Embed Size (px)

Citation preview

Credit Research

Sector Thinking - Green Bonds/ESG

6 July 2020

UniCredit Research page 1 See last pages for disclaimer.

ESG analysis and green bonds in the telecoms sector

■ With the influx of investment from ESG investors, ESG analysis in the telecom industry is becoming more significant. Governance and social risks have had the greatest impact on credit analysis, with governance considerations in particular tipping the balance in favor of certain rating decisions. Social risks have so far focused mostly on relations between management and labor, although data security is likely to become more significant with the transition to 5G technology. Since some prominent rating services view environmental exposure as quite uniform within the telecom industry, we think ESG investors that rely on these rankings may be overly emphasizing traditional labor and corporate governance concerns over the significant environmental initiatives that are underway in the telecom industry.

■ Green bonds are the most important way that investors can gain exposure to telecom companies that have made environmental initiatives a priority. Green-bond issuers must commit to specific environmental targets for the use of the proceeds. Compliance with these targets is regularly monitored to ensure that the funds are being used according to their intended purposes. Telefonica (marketweight) and Verizon (overweight) opened the telco green-bond market in February 2019. Telefonica also placed the industry’s first hybrid bond in February 2020. Vodafone (overweight), Telia (underweight) and Swisscom (marketweight) have also issued green bonds since then.

■ Two of the most important investment fields for telecom companies in the coming years – fiber and 5G – have positive environmental implications. Fiber is 85% more energy efficient and less material-intensive than copper technology. Based on preliminary testing, Swisscom estimates that 5G technology is 50-70% less energy intensive than 4G technology, which already represented a major improvement over 2G and 3G. 5G also has the potential to unlock major gains in green technologies throughout society with applications such as smart metering, smart cities and electrical vehicle charging. However, one question that is often raised by green-bond investors is whether these investments represent new green initiatives or are simply “business-as-usual” investments by the telcos. Given the positive environmental implications of fiber and 5G technology, this line is admittedly blurry but companies need to demonstrate that the proceeds from green-bond issuance will support more environmentally friendly investments than they would make with non-green-bond issuance. However, since telcos’ most pressing investment needs appear to be well aligned with sustainable technologies, we think the conditions for further green-bond issuance in the sector look quite supportive.

■ Green-bond issuance should also be boosted by the attractive pricing issuers have achieved. Additional demand from a growing ESG investor base appears to support pricing relative to non-green bonds. This – as well as the positive image in society companies gain for supporting green investment – justifies the additional scrutiny issuers face by operating a green-bond program. Recent green telco bond issuance and the experience in secondary trading indicates that investor demand for green bonds appears to be strengthening.

Contents ESG risk and the telecoms industry 2ESG rating methodologies 6Telco green bonds 10Green-bond performance and relative value 13 Recommendations on green-bond issuers Swisscom (Marketweight) Telefonica (Marketweight) Telia (Underweight) Verizon (Overweight) Vodafone (Overweight)

RELATIVE PERFORMANCE OF GREEN BONDS

Source: Bloomberg, iBoxx, UniCredit Research

SHARE OF IBOXX GREEN BONDS BY SECTOR

Source: Bloomberg, iBoxx, UniCredit Research

Author Jonathan Schroer, CFA, Senior Credit Analyst Telecoms, Media/Cable (UniCredit Bank, Munich) +49 89 378-13212 [email protected]

Bloomberg: UCCR Internet: www.unicreditresearch.eu

40

60

80

100

120

140

160

180

200

Jul-19 Oct-19 Jan-20 Apr-20 Jul-20

bp

iBoxx € Non-Financials Green Bonds

iBoxx € Non-Financials Non Green Bonds

UTI88.3%

IGS3.5%

TEL5.5%

ATO1.2% CNS

1.5%

6 July 2020 Credit Research

Sector Thinking - Green Bonds/ESG

UniCredit Research page 2 See last pages for disclaimer.

ESG risk and the telecoms industry

Companies are paying more attention to ESG concerns as investor demand for sociallyresponsible investments continues to grow. Evaluation methodologies are still beingdeveloped and industry benchmarking often lacks transparency. With the telecommunicationsindustry, ESG has been less topical than for industrial companies since the telcos tend tohave similar investment profiles and strategies and because telecommunications does notface many of the hazards that more industrial segments do. In an industry assessment, S&Prates the telecoms industry as having below-average environmental exposure. Nevertheless,ESG topics are already relevant for telecommunications companies and can impact corporateratings. We expect ESG concerns to increase in the coming years as the companies roll out5G services, which entail new ESG risks and opportunities.

S&P’S RANKING OF ENVIRONMENTAL EXPOSURE BY INDUSTRY

Source: Standard & Poor’s

Social and governance risks have dominated ESG analysis so far

Social risks are often linked to governance risks. The current focus on relationsbetween labor and management should increasingly incorporate data-security issueswith the advent of 5G networks. Social-risk analysis has tended to focus on management’sability or willingness to implement major restructuring programs. Especially if a restructuringprogram attracts negative attention from the broader society as being especially harsh, thenthis can damage a company’s brand and image in a society and can ultimately impactoperating growth. For example, Moody’s has mentioned the negative environment created byOrange’s cost cutting as a source of concern in recent years.

6 July 2020 Credit Research

Sector Thinking - Green Bonds/ESG

UniCredit Research page 3 See last pages for disclaimer.

On the other hand, companies that successfully implement diversity policies or that haveprogressive labor policies tend to be viewed positively in this category.

Data security is a rising social risk with the advent of 5G

Data security and privacy is also an area of social risk that we expect to rise inimportance. Telecoms operators that are increasingly involved in cloud or other industrialapplications are taking on additional security risks with this business. As 5G networks becomeoperational, data leaks and security risks are becoming more of a concern due to the industrialapplications these networks will support. Any network outages or security breaches could beincreasingly damaging for companies’ reputations and, consequently, for their operations. Sofar, there have been few such outages or security breaches that have been significant enough toimpact companies’ operations, but this is set to be a rising concern as telecoms companiesstrive to add more cloud products and mission-critical services in the 5G world.

Environmental risk has been more in the background, but is rising in importance

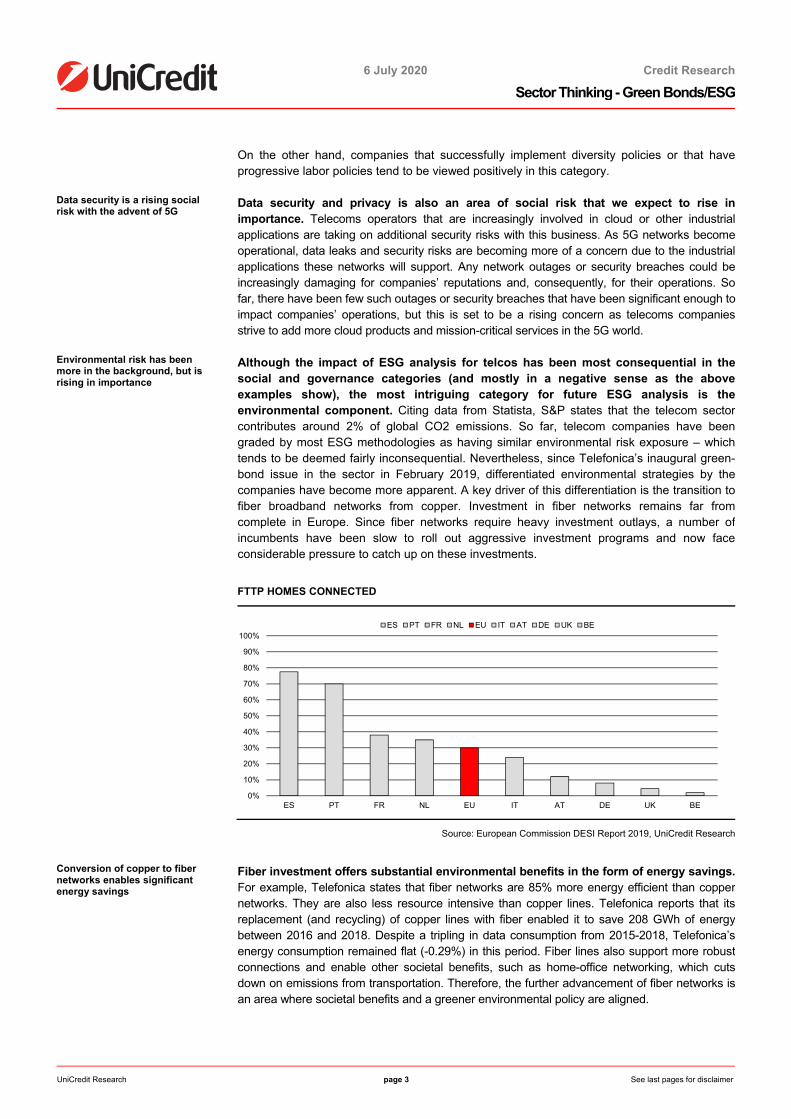

Although the impact of ESG analysis for telcos has been most consequential in thesocial and governance categories (and mostly in a negative sense as the aboveexamples show), the most intriguing category for future ESG analysis is theenvironmental component. Citing data from Statista, S&P states that the telecom sectorcontributes around 2% of global CO2 emissions. So far, telecom companies have beengraded by most ESG methodologies as having similar environmental risk exposure – whichtends to be deemed fairly inconsequential. Nevertheless, since Telefonica’s inaugural green-bond issue in the sector in February 2019, differentiated environmental strategies by thecompanies have become more apparent. A key driver of this differentiation is the transition tofiber broadband networks from copper. Investment in fiber networks remains far fromcomplete in Europe. Since fiber networks require heavy investment outlays, a number ofincumbents have been slow to roll out aggressive investment programs and now faceconsiderable pressure to catch up on these investments.

FTTP HOMES CONNECTED

Source: European Commission DESI Report 2019, UniCredit Research

Conversion of copper to fiber networks enables significant energy savings

Fiber investment offers substantial environmental benefits in the form of energy savings.For example, Telefonica states that fiber networks are 85% more energy efficient than coppernetworks. They are also less resource intensive than copper lines. Telefonica reports that itsreplacement (and recycling) of copper lines with fiber enabled it to save 208 GWh of energybetween 2016 and 2018. Despite a tripling in data consumption from 2015-2018, Telefonica’senergy consumption remained flat (-0.29%) in this period. Fiber lines also support more robustconnections and enable other societal benefits, such as home-office networking, which cutsdown on emissions from transportation. Therefore, the further advancement of fiber networks isan area where societal benefits and a greener environmental policy are aligned.

0%

10%

20%

30%

40%

50%

60%

70%

80%

90%

100%

ES PT FR NL EU IT AT DE UK BE

ES PT FR NL EU IT AT DE UK BE

6 July 2020 Credit Research

Sector Thinking - Green Bonds/ESG

UniCredit Research page 4 See last pages for disclaimer.

5G continues a trend of improving energy savings despite higher data demand

In the coming years, 5G networks open new possibilities for investment in greenertechnologies. Technological advancements have reduced the energy intensity of mobile datatransmission, which has helped to offset the rapid increase in mobile data consumption inrecent years. 5G will help to accelerate this trend since it is less energy intensive. Forexample, Swisscom says that it only takes 0.2 watts to transfer one megabyte of data over 5Gnetworks. This compares to 5,400 watts with 2G. Swisscom’s research forecasts that it canachieve energy savings of between 50% and 70% by replacing 4G technology with 5G.Therefore, it appears that 5G technology can improve the energy efficiency of the telecomsindustry. This would continue the trend from recent years where technological improvements– including the migration from 2G to 4G – has helped to stabilize the industry’s energyconsumption despite the rapid increase in data consumption.

VODAFONE’S IMPROVED ENERGY EFFICIENCY IS OFFSETTING SURGING DATA USAGE

Energy efficiency gains offset rising data usage… …resulting in declining GHG emissions

Source: Vodafone, UniCredit Research

5G technology offers further environmental benefits for society as a whole

In addition to the energy savings, 5G technology can support a number ofenvironmentally friendly industrial applications. Internet-of-things (IoT) applications suchas smart metering, smart logistics and electric vehicle charging can be run over a low-powernetwork that can help to ease network congestion and use energy more efficiently. Theseindustrial applications also help to save energy consumption and lower CO2 emissions. Onegoal of these applications is to decouple energy consumption and CO2 emissions from theinevitable data-traffic growth. The prospects for these energy-reducing technologies is asecond-round effect of green technology that the telecoms companies can offer through theirindustrial customers that goes beyond the first-round effect of the telecom companies’ owndirect energy usage. As a result, 5G technology is expected to be a key enabler of energy-efficient technologies in other industrial sectors.

0

100

200

300

400

500

600

700

0

1

2

3

4

5

6

7

FY18 FY19 FY20

Ton

s o

f CO

2e

GB

Monthly mobile data usage GHG Emissions per petabyte

0.29 0.26 0.28

1.78 1.761.56

0

0.5

1

1.5

2

2.5

FY18 FY19 FY20

mn

ton

s o

f CO

2e

Scope 1 Scope 2

2.07 2.011.84

6 July 2020 Credit Research

Sector Thinking - Green Bonds/ESG

UniCredit Research page 5 See last pages for disclaimer.

ENVIRONMENTAL IMPACT OF DIGITALIZATION ON CUSTOMERS

Source: Telefonica

6 July 2020 Credit Research

Sector Thinking - Green Bonds/ESG

UniCredit Research page 6 See last pages for disclaimer.

ESG rating methodologies

Various ESG methodologies produce very different rankings

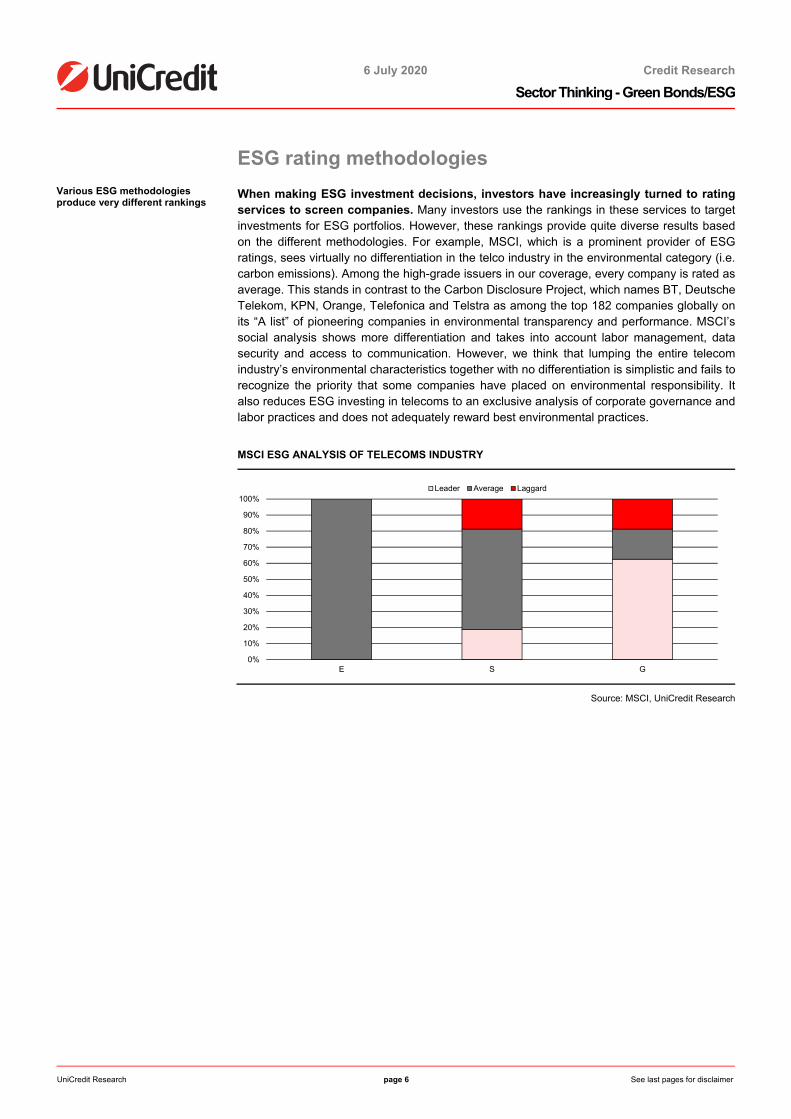

When making ESG investment decisions, investors have increasingly turned to ratingservices to screen companies. Many investors use the rankings in these services to targetinvestments for ESG portfolios. However, these rankings provide quite diverse results basedon the different methodologies. For example, MSCI, which is a prominent provider of ESGratings, sees virtually no differentiation in the telco industry in the environmental category (i.e.carbon emissions). Among the high-grade issuers in our coverage, every company is rated asaverage. This stands in contrast to the Carbon Disclosure Project, which names BT, DeutscheTelekom, KPN, Orange, Telefonica and Telstra as among the top 182 companies globally onits “A list” of pioneering companies in environmental transparency and performance. MSCI’ssocial analysis shows more differentiation and takes into account labor management, datasecurity and access to communication. However, we think that lumping the entire telecomindustry’s environmental characteristics together with no differentiation is simplistic and fails torecognize the priority that some companies have placed on environmental responsibility. Italso reduces ESG investing in telecoms to an exclusive analysis of corporate governance andlabor practices and does not adequately reward best environmental practices.

MSCI ESG ANALYSIS OF TELECOMS INDUSTRY

Source: MSCI, UniCredit Research

0%

10%

20%

30%

40%

50%

60%

70%

80%

90%

100%

E S G

Leader Average Laggard

6 July 2020 Credit Research

Sector Thinking - Green Bonds/ESG

UniCredit Research page 7 See last pages for disclaimer.

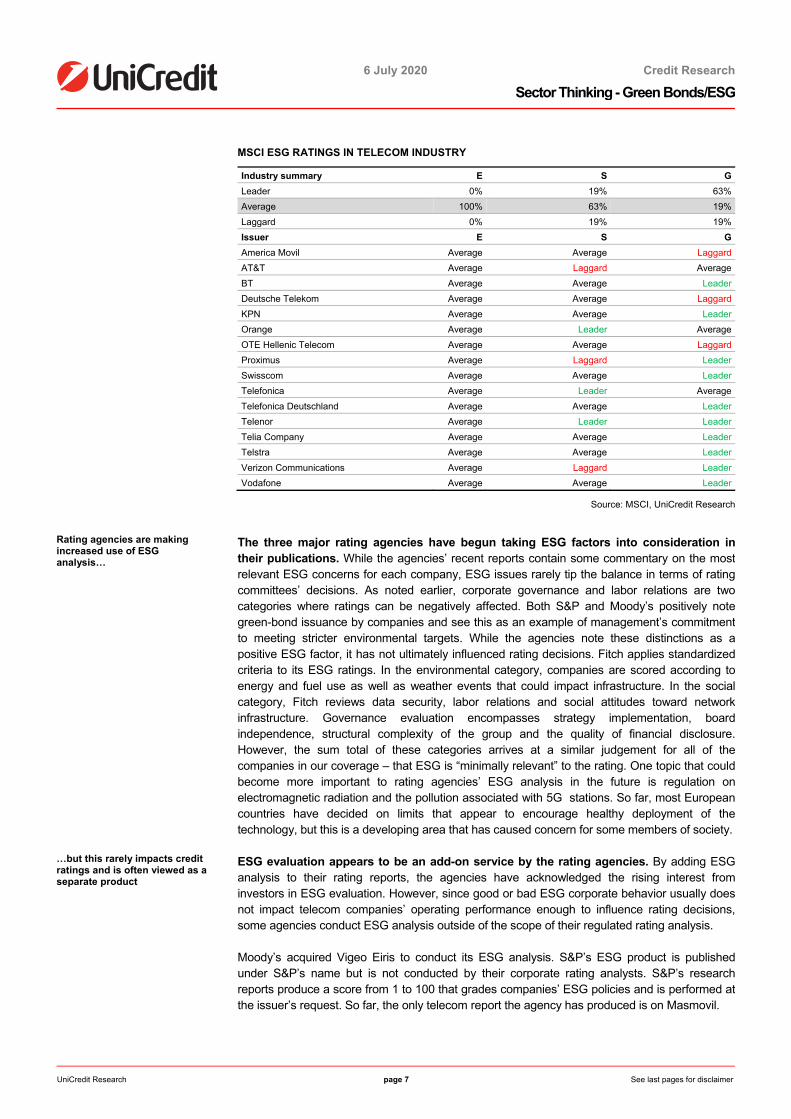

MSCI ESG RATINGS IN TELECOM INDUSTRY

Industry summary E S G

Leader 0% 19% 63%

Average 100% 63% 19%

Laggard 0% 19% 19%

Issuer E S G

America Movil Average Average Laggard

AT&T Average Laggard Average

BT Average Average Leader

Deutsche Telekom Average Average Laggard

KPN Average Average Leader

Orange Average Leader Average

OTE Hellenic Telecom Average Average Laggard

Proximus Average Laggard Leader

Swisscom Average Average Leader

Telefonica Average Leader Average

Telefonica Deutschland Average Average Leader

Telenor Average Leader Leader

Telia Company Average Average Leader

Telstra Average Average Leader

Verizon Communications Average Laggard Leader

Vodafone Average Average Leader

Source: MSCI, UniCredit Research

Rating agencies are making increased use of ESG analysis…

The three major rating agencies have begun taking ESG factors into consideration intheir publications. While the agencies’ recent reports contain some commentary on the mostrelevant ESG concerns for each company, ESG issues rarely tip the balance in terms of ratingcommittees’ decisions. As noted earlier, corporate governance and labor relations are twocategories where ratings can be negatively affected. Both S&P and Moody’s positively notegreen-bond issuance by companies and see this as an example of management’s commitmentto meeting stricter environmental targets. While the agencies note these distinctions as apositive ESG factor, it has not ultimately influenced rating decisions. Fitch applies standardizedcriteria to its ESG ratings. In the environmental category, companies are scored according toenergy and fuel use as well as weather events that could impact infrastructure. In the socialcategory, Fitch reviews data security, labor relations and social attitudes toward networkinfrastructure. Governance evaluation encompasses strategy implementation, boardindependence, structural complexity of the group and the quality of financial disclosure.However, the sum total of these categories arrives at a similar judgement for all of thecompanies in our coverage – that ESG is “minimally relevant” to the rating. One topic that couldbecome more important to rating agencies’ ESG analysis in the future is regulation onelectromagnetic radiation and the pollution associated with 5G stations. So far, most Europeancountries have decided on limits that appear to encourage healthy deployment of thetechnology, but this is a developing area that has caused concern for some members of society.

…but this rarely impacts credit ratings and is often viewed as a separate product

ESG evaluation appears to be an add-on service by the rating agencies. By adding ESGanalysis to their rating reports, the agencies have acknowledged the rising interest frominvestors in ESG evaluation. However, since good or bad ESG corporate behavior usually doesnot impact telecom companies’ operating performance enough to influence rating decisions,some agencies conduct ESG analysis outside of the scope of their regulated rating analysis.

Moody’s acquired Vigeo Eiris to conduct its ESG analysis. S&P’s ESG product is publishedunder S&P’s name but is not conducted by their corporate rating analysts. S&P’s researchreports produce a score from 1 to 100 that grades companies’ ESG policies and is performed atthe issuer’s request. So far, the only telecom report the agency has produced is on Masmovil.

6 July 2020 Credit Research

Sector Thinking - Green Bonds/ESG

UniCredit Research page 8 See last pages for disclaimer.

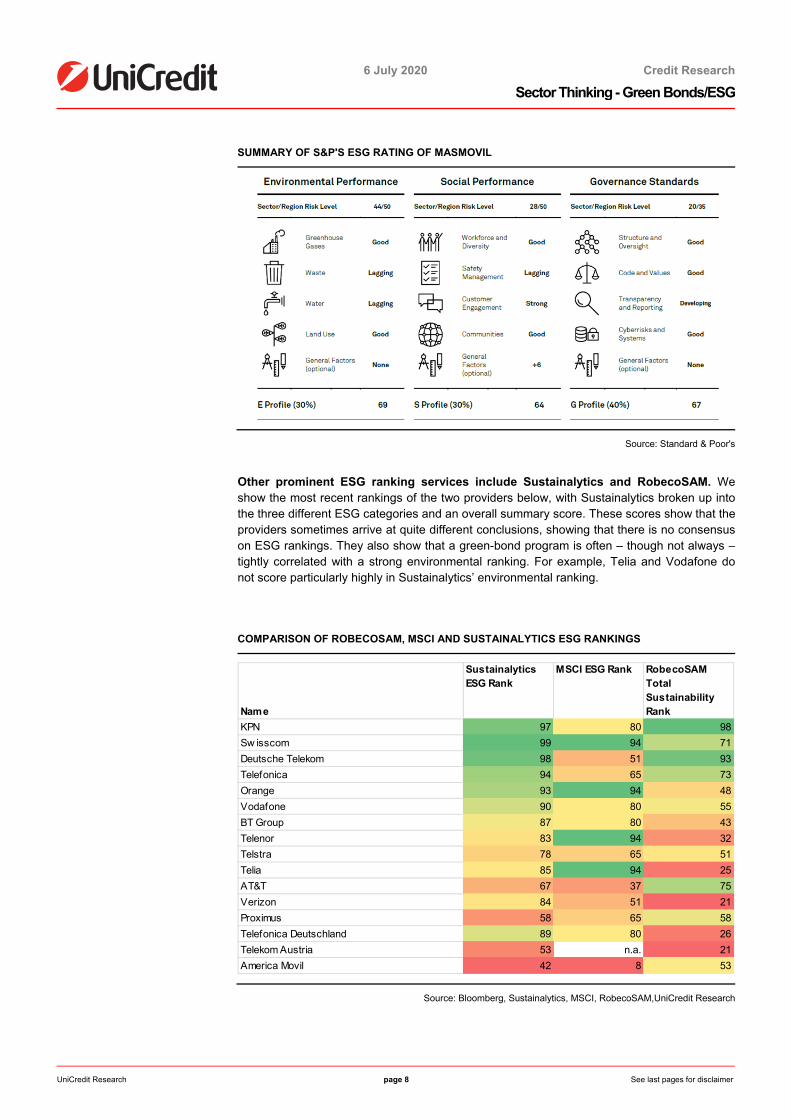

SUMMARY OF S&P'S ESG RATING OF MASMOVIL

Source: Standard & Poor's

Other prominent ESG ranking services include Sustainalytics and RobecoSAM. Weshow the most recent rankings of the two providers below, with Sustainalytics broken up intothe three different ESG categories and an overall summary score. These scores show that theproviders sometimes arrive at quite different conclusions, showing that there is no consensuson ESG rankings. They also show that a green-bond program is often – though not always –tightly correlated with a strong environmental ranking. For example, Telia and Vodafone donot score particularly highly in Sustainalytics’ environmental ranking.

COMPARISON OF ROBECOSAM, MSCI AND SUSTAINALYTICS ESG RANKINGS

Source: Bloomberg, Sustainalytics, MSCI, RobecoSAM,UniCredit Research

Name

Sustainalytics ESG Rank

MSCI ESG Rank RobecoSAM Total Sustainability Rank

KPN 97 80 98

Sw isscom 99 94 71

Deutsche Telekom 98 51 93

Telefonica 94 65 73

Orange 93 94 48

Vodafone 90 80 55

BT Group 87 80 43

Telenor 83 94 32

Telstra 78 65 51

Telia 85 94 25

AT&T 67 37 75

Verizon 84 51 21

Proximus 58 65 58

Telefonica Deutschland 89 80 26

Telekom Austria 53 n.a. 21

America Movil 42 8 53

6 July 2020 Credit Research

Sector Thinking - Green Bonds/ESG

UniCredit Research page 9 See last pages for disclaimer.

OVERVIEW OF SUSTAINALYTICS’ ESG RATINGS ON TELCOS

Source: Bloomberg, Sustainalytics, UniCredit Research

Name

Sustainalytics ESG Rank

Sustainalytics Environment Percentile

Sustainalytics Social Percentile

Sustainalytics Governance Percentile

KPN 97 99 94 97

Sw isscom 99 100 98 93

Deutsche Telekom 98 93 99 96

Telefonica 94 95 95 81

Orange 93 98 91 74

Vodafone 90 69 87 88

BT Group 87 75 84 84

Telenor 83 67 90 72

Telstra 78 74 72 76

Telia 85 77 82 86

AT&T 67 79 64 52

Verizon 84 85 79 91

Proximus 58 88 73 5

Telefonica Deutschland 89 89 74 92

Telekom Austria 53 62 41 51

America Movil 42 45 47 24

6 July 2020 Credit Research

Sector Thinking - Green Bonds/ESG

UniCredit Research page 10 See last pages for disclaimer.

Telco green bonds

Green bonds increase the importance of environmental analysis

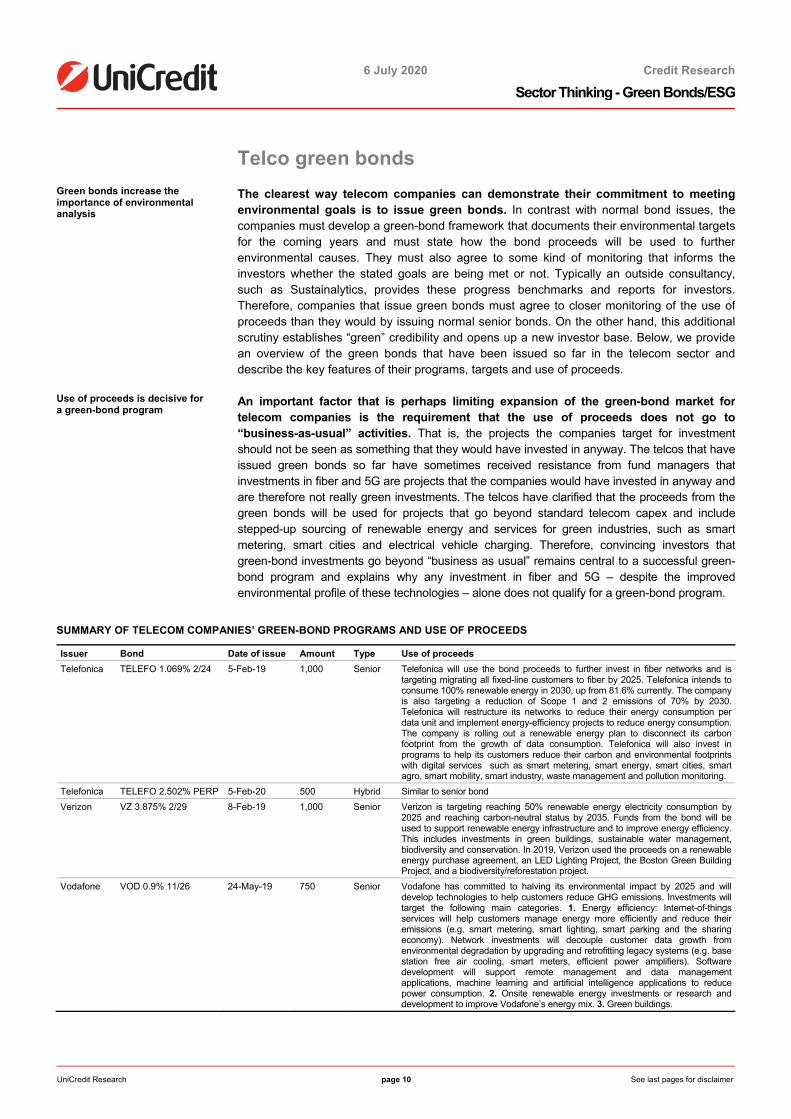

The clearest way telecom companies can demonstrate their commitment to meetingenvironmental goals is to issue green bonds. In contrast with normal bond issues, thecompanies must develop a green-bond framework that documents their environmental targetsfor the coming years and must state how the bond proceeds will be used to furtherenvironmental causes. They must also agree to some kind of monitoring that informs theinvestors whether the stated goals are being met or not. Typically an outside consultancy,such as Sustainalytics, provides these progress benchmarks and reports for investors.Therefore, companies that issue green bonds must agree to closer monitoring of the use ofproceeds than they would by issuing normal senior bonds. On the other hand, this additionalscrutiny establishes “green” credibility and opens up a new investor base. Below, we providean overview of the green bonds that have been issued so far in the telecom sector anddescribe the key features of their programs, targets and use of proceeds.

Use of proceeds is decisive for a green-bond program

An important factor that is perhaps limiting expansion of the green-bond market fortelecom companies is the requirement that the use of proceeds does not go to“business-as-usual” activities. That is, the projects the companies target for investmentshould not be seen as something that they would have invested in anyway. The telcos that haveissued green bonds so far have sometimes received resistance from fund managers thatinvestments in fiber and 5G are projects that the companies would have invested in anyway andare therefore not really green investments. The telcos have clarified that the proceeds from thegreen bonds will be used for projects that go beyond standard telecom capex and includestepped-up sourcing of renewable energy and services for green industries, such as smartmetering, smart cities and electrical vehicle charging. Therefore, convincing investors thatgreen-bond investments go beyond “business as usual” remains central to a successful green-bond program and explains why any investment in fiber and 5G – despite the improvedenvironmental profile of these technologies – alone does not qualify for a green-bond program.

SUMMARY OF TELECOM COMPANIES’ GREEN-BOND PROGRAMS AND USE OF PROCEEDS

Issuer Bond Date of issue Amount Type Use of proceeds

Telefonica TELEFO 1.069% 2/24 5-Feb-19 1,000 Senior Telefonica will use the bond proceeds to further invest in fiber networks and is targeting migrating all fixed-line customers to fiber by 2025. Telefonica intends to consume 100% renewable energy in 2030, up from 81.6% currently. The company is also targeting a reduction of Scope 1 and 2 emissions of 70% by 2030. Telefonica will restructure its networks to reduce their energy consumption per data unit and implement energy-efficiency projects to reduce energy consumption. The company is rolling out a renewable energy plan to disconnect its carbon footprint from the growth of data consumption. Telefonica will also invest in programs to help its customers reduce their carbon and environmental footprints with digital services such as smart metering, smart energy, smart cities, smart agro, smart mobility, smart industry, waste management and pollution monitoring.

Telefonica TELEFO 2.502% PERP 5-Feb-20 500 Hybrid Similar to senior bond

Verizon VZ 3.875% 2/29 8-Feb-19 1,000 Senior Verizon is targeting reaching 50% renewable energy electricity consumption by 2025 and reaching carbon-neutral status by 2035. Funds from the bond will be used to support renewable energy infrastructure and to improve energy efficiency. This includes investments in green buildings, sustainable water management, biodiversity and conservation. In 2019, Verizon used the proceeds on a renewable energy purchase agreement, an LED Lighting Project, the Boston Green Building Project, and a biodiversity/reforestation project.

Vodafone VOD 0.9% 11/26 24-May-19 750 Senior Vodafone has committed to halving its environmental impact by 2025 and will develop technologies to help customers reduce GHG emissions. Investments will target the following main categories. 1. Energy efficiency: Internet-of-things services will help customers manage energy more efficiently and reduce their emissions (e.g. smart metering, smart lighting, smart parking and the sharing economy). Network investments will decouple customer data growth from environmental degradation by upgrading and retrofitting legacy systems (e.g. base station free air cooling, smart meters, efficient power amplifiers). Software development will support remote management and data management applications, machine learning and artificial intelligence applications to reduce power consumption. 2. Onsite renewable energy investments or research and development to improve Vodafone’s energy mix. 3. Green buildings.

6 July 2020 Credit Research

Sector Thinking - Green Bonds/ESG

UniCredit Research page 11 See last pages for disclaimer.

Telia TELIAS 1.375% 5/81 11-Feb-20 500 Hybrid Telia is targeting zero CO2 emissions throughout the value chain by 2030 thanks to a combination of reducing the company’s own emissions and working with its suppliers throughout the value chain. The use of proceeds from the bond issue will include the following: 1. investments in renewable energy by the construction and maintenance of renewable energy facilities (wind or solar); 2. green digital solutions for technology that increases energy efficiency and mitigates customers’ GHG emissions (e.g. 5G and other internet-of-things solutions, data analytics and cloud products); 3. network equipment upgrades to increase energy efficiency (e.g. fiber and high-speed mobile networks to replace copper-based networks, more energy-efficient network equipment and cooling solutions); 4. green buildings through acquisition or leasing contracts.

Swisscom SCMNVX 0.375% 11/28 14-May-20 500 Senior Swisscom will use the proceeds from its green bond to fund three main development objectives: 1. Projects to reduce energy demand including FTTH expansion, phasing out TDM analog platforms and replacing them with All-IP, 5G communication. Energy demand can also be reduced by installing virtual servers to replace multiple servers in data centers and by investing in efficient network-cooling technology. 2. IoT network expansion to help clients save energy, including a low power network, smart metering, smart logistics, smart cities and electric vehicle charging. 3. Investments in the energy efficiency of new or existing buildings.

Source: company data, UniCredit Research

A fine line exists between “business as usual” and green investments

As can be seen by the investment programs summarized above, the green-bondinvestments so far tend to combine some business-as-usual elements with more novelgreen-focused technologies. For example, copper replacement by fiber is environmentallyfriendly since it leads to lower energy consumption per data unit and 5G applications forindustrial networking will also be part of all companies’ capex spending in the coming years.However, it appears that some aspects of these investments, such as enhanced sourcing ofrenewable energy and green industry applications go beyond what might be expected ofstandard industry capex. Still, these lines are blurred and remain an area where issuers needto justify their green-bond frameworks to investors. Despite some friction here in terms of the“business-as-usual” debate, we think that the doors are open to more green-bond issuance inthe telecom sector in the future as fiber and 5G investments support development that canlead to greener technologies throughout societies.

Green bonds require specific KPIs and third-party monitoring

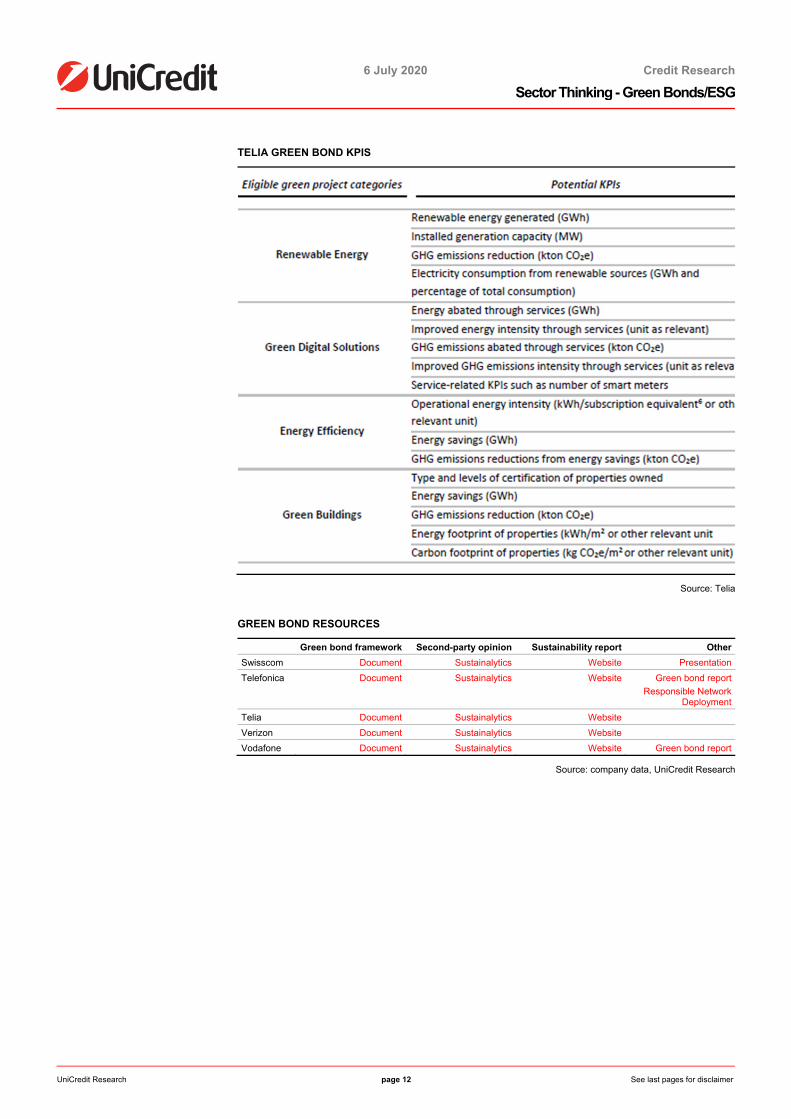

Green-bond issuers are subject to occasional investment reviews of the use ofproceeds. These reviews are conducted by third-party specialists, such as Sustainalytics.The projects need to clearly state the targets and the KPIs that will be monitored. Thisassures the green investor base that the proceeds are not being used to fund “business-as-usual” projects and that they are having a positive environmental impact. Below is an exampleof Telia’s KPIs for the projects it intends to fund with its green-bond program.

6 July 2020 Credit Research

Sector Thinking - Green Bonds/ESG

UniCredit Research page 12 See last pages for disclaimer.

TELIA GREEN BOND KPIS

Source: Telia

GREEN BOND RESOURCES

Green bond framework Second-party opinion Sustainability report Other

Swisscom Document Sustainalytics Website Presentation

Telefonica Document Sustainalytics Website Green bond report

Responsible Network Deployment

Telia Document Sustainalytics Website

Verizon Document Sustainalytics Website

Vodafone Document Sustainalytics Website Green bond report

Source: company data, UniCredit Research

6 July 2020 Credit Research

Sector Thinking - Green Bonds/ESG

UniCredit Research page 13 See last pages for disclaimer.

Green-bond performance and relative value

Green bonds should remain a category of high-grade investing

So far, green bonds remain mainly a feature of investment-grade investing. In the high-grade category, they have opened up a new asset class with distinct investmentfeatures and an enlarged investor base. Within the high-yield space, we think it is unlikelythat companies will issue green bonds in the near term since high-yield investing tends tofocus on more-urgent credit drivers, such as liquidity. Given the tight spreads and more-stableperformance within the high-grade space, green-bond issues stand out from traditional bondissues. The only green high-yield telco bond that has been issued so far is the Telefonica2.502% hybrid, which, at BB+, is rated two notches below Telefonica’s corporate rating.

Green bonds appear to price tighter in the primary market

Based on the experience so far with green telecom bonds, it appears that green issuesare experiencing an improving performance over time. This is probably attributable to theadditional ESG investor base competing for these assets. According to a report by theClimate Bonds Initiative, around half of green bonds were allocated to green investors in2H19. When we look at the first TELEFO, VOD and VZ green bonds that were issued at thestart of 2019, they tended to price in line with their closest peers. However, some of the morerecent issues – such as the TELIAS and TELEFO hybrids – appear to have priced tighter thancomparable bonds. Even a slight pricing advantage should justify the additional monitoring thecompanies subject themselves to by issuing a green bond. The outperformance relative tonon-green bonds should make green-bond issuance attractive to companies and sustainfurther deal flow in the coming years.

Pricing advantages appear to be sustained in secondary trading

The experience of green-bond performance on the secondary market also showsmostly positive trends. As shown on the cover page of this report, overall green-bondperformance across sectors has been better than that of normal corporate investment-gradebonds and this has been unaffected by the COVID-19 crisis. In the telco sector, this positiverelative performance also appears to be intact, although it is not consistent or uniform andinvolves complexities when analyzed on an issue-by-issue basis.

TELEFONICA

TELEFO senior TELEFO hybrid

Source: Bloomberg, UniCredit Research

Telefonica Telefonica currently has the most advanced green-bond program in the telecomsindustry with the EUR 1,000mn senior bond and EUR 500mn hybrid bond outstanding.As depicted in the charts above, the green bonds have tended to trade tighter thancomparable senior bonds.

0

20

40

60

80

100

120

140

160

Feb-19 May-19 Aug-19 Nov-19 Feb-20 May-20

bp

TELEFO 1.069% 2/24 TELEFO 1.528% 1/25 TELEFO 3.987% 1/23

0

100

200

300

400

500

600

Jan-20 Apr-20

bp

TELEFO 2.502% PERP (Other) TELEFO 2.875% PERP (Other)

6 July 2020 Credit Research

Sector Thinking - Green Bonds/ESG

UniCredit Research page 14 See last pages for disclaimer.

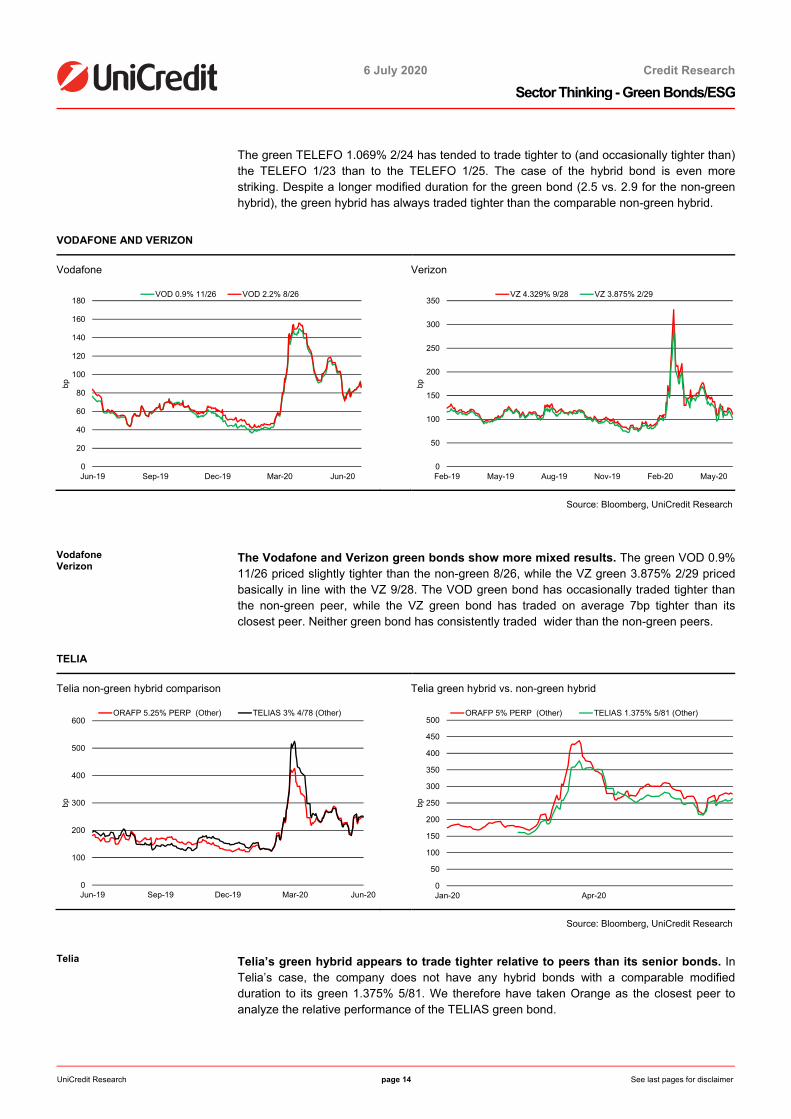

The green TELEFO 1.069% 2/24 has tended to trade tighter to (and occasionally tighter than)the TELEFO 1/23 than to the TELEFO 1/25. The case of the hybrid bond is even morestriking. Despite a longer modified duration for the green bond (2.5 vs. 2.9 for the non-greenhybrid), the green hybrid has always traded tighter than the comparable non-green hybrid.

VODAFONE AND VERIZON

Vodafone Verizon

Source: Bloomberg, UniCredit Research

Vodafone Verizon

The Vodafone and Verizon green bonds show more mixed results. The green VOD 0.9%11/26 priced slightly tighter than the non-green 8/26, while the VZ green 3.875% 2/29 pricedbasically in line with the VZ 9/28. The VOD green bond has occasionally traded tighter thanthe non-green peer, while the VZ green bond has traded on average 7bp tighter than itsclosest peer. Neither green bond has consistently traded wider than the non-green peers.

TELIA

Telia non-green hybrid comparison Telia green hybrid vs. non-green hybrid

Source: Bloomberg, UniCredit Research

Telia Telia’s green hybrid appears to trade tighter relative to peers than its senior bonds. InTelia’s case, the company does not have any hybrid bonds with a comparable modifiedduration to its green 1.375% 5/81. We therefore have taken Orange as the closest peer toanalyze the relative performance of the TELIAS green bond.

0

20

40

60

80

100

120

140

160

180

Jun-19 Sep-19 Dec-19 Mar-20 Jun-20

bp

VOD 0.9% 11/26 VOD 2.2% 8/26

0

50

100

150

200

250

300

350

Feb-19 May-19 Aug-19 Nov-19 Feb-20 May-20

bp

VZ 4.329% 9/28 VZ 3.875% 2/29

0

100

200

300

400

500

600

Jun-19 Sep-19 Dec-19 Mar-20 Jun-20

bp

ORAFP 5.25% PERP (Other) TELIAS 3% 4/78 (Other)

0

50

100

150

200

250

300

350

400

450

500

Jan-20 Apr-20

bp

ORAFP 5% PERP (Other) TELIAS 1.375% 5/81 (Other)

6 July 2020 Credit Research

Sector Thinking - Green Bonds/ESG

UniCredit Research page 15 See last pages for disclaimer.

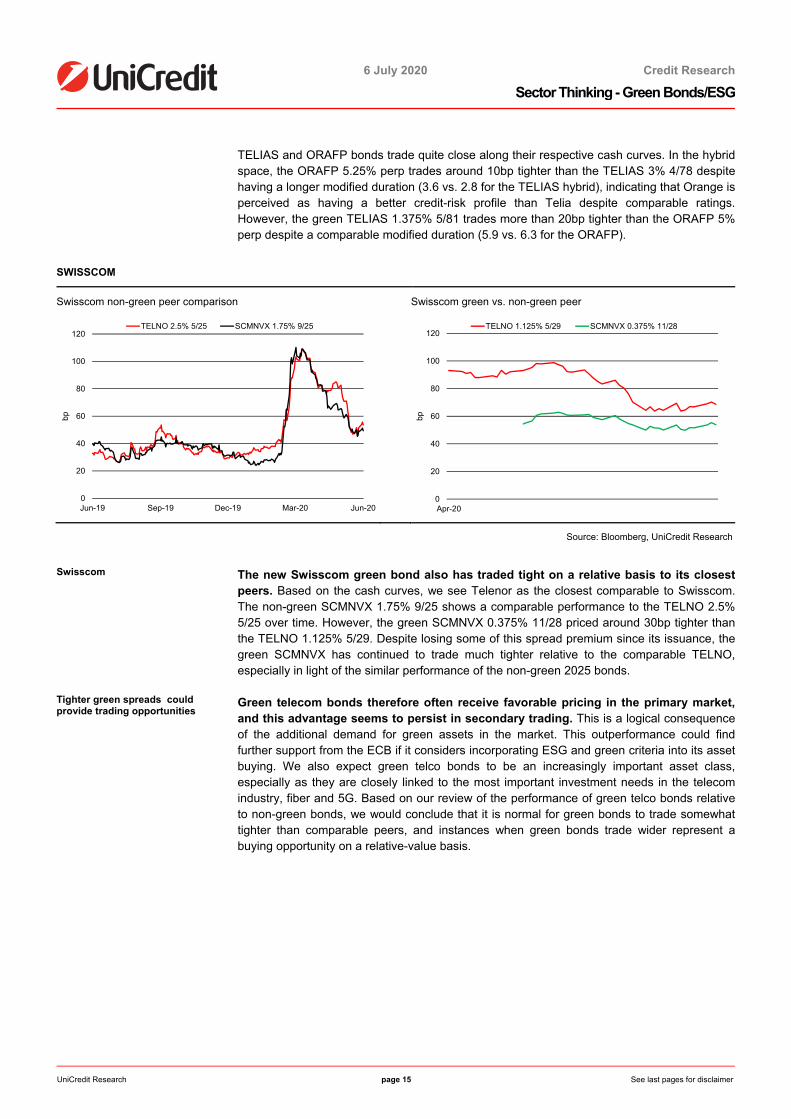

TELIAS and ORAFP bonds trade quite close along their respective cash curves. In the hybridspace, the ORAFP 5.25% perp trades around 10bp tighter than the TELIAS 3% 4/78 despitehaving a longer modified duration (3.6 vs. 2.8 for the TELIAS hybrid), indicating that Orange isperceived as having a better credit-risk profile than Telia despite comparable ratings.However, the green TELIAS 1.375% 5/81 trades more than 20bp tighter than the ORAFP 5%perp despite a comparable modified duration (5.9 vs. 6.3 for the ORAFP).

SWISSCOM

Swisscom non-green peer comparison Swisscom green vs. non-green peer

Source: Bloomberg, UniCredit Research

Swisscom The new Swisscom green bond also has traded tight on a relative basis to its closestpeers. Based on the cash curves, we see Telenor as the closest comparable to Swisscom.The non-green SCMNVX 1.75% 9/25 shows a comparable performance to the TELNO 2.5%5/25 over time. However, the green SCMNVX 0.375% 11/28 priced around 30bp tighter thanthe TELNO 1.125% 5/29. Despite losing some of this spread premium since its issuance, thegreen SCMNVX has continued to trade much tighter relative to the comparable TELNO,especially in light of the similar performance of the non-green 2025 bonds.

Tighter green spreads could provide trading opportunities

Green telecom bonds therefore often receive favorable pricing in the primary market,and this advantage seems to persist in secondary trading. This is a logical consequenceof the additional demand for green assets in the market. This outperformance could findfurther support from the ECB if it considers incorporating ESG and green criteria into its assetbuying. We also expect green telco bonds to be an increasingly important asset class,especially as they are closely linked to the most important investment needs in the telecomindustry, fiber and 5G. Based on our review of the performance of green telco bonds relativeto non-green bonds, we would conclude that it is normal for green bonds to trade somewhattighter than comparable peers, and instances when green bonds trade wider represent abuying opportunity on a relative-value basis.

0

20

40

60

80

100

120

Jun-19 Sep-19 Dec-19 Mar-20 Jun-20

bp

TELNO 2.5% 5/25 SCMNVX 1.75% 9/25

0

20

40

60

80

100

120

Apr-20

bp

TELNO 1.125% 5/29 SCMNVX 0.375% 11/28

6 July 2020 Credit Research

Sector Thinking - Green Bonds/ESG

UniCredit Research page 16 .

Legal Notices

Glossary

A comprehensive glossary for many of the terms used in the report is available on our website: https://www.unicreditresearch.eu/index.php?id=glossary

Disclaimer Our recommendations are based on information obtained from or are based upon public information sources that we consider to be reliable, but for the completeness and accuracy of which we assume no liability. All information, estimates, opinions, projections and forecasts included in this report represent the independent judgment of the analysts as of the date of the issue unless stated otherwise. We reserve the right to modify the views expressed herein at any time without notice. Moreover, we reserve the right not to update this information or to discontinue it altogether without notice. This report may contain links to websites of third parties, the content of which is not controlled by UniCredit Bank. No liability is assumed for the content of these third-party websites.

This report is for information purposes only and (i) does not constitute or form part of any offer for sale or subscription of or solicitation of any offer to buy or subscribe for any financial, money market or investment instrument or any security, (ii) is neither intended as such an offer for sale or subscription of or solicitation of an offer to buy or subscribe for any financial, money market or investment instrument or any security nor (iii) as marketing material within the meaning of applicable prospectus law . The investment possibilities discussed in this report may not be suitable for certain investors depending on their specific investment objectives and time horizon or in the context of their overall financial situation. The investments discussed may fluctuate in price or value. Investors may get back less than they invested. Fluctuations in exchange rates may have an adverse effect on the value of investments. Furthermore, past performance is not necessarily indicative of future results. In particular, the risks associated with an investment in the financial, money market or investment instrument or security under discussion are not explained in their entirety.

This information is given without any warranty on an "as is" basis and should not be regarded as a substitute for obtaining individual advice. Investors must make their own determination of the appropriateness of an investment in any instruments referred to herein based on the merits and risks involved, their own investment strategy and their legal, fiscal and financial position. As this document does not qualify as an investment recommendation or as a direct investment recommendation, neither this document nor any part of it shall form the basis of, or be relied on in connection with or act as an inducement to enter into, any contract or commitment whatsoever. Investors are urged to contact their bank's investment advisor for individual explanations and advice.

Neither UniCredit Bank AG, UniCredit Bank AG London Branch, UniCredit Bank AG Milan Branch, UniCredit Bank AG Vienna Branch, UniCredit Bank Austria AG, UniCredit Bulbank, Zagrebačka banka d.d., UniCredit Bank Czech Republic and Slovakia, ZAO UniCredit Bank Russia, UniCredit Bank Czech Republic and Slovakia Slovakia Branch, UniCredit Bank Romania, UniCredit Bank AG New York Branch nor any of their respective directors, officers or employees nor any other person accepts any liability whatsoever (in negligence or otherwise) for any loss howsoever arising from any use of this document or its contents or otherwise arising in connection therewith.

This report is being distributed by electronic and ordinary mail to professional investors, who are expected to make their own investment decisions without undue reliance on this publication, and may not be redistributed, reproduced or published in whole or in part for any purpose.

This report was completed and first published on 6 July 2020 at 13:38.

Responsibility for the content of this publication lies with:

UniCredit Group and its subsidiaries are subject to regulation by the European Central Bank a) UniCredit Bank AG (UniCredit Bank, Munich or Frankfurt), Arabellastraße 12, 81925 Munich, Germany, (also responsible for the distribution pursuant to §85 WpHG). Regulatory authority: “BaFin“ – Bundesanstalt für Finanzdienstleistungsaufsicht, Marie-Curie-Str. 24-28, 60439 Frankfurt, Germany. b) UniCredit Bank AG London Branch (UniCredit Bank, London), Moor House, 120 London Wall, London EC2Y 5ET, United Kingdom. Regulatory authority: “BaFin“ – Bundesanstalt für Finanzdienstleistungsaufsicht, Marie-Curie-Str. 24-28, 60439 Frankfurt, Germany and subject to limited regulation by the Financial Conduct Authority, 12 Endeavour Square, London E20 1JN, United Kingdom and Prudential Regulation Authority 20 Moorgate, London, EC2R 6DA, United Kingdom. Further details regarding our regulatory status are available on request. c) UniCredit Bank AG Milan Branch (UniCredit Bank, Milan), Piazza Gae Aulenti, 4 - Torre C, 20154 Milan, Italy, duly authorized by the Bank of Italy to provide investment services. Regulatory authority: “Bank of Italy”, Via Nazionale 91, 00184 Roma, Italy and Bundesanstalt für Finanzdienstleistungsaufsicht, Marie-Curie-Str. 24-28, 60439 Frankfurt, Germany. d) UniCredit Bank AG Vienna Branch (UniCredit Bank, Vienna), Rothschildplatz 1, 1020 Vienna, Austria. Regulatory authority: Finanzmarktaufsichtsbehörde (FMA), Otto-Wagner-Platz 5, 1090 Vienna, Austria and subject to limited regulation by the “BaFin“ – Bundesanstalt für Finanzdienstleistungsaufsicht, Marie-Curie-Str. 24-28, 60439 Frankfurt, Germany. Details about the extent of our regulation by the Bundesanstalt für Finanzdienstleistungsaufsicht are available from us on request. e) UniCredit Bank Austria AG (Bank Austria), Rothschildplatz 1, 1020 Vienna, Austria. Regulatory authority: Finanzmarktaufsichtsbehörde (FMA), Otto-Wagner-Platz 5, 1090 Vienna, Austria f) UniCredit Bulbank, Sveta Nedelya Sq. 7, BG-1000 Sofia, Bulgaria. Regulatory authority: Financial Supervision Commission (FSC), 16 Budapeshta str., 1000 Sofia, Bulgaria g) Zagrebačka banka d.d., Trg bana Josipa Jelačića 10, HR-10000 Zagreb, Croatia. Regulatory authority: Croatian Agency for Supervision of Financial Services, Franje Račkoga 6, 10000 Zagreb, Croatia h) UniCredit Bank Czech Republic and Slovakia, Želetavská 1525/1, 140 92 Praga 4, Czech Republic. Regulatory authority: CNB Czech National Bank, Na Příkopě 28, 115 03 Praga 1, Czech Republic i) ZAO UniCredit Bank Russia (UniCredit Russia), Prechistenskaya nab. 9, RF-119034 Moscow, Russia. Regulatory authority: Federal Service on Financial Markets, 9 Leninsky prospekt, Moscow 119991, Russia j) UniCredit Bank Czech Republic and Slovakia, Slovakia Branch, Šancova 1/A, SK-813 33 Bratislava, Slovakia. Regulatory authority: CNB Czech National Bank, Na Příkopě 28, 115 03 Praha 1, Czech Republic and subject to limited regulation by the National Bank of Slovakia, Imricha Karvaša 1, 813 25 Bratislava, Slovakia. Regulatory authority: National Bank of Slovakia, Imricha Karvaša 1, 813 25 Bratislava, Slovakia k) UniCredit Bank Romania, Bucharest 1F Expozitiei Boulevard, 012101 Bucharest 1, Romania. Regulatory authority: National Bank of Romania, 25 Lipscani Street, 030031, 3rd District, Bucharest, Romania l) UniCredit Bank AG New York Branch (UniCredit Bank, New York), 150 East 42nd Street, New York, NY 10017. Regulatory authority: “BaFin“ – Bundesanstalt für Finanzdienstleistungsaufsicht, Marie-Curie-Str. 24-28, 60439 Frankfurt, Germany and New York State Department of Financial Services, One State Street, New York, NY 10004-1511

Further details regarding our regulatory status are available on request.

ANALYST DECLARATION The analyst’s remuneration has not been, and will not be, geared to the recommendations or views expressed in this report, neither directly nor indirectly. All of the views expressed accurately reflect the analyst’s views, which have not been influenced by considerations of UniCredit Bank’s business or client relationships.

POTENTIAL CONFLICTS OF INTERESTS You will find a list of keys for company specific regulatory disclosures on our website https://www.unicreditresearch.eu/index.php?id=disclaimer.

RECOMMENDATIONS, RATINGS AND EVALUATION METHODOLOGY You will find the history of rating regarding recommendation changes as well as an overview of the breakdown in absolute and relative terms of our investment ratings, and a note on the evaluation basis for interest-bearing securities on our website https://www.unicreditresearch.eu/index.php?id=disclaimer and https://www.unicreditresearch.eu/index.php?id=legalnotices.

ADDITIONAL REQUIRED DISCLOSURES UNDER THE LAWS AND REGULATIONS OF JURISDICTIONS INDICATED You will find a list of further additional required disclosures under the laws and regulations of the jurisdictions indicated on our website https://www.unicreditresearch.eu/index.php?id=disclaimer.

E 20/1

6 July 2020 Credit Research

Sector Thinking - Green Bonds/ESG

UniCredit Research page 17 .

UniCredit Research* Credit Research

Erik F. Nielsen Group Chief Economist Global Head of CIB Research +44 207 826-1765 [email protected]

Dr. Ingo Heimig Head of Research Operations & Regulatory Controls +49 89 378-13952 [email protected]

Head of Credit Research

Dr. Sven Kreitmair, CFA Head of Credit Research +49 89 378-13246 [email protected]

Financials Credit Research

Franz Rudolf, CEFA Head Covered Bonds +49 89 378-12449 [email protected]

Dr. Michael Teig Deputy Head Banks +49 89 378-12429 [email protected]

Matthias Dax Sub-Sovereigns & Agencies, ESG +49 89 378-13946 [email protected]

Florian Hillenbrand, CFA Securitization +49 89 378-12004 [email protected]

Tobias Keller Banks +49 89 378-12960 [email protected]

Julian Kreipl, CFA Covered Bonds +49 89 378-12961 [email protected]

Natalie Tehrani Monfared Regulatory & Accounting Service, Insurance, Real Estate +49 89 378-12242 [email protected]

Corporate Credit Research

Christian Aust, CFA Head Industrials, Oil & Gas +49 89 378-17564 [email protected]

Gianfranco Arcovito, CFA Telecoms, Technology, Gaming +49 89 378-15449 [email protected]

Sergey Bolshakov EEMEA Corporates & Financials +44 207 826-1772 [email protected]

Dr. Sven Kreitmair, CFA Automotive & Mobility +49 89 378-13246 [email protected]

Ulrich Scholz, CFA, FRM Utilities, Hybrids +49 89 378-41847 [email protected]

Jonathan Schroer, CFA Telecoms, Media/Cable +49 89 378-13212 [email protected]

Jana Schuler, CFA Industrials +49 89 378-13211 [email protected]

Dr. Silke Stegemann, CEFA Health Care & Pharma, Consumer +49 89 378-18202 [email protected]

UniCredit Research, Corporate & Investment Banking, UniCredit Bank AG, Am Eisbach 4, D-80538 Munich, [email protected] Bloomberg: UCCR, Internet: www.unicreditresearch.eu CR 20/2

*UniCredit Research is the joint research department of UniCredit Bank AG (UniCredit Bank, Munich or Frankfurt), UniCredit Bank AG London Branch (UniCredit Bank, London), UniCredit Bank AG Milan Branch (UniCredit Bank, Milan), UniCredit Bank AG Vienna Branch (UniCredit Bank, Vienna), UniCredit Bank Austria AG (Bank Austria), UniCredit Bulbank, Zagrebačka banka d.d., UniCredit Bank Czech Republic and Slovakia, ZAO UniCredit Bank Russia (UniCredit Russia), UniCredit Bank Romania.