Embed Size (px)

Citation preview

Fernando Hervás

Sixth IRIMA Workshop on: 'R&D Investment and Firm Dynamics' Brussels, 3rd December 2015

EU Industrial R&D Scoreboard

2015

Policy context

Growth, Jobs and Investment priority - Research and innovation agenda, 3% R&D investment target - Industrial modernisation, advanced manufacturing, KETs Activities

SURVEY (9 years)

MONITORING SCOREBOARD (10 years)

ANALYSIS WORKING PAPERS

Technical reports

DISSEMINATION POLICY BRIEFS

Workshops Conferences

Policy message

Need to increase the weight of knowledge intensive and high-value industrial segments in the European economy

WHY?

Global Value Chains

EU industrial structure

Shift towards more knowledge

intensive activities will make it

more resilient and competitive in

a global economy

Investment

Knowledge Based Capital

Investments in intangible assets

are main source of

Growth and Employment

New technologies

Technological development

Key and emerging technologies contribute to

solve grand societal challenges

4

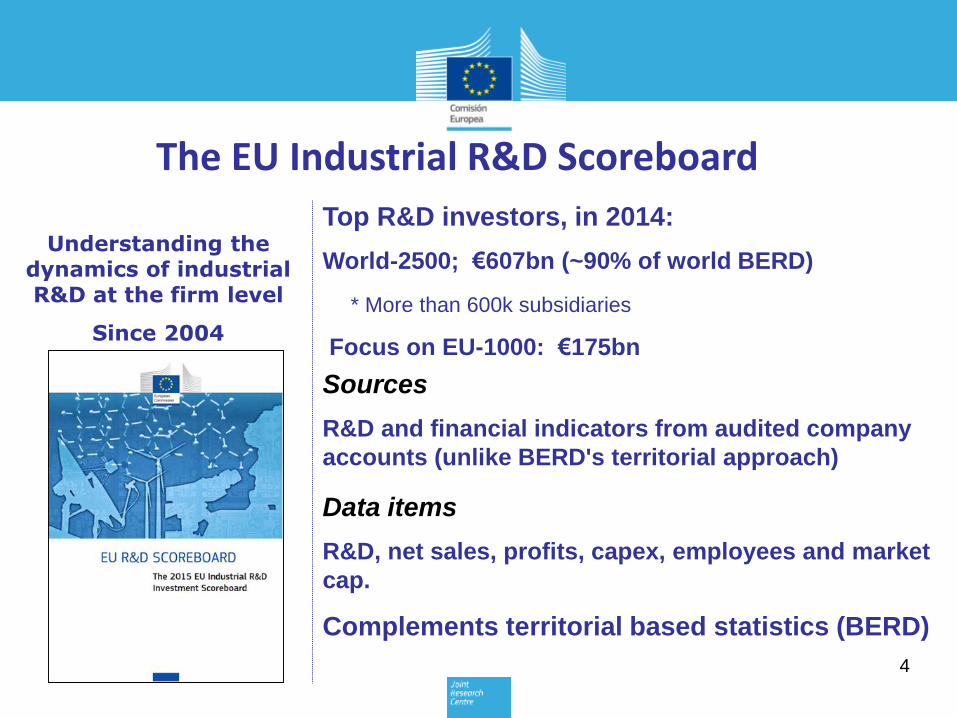

Understanding the dynamics of industrial R&D at the firm level

Since 2004

Top R&D investors, in 2014:

World-2500; €607bn (~90% of world BERD)

* More than 600k subsidiaries

Focus on EU-1000: €175bn

Sources

R&D and financial indicators from audited company

accounts (unlike BERD's territorial approach)

Data items

R&D, net sales, profits, capex, employees and market

cap.

Complements territorial based statistics (BERD)

The EU Industrial R&D Scoreboard

The top 2500 companies invested €607.2 billion in R&D, which is 55% of the

total expenditure on R&D worldwide (GERD) and about 90% of the R&D

expenditure financed by the business sector worldwide (BERD).

Distribution of the 2500 companies in the 2015 Scoreboard by country

Note: The map only includes countries with 9 or more companies. Source: The 2015 EU Industrial R&D Investment Scoreboard, European Commission, JRC/DG RTD.

Distribution of the 608 EU companies in the 2015 Scoreboard by country

Source: The 2015 EU Industrial R&D Investment Scoreboard, European Commission, JRC/DG RTD.

Top R&D investors – investment share by main world region

Source: The 2015 EU Industrial R&D Investment Scoreboard, European Commission, JRC/DG RTD.

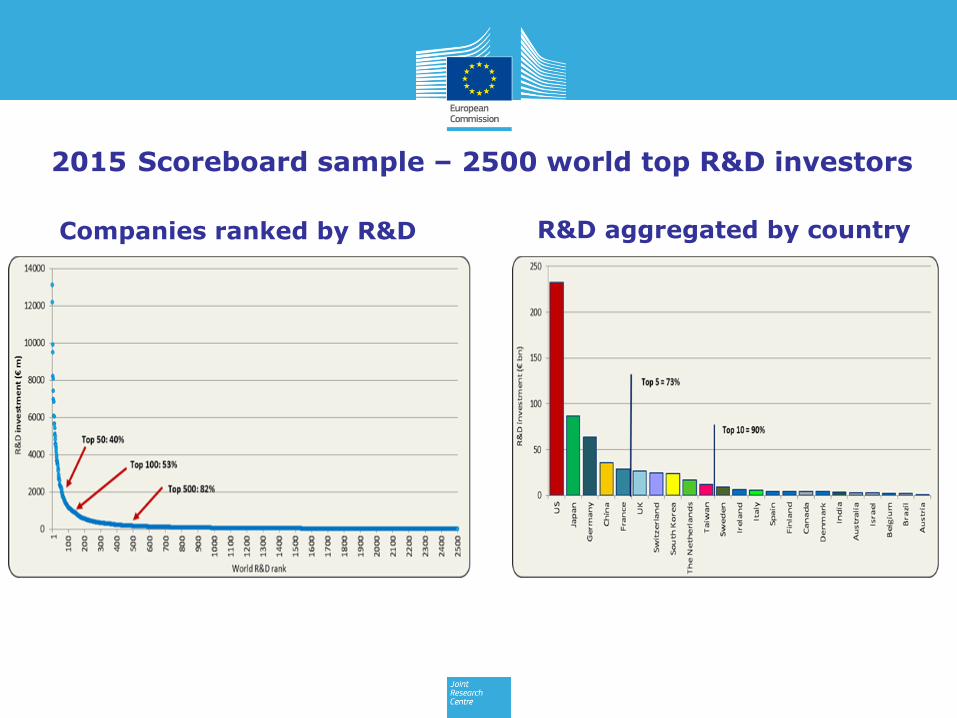

Companies ranked by R&D R&D aggregated by country

2015 Scoreboard sample – 2500 world top R&D investors

As in the previous Scoreboard edition, the top R&D investors are VW,

Samsung, Microsoft, Intel and Novartis.

The most significant changes at the top of the ranking in 2014 are the climb of

Google to 6th place (from 9th), and Pfizer to 10th place (from 15th). Huawei (15th)

and Apple (18th) accelerated in 2014 their race towards the top 10, jumping 11 and

17 positions, respectively. By main sector, the top investors are:

Pharmaceuticals & Biotech. Automobiles & Parts Technology Hardware & Equip.

NOVARTIS Switzerland VOLKSWAGEN Germany INTEL US

ROCHE Switzerland TOYOTA MOTOR Japan CISCO SYSTEMS US

JOHNSON & JOHNSON US GENERAL MOTORS US APPLE US

Software & Computer Services Electronic & Electrical Equipment Industrial Engineering

MICROSOFT US SAMSUNG South Korea VOLVO Sweden

GOOGLE US SIEMENS Germany CATERPILLAR US

ORACLE US HITACHI Japan ABB Switzerland

Chemicals Aerospace & Defence General Industrials

BASF Germany AIRBUS The Netherlands GENERAL ELECTRIC US

DUPONT US BOEING US TOSHIBA Japan

MONSANTO US UNITED TECHNOLOGIES US PHILIPS The Netherlands

Leisure Goods Health Care Equipment & Services Oil & Gas Producers

SONY Japan MEDTRONIC PLC Ireland PETROCHINA China

PANASONIC Japan BAXTER INTERNATIONAL US TOTAL France

LG ELECTRONICS South Korea BOSTON SCIENTIFIC US ROYAL DUTCH SHELL UK

Differences in region's

industrial structures –

R&D intensive sectors

Pharma & Bio18%

Tech. Hardware & Equipment

9%

Software4%

Aerospace & Defence6%

other high2%

Automobiles & parts27%

Industrials2%

Electr. Equipment

5%

Chemicals3%

other medium-high8%

medium-low6%

low10%

EU 608 companies€171 bn R&D

high 39%

medium-high 45%

Pharma & Bio21%

Tech. Hardware & Equipment

25%Software

21%

Aerospace & Defence

3%

other high4%

Automobiles & parts7%

Industrials3%

Electr. Equipment

3%

Chemicals3%

other medium-high5%

medium-low4% low

1%

US829 companies €232 bn R&D

high 74%

medium-high 21%

Pharma & Bio2%

Tech. Hardware & Equipment

13%

Software10%

other high2%

Automobiles & parts

10%

Industrials3%

Electr. Equipment

6%

Chemicals1%

other medium-high

25%

medium-low2%

low26%

China301 companies

€36 bn R&D

high27%

medium-high 45%

Pharma & Bio11%

Tech. Hardware & Equipment

7%

Software3%

other high10%

Automobiles & parts

29%

Industrials6%

Electr. Equipment

13%

Chemicals7%

other medium-high

7%

medium-low4% low

3%

Japan 360 companies

€87 bn R&D

high 31%

medium-high 62%

Company R&D investment by sector (2006 vs 2014)

Source: The 2015 EU Industrial R&D Investment Scoreboard, European Commission, JRC/DG RTD.

Our Evidence

Source: The 2015 EU Industrial R&D Investment Scoreboard, European Commission, JRC/DG RTD.

Top R&D investors are also top employers

The country distribution of patents filed by the world's top R&D investors is a

good proxy for the location of companies' innovation activities.

80% of patents were developed by inventors

residing in the same world region as the

parent company owning the rights: Inventor location

EU USA Japan RoW Switzerland

Co

mp

any'

s h

ead

qu

arte

r lo

cati

on

EU (6,635)

72.2% 21.6% 1.3% 3.9% 1.0%

USA (8,619)

10.3% 81.2% 1.7% 5.0% 1.8%

Japan (1,342)

5.8% 18.5% 67.8% 7.7% 0.21%

RoW (860)

18.1% 30.5% 0.1% 50.3% 1.12%

Switzerland (2,897)

31.0% 43.7% 2.6% 3.8% 18.8%

Inventor location

EU USA Japan Asian Tigers RoW

Co

mp

any'

s h

ead

qu

arte

r lo

cati

on

EU (14,609)

84.9% 10.6% 1.2% 0.9% 2.4%

USA (7,172)

28.1% 65.8% 0.8% 0.4% 4.8%

Japan (17,508)

1.6% 7.8% 89.9% 0.0% 0.58%

Asian Tigers (2,520)

0.2% 0.8% 0.4% 97.0% 1.54%

RoW (118)

71.4% 5.3% 23.3%

Pharma & biotech

Automobiles

& parts

High-performing R&D driven innovators in the EU

Identification exercise, based on multiple performance criteria over the period 2000-2013: R&D and sales growth, R&D intensity, labour productivity, profits. Key findings: - Concentrated in few countries including the UK, Germany, France and Sweden. - High-tech firms are, on average, younger than those in other sector groups and are also relatively more numerous. - Very heterogeneous corporate trajectories, including dynamic ICT firms and few older companies from less R&D intensive sectors. - Eight firms showing particularly strong performance (R&D intensity above 10%, net sales growth above 10%), positive profits and well above sectoral labour productivity average: Dialog Semiconductor, Gameloft, Bavarian Nordic, Wirecard, Parrot, Playtech, HMS Networks and Generix.

IRIMA research agenda

The role of intangibles (patents, TM , other) in firm's

performance and the obstacles to firms competitiveness

Disentangling the casual links underlying the success of firms

(birth and scaling-up)

Analysis of value chains in strategic knowledge intensive industrial sectors

Thank you More information at:

IRIMA:

http://iri.jrc.ec.europa.eu/

JRC - Joint Research Centre:

https://ec.europa.eu/jrc/

Contact information:

[email protected] Economics of Industrial Research and Innovation

European Commission

JRC-IPTS’s Knowledge for Growth Unit

Edf. Expo, Calle Inca Garcilaso n. 3

41092 Seville (Spain)

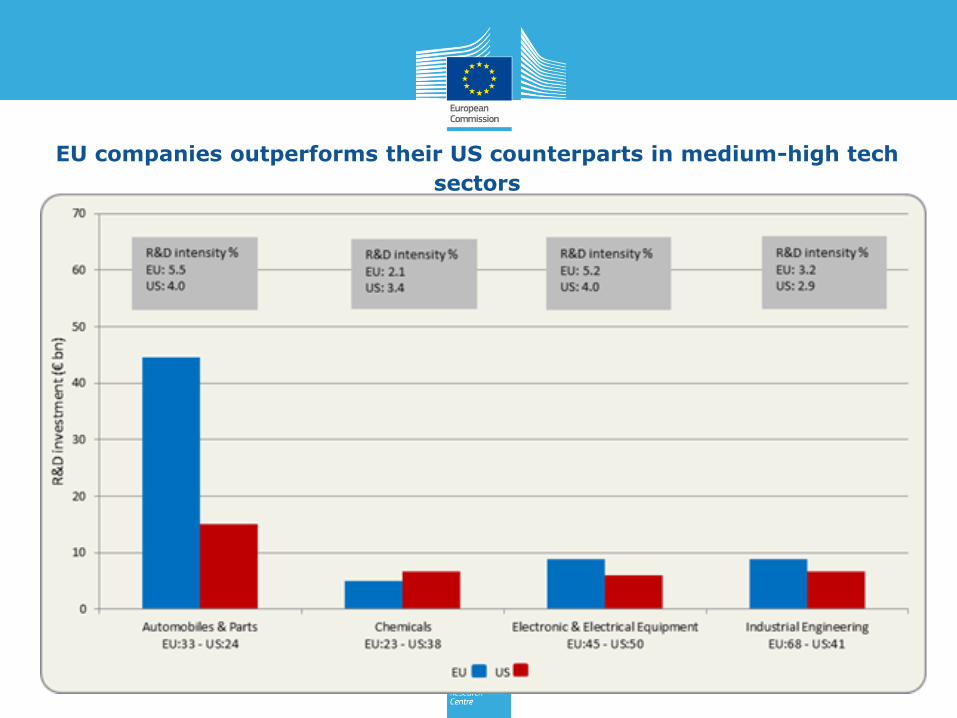

EU/US gap largely determined by differences in high-tech sectors related to

health and ICT

EU companies outperforms their US counterparts in medium-high tech

sectors