Embed Size (px)

Citation preview

Estimates of Real-Time Volatility in Interest Rate

Futures

Ramnik AroraAdvisor: Robert Almgren

December 21, 2011

Contents

1 Introduction 2

2 Volatility Estimators 62.1 Evaluation of Volatility Estimators . . . . . . . . . . . . . . . 62.2 Realized Variance . . . . . . . . . . . . . . . . . . . . . . . . . 7

2.2.1 Criticism . . . . . . . . . . . . . . . . . . . . . . . . . 72.3 Garman-Klass Estimators . . . . . . . . . . . . . . . . . . . . 8

2.3.1 Criticism . . . . . . . . . . . . . . . . . . . . . . . . . 92.4 Hawkes Process . . . . . . . . . . . . . . . . . . . . . . . . . . 9

2.4.1 Criticism . . . . . . . . . . . . . . . . . . . . . . . . . 92.5 Brownian Motion with Invisible Bands . . . . . . . . . . . . . 9

2.5.1 Criticism . . . . . . . . . . . . . . . . . . . . . . . . . 10

3 AR(1) Model 123.1 Characteristics of the Market . . . . . . . . . . . . . . . . . . 123.2 Daily Estimator . . . . . . . . . . . . . . . . . . . . . . . . . . 13

3.2.1 Volatility Forecasting and Comparisons . . . . . . . . 133.2.2 TWAP Schedules . . . . . . . . . . . . . . . . . . . . . 14

3.3 Real-time Volatility Estimator . . . . . . . . . . . . . . . . . 163.3.1 Constant β . . . . . . . . . . . . . . . . . . . . . . . . 163.3.2 Real-time AR(1) Volatility . . . . . . . . . . . . . . . 163.3.3 Correlations and Clustering . . . . . . . . . . . . . . . 16

3.4 Extensions . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 193.4.1 Binary-Tree Model . . . . . . . . . . . . . . . . . . . . 213.4.2 Vector Autoregressive Model . . . . . . . . . . . . . . 21

3.5 Contrast with other models . . . . . . . . . . . . . . . . . . . 223.6 Conclusion . . . . . . . . . . . . . . . . . . . . . . . . . . . . 22

A Appendix 24A.1 Properties of Interest Rate Futures . . . . . . . . . . . . . . . 24A.2 Diffusion with Barriers . . . . . . . . . . . . . . . . . . . . . . 24A.3 AR(1) Coefficient Update . . . . . . . . . . . . . . . . . . . . 26

1

Chapter 1

Introduction

Volatility is an estimate of the fluctuations in the price of a underlying con-tract, and is used to measure the uncertainty or risk posed by the financialinstrument. It signifies the risk associated with the price process, and usefulin many applications, such as risk-management, option pricing, portfolio al-location and execution. While executing a order we have a trading schedule,which we try to adhere to (often determined by the benchmark, for exampleTime Weighted Average Price or Volume Weighted Average Price), and someforward and behind boundaries which will make sure we don’t stray too faraway from the trade schedule. However, these bands must be constricted inaccordance to our forecast of the risk, in a mean-variance framework. Often,volume is used as a proxy for risk1, but this relationship is not exact, andfrequently large volumes print without significant large price movements.

The question of volatility estimation is closely related to fitting a modelto the market prices2, and in a “random walk plus microstructure effects”framework, we are concerned with the quadratic variation of the true price.However, the market prices don’t follow a model perfectly, and moreoverwe only have access to the discretized observations3 of a continuous latentunderlying price process, making this a difficult ordeal. To further compli-cate matters, the price series have irregular temporal spacing, and peculiardiurnal patterns.

It is desirable of any real-time estimator to reproduce the properties andcharacteristics of high frequency data. Owing to the large amounts of data,

1The correlation between volume traded and range(maximum price - minimum pricewithin the timeperiod) in prices, in 15-minute bins for Sept’13 Eurodollar on 2011.12.06is 0.73.

2A familiar example is implied volatility which is deeply connected with lognormal assetprices, in the Black-Scholes framework.

3The minimum price increments are ridiculously large in the interest rate future, andthe price movements are very discrete, often not changing for large periods in time. Seereftab:tick for details on tick size.

2

9897½

9898

9898½

02:50:30 02:50:40 02:50:50 02:51:00 02:51:10 02:51:20 02:51:30

CST time on Tue 06 Dec 2011

500 lots

● ● ● ● ●

AR1−Volatility for GEH4

Volatility in 15 Minute bins

AR−1 Coefficient

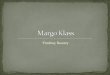

Figure 1.1: An illustration of the orderbook for March’14 Eurodollar on2011.12.06. The microprice is depicted in black, the midprice in thegreen(dashed) while the trade prints at shown by dark green dots. Thebid/ask volume is represented accordingly. It is interesting to note the flick-ering quotes, and the presence of ghost liquidity. The market is essentiallymulti-tick, with often people narrowing the spreads.

3

the need for a fast estimation process is heightened. Besides, it would bevery useful if the estimation process, converted volatility to be an observ-able (much like volume traded), since it would allow greater use cases inthe algorithm. Rather than provide volatility per unit time, the algorithmcould subscribe to it’s own measure based on requirements. Another crucialproperty of real-time estimator is that it must be parameter-free, since itwould be difficult to guesstimate appropriate parameters, which maybe de-pendent on the changing market conditions. As a matter of usage, we willcompute volatility in terms of ticks4 per unit time, in order to standardizeover different interest rate futures contracts.

Price changes are often unstable, and rapid reversions in the prices arerampant. An example would be that for the market to actually move, onewould require either the bid moves down first and the ask follows down, orthe ask moves up followed by the bid moving up. Rarely do both the actionsoccur simultaneously, and the multi-tick mode5 is transient. Our model mustsomehow minimize the impact of these unstable quotes, or rapidly-revertingprices changes(see figure 1.1).

In order to devise a volatility estimator, various data series maybe used(Seefigure 1.1 for illustration). The market provides us with trade/order bookdata, and both may very well be used for a real-time volatility estimator.

1. Trade data: Trade data represents the timestamped series of the tradesobserved by the market. Since trade prices may print on the bid orthe ask, these inherently contain microstructure noise and are un-suitable for direct usage. Plenty of real-time estimators have beenproposed using high-frequency trade data, but all these make signifi-cant assumption on microstructure noise[Zhou(1992)]. A recent paper[Gatheral(2010)] concludes that in a Zero-intelligence model, in termsof sampling, the midprice and microprice are 40-60 times less noisythan trade data (as measured by microstructure noise variance). Forthese reasons, we choose not to use trade prints from the markets.

2. Microprice: Micro-price is defined as (bid volume) * ask + (ask vol-ume) * bid, and is representative of the current state of the mar-ket. However, this metric is gameable, by ghost liquidity, and in[Gatheral(2010)], the mid-quote is weakly preferred over micro-pricein a zero-intelligence setup.

3. Midprice: Mid-price is defined as the arithematic mean of the insidequote, or the mean of the bid and the ask. This is known to be more

4A tick is used to denote the minimum price increment allowed by the CME for theparticular contract. Please see A.1 for contract-wise details.

5Multi-tick markets are when the bid-ask spread exceeds the minimum tick, for examplewhen the bid moves down or the ask moves up.

4

stable (albeit discontinuous) and doesn’t incorporate microstructurenoise.

For the study, the interest rate futures tick-by-tick data from the CMEhas been used. Although we only present the results for volatility estimatesfrom Eurodollar and Treasury future outrights, similar property are observedin Packs, Spreads and Butterfly contracts on these outrights. In section 2we briefly discuss a few models for real-time volatility estimators, like sumof squared returns, Garman-Klass estimator, modelling based on Hawkesprocess, and use of invisible bands around midprices for mean-revertingcharacteristics of the market. In section 3 we choose to study the sum ofsquares of AR(1) corrected residuals in greater details, and it’s suitabilityin a high-frequency environment.

5

Chapter 2

Volatility Estimators

In this chapter, we will discuss some of the volatility estimators implementedand the corresponding results obtained. These estimators were eventuallydiscarded and a quick discussion of their suitability is presented.

2.1 Evaluation of Volatility Estimators

A critical problem one faces in volatility estimation is reliable quantitativecomparison of various estimators. A test for volatility estimators is to nor-malize the period returns by the volatility estimates, and one must havea draw from a standard gaussian distribution. The empirical distributionmaybe tested against a standard gaussian distribution, and metric suitablydefined on the performance of the metric. However, hereby we are assumingthat the distribution of returns is normally distributed, and this observa-tion is empirically flawed. This test is strict and would not be met by anyestimator perfectly, owing to the large error introduced from discretization,leptokurtosis of return series, microstructure noise amongst other factors. Itdoes however form a suitable benchmark for comparison.

There are some empirical observations that every volatility estimatormust satisfy:

1. Eurodollar volatility should mostly be in increasing order of time tomaturity, since the uncertainity is greatest for far out contracts.

2. Amongst the treasury future outrights, the five-year are the mostvolatile, while the two-year behave similar to the Eurodollars.

3. Any metric imposed on the correlations amongst treasuries shouldcluster them in increasing order of time to maturity.

4. Volatility should spike up around Non-Farm Payroll, FOMC Meetingsand other significant number releases.

6

−2 −1 0 1 2

0

100

200

300

400

500

Returns/Volatility

Fre

quen

cy

Daily AR(1) Volatility/Realized Variance/Garman−Klass Estimator N(0, 1) − IdealRealized VolatilityAR(1) VolatilityGarman−Klass Estimator

Figure 2.1: A comparison of the Realized Variance, Garman-Klass andAR(1) corrected daily volatility estimators. The curves represent the dailyreturns normalized by the volatility estimator, and a histogram is comparedwith the a histogram from standard gaussian distribution.

5. Volatility should spike around May 6th 2010(Flash Crash) and 12th

August 2011(US Sovereign Downgrade).

2.2 Realized Variance

Realized Variance is a simple estimator given by the quadratic variation ofthe return series, which in single tick markets often reduces to counting thetotal number of price changes. Because of large serial autocorrelation be-tween returns, arising from microstructure noise, we expect realized varianceto overestimate the variance in a period.

In figure 2.2 we compare the daily returnsrealized volatility against a standard gaus-

sian distribution (green curve for standard gaussian, while blue for returnsnormalized using realized volatility), and in 2.3, the blue curve representthe squared sum of returns for front month Eurodollar from 2011.01.01-2011.12.06.

2.2.1 Criticism

Realized Variance is a naive estimator since it doesn’t discount for unsta-ble quotes or mean reversion of interest rate future returns. Although theestimator can be computed rapidly, and would treat volatility as an observ-able, it doesn’t replicate the characteristics of high-frequency data. In early

7

2011−01−26 2011−03−17 2011−05−06 2011−06−25 2011−08−14 2011−10−03 2011−11−22

0

5

10

15

20

25

30

AR1 VolatilityRealized VolGarman−Klass Variance

Date

Vol

atili

ty in

Tic

ks/D

ay

Realized Volatility/AR1 Volatility/Garman−Klass Volatility for Eurodollar with TTM = [0, 3) months

US

Debt dow

ngradeFOMC AnnoucementNon−farm Payroll

Figure 2.2: A plot of the Realized, AR(1) and Garman-Klass Volatility Es-timators. The impact of US Debt downgrade, the unusual non-farm payroll,important FOMC announcements and the Eurozone debt crisis is evident.

literature[Andersen(2000)], the general prescription is to sample at intervalssuch that microstructure effects are negated, but this is in contrast with ourneeds for a real-time estimator.

2.3 Garman-Klass Estimators

A standard approach to daily realized volatility estimation was provided in[Garman-Klass(1980)]. Their volatility estimators use open, high, low, closeprices for the given period to estimate the volatility.

σ2 =1

2(loge High− loge Low)2 − (2 loge 2− 1)2(loge Close− loge Open)2

A comparison of the Garman-Klass estimator with the Realized variance,and the AR(1)-Volatility estimator can be seen in 2.2. Although Garman-Klass seems to do fairly well as a estimator of daily volatility, it breaksdown as we increase the sampling frequency. In figure 2.3, the GarmanKlass volatility estimator for daily returns is presented for front Eurodol-lar contract between 2011.01.01-2011.12.06. Garman-Klass estimator allowssubsampling a time period, which was briefly looked into revealing similarresults.

8

2.3.1 Criticism

Garman-Klass estimators only rely on the OHLC data for volatility esti-mation, and discard the remaining data. Garman Klass estimator were de-signed for low frequency data and fail to capture the perculiar characteristicsof interest rate futures.

2.4 Hawkes Process

In the paper [Bacry(2010)] the authors model microstructure noise usingHawkes process for tick-by-tick variation. Two stochastic counting processesare associated with the price processes, for the positive and negative jumpsin prices. These stochastic processes, are assumed to be mutually stim-ulating, which is helpful to reproduce the high-frequency mean-reversioncharacteristics observed in the data.

The volatility maybe expressed as the limit of the signature plot1 of themid-price series. The paper prescribes the calibration of the limit using a 3parameter model.

2.4.1 Criticism

The model parameters converge to un-intuitive values, suggesting that thebase diffusion rate is close to zero and the processes are simply mutuallystimulated, making them unstable. These are not responsive in real-timeand are useful for calibrating volatilites using lower frequency data.

2.5 Brownian Motion with Invisible Bands

An interesting approach to high-frequency volatility is proposed in [Robert(2011)].They suggest that the underlying latent process X(t) is observed on dis-cretized bands and incorporate the market characteristics using uncertainityzones, which are bands around the mid-tick grid where the efficient price istoo far from the tick grid to trigger a price change.

Assuming we have two absorbing barriers, at [0, 1], with a particle start-ing at α ∈ [0, 1]. We can calculate the total probability of the particle being

1The signature plot of a time series X(t), corresponds to the realized variance atdifferent sampling frequency. Thus, it’s a plot of C, over a time period [0, T ] at a scaleτ > 0, where C is defined as:

C(τ) =1

T

n=T/τ∑n=0

(X((n+ 1)τ) −X(nτ))2

9

0 200 400 600 800 1000

05

1015

2025

3035

Sampling Time

Rea

lized

Var

ianc

e

EmpiricalStartingOptima OriginalOptima Gradient

mu = (0.419, 0.417), alpha = (0.007, 0.007), beta = (0.007, 0.007) Estimate of Volatility = 9.40 and 9.42

mu_0 = 10.00, alpha_0 = 5.00 beta_0 = 14.00

Figure 2.3: The signature plot for for March’12 Eurodollar with samplingfrequency varying from 15-1015 seconds. As can be seen the signature plotis very choppy, and the smooth approximation is shown by the red/greencurves, whose aymptotic limits represent the volatility.

absorbed at the two barriers analytically as a function of time(t)(see Ap-pendix A.2). The probability of being absorbed at the lower boundary is1−α, while at the upper boundary is α. This maybe empirically calibratedfrom the market, where absorption to the lower boundary can be treated asreversals, and absorption by the upper boundary is equivalent to continua-tion moves. The scaling in time whereby the two curves are closest (in L2)would be representative of volatility, which is equivalent to scaling in time.

2.5.1 Criticism

From the figure 2.4 it can be seen that the model doesn’t calibrate verywell to the market, especially for continuations. In the market, a largenumber of times (and especially during events), the market has a strongdirectional trend, which is not captured by this model. Assuming that thelatent underlying process follows a Simple Brownian Motion seems like anoversimplification. It maybe benificial to extend the model for generic Levyprocesses to account for rapid continuations.

10

Figure 2.4: The shaded region represents the cumulative flux for a brown-ian motion, starting at point α(calibrated using market data as the mean-reversion probability), and the dotted line is the scaled empirical cumulativeflux observed from market data. Notice the significant difference in the cu-mulative flux of continuations with respect to the analytical results.

11

Chapter 3

AR(1) Model

3.1 Characteristics of the Market

As has been alluded to often in the report, the returns have a serial au-tocorrelation. As can be seen in figure 3.1, the midpoint changes in singletick market have a negative AR(1) coefficient, or are mean-reverting. Thisis quite unlike daily returns, which have been empirically observed to havezero serial autocorrelation[Engle(1995)]. This is a critical observation, anda defining characteristic of the market.

Let rt be the midpoint changes in single tick markets. We hypothesize that:

rt = βtrt−1 + εt

whereby εt is a mean zero process. The quadratic variation of the residualsεt would be the volatility of the return series.

This metric is consistent, since volatility is the conditional variance ofasset returns1, or mathematically:

σt2 = E[(rt − µt)2|Ft−1]

where Ft−1 is the information available till t− 1, and µt = E[rt|Ft−1], whichdisplays a definite AR(1) structure.

A lucid illustration of this measure is provided in 3.2, where we plot theactual prices, and the scaled (to same range) the AR(1) corrected price se-ries, assuming a constant β for the day2. In our measure of AR(1) corrected

1To quote Paul Wilmott from his blog, ‘’The definition of volatility is subtly differentwhen there is SAC[serial autocorrelation]. The sequence +1, -1, +1, -1, +1, has perfectnegative SAC and a volatility of zero!”.

2Let yt be the AR(1) corrected price series. This is computed as yt = x0 +∑k≤t εk,

where x0 is the starting price of the underlier. Scaling is done such that the series underlierprice series(xt), and AR(1) corrected price series(yt) have the same range.

12

0 1 2 3 4 5

−1.00

−0.75

−0.50

−0.25

0.00

0.25

0.50

0.75

1.00ACF/PACF for return series of GEH2 on 2011.12.06

PAC

F/A

CF

Lags

ACFPACF

Figure 3.1: A plot depicting the ACF/PACF of the midpoint changes insingle tick market. The ACF/PACF clearly indicate that returns are mean-reverting.

volatility, we are effectively (loosely speaking, because of scaling) taking thequadratic variation of returns from the AR(1) corrected price series (shownin blue), which seems to dampen the mean reverting quotes.

3.2 Daily Estimator

Using the above formulation, we initially come up with daily estimators ofvolatility. Given a day’s data, we compute the first-order serial autocorrela-tion of the returns in single-tick wide markets, and the quadratic variationof the residual represents the AR(1) variance for the given contract on thegiven day. Figure 2.2 plots the normalized AR(1) volatility realized returnsagainst equal draws from a standard normal for the first(rolling) eight eu-rodollar contracts between 2011.01.01-2011.12.06. Figure 2.3 is a plot of theAR(1) volatility of the near expiry contract between the same time period.

3.2.1 Volatility Forecasting and Comparisons

The quadratic variation of the residuals may also be computed in non-intersecting 15-minute bins, spanning the entire day using historical data.An exponential weighted average of previous periods, super-imposing the

13

Time in Midpoint Change Time

Pric

es

Price Series for GEH3 on date 2011.12.06

0 50 100 150 200 250

9928

.099

29.0

9930

.0

Midprice SeriesScaled AR(1) Series

Figure 3.2: The black line is the price for March’13 Eurodollar on 6th De-cember 2011, and the blue line is the scaled AR(1) corrected price series.As is evident, the AR(1) corrected price series dampen the contribution toquadratic variation from mean-reverting quotes.

event model3, yields the volatility forecast for the various Interest RateFutures complex in 15-minute bins. Figure 3.3 is a forecast of the Eurodol-lar complex volatility forecast generated on 2011.12.05 for the trading day2011.12.06, while the comparisons with realized AR(1) volatility are pre-sented to the right.

3.2.2 TWAP Schedules

Given our forecast of volatility, we adjust out forward and backward bound-ary in accordance with our volatility forecast3. Figure 3.4 is an illustrationof this behaviour, where boundaries are adjusted on the basis of volumeand volatility respectively. The volume and volatility profile can easily becontrasted here, and the difference in the ahead and behind boundariesis noticiable. The contrast between volume and volatility is extreme on2011.09.21, an important FOMC meeting announcement, and the constric-tion of the forward and behind boundaries is obvious.

3This is proprietary to Quantitative Brokers, and not a part of this project.

14

Eurodollar

chicago time

vola

tility

in 1

5 m

inut

es (t

icks)

00:00 01:00 02:00 03:00 04:00 05:00 06:00 07:00 08:00 09:00 10:00 11:00 12:00 13:00 14:00 15:00 16:00

0

1

2

CME

CLO

SE

No Events

2−Year Note

chicago time

vola

tility

in 1

5 m

inut

es (t

icks)

00:00 01:00 02:00 03:00 04:00 05:00 06:00 07:00 08:00 09:00 10:00 11:00 12:00 13:00 14:00 15:00 16:00

0

1

CME

CLO

SE

No Events

5−Year Note

chicago time

vola

tility

in 1

5 m

inut

es (t

icks)

00:00 01:00 02:00 03:00 04:00 05:00 06:00 07:00 08:00 09:00 10:00 11:00 12:00 13:00 14:00 15:00 16:00

0

2

4

6

8

CME

CLO

SE

No Events

10−Year Note

chicago time

vola

tility

in 1

5 m

inut

es (t

icks)

00:00 01:00 02:00 03:00 04:00 05:00 06:00 07:00 08:00 09:00 10:00 11:00 12:00 13:00 14:00 15:00 16:00

0

1

2

3

4

5

6

7

8

9

CME

CLO

SE

No Events

T−Bond

chicago time

vola

tility

in 1

5 m

inut

es (t

icks)

00:00 01:00 02:00 03:00 04:00 05:00 06:00 07:00 08:00 09:00 10:00 11:00 12:00 13:00 14:00 15:00 16:00

0

2

4

6

8

CME

CLO

SE

No Events

U−Bond

chicago time

vola

tility

in 1

5 m

inut

es (t

icks)

00:00 01:00 02:00 03:00 04:00 05:00 06:00 07:00 08:00 09:00 10:00 11:00 12:00 13:00 14:00 15:00 16:00

0

2

4

6

8

10

12

CME

CLO

SE

No Events

Eurodollar

chicago time

vola

tility

in 1

5 m

inut

es (t

icks)

00:00 01:00 02:00 03:00 04:00 05:00 06:00 07:00 08:00 09:00 10:00 11:00 12:00 13:00 14:00 15:00 16:00

0

1

2

3

4

5

CME

CLO

SE

No Events

2−Year Note

chicago time

vola

tility

in 1

5 m

inut

es (t

icks)

00:00 01:00 02:00 03:00 04:00 05:00 06:00 07:00 08:00 09:00 10:00 11:00 12:00 13:00 14:00 15:00 16:00

0

1

2

3

CME

CLO

SENo Events

5−Year Note

chicago time

vola

tility

in 1

5 m

inut

es (t

icks)

00:00 01:00 02:00 03:00 04:00 05:00 06:00 07:00 08:00 09:00 10:00 11:00 12:00 13:00 14:00 15:00 16:00

0

2

4

6

8

10

CME

CLO

SE

No Events

10−Year Note

chicago time

vola

tility

in 1

5 m

inut

es (t

icks)

00:00 01:00 02:00 03:00 04:00 05:00 06:00 07:00 08:00 09:00 10:00 11:00 12:00 13:00 14:00 15:00 16:00

0

1

2

3

4

5

6

7

8

9

CME

CLO

SE

No Events

T−Bond

chicago time

vola

tility

in 1

5 m

inut

es (t

icks)

00:00 01:00 02:00 03:00 04:00 05:00 06:00 07:00 08:00 09:00 10:00 11:00 12:00 13:00 14:00 15:00 16:00

0

2

4

6

8

10

CME

CLO

SE

No Events

U−Bond

chicago time

vola

tility

in 1

5 m

inut

es (t

icks)

00:00 01:00 02:00 03:00 04:00 05:00 06:00 07:00 08:00 09:00 10:00 11:00 12:00 13:00 14:00 15:00 16:00

0

2

4

6

8

10

12

14

CME

CLO

SE

No Events

Figure 3.3: Volatility Forecasts and realized AR(1) Volatility produced on2011.12.05 for the trade day 2011.12.06, in 15-minute bars.

GE Adjusted TWAP schedule − 2011−12−06

Time (Chicago)01:00 03:00 05:00 07:00 09:00 11:00 13:00

0

20

40

60

80

100

Fille

d Pe

rcen

tage

0.00

0.05

0.10

0.15

Vola

tility

(Tic

ks)

0.0

0.5

1.0

1.5

2.0

Volu

me

(in T

hous

ands

)

Volatility ForecastVolume ForecastVolatility Adjusted BandsVolume Adjusted Bands

ZT Adjusted TWAP schedule − 2011−12−06

Time (Chicago)01:00 03:00 05:00 07:00 09:00 11:00 13:00

0

20

40

60

80

100Fi

lled

Perc

enta

ge

0.00

0.02

0.04

0.06

0.08

Vola

tility

(Tic

ks)

0.0

0.1

0.2

0.3

0.4

Volu

me

(in T

hous

ands

)

Volatility ForecastVolume ForecastVolatility Adjusted BandsVolume Adjusted Bands

ZF Adjusted TWAP schedule − 2011−12−06

Time (Chicago)01:00 03:00 05:00 07:00 09:00 11:00 13:00

0

20

40

60

80

100

Fille

d Pe

rcen

tage

0.0

0.1

0.2

0.3

0.4

0.5

0.6

Vola

tility

(Tic

ks)

0.0

0.2

0.4

0.6

0.8

1.0

1.2

Volu

me

(in T

hous

ands

)

Volatility ForecastVolume ForecastVolatility Adjusted BandsVolume Adjusted Bands

ZN Adjusted TWAP schedule − 2011−12−06

Time (Chicago)01:00 03:00 05:00 07:00 09:00 11:00 13:00

0

20

40

60

80

100

Fille

d Pe

rcen

tage

0.0

0.1

0.2

0.3

0.4

0.5

0.6

Vola

tility

(Tic

ks)

0.0

0.5

1.0

1.5

2.0

2.5

Volu

me

(in T

hous

ands

)

Volatility ForecastVolume ForecastVolatility Adjusted BandsVolume Adjusted Bands

ZB Adjusted TWAP schedule − 2011−12−06

Time (Chicago)01:00 03:00 05:00 07:00 09:00 11:00 13:00

0

20

40

60

80

100

Fille

d Pe

rcen

tage

0.0

0.1

0.2

0.3

0.4

0.5

0.6

Vola

tility

(Tic

ks)

0.0

0.2

0.4

0.6

Volu

me

(in T

hous

ands

)

Volatility ForecastVolume ForecastVolatility Adjusted BandsVolume Adjusted Bands

UB Adjusted TWAP schedule − 2011−12−06

Time (Chicago)01:00 03:00 05:00 07:00 09:00 11:00 13:00

0

20

40

60

80

100

Fille

d Pe

rcen

tage

0.0

0.2

0.4

0.6

0.8

Vola

tility

(Tic

ks)

0.00

0.02

0.04

0.06

0.08

0.10

Volu

me

(in T

hous

ands

)

Volatility ForecastVolume ForecastVolatility Adjusted BandsVolume Adjusted Bands

GE Adjusted TWAP schedule − 2011−09−21

Time (Chicago)02:00 04:00 06:00 08:00 10:00 12:00 14:00

0

20

40

60

80

100Fi

lled

Perc

enta

ge

0.0

0.1

0.2

0.3

0.4

0.5

0.6

Vola

tility

(Tic

ks)

02

46

810

12

Volu

me

(in T

hous

ands

)

Volatility ForecastVolume ForecastVolatility Adjusted BandsVolume Adjusted Bands

ZT Adjusted TWAP schedule − 2011−09−21

Time (Chicago)02:00 04:00 06:00 08:00 10:00 12:00 14:00

0

20

40

60

80

100

Fille

d Pe

rcen

tage

0.0

0.1

0.2

0.3

0.4

0.5

Vola

tility

(Tic

ks)

0.0

0.5

1.0

1.5

Volu

me

(in T

hous

ands

)

Volatility ForecastVolume ForecastVolatility Adjusted BandsVolume Adjusted Bands

ZF Adjusted TWAP schedule − 2011−09−21

Time (Chicago)02:00 04:00 06:00 08:00 10:00 12:00 14:00

0

20

40

60

80

100

Fille

d Pe

rcen

tage

0.0

0.5

1.0

1.5

2.0

Vola

tility

(Tic

ks)

01

23

4

Volu

me

(in T

hous

ands

)

Volatility ForecastVolume ForecastVolatility Adjusted BandsVolume Adjusted Bands

ZN Adjusted TWAP schedule − 2011−09−21

Time (Chicago)02:00 04:00 06:00 08:00 10:00 12:00 14:00

0

20

40

60

80

100Fi

lled

Perc

enta

ge

0.0

0.5

1.0

1.5

Vola

tility

(Tic

ks)

02

46

Volu

me

(in T

hous

ands

)

Volatility ForecastVolume ForecastVolatility Adjusted BandsVolume Adjusted Bands

ZB Adjusted TWAP schedule − 2011−09−21

Time (Chicago)02:00 04:00 06:00 08:00 10:00 12:00 14:00

0

20

40

60

80

100

Fille

d Pe

rcen

tage

0.0

0.5

1.0

1.5

Vola

tility

(Tic

ks)

0.0

0.5

1.0

1.5

2.0

Volu

me

(in T

hous

ands

)

Volatility ForecastVolume ForecastVolatility Adjusted BandsVolume Adjusted Bands

UB Adjusted TWAP schedule − 2011−09−21

Time (Chicago)02:00 04:00 06:00 08:00 10:00 12:00 14:00

0

20

40

60

80

100

Fille

d Pe

rcen

tage

0.0

0.5

1.0

1.5

Vola

tility

(Tic

ks)

0.00

0.05

0.10

0.15

0.20

0.25

0.30

Volu

me

(in T

hous

ands

)

Volatility ForecastVolume ForecastVolatility Adjusted BandsVolume Adjusted Bands

Figure 3.4: The forward and behind boundaries for trading the Eurodollarcomplex on 2011.12.06 and 2011.09.21. High volume and volatility was ex-pected around FOMC announcement on 2011.09.21, and we force ourselvesto return to our trading schedule (in this case TWAP) before the annouce-ment by contricting the bands.

15

3.3 Real-time Volatility Estimator

3.3.1 Constant β

For daily volatility numbers, we assume that β is constant for the entireday, and is calibrated using the entire days data. In support of this assump-tion, we fit a time varying AR-1 model using Kalman filter. Essentially, weassume:

βt = βt−1 + zt with zt ∼ IIDN(0, σ21)

rt = βtrt−1 + vt with vt ∼ IIDN(0, σ22)

In figure 3.5, we can see the assumption of constant β versus filtered β4 versusreal-time β are pretty close to each other, especially during market hours.For real-time estimation, we’ll continue with the assumption of constant βfor the entire day, but our estimator for β at time t will use data until timet, as discussed below. Graphically, this corresponds to the yellow line on thefigure 3.5, which seems to track the green line really well.

3.3.2 Real-time AR(1) Volatility

Given the assumption of constant β, the algorithm for online update of theAR(1) coefficient is O(1), and can be computed rapidly in a real-time system(See appendix A.3 for details). In figure 3.6 we implement the algorithm forthe March’13 Eurodollar contract on 2011.12.06, between 07:30-07:46 a.m.CST. The volatility estimated in the period is 3.67 ticks, while the residualsεt can also be seen in the plots. The AR(1) coefficient is -0.64. It is crucial tonote that the mean-reverting flickering quotes contributions to the volatilityis nominal in comparison to continuations. The behaviour close to 07:44 a.m.is particularly characteristic of the interest rate futures markets wherebythe market is essentially in a multi-tick mode, and frequently participantsare closing the gap. Any metric such as realized variance, Garman-Klassestimator would be unable to cancel out this noise.

3.3.3 Correlations and Clustering

One would expect a strong correlation within the volatility of neighbouringcontracts in the eurodollar complex since segments of the yield curve oftenmove together in unison. Table 3.1 plots the correlation matrix between thefront end of the yield curve, and the US Treasury complex for 2011.12.06. Anagglomerative clustering of the volatility series, based on 15-minute AR(1)

4Using σ21 = 0.01, σ2

2 = 0.4, β0 = −0.8 for the specified model.

16

00:0

0

04:0

0

08:0

0

12:0

0

16:0

0

20:0

0

23:0

014:20 21:00Floor

−1.

1−

1.0

−0.

9−

0.8

−0.

7−

0.6

−0.

5−

0.4

ReturnsAR−1 DayAR−RealtimeAR−Kalman

Time from market openFor GEH3 on 2011.12.06

Figure 3.5: A plot of the returns (in black, where returns vary between {-1,1}), the AR-1 coefficient for the day (in red, which is used for daily esti-mator), AR-1 coeffient in realtime using data till time t(in yellow, used forreal-time volatility estimator), and AR-1 coefficient learned through Kalmanfiltering model (in green). Note that during market hours, or generally inhigh volume periods, we tend to do reasonably well with the given assump-tion of constant AR-1 coefficient.

17

9927½

9928

9928½

9929

9929½

07:30 07:32 07:34 07:36 07:38 07:40 07:42 07:44 07:46

CST time on Tue 06 Dec 2011

2000 lots

●●●●●●●●●●● ● ●●●●●●●●●●●●●● ● ●● ●●●●●●●● ●● ● ●

●●●●●●●●●●●●●●●●●●●●●

●●●●●●●●●●●● ●●●● ●●

●●●●●●●●●●●●●●●●●●●●●●●●●●●●●●●

●●●● ●● ● ●● ●●●●●●●●●●●●●●●●●●●●●●●●●●●●●●● ● ● ●

●●●●●●●●●●●●●●●●●●●●●●

●●

●●●●●●●●● ●● ●

●

●● ● ● ●● ●●●●●●

●

●●●●

●●●●●●●●●●●●● ●●●●●● ●●●●●●●●● ● ●● ●●●●●● ●● ●●● ●●●● ● ●●●●●●●●●●●

●●●●●●●●

●● ●●● ● ●

3.67

−0.64

−0.36

0.36

−0.36

−1.65

0.37

1.64

−0.38

0.38

−0.37

−1.63

0.38

−0.38

0.38

1.63

−0.39

0.38

−0.38

0.38

−0.38

0.37

−0.37

0.37

−0.36

0.36

−0.36

0.35

1.65

AR1−Volatility for GEH3

Volatility in 15 Minute bins

AR−1 Coefficient

Figure 3.6: Real-time estimate of AR(1) volatility. The AR(1) residual isshown on each price change alongwith the AR(1) coefficient and the periodvolatility. Contribution from mean-reverting quotes is removed, and onlycontinuations contribute to the volatility number.

18

GEZ

1GEH

2GEM

2 GEU

2GEZ

2GEH

3GEM

3GEU

3GEZ

3GEH

4GEM

4 GEU

4GEZ

4GEH

5GEM

5GEU

5GEZ

5GEH

6GEM

6GEU

6 ZFZ1

ZNZ1 ZBZ1

UBZ

1ZTZ1

Dendrogram for the various Interest Rate Futures

2011.11.29

Figure 3.7: An Agglomerative Hierarchical Clustering of the Interest RateFutures based on the real-time volatility estimate. Clusters of the white(First 4 Eurodollars), reds (1-2 Year out) and the others are clearly seen.The treasury futures are differ than the Eurodollars, and the Two-YearFutures display a suprisingly different volatility characteristics.

volatility, using L1 norm for 2011.11.29 reveal a very intuitive structure. Thewhites (first four Eurodollars), reds(4-8 Eurodollars) are very highly corre-lated, while the greens and blues behave similarly. Amongst the treasuryfutures, the two-year behave distinctly5, while the 5, 10 and the T-Bond areclosely related.

3.4 Extensions

Hereby, we suggest some improvements, and extensions to the AR(1) modeldiscussed before.

5Their trading is patchy, and in alignment with empirical observations.

19

GE

Z1

GE

H2

GE

M2

GE

U2

GE

Z2

GE

H3

GE

M3

GE

U3

GE

Z3

GE

H4

GE

M4

GE

U4

ZT

H2

ZF

H2

ZN

H2

ZB

H2

GE

Z1

1.0

00.8

10.7

50.7

50.5

10.6

50.4

50.4

20.2

10.1

40.2

60.3

50.0

60.1

90.2

40.2

5G

EH

20.8

11.0

00.8

50.8

40.5

70.6

40.5

00.5

10.2

30.2

30.3

30.4

6-0

.07

0.2

70.2

90.3

2G

EM

20.7

50.8

51.0

00.9

40.6

90.7

30.6

10.6

10.3

20.2

90.4

10.5

0-0

.08

0.2

20.2

20.2

5G

EU

20.7

50.8

40.9

41.0

00.7

40.7

40.6

50.6

10.3

20.2

50.3

80.4

6-0

.10

0.2

20.2

30.2

6G

EZ

20.5

10.5

70.6

90.7

41.0

00.8

30.7

60.6

90.5

20.4

80.5

00.4

6-0

.12

0.2

60.3

00.3

2G

EH

30.6

50.6

40.7

30.7

40.8

31.0

00.7

30.6

40.4

70.4

00.4

80.5

0-0

.02

0.2

50.2

80.2

9G

EM

30.4

50.5

00.6

10.6

50.7

60.7

31.0

00.8

20.4

80.4

70.4

70.4

9-0

.08

0.3

10.3

20.3

7G

EU

30.4

20.5

10.6

10.6

10.6

90.6

40.8

21.0

00.6

40.6

20.6

30.6

0-0

.03

0.3

90.4

10.4

9G

EZ

30.2

10.2

30.3

20.3

20.5

20.4

70.4

80.6

41.0

00.7

00.6

20.5

80.0

50.3

80.4

30.4

7G

EH

40.1

40.2

30.2

90.2

50.4

80.4

00.4

70.6

20.7

01.0

00.6

80.6

40.1

40.4

20.4

00.4

9G

EM

40.2

60.3

30.4

10.3

80.5

00.4

80.4

70.6

30.6

20.6

81.0

00.7

70.0

30.5

30.4

80.5

8G

EU

40.3

50.4

60.5

00.4

60.4

60.5

00.4

90.6

00.5

80.6

40.7

71.0

0-0

.04

0.6

10.5

40.6

2Z

TH

20.0

6-0

.07

-0.0

8-0

.10

-0.1

2-0

.02

-0.0

8-0

.03

0.0

50.1

40.0

3-0

.04

1.0

00.1

40.1

60.1

3Z

FH

20.1

90.2

70.2

20.2

20.2

60.2

50.3

10.3

90.3

80.4

20.5

30.6

10.1

41.0

00.9

20.8

8Z

NH

20.2

40.2

90.2

20.2

30.3

00.2

80.3

20.4

10.4

30.4

00.4

80.5

40.1

60.9

21.0

00.9

1Z

BH

20.2

50.3

20.2

50.2

60.3

20.2

90.3

70.4

90.4

70.4

90.5

80.6

20.1

30.8

80.9

11.0

0

Tab

le3.1

:T

he

corr

elat

ion

matr

ixof

the

AR

(1)

vol

atil

ity

ofth

efi

rst

twel

ve

Eu

rod

olla

rs,

and

the

mos

tli

quid

2,5,

10,

Lon

gU

ST

reas

ury

Fu

ture

s.

20

3.4.1 Binary-Tree Model

In the pervious AR(1) formulation, we have assumed εt to be normallydistributed. However, since we are taking midpoint changes in tick, weknow that rt takes mostly {+1,−1} values. Since returns have a mean-zero,εt must also be a zero-mean process, with distribution:

εt :=

{1− βrt−1 with probability 1+βtrt−1

2

−1− βrt−1 with probability 1−βtrt−1

2

(3.1)

Now, we can construct a markovian binary tree such that each noderetains the knowledge of the last path(up/down), that led to the node. Inparticular, we can define:

unj = Pr(At node = j, time = n, last step was up)

andvnj = Pr(At node = j, time = n, last step was up)

Now, given β as the AR(1) coefficient, we can write a recursive relation forthe probabilities unj and vnj as:

unj = un−1j−11 + β

2+ vn−1j−1

1− β2

and similarly

vnj = un−1j

1− β2

+ vn−1j

1 + β

2

Also, since the sum of the probabilities should sum to 1 at each time step,we must have:

n∑j=0

(unj + vnj ) = 1, ∀ n ≥ 0

This presents us with a interesting formulation, since we may calculatethe distribution any number of time steps out. The number of time stepsis an observable which maybe obtained from the market using the num-ber of moves in the last period, or historically over the given time period.However, in the markets, often the average time taken for continuations arevastly greater than the average time for reversal, and somehow this must beincorporated in the tree structure for practical usage.

3.4.2 Vector Autoregressive Model

An obvious extension to a univariate AR(1) model would be an Vector Au-toregressive Model whereby segments of the yield curve maybe modelleddirectly. It is easy to imagine two price series being modelled on a grid,but an added complexity arises from moving to the return space. Owing

21

to irregular temporal spacing, the returns vector could not only include thestates whereby the midpoint changed, but the states whereby, for a particu-lar contract, there was no change in the in the midpoint (while the midpointmay have changed on another contract). This problem maybe mitigated bysampling the price series at fixed time interval, and using this to constructthe return series.

3.5 Contrast with other models

In literature (see [Gatheral(2010)]), a number of models for real-time volatil-ity estimation have been discussed, and we contrast the AR(1)-volatilitymodel with the some of the popular estimators.

• ARCH/GARCH estimators[Engle(1995)]: In ARCH we assumethat the returns are draws from a gaussian distribution, with thevariance following an ARMA model. The fundamental observationleading to GARCH was the positive autocorrelation in r2t , while near-zero autocorrelation in rt. These observation are invalid for the high-frequency returns in the interest-rate futures markets, and not a rep-resentative characteristic of the market.

• Zhou’s Model[Zhou(1992)]: The author comes up with volatility es-timate using tick-by-tick data for foreign exchange rates. Zhou ob-serve a very high negative first-order autocorrelation in the returns,close to -0.45 for DEM/USD rates, owing to the microstructure noiseattributed to the bid-ask bounce in trade print. This is again not adefining characteristic of the market, and would not incorporate thelarge negative serial autocorrelation in the midprice owing to flickeringquotes.

3.6 Conclusion

The quadratic variation of the residuals in the presence of an AR-1 model is apretty nice estimate for volatility. It seems to be a reliable estimator, suitablefor practical application. In particular, some of the appealing properties ofthe estimator are:

• It reproduces the characteristics and properties of the mean-revertinghigh frequency midprice changes.

• We are able to treat volatility as a observable. The process of updateof AR-1 coefficient is very fast, and this is suitable for high frequencystrategies.

22

• The parameters in the model are calibrated from the data directly,and don’t require us to tweak any parameters.

• The model inherently dampens contribution from flickering/unstablequotes.

23

Appendix A

Appendix

A.1 Properties of Interest Rate Futures

We list some of the properties of Interest Rate futures which have a signifi-cant impact on the microstructure noise.

The interest rate futures have very large minimum price increments (ticksize), as can be seen in table A.1. This forces high percentage of the liquidityto accumulate on the inside levels(See figure A.1) and crossing the spread ismore expensive.

Owing to the large minimum tick size, the interest rate futures marketsare generally single tick wide(See A.2). The multi-tick mode is often atransient state necessary for price changes, and inherently unstable.

A.2 Diffusion with Barriers

Suppose a brownian motion has absorbing barriers at x = 0 and x = 1,and the starting point is z ∈ (0, 1). Let u(x, t) be the probability density

Contract $ Value of Tick Minimum Tick Notional $ Value

Eurodollar 12.5$ 0.5 1M$2-Year Futures 15.625$ 1/128 200K$5-Year Futures 7.8125$ 1/128 100K$10-Year Futures 15.625$ 1/64 100K$

Treasury-Bond Futures 31.25$ 1/32 100K$

Table A.1: A synopsis of the minimum price increments and the notionalvalue of interest rate futures outrights contracts.

24

010

2030

4050

6070

Bid L5 Bid L4 Bid L3 Bid L2 Bid L1 Ask L1 Ask L2 Ask L3 Ask L4 Ask L5

GEH1GEM1GEU1GEZ0GEZ1ZBZ0ZFZ0ZNZ0ZTZ0

Order Book Shape

Order Book Levels

% o

f Tot

al V

olum

e in

Ord

er B

ook

Figure A.1: Figure shows the percentage of total posted liquidity at the var-ious levels on the bid and the offer. It’s important to notice that Eurodollarsand Treasuries have very thin liquidity at far away levels. [Courtesy: HaiderAli, Quantitative Brokers]

25

Contract Spread Entire Day Floor hours

Treasury Futures

(minimum ticks) %age Time %age Count %age Time %age Count

ZTH2 1 99.99 99.97 100 100

ZFZ21 93.91 97.35 99.28 98.992 5.62 2.64 0.71 1.01

ZNH21 98.62 99.05 99.91 99.742 1.37 0.94 0.09 0.26

ZBH21 93.78 96.19 98.30 97.742 6.2 3.81 1.69 2.62

Eurodollar Futures

GEH21 99.59 98.80 99.78 98.762 0.40 1.20 0.22 1.24

GEH31 91.12 97.66 99.80 99.192 8.87 2.33 0.22 0.80

GEH41 90.38 92.49 96.23 94.352 8.63 7.47 3.77 5.65

Table A.2: The amount of time and the quote changes spent in multitickmode. It is evident from the numbers that the markets (even more so duringthe floor hours) are primarily one minimum tick wide.

function associated with the particle satisfies:

ut =1

2uxx

with the boundary conditions that u(0, t) = 0 and u(1, t) = 0. The solutionfor the probability density function maybe found using infinite number ofpositive and negative sources, which yields the solution:

u(x, t) =∞∑

k=−∞[e−(x−z−2k)

2/2t − e−(x+z−2k)2/2t]

The flux φ = −12ux,

φ(x, t) =1

2t√

2πt

∞∑k=−∞

[(x−z−2k)e−(x−z−2k)2/2t−(x+z−2k)e−(x+z−2k)/2t]

A.3 AR(1) Coefficient Update

Given the regression coefficient until time t, on receiving an additional obser-vation, we may dynamically update the regression coefficient. This propertyis very useful in maintaining a real-time system, since on each inside quoteupdate, we must not retrieve the entire day’s data again. Suppose we havethe regression coefficient βt−1 and an additional data set (yt, xt) arrives,

26

where yt is the independent variable, and xt, the dependent variable. Then,

βt = (X ′tXt)−1X ′tYt

= ((Xt−1xt)′(Xt−1xt))

−1(Xt−1xt)′(Yt−1yt)

= (X ′t−1Xt−1 + x′txt)−1(X ′t−1Yt−1 + x′tyt)

where Xt = (x1, x2, . . . xt)′, and similarly Yt = (y1, y2, . . . yt)

′. Thus, if wejust store the running sum of X ′tXt and X ′tYt, then we βt+1 in O(1), withoutaccessing previous data. This makes our algorithm very fast, and we canalso calculate εt as yt − βtxt.

27

Bibliography

[Andersen(2000)] Torben G. Andersen, Tim Bollerslev, Francis X. Diebold,and Heiko Ebens. The distribution of stock return volatility. WorkingPaper 7933, National Bureau of Economic Research, October 2000.

[Bacry(2010)] E. Bacry, S. Delattre, M. Hoffmann, and J. F. Muzy. Mod-elling microstructure noise with mutually exciting point processes. sub-mitted to quantitative finance, 2010.

[Engle(1995)] Robert F. Engle. ARCH: Selected Readings. Oxford Univer-sity Press, 1995.

[Garman-Klass(1980)] Mark B Garman and Michael J Klass. On the esti-mation of security price volatilities from historical data. The Journal ofBusiness, 53(1):67–78, January 1980.

[Gatheral(2010)] Jim Gatheral and Roel C. A. Oomen. Zero-intelligencerealized variance estimation. Finance and Stochastics, 14(2):249–283,2010.

[Robert(2011)] Christian Y. Robert and Mathieu Rosenbaum. A new ap-proach for the dynamics of ultra-high frequency data: The model withuncertainity zones. Journal of Financial Econometrics, 9(2), July 2011.

[Zhou(1992)] B. Zhou and International Financial Services Research Center.High frequency data and volatility in foreign exchange rates. Workingpaper. International Financial Services Research Center, Sloan School ofManagement, Massachusetts Institute of Technology, 1992.

28