Embed Size (px)

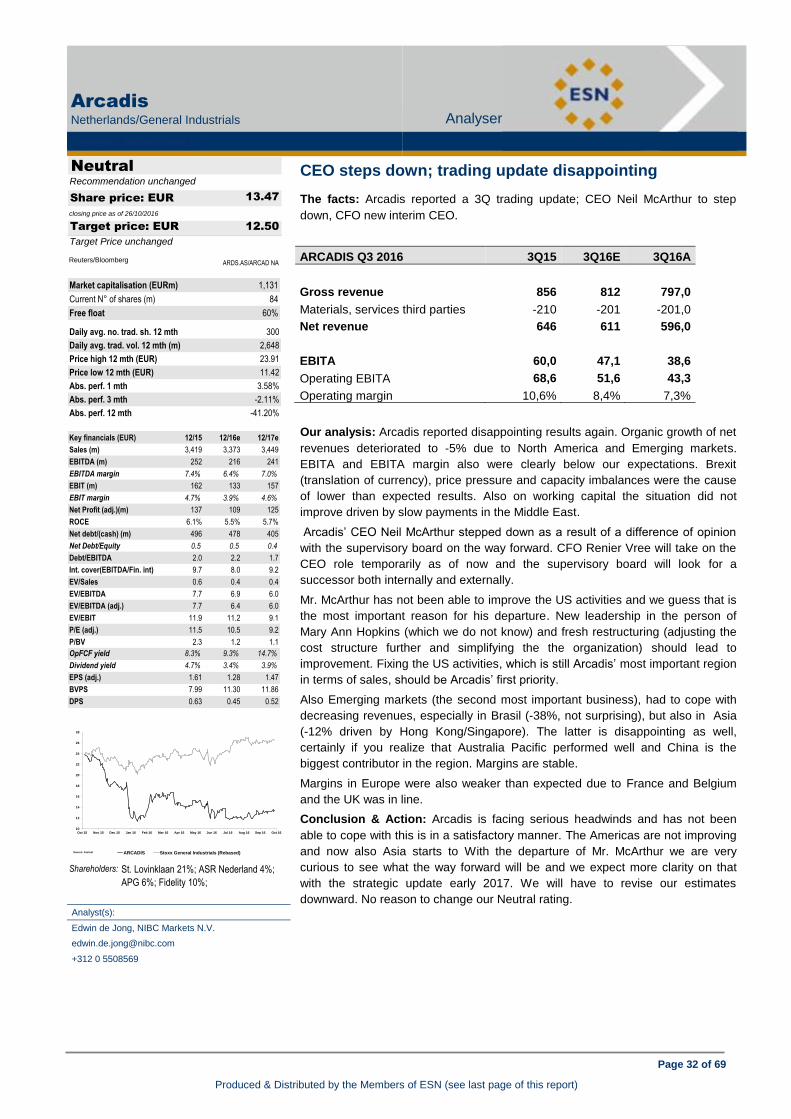

Citation preview

ESN Analyser

Investment Research

Page 1 of 69

Produced & Distributed by the Members of ESN (see last page of this report)

ESN Analyser

Investment Research

27 October 2016

ESN Top Picks

Roadshows

Corporate Events

Tactical Sector Views

RECOMMENDATION CHANGES

UniCredit downgraded to Accumulate from Buy Possible liability management exercise?

Nordea downgraded to Neutral from Accumulate Increased certainty about dividend but 2017 earnings under pressure

Bittium Corporation downgraded to Accumulate from Buy Q3 preview: Will the Mexsat design project alter H2 profitability?

Vaisala upgraded to Buy from Accumulate Profitability heading towards the target of 15%

Cramo upgraded to Accumulate from Neutral Convincingly controlled earnings growth

Fcc downgraded to Neutral from Accumulate EBITDA and working capital recovering

NEWS BY SECTOR

AEROSPACE & DEFENSE

Lisi (Accumulate) Q3-2016 sales: a gradual increase in growth

AUTOMOBILES & PARTS

Bittium Corporation (Accumulate) Q3 preview: Will the Mexsat design project alter H2 profitability?

ElringKlinger (Neutral) Acquisition of a minority stake in hofer AG

BANKS

Sector News Portuguese Banks: Exposure to Mozambique

Banco Sabadell (Buy) 3Q’16 forecasts: EUR215m (-5.4% Y/Y)

BBVA (Buy) 9M 16 earnings: EUR2,797m (-0.6% adjusted)

BPI (Neutral) 9M16 results: Positive results (NII in Angola and provisions/asset quality in Portugal). ROE at 10.5%

BPI (Neutral) GSM to vote on the sale of 2% of BFA (Angola) to Unitel

CaixaBank (Neutral) 3Q’16 results preview: EUR930m (-6.7% Y/Y)

Deutsche Bank (Neutral) Q3 results above expectations due to lower one-offs

Mediobanca (Accumulate) Q1 results preview

Nordea (Neutral) Increased certainty about dividend but 2017 earnings under pressure

UniCredit (Accumulate) Possible liability management exercise?

BASIC RESOURCES

Acerinox (Buy) Comments from 3Q’16 results presentation

Ence (Buy) 9m’16 results

Europac (Accumulate) Good 9m’16 results

CHEMICALS

Kemira (Accumulate) Defending the margins

ESN Analyser

Investment Research

Page 2 of 69

Produced & Distributed by the Members of ESN (see last page of this report)

ELECTRONIC & ELECTRICAL EQUIPMENT

Kontron (Buy) Weak Q4 guidance but restructuring in focus

Vaisala (Buy) Profitability heading towards the target of 15%

FINANCIAL SERVICES

FinecoBank (Buy) The new cyborg advisory platform became fully operational

FOOD & BEVERAGE

Atria (Accumulate) Q3 results fell short of forecasts, the acquisition price of Well Beef Ltd very cheap

Ebro Foods (Neutral) Good 9m’16 results and 2016 close anticipated

Rémy Cointreau (Neutral) Small acquisition in premium whiskey

FOOD & DRUG RETAILERS

Kesko (Neutral) Earnings outlook improved, a good selling price for grocery trade in Russia

GENERAL INDUSTRIALS

Arcadis (Neutral) CEO steps down; trading update disappointing

Huhtamäki (Accumulate) Earnings missed expectations – focus remains on growth

HEALTHCARE

Amplifon (Accumulate) 9M 16 results: sales and profitability better than expected

Recordati (Accumulate) 9M 16 results preview

INDUSTRIAL ENGINEERING

Kone (Neutral) Alleviation to concerns related to China

Konecranes (Neutral) Weak orders, savings advancing

INSURANCE

Banca Mediolanum (Accumulate) ECB against Fininvest’s significant stake in BMED

MATERIALS, CONSTRUCTION & INFRASTRUCTURE

Abertis (Accumulate) Better profitability and good traffic growth

Cramo (Accumulate) Convincingly controlled earnings growth

Fcc (Neutral) EBITDA and working capital recovering

Ferrovial (Accumulate) Neutral results

MEDIA

Gruppo Ed. L'Espresso (Accumulate) 9m 2016 Post: surprising advertising growth in Q3

Ipsos (Buy) Confirmation of the return to growth with a good Q3-16

Mediaset Espana (Buy) Weak 3Q results, but cost guidance improved

OIL & GAS PRODUCERS

Eni (Buy) Q3 2016 preview: one-offs are due to affect production

Repsol (Buy) Agreement in Bolivia

OIL SERVICES

Technip (Buy) Q3 results better than expected, 2016 outlook raised

Vopak (Buy) Updates estimates and target + VTTI deal read through

ESN Analyser

Investment Research

Page 3 of 69

Produced & Distributed by the Members of ESN (see last page of this report)

SOFTWARE & COMPUTER SERVICES

Altran (Buy) Q3-2016 revenue in line

ICT Group (Accumulate) Ongoing good revenue growth, guidance reiterated

SUPPORT SERVICES

Ei Towers (Accumulate) Q3 2016 Pre: uneventful quarter in sight

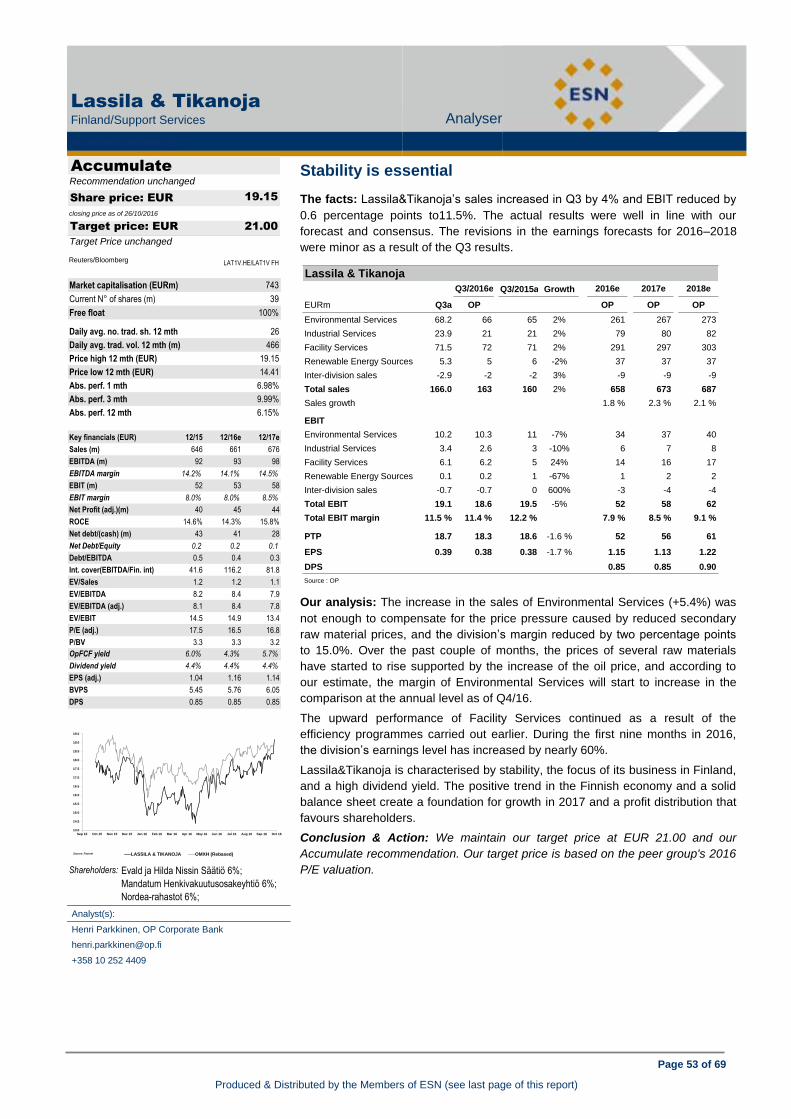

Lassila & Tikanoja (Accumulate) Stability is essential

TECHNOLOGY HARDWARE & EQUIPMENT

ASM International (Buy) Q3 numbers ok; outlook weakish

Besi (Neutral) Another strong quarter

Ingenico (Buy) Mixed trends with no improvement in the outlook

SLM Solutions (Buy) Fundamentals now in focus

STMicroelectronics (Neutral) Q3 & 9M 16 release: positive results

TELECOMMUNICATIONS

KPN Telecom (Buy) 3Q16: EBITDA increases YoY but FCF disappoints

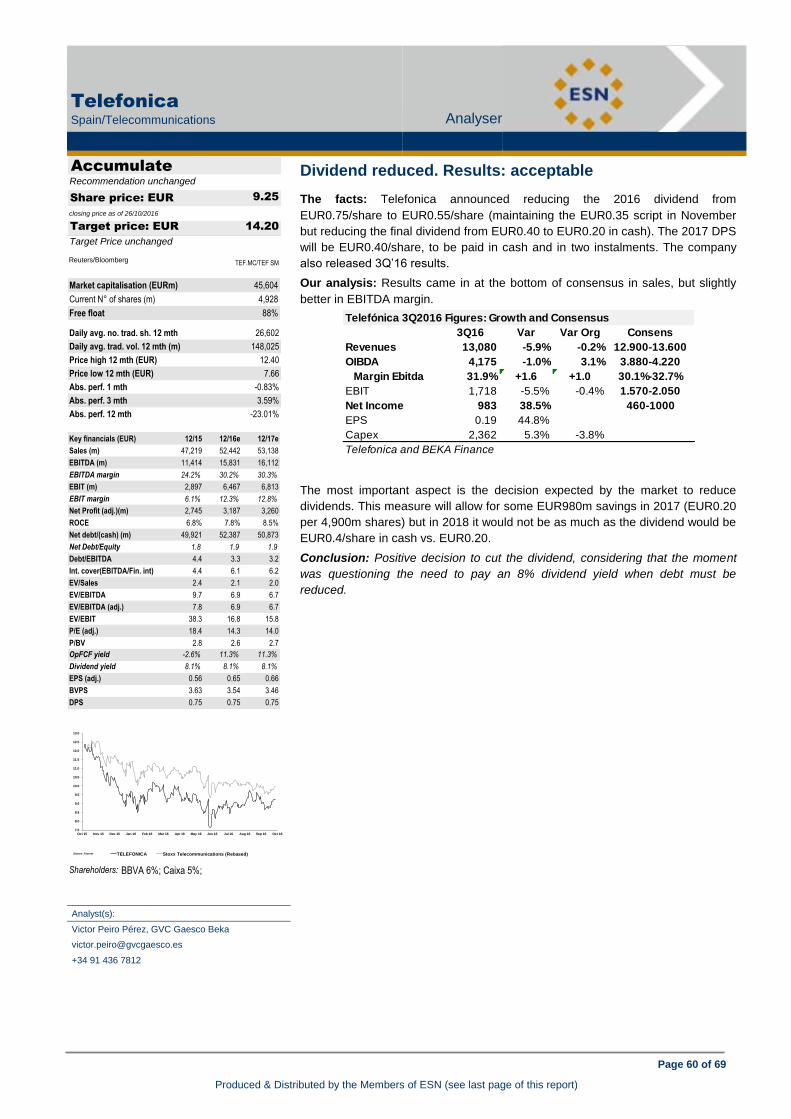

Telefonica (Accumulate) Dividend reduced. Results: acceptable

TRAVEL & LEISURE

Int. Airlines Group (Buy) Agreement in principle of the NAPS

UTILITIES

EDP Renováveis (Buy) 9M16 results preview: comparisons affected by positives one offs in the previous year and

increase in financial costs

Terna (Neutral) Not on the seaside this summer

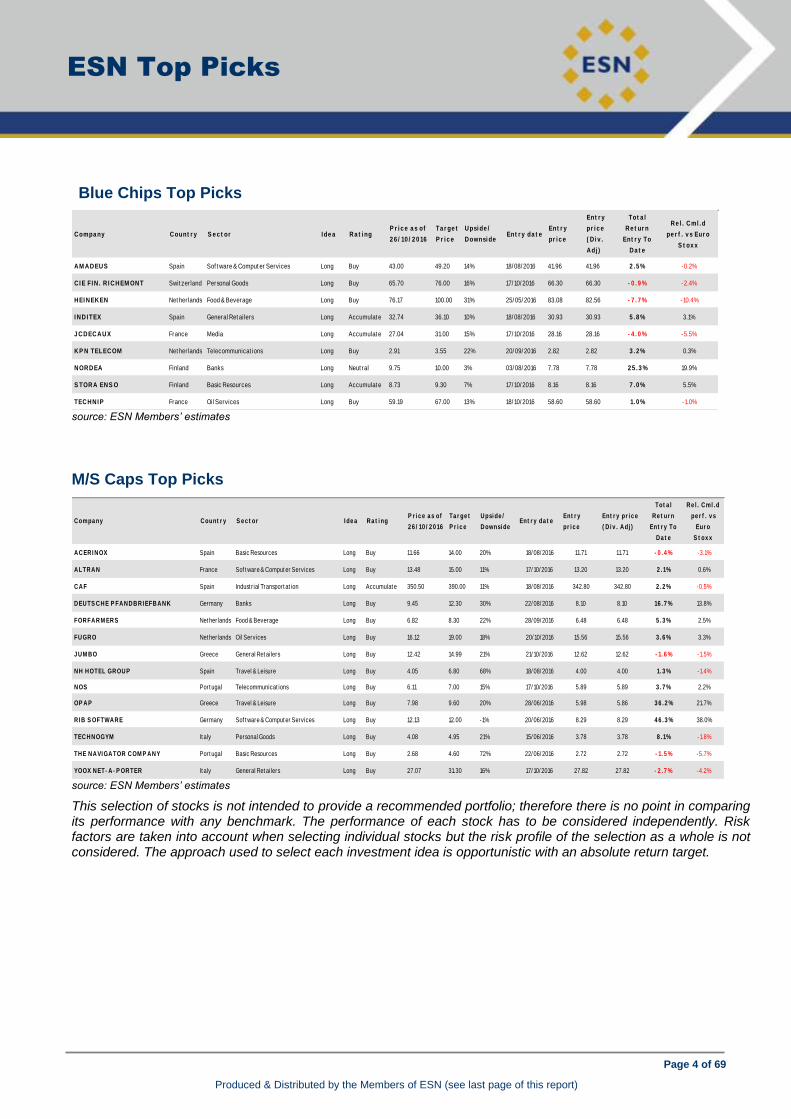

ESN Top Picks

Page 4 of 69

Produced & Distributed by the Members of ESN (see last page of this report)

Blue Chips Top Picks

Compa ny Count r y S e c t or I de a Ra t i ngP r i c e a s of

2 6 / 10 / 2 0 16

Ta r ge t

P r i c e

Upsi de /

Downsi deEnt r y da t e

Ent r y

pr i c e

Ent r y

pr i c e

( D i v .

Adj )

Tot a l

Re t ur n

Ent r y To

Da t e

Re l . Cml . d

pe r f . v s Eur o

S t ox x

AM ADEUS Spain Sof t ware & Comput er Services Long Buy 43.00 49.20 14% 18/ 08/ 2016 41.96 41.96 2 . 5 % -0.2%

CI E FI N . R I CHEM ONT Swit zerland Personal Goods Long Buy 65.70 76.00 16% 17/ 10/ 2016 66.30 66.30 - 0 . 9 % -2.4%

HEI NEKEN Net herlands Food & Beverage Long Buy 76.17 100.00 31% 25/ 05/ 2016 83.08 82.56 - 7 . 7 % -10.4%

I NDI TEX Spain General Ret ailers Long Accumulat e 32.74 36.10 10% 18/ 08/ 2016 30.93 30.93 5 . 8 % 3.1%

J CDECAUX France Media Long Accumulat e 27.04 31.00 15% 17/ 10/ 2016 28.16 28.16 - 4 . 0 % -5.5%

KP N TELECOM Net herlands Telecommunicat ions Long Buy 2.91 3.55 22% 20/ 09/ 2016 2.82 2.82 3 . 2 % 0.3%

NORDEA Finland Banks Long Neut ral 9.75 10.00 3% 03/ 08/ 2016 7.78 7.78 2 5 . 3 % 19.9%

S TORA ENS O Finland Basic Resources Long Accumulat e 8.73 9.30 7% 17/ 10/ 2016 8.16 8.16 7 . 0 % 5.5%

TECHNI P France Oil Services Long Buy 59.19 67.00 13% 18/ 10/ 2016 58.60 58.60 1. 0 % -1.0% source: ESN Members’ estimates

M/S Caps Top Picks

Compa ny Count r y S e c t or I de a Ra t i ngP r i c e a s of

2 6 / 10 / 2 0 16

Ta r ge t

P r i c e

Upsi de /

Downsi deEnt r y da t e

Ent r y

pr i c e

Ent r y pr i c e

( D i v . Adj )

Tot a l

Re t ur n

Ent r y To

Da t e

Re l . Cml . d

pe r f . v s

Eur o

S t ox x

ACERI NOX Spain Basic Resources Long Buy 11.66 14.00 20% 18/ 08/ 2016 11.71 11.71 - 0 . 4 % -3.1%

ALTRAN France Sof t ware & Comput er Services Long Buy 13.48 15.00 11% 17/ 10/ 2016 13.20 13.20 2 . 1% 0.6%

CAF Spain Indust r ial Transport at ion Long Accumulat e 350.50 390.00 11% 18/ 08/ 2016 342.80 342.80 2 . 2 % -0.5%

DEUTS CHE P FANDBRI EFBANK Germany Banks Long Buy 9.45 12.30 30% 22/ 08/ 2016 8.10 8.10 16 . 7 % 13.8%

FORFARM ERS Net herlands Food & Beverage Long Buy 6.82 8.30 22% 28/ 09/ 2016 6.48 6.48 5 . 3 % 2.5%

FUGRO Net herlands Oil Services Long Buy 16.12 19.00 18% 20/ 10/ 2016 15.56 15.56 3 . 6 % 3.3%

J UM BO Greece General Ret ailers Long Buy 12.42 14.99 21% 21/ 10/ 2016 12.62 12.62 - 1. 6 % -1.5%

NH HOTEL GROUP Spain Travel & Leisure Long Buy 4.05 6.80 68% 18/ 08/ 2016 4.00 4.00 1. 3 % -1.4%

NOS Port ugal Telecommunicat ions Long Buy 6.11 7.00 15% 17/ 10/ 2016 5.89 5.89 3 . 7 % 2.2%

OP AP Greece Travel & Leisure Long Buy 7.98 9.60 20% 28/ 06/ 2016 5.98 5.86 3 6 . 2 % 21.7%

RI B S OFTWARE Germany Sof t ware & Comput er Services Long Buy 12.13 12.00 -1% 20/ 06/ 2016 8.29 8.29 4 6 . 3 % 38.0%

TECHNOGYM It aly Personal Goods Long Buy 4.08 4.95 21% 15/ 06/ 2016 3.78 3.78 8 . 1% -1.8%

THE NAVI GATOR COM P ANY Port ugal Basic Resources Long Buy 2.68 4.60 72% 22/ 06/ 2016 2.72 2.72 - 1. 5 % -5.7%

YOOX NET- A- P ORTER It aly General Ret ailers Long Buy 27.07 31.30 16% 17/ 10/ 2016 27.82 27.82 - 2 . 7 % -4.2%

source: ESN Members’ estimates

This selection of stocks is not intended to provide a recommended portfolio; therefore there is no point in comparing its performance with any benchmark. The performance of each stock has to be considered independently. Risk factors are taken into account when selecting individual stocks but the risk profile of the selection as a whole is not considered. The approach used to select each investment idea is opportunistic with an absolute return target.

Roadshows

Page 5 of 69

Produced & Distributed by the Members of ESN (see last page of this report)

SUBJECT LOCATION EVENT DATE

EDENRED Geneva Cross-country Company Roadshow 09/11/2016

EDENRED Zurich Cross-country Company Roadshow 10/11/2016

Mediaset España Madrid Local Company Roadshow 10/11/2016

Kemira Lisboa Cross-country Company Roadshow 11/11/2016

Corporate Events

Page 6 of 69

Produced & Distributed by the Members of ESN (see last page of this report)

Corporate Events today

Source: Precise

CompanyBloomberg

codeDate Event Type Description

ALTRAN ALT FP 27/10/16 Trading Update Q3 2016 Sales conference call

ARCADIS ARCAD NA 27/10/16 Trading Update Q3 2016 Trading statement conference call

AREVA AREVA FP 27/10/16 Trading Update Q3 2016 Sales

ASM INTERNATIONAL ASM NA 27/10/16 Results Q3 2016 Earnings conference call / Webcast

ASPO ASPO FH 27/10/16 Results Q3 2016 Press conference

BBVA BBVA SM 27/10/16 Results Q3 2016 Webcast

BESI BESI NA 27/10/16 Results Q3 2016 Earnings conference call / Webcast

CORP. FINANCIERA ALBA ALB SM 27/10/16 Ex Dividend Date Interim 2016 Ex-dividend date EUR 0.50

ELISA ELISA FH 27/10/16 Capital Markets Day Capital Markets Day

ENCE ENC SM 27/10/16 Results Q3 2016 Earnings conference call / Webcast

IMERYS NK FP 27/10/16 Results Q3 2016 Results

KESKO KESBV FH 27/10/16 Results Q3 2016 Press & analyst meeting / Webcast

LEMMINKÄINEN LEM1S FH 27/10/16 Analyst Meeting Q3 2016 Press & analyst meeting

NATUREX NRX FP 27/10/16 Analyst Meeting Capital Markets Day

NOKIA NOKIA FH 27/10/16 Results Q3 2016 Earnings conference call / Webcast

NORDEA NDA1V FH 27/10/16 Analyst Meeting Q3 2016 Analyst meeting

PKC GROUP PKC1V FH 27/10/16 Results Q3 2016 Press conference

RECORDATI REC IM 27/10/16 Results Q3 2016 Earnings conference call

SCHNEIDER ELECTRIC SE SU FP 27/10/16 Trading Update Q3 2016 Earnings conference call

SU FP 27/10/16 Analyst Meeting Investor Day

STMICROELECTRONICS STM IM 27/10/16 Results Q3 2016 Earnings conference call / Webcast

STM IM 27/10/16 Results Q3 2016 Results

TECHNIP TEC FP 27/10/16 Results Q3 2016 Results

TEC FP 27/10/16 Results Q3 2016 Earnings conference call / Webcast

TELEFONICA TEF SM 27/10/16 Results Q3 2016 Earnings conference call / Webcast

TF1 TFI FP 27/10/16 Results Q3 2016 Earnings conference call / Webcast

VALMET VALMT FH 27/10/16 Results Q3 2016 Earnings conference call / Webcast {simultaneous}

VALMT FH 27/10/16 Analyst Meeting Q3 2016 Press & analyst meeting

VISCOFAN VIS SM 27/10/16 Results Q3 2016 Results

YIT YTY1V FH 27/10/16 Analyst Meeting Q3 2016 Press & analyst meeting {English}

YTY1V FH 27/10/16 Results Q3 2016 Earnings conference call / Webcast {simultaneous}

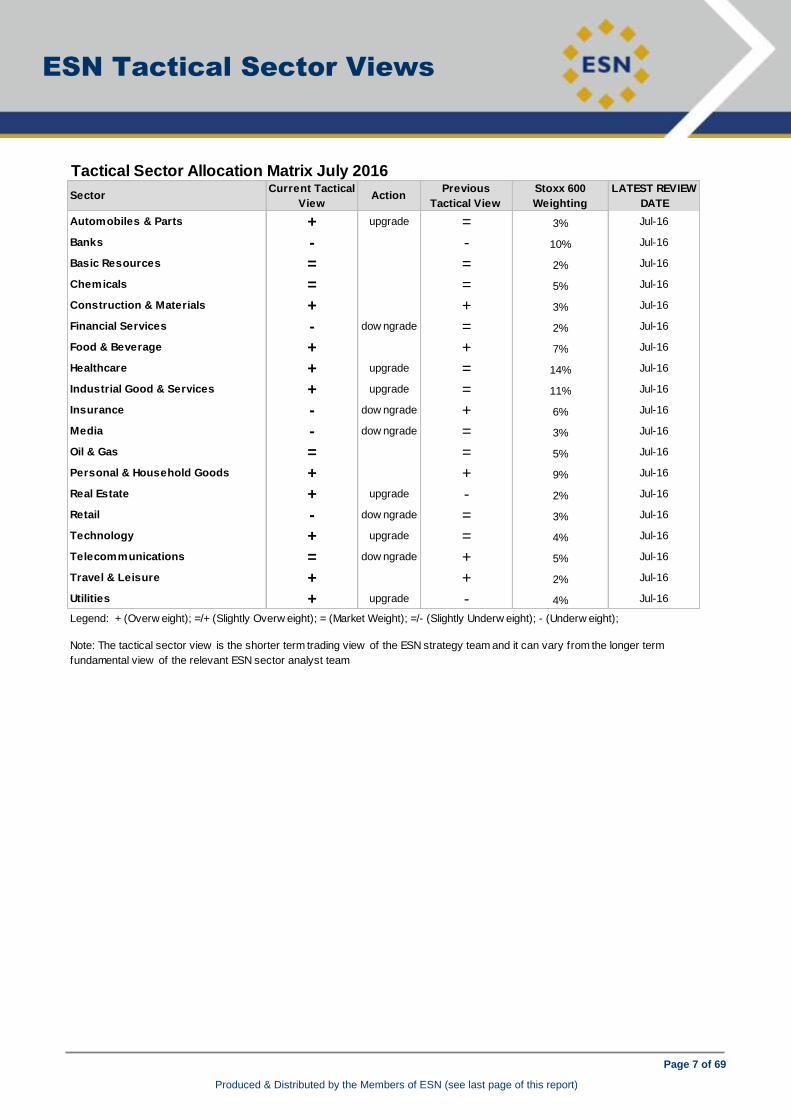

ESN Tactical Sector Views

Page 7 of 69

Produced & Distributed by the Members of ESN (see last page of this report)

Tactical Sector Allocation Matrix July 2016

SectorCurrent Tactical

ViewAction

Previous

Tactical View

Stoxx 600

Weighting

LATEST REVIEW

DATE

Automobiles & Parts + upgrade = 3% Jul-16

Banks - - 10% Jul-16

Basic Resources = = 2% Jul-16

Chemicals = = 5% Jul-16

Construction & Materials + + 3% Jul-16

Financial Services - dow ngrade = 2% Jul-16

Food & Beverage + + 7% Jul-16

Healthcare + upgrade = 14% Jul-16

Industrial Good & Services + upgrade = 11% Jul-16

Insurance - dow ngrade + 6% Jul-16

Media - dow ngrade = 3% Jul-16

Oil & Gas = = 5% Jul-16

Personal & Household Goods + + 9% Jul-16

Real Estate + upgrade - 2% Jul-16

Retail - dow ngrade = 3% Jul-16

Technology + upgrade = 4% Jul-16

Telecommunications = dow ngrade + 5% Jul-16

Travel & Leisure + + 2% Jul-16

Utilities + upgrade - 4% Jul-16

Legend: + (Overw eight); =/+ (Slightly Overw eight); = (Market Weight); =/- (Slightly Underw eight); - (Underw eight);

Note: The tactical sector view is the shorter term trading view of the ESN strategy team and it can vary from the longer term

fundamental view of the relevant ESN sector analyst team

Page 8 of 69

Produced & Distributed by the Members of ESN (see last page of this report)

Lisi

France/Aerospace & Defense Analyser

AEROSPACE & DEFENSE

Lisi (Accumulate) Q3-2016 sales: a gradual increase in growth

Q3-2016 sales: a gradual increase in growth

The facts: Q3-2016 sales: EUR379m, +12% (of which organic growth +6.9%).

Aerospace: Q3 sales: EUR236m (+8.9%, of which organic growth +8.5%)

Auto: Q3 sales: EUR109m (+4.6%, of which organic growth +4.8%)

Medical: Q3 sales: EUR35m (+90%, organic growth +1%).

Our analysis: Sales in the first nine months came out at EUR1,174m, up 7.2% (of

which organic growth +4.6%). Q3 therefore brought an increase in organic growth

after a slow start to 2016. Recap of sales performance in 2016: Q1 +1.8; Q2 +5.4%.

AERO: A sharp ramp-up for the A350 (EUR1m/jet) and in parts for Leap.

Continued decline for Boeing: not yet back to normative levels. Acceleration

and operational efforts in relation to structural components, no halt in

recruitment, settlement of machines: development costs until mid-2017. Q4

and 2017 are both set to be strong periods.

AUTO: Began the year in decline, but Europe now shows growth. New

products: +10%, a record quarter, with a ramp-up in production anticipated for

several prototypes, and order intake to be converted to manufacturing stage.

Confirmation of recovery thanks to the hardware plan. Normative margin of 7%

targeted, which is higher than that mentioned in the report (4%) prepared to

determine an intrinsic value of EUR28.

Medical: First quarter with Remele complete, and new orders, therefore

extension of the Minneapolis plan authorised, while the Caen plant is faring

well.

Conclusion & Action: A very good third quarter, and Q4 and 2017 are set to

show even better results.

A quality stock, whose price has naturally corrected.

Bear in mind that one year ago, sales were falling by -3.1%, and there was a small

adjustment of forecasts.

This year the situation has completely turned around.

Analyst(s):

Agnès Blazy, CM - CIC Market Solutions

+33 1 53 48 80 67

Accumulate

27.05

closing price as of 26/10/2016

28.00

Target Price unchanged

Recommendation unchanged

Target price: EUR

Share price: EUR

Reuters/Bloomberg GFII.PA/FII FP

Market capitalisation (EURm) 1,461

Current N° of shares (m) 54

Free float 30%

Daily avg. no. trad. sh. 12 mth 13

Daily avg. trad. vol. 12 mth (m) 477

Price high 12 mth (EUR) 27.15

Price low 12 mth (EUR) 19.04

Abs. perf. 1 mth 12.64%

Abs. perf. 3 mth 21.25%

Abs. perf. 12 mth 14.91%

Key financials (EUR) 12/15 12/16e 12/17e

Sales (m) 1,458 1,531 1,608

EBITDA (m) 204 222 247

EBITDA margin 14.0% 14.5% 15.4%

EBIT (m) 146 157 176

EBIT margin 10.0% 10.2% 10.9%

Net Profit (adj.)(m) 82 93 105

ROCE 9.7% 9.9% 10.6%

Net debt/(cash) (m) 157 138 109

Net Debt/Equity 0.2 0.2 0.1

Debt/EBITDA 0.8 0.6 0.4

Int. cover(EBITDA/Fin. int) 33.1 49.8 66.1

EV/Sales 1.1 1.1 1.0

EV/EBITDA 7.6 7.4 6.5

EV/EBITDA (adj.) 7.6 7.4 6.5

EV/EBIT 10.5 10.4 9.1

P/E (adj.) 16.5 15.7 13.9

P/BV 1.7 1.7 1.5

OpFCF yield 3.4% 1.6% 2.3%

Dividend yield 1.4% 1.5% 1.7%

EPS (adj.) 1.52 1.73 1.94

BVPS 14.66 16.00 17.54

DPS 0.39 0.42 0.45

19

20

21

22

23

24

25

26

27

28

Oct 15 Nov 15 Dec 15 Jan 16 Feb 16 Mar 16 Apr 16 May 16 Jun 16 Jul 16 Aug 16 Sep 16 Oct 16

vvdsvdvsdy

LISI CAC Small & Mid 190 (Rebased)Source: Factset

Shareholders: CID-Compagnie Industrielle de Delle

55%; VMC-VIELLARD-MIGEON&Cie 6%;

FFP Invest 5%; Treasury shares 3%;

Employees 1.24%;

Page 9 of 69

Produced & Distributed by the Members of ESN (see last page of this report)

Bittium Group

Q3 2015a

M€ OP Cons. Diff. OP Cons. Diff.

Sales 14.8 12.9 15% 0 11.1 0 64 64 0%

EBIT 1.3 0.4 280% # 0.0 0 4 3 28%

EBIT margin 9.0 % 2.7 % 0.0 % # 0.0 % # 6.3 % 4.9 %

PTP 1.5 0.5 240% 0 0.1 0 4.6 3.8 20%

EPS 0.04 0.01 291% 0.00 0.12 0.10 19%

DPS 0.30 0.30 # 0.03 # 0.06 0.07 -12%

Source: OP and FactSet

2016eQ3 2016e

Bittium Corporation

Finland/Automobiles & Parts Analyser

AUTOMOBILES & PARTS

Bittium Corporation (Accumulate) Q3-2016 sales: a gradual increase in growth

Q3 preview: Will the Mexsat design project alter H2 profitability?

The facts: Bittium will report its Q3 figures on Thursday, 3 November at 7.00 am

CET. Bittium expects 2016 sales to be above the level of 2015 (EUR 56.8m). It

has no profitability guidance, which the company justifies by its ongoing strategy

process as well as the transaction at the turn of the year concerning tactical

communication systems. The schedule of the transaction is not yet certain.

Our analysis: Bittium's share price has been depressed by the company's

release on the possible impact of the reduced cooperation with Ericsson. Bittium

estimates that if the measures planned by Ericsson are realised in full, the

measures may have a negative impact on Bittium's 2017 sales and EBIT. We do

not expect the decline in the share of Ericsson to have a significant impact on

Bittium's growth drivers. Revenues of over EUR 10m from the design project

concerning Mexsat devices will be recognised this year. The cash flow of design

projects is typically back-end loaded, which is why we expect the project to

support H2. After the termination of the design project, actual deliveries of

equipment will start in 2017. We estimate that the biggest impact from the tactical

communication system deliveries will in any case be seen in 2017 irrespective of

the publication date of the transaction.

In the future, communication systems in the public safety markets will be based

on commercial mobile network technology. We believe that Bittium stands to gain

from this development trend as it has long experience from designing mobile

network solutions. Bittium's potential deals will be large in proportion to its size,

and an individual quarter will therefore be of minor importance in terms of the

future outlook. In quarterly comparison one should that Bittium's earnings are

highly volatile.

Conclusion & Action: Our target price is based on DCF (70%) and peer

company (30%) valuation (P/E and EV/EBITDA). We are assigning more weight

to DCF because the potential arising from large projects is beyond our present

forecast horizon. We have made no changes to our 2017–2018 forecasts and

maintain our target price of EUR 6.60. Due to the share price rise, our

recommendation falls to Accumulate (from Buy).

Analyst(s):

Hannu Rauhala, OP Corporate Bank

+358 10 252 4392

Accumulate

5.97

closing price as of 26/10/2016

6.60

Target Price unchanged

from Buy

Target price: EUR

Share price: EUR

Reuters/Bloomberg BITTI.HE/BITTI FH

Market capitalisation (EURm) 213

Current N° of shares (m) 36

Free float 86%

Daily avg. no. trad. sh. 12 mth 97

Daily avg. trad. vol. 12 mth (m) 228

Price high 12 mth (EUR) 7.54

Price low 12 mth (EUR) 5.17

Abs. perf. 1 mth -11.03%

Abs. perf. 3 mth 9.14%

Abs. perf. 12 mth 1.53%

Key financials (EUR) 12/15 12/16e 12/17e

Sales (m) 57 64 69

EBITDA (m) 8 10 11

EBITDA margin 13.2% 15.1% 16.6%

EBIT (m) 2 4 7

EBIT margin 4.1% 6.3% 9.6%

Net Profit (adj.)(m) 536 4 6

ROCE 10.2% 10.0% 15.0%

Net debt/(cash) (m) (122) (110) (110)

Net Debt/Equity -0.9 -0.8 -0.8

Debt/EBITDA -16.2 -11.5 -9.6

Int. cover(EBITDA/Fin. int) high high high

EV/Sales 2.2 1.6 1.5

EV/EBITDA 17.0 10.6 8.8

EV/EBITDA (adj.) 17.0 10.6 8.8

EV/EBIT 55.4 25.4 15.1

P/E (adj.) 0.5 nm 32.9

P/BV 1.8 1.5 1.5

OpFCF yield 3.8% -4.3% 1.0%

Dividend yield 5.0% 1.0% 1.5%

EPS (adj.) 15.06 0.12 0.18

BVPS 3.86 3.92 4.04

DPS 0.30 0.06 0.09

5.0

5.5

6.0

6.5

7.0

7.5

8.0

Sep 15 Oct 15 Nov 15 Dec 15 Jan 16 Feb 16 Mar 16 Apr 16 May 16 Jun 16 Jul 16 Aug 16 Sep 16 Oct 16

vvdsvdvsdy

BITTIUM CORPORATION OMXH (Rebased)Source: Factset

Shareholders: Harju Jukka 5%; Hulkko Juha 5%;

Veikkolainen Erkki 4%;

Page 10 of 69

Produced & Distributed by the Members of ESN (see last page of this report)

ElringKlinger

Germany/Automobiles & Parts Analyser

AUTOMOBILES & PARTS

ElringKlinger (Neutral) Q3 preview: Will the Mexsat design project alter H2 profitability?

Acquisition of a minority stake in hofer AG

The facts: ElringKlinger has announced this morning that it has acquired a

strategic 27% minority stake in the engineering company hofer AG. Additionally,

the transaction includes the acquisition of a 53% stake in hofer’s subisidiary

powertrain products GmbH. The price of the transaction is in the double digit EUR

million range. Closing will be in 2017.

Our analysis: hofer AG is an engineering services company, specialised in

powertrain development, mainly for small series production for sports and luxury

cars.

powertrain products GmbH is a production company, which produces the

developments of the mother company in small series production.

The strategic rationale behind the deal makes sense in our view, as it helps

ElringKlinger in getting better and earlier insides into the development of new

powertrain solutions. This is especially important as the company’s product

portfolio is heavily skewed towards products which are not necessary in electrical

cars anymore.

The deal is strategic and will not add much to the P&L in the short term. No

fundamentals were disclosed, but according to the Bundesanzeiger, hofer AG

recorded revenues of EUR 47.7m in FY 2014 and showed an operating result of

EUR 0.4m.

We estimate the price of the transaction to be around EUR 20m, which would

clearly be a strategic price.

Conclusion & Action: We believe that the transaction makes sense for

ElringKlinger. Nonetheless, it will not add much to the P&L in the short term and

also reminds us how important it is for the company to manage the transition

towards electrical drivetrains.

Analyst(s):

Tim Schuldt, CFA, equinet Bank

+49 69 5899 7433

Neutral

15.01

closing price as of 26/10/2016

17.00

Target Price unchanged

Recommendation unchanged

Target price: EUR

Share price: EUR

Reuters/Bloomberg ZILGn.DE/ZIL2 GR

Market capitalisation (EURm) 951

Current N° of shares (m) 63

Free float 48%

Daily avg. no. trad. sh. 12 mth 216

Daily avg. trad. vol. 12 mth (m) 2,404

Price high 12 mth (EUR) 24.09

Price low 12 mth (EUR) 14.92

Abs. perf. 1 mth -2.22%

Abs. perf. 3 mth -5.03%

Abs. perf. 12 mth -23.48%

Key financials (EUR) 12/15 12/16e 12/17e

Sales (m) 1,507 1,570 1,649

EBITDA (m) 222 239 265

EBITDA margin 14.7% 15.2% 16.1%

EBIT (m) 135 146 169

EBIT margin 9.0% 9.3% 10.2%

Net Profit (adj.)(m) 95 99 116

ROCE 5.4% 5.4% 6.0%

Net debt/(cash) (m) 487 511 494

Net Debt/Equity 0.6 0.6 0.5

Debt/EBITDA 2.2 2.1 1.9

Int. cover(EBITDA/Fin. int) 34.2 29.8 35.4

EV/Sales 1.4 1.0 1.0

EV/EBITDA 9.6 6.8 6.1

EV/EBITDA (adj.) 9.6 6.8 6.1

EV/EBIT 15.7 11.2 9.6

P/E (adj.) 15.6 9.6 8.2

P/BV 1.8 1.1 1.0

OpFCF yield -4.5% 1.1% 5.5%

Dividend yield 3.7% 3.3% 4.0%

EPS (adj.) 1.51 1.57 1.83

BVPS 12.97 14.02 15.34

DPS 0.55 0.50 0.60

14

15

16

17

18

19

20

21

22

23

24

25

Sep 15 Okt 15 Nov 15 Dez 15 Jan 16 Feb 16 Mrz 16 Apr 16 Mai 16 Jun 16 Jul 16 Aug 16 Sep 16 Okt 16

vvdsvdvsdy

ELRINGKLINGER Stoxx Automobiles & Parts (Rebased)Source: Factset

Shareholders: Lechler Family 52%;

Page 11 of 69

Produced & Distributed by the Members of ESN (see last page of this report)

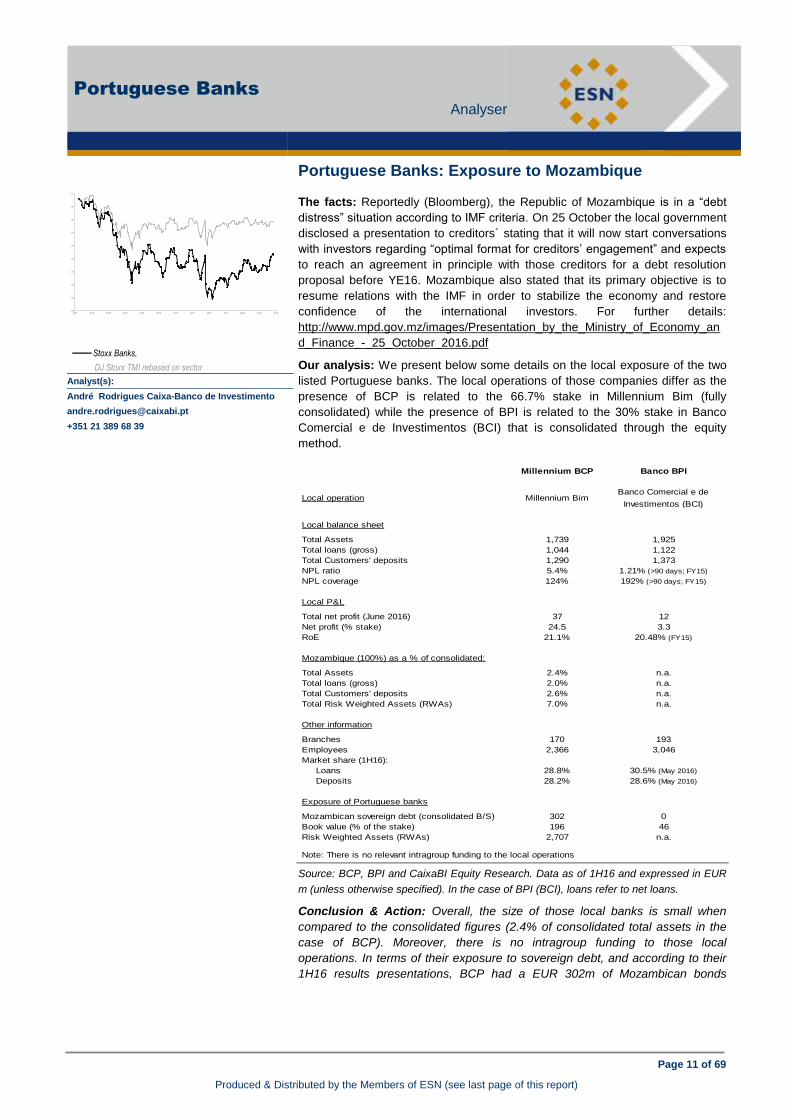

Portuguese Banks

Analyser

BANKS

Acquisition of a minority stake in hofer AG Portuguese Banks: Exposure to Mozambique

110

120

130

140

150

160

170

180

190

200

out 15 nov 15 dez 15 jan 16 fev 16 mar 16 abr 16 mai 16 jun 16 jul 16 ago 16 set 16 out 16

vvdsvdvsdy

The facts: Reportedly (Bloomberg), the Republic of Mozambique is in a “debt

distress” situation according to IMF criteria. On 25 October the local government

disclosed a presentation to creditors´ stating that it will now start conversations

with investors regarding “optimal format for creditors’ engagement” and expects

to reach an agreement in principle with those creditors for a debt resolution

proposal before YE16. Mozambique also stated that its primary objective is to

resume relations with the IMF in order to stabilize the economy and restore

confidence of the international investors. For further details:

http://www.mpd.gov.mz/images/Presentation_by_the_Ministry_of_Economy_an

d_Finance_-_25_October_2016.pdf

Our analysis: We present below some details on the local exposure of the two

listed Portuguese banks. The local operations of those companies differ as the

presence of BCP is related to the 66.7% stake in Millennium Bim (fully

consolidated) while the presence of BPI is related to the 30% stake in Banco

Comercial e de Investimentos (BCI) that is consolidated through the equity

method.

Source: BCP, BPI and CaixaBI Equity Research. Data as of 1H16 and expressed in EUR

m (unless otherwise specified). In the case of BPI (BCI), loans refer to net loans.

Conclusion & Action: Overall, the size of those local banks is small when

compared to the consolidated figures (2.4% of consolidated total assets in the

case of BCP). Moreover, there is no intragroup funding to those local

operations. In terms of their exposure to sovereign debt, and according to their

1H16 results presentations, BCP had a EUR 302m of Mozambican bonds

(available for sale portfolio) while BPI did not report any exposure.

---------- Stoxx Banks,

DJ Stoxx TMI rebased on sector

Analyst(s):

André Rodrigues Caixa-Banco de Investimento

+351 21 389 68 39

Millennium BCP Banco BPI

Local operation Millennium BimBanco Comercial e de

Investimentos (BCI)

Local balance sheet

Total Assets 1,739 1,925

Total loans (gross) 1,044 1,122

Total Customers' deposits 1,290 1,373

NPL ratio 5.4% 1.21% (>90 days; FY15)

NPL coverage 124% 192% (>90 days; FY15)

Local P&L

Total net profit (June 2016) 37 12

Net profit (% stake) 24.5 3.3

RoE 21.1% 20.48% (FY15)

Mozambique (100%) as a % of consolidated:

Total Assets 2.4% n.a.

Total loans (gross) 2.0% n.a.

Total Customers' deposits 2.6% n.a.

Total Risk Weighted Assets (RWAs) 7.0% n.a.

Other information

Branches 170 193

Employees 2,366 3,046

Market share (1H16):

Loans 28.8% 30.5% (May 2016)

Deposits 28.2% 28.6% (May 2016)

Exposure of Portuguese banks

Mozambican sovereign debt (consolidated B/S) 302 0

Book value (% of the stake) 196 46

Risk Weighted Assets (RWAs) 2,707 n.a.

Note: There is no relevant intragroup funding to the local operations

Page 12 of 69

Produced & Distributed by the Members of ESN (see last page of this report)

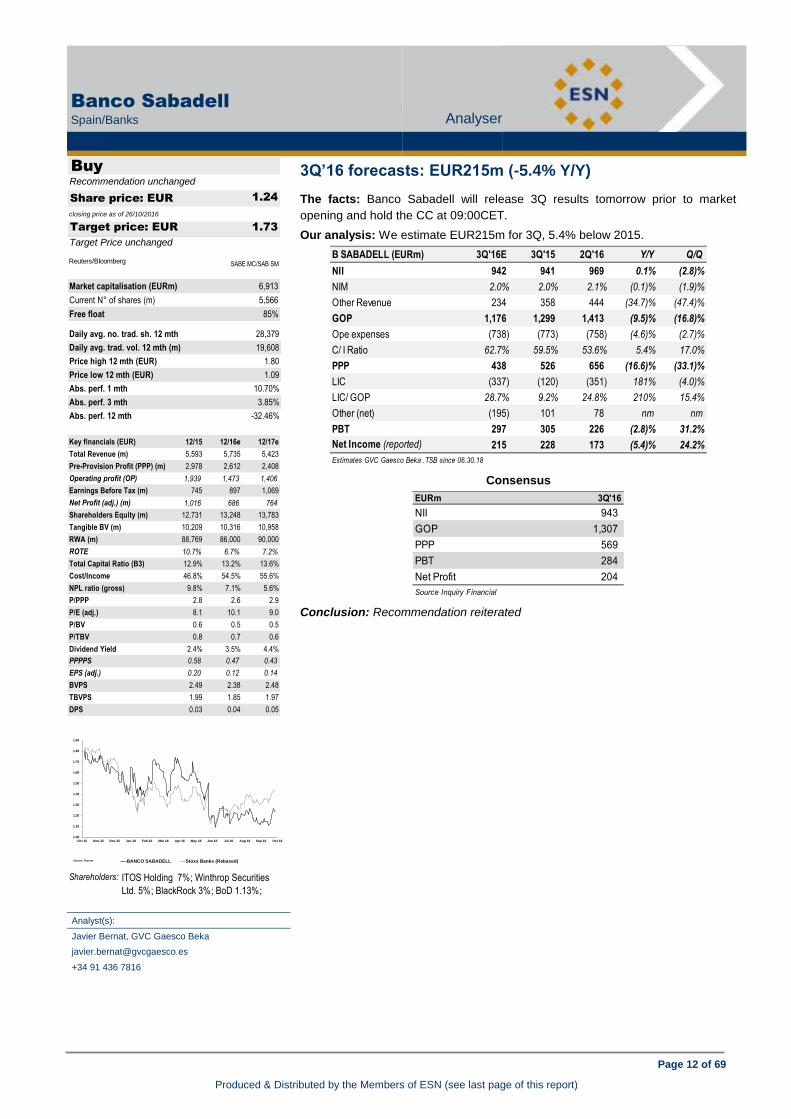

Banco Sabadell

Spain/Banks Analyser

BANKS

Banco Sabadell (Buy) Portuguese Banks: Exposure to Mozambique

3Q’16 forecasts: EUR215m (-5.4% Y/Y)

The facts: Banco Sabadell will release 3Q results tomorrow prior to market

opening and hold the CC at 09:00CET.

Our analysis: We estimate EUR215m for 3Q, 5.4% below 2015.

Consensus

Conclusion: Recommendation reiterated

Analyst(s):

Javier Bernat, GVC Gaesco Beka

+34 91 436 7816

Buy

1.24

closing price as of 26/10/2016

1.73

Target Price unchanged

Recommendation unchanged

Target price: EUR

Share price: EUR

Reuters/Bloomberg SABE.MC/SAB SM

Market capitalisation (EURm) 6,913

Current N° of shares (m) 5,566

Free float 85%

Daily avg. no. trad. sh. 12 mth 28,379

Daily avg. trad. vol. 12 mth (m) 19,608

Price high 12 mth (EUR) 1.80

Price low 12 mth (EUR) 1.09

Abs. perf. 1 mth 10.70%

Abs. perf. 3 mth 3.85%

Abs. perf. 12 mth -32.46%

Key financials (EUR) 12/15 12/16e 12/17e

Total Revenue (m) 5,593 5,735 5,423

Pre-Provision Profit (PPP) (m) 2,978 2,612 2,408

Operating profit (OP) 1,939 1,473 1,406

Earnings Before Tax (m) 745 897 1,069

Net Profit (adj.) (m) 1,016 686 764

Shareholders Equity (m) 12,731 13,248 13,783

Tangible BV (m) 10,209 10,316 10,958

RWA (m) 88,769 86,000 90,000

ROTE 10.7% 6.7% 7.2%

Total Capital Ratio (B3) 12.9% 13.2% 13.6%

Cost/Income 46.8% 54.5% 55.6%

NPL ratio (gross) 9.8% 7.1% 5.6%

P/PPP 2.8 2.6 2.9

P/E (adj.) 8.1 10.1 9.0

P/BV 0.6 0.5 0.5

P/TBV 0.8 0.7 0.6

Dividend Yield 2.4% 3.5% 4.4%

PPPPS 0.58 0.47 0.43

EPS (adj.) 0.20 0.12 0.14

BVPS 2.49 2.38 2.48

TBVPS 1.99 1.85 1.97

DPS 0.03 0.04 0.05

B SABADELL (EURm) 3Q'16E 3Q'15 2Q'16 Y/Y Q/Q

NII 942 941 969 0.1% (2.8)%

NIM 2.0% 2.0% 2.1% (0.1)% (1.9)%

Other Revenue 234 358 444 (34.7)% (47.4)%

GOP 1,176 1,299 1,413 (9.5)% (16.8)%

Ope expenses (738) (773) (758) (4.6)% (2.7)%

C/ I Ratio 62.7% 59.5% 53.6% 5.4% 17.0%

PPP 438 526 656 (16.6)% (33.1)%

LIC (337) (120) (351) 181% (4.0)%

LIC/ GOP 28.7% 9.2% 24.8% 210% 15.4%

Other (net) (195) 101 78 nm nm

PBT 297 305 226 (2.8)% 31.2%

Net Income (reported) 215 228 173 (5.4)% 24.2%

Estimates GVC Gaesco Beka .TSB since 06.30.18

EURm 3Q'16

NII 943

GOP 1,307

PPP 569

PBT 284

Net Profit 204

Source Inquiry Financial

1.00

1.10

1.20

1.30

1.40

1.50

1.60

1.70

1.80

1.90

Oct 15 Nov 15 Dec 15 Jan 16 Feb 16 Mar 16 Apr 16 May 16 Jun 16 Jul 16 Aug 16 Sep 16 Oct 16

vvdsvdvsdy

BANCO SABADELL Stoxx Banks (Rebased)Source: Factset

Shareholders: ITOS Holding 7%; Winthrop Securities

Ltd. 5%; BlackRock 3%; BoD 1.13%;

Page 13 of 69

Produced & Distributed by the Members of ESN (see last page of this report)

BBVA

Spain/Banks Analyser

BANKS

BBVA (Buy) 3Q’16 forecasts: EUR215m (-5.4% Y/Y)

9M 16 earnings: EUR2,797m (-0.6% adjusted)

The facts: in 9m 15, BBVA reported a net profit of EUR2,797bn, 64.3% above

9m’15 and in line with our forecast and the consensus. Adjusting for the impact of

corporate operations, BBVA’s net profit would be similar to that obtained in the

same period 2015 (EUR2.815m).

Our analysis: this result includes the incorporation of Catalunya Banc accounts

since 24.04.15 and the purchase of the 14.89% additional in the Turkish bank

Garanti from the 3Q15.

Efficiency: Sep16 (51.8%) improves the 52.0% of Dic15 of 52% despite the new

incorporations.

Credit quality: The NPL ratio comes to 5.1%, implying a slight improvement over

5.4% at Dec15. NPLK coverage at 72% and CoR improves to 0.9% vs. 1.1% of

Dic15.

Solvency: the CET1 ratio ends at 11.0%, reaching the 2016 goal (includes impact

of 15pbs due to the sovereign rating downgrade of Turkey). For its part, the

leverage ratio stands at 6.1%, one of the highest in the banking industry.

Mexico (41.2% w/profit): records double-digit growth rates, both in loans and

customer funds. The NPL ratio ends at 2.5% and PL coverage is 122%. 9m 16

net profit grows 11.4% y/y to EUR 1.441 m.

Conclusion: first impression positive (CC @ 9:30), after a recovery of the RoTE

9.0% vs 6.4% (Dec15) and the RORWA at 1.26%. Recommendation reiterated.

Analyst(s):

Javier Bernat, GVC Gaesco Beka

+34 91 436 7816

Buy

6.43

closing price as of 26/10/2016

6.70

Target Price unchanged

Recommendation unchanged

Target price: EUR

Share price: EUR

Reuters/Bloomberg BBVA.MC/BBVA SM

Market capitalisation (EURm) 41,669

Current N° of shares (m) 6,480

Free float 96%

Daily avg. no. trad. sh. 12 mth 47,963

Daily avg. trad. vol. 12 mth (m) 206,247

Price high 12 mth (EUR) 8.19

Price low 12 mth (EUR) 4.76

Abs. perf. 1 mth 21.07%

Abs. perf. 3 mth 25.32%

Abs. perf. 12 mth -21.04%

Key financials (EUR) 12/15 12/16e 12/17e

Total Revenue (m) 23,366 23,956 25,668

Pre-Provision Profit (PPP) (m) 13,283 11,386 12,236

Operating profit (OP) 8,944 7,063 7,846

Earnings Before Tax (m) 4,602 6,068 6,851

Net Profit (adj.) (m) 2,701 3,722 4,202

Shareholders Equity (m) 47,291 50,097 53,342

Tangible BV (m) 40,480 43,286 46,531

RWA (m) 401,346 456,729 487,698

ROTE 6.4% 8.9% 9.4%

Total Capital Ratio (B3) 15.0% 16.3% 16.4%

Cost/Income 43.2% 52.5% 52.3%

NPL ratio (gross) 7.0% 5.5% 4.6%

P/PPP 3.2 3.7 3.4

P/E (adj.) 15.9 11.2 9.9

P/BV 0.9 0.8 0.8

P/TBV 1.1 1.0 0.9

Dividend Yield 2.5% 2.9% 3.8%

PPPPS 2.09 1.76 1.89

EPS (adj.) 0.42 0.57 0.65

BVPS 7.43 7.73 8.23

TBVPS 6.36 6.68 7.18

DPS 0.16 0.19 0.24

BBVA (EURm) 9M16 9M15 Y/Y (m) Y/Y (%)

GOP 18,431 17,534 897 5.1%

NII 12,674 12,011 663 5.5%

Fees & Comm. 3,557 3,442 115 3.3%

Trading 1,753 1,558 195 12.5%

Op Expense (9,549) (9,024) (525) 5.8%

Impairments (3,114) (3,283) 169 (5.1)%

% GOP (16.9)% (18.7)% 0 (9.8)%

PBT 5,107 4,335 772 17.8%

Net Inc. (reported) 2,797 1,702 1,095 64.3%

Net Inc. (adjust): 2,797 2,815 (18) (0.6)%

Financial ratios: Sep 2016 Dec 2015 YTDbp YTD (%)

CET1-FL (%) 11.00 10.30 70.0 6.8%

Total capital ratio (%) 15.50 14.40 110.0 7.6%

C /I Ratio (%) 51.80 52.00 (20.0) (0.4)%

NPL Coverage (%) 72.00 74.00 (200.0) (2.7)%

NPL Ratio (%) 5.10 5.40 (30.0) (5.6)%

CoR (%) 0.90 1.10 (20.0) (18.2)%

RoRWA (%) 1.26 0.87 39.0 44.8%

RoTE (%) 9.00 6.40 260.0 40.6%

Source Company

4.5

5.0

5.5

6.0

6.5

7.0

7.5

8.0

8.5

Oct 15 Nov 15 Dec 15 Jan 16 Feb 16 Mar 16 Apr 16 May 16 Jun 16 Jul 16 Aug 16 Sep 16 Oct 16

vvdsvdvsdy

BBVA Stoxx Banks (Rebased)Source: Factset

Shareholders: BlackRock 4%;

Page 14 of 69

Produced & Distributed by the Members of ESN (see last page of this report)

BPI

Portugal/Banks Analyser

BANKS

BPI (Neutral) 9M 16 earnings: EUR2,797m (-0.6% adjusted)

9M16 results: Positive results (NII in Angola and provisions/asset quality in Portugal). ROE at 10.5%

The facts: BPI disclosed its 9M16 results yesterday after the market close. Today

the management will host a Conference call with analysts (11:00 Local time).

Our analysis: Consolidated net profit stood at EUR 182.9m in 9M16 (+21.2%

YoY) from the EUR 151m in 9M15. On a quarterly basis the net profit stood at EUR

77m (+27.8% QoQ) and +3% YoY vs. EUR 74.8m of 3Q15. The positive YoY

evolution was mainly due to the growth of the net interest income (+12.7% YoY in

consolidated terms, with +15.4% in the domestic operation) and also to the strong

drop in loan impairments (-53.3% YoY), in spite of the EUR 41.6m (vs. EUR 18m

in 9M15) of “other impairments and provisions” booked in 9M16, including

impairments in bonds of PT Int. Finance (Oi Group) of EUR 18m.

This result was equivalent to an ROE of 10.5% (with 4.1% in Portugal, a net profit

of EUR 57.5m). International units presented a profit of EUR 125.4m (+12% YoY),

an ROE of 38.5% and 68.6% of the consolidated net profit. The domestic NII

continued to benefit from the fall in the cost of term deposits (average rate close to

0% for new deposits originated in September 2016 vs. 0.03% in June). The main

deviation vs. our estimates came from Angola where the NII stood at EUR 96m in

3Q15 (+9.6% QoQ) and c. EUR 11m above our estimate.

In terms of costs, the recurrent figure stood at EUR 498.4m (+0.1% YoY). On the

top of that, BPI booked EUR 50.5m for costs with early retirements (for 276 early

retirements, of which 75 were concluded in 3Q16 and 200 will occur before YE16).

The amount reported as “non-recurring costs” in 9M16 is close to EUR 7m as it

also includes a gain of EUR 43m due to a revision in the Collective Labour

Agreement of the Banking Sector (ACT). Cost-to-income stood at 55.4% in 9M16.

Asset quality - Credit at risk ratio drop by 20bps YoY to 4.6% from 4.8% in 9M15

(-10bps QoQ) with a total coverage by impairments of 85%. In terms of net new

entries (NPL > 90 days) it was visible a strong improvement in 3Q16 with only EUR

8.5m vs. EUR 30.1m in 2Q16. In this context, the cost of credit risk (after

recoveries) drop from 54bps in 9M15 to only 22bps in 9M16, with only 16bps in the

domestic operation and 127bps in the international activity.

Capital - CET 1 ratio fully loaded was at 11.0% (11.4% phasing in) from 9.3% and

10.4%, respectively in September 2015.

Overall, 3Q16 should note be a trigger for BPI. In any case, we have a positive first

impression on these results. NII continued to evolve positively (and above our

estimate), recurrent costs stood stable YoY and loan impairments (namely in

Portugal) were a positive surprise in a context of a FL CET1 ratio of 11.0%. More

details after today’s Conference call.

Analyst(s):

André Rodrigues, Caixa-Banco de Investimento

+351 21 389 68 39

Neutral

1.13

closing price as of 26/10/2016

1.20

Target Price unchanged

Recommendation unchanged

Target price: EUR

Share price: EUR

Reuters/Bloomberg BBPI.LS/BPI PL

Market capitalisation (EURm) 1,646

Current N° of shares (m) 1,457

Free float 26%

Key financials (EUR) 12/15 12/16e 12/17e

Total Revenue (m) 1,182 1,169 1,193

Pre-Provision Profit (PPP) (m) 492 484 497

Operating profit (OP) 373 391 413

Earnings Before Tax (m) 407 425 448

Net Profit (adj.) (m) 236 229 245

Shareholders Equity (m) 2,407 2,546 2,791

Tangible BV (m) 2,407 2,546 2,791

RWA (m) 23,294 24,419 25,404

ROTE 10.4% 9.2% 9.2%

Total Capital Ratio (B3) 11.1% 11.5% 12.0%

Cost/Income 56.7% 56.8% 56.7%

NPL ratio (gross) 3.6% 3.7% 3.7%

P/PPP 3.2 3.4 3.3

P/E (adj.) 6.7 7.2 6.7

P/BV 0.7 0.6 0.6

P/TBV 0.7 0.6 0.6

Dividend Yield 0.0% 0.0% 0.0%

PPPPS 0.34 0.33 0.34

EPS (adj.) 0.16 0.16 0.17

BVPS 1.65 1.75 1.92

TBVPS 1.65 1.75 1.92

DPS 0.00 0.00 0.00

0.70

0.80

0.90

1.00

1.10

1.20

1.30

1.40

out 15 nov 15 dez 15 jan 16 fev 16 mar 16 abr 16 mai 16 jun 16 jul 16 ago 16 set 16 out 16

vvdsvdvsdy

BPI Stoxx Banks (Rebased)Source: Factset

Shareholders: Caixabank 44%; Santoro 19%; Allianz

8%;

3Q16 3Q15 D YoY 2Q16 D QoQ 9M16 9M15 D YoY 3Q16e D D (%)

Net interest income (narrow sense) 186.8 153.9 21.4% 180.0 3.8% 525.5 466.2 12.7% 176.2 10.6 6.0%

Unit Link products gross margin 3.3 3.7 -10.8% 3.4 -2.9% 10.3 9.1 13.6% 3.4 (.1) -3.4%

Income from securities - - n.m. 3.9 n.m. 3.9 3.6 8.4% - - n.m.

Commissions (deferred cost) 5.3 4.7 12.8% 5.1 3.9% 15.8 14.6 8.7% 5.1 .2 3.7%

Net interest income 195.3 162.3 20.3% 192.4 1.5% 555.6 493.5 12.6% 184.7 10.6 5.7%

Technical result from insurance 5.4 8.2 -34.1% 5.6 -3.6% 18.9 27.6 -31.6% 5.6 (.2) -3.8%

Commissions (net) 81.0 81.7 -0.9% 79.8 1.5% 234.9 237.1 -0.9% 79.5 1.5 1.9%

Results - Financial operations 33.1 58.3 -43.2% 53.3 -37.9% 138.4 153.6 -10.0% 31.8 1.3 4.2%

Operating income and charges (9.2) (3.1) 196.8% (25.5) -63.9% (39.7) (17.3) 129.2% (1.3) (7.9) 625.8%

Net operating income 305.6 307.3 -0.6% 305.6 0.0% 908.0 894.5 1.5% 300.3 5.3 1.8%

Personnel costs (92.8) (94.8) -2.1% (97.3) -4.6% (284.8) (283.9) 0.3% (97.7) 4.9 -5.0%

Non-recurring costs (4.7) (4.6) 2.2% (2.3) 104.3% (7.6) (4.6) 63.2% - (4.7) n.m.

Other administrative expenses (60.4) (60.7) -0.5% (67.1) -10.0% (188.1) (187.7) 0.2% (65.4) 5.0 -7.7%

Depreciation of fixed Assets (8.5) (8.7) -2.3% (8.4) 1.2% (25.5) (26.2) -2.7% (8.4) (.1) 0.8%

Total Expenses (166.4) (168.8) -1.4% (175.0) -4.9% (505.9) (502.5) 0.7% (171.6) 5.2 -3.0%

Operating profit exc. provisions 139.2 138.5 0.5% 130.6 6.6% 402.0 392.1 2.5% 128.7 10.5 8.2%

Recovery of loans written-off 5.9 6.5 -9.2% 3.6 63.9% 14.2 14.3 -0.7% 3.6 2.3 63.0%

Loan provisions and impairments (5.7) (26.5) -78.5% (16.6) -65.7% (53.0) (113.4) -53.3% (17.6) 11.9 -67.5%

Other impairments and provisions (6.0) (2.0) 200.0% (31.5) -81.0% (41.6) (18.0) 131.5% (4.0) (2.0) 50.0%

Profits before taxes 133.4 116.5 14.5% 86.1 54.9% 321.6 274.9 17.0% 110.8 22.6 20.4%

Corporate income tax (16.0) (12.1) 32.2% 1.9 n.m. (37.6) (37.6) -0.1% (13.9) (2.1) 14.8%

Equity-accounted results 4.0 10.4 -61.5% 15.8 -74.7% 25.4 23.2 9.7% 6.4 (2.4) -37.4%

Minorities (44.5) (40.1) 11.0% (43.6) 2.1% (126.5) (109.5) 15.5% (44.8) .3 -0.6%

Net Profit 77.0 74.8 3.0% 60.2 27.9% 182.9 151.0 21.2% 58.5 18.5 31.7%

Accumulated BPI vs. CaixaBIQuarterly

Page 15 of 69

Produced & Distributed by the Members of ESN (see last page of this report)

BPI

Portugal/Banks Analyser

BANKS

BPI (Neutral) 9M16 results: Positive results (NII in Angola and provisions/asset quality in Portugal). ROE at 10.5%

Neutral

1,13

closing price as of 26/10/2016

1,20

Target Price unchanged

Recommendation unchanged

Target price: EUR

Share price: EUR

Reuters/Bloomberg BBPI.LS/BPI PL

Market capitalisation (EURm) 1.646

Current N° of shares (m) 1.457

Free float 26%

Daily avg. no. trad. sh. 12 mth 2.301

Daily avg. trad. vol. 12 mth (m) 772

Price high 12 mth (EUR) 1,33

Price low 12 mth (EUR) 0,91

Abs. perf. 1 mth 0,00%

Abs. perf. 3 mth 1,71%

Abs. perf. 12 mth 3,29%

Key financials (EUR) 12/15 12/16e 12/17e

Total Revenue (m) 1.182 1.169 1.193

Pre-Provision Profit (PPP) (m) 492 484 497

Operating profit (OP) 373 391 413

Earnings Before Tax (m) 407 425 448

Net Profit (adj.) (m) 236 229 245

Shareholders Equity (m) 2.407 2.546 2.791

Tangible BV (m) 2.407 2.546 2.791

RWA (m) 23.294 24.419 25.404

ROTE 10,4% 9,2% 9,2%

Total Capital Ratio (B3) 11,1% 11,5% 12,0%

Cost/Income 56,7% 56,8% 56,7%

NPL ratio (gross) 3,6% 3,7% 3,7%

P/PPP 3,2 3,4 3,3

P/E (adj.) 6,7 7,2 6,7

P/BV 0,7 0,6 0,6

P/TBV 0,7 0,6 0,6

Dividend Yield 0,0% 0,0% 0,0%

PPPPS 0,34 0,33 0,34

EPS (adj.) 0,16 0,16 0,17

BVPS 1,65 1,75 1,92

TBVPS 1,65 1,75 1,92

DPS 0,00 0,00 0,00

GSM to vote on the sale of 2% of BFA (Angola) to Unitel

The facts: BPI informed the market that its Board of Directors has requested the

appointment of a General Shareholders Meeting (date to be confirmed) in order to

decide, among others, on the sale of a 2% stake on the share capital of BFA to

Unitel in Angola.

Our analysis: On 7 October, BPI informed the market that Unitel (controlled by

Mrs. Isabel dos Santos) has given its agreement to the proposal presented by BPI

related to Banco de Fomento Angola (BFA) In this context, the two parties

agreed:

The contract for the purchase and sale of BFA shares corresponding to

2% of its share capital (for an amount of EUR 28m). Following this

operation, Banco BPI’s and Unitel’s holdings in BFA’s share capital will

stand at, respectively, 48.1% and 51.9%;

The new shareholder agreement relating to BFA. This shareholder

agreement will come into effect on the date on which the transfer to

Unitel of the 2% shareholding in BFA is completed, without prejudice to

the immediate entry into force of certain rules concerning the

composition of BFA’s governing bodies.

According to BPI statement, this operation (including the change in BFA’s

statutes) is dependent on the authorization from Banco Nacional de Angola (BNA)

and should also be approved by Banco BPI General Shareholders Meeting.

Link to CaixaBank offer on BPI - It is important to recall that this proposal is

accepted in a context where the holding Santoro Finance (2nd largest

shareholder of Banco BPI with a stake of 18.6% and also controlled by Isabel dos

Santos) did not oppose to the removal of voting rights limits from BPI bylaws in

the GSM held on 21 September (essential condition for the success of the offer

presented by CaixaBank to control Banco BPI). In fact, the proposal of Banco BPI

for the sale of the 2% stake of BFA to Unitel was dependent on the removal of the

current voting right limit defined in BPI bylaws.

As we stated when BPI presented its proposal to Unitel on 20 September, this

newsflow should be seen positively for the investment case. In fact, this offer will

imply a solution for the current breach of large exposures limits to Angola (which

continues to be a key issue for the bank and a reason for ECB to pressure its

responsible to present a solution).

0,70

0,80

0,90

1,00

1,10

1,20

1,30

1,40

ott 15 nov 15 dic 15 gen 16 feb 16 mar 16 apr 16 mag 16 giu 16 lug 16 ago 16 set 16 ott 16

vvdsvdvsdy

BPI Stoxx Banks (Rebased)Source: Factset Shareholders: Caixabank 44%; Santoro 19%; Allianz

8%;

Analyst(s):

André Rodrigues, Caixa-Banco de Investimento

+351 21 389 68 39

Page 16 of 69

Produced & Distributed by the Members of ESN (see last page of this report)

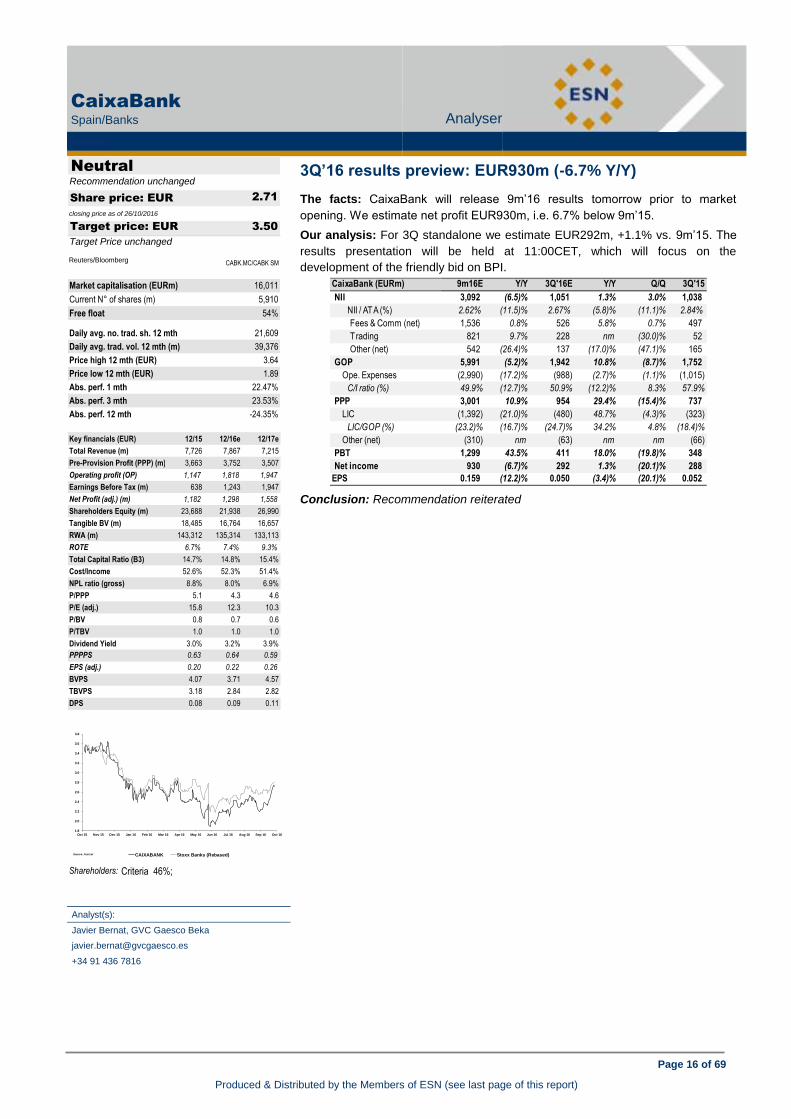

CaixaBank

Spain/Banks Analyser

BANKS

CaixaBank (Neutral) GSM to vote on the sale of 2% of BFA (Angola) to Unitel

3Q’16 results preview: EUR930m (-6.7% Y/Y)

The facts: CaixaBank will release 9m’16 results tomorrow prior to market

opening. We estimate net profit EUR930m, i.e. 6.7% below 9m’15.

Our analysis: For 3Q standalone we estimate EUR292m, +1.1% vs. 9m’15. The

results presentation will be held at 11:00CET, which will focus on the

development of the friendly bid on BPI.

Conclusion: Recommendation reiterated

Analyst(s):

Javier Bernat, GVC Gaesco Beka

+34 91 436 7816

Neutral

2.71

closing price as of 26/10/2016

3.50

Target Price unchanged

Recommendation unchanged

Target price: EUR

Share price: EUR

Reuters/Bloomberg CABK.MC/CABK SM

Market capitalisation (EURm) 16,011

Current N° of shares (m) 5,910

Free float 54%

Daily avg. no. trad. sh. 12 mth 21,609

Daily avg. trad. vol. 12 mth (m) 39,376

Price high 12 mth (EUR) 3.64

Price low 12 mth (EUR) 1.89

Abs. perf. 1 mth 22.47%

Abs. perf. 3 mth 23.53%

Abs. perf. 12 mth -24.35%

Key financials (EUR) 12/15 12/16e 12/17e

Total Revenue (m) 7,726 7,867 7,215

Pre-Provision Profit (PPP) (m) 3,663 3,752 3,507

Operating profit (OP) 1,147 1,818 1,947

Earnings Before Tax (m) 638 1,243 1,947

Net Profit (adj.) (m) 1,182 1,298 1,558

Shareholders Equity (m) 23,688 21,938 26,990

Tangible BV (m) 18,485 16,764 16,657

RWA (m) 143,312 135,314 133,113

ROTE 6.7% 7.4% 9.3%

Total Capital Ratio (B3) 14.7% 14.8% 15.4%

Cost/Income 52.6% 52.3% 51.4%

NPL ratio (gross) 8.8% 8.0% 6.9%

P/PPP 5.1 4.3 4.6

P/E (adj.) 15.8 12.3 10.3

P/BV 0.8 0.7 0.6

P/TBV 1.0 1.0 1.0

Dividend Yield 3.0% 3.2% 3.9%

PPPPS 0.63 0.64 0.59

EPS (adj.) 0.20 0.22 0.26

BVPS 4.07 3.71 4.57

TBVPS 3.18 2.84 2.82

DPS 0.08 0.09 0.11

CaixaBank (EURm) 9m16E Y/Y 3Q'16E Y/Y Q/Q 3Q'15

NII 3,092 (6.5)% 1,051 1.3% 3.0% 1,038

NII / ATA (%) 2.62% (11.5)% 2.67% (5.8)% (11.1)% 2.84%

Fees & Comm (net) 1,536 0.8% 526 5.8% 0.7% 497

T rading 821 9.7% 228 nm (30.0)% 52

Other (net) 542 (26.4)% 137 (17.0)% (47.1)% 165

GOP 5,991 (5.2)% 1,942 10.8% (8.7)% 1,752

Ope. Expenses (2,990) (17.2)% (988) (2.7)% (1.1)% (1,015)

C/I ratio (%) 49.9% (12.7)% 50.9% (12.2)% 8.3% 57.9%

PPP 3,001 10.9% 954 29.4% (15.4)% 737

LIC (1,392) (21.0)% (480) 48.7% (4.3)% (323)

LIC/GOP (%) (23.2)% (16.7)% (24.7)% 34.2% 4.8% (18.4)%

Other (net) (310) nm (63) nm nm (66)

PBT 1,299 43.5% 411 18.0% (19.8)% 348

Net income 930 (6.7)% 292 1.3% (20.1)% 288

EPS 0.159 (12.2)% 0.050 (3.4)% (20.1)% 0.052

1.8

2.0

2.2

2.4

2.6

2.8

3.0

3.2

3.4

3.6

3.8

Oct 15 Nov 15 Dec 15 Jan 16 Feb 16 Mar 16 Apr 16 May 16 Jun 16 Jul 16 Aug 16 Sep 16 Oct 16

vvdsvdvsdy

CAIXABANK Stoxx Banks (Rebased)Source: Factset

Shareholders: Criteria 46%;

Page 17 of 69

Produced & Distributed by the Members of ESN (see last page of this report)

Deutsche Bank

Germany/Banks Analyser

BANKS

Deutsche Bank (Neutral) 3Q’16 results preview: EUR930m (-6.7% Y/Y)

Q3 results above expectations due to lower one-offs

The facts: This morning DBK has reported better than expected Q3 results

mainly due to lower than forecasted costs. While one-offs came in well below our

forecast, underlying costs developed also better than expected. Total revenues

increased by 2% yoy to EUR 7.5bn (EUR 7.2bn). CT1 ratio increased by 30 bp’s

to 11.1% (equinet: 10.8%); this is excluding the positive impact from the sale of

the stake in Hua Xia Bank of around 50 bp’s. Litigation reserves increased by

EUR 0.4bn qoq to EUR 5.9bn. Liquidity reserve was down by 10% qoq to EUR

200bn.

Our analysis: FICC revenues underperformed our expectation with an increase

by 14% yoy (equinet: +25% yoy), equity trading revenues performed slightly

better than expected (-5% yoy vs. -10% yoy). Litigation costs amounted to EUR

0.5bn (equinet: EUR 0.6bn) and restructuring expenses to EUR 0.1bn (equinet:

EUR 0.5bn) and were thus below our forecast. Main difference to our forecast

was the absence of a goodwill write-down linked to the sale of Abbey; we had

expected EUR 0.8bn to be booked in Q3 ’16 – this will however be booked in

Q4’16 or Q1’17. Positively underlying costs have declined by 6% yoy to EUR

5.9bn the lowest quarterly level since at least Q1 ’15.

In Global Markets pretax profit improved to EUR 330m (Q3 ’15: EUR -2bn), higher

revenues (+10% yoy) and significantly lower costs (-49% yoy) were the main

drivers. Positively, compensation costs were down by 19% yoy. The increase of

FICC revenues by 14% yoy compares with an average of selected US Investment

Banks by 37%. In CIB improved from negative EUR 188m to EUR 640m, 45%

lower costs having been the reason, while revenues were slightly down yoy. QoQ

profit was up by 48%. In PW&CC pretax profit improved to EUR 117m due to

lower costs (-38% yoy) and higher revenues (+20% yoy). QoQ pretax profit was

down by 37%. DAM showed a pretax profit of EUR 216m (+52% yoy, +26% qoq),

higher revenues (+30% yoy, +17% qoq) more than offset higher costs (+24% yoy,

+13% qoq).

Conclusion & Action: The better than expected Q3 results are clearly a positive

surprise although the differences to our forecast stems to a large extent from

lower than forecasted one-off costs. Positively, the CT1 ratio increased by 30 bp’s

qoq to 11.2%. We stick to our Neutral recommendation with a target price of EUR

13.00. Litigation remains the key risk factor for DBK and linked to this the risk of a

capital risk.

Analyst(s):

Philipp Häßler, CFA, equinet Bank

+49 69 58997 414

Neutral

13.30

closing price as of 26/10/2016

13.00

Target Price unchanged

Recommendation unchanged

Target price: EUR

Share price: EUR

Reuters/Bloomberg DBKGn.DE/DBK GY

Market capitalisation (EURm) 18,453

Current N° of shares (m) 1,388

Free float 100%

Daily avg. no. trad. sh. 12 mth 11,659

Daily avg. trad. vol. 12 mth (m) 139,760

Price high 12 mth (EUR) 27.48

Price low 12 mth (EUR) 10.55

Abs. perf. 1 mth 26.02%

Abs. perf. 3 mth 3.46%

Abs. perf. 12 mth -51.43%

Key financials (EUR) 12/15 12/16e 12/17e

Total Revenue (m) 33,322 30,007 31,959

Pre-Provision Profit (PPP) (m) -5,345 1,802 4,466

Operating profit (OP) -6,301 602 3,266

Earnings Before Tax (m) -6,097 602 3,266

Net Profit (adj.) (m) -7,021 -121 1,664

Shareholders Equity (m) 62,678 62,154 63,818

Tangible BV (m) 57,788 57,264 58,928

RWA (m) 396,714 396,714 396,714

ROTE -12.0% -0.2% 2.9%

Total Capital Ratio (B3) 15.4% 16.0% 16.3%

Cost/Income nm 94.0% 86.0%

NPL ratio (gross) 1.9% 1.8% 1.7%

P/PPP -5.8 10.2 4.1

P/E (adj.) nm nm 11.1

P/BV 0.5 0.3 0.3

P/TBV 0.5 0.3 0.3

Dividend Yield 0.0% 0.0% 3.8%

PPPPS -3.85 1.30 3.22

EPS (adj.) -5.06 -0.09 1.20

BVPS 45.17 44.78 45.98

TBVPS 41.64 41.26 42.46

DPS 0.00 0.00 0.50

10

12

14

16

18

20

22

24

26

28

Sep 15 Oct 15 Nov 15 Dec 15 Jan 16 Feb 16 Mar 16 Apr 16 May 16 Jun 16 Jul 16 Aug 16 Sep 16 Oct 16

vvdsvdvsdy

DEUTSCHE BANK Stoxx Banks (Rebased)Source: Factset

Shareholders:

Deutsche Bank - Q3 2016

EUR m Q3 2016 Q3 2016e (eq) Q3 2015 yoy Cons. delta

Revenues 7,493 7,150 7,330 2% 7,116 5%

of which NII 3,525 3,700 3,693 -5% na

Expenses 6,547 7,901 13,223 -50% 7,415 -12%

CIR 87.4% 110.5% 180.4% -6989 Bo na

Risk provis. 327 280 207 58% 283 16%

EBT 619 -1,031 -6,100 -110% -582 -206%

Net income 256 -482 -6,013 -104% -605 -142%

Sources: Deutsche Bank, equinet Research

Page 18 of 69

Produced & Distributed by the Members of ESN (see last page of this report)

Mediobanca

Italy/Banks Analyser

BANKS

Mediobanca (Accumulate) Q3 results above expectations due to lower one-offs

Q1 results preview

The facts: Mediobanca is due to publish and present (conference call at 8.45am)

Q1 results of the 2016/17 financial year and hold the AGM on 28Th

Oct.

Our analysis: We summarize our preview in the following table:

(EUR m) Q1 16/17E Q1 15/16A Y/Y Q4 15/16A Q/Q

Revenues 521 507 2.8% 528 -1.3%

Operating costs -213 -197 8.1% -249 -14.5%

GOP 308 310 -0.6% 279 10.4%

Loan provisions -105 -115 -8.7% -100 5.0%

Net Profit 156 244 nm 162 -3.7%

Mediobanca finalised the acquisition of Barclays Italian retail operations over the

summer and consolidates them for just one month in Q1, with a limited impact of

approx. EUR 8m both on revenues (ca. EUR 5m NII and EUR 3m net

commissions) and operating costs.

Although figures are not fully comparable with previous quarters, we forecast total

revenues increasing 2.8% Y/Y to EUR 521m, driven by a 9% rise in net

commissions to EUR 105m thanks to a recovery in CIB and higher contribution

from Che Banca! The trading income is estimated at EUR 32m vs. 26m one year

ago, while the NII is seen up 1.6% Y/Y to EUR 307.5m. On the other hand, the

associates’ contribution (mainly Generali) is anticipated down 7% Y/Y to EUR

77m.

Operating costs are expected to increase 8% Y/Y to EUR 213m, fuelled by

continuous hiring and the Barclays retail consolidation, leading to a gross

operating profit (GOP) almost flat Y/Y at EUR 308m, with a C/I ratio of roughly

41%.

Loan impairments are seen down almost 9% Y/Y to EUR 105m thanks to a

benign credit cycle in consumer credit.

The expected net profit of EUR 156m is not comparable with EUR 244m booked

one year ago, which included EUR 88.5m capital gains from the disposal of the

stake held in Pirelli.

The CET1 ratio was 12.1% phased-in and 12.6% fully-loaded last June and the

Barclays retail acquisition is expected to absorb ca. 20bps.

Conclusion & Action. We expect Mediobanca’s top mgmt. to reiterate a

confident and positive message on the bank’s prospects ahead of the business

plan presentation expected next month. We stick to Accumulate with EUR 7.5

target price.

Analyst(s):

Luigi Tramontana, Banca Akros

+39 02 4344 4239

Accumulate

6.88

closing price as of 26/10/2016

7.50

Target Price unchanged

Recommendation unchanged

Target price: EUR

Share price: EUR

Reuters/Bloomberg MDBI.MI/MB IM

Market capitalisation (EURm) 5,992

Current N° of shares (m) 871

Free float 69%

Daily avg. no. trad. sh. 12 mth 4,456

Daily avg. trad. vol. 12 mth (m) 23,269

Price high 12 mth (EUR) 9.35

Price low 12 mth (EUR) 4.63

Abs. perf. 1 mth 15.92%

Abs. perf. 3 mth 17.61%

Abs. perf. 12 mth -24.64%

Key financials (EUR) 06/16 06/17e 06/18e

Total Revenue (m) 2,047 2,163 2,270

Pre-Provision Profit (PPP) (m) 1,155 1,242 1,318

Operating profit (OP) 736 824 901

Earnings Before Tax (m) 736 794 871

Net Profit (adj.) (m) 588 637 684

Shareholders Equity (m) 8,922 9,283 9,026

Tangible BV (m) 8,518 8,879 8,622

RWA (m) 53,862 55,862 57,362

ROTE 6.6% 7.0% 7.5%

Total Capital Ratio (B3) 15.3% 15.4% 15.6%

Cost/Income 43.6% 42.6% 41.9%

NPL ratio (gross) 0.0% 0.0% 0.0%

P/PPP 3.9 4.8 4.5

P/E (adj.) 7.6 9.4 8.8

P/BV 0.5 0.6 0.7

P/TBV 0.5 0.7 0.7

Dividend Yield 3.9% 4.4% 5.1%

PPPPS 1.33 1.43 1.51

EPS (adj.) 0.68 0.73 0.79

BVPS 10.24 10.66 10.36

TBVPS 9.78 10.19 9.90

DPS 0.27 0.30 0.35

4.5

5.0

5.5

6.0

6.5

7.0

7.5

8.0

8.5

9.0

9.5

Sep 15 Oct 15 Nov 15 Dec 15 Jan 16 Feb 16 Mar 16 Apr 16 May 16 Jun 16 Jul 16 Aug 16 Sep 16 Oct 16

vvdsvdvsdy

MEDIOBANCA Stoxx Banks (Rebased)Source: Factset

Shareholders: Shareholder Pact 31%;

Page 19 of 69

Produced & Distributed by the Members of ESN (see last page of this report)

Nordea

Q3/2015a

M€ Q3 OP Diff. Cons. Diff. OP Cons. Diff.

Net interest income 1,178 1,196 -1% 1,188 -1% 1,233 4746 4733 0%

Net fee income 795 787 1% 793 0% 767 3,196 3,206 0%

Net fair value items 480 388 24% 403 19% 211 1,551 1,511 3%

Total income 2,466 2,413 2% 2,413 2% 2,253 9,762 9,715 0%

Total expenses -1,183 -1,170 -01 % -1,197 1% -1,108 -4,845 -4,824 -0 %

Loan losses -135 -142 5% -147 8% -112 -529 -540 2%

Operating profit 1,148 1,101 4% 1,081 6% 1033 4,387 4,345 1%

Net profit 888 848 5% 827 7% 780 3,440 3,407 1%

EPS 0.22 0.21 5% 0.20 10% 0.19 0.85 0.84 1%

DPS 0.00 0% 0.00 0.00 0.65 0.64 2%

Source: OP and SME Direkt

Q3 2016e 2016e

Nordea

Finland/Banks Analyser

BANKS

Nordea (Neutral) Q1 results preview

Increased certainty about dividend but 2017 earnings under pressure

The facts: Nordea's Q3 operating profit of EUR 1,148m was higher than expected

(OP: EUR 2,413m; cons: EUR 2,413m), which can, however, be explained by the

heavily fluctuating fair value changes. Net interest income and net fee and

commission income nearly matched expectations. Net interest income grew 1%

QoQ on account of the partly rising lending margins. Lending remained subdued

with the exception of the strongly performing Swedish housing market. Net

interest income grew 17% YoY in Swedish retail banking operations but shrank

clearly in the large customer segment (-21% YoY). Nordea expects net interest

income to increase in Q4 2016 vs. Q3 2016 with the support of repricing

measures. Volume growth will probably remain muted on group level relative to

the peers. Fee and commission income grew 4% YoY thanks to the very strong

sentiment in asset management and record-high net inflow.

Our analysis: Even though costs were in line with expectations in the quarter, the

bank's cost control is starting to slip slightly. Costs are still expected to grow 3%

YoY in 2016, but now the estimate includes a positive non-recurring item of EUR

80–85m to be recorded for Q4 2016. Thus, comparable costs for 2016 rise by

nearly 5%. In addition, management estimates that costs will increase slightly in

2017 as well. The costs of the Temenos IT system project continue to undermine

Nordea's earnings outlook in the next few years and the anticipated significant

benefits will not become visible until in 2019-2020.

Conclusion & Action: We are downgrading our recommendation to Neutral

(from Accumulate) after the Q3 report. Although net interest income has turned to

moderate growth, we estimate that EPS will continue to decline mildly in 2017 as

the cost level and tax burdens are edging up. Earnings should return to growth in

2018, when the entry into force of the new PSD2 Directive and the planned bank

tax in Sweden will, however, bring uncertainty to the development of payment

income and the tax rate. As there are no positive drivers, we see limited upside in

the share, especially as the bank's valuation (2017 P/E 11.6) is higher than

normal. The high dividend yield (6.7%) will, however, efficiently limit the risk of a

share price decline. Our target price remains at EUR 10.

Analyst(s):

Antti Saari, OP Corporate Bank

+358 10 252 4359

Neutral

9.75

closing price as of 26/10/2016

10.00

Target Price unchanged

from Accumulate

Target price: EUR

Share price: EUR

Reuters/Bloomberg NDA1V.HE/NDA1V FH

Market capitalisation (EURm) 39,458

Current N° of shares (m) 4,047

Free float 79%

Daily avg. no. trad. sh. 12 mth 1,339

Daily avg. trad. vol. 12 mth (m) 15,914

Price high 12 mth (EUR) 10.56

Price low 12 mth (EUR) 7.10

Abs. perf. 1 mth 11.75%

Abs. perf. 3 mth 22.18%

Abs. perf. 12 mth -5.89%

Key financials (EUR) 12/15 12/16e 12/17e

Total Revenue (m) 10,140 9,804 9,912

Pre-Provision Profit (PPP) (m) 5,182 4,961 4,996

Operating profit (OP) 4,703 4,445 4,453

Earnings Before Tax (m) 4,703 4,445 4,453

Net Profit (adj.) (m) 3,662 3,493 3,393

Shareholders Equity (m) 30,946 31,152 31,874

Tangible BV (m) 28,371 28,577 29,299

RWA (m) 143,294 135,630 137,561

ROTE 11.8% 11.2% 10.6%

Total Capital Ratio (B3) 21.6% 24.3% 24.5%

Cost/Income 48.9% 49.4% 49.6%

NPL ratio (gross) 1.8% 1.9% 1.8%

P/PPP 7.9 8.0 7.9

P/E (adj.) 11.2 11.3 11.6

P/BV 1.3 1.3 1.2

P/TBV 1.4 1.4 1.3

Dividend Yield 6.6% 6.7% 6.8%

PPPPS 1.28 1.23 1.23

EPS (adj.) 0.90 0.86 0.84

BVPS 7.65 7.70 7.88

TBVPS 7.01 7.06 7.24

DPS 0.64 0.65 0.66

6.0

6.5

7.0

7.5

8.0

8.5

9.0

9.5

10.0

10.5

11.0

Sep 15 Oct 15 Nov 15 Dec 15 Jan 16 Feb 16 Mar 16 Apr 16 May 16 Jun 16 Jul 16 Aug 16 Sep 16 Oct 16

vvdsvdvsdy

NORDEA Stoxx Banks (Rebased)Source: Factset

Shareholders: Sampo plc 21%; Nordea Fonden 4%;

Swedbank Robus Funds 3%;

Page 20 of 69

Produced & Distributed by the Members of ESN (see last page of this report)

UniCredit

Italy/Banks Analyser

BANKS

UniCredit (Accumulate) Increased certainty about dividend but 2017 earnings under pressure

Possible liability management exercise?

The facts: According to the Italian press, UniCredit would be studying a liability

mgmt. exercise on the CASHES issued early-2009 as part of the capital plan to

be announced on 13th

Dec.

Our analysis: The CASHES are equity-linked instruments, issued for a

countervalue of EUR 2,983m in Feb 2009 with a maturity on Dec 2050 and

convertible, under certain conditions, into 96.75m ordinary shares underwritten by

Mediobanca.

Such shares are legitimately issued and are fully loss absorbing, but their amount

is reclassified within Additional Tier1 capital for an amount of EUR 609m (or

15bps).

The press highlights the CASHES are currently priced 35-36% of their nominal

value and the buy-back by UniCredit at a premium would offer a hefty capital gain

to the bank.

More importantly, the current holders, among which the local Foundations CRT

Carimonte and Cassamarca, as well as the Sovereign funds of Abu Dhabi and

Libya, would exit an illiquid asset for cash that could be re-invested in the

forthcoming rights issue of the group.

Conclusion & Action: Following the recent stock rally, a limited 13% upside is

left on our EUR 2.6 TP and we downgrade the stock from Buy to Accumulate.

Analyst(s):

Luigi Tramontana, Banca Akros

+39 02 4344 4239

Accumulate

2.32

closing price as of 26/10/2016

2.60

Target Price unchanged

from Buy

Target price: EUR

Share price: EUR

Reuters/Bloomberg CRDI.MI/UCG IM

Market capitalisation (EURm) 13,820

Current N° of shares (m) 5,967

Free float 66%

Daily avg. no. trad. sh. 12 mth 93,313

Daily avg. trad. vol. 12 mth (m) 160,997

Price high 12 mth (EUR) 5.78

Price low 12 mth (EUR) 1.75

Abs. perf. 1 mth 11.88%

Abs. perf. 3 mth 3.30%

Abs. perf. 12 mth -59.92%

Key financials (EUR) 12/15 12/16e 12/17e

Total Revenue (m) 22,405 22,185 22,837

Pre-Provision Profit (PPP) (m) 7,202 7,433 8,624

Operating profit (OP) 3,088 3,956 5,498

Earnings Before Tax (m) 2,671 3,476 5,498

Net Profit (adj.) (m) 2,089 1,744 3,338

Shareholders Equity (m) 50,087 50,789 51,262

Tangible BV (m) 46,468 47,171 47,644

RWA (m) 390,599 399,747 423,739

ROTE 4.5% 3.7% 7.0%

Total Capital Ratio (B3) 14.4% 13.5% 13.8%

Cost/Income 60.8% 59.6% 56.9%

NPL ratio (gross) 8.7% 8.7% 8.7%

P/PPP 4.1 1.9 1.6

P/E (adj.) 14.1 7.9 4.1

P/BV 0.6 0.3 0.3

P/TBV 0.6 0.3 0.3

Dividend Yield 5.2% 5.2% 5.2%

PPPPS 1.21 1.25 1.44

EPS (adj.) 0.35 0.29 0.56

BVPS 7.78 7.90 7.98

TBVPS 7.78 7.90 7.98

DPS 0.12 0.12 0.12

1.5

2.0

2.5

3.0

3.5

4.0

4.5

5.0

5.5

6.0

set 15 ott 15 nov 15 dic 15 gen 16 feb 16 mar 16 apr 16 mag 16 giu 16 lug 16 ago 16 set 16 ott 16

vvdsvdvsdy

UNICREDIT Stoxx Banks (Rebased)Source: Factset

Shareholders: Fondaz. Cariverona 4%; Fondaz. CRT

3%; Carimonte Holding 2%; Central Bank

of Libya 3%; Aabar 5%; Del Vecchio 3%;

Page 21 of 69

Produced & Distributed by the Members of ESN (see last page of this report)

Acerinox

Spain/Basic Resources Analyser

BASIC RESOURCES

Acerinox (Buy) Possible liability management exercise?

Comments from 3Q’16 results presentation

The facts: Acerinox held its 3Q’16 results presentation yesterday.

Our analysis: The most relevant aspects from these results were:

Acerinox expects 4Q’16 to be below 3Q’16 (EUR103m) but EBITDA will allow

the full year EBITDA grow at double digits. This implies obtaining between

EUR92 and 102m EBITDA in 4Q. Hence, the annual EBITDA would reach

between EUR315m and EUR325m, practically in line with consensus’

EUR321m EBITDA for 2016. Our estimates are 6% higher. Net debt is also

performing better than expected.

Prices in Europe: Acerinox announced a rise of EUR50/t in Spain and

Portugal where the Company holds 60% market share. This price hike will be

seen in 1Q’17. We expect to see more rises in base prices in other European

countries, as these are less pressured and the conditions in demand and

stocks accompany the rise. Prices in US: stable following three hikes in

1H’16. New price hikes took place in specific qualities and there is room for

more, but would prefer to increase prices again when the moment is ripe, not

in 4Q’16 but possibly in 1Q’17.

Conclusion: We are positive with Acerinox’ results that will improve but a little

slower than estimated.

Analyst(s):

Iñigo Recio Pascual, GVC Gaesco Beka

+34 91 436 7814

Buy

11.66

closing price as of 26/10/2016

14.00

Target Price unchanged

Recommendation unchanged

Target price: EUR

Share price: EUR

Reuters/Bloomberg ACX.MC/ACX SM

Market capitalisation (EURm) 3,219

Current N° of shares (m) 276

Free float 40%

Daily avg. no. trad. sh. 12 mth 1,933

Daily avg. trad. vol. 12 mth (m) 22,273

Price high 12 mth (EUR) 11.96

Price low 12 mth (EUR) 7.15

Abs. perf. 1 mth 0.13%

Abs. perf. 3 mth 1.70%

Abs. perf. 12 mth 10.68%

Key financials (EUR) 12/15 12/16e 12/17e

Sales (m) 4,221 4,016 4,750

EBITDA (m) 286 340 482

EBITDA margin 6.8% 8.5% 10.1%

EBIT (m) 121 175 316

EBIT margin 2.9% 4.4% 6.6%

Net Profit (adj.)(m) 43 93 180

ROCE 3.1% 4.5% 7.8%

Net debt/(cash) (m) 711 715 778

Net Debt/Equity 0.4 0.4 0.4

Debt/EBITDA 2.5 2.1 1.6

Int. cover(EBITDA/Fin. int) 6.1 9.4 12.9

EV/Sales 0.7 1.0 0.8

EV/EBITDA 10.9 11.2 8.0

EV/EBITDA (adj.) 10.9 11.2 8.0

EV/EBIT 25.9 21.8 12.3

P/E (adj.) nm 34.7 17.9

P/BV 1.3 1.7 1.6

OpFCF yield -7.3% 3.6% 1.9%

Dividend yield 3.9% 3.9% 3.9%

EPS (adj.) 0.16 0.34 0.65

BVPS 7.23 6.90 7.10

DPS 0.45 0.45 0.45

6

7

8

9

10

11

12

13

Oct 15 Nov 15 Dec 15 Jan 16 Feb 16 Mar 16 Apr 16 May 16 Jun 16 Jul 16 Aug 16 Sep 16 Oct 16

vvdsvdvsdy

ACERINOX Stoxx Basic Resources (Rebased)Source: Factset

Shareholders: CF Alba 20%; Omega Capital 12%;

Nisshin Steel 15%;

Page 22 of 69

Produced & Distributed by the Members of ESN (see last page of this report)

Ence

Spain/Basic Resources Analyser

BASIC RESOURCES

Ence (Buy) Comments from 3Q’16 results presentation

9m’16 results

The facts: Ence presented results at market close yesterday.

Our analysis: Results in line with our forecasts.

The quarter was characterised by the -3.1% drop vs. 2Q’16 in average pulp prices

in USD, offset by the slightly more favourable USD/EUR for Ence

(USD/EUR1.116 vs. 1.129 2Q). Tons sold were below forecasts, according to

Ence due to the price hike announced for 4Q’16 – quarter in which the Company

expects higher volumes.

Net debt dropped in 3Q to EUR233.5m, EUR7.7m below 2015.

Conclusion: Results in line with forecasts, with greater volume from the capital

gains proceeding from land sales. Ence announced a USD10/t price hike as from

October and FOEX prices include a small rise up to USD656.69/t, thus we could

see the beginning of stabilising/rebounding prices, which would be positive news.

Conference call today at 16:00.

Analyst(s):

Iñigo Recio Pascual, GVC Gaesco Beka

+34 91 436 7814

Buy

2.05

closing price as of 26/10/2016

2.90

Target Price unchanged

Recommendation unchanged

Target price: EUR

Share price: EUR

Reuters/Bloomberg ENC.MC/ENC SM

Market capitalisation (EURm) 512

Current N° of shares (m) 250

Free float 39%

Daily avg. no. trad. sh. 12 mth 1,174

Daily avg. trad. vol. 12 mth (m) 3,726

Price high 12 mth (EUR) 3.75

Price low 12 mth (EUR) 1.81

Abs. perf. 1 mth 0.99%

Abs. perf. 3 mth -7.88%

Abs. perf. 12 mth -38.96%

Key financials (EUR) 12/15 12/16e 12/17e

Sales (m) 664 602 597

EBITDA (m) 192 115 115

EBITDA margin 28.9% 19.1% 19.3%

EBIT (m) 133 49 48

EBIT margin 20.1% 8.1% 8.1%

Net Profit (adj.)(m) 79 21 22

ROCE 13.6% 5.4% 5.3%

Net debt/(cash) (m) 241 214 205

Net Debt/Equity 0.4 0.4 0.4

Debt/EBITDA 1.3 1.9 1.8

Int. cover(EBITDA/Fin. int) 3.6 5.7 6.0

EV/Sales 1.7 1.2 1.2

EV/EBITDA 5.9 6.3 6.2

EV/EBITDA (adj.) 5.9 6.3 6.2

EV/EBIT 8.4 14.7 14.7

P/E (adj.) 11.1 24.0 23.7

P/BV 1.5 0.9 0.9

OpFCF yield 4.4% 7.6% 4.7%

Dividend yield 7.0% 2.9% 2.9%

EPS (adj.) 0.32 0.09 0.09

BVPS 2.27 2.21 2.24

DPS 0.14 0.06 0.06

ENCE: 9M16 RESULTS

9M15 %sles 9M16 %sles % y/y 9M16e % dev

Total sales 486,7 100% 429,7 100% -12% 440,8 -3%

EBITDA 129,7 27% 83,4 19% -36% 84,0 -1%

Depreciation & provs -46,0 -9% -39,5 -9% -14% -41,7 -5%

EBIT 83,7 17% 43,9 10% -48% 42,3 4%

Financial Results -35,5 -7% -12,0 -3% -66% -13,9 -14%

EBT 48,1 10% 31,9 7% -34% 28,4 12%

Taxes -13,1 -3% -7,6 -2% -42% -7,5 2%

Net Profit 35,0 7% 24,3 6% -31% 20,9 16%

Source: GVC Gaesco Beka estimates

1.8

2.0

2.2

2.4

2.6

2.8

3.0

3.2

3.4

3.6

3.8

Oct 15 Nov 15 Dec 15 Jan 16 Feb 16 Mar 16 Apr 16 May 16 Jun 16 Jul 16 Aug 16 Sep 16 Oct 16

vvdsvdvsdy

ENCE IGBM (Rebased)Source: Factset

Shareholders: Retos Operativos XXI 26%; Alcor Holding

10%; Fuente Salada 5%;

Page 23 of 69

Produced & Distributed by the Members of ESN (see last page of this report)

Europac

Spain/Basic Resources Analyser

BASIC RESOURCES

Europac (Accumulate) 9m’16 results

Good 9m’16 results

The facts: Europac presented 3Q’16 results

Our analysis: In our previous note we mentioned that 3Q’16 results could drop a

little based on the seasonal effects and the downward inertia of prices in 1H’16

and, in the end, the fall in EBITDA was hardly noted, despite the small drop in

prices.

Conclusion: Results are still positive and in line with forecasts, despite paper

prices dropping during the year. The accumulated correction and bonus issue are

reasons to buy shares. If testliner prices stabilise, these would further support our

positive opinion on the company.

Analyst(s):

Iñigo Recio Pascual, GVC Gaesco Beka

+34 91 436 7814

Accumulate

4.90

closing price as of 26/10/2016

5.90

Target Price unchanged

Recommendation unchanged

Target price: EUR

Share price: EUR

Reuters/Bloomberg PYCE.MC/PAC SM

Market capitalisation (EURm) 459

Current N° of shares (m) 94

Free float 38%

Daily avg. no. trad. sh. 12 mth 54

Daily avg. trad. vol. 12 mth (m) 318

Price high 12 mth (EUR) 5.60

Price low 12 mth (EUR) 4.32

Abs. perf. 1 mth 1.14%

Abs. perf. 3 mth -4.95%

Abs. perf. 12 mth 1.31%

Key financials (EUR) 12/15 12/16e 12/17e

Sales (m) 806 831 849

EBITDA (m) 111 121 129