-congestion a priority for most countries

•Environmental concerns push investment in energy, railways and urban transport

•London Olympics in 2012 — program focuses on rail systems

Copyright © 2009 IHS Global Insight. All Rights Reserved.

Western European

Stimulus Packages

• Slower recoveries in Europe are in part a function of less-aggressive stimulus policies

5% energy efficient construction

80% public works infrastructure10.5 billion14.4 billionSpain

100% infrastructure projects5 billion114 billionItaly

4% other transport infrastructure

10% housing construction

80% rail and energy infrastructure6.3 billion34.5 billionFrance

9% other transport infrastructure

13% energy efficient construction

20% education construction

55% road and rail repair32.4 billion81 billionGermany

24% motorways and roads

26% housing investment

27% education construction

4.6 billion31 billionUnited Kingdom

Construction Stimulus Details (Approximation)Construction StimulusTotal StimulusCountry

Copyright © 2009 IHS Global Insight. All Rights Reserved.

Scandinavian Countries See

Slightly More Modest Declines

• The region is gradually becoming more distressed by the global credit squeeze as business and consumer investment continue to weaken �

The construction outlook follows accordingly:

-8%

-6%

-4%

-2%

0%

2%

4%

6%

Denmark Finland Norway Sweden

2009 2010 2011 2012

Copyright © 2009 IHS Global Insight. All Rights Reserved.

Infrastructure LeadsScandinavian Construction Outlook

4.0%

0.3%

-1.5%

0.6%

-4% -3% -2% -1% 1% 2% 3% 4% 5%

Infrastructure

Structures

Residential

Total

Compound Annual Growth Rate 2008-13

Copyright © 2009 IHS Global Insight. All Rights Reserved.

Eastern European Construction Fares Better than Western Europe

-6%

-4%

-2%

0%

2%

4%

6%

8%

10%

12%

14%

16%

18%

2004 2006 2008 2010 2012 2014 2016 2018

Ye

ar-

Ov

er-

Ye

ar

Gro

wth

World

EasternEurope

Copyright © 2009 IHS Global Insight. All Rights Reserved.

But Eastern Europe Still Facing

Challenges in the Near-Term

• Main export markets are in recession

• Tight credit conditions threaten domestic demand which has been driven by credit expansion based largely on foreign borrowing

• Business and consumer confidence has eroded

• Lower oil prices inflict even more pain

Copyright © 2009 IHS Global Insight. All Rights Reserved.

-6

-4

-2

0

2

4

6

8

Russia Turkey Poland Czech

Republic

Hungary Romania

2008 2009 2010 2011

Real GDP Growth in Emerging Europe

(Percent change)

Copyright © 2009 IHS Global Insight. All Rights Reserved.

Eastern European Countries

Construction Market Outlook

(Percent change)

-20%

-15%

-10%

-5%

0%

5%

10%

15%

20%

Romania Poland Russia Bulgaria Slovakia Czech

Republic

Hungary Ukraine

2008 2009 2010 2011

Copyright © 2009 IHS Global Insight. All Rights Reserved.

Infrastructure Leads EasternEuropean Construction Markets

4.9%

1.1%

-0.6%

2.0%

-2% -1% 1% 2% 3% 4% 5% 6%

Infrastructure

Structures

Residential

Total Construction

Compound Annual Growth Rate 2008-13

Copyright © 2009 IHS Global Insight. All Rights Reserved.

IMF Programs in Eastern Europe

August 2008 – May 2009

Not yet specifiedNot yet approved*estimate:

US$25,000Stand-byTurkey

18,35755,993Total

5-May-106-May-09013,690Flexible Credit

LinePoland

ERBD: U.S. $60 million36 monthsNot yet approved*01,010Stand-byBosnia

EU: U.S.$6.76 billion, World Bank: U.S.$1.35 billion, EBRD and others: U.S.$1.35 billion3-May-114-May-094,37011,400Stand-byRomania

5-Jun-116-Mar-09162368

Stand-by/ Emergency FinancingArmenia

14-May-1115-May-097022,620Stand-bySerbia

15-Apr-1016-Jan-090351Stand-bySerbia**

11-Apr-1012-Jan-095181,618Stand-byBelarus

EU, EBRD, and EU member countries: U.S. $8.8 billion22-Mar-1123-Dec-085351,522Stand-byLatvia

Two loans from World Bank (U.S.$400 and US$500 million)4-Nov-105-Nov-084,90011,000Stand-byUkraine

EU and EU member countries: U.S. $9.1 billion5-Apr-106-Nov-086,32310,538Stand-byHungary

Northern European countries: U.S. $2.5 billion18-Nov-1019-Nov-085601,400

Stand-by/ Emergency FinancingIceland

15-Mar-1015-Sep-08288477Stand-byGeorgia

Complementary Lending to the Sovereign from other SourcesDate of Expiration

Date of Arrangement

Amount Drawn

Amount

Approved*Type of ProgramCountry

*By IMF board of Directors

** Initial program was enhanced and replaced Sources: IMF, IHS Global Insight

All data in million SDR, unless otherwise stated (U.S.$1=0.672592 SDR)

Copyright © 2009 IHS Global Insight. All Rights Reserved.

Special Focus: Russia

• Declines in commodity prices will hurt export income, a key driver of consumer and business spending

• Oil exports are declining due to capacity limits and rising domestic needs

• Expansionary monetary policies have fueled inflation

• The global financial crisis has exacerbated the stock market correction, international capital flight, and the ruble’s collapse

Copyright © 2009 IHS Global Insight. All Rights Reserved.

Crude Oil Output and Exports

Now in Decline

-10

0

10

20

2002 2003 2004 2005 2006 2007 2008

Crude Oil Output Crude Oil Exports

(Percent change from a year earlier)

Copyright © 2009 IHS Global Insight. All Rights Reserved.

-3

0

3

6

9

12

2000 2002 2004 2006 2008 2010 2012

Real GDP Growth (%)

Russia Not Expected to Recover

to 2008 Growth in Near-Term

Copyright © 2009 IHS Global Insight. All Rights Reserved.

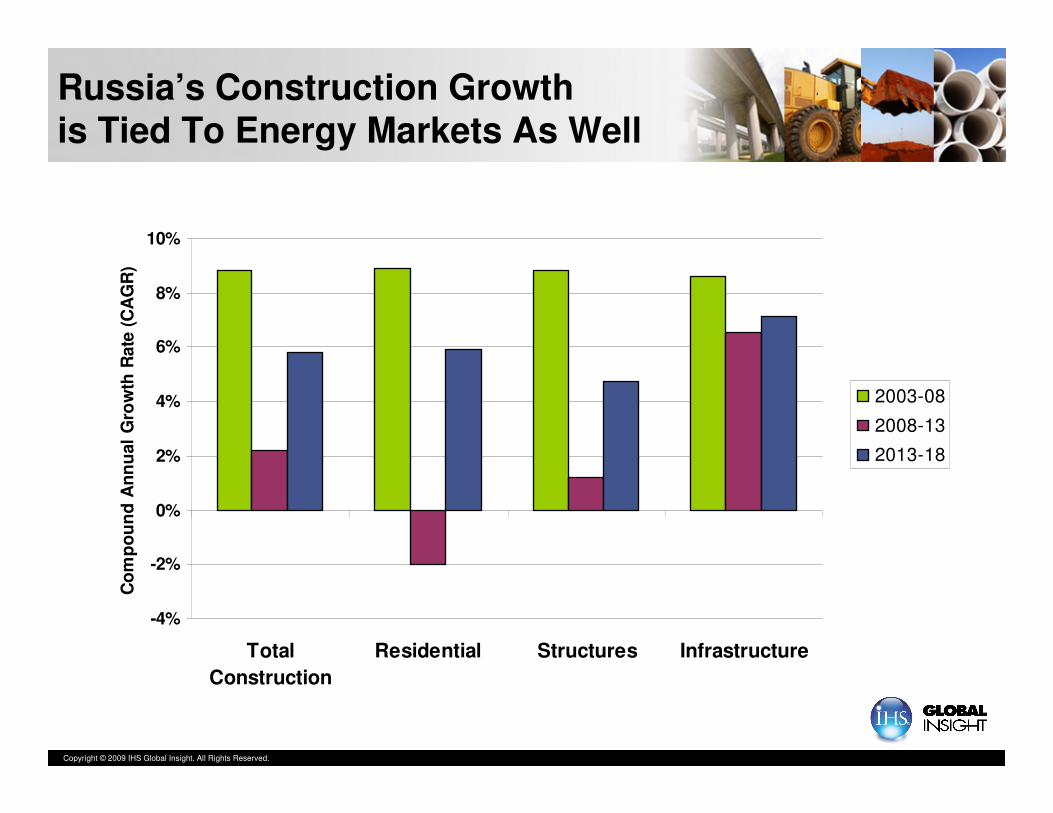

Russia’s Construction Growth is Tied To Energy Markets As Well

-4%

-2%

0%

2%

4%

6%

8%

10%

Total

Construction

Residential Structures Infrastructure

Co

mp

ou

nd

An

nu

al

Gro

wth

Rate

(C

AG

R)

2003-08

2008-13

2013-18

Copyright © 2009 IHS Global Insight. All Rights Reserved.

Summary Tables: Western Europe

12(-1.1%)(-3.9%)(-7.5%)1788.02Western Europe

13(-6.7%)(-7.8%)(-26.0%)26.07Ireland

11(-0.2%)(-2.4%)(-5.8%)29.89Finland

15+1.2%(-0.2%)(-4.0%)31.66Portugal

12+0.5%(-1.5%)(-5.7%)34.07Denmark

11+0.7%(-1.0%)(-2.9%)34.43Sweden

13+0.7%(-1.4%)(-1.3%)38.33Norway

10+0.5%(-1.0%)(-1.2%)41.11Switzerland

12+0.2%(-2.3%)(-3.3%)42.70Austria

15+1.9%(-0.3%)(-2.6%)45.92Greece

32+1.4%(-4.3%)(-4.2%)47.24Turkey

13+0.4%(-0.2%)(-3.8%)61.54Belgium

12(-0.3%)(-2.6%)(-5.5%)89.20Netherlands

14(-0.5%)(-2.3%)(-4.6%)233.81Italy

12(-0.3%)(-1.7%)(-3.7%)240.56Germany

11(-4.4%)(-10.1%)(-14.7%)242.82United Kingdom

12(-0.3%)(-3.9%)(-5.9%)269.41France

13(-2.6%)(-5.1%)(-11.9%)279.24Spain

CAGR, 2008-132009-102008-092009

Percent2005 U.S.$ Billions

Construction

Five Year Risk

Score

Total Real Construction Spending GrowthTotal Construction

Spending

Copyright © 2009 IHS Global Insight. All Rights Reserved.

Summary Tables: Eastern Europe

28+2.0%(-0.6%)(-3.9%)266.33Eastern Europe

17+4.1%+1.0%(-0.3%)7.35Bulgaria

32(-1.1%)(-3.6%)(-13.9%)9.54Ukraine

19(-0.2%)(-2.0%)(-6.4%)11.49Hungary

16+2.6%+2.5%(-2.5%)11.49Slovakia

23+3.2%+1.0%(-0.5%)24.89Romania

19+2.2%+0.3%(-5.8%)29.19Czech Republic

20+1.8%(-0.7%)(-0.1%)65.81Poland

34+2.2%(-1.2%)(-5.4%)106.55Russia

CAGR, 2008-132009-102008-092009

Percent 2005 U.S.$ Billions

Construction

Five Year Risk Score

Total Real Construction Spending GrowthTotal Construction

Spending

Copyright © 2009 IHS Global Insight. All Rights Reserved.

Implications For Your Business

• This is the worst year, and worst outlook, for the European construction market in two decades

• While fiscal stimulus and support from the IMF has certainly improved the infrastructure construction outlook in particular, growth in the European construction markets will not return to the levels enjoyed a few years ago

• Eastern Europe, although more risky, is expected to rebound more quickly than Western Europe