Embed Size (px)

Citation preview

This article was downloaded by: [Moskow State Univ Bibliote]On: 14 November 2013, At: 00:19Publisher: RoutledgeInforma Ltd Registered in England and Wales Registered Number: 1072954 Registeredoffice: Mortimer House, 37-41 Mortimer Street, London W1T 3JH, UK

Accounting Education: AnInternational JournalPublication details, including instructions for authors andsubscription information:http://www.tandfonline.com/loi/raed20

Ethics and accounting education inthe UK — a professional approach?A.I.M. Fleming aa University of PaisleyPublished online: 28 Jul 2006.

To cite this article: A.I.M. Fleming (1996) Ethics and accounting education in the UK — aprofessional approach?, Accounting Education: An International Journal, 5:3, 207-217, DOI:10.1080/09639289600000021

To link to this article: http://dx.doi.org/10.1080/09639289600000021

PLEASE SCROLL DOWN FOR ARTICLE

Taylor & Francis makes every effort to ensure the accuracy of all the information (the“Content”) contained in the publications on our platform. However, Taylor & Francis,our agents, and our licensors make no representations or warranties whatsoeveras to the accuracy, completeness, or suitability for any purpose of the Content. Anyopinions and views expressed in this publication are the opinions and views of theauthors, and are not the views of or endorsed by Taylor & Francis. The accuracy ofthe Content should not be relied upon and should be independently verified withprimary sources of information. Taylor and Francis shall not be liable for any losses,actions, claims, proceedings, demands, costs, expenses, damages, and other liabilitieswhatsoever or howsoever caused arising directly or indirectly in connection with, inrelation to or arising out of the use of the Content.

This article may be used for research, teaching, and private study purposes. Anysubstantial or systematic reproduction, redistribution, reselling, loan, sub-licensing,systematic supply, or distribution in any form to anyone is expressly forbidden. Terms& Conditions of access and use can be found at http://www.tandfonline.com/page/terms-and-conditions

Accounting Education 5 (3), 207-217 (1996)

Ethics and accounting education in the UK - a professional approach?

A.I .M. F L E M I N G

University of Paisley

l Revised February 1995; June 1995 1 and accepted August 1995

Abstract

Although the expectation of accountants is that they will always employ high ethical standards, empirical evidence suggests that individual accountants are, at best, no more ethically aware than average. This gap between expectation and reality could be the result of inadequate education. Universities cannot be relied upon to teach accounting ethics to prospective professional accountants principally because too few accountants have an accounting degree and because of the surface nature of accounting students' learning. The professional bodies pay only lip-service to ethics education in their syllabi and their treatment of ethics is thus both quantitatively and qualitatively inadequate. Accountants are consequently ill-prepared to face ethical dilemmas.

Keywords: accounting, ethical education, universities, profession

Introduction

There is an expectation placed on practising accountants that they will always employ high ethical standards in professional practice and conduct. This expectation is at its most obvious when expressed by the professional accounting bodies in their various 'guides to professional ethics', Bye-laws, and Regulations. CIMA, for example, in its Bye-laws talks of members being guilty of 'dishonourable or unprofessional conduct' and, in its Ethical Guidelines, requires its members to 'refrain from any conduct which might bring discredit to the profession'. In similar sentiment, ACCA requires its members to 'observe proper standards of professional conduct' and to 'refrain from ... misconduct which includes any act or default likely to bring discredit to themselves, the Association, or the accountancy profession'.

In addition to the expectations of the professional bodies, there also appears to be a more widespread belief that professional accountants should always act not only with professional competence but also with high standards of integrity (see, for example, Cohen and Plant, 1992; or Huss and Patterson, 1993). The available evidence, however, is not conclusive as to whether accountants are in fact more or less ethical than other business professionals despite the high and exacting standards apparently placed on them by the profession.

The tendency of the evidence is to suggest, if anything, that accountants either occupy the middle ground or lean towards an amoral ethical position. Burke et al. (1993) were

Address for correspondence: A.I.M. Fleming, Department of Economics and Management, University of Paisley, High Street, Paisley PA1 2BE, Scotland

0963-9284 0 1996 Chapman & Hall

Dow

nloa

ded

by [

Mos

kow

Sta

te U

niv

Bib

liote

] at

00:

19 1

4 N

ovem

ber

2013

208 Flem ing

able to report the rather conflicting situation that although accountants generally occupied the moral middle ground nonetheless the closer an individual manager was to the finance function the less concerned he/she became with ethical matters. Armstrong (1987) reported that accountants' moral maturity, when compensated for age and levels of education, is less than that for the population as a whole and Ponemon (1990) was able to conclude that the promotion of an accountant could be associated with a decline in ethical reasoning.

There does appear to be a strong contradiction between the ethical rules of the profes- sional bodies and the ethical behaviour observed by researchers. This new 'expectations gap' ought to be of concern to the profession for, without the element of ethical behaviour, the profession will be little more than a loose association of individuals with broadly similar skills and abilities.

Purpose of paper

The purpose of this study is therefore to examine when prospective professional accoun- tants are exposed to ethical considerations in accounting and to assess the relative importance placed by the accounting profession on the ethical development of its students. Secondarily, this paper will also discuss those factors which currently exist and appear to prevent the professional bodies from successfully integrating an effective ethics education into their assessment schemes for prospective members.

Teaching ethics: goals and methods

A knowledge of ethical rules cannot, on its own, be said to evidence an individual's ethical development and maturity any more than a knowledge of any law can be said to show that the individual is a law-abider. Ethical maturity is seen in individuals who, starting with a background knowledge of the rules or codes, will progress to use the spirit of the ethic as a basis for forming ethical judgements. The most widely noted analysis of this evolutionary process towards ethical maturity is seen in Kohlberg's levels of ethical development (see, for example, Kohlberg, 1969 and 1973).

The objective of teaching ethics to accountants must therefore go beyond the mere passing on of the profession's ethical codes and guidelines (a process which would be relatively easy to teach, learn, and assess) to a stage which Loeb (1988) describes as setting the scene for 'a change in ethical behavior'. This does not mean that students should be taught 'right' and 'wrong'. Indeed, there are powerful arguments which suggest that this cannot be done, ethical relativism being just one. Rather, students ought to be placed in a position which allows them to acquire those attributes which then enable the individual to identify and analyse ethical dilemmas. In this way, ethical maturity develops (Trevino, 1992).

Weber (1990) was able to show that the experience of the undergraduate is an important function in the ethical development of the student and that those students who are exposed to the teaching of ethics demonstrate some improvement in their ethical awareness and ability to analyse ethical problems. Hiltebeitel and Jones (1992) are also able to demon- strate that relatively short courses in accounting ethics produced a positive result in enhancing students' ethical sensitivity and reasoning ability. Although the evidence which suggests that there is a close and long-lasting correlation between the teaching of ethics and positive changes in individuals' behaviour is not substantial, there appears to be

Dow

nloa

ded

by [

Mos

kow

Sta

te U

niv

Bib

liote

] at

00:

19 1

4 N

ovem

ber

2013

Ethics and accounting education in the UK - a professional approach? 209

sufficient to suggest that such a correlation does exist. In particular, the teaching of ethics seems to move students up to the higher levels of Kohlberg's classification. Thereafter, some negative and external influence in later life would be required to move the individual ethical sensitivity downward towards the more elementary ethical positions.

Gray et al. (1993) point out that the development of ethical reasoning and responses requires students to adopt a deep approach to learning whereas Burton et al. (1991) concluded that the use of case studies and discussion had a significantly greater effect on students' ethical attitudes and perceptions than any other method of instruction examined. It would therefore appear that the teaching of ethics ought to involve learning processes which are significantly different to passive self-learning or even lecture-based programmes.

The educators' role: the universities

A substantial body of evidence has accumulated which suggests that accounting education in universities is surface rather than deep (see, for example, Gibb, 1993, and French et al., 1992) where the student accepts ideas passed on to himlher, facts are learnt and procedures memorized, instead of the emphasis being on understanding, interpretation, and critical analysis. (For a fuller discussion of 'deep and surface' teaching and learning styles see, for example, Entwhistle et al., 1992, and the Committee of Scottish University Principals Report, 1992). In this view, many accounting educators tend to accept the subject as technical and value-free and that the emphasis therefore should justifiably be on those techniques. It is this approach to accounting education which limits the development of a deep approach to the subject and, just as importantly, to other disciplines (see Power, 1991). Indeed, it may be the surface approach taken in teaching accounting itself which leads to the ossification or decline of moral development in accountants found by Ponemon and others since accounting graduates will not have acquired the deep learning skills needed for complex ethical reasoning.

In addition to stultifying the accounting student's enquiring and critical functions generally, there is also evidence that where universities do cover ethics for accountants they do so in a peremptory manner (Hiltebeitel and Jones, 1992, and Loeb, 1988). Lehman (1988) suggests that it is highly unlikely that such an ill-considered and inadequate approach to teaching ethics will have any long-lasting beneficial effect on students, this perhaps being particularly so when associated with the generally surface approach to learning adopted by most accounting students (although this can be contrasted with Hiltebeitel and Jones' conclusions). It may be that universities are the 'right' place to teach ethics to accounting students, but it does appear that either they are doing the job badly (as discussed above) or may, in fact, not be the most appropriate vehicle to inculcate ethical reasoning in future members of the profession.

The principal reason why universities should not be relied upon as being best placed to educate future members of the profession in ethics is one of numbers. All accountancy bodies permit non-accountancy graduates to undertake professional training, yet it is only in the Institute of Chartered Accountants of Scotland where the majority of the annual in- take are accountancy graduates (about 80%). In the Institute of Chartered Accountants in England and Wales, the proportion of accountancy graduates in the annual in-take has remained stable at 19 or 20% for the last seven years up to 1994. If the professional bodies believe that it is in universities that their members ought to receive an education on ethics,

1 then only a small proportion of all qualified accountants will be 'ethically aware'. That

Dow

nloa

ded

by [

Mos

kow

Sta

te U

niv

Bib

liote

] at

00:

19 1

4 N

ovem

ber

2013

Fleming

proportion will be determined by the number of accounting students accepted by the professional bodies as a percentage of total students including all non-accounting grad- uates. In addition, the number of accounting graduates with some background in account- ing ethics will depend on the number of universities which includes ethics in their curricula and, as Wild and Ahmed (1994) point out, that too is in the minority. However, just because the universities produce a minority of entrants into the accounting profession, this should not be used to allow accounting departments to ignore the issue of ethical development. The ability to make sound ethical judgements and to be able to evaluate l

accounting's ethical dilemmas remains central to fully understanding accounting and its framework (Schweikart, 1992).

An additional question, and one which must be considered by the professional bodies as well as the universities, is whether or not accountants are best placed to teach accounting ethics to prospective students. There appears to be a lack of published research in this field although anecdotal evidence suggests that when ethics are taught to accounting students by non-accountants the topic becomes viewed as irrelevant to practical accounting. It may be that accountants should teach accounting ethics if only so that the topic can be perceived as being important to the profession.

If universities are not to be the means by which all, or even a significant percentage of, qualified accountants receive an ethics education then all that remains is that the profes- sional bodies do it themselves. There are, however, significant difficulties in the profes- sional bodies trying to teach ethics and ethical development.

The educators' role: the professional bodies

The professional accounting bodies in the UK are all quite clear on what they mean by 'ethics' in that each body produces its own guidelines on ethical matters. Such ethics are profession-based and may be seen as having evolved to serve the best interests of the profession rather than the individual members or, at times, even the client. Thus, for example, we see CIPFA's Guideline on Ethics saying that, on appointment, a new accountant should inform any existing accountant of the appointment and that should the client insist that the existing accountant not be informed then such 'disinclination by the client for communication with the existing accountant would not be a satisfactory reason (for not communicating with the existing client)'. Here, for the benefit of the profession as a whole, the accountant must not serve the express wishes of the client. Similarly, it may well be in the individual member's interest to accept a high fee earning client but it has to be refused if it exceeds 15% of gross practice income as independence may then be compromised - a case here of ethical rules protecting the public perception of the profession as opposed to benefiting the individual member.

The ethical guidelines of the professional bodies are, however, unclear about the primary responsibility of members. Given differing circumstances, it appears that the primary duty of the member is moveable; changing from the profession to the public interest to the client. This is not a uniquely UK phenomenon but may be seen in other countries' accounting ethics (see, for example, Brooks, 1989). If the Guidelines of the professional bodies are complex in this respect, an ability to critically examine and analyse circumstances and apply reasoned solutions is essential. This ability, however, is depen- dent on the individual having benefited from a 'deep learning' teaching strategy of the ethical foundations of accounting; a strategy which is not always evident in university

Dow

nloa

ded

by [

Mos

kow

Sta

te U

niv

Bib

liote

] at

00:

19 1

4 N

ovem

ber

2013

Ethics and accounting education in the UK - a professional approach?

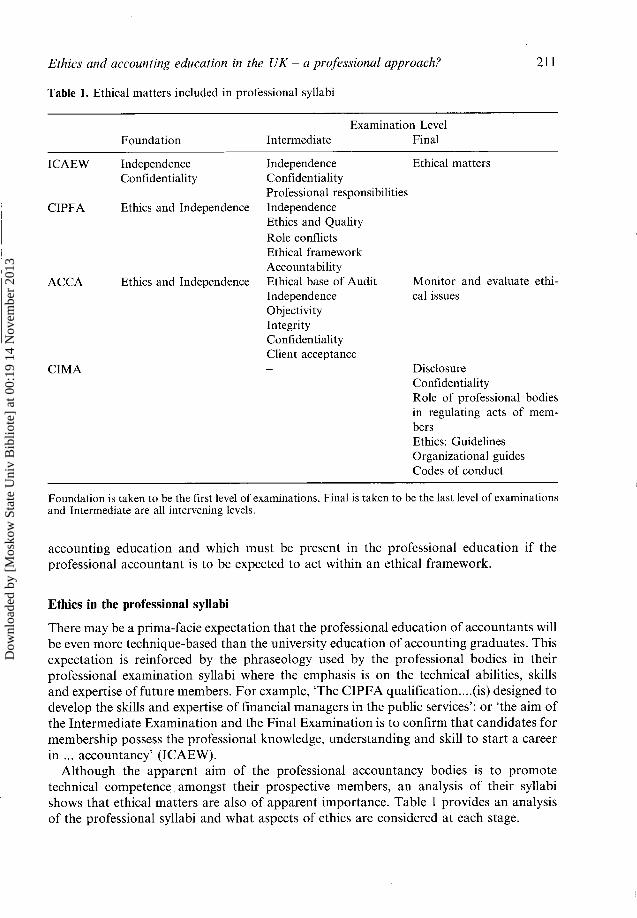

Table l. Ethical matters included in professional syllabi

Foundation Examination Level

Intermediate Final

ICAEW Independence Independence Ethical matters Confidentiality Confidentiality

Professional responsibilities CIPFA Ethics and Independence Independence

Ethics and Quality Role conflicts

I Ethical framework Accountability

ACCA Ethics and Independence Ethical base of Audit Monitor and evaluate ethi- Independence cal issues Objectivity Integrity Confidentiality Client acceptance

CIM A Disclosure Confidentiality Role of professional bodies in regulating acts of mem- bers Ethics: Guidelines Organizational guides Codes of conduct

Foundation is taken to be the first level of examinations, Final is taken to be the last level of examinations and Intermediate are all intervening levels.

accounting education and which must be present in the professional education if the professional accountant is to be expected to act within an ethical framework.

Ethics in the professional syllabi

There may be a prima-facie expectation that the professional education of accountants will be even more technique-based than the university education of accounting graduates. This expectation is reinforced by the phraseology used by the professional bodies in their professional examination syllabi where the emphasis is on the technical abilities, skills and expertise of future members. For example, 'The CIPFA qualification ....( is) designed to develop the skills and expertise of financial managers in the public services': or 'the aim of the Intermediate Examination and the Final Examination is to confirm that candidates for membership possess the professional knowledge, understanding and skill to start a career in ... accountancy' (ICAEW).

Although the apparent aim of the professional accountancy bodies is to promote technical competence amongst their prospective members, an analysis of their syllabi shows that ethical matters are also of apparent importance. Table 1 provides an analysis of the professional syllabi and what aspects of ethics are considered at each stage.

Dow

nloa

ded

by [

Mos

kow

Sta

te U

niv

Bib

liote

] at

00:

19 1

4 N

ovem

ber

2013

212 Fleming

Table 2. Comparison of ethical weights to total weights within final stage examinations

Total marks Weight given Proportion (%) in final stage to ethical matters

ICAEW 400 6.66 1.66 ACC A 600 6.25 1.04 CIMA 400 15 3.75 CIPFA 400 4.3 1.07 ~

It seems that the emphasis generally during the earlier stages of professional education is on those aspects of ethical conduct which promote the role of the profession (for example, independence and confidentiality) with the obvious exception being CIMA. Similarly, the emphasis in the Final stages generally appears to be more broad-based with most profes- sional bodies talking in their syllabi about wide ranging ethical 'issues' or 'matters'.

Independence, confidentiality and similar early years' material is, however, relatively easy to define and teach since these terms are all defined in the professional guides as are the expectations placed on members of the profession. In those terms, deep learning is not required and may not even be sought - it is simply a question of knowing the rules and when and how to apply them. The possibility of a requirement for deep learning occurs when ethics is covered in the Final examinations of the Institutes, when students may be expected to 'evaluate' issues. The weighting attached to ethical matters by the professional bodies in their syllabi suggests, however, that such matters are not of vital importance.

The ACCA cover ethics in their final examinations within the syllabus 'Financial Reporting Environment' where no weighting to ethics is given but it is mentioned along with 15 other topics - some of which are further subdivided into as many as nine sub- topics. ICAEW covers ethics within 'Auditing and Financial Reporting', it being one-third of a section which has a 20% weighting attached to it. CIMA considers ethics in two of its final papers, once in 'Strategic Management Accounting and Marketing' where it has a weighting of 10% and again within 'Management Accounting Control Systems' where it forms a third of a section with a total weighting of 15%. CIMA additionally notes within 'Strategic Management Accounting and Marketing' that the area of corporate social responsibility and professional ethics is 'likely to increase in importance'.

Table 2 compares the weighting given to ethical matters in the professional stage syllabi to the total weights, or marks available, within the Final stage examination diet. For ACCA it has been assumed that the topics mentioned within 'Financial Reporting En- vironment' have equal weighting and a similar assumption has been made within the relevant subjects of Professional Stage 2 CIPFA examinations (CIPFA's Professional Stage 3 was discounted in this part of the study since it consists solely of a multi- disciplinary case study and a Project).

There is proportionately very little accounting ethics within the professional bodies' Final examination syllabi. However, no amount of ethics education will prevent people who are so inclined from performing unethical or amoral acts and the intention of an adequate ethical education should not simply be to prevent 'bad practice' but to instill qualities within individuals which will allow them to recognize and cope with moral dilemmas and to be more sensitized to injustice. The proportionate weighting attached to ethical matters by the professional bodies suggests that technical competence remains of paramount importance and that ethics is, almost, an optional add-on of little importance

Dow

nloa

ded

by [

Mos

kow

Sta

te U

niv

Bib

liote

] at

00:

19 1

4 N

ovem

ber

2013

1 Ethics and accounting education in the UK - a professional approach? 213

1 in its own right. By implication, it may be seen that the professional bodies do not place a high priority on developing their prospective members' sensitivity to moral and ethical justice.

This apparent lack of substantial encouragement for the development of ethics and ethical sensitivity during the professional training period may also be seen to be extended into the post-qualifying period. For example, very little support is given by any profes- sional body to employee members who wish to adopt ethical positions when confronted by unethical situations in their places of work. In such circumstances, the only support given by the professional bodies is the offer of confidential advice and the provision of a limited number of hours of free legal consultation. Apart from that, the individual member is left alone to pursue his/her own course of ethical action up to the point of resignation. All the professional bodies refuse to support the 'ethical' member in pursuing a case against the employer, considering such cases to be personal disputes between employer and employee. CIMA specifically states that it will not become involved in such employee/employer conflicts.

Love11 (1993) argues that in such circumstances it is unreasonable for the professional bodies to claim a 'public interest' commitment for they are unwilling to publicly defend a member who, through conscience, wishes to pursue the public good. When this is combined with the apparently low priority placed by the Institutes on developing ethical maturity in their prospective members, it may begin to appear that the profession is more interested in seeming to be concerned about ethics and ethical attributes within its members than in actually pursuing policies and courses of action designed to enhance the ethical position of the profession and its members.

Teaching methods

A further problem inherent in inculcating ethics by the professional bodies is the means by which it is taught. It is possible that lecture-based courses of study and even the use of case studies are only effective in transferring theoretical knowledge and do not adequately prepare the individual for the realities of life-based ethical dilemmas (MacLagan, 1993), although it could be argued that the case study analysis method of instruction approaches a deep learning strategy more so than ordinary lectures and is therefore to be preferred in teaching ethics. Where 'teaching' is remote, or where the student has to rely on self-study techniques, then the adequacy of preparation of the individual to critically analyse ethical problems is diminished further as found by Burton et al. (1991). In such circumstances, the learner lacks any contact with other people's views and analyses and must rely solely on personal, undeveloped, opinion and that of the author of whatever text-book is being studied.

All professional accounting bodies, with the exception of the Institute of Chartered Accountants of Scotland, permit students to study for all their examinatioris in private employing a variety of distance learning techniques. By implication this means that students are not necessarily exposed to the views of their peers, and others, during their education and although this may be acceptable in the acquisition of accounting techniques it is detrimental in the development of ethical awareness. The method of teaching ethics adopted by the professional accountancy bodies appears, therefore, inappropriate for the preparation of ethically aware professional accountants.

Dow

nloa

ded

by [

Mos

kow

Sta

te U

niv

Bib

liote

] at

00:

19 1

4 N

ovem

ber

2013

Fleming

Assessment procedures

Where the purpose of ethical education is to promote the acceptance of rules of conduct then it may be acceptable to test the knowledge of such rules through the medium of a formal written examination. As shown above, most ethical knowledge required of profes- sional accountancy students in the earlier stages of training is that of the rules, mostly on confidentiality, independence, and the importance of objectivity. Assessing an under- standing of these matters can be made through formal exams and, indeed, the profession does just that. However, it is unlikely that a formal three hour examination is the most appropriate vehicle to test responses to ethical questions and dilemmas when more is expected than a comparison of the scenario to the rules of conduct and a rehash of the l stated course(s) of action.

Where the various Institutes try, in the later or Final examination stages, to cover ethical matters and issues of a broader or more general nature than, for example, the need for and definition of independence, assessment procedures ought to be appropriate. In many cases there will be no correct answer and what will be sought is evidence of analysis, an understanding of the consequences of differing actions and inactions, and an increase in the individual's ethical sensitivity. Such attributes are unlikely to be successfully assessed in an unseen examination question where the student is expected to write a 750 word essay under severe time pressure and in circumstances which will never again be experienced. The more appropriate test methods would be long-term and practical, where the student's growing ethical awareness could be gauged by observation of what the person actually does in conflict situations rather than what he/she has learned from a Code of Ethics/ Conduct.

Such long-term, continuous assessment techniques cause obvious problems for profes- sional accountancy bodies as they would not fit in with the other testing methods employed by the professional bodies, i.e. standard examinations. In addition, given the relative quantitative unimportance attached to broader ethical matters by the various Institutes, it is unlikely that the Institutes would consider employing any testing mechan- ism other than examinations as a testing method for 'ethics'.

The profession, however, may also be seen to be assessing a prospective member's ethical maturity in a much more subtle and unquantifiable way when it asks for profes- sional referees prior to admission to membership. It may also be assuming that significant moral development is undertaken during the period of professional training through experiential learning rather than through a structured mechanism and that this can be assessed by the professional referee.

By asking sponsors if an individual is a fit and proper person to be a member of a particular Institute, the question implies a subjective assessment of the applicant's char- acter. Such an approach has obvious associated problems:

there are no objective criteria which the professional referee can employ or reference; there can be no assurance that the professional referee is capable of making an informed assessment of the student's ethical maturity; the professional referee may be subject to bias - particularly from the ethos of the firm's operational philosophy and organization.

In much the same way, it is inappropriate to assume that experiential learning in the work-place is the most suitable means of ensuring moral development. Organizational

Dow

nloa

ded

by [

Mos

kow

Sta

te U

niv

Bib

liote

] at

00:

19 1

4 N

ovem

ber

2013

I Ethics and accounting education in the UK - a professional approach? 215

structures and philosophies can inhibit or encourage moral development. MacLagan (1993) considers that it is only those firms which have a participative management style, where the language used by managers encourages ethical debate, and where formalized codes of conduct (if they exist) are used as guides rather than statutes which facilitate an individual's progression towards the higher levels of Kohlberg's ladder of moral maturity. Clearly those firms which are direct negatives to the above will inhibit individual moral development. Since the profession cannot control the organizational structure and philo- sophy of training firms, it cannot, therefore, rely on these firms to provide a suitable environment for acceptable experiential learning and moral development of its trainees.

l Conclusion

There is an expectation that accountants will always employ high ethical standards in the performance of their duties. However, the available evidence suggests that accountants either occupy the middle ground of ethics or lean slightly towards an amoral ethical position and consequently there does appear to be a significant difference between the ethical expectation placed on accountants and the ethical behaviour actually observed in practice.

The responsibility for the ethical education of professional accountants cannot be placed solely, or even largely, on the universities for a number of reasons, some of which may not be necessarily unique to accounting education in the university sector:

(1) Since the majority of student accountants do not have an accountancy degree, if ethical education was left solely to the universities then the majority of professional accountants would not receive any ethical education.

(2) Accounting teaching is generally technique driven which, in turn, leads students to generally adopt a surface learning approach to all matters. Ethics education requires a deep learning approach.

(3) When universities teach ethics for accountants, the manner tends to be peremptory and inadequate resulting in no long-lasting effects.

As universities currently do not provide an ethical education for the majority of professional accountants, this does mean that they are necessarily precluded from making a significant contribution to improving the situation in the future. Where the sole objective is student success in the professional examinations, it is unlikely that those institutions and other learning environments which have that objective will effectively promote ethics in accounting students for, where the educational impetus is for technical competence only, there is little or no role for matters in the curriculum which are not significantly assessed by the professional bodies. It is essentially only in the university sector, where the pressures of the professional syllabus are not so obvious, that the opportunity exists in terms of resources and orientation for both the adoption of teaching styles which encourage 'deep learning' by the student and the introduction and development of ethical reasoning within an accounting framework.

Since the accounting degrees from the university sector currently do not produce the majority of professional accountants nor provide a uniformly good standard of ethical education for the remaining minority, the responsibility for ensuring the ethical education of professional accountants must currently lie with the professional Institutes themselves. Although the declared aim of the professional bodies is to promote technical abilities, an

Dow

nloa

ded

by [

Mos

kow

Sta

te U

niv

Bib

liote

] at

00:

19 1

4 N

ovem

ber

2013

Fleming

analysis of their professional syllabi shows that ethical matters are also of apparent importance. However, the weights attached to ethical matters when compared to all other matters in the Final stage examinations suggests that ethics may not, in fact, be considered to be of vital importance.

Two other factors currently exist which prevent the professional bodies from success- fully integrating an effective ethics education into their assessment schemes for prospective members:

(1) All accounting bodies (except ICAS) permit distance learning, without the necessity for group teaching. Without contact with other people in the learning environment, the student is unable to experience the example of anyone except himlherself and the author of the text being studied.

(2) The formal examination technique employed by the Institutes is inappropriate in assessing ethical development.

It therefore appears that members of the accountancy profession are expected to display exemplary ethical standards but do not receive an acceptable ethical education either before entering the profession or after they have joined it. This being so, it should come as no surprise to find that accountants do not always, or only rarely, live up to the expectation placed on them and that when they do it is because of a personal morality rather than a professional ethos.

So long as the accounting profession remains open to non-accounting graduates, the onus on ensuring that future members in general have an ethically mature perspective remains with the profession. The current situation is ineffective and suggestions could be put forward as to how it could be improved such as a pre-qualifying examination on ethical rules and their application, compulsory weekend schools, or a more formal and rigorous approach to assessing potential members' ethical maturity on application to join. A pre-qualifying examination on ethical rules and their application would be simple enough to set but would only be assessing knowledge rather than ethical maturity whereas compulsory weekend schools could employ techniques which encourage deep learning and foster ethical awareness and sensitivity. Formal assessments of prospective members' ethical maturity is, of course, much more problematic involving the development of standards of ethical reasoning and maturity together with appropriate assessment meth- ods. Obtaining a consensus on what should constitute acceptable ethical maturity or on how it should be assessed would not be easy. Of paramount importance is a reorientation of the profession itself to accepting the importance of having an ethically mature member- ship for without such a reorientation it is unlikely that the additional costs inherent in assessing ethical maturity (administrative, assessor development, or political) would be borne.

References l

l ACCA (1993) The ACCA Examination Syllabus, London: ACCA. Armstrong, M.B. (1987) Moral development and accounting education, Journal of Accounting

Education, 5, 2743. Brooks, L.J. (1989) Ethical codes of conduct; deficient in guidance Canadian accountancy

profession, Journal of Business Ethics, 8(5), 325-36. Burke, T., Maddock, S. and Rose, A. (1993) How ethical is British business? Working Paper Series 2

Dow

nloa

ded

by [

Mos

kow

Sta

te U

niv

Bib

liote

] at

00:

19 1

4 N

ovem

ber

2013

Ethics and accounting education in the UK - a professional approach?

No 1, Faculty of Business, University of Westminster. Burton, S., Johnstone, M.W., Wilson, E.J. (1991) An experimental assessment of alternative

approaches for introducing business ethics to undergraduate business students, Journal of Business Ethics, 10(7), 507-17.

CIMA (1994) Syllabus, London: CIMA. CIPFA (1993) Syllabus and Regulations, London: CIPFA. Cohen, J.R. and Plant, L.W. (1992) Beyond bean counting: establishing high ethical standards in the

I public accounting profession, Journal of Business Ethics, 11(9), 45-56. Committee of Scottish University Principals (1992) Teaching and Learning in an Expanding Higher

Education System, Lasswade: Polton House Press, p. 5. Entwhistle, N., Thompson, S and Tait, H. (1992) Guidelinesfor Promoting Eflective Learning in

Higher Education. Centre for Research on Learning and Instruction, University of Edinburgh.

1 French, P.A., Jensen, R.E. and Robertson, K.R. (1992) Undergraduate student research programs: are viable for accounting as they are in science and the humanities, Critical Perspectives on Accounting, 3(4), 337-57.

Gibb, R. (1993) Reform needed to build profession's confidence, Accountancy Age, 25/2/1993, p. X. Gray, R., Bebbington, J. and McPhail, K. (1993) Teaching ethics in accounting and the ethics of

accounting teaching. Discussion Paper ACC/9305, Centre for Social and Environmental Accounting Research, University of Dundee.

Hiltebeitel, K.M. and Jones, S.K. (1992) An assessment of ethics instruction in education, Journal of Business Ethics, 11(1), 3746.

Huss, H.F. and Patterson, D.M. (1993) Ethics in accounting; values education without indoctrination, Journal of Business Ethics, 12(3), 23543.

ICAEW (ad.) Examinations Conduct and Syllabuses 1993-94, London: ICAEW. Kohlberg, L. (1969) Stages and sequences: the cognitive approach to socialization. In Handbook of

Socialization Theory and Research, edited by D. Goslin, Chicago: Rand McNally, pp. 347480. Kohlberg, L. (1973) Continuities in childhood and adult moral development revisited. In Life-Span

Developmental Psychology: Personality and Socialization, edited by P.B. Baltes and K.W. Schaie, New York: Academic Press.

Lehman, C. (1988) Accounting ethics: surviving survival of the fittest, in Advances in Public Interest Accounting, Vol. 2, edited by M. Niemark, JAI Press, pp. 71- 82.

Loeb, S.E. (1988) Teaching students accounting ethics; some crucial issues, Issues in Accounting Education, Fall, 3 16-29.

Lovell, A. (1993) Ethical dilemmas of and for accountants. Paper presented to BAA Annual Conference, University of Strathclyde.

MacLagan, P. (1993) Issues concerning the moral development of people in organisations. Working paper HUSM/PWM/20, University of Hull.

Ponemon, L.A. (1990) Ethical judgements in accounting; a cognitive development perspective, Critical Perspectives on Accounting, 1(2), 19 1-2 15.

Power, M. (1991) Educating accountants: towards a critical ethnography, Accounting Organizations, and Society, 17(5), 333-53.

Schweikart, J.A. (1992) Cognitive-contingency theory and the study of ethics in accounting, Journal of Business Ethics, 11(5/6), 471-8.

Trevino, L.K. (1992) Moral reasoning and business ethics; implications for research, education and management, Journal of Business Ethics, 11(5/6), 445-59.

Weber, J. (1990) Measuring the impact of teaching ethics to managers; a review, assessment, and recommendations, Journal of Business Ethics, 9(3), 183-90.

Wild, W. and Ahmed, P.K. (1994) The teaching of ethics on accounting courses. Paper to the BAA Annual Conference, Winchester.

Dow

nloa

ded

by [

Mos

kow

Sta

te U

niv

Bib

liote

] at

00:

19 1

4 N

ovem

ber

2013

Dow

nloa

ded

by [

Mos

kow

Sta

te U

niv

Bib

liote

] at

00:

19 1

4 N

ovem

ber

2013