Embed Size (px)

DESCRIPTION

Description

Citation preview

2012 ETF Review

prOFESSIONAL & institutional portfolio

PIP REVIEWS

ETF Review 2012

A snapshot of current views, facts and ideas from professionals in the ETF industry. We sincerely hope you enjoy reading this edition as it has been a pleasure to compile for a wider audience.

Sunil Maya Managing Director PIP Reviews

IBPC 153 Fenchurch Street London EC3M 6BB

[email protected] Tel: +44 207 220 0440 Fax: +44 207 220 0445

Although every effort has been made to ensure the accuracy of the information contained in this book the publishers can accept no liability for inaccuracies that may appear.

All rights reserved. No part of this publication may be reproduced in any material form by any means whether graphic, electronic, mechanical or means including photocopying, or information storage and retrieval systems without the written permission of the publisher and where necessary any relevant other copyright owner. This publication – in whole or in part – may not be used to prepare or compile other directories or mailing lists, without written permission from the publisher. The use of cuttings taken from this directory in connection with the solicitation of insertions or advertisements in other publications is expressly prohibited. Measures have been adopted during the preparation of this publication which will assist the publisher to protect its copyright. Any unauthorised use of this data will result in immediate proceedings.

© Copyright rests with the publishers, ibpc, England.

The material in this publication has been prepared solely for the distribution to professional and qualified investors.

The information in this publication you are about to read is intended for Professional and Qualified Investors. Including regulated financial intermediaries such as banks and securities brokers, regulated insurance companies, government or public authorities, corporate treasurers and financial advisers.

The information contained in this publication should not be considered as an offer, or solicitation, to deal in any of the investments or funds mentioned herein, by anyone in any jurisdiction in which such offer or solicitation would be unlawful or in which the person making such offer or solicitation is not qualified to do so or to anyone to whom it is unlawful to make such offer or solicitation.

The market commentaries represent an assessment of the market environment at a specific point in time and are not intended to be a forecast of future events, or a guarantee of future results. This publication is not prepared for any particular investment objectives, financial situation or requirements of any specific investor and does not constitute a representation that any investment strategy is suitable or appropriate to an investor’s individual circumstances or otherwise constitute a personal recommendation. The information in this publication is being provided strictly for informational purposes only and does not constitute an advertisement.

The commentaries should not be regarded by investors as a substitute for independent financial advice or the exercise of their own judgment.

IBPC does not warrant the accuracy, adequacy or completeness of the information and materials contained in the publication and expressly disclaims liability for errors or omissions in such information and materials. Accordingly, no warranty whatsoever is given and no liability whatsoever is accepted for any loss arising whether directly or indirectly as a result of the reader, the investor, any person or group of persons acting on any information, opinion or estimate contained in the website. IBPC reserves the right to make changes and corrections to any information on this publication at any time, without notice.

Past performance is not a guide to the future. Market and exchange rate movements may cause the capital value of investments and the income from them, to go down as well as up and the investor may not get back the amount originally invested. Investments involve risks. Before making any investment decision, you should read the relevant offering documents and in particular the investment policies and the risk factors. You should ensure you fully understand the risks associ-ated with the investment and should also consider your own investment objective and risk tolerance level. Remember, you are responsible for your investment decision. If in doubt, please get independent financial professional advice.

32 ETF Review ETF Review

01 Deutsche Bank - What does 2012 hold for the European ETF Industry?

4

02 Claymore Investments - The Basics of Fundamental Index® Investing

7

03 Commerzbank - Lucrative Component for Investments 804 iShares Switzerland - Friend or Foe? The Impact of

Inflation on Local Currency Emerging Market Bonds9

05 UBS - Index Investments that Shine 12

06 Natixis - Focus on Enhanced Beta Strategies 1407 Detlef Glow, Head of Lipper EMEA Research, Lipper -

Are ETFs in Trouble?16

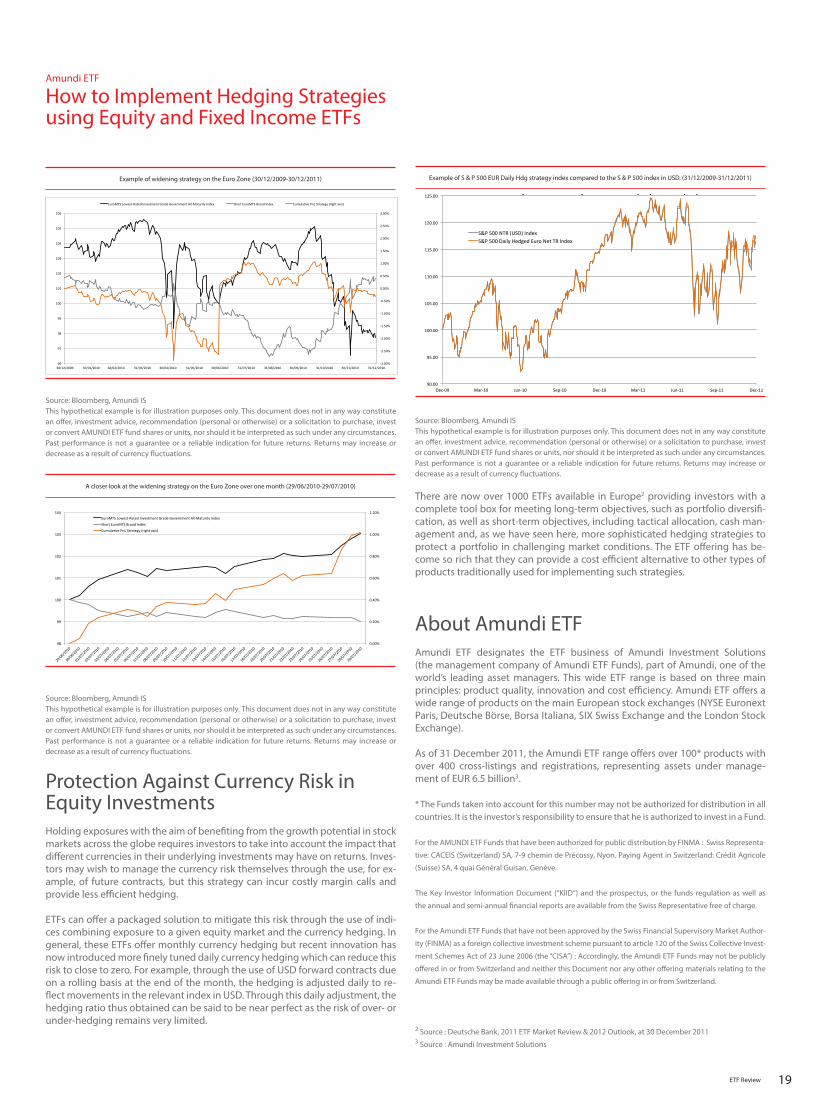

08 Amundi ETF - How to Implement Hedging Strategies using ETFs

17

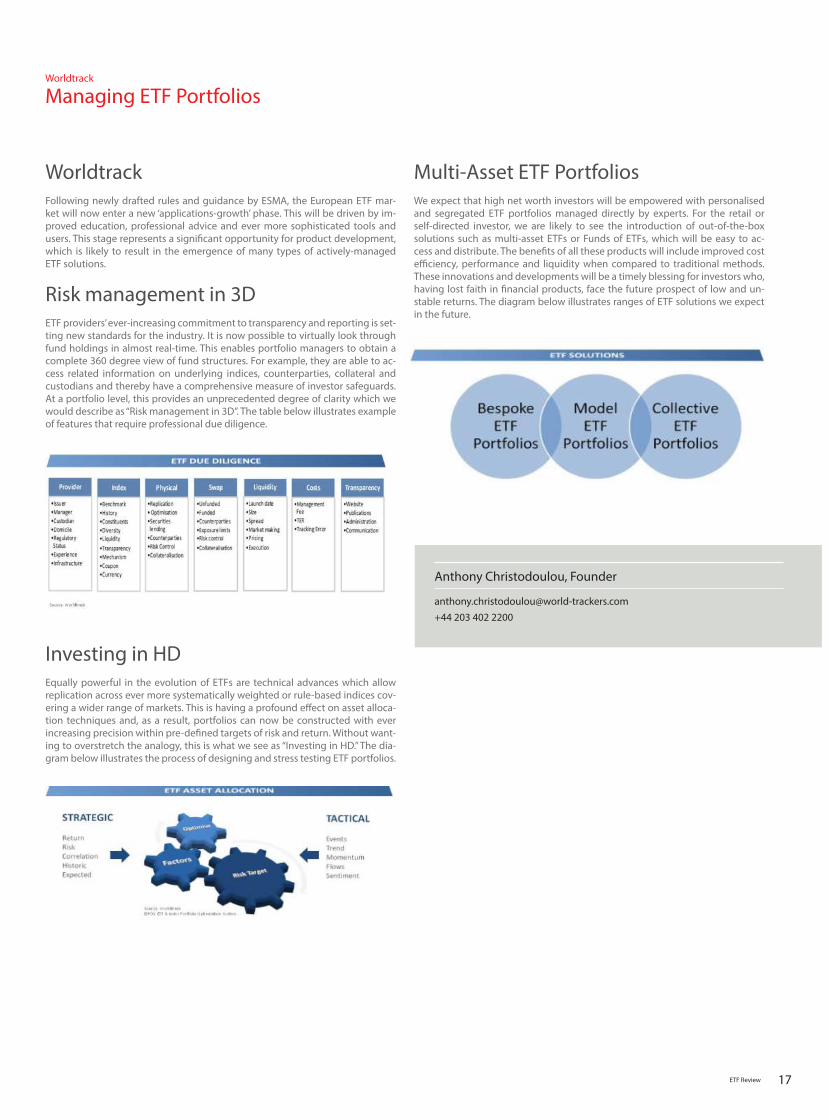

09 Worldtrack - Managing ETF Portfolios 19

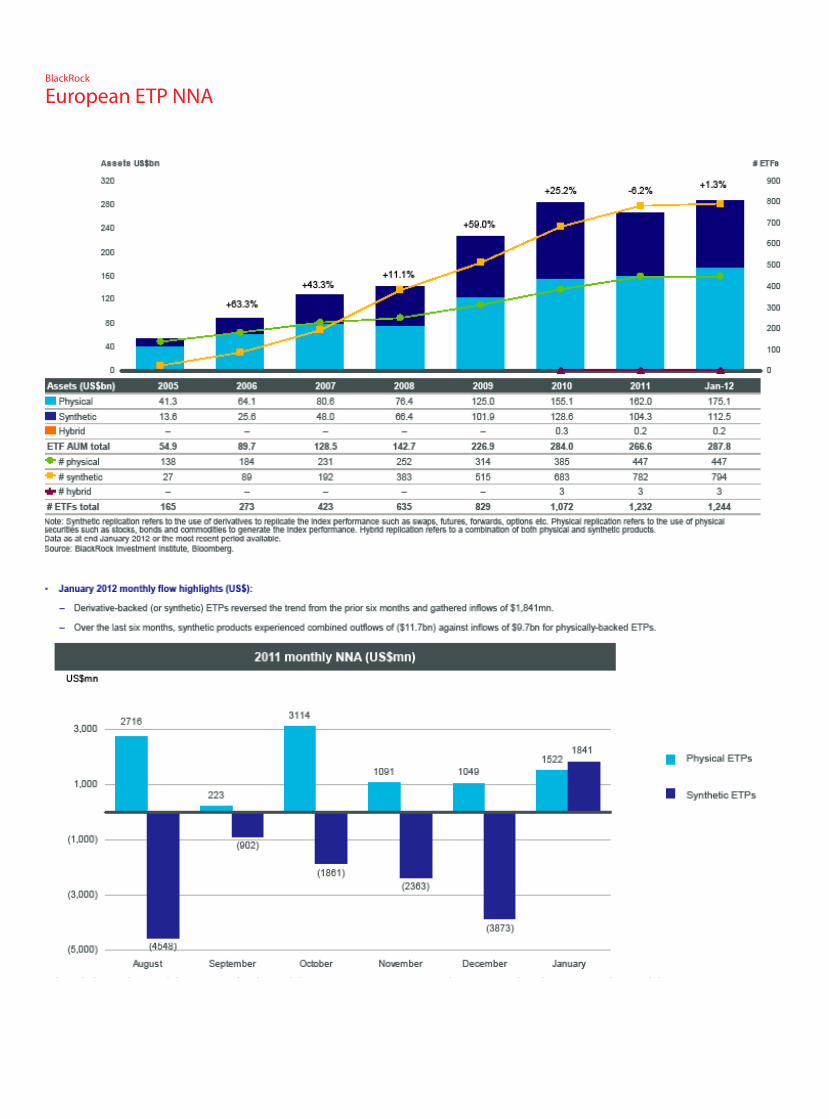

10 BlackRock - European ETP NNA 20

Contents

32 ETF Review ETF Review

Rebalancing Act2011 was a good year overall for the ETF industry. Amid challenging market conditions the global ETF industry grew by 3.2%. Comparing this to prior year growth rates, often over 30%, could provide an unfavorable picture and be per-ceived as a slowing down of the industry. However, this observation on the sur-face masks the fall in asset prices over the year, which contributed a decline of 9.3% to global ETF assets.

Some of the most positive news came from the fact that new money flowing into the global ETF industry [cash flows] for 2011 totalled $163.8 billion. This was marginally higher than the prior year’s [$162.3 billion] cash flows, when the industry had grown by 27.4%. Market prices shaved off an average of 9.3% of global ETF asset levels over the 2011, but investors interest, as expressed by new money, outpaced asset price falls and contributing 12.5%, making it a positive year for ETFs.

The growth story for European ETF market however was a bit different. European ETF assets shrunk by 4.9% over 2011. Cash flows for Europe were positive, total-ling $22.1 billion, however they were half of those experienced in 2010 [$45.0 billion]. There are mainly two reasons for the reduction in European ETF cash flows. Firstly, 2012 was a year of two minds in terms of investors’ risk appetite. The first half brought healthy flows to the equity market, including the ETF market, however, starting in August, the risk-off trade prevailed and cash flows started trending negative. Market uncertainty, primarily caused by the Euro sov-ereign debt crisis, also kept investors away from sovereign benchmarked ETFs, Europe’s largest fixed income ETF market component. In addition, in 2011, ETFs received much attention from regulators, a lot of which was fuelled by general credit concerns in the market. These two factors contributed to a slower year, than other global territories, for European ETFs.

However, there are hopeful signs that things are turning around and that the European industry is overcoming some of these hurdles. In the first two weeks of 2012, European ETFs received strong cash flows totalling €2.2billion of new inflows and saw their assets rise by 3.9% to reach €216.1 billion. Furthermore, a lot of the regulator discussions have gone through a full review cycle and the European Markets and Securities Authority [ESMA], the European asset manage-ment industry regulator, is undergoing a second, and perhaps final consultation before issuing guidance.

A lot of what materializes in terms of growth in ETF industry asset growth is af-fected by equity market conditions. In a good equity market year, ETF cash flows tend to be higher, especially as equities are by far the industry’s largest com-ponent [close to 70%]. Therefore, depending on how the European sovereign crisis evolves, we expect the ETF industry to continue growing. If 2011 was a year during which regulators digested the issues raised about ETFs, 2012 should be a year during which resolution materializes. With increased education and follow-

ing comprehensive discussions, many of the issues initially raised by regulators have been dropped. We anticipate that regulators will come out with additional ETF specific guidance but will otherwise refrain from making drastic changes, for the time being, that are more relevant to the entire asset management industry and not just ETFs. One important realization that has transpired from the ETF regulatory discussion, is that ETFs are the golden standard when it comes to dis-closure and transparency across the fund industry. These developments should boost ETF usage as now with the regulatory reviews reaching a conclusion, the industry will likely benefit and continue to attract investors at rates seen prior the middle of 2011.

We therefore expect asset level growth rates in the European ETF industry to range between 10% and 20%, the majority of this growth coming from new money flowing into the industry. The actual growth will largely depend over equity market conditions over 2012 and how asset prices evolve. If market un-certainty declines, growth could be closer to 20%, however, if European govern-ment debt woes continue the growth is more likely to be closer to 10%.

ETF launches, which direction are they going?The ETF industry is fairly concentrated in terms of providers, at the industry’s top echelon. In Europe, the top 5 ETF providers manage close to 80% of the in-dustry’s assets, while the comparable number in the US is closer to 90%. How-ever, a closer look at the very strong ETF product launch calendar over 2011 can shed more light about industry competitive dynamics as well as product launch trends. The European ETF industry experienced 165 new product launches over 2011, while the global total reached 554 new launches.

Due to increasingly challenging market conditions, investors have become more inquisitive about benchmarking that can deliver consistently positive returns. As a result, ETF providers have responded by building on the currently strong ETF industry traditional beta base. This trend has also provided a viable entry point for new entrants in the industry. Over 2011, there were three new entrants in the US industry and an equivalent number in the European industry. Out of these six new entrants, four launched products that are benchmarked to non-capitalization weighted indices. A trend that was started by RAFI in 2006 in the US, seems to be gathering pace. In addition to alternative index weighting tech-niques, many of the new products are tracking more active strategies that aim for positive returns irrespective of market conditions. Such products range from strategies driven on purely quantitative models to fully discretionary strategies such as hedge funds.

Figure 2 gives a mapping of investment strategies followed by products current-ly in the European ETF market. Products range from beta, which offer diversi-fied capitalization weighted indices, to alpha, which offer manager discretionary market access. Semi-active products include ETFs that track leveraged, double long and short indices, aiming to deliver superior returns. Semi-active products include non capitalization weighted indexed products. While 97% of ETF prod-ucts are beta benchmarked, it is important to note that many investment man-agers are increasingly using these products as building blocks for more active strategies in their portfolios.

Deutsche Bank

What does 2012 hold for the European ETF Industry?

Figure 1: European ETF in

2003 2004 2005 2006 2007 2008 2009 2010 20112 012* *

Other - --- 96 1681 ,078 1,9871 ,867 2,089Comm odity -- 3401 ,402 2,3203 ,596 10,664 19,483 23,219 24,841Fixed Income 8012 ,034 4,0029 ,370 13,743 29,857 35,871 42,343 43,354 43,787Equity 15,532 21,815 37,907 57,029 70,771 65,489 1 10,657 1 47,766 1 39,463 1 45,391Total 16,332 23,849 42,249 67,801 86,930 99,110 1 58,270 2 11,579 2 07,902 2 16,108Number of ETFs* 1001 14 1632 67 4186 15 8191 ,072 1,2371 ,247

0

200

400

600

800

1,000

1,200

1,400

0

50,000

100,000

150,000

200,000

250,000

Num

ber o

f ETF

s

€mill

ion

Source: Deutsche Bank ETF Research, Weekly European ETF Market Monitor

** As of 13/01/11

54 ETF Review ETF Review

The increased use of ETFs as building blocks in portfolios is precisely what is driving the launch of more niche products by both existing as well as new mar-ket entrants. The rate of entry of smaller providers through the ‘niche channel’ is increasing the pressure on existing providers to diversify their product ranges in order to avoid losing assets. Over 2011, the larger five ETF providers lost a collective 2.2% of market share, this was gained by smaller providers and rising stars. Some of the growth was also absorbed by however established providers beefing up their product ranges by launching beta products.

How are ETF usage patterns changing?ETFs became more widely used over 2011 and this is captured by two key mar-ket metrics: The percentage of ETF flows and assets when compared to the rel-evant mutual fund statistics and the percentage of ETF turnover as compared to that of cash equities in general. A comparison with the mutual fund industry yields important information about the comparative use of different type of fund products, often termed by many as the ETF adoption rate. ETF turnover comparisons with cash equities turnover give a good insight about how actively ETFs are traded compared to other cash equity instruments, including single stocks and basket products. ETFs are now almost a third [29.6%] of the cash equities turnover in the US as of the end of 2011, up from 24.0% in December 2011. The comparable number for Europe registered at 8.7%, up from 6.9% over December 2010.

Furthermore, ETFs continue to advance against mutual funds, registering at 9.0% in the US and 2.8% in Europe, up from 8.4% and 2.7% last year respectively. Perhaps most impressive is the comparison of new money that listed [ETFs] and unlisted [mutual] funds have received over 2011. US ETFs received 2.8x higher flows than the ten-fold larger mutual fund industry. European ETFs received 2.2x higher flows than the thirty-plus-fold larger UCITS mutual fund industry. The numbers in Europe point to the conclusion that the weakness in the local ETF market is not specific to ETFs but more likely due to uncertain market conditions.

There are a number of developments to watch out for in terms of ETF usage over the coming year. Currently ETFs in Europe are more popular with institutional investors. While there are no official statistics, we estimate that upwards of 90% of investors in the ETF industry are institutional. On the institutional usage com-ponent, ETF gains will come by increased usage for ETFs that are benchmarked to indices for which no other wrapper – such as futures contracts – is available. Furthermore, due to heightened risk oversight with many investment managers, ETFs are favoured over derivative products such as futures, options and swaps. The challenge for ETFs, in capturing more of these institutional users, lies in in-creasing usage and turnover levels in these ETF unique products. It is a bit of a chicken and egg dilemma, however, there are signs that open interest in futures usage, especially on mainstream equity indices, is on the decline, while ETF as-

sets benchmarked to these same indices, are on the rise.

Beyond institutional investors, the next big piece in the ETF industry participant puzzle is the retail investor. There is currently retail money invested in ETFs, how-ever, the majority of these are found in mandates managed by pension funds and asset managers. Direct retail investor participation is still very low, even though some early adopters, in the form of discount brokerage clients, are fre-quent ETF users. The high level of regulatory scrutiny that we have witnessed over 2011 is a sign that there is now consensus among policy makers that ETFs are about to get closer to the retail investor in Europe. Structural changes, pri-marily through MiFiD, have made the overall asset management product dis-tribution process more efficient and for the first time, ETFs have a real shot at competing on a level ground with other types of funds. This is a medium to long term goal though as it will take time for ETF awareness to built up with retail investors directly. In addition, intermediaries that look after retail money, such as Independent Financial Advisors in the UK, will take time to get to know the product and alter their current instrument selection practices.

Direction forward for ETFs: Where to?Much of Europe’s ETF market fortunes in the coming year will depend on what happens outside the ETF market over 2011. The resolution, or at least softening, of the Euro Sovereign crisis, and the impact it will have on market mood will be crucial in forming asset allocation patterns. However, other forces are begin-ning to shift in Europe. At the moment, the European market is dominated by US asset managers and European investment banks. The large European asset management houses remain largely absent from the ETF market. Currently, ETF providers in Europe are comprised of US based asset managers and European investment banks. Changing competitive dynamics on how mutual funds are sold across the European market are creating more incentives for European asset managers to engage in the ETF industry. Increased scrutiny by regulators in Eu-rope also signals the belief that more retail and smaller investors are beginning to embrace the ETF product.

We expect ETFs to continue growing in 2012 and while much of the growth will be determined by general market mood, ETFs are at a stage where they it is exhibiting signs of functioning as an independent – portfolio building - market. In the US market, fixed income ETFs over 2011 have reflected broader economic risk themes, proving that ETFs grow not only when the equity market is rising. Gold exchange-traded products [ETPs] also played an important role in filling the risk off trade both in the US and Europe. A balancing of asset class sizes in the ETP industry can also help growth prospects going forward.

The European fixed income ETF market has not been the beneficiary of the same high level of interest as its US counterpart over 2011. The sector’s large sover-eign benchmarked component, together with the Euro sovereign crisis did not do much to help. However, 2012 might just hold the key to reversing sovereign benchmarked product dominance in the European fixed income ETF market. As the European ETF market is largely populated by equity-driven investors, con-tinued turbulence in the equity market and an elevation of credit to an equity equivalent return source, could just entice equity-driven investors to increase usage of fixed income ETFs. This increased usage is likely to come from products offering various types of credit related exposure, such as those ETFs that track iTraxx indices, rather than from the more traditional duration oriented fixed in-come benchmarks. Given the low interest rate environment, credit is likely to play a much larger role in portfolio construction in the year ahead, and the Eu-ropean ETF industry is very well positioned with a total number of ETF products that reached 245 as of the end of 2011, as compared to 166 in the US and 20 in Asia.

But the industry is at a turning point in its evolution as growth rates in both the US and Europe appear to be normalizing. Failure to proceed with a swift reso-lution in the regulatory investigations could negatively impact European ETF growth in 2012. In the last three months of 2011, increased regulatory scrutiny

Figure 2: nt strategy type

Passive,$262.7 bil.

Passive plus,$4.4 bil.

$0.6 bil.

$2.2 bil.

LeverageTracker

97%

Source: Deutsche Bank ETF Research, 2011 ETF Market Review & 2012 Outlook, data as of 31/12/11

Deutsche Bank

What does 2012 hold for the European ETF Industry?

54 ETF Review ETF Review

Christos Costandinides

[email protected]+44(20)754-71975

and general credit concerns clearly played a significant impact on how investors chose products. Additionally, prolonged uncertainty in the equity markets, both in the US and Europe, could slow down allocations in the industry’s larger com-partment, equity. Gold ETPs, a major beneficiary of the credit crisis accounting for 8.1% of the global ETP industry, could see big outflows if the outlook for the price of gold changes. Much of the investment in gold ETPs is concentrated in a handful of products in the US and Europe.

These are all factors to watch out for in the first half of 2012. We don’t believe they pose a vital threat to the general health of the global industry, they could however generate shocks which could drag ETFs to reflect conditions prevalent in the rest of the wider – confidence stricken –market and thus push growth in the slower lane, especially in Europe.

The author is an employee of Deutsche Bank, views expressed here may have been previously published in research by Deutsche Bank.

DisclaimerThe information and opinions in this report were prepared by Deutsche Bank AG or one of its affiliates (collectively “Deutsche Bank”). The information herein is believed to be reliable and has been obtained from public sources believed to be reliable. Deutsche Bank makes no representation as to the accuracy orcom-pleteness of such information.

Deutsche Bank may engage in securities transactions, on a proprietary basis or otherwise, in a manner inconsistent with the view taken in this research re-port. In addition, others within Deutsche Bank, including strategists and sales staff, may take a view that is inconsistent with that taken in this research report. Deutsche Bank may be an issuer, advisor, manager, distributor or administrator of, or provide other services to, an ETF included in this report, for which it re-ceives compensation.

Opinions, estimates and projections in this report constitute the current judge-ment of the author as of the date of this report. They do not necessarily reflect the opinions of Deutsche Bank and are subject to change without notice. Deutsche Bank has no obligation to update, modify or amend this report or to otherwise notify a recipient thereof in the event that any opinion, forecast or estimate set forth herein, changes or subsequently becomes inaccurate. Prices and availabil-ity of financial instruments are subject to change without notice. This report is provided for informational purposes only. It is not an offer or a solicitation of anoffer to buy or sell any financial instruments or to participate in any particular trading strategy. Target prices are inherently imprecise and a product of the ana-lyst judgement.

As a result of Deutsche Bank’s March 2010 acquisition of BHF-Bank AG, a security may be covered by more than one analyst within the Deutsche Bank group. Each of these analysts may use differing methodologies to value the security; as a result, the recommendations may differ and the price targets and estimates of each may vary widely. In August 2009, Deutsche Bank instituted a new policy whereby analysts may choose not to set or maintain a target price of certain issuers under coverage with a Hold rating. In particular, this will typically occur for “Hold” rated stocks having a market cap smaller than most other companies in its sector or region. We believe that such policy will allow us to make best use

of our resources. Please visit our website at http://gm.db.com to determine the target price of any stock.

The financial instruments discussed in this report may not be suitable for all in-vestors and investors must make their own informed investment decisions. Stock transactions can lead to losses as a result of price fluctuations and other factors. If a financial instrument is denominated in a currency other than an investor’s currency, a change in exchange rates may adversely affect the investment. All prices are those current at the end of the previous trading session unless other-wise indicated. Prices are sourced from local exchanges via Reuters, Bloomberg and other vendors. Data is sourced from Deutsche Bank and subject companies.

Past performance is not necessarily indicative of future results. Deutsche Bank may with respect to securities covered by this report, sell to or buy from cus-tomers on a principal basis, and consider this report in deciding to trade on a proprietary basis.

Derivative transactions involve numerous risks including, among others, mar-ket, counterparty default and illiquidity risk. The appropriateness or otherwise of these products for use by investors is dependent on the investors’ own cir-cumstances including their tax position, their regulatory environment and the nature of their other assets and liabilities and as such investors should take ex-pert legal and financial advice before entering into any transaction similar to or inspired by the contents of this publication. Trading in options involves riskand is not suitable for all investors. Prior to buying or selling an option investors must review the “Characteristics and Risks of Standardized Options,” at http://www.theocc.com/components/docs/riskstoc.pdf If you are unable to access the website please contact Deutsche Bank AG at +1 (212) 250-7994, for a copy of this important document.

The risk of loss in futures trading, foreign or domestic can be substantial. As a result of the high degree of leverage obtainable in futures trading, losses may be incurred that are greater than the amount of funds initially deposited.

Unless governing law provides otherwise, all transactions should be executed through the Deutsche Bank entity in the investor’s home jurisdiction. In the U.S. this report is approved and/or distributed by Deutsche Bank Securities Inc., a member of the NYSE, the NASD, NFA and SIPC. In Germany this report is ap-proved and/or communicated by Deutsche Bank AG Frankfurt authorized by the BaFin. In the United Kingdom this report is approved and/or communicated by Deutsche Bank AG London, a member of the London Stock Exchange and regu-lated by the Financial Services Authority for the conduct of investment business in the UK and authorized by the BaFin. This report is distributed in Hong Kong by Deutsche Bank AG, Hong Kong Branch, in Korea by Deutsche Securities Ko-rea Co. This report is distributed in Singapore by Deutsche Bank AG, Singapore Branch, and recipients in Singapore of this report are to contact Deutsche Bank AG, Singapore Branch in respect of any matters arising from, or in connection with, this report. Where this report is issued or promulgated in Singapore to a person who is not an accredited investor, expert investor or institutional in-vestor (as defined in the applicable Singapore laws and regulations), Deutsche Bank AG, Singapore Branch accepts legal responsibility to such person for the contents of this report. In Japan this report is approved and/or distributed by Deutsche Securities Inc. The information contained in this report does not constitute the provision of investment advice. In Australia, retail clients should obtain a copy of a Product Disclosure Statement (PDS) relating to any financial product referred to in this report and consider the PDS before making any deci-sion about whether to acquire the product. Deutsche Bank AG Johannesburg is incorporated in the Federal Republic of Germany (Branch Register Number in South Africa: 1998/003298/10). Additional information relative to securities, oth-er financial products or issuers discussed in this report is available upon request. This report may not be reproduced, distributed or published by any person for any purpose without Deutsche Bank’s prior written consent. Please cite source when quoting.

Copyright © 2012 Deutsche Bank AG

Deutsche Bank

What does 2012 hold for the European ETF Industry?

76 ETF Review ETF Review

Indexing has demonstrated its worth as a great investment idea and has pro-vided the essential building block for developing ETFs. However, traditional market capitalization-weighted indexes, such as the S&P/TSX 60 Index and S&P 500 Index, have one structural flaw—they link market price with the weight-ing of a security, therefore systematically overweight overvalued securities and underweight undervalued securities. Traditional indexing can create periods of extreme volatility and lead to a drag in performance.

For this reason, institutional and retail investors around the world are becom-ing increasingly interested in alternative indexes designed to counter the flaws of market capitalization. Most notably, investors are turning to Claymore and our lineup of Fundamental Index® ETFs, a methodology designed by Research Affiliates in Newport Beach, California, to overcome the basic shortcomings of the traditional index structure. The trend towards alternative indexes is demon-strated in Canada by the increasing popularity of the Claymore Canadian Fun-damental Index® ETF.

The Research Affiliates Fundamental Index® (RAFI®) methodology selects and al-lots index security weights based on four key financial measures of a company. These measures are indifferent to its stock price and consequently to its market cap or weighting in an index. The methodology, which is designed to work in inefficient markets, limits exposure to pricing errors and fads.

Award Winning MethodologyThe concept of fundamental-indexing was first developed in 2005 by Robert Ar-nott, the chairman of Research Affiliates. In the research published by Research Affiliates in 2005, Rob Arnott demonstrated that the RAFI® methodology pro-duced a 2 per cent greater return than the S&P 500 performance from 1962-2004 with very little to no extra risk.

The RAFI® methodology determines index weights of a company based on the following four financial measures to avoid overvaluing or undervaluing stocks:

1. Total Sales—(five-year average total sales) 2. Book Equity Value—(current period book equity value)3. Cash Flow—(five-year average cash flow)4. Gross Dividends—(five-year average of all regular and special distri-butions)

By using fundamental factors rather than prices to weight stocks, fundamental-indexing takes advantage of price movements and at rebalance date, reduces the index’s constituents whose prices have risen relative to other constituents, and increases holdings in companies whose prices has fallen behind. When a company’s stock goes up and appreciates faster than its fundamentals do, it’s rebalanced downward. This is effectively a buy-low, sell-high strategy.

A Fundamental DifferenceA capitalization-weighted index, such as the S&P 500 Index, weights its compo-nents (or companies included in the index) by the total market value of their out-standing shares. The math is simple: number of shares outstanding multiplied by current market price. The impact of each component stock’s price change on the index is proportional to its overall market value, not the fundamental value of the stock itself. In other words, the more a stock increases in price, the higher its weighting in the portfolio.

“In the past five years, the RAFI® methodology has generated superior performance, even during a period of market turmoil.”

Rob ArnottChairman & CEO, Research Affiliates, LLC.March 2011

On the other hand, in a Fundamental Index® portfolio, stocks are weighted by their fundamental accounting factors rather than market value—these factors include sales, book value, cash flow and dividends. Breaking the link between

stock price and index weighting is critical—it eliminates the return drag built into cap-weighted indexes. This change in weighting methodology can add up substantially over time.

The Fundamental Index® concept works globally. It’s more than luck – it’s the intelligence and discipline of the process.

The Fundamental Index® methodology is based on the theory that day-to-day, markets and stock prices are not perfectly efficient (individual stocks are over-valued and undervalued from time to time), and that prices revert to their “fair value” over time. Weighting using fundamentals creates a stable anchor to trade against the market’s constantly shifting expectations, fads and bubbles. In fact, this “contra rebalancing” provides a significant source of added value over time.

The Claymore Canadian Fundamental Index ETFClaymore ETFs is the exclusive provider of ETFs based on the FTSE RAFI® Fun-damental Index Series in Canada. In March 2011, the Claymore Canadian Fun-damental Index® ETF (CRQ) celebrated its 5 year anniversary with impressive results.

CRQ offers investors the highlights of a passive investment: low cost, lower turn-over, and transparency. Fundamental-weighting decreases exposure to high P/E stocks during episodes of unsustainable P/E expansion, thus avoiding over-exposure to the more overvalued stocks.

Over the past five years (February 2006-December 2011), CRQ has outperformed the benchmark S&P/TSX 60 Index and the majority of mutual funds in the Ca-nadian equity category. CRQ is the #4 ranked fund (out of 93 funds with 5 year track records) in the Canadian Equity fund category to the end of December 2011 and received a Five-Star rating from Morningstar.

In addition to CRQ, Claymore offers Canadian investors four additional ETFs that utilize the RAFI methodology, including

Claymore Investments

The Basics of Fundamental Index® Investing

3 Year 5 Year Claymore Fundamental Index ETF 12.78% 2.38% S&P/TSX 60 Index 10.31% 1.57%

Source: Bloomberg as of 12/31/11

ETF Name Ticker Claymore US Fundamental Index ETF -‐ C$ Hedged CLU Claymore US Fundamental Index ETF -‐ Non-‐Hedged CLU.C Claymore International Fundamental Index ETF CIE Claymore Japan Fundamental Index ETF -‐ C$ Hedged CJP

Som Seif

President & CEO Claymore Investments, Inc. [email protected]

76 ETF Review ETF Review

In psychology, passive means an experience without doing anything oneself. And this is something that stock market play-ers are increasingly coming to like. A certain degree of passiv-ity can be advantageous in many cases. We are talking about passive investments. Tests have shown that only around one in five actively managed equity funds manages to outperform the benchmark over the long term. So why not just invest in the benchmark in the first place?

John C. Bogle is a pioneer in this area - he founded the first index fund in the USA. His investment strategy is both simple and effi-cient: He aims to acquire all of the listed companies in a country in a package. This allows investors to participate in the perfor-mance of the entire market.

Nowadays, putting theory into practice just takes a single order. Exchange traded funds (ETFs) allow passive investments to be implemented cheaply. ETFs are enjoying a strong increase in popularity with both retail and institutional investors These fi-nancial instruments participate one-to-one in the performance of the underlying, and have a very low cost ratio. As each inves-tor has their own personal preferences, ETFs now offer a wide range of index products and underlyings. In spite of this, how-ever, the aim is to test each index exactly in order to exclude a cluster risk. Weighting a few shares too strongly would nega-tively impact diversification.

ETFs have an open-ended structure. This allows investors to in-vest in the markets they have selected without a limited dura-tion. A key criterion, which John C. Bogle also describes in his best-seller “Common sense on mutual funds”: “The longer the investment horizon, the lower the deviations in the average an-nual income are.” That is why investors should not underestimate the timespan for their investment, according to the investment expert. For example, S&P 500 has yielded impressive returns in the past two years. Since the start of the 1990s, the index has brought a total return of 335 per cent or a respectable 7.6 pres-ent per year. Our own SPI has even performed slightly better, with annual returns of almost 8 per cent. That means that the capital employed has increased more than five-fold during this investment period. The Swiss “Gesamtmarktindex” (total market index) has 217 members, and a very broad investment base, as is the case for the S&P 500. This is not the case for the DAX which comprises just 30 blue chips. However, in terms of performance (6.4% p.a.), the DAX has no reason to hide itself away. In addi-tion, the key German index also has a high dividend return of 4.6 per cent. This is benefits shareholders if the product selected is based on “total return”, which is generally the case for ETFs, even for price indices.

Investors who want to invest in a specific barometer should have a well-founded opinion of the markets. If this is the case, index products are an optimum instrument for retail investors to participate in the markets. They allow risks to be spread rea-

sonably and they are also low priced. Well-established markets in Europe are available with low annual fees of 0.12 per cent and less. “Performance from costs that have not arisen” is an excel-lent way to summarize ETFs compared to active funds. Inves-tors pay a management fee of 1.5 per cent and more on aver-age for actively managed portfolios - not to mention possible performance-related fees. An important factor: investors should always keep an eye on their own risk management. If the under-lying political or economic conditions change - which would not be surprising given the current insecure phase - investors may have to reshuffle.

Commerzbank

Lucrative Component for Investments

Dominique Boehler

Phone +41 (0) 44 563 69 82mailto:[email protected] www.comstage-etf.ch

98 ETF Review ETF Review

Post the 2008 global credit crisis the success of the emerging markets story has been the focus of much commentary. With economic growth rates in these countries continuing to be above that of the developed world, it is entirely understandable that investors continue to look towards these markets in in-creasing numbers. The noticeably higher yields offered by these bonds is the key feature that attracts investors, but in light of the fact that the cash flows are denominated in the local currency, this exposes the investor to currency risk.

We examine the historical relationship between the local currency exchange rates as measured against the dollar and the level of inflation prevalent in the countries issuing the government debt. We find there is a significant relationship between these FX rates and the level of inflation, which can be loosely explained by the rate setting policies of the local central banks. While the onset of infla-tion can unduly affect the FX cross-rate against the dollar, the impact is not one-directional, and for a long-term investor offers the possibility that the impact on returns could cancel out.

With the continuing growth of the ETF market, more corners of the invest-ment world are now accessible via a single security. In particular with the re-cent launch of the iShares Barclays Capital Emerging Markets Local Government Bond ETF, one can gain access to the eight largest and most liquid emerging market local government bond markets. This ETF directly invests in the physical bonds, and aims to track the Barclays Capital Emerging Markets Local Currency Core Government Index. The index comprises approximately 100 fixed-rate local currency government bonds across eight countries and three regions.

while performing not too badly in their local currencies, did not perform very well in the second half of 2008 when converted into dollars. Since the beginning of 2009, all but one of the local currencies in the index have appreciated against the dollar.

Potential Currency AppreciationWhen looking at the fundamentals of emerging market countries compared to developed countries, there is potential for the emerging currencies to appreci-ate against the dollar. This is one of the benefits of the emerging market local currency bond market.

Firstly, most of the emerging market countries have a very strong balance sheet. Lower debt levels mean that a more flexible monetary policy can be applied in response to the global financial crisis. For many of the developed countries, with relatively high levels of debt, this is not so easily the case.

A second reason for emerging currencies to appreciate against the dollar is their higher purchasing power in dollars. As emerging countries grow in productivity, the purchasing power of the dollar in those countries is likely to decline, result-ing in an appreciation of their local currencies against the dollar.

A third reason for a potential currency appreciation lies in the favourable demo-graphics of emerging market countries. Working age adults are at a relatively high proportion and many young people are entering the workforce in the coming years. With a growing workforce and a growing number of consumers, emerging countries should achieve additional GDP growth.

Woe Betide InflationOne should of course not forget that currency appreciation or depreciation can – to some extent – be controlled by central banks. Some of the emerging coun-tries have already started in tackling high capital inflows. This can be done in various different ways. Brazil, at the time of writing, has increased its so-called IOF-tax on foreign investments of fixed income products to 6%, thus trying to prevent an increase in capital inflow which can appreciate the currency against the dollar. This is offset by a very high yield to maturity at currently 12.3% and an investor with a 1-year investment horizon will still earn a yield of around 6.3%. Indonesia is imposing capital gains and withholding tax of 20% and Poland has introduced a withholding tax of 10%. In controlling capital inflows all three countries are trying to combat inflation.

Historically inflation has been one of the major concerns for investors in the emerging market bond sector. In the past, hyper-inflation has had the capacity to destroy an economy and its ability to meet its debt repayments.

Excluding the periods where hyper-inflation was the order of the day, the level of the local exchange rate against the dollar appears to loosely mean-revert around the level of inflation. For active managers, the exact nature of this relationship

Attractive yieldsCompared to the yields in other fixed income areas, be it developed market government or investment-grade corporate bonds, the yields of the emerging markets local currency bonds seem very attractive. The only comparative yields in developed markets are those of high-yield bonds. On top of that, there is the potential of further economic growth in emerging markets which could lead to an increase in bond prices in local currency and to the currencies appreciating against the dollar. These factors combined make this a very attractive market as a conservative allocation to the ETF should provide enhanced returns and diversification within a portfolio.

Strong performance historicallyThe performance in emerging market local currency bonds has been quite high in recent years. While one may not expect the very high returns of the year 2009 of more than 21% in the future, the market seems still attractive. The returns will depend on two main factors: 1) the returns of bond prices in the local market and 2) the appreciation/depreciation of the local currency compared to the dol-lar.

With the flight to quality during the global financial crisis, the dollar appreci-ated significantly compared to most other currencies. The local currency bonds,

iShares Switzerland

Friend or Foe? The Impact of Inflation on Local Currency Emerging Market Bonds

What Makes This Product Attractive?

Figure 1 – Comparison of cumulative returns in USD and FX appreciation of the local currencies against the dollar

98 ETF Review ETF Review

is almost certainly a source of alpha, where one would look to exploit the lead/lag effect of the central bank’s rate setting policy. Whereas for a long-term buy and hold investor this propensity for the exchange rate to over- or undershoot means that this effect may cancel out.

The last decade has seen structural changes in both the macro economic poli-cies of the central banks and the stability of a number of the core countries con-tributing to the Barclays Capital index. This improved landscape is also evident in the strong GDP figures that have been a feature of the last few years. The case study that provides the best backdrop from which to understand the extent of the political and economic reform is Brazil.

When Luiz Inácio Lula da Silva was the leading candidate for the presidential election the markets were concerned about how Lula’s policies would impact Brazil’s economy. Having been seen as very left wing in his ideologies, the cur-rency very rapidly depreciated. Successfully winning the bid for presidency, Lula then had the challenge of winning over the confidence of the markets. He re-newed the agreement with the IMF and within two to three years Brazil’s poor reputation as a country which was unable to meet its debt obligations to one that was in budget surplus was restored.

Looking at the relationship between Brazil’s central bank target rate, the level of inflation and the USD/Brazilian Real exchange rate over the last ten years reveals the extent to which the Brazilian authorities have succeeded in their aims during the last decade. emerging countries should achieve additional GDP growth.

The start of the appreciation of the Real against the dollar was underway and Brazil was to end the decade as the poster child of the emerging markets sector.

It is this conversion from an economy with the historical threat of inflation get-ting out of control, to one based on orthodox policies and a sustainable central banking infrastructure that offers the most promise for a long-term investor in the iShares Barclays Capital Emerging Markets Local Government Bond ETF.

Main Drivers of ReturnsThe local currency emerging markets bond market behaves somewhat differ-ently from its USD-denominated counterpart. In this section, we highlight the main drivers of returns of the local currency bond market and where the risk factors lie.

Credit riskAccording to the study in “This time is different” by the economists Reinhard and Rogoff, governments have historically been slightly more likely to default on USD-denominated debt than on debt issued in their local currency. If a gov-ernment has difficulty repaying its local debt, it will, to some extent, be able to increase local tax and/or depreciate its currency such that it is easier to repay the

debt. For debt issued in dollars, this is not possible.

After the defaults of some of the emerging countries, there is now a growing trend in issuing more debt in local currencies rather than in USD. The percent-age of domestic debt as part of the overall debt issued has recently increased to around 80% . This leaves the countries less vulnerable to a sudden dollar appre-ciation, which can increase the cost of servicing its debt quite substantially. The servicing cost is foreseeable and can be much easier matched with debt issued in local currency.

To see this one simply needs to look at the different credit ratings that Stan-dard & Poor’s assigns to domestic and foreign debt of emerging countries. The domestic credit rating is either higher or the same as the foreign credit rating.

Interest rate risk

As the price of a bond is inversely correlated to changes in interest rates, we need to ask ourselves what drives the yield curve in emerging market coun-tries. Similarly to developed countries, interest rates change due to actual and perceived changes in inflation and monetary policy intervention. The central banks of emerging market countries will need to weigh the same factors as for developed countries when deciding whether to change the policy rate. These factors are economic growth, inflation and currency appreciation/depreciation. The difference is that growth and inflation rates are usually higher in emerging countries.

FX riskSimilar to changes in interest rates, the FX rates fluctuate due to actual and per-ceived changes in the values of economic growth and inflation. If the growth in a country is low, the currency tends to depreciate. A certain level of growth is seen as healthy, which means that the economy is getting stronger, which in turn leads to currency appreciation. With strong growth often comes high inflation, which is usually higher in emerging market countries than in the developed world. Therefore, a certain level of “acceptable” inflation can often be coupled with currency appreciation and not depreciation. If inflation gets too high on the other hand, a country is usually in trouble and the currency will depreciate. Infla-tion may spike quickly and is often coupled with a depreciation of the currency. One can observe that in general the rate of currency appreciation/depreciation is mean-reverting around the inflation rate.

The FX rate is also affected by interest rate changes. If the interest rate in a coun-try rises, more investors will move their money into bonds in that country to benefit from the higher rates. This leads to currency appreciation and vice versa. The expectation of a future interest rate hike can therefore drive changes in ex-change rates.

iShares Switzerland

Friend or Foe? The Impact of Inflation on Local Currency Emerging Market Bonds

Figure 2 - Brazilian central bank target rate compared with CPI and the USD-BRL exchange rate

Table 2 - Domestic and foreign country credit ratings

1110 ETF Review ETF Review

This is a shortened version of the original paper that can be found at www.iS-hares.ch. To read the entire paper “Friend or Foe? – The Impact of Inflation on Local Currency Emerging Markets Bonds” contact your iShares Switzerland team (0800 33 66 88), email [email protected] or visit www.iShares.ch.

Regulatory Information: BlackRock Advisors (UK) Limited, which is authorised and regulated by the Financial Services Authority (‘FSA’), has issued this docu-ment for access in Switzerland only and no other person should rely upon the information contained within it. iShares plc, iShares II plc and iShares III plc (to-gether ‘the Companies’) are open-ended investment companies with variable capital having segregated liability between their funds organised under the laws of Ireland and authorised by the Financial Regulator.

For investors in Switzerland: This document is directed at ‘qualified investors’ only, as defined by Clause 10 (3) of the Swiss Act on Collective Investment Schemes (‘CISA’) and Clause 6 of the Swiss Ordinance on Collective Investment Schemes (‘CISO’). Certain of the funds are not registered with the Swiss Financial Supervisory Authority FINMA which acts as supervisory authority in investment fund matters. In respect of these funds, the shares or units of these funds may not be offered or distributed in or from Switzerland unless they are placed with-out ‘public solicitation’ as such term is defined under the practice of the FINMA from time to time. With respect to those funds that are registered, the FINMA has authorised BlackRock Asset Management Schweiz AG, Claridenstrasse 25, 8002 Zurich, to act as Swiss Representative and JPMorgan Chase Bank, National As-sociation, Columbus, Zurich branch, Dreikönigstrasse 21, 8002 Zurich, to act as Swiss Paying Agent of the Companies. The prospectus, complete and simplified, the Articles of Incorporation, the latest and any previous annual and semi-annu-al reports of the Companies as well as a list of purchases and sales undertaken on behalf of the Companies are available free of charge from the Swiss repre-sentative. Before investing please read the prospectus, complete and simplified, copies of which can be obtained from the Swiss representative.

Restricted Investors: This document is not, and under no circumstances is to be construed as, an advertisement, or any other step in furtherance of a public of-fering of shares in the United States or Canada. This document is not aimed at persons who are resident in the United States, Canada or any province or terri-tory thereof, where the Companies are not authorised or registered for distribu-tion and where no prospectus for the Companies has been filed with any securi-ties commission or regulatory authority. The Companies may not be acquired or owned by, or acquired with the assets of, an ERISA Plan.

Risk Warnings: Shares in the Companies may or may not be suitable for all inves-tors. BlackRock Advisors (UK) Limited does not guarantee the performance of the shares or funds. The price of the investments (which may trade in limited markets) may go up or down and the investor may not get back the amount invested. Your income is not fixed and may fluctuate. Past performance is not a reliable indicator of future results. The value of the investment involving expo-sure to foreign currencies can be affected by exchange rate movements. We re-mind you that the levels and bases of, and reliefs from, taxation can change. Af-filiated companies of BlackRock Advisors (UK) Limited may make markets in the securities mentioned in this document. Further, BlackRock Advisors (UK) Limited and/or its affiliated companies and/or their employees from time to time may hold shares or holdings in the underlying shares of, or options on, any security included in this document and may as principal or agent buy or sell securities.

Index Disclaimers: Barclays Capital’ is a trade mark of Barclays Capital, the invest-ment banking division of Barclays Bank PLC (‘Barclays Capital’), and is used by BlackRock Advisors (UK) Limited under licence. With a distinctive business mod-el, Barclays Capital provides corporates, financial institutions, governments and supranational organisations with solutions to their financing and risk manage-ment needs. Barclays Capital compiles, maintains and owns rights in and to the iShares Barclays Capital Emerging Markets Local Govt Bond (the ‘index’). iShares Barclays Capital Emerging Markets Local Govt Bond (‘the fund’) is not sponsored, endorsed, sold or promoted by Barclays Capital and Barclays Capital makes no representation regarding the advisability of investing in the funds.iShares is a registered trademark of BlackRock Institutional Trust Company, N.A. All other trademarks, servicemarks or registered trademarks are the property of their respective owners. © 2011 BlackRock Advisors (UK) Limited. Registered Company No. 00796793. All rights reserved. Calls may be monitored or recorded.

iShares Switzerland

Friend or Foe? The Impact of Inflation on Local Currency Emerging Market Bonds

iShares Switzerland

Dr Andreas [email protected]+4144 2977340

Mathieu [email protected]+41 44 297 73 44

1110 ETF Review ETF Review

In view of ongoing debt problems, precious metals are attracting increasing investor attention. Index products such as ETFs not only offer low-cost and ef-ficient access to this asset class but can also help to improve portfolio diversifi-cation

The confidence of many investors in the stability of the global financial system has been shattered. The period of recovery from the crisis that shook the finan-cial world in 2008 proved to be short-lived. The subprime crisis that emanated from the US has been succeeded over the past two years by the debt problems experienced by a number of European countries. The debt crisis has left most major financial markets in turmoil. Share prices fell and bond yields for many eu-rozone countries skyrocketed as currencies perceived as safe havens – the Swiss franc and the Japanese yen, for example – appreciated so much in value that central banks saw themselves forced to intervene. And all the while the gold price hit a series of record highs in rapid succession. This is not the only reason why precious metal investments have started to play a key role for institutional investors and the public sector too. According to the World Gold Council (WGC), for example, central banks’ demand for gold reached just short of 150 tonnes in the third quarter of 2011 alone. During the preceding decades they had tended largely to act as net sellers of it.

That precious metals are currently in such high demand is evidence of the fact that the twofold crisis of recent years has marked a sea change. The investment world has undergone a transformation – although the major catastrophe that had been predicted by a number of forecasters did not materialize. This has to do as much with the crises themselves as with the measures chosen by cen-tral banks and policymakers in order to deal with them. Rather than opting for debt reduction on a grand scale, they shifted debt mainly from the private to the public sector – this pushed the sustainability of national budgets to the limit, and, in some cases, over it. The US Fed’s innovative response to the crisis and to persistent weak economic growth included buying up government bonds and expanding its balance sheet to an unprecedented extent; the European Central Bank is increasingly having recourse to similar measures.

This scenario is favorable to investment in precious metals, and for a variety of reasons. For one, the overall low level of interest rates in connection with cen-tral bank bond purchases in many cases results in negative real interest rates on investments perceived as default-free, such as government bonds issued by the US or Germany. The opportunity cost of investing in precious metals has fallen to a lower level than has been seen in years. For another, a number of factors indicate that the strong money supply expansion could lead to higher inflation in the medium to long term. It is inevitable that investors will turn to precious metals and other commodities for protection against unexpected rises in infla-tion. Gold in particular, having a real value, lends itself to use as a hedge against inflation. With the right type of investment, physical gold, thanks to its low corre-lation with other asset classes, offers diversification benefits and can potentially improve the risk/return profile of portfolios.

The price of gold tends for the most part to move independently of stock prices. For that reason, it has continued to shine even during the most recent stock market turmoil. While many major stock indices plummeted within the span of a few days and the value of the US dollar fell against other currencies, the price of gold has soared from one record high to the next.

This shows that precious metals such as gold can help to enrich and stabilize a portfolio. The World Gold Council arrived at the same conclusion in a study covering the period from December 1987 to July 2010. In 18 out of 24 crises and extreme events analyzed, i.e. in 75 percent of the cases, portfolios that included gold outperformed those that did not.

Even more than other investors, however, institutional investors are faced with the question of how to make a commodity investment as cost-efficient and effective as possible. Physical precious metals provide a high level of security without any counterparty risk but at the same time also present major problems – for instance, in terms of safekeeping and tradability, as well as trade currency. Moreover, the purchase of physical precious metals such as silver or platinum is subject to value-added tax in many countries. In addition, laws and regulations prohibit many organizations from directly buying physical precious metals.

There are various investment instruments available to institutional investors that offer them the opportunity to invest in precious metals, thus enabling them to improve their risk/return profile while providing them with access to this attrac-tive asset class. The available instruments will differ substantially, however, de-pending on whether a given precious metal investment is implemented using futures, structured products (certificates), physically backed ETCs or ETFs.

Futures: liquid but complexFutures have the advantage of being liquidly tradable. As their maturity is lim-ited, however, expiring contracts must be regularly replaced by contracts with longer maturities. This complicates an investment. On the one hand, this fea-ture of futures markets offers investors the opportunity not only to participate in spot price increases but also to additionally earn a positive roll return if longer term contracts are cheaper than expiring ones (backwardation); on the other, there is the risk of roll loss if the situation is the other way around and the futures are trading in contango. The problem of rolls means also that precious metal in-vestments using futures may not correlate exactly with the spot price. Changes in the futures curve are difficult to predict. Moreover, in order to carry out futures transactions investors must first open a margin account with a bank. For these reasons, investors interested in participating as fully as possible in the spot price appreciation of gold, silver, platinum or palladium should consider other invest-ment options.

Structured products: a wide range of in-vestments, but with issuer riskInvestment certificates are one such option. A wide range of structured prod-ucts allow investors to participate in the spot price performance and also in the performance of precious metal futures, as well as in diversified precious metal and commodity indices. Certificates offer a wide variety of opportunities in this respect. However, as they are – as a rule unsecured – bearer bonds, they always entail an issuer risk.

Exchange-traded commodities (ETCs) are meant to offer a way out of this di-lemma. These exchange-traded products allow investors to participate in the performance of individual commodities exactly as they would using certificates. ETCs track the performance either of the spot price or of futures. They are, as a

UBS

Index Investments that Shine

Risk spreading: Gold exhibits only a low correlation with most standard asset classes

-0.3 -0.2 -0.1 0 0.1 0.2 0.3 0.4

D J Industrial A verag e

S&P 500

CA C40

D A X 30

FTSE 100

SMI

Barclays G lobal TreasuryIndex

Barclays US Credit Index

1312 ETF Review ETF Review

rule, secured or unsecured debt securities issued by a bank, with government bonds or physical precious metals serving as collateral, depending on the prod-uct version. Collateral is used to mitigate the default risk associated with debt securities in the event of issuer bankruptcy. Investors are well advised to pay particular attention to the type of collateral used.

ETFs: the best of both worldsExchange-traded funds (ETFs) offer even greater security. They combine various advantages of the investment opportunities mentioned above. As ETFs repre-sent special assets, they meet stringent regulatory requirements and provide investors with a particularly high level of security. They are approved by at least one regulatory agency. There is absolutely no issuer risk. ETFs on precious met-als invest in them almost exclusively in physical form. ETF investors accordingly participate in the precious metal spot price performance. As a rule, the precious metal bars are physically segregated and stored in a designated high-security vault in Switzerland. Hence, there is no risk of theft, and custody and insurance costs can be kept low. For ETFs on precious metals domiciled in Switzerland, a number of providers offer an in-kind redemption option in Switzerland – that is, the delivery of physical precious metals in exchange for ETF units. This is an addi-tional option available to investors for a fee – alongside selling their units on the stock exchange – should they wish to take it upon themselves to sell their ETF units. However, physical delivery is recommended in extreme situations only. Most providers forego the use of gold derivatives and invest exclusively in physi-cally held gold.

To meet the special needs of institutional and high-net-worth private clients, a number of providers offer special unit classes for this investor group in your precious metal ETFs.

In addition, currency-hedged versions are also available. By investing in a unit class that features currency hedging, you can eliminate the exchange rate risk of the US dollar – the currency in which gold is traded – versus the Swiss franc or euro. This is not possible when investing in purely physical precious metals. Clients with the EUR as their base currency gain an advantage from currency hedging when the USD is weaker -> the hedged unit class is the better invest-ment choice. In an environment with a strong USD, currency hedging results in a loss -> EUR unit class (without currency hedging) or USD unit class is the better choice.These ETFs in fact combine the advantages of physical investments and securi-ties: They are as secure as genuine precious metals and may be traded as flex-ibly as equities. They may be traded in multiple trading currencies on SIX Swiss Exchange. Multiple market makers provide good intraday liquidity.

In view of the ongoing debt problems, the addition of gold, silver, platinum or palladium should prove to be a sensible approach for many investors – because precious metals can significantly improve a portfolio’s risk/return profile owing to their favorable correlation properties. Thanks to their easy tradability and transparency, as well as the possibility of currency hedging, exchange-traded in-dex products, in particular ETFs on precious metals, provide a good opportunity to participate in the performance of precious metals and to incorporate them into the asset allocation mix.

UBS

Index Investments that Shine

Clemens Reuter

Tel: +41-44-234 75 [email protected]

1312 ETF Review ETF Review

The new passive investing Index strategies that deliver passive market exposure – or beta – have long at-tracted investors. In response to the systematic rise in volatility across global asset classes, along with weaknesses of market capitalisation indices, a growing number of investors are now exploring new passive approaches.

Often called “enhanced beta” or “smart beta” strategies, this innovative indexing is helping investors address today’s need to build more resilient portfolios. Smart beta indices harness the power of technology to deliver repeatable sources of returns that are often based on well-established investment theory. The devel-opment of new approaches has led to new betas which even replicate strategies employed by active managers. Investors can often benefit from implementing these strategies at significantly lower costs, reduced governance requirements, high levels of transparency and liquidity, and an improved efficiency of their risk budget.

Ossiam, a research-led asset management firm based in Paris, specialises in delivering enhanced beta solutions notably through ETF, including minimum variance and equal weight strategies. Ossiam recently listed the first Minimum Variance ETF on the Swiss Stock Exchange. This offering is designed to reduce portfolio volatility and minimise drawdowns while generating performance above the market capitalisation index over the economic cycle.

“A natural question investors ask is: is it possible to maintain a full exposure to the equity market while mitigating its risk? The approach initiated by Ossiam’s research and investment management team intends to obtain an optimized portfolio that includes a selection of stocks where volatility is among the lowest in the investment universe, and historical correlations are moderate enough to allow for risk reduction.” says Isabelle Bourcier, director of development at Os-siam. “Empirical studies show that low volatility stocks have had very attractive performance.” Bourcier also points out the enhanced beta attributes of equally weighted strategies. “The concept aims to provide investors with a more diversi-fied exposure to a given stock market, avoiding the dominance of a small group of stocks.”

Ossiam’s research team has written a number of research papers on enhanced beta topics which can be found on www.ossiam.com

Below we have included a brief summary of their minimum variance piece: Max-imising risk efficiency with a minimum variance approach market that serves offshore corporates for trade settlements. By design and through regulation, all these markets trade separately from each other.

Maximising risk efficiency with a mini-mum variance approach Quote: “A properly designed minimum variance investment approach can be rel-evant for investors seeking risk-efficient passive equity allocation.” Ksenya Rulik, PhD, Ossiam’s head of Quantitative Research

Since Harry Markowitz’s seminal work in 1952, the investment community has embraced the concept of an optimal portfolio. While simple in its objective, building an optimal portfolio is a daunting task requiring implicit or explicit as-sumptions about future risk and returns. As a consequence, the resulting alloca-tion remains optimal on an ex-ante basis whilst its ex-post performance may be compromised by forecasting errors.

The Capital Asset Pricing Model (CAPM) brought an elegant solution to the op-timisation problem in the 1960s arguing that the most efficient portfolio is a broad market portfolio using mean-variance optimisation with market-implied forecasts of risk and returns. This idea gained enormous influence and reshaped equity investing over the past 35 years.

The mean-variance framework suggests another definition of passive equity in-vesting: an investment process aimed at providing access to the equity market or one of its segments that does not require return forecasts for the stocks inside the chosen universe. The objective of a “new passive” approach is to shape the portfolio in such a way that the equity exposure gives the best possible risk-adjusted performance.

Mathematically, the Minimum Variance Portfolio is an optimal portfolio con-structed by minimising portfolio variance. The only input that is used by the minimum variance construction is the covariance matrix of the stocks, which generally is estimated on the historical data. Once the covariance matrix is built, various constraints allow the technique to incorporate ex-ante risk management features in the portfolio (e.g., limiting exposure to single names at 4.5%) and specific investor requirements (e.g., long only). Minimum variance strategies are largely shaped by the constraints used in the optimisation, and the right balance should be found between volatility reduction and portfolio diversification.

Overall, we believe that a well-designed minimum variance investment ap-proach can be relevant for investors seeking risk-efficient passive equity alloca-tion.

Ossiam investment line-up Ossiam offers the following range of specialty ETFs. • OSSIAM ETF iSTOXX™ EUROPE MINIMUM VARIANCE Reference investment universe: STOXX® Europe 600 • OSSIAM ETF US MINIMUM VARIANCE NR Reference investment universe: S&P 500 • OSSIAM ETF EURO STOXX 50® EQUAL WEIGHT NR • OSSIAM ETF STOXX® EUROPE 600 EQUAL WEIGHT NR

Ossiam Research Analysts

Further information including the fund prospectus can be downloaded from www.ossiam.com.

Natixis

Focus on Enhanced Beta Strategies

Natixis Global Asset Management Switzerland Ksenya Rulik, Bruno Monnier Ossiam Research Analysts

1514 ETF Review ETF Review

The fund’s representative and paying agent in Switzerland is RBC Dexia Inves-tor Services Bank S.A., Zurich Branch, Badenerstrasse 567, 8048 Zurich. The full prospectus, the Key Investor Information, and the annual / semi-annual reports of Ossiam Lux, a Luxembourg-domiciled SICAV, can be obtained free of charge from the Representative together with the initial articles of association of the fund and any subsequent changes to such articles.

Investments decision should only be made on the basis of the above mentioned documents. Past performance is no guarantee for future returns and does not take into consideration any commissions charged for purchase, redemption or conversion of shares.

The iStoxx Europe Minimum Variance Index is an index initiated by Ossiam and calculated and maintained by STOXX.

“The STOXX® Indices and the data comprised therein (the “Index Data”) are the intellectual property (including registered trademarks) of STOXX Limited, Zurich, Switzerland (“STOXX”) and/or its licensors (the “STOXX Licensors”). The use of the Index Data requires a license from STOXX. STOXX and the STOXX Licensors do not make any warranties or representations, express or implied with respect to the timeliness, sequency, accuracy, completness, currentness, merchantability, quality or fitness for any particular purpose of the Index Data. In particular, the inclusion of a company in a STOXX® Index does not in any way reflect an opinion of STOXX or the STOXX Licensors on the merits of that company. STOXX and the STOXX Licensors are not providing investment, tax or other professional advice through the publication of the STOXX® Indices or in connection therewith.

Ossiam US Minimum Variance Nr Index is the exclusive property of Ossiam, which has contracted with Standard & Poor’s Financial Services LLC (“S&P”) to maintain and calculate the Index. Standard & Poor’s® and S&P® are registered trademarks of Standard & Poor’s Financial Services LLC “Calculated by S&P Cus-tom Indices” and its related stylized mark(s) are service marks of Standard & Poor’s Financial Services LLC and have been licensed for use by Ossiam. S&P and its affiliates shall have no liability for any errors or omissions in calculating the Index. The Ossiam ETF US Minimum Variance based on the Ossiam US Minimum Variance NR Index is in no way sponsored, endorsed, sold or promoted by S&P.

About Ossiam

Ossiam is an affiliate of Natixis Global Asset Management. Headquartered in Paris, France, Ossiam is the first ETF company in Europe to offer access to multi-ple financial asset classes via a diverse range of specialty ETFs and funds, based on quantitative and fundamental analysis. Its team has extensive experience in fund management, ETF structuring, fundamental and quantitative research and trading.

www.ossiam.com

About Natixis Global Asset Management

Natixis Global Asset Management is one of the 15 largest asset managers in the world based on assets under management. Its affiliated asset management companies provide investment products that seek to enhance and protect the wealth and retirement assets of both institutional and individual investor cli-ents. Its proprietary distribution network helps package and deliver its affiliates’ products around the world. Natixis Global Asset Management brings together the expertise of multiple specialized investment managers based in Europe, the United States and Asia to offer a wide spectrum of equity, fixed-income and al-ternative investment strategies.

Headquartered in Paris and Boston, Natixis Global Asset Management’s assets under management were €525 billion as of September 30, 2011.

Natixis Global Asset Management is part of Natixis. Listed on the Paris Stock Exchange, Natixis is a subsidiary of BPCE, the second-largest banking group

in France. Natixis Global Asset Management’s affiliated investment manage-ment firms and distribution and service groups include: Absolute Asia Asset Management; AEW Capital Management; AEW Europe; AlphaSimplex Group; Aurora Investment Management; Capital Growth Management; Caspian Capital Management; Darius Capital Partners; Gateway Investment Advisers; H2O As-set Management; Hansberger Global Investors; Harris Associates; Loomis, Sayles & Company; Natixis Asset Management; Natixis Multimanager; Ossiam; Reich & Tang Asset Management; Snyder Capital Management; and Vaughan Nelson In-vestment Management.

Natixis Global Asset Management also includes business development units located across the globe, including NGAM S.A., a Luxembourg management company that is authorized by the CSSF, and a distribution office in Switzerland (NGAM, Switzerland Sàrl). http://ngam.natixis.com

Natixis

Focus on Enhanced Beta Strategies

Natixis Global Asset Management Switzerland

[email protected] 022 817 80 20

1514 ETF Review ETF Review

Exchange traded funds (ETFs) have found themselves under ever more scrutiny from regulators and market participants this year and expectations are that new rules for the sector are just a matter of time.

It’s tempting to think of ETFs as unwilling victims of new regulation, but to my mind, ETFs have much to gain.

The point is that it isn’t just regulators who are seeking improved transparency on fund holdings and on the use of derivatives by mutual funds, crucially it is end-investors too. And once the fog has cleared, they might come to see ETFs — with daily published portfolios and clearer statements on the use of derivatives in general — as a role model for all kinds of mutual funds.

The discussion surrounding ETFs could leave you with the feeling that they are unregulated products; that fund promoters can go wild when creating new products and with the use of derivatives in the portfolios. In reality though, ETFs follow the same local and/or international legislation of any other mutual fund; the EU UCITS regime for example.

So, why all the fuss around ETFs? In my opinion, there is nothing uniquely wrong with these products as they are using the same tools and techniques used by other funds under the UCITS regime. Some authorities, however, have raised questions as ETFs grow in popularity among professional investors. A deeper look into the questions posed shows that the points made by the critics are not only applicable to ETFs, but to any mutual fund.

ConcernI wonder if the popularity of ETFs, which have sold well in tough market condi-tions, has made them a useful conduit to raise more general concerns about the mutual fund industry as a whole.

Of course, some of the concerns mentioned by market authorities are reason-able points to make, but they apply far more broadly; derivatives in general and swaps in particular are nothing new, and alongside stock lending, are widely used within the asset management industry.