Embed Size (px)

Citation preview

ESMA Risk Dashboard No. 1, 2018

ESMA Risk Dashboard No. 1, 2018 2

ESMA Risk Dashboard No. 1, 2018

© European Securities and Markets Authority, Paris, 2018. All rights reserved. Brief excerpts may be reproduced or translated provided the source is cited adequately. The reporting period of this Report is 1 October 2017 to 31 December 2017, unless indicated otherwise. Legal reference of this Report: Regulation (EU) No 1095/2010 of the European Parliament and of the Council of 24 November 2010 establishing a European Supervisory Authority (European Securities and Markets Authority), amending Decision No 716/2009/EC and repealing Commission Decision 2009/77/EC, Article 32 “Assessment of market developments”, 1. “The Authority shall monitor and assess market developments in the area of its competence and, where necessary, inform the European Supervisory Authority (European Banking Authority), and the European Supervisory Authority (European Insurance and Occupational Pensions Authority), the ESRB and the European Parliament, the Council and the Commission about the relevant micro-prudential trends, potential risks and vulnerabilities. The Authority shall include in its assessments an economic analysis of the markets in which financial market participants operate, and an assessment of the impact of potential market developments on such financial market participants.” The information contained in this publication, including text, charts and data, exclusively serves analytical purposes. It does not provide forecasts or investment advice, and does not prejudice, preclude or influence in any way past, existing or future regulatory or supervisory obligations on market participants. The charts and analyses in this report are, fully or in parts, based on data not proprietary to ESMA, including from commercial data providers and public authorities. ESMA uses these data in good faith and does not take responsibility for their accuracy or completeness. ESMA is committed to constantly improving its data sources and reserves the right to alter data sources at any time. The third-party data used in this publication may be subject to provider-specific disclaimers, especially regarding its ownership, its reuse by non-customers and, in particular, the accuracy, completeness or timeliness of the data provided and the provider’s liability related to those. Please consult the websites of the individual data providers, whose names are detailed throughout this report, for more details on these disclaimers. Where third-party data are used to create any chart, table or analysis the third party is identified and credited as the source. In each case, ESMA is cited by default as a source, reflecting any data management, cleaning, processing, matching, analytical, editorial or other adjustments to raw data undertaken.

European Securities and Markets Authority (ESMA) Risk Analysis and Economics Department 103, Rue de Grenelle FR–75007 Paris [email protected]

ESMA Risk Dashboard No. 1, 2018 3

ESMA Risk Dashboard

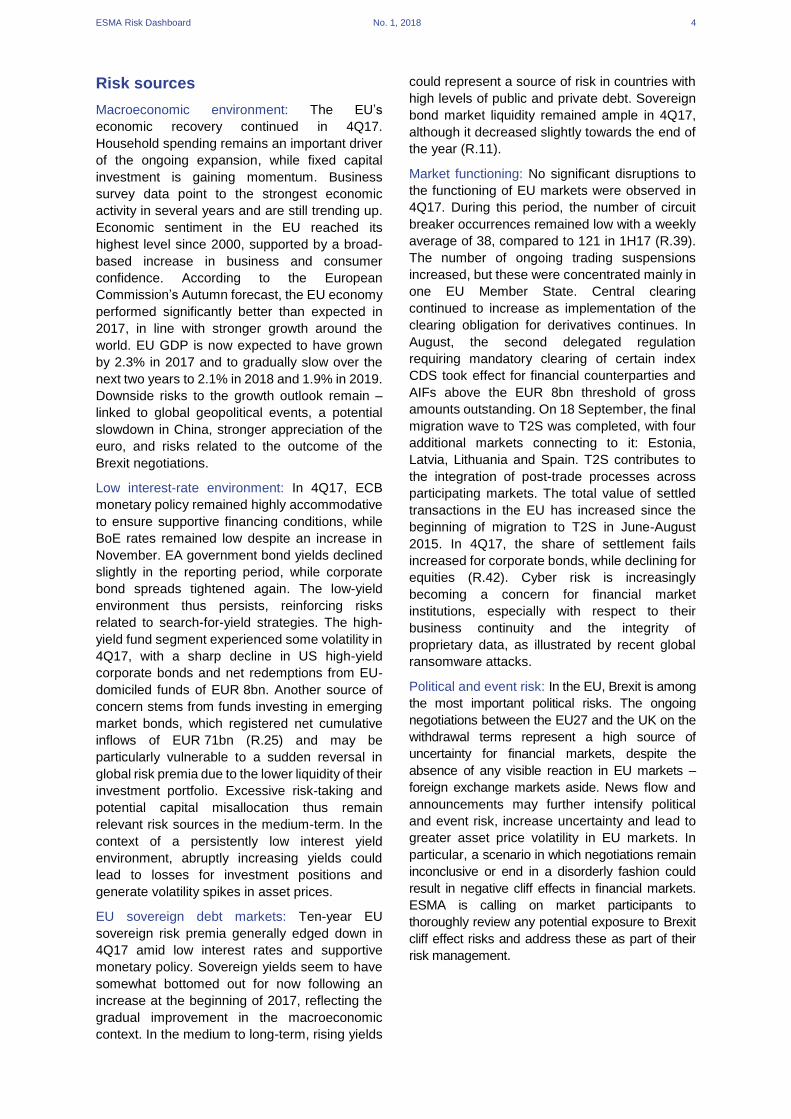

R.1

Main risks

Risk segments Risk categories Risk sources

Risk Outlook Risk Outlook

Outlook

Overall ESMA remit Liquidity

Macroeconomic environment

Systemic stress Market

Low interest rate environment

Securities markets Contagion

EU sovereign debt markets

Investors Credit

Infrastructure disruptions, incl. cyber risks

Infrastructures and services Operational

Political and event risks

Note: Assessment of main risks by risk segments for markets under ESMA remit since last assessment, and outlook for forthcoming quarter. Assessment of main risks by risk categories and sources for markets under ESMA remit since last assessment, and outlook for forthcoming quarter. Risk assessment based on categorisation of the ESA Joint Committee. Colours indicate current risk intensity. Coding: green=potential risk, yellow=elevated risk, orange=high risk, red=very high risk. Upward arrows indicate an increase in risk intensities, downward arrows a decrease, horizontal arrows no change. Change is measured with respect to the previous quarter; the outlook refers to the forthcoming quarter. ESMA risk assessment based on quantitative indicators and analyst judgement.

ESMA’s 4Q17 overall risk assessment is unchanged from 3Q17. EU financial markets remained calm during the quarter, with limited reactivity to global geopolitical events. While benign market conditions prevailed during the reporting period, February 2018 saw severe market corrections and the return of equity market volatility, confirming our prevailing valuation concerns. ESMA’s market risk assessment remains very high. However, our assessment for credit risk has improved from very high to high. The outlook for market, liquidity and contagion risks is stable. Operational risk continues to be elevated, with a deteriorating outlook, due to Brexit-related risk to business operations and the mounting risk of cyber-attacks. The main sources of risk remain a potential repricing of risk premia and geopolitical developments whose effects may spill over to global financial markets. On the perimeter of global securities markets, the latter months saw extreme volatility in the prices of virtual currencies and strong growth in Initial Coin Offerings.

Risk summary

Risks in the markets under ESMA’s remit

remained at high levels, reflecting very high risk

in securities markets and elevated risk for

investors, infrastructures and services. ESMA’s

market risk assessment was again very high.

While benign market conditions prevailed during

the reporting period, the beginning of February

2018 saw severe market corrections and the

return of equity market volatility, confirming our

prevailing valuation concerns. On the other hand,

the level of credit risk eased from very high to

high, reflecting a strengthening macroeconomic

environment and higher credit ratings in several

EU member states, although the deterioration in

outstanding corporate ratings persisted. Liquidity

risk in 4Q17 remained high despite

improvements in securities markets. Operational

risk was elevated, but with a deteriorating risk

outlook as concerns mount over potential cyber-

attacks. The risk outlook was stable across the

other risk categories. On the perimeter of global

securities markets, the latter months saw an

extraordinary rise and subsequent fall in prices of

virtual currencies, as well as growing issuance of

Initial Coin Offerings (ICOs). ESMA has warned

against the substantial risks associated with

investments in virtual currencies and ICOs.

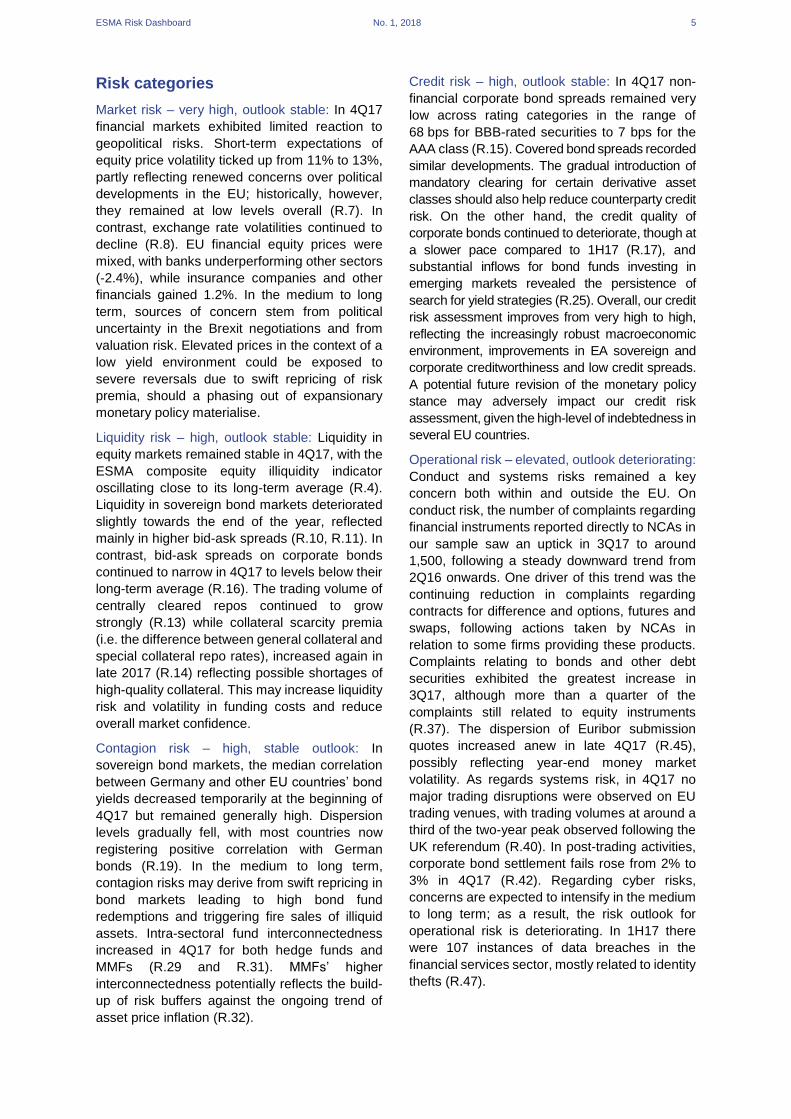

Systemic stress remained at very low levels in

4Q17, based on the composite systemic stress

indicator (R.2). Within securities markets, bond

markets again registered the highest contribution

to the systemic stress measure.

R.2 ESMA composite systemic stress indicator

Systemic risk broadly stable

-0.4

-0.2

0

0.2

0.4

0.6

Dec-13 Dec-14 Dec-15 Dec-16 Dec-17

Equity market contribution Bond market contribution

Money market contribution ESMA CISS

Correlation contribution

Note: ESMA version of the ECB-CISS indicator measuring sys temic str ess insecurities markets. It focuses on three financial market segments: equity , bondand money markets , aggregated through standard portfolio theory. It is based on

securities market indicators such as volatilities and risk spreads.Sources: ECB, ESMA.

ESMA Risk Dashboard No. 1, 2018 4

Risk sources

Macroeconomic environment: The EU’s

economic recovery continued in 4Q17.

Household spending remains an important driver

of the ongoing expansion, while fixed capital

investment is gaining momentum. Business

survey data point to the strongest economic

activity in several years and are still trending up.

Economic sentiment in the EU reached its

highest level since 2000, supported by a broad-

based increase in business and consumer

confidence. According to the European

Commission’s Autumn forecast, the EU economy

performed significantly better than expected in

2017, in line with stronger growth around the

world. EU GDP is now expected to have grown

by 2.3% in 2017 and to gradually slow over the

next two years to 2.1% in 2018 and 1.9% in 2019.

Downside risks to the growth outlook remain ‒

linked to global geopolitical events, a potential

slowdown in China, stronger appreciation of the

euro, and risks related to the outcome of the

Brexit negotiations.

Low interest-rate environment: In 4Q17, ECB

monetary policy remained highly accommodative

to ensure supportive financing conditions, while

BoE rates remained low despite an increase in

November. EA government bond yields declined

slightly in the reporting period, while corporate

bond spreads tightened again. The low-yield

environment thus persists, reinforcing risks

related to search-for-yield strategies. The high-

yield fund segment experienced some volatility in

4Q17, with a sharp decline in US high-yield

corporate bonds and net redemptions from EU-

domiciled funds of EUR 8bn. Another source of

concern stems from funds investing in emerging

market bonds, which registered net cumulative

inflows of EUR 71bn (R.25) and may be

particularly vulnerable to a sudden reversal in

global risk premia due to the lower liquidity of their

investment portfolio. Excessive risk-taking and

potential capital misallocation thus remain

relevant risk sources in the medium-term. In the

context of a persistently low interest yield

environment, abruptly increasing yields could

lead to losses for investment positions and

generate volatility spikes in asset prices.

EU sovereign debt markets: Ten-year EU

sovereign risk premia generally edged down in

4Q17 amid low interest rates and supportive

monetary policy. Sovereign yields seem to have

somewhat bottomed out for now following an

increase at the beginning of 2017, reflecting the

gradual improvement in the macroeconomic

context. In the medium to long-term, rising yields

could represent a source of risk in countries with

high levels of public and private debt. Sovereign

bond market liquidity remained ample in 4Q17,

although it decreased slightly towards the end of

the year (R.11).

Market functioning: No significant disruptions to

the functioning of EU markets were observed in

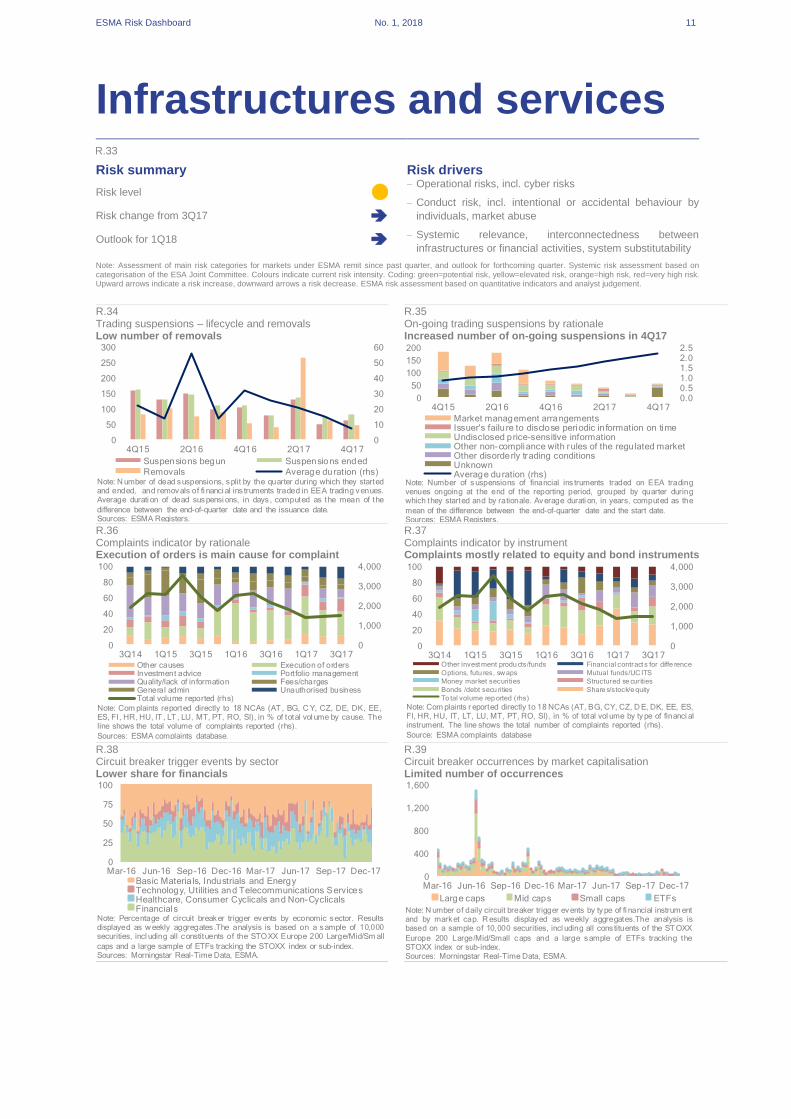

4Q17. During this period, the number of circuit

breaker occurrences remained low with a weekly

average of 38, compared to 121 in 1H17 (R.39).

The number of ongoing trading suspensions

increased, but these were concentrated mainly in

one EU Member State. Central clearing

continued to increase as implementation of the

clearing obligation for derivatives continues. In

August, the second delegated regulation

requiring mandatory clearing of certain index

CDS took effect for financial counterparties and

AIFs above the EUR 8bn threshold of gross

amounts outstanding. On 18 September, the final

migration wave to T2S was completed, with four

additional markets connecting to it: Estonia,

Latvia, Lithuania and Spain. T2S contributes to

the integration of post-trade processes across

participating markets. The total value of settled

transactions in the EU has increased since the

beginning of migration to T2S in June-August

2015. In 4Q17, the share of settlement fails

increased for corporate bonds, while declining for

equities (R.42). Cyber risk is increasingly

becoming a concern for financial market

institutions, especially with respect to their

business continuity and the integrity of

proprietary data, as illustrated by recent global

ransomware attacks.

Political and event risk: In the EU, Brexit is among

the most important political risks. The ongoing

negotiations between the EU27 and the UK on the

withdrawal terms represent a high source of

uncertainty for financial markets, despite the

absence of any visible reaction in EU markets ‒

foreign exchange markets aside. News flow and

announcements may further intensify political

and event risk, increase uncertainty and lead to

greater asset price volatility in EU markets. In

particular, a scenario in which negotiations remain

inconclusive or end in a disorderly fashion could

result in negative cliff effects in financial markets.

ESMA is calling on market participants to

thoroughly review any potential exposure to Brexit

cliff effect risks and address these as part of their

risk management.

ESMA Risk Dashboard No. 1, 2018 5

Risk categories

Market risk – very high, outlook stable: In 4Q17

financial markets exhibited limited reaction to

geopolitical risks. Short-term expectations of

equity price volatility ticked up from 11% to 13%,

partly reflecting renewed concerns over political

developments in the EU; historically, however,

they remained at low levels overall (R.7). In

contrast, exchange rate volatilities continued to

decline (R.8). EU financial equity prices were

mixed, with banks underperforming other sectors

(-2.4%), while insurance companies and other

financials gained 1.2%. In the medium to long

term, sources of concern stem from political

uncertainty in the Brexit negotiations and from

valuation risk. Elevated prices in the context of a

low yield environment could be exposed to

severe reversals due to swift repricing of risk

premia, should a phasing out of expansionary

monetary policy materialise.

Liquidity risk – high, outlook stable: Liquidity in

equity markets remained stable in 4Q17, with the

ESMA composite equity illiquidity indicator

oscillating close to its long-term average (R.4).

Liquidity in sovereign bond markets deteriorated

slightly towards the end of the year, reflected

mainly in higher bid-ask spreads (R.10, R.11). In

contrast, bid-ask spreads on corporate bonds

continued to narrow in 4Q17 to levels below their

long-term average (R.16). The trading volume of

centrally cleared repos continued to grow

strongly (R.13) while collateral scarcity premia

(i.e. the difference between general collateral and

special collateral repo rates), increased again in

late 2017 (R.14) reflecting possible shortages of

high-quality collateral. This may increase liquidity

risk and volatility in funding costs and reduce

overall market confidence.

Contagion risk – high, stable outlook: In

sovereign bond markets, the median correlation

between Germany and other EU countries’ bond

yields decreased temporarily at the beginning of

4Q17 but remained generally high. Dispersion

levels gradually fell, with most countries now

registering positive correlation with German

bonds (R.19). In the medium to long term,

contagion risks may derive from swift repricing in

bond markets leading to high bond fund

redemptions and triggering fire sales of illiquid

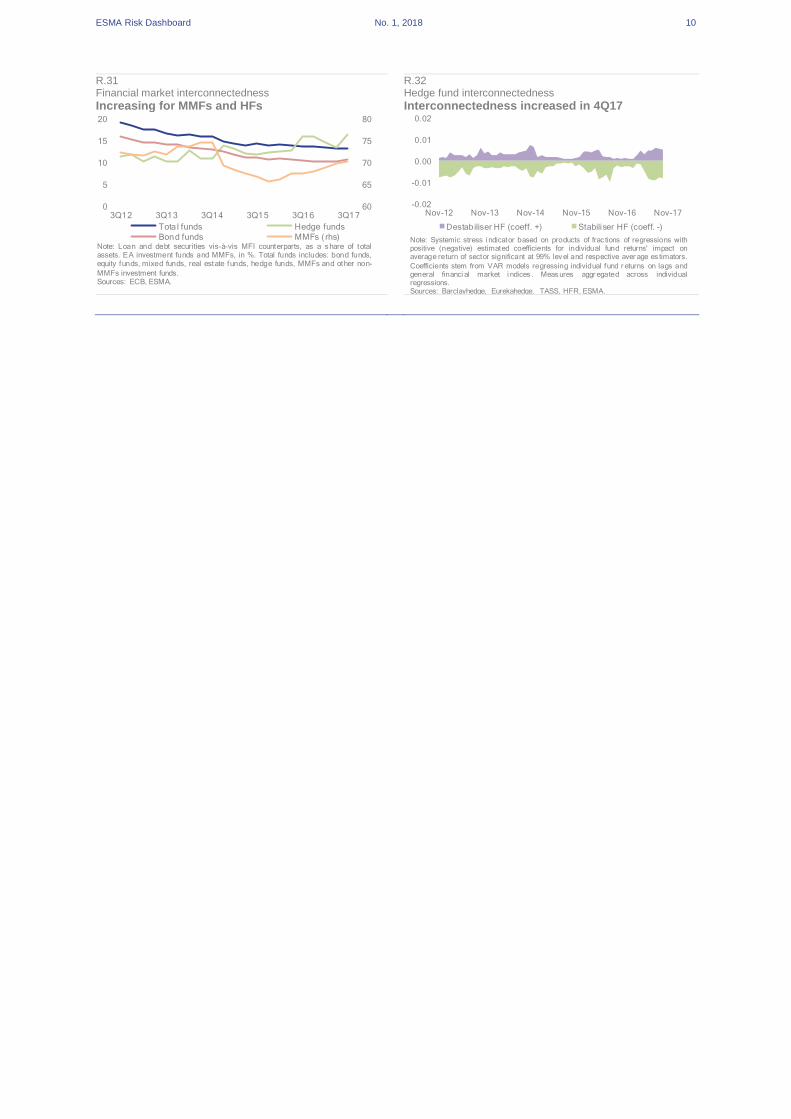

assets. Intra-sectoral fund interconnectedness

increased in 4Q17 for both hedge funds and

MMFs (R.29 and R.31). MMFs’ higher

interconnectedness potentially reflects the build-

up of risk buffers against the ongoing trend of

asset price inflation (R.32).

Credit risk – high, outlook stable: In 4Q17 non-

financial corporate bond spreads remained very

low across rating categories in the range of

68 bps for BBB-rated securities to 7 bps for the

AAA class (R.15). Covered bond spreads recorded

similar developments. The gradual introduction of

mandatory clearing for certain derivative asset

classes should also help reduce counterparty credit

risk. On the other hand, the credit quality of

corporate bonds continued to deteriorate, though at

a slower pace compared to 1H17 (R.17), and

substantial inflows for bond funds investing in

emerging markets revealed the persistence of

search for yield strategies (R.25). Overall, our credit

risk assessment improves from very high to high,

reflecting the increasingly robust macroeconomic

environment, improvements in EA sovereign and

corporate creditworthiness and low credit spreads.

A potential future revision of the monetary policy

stance may adversely impact our credit risk

assessment, given the high-level of indebtedness in

several EU countries.

Operational risk – elevated, outlook deteriorating:

Conduct and systems risks remained a key

concern both within and outside the EU. On

conduct risk, the number of complaints regarding

financial instruments reported directly to NCAs in

our sample saw an uptick in 3Q17 to around

1,500, following a steady downward trend from

2Q16 onwards. One driver of this trend was the

continuing reduction in complaints regarding

contracts for difference and options, futures and

swaps, following actions taken by NCAs in

relation to some firms providing these products.

Complaints relating to bonds and other debt

securities exhibited the greatest increase in

3Q17, although more than a quarter of the

complaints still related to equity instruments

(R.37). The dispersion of Euribor submission

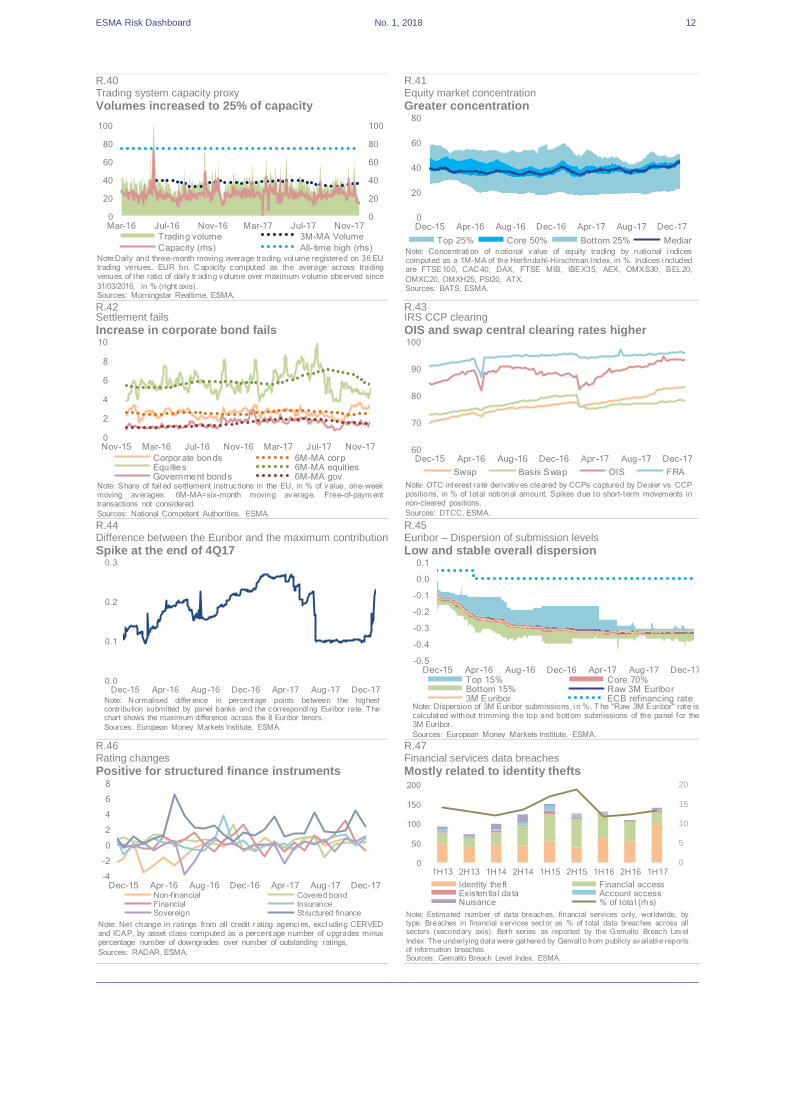

quotes increased anew in late 4Q17 (R.45),

possibly reflecting year-end money market

volatility. As regards systems risk, in 4Q17 no

major trading disruptions were observed on EU

trading venues, with trading volumes at around a

third of the two-year peak observed following the

UK referendum (R.40). In post-trading activities,

corporate bond settlement fails rose from 2% to

3% in 4Q17 (R.42). Regarding cyber risks,

concerns are expected to intensify in the medium

to long term; as a result, the risk outlook for

operational risk is deteriorating. In 1H17 there

were 107 instances of data breaches in the

financial services sector, mostly related to identity

thefts (R.47).

ESMA Risk Dashboard No. 1, 2018 6

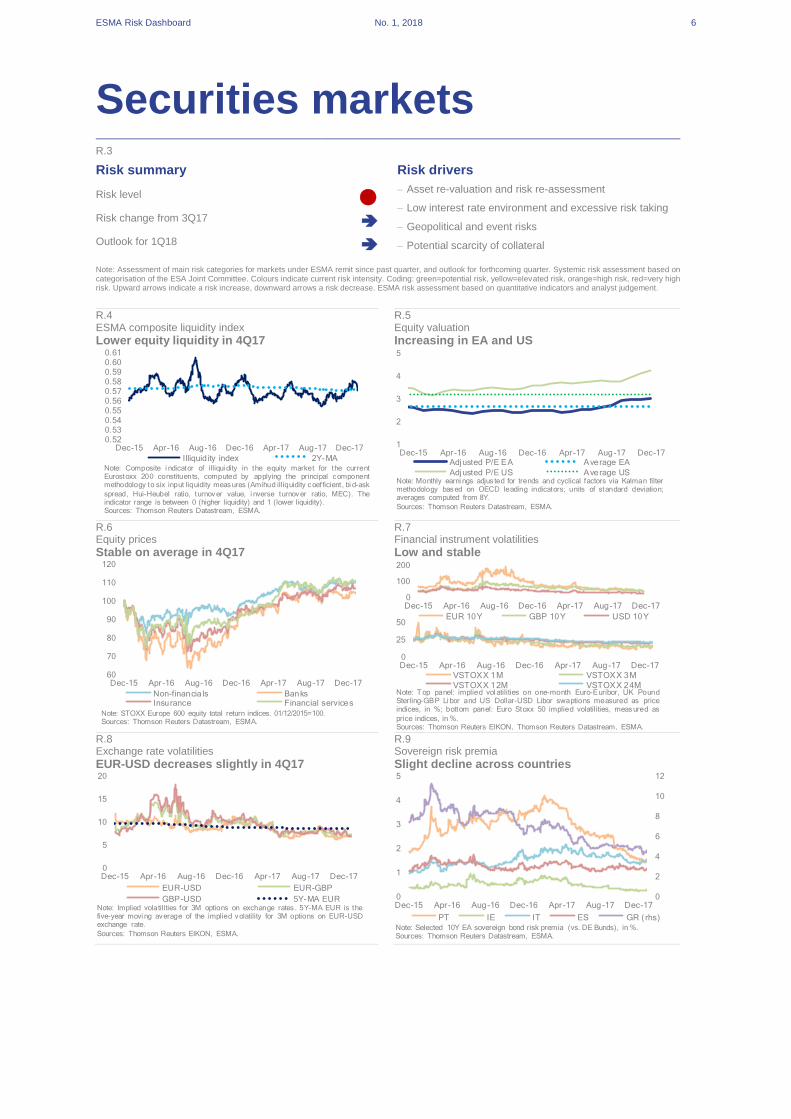

Securities markets R.3

Risk summary Risk drivers

Risk level – Asset re-valuation and risk re-assessment

– Low interest rate environment and excessive risk taking

– Geopolitical and event risks

– Potential scarcity of collateral

Risk change from 3Q17

Outlook for 1Q18

Note: Assessment of main risk categories for markets under ESMA remit since past quarter, and outlook for forthcoming quarter. Systemic risk assessment based on categorisation of the ESA Joint Committee. Colours indicate current risk intensity. Coding: green=potential risk, yellow=elevated risk, orange=high risk, red=very high risk. Upward arrows indicate a risk increase, downward arrows a risk decrease. ESMA risk assessment based on quantitative indicators and analyst judgement.

R.4 R.5 ESMA composite liquidity index Equity valuation

Lower equity liquidity in 4Q17 Increasing in EA and US

R.6 R.7 Equity prices Financial instrument volatilities

Stable on average in 4Q17 Low and stable

R.8 R.9 Exchange rate volatilities Sovereign risk premia

EUR-USD decreases slightly in 4Q17 Slight decline across countries

0.520.530.540.550.560.570.580.590.600.61

Dec-15 Apr-16 Aug-16 Dec-16 Apr-17 Aug-17 Dec-17

Illiquid ity index 2Y-MANote: Composite i ndicator of illiqui dity in the equity market for the currentEurostoxx 200 constituents, computed by applying the principal componentmethodology to six input liquidity measures (Amihud illiquidity coefficient, bi d-ask

spread, Hui-Heubel ratio, turnover value, i nverse turnover ratio, MEC). Theindicator range is between 0 (higher liquidity) and 1 (lower liquidity).Sources: Thomson Reuters Datastream, ESMA.

1

2

3

4

5

Dec-15 Apr-16 Aug-16 Dec-16 Apr-17 Aug-17 Dec-17Adjusted P/E EA Average EA

Adjusted P/E US Average USNote: Monthly earni ngs adjus ted for trends and cyclical factors via Kalman filtermethodology based on OECD leading indicators; units of standard deviation;averages computed from 8Y.

Sources: Thomson Reuters Datastream, ESMA.

60

70

80

90

100

110

120

Dec-15 Apr-16 Aug-16 Dec-16 Apr-17 Aug-17 Dec-17

Non-financia ls BanksInsurance Financial services

Note: STOXX Europe 600 equity total return indices. 01/12/2015=100.Sources: Thomson Reuters Datastream, ESMA.

0

25

50

Dec-15 Apr-16 Aug-16 Dec-16 Apr-17 Aug-17 Dec-17

VSTOXX 1M VSTOXX 3M

VSTOXX 12M VSTOXX 24MNote: T op panel: implied vol atilities on one-month Euro-Euribor, UK PoundSterling-GBP Li bor and US Dollar-USD Libor swaptions measured as priceindices, in %; bottom panel: Euro Stoxx 50 implied volatilities, measured as

price indices, in %.Sources: Thomson Reuters EIKON, Thomson Reuters Datastream, ESMA.

0

100

200

Dec-15 Apr-16 Aug-16 Dec-16 Apr-17 Aug-17 Dec-17

EUR 10Y GBP 10Y USD 10Y

0

5

10

15

20

Dec-15 Apr-16 Aug-16 Dec-16 Apr-17 Aug-17 Dec-17

EUR-USD EUR-GBP

GBP-USD 5Y-MA EURNote: Implied volatilities for 3M options on exchange rates . 5Y-MA EUR is thefive-year movi ng average of the implied volatility for 3M options on EUR-USDexchange rate.

Sources: Thomson Reuters EIKON, ESMA.

0

2

4

6

8

10

12

0

1

2

3

4

5

Dec-15 Apr-16 Aug-16 Dec-16 Apr-17 Aug-17 Dec-17

PT IE IT ES GR (rhs)Note: Selected 10Y EA sovereign bond risk premia (vs. DE Bunds), in %.Sources: Thomson Reuters Datastream, ESMA.

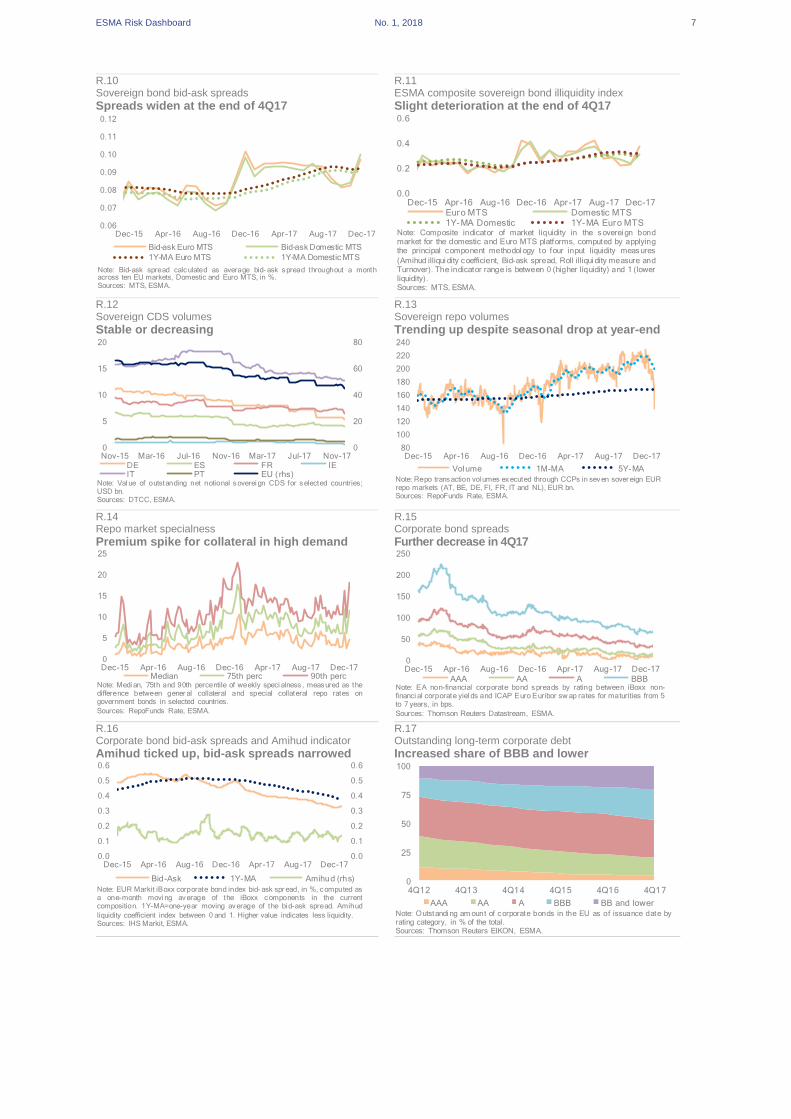

ESMA Risk Dashboard No. 1, 2018 7

R.10 R.11 Sovereign bond bid-ask spreads ESMA composite sovereign bond illiquidity index

Spreads widen at the end of 4Q17 Slight deterioration at the end of 4Q17

R.12 R.13 Sovereign CDS volumes

Sovereign repo volumes

Stable or decreasing Trending up despite seasonal drop at year-end

R.14 R.15 Repo market specialness Corporate bond spreads

Premium spike for collateral in high demand Further decrease in 4Q17

R.16 R.17 Corporate bond bid-ask spreads and Amihud indicator Outstanding long-term corporate debt

Amihud ticked up, bid-ask spreads narrowed Increased share of BBB and lower

0.06

0.07

0.08

0.09

0.10

0.11

0.12

Dec-15 Apr-16 Aug-16 Dec-16 Apr-17 Aug-17 Dec-17

Bid-ask Euro MTS Bid-ask Domestic MTS

1Y-MA Euro MTS 1Y-MA Domestic MTS

Note: Bid-ask spread calculated as average bid- ask spread throughout a monthacross ten EU markets, Domestic and Euro MTS, in %.Sources: MTS, ESMA.

0.0

0.2

0.4

0.6

Dec-15 Apr-16 Aug-16 Dec-16 Apr-17 Aug-17 Dec-17Euro MTS Domestic MTS1Y-MA Domestic 1Y-MA Euro MTS

Note: Composite indicator of market liquidity in the soverei gn bondmarket for the domestic and Euro MTS platforms, computed by applyingthe principal component methodol ogy to four input liquidity measures

(Amihud illiqui dity coefficient, Bid-ask spread, Roll illiqui dity measure andTurnover). The indicator range is between 0 (higher liquidity) and 1 (lowerliquidity).Sources: MTS, ESMA.

0

20

40

60

80

0

5

10

15

20

Nov-15 Mar-16 Jul-16 Nov-16 Mar-17 Jul-17 Nov-17DE ES FR IEIT PT EU ( rhs)

Note: Val ue of outstanding net notional soverei gn CDS for selected countries;USD bn.Sources: DTCC, ESMA.

80

100

120

140

160

180

200

220

240

Dec-15 Apr-16 Aug-16 Dec-16 Apr-17 Aug-17 Dec-17

Volume 1M-MA 5Y-MA

Note: Repo transaction vol umes executed through CCPs in seven sover eign EURrepo markets (AT, BE, DE, FI, FR, IT and NL), EUR bn.Sources: RepoFunds Rate, ESMA.

0

5

10

15

20

25

Dec-15 Apr-16 Aug-16 Dec-16 Apr-17 Aug-17 Dec-17Median 75th perc 90th perc

Note: Medi an, 75th and 90th percentile of weekly speci alness , measured as thedifference between gener al collateral and special collateral repo rates ongovernment bonds in selected countries.

Sources: RepoFunds Rate, ESMA.

0

50

100

150

200

250

Dec-15 Apr-16 Aug-16 Dec-16 Apr-17 Aug-17 Dec-17

AAA AA A BBBNote: EA non-financial corporate bond spreads by rating between iBoxx non-financi al corporate yiel ds and ICAP Euro Euribor sw ap rates for maturities from 5to 7 years, in bps.

Sources: Thomson Reuters Datastream, ESMA.

0.0

0.1

0.2

0.3

0.4

0.5

0.6

0.0

0.1

0.2

0.3

0.4

0.5

0.6

Dec-15 Apr-16 Aug-16 Dec-16 Apr-17 Aug-17 Dec-17

Bid-Ask 1Y-MA Amihud (rhs)

Note: EUR Markit iBoxx corporate bond index bid- ask spr ead, in %, computed asa one-month movi ng average of the iBoxx components in the currentcomposition. 1Y-MA=one-year moving average of the bi d-ask spread. Amihud

liquidity coefficient index between 0 and 1. Higher value indicates less liquidity.Sources: IHS Markit, ESMA.

0

25

50

75

100

4Q12 4Q13 4Q14 4Q15 4Q16 4Q17

AAA AA A BBB BB and lowerNote: Outstandi ng am ount of corporate bonds in the EU as of issuance date byrating category, in % of the total.Sources: Thomson Reuters EIKON, ESMA.

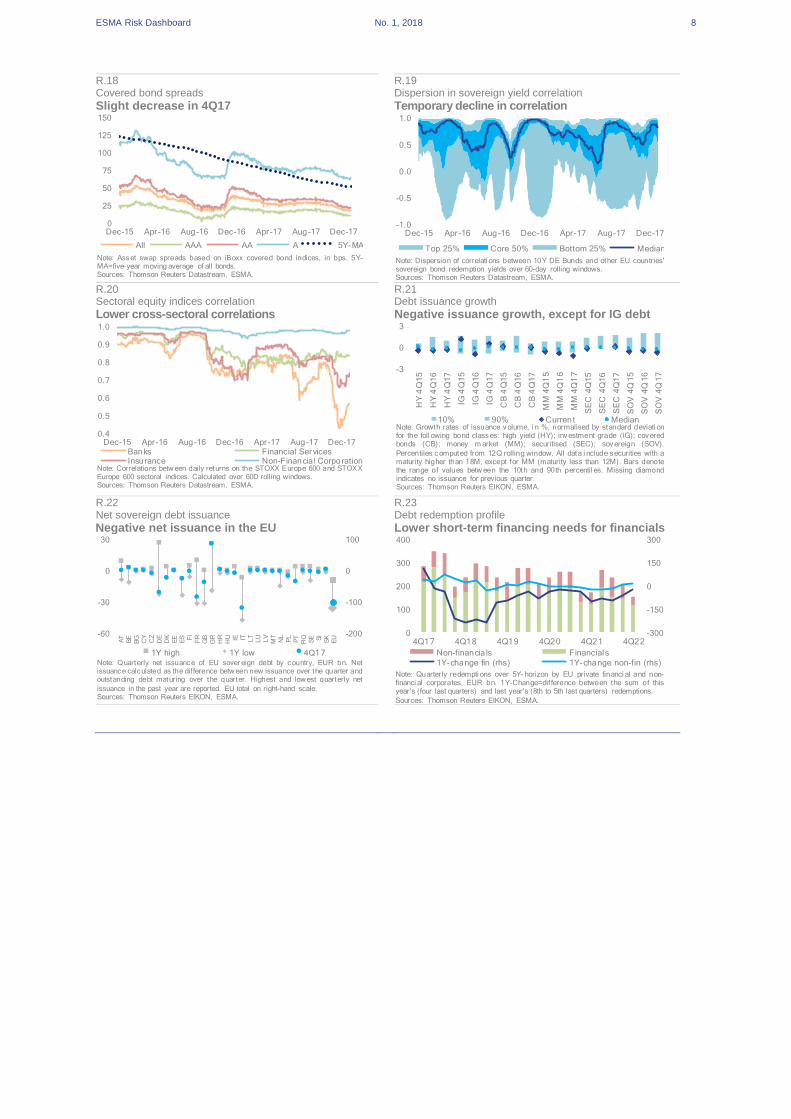

ESMA Risk Dashboard No. 1, 2018 8

R.18 R.19 Covered bond spreads

Dispersion in sovereign yield correlation

Slight decrease in 4Q17 Temporary decline in correlation

R.20 R.21 Sectoral equity indices correlation Debt issuance growth

Lower cross-sectoral correlations Negative issuance growth, except for IG debt

R.22 R.23 Net sovereign debt issuance Debt redemption profile

Negative net issuance in the EU Lower short-term financing needs for financials

0

25

50

75

100

125

150

Dec-15 Apr-16 Aug-16 Dec-16 Apr-17 Aug-17 Dec-17

All AAA AA A 5Y-MA

Note: Asset swap spreads based on iBoxx covered bond indices, in bps. 5Y-MA=five-year moving average of all bonds.Sources: Thomson Reuters Datastream, ESMA.

-1.0

-0.5

0.0

0.5

1.0

Dec-15 Apr-16 Aug-16 Dec-16 Apr-17 Aug-17 Dec-17

Top 25% Core 50% Bottom 25% Median

Note: Dispersion of correlati ons between 10Y DE Bunds and other EU countries'sovereign bond redemption yields over 60-day rolling windows.Sources: Thomson Reuters Datastream, ESMA.

0.4

0.5

0.6

0.7

0.8

0.9

1.0

Dec-15 Apr-16 Aug-16 Dec-16 Apr-17 Aug-17 Dec-17Banks Financial ServicesInsurance Non-Financia l Corporation

Note: Correlations betw een daily returns on the STOXX Europe 600 and STOXXEurope 600 sectoral indices. Calculated over 60D rolling windows.Sources: Thomson Reuters Datastream, ESMA.

-3

0

3

HY

4Q

15

HY

4Q

16

HY

4Q

17

IG 4

Q1

5

IG 4

Q1

6

IG 4

Q1

7

CB

4Q

15

CB

4Q

16

CB

4Q

17

MM

4Q

15

MM

4Q

16

MM

4Q

17

SE

C 4

Q1

5

SE

C 4

Q1

6

SE

C 4

Q1

7

SO

V 4

Q1

5

SO

V 4

Q1

6

SO

V 4

Q1

7

10% 90% Current MedianNote: Growth rates of issuance volume, i n %, normalised by standard deviati onfor the foll owing bond classes: high yield (HY); investment grade (IG); coveredbonds (CB); money m arket (MM); securitised (SEC); sovereign (SOV).

Percentiles computed from 12Q rolling window. All data i nclude securities with amaturity higher than 18M, except for MM (maturity less than 12M). Bars denotethe range of values betw een the 10th and 90th percentil es. Missing diamondindicates no issuance for previous quarter.Sources: Thomson Reuters EIKON, ESMA.

-200

-100

0

100

-60

-30

0

30

AT

BE

BG

CY

CZ

DE

DK

EE

ES FI

FR

GB

GR

HR

HU IE IT LT

LU

LV

MT

NL

PL

PT

RO

SE SI

SK

EU

1Y high 1Y low 4Q17Note: Quarterly net issuance of EU sover eign debt by country, EUR bn. Netissuance calculated as the dif ference betw een new issuance over the quarter andoutstanding debt maturing over the quarter. Highest and low est quarterly net

issuance in the past year are reported. EU total on right-hand scale.Sources: Thomson Reuters EIKON, ESMA.

-300

-150

0

150

300

0

100

200

300

400

4Q17 4Q18 4Q19 4Q20 4Q21 4Q22

Non-financia ls Financials

1Y-change fin (rhs) 1Y-change non-fin (rhs)

Note: Quarterly redempti ons over 5Y- horizon by EU private financi al and non-financi al corporates, EUR bn. 1Y-Change=dif ference between the sum of thisyear's (four last quarters) and last year's (8th to 5th last quarters) redemptions.

Sources: Thomson Reuters EIKON, ESMA.

ESMA Risk Dashboard No. 1, 2018 9

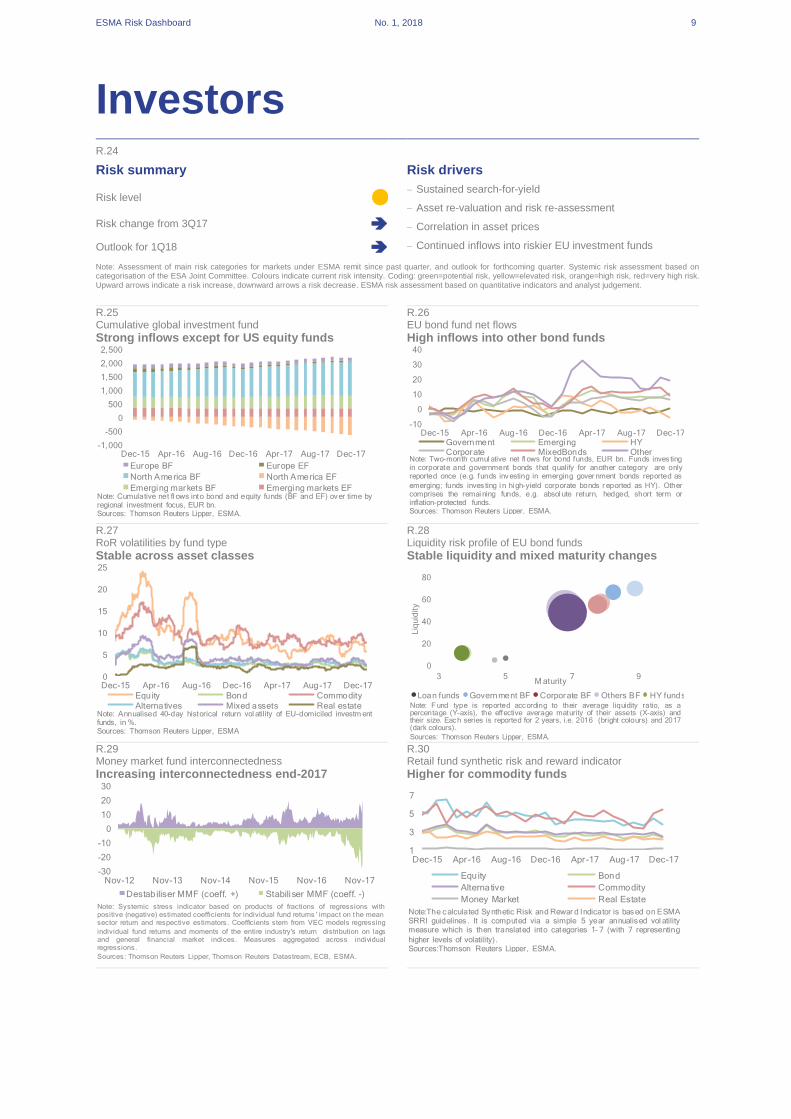

Investors R.24

Risk summary Risk drivers

Risk level – Sustained search-for-yield

– Asset re-valuation and risk re-assessment

– Correlation in asset prices

– Continued inflows into riskier EU investment funds

Risk change from 3Q17

Outlook for 1Q18

Note: Assessment of main risk categories for markets under ESMA remit since past quarter, and outlook for forthcoming quarter. Systemic risk assessment based on categorisation of the ESA Joint Committee. Colours indicate current risk intensity. Coding: green=potential risk, yellow=elevated risk, orange=high risk, red=very high risk. Upward arrows indicate a risk increase, downward arrows a risk decrease. ESMA risk assessment based on quantitative indicators and analyst judgement.

R.25 R.26 Cumulative global investment fund EU bond fund net flows

Strong inflows except for US equity funds High inflows into other bond funds

R.27 R.28 RoR volatilities by fund type Liquidity risk profile of EU bond funds

Stable across asset classes Stable liquidity and mixed maturity changes

R.29 R.30 Money market fund interconnectedness Retail fund synthetic risk and reward indicator

Increasing interconnectedness end-2017 Higher for commodity funds

-1,000

-500

0

500

1,000

1,500

2,000

2,500

Dec-15 Apr-16 Aug-16 Dec-16 Apr-17 Aug-17 Dec-17

Europe BF Europe EF

North America BF North America EF

Emerging markets BF Emerging markets EFNote: Cumulative net fl ows into bond and equity funds (BF and EF) over time byregional investment focus, EUR bn.Sources: Thomson Reuters Lipper, ESMA.

-10

0

10

20

30

40

Dec-15 Apr-16 Aug-16 Dec-16 Apr-17 Aug-17 Dec-17Government Emerging HYCorporate MixedBonds Other

Note: Two-month cumul ative net fl ows for bond funds, EUR bn. Funds inves tingin corporate and government bonds that qualify for another category are onlyreported once (e.g. funds investing in emerging gover nment bonds reported as

emerging; funds inves ting i n hi gh-yield corporate bonds r eported as HY). Othercomprises the remai ning funds, e.g. absol ute return, hedged, short term orinflation-protected funds.Sources: Thomson Reuters Lipper, ESMA.

0

5

10

15

20

25

Dec-15 Apr-16 Aug-16 Dec-16 Apr-17 Aug-17 Dec-17

Equity Bond Commodity

Alternatives Mixed assets Real estateNote: Annualised 40-day historical return vol atility of EU-domiciled investm entfunds, in %.Sources: Thomson Reuters Lipper, ESMA

0

20

40

60

80

3 5 7 9

Liq

uid

ity

M aturity

Loan funds Government BF Corporate BF Others BF HY fundsNote: F und type is reported according to their average liquidity ratio, as apercentage (Y-axis), the effective average maturity of their assets (X-axis) andtheir size. Each series is reported for 2 years, i.e. 2016 (bright colours) and 2017(dark colours).

Sources: Thomson Reuters Lipper, ESMA.

-30

-20

-10

0

10

20

30

Nov-12 Nov-13 Nov-14 Nov-15 Nov-16 Nov-17

Destabiliser MMF (coeff. +) Stabiliser MMF (coeff. -)

Note: Systemic stress indicator based on products of fractions of regressions withpositive (negative) estimated coefficients for individual fund returns ' impact on t he meansector return and respective estimators. Coefficients stem from VEC models regressing

individual fund returns and moments of the entire industry's return distribution on lagsand general financial market indices. Measures aggregated across individualregressions.

Sources: Thomson Reuters Lipper, Thomson Reuters Datastream, ECB, ESMA.

1

3

5

7

Dec-15 Apr-16 Aug-16 Dec-16 Apr-17 Aug-17 Dec-17

Equity Bond

Alternative Commodity

Money Market Real Estate

Note:The calculated Synthetic Risk and Rewar d Indicator is based on ESMASRRI guidelines . It is computed via a simple 5 year annualised vol atilitymeasure which is then translated into categories 1- 7 (with 7 representing

higher levels of volatility).Sources:Thomson Reuters Lipper, ESMA.

ESMA Risk Dashboard No. 1, 2018 10

R.31 R.32 Financial market interconnectedness Hedge fund interconnectedness

Increasing for MMFs and HFs Interconnectedness increased in 4Q17

60

65

70

75

80

0

5

10

15

20

3Q12 3Q13 3Q14 3Q15 3Q16 3Q17

Tota l funds Hedge funds

Bond funds MMFs ( rhs)Note: Loan and debt securities vis-à-vis MFI counterparts, as a share of totalassets. EA investment funds and MMFs, in %. Total funds includes: bond funds,equity funds, mixed funds, real estate funds, hedge funds, MMFs and other non-

MMFs investment funds.Sources: ECB, ESMA.

-0.02

-0.01

0.00

0.01

0.02

Nov-12 Nov-13 Nov-14 Nov-15 Nov-16 Nov-17

Destabiliser HF (coeff. +) Stabiliser HF (coeff. -)

Note: Systemic stress i ndicator based on products of frac tions of regressions withpositive (negative) estimated coefficients for individual fund returns' impact onaverage return of sector significant at 99% level and respective aver age es timators.

Coefficients stem from VAR models regressing individual fund r eturns on lags andgeneral financi al market i ndices . Measures aggr egated across individualregressions.Sources: Barclayhedge, Eurekahedge, TASS, HFR, ESMA.

ESMA Risk Dashboard No. 1, 2018 11

Infrastructures and services R.33

Risk summary Risk drivers

Risk level – Operational risks, incl. cyber risks

– Conduct risk, incl. intentional or accidental behaviour by

individuals, market abuse

– Systemic relevance, interconnectedness between

infrastructures or financial activities, system substitutability

Risk change from 3Q17

Outlook for 1Q18

Note: Assessment of main risk categories for markets under ESMA remit since past quarter, and outlook for forthcoming quarter. Systemic risk assessment based on categorisation of the ESA Joint Committee. Colours indicate current risk intensity. Coding: green=potential risk, yellow=elevated risk, orange=high risk, red=very high risk. Upward arrows indicate a risk increase, downward arrows a risk decrease. ESMA risk assessment based on quantitative indicators and analyst judgement.

R.34 R.35 Trading suspensions – lifecycle and removals On-going trading suspensions by rationale Low number of removals Increased number of on-going suspensions in 4Q17

R.36 R.37 Complaints indicator by rationale Complaints indicator by instrument Execution of orders is main cause for complaint Complaints mostly related to equity and bond instruments

R.38 R.39 Circuit breaker trigger events by sector Circuit breaker occurrences by market capitalisation Lower share for financials Limited number of occurrences

0

10

20

30

40

50

60

0

50

100

150

200

250

300

4Q15 2Q16 4Q16 2Q17 4Q17

Suspensions begun Suspensions ended

Removals Average duration (rhs)Note: N umber of dead suspensions, split by the quarter during which they startedand ended, and removals of fi nanci al ins truments traded in EEA trading venues.Average durati on of dead suspensi ons, in days , computed as the mean of the

difference between the end-of-quarter date and the issuance date.Sources: ESMA Registers.

0.00.51.01.52.02.5

0

50

100

150

200

4Q15 2Q16 4Q16 2Q17 4Q17

Market management arrangementsIssuer's failure to disclose periodic in formation on timeUndisclosed price-sensitive informationOther non-compliance with rules of the regulated marketOther disorderly trading conditionsUnknownAverage duration (rhs)

Note: Number of suspensions of financial ins truments traded on EEA tradingvenues ongoing at the end of the reporting period, grouped by quarter duringwhich they started and by rationale. Average durati on, in years, computed as the

mean of the difference between the end-of-quarter date and the start date.Sources: ESMA Registers.

0

1,000

2,000

3,000

4,000

0

20

40

60

80

100

3Q14 1Q15 3Q15 1Q16 3Q16 1Q17 3Q17Other causes Execution of ordersInvestment advice Portfolio managementQuality/lack of information Fees/chargesGeneral admin Unauthorised businessTotal volume reported (rhs)

Note: Com plaints reported directly to 18 NCAs (AT , BG, C Y, CZ, DE, DK, EE,ES, FI, HR, HU, IT , LT , LU, MT, PT, RO, SI), in % of total vol ume by cause. Theline shows the total volume of complaints reported (rhs).

Sources: ESMA complaints database.

0

1,000

2,000

3,000

4,000

0

20

40

60

80

100

3Q14 1Q15 3Q15 1Q16 3Q16 1Q17 3Q17Other invest ment produ cts/funds Financial contract s for diffe rence

Options, futu res, sw aps Mutual funds/UCITS

Money market securities Structured se curities

Bonds /debt secu rities Share s/stock/e quity

To tal volume rep orted (rhs)

Note: Com plaints r eported directly to 18 NCAs (AT, BG, CY, CZ, D E, DK, EE, ES,FI, HR, HU, IT, LT, LU, MT, PT, RO, SI), in % of total vol ume by type of financi alinstrument. The line shows the total number of complaints reported (rhs).

Source: ESMA complaints database

0

25

50

75

100

Mar-16 Jun-16 Sep-16 Dec-16 Mar-17 Jun-17 Sep-17 Dec-17Basic Materia ls, Industrials and EnergyTechnology, Utilities and Telecommunications ServicesHealthcare, Consumer Cyclicals and Non-CyclicalsFinancials

Note: Percentage of circuit breaker trigger events by economic sector. Resultsdisplayed as w eekly aggregates.The analysis is based on a sample of 10,000securities, incl uding all constituents of the STOXX Europe 200 Large/Mid/Sm all

caps and a large sample of ETFs tracking the STOXX index or sub-index.Sources: Morningstar Real-Time Data, ESMA.

0

400

800

1,200

1,600

Mar-16 Jun-16 Sep-16 Dec-16 Mar-17 Jun-17 Sep-17 Dec-17

Large caps Mid caps Small caps ETFs

Note: N umber of daily circuit breaker trigger events by type of fi nancial instrum entand by market cap. R esults displayed as weekly aggregates.The analysis isbased on a sample of 10,000 securities, incl uding all cons tituents of the ST OXX

Europe 200 Large/Mid/Small caps and a large sample of ETFs tracking theSTOXX index or sub-index.Sources: Morningstar Real-Time Data, ESMA.

ESMA Risk Dashboard No. 1, 2018 12

R.40 R.41 Trading system capacity proxy Equity market concentration

Volumes increased to 25% of capacity Greater concentration

R.42 R.43 Settlement fails IRS CCP clearing

Increase in corporate bond fails OIS and swap central clearing rates higher

R.44 R.45 Difference between the Euribor and the maximum contribution Euribor – Dispersion of submission levels

Spike at the end of 4Q17 Low and stable overall dispersion

R.46 R.47 Rating changes Financial services data breaches

Positive for structured finance instruments Mostly related to identity thefts

0

20

40

60

80

100

0

20

40

60

80

100

Mar-16 Jul-16 Nov-16 Mar-17 Jul-17 Nov-17

Trading volume 3M-MA Volume

Capacity (rhs) All- time high (rhs)Note:Daily and three-month moving average trading vol ume registered on 36 EUtrading venues, EUR bn. C apacity computed as the average across tradingvenues of the ratio of daily tr ading volume over maximum volume observed since

31/03/2016, in % (right axis).Sources: Morningstar Realtime, ESMA.

0

20

40

60

80

Dec-15 Apr-16 Aug-16 Dec-16 Apr-17 Aug-17 Dec-17

Top 25% Core 50% Bottom 25% MedianNote: Concentrati on of notional value of equity trading by national i ndicescomputed as a 1M-MA of the Herfindahl-Hirschman Index, in %. Indices i ncludedare FTSE100, CAC 40, DAX, FTSE MIB, IBEX35, AEX, OMXS30, BEL20,

OMXC20, OMXH25, PSI20, ATX.Sources: BATS, ESMA.

0

2

4

6

8

10

Nov-15 Mar-16 Jul-16 Nov-16 Mar-17 Jul-17 Nov-17

Corporate bonds 6M-MA corpEquities 6M-MA equitiesGovernment bonds 6M-MA gov

Note: Share of fail ed settlement instruc tions in the EU, in % of value, one-weekmoving averages. 6M-MA=six-month moving average. Free-of-paym enttransactions not considered.

Sources: National Competent Authorities, ESMA.

60

70

80

90

100

Dec-15 Apr-16 Aug-16 Dec-16 Apr-17 Aug-17 Dec-17

Swap Basis Swap OIS FRA

Note: OTC interest rate derivatives cleared by CCPs captured by Dealer vs. CCPpositions, in % of total noti onal amount. Spikes due to short-term movements innon-cleared positions.

Sources: DTCC, ESMA.

0.0

0.1

0.2

0.3

Dec-15 Apr-16 Aug-16 Dec-16 Apr-17 Aug-17 Dec-17

Note: N ormalised differ ence in percentage points between the highestcontribution submitted by panel banks and the correspondi ng Euribor rate. T hechart shows the maximum difference across the 8 Euribor tenors.

Sources: European Money Markets Institute, ESMA.

-0.5

-0.4

-0.3

-0.2

-0.1

0.0

0.1

Dec-15 Apr-16 Aug-16 Dec-16 Apr-17 Aug-17 Dec-17Top 15% Core 70%Bottom 15% Raw 3M Euribor3M Euribor ECB refinancing rate

Note: Dispersion of 3M Euribor submissions, i n %. T he "Raw 3M Euribor" rate iscalculated without trimming the top and bottom submissions of the panel for the3M Euribor.

Sources: European Money Markets Institute, ESMA.

-4

-2

0

2

4

6

8

Dec-15 Apr-16 Aug-16 Dec-16 Apr-17 Aug-17 Dec-17Non-f inancial Covered bondFinancial InsuranceSovereign Structured finance

Note: Net change in ratings from all credit r ating agenci es, excl uding CERVEDand ICAP, by asset class computed as a percentage number of upgrades minuspercentage number of downgrades over number of outstanding ratings.

Sources: RADAR, ESMA.

0

5

10

15

20

0

50

100

150

200

1H13 2H13 1H14 2H14 1H15 2H15 1H16 2H16 1H17

Identity theft Financial accessExistentia l data Account accessNuisance % of tota l (rhs)

Note: Estimated number of data breaches, financial services only, worldwide, bytype. Breaches in financial services sector as % of total data breaches across allsectors (secondary axis). Both series as reported by the Gemalto Breach Level

Index. The underlying data were gathered by Gemalto from publicly availabl e reportsof information breaches.Sources: Gemalto Breach Level Index, ESMA.

ESMA Risk Dashboard No. 4, 2017 13