Embed Size (px)

DESCRIPTION

Philadelphia housing market show strong increase in the second quarter of 2013.

Citation preview

Econsult Solutions, Inc. | 1435 Walnut Street, Ste. 300 | Philadelphia, PA 19102

215-717-2777 | econsultsolutions.com

ECONSULT SOLUTIONS, INC.

PHILADELPHIA HOUSING

INDEX (PHI) - 2013 Q2

TABLE OF CONTENTS

Quarterly Index

Sales by Price per Square Foot

Sales Volume by Price Range Statistics by District

Quarterly Index by Subregion

Major Markets Comparison Background and Notes

...................................... 1

............. 2

............... 3

.................................. 4

............... 5

................ 6-7 .......................... 8

Low High

Price per Square Foot

Econsult Solutions, Inc. | 1435 Walnut Street, Ste. 300 | Philadelphia, PA 19102

215-717-2777 | econsultsolutions.com

ECONSULT SOLUTIONS, INC.

PHILADELPHIA HOUSING

INDEX - 2013 Q2

QUARTERLY INDEX

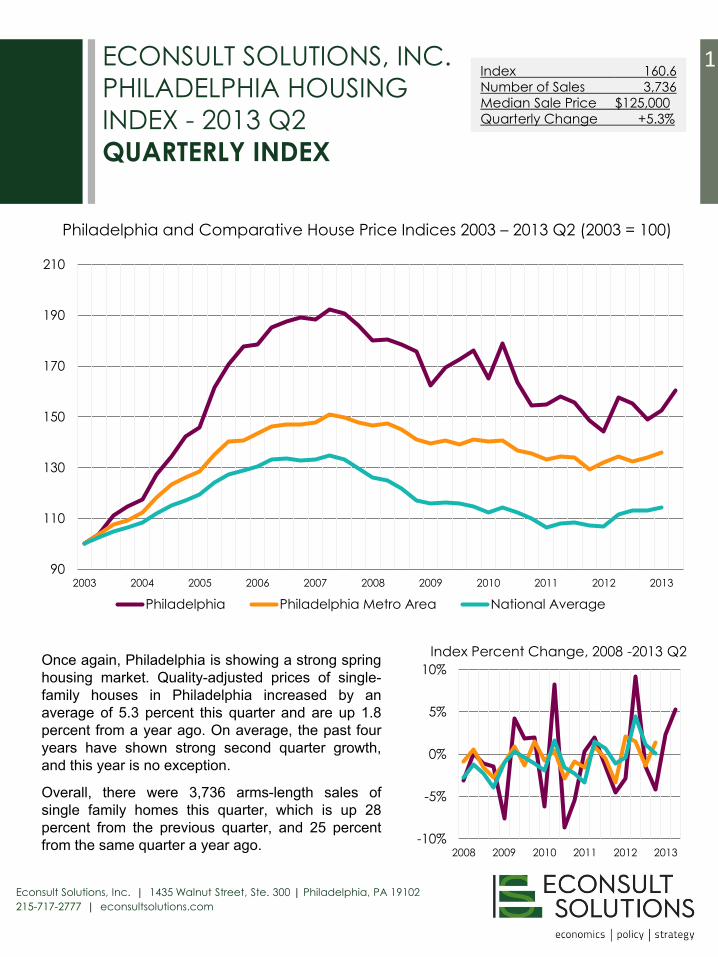

Once again, Philadelphia is showing a strong spring

housing market. Quality-adjusted prices of single-

family houses in Philadelphia increased by an

average of 5.3 percent this quarter and are up 1.8

percent from a year ago. On average, the past four

years have shown strong second quarter growth,

and this year is no exception.

Overall, there were 3,736 arms-length sales of

single family homes this quarter, which is up 28

percent from the previous quarter, and 25 percent

from the same quarter a year ago.

Philadelphia and Comparative House Price Indices 2003 – 2013 Q2 (2003 = 100)

1

Index Percent Change, 2008 -2013 Q2

Index 160.6

Number of Sales 3,736

Median Sale Price $125,000

Quarterly Change +5.3%

90

110

130

150

170

190

210

2003 2004 2005 2006 2007 2008 2009 2010 2011 2012 2013

Philadelphia Philadelphia Metro Area National Average

-10%

-5%

0%

5%

10%

2008 2009 2010 2011 2012 2013

Econsult Solutions, Inc. | 1435 Walnut Street, Ste. 300 | Philadelphia, PA 19102

215-717-2777 | econsultsolutions.com

More than $200

$150 to $200

$101 to $150

$51 to $100

$26 to $50

$25 or Less

477

426

830

1029

438

514

ECONSULT SOLUTIONS, INC.

PHILADELPHIA HOUSING

INDEX - 2013 Q2

SALES BY PRICE PER

SQUARE FOOT

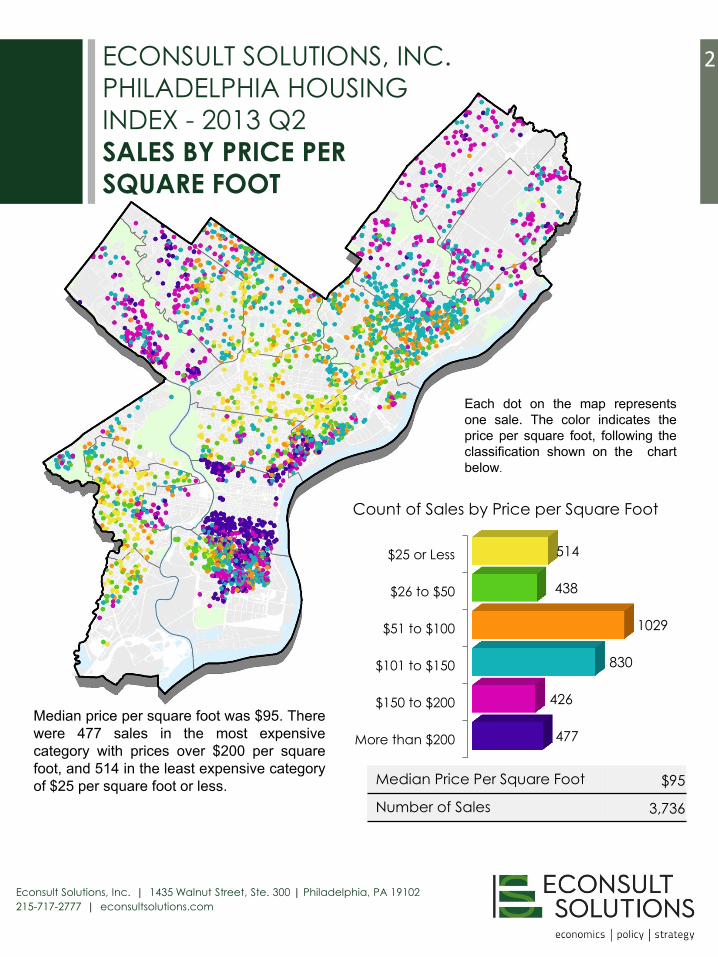

Median price per square foot was $95. There

were 477 sales in the most expensive

category with prices over $200 per square

foot, and 514 in the least expensive category

of $25 per square foot or less.

Each dot on the map represents

one sale. The color indicates the

price per square foot, following the

classification shown on the chart

below.

2

Median Price Per Square Foot $95

Number of Sales 3,736

Count of Sales by Price per Square Foot

Econsult Solutions, Inc. | 1435 Walnut Street, Ste. 300 | Philadelphia, PA 19102

215-717-2777 | econsultsolutions.com

ECONSULT SOLUTIONS, INC.

PHILADELPHIA HOUSING

INDEX - 2013 Q2

SALES VOLUME BY PRICE RANGE

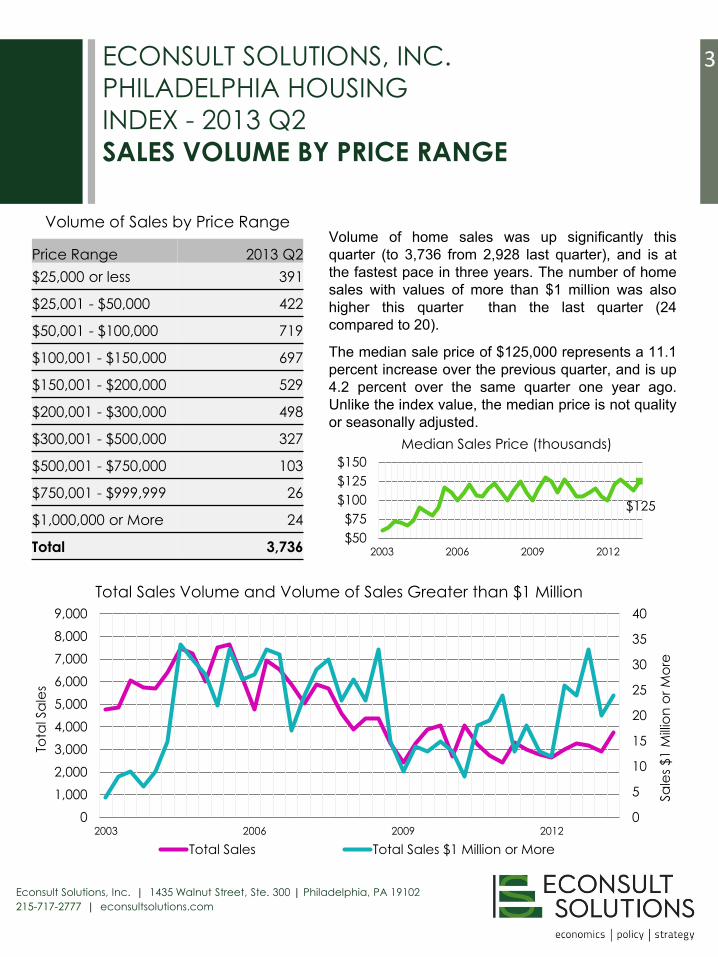

Volume of home sales was up significantly this

quarter (to 3,736 from 2,928 last quarter), and is at

the fastest pace in three years. The number of home

sales with values of more than $1 million was also

higher this quarter than the last quarter (24

compared to 20).

The median sale price of $125,000 represents a 11.1

percent increase over the previous quarter, and is up

4.2 percent over the same quarter one year ago.

Unlike the index value, the median price is not quality

or seasonally adjusted.

Price Range 2013 Q2

$25,000 or less 391

$25,001 - $50,000 422

$50,001 - $100,000 719

$100,001 - $150,000 697

$150,001 - $200,000 529

$200,001 - $300,000 498

$300,001 - $500,000 327

$500,001 - $750,000 103

$750,001 - $999,999 26

$1,000,000 or More 24

Total 3,736

Total Sales Volume and Volume of Sales Greater than $1 Million

Volume of Sales by Price Range

3

Median Sales Price (thousands)

$125

$50

$75

$100

$125

$150

2003 2006 2009 2012

0

5

10

15

20

25

30

35

40

0

1,000

2,000

3,000

4,000

5,000

6,000

7,000

8,000

9,000

2003 2006 2009 2012

Sa

les

$1

Mill

ion

or

Mo

re

Tota

l Sa

les

Total Sales Total Sales $1 Million or More

Econsult Solutions, Inc. | 1435 Walnut Street, Ste. 300 | Philadelphia, PA 19102

215-717-2777 | econsultsolutions.com

ECONSULT SOLUTIONS, INC.

PHILADELPHIA HOUSING

INDEX - 2013 Q2

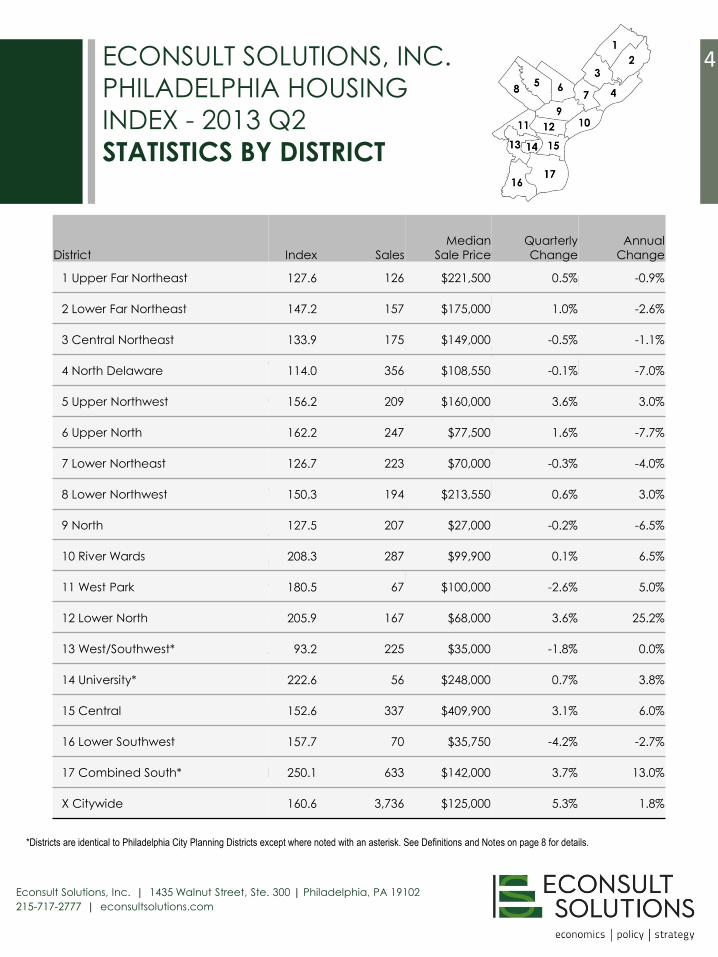

STATISTICS BY DISTRICT

*Districts are identical to Philadelphia City Planning Districts except where noted with an asterisk. See Definitions and Notes on page 8 for details.

4

District Index Sales

Median

Sale Price

Quarterly

Change

Annual

Change

1 Upper Far Northeast 127.6 126 $221,500 0.5% -0.9%

2 Lower Far Northeast 147.2 157 $175,000 1.0% -2.6%

3 Central Northeast 133.9 175 $149,000 -0.5% -1.1%

4 North Delaware 114.0 356 $108,550 -0.1% -7.0%

5 Upper Northwest 156.2 209 $160,000 3.6% 3.0%

6 Upper North 162.2 247 $77,500 1.6% -7.7%

7 Lower Northeast 126.7 223 $70,000 -0.3% -4.0%

8 Lower Northwest 150.3 194 $213,550 0.6% 3.0%

9 North 127.5 207 $27,000 -0.2% -6.5%

10 River Wards 208.3 287 $99,900 0.1% 6.5%

11 West Park 180.5 67 $100,000 -2.6% 5.0%

12 Lower North 205.9 167 $68,000 3.6% 25.2%

13 West/Southwest* 93.2 225 $35,000 -1.8% 0.0%

14 University* 222.6 56 $248,000 0.7% 3.8%

15 Central 152.6 337 $409,900 3.1% 6.0%

16 Lower Southwest 157.7 70 $35,750 -4.2% -2.7%

17 Combined South* 250.1 633 $142,000 3.7% 13.0%

X Citywide 160.6 3,736 $125,000 5.3% 1.8%

Econsult Solutions, Inc. | 1435 Walnut Street, Ste. 300 | Philadelphia, PA 19102

215-717-2777 | econsultsolutions.com

ECONSULT SOLUTIONS, INC.

PHILADELPHIA HOUSING

INDEX - 2013 Q2

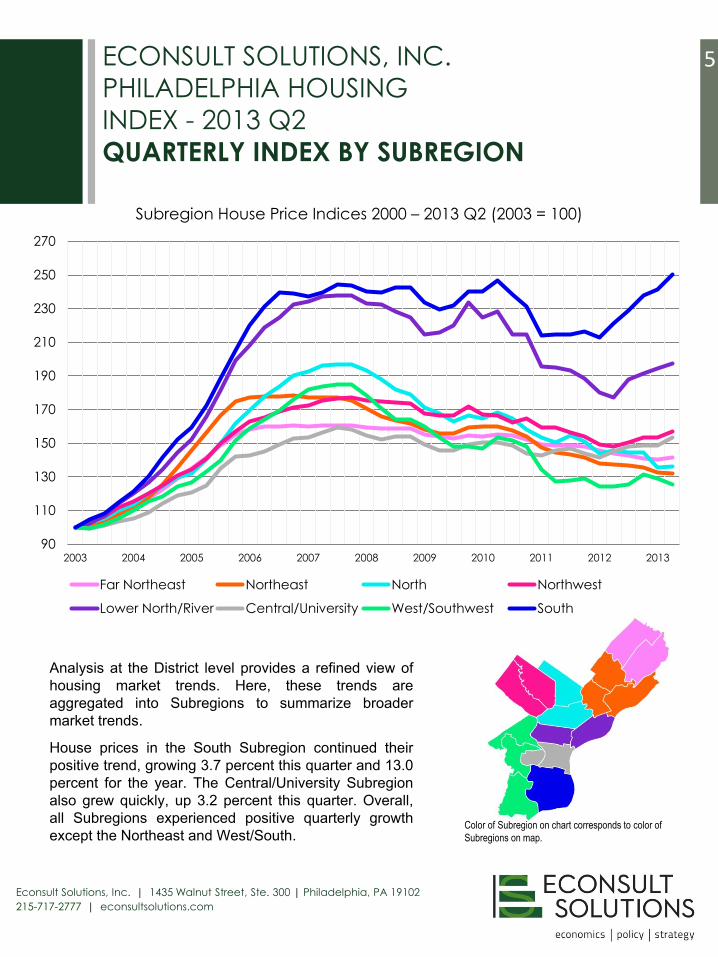

QUARTERLY INDEX BY SUBREGION

Analysis at the District level provides a refined view of

housing market trends. Here, these trends are

aggregated into Subregions to summarize broader

market trends.

House prices in the South Subregion continued their

positive trend, growing 3.7 percent this quarter and 13.0

percent for the year. The Central/University Subregion

also grew quickly, up 3.2 percent this quarter. Overall,

all Subregions experienced positive quarterly growth

except the Northeast and West/South.

Subregion House Price Indices 2000 – 2013 Q2 (2003 = 100)

5

Color of Subregion on chart corresponds to color of

Subregions on map.

90

110

130

150

170

190

210

230

250

270

2003 2004 2005 2006 2007 2008 2009 2010 2011 2012 2013

Far Northeast Northeast North Northwest

Lower North/River Central/University West/Southwest South

Econsult Solutions, Inc. | 1435 Walnut Street, Ste. 300 | Philadelphia, PA 19102

215-717-2777 | econsultsolutions.com

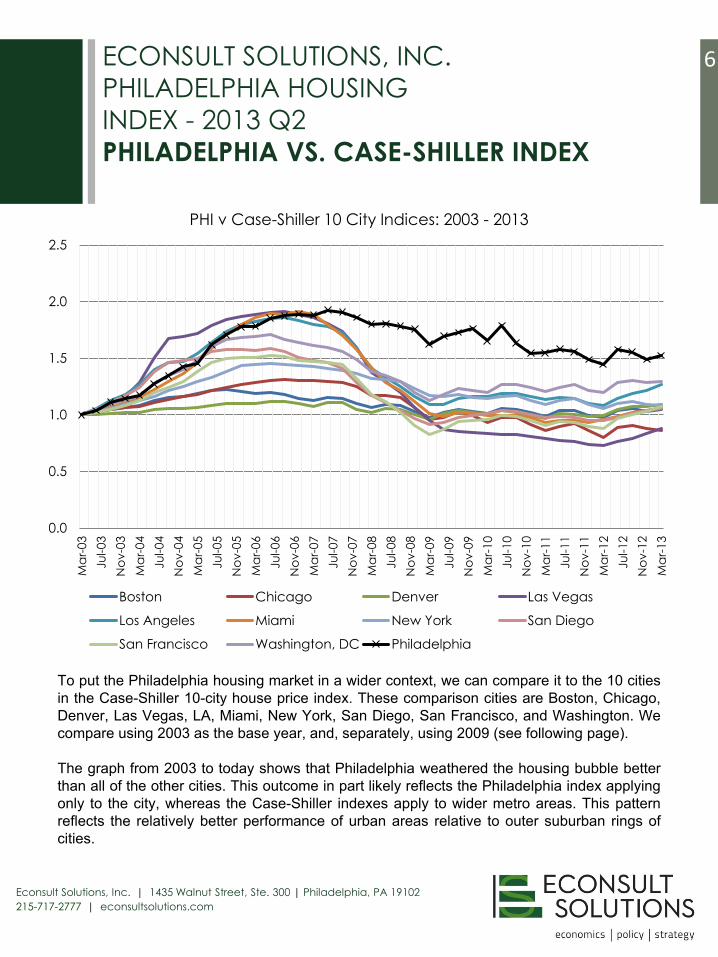

To put the Philadelphia housing market in a wider context, we can compare it to the 10 cities

in the Case-Shiller 10-city house price index. These comparison cities are Boston, Chicago,

Denver, Las Vegas, LA, Miami, New York, San Diego, San Francisco, and Washington. We

compare using 2003 as the base year, and, separately, using 2009 (see following page).

The graph from 2003 to today shows that Philadelphia weathered the housing bubble better

than all of the other cities. This outcome in part likely reflects the Philadelphia index applying

only to the city, whereas the Case-Shiller indexes apply to wider metro areas. This pattern

reflects the relatively better performance of urban areas relative to outer suburban rings of

cities.

ECONSULT SOLUTIONS, INC.

PHILADELPHIA HOUSING

INDEX - 2013 Q2

PHILADELPHIA VS. CASE-SHILLER INDEX

6

0.0

0.5

1.0

1.5

2.0

2.5

Ma

r-03

Ju

l-03

No

v-0

3

Ma

r-04

Ju

l-04

No

v-0

4

Ma

r-05

Ju

l-05

No

v-0

5

Ma

r-06

Ju

l-06

No

v-0

6

Ma

r-07

Ju

l-07

No

v-0

7

Ma

r-08

Ju

l-08

No

v-0

8

Ma

r-09

Ju

l-09

No

v-0

9

Ma

r-10

Ju

l-10

No

v-1

0

Ma

r-11

Ju

l-11

No

v-1

1

Ma

r-12

Ju

l-12

No

v-1

2

Ma

r-13

PHI v Case-Shiller 10 City Indices: 2003 - 2013

Boston Chicago Denver Las Vegas

Los Angeles Miami New York San Diego

San Francisco Washington, DC Philadelphia

Econsult Solutions, Inc. | 1435 Walnut Street, Ste. 300 | Philadelphia, PA 19102

215-717-2777 | econsultsolutions.com

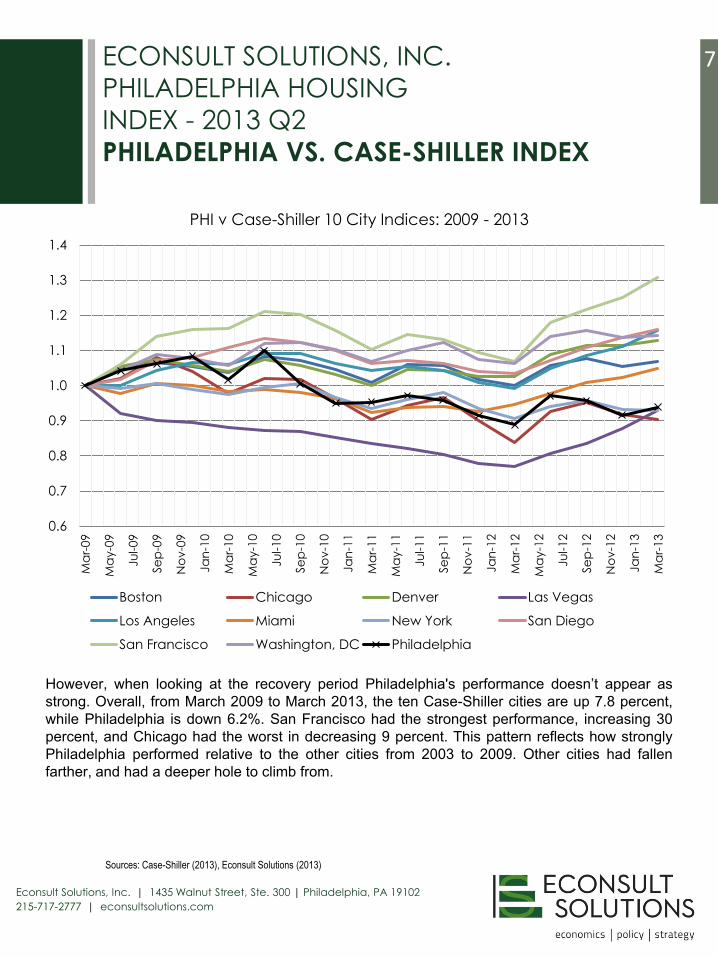

However, when looking at the recovery period Philadelphia's performance doesn’t appear as

strong. Overall, from March 2009 to March 2013, the ten Case-Shiller cities are up 7.8 percent,

while Philadelphia is down 6.2%. San Francisco had the strongest performance, increasing 30

percent, and Chicago had the worst in decreasing 9 percent. This pattern reflects how strongly

Philadelphia performed relative to the other cities from 2003 to 2009. Other cities had fallen

farther, and had a deeper hole to climb from.

ECONSULT SOLUTIONS, INC.

PHILADELPHIA HOUSING

INDEX - 2013 Q2

PHILADELPHIA VS. CASE-SHILLER INDEX

7

Sources: Case-Shiller (2013), Econsult Solutions (2013)

0.6

0.7

0.8

0.9

1.0

1.1

1.2

1.3

1.4

Ma

r-09

Ma

y-0

9

Ju

l-09

Se

p-0

9

No

v-0

9

Ja

n-1

0

Ma

r-10

Ma

y-1

0

Ju

l-10

Se

p-1

0

No

v-1

0

Ja

n-1

1

Ma

r-11

Ma

y-1

1

Ju

l-11

Se

p-1

1

No

v-1

1

Ja

n-1

2

Ma

r-12

Ma

y-1

2

Ju

l-12

Se

p-1

2

No

v-1

2

Ja

n-1

3

Ma

r-13

PHI v Case-Shiller 10 City Indices: 2009 - 2013

Boston Chicago Denver Las Vegas

Los Angeles Miami New York San Diego

San Francisco Washington, DC Philadelphia

Econsult Solutions, Inc. | 1435 Walnut Street, Ste. 300 | Philadelphia, PA 19102

215-717-2777 | econsultsolutions.com

ECONSULT SOLUTIONS, INC.

PHILADELPHIA HOUSING

INDEX - 2013 Q2

BACKGROUND AND NOTES

8

Background and Contact

Econsult Solutions, Inc. (ESI) provides the Philadelphia Housing Index (PHI) free of charge to the public. Thanks to Azavea

and the Office of Property Assessment for providing some of the data used in our analysis.

Sales are arms-length transactions of single-family homes only. The price indexes are estimated by Econsult Solutions,

Inc. using a quality controlled measure of average sale appreciation using hedonic regression analysis.

Questions and press inquiries should be directed to Econsult Solutions, Inc. President Richard P. Voith at

Notes

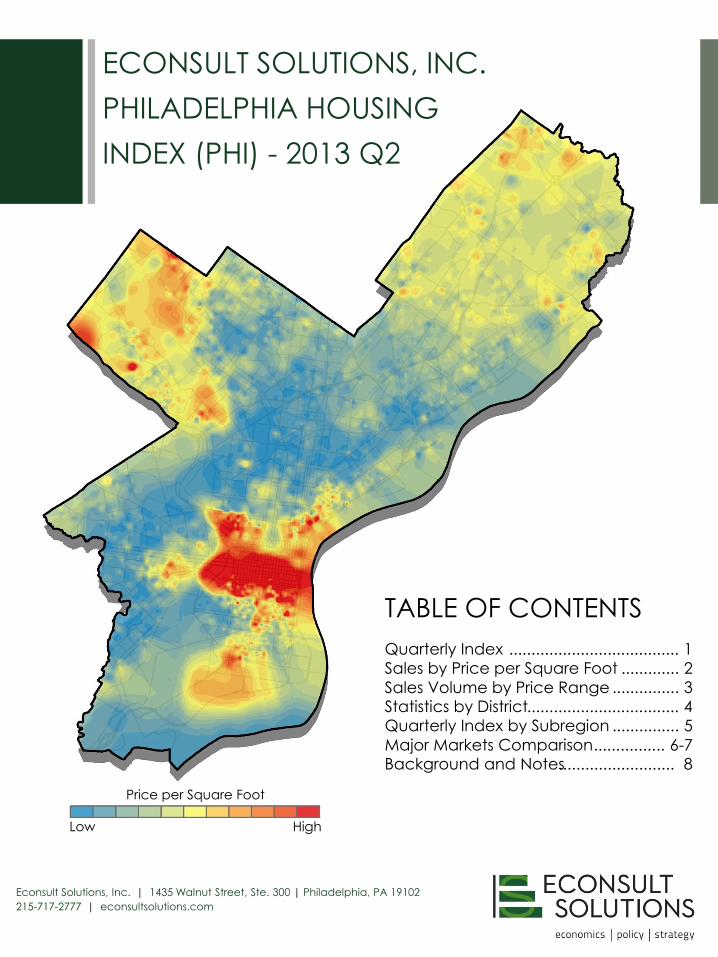

Cover: Map displays interpolated (inverse-distance weighted) cost surface based on price per square foot of sales. Lower

values of price per square foot are deep blue; higher values are red; yellow and green shades are in the middle. The image

is provided for illustrative purposes only and does not represent predictions of home values.

Page 1: National and Philadelphia Metro Indexes are from the Seasonally Adjusted Purchase Only Series from the Federal

Housing Finance Agency. Philadelphia Metro refers to the Pennsylvania Division of the Metropolitan Statistical Area,

which includes the Philadelphia, Bucks, Chester, Delaware, and Montgomery counties.

Page 4: Econsult Solutions, Inc. Districts are identical to those used by the Philadelphia City Planning Commission (PCPC)

except: PCPC’s “Lower South” is included in “South”; University City is carved out from PCPC’s “University/SouthWest”,

and the remaining Southwest is combined with West to form “West/Southwest”.

Pages 4 and 5: District and Subregion indexes are smoothed to reduce volatility and capture underlying market trends. The

smoothing means that overall district and subregion prices tend to reflect overall citywide price changes with a slight lag.

Page 5: For ease of presentation, Districts are further aggregated into “Subregions,” as shown on the map.

Page 6 & 7: 10 City Indices courtesy of Case-Shiller

![Highlights of ESI[truck] North America ESI[truck] North](https://img.pdfslide.us/doc/110x75/628b4a9ff91dad22754155f1/highlights-of-esitruck-north-america-esitruck-north-.jpg)