Embed Size (px)

Citation preview

Page 1 of 21

Essex Fire Authority Essex County Fire & Rescue Service

MEETING

Policy & Strategy Committee

AGENDA ITEM

5 MEETING DATE

9 May 2012

REPORT NUMBER

EFA/053/12

SUBJECT

Cycle to work Scheme

REPORT BY

The Chief Fire Officer, David Johnson

PRESENTED BY

The Director of HR & Organisational Development, Lindsey Stafford-Scott

SUMMARY The purpose of this report is to inform members of the Policy & Strategy Committee of outcomes of a recent survey into the benefits derived from previous cycle schemes run in the Service and its compliance with the ethos and rules of the Government scheme. The report recommends that ECFRS should adopt the scheme again and requests initial outlay funding through an increase in the 2012/13 capital budget. RECOMMENDATIONS Members of the Policy & Strategy Committee are asked to: 1. Agree to the running of the Cycle to Work Scheme; 2. Support initial outlay funding for the scheme of £150k within the 2012/13 capital budget. BACKGROUND The Cycle to work scheme is Government led and allows employees to hire a bike1 from an employer. The employee can choose to buy or return the bike at the end of the hire period. Whilst the organisation pays for the bike initially, this money is recouped from the employee’s salary at source over the duration of the hire period and therefore the employer does not incur any direct costs The employer recovers the VAT on the bike and has reduced NI contributions because of the

amount the employee pays to hire the bike. The overall impact, after allowing for capital financing costs will be a £10k reduction in costs for the Authority if the whole amount allocated for the scheme is utilised.

1 Bike – means bicycle and accessories

Agenda Item 5 Report No: EFA/053/12

Page 2 of 21

Page 2 of 21

The employee does not pay tax or NI contributions on the amount they pay to hire the bike. Most employees will save about 32% of the cost of the bike over the period of the hire and subsequent purchase of the bike.

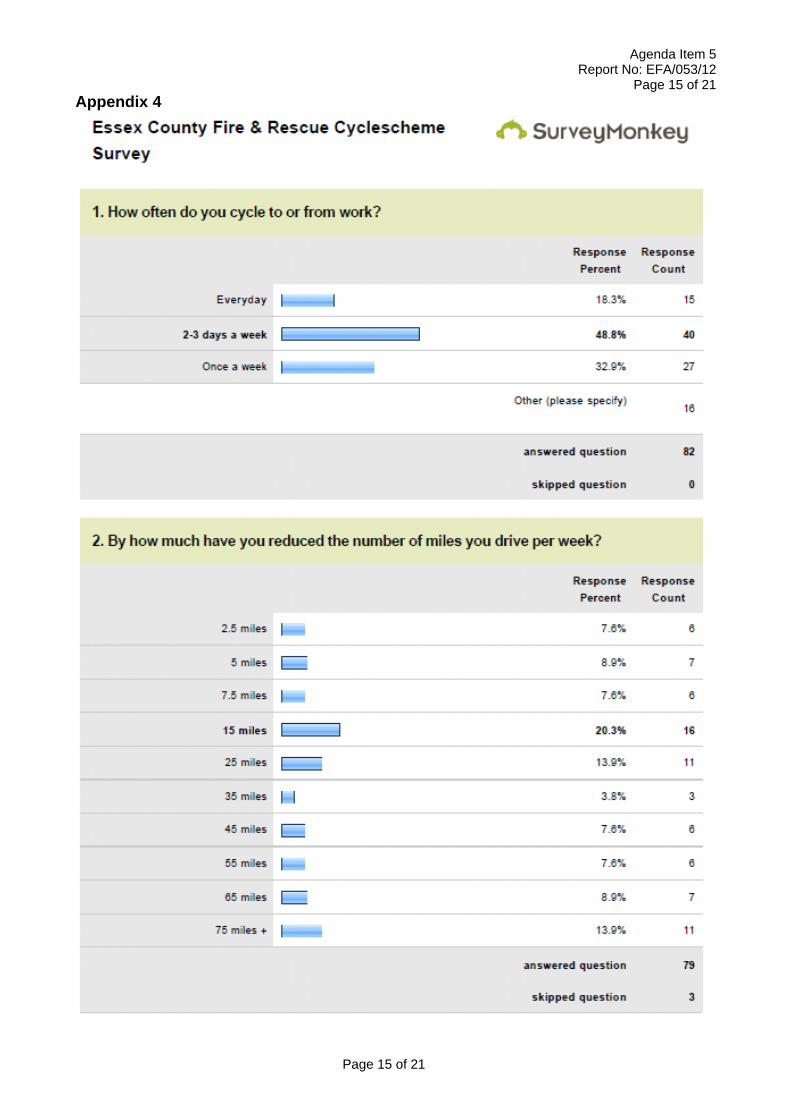

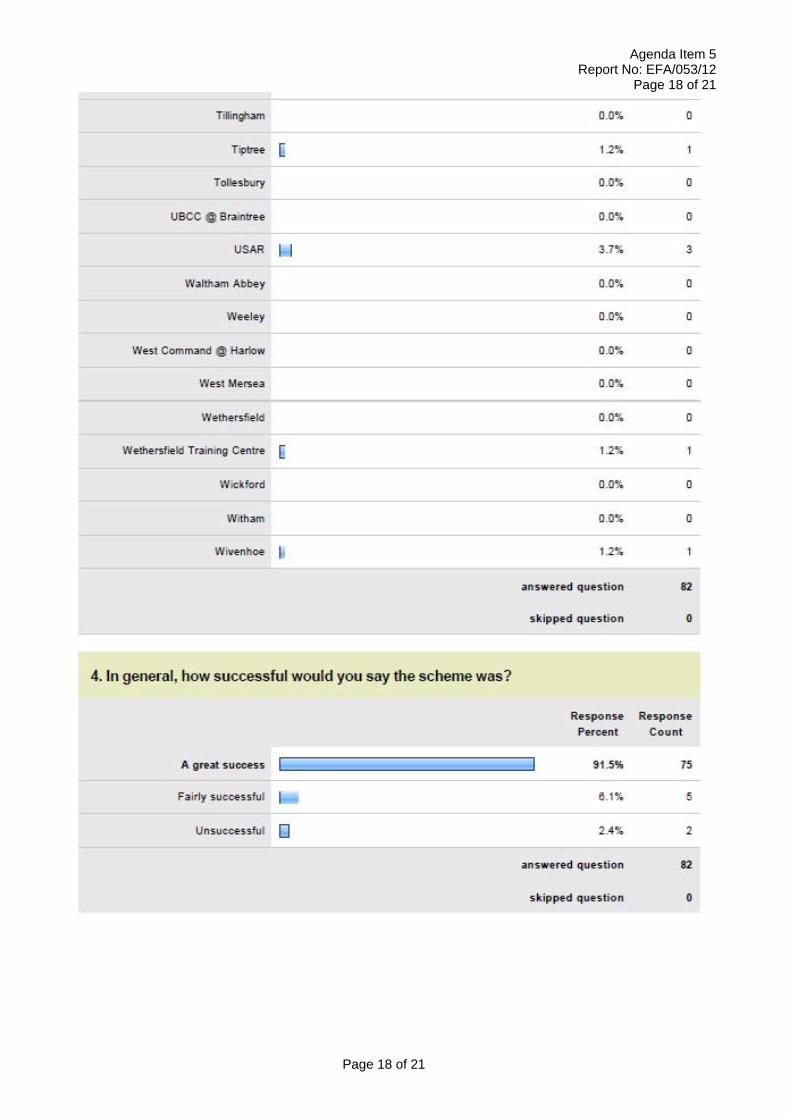

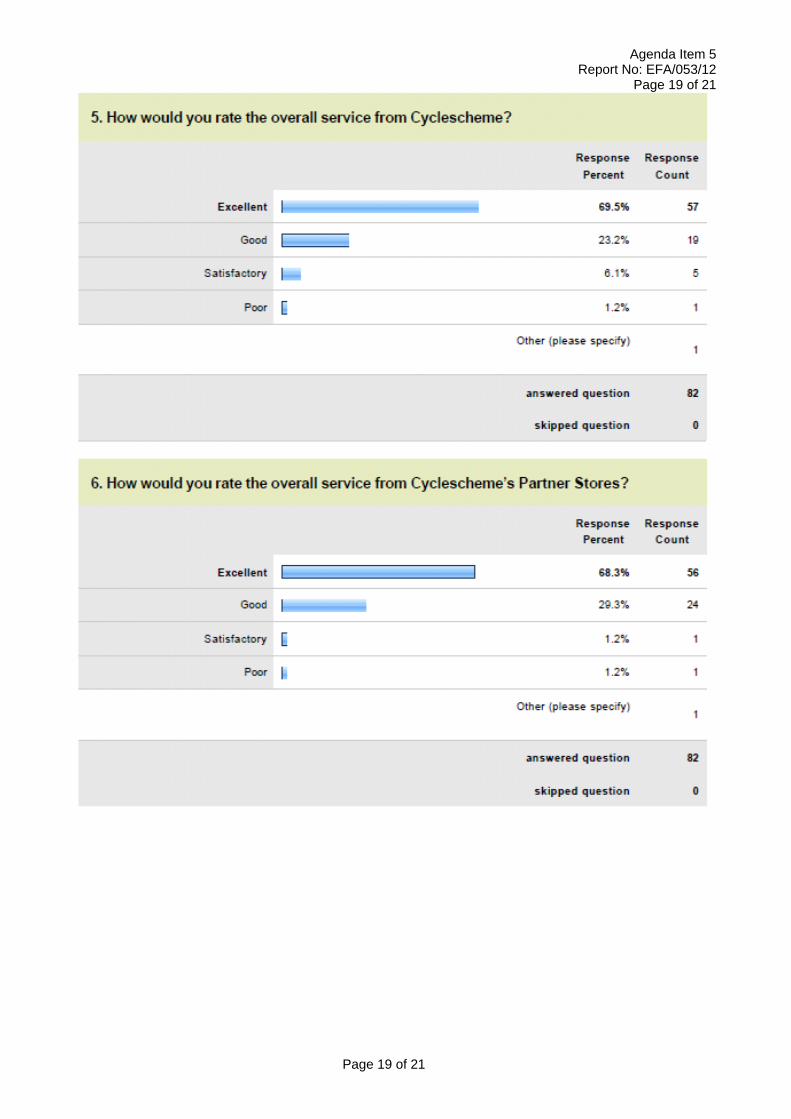

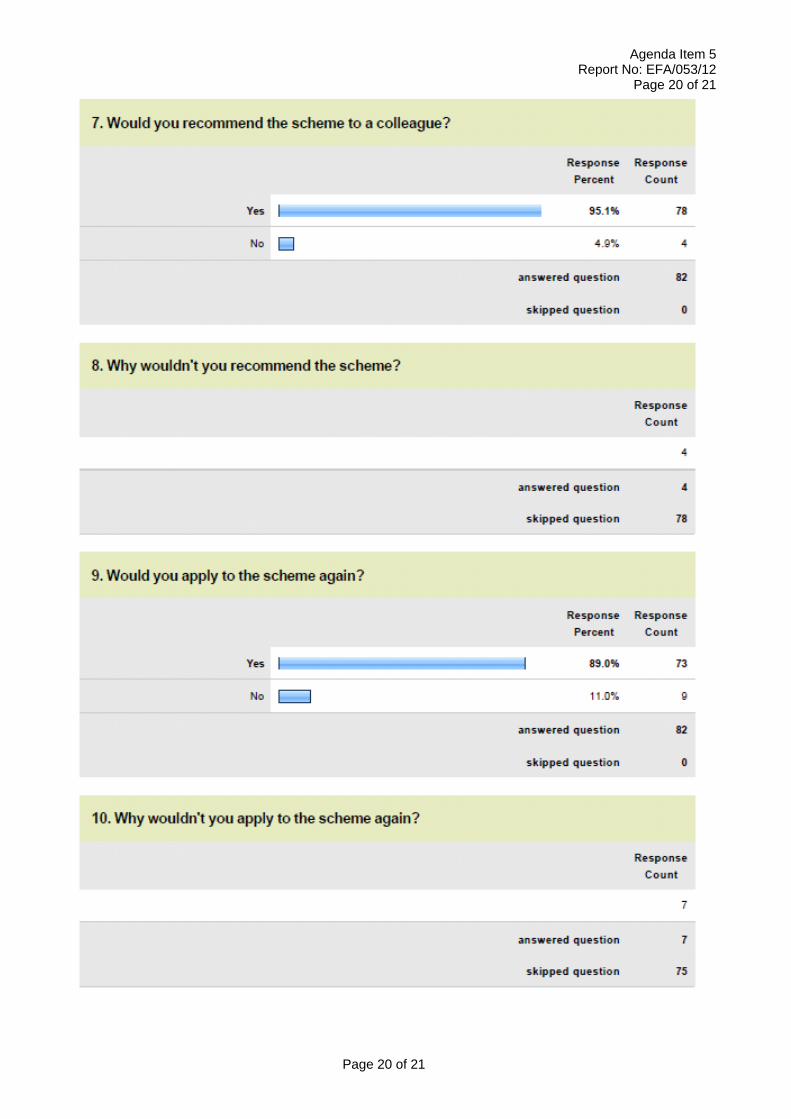

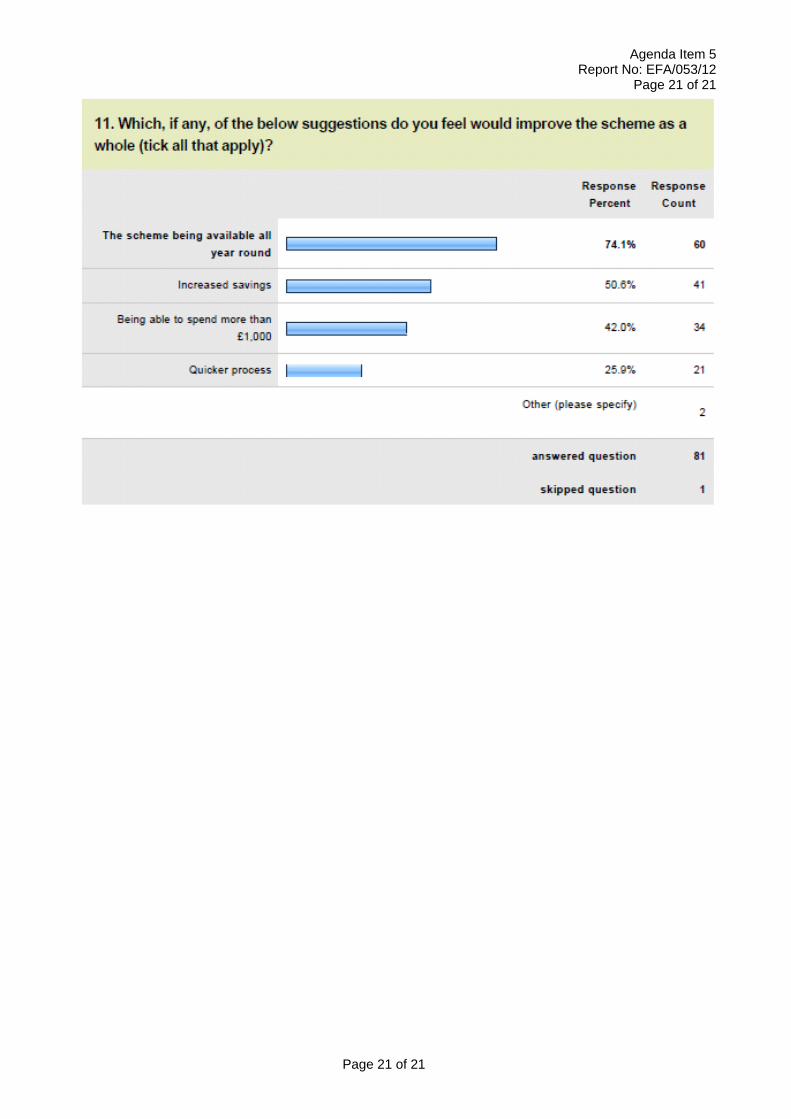

Employees should use the bike mainly for commuting to and, if relevant, between work places (at least 50% of the bike’s use should be for work purposes). However, the bike can also be used for non-work purposes and there is no need for employers to monitor individual usage or for employees to keep a mileage log. The government scheme has changed since the last time it was adopted by the Service and whilst the changes lead to longer hire periods for employees the difference in savings for both the employees and employer are negligible (see Appendix 1 – Cycle Scheme Market Value – End of Scheme Calculation). Between 2008 and 2010 a total of 496 people have chosen to take part in the ECFRS cycle to Work scheme, spending an average of £740 each. Cycles and accessories with a value of £367,000 have been purchased. The processes for both the employer and employee have not changed. (see Appendix 2 – Cycle Scheme – Process Flowchart) A survey was completed (targeting recipients of the scheme) which attracted a 16.5% response of all users of the scheme ~ 82. The results of the survey are included in Appendix 3. They report that they cycle much more than 2595 miles per week or 134,940 miles a year. At 40 miles per gallon that saves 3373 gallons of petrol or a cost of over £21,000 pounds for the 82 employees. At 1.2lb2 of carbon per mile that would be 161928lbs or 74 metric tonnes of carbon per year saved. SDO Hill has championed all ECFRS cycle to work schemes so far, and been responsible for its administration and delivery. If required he is willing to deliver the same commitment to the scheme. (It should be noted SDO Hill is not a cyclist and so there is no potential for a conflict of interest). Whilst the benefits of the scheme captured in the survey are significant and laudable in themselves, they are not the most significant. The benefits of fit and Healthy employees, valuing employees and delivering opportunity to save money, being seen to act in an environmentally responsible way, and creating a workplace that is pleasant and supportive, are not quantified but are also not undervalued. There are a number of providers of the cycle to scheme, and a tender process was completed to decide which scheme to adopt in 2008. There are no significant changes to the user requirements or the providers of the scheme in the market place. Users are demonstrably happy with the provider and there is no reason to change. There is a great deal of guidance available on the internet from Government websites and providers of the scheme. The most significant for ECFRS can be accessed via: http://assets.dft.gov.uk/publications/cycle-to-work-guidance/cycle-to-work-guidance.doc USE OF RESOURCES The scheme does have an impact on the finance section and there is a need for an entry into all participants pay records. There are also inevitable enquiries and a few issues during the life of the scheme that will need to be managed. Previous schemes have provided evidence that this is not significant and can be managed within existing resources. 2 reference: http://www.sightline.org/maps/charts/climate-CO2byMode

Agenda Item 5 Report No: EFA/053/12

Page 3 of 21

Page 3 of 21

FINANCIAL IMPLICATIONS A Cycle to Work scheme that takes advantage of the 1999 tax exemption does not require the prior approval of HMRC. Similarly, prior approval by HMRC is not required where salary sacrifice arrangements are used to offset cost. The scheme enables the Authority to recover the VAT element of the purchase price from HM Revenue and Customs and the balance from employees through a salary sacrifice scheme over the next twelve months. This cost recovery offsets the capital financing charge for the expenditure. The Authority has sufficient cash resources so that the overall loss of interest on the average outstanding balance of £75k will be under £8k and the reduction in employers’ national insurance contributions will be around £17k. ECFRS has, over the course of all previous schemes reduced employers national insurance contributions by £42k The impact on employees is outlined in Appendix .1. LEGAL IMPLICATIONS The arrangements for the salary sacrifice scheme allow the Authority to deduct any outstanding balance should an employee leave our employment during the period they are in the scheme.. EQUALITY IMPLICATIONS Access to the scheme will be dependent on the provisions of the government scheme and so no equality implications result from the content of this paper. ENVIRONMENTAL IMPLICATIONS There is a calculation of the carbon difference between car and bicycle use from the 82 responders to the survey above. The key issues in the environmental debate that surround the drive towards unmotorised transport are included below: Transport is the one sector of the economy whose emissions are still rising: since 1990,

emissions from road transport have gone up by at least 11%. The sector is responsible for at least 21.7% of carbon emissions.

According to official estimates, emissions from road traffic dominate the domestic transport sector: they accounted for approximately 92% of the total.

Commuting trips are responsible for the greatest proportion of carbon emissions from household car journeys (~25%); and journeys under 5 miles account for about 20% of carbon emissions from household car journeys.

If the amount of mileage cycled in Britain were doubled by reducing car use, this would reduce carbon emissions by 0.6 million tonnes per year.

CTC (UK’s National Cyclist Organisation) calculates that the average person making a typical daily commute of 4 miles each way would save half a tonne of carbon per year – or 6% of their personal carbon footprint – by switching from driving to cycling.

The Government and the NHS acknowledge the threat to the nation’s health of the twin crises of obesity and climate change. Cycling has the potential to help tackle both.

RISK MANAGEMENT IMPLICATIONS There are no significant risk management implications as a result of the content of this paper.

Agenda Item 5 Report No: EFA/053/12

Page 4 of 21

Page 4 of 21

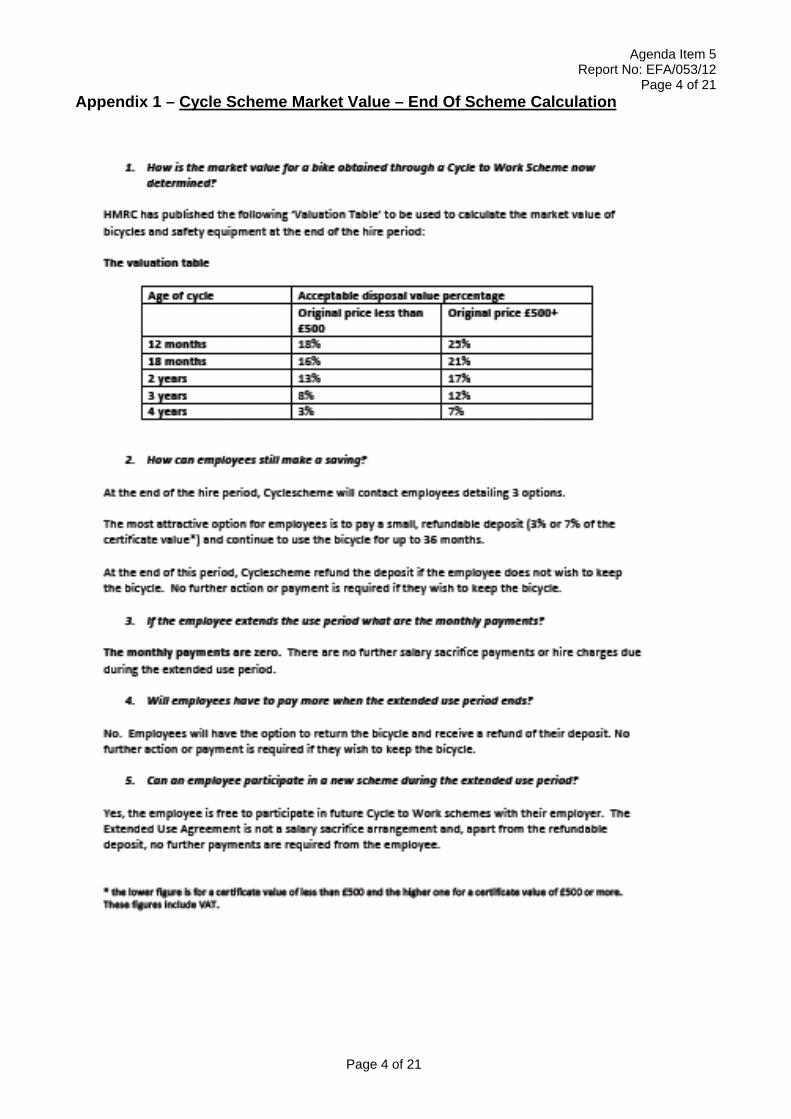

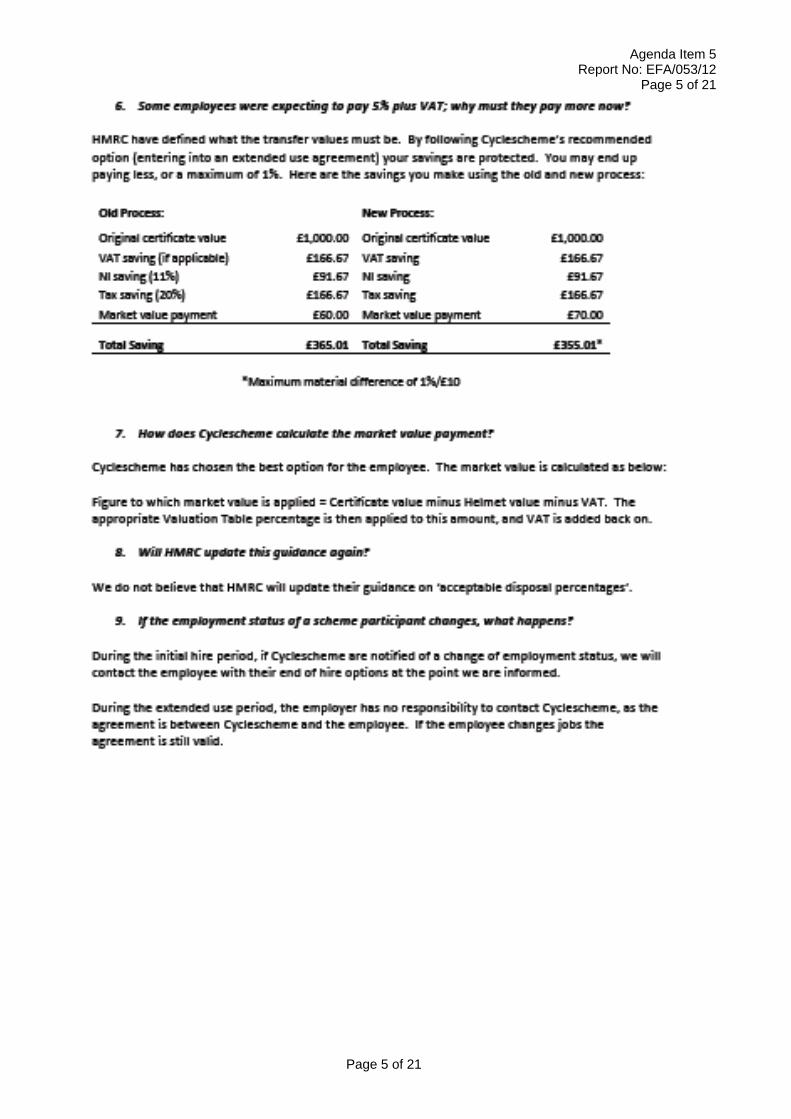

Appendix 1 – Cycle Scheme Market Value – End Of Scheme Calculation

Agenda Item 5 Report No: EFA/053/12

Page 5 of 21

Page 5 of 21

Agenda Item 5 Report No: EFA/053/12

Page 6 of 21

Page 6 of 21

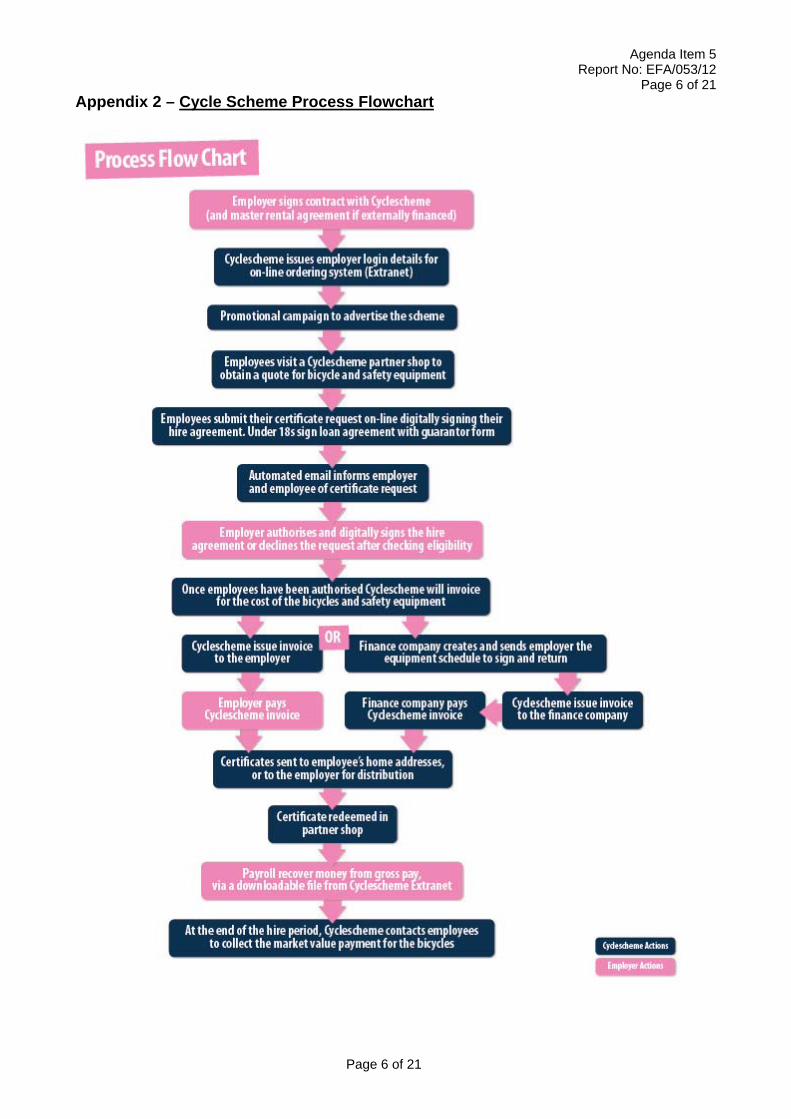

Appendix 2 – Cycle Scheme Process Flowchart

Agenda Item 5 Report No: EFA/053/12

Page 7 of 21

Page 7 of 21

Appendix 3 - Frequently Asked Questions when using the ‘Cycle Scheme Provider’ What is the cycle to work scheme and who are Cyclescheme? The cycle to work initiative enables employers to lease bicycles and associated safety equipment to their employees through what’s called salary sacrifice. This means that employees receive income tax and National Insurance savings that can be equivalent up to 41% (average 32%) of the suggested retail price of the chosen bike and safety equipment package. How does the scheme work? 1. Go to the Cyclescheme website to check your savings at www.cyclescheme.co.uk/employercode 2. You find your local Cyclescheme Partner Shop by visiting the Cyclescheme website or by contacting the Cyclescheme helpdesk on 0844 879 5 101 or [email protected]; 3. Visit a shop and choose bike and equipment- the shop will complete a Cyclescheme Quotation Form detailing the equipment; 4. You then enter the details from the shop online via the following link: www.cyclescheme.co.uk/employercode An online hire agreement will also be signed at this stage; 5. Your employer will need to approve your request and then pay an invoice from Cyclescheme for the full retail amount of your bike package; 6. Cyclescheme posts out the certificate, to your home address, via first class post; 7. You take the certificate to the bike shop, along with photographic ID, and sign the certificate to acknowledge receipt of the bike and equipment; 8. Your gross salary is reduced by the salary sacrifice amount and spread over the agreed payment period of 12 months; 9. On completion of the hire term Cyclescheme will contact you to discuss your end of hire options What is a salary sacrifice arrangement? A salary sacrifice happens when an employee agrees to give up part of their pay in return for some form of non-cash benefit, in this case the loan of a bicycle and related safety equipment provided by their employer. How are savings made? Savings are made because salary sacrifice reduces the gross salary - before any tax or NI has been deducted - so the amount of tax and NI paid is less than usual. What are the savings? Typical savings are 32% of the price of the bike and equipment for employees who pay the basic rate of tax - the precise amount depends on your personal tax band. An individual being taxed at the higher rate will save 41%. Adding the ability to spread payments over one year still means that great benefits are to be made. For an example of your potential savings, please see the savings calculator on www.cyclescheme.co.uk/employercode should you have any problems with accessing this, please contact Cyclescheme’s helpdesk on; 0844 879 5 101 or [email protected] What eligibility checks are made?

Agenda Item 5 Report No: EFA/053/12

Page 8 of 21

Page 8 of 21

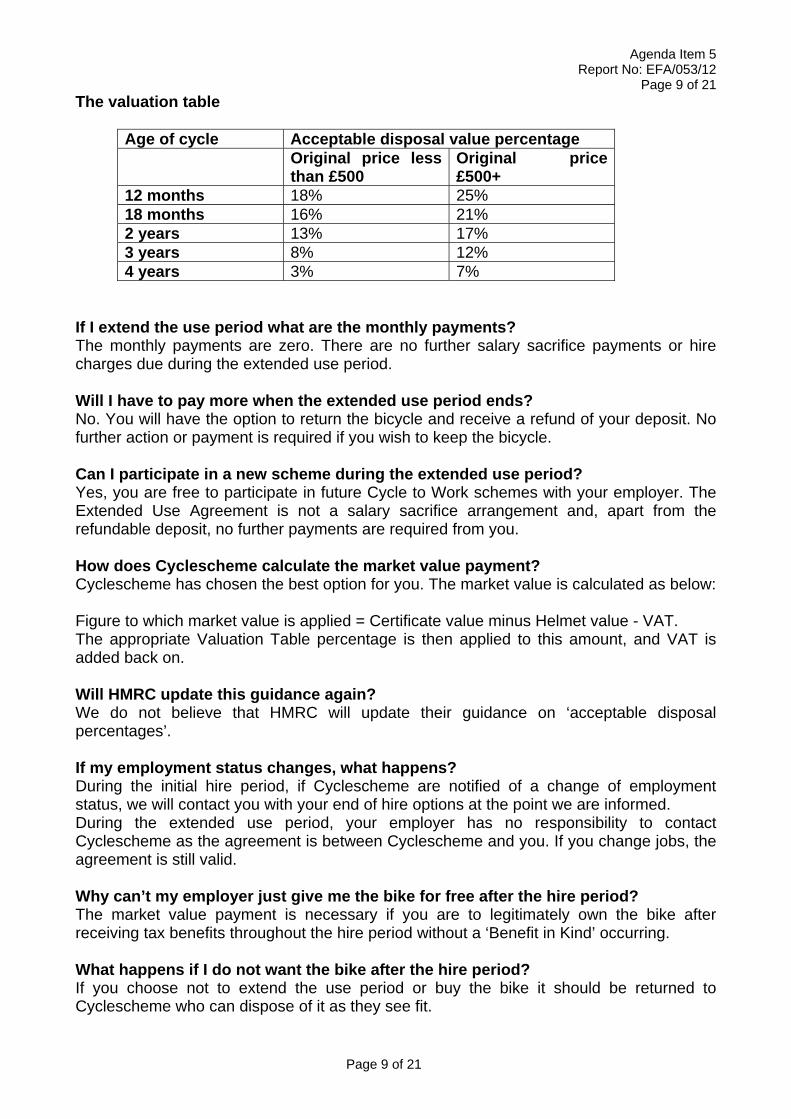

Your employer will check that your gross pay remains above the National Minimum Wage once your requested certificate value is taken into account. How long does it take to get a certificate through the scheme? Please allow up to 4 to 6 weeks from applying to receive your certificate through the post. How do I get my certificate? Cyclescheme will post the certificate directly to your home address. How long is a certificate valid for? Cyclescheme certificates are valid for 60 days from the date of issue. Can certificates be cancelled? Once the hire agreement is signed the agreement is non-cancellable after 7 days following the day after collection of the goods. What happens if I leave my employment or made redundant during the hire period? All outstanding money must be recovered from your net salary. This is because the bike is no longer being used to ride to work so no longer qualifies for any tax exemption. Cyclescheme will then contact you to discuss end of hire options. What is an employer code? An employer code is a unique code that follows the usual Cyclescheme web address and gains you access to your employers’ Cyclescheme web portal www.cyclescheme.co.uk/employercode From here, you can obtain accurate savings calculations, find a local bike shop, and request a certificate. Who actually owns the bike? The bike and equipment remain the property of your employer throughout the hire period. The ownership is then transferred to Cyclescheme at the end of your hire period who will contact you to discuss your options. What happens at the end of the hire period? Cyclescheme will then contact you at the end of the hire period detailing 3 options. The most attractive option for you is to pay a small, one-off, refundable deposit (3% or 7% of the certificate value*) and continue to use the bicycle for up to 36 months. At the end of this period, Cyclescheme refund the deposit if you do not wish to keep the bicycle. No further action or payment is required if you wish to keep the bicycle. How is the market value for a bike obtained through a Cycle to Work Scheme now determined? HMRC has published the following ‘Valuation Table’ to be used to calculate the market value of bicycles and safety equipment at the end of the hire period:

Agenda Item 5 Report No: EFA/053/12

Page 9 of 21

Page 9 of 21

The valuation table

Age of cycle Acceptable disposal value percentage Original price less

than £500 Original price £500+

12 months 18% 25% 18 months 16% 21% 2 years 13% 17% 3 years 8% 12% 4 years 3% 7%

If I extend the use period what are the monthly payments? The monthly payments are zero. There are no further salary sacrifice payments or hire charges due during the extended use period. Will I have to pay more when the extended use period ends? No. You will have the option to return the bicycle and receive a refund of your deposit. No further action or payment is required if you wish to keep the bicycle. Can I participate in a new scheme during the extended use period? Yes, you are free to participate in future Cycle to Work schemes with your employer. The Extended Use Agreement is not a salary sacrifice arrangement and, apart from the refundable deposit, no further payments are required from you. How does Cyclescheme calculate the market value payment? Cyclescheme has chosen the best option for you. The market value is calculated as below: Figure to which market value is applied = Certificate value minus Helmet value - VAT. The appropriate Valuation Table percentage is then applied to this amount, and VAT is added back on. Will HMRC update this guidance again? We do not believe that HMRC will update their guidance on ‘acceptable disposal percentages’. If my employment status changes, what happens? During the initial hire period, if Cyclescheme are notified of a change of employment status, we will contact you with your end of hire options at the point we are informed. During the extended use period, your employer has no responsibility to contact Cyclescheme as the agreement is between Cyclescheme and you. If you change jobs, the agreement is still valid. Why can’t my employer just give me the bike for free after the hire period? The market value payment is necessary if you are to legitimately own the bike after receiving tax benefits throughout the hire period without a ‘Benefit in Kind’ occurring. What happens if I do not want the bike after the hire period? If you choose not to extend the use period or buy the bike it should be returned to Cyclescheme who can dispose of it as they see fit.

Agenda Item 5 Report No: EFA/053/12

Page 10 of 21

Page 10 of 21

What is the hire period? 12 months with the same period for salary sacrifice. What happens if I leave my employment before the end of the hire period? Under the terms of the Hire Agreement and the Credit Consumer Act, the agreement to pay the loan is non-cancellable. All outstanding monies must be paid to your employer from your net salary. Cyclescheme will then contact you to discuss transfer options at the end of the hire period. How many times can I take part in the scheme? Once per year - you can take part in the scheme again once the initial hire term is over. How often does the bike have to be used for work? Neither you nor your employer is required to keep a mileage log. The bike can be used out of work but you are expected to use the bike mainly for qualifying journeys (between home and workplace or between one workplace and another). You may be liable to lose your tax exemption if they do not use the bike mainly for qualifying journeys. Typically, your employer would report this benefit in kind on form PIID and you would be liable for the tax due. Is there a minimum or maximum spend? There is no minimum spend for bike applications, however, a complete bike must be obtained (i.e. not bike components or safety equipment only). As for maximum spend, the government has issued a blanket Consumer Credit Licence to all participating employers buying bike packages up to £1000. Can I pay my own money over £1000 to get a more expensive bike? Cyclescheme do not allow for a cash contribution from you to top up the certificate as this may cause shared ownership issues. You may select a bike up to the maximum of £1000, but in this case any safety equipment must be paid for with your own money. Who is responsible for maintaining the bike? By signing the Hire Agreement you are agreeing to maintain the bike in accordance with the manufacturers instructions. Whose responsibility is it to insure the bike? You are responsible to adequately insure the bike, even though your employer owns it. When you sign the hire agreement you are agreeing to insure the bike. Insurance companies should be advised that your employer has an interest in the goods to be insured. Most home contents insurance covers cycles to a certain value, but should other insurance be required, Cyclescheme recommends Cycleguard who offers 10% discount for Cyclescheme customers. See www.cycleguard.co.uk/cs for more information. What happens if the bike gets stolen or damaged beyond repair before the end of the hire period? If the bike is adequately insured, the insurance company will replace the bike and the hire agreement will continue. If the bike is not adequately insured and the bike is not replaced, the hire agreement will be terminated by all remaining reductions coming out of the net salary and no further tax benefits will be received.

Agenda Item 5 Report No: EFA/053/12

Page 11 of 21

Page 11 of 21

What bike shops can be used? Cyclescheme is partnered with nearly all-independent bike shops in the UK, which means that you can choose almost any bike and safety equipment you wish. Local shops can be found via a postcode search on the Cyclescheme website or by contacting the Cyclescheme helpdesk on 0844 879 5 101 or [email protected]; Please note that Halfords, Evans, and Wheelies are not Cyclescheme Partner Shops. If I already have a bike, can bike components or just safety equipment be obtained through the scheme? No, a complete bike must be obtained with each certificate obtained through the scheme. What does ‘safety equipment’ include? The bike shop will be able to advise as to what is permitted under the rules of the scheme and it is ultimately the decision of your employer, but as a guide, child seats, helmets, lights (including dynamos), mirrors, mudguards, cycle clips and dress guards, panniers, locks, bells, pumps, puncture repair kits, multi- tools, reflective clothing and spoke reflectors are all permitted. Children’s bikes and bikes for other family members/ friends are not permitted. Can more than one bike be obtained on the same certificate? It is possible to hire two bikes to you, if for example, you needed a bike at either end of a train journey between your home and place of work, but the maximum spend of £1,000 per certificate must still be adhered to. Can sale bikes be obtained through Cyclescheme? Any new bike from any Cyclescheme Partner Shop can be obtained, including sale bikes. However, as Partner Shops have agreed to sacrifice a small commission to Cyclescheme, if a bike shop has marked a bike down in the sale to a price which would have an extremely low profit margin on it, or even be sold at a loss to the shop, then they may wish to add a 10 or 12% surcharge to the bike. This is only permitted if made explicit to the customer before a quotation form is completed. The only other occasion when a charge of up to 12% may be applied to the retail price of a bike is when purchasing custom bikes. This is because the profit margins on custom bikes built in the UK, are lower than those available on standard, mass-produced bikes. The shop also has additional administration when building a custom bike, as parts have to be ordered in advance and in-house builds coordinated amongst other daily work. Can bikes be procured via a mail order specialist? Cyclescheme’s Partner Shops are capable of supplying bike packages mail order from their shops through the Cycle to Work scheme. However, there are distinct advantages when getting a bike from a local bike shop which will be the first port of call for advice, servicing, after sales and warranty. Please note that, because of this deficiency, some mail- order or on-line specialists are not part of the Cyclescheme Partner network. Can special-order bikes be obtained or must existing stock be selected? Partner Shops can order bikes and accessories but may wish to either take a deposit or have any carriage fees covered to prevent them from being left with a special-order bike or paying extra carriage fees. Any deposits taken on a credit card will be credited back when the certificate is redeemed. Please note that Cyclescheme does not insist on deposits being taken and all such transaction requests are at the discretion of the bike shop or at the request of the Employee.

Agenda Item 5 Report No: EFA/053/12

Page 12 of 21

Page 12 of 21

Are electric-assist bikes allowed in the scheme? Yes, electric-assist bikes are available through the scheme. Are bikes for disabled people available on the scheme? Yes, any new bike that will be used for the correct purposes from any Cyclescheme Partner Shop can be obtained through the scheme. However, there is usually a £1000 maximum certificate amount that must be adhered to. Can second hand bikes be obtained through Cyclescheme? Cyclescheme does not allow second hand bikes to be obtained because your rights are not protected to the same extent as with new bikes. We are also concerned that the right size of bike may not be obtained and that existing wear and tear could compromise the first year’s hire during which time you are responsible for its maintenance and roadworthiness. Your employer will also want a full warranty to be available during the hire period and it is unlikely that the Partner Shop can provide this with a used bike. Is there a credit check? There is no credit check. How will salary sacrifice affect out of hours payments paid on top of salary? In calculating all other payments to employees such as out of hour’s payments, the total unreduced pay will be used. What happens when there is a pay award? You will receive any relevant pay awards based on their unreduced salary. How will salary sacrifice affect pension? The scheme will not affect your pension. Pensionable earnings are calculated on your gross pay before any salary sacrifice you may have in place. How will salary sacrifice affect approved unpaid leave? During approved unpaid leave such as extended maternity leave or career break, up to a maximum of six months, the Hire Agreement period may be extended by the number of months when the salary was not paid and your employer were not able to collect payments How will salary sacrifice affect sickness leave? If you are absent from work during the Hire Period the salary sacrifice will continue to reduce any pay that is received during the period of absence, as long as and to the extent that: the pay is of a kind against which Salary Sacrifice reductions can legally be made

and so excluding for example, statutory maternity pay, paternity, adoption and sick pay; and

the continuation of salary sacrifice arrangements is not in breach of the National Minimum Wage regulations.

If during a period of absence from work you are temporarily not in receipt of sufficient pay so as to allow for the Salary Sacrifice to continue, but they remain an employee of your employer, then to the extent allowable by law: the Salary Sacrifice payments envisaged by this agreement will be suspended for the

period in question; and

Agenda Item 5 Report No: EFA/053/12

Page 13 of 21

Page 13 of 21

the Hire Period will be extended for an equivalent period of time to allow payments to be made-up once they return to work.

How will salary sacrifice affect maternity, paternity, or parental leave? Your employer now have to provide non-cash contractual benefits for the whole of the Maternity Pay Period (MPP) - this covers Ordinary Maternity Leave (the first 26 weeks) and Additional Maternity Leave (the following 26 weeks). Your employer must allow the hire of the cycle to continue during maternity the leave in question, but that the underlying salary sacrifice arrangement can only operate against any Enhanced Maternity Pay as detailed above and not Statutory Maternity Pay (SMP) as SMP cannot be reduced under any circumstances. Your employer will allow you to remain in possession of the bike and the salary sacrifice reductions can continue when you return, only if the hire period has not expired. If you do not return to work, you will be considered an early leaver, and any remaining balance left if the hire period has not expired should be paid by you within 14 days of employment ceasing. What happens if I am made redundant or my contract is terminated? Employees with sufficient service and who meet certain other conditions may be entitled to statutory payments on redundancy. It is possible, though unlikely, that such payments could be affected when you join the scheme. If you leave your employer before the final reduction has been made from salary, you will be obliged to pay the remaining amount in full, without any tax exemptions as described in ‘What I leaves my employer before the end of the hire period?’ How will salary sacrifice affect student loan payments? Student loan repayment is based on a percentage of earnings over an allocated amount. This will alter as the trigger point is based on the salary on which you are liable to pay National Insurance Contributions (NICS). Under salary sacrifice the total gross salary on which NI is paid will reduce, so the loan repayments will reduce. How will salary sacrifice affect Childcare Tax Credit? Current advice from the Inland Revenue suggests that individuals can still apply for Childcare Tax Credit whilst being in a salary sacrifice scheme. For more information, check with the Inland Revenue advice line on 0845 300 3900. How will salary sacrifice affect Working Tax Credit? The vast majority of staff will benefit from joining the scheme. However, personal circumstances may mean that it is not beneficial. This is most likely to be the case for those on a low income affected by Working Tax Credit, which may cancel out the savings made on Income Tax and National Insurance Contributions. Please seek advice from the Inland Revenue Tax Credits helpline on 0845 300 3900. Why does the Hire Agreement show a much lower saving than expected? The salary sacrifice amount shown on the Hire Agreement states that it will come from the gross salary – before any tax or NI has come off – meaning that the amount of tax and NI that will be paid is reduced (as PAYE and NI are calculated as a percent of salary). Cyclescheme is unable to put the actual (net) amount that will be deducted, as we do not

Agenda Item 5 Report No: EFA/053/12

Page 14 of 21

Page 14 of 21

know how much tax you pay. The easiest way to establish the near-exact monthly savings can be found on our website savings calculator at www.cyclescheme.co.uk/employercode.

Agenda Item 5 Report No: EFA/053/12

Page 15 of 21

Page 15 of 21

Appendix 4

Agenda Item 5 Report No: EFA/053/12

Page 16 of 21

Page 16 of 21

Agenda Item 5 Report No: EFA/053/12

Page 17 of 21

Page 17 of 21

Agenda Item 5 Report No: EFA/053/12

Page 18 of 21

Page 18 of 21

Agenda Item 5 Report No: EFA/053/12

Page 19 of 21

Page 19 of 21

Agenda Item 5 Report No: EFA/053/12

Page 20 of 21

Page 20 of 21

Agenda Item 5 Report No: EFA/053/12

Page 21 of 21

Page 21 of 21