Embed Size (px)

Citation preview

European Banking Barometer – 2015 Reflecting a challenged industry

European Banking Barometer – 2015

Contents

Page 1 Economic environment 9 2 Business outlook and focus areas 12 3 Business priorities and product line expectations 28 4 Headcount and compensation 36 5 Contacts 45

Page 2

European Banking Barometer – 2015

Introduction

The European Banking Barometer provides an overview of the macro-economic outlook and its impact on the European banking industry, as well as the priorities banks will focus on over the next 12 months. Now in its sixth edition, the latest survey consists of 226 interviews with senior bankers across 11 markets: Austria, Belgium, France, Germany, Italy, the Netherlands, the Nordics, Poland, Spain, Switzerland and the UK.

The fieldwork was conducted via an online questionnaire and telephone interviews during November and December 2014. Respondents were interviewed from a range of financial institutions covering at least 50%* of banking assets in each market.

A range of bank types were interviewed in each market to help ensure the study was a fair reflection of each country’s banking industry. Interviews were not conducted with subsidiaries of member or group banks.

The results in this report are presented in an aggregate market format and shown in percentages. Aggregated European-wide results have been weighted in proportion to countries’ banking assets. All country-level data is unweighted.

Please note that some charts may not add up to 100%, and net increase totals may differ slightly from the numbers shown in the charts, as percentages have been rounded to the nearest whole number. Where possible, we have compared and contrasted the data with that in our European Banking Barometer – 2014.**

We would like to thank all the research participants for their contributions to the study.

If you would like to take part in our next European Banking Barometer study, please speak to your usual EY contact or refer to your local country contact on page 46.

Page 3

* Austria represents 31% of its market's banking assets. ** The European Banking Barometer – 2014 was conducted in March and April 2014, and respondents were asked about their six-month outlook, whereas the European Banking Barometer – 2015 is based on respondents' 12-month outlook.

European Banking Barometer – 2015 Page 4

Composition of the survey sample by bank type

23

13

12 14

38

Bank type*

Universal (large-scale banking group or major bank)

Corporate and investment

Private bank or wealth manager

Specialist (e.g., consumer credit, savings or a bank that doesn’t offer a current account)

Retail and business (SME business banking)

* Numbers in the pie chart reflect the percentage of respondents who answered. Percentages were calculated using unweighted data. Please note that, given the structure of the German and Swiss banking markets, respondents in these two countries were provided with country-specific bank types that have been reallocated to our five European bank types as follows: In Germany, big banks and regional banks were reallocated to universal banks; foreign banks (not headquartered in Germany) were reallocated to corporate and investment banks; private bankers were reallocated to private banks or wealth management; savings banks and cooperative banks were reallocated to retail and business banks; and central building societies, building loan associations and mortgage banks were reallocated to specialist banks. In Switzerland, major banks were reallocated to universal banks; investment banks were reallocated to corporate and investment banks; private bankers (general or limited partnership) and banks under foreign control were reallocated to private banks/wealth management; cantonal banks, and regional and savings banks were reallocated to retail and business banks; and securities traders were reallocated to specialist banks.

European Banking Barometer – 2015

Composition of the survey sample by bank type

Market Total Universal Corporate and

investment

Private bank or wealth

management Specialist

Retail and business

(cooperative)

Retail and business

(state owned)

Retail and business (privately

owned)

Austria 6 4 0 1 0 1 0 0 Belgium 21 5 2 4 1 1 1 7 France 11 5 1 0 2 1 1 1 Germany 50 9 1 3 9 9 17 2 Italy 20 5 2 0 3 8 1 1 Netherlands 7 2 1 0 3 0 1 0 Nordics 16 6 3 1 2 0 0 4 Poland 13 8 3 1 0 0 1 0 Spain 9 1 1 0 0 2 1 4 Switzerland 42 2 1 14 6 4 8 7 UK 31 5 14 2 6 1 1 2

Europe** 226 52 29 26 32 27 32 28

Page 5

Type of bank*

* Given the structure of the German and Swiss banking markets, respondents in these two countries were provided with country-specific bank types that have been reallocated to our five European bank types as follows: In Germany, big banks and regional banks were reallocated to universal banks; foreign banks (not headquartered in Germany) were reallocated to corporate and investment banks; private bankers were reallocated to private banks or wealth management; savings banks and cooperative banks were reallocated to retail and business banks; and central building societies, building loan associations and mortgage banks were reallocated to specialist banks. In Switzerland, major banks were reallocated to universal banks; investment banks were reallocated to corporate and investment banks; private bankers (general or limited partnership) and banks under foreign control were reallocated to private banks or wealth management; cantonal banks, and regional and savings banks were reallocated to retail and business banks; and securities traders were reallocated to specialist banks.

** European totals in the table reflect the unweighted number of respondents who answered. All European aggregated percentages in the report are weighted in proportion to markets’ banking assets, as reported by The Banker database in June 2014 and SNL Financial. All market level figures in this report reflect unweighted data.

European Banking Barometer – 2015

European overview

The prospects for a European economic recovery are weaker than in 2014, but most bankers remain positive about their own institution’s performance. The broad-based optimism about the economy seen in our previous edition has evaporated: just over a third of bankers now expect the economy to strengthen, and more than a quarter anticipate a deterioration in outlook.

Despite this, most bankers still expect their institution’s financial performance to improve – but only slightly, as institutions continue to grapple with a complex and evolving regulatory agenda. With the industry still struggling to deliver sustainable returns, pay expectations are more modest than in 2014.

The economic recovery will be weaker, but the (gradual) improvement in banks’ financial performance will continue.

► In 2014, 64% of respondents expected the economic outlook to improve. In our latest survey, just 38% do. Furthermore, 27% now believe that the economic outlook will deteriorate.

► Despite this, 56% of respondents still believe that the financial performance of their own bank will improve, compared with 60% in 2014. Bankers remain most positive about the outlook for private banking and wealth management; 62% believe the outlook is good for that segment. More than half of respondents also thought the outlook was good for retail banking, corporate banking, and debt and equity issuance.

► We estimate that, unless banks exceed the 3.5% revenue growth and 1.6% cost reduction they anticipate, they are likely to improve return on equity (ROE) by only around half of the 1.6% they hope to achieve.

Page 6

European Banking Barometer – 2015

European overview

The industry is now more resilient, supporting lending growth, but banks will continue to adjust their funding profiles.

► Bankers continue to expect corporate lending policies to become less restrictive across most sectors in the coming year, and 51% expect to increase lending to customers. However, as banks continue to de-risk their balance sheets, the transport, financial services, construction and commercial real estate sectors will face further restrictions.

► Banks are increasingly likely to seek funding through wholesale markets, which are now easier to access, and as ultra-low interest rates in Europe make deposit funding expensive. Forty-seven percent of respondents believe they are now more likely to seek wholesale funding, compared with 42% in 2014. By contrast, just 35% of respondents expect to introduce incentives to increase customer deposits, compared to 51% last year.

Although banks continue to look for opportunities to grow, risk and regulation remain banks’ top priorities.

► Launching initiatives to promote growth remains a key focus for many European banks: half of bankers expect this to be an area of increased focus in 2015. However, when considering banks’ overall list of priorities, innovation and growth activities are eclipsed by cost reduction and efficiency initiatives, and risk and regulatory programs. As a result, banks will continue to invest in technology as they continue to streamline process, strengthen cybersecurity and tackle financial crime.

► Risk and regulation will remain firmly at the top of bankers’ priorities in 2015. Seventy-one percent of respondents see risk management as particularly important, compared with 56% in 2014. Capital, liquidity and the leverage ratio will receive even greater attention in the coming year as the Financial Stability Board progresses its consultation on Total Loss Absorbing Capital (TLAC).

► Although reputational risk is the third most important priority for banks for 2015, developing new remuneration systems, which many see as a key driver of cultural transformation across the industry, and central to mitigating conduct risk are ranked 21st.

Page 7

European Banking Barometer – 2015

European overview

Post-AQR industry restructuring will gather pace, but sector consolidation remains some way off.

► Sector restructuring had slowed ahead of the ECB’s comprehensive assessment but, following the exercise’s completion, banks are now once more reassessing their business and geographic footprints. Asset disposals and acquisitions are likely to be driven by the structural reform agenda, with 41% of universal banks expecting to sell assets.

► Acquisitions are likely to be small in scale and focused on strengthening core businesses and existing capabilities. Significant sector consolidation remains unlikely: just 28% of banks expect large- or medium-scale consolidation in the coming year. Although 53% of bankers expect significant consolidation within three years, this has fallen from 65% in 2014.

The pace of job cuts is picking up, and pay expectations are beginning to reflect a challenged industry. ► Forty-three percent of bankers expect headcount to fall, compared with 38% in our last survey, with headcount reductions

focused in operations and IT, other head-office functions and retail banking. The UK is the only market where more respondents expect headcount to rise than fall.

► The combination of low growth, continued industry restructuring and further job cuts means bankers are now less optimistic about the prospects for industry pay. Although 22% of respondents expect aggregate pay to increase, 19% expect it to fall. Notably, although 4% expected aggregate pay to increase by over 10% in 2014, none do this year. In fact, 10% of respondents now anticipate a double-digit reduction in pay.

Page 8

European Banking Barometer – 2015

Economic environment

Page 9

Section 1

European Banking Barometer – 2015

1 26 35 35 3

Bankers are now less positive about the prospect of an economic recovery, but expectations differ widely by market

How do you expect the general economic outlook in your market to change over the next 12 months?*

Page 10

* Numbers reflect the percentage of respondents who answered. Base excludes respondents who answered “Don’t know.”

Comments: Optimism about the economic recovery had been increasing in the previous three editions of our European Banking Barometer. This edition highlights a stark reversal of that trend, pointing to a slowing economic recovery. This is in line with the International Monetary Fund’s (IMF’s) recent downward revision of Euro Area growth prospects for 2015. Just 38% of respondents expect the economic outlook to improve, compared with 64% in 2014. Furthermore, 28% expect the economic outlook to deteriorate, compared with just 9% in 2014. However, expectations vary between markets. While the bankers in the UK, Poland and Spain anticipate a stronger economy, driven by a mixture of rising consumption, investment and employment, more Belgian, French and German bankers expect their economy to contract than to grow.

1 8 27 56 8

Worsen significantly Worsen slightly Stay the same Improve slightly Improve significantly

2014

2015

European Banking Barometer – 2015

5

2

1

13

14

23

25

10

34

64

26

25

33

27

48

22

15

50

57

45

44

18

35

55

33

57

36

56

62

25

43

40

20

18

35

20

33

3

2

22

3

UK

Switzerland

Spain

Poland

Nordics

Netherlands

Italy

Germany

France

Europe

Belgium

Austria

Worsen significantly Worsen slightly Stay the same Improve slightly Improve significantly

How do you expect the general economic outlook in your market to change over the next 12 months?*

2015

Two-thirds of French bankers expect the economic outlook to worsen, but 78% of Spanish bankers expect it to improve

Page 11

2014 Net

increase Net

increase

0

-5

11

-45

-16

25

43

0

38

78

24

47

* Numbers reflect the percentage of respondents who answered. Base excludes respondents who answered “Don’t know.”

7

1

6

5

10

5

6

17

8

6

23

14

24

10

8

10

14

20

43

52

27

35

31

57

76

65

58

80

86

75

50

21

56

59

46

23

20

33

1

3

8

UK

Switzerland

Spain

Poland

Nordics

Netherlands

Italy

Germany

France

Europe

Belgium

Austria 23

53

54

0

46

70

86

70

92

80

76

74

European Banking Barometer – 2015

Business outlook and focus areas

Page 12

Section 2

European Banking Barometer – 2015

Despite a weaker economic outlook, most bankers still expect their institution’s financial performance to improve …

How do you expect your bank’s financial performance to change over the next 12 months?*

Page 13

* Numbers reflect the percentage of respondents who answered. Base excludes respondents who answered “Don’t know.”

1 13 26 50 10

Weaken significantly Weaken slightly Stay the same Strengthen slightly Strengthen significantly

2014

Comments: Cost reduction and revenue growth initiatives will gather pace, yet banks will still struggle to deliver even the modest improvement in ROE they anticipate. Across Europe, bankers expect costs to fall by an average of 1.57% – more than three times the cost reduction anticipated last year. Similarly, anticipated revenue growth of 3.46% exceeds last year’s expectation. Although respondents hope that these improvements will deliver an average improvement of 1.62% in ROE, EY analysis suggests that they will only boost ROE by around half that amount. Furthermore, European banks would need to reduce costs by about 21% and grow revenues simultaneously by 15% just to achieve their average cost of equity (9.4%). Bankers in Poland, the Netherlands and Germany actually anticipate a slight fall in ROE. By contrast, bankers in Spain, the UK, the Nordics and Austria all expect ROE increases in excess of 3.5%.

1 15 27 48 8

2015

European Banking Barometer – 2015

-6.00 -5.00 -4.00 -3.00 -2.00 -1.00 0.00 1.00 2.00 3.00 4.00 5.00 6.00UK

Switzerland

Spain

Poland

Nordics

Netherlands

Italy

Germany

France

Europe

Belgium

Austria

… but ROE growth will remain modest as banks continue to struggle to cut costs or grow revenues significantly

How do you expect your bank’s performance measures to change over the next 12 months?*

Page 14

* Numbers reflect the mean percentage change expected. Base excludes respondents who answered “Don’t know.”

Increase Percentage increase

Revenue

Average percentage change

4.10

3.19

3.46

4.14

0.79

2.63

5.00

3.00

2.33

4.17

2.24

4.57

Cost base

-5.83

-1.15

-1.57

-1.80

-0.43

-3.29

5.50

-3.58

0.75

-3.14

0.64

-2.64

ROE

4.00

2.37

1.62

0.38

-0.50

2.23

-0.25

3.77

-1.00

3.60

0.57

3.75

4.10

3.19

3.46

4.14

0.79

2.63

5.00

3.00

2.33

4.17

2.24

4.57

-5.83

-1.15

-1.57

-1.80

-0.43

-3.29

5.50

-3.58

-3.14

0.64

-2.64

4.00

2.37

1.62

0.38

2.23

3.77

-1.00

3.60

0.57

3.75

-0.25

0.75

-0.50

European Banking Barometer – 2015

Almost one-third of bankers still expect to increase their loan loss provisions …

Over the next 12 months, what do you expect your bank’s total provisions against loan losses to do?*

Page 15

* Numbers reflect the percentage of respondents who answered. Base excludes respondents who answered “Don’t know.”

Comments: Slightly more banks now expect to raise loan loss provisions (LLPs) than in 2014. Provisions are likely to rise as banks move to comply with IFRS 9, a new accounting standard due to take effect on 1 January 2018. Under the IFRS 9 standard on financial instruments, a new expected-loss impairment model will require banks to recognize not only credit losses that have already occurred, but also losses that are expected in the future. It is likely that the effect of the higher provisions will be moderate for banks that use an internal approach to calculating regulatory capital; however, the impact will be greater for banks using the Basel standardized approach. Despite this, with many European banks having significantly strengthened their balance sheets to ensure they passed last year’s ECB Asset Quality Review (AQR), 29% now expect to be able to release provisions to improve their financial performance, compared with just 23% in our previous survey.

3 26 39 28 4

1 22 46 27 3

Decrease significantly Decrease slightly Stay the same Increase slightly Increase significantly

2014

2015

European Banking Barometer – 2015

… but bankers in Austria, Belgium, Spain and the UK expect to release provisions, which may boost financial performance

Over the next 12 months, what do you expect your bank’s total provisions against loan losses to do?*

Page 16

* Numbers reflect the mean scores of respondents who answered on a scale of 1 to 5 where 1 denotes “Decrease significantly” and 5 denotes “Increase significantly.” Base excludes respondents who answered “Don’t know.”

1 2 3 4 5UK

Switzerland

Spain

Poland

Nordics

Netherlands

Italy

Germany

France

Europe

Belgium

Austria2.83

2.90

3.06

3.18

3.00

3.00

3.31

2.78

2.90

3.69

3.12

3.10

3.20

3.01

3.25

3.00

2.90

3.00

3.80

3.24

2.69

2015 2014

3.21

3.30

Decrease significantly

Increase significantly Stay the same

European Banking Barometer – 2015

38 33

27 23 19

11 24

17 11

17 17 18

18 19 19 21 25 29 30 31

39 40 44

52

More restrictive Less restrictive

34 30 30 28

21 15

25 28

17 16 12 16

29 26

21 19

33 27 26

19 24

39 36

45

Commercial real estateConstruction

Financial servicesTransport (incl. automotive and shipping)**

Retail and consumer products**Commercial and professional services**

Energy, mining and minerals**Media and telecommunications

ITManufacturing and industrials (incl. chemicals, eng.)**

Health careSMEs 29

24 23 7 -9 1 12 12 -9 -8 -4 -5

Stronger balance sheets will allow banks to loosen lending policies for most sectors

How do you expect the corporate lending policies of banks in your market to change in each of the following sectors over the next 12 months?*

Page 17

* Numbers reflect the percentage of respondents who answered. Respondents answering “Remain unchanged” are not displayed. Base excludes respondents who answered “Don’t know.” ** Energy and mining includes minerals; manufacturing includes industries, chemicals and engineering; commercial services includes professional services; retail includes consumer products; and transport includes automotive and shipping.

2015 2014 Net less

restrictive Net less

restrictive

Comments: Despite a weaker economic outlook, bankers continue to expect corporate lending policies to become less restrictive across most sectors in the coming year. As a result of recent regulatory and supervisory actions, which have contributed to improvements in banks’ funding conditions, and improved capital and liquidity positions, banks are now better positioned to expand corporate lending. However, the transport, financial services, construction and commercial real estate sectors will face further restrictions, as banks continue to de-risk their balance sheets and reduce their exposure to riskier or more capital intensive sectors. For example, the CRD IV Net Stable Funding Ratio makes it less attractive to provide longer-term loans to sectors such as shipping.

34 28 24 28 13 6 18 6 -2 -8 -14 -21

■ More restrictive ■ Less restrictive

European Banking Barometer – 2015

71 29 29

33 17 14 14

33 17

43 43

14

29 14

17 29 29

50 14

29 43

26 21

26 26 21

8 42

16 16 11

16 11

34 34

8 18

13 21

29 24 29 32 34

55

Commercial real estateConstruction

Financial servicesTransport**

Retail**Commercial services**

Energy and mining**Media and telecomms

ITManufacturing**

Health careSMEs

Austria

Germany

Belgium

Italy

France

Netherlands

Lending policies for SMEs are expected to be less restrictive in all markets except the Netherlands How do you expect the corporate lending policies of banks in your market to change in each of the following sectors over the next 12 months?*

Page 18

* Numbers reflect the percentage of respondents who answered. Respondents answering “Stay the same” are not displayed. Base excludes respondents who answered “Don’t know.” ** Energy and mining includes minerals; manufacturing includes industries, chemicals and engineering; commercial services includes professional services; retail includes consumer products; and transport includes automotive and shipping.

80 73

33 7

20 7 7

14 7

13 7

20

13 7 7

33 47

40 27

43 53

67 67

73

50 100

25 25 25

50 50

25

25

25 25

50 50

75 75

50 75

Commercial real estateConstruction

Financial servicesTransport**

Retail**Commercial services**

Energy and mining**Media and telecomms

ITManufacturing**

Health careSMEs

42 25

15 15

19 23 18

23 8 8 7

14

8 8 15 15

31 23

18 15

31 15

29 50

25 50

25 50

25 25 25 25 25 25 25

50

25

25 25

25 25

50 25 25

■ More restrictive ■ Less restrictive

European Banking Barometer – 2015

11 32 30 26 28

12 21 21

11 11 11

28

44 21 25 26

17 24

37 32

26 42

63 50

17 36

27 8

18

33

18

20 10

17 18 18

25 27

40 25

60 45

55 50

70

22 22

13

14 11

11 38

71 62

57 62

75 86 88

71 78

Nordics

Switzerland

Poland

UK

Spain

Lending policies for commercial real estate is expected to be less restrictive in the UK How do you expect the corporate lending policies of banks in your market to change in each of the following sectors over the next 12 months?*

Page 19

* Numbers reflect the percentage of respondents who answered. Respondents answering “Stay the same” are not displayed. Base excludes respondents who answered “Don’t know.” ** Energy and mining includes minerals; manufacturing includes industries, chemicals and engineering; commercial services includes professional services; retail includes consumer products; and transport includes automotive and shipping.

■ More restrictive ■ Less restrictive

45 41

27 14

18 5

36 19 18 14

18

14 9 18

9 23 23

5 29

18 32 36

32

Commercial real estateConstruction

Financial servicesTransport**

Retail**Commercial services**

Energy and mining**Media and telecomms

ITManufacturing**

Health careSMEs

30 18

33 27

18 9

45

18

9

20 9

25 9 9 18

9 36

18 18

27 36

Commercial real estateConstruction

Financial servicesTransport**

Retail**Commercial services**

Energy and mining**Media and telecomms

ITManufacturing**

Health careSMEs

European Banking Barometer – 2015

1 2 3 4 5

Launching initiatives to promote growth

Seeking funding from wholesale capital markets

Lending to customers

Selling assets outside Europe

Repaying central bank funding programs

Reducing loan to deposit ratios

Selling assets outside home markets

Introduction/increasing incentives to increase customer deposits

Reducing the balance sheet

Accessing central bank funding programs

Banks continue to prioritize growth and moving away from retail funding to cheaper wholesale funding

How likely are the banks in your market to be engaged in the following activities over the next 12 months?*

Page 20

* Numbers reflect the mean scores of respondents who answered on a scale of 1 to 5 where 1 denotes “Significantly less” and 5 denotes “Significantly more.”

Comments: Growth remains a key priority for European banks. Fifty-nine percent of respondents believe banks in their markets are more likely to launch growth initiatives this year, while 51% also expect to increase lending. Banks will also rebalance their funding mix toward wholesale funding. Capital markets are now easier to access, while deposit funding has become more expensive due to ultra-low interest rates in the Euro Area; as a result, just 35% of respondents expect to introduce incentives to increase customer deposits, compared with 51% last year.

Significantly less

Significantly more

3.64

3.52

3.39

3.31

3.29

3.21

3.19

3.14

3.10

2.88

3.59

3.32

3.42

3.22

3.27

3.26

3.24

3.44

3.17

2.61

Significantly less

Significantly more Stay the same

2015 2014

European Banking Barometer – 2015

14

29

14

14

14

29

14

57

43

43

14

14

57

14

14

43

43

29

43

29

14

14

14

14

10

25

15

10

30

15

10

5

5

5

10

10

5

5

15

5

15

25

30

25

25

35

25

40

30

60

25

10

10

5

5

20

15

30

15

15

14

5

20

20

35

30

62

33

48

14

5

10

20

10

10

19

25

29

48

15

20

25

10

5

10

25

5

5

5

10

5

14

44

24

38

27

25

35

22

18

40

22

4

4

12

4

4

4

2

10

6

4

14

35

22

13

6

24

27

29

12

31

2

13

6

6

9

10

8

2

27

55

45

45

73

45

55

36

18

36

18

18

9

9

18

36

18

36

18

9

9

9

27

9

9 50

33

67

17

17

50

33

50

17

17

17

17

17

50

17

17

17

17

33

Austria

Germany

Belgium

Italy

France

Netherlands

More than three-quarters of respondents in Italy plan to launch initiatives to promote growth

How likely are the banks in your market to be engaged in the following activities over the next 12 months?*

Page 21

* Numbers reflect the percentage of respondents who answered. Respondents answering “About the same” are not displayed. Base excludes respondents who answered “Don’t know.”

Significantly more Slightly more Significantly less Slightly less

Launching initiatives to promote growth

Seeking funding from wholesale capital markets

Lending to customers

Selling assets outside Europe

Repaying central bank funding programs

Reducing loan to deposit ratios

Selling assets outside home markets

Introduction/increasing incentives to increase customer deposits

Reducing the balance sheet

Accessing central bank funding programs

Launching initiatives to promote growth

Seeking funding from wholesale capital markets

Lending to customers

Selling assets outside Europe

Repaying central bank funding programs

Reducing loan to deposit ratios

Selling assets outside home markets

Introduction/increasing incentives to increase customer deposits

Reducing the balance sheet

Accessing central bank funding programs

European Banking Barometer – 2015

More than 74% of Polish, Spanish and British respondents are planning to launch new initiatives to promote growth

How likely are the banks in your market to be engaged in the following activities over the next 12 months?*

Page 22

* Numbers reflect the percentage of respondents who answered. Respondents answering “About the same” are not displayed. Base excludes respondents who answered “Don’t know.”

Significantly more Slightly more Significantly less Slightly less

Launching initiatives to promote growth

Seeking funding from wholesale capital markets

Lending to customers

Selling assets outside Europe

Repaying central bank funding programs

Reducing loan to deposit ratios

Selling assets outside home markets

Introduction/increasing incentives to increase customer deposits

Reducing the balance sheet

Accessing central bank funding programs

Launching initiatives to promote growth

Seeking funding from wholesale capital markets

Lending to customers

Selling assets outside Europe

Repaying central bank funding programs

Reducing loan to deposit ratios

Selling assets outside home markets

Introduction/increasing incentives to increase customer deposits

Reducing the balance sheet

Accessing central bank funding programs 29

19

13

10

3

10

19

16

23

10

3

3

6

3 /

6

3

16

26

26

48

48

26

45

48

32

45

16

3

6

3

10

10

6

26

29

8

8

54

23

8

8

15

69

54

54

8

8

15

23

23

69

15

38

15

8

8

8

8

8

34

17

29

20

16

33

22

26

26

16

5

5

5

3

3

2

8

12

2

3

17

14

10

25

16

12

13

24

10

30

5

5

10

5

2

15

5

12

19

11

22

11

22

22

44

33

44

22

33

44

11

11

11

22

33

33

44

22

11

22

22

11

11

22

22

11

11

11

11

11 44

25

44

19

13

19

37

37

6

6

6

6

7

6

6

13

25

13

19

31

37

6

7

6

6

25

Nordics

Switzerland

Poland

UK

Spain

European Banking Barometer – 2015

Following the ECB’s comprehensive assessment, sector restructuring is expected to gather pace …

Which, if any, of the following is your bank likely to consider over the next 12 months in relation to the countries in which it operates?*

Page 23

* Numbers reflect the percentage of respondents who answered. Respondents could select more than one option.

23 24 24

45

26 30

34 31

Sell assets Buy assets Partnerships orjoint ventures

None of these

2014 2015

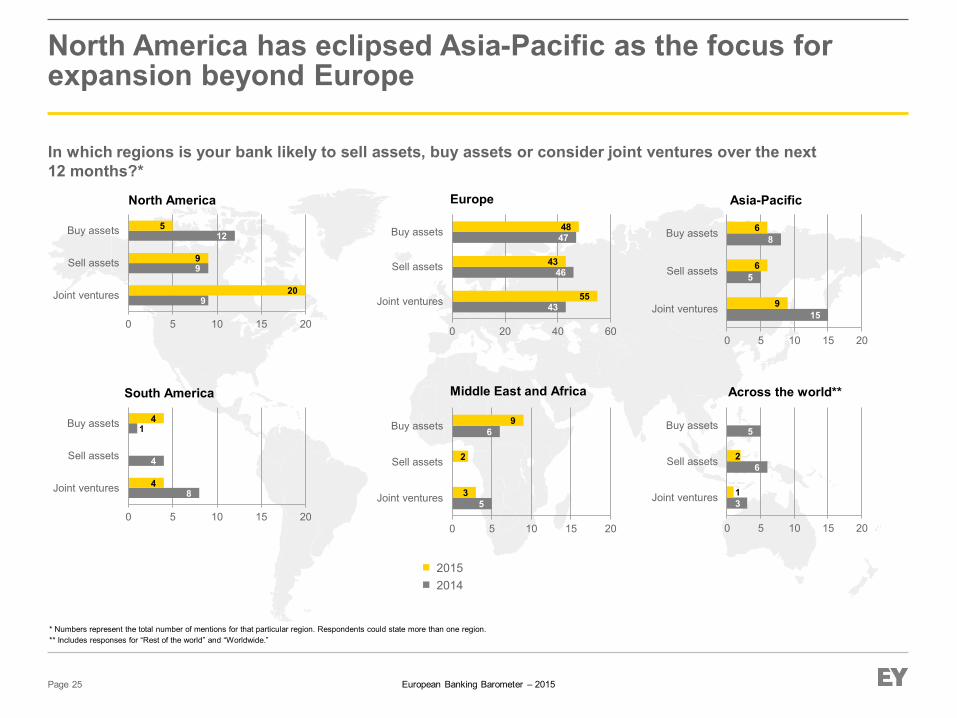

Comments: Sector restructuring had slowed ahead of the AQR and stress test. Following the comprehensive assessment, banks are once more reassessing their business and geographic footprints. The structural reform agenda will be a key driver of this activity, with 41% of universal banks expecting to sell assets, compared with 33% of corporate and investment banks, and just 20% of retail banks. Redefining the core activities of a bank will also be crucial to delivering improved profitability for institutions in the longer term (see Global banking outlook 2015: Transforming banking for the next generation). The weaker economic outlook means profitable growth will be hard to achieve organically. As a result, banks are now more likely to consider inorganic growth opportunities. However, as Basel III requires banks to hold additional capital against stakes in other financial institutions, acquisitions are likely to be of specific books of business, rather than of major operations. Partnerships are the preferred form of inorganic growth and, notably, banks are now more likely to consider partnerships in North America, and less likely to consider them in the Asia-Pacific region, than in 2014. This reflects the sustained economic recovery in the US, and concerns about the economic outlook for China and its impact on regional growth.

European Banking Barometer – 2015

… with more than half of bankers in the UK considering acquisitions and 45% in France considering divestments

Which, if any, of the following is your bank likely to consider over the next 12 months in relation to the countries in which it operates?*

Page 24

* Numbers reflect the percentage of respondents who answered. Respondents could select more than one option.

Sell assets Buy assets Partnerships or joint ventures None of these

26

12

45

17

15

14

35

7

23

23

35

38

35

14

11

23

19

14

25

14

45

26

24

33

UK

Switzerland

Spain

Poland

Nordics

Netherlands

Italy

Germany

France

Europe

Belgium

Austria

17

18

40

0

30

14

15

10

40

24

24

31

52

17

33

23

19

0

25

26

27

30

38

33

23

29

30

17

10

14

20

14

37

24

29

15

35

40

33

15

31

29

15

34

45

34

14

17

51

59

5

67

50

57

45

73

30

45

35

23

23

33

56

54

44

57

50

32

9

31

33

17

2015 2014

European Banking Barometer – 2015

North America has eclipsed Asia-Pacific as the focus for expansion beyond Europe

In which regions is your bank likely to sell assets, buy assets or consider joint ventures over the next 12 months?*

Page 25

* Numbers represent the total number of mentions for that particular region. Respondents could state more than one region. ** Includes responses for “Rest of the world” and “Worldwide.”

9

9

12

20

9

5

0 5 10 15 20

Joint ventures

Sell assets

Buy assets

North America

15

5

8

9

6

6

0 5 10 15 20

Joint ventures

Sell assets

Buy assets

Asia-Pacific

43

46

47

55

43

48

0 20 40 60

Joint ventures

Sell assets

Buy assets

Europe

8

4

1

4

4

0 5 10 15 20

Joint ventures

Sell assets

Buy assets

South America

5

6

3

2

9

0 5 10 15 20

Joint ventures

Sell assets

Buy assets

Middle East and Africa

3

6

5

1

2

0 5 10 15 20

Joint ventures

Sell assets

Buy assets

Across the world**

2015 2014

European Banking Barometer – 2015

15

38

40

6

Despite the growing pace of restructuring, fewer bankers now expect significant consolidation across the industry

To what extent do you anticipate consolidation of the banking industry over the next 12 months and within the next three years?*

Page 26

* Numbers reflect the percentage of respondents who answered. Base excludes respondents who answered “Don’t know.”

Within three years 12 months

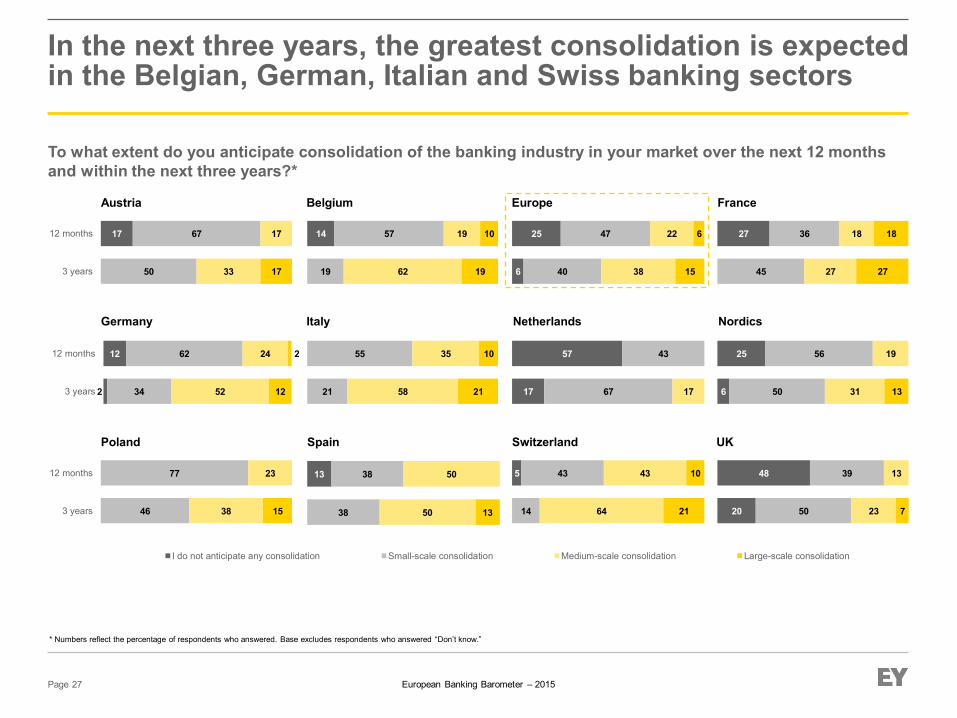

Comments: Over three-quarters of respondents anticipate some industry consolidation in the next year, and 94% expect some consolidation within the next three years. Most of this activity will be small in scale, suggesting banks will continue to restructure and generally only make disposals or acquisitions of small books of business that are closely aligned to their core strategy. The evolving regulatory landscape means many banks remain cautious of significant acquisitions in the short term, with just 28% of banks expecting medium- or large-scale consolidation in the coming year. Furthermore, although 53% of bankers expect significant consolidation within the next three years – with the greatest consolidation anticipated in markets where banks were shown to have capital shortfalls or where there is overcapacity – this has fallen from 65% in 2014.

6

22

47

25

2015 2014

Within three years 12 months

7

28

43

22 21

44

29

6

I do not anticipate any consolidation Small-scale consolidation Medium-scale consolidation Large-scale consolidation

European Banking Barometer – 2015

13

38

38

50

50

13

I do not anticipate any consolidation Small-scale consolidation Medium-scale consolidation Large-scale consolidation

In the next three years, the greatest consolidation is expected in the Belgian, German, Italian and Swiss banking sectors

To what extent do you anticipate consolidation of the banking industry in your market over the next 12 months and within the next three years?*

Page 27

* Numbers reflect the percentage of respondents who answered. Base excludes respondents who answered “Don’t know.”

Austria Belgium

Germany

Europe

Netherlands

17

50

67

33

17

17 3 years

12 months

Nordics

Switzerland Poland UK Spain

14

19

57

62

19

19

10

6

25

40

47

38

22

15

6

Italy

France

27

45

36

27

18

27

18

2

12

34

62

52

24

12

2

3 years

12 months

21

55

58

35

21

10

17

57

67

43

17 6

25

50

56

31

19

13

46

77

38

23

15 3 years

12 months 5

14

43

64

43

21

10

20

48

50

39

23

13

7

European Banking Barometer – 2015

Business priorities and product line expectations

Page 28

Section 3

European Banking Barometer – 2015

16

18

25

26

30 30

36

48 48

50

61 64

71

5 7

12 12

25

37

57

15

17

20 20

28

43

Reducing the number of productsOffshoring

OutsourcingDisposing of assets or businesses

Acquiring new assets or businessesNew remuneration systems

Establishing new business segmentsFinancial Transaction Tax

Developing partnerships with non-banksNew foreign markets/internationalization

Restructuring the business to comply with regulationsRestructuring the business to cut costs

Diversity requirements relating to CRD IV²Developing/introducing new products

Current changes in financial reporting/IFRSDeveloping recovery and resolution plans

The threat of financial crimeMinimizing all non-essential expenditure/cutting costs

Investing in customer-facing technologyCompliance with consumer regulation/remediation

Cybersecurity/data securityCompliance with capital market regulations

Streamlining processesReputational risk¹

Capital, liquidity and the leverage ratioRisk management2015

Page 29

Risk and regulation remain at the top of banks’ agendas

* Respondents were asked to rank the importance of activities on a scale of 0 to 10, where 0 denotes “Not at all important” and 10 denotes “Very important.” Numbers show the percentage of respondents selecting either 8, 9 or 10. Base excludes respondents answering “Does not apply.” In the European Banking Barometer – 2014 “Cutting costs” was listed as an individual answer and was ranked seventh.

1 Reputational risk includes tax transparency; compliance with capital markets regulations, i.e., MiFID II or EMIR; and investing in new customer-facing technology, e.g., mobile solutions. 2 Diversity requirements relating to CRD IV – putting in place a policy to promote diversity on the management board.

Rank the importance of the following agenda items for your organization*

Comments: An ever-increasing regulatory burden means risk and regulation remain firmly at the top of bankers’ priorities in 2015. Risk management is cited as particularly important by 71% of respondents, compared with 56% in 2014. With the recent comprehensive assessment giving banks greater clarity on prudential expectations, combined with new proposals for increasing banks’ TLAC, capital, liquidity and the leverage ratio is now the second most important priority for bankers. It is notable that, while reputational risk is the third most important priority for banks in 2015, development of the new remuneration systems that many see as a key driver of cultural transformation across the industry – and central to mitigating conduct risk – are ranked 21st. Banks will also continue to invest in technology as they continue to streamline process, strengthen cybersecurity and tackle financial crime.

2014 2015 Rank order of importance

1 2 3 4 5 6 7 8 9 10 11 12 13 14 15 16 17 18 19 20 21 22 23 24 25 26

1 5 2 4 6 3 10 8

9//7 11 16 15 9 21 12 18 13 19 17 14 24 20 25 23 26 22

Risk and regulation Cost cutting and efficiency

Innovation and growth

European Banking Barometer – 2015

0

20

27

20 14

6

36 34

42

14 54

56

12

40

56

4 4

10

34

Financial Transaction TaxDeveloping partnerships with non-banksNew foreign markets/internationalization

Restructuring the business to comply with regulationsRestructuring the business to cut costs

Diversity requirements relating to CRD IV²Developing/introducing new products

Current changes in financial reporting/IFRSDeveloping recovery and resolution plans

The threat of financial crimeMinimizing all non-essential expenditure/cutting costs

Investing in customer-facing technologyCompliance with consumer regulation/remediation

Cybersecurity/data securityCompliance with capital market regulations

Streamlining processesReputational risk¹

Capital, liquidity and the leverage ratioRisk management

17

14

29

43 29

0

43 14

83

86 71

86

17

29

57

14 29

0

43

36

10

30

36 40

60

55 80

27

64 73

82

27

18

45

27 18

18

36

17

33

50

33 50

83

67 67

80

80 50

80

17

50

83

50 0

83

50

Financial Transaction TaxDeveloping partnerships with non-banksNew foreign markets/internationalization

Restructuring the business to comply with regulationsRestructuring the business to cut costs

Diversity requirements relating to CRD IV²Developing/introducing new products

Current changes in financial reporting/IFRSDeveloping recovery and resolution plans

The threat of financial crimeMinimizing all non-essential expenditure/cutting costs

Investing in customer-facing technologyCompliance with consumer regulation/remediation

Cybersecurity/data securityCompliance with capital market regulations

Streamlining processesReputational risk¹

Capital, liquidity and the leverage ratioRisk management

11

28

39

47 25

11

33 11

47

63 61

74

32

47

67

28 33

39

59

30

15

30

33 15

38

50 62

43

62 53

81

35

52

71

15 6

29

71

Italy Germany

Page 30

Banks across Europe are also refocusing on efficiency, at the expense of innovation and growth initiatives

* Respondents were asked to rank the importance of activities on a scale of 0 to 10, where 0 denotes “Not at all important” and 10 denotes “Very important.” Numbers show the percentage of respondents selecting either 8, 9 or 10. Base excludes respondents answering “Does not apply.” In the European Banking Barometer – 2014 “Cutting costs” was listed as an individual answer and was ranked seventh.

1 Reputational risk includes tax transparency; compliance with capital markets regulations, i.e., MiFID II or EMIR; and investing in new customer-facing technology, e.g., mobile solutions. 2 Diversity requirements relating to CRD IV – putting in place a policy to promote diversity on the management board.

Risk and regulation Cost cutting and efficiency

Innovation and growth

Austria Belgium France

Netherlands

Rank the importance of the following agenda items for your organization*

European Banking Barometer – 2015

5

12

5

27 7

20

24 38

48

46 50

43

20

43

45

7 12

37

29

Financial Transaction TaxDeveloping partnerships with non-banksNew foreign markets/internationalization

Restructuring the business to comply with regulationsRestructuring the business to cut costs

Diversity requirements relating to CRD IV²Developing/introducing new products

Current changes in financial reporting/IFRSDeveloping recovery and resolution plans

The threat of financial crimeMinimizing all non-essential expenditure/cutting costs

Investing in customer-facing technologyCompliance with consumer regulation/remediation

Cybersecurity/data securityCompliance with capital market regulations

Streamlining processesReputational risk¹

Capital, liquidity and the leverage ratioRisk management

7

47

13

25 33

44

47 37

63

63 60

56

31

44

69

33 20

31

56

Financial Transaction TaxDeveloping partnerships with non-banksNew foreign markets/internationalization

Restructuring the business to comply with regulationsRestructuring the business to cut costs

Diversity requirements relating to CRD IV²Developing/introducing new products

Current changes in financial reporting/IFRSDeveloping recovery and resolution plans

The threat of financial crimeMinimizing all non-essential expenditure/cutting costs

Investing in customer-facing technologyCompliance with consumer regulation/remediation

Cybersecurity/data securityCompliance with capital market regulations

Streamlining processesReputational risk¹

Capital, liquidity and the leverage ratioRisk management

13

43

38

38 50

25

62 38

67

78 88

78

13

44

33

22 33

44

44

Poland

0

18

33

15 15

38

17 58

31

62 46

69

8

54

77

33 22

54

54

27

37

23

20 35

60

61 61

60

81 61

77

37

39

68

19 30

40

47

Switzerland

Nordics

UK

Page 31

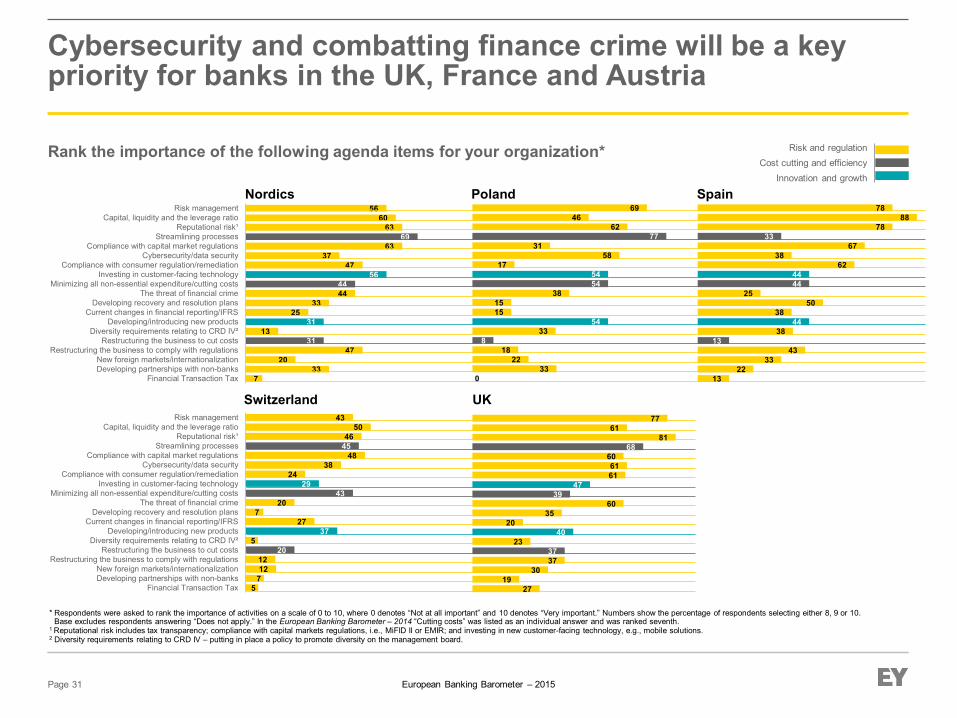

Cybersecurity and combatting finance crime will be a key priority for banks in the UK, France and Austria

* Respondents were asked to rank the importance of activities on a scale of 0 to 10, where 0 denotes “Not at all important” and 10 denotes “Very important.” Numbers show the percentage of respondents selecting either 8, 9 or 10. Base excludes respondents answering “Does not apply.” In the European Banking Barometer – 2014 “Cutting costs” was listed as an individual answer and was ranked seventh.

1 Reputational risk includes tax transparency; compliance with capital markets regulations, i.e., MiFID II or EMIR; and investing in new customer-facing technology, e.g., mobile solutions. 2 Diversity requirements relating to CRD IV – putting in place a policy to promote diversity on the management board.

Rank the importance of the following agenda items for your organization* Risk and regulation Cost cutting and efficiency

Innovation and growth

Spain

European Banking Barometer – 2015

Bankers continue to anticipate an improved outlook for all business lines …

How do you rate the outlook for your bank over the next 12 months in each of the following business lines?*

Page 32

* Numbers reflect the percentage of respondents who answered. Respondents answering “Neither good, nor poor” are not displayed. Base excludes respondents answering “Does not apply” or chose not to answer.

18

17

17

14

13

9

12

6

7

2

2

2

1

2

4

1

1

27

37

38

38

37

43

41

53

53

5

6

5

6

8

11

14

5

9

Securities trading

Transaction advisory (e.g., M&A)

Deposit business

Securities services

Asset management

Debt and equity issuance

Retail banking

Corporate banking

Private banking and wealth management

35

33

43

36

40

32

44

43

57

3

6

6

4

13

9

10

7

10

19

8

8

12

10

10

10

8

5

3

3

2

3

3

3

2

1

3

Securities trading

Transaction advisory (e.g., M&A)

Deposit business

Securities services

Asset management

Debt and equity issuance

Retail banking

Corporate banking

Private banking and wealth management

Net increase

59

40

42

29

41

24

39

26

16

Net increase

2015 2014

54

51

44

40

30

29

25

24

13

Very good Fairly good Very poor Fairly poor

Comments: Bankers remain most optimistic about the outlook for private banking and wealth management. As highlighted in our previous edition, it is an attractive segment, given its capital-light business model and the fact it is a growing market. More surprisingly, given the weak economic outlook, most bankers also expect an improved outlook for retail and corporate banking. However, the ECB’s low base rate and quantitative easing (QE) should enable banks to improve margins while lending to customers that are good credit risks. The most improved outlook is for debt and equity issuance. Increased capital markets activity is likely as QE boosts demand for capital markets funding from non-financial corporations. In addition, there is likely to be significant capital raising by those financial institutions that failed the comprehensive assessment, as well as by other institutions in anticipation of TLAC requirements. Unsurprisingly, following the ECB’s introduction of a negative deposit rate in June 2014, the outlook for deposit business is also less positive than last year. The outlook is least positive for securities trading, a business line that is grappling with transformative regulation of Dodd Frank, EMIR and MiFID II.

European Banking Barometer – 2015

… with the strongest performance expected in wealth management, retail and corporate banking

How do you rate the outlook for your bank over the next 12 months in each of the following business lines?*

Page 33

* Numbers reflect the percentage of respondents who answered. Respondents answering “Neither good, nor poor” are not displayed. Base excludes respondents answering “Does not apply” or chose not to answer.

52

35

75

40

42

25

73

48

56

53

69

60

5

8

13

10

17

25

8

11

9

13

19

15

20

7

8

7

5

3

1

UK

Switzerland

Spain

Poland

Nordics

Netherlands

Italy

Germany

France

Europe

Belgium

Austria

Private banking and wealth management

Very good Fairly good Very poor Fairly poor

Retail banking

50

43

44

73

57

50

53

42

11

41

69

50

5

5

11

9

14

25

6

10

33

14

6

10

3

22

7

29

13

11

12

5

UK

Switzerland

Spain

Poland

Nordics

Netherlands

Italy

Germany

France

Europe

Belgium

Austria

Corporate banking

67

31

56

54

64

40

53

35

60

53

64

67

8

11

8

10

5

7

8

11

15

14

27

6

6

7

3

7

2

1

UK

Switzerland

Spain

Poland

Nordics

Netherlands

Italy

Germany

France

Europe

Belgium

Austria

Debt and equity issuance

61

23

43

64

69

80

20

18

44

43

36

25

4

14

18

15

20

13

22

11

25

9

6

14

9

7

14

11

9

18

25

11

7

16

4

UK

Switzerland

Spain

Poland

Nordics

Netherlands

Italy

Germany

France

Europe

Belgium

Austria

European Banking Barometer – 2015

However, the outlook for asset management and deposit business is slightly less positive than before …

How do you rate the outlook for your bank over the next 12 months in each of the following business lines?*

Page 34

* Numbers reflect the percentage of respondents who answered. Respondents answering “Neither good, nor poor” are not displayed. Base excludes respondents answering “Does not apply” or chose not to answer.

Very good Fairly good Very poor Fairly poor

62

30

33

54

50

20

25

25

40

38

39

8

11

8

6

4

10

5

6

20

12

20

23

14

19

31

20

17

28

20

4

11

2

UK

Switzerland

Spain

Poland

Nordics

Netherlands

Italy

Germany

France

Europe

Belgium

Austria

Deposit business

35

21

80

22

50

25

18

17

57

37

20

40

10

3

11

10

50

2

6

40

21

33

27

21

17

30

20

6

2

2

20

UK

Switzerland

Spain

Poland

Nordics

Netherlands

Italy

Germany

France

Europe

Belgium

Austria

Transaction advisory (e.g., M&A)

Securities services

43

32

38

30

45

25

23

36

44

38

46

20

5

8

13

10

25

8

4

6

20

19

15

10

8

15

22

14

31

20

9

1

UK

Switzerland

Spain

Poland

Nordics

Netherlands

Italy

Germany

France

Europe

Belgium

Austria

Asset management

42

39

25

22

64

53

44

22

37

45

40

11

5

13

7

20

2

11

8

9

11

8

13

22

20

27

15

11

13

18

40

5

3

7

2

UK

Switzerland

Spain

Poland

Nordics

Netherlands

Italy

Germany

France

Europe

Belgium

Austria

European Banking Barometer – 2015

42

26

13

40

23

25

25

18

33

27

11

20

8

3

25

10

6

2

5

19

15

13

20

8

50

6

12

22

18

22

40

4

4

2

UK

Switzerland

Spain

Poland

Nordics

Netherlands

Italy

Germany

France

Europe

Belgium

Austria

… while securities trading continues to struggle with a complex regulatory agenda

How do you rate the outlook for your bank over the next 12 months in each of the following business lines?*

Page 35

* Numbers reflect the percentage of respondents who answered. Respondents answering “Neither good, nor poor” are not displayed. Base excludes respondents answering “Does not apply” or chose not to answer.

Very good Fairly good Very poor Fairly poor

Securities trading

European Banking Barometer – 2015

Headcount and compensation

Page 36

Section 5

European Banking Barometer – 2015

2015

A further decline is anticipated in overall headcount, with the pace of cuts increasing in most markets …

Over the next 12 months, how do you expect the headcount of your bank to change?*

Page 37

* Numbers reflect the percentage of respondents who answered. Respondents answering “Stay the same” are not displayed. Base excludes respondents answering “Don’t know.”

Comments: The pace of job cuts is expected to rise in 2015 to levels last seen in our European Banking Barometer – 2H13. Although, in the aftermath of the global financial crisis, European banks cut staff through a combination of restructuring efforts, asset sales and redundancies, aggregate headcount is just 4.4% down from 2007 levels. Staff costs remain around 54% of the sector’s operating costs; with the industry anticipating further restructuring and requiring additional cost reduction to achieve profitability targets, further staff cuts remain inevitable. Forty-three percent of bankers expect headcount to fall, compared with 38% in our last survey. The greatest job losses are anticipated in the Nordics, Italy and Austria, while the UK is the only market where more respondents anticipate hiring than firing.

Increase significantly Increase slightly Decrease significantly Decrease slightly

2014

Net increase

-15

-8 27 3 31 7

27 2 35 8

European Banking Barometer – 2015

27

31

50

46

56

29

35

44

27

35

33

17

7

8

13

14

20

2

9

8

19

33

43

21

13

31

19

29

20

22

27

27

24

17

5

13

2

10

UK

Switzerland

Spain

Poland

Nordics

Netherlands

Italy

Germany

France

Europe

Belgium

Austria -33

-19

-15

-9

-24

-35

-14

-50

-23

-25

-5

10

… except France, the Netherlands and Switzerland, while the UK is the only market where headcount is expected to rise

Over the next 12 months, how do you expect the headcount of your bank to change?*

Page 38

* Numbers reflect the percentage of respondents who answered. Respondents answering “Stay the same” are not displayed. Base excludes respondents answering “Don’t know.”

2015

23

35

20

27

16

57

50

32

33

31

29

38

3

20

18

5

14

5

3

7

7

18

15

40

18

30

27

47

14

25

21

20

27

29

23

9

5

3

6

8

UK

Switzerland

Spain

Poland

Nordics

Netherlands

Italy

Germany

France

Europe

Belgium

Austria

2014 Net increase

-23

-12

-8

-20

-14

-30

-57

26

-18

-5

-18

23

Net increase

Increase significantly Increase slightly Decrease significantly Decrease slightly

European Banking Barometer – 2015

2

5

6

7

10

10

12

13

31

7

28

17

12

32

7

7

4

11

7

10

8

11

11

9

26

10

27

18

7

27

8

12

Other head-office functions

Asset management

Operations and IT

Investment banking

Compliance, risk and finance

Retail and business banking

Private banking and wealth management

Corporate banking

Recruitment will be focused on growth sectors, such as corporate banking, private banking and wealth management

In which areas of the business do you expect headcount to increase or decrease?*

Page 39

* Numbers reflect the percentage of respondents who answered. Respondents answering “Stay the same” are not displayed. Base excludes respondents answering “Don’t know.”

■ Decrease ■ Increase

2015 2014 -3

3

-16

2

-7

-21

0

-22

Net increase

Net increase

7

4

-22

-2

-10

-21

-1

-29

Comments: Unsurprisingly, headcount reductions continue to be focused on operations and IT, other head-office functions and retail banking, where banks have launched numerous process simplification activities. Surprisingly, given the volume of regulation banks are grappling with, slightly more respondents expect to reduce rather than recruit compliance staff. This may, however, be discounting the growth of risk and compliance contractors across organizations. Only corporate banking, and private banking and wealth management, which were identified by respondents as growth areas, are likely to see a net increase in staff.

European Banking Barometer – 2015

40

40

20

40

20

40

20

20

60

40

20

14

14

14

14

14

14

29

14

29

7

7

7

20

7

7

33

7

20

13

40

7

13

6

22

22

17

22

6

39

6

33

11

6

33

6

11

25

25

50

50

50

50

25

Other head-office functions

Asset management

Operations and IT

Investment banking

Compliance, risk and finance

Retail and business banking

Private banking and wealth management

Corporate banking

Germany

Belgium

Italy

France

Netherlands

Significant cuts in retail banking, head-office functions, operations and IT jobs will continue unabated …

In which areas of the business do you expect headcount to increase or decrease?*

Page 40

* Numbers reflect the percentage of respondents who answered. Respondents answering “Stay the same” are not displayed. Base excludes respondents answering “Don’t know.”

Austria

■ Decrease ■ Increase

6

3

6

3

15

9

3

9

24

12

26

9

29

6

9

Other head-office functions

Asset management

Operations and IT

Investment banking

Compliance, risk and finance

Retail and business banking

Private banking and wealth management

Corporate banking

European Banking Barometer – 2015

17

33

17

17

50

17

17

50

9

36

9

9

36

9

27

9

9

… and modest reductions in compliance staff are also anticipated in many markets

In which areas of the business do you expect headcount to increase or decrease?*

Page 41

* Numbers reflect the percentage of respondents who answered. Respondents answering “Stay the same” are not displayed. Base excludes respondents answering “Don’t know.”

Switzerland

Poland

UK

Spain Nordics

■ Decrease ■ Increase

7

7

7

7

50

50

14

7

36

7

7

Other head-office functions

Asset management

Operations and IT

Investment banking

Compliance, risk and finance

Retail and business banking

Private banking and wealth management

Corporate banking

13

4

13

13

9

17

26

30

39

26

17

17

4

4

8

4

4

4

13

13

17

13

13

8

21

21

4

Other head-office functions

Asset management

Operations and IT

Investment banking

Compliance, risk and finance

Retail and business banking

Private banking and wealth management

Corporate banking

European Banking Barometer – 2015

3

14

5

22

2

5

1

6

4

18

+/- 10%

+/- 8%–10%

+/- 5%–8%

+/- 2%–5%

+/- 1%–2%

Total

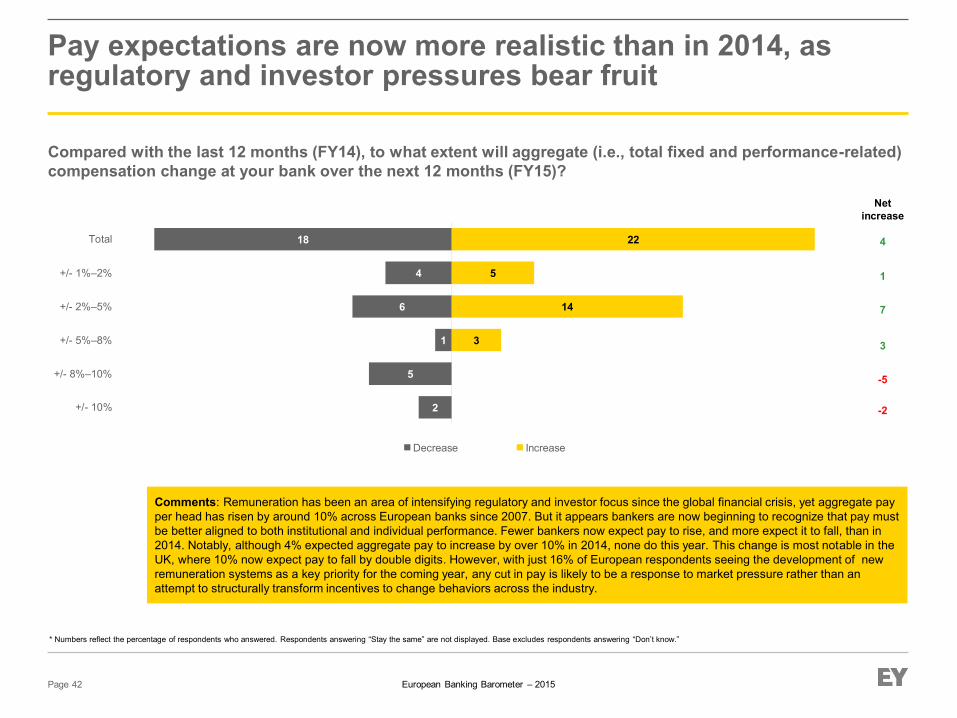

Pay expectations are now more realistic than in 2014, as regulatory and investor pressures bear fruit

Compared with the last 12 months (FY14), to what extent will aggregate (i.e., total fixed and performance-related) compensation change at your bank over the next 12 months (FY15)?

Page 42

* Numbers reflect the percentage of respondents who answered. Respondents answering “Stay the same” are not displayed. Base excludes respondents answering “Don’t know.”

Decrease Increase

Comments: Remuneration has been an area of intensifying regulatory and investor focus since the global financial crisis, yet aggregate pay per head has risen by around 10% across European banks since 2007. But it appears bankers are now beginning to recognize that pay must be better aligned to both institutional and individual performance. Fewer bankers now expect pay to rise, and more expect it to fall, than in 2014. Notably, although 4% expected aggregate pay to increase by over 10% in 2014, none do this year. This change is most notable in the UK, where 10% now expect pay to fall by double digits. However, with just 16% of European respondents seeing the development of new remuneration systems as a key priority for the coming year, any cut in pay is likely to be a response to market pressure rather than an attempt to structurally transform incentives to change behaviors across the industry.

Net increase

4

1

7

3

-5

-2

European Banking Barometer – 2015

12

16

29

4

8

12

+/- 10%

+/- 8%–10%

+/- 5%–8%

+/- 2%–5%

+/- 1%–2%

Total

5

5

10

5

5

10

17

17

+/- 10%

+/- 8%–10%

+/- 5%–8%

+/- 2%–5%

+/- 1%–2%

Total

Austria

Germany

Belgium

Italy

France

Netherlands

Page 43

An increase in aggregate compensation is expected in Austria, France, Germany, the Netherlands …

* Numbers reflect the percentage of respondents who answered. Respondents answering “Stay the same” are not displayed. Base excludes respondents answering “Don’t know.”

5

10

5

20

5

25

30

36

36

9

9

18

Decrease Increase

Net increase

17

17

0

0

0

0

Net increase

-10

5

-15

0

0

0

Net increase

18

-9

27

0

0

0

Net increase

17

8

8

0

0

0

Net increase

0

5

0

0

-5

0

Net increase

14

0

14

14

-14

0

Compared with the last 12 months (FY14), to what extent will aggregate (i.e., total fixed and performance-related) compensation change at your bank over the next 12 months (FY15)?

14

14

29

14

14

European Banking Barometer – 2015

11

11

11

11

7

7

14

7

7

29

+/- 10%

+/- 8%–10%

+/- 5%–8%

+/- 2%–5%

+/- 1%–2%

Total

8

23

31

8

8

5

14

19

2

2

14

2

21

+/- 10%

+/- 8%–10%

+/- 5%–8%

+/- 2%–5%

+/- 1%–2%

Total

3

10

14

10

7

7

24

Nordics

Switzerland

Poland

UK

Spain

Page 44

… and Poland, but many respondents in the Nordics and the UK anticipate a significant fall in remuneration

* Numbers reflect the percentage of respondents who answered. Respondents answering “Stay the same” are not displayed. Base excludes respondents answering “Don’t know.”

Net increase

-22

-7

0

0

-14

0

Net increase

23

0

15

8

0

0

Net increase

0

0

0

11

-11

0

Net increase

-2

12

-9

-2

0

-2

Net increase

-10

0

3

3

-7

-10

Decrease Increase

Compared with the last 12 months (FY14), to what extent will aggregate (i.e., total fixed and performance-related) compensation change at your bank over the next 12 months (FY15)?

European Banking Barometer – 2015

Contacts

Page 45

Section 6

European Banking Barometer – 2015

Contacts

For more information on how we can help, please contact our team:

EMEIA:

Marie-Laure Delarue +33 1 46 93 73 21 [email protected] Steven Lewis +44 20 7951 9471 [email protected] Karl Meekings +44 20 7783 0081 [email protected] Austria:

Friedrich Hief +43 1 21170 1352 [email protected]

Belgium:

Jean-François Hubin +32 2 774 9266 [email protected]

France:

Luc Valverde +33 1 46 93 63 04 [email protected]

Germany:

Dirk Müller-Tronnier +49 6196 996 27429 [email protected]

Italy:

Massimo Testa +39 02 7221 2306 [email protected]

Netherlands:

Wouter Smit +31 88 407 1574 [email protected]

Nordics:

Lars Weigl +46 8 520 590 45 [email protected]

Poland:

Iwona Kozera +48 22 557 7491 [email protected]

Spain:

José Carlos Hernández Barrasús +34 91 572 7291 [email protected]

Switzerland:

Olaf Toepfer +41 58 286 4471 [email protected]

UK:

Omar Ali +44 20 7951 1789 [email protected]

Page 46

EY | Assurance | Tax | Transactions | Advisory

About EY

EY is a global leader in assurance, tax, transaction and advisory services. The insights and quality services we deliver help build trust and confidence in the capital markets and in economies the world over. We develop outstanding leaders who team to deliver on our promises to all of our stakeholders. In so doing, we play a critical role in building a better working world for our people, for our clients and for our communities.

EY refers to the global organization, and may refer to one or more, of the member firms of Ernst & Young Global Limited, each of which is a separate legal entity. Ernst & Young Global Limited, a UK company limited by guarantee, does not provide services to clients. For more information about our organization, please visit ey.com.

About EY’s Global Banking & Capital Markets Center

In today’s globally competitive and highly regulated environment, managing risk effectively while satisfying an array of divergent stakeholders is a key goal of banks and securities firms. EY’s Global Banking & Capital Markets Center brings together a worldwide team of professionals to help you succeed – a team with deep technical experience in providing assurance, tax, transaction and advisory services. The Center works to anticipate market trends, identify the implications and develop points of view on relevant sector issues. Ultimately it enables us to help you meet your goals and compete more effectively.

© 2015 EYGM Limited. All Rights Reserved.

EYG no. EK0355

ED None

This material has been prepared for general informational purposes only and is not intended to be relied upon as accounting, tax, or other professional advice. Please refer to your advisors for specific advice.

ey.com/ebb