Embed Size (px)

Citation preview

Estimating Real and Nominal Term Structuresusing Treasury Yields, Inflation,

Inflation Forecasts, and Inflation Swap Rates

by J. Haubrich, G. Pennacchi, and P. Ritchken

Discussed byMikhail Chernov, London Business School and CEPR

1/ 16

Outline

What does the paper do?

→ Questions

→ Motivation

→ Results

Why are inflation swaps important?

→ “Online” decision making

→ Inflation swaps vs TIPS

→ Model estimation

→ Uncovering the role of volatility

Concluding remarks

2 / 16

Questions

What is a realistic no-arbitrage joint model of real and nominalU.S. yield curves?

Notable features of the approach:

→ GARCH volatility

→ Use of inflation swap data

What is the role of the various data sources in the modelestimation?

What is the behavior of the real term premium?

What is the behavior of the inflation risk premium?

3/ 16

Motivation

There are a lot of studies focusing on no-arbitrage models of thenominal/real yield curve using some combination of nominalTreasuries, inflation rate and inflation survey forecasts

Few studies use TIPS

→ D’Amico, Kim, and Wei (2007), Adrian and Wu (2008)

Nobody uses inflation swaps

Few papers look at heterogenous shocks in the context ofmacro-finance models

RS: Ang, Bekaert, and Wei (2008), Bikbov and Chernov (2008)

SV: Adrian and Wu (2008), Campbell, Sundarem and Viceira(2008)

Are these new data / modeling features important?

4 / 16

Results

Build a seven-factor model (four factors are GARCH volatilities)

→ Value all the relevant assets similar to affine models

→ Estimate using monthly data from 1982.01 to 2008.06(inflation swaps are from 2003.04)

5 / 16

Results

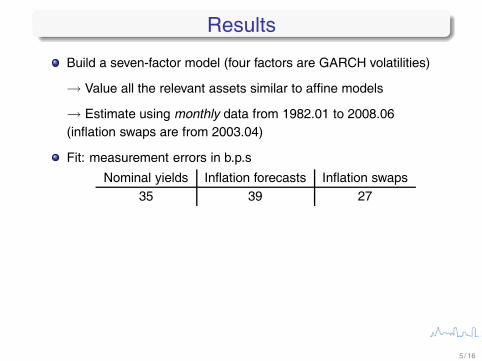

Build a seven-factor model (four factors are GARCH volatilities)

→ Value all the relevant assets similar to affine models

→ Estimate using monthly data from 1982.01 to 2008.06(inflation swaps are from 2003.04)

Fit: measurement errors in b.p.s

Nominal yields Inflation forecasts Inflation swaps35 39 27

5/ 16

Results

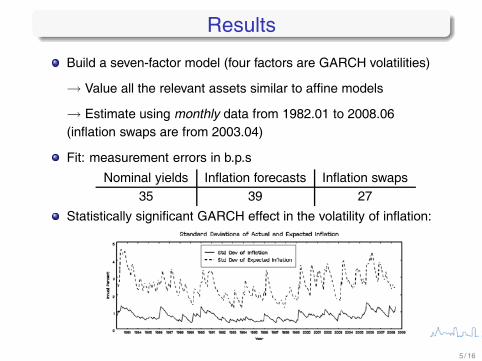

Build a seven-factor model (four factors are GARCH volatilities)

→ Value all the relevant assets similar to affine models

→ Estimate using monthly data from 1982.01 to 2008.06(inflation swaps are from 2003.04)

Fit: measurement errors in b.p.s

Nominal yields Inflation forecasts Inflation swaps35 39 27

Statistically significant GARCH effect in the volatility of inflation:

5 / 16

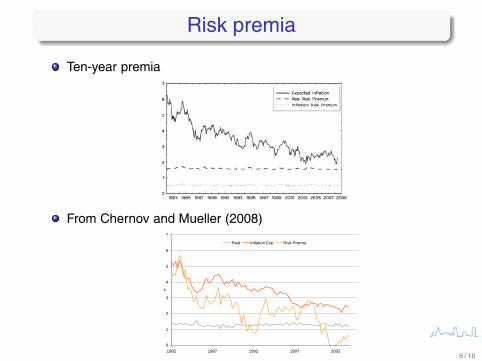

Risk premia

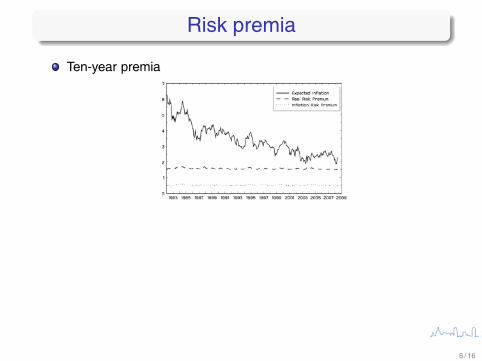

Ten-year premia

6 / 16

Risk premia

Ten-year premia

From Chernov and Mueller (2008)

0

1

2

3

4

5

6

7

1982 1987 1992 1997 2002

%

Real Inflation Exp Risk Premia

6 / 16

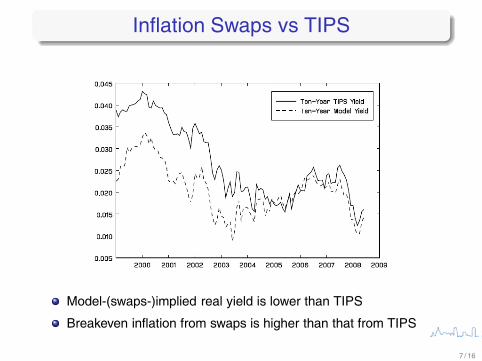

Inflation Swaps vs TIPS

Model-(swaps-)implied real yield is lower than TIPS

Breakeven inflation from swaps is higher than that from TIPS

7/ 16

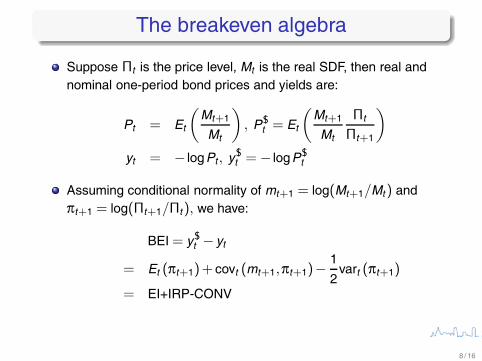

The breakeven algebra

Suppose Πt is the price level, Mt is the real SDF, then real andnominal one-period bond prices and yields are:

Pt = Et

(Mt+1

Mt

), P$

t = Et

(Mt+1

Mt

Πt

Πt+1

)

yt = − logPt , y$t = − logP$

t

Assuming conditional normality of mt+1 = log(Mt+1/Mt) andπt+1 = log(Πt+1/Πt), we have:

BEI = y$t − yt

= Et (πt+1)+ covt (mt+1,πt+1)− 1

2vart (πt+1)

= EI+IRP-CONV

8/ 16

“Online” decision making

Inflation swaps are an immediate measure of market inflationexpectations

9 / 16

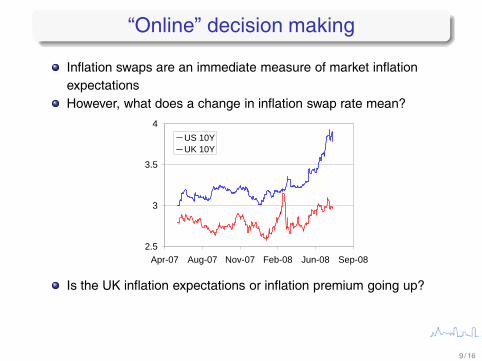

“Online” decision making

Inflation swaps are an immediate measure of market inflationexpectationsHowever, what does a change in inflation swap rate mean?

9/ 16

“Online” decision making

Inflation swaps are an immediate measure of market inflationexpectationsHowever, what does a change in inflation swap rate mean?

2.5

3

3.5

4

Apr-07 Aug-07 Nov-07 Feb-08 Jun-08 Sep-08

US 10YUK 10Y

9 / 16

“Online” decision making

Inflation swaps are an immediate measure of market inflationexpectationsHowever, what does a change in inflation swap rate mean?

2.5

3

3.5

4

Apr-07 Aug-07 Nov-07 Feb-08 Jun-08 Sep-08

US 10YUK 10Y

Is the UK inflation expectations or inflation premium going up?

9/ 16

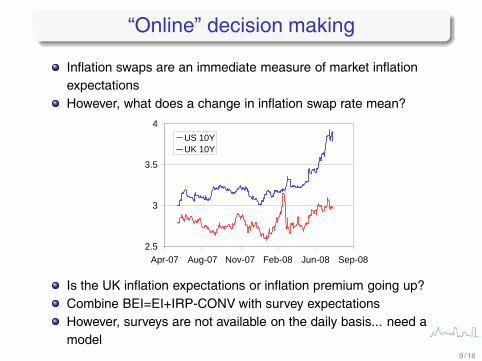

“Online” decision making

Inflation swaps are an immediate measure of market inflationexpectationsHowever, what does a change in inflation swap rate mean?

2.5

3

3.5

4

Apr-07 Aug-07 Nov-07 Feb-08 Jun-08 Sep-08

US 10YUK 10Y

Is the UK inflation expectations or inflation premium going up?Combine BEI=EI+IRP-CONV with survey expectationsHowever, surveys are not available on the daily basis... need amodel

9 / 16

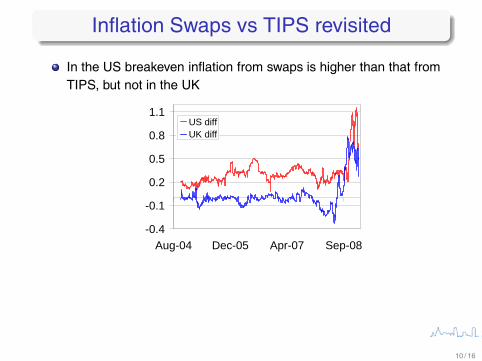

Inflation Swaps vs TIPS revisited

In the US breakeven inflation from swaps is higher than that fromTIPS, but not in the UK

-0.4

-0.1

0.2

0.5

0.8

1.1

Aug-04 Dec-05 Apr-07 Sep-08

US diffUK diff

10 / 16

What is the source of the disparity?

No natural inflation payers/sellers in the US private sector.

→ Different accounting treatment of inflation hedging in the USand Europe.

Post-Lehman spike in funding costs led to a further increase inthe TIPS yields and affected UK

Modelling implication:

→ Need an extra factor for inflation swaps

→ Perhaps, use TIPS instead, but see D’Amico, Kim, and Wei(2007)

11 / 16

Model estimation

The authors argue that inflation forecasts and inflation swaps arerequired to identify parameters pertaining to the real yield curve

Ang, Bekaert, and Wei (2008) show that one can identify the realcurve and inflation premia provided one of the factors is inflation

12 / 16

Model estimation

The authors argue that inflation forecasts and inflation swaps arerequired to identify parameters pertaining to the real yield curve

Ang, Bekaert, and Wei (2008) show that one can identify the realcurve and inflation premia provided one of the factors is inflation

Inflation forecasts and inflation swaps are useful as additionalsignals about the unobservable state of the economy

→ One has to be careful in assigning weights to these signals

→ One important issue is whether inflation swaps are useful inextracting information about volatility

12 / 16

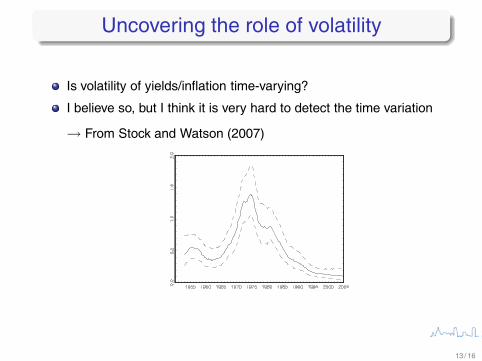

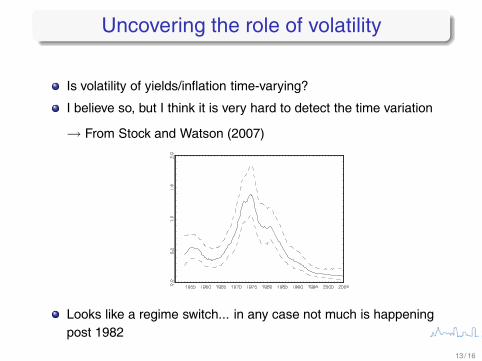

Uncovering the role of volatility

Is volatility of yields/inflation time-varying?

13 / 16

Uncovering the role of volatility

Is volatility of yields/inflation time-varying?

I believe so, but I think it is very hard to detect the time variation

13 / 16

Uncovering the role of volatility

Is volatility of yields/inflation time-varying?

I believe so, but I think it is very hard to detect the time variation

→ From Stock and Watson (2007)

13 / 16

Uncovering the role of volatility

Is volatility of yields/inflation time-varying?

I believe so, but I think it is very hard to detect the time variation

→ From Stock and Watson (2007)

Looks like a regime switch... in any case not much is happeningpost 1982

13 / 16

What is to be done?

Bikbov and Chernov (2004) show that one can estimate anARCH model using yields simulated from a Gaussian termstructure model

→ We propose to use options to detect stochastic volatility

Adrian and Wu (2008), in the absence of options on TIPS,propose to match a GARCH volatility estimated using yieldsobserved at higher frequency

→ Campbell, Sundarem and Viceira (2008) use a related trick

Perhaps, inflation swaps can serve a similar role...

14 / 16

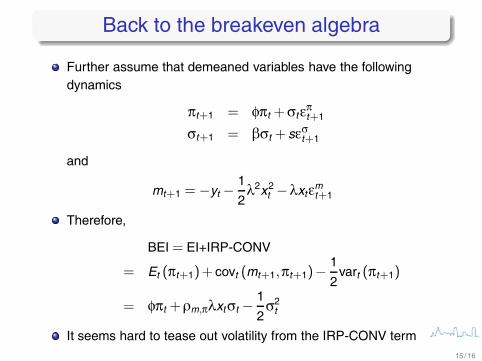

Back to the breakeven algebra

Further assume that demeaned variables have the followingdynamics

πt+1 = φπt +σtεπt+1

σt+1 = βσt + sεσt+1

and

mt+1 = −yt − 1

2λ2x2

t −λxtεmt+1

Therefore,

BEI = EI+IRP-CONV

= Et (πt+1)+ covt (mt+1,πt+1)− 1

2vart (πt+1)

= φπt +ρm,πλxtσt − 1

2σ2

t

It seems hard to tease out volatility from the IRP-CONV term15 / 16

Concluding remarks

This is a fascinating topic!

Are inflation swaps useful?

→ Invaluable for back-of-the-envelope computations

→ Perhaps, less valuable (as compared to TIPS) for a moreprecise, model-based inference

→ These markets have to be developed further taking a cue fromthe £/C areas

16 / 16

![23.Inflation - pdg.lbl.govpdg.lbl.gov/2017/reviews/rpp2017-rev-inflation.pdf · 23.Inflation 5 models [22,23,24], where inflation inside the bubble has a finite duration, leaving](https://img.pdfslide.us/doc/110x75/5e11caf48b6af83dd22a3107/23iniation-pdglbl-23iniation-5-models-222324-where-iniation-inside.jpg)