Embed Size (px)

Citation preview

AFRICAN DEVELOPMENT FUND

PROJECT COMPLETION REPORT

ADDIS ABABA INTERNATIONAL AIRPORT DEVELOPMENT PROJECT

FEDERAL DEMOCRATIC REPUBLIC OF ETHIOPIA

TRANSPORT DIVISION INFRASTRUCTURE DEPARTMENT-NORTH, EAST & SOUTH REGION

FEBRUARY 2006

TABLE OF CONTENTS

No. of Pages Equivalents and Abbreviations (i) Project Matrix (ii) Basic Project Data (iii-v) Executive Summary (vi-x)

1. INTRODUCTION 1 2. PROJECT OBJECTIVE AND FORMULATION 1 2.1 Project Objective 1

2.2 Description of the Project 1 2.3 Formulation, Evaluation and Approval 2

3. PROJECT EXECUTION 2 3.1 Effectiveness and Start-up 2 3.2 Modifications 2 3.3 Implementation Schedule 3 3.4 Reporting 4

3.5 Procurement 4 3.6 Financial Sources and Disbursements 5 4. PROJECT PERFORMANCE AND RESULTS 7 4.1 Overall Assessment 7 4.2 Operating Results 7 4.3 Institutional Performance 8 4.4 Management and Organisational Effectiveness 10 4.5 Staff Recruitment, Training and Development 10 4.6 Performance of Consultants, Contractors and Borrower 11 4.7 Conditions/Covenants 11 4.8 Economic Performance 11 4.9 Financial Performance 12 5. SOCIAL AND ENVIRONMENTAL IMPACT 13 5.1 Social Impact 13 5.2 Environmental Impact 13 6. PROJECT SUSTAINABILITY 13 7. PERFORMANCE OF THE BANK 14 8. OVERALL PERFORMANCE AND RATING 14 9. CONCLUSIONS, LESSONS LEARNT AND RECOMMENDATIONS 15

9.1 Conclusions 15 9.2 Lessons Learnt 16 9.3 Recommendations 17 This Report was prepared by Messrs. D.R.RAO, Consultant -Transport Engineer, D. GEBREMEDHIN, Consultant - Transport Economist and A. AKINTUNDE, Consultant-Financial Analyst, following their mission to Ethiopia from 31st December 2005 to 20th January 2006. The Task Manager is Mr. M.O.Ajijo, Principal Transport Economist, ONIN.3, Ext. 3110. Any inquiries relating to this report may be referred either to the Task Manager or to Mr. J. RWAMABUGA, Division Manager, ONIN.3, Ext. 2181.

LIST OF ANNEXES

Annex No. of No. Titles Pages

1. Project Location Map 1

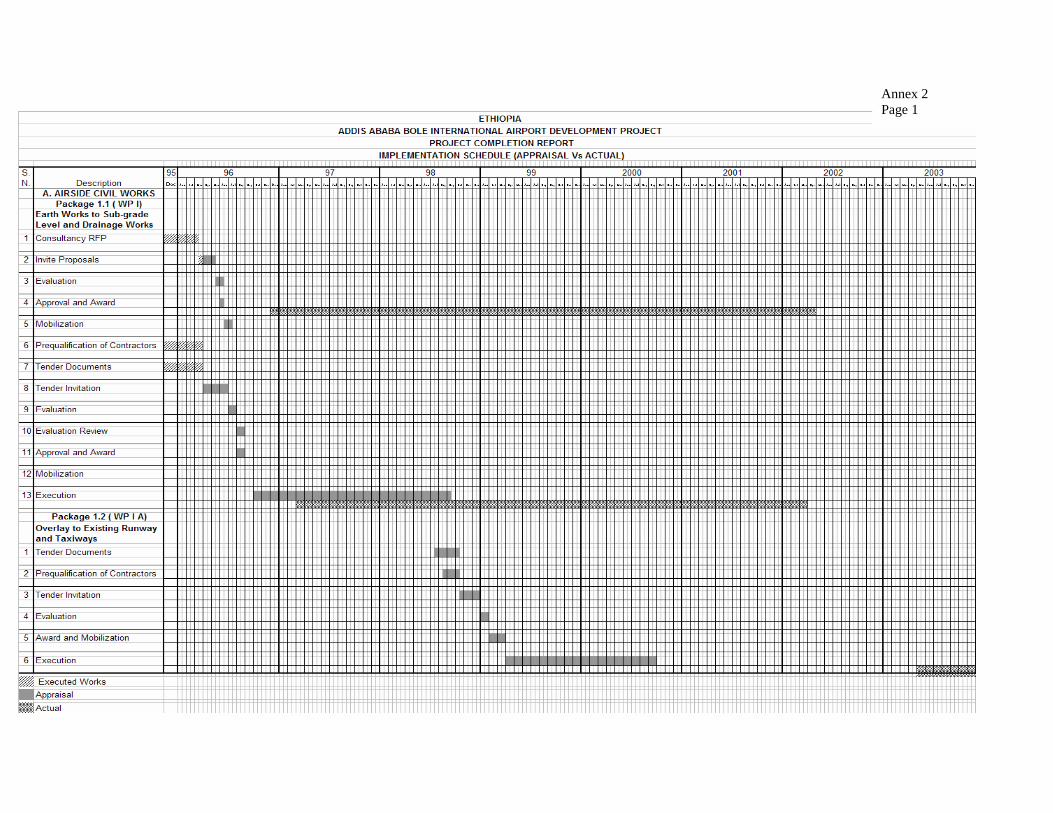

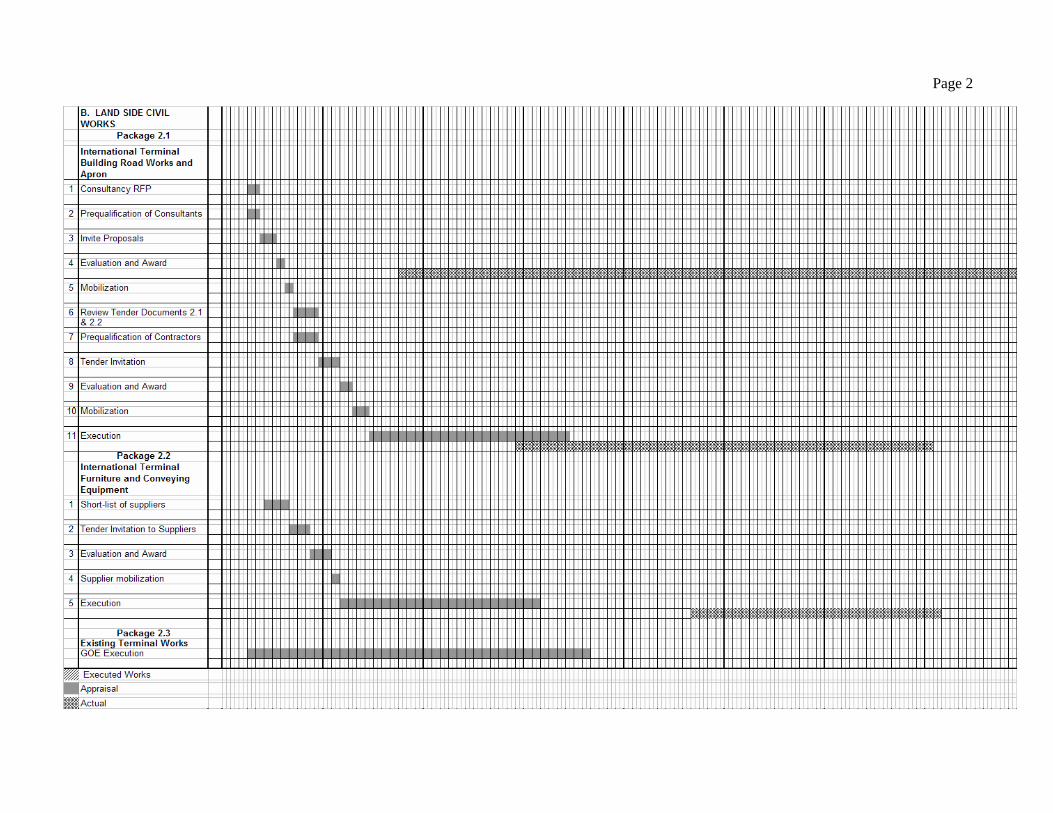

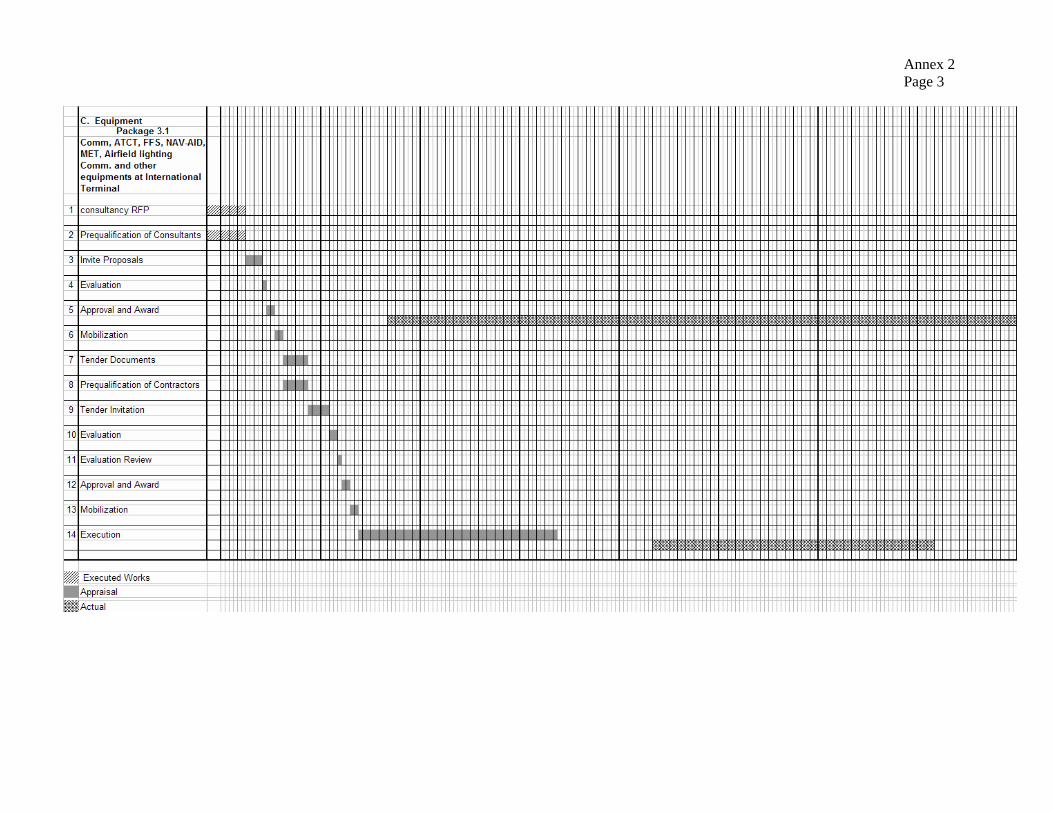

2 Implementation Schedule (Appraisal Vs Actual) 3

3. Actual Project Costs (Component & Source) and Categories of Expenditure 5 4. Yearly Disbursements by Source of Funds 2

5. Comparison of actual with projected revenue and expenditure 1

6. Calculation of Financial Rate of Return 2

7 Calculation of Economic Rate of Return 7

8. Performance Evaluation and Rating 4

9. Recommendations and Follow-up Matrix 1

10. Sources of Information 1

i

EQUIVALENTS AND ABBREVIATIONS

CURRENCY EQUIVALENTS PCR Appraisal

1 UA = ETB 12.3595 9.1892

WEIGHTS AND MEASURES

1.00 meter (m) = 3.281 ft. 1.00 kilometre (km) = 0.621 mile 1.00 square kilometre (km2) = 0.386 square mile (mi2) 1.00 hectare (ha) = 2.471 acres 1.00 kilogram (kg) = 2.205 lbs.

FISCAL YEAR : 8th July – 7th July ABBREVIATIONS

ADB = African Development Bank ADF = African Development Fund APA = Advance Procurement Action CAA = Civil Aviation Authority DCF = Discounted Cash flow Analysis EA = Executing Agency EAE = Ethiopian Airport Enterprise EAL = Ethiopian Air lines ECAA = Ethiopian Civil Aviation Authority EIA = Environmental Impact Assessment EIRR = Economic Internal Rate of Return ETB = Ethiopian Birr FE = Foreign Exchange FIRR = Financial Internal Rate of Return GOE = Government of Ethiopia ICAO = International Civil Aviation Organisation ICB = International Competitive Bidding ILS = Instrument Landing System LC = Local Cost MOTAC = Ministry of Transport and Communications NPV = Net Present Value PCR = Project Completion Report PIU = Project Implementation Unit RE = Resident Engineer RFP = Request for Proposals TAF = Technical Assistance Fund TCDE = Transport Construction Design Enterprise TOR = Terms of Reference UA = Unit of Account UNDP = United Nations Development Programme WP 1 = Works Package for Airside Works WP 1 A = Works Package for Pavement Strengthening Works (Overlays)

iiETHIOPIA

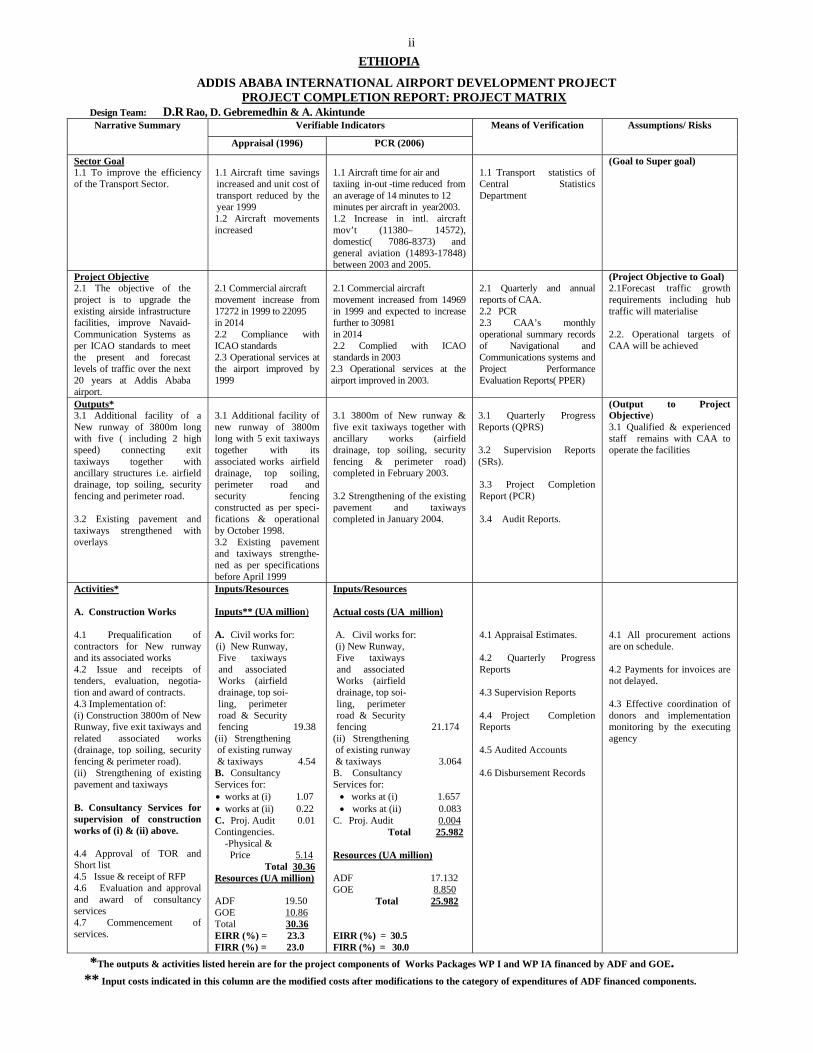

ADDIS ABABA INTERNATIONAL AIRPORT DEVELOPMENT PROJECT PROJECT COMPLETION REPORT: PROJECT MATRIX

Design Team: D.R Rao, D. Gebremedhin & A. Akintunde Verifiable Indicators Narrative Summary

Appraisal (1996) PCR (2006)

Means of Verification Assumptions/ Risks

Sector Goal 1.1 To improve the efficiency of the Transport Sector.

1.1 Aircraft time savings increased and unit cost of transport reduced by the year 1999 1.2 Aircraft movements increased

1.1 Aircraft time for air and taxiing in-out -time reduced from an average of 14 minutes to 12 minutes per aircraft in year2003. 1.2 Increase in intl. aircraft mov’t (11380– 14572), domestic( 7086-8373) and general aviation (14893-17848) between 2003 and 2005.

1.1 Transport statistics of Central Statistics Department

(Goal to Super goal)

Project Objective 2.1 The objective of the project is to upgrade the existing airside infrastructure facilities, improve Navaid-Communication Systems as per ICAO standards to meet the present and forecast levels of traffic over the next 20 years at Addis Ababa airport.

2.1 Commercial aircraft movement increase from 17272 in 1999 to 22095 in 2014 2.2 Compliance with ICAO standards 2.3 Operational services at the airport improved by 1999

2.1 Commercial aircraft movement increased from 14969 in 1999 and expected to increase further to 30981 in 2014 2.2 Complied with ICAO standards in 2003 2.3 Operational services at the airport improved in 2003.

2.1 Quarterly and annual reports of CAA. 2.2 PCR 2.3 CAA’s monthly operational summary records of Navigational and Communications systems and Project Performance Evaluation Reports( PPER)

(Project Objective to Goal) 2.1Forecast traffic growth requirements including hub traffic will materialise 2.2. Operational targets of CAA will be achieved

Outputs* 3.1 Additional facility of a New runway of 3800m long with five ( including 2 high speed) connecting exit taxiways together with ancillary structures i.e. airfield drainage, top soiling, security fencing and perimeter road. 3.2 Existing pavement and taxiways strengthened with overlays

3.1 Additional facility of new runway of 3800m long with 5 exit taxiways together with its associated works airfield drainage, top soiling, perimeter road and security fencing constructed as per speci- fications & operational by October 1998. 3.2 Existing pavement and taxiways strengthe- ned as per specifications before April 1999

3.1 3800m of New runway & five exit taxiways together with ancillary works (airfield drainage, top soiling, security fencing & perimeter road) completed in February 2003. 3.2 Strengthening of the existing pavement and taxiways completed in January 2004.

3.1 Quarterly Progress Reports (QPRS) 3.2 Supervision Reports (SRs). 3.3 Project Completion Report (PCR) 3.4 Audit Reports.

(Output to Project Objective) 3.1 Qualified & experienced staff remains with CAA to operate the facilities

Activities* A. Construction Works 4.1 Prequalification of contractors for New runway and its associated works 4.2 Issue and receipts of tenders, evaluation, negotia- tion and award of contracts. 4.3 Implementation of: (i) Construction 3800m of New Runway, five exit taxiways and related associated works (drainage, top soiling, security fencing & perimeter road). (ii) Strengthening of existing pavement and taxiways B. Consultancy Services for supervision of construction works of (i) & (ii) above. 4.4 Approval of TOR and Short list 4.5 Issue & receipt of RFP 4.6 Evaluation and approval and award of consultancy services 4.7 Commencement of services.

Inputs/Resources Inputs** (UA million) A. Civil works for: (i) New Runway, Five taxiways and associated Works (airfield drainage, top soi- ling, perimeter road & Security fencing 19.38 (ii) Strengthening of existing runway & taxiways 4.54 B. Consultancy Services for: • works at (i) 1.07 • works at (ii) 0.22 C. Proj. Audit 0.01 Contingencies.

-Physical & Price 5.14

Total 30.36 Resources (UA million) ADF 19.50 GOE 10.86 Total 30.36 EIRR (%) = 23.3 FIRR (%) = 23.0

Inputs/Resources Actual costs (UA million) A. Civil works for: (i) New Runway, Five taxiways and associated Works (airfield drainage, top soi- ling, perimeter road & Security fencing 21.174

(ii) Strengthening of existing runway & taxiways 3.064 B. Consultancy Services for: • works at (i) 1.657 • works at (ii) 0.083

C. Proj. Audit 0.004 Total 25.982 Resources (UA million) ADF 17.132 GOE 8.850 Total 25.982 EIRR (%) = 30.5 FIRR (%) = 30.0

4.1 Appraisal Estimates. 4.2 Quarterly Progress Reports 4.3 Supervision Reports 4.4 Project Completion Reports 4.5 Audited Accounts 4.6 Disbursement Records

4.1 All procurement actions are on schedule. 4.2 Payments for invoices are not delayed. 4.3 Effective coordination of donors and implementation monitoring by the executing agency

*The outputs & activities listed herein are for the project components of Works Packages WP I and WP IA financed by ADF and GOE. ** Input costs indicated in this column are the modified costs after modifications to the category of expenditures of ADF financed components.

iii

BASIC PROJECT DATA

1. Country : Ethiopia 2. Project : Addis Ababa International Airport Development Project 3. Loan Number : 2100150000304 4. Borrower : Government of Ethiopia 5. Beneficiary : Government of Ethiopia 6. Executing Agency : Civil Aviation Authority (CAA) A. LOAN DETAILS

Description At Appraisal

Actual

1.ADF Loan (UA million) 19.50 17.132 2. Commitment Fees 3. Service Charge

0.5% per annum on the un disbursed portion commencing 90 days after the signing of the loan agreement 0.75% per annum on amounts disbursed and outstanding.

4. Repayment Period 40 years

5. Grace Period 10 years

6. Repayment 1% of the principal each year from the eleventh to twentieth year inclusive and 3% each year thereafter.

7.Loan Negotiation Date 29-30 August 1996 8. Loan Approval Date 31-10-1996 9. Loan Signature Date 20-12-1996 10.Date of Entry into Force 11-07-1997

B. PROJECT DATA 1. Project Costs*

Item of Cost Appraisal Modified Actual Foreign Exchange Component 20.50 20.50 18. 219 Local Cost Component 12.43 9.86 7. 763 Total Cost 32.93 30.36 25. 982

(*Project Costs include for both Work packages WP1 & WP1A and Supervision services) 2. Source of Finance*

In UA Million Appraisal Modified Actual Source of

Finance F.E. L.C. Total F.E. L.C. Total F.E. L.C. Total

ADF 19.50 - 19.50 19.50 - 19.50 17.132 - 17.132 GOE 1.00 12.43 13.43 1.00 9.86 10.86 1.087 7.763 8.850 Total 20.50 12.43 32.93 20.50 9.86 30.36 18.219 7.763 25.982

(* Source of Finance includes for both Work packages WP1 & WP1A and Supervision services) Appraisal Actual 3. Effective Date of First Disbursement: - 07 August 1997 4. Effective Date of Last Disbursement: 31 December 1999 31 December 2004 5. Commencement of Project: November 1996 March 1997 6. Completion of Project November 1998 January 2004

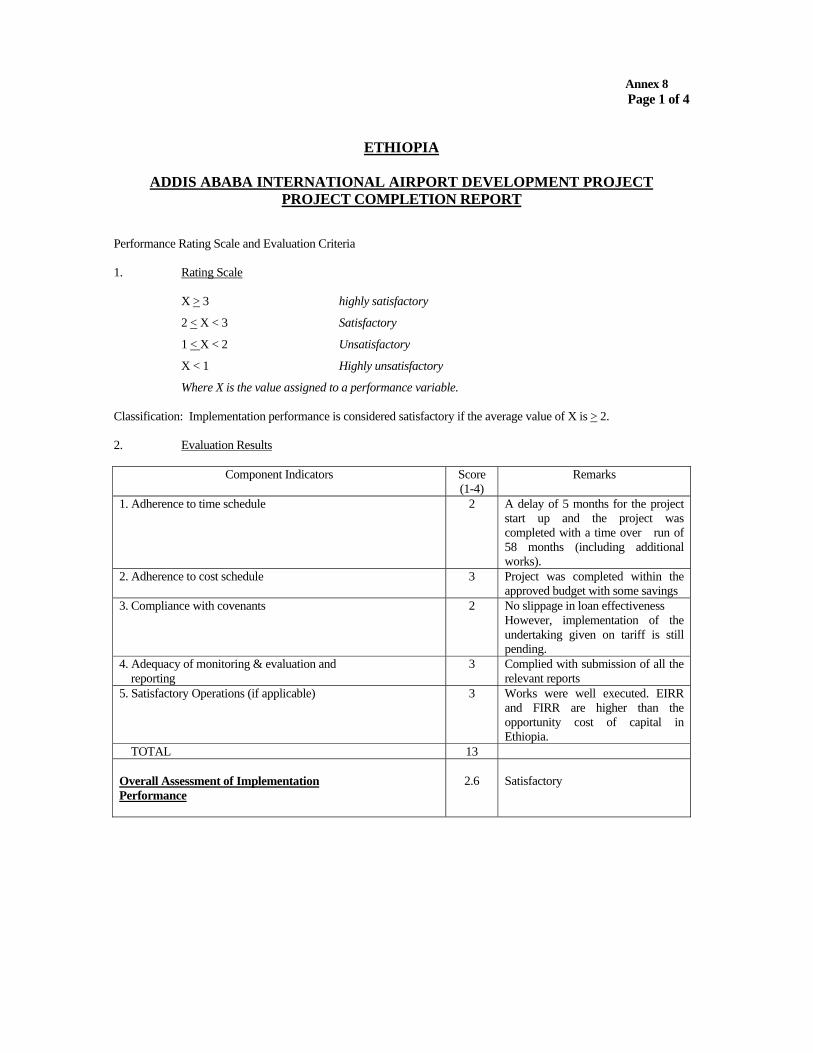

ivC. PERFORMANCE INDICATORS 1. Cost Under-run : 14.43% 2. Time Overrun( including additional works) : 58 months * Slippage on Effectiveness (%) : Nil * Slippage on Completion Date : 242% * Slippage on Last Disbursement : 500% * Number of Extensions of Loan Validity Period : 5 3. Project Implementation Status : Completed 4. List of Verifiable Indicators and Levels of Achievement

Score Evaluation Criterion Maximum Actual

1. Time Overruns 2. Cost Overruns / Under Run 3. Adherence to Contractual Conditions 4. Adequacy of Supervision and Reports 5. Operational Performance Total Score

4 4 4 4 4 20

2 3 2 3 3

13 5. Implementation Performance

* Institutional Performance : Satisfactory * Consultant’s Performance : Satisfactory * Contractor’s Performance : Satisfactory

6. Economic Internal Rate of Return (EIRR): Appraisal : 23.3%

Actual : 30.5% 7. Financial Internal Rate of Return( FIRR): Appraisal : 23% Actual : 30% D. MISSIONS

Project Cycle M/Y Numbers of Persons Composition Man Days 1. Identification - - - - 2. Preparation - - - - 3. Appraisal 05/1996 3 T.Engr, T.Econ, F.A 42 4. Supervision/follow up 03/ 1998

12/1998 09/1999 06/2000 11/2000 07/2001 11/2001 06/2002 12/2002 06/2003 11/2003 04/2004 11/2004

2 2 2 3 2 2 1 2 1 2 2 1 3

T.Engr;T.Econ T.Engr, F.A T.Engr,F.A DM,T.Engr,T.Econ T.Engr,T.Econ T.Engr,T.Econ T.Econ. T.Econ, T.Engr T.Econ. T.Econ, T.Engr T.Econ,T.Engr T.Econ. DM,T.Econ,T.Engr

42 28 28 50 42 42 14 42 19 28 28 10 42

5. PCR 01/2005 3 T.Engr, T.Econ, F.A 44 DM: Division Manager; T.Engr: Transport Engineer; T.E: Transport Economist; F.A: Financial Analyst.

v

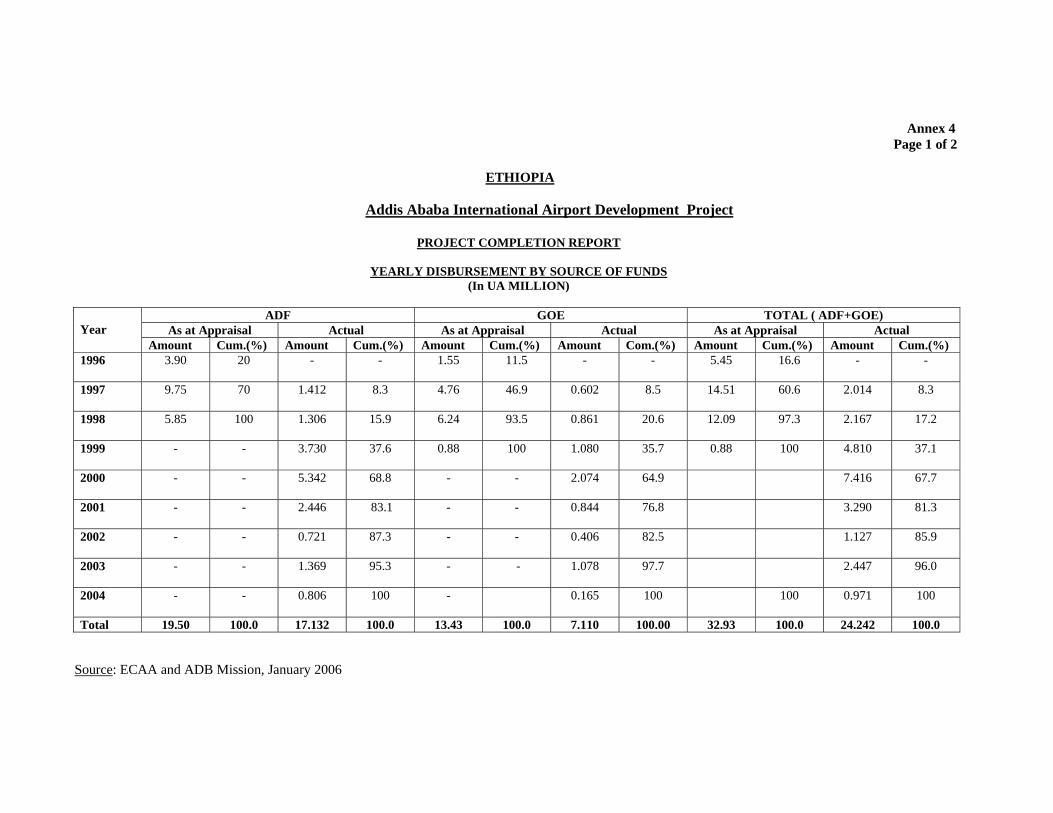

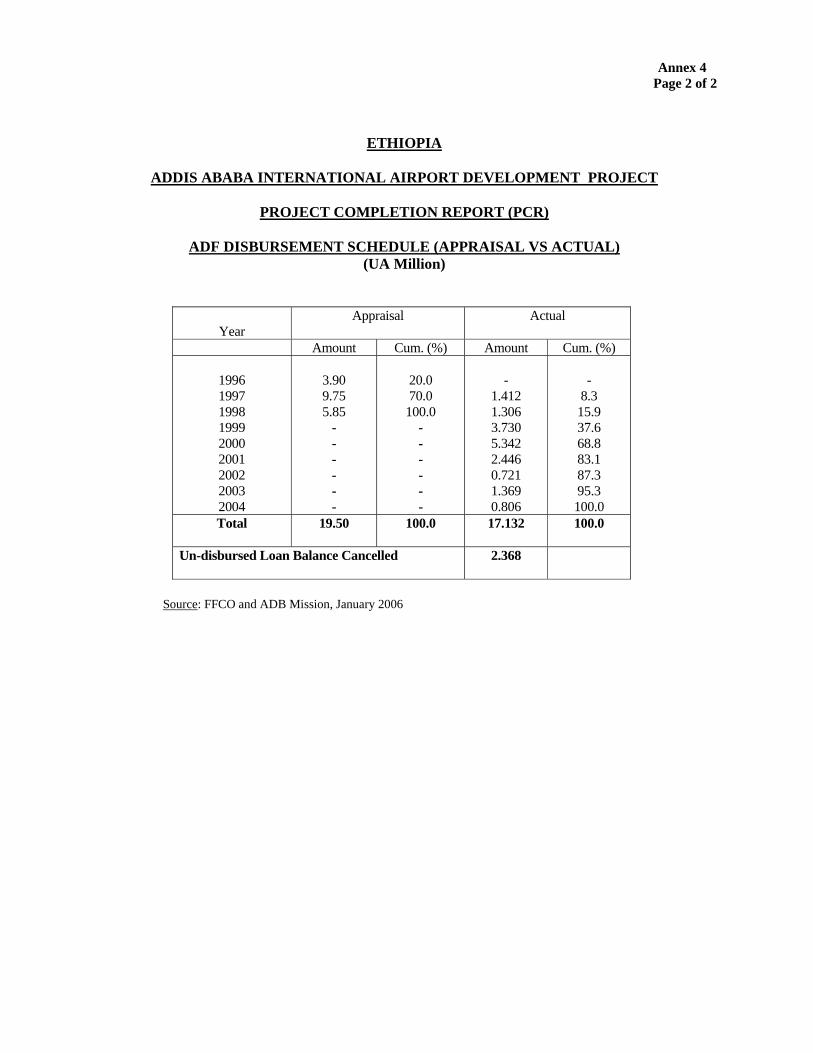

E. BANK LOAN –DISBURSEMENTS (UA MILLION)

Appraisal Actual Year Amount Cum. (%) Amount Cum. (%)

1996 1997 1998 1999 2000 2001 2002 2003 2004

3.90 9.75 5.85

- - - - - -

20.0 70.0 100.0

- - - - - -

-

1.412 1.306 3.730 5.342 2.446 0.721 1.369 0.806

-

8.3 15.9 37.6 68.8 83.1 87.3 95.3 100.0

Total 19.50 100.0 17.132 100.0 Un-disbursed Loan Balance Cancelled

2.368

F. CONTRACTOR ( Package WP1 ) Name : Kajima-Keangnam JV (Japan-S. Korea)

Contract Description : Package WP1: Construction works for New Runway, 5 Taxiways, drainage structures, Perimeter Road &Security fencing Date Works Commenced : 14th March 1997

Date Contract Completed : February 2001 (excluding defects liability period of 12 months) Contract Duration : 59 months Amount : ETB 175.27 million (actual ETB 190.88 million) CONTRACTOR ( Package WP 1A) Name : M.A.Al-Kharafi and Sons ( Kuwait)

Contract Description : Package WP1A: Strengthening of Existing Runway and Taxiway Date Works Commenced : 4th April 2003

Date Contract Completed : 31 January 2004 (excluding defects liability period of 12 months) Contract Duration : 9 months Amount : ETB 45.94 million (actual ETB 32.45 million) G CONSULTANT ( Supervision of works for Package WP1, GOE financing) Name : Dar -Al Handasah (Lebanon) Contract Description : Supervision of Works for Works Package WP1 Date Contract Signed : 15th August 1996 Date Supervision Commenced : 15th August 1996 Date Contract Completed : 31 December 1998 (extended up to 28 Feb 2002) Contract Duration : 27 months, extended to 66 months Amount : US $ 1. 28 million + ETB 3.29 million (actual ETB 16.78 million) CONSULTANT ( Supervision of works for Package WP1A, GOE Financing) Name : Transport Construction Design Enterprise, TCDE (Ethiopia) Contract Description : Supervision of Works for Works Package WP 1A Date Contract Signed : 1st November 2001 Date Supervision Commenced : 1st November 2001 Date Contract Completed : 31 January 2004 Contract Duration : 27 months Amount : ETB 0.925 million

vi

EXECUTIVE SUMMARY

1. INTRODUCTION 1.1 Ethiopia, situated in the North-Eastern corner of Africa has an area of about 1.14 million km2 land. The country is bounded in the North by Eritrea, in the West by Sudan, in the East by Somalia and Djibouti, and in the South by Kenya (Annex 1). The projected population of the country is 73 million in 2005. The project is located within the capital city (Addis Ababa) international airport at Bole. 1.2 As a part of overall strategy to promote economic growth, priority was given by the Government of Ethiopia (GOE) to the development of transport infrastructure of the country with emphasis on airport infrastructure. As a follow up, Addis Ababa Airport which is the country’s main international and domestic airport, situated at Bole on the southern outskirts of the city, was accorded priority for its immediate development to the requirements of ICAO standards. Initial master plan studies for the Addis Ababa Airport were carried out under the UNDP-ICAO technical assistance. The Bank has to date approved two projects and one study in the air sub-sector, these have been successfully completed. 1.3 The detailed economic feasibility and engineering design of the project (both landside and airside packages) were completed in December 1993 with the assistance of ADF /TAF resources. During a Donors meeting in November 1995, the Bank agreed to finance some components of the airside package which included the construction of the new runway of 3800 m with five exit taxiways together with its ancillary structures. A Bank’s mission visited Ethiopia in May 1996 to appraise the project. The loan conditions were negotiated and there were no issues of disagreement raised by the Bank or the Borrower. The loan amount of UA 19.50 million was approved by the Board in October 1996, signed in December 1996 and declared effective in July 1997. 1.4 This Project Completion Report (PCR) is based on the appraisal report, project files in the Bank, Borrower’s quarterly progress reports, Construction final reports and PCR, interviews and site inspection conducted during an ADB mission to Ethiopia in January 2006. Project Objective and Description 1.5 The objective of the project is to upgrade the existing airside infrastructure facilities, improve Navaid-Communication Systems as per ICAO standards to meet the present and forecast levels of traffic over the next twenty years at Addis Ababa airport. 1.6 The project consists basically of six components:

(i) Civil works for (a) construction of a new runway of 3800m long with five exit taxi

ways; (b) airfield drainage and top soiling; and (c) security fencing and perimeter road;

(ii) Supply, installation and commissioning of Airside equipment, Airfield lighting and Navaid communication systems;

(iii) Construction of new rigid apron of 70,000 sq.m; (iv) Construction works for strengthening of existing pavements ( overlays); (v) Institutional Support to Project Management Unit ; (vi) Consultancy services for supervision of components (i) to (iv) above, and audit of

civil works of (i) above.

At appraisal, the ADF financed components were at (i) above and the audit of civil works under the component (vi). However, during implementation, after realising some savings under the approved ADF loan, the Bank at the request of the GOE, agreed to finance the strengthening works for the existing pavement (overlays) component at (iv) above, that was to be financed fully by the Government. GOE financed the supervision consultancy services for the above both components.

vii

1.7 There was no change in the project objective, however some modifications to the design were effected during implementation, due to the site conditions. Project Execution and Implementation Schedule

1.8 The Project was executed by the Civil Aviation Authority (CAA) through the Project Coordinator of the established Project Implementation Unit (PIU) and with the support of the supervision consultant. 1.9 The ADF financed components (airside package works) of the project as envisaged at appraisal was to commence in November 1996 and completed in November 1998 (24 months). Though procurement actions for the works were completed as early as in October 1996, due to protracted negotiations, the contract was awarded only on 8th March 1997 to the lowest evaluated bidder, i.e. M/s Kajima Keangnam, JV (Japan- S. Korea); works commenced on 14 March 1997 and were completed in all respects in February 2002 with long delay due to modifications to the pavement design, adverse weather conditions coupled with constraints of execution of works under the operational airport. The contract for the “Strengthening works of the existing pavement, WP 1A (overlays)”, was awarded to M/s M. A. Al-Kharafi & Sons (Lebanon) on 1st April 2003, and were completed in January 2004. 1.10 Consultancy services for supervision of ADF financed airside package WP I works (financed by GOE) was awarded to M/s Dar –Al Handsah (Lebanon). Services commenced on 15 August 1996 and were completed in February 2002. Similarly, consultancy services for the supervision of the strengthening works (WP IA) was awarded to Transport Construction Design Enterprise, TCDE (Ethiopia) on 1st November 2001 and continued until the completion of the strengthening works in January 2004. 1.11 In spite of delays during implementation, the final outputs of the new runway and its ancillary structures were well executed. The new facilities provided under the project at Addis Ababa Airport, benefited the country in the improvement of air transport services both in international and domestic routes. Annex 2 shows the implementation schedule at Appraisal vs Actual.

Project Costs and Financial Resources

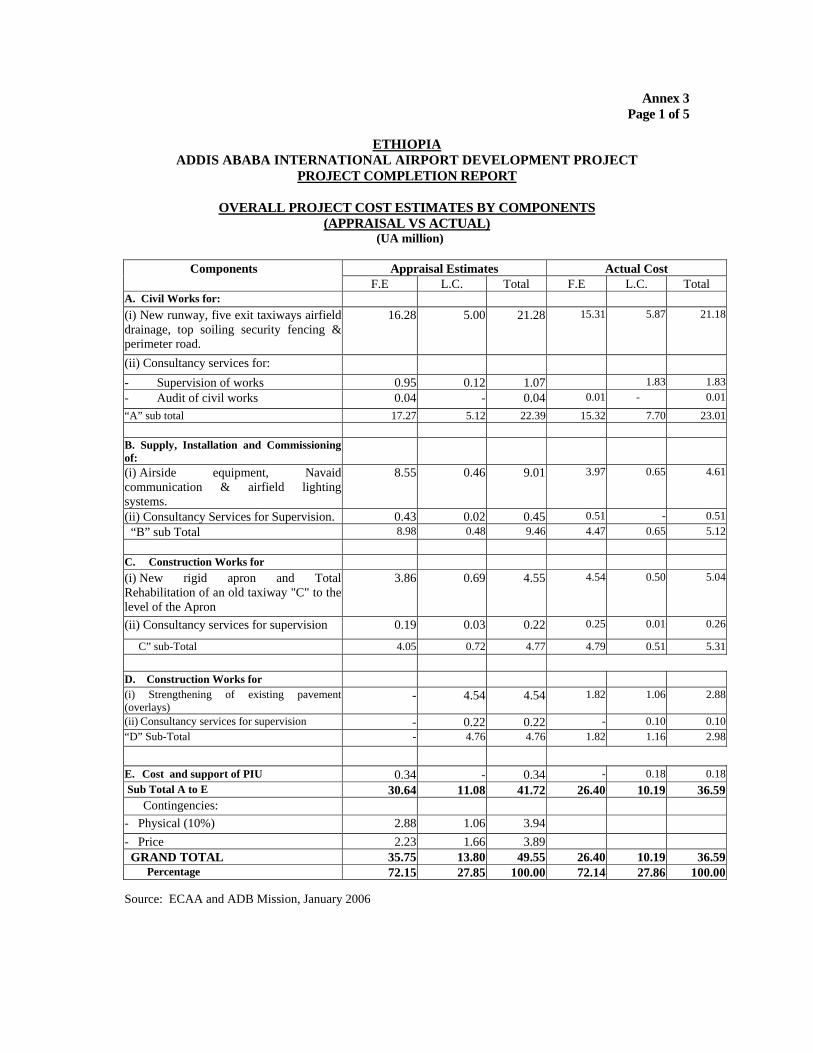

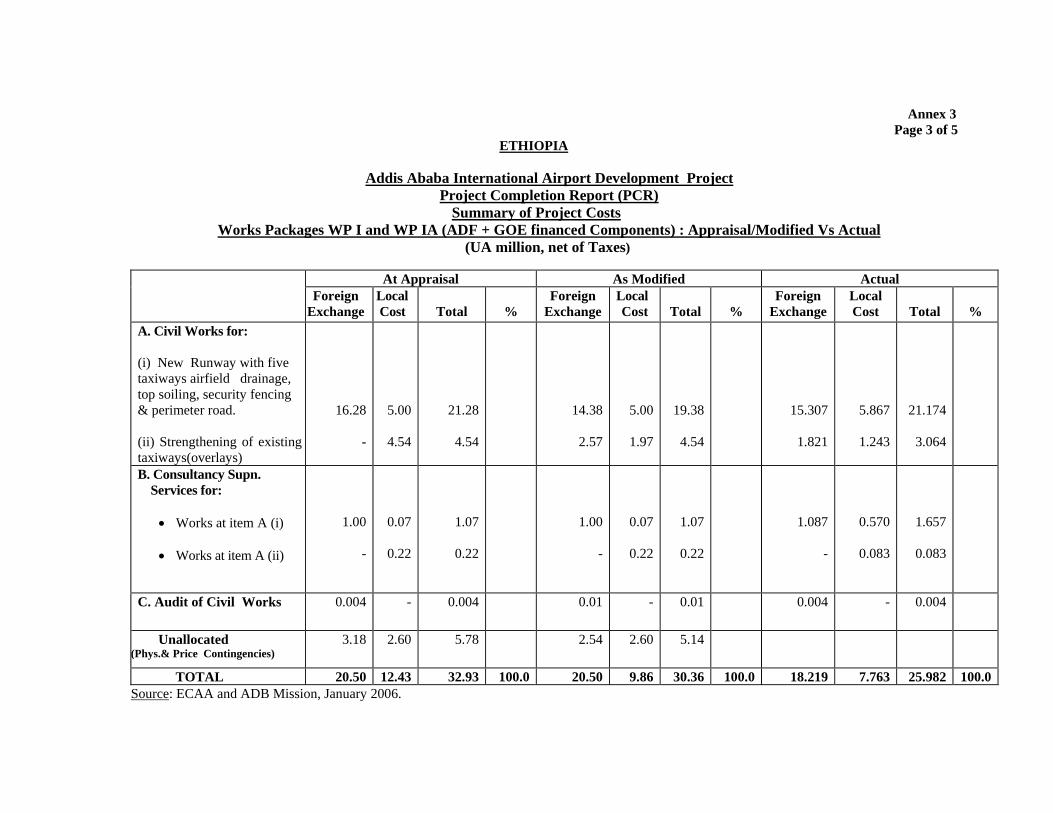

1.12 At appraisal, the cost of the ADF financed works package WP I and WP IA (including project audit and supervision of works financed by GOE) was estimated at UA 32.93 million. The actual total cost of completion of the ADF financed package works WP 1 and WP 1A (including project audit and consultancy services for supervision) was UA 25.982 million. 1.13 The total completed cost of the ADF components of the project (UA 17.132 million) for both packages, i.e. WP 1 (New Runway and ancillary works) and WP 1A (strengthening works), was noted to be less than the approved loan amount of UA 19.50 million. The Bank with the consent of the Government cancelled the balance of UA 2.368 million realized as savings under the ADF loan. A summary of the project costs at appraisal, modified and actual is shown in Table 3.1 and details in Annex 3. Overall, there was a cost under run of about UA 4.38 million.

Overall Assessment 1.14 In spite of some delays during project implementation, a well designed new runway facility with Navaid and Communication systems at the Addis Ababa airport conforming to ICAO standards, had benefited the country with significant improvements in the air transport services both on the international and domestic routes. The operation of the airport with new facilities provided under the project, significantly reduced the aircraft movements time especially in taxi in- and -out times.

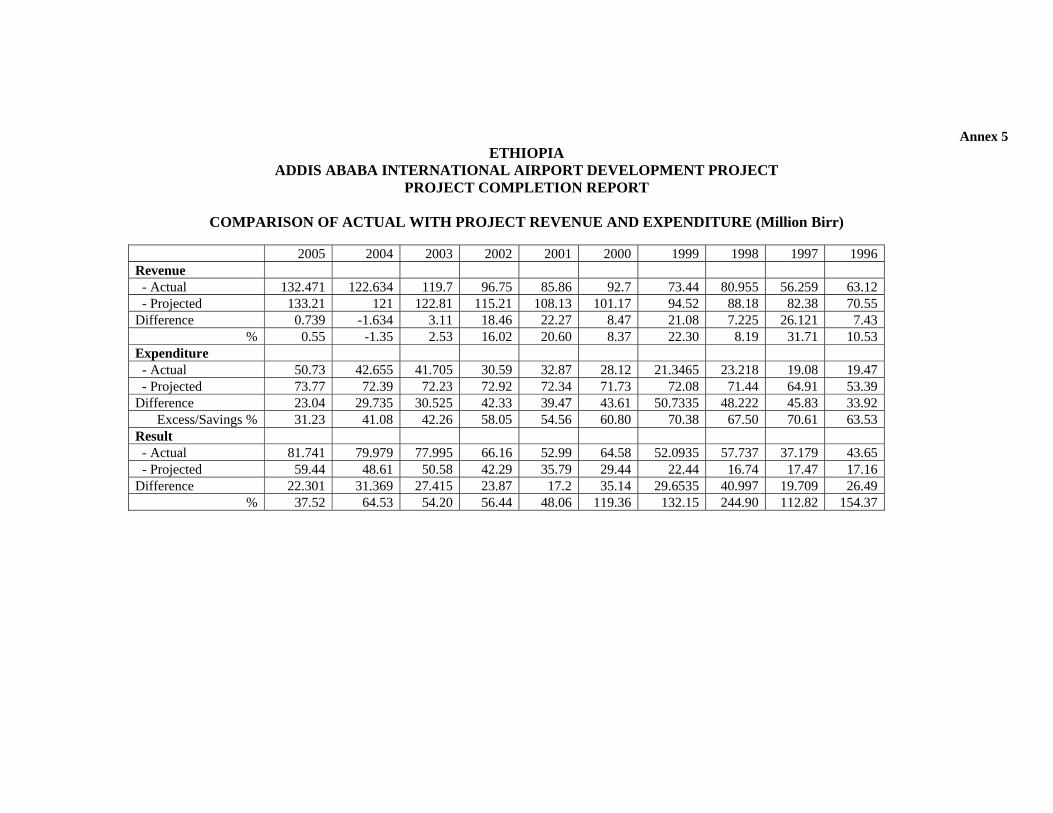

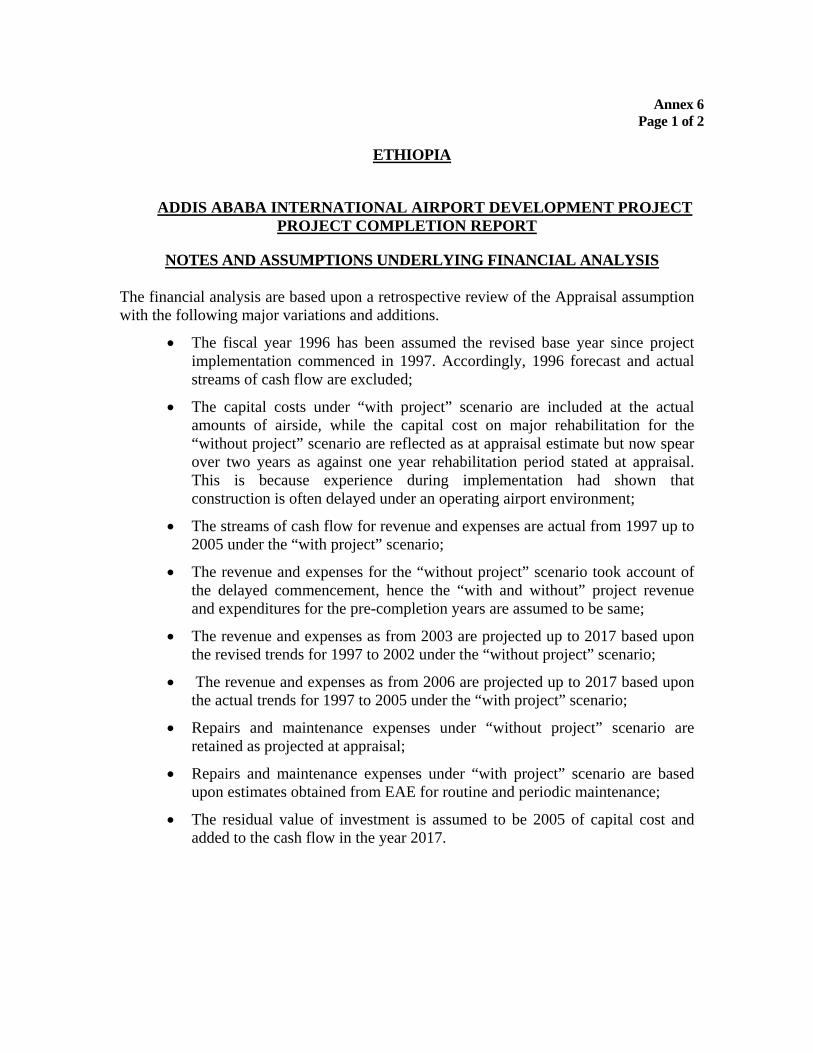

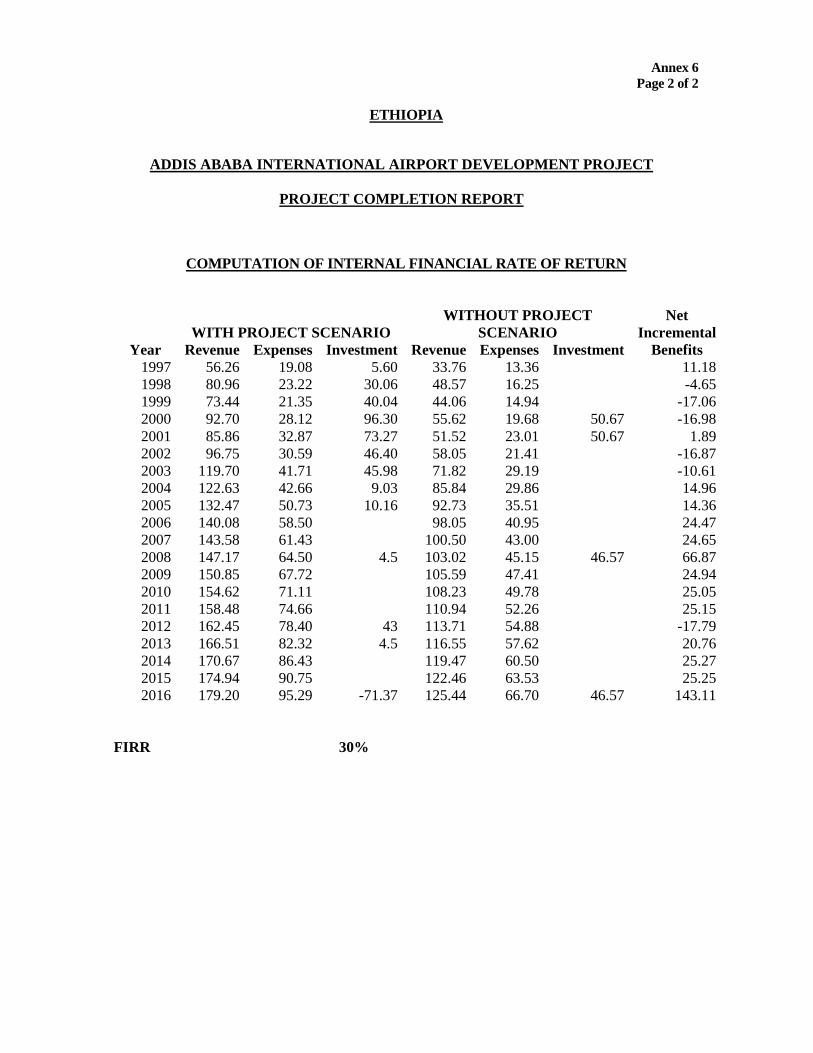

viii Economic Performance 1.15 The traffic projection at appraisal has been revised taking into account the 1994-2005 data, which is used as the basis for traffic forecast. The actual traffic after the project completion (2003 – 2005) shows an annual growth rate of 21.8% (international passengers), 8.8% (domestic passengers), 13.3% (international commercial aircraft movement), 8.7% (domestic aircraft movement), 9.5% (general aviation movement) and 32.3% (EAL cargo). However, a decline of 20.0% was recorded for foreign carrier cargo. Based on the historical traffic annual growth rates, the international passenger, domestic passenger, international aircraft, domestic aircraft, general aviation, EAL and foreign carrier cargo are projected to grow at an average annual growth rate of 3% to 6% between 2006 and 2010 and after the year 2011 by 2% to 4%. 1.16 The actual traffic for the year 2005 when compared with the appraisal forecasts shows an increase of 13.8%, 13.9%, 66.5% for international passenger, commercial international aircraft and general aircraft movement respectively. On the other hand, the domestic passenger, commercial domestic aircraft movement, EAL and foreign carrier cargoes have declined by 32.4 %, 25.6%, 66.4% and 49.2% respectively. The recalculated EIRR has been estimated to be 30.5 % (Annex 7 page 7 of 7). This compared with 23.3 % at appraisal is high, due to the growth in the international passenger, aircraft and general aircraft movement, 23.9 % reduction in the airside construction cost and capital cost disbursement over eight years period as compared to four years anticipated at appraisal. This EIRR of 30.5 % is well above the opportunity cost of capital of 11% in Ethiopia Financial Performance 1.17 The appraisal forecasts were in excess of actual revenue by an average of 12% per annum over the period. The projected expenses were equally over-estimated with actual performance yielding average savings of about 56% per annum over the same period. Consequently, the actual financial results surpassed appraisal forecasts on the average by as much as 100% per annum. The comparison of the actual with estimated revenue and expenses is presented in Annex 5. 1.18 A retrospective financial analysis based upon the resulting stream of cash flows adopting with and without scenarios is presented in Annex 6. Based on this, the financial internal rate of return is estimated to be 30%, which is well above the appraisal estimate of 23% and the current opportunity cost of capital of 11% in Ethiopia. This performance is accounted for by increased cash flows resulting from better margins than envisaged at appraisal, savings on project cost and longer spread of disbursements.

2. CONCLUSIONS, LESSONS LEARNT AND RECOMMENDATIONS

Conclusions

2.1 The overall objectives of the project have been fully achieved. The additional facilities provided at the Addis Ababa Airport with a new runway and its ancillary structures, significantly improved the air transport services both on international and domestic routes. The constructed new runway has a good riding smooth surface and found to be safe in landing and taking off operations and is environmentally protected. The value and quality of the project was greatly enhanced despite some delays during the project implementation. The re-calculated EIRR and FIRR at PCR in respect of the ADF components are 30.5 % and 30.0% respectively.

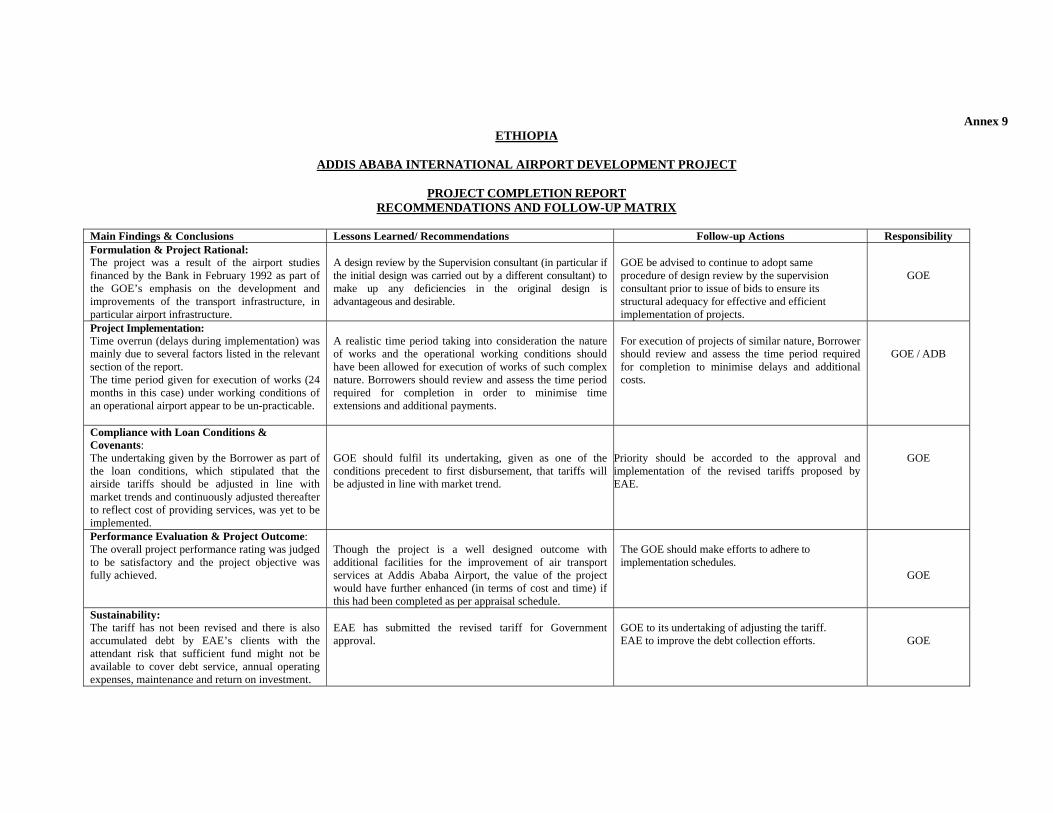

ix Lessons Learned 2.2 Lessons from the project are: The lessons learned from the project are given hereunder: The time period given for execution of works (24 months in this case) under working conditions of an operational airport appear to be un-practicable. A realistic time period taking into consideration the nature of works and the operational working conditions should have been allowed for execution of works of such complex nature. (para 3.3.3);

• Adequate attention is necessary by the concerned disbursement officers of the Bank when apportioning currencies of payments to the concerned parties, before effecting the disbursements. (para 3.6.4);

• The Bank ought to have followed up, during negotiation, some of the weaknesses observed at appraisal concerning the accounting and management practices of the EA, to obtain an undertaking from the Borrower to strengthen those weaknesses. (paras 4.3.3 and 4.3.8);

• The non-audit of financial statements of EAs also borders on non-compliance with local laws. The Bank ought to have ensured submission of the EAs audited accounts at the same time the project’s audited accounts were being submitted. (paras 4.3.5 and 4.3.6);

• In order to protect the investment, the tariff revision is important. GOE should therefore expedite approval of the recommendations of the tariff proposed by EAE for implementation without further delay. (paras 4.3.9 and 4.7.1);

• A pre-design review (before issue of tender bids) by the selected consultant (if different from the original detailed design consultant) before launching the bids is always preferable, as this would bring out the deficiencies if any, in the original design and at the same time avoid modifications (involving additional costs) during execution. In the case at hand, though there was an initial delay in the start up of the project construction due to pre-design review; this proved to be effective in the review of design deficiencies at the early stages and elimination of the unexpected risks and difficulties. The project was executed and completed successfully with no modifications during the execution stage. It is understood that this is now being followed for all Bank financed projects. (para 4.6.1). Recommendations

2.3 It is recommended that:

For the Borrower

• For execution of projects of similar nature (in particular under operational conditions), Borrowers should review and assess the time period required for completion in order to minimise time extensions and additional payments. (para 3.3.3);

• Rectify the defects observed during the field inspection of the completed project (Para. 4.2.2); • GOE should ensure strengthening of the financial management capacity of ECAA and EAE.

Specifically, the introduction of fixed assets register, aggressive debt collection, and preparation of periodic accounts on a timely basis should receive immediate attention. (para 4.3.3);

• GOE to ensure that the audit of financial statements of ECAA and EAE are undertaken firstly to clear the backlog and thereafter on a regular annual basis to ensure that they do not fall into arrears again in the future. (paras 4.3.5 and 4.3.6); and

• GOE should fulfil its undertaking given as one of the conditions precedent to first disbursement, that tariffs will be adjusted in line with market trend. Priority should be accorded to the approval and implementation of the revised tariffs proposed by EAE (paras 4.3.9 and 4.7.1).

For the Bank

• Bank should be more practical in examining and specifying realistic time period required (during appraisal stage) for execution of projects of similar nature (in particular under operational conditions). (para 3.3.3);

• Adequate care should be exercised in making entries concerning apportionment of currencies especially at the contract entry into SAP. (para 3.6.4);

x • Future Bank operations should not only look at the financial management capacity and health of

EAs, but also ensure where appropriate, insertion of clauses requiring that observed weaknesses in the accounting and management practices are strengthened to safeguard Bank’s investment. (para 4.3.3);

• Future Bank operations should ensure as a matter of routine, the enforcement of submission of audit reports of both the EA and project on timely basis. (paras 4.3.5 and 4.3.6);

• Bank to follow up with the GOE on the fulfillment of the undertaking on tariff adjustments given as part of the loan conditions. ( paras 4.3.9 and 4.7.1);

• The problems surrounding the non-fulfilment of loan conditions, weaknesses in financial and management practices of ECAA and EAE, non-audit of accounts should be taken up as issues for future policy dialogue with GOE; and

• The Bank should develop appropriate response to future similar laxities and non-fulfilment of loan conditions by Borrowers.

1

1. INTRODUCTION 1.1 Ethiopia, situated in the North-Eastern corner of Africa has an area of about 1.14 million square km2 land area. The country is landlocked and is bounded in the North by Eritrea, in the West by Sudan, in the East by Somalia and Djibouti, and in the South by Kenya (Annex 1). The projected population of the country is 73 million in 2005. The project is located within the capital city (Addis Ababa) international airport at Bole. 1.2 The transport system of Ethiopia consists of four modes of which road is the dominant. The four modes are: (i) a road network of about 37, 018 km, (ii) 781 km of railways, (iii) minor river and lake transport services; and (iv) fifteen commercial airports and several rudimentary airstrips. The country is served by two international airports (Addis Ababa and Dire Dawa), seven major and six medium sized domestic airports. At the time of the project appraisal, most of the airports ( including Addis Ababa airport at Bole) does not fully conform to the ICAO standard infrastructure requirements, as most of the main facilities, such as runway, taxi track etc had significantly deteriorated due to various factors. 1.3 As a part of overall strategy to promote economic growth, priority was given by the Government of Ethiopia (GOE) to the development of transport infrastructure of the country with emphasis on airport infrastructure. As a follow up, Addis Ababa airport which is the country’s main international and domestic airport, situated at Bole on the southern outskirts of the city, was accorded priority for its immediate development to the requirements of ICAO standards. Consequently, the GOE commissioned the initial master plan studies for the major international airports of the country under the UNDP-ICAO technical assistance. 1.4 The detailed economic feasibility and engineering design of the project (both landside and airside packages) were completed in December 1993 with the assistance of ADF /TAF resources. In order to mobilise the resources for both packages (airside and landside) of the project, a donors meeting was organised in November 1995; the Bank agreed to finance some components of the airside package which included the construction of the new runway with five exit taxiways together with its ancillary structures. A Bank’s mission visited Ethiopia in May 1996 to appraise the airside components of the project. The loan was approved by the Board in October 1996 and was signed in December 1996 for an amount of UA 19.50 million. 1.5 This Project Completion Report (PCR) is based on the appraisal report, project files in the Bank, Borrower’s quarterly progress reports and PCR, interviews and site inspection conducted during an ADB mission to Ethiopia in January 2006. 2. PROJECT OBJECTIVE AND FORMULATION

2.1 Project Objective The objective of the project is to upgrade the existing airside infrastructure facilities, improve Navaid-Communication Systems as per ICAO standards to meet the present and forecast levels of traffic over the next twenty years at Addis Ababa airport. 2.2 Description 2.2.1 The project consists basically of six components:

(i) Civil works for (a) construction of a new runway of 3800m long with five exit taxi

ways; (b) airfield drainage and top soiling; and (c) security fencing and perimeter road; (ii) Supply, installation and commissioning of Airside equipment, Airfield lighting and

Navaid communication systems; (iii) Construction of new rigid apron of 70,000 sq.m; (iv) Construction works for strengthening of existing pavements (overlays); (v) Institutional Support to Project Management Unit ; and (vi) Consultancy services for supervision of components (i) to (iv) above, and audit of civil

works of (i) above.

2

2.2.2 At appraisal, the ADF financed components were at (i) above and the audit of civil works under the component (vi). However, during implementation, after realising some savings under the approved ADF loan, the Bank at the request of the GOE, agreed to finance the strengthening works for the existing pavement ( overlays) component at (iv) above, that was to be financed fully by the Government.

2.3 Formulation, Evaluation and Approval

2.3.1 The necessity for improvements and development of national airports which are vital for the country’s economy was identified by the GOE in 1988 as an objective of its transport policy. A master plan study covering five major airports (including Addis Ababa) was undertaken and completed in May 1990. Due to fast deterioration of the only runway at Addis Ababa International Airport, the Government requested the assistance of the Bank for an update of the master plan study including preparation of the detailed engineering studies. Consequently, the feasibility update and detailed engineering design reports were completed in December 1993, which recommended three packages, viz. (i) airside works, Works Package WP I ( new runway, taxiways, (ii) landside works WP II ( New terminal building and associated works), and (iii) Navaid -Communication systems, Works Package WP III.

2.3.2 In early 1993, GOE had formally requested the Bank to finance the airside package. A donor

meeting was organised in November 1995 to secure funds for all the three packages of the project. Funds were mobilized for all the three packages and ADF participated in the financing of some components of the airside package. An appraisal mission comprising a Transport Engineer, a Transport Economist and a Financial Analyst visited Ethiopia in May 1996 to appraise the project. The loan conditions were negotiated and there were no issues of disagreement raised by the Bank or the Borrower concerning the project. The ADF loan amount of UA 19.50 million was approved on 31 October 1996.

3. PROJECT EXECUTION

3.1 Effectiveness and Start-up The loan was approved on 31 October 1996, signed on 20 December 1996 and declared effective on 11 July 1997. The loan was signed 36 days after approval (maximum allowable 180 days) and declared effective 8 months after approval (maximum allowable 12 months). In accordance with Clauses 9.01 and 15.01 of the General Conditions Applicable to Loan Agreement and Guarantee Agreement of the ADF, there were no slippages either in the loan signature or for the loan effectiveness.

3.2 Modifications 3.2.1 In the course of the project implementation, some modifications were effected in respect of (i) scope of work, and (ii) pavement design specification, after approval by the ADF Board of Directors. The relevant modifications are summarized below:

(a) Scope of Works

• A review of the total expenditure after substantial completion on the Bank

financed airside package works WPI, indicated some savings under the loan. Accordingly, GOE requested the Bank to undertake financing the foreign exchange costs (out of the savings) for component D, i.e. Strengthening works of existing pavement, WP IA (Overlays). The Bank agreed to the proposal and a modification to the original categories of expenditure was approved on 12 April 2001 to include this component for additional works.

3

(b) Design Modifications

• During implementation, two modifications were carried out to the original design.

The first change in design was in respect of the black cotton soil (BCS) that was recommended as fill material to form an embankment upon which the runway is laid with preloading of BCS with a top surcharge of 1.0m above the finished pavement level for a period of 6 months. However, after detailed investigation by the expert engineers, it was felt that a revision was necessary to the original proposal that a non-swelling fill material be used instead to minimise the potential risk of damage to the pavement structure.

• The second change in the design was for the drainage under the pavement, i.e.

provision of vertical sand drains vs vertical trenching. After a field test, it was found that drainage by trenching method was found to be much faster and efficient when compared to the sand drains; as such vertical trenching method was finally adopted.

(c) Pavement Design specifications

• Due to change in soil conditions and filling material, some modifications were effected and the original thickness of the pavement was revised. The crushed stone base course thickness of 405 mm (provided in the original design) was modified with a thickness varying from 405 mm to 520 mm. Similarly, the bituminous base course thickness of 200 mm was modified in the revised design and it varied from 200 to 280 mm. However, the crushed stone sub-base thickness of 710 mm (as per original design) was adopted for most part of the length of the runway pavement, except at very few places it was reduced to 640 mm. The above changes in the pavement thickness had resulted in increase in quantities of some items.

In addition, the constant thickness of bituminous wearing course of 125 mm for the total width of the pavement was modified in the revised design. The thickness was gradually reduced from 125 mm at the crown to 90 mm at the edges, based on the distribution load intensity of the aircraft. This modification of varying thickness had resulted in some reduction in the quantity of bituminous wearing course material.

• Minor additions to drainage were carried out based on the site conditions, by providing saucer drains at both ends of the blast pads for improving drainage.

3.3 Implementation Schedule

3.3.1 The Project was executed by the Civil Aviation Authority (CAA) through the Project Coordinator of the established Project Implementation Unit (PIU) and with the support of the supervision consultant. 3.3.2 The ADF financed components (airside package works) of the project as envisaged at appraisal was to commence in November 1996 and completed in November 1998 (24 months). The process for procurement of contractor (pre-qualification, floating of tenders, evaluation etc) for construction works was through Advance Procurement Action (APA) approved by the Bank. Even though, procurement actions for the construction works were completed as early as in October 1996, the contract was awarded only on 8th March 1997 to the lowest evaluated bidder, i.e. M/s Kajima Keangnam, JV (Japan- S. Korea); works commenced on 14 March 1997 and completed in February 2002. 3.3.3 There was substantial delay in the completion of the works package WP I due to various factors, some of them are given hereunder. It was noted that during implementation, a total of 5 time extensions were given to the contractor:

4

Delay in sub-soil investigation related to foundation design and treatment; modifications to foundation drainage (trench method vis-à-vis vertical sand drains); working conditions’ constraints under an operational airport; adverse weather conditions coupled with unexpected heavy rains; increase in quantities due to change in pavement design; additional ducting works for electrical cables; and interruption of works at taxiway junction (during airport operations) with the existing

runway. In addition, with execution of additional works, WP I A of Strengthening of the existing pavement (Overlays), the overall completion was further delayed up to January 2004, making thus a total delay of 58 months.

3.3.4 The contract for the “Strengthening works of the existing pavement (WP 1A)”, was awarded to the lowest bidder M/s M. A. Kharafi & Sons on 1st April 2003. Works for this component were commenced on 4th April 2003 and completed in January 2004. It was noted that in both procurements, there were no disputes or complaints in the award of contracts to these firms. 3.3.5 Consultancy services (financed by GOE) for supervision of ADF financed airside package (WP I) works was awarded to M/s Dar –Al Handsah (Lebanon) in August 1996 with a completion period of 27 months. Consultancy services commenced on 15 August 1996 and were to be completed on 15th November 1998. However, due to delays in the execution of construction works for the reasons indicated in para 3.3.3 above, the services continued until February 2003 with seven extensions through seven addenda. Similarly, consultancy services for the supervision of the strengthening works (WP IA) was awarded to M/s Transport Construction Design Enterprise, TCDE (Ethiopia) on 1st November 2001 and continued until the completion of the strengthening works in January 2004. 3.3.6 In spite of delays during implementation, the final outputs of new runway and its ancillary structures were well executed. The new facilities provided at Addis Ababa Airport under the project, benefited the country in the improvement of air transport services both on international and domestic routes. Annex 2 shows the implementation schedule at Appraisal vs Actual.

3.4 Reporting 3.4.1 The implementation of the project was monitored through monthly progress reports prepared by the consultants and quarterly progress reports prepared by the Government in the Bank’s format. In addition, the project was monitored through regular Bank’s supervision and follow up missions.

3.4.2 Pursuant to the provisions of the General Conditions of the Loan Agreement, the GOE submitted quarterly progress reports, the Consultant's final construction report, annual audit reports and the Borrower's PCR. The contents of the progress reports in terms of keeping the Bank informed continuously of the project status, was noted to be satisfactory. However, it was noted that the project audit reports (financed by the Bank) do not meet the requirements given in the guidelines for audit of Bank financed projects.

3.5 Procurement

Consultancy Services for Airside Works Package WP 1 (financed by GOE) 3.5.1 The consultant for the supervision of construction works was selected through a shortlist of qualified firms in accordance with the GOE’s procurement rules. Request for Proposals (RFP) was issued to twelve international consultants. It was noted that the TOR stipulated a review of the detailed design carried out by the original design consultant (TAMS, USA), before issue of tenders. Even though, this component was financed by GOE, being a condition precedent to the first disbursement, GOE obtained the consent of the Bank in respect of appointment of the supervision consultant for the works. The supervision contract was awarded to M/s Dar – Al Handasah (Lebanon) in August 1996.

5

Consultancy Services for Strengthening Works ( Overlays) Package WP 1 A (financed by GOE)

3.5.2 The consultancy services for the supervision of strengthening works (Overlays), financed under GOE resources was selected in accordance with GOE’s procurement rules. Based on the experience in design and supervision of airport projects, GOE procured the consultant TCDE (a Government owned entity) through direct negotiations to supervise the works under this package. The Bank reviewed the selection process and gave its “no objection” for its procurement; the contract was awarded to M/s TCDE in November 2001. Civil Construction Works for Airside Package WP I ( financed by ADF) 3.5.3 The Executing Agency (CAA) followed the Bank’s Rules of Procedure for Procurement of Goods and Works. The Civil Works contractor was procured on the basis of International Competitive Bidding procedures (ICB) with pre-qualification of contractors. Twenty ne applicants were pre-qualified for the works. Tenders were issued on 28 March 1996 and twelve firms submitted the bids by the closing date. Bids were opened on 28 June 1996 and were evaluated in accordance with Bank’s Rules of Procedure for procurement of works. In order to accommodate the pavement design modifications as indicated in section 3.2.1 above, the selection of the contractor was delayed by about six months. After protracted negotiations with the lowest evaluated bidder, the contract for the construction of New runway and its ancillary structures was awarded to the lowest bidder M/s Kajima- Keangnam, JV (Japan- S.Korea) on 8 March 1997. Civil Works for Strengthening Works ( Overlays) Package WP I A ( financed by ADF) 3.5.4 The Executing Agency (CAA) followed the Bank’s rules of procedure applicable for medium contracts following ICB procedures, for procurement of contractor for the execution of these works component. Tenders were issued on 30 September 2001 to seven firms, but only five submitted the bids by the closing date. Tender bids were opened on 30 November 2001, evaluated in accordance with Bank’s Rules of Procedures and the second lowest bidder (M/s M.A. Al- Kharafi, Kuwait) was chosen, since the lowest bidder’s offer was unacceptable as the bidder had asked for a longer period for mobilization. The Bank reviewed the selection process and gave its “no objection” for the award of the contract to the second lowest bidder. A letter of acceptance was given on 22 December 2002 and the contract was awarded to M/s M.A. Al- Kharfi ( Kuwait) on 1st April 2003. 3.6 Financial Sources and Disbursements Project Costs 3.6.1 The estimated overall cost (net of all taxes) of the project, at appraisal, was UA 49.55 million (ETB 455.04 million) of which the foreign exchange cost was UA 35.75 million (ETB 328.58 million) or 72.15 % of the total and the local cost was UA 13.80 million (ETB 126.50 million) or 27.85 % of the total. The actual overall cost at completion was UA 36.83 million of which the foreign exchange cost was UA 26.28 million or 71.34 % of the total and the local cost was UA 10.56 million or 28.66 % of the total. The overall project cost at appraisal vs actual by component is presented in Annex 3 (page 1 of 5) while the summary by component and source is given in Annex 3 (page 2 of 5). 3.6.2 At appraisal, the ADF financed package of the project, WP 1 (excluding consultancy services for supervision, but inclusive of Project Audit services) was estimated to cost UA 26.10 million of which, the foreign exchange component was UA 19.50 million and the balance of UA 6.60 million was the local cost component. The total cost at appraisal including supervision (financed by GOE) and audit for works package WP 1 was UA 27.25 million, of which the FE was UA 20.50 and the remaining UA 6.75 was the local cost. The actual total cost of completion of the ADF financed package works WP 1 and WP 1A (excluding consultancy services for supervision, but including audit) was UA 24.242 million, of which the FE was UA 17.132 million and the remaining UA 7.110 was the local costs. The actual total cost of completion of the Works Package WP 1 and WP 1A (including consultancy services for supervision and audit) was UA 25.982 million, of which the FE was UA 18.219 million and the

6

remaining UA 7.763 was the local costs. Overall, there was a cost under-run of about UA 4.38 million under the ADF financed airside package works of the project. 3.6.3 The completion cost (UA 17.132 million) of the ADF components of the project (both packages (New Runway and ancillary works, WPI and Strengthening of Pavement works, WPIA), was found to be less than the approved loan amount of UA 19.50 million. The reduction in the completion cost vis-à-vis appraisal costs was due to keen competition and submission of cost effective competitive offers by the bidders. As a result of this, a saving of UA 2.368 million was realized under the ADF loan, and the Bank with the consent of the Government, had cancelled this balance. A summary of the project costs at appraisal, as modified and actual is shown in Table 3.1 below and details in Annex 3 (page 3 of 5).

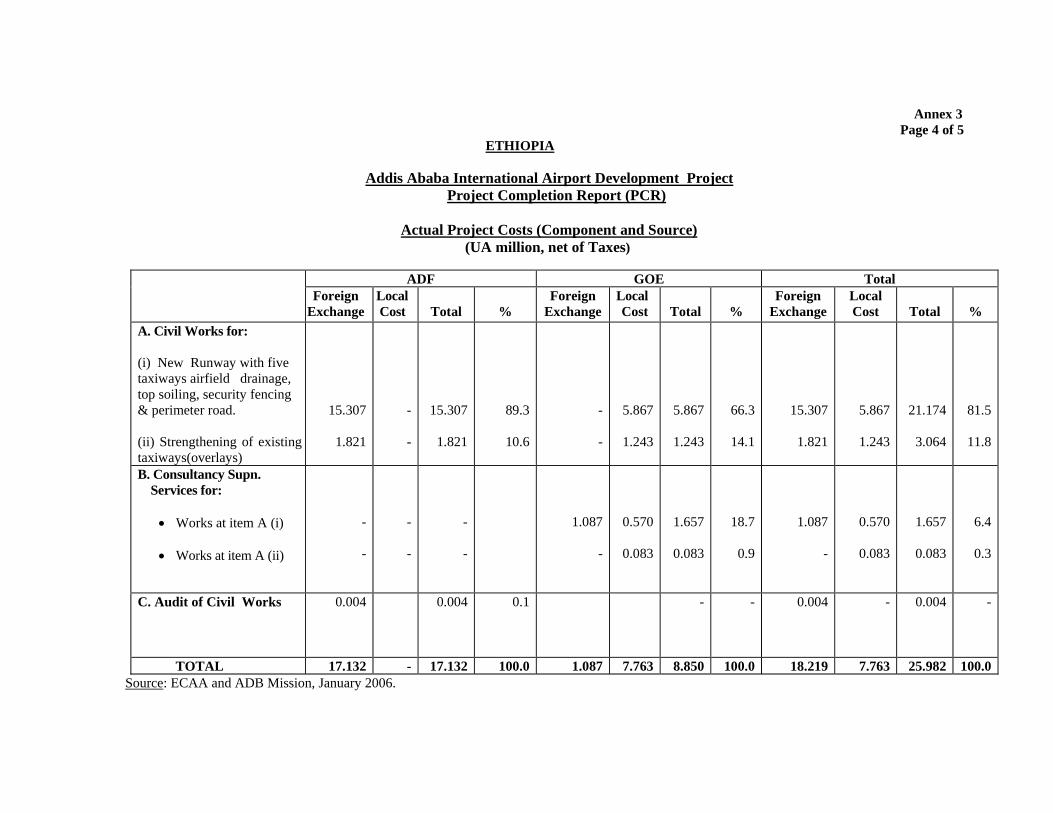

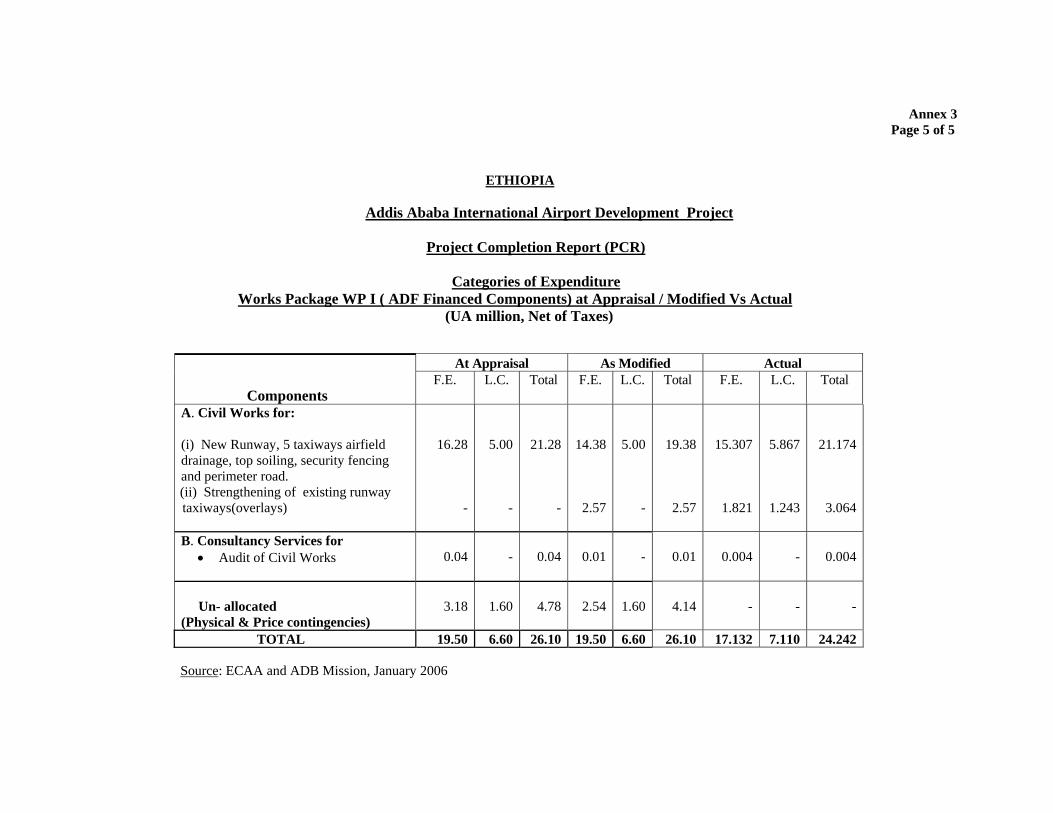

Table 3.1: Summary of Project Costs at Appraisal, Modified and Actual

(UA Million, net of taxes)

Appraisal Modified Actual Component F.E. L.C. Total F.E. L.C. Total F.E. L.C. Total

A. Civil Works for: (i) New Runway, 5 taxiways airfield drainage, top soiling, security fencing & perimeter road. (ii) Strengthening of existing runway and taxiways(overlays)

16.28

-

5.00

4.54

21.28

4.54

14.38

2.57

5.00

1.97

19.38

4.54

15.307

1.821

5.867

1.243

21.174

3.064 B. Consultancy Supn for:

• Works at item A (i) • Works at item A (ii)

1.00 -

0.07 0.22

1.07 0.22

1.00 -

0.07 0.22

1.07 0.22

1.087 -

0.570 0.083

1.657 0.083

C. Audit of Civil Works Un- allocated (Physical & Price contingencies)

0.04

3.18

-

2.60

0.04

5.78

0.01

2.54

-

2.60

0.01

5.14

0.004

-

-

-

0.004

-

TOTAL 20.50 12.43 32.93 20.50 9.86 30.36 18.219 7.763 25.982 Financial Resources

3.6.4 The project was co-financed by ADF, EIB, Kuwait Fund/BADEA/OPEC Fund, UNDP and GOE. The overall project cost at appraisal vs actual by component and source is summarised in Annex 3 (page 2 of 5). The financing plan for the ADF package at appraisal, as modified and actual expenditures (in UA terms) by source of finance using historical exchange rates in the computation of local costs is presented below in Table 3.2. As can be seen from the table, there was a change in the overall financing plan with ADF’s contribution (modified slightly as explained in paragraph 3.2.1(a) above), increased from 64.2% to 65.9%, while GOE’s contribution decreased from 35.8% to 34.1%. The final completion cost of the project indicated a cost under run of UA 4.38 million relative to the modified appraisal estimate.

Table 3.2: Financing Plan – Appraisal, Modified Vs Actual (UA million)

Appraisal Modified Actual Source of Finance

F.E. L.C. Total % F.E. L.C. Total % F.E. L.C. Total %

ADF 19.50 - 19.50 59.2 19.50 - 19.50 64.2 17.132 - 17.132 65.9 GOE 1.00 12.43 13.43 40.8 1.00 9.86 10.86 35.8 1.087 7.763 8.850 34.1 Total 20.50 12.43 32.93 100 20.50 9.86 30.36 100 18.219 7.763 25.982 100

7

7

Disbursements

3.6.5 The ADF loan funds were disbursed by direct method to contractors. However, the slippage in the implementation schedule had significantly affected the disbursement schedules. The disbursements, which were to start as per appraisal in November 1996, actually commenced from August 1997. The loan amount, as per the original appraisal schedule, was to be fully disbursed between 1996 and 1998, but due to delays in the start up of project construction, the first disbursement on ADF loan was effected in August 1997 and the last disbursement took place in January 2005. There were some disbursements delays during the construction activities due to (i) relocation of the Bank’s Headquarters to the TRA in Tunis, and (ii) wrong apportionment of currencies for ADF share of FE payments to the contractor. As a result of the delayed disbursements, GOE incurred interest costs in the sum of USD 28,230.13 and Yen 485,828. It was noted that the GOE made adequate budgetary allocations and payment of its own share of the project costs without delay. Annex 4 presents the disbursement profile at appraisal vs actual. The un-disbursed balance of UA 2.368 million on the ADF loan was cancelled in March 2005. 4. PROJECT PERFORMANCE AND RESULTS

4.1 Overall Assessment 4.1.1 The project was well executed. The Borrower in consultation with the Bank had provided appropriate responses and solutions to the problems which arose during the course of implementation. Coordination and efforts of all parties (Bank, Borrower, Contractors and Consultants) involved was effective which resulted in successful completion of the project. 4.1.2 The loan covenants /conditions were appropriate and valuable to the execution of the project. The success of the project itself is evidence that the loan conditions were sufficient and no more additional conditions were necessary. Since the new facilities included under the project were of utmost importance to the country’s economy, GOE took no time to fulfil the stipulated conditions. However, due to various factors indicated earlier coupled with additional works, have contributed significantly to delays in the completion of the project.

4.2 Operating Results Civil Works 4.2.1 The ADF financed components of the project were inspected after 2 years of its completion. During field inspection, it was noted that the completed new runway and its ancillary structures were well executed. The workmanship and overall quality of work executed by the contractor was good. 4.2.2 The completed New Runway is in good condition having a smooth riding surface with no distress or deformations. Proper vertical and horizontal alignments complying with the required design were provided with good drainage systems. The culverts and other drainage structures constructed along the runway are structurally sound with no signs of distress. At few locations along the runway, the aircraft guide path markings along the centreline were faded. Similarly, some deformations/ swellings were noted at some locations of the perimeter road.

4.2.3 The Mission advised GOE to take appropriate remedial measures in order to protect the

investment.

Traffic 4.2.4 Ethiopian Air Lines (EAL) dominates both domestic and international air transport services in Ethiopia. The international passengers carried between 1996 to 2004 shows an annual average market share of 82 % as against 65 % at appraisal. This is mainly due to the increase in the fleet of EAL, from 35 (15 were small planes) at appraisal to 47 (21 are small planes) at PCR. In addition, EAL is planning to have ten B -787 in the coming years. At present EAL renders services to 41 international and 24 domestic destinations with ten foreign carriers providing international services at Addis Ababa Airport.

8

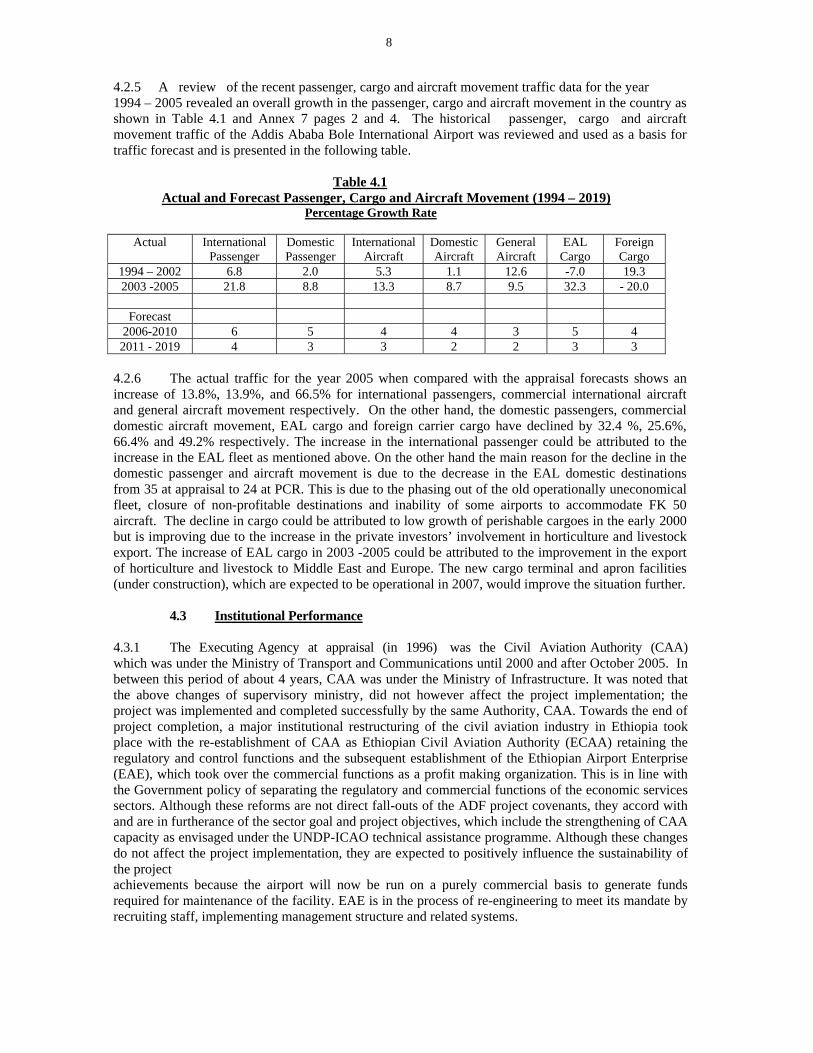

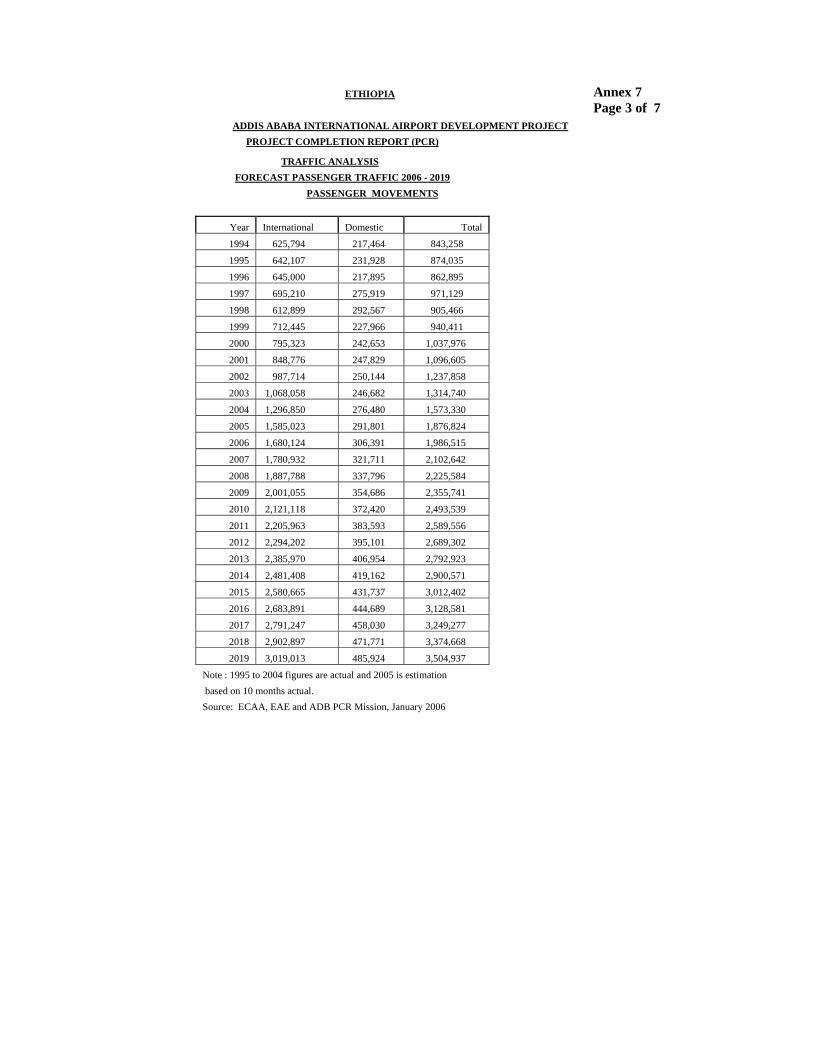

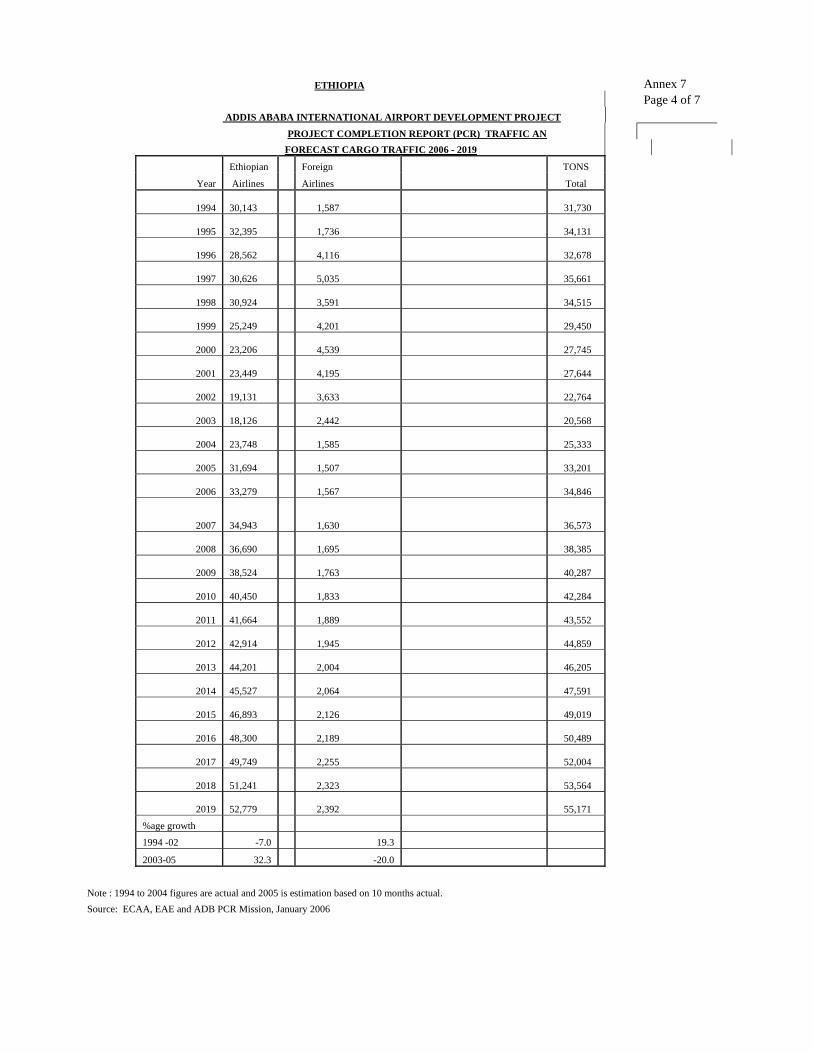

4.2.5 A review of the recent passenger, cargo and aircraft movement traffic data for the year 1994 – 2005 revealed an overall growth in the passenger, cargo and aircraft movement in the country as shown in Table 4.1 and Annex 7 pages 2 and 4. The historical passenger, cargo and aircraft movement traffic of the Addis Ababa Bole International Airport was reviewed and used as a basis for traffic forecast and is presented in the following table.

Table 4.1 Actual and Forecast Passenger, Cargo and Aircraft Movement (1994 – 2019) Percentage Growth Rate

Actual International Passenger

Domestic Passenger

International Aircraft

Domestic Aircraft

General Aircraft

EAL Cargo

Foreign Cargo

1994 – 2002 6.8 2.0 5.3 1.1 12.6 -7.0 19.3 2003 -2005 21.8 8.8 13.3 8.7 9.5 32.3 - 20.0

Forecast

2006-2010 6 5 4 4 3 5 4 2011 - 2019 4 3 3 2 2 3 3

4.2.6 The actual traffic for the year 2005 when compared with the appraisal forecasts shows an increase of 13.8%, 13.9%, and 66.5% for international passengers, commercial international aircraft and general aircraft movement respectively. On the other hand, the domestic passengers, commercial domestic aircraft movement, EAL cargo and foreign carrier cargo have declined by 32.4 %, 25.6%, 66.4% and 49.2% respectively. The increase in the international passenger could be attributed to the increase in the EAL fleet as mentioned above. On the other hand the main reason for the decline in the domestic passenger and aircraft movement is due to the decrease in the EAL domestic destinations from 35 at appraisal to 24 at PCR. This is due to the phasing out of the old operationally uneconomical fleet, closure of non-profitable destinations and inability of some airports to accommodate FK 50 aircraft. The decline in cargo could be attributed to low growth of perishable cargoes in the early 2000 but is improving due to the increase in the private investors’ involvement in horticulture and livestock export. The increase of EAL cargo in 2003 -2005 could be attributed to the improvement in the export of horticulture and livestock to Middle East and Europe. The new cargo terminal and apron facilities (under construction), which are expected to be operational in 2007, would improve the situation further. 4.3 Institutional Performance 4.3.1 The Executing Agency at appraisal (in 1996) was the Civil Aviation Authority (CAA) which was under the Ministry of Transport and Communications until 2000 and after October 2005. In between this period of about 4 years, CAA was under the Ministry of Infrastructure. It was noted that the above changes of supervisory ministry, did not however affect the project implementation; the project was implemented and completed successfully by the same Authority, CAA. Towards the end of project completion, a major institutional restructuring of the civil aviation industry in Ethiopia took place with the re-establishment of CAA as Ethiopian Civil Aviation Authority (ECAA) retaining the regulatory and control functions and the subsequent establishment of the Ethiopian Airport Enterprise (EAE), which took over the commercial functions as a profit making organization. This is in line with the Government policy of separating the regulatory and commercial functions of the economic services sectors. Although these reforms are not direct fall-outs of the ADF project covenants, they accord with and are in furtherance of the sector goal and project objectives, which include the strengthening of CAA capacity as envisaged under the UNDP-ICAO technical assistance programme. Although these changes do not affect the project implementation, they are expected to positively influence the sustainability of the project achievements because the airport will now be run on a purely commercial basis to generate funds required for maintenance of the facility. EAE is in the process of re-engineering to meet its mandate by recruiting staff, implementing management structure and related systems.

9

4.3.2 The technical performance of Executing Agency was noted to be satisfactory as supported by the quality of works completed. The Project coordinator had performed his functions to the satisfaction of the Bank and the Executing Agency (CAA). Effective contact was established between the Bank, Executing Agency, Consultants as well as the Contractors. Accounting and Budgeting 4.3.3 The accounting system of ECAA still remain weak as observed at appraisal. The periodic accounting and management information reports needed for management to make important decisions were not prepared on a timely basis. Even when eventually produced, the figures often appear unreliable. This situation was clearly manifested on the draft annual accounts for the accounting periods 1999/2000 to 2003/2004 whereby the turnover shown thereon in no way reflects the actual performance of the authority. As for EAE, the accounting system also needs to be strengthened especially as this is a profit making organization. The enterprise presented two versions of accounts for the same period (year ended 7th July 2005) thus casting doubts on the reliability of some of the figures. Both ECAA and EAE as of the PCR were not maintaining fixed assets registers despite being required to do so at appraisal. The importance of the register cannot be overemphasized as these are required to safeguard the assets of the organization because it does not take long to lose sight of some assets unless records are kept. 4.3.4 The budgeting processes for ECAA being undertaken by the Air Transport and Planning Department appear adequate to meet the need of the organization. Notwithstanding, it is still necessary to harmonize the financial forecasts with the outputs of the Finance Department especially the historical and budgeted figures or projections. The EAE has also not been able to harmonise its financial budgeting with operations. In actual fact, the enterprise could only prepare budget for one year and had not projected for say five or ten years as would be expected for such an organization. There is thus the need to establish a budgeting and budgetary control system to provide appropriate tools for planning and control, and to train the appropriate personnel in the planning, finance and other departments in the application of those tools.

Auditing and Insurance 4.3.5 The audits of ECAA accounts were in arrears for six years, the latest audited accounts being for the year ended 7th July 1999. This contravenes the ECAA re-establishment proclamation, which requires the authority to maintain full and accurate accounts of its revenue and expenditures, and to submit duly audited accounts to the supervising ministry within a period of six months after the expiry of each fiscal year. It should be emphasized that ECAA must ensure proper accounting and audits for statutory compliance, transparency and accountability. 4.3.6 The accounts of EAE as well have not been audited since establishment of the enterprise. The draft accounts up to 7th July 2005 were however ready and the selection process for an audit firm just completed. EAE should also ensure strict compliance with the auditing requirements. 4.3.7 The assets of EAE namely the runway, terminal and vehicles were insured. The runway insurance in particular addresses the Bank’s concern at appraisal that ADF financed assets should be insured.

Billings and Collection

4.3.8 The concern expressed during appraisal regarding the need for effective billing and collection policy and procedures were yet to be addressed. The Finance Department of EAE responsible for billing and collection appears to operate a weak accounting and management information system coupled with poor credit control policy leading to accumulation of collectibles, which stood at ETB 508 million as at 7th July 2004 as against a total revenue of ETB 136 million for the year ended on that date. Unless drastic actions are taken, this could jeopardise the very existence of EAE.

10

Tariff Policy and Structure 4.3.9 The tariff policy and structure for the airside services remain substantial unchanged since project appraisal. One of the conditions precedent to entry into force of the ADF loan was the undertaking by the Borrower that airside tariffs will be adjusted in line with market trends not later than 30th June 1999 and will be continually adjusted thereafter to reflect the cost of providing services. GOE fulfilled this condition by submitting the appropriate letter of undertaking. However, the time for fulfilment of the undertaking had lapsed and GOE was yet to adjust the tariff as required. It was understood that EAE had, based upon a tariff study, submitted proposals tariff revision for GOE approval. Although the project had been completed since the year 2003, GOE was yet to give approval for tariff adjustment as proposed by EAE.

4.4 Management and Organisational Effectiveness 4.4.1 A slight modification was made to the established PIU by the way of introduction of the post of a Deputy Project Coordinator. This was necessitated by the volume of work involved on the various components of the project. Apart from the Project Coordinator and his Deputy, there were 15 other members of staff comprising 3 Civil Engineers, 2 Electrical Engineers, 1 Finance Officer, 2 Accountants, 2 Secretaries, 1 Clerical Officer and 4 support staff. Following the aviation industry reform, the PIU was eventually attached to EAE where the project would be closed and the staff re-assigned. The enterprise now has in place, a separate management structure for the management of the Addis Ababa International Airport as recommended in the appraisal report but with slight modifications. These reforms in the aviation industry have positive implications for the project sustainability. 4.4.2 At present, both ECAA and EAE are under the MOTAC. ECAA has seven departments, namely Air Transport & Planning, Human Resources & Property, Finance, Training, Aerodrome Engineering, Air Navigation and Flight Safety. EAE is functioning with seven departments, namely, manpower administration, finance, purchasing & property administration, airport engineering, corporate marketing, Addis Ababa International and Regional Airports. EAE is in the process of re-engineering to meet its mandate by recruiting staff, implementing management structure and related systems. Being a performance oriented semi-autonomous commercial organization; the enterprise will be managed by qualified staffs that have the required skilled personnel to implement its mandate.

4.5 Staff Recruitment, training and Development 4.5.1 Both the ECAA and EAE have established posts required to be filled in accordance with their respective organization structure. Apart from the key personnel inherited from the defunct CAA, EAE has been recruiting from the open market in order to fill established vacancies created as a result of its management structure. It is rather too early to start assessing the staff turnover as a measure of EAE’s ability to attract and retain personnel since the organization is still young and now in its third year of operation. As at 6th July 2005, there were 1,605 established positions (Head office 272, Addis Ababa Airport 503, and Regional offices 830) of which 741 had been filled. A manpower requirements plan is in place to fill the remaining vacancies over the next 5 years. At the moment the Enterprise is contracting out and out outsourcing some of the activities to private sector organizations in order to efficiently utilize the airport facilities. It is expected that EAE will base the exercise on a well-articulated and rational human capital strategy in which case the long-term viability would be assured. 4.5.2 ECAA’s in-house training program covers in Air Traffic Services, Aeronautical Radio Maintenance, Navigational Aid Maintenance, Aeronautical Information Service, Basic Fire Fighting, Computer Operation, Basic Aviation Security, Aviation Supervisory Management and Team Building Workshops. In addition, it also arranges foreign training and workshops in regulatory and air traffic services. EAE does not have training program for its employees but maintains a budget allocation for local and foreign studies. Although some of the training programmes are donor sponsored, it is advisable that these be monetized and reflected in the budgets. Furthermore, the budgetary allocations for those to be financed from ECAA and EAE own resources appear inadequate considering the enormous need to update the manpower skill in virtually all technical and non-technical areas.

11

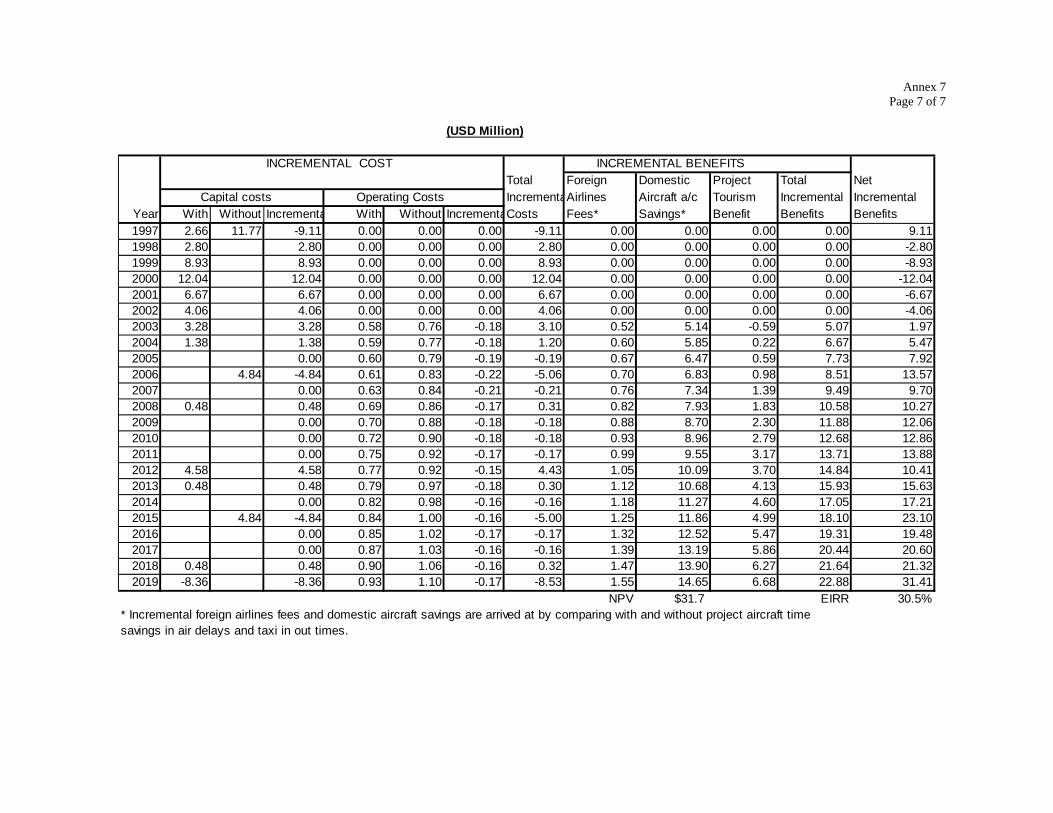

4.6 Performance of Consultants, Contractors and Borrower Consultants (M/s Dar –Al Handasah of Lebanon & Transport Construction Design Enterprise, TCDE) of Ethiopia ) 4.6.1 The overall performance of the consultants, M/s Dar –Al Handasah (Lebanon) & TCDE (Ethiopia) were noted to be satisfactory and to the satisfaction of the Government and the Bank. The preliminary design review carried out on the original design (undertaken by a different consultant TAMS of USA), in particular on the black cotton soil as fill material and the pavement drainage aspects, have eliminated the potential risk of damage to the pavement structure. The consultant’s (M/s Dar Al- Handasah) efforts, especially the pre-tender design review of the contract services and modifications proposed to the pavement structure, were really to be commended. The improvements suggested to the original design that were carried out in the field was mainly to produce a project with high quality standards. The Resident Engineer conducted regular pavement field tests as stipulated in the contract documents to conform to the specified requirements before incorporation in the works. Constant supervision of project works was undertaken under operational conditions by the Project Coordinator of the PIU and the supervision consultants at every stage to maintain the quality of works. Adding to this, the Consultants were regular in submitting progress reports to the EA for review and onward transmission to the Bank. Good coordination existed through out the execution between the Consultants and the Contractors. There were no complaints or disputes during execution of the works. 4.6.2 The Executing Agency had maintained close working relationship with the selected supervising consultants during the course of the project implementation. Contractors ( M/s Kajima- Keangnam of Japan- S. Korea & M/s M.A. Al- Kharafi) 4.6.3 The contractors selected for the project components have been active in Africa with several years of experience and executed many similar projects in other countries. The technical performances of the contractors in the execution of works especially the quality and workmanship were satisfactory. The Borrower 4.6.4 The Loan Agreement was signed by the Borrower on 20 December 1996 and declared effective on 11 July 1997. The loan was signed 36 days after approval (maximum allowable 180 days) and declared effective 8 months after approval (maximum allowable 12 months). As such, there was no slippage either on the signature or on the effectiveness. The performance of the Borrower with regard to fulfilment of the loan conditions for the loan effectiveness was satisfactory. 4.6.5 The Borrower had submitted regularly the quarterly progress reports and annual audit reports to the Bank as stated in paragraph 3.4.2. In conclusion, the performance of the Borrower can be rated as satisfactory. 4.7 Conditions/Covenants The GOE took about 6 months to fulfil the stipulated conditions precedent to the entry into force of the Loan Agreement, from the date of loan signature to the loan effectiveness date of 7th July 1997. Regarding the condition on the undertaking for “adjustment of air tariffs not later than 30 June 1999 in line with market trends and thereafter to reflect the cost of services”, GOE was yet to fulfil the undertaking. As stated in paragraph 4.3.9 above, two years after project completion, the tariff approval was yet to be given in order to fully accomplish the loan condition. 4.8 Economic Performance 4.8.1 At appraisal, the implementation of the airside works of the Addis Ababa Airport Project economic justification was evaluated based on an assessment of net incremental benefits by comparing

12

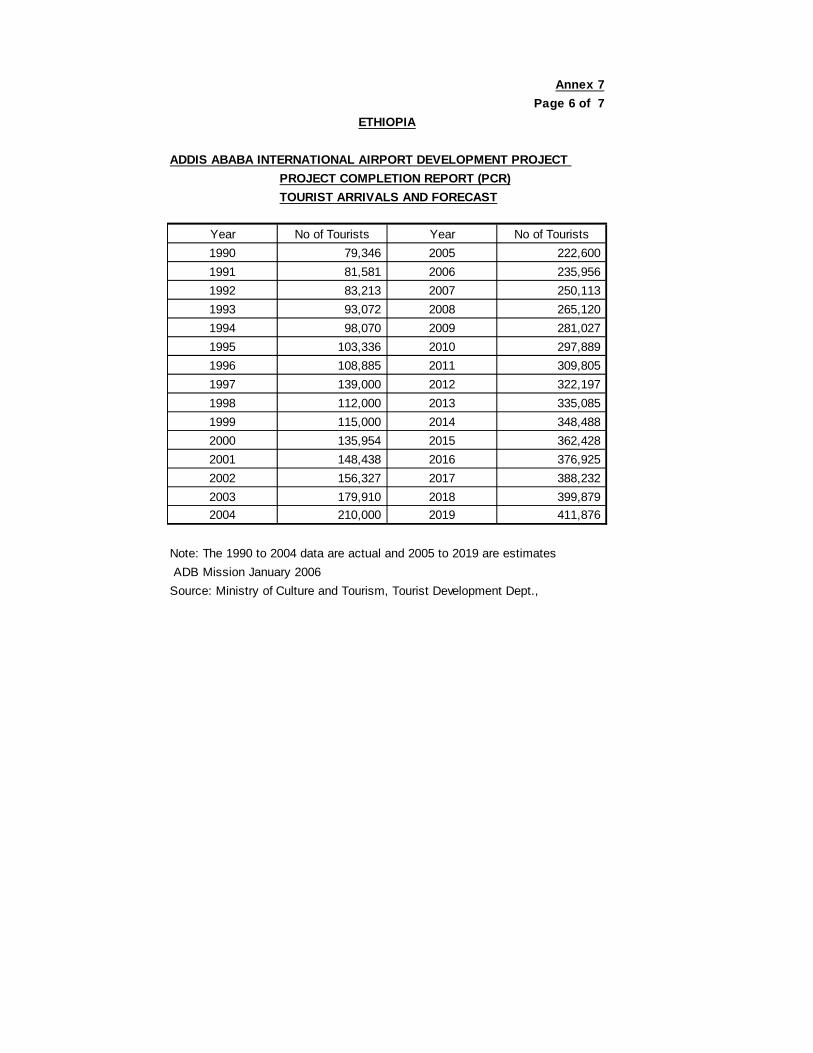

“With” and “Without” the project scenarios. The analysis was conducted using January 1996 prices, assuming construction would commence in November 1996 and would last for 32 months period, being complete in May 1999. A seventeen years analysis period (1999-2015) and 20% residual value by the end of 2015 have been assumed. The economic costs included construction, supervision and maintenance costs while the benefits were based on three types namely, incremental foreign carrier user fees; domestic aircraft operation cost savings; and incremental foreign exchange earnings from tourism. Net economic benefits were calculated from 2015 and discounted to the base year 1996. Based on the economic costs and benefits, the resulting economic internal rate of return of the Addis Ababa Airport Project was estimated at 23.3%. 4.8.2 The estimates of project benefits at PCR were based on incremental foreign carrier user fees; domestic aircraft operation cost savings; and incremental foreign exchange earnings from tourism with projected traffic growth as presented under Table 4.1 above. Summary of Economic Analysis at PCR is attached as Annex 7 page 1 of 7. The analysis was conducted in economic terms, which was derived from the financial costs using the relevant conversion factors applicable to Ethiopia. The actual construction, supervision, maintenance economic costs and a 20% residual value as well as the benefits emanating from the revised traffic forecasts, formed the basis in the re-calculation of EIRR. The re-calculated EIRR is 30.5 % and Net Present Value (NPV) of US$31.7 million at 11% discount rate (Annex 7 page 7 of 7). This EIRR of 30.5 % (when compared with 23.3% at appraisal) is high mainly due to the traffic growth in the international passenger, international aircraft and general aircraft movement (as presented in para 4.2.6), 23.9 % reduction in the airside construction cost and capital cost disbursement over eight years period when compared to four years anticipated at appraisal. The EIRR at 30.5 % is well above the opportunity cost of capital of 11% in Ethiopia. 4.8.3 Other indirect economic benefits derived from the implementation of the Addis Ababa Airport Project are expanded foreign trade and other private business activity; air traffic safety and security, multiplier effect of tourism development through out the economy, accelerated human resource development and job creation in air transport. The number of tourist arrival is expected to grow by 74.5% between 2006 and 2019 and revenue attributed to the project to increase from USD 0.22 million to USD 6.68 million during the same period. Besides, the project has also benefited the ECAA/ EAE in the foreign exchange revenue generation. Given the Country’s land -locked context, plans are underway to develop it as a regional airport for hub traffic, to other destinations in Africa to promote regional integration. 4.9 Financial Performance 4.9.1 The project was evaluated at appraisal on a “net incremental cash flow” basis whereby airside revenue and expenditures expected to accrue were compared in with and without project scenarios. The appraisal analyses gave a financial internal rate of return (FIRR) of 23% for the airside investment, well above the prevailing opportunity cost of capital then 11% thus asserting the financial viability of the project. A comparison of the actual revenue and expenditure over a period of 10 years, covering the entire period of project implementation and thereafter, indicates that airside revenue estimates were in excess of actual revenue by an average of 12% per annum over the period. The projected expenses were above the actual performance, yielding average savings of about 56% per annum over the same period. Consequently, the actual financial results (margins) surpassed appraisal forecasts on the average by as much as 100% per annum. The comparison of the actual with estimated revenue and expenditure is presented in Annex 5. 4.9.2 A retrospective financial analysis based upon the resulting stream of cash flows also adopting with and without scenarios is presented in Annex 6. The retrospective financial internal rate of return is estimated to be 30%, which is well above the appraisal estimate of 23% and the current opportunity cost of capital of 11% in Ethiopia. This performance is accounted for by the increased cash flows resulting from better margins than envisaged at appraisal, savings on project cost and longer spread of disbursements. It must however be pointed out that these results should not be the sole yardstick for measuring the project achievement or even the good health of the responsible institution. As mentioned in paragraph 4.3.8 above, EAE continues to carry a huge pile of collectibles, which could wipe of the gains, if appropriate steps are not taken on debt recovery.

13