Embed Size (px)

Citation preview

ESTUDIOS MONETARIOS Y FINANCIEROS

THE IMPACT OF FINANCIAL VARIABLES ON FIRMS’ REAL DECISIONS: EVIDENCE FROM SPANISH FIRM-LEVEL DATA

Ignacio Hernando

Carmen Martínez-Carrascal

WORKSHOP ON CORPORATE FINANCE AND MONETARY POLICY

15-16 May 2006

2ESTUDIOS MONETARIOS Y FINANCIEROS

INTRODUCTION

Financial position of the corporate sector may influence the performance of the real economy and the stability of the financial system

In its turn, the financial position of the corporate sector is relevant to determine the magnitude of the effects of monetary policy shocks

Adjustment by companies as a result of monetary policy shift can potentially involve a wide range of activities, but their response might depend on the degree of financial pressure they face

Distribution of financial position matters. Financial fragility of certain firms are not offset by soundness of others. The effect of aggregate financial indicators on business activity in estimates at macro level has been elusive.

Aim of this paper: describing aspects of the financial situation of the corporate sector in Spain and analyzing how companies adjust investment and employment to variations in financial pressure

3ESTUDIOS MONETARIOS Y FINANCIEROS

KEY ISSUES OF THE PAPER

I. Overall picture of the financial position of Spanish non-financial firms- Substantial cross-sectional dispersion in terms of the degree of financial tightness

II. The impact of financial position on business activity. - Financial position, proxied by alternative financial variables, matters for business activity

III. Shape of the relationship- The impact is non-linear and becomes more intense when financial pressure exceeds a certain threshold

IV. Construction of composite indicators for the impact of corporate financial health on real decisions- Indicators based on aggregate data may not be reliable enough to capture the impact of corporate financial health on real decisions

4ESTUDIOS MONETARIOS Y FINANCIEROS

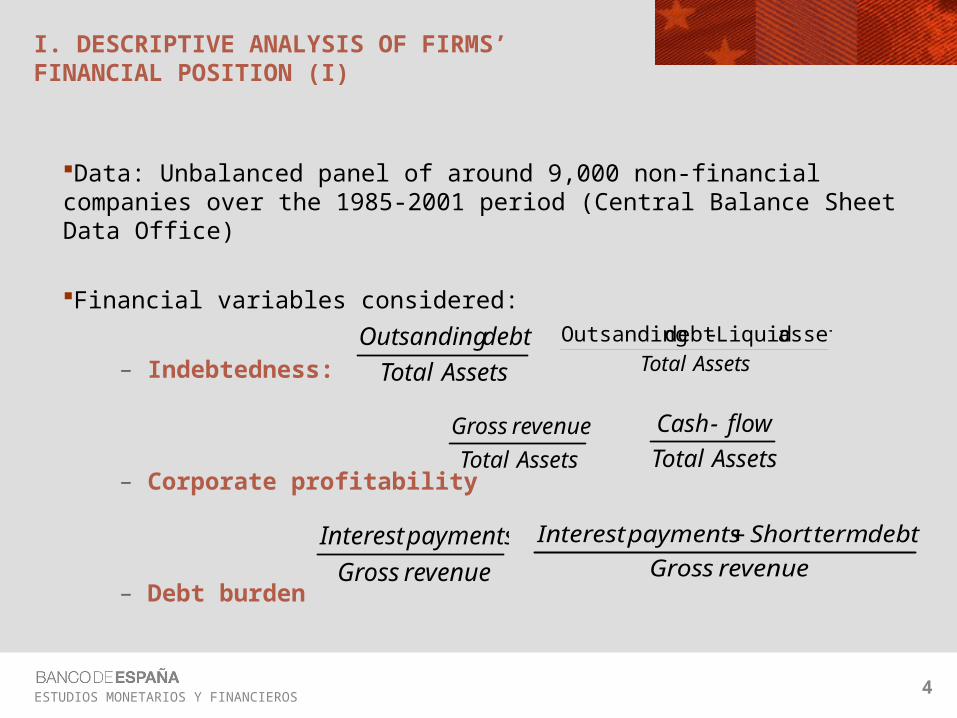

I. DESCRIPTIVE ANALYSIS OF FIRMS’ FINANCIAL POSITION (I)

Data: Unbalanced panel of around 9,000 non-financial companies over the 1985-2001 period (Central Balance Sheet Data Office)

Financial variables considered:

– Indebtedness:

– Corporate profitability

– Debt burden

AssetsTotal

assetsLiquid-debtOutsanding

AssetsTotal

revenueGross

revenueGross

debttermShortpaymentsInterest

AssetsTotal

debtOutsanding

AssetsTotal

flow-Cash

revenueGross

paymentsInterest

5ESTUDIOS MONETARIOS Y FINANCIEROS

I. DESCRIPTIVE ANALYSIS OF FIRMS’ FINANCIAL POSITION (II)

0

15

30

45

60

85 87 89 91 93 95 97 99 01

p25 p50 p75

DEBT / TOTAL ASSETS

%

0

10

20

30

40

85 87 89 91 93 95 97 99 01

p25 p50 p75

GROSS REVENUE / TOTAL ASSETS

%

Substantial cross-sectional variation in the distribution of Spanish firms for indebtedness, profitability and debt burden indicators

0

5

10

15

20

25

85 87 89 91 93 95 97 99 01

p25 p50 p75CASH FLOW / TOTAL ASSETS

%

-15

0

15

30

45

60

85 87 89 91 93 95 97 99 01

p25 p50 p75

NET DEBT / TOTAL ASSETS

%

6ESTUDIOS MONETARIOS Y FINANCIEROS

I. DESCRIPTIVE ANALYSIS OF FIRMS’ FINANCIAL POSITION (III)

0

15

30

45

60

75

85 87 89 91 93 95 97 99 01

p25 p50 p75

INTEREST DEBT BURDEN

%

0

100

200

300

400

85 87 89 91 93 95 97 99 01

p25 p50 p75TOTAL DEBT BURDEN

%

7ESTUDIOS MONETARIOS Y FINANCIEROS

KEY ISSUES OF THE PAPER

I. Overall picture of the financial position of Spanish non-financial companies. Cross-sectional dispersion

II. The impact of financial position on business activity. Relative importance of alternative financial variables

III. This impact is non-linear and becomes more intense when financial pressure exceeds a certain threshold

IV. Construction of composite indicators for the impact of corporate financial health on real decisions

8ESTUDIOS MONETARIOS Y FINANCIEROS

II. THE IMPACT OF FINANCIAL POSITION ON INVESTMENT AND EMPLOYMENT DECISIONS

Estimation method: System- GMM

tittitititi

itii

ti

XykyyK

I

K

I,

',2,41,3,2

1,1

,

)(****

tittitititititiiti Xwwknn ,',,5,41,3,21,1, ****

9ESTUDIOS MONETARIOS Y FINANCIEROS

II. THE IMPACT OF FINANCIAL POSITION ON INVESTMENT AND EMPLOYMENT DECISIONS. EMPIRICAL RESULTS

When included one at a time, all financial indicators are significant

When simultaneously included, the indicators of debt-service burden are those that display a more robust effect

Preferred specifications:

– Investment: total debt burden, gross revenue over total assets and net debt over total assets

– Employment: total debt burden and gross revenue over total assets

10ESTUDIOS MONETARIOS Y FINANCIEROS

KEY ISSUES OF THE PAPER

I. Overall picture of the financial position of Spanish non-financial companies. Cross-sectional dispersion

II. The impact of financial position on business activity. Relative importance of alternative financial variables

III. This impact is non-linear and becomes more intense when financial pressure exceeds a certain threshold

IV. Construction of composite indicators for the impact of corporate financial health on real decisions

11ESTUDIOS MONETARIOS Y FINANCIEROS

III. a. NON-LINEAR LINK BETWEEN FINANCIAL POSITION AND INVESTMENT. DESCRIPTIVE EVIDENCE

5

10

15

20

25

30

35

86 89 92 95 98 01

High br Med br Low br INVESTMENT RATE - INTEREST DEBT BURDEN

%

0

5

10

15

20

25

30

35

86 89 92 95 98 01

High tdb Med tdb Low tdb

INVESTMENT RATE - TOTAL DEBT BURDEN

%

12ESTUDIOS MONETARIOS Y FINANCIEROS

III. b. NON-LINEAR LINK BETWEEN FINANCIAL POSITION AND EMPLOYMENT. DESCRIPTIVE EVIDENCE

-12

-8

-4

0

4

8

12

86 89 92 95 98 01

High br Med br

Low br

EMPLOYMENT GROWTH - INTEREST DEBT BURDEN

%

-12

-8

-4

0

4

8

12

86 89 92 95 98 01

High tdb Med tdb Low tdb

EMPLOYMENT GROWTH - TOTAL DEBT BURDEN

%

13ESTUDIOS MONETARIOS Y FINANCIEROS

III. c. NON-LINEAR LINK BETWEEN FINANCIAL POSITION AND INVESTMENT. EMPIRICAL RESULTS

titF

tiF

tiF

ti

tititi

itii

ti

DFDFDF

ykyyK

I

K

I

,100901,390751,27501,1

2,41,3,21,

1,

)(****

Degree of financial Debt burdenpressure

B/A (B-m)/A br tdb GR/A CF/A

LOW 0.072 -0.061 -0.081 -0.007 0.202 0.331

MODERATE -0.013 -0.147 -0.100 -0.005 0.662 3.470

HIGH -0.052 -0.127 -0.031 -0.004 0.658 0.890

Non-linear effects of financial variables on investment

Indebtedness Profitability

14ESTUDIOS MONETARIOS Y FINANCIEROS

KEY ISSUES OF THE PAPER

I. Overall picture of the financial position of Spanish non-financial companies. Cross-sectional dispersion

II. The impact of financial position on business activity. Relative importance of alternative financial variables

III. This impact is non-linear and becomes more intense when financial pressure exceeds a certain threshold

IV. Construction of composite indicators for the impact of corporate financial health on real decisions

15ESTUDIOS MONETARIOS Y FINANCIEROS

IV. COMPOSITE INDICATOR OF THE IMPACT OF FINANCIAL CONDITIONS ON INVESTMENT AND EMPLOYMENT

This indicator must take into account the following elements:–Cross-sectional dispersion in firms’ financial position–Differences across firms in the sensitivity of their real decisions to their financial position–Relative weight of each firm for the evolution of aggregate investment

Our preferred non-linear specifications include:– total debt-burden, net debt and gross revenue (investment)– total debt-burden and gross revenue (employment)

kti

k

kti XFCII ,, ˆ k

tik

kti XFCIE ,, ˆ

16ESTUDIOS MONETARIOS Y FINANCIEROS

IV. COMPOSITE INDICATOR OF THE IMPACT OF FINANCIAL CONDITIONS ON INVESTMENT

Figure 4COMPOSITE INDICATORS OF THE IMPACT OF FINANCIAL CONDITIONS ON

INVESTMENT

Median Weighted average 90th

50

100

150

200

250

300

85 87 89 91 93 95 97 99 01

50

100

150

200

250

300250

400

550

700

250

400

550

700

50100150200250300

85 87 89 91 93 95 97 99 01

50100150200250300

100300500700900

1,100

1003005007009001,100

17ESTUDIOS MONETARIOS Y FINANCIEROS

IV. COMPOSITE INDICATOR OF THE IMPACT OF FINANCIAL CONDITIONS ON EMPLOYMENT

Figure 4

COMPOSITE INDICATOR OF THE IMPACT OF FINANCIAL CONDITIONS ON EMPLOYMENT

Median Weighted average 90th

50

100

150

200

250

300

85 87 89 91 93 95 97 99 01

50

100

150

200

250

300

150

400

650

900

1,150

150

400

650

900

1,150

50100150200250300

85 87 89 91 93 95 97 99 01

50100150200250300

100300500700900

1,100

1003005007009001,100

18ESTUDIOS MONETARIOS Y FINANCIEROS

V. USES OF COMPOSITE INDICATORS OF THE IMPACT OF FINANCIAL CONDITIONS ON EMPLOYMENT AND INVESTMENT (I)

Regularly analyzed to assess investment prospects

–Updated using CBSO (annual and quarterly) data •Annual CBSO data: available with an approximate lag of 1 year.

Quarterly CBSO data: available with a lag of 1 quarter

•The annual database contains approximately 8000 firms per year. The quarterly database contains on average 900 firms per quarter•Large companies have a predominant weight

19ESTUDIOS MONETARIOS Y FINANCIEROS

V. USES OF COMPOSITE INDICATORS OF THE IMPACT OF FINANCIAL CONDITIONS ON EMPLOYMENT AND INVESTMENT (I)

Regularly analyzed to assess investment prospects

-200

-100

0

100

200

300

400

500

90 92 94 96 98 00 02 04 I II 2005

III IV

COMPOSITE INDICATOR OF FINANCIAL PRESSURE ON INVESTMENT

1990=100

-350

-200

-50

100

250

91 93 95 97 99 01 03 05

CONTRIBUTION OF INDEBTEDNESS

CONTRIBUTION OF DEBT-SERVICE BURDEN

CONTRIBUTION OF PROFITABILITY

TOTAL CHANGE IN THE INDICATOR

CHANGE IN COMPOSITE INDICATOR OF FINANCIAL PRESSURE ON INVESTMENT AND CONTRIBUTION OF ITS COMPONENTS

20ESTUDIOS MONETARIOS Y FINANCIEROS

V. USES OF COMPOSITE INDICATORS OF THE IMPACT OF FINANCIAL CONDITIONS ON EMPLOYMENT AND INVESTMENT (II)

-10

-5

0

5

10

15

20

95 96 97 98 99 00 01 02 03

Y

USER COST

CF

NON-EXPLAINED

INVESTMENT GROWTH RATE

QUARTERLY MODEL

%

Explanatory power to explain aggregate productive investment growth rate, using the quarterly macroeconometric model of the Spanish economyThe introduction of composite indicator results in a reduction of the non-explained component. The contribution of the rest of the variables remains broadly unchanged

-10

-5

0

5

10

15

95 96 97 98 99 00 01 02 03

Y

USER COSTCF

NON-EXPLAINEDC.INDICATOR

INVESTMENT GROWTH RATE

QUARTERLI MODEL, REESTIMATED INCLUDING COMPOSITE INDICATOR

%

21ESTUDIOS MONETARIOS Y FINANCIEROS

KEY FINDINGS

Substantial cross-sectional dispersion in terms of the degree of financial tightness

Financial position matters for business activity

This link is non-linear and becomes more intense when financial pressure exceeds a certain threshold

Indicators based on aggregate data are not reliable enough to capture the impact of corporate financial health on real decisions

ESTUDIOS MONETARIOS Y FINANCIEROS

THANK YOU FOR YOUR ATTENTION