Embed Size (px)

Citation preview

Ernst & Young IREM/BOMA Real Estate Forecast BreakfastCommercial Real Estate Conditions and Outlook29 January 2009

Page 2 EY 2009 Real Estate Update

Agenda

► Historical trends and effect of contracting economy on different product types

► 2008 transactions and status of commercial real estate since the collapse of the capital markets

► 2009 outlook: capitalization and discount rates and real estate fundamentals

Page 3 EY 2009 Real Estate Update

Southern California Office Trends Vacancy Rates

5.00%

10.00%

15.00%

20.00%

2002 2003 2004 2005 2006 2007 2008

Vac

ancy

National Los Angeles Orange County San Diego

Source: REIS

Page 4 EY 2009 Real Estate Update

Southern California Office Trends Rental Rates

$18.00

$22.00

$26.00

$30.00

2002 2003 2004 2005 2006 2007 2008

Ren

tal R

ate

National Los Angeles Orange County San Diego

Source: REIS

Page 5 EY 2009 Real Estate Update

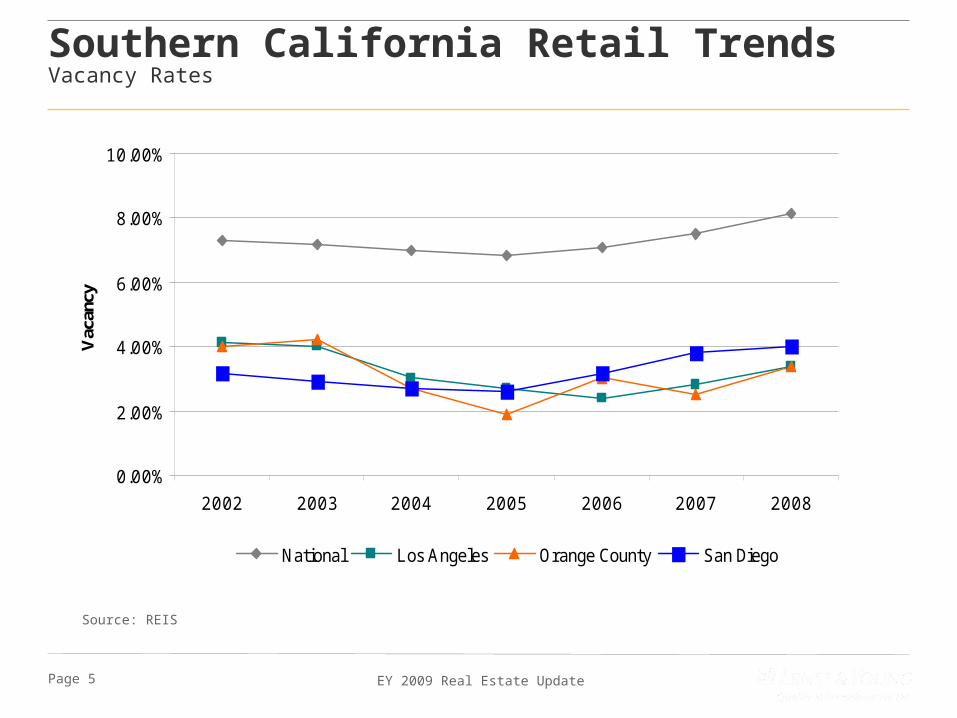

Southern California Retail Trends Vacancy Rates

0.00%

2.00%

4.00%

6.00%

8.00%

10.00%

2002 2003 2004 2005 2006 2007 2008

Vac

ancy

National Los Angeles Orange County San Diego

Source: REIS

Page 6 EY 2009 Real Estate Update

Southern California Retail Trends Rental Rates

$10.00

$15.00

$20.00

$25.00

$30.00

2002 2003 2004 2005 2006 2007 2008

Ren

tal R

ate

National Los Angeles Orange County San Diego

Source: REIS

Page 7 EY 2009 Real Estate Update

Southern California Multifamily Trends Vacancy Rates

2.00%

3.00%

4.00%

5.00%

2002 2003 2004 2005 2006 2007 2008

Vac

ancy

National Los Angeles Orange County San Diego

Source: REIS

Page 8 EY 2009 Real Estate Update

Southern California Multifamily Trends Rental Rates

$800

$1,000

$1,200

$1,400

$1,600

2002 2003 2004 2005 2006 2007 2008

Ren

tal R

ate

National Los Angeles Orange County San Diego

Source: REIS

Page 9 EY 2009 Real Estate Update

Southern California Hospitality TrendsOccupancy

50.0%

60.0%

70.0%

80.0%

2002 2003 2004 2005 2006 2007 2008

Occ

upan

cy

National Los Angeles San Diego

Source: Smith Travel Research

Page 10 EY 2009 Real Estate Update

Southern California Hospitality TrendsRevenue per Available Room (“RevPAR”)

$40.00

$60.00

$80.00

$100.00

$120.00

2002 2003 2004 2005 2006 2007 2008

Rev

PA

R

National Los Angeles San Diego

Source: Smith Travel Research

Page 11 EY 2009 Real Estate Update

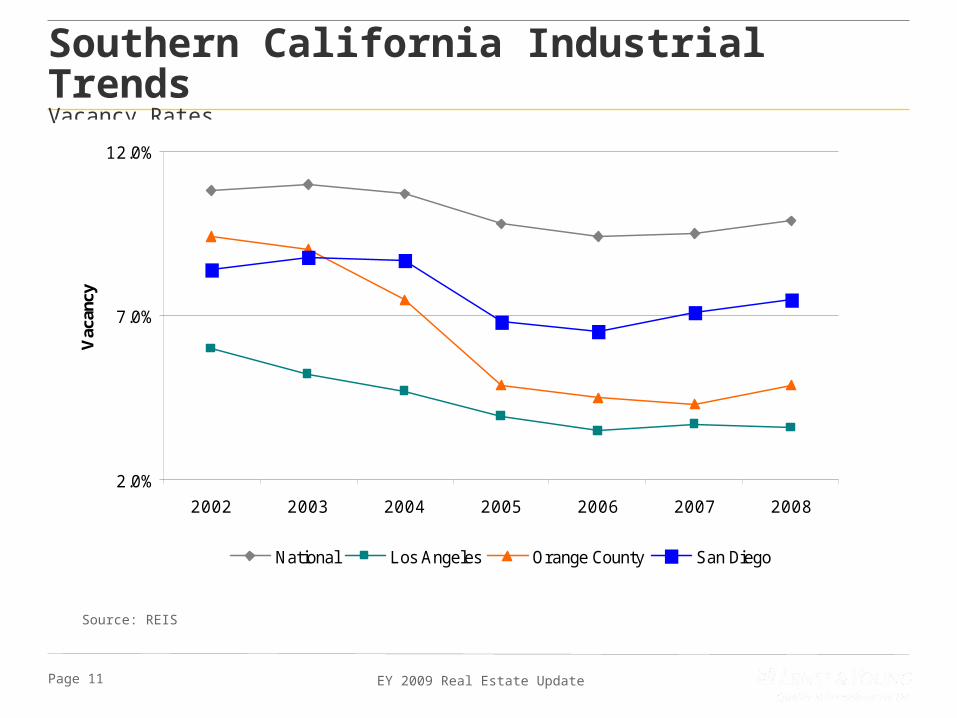

Southern California Industrial Trends Vacancy Rates

Source: REIS

2.0%

7.0%

12.0%

2002 2003 2004 2005 2006 2007 2008

Vac

ancy

National Los Angeles Orange County San Diego

Page 12 EY 2009 Real Estate Update

Southern California Industrial Trends Rental Rates

Source: REIS

$4.00

$5.00

$6.00

$7.00

2002 2003 2004 2005 2006 2007 2008

Ren

tal R

ate

National Los Angeles Orange County San Diego

Page 13 EY 2009 Real Estate Update

SECTOR DEAL TERMS

Leasing Northrop Grumman Corp., office lease, 101 Continental Boulevard

$120mm

Hyundai Motor Finance Co., 100,000-sf lease, Park Place

N/A

Development Kearny Real Estate Co., and Morgan Stanley Real Estate, Century Business Center

$45mm

City of Ontario, 225,000-sf arena, Ontario $150mm

Boulevards at South, mixed-use, Carson $850mm

Finance Douglas Emmett Inc., refinance of a six-building portfolio totaling 1.4 million

$365mm

Meruelo Maddux Properties., construction loan, 717 W. Ninth St.

$84mm

HCP Inc., placed secured debt on 16 senior-housing projects

$319mm

Macerich, loans on five properties and commitment on sixth

$1bnSource: Real Estate Southern California, September 2008

2008 Transactions Leasing, Development and Finance

Page 14 EY 2009 Real Estate Update

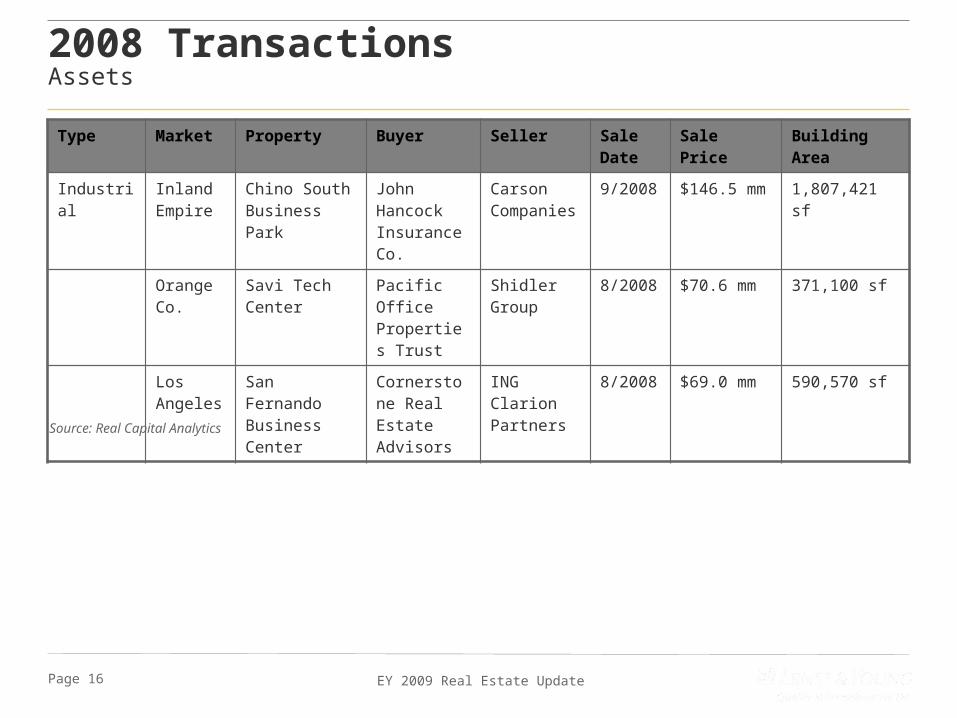

2008 TransactionsAssets

Type Market Property Buyer Seller Sale Date

Sale Price Building Area

Office Los Angeles

Citigroup Center

Hines Interests

Broadway Real Estate Partners

9/2008 $280.0 mm 891,000 sf

Orange Co.

Main Plaza Towers

Shorenstein Partners

Maguire Properties

8/2008 $211.1 mm 587,000 sf

Orange Co.

Centerpointe La Palma

TA Associates Realty

Arden Realty Inc.

9/2008 $105.4 mm 532,000 sf

Retail Inland empire

Palm Grove JH Real Estate Partners

House Land Development

9/2008 $65.0 mm 255,000 sf

Inland empire

Gateway Village

Gateway Village-III LP

Hanley Investment Group

5/2008 $47.2 mm 96,959 sf

Los Angeles

Diamond Hills Plaza

Sarofim Realty Advisors

AEW Capital JV MCC Construction Corp.

5/2008 $45.8 mm 157,408 sf

Source: Real Capital Analytics

Page 15 EY 2009 Real Estate Update

2008 TransactionsAssets

Type Market Property Buyer Seller Sale Date

Sale Price Building Area

Multi-family

Los Angeles

Pegasus Buchanan Street Partners JV CalPERS

KOR Group JV Lubert-Adler

7/2008 $100.0 mm 322 units

Orange Co.

Mesa Verde Hills

United Dominion Realty Trust

Sares Regis Group JV Invesco Realty Adv.

5/2008 $87.3 mm 296 units

Orange Co.

Prado at Laguna Hills

TGM Associates

RREEF Funds

7/2008 $77.0 mm 360 units

Hotel Los Angeles

Westin Century Plaza

DE Shaw Group JV Woodridge Capital LLC

Sunstone Hotel Investors JV Hyatt Hotels

6/2008 $366.5 mm 726 units

Los Angeles

Ritz Carlton Huntington Hotel

Langham Hotels

Cornerstone Real Estate Advisors

1/2008 $165.0 mm 392 units

Orange Co.

Hyatt Regency Orange County

Inland American Real Estate Trust

Ashford Hospitality Trust

10/2008 $112.0 mm 654 units

Source: Real Capital Analytics

Page 16 EY 2009 Real Estate Update

2008 TransactionsAssets

Type Market Property Buyer Seller Sale Date

Sale Price Building Area

Industrial Inland Empire

Chino South Business Park

John Hancock Insurance Co.

Carson Companies

9/2008 $146.5 mm 1,807,421 sf

Orange Co.

Savi Tech Center

Pacific Office Properties Trust

Shidler Group

8/2008 $70.6 mm 371,100 sf

Los Angeles

San Fernando Business Center

Cornerstone Real Estate Advisors

ING Clarion Partners

8/2008 $69.0 mm 590,570 sf

Source: Real Capital Analytics

Page 17 EY 2009 Real Estate Update

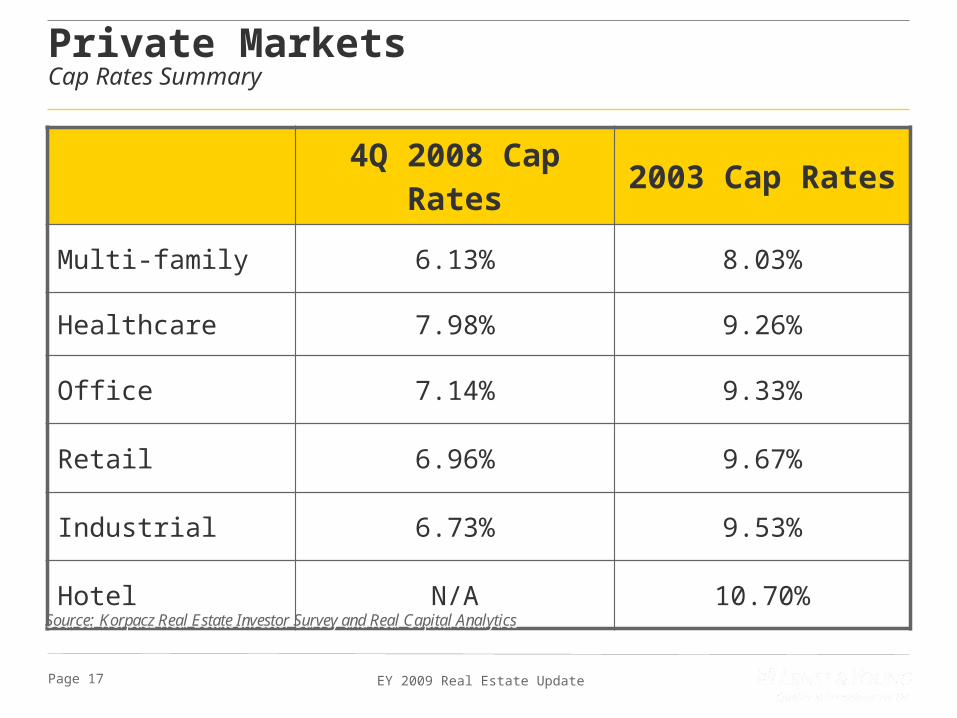

Private MarketsCap Rates Summary

4Q 2008 Cap Rates

2003 Cap Rates

Multi-family 6.13% 8.03%

Healthcare 7.98% 9.26%

Office 7.14% 9.33%

Retail 6.96% 9.67%

Industrial 6.73% 9.53%

Hotel N/A 10.70%Source: Korpacz Real Estate Investor Survey and Real Capital AnalyticsSource: Korpacz Real Estate Investor Survey and Real Capital Analytics

Page 18 EY 2009 Real Estate Update

Summary

Commercial real estate will re-price by at least 20% of their 2007 peak given lack of debt and changing loan terms to percentages equal to REIT drops in value

There is no urgency in the market, as investors are motivated by distressed situations and are waiting on the side lines for non-performing debt to trade; it may be better to be late than early

Property owners who are unable to roll over their debts and are forced to sell assets will further put downward pressure on real estate values

Required yields for CRE investment are rising with a much higher real estate risk premium

Banks will continue to take losses, sell loans to borrowers at discounts and create a new distressed debt market

Declining fundamentals (occupancy and rents) due to economic conditions.

Begin Again in 2010………………

Page 19 EY 2009 Real Estate Update

How you feel today has a lot to do with your vantage point…

Thank you.

Troy L. Jones

Ernst & Young LLPPrincipal, Transaction Real EstatePhone: + 1 213 977 3338

Email: [email protected]