Embed Size (px)

Citation preview

> Erste BankConsolidating the opportunity in CEE

> Goldman Sachs European Financials Conference 2005

> Puerto Banus, June 8 – 10, 2005

> Andreas Treichl, CEO

2Goldman Sachs European Financials Conference 2005Puerto Banus, 8-10 June, 2005

> Disclaimer

THE INFORMATION CONTAINED IN THIS DOCUMENT HAS NOT BEEN INDEPENDENTLY VERIFIEDAND NO REPRESENTATION OR WARRANTY EXPRESSED OR IMPLIED IS MADE AS TO, AND NORELIANCE SHOULD BE PLACED ON, THE FAIRNESS, ACCURACY, COMPLETENESS ORCORRECTNESS OF THS INFORMATION OR OPINIONS CONTAINED HEREIN

CERTAIN OF THE STATEMENTS CONTAINED IN THIS DOCUMENT MY BE STATEMENTS OF FUTUREEXPECTATIONS AND OTHER FORWARD-LOOKING STATEMENTS THAT ARE BASED ONMANAGEMENT’S CURRENT VIEWS AND ASSUMPTIONS AND INVOLVE KNOWN AND UNKNOWNRSIKS AND UNCERTAINTIES THAT COULD CAUSE ACTUAL RESULTS, PERFORMANCE OR ENVENTSTO DIFFER MATERIALLY FROM THOSE EXPRESSED OR IMPLIED IN SUCH STATEMENTS.

NONE OF ERSTE BANK OR ANY OF ITS AFFILIATES, ADVISORS OR REPRESENTATIVES SHALL HAVEANY LIABILITY WHATSOEVER (IN NEGLIGENCE OR OTHERWISE) FOR ANY LOSS HOWSOEVERARISING FROM ANY USE OF THIS DOCUMENT OR ITS CONTENT OR OTHERWISE ARISING INCONNECTION WITH THIS DOCUMENT

THIS DOCUMENT DOES NOT CONSTITUTE AN OFFER OR INVITATION TO PURCHASE ORSUBSCRIBE FOR ANY SHARES AND NEITHER IT NOR ANY PART OF IT SHALL FORM THE BASIS OFOR BE RELIED UPON IN CONNECTION WITH ANY CONTRACT OR COMMITMENT WHATSOEVER

Cautionary note regarding forward-looking statements

3Goldman Sachs European Financials Conference 2005Puerto Banus, 8-10 June, 2005

> Presentation topics

1. The opportunity

2. Focused growth strategy

3. Growing contribution

4. Financial highlights

4Goldman Sachs European Financials Conference 2005Puerto Banus, 8-10 June, 2005

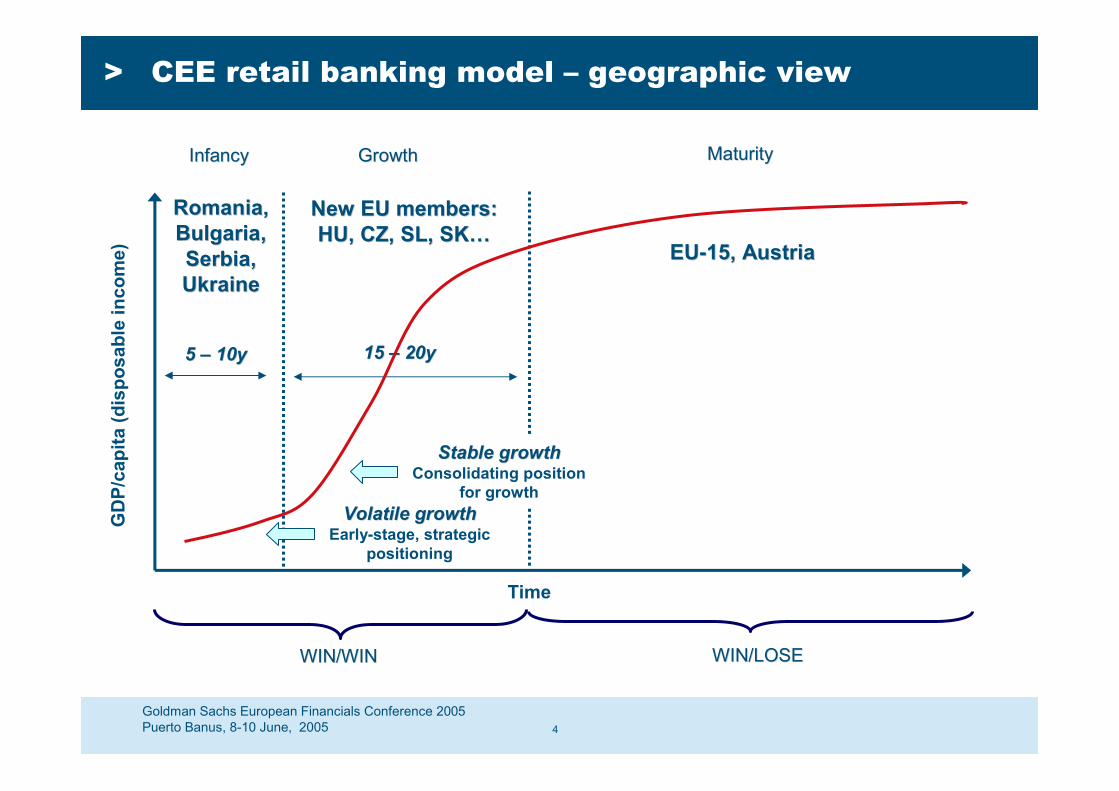

> CEE retail banking model – geographic view

InfancyInfancy GrowthGrowth MaturityMaturity

WIN/WINWIN/WIN WIN/LOSEWIN/LOSE

Romania,Romania,Bulgaria,Bulgaria,Serbia,Serbia,UkraineUkraine

New EU members:New EU members:HU, CZ, SL, SKHU, CZ, SL, SK……

Volatile growthVolatile growthEarly-stage, strategic

positioning

EUEU--15, Austria15, Austria

Stable growthStable growthConsolidating position

for growth

55 –– 10y10y 1515 –– 20y20y

GD

P/ca

pita

(dis

posa

ble

inco

me)

Time

5Goldman Sachs European Financials Conference 2005Puerto Banus, 8-10 June, 2005

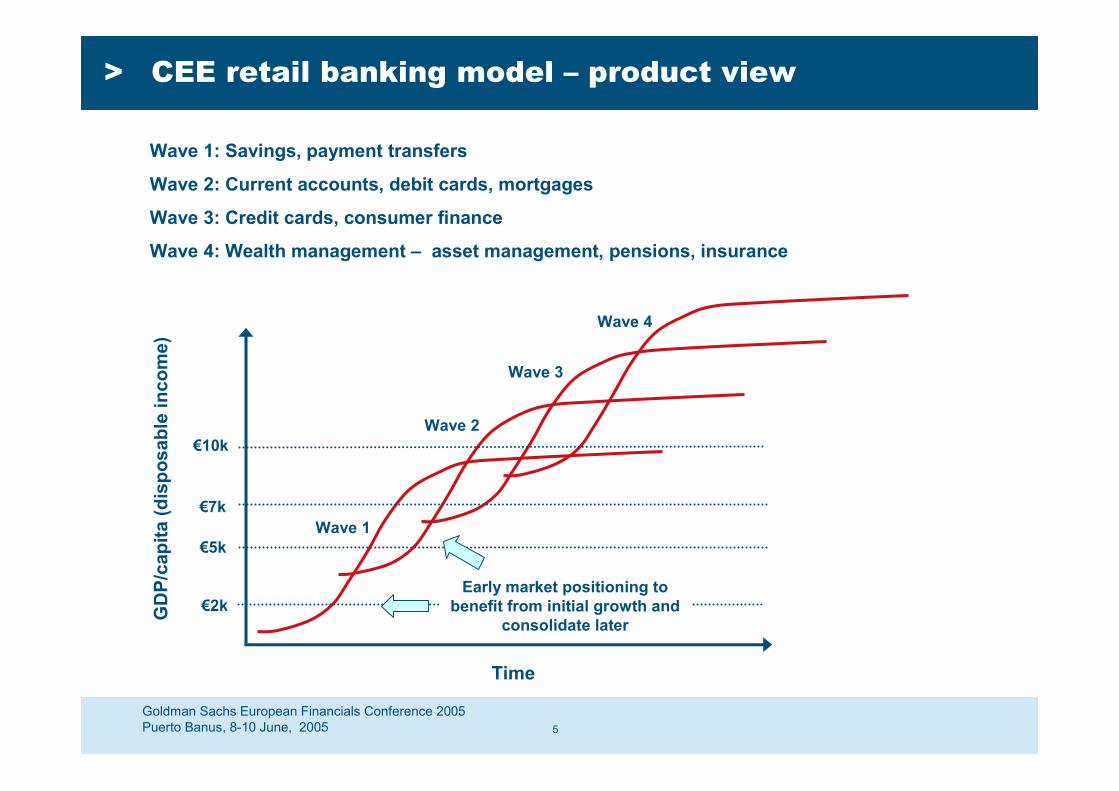

> CEE retail banking model – product view

Wave 1: Savings, payment transfers

Wave 2: Current accounts, debit cards, mortgages

Wave 3: Credit cards, consumer finance

Wave 4: Wealth management – asset management, pensions, insurance

GD

P/ca

pita

(dis

posa

ble

inco

me)

Time

€2k

€5k

€7k

€10k

Early market positioning tobenefit from initial growth and

consolidate later

Wave 1

Wave 2

Wave 3

Wave 4

6Goldman Sachs European Financials Conference 2005Puerto Banus, 8-10 June, 2005

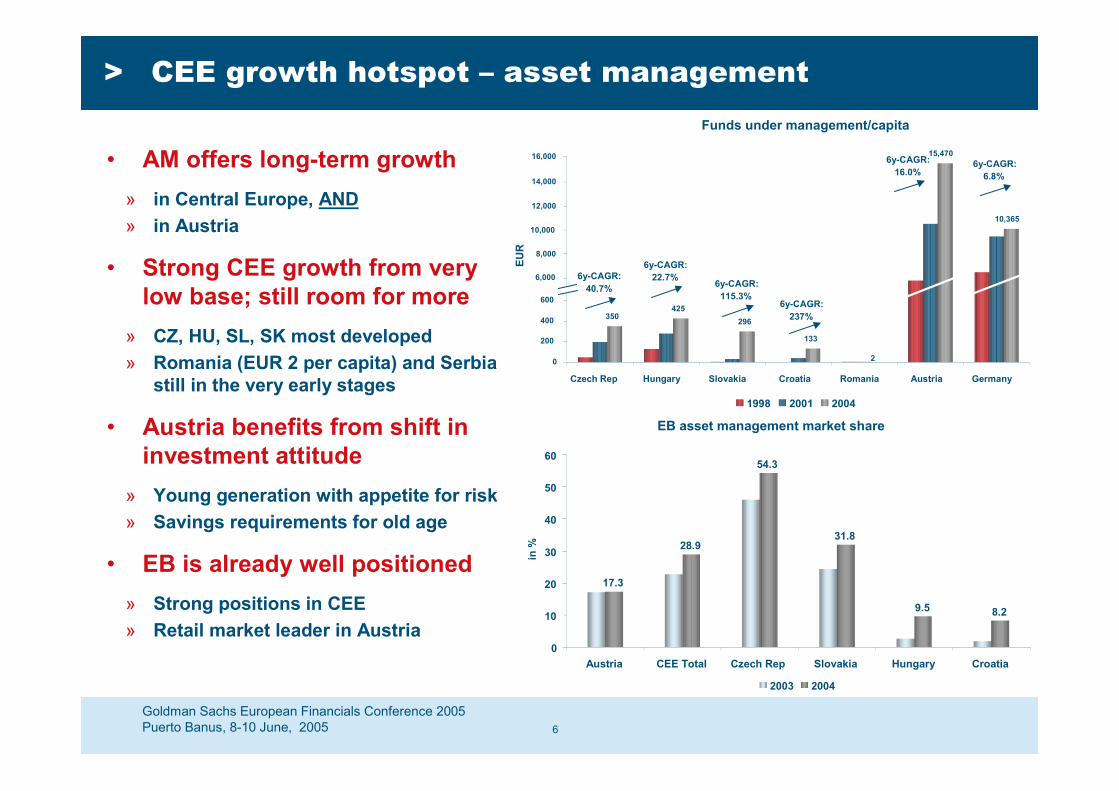

> CEE growth hotspot – asset management

EB asset management market share

17.3

28.9

54.3

31.8

9.5 8.2

0

10

20

30

40

50

60

Austria CEE Total Czech Rep Slovakia Hungary Croatia

in %

2003 2004

• AM offers long-term growth» in Central Europe, AND» in Austria

• Strong CEE growth from verylow base; still room for more

» CZ, HU, SL, SK most developed» Romania (EUR 2 per capita) and Serbia

still in the very early stages

• Austria benefits from shift ininvestment attitude

» Young generation with appetite for risk» Savings requirements for old age

• EB is already well positioned» Strong positions in CEE» Retail market leader in Austria

Funds under management/capita

350425

296

133

15,470

10,365

0

200

400

600

6,000

8,000

10,000

12,000

14,000

16,000

Czech Rep Hungary Slovakia Croatia Romania Austria Germany

EUR

1998 2001 2004

6y-CAGR:40.7%

6y-CAGR:16.0%

6y-CAGR:237%

6y-CAGR:115.3%

6y-CAGR:22.7%

6y-CAGR:6.8%

2

7Goldman Sachs European Financials Conference 2005Puerto Banus, 8-10 June, 2005

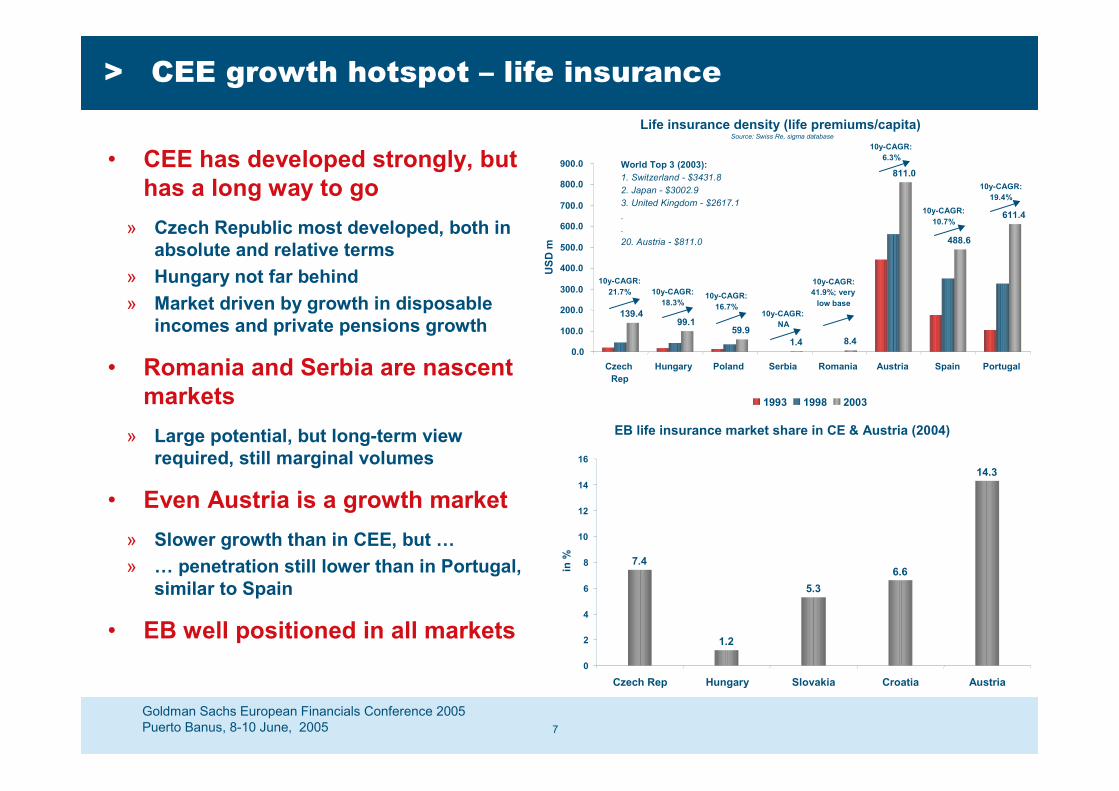

> CEE growth hotspot – life insurance

• CEE has developed strongly, buthas a long way to go

» Czech Republic most developed, both inabsolute and relative terms

» Hungary not far behind» Market driven by growth in disposable

incomes and private pensions growth

• Romania and Serbia are nascentmarkets

» Large potential, but long-term viewrequired, still marginal volumes

• Even Austria is a growth market» Slower growth than in CEE, but …» … penetration still lower than in Portugal,

similar to Spain

• EB well positioned in all markets

Life insurance density (life premiums/capita)Source: Swiss Re, sigma database

139.499.1

59.91.4 8.4

811.0

488.6

611.4

0.0

100.0

200.0

300.0

400.0

500.0

600.0

700.0

800.0

900.0

CzechRep

Hungary Poland Serbia Romania Austria Spain Portugal

USD

m

1993 1998 2003

10y-CAGR:21.7%

10y-CAGR:19.4%

10y-CAGR:10.7%

10y-CAGR:6.3%

10y-CAGR:41.9%; very

low base10y-CAGR:

NA

10y-CAGR:16.7%

10y-CAGR:18.3%

World Top 3 (2003):1. Switzerland - $3431.82. Japan - $3002.93. United Kingdom - $2617.1..20. Austria - $811.0

EB life insurance market share in CE & Austria (2004)

7.4

1.2

5.36.6

14.3

0

2

4

6

8

10

12

14

16

Czech Rep Hungary Slovakia Croatia Austria

in %

8Goldman Sachs European Financials Conference 2005Puerto Banus, 8-10 June, 2005

> Presentation topics

1. The opportunity

2. Focused growth strategy

3. Growing contribution

4. Financial highlights

9Goldman Sachs European Financials Conference 2005Puerto Banus, 8-10 June, 2005

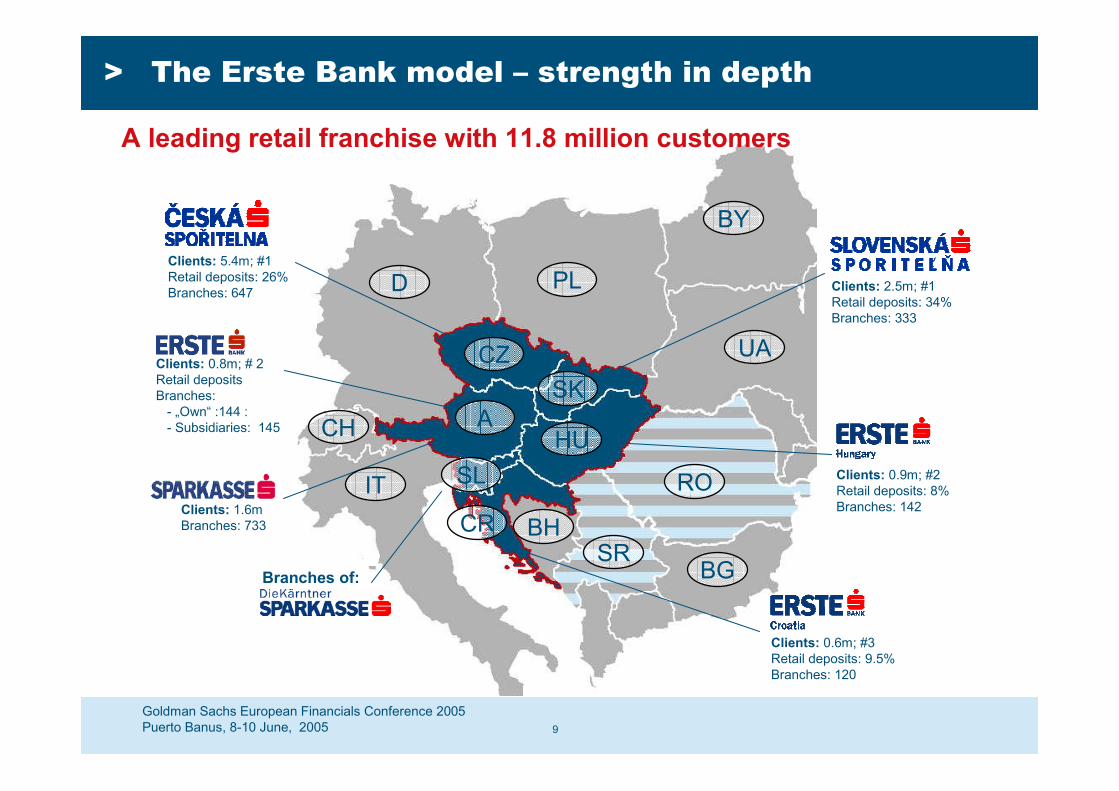

> The Erste Bank model – strength in depth

A leading retail franchise with 11.8 million customers

Clients: 5.4m; #1Retail deposits: 26%Branches: 647 Clients: 2.5m; #1

Retail deposits: 34%Branches: 333

Clients: 0.9m; #2Retail deposits: 8%Branches: 142

Clients: 0.6m; #3Retail deposits: 9.5%Branches: 120

Branches of:

Clients: 1.6mBranches: 733

Clients: 0.8m; # 2Retail depositsBranches:

- „Own“ :144 :- Subsidiaries: 145 A

CZ

SL

SK

HU

CR

D PL

IT

BH

CH

UA

BY

RO

SRBG

10Goldman Sachs European Financials Conference 2005Puerto Banus, 8-10 June, 2005

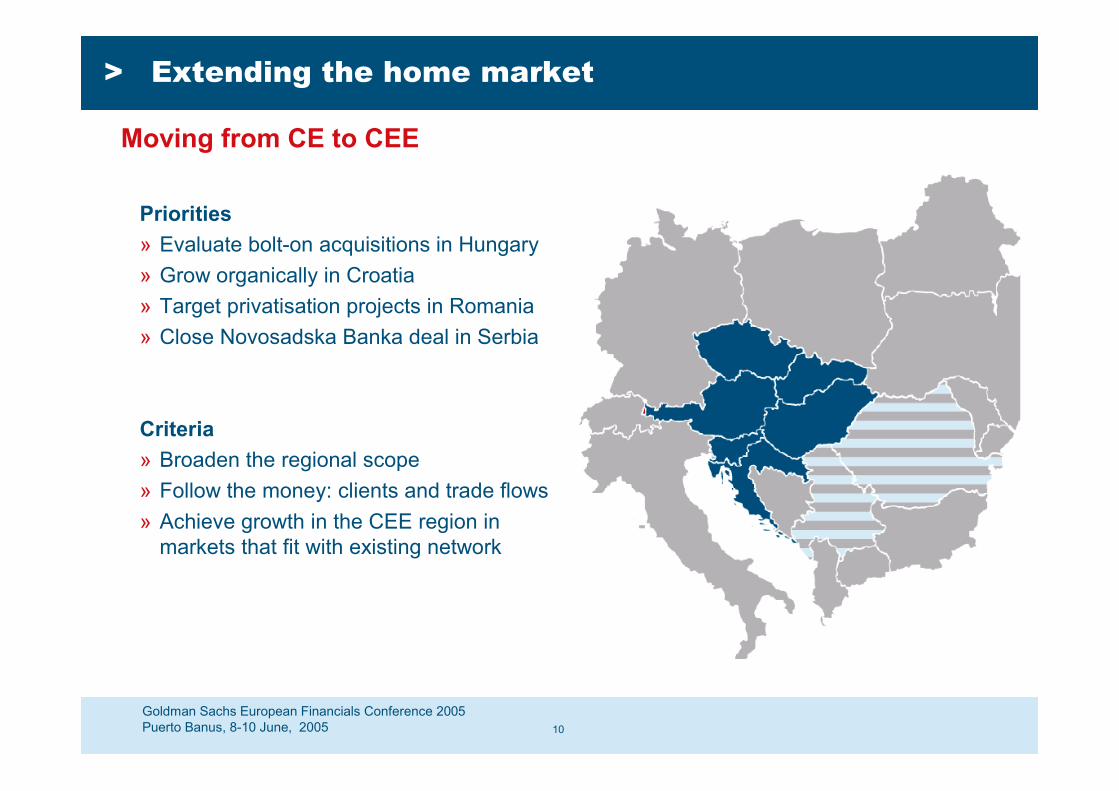

> Extending the home market

Moving from CE to CEE

Priorities» Evaluate bolt-on acquisitions in Hungary» Grow organically in Croatia» Target privatisation projects in Romania» Close Novosadska Banka deal in Serbia

Criteria» Broaden the regional scope» Follow the money: clients and trade flows» Achieve growth in the CEE region in

markets that fit with existing network

11Goldman Sachs European Financials Conference 2005Puerto Banus, 8-10 June, 2005

> Presentation topics

1. The opportunity

2. Focused growth strategy

3. Growing contribution

4. Financial highlights

12Goldman Sachs European Financials Conference 2005Puerto Banus, 8-10 June, 2005

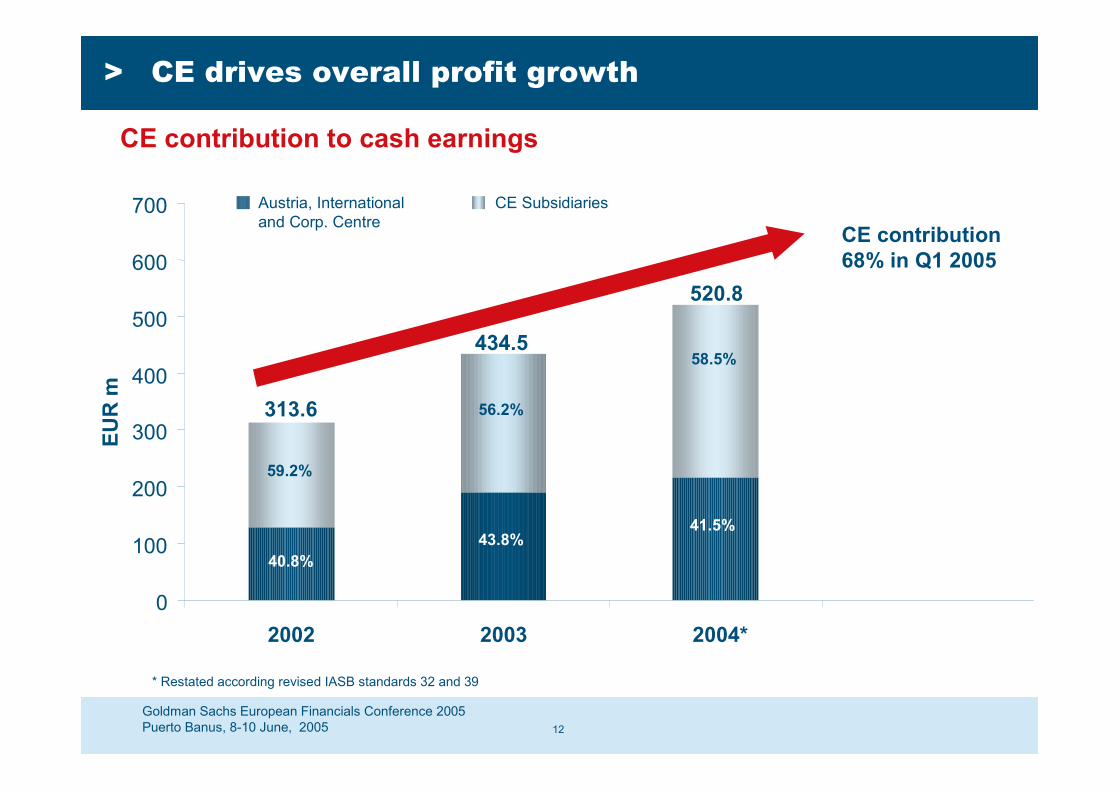

> CE drives overall profit growth

CE contribution to cash earnings

0

100

200

300

400

500

600

700

2002 2003 2004*

EUR

m

CE Subsidiaries

* Restated according revised IASB standards 32 and 39

313.6

434.5

520.8

40.8%

59.2%

56.2%

58.5%

43.8%41.5%

CE contribution68% in Q1 2005

Austria, Internationaland Corp. Centre

13Goldman Sachs European Financials Conference 2005Puerto Banus, 8-10 June, 2005

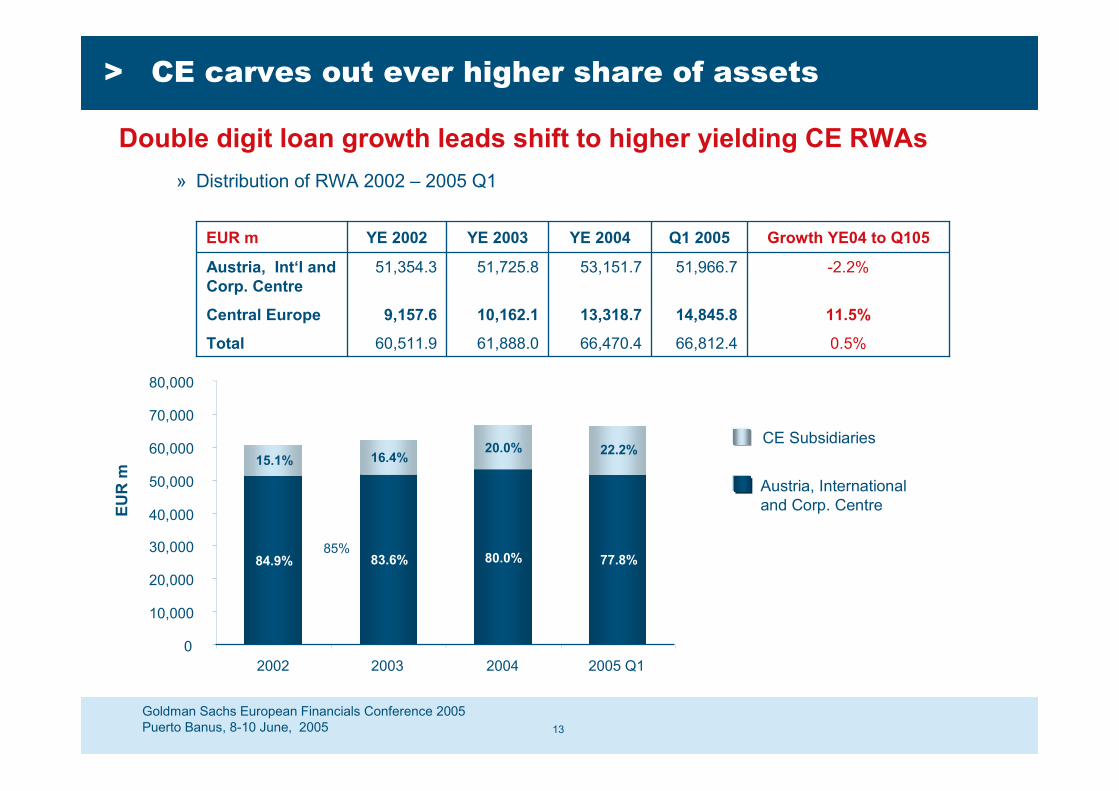

> CE carves out ever higher share of assets

Double digit loan growth leads shift to higher yielding CE RWAs» Distribution of RWA 2002 – 2005 Q1

Austria, Internationaland Corp. Centre

CE Subsidiaries

85% 84%80%

66,812.4

14,845.8

51,966.7

Q1 2005

66,470.4

13,318.7

53,151.7

YE 2004

0.5%61,888.060,511.9Total

11.5%10,162.19,157.6Central Europe

-2.2%51,725.851,354.3Austria, Int‘l andCorp. Centre

Growth YE04 to Q105YE 2003YE 2002EUR m

84.9% 83.6% 80.0% 77.8%

15.1% 16.4%20.0% 22.2%

0

10,000

20,000

30,000

40,000

50,000

60,000

70,000

80,000

2002 2003 2004 2005 Q1

EUR

m

14Goldman Sachs European Financials Conference 2005Puerto Banus, 8-10 June, 2005

> Presentation topics

1. The opportunity

2. Focused growth strategy

3. Growing contribution

4. Financial highlights

15Goldman Sachs European Financials Conference 2005Puerto Banus, 8-10 June, 2005

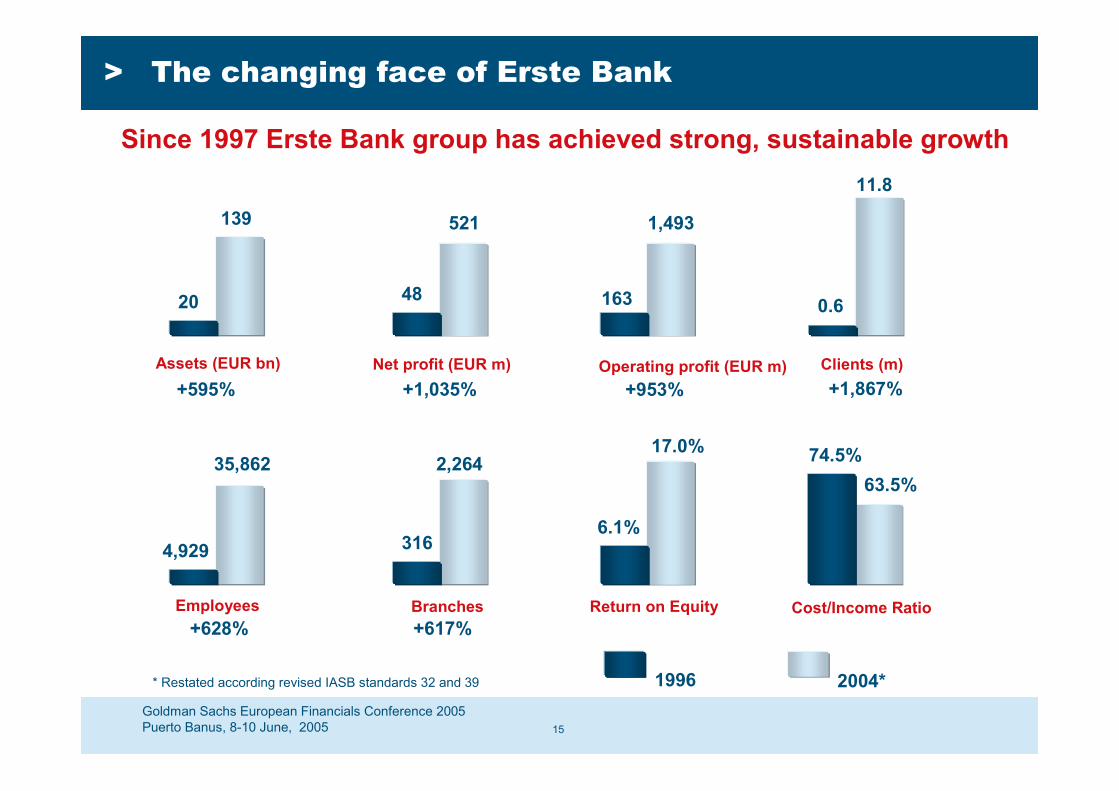

> The changing face of Erste Bank

Since 1997 Erste Bank group has achieved strong, sustainable growth

Assets (EUR bn)

20

139

Net profit (EUR m)

48

521

Clients (m)

0.6

11.8

Operating profit (EUR m)

163

1,493

+595% +1,035% +1,867%+953%

Employees

4,929

35,862

Branches

316

2,264

Return on Equity

6.1%

17.0%

Cost/Income Ratio

74.5%63.5%

+628% +617%

2004*1996* Restated according revised IASB standards 32 and 39

16Goldman Sachs European Financials Conference 2005Puerto Banus, 8-10 June, 2005

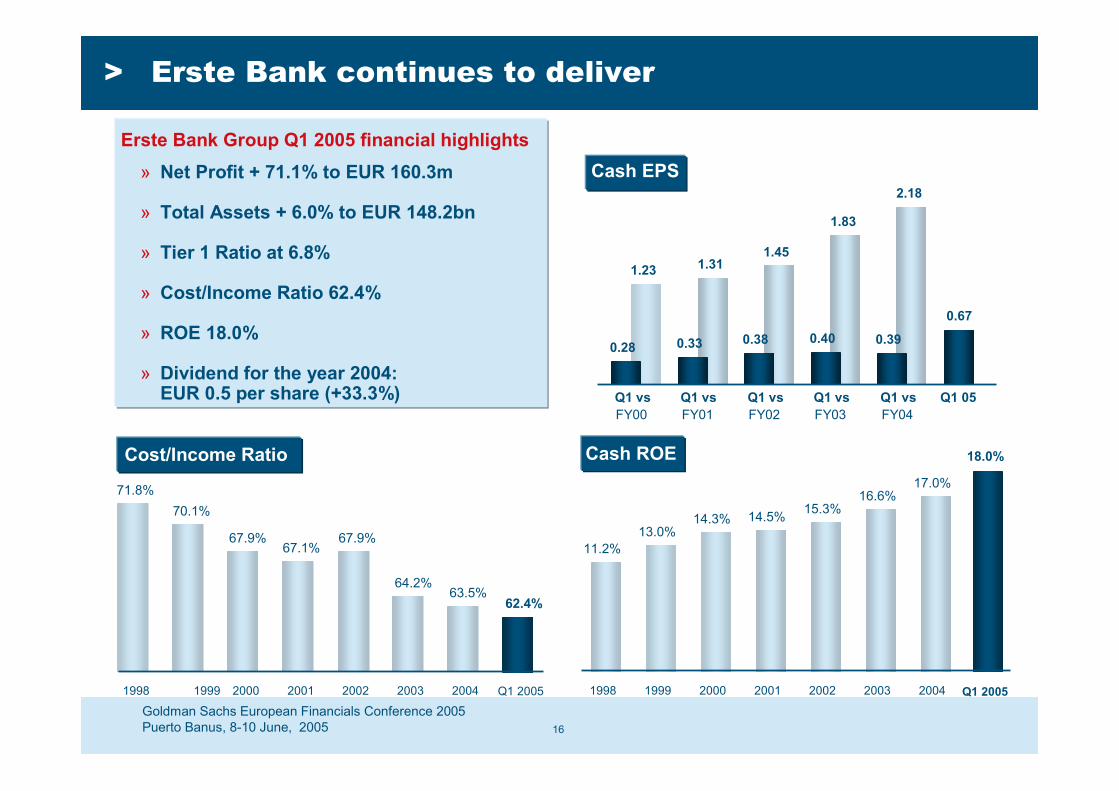

> Erste Bank continues to deliver

» Net Profit + 71.1% to EUR 160.3m

» Total Assets + 6.0% to EUR 148.2bn

» Tier 1 Ratio at 6.8%

» Cost/Income Ratio 62.4%

» ROE 18.0%

» Dividend for the year 2004:EUR 0.5 per share (+33.3%)

Cash EPS

Cost/Income Ratio Cash ROE

71.8%70.1%

67.9%67.1%

67.9%

64.2%63.5%

1998 1999 2000 2001 2002 2003 2004

11.2%13.0%

14.3% 14.5% 15.3%16.6%

17.0%

1998 1999 2000 2001 2002 2003 2004

Erste Bank Group Q1 2005 financial highlights

0.28 0.33 0.38 0.40 0.39

0.67

1.23 1.311.45

1.83

2.18

Q1 vsFY00

Q1 vsFY01

Q1 vsFY02

Q1 vsFY03

Q1 vsFY04

Q1 05

62.4%

Q1 2005

18.0%

Q1 2005

17Goldman Sachs European Financials Conference 2005Puerto Banus, 8-10 June, 2005

Fax +43 (0)5 0100-13112E-mail: [email protected]: www.erstebank.com

Reuters: ERST.VI Bloomberg: EBS AVDatastream: O:ERS Securities ID: 065201

Gabriele WerzerTel: +43 (0)5 0100-11286 E-Mail: [email protected]

Thomas SommerauerTel: +43 (0)5 0100-17326 E-Mail: [email protected]

Monika PerausTel: +43 (0)5 0100-11282 E-Mail: [email protected]

> Investor relations contacts

Investor relations

Erste Bank, Graben 21, 1010 Vienna