Embed Size (px)

Citation preview

ESSENTIALThe Private Sector’s Role in Development

IFC Presentation, Dec 8, 2015 to RGIT

1

Vorbemerkung

Dr. Thomas Rehermann

Senior Strategy Officer

Corporate Strategy Department

International Finance Corporation – The World Bank Group, Washington, DC

The slides carry the name of the author and should be cited accordingly. The findings,

interpretations, and conclusions expressed in these slides are entirely those of the

author. They do not necessarily represent the views of the International Finance

Corporation / World Bank and its affiliated organizations, or those of the Executive

Directors of the World Bank or the governments they represent.

TABLE OF CONTENTS

2

IFC and the World Bank Group (Slides 2- 4)

Introduction to IFC (Slides 5 -12)

How IFC Creates Opportunity (Slides 13 - 16)

IFC's Business, Reach and Results (Slides 17 - 36)

PROVIDING DEVELOPMENT SOLUTIONS … Customized To Meet Client Needs

A member of the World Bank Group

Provides investment, advice,

resource mobilization

AAA credit rating; nearly 60-year

history in emerging markets

Present in 100 countries

3

IFC is the largest global development institution focused exclusively

on the private sector in developing countries.

4

Conciliation

and arbitration

of investment

disputes

Guarantees of

foreign direct

investment’s

non-

commercial

risks

Interest-free

loans and

grants to

governments

of poorest

countries

Loans to

middle-income

and credit-

worthy low-

income country

governments

Solutions

in

private

sector

development

IBRD

International

Bank for

Reconstruction

and

Development

IDA

International

Development

Association

IFC

International

Finance

Corporation

MIGA

Multilateral

Investment

Guarantee

Agency

ICSID

International

Centre for

Settlement of

Investment

Disputes

IFC: A MEMBER OF THE WORLD BANK GROUP

Ending

Extreme

Poverty

Boosting

Shared

Prosperity

From 18%

to 3% of world

population by

2030

Increased incomes

for bottom 40% of

every country

Private sector investment is ESSENTIAL

5

THE WORLD BANK GROUP’S TWIN GOALS

6

7

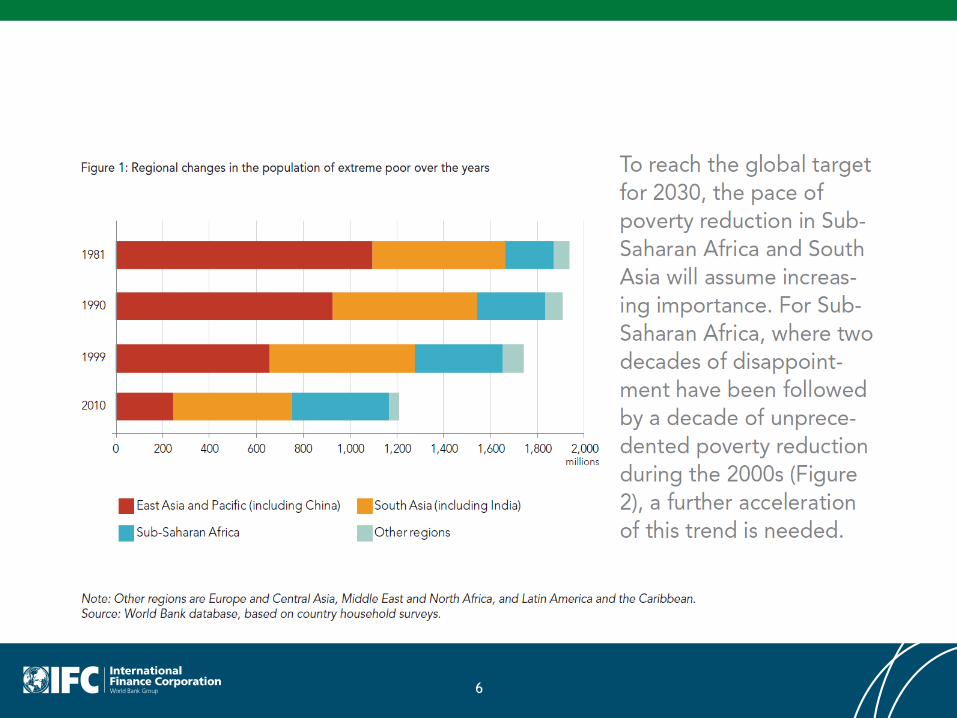

The extreme Poor since 1820

• Around 1820, there were about one billion people living

in poverty by the standards of today’s poorest countries.

• That was then over 80% of the world’s population.

• On a comparable basis (as best we can determine),

there are still over one billion people who are poor by

this measure today.

• But now less than 20%.

8Source: Martin Ravallion, More relatively-poor people in a less absolutely-poor world. Presentation

provided at WBG, Dec 3, 2013.

Huge progress over 200 years

9

0

20

40

60

80

100

1800 1820 1840 1860 1880 1900 1920 1940 1960 1980 2000

Bourguignon-Morrisson

Chen-RavallionGlobal poverty rate (% below $1 a day)

1.5 billion people!

1950 saw a turning point, with much faster progress against extreme poverty

Source: Martin Ravallion, More relatively-poor people in a less absolutely-poor world. Presentation

provided at WBG, Dec 3, 2013.

Uneven but huge overall progress against

absolute poverty in China since 1980

10

0

20

40

60

80

100

1980 1984 1988 1992 1996 2000 2004 2008 2012

Poverty rate for China

Poverty rate for developing world less China

Poverty rate (% of population living below $1.25 a day at 2005 PPP)

Source: Martin Ravallion, More relatively-poor people in a less absolutely-poor world. Presentation

provided at WBG, Dec 3, 2013.

But this is not just about success in China!

Since 2000 we have

seen a marked

acceleration in

absolute poverty

reduction outside

China.

11

0

10

20

30

40

50

1980 1983 1986 1989 1992 1995 1998 2001 2004 2007 2010

Headcount index (% below $1.25 a day; excluding China)

0.4% point per year

1.0% point per year

MDGs?

Source: Martin Ravallion, More relatively-poor people in a less absolutely-poor world. Presentation

provided at WBG, Dec 3, 2013.

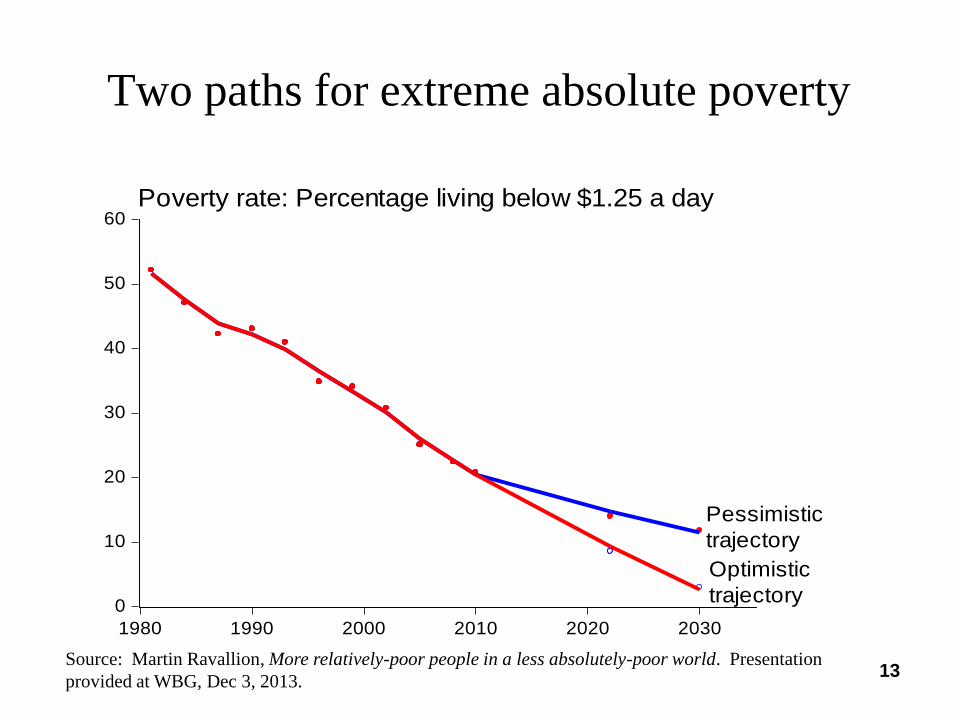

Looking forward: the pessimistic benchmark

for absolute poverty

• This assumes that the developing world outside China

returns to its pre-2000 pace of poverty reduction, but

China remains on track.

• Projecting the series forward, this implies that the

number of poor would fall from 1.1 billion in 2012 to 0.9

billion by 2022, and 0.8 billion by 2030.

• Almost one billion people will still be poor in 2030.

• This path will take 50 years to lift one billion people out

of poverty!

12Source: Martin Ravallion, More relatively-poor people in a less absolutely-poor world. Presentation

provided at WBG, Dec 3, 2013.

Two paths for extreme absolute poverty

13

0

10

20

30

40

50

60

1980 1990 2000 2010 2020 2030

Poverty rate: Percentage living below $1.25 a day

Optimistic

trajectory

Pessimistic

trajectory

Source: Martin Ravallion, More relatively-poor people in a less absolutely-poor world. Presentation

provided at WBG, Dec 3, 2013.

Where the poor are - absolutely and most prevalently

14

*Top ten countries according to share of global poor at $1.25/day: India (34.0%), China (13.30%), Nigeria (9.1%), Bangladesh (5.5%), DRC (4.4%), Indonesia (3.7%),

Pakistan (3.0%), Tanzania (2.4%), Ethiopia (2.2%), Philippines (1.4%)

**Top ten countries according to poverty headcount ratio at $1.25/day: DRC (87.7%), Liberia (83.8%), Madagascar (81.3%), Burundi (81.3%), Malawi (73.9%), Zambia

(68.5%), Nigeria (68.0%), Tanzania (67.9%), Rwanda (63.2%), Central African Republic (62.8%),

Source: PovCalNet URL: “http://iresearch.worldbank.org/PovcalNet/index.htm?0”

• India (IDA Blend) and China

(non-IDA) house approx. 558

million, 47% of world’s

extreme poor

• Nearly 80% of world’s

extreme poor are in ten

countries*: India, China,

Nigeria, Bangladesh, DRC,

Indonesia, Pakistan, Tanzania,

Ethiopia, Philippines. Almost

90% are in 20 countries,

• On poverty headcount ratio (%

population poor), most

prevalently poor in this

cohort are in Africa

15

Frontier markets

Climate change

and environmental

& social sustainability Local financial

markets

Long-term

client relationships

in emerging markets

Strategic

Focus

Areas

Constraints to private sector growth in infrastructure,

health, education, and the food supply chain

HOW IFC HELPS END EXTREME POVERTY

AND BOOST SHARED PROSPERITY

16

Loans, grants, equity

investments, guarantees,

and advice to support

development

*Excluding mobilizations

($7.1 bn)

Recipient-Executed

Trust Funds

$3.9

IFC* – $10.6

MIGA

$2.8

IDA

$19

IBRD

$23.5

All dollar figures are in US$ bn

39%

17%

32%

5%7%

WORLD BANK GROUP COMMITMENTS, FY15Total Commitments: Nearly $60 BN

17

IFC’S HISTORYA Global Institution, Now Owned By 184 Member Countries

IFC Launch

PSD added to

the global

economic

agenda

IFC coins

term

“emerging

markets”

IFC scales up

Investments

and builds

global

advisory

footprint

The global

leader in

private

sector

development

1990-

2000s19801956 Today

18

30+ IFIs/DFIs

Host County

Governments

Sovereign

Wealth Funds/

Institutional

Investors

900 Financial

Institution Clients

Civil Society

2,000+ Clients

20+ Bilateral Donors/

15+ Private

Foundations

IFC’S GLOBAL

NETWORK FOR

SOLUTIONS

THE POWER OF PARTNERSHIPS

IFC: A VALUABLE PARTNERWe Help Clients In Good Times And Bad By Offering:

19

A strong financial position, strategy, staff

Low leverage ratios, prudent risk management policies

A long-term partnership perspective, providing clients important

countercyclical financing when commercial banks cut back

The expertise and experience needed to make a difference,

focusing on innovative transactions where our development

impact is the highest

20

WHAT CLIENTS VALUE ABOUT IFC Results of IFC Client Survey

Long-Term

Partner Role

Stamp of

Approval

Financing

Not Readily

Available

Elsewhere

Worldwide

Presence

Global

Expertise and

Knowledge

Affiliation

with the

World Bank

Group

Ability to

Mobilize

Additional

Funds

Pricing

21

BUSINESS RESULTS:

Profitability,

Competitiveness,

Client Satisfaction

IFC’s Results

DEVELOPMENT IMPACT:

Helping the Private Sector

Reduce Poverty &

Foster Inclusive Growth

IFC

Clients

INNOVATION Innovation in key areas

INFLUENCEInfluence on outcomes

DEMONSTRATIONDemonstration effect on

others

IMPACTImpact on development

IFC’s Brand Value

CREATING OPPORTUNITY WHERE IT’S NEEDED MOST What IFC Delivers

Creating OPPORTUNITY

Unlocking CAPITAL

Promoting GROWTH

Driving IMPACT

22

BUILDING THE PRIVATE SECTOR’S ROLE IN

4 ESSENTIAL WAYS

Create jobs

Expand women’s

opportunities

Modernize health and

education

23

DEMOCRATIC REPUBLIC OF CONGO

Helping the private sector:

The private sector provides 90%

of the developing world’s jobs.

Inclusive growth is ESSENTIAL.

ESSENTIALHow IFC Creates OPPORTUNITY

Mitigate risks

Raise environmental,

social, and governance

standards

Attract new investment

needed for growth

24

BHUTAN

Helping the private sector:

90% of the world’s future population

growth will be in cities.

Sustainable urbanization is ESSENTIAL.

ESSENTIALHow IFC Unlocks CAPITAL

Strengthen infrastructure

Boost SMEs

Provide access to finance

25

INFRASTRUCTURE

Helping the private sector:

There is enormous need for new infrastructure.

Increased private investment is ESSENTIAL.

ESSENTIALHow IFC Promote GROWTH

Spark innovation

Provide essential goods

and services

Promote inclusive growth

26

EGYPT

Helping the private sector:

2.5 billion adults still lack access to basic

financial services.

Greater financial inclusion is ESSENTIAL.

ESSENTIALHow IFC Drives IMPACT

27

INVESTMENT

(Loans, Equity, Trade Finance, Syndications,

Derivative and Structured Finance, Blended Finance)

ADVICE

(Value-adding knowledge; either integrated into IFC investments or

standing alone at a broader level)

IFC ASSET MANAGEMENT COMPANY

(Mobilizing and Managing Capital for Investment)

4 Focus

Industries:

3 Product

Areas:

MANUFACTURING

AGRIBUSINESS

AND SERVICES

FINANCIAL

INSTITUTIONS

INFRASTRUCTURE

AND NATURAL

RESOURCES

TELECOMMUNICATIONS

AND INFORMATION

TECHNOLOGY

Creating Opportunity Where It’s Needed Most

WHAT WE DO: THREE MUTUALLY REINFORCING SERVICESIntegrated Solutions, Increased Impact

28

Loans Project and corporate financing

On-lending through intermediary institutions

Equity Direct equity investments

Private equity funds

Trade Finance

And Supply

Chain

Guarantee of trade-related payment obligations of

approved financial institutions

Syndications Capital mobilization to serve developmental needs

Over 60 co-financiers: banks, funds, DFIs

Derivative and

Structured

Finance

Derivative products to hedge interest rate, currency, or

commodity-price exposures of IFC clients

Blended Finance Augmenting IFC resources with donor funds

INVESTMENT

29

Financial Sector Increasing access to finance

Helping financial institutions increase financing for

housing, sustainable energy, and micro/SMEs

Investment

Climate

Supporting government reforms that attract and retain

private investment

Public-Private

Partnerships

Helping governments with PPPs in power, water, health

and education

Agribusiness Improving clients’ productivity and standards

Focusing on efficient food value chains and food security

Energy and

Resource

Efficiency

Helping clients develop solutions across the value chain

Accelerating development of commercial markets for

renewables

Cross-Cutting Gender, corporate governance, supply chains, others

ADVICE

IFC Capitalization Fund

IFC African, Latin American

Africa Capitalization Fund

IFC Russian Bank Capitalization Fund

IFC Catalyst Fund

IFC Global Infrastructure Fund

China-Mexico Fund

IFC Financial Institutions Growth Fund

IFC Global Emerging Markets Fund Of Funds

30

AMC FUNDS

IFC Asset

Management

Company had about

$8.5 BILLION in assets under

management in FY15

IFC ASSET MANAGEMENT COMPANY

IFC’S GLOBAL REACH

108 regional offices present in 100

countries worldwide, AAA credit rating

3,358 staff (59% are based outside

Washington DC)

31

32 32

Note: IFC changed its reporting practice regarding investment amounts, beginning in the current fiscal year. To align our

approach with that of commercial banks, we now report short-term finance investments separately from long-term

investments. Short-term investments are reported as the average outstanding balance for the year. This chart reflects five

years’ worth of data, calculated under the new reporting policy.

7.5

9.2

11.010.0

10.6

6.5 5.0

6.5

5.1

7.1

0.0

2.0

4.0

6.0

8.0

10.0

12.0

14.0

16.0

18.0

20.0

FY11 FY12 FY13 FY14 FY15

IFC's Own Account Mobilization

$17.7 bn

$15.1 bn

$17.5 bn

$14.2 bn$14 bn

FY15 LONG-TERM INVESTMENT COMMITMENTS: $17.7 Billion

45%

19%

13%

7%

5%

5%3%3%

Financial Markets

Infrastructure

Agribusiness & Forestry

Consumer & SocialServices

Oil, Gas, & Mining

Funds

Manufacturing

Telecommunications &Information Technology

33

FY15 LONG-TERM COMMITMENTS BY INDUSTRYCommitments For IFC’s Account: 10.6 Billion

23%

22%

17%

15%

13%

8%2%

Latin America and theCaribbean

East Asia and thePacific

Sub-Saharan Africa

Europe and Central Asia

South Asia

Middle East and NorthAfrica

Global

34

FY15 LONG-TERM COMMITMENTS BY REGIONCommitments For IFC’s Account: 10.6 Billion

32%

20%11%

8%

8%

7%

5%

5%4%

Financial Markets

Infrastructure

Manufacturing

Consumer & Social Services

Funds

Agribusiness & Forestry

Oil, Gas, & Mining

Trade Finance

Telecommunications &Information Technology

35

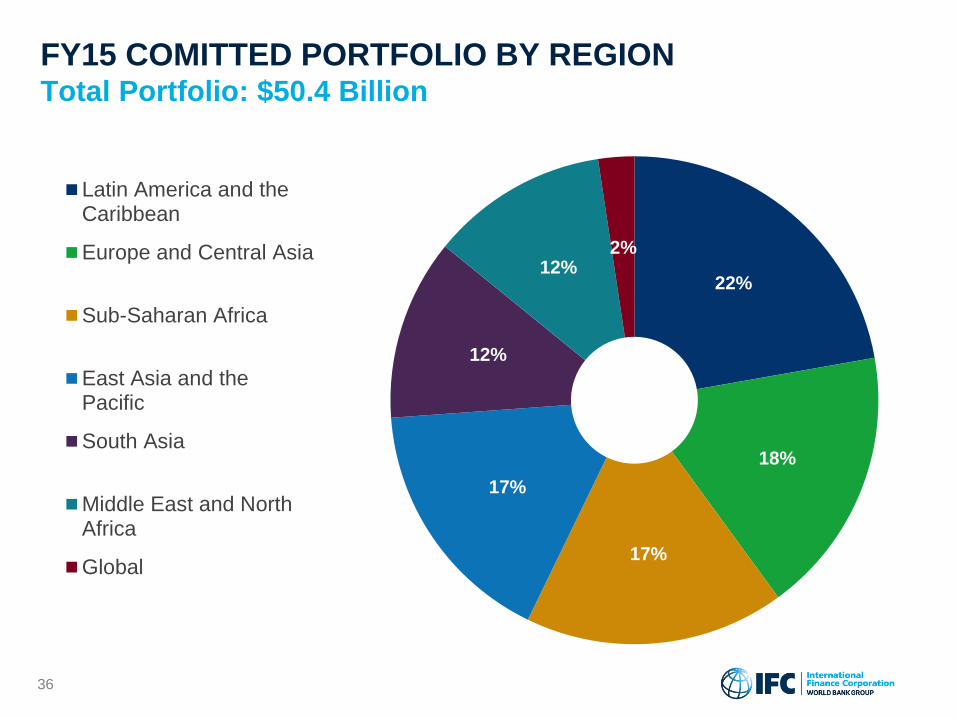

FY15 COMITTED PORTFOLIO BY INDUSTRYTotal Portfolio: $50.4 Billion

22%

18%

17%

17%

12%

12%2%

Latin America and theCaribbean

Europe and Central Asia

Sub-Saharan Africa

East Asia and thePacific

South Asia

Middle East and NorthAfrica

Global

36

FY15 COMITTED PORTFOLIO BY REGIONTotal Portfolio: $50.4 Billion

37

BUSINESS

LINES

CLIENT

ENGAGEMENTS

Financial Sector* 425

Investment Climate* 151

Public-Private Partnerships 102

Agribusiness 102

Energy & Resource Efficiency 102

Cross-Industry 102

*Delivered through integrated WBG global practices

Total Portfolio: $1.2 Billion

FY15 ACTIVE ADVISORY PORTFOLIO

BY BUSINESS LINE

38

ANNEX

39

2.5 million jobs

Health services to 17.3 million

patients

Education to 3.5 million students

Improved opportunities for 3.4 million

farmers

Power generated for 55.8 million

customers

Water distribution to 23.4 million

people

THE REACH OF IFC’S

PROJECTS—2015

INDIA

48 million microfinance and SME loans,

totaling $270 billion

965,000 housing finance loans,

totaling $22 billion

237 million people receiving phone

connections

26.4 million people purchasing

affordable off-grid lighting

16 million people with improved

infrastructure and health services from

18 new PPPs

40

THE REACH OF IFC’S

PROJECTS—2015

TURKEY

41

$17.7 billion in long-term investment:

• $10.6 billion for IFC’s own account,

• $7.1 billion mobilized

$50.4 billion committed portfolio

$4.7 billion invested in IDA Countries

Long-Term Investments: 406 new

projects in 83 countries

Advice: 65% of program in IDA

countries, 20% in fragile and conflict-

affected areas

FISCAL YEAR 2015

HIGHLIGHTS

PHILIPPINES

42

1Assessment and management of environmental and social risks and impacts

2 Labor and working conditions

3 Resource efficiency and pollution prevention

4 Community, health, safety and security

Land acquisition and involuntary resettlement

Biodiversity conservation and sustainable management of living natural resources

Cultural heritage

Indigenous peoples

5

6

7

8

STANDARD SETTINGOur Performance Standards

43

Moscow

Minsk

Kiev

WarsawLondon

Frankfurt

Zagreb BelgradeBucharest

SofiaTirana Istanbul

Tbilisi

Yerevan Baku

Dushanbe

BishkekAlmaty

Rabat

Cairo

Jerusalem

Dubai

Tashkent

KabulIslamabad

Karachi

Sana’a

Paris

Brussels

Beirut

Amman

Tunis

ATLANTIC

OCEAN

Mediterranean

Sea

Black Sea

Aral

Sea

Barents

Sea

North

Sea

IFC Hub Offices

IFC Operational Centers

IFC Offices

Vienna

Baghdad

Sarajevo Pristina

IFC IN WESTERN EUROPE, THE MIDDLE EAST,AND NORTH AFRICA

44

Istanbul

St. Petersburg

Tirana

Zagreb

Sarajevo

Moscow

Warsaw

Belgrade

SofiaSkopje

Bucharest

Kiev

Minsk

Tbilisi

Yerevan Baku

Dushanbe

Kabul

Tashkent

BishkekAlmaty

IFC Hub Offices

IFC Operational Centers

IFC Offices

Vienna

IFC IN EUROPE AND CENTRAL ASIA

45

PACIFIC

OCEAN

INDIAN

OCEAN

Ulaanbaatar

BishkekTashkent

DushanbeKabul

Islamabad

Karachi

New Delhi

Mumbai

Colombo

Beijing

Tokyo

Dhaka

HanoiVientiane

Ho Chi Minh City

Phnom Penh

Bangkok

Hong Kong

Manila

JakartaDili Port Moresby

Sydney

Almaty

Yangon

Kathmandu

Thimphu (Bhutan)

Singapore

Honiara

IFC Hub Offices

World Bank Group Hub Office

IFC Country Offices

Seoul

IFC IN ASIA AND THE PACIFIC

IFC Hub Offices

IFC Country Offices

Caribbean Sea

ATLANTIC

OCEAN

Gulf of Mexico

PACIFIC

OCEAN

ATLANTIC

OCEAN

Rio de Janeiro

Buenos Aires

La Paz

Lima

Bogota

Port-of-Spain

Santo Domingo

Managua

Mexico City

São Paulo

Port-au-Prince

TegucigalpaGuatemala City

Kingston

San Salvador

46

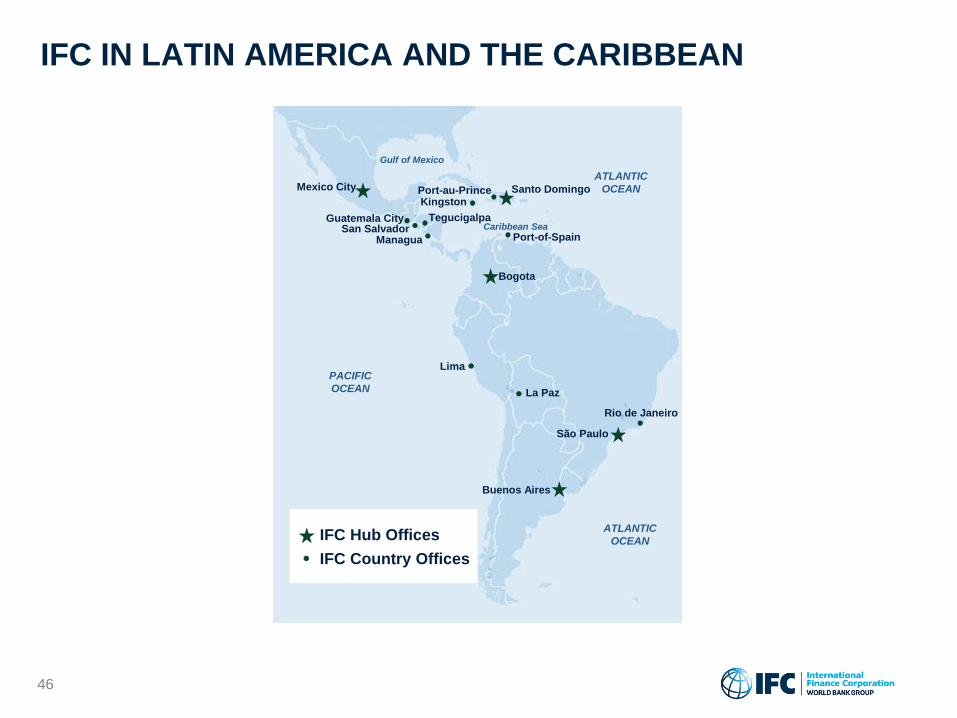

IFC IN LATIN AMERICA AND THE CARIBBEAN

47

IFC Hub Offices

IFC Country Offices

ATLANTIC

OCEAN

Mediterranean

Sea

INDIAN

OCEAN

JohannesburgMaputo

Antananarivo

Lusaka

Freetown

NairobiKigali

Douala

N’Djamena

LagosAccra

Ouagadougou

Abidjan

Dakar

CairoAmman

JerusalemBeirut

Algiers

Rabat

Sana’a

Dubai

Monrovia

Kinshasa

Addis Ababa

Dar es-Salaam

Bujumbura

Bamako

Bangui Juba

Tunis

AbujaConakry

IFC IN SUB-SAHARAN AFRICA