Embed Size (px)

Citation preview

Equity marketsOncology | 14 August 2015Chief Investment Office WMLachlan Towart, analyst, [email protected]

• Our oncology investment theme recommends companies that webelieve are potential winners in the current USD 100bn cancertherapeutics market.

• New therapies are changing the standard of care and improvingsurvival in lung cancer and melanoma. The market opportunity inthese cancers could be USD 10bn or more, while expanding use toother cancer types could add another USD 15bn.

• We expect significant clinical data to be published over thenext year, helping to crystallize the market opportunity for newtherapies in these and other indications. We also see excitingemerging technologies in T-cell engineering and personalizedcancer treatment.

• We believe our selection of oncology-related stocks will outperformthe broader healthcare sector due to sector-beating earningsgrowth and new clinical data that will increase the visibility of keycancer products in development. Given the length of time taken todevelop new drugs, a long-term investment horizon is needed.

Investment GuidanceCancer is among the leading causes of death worldwide and resultsin among the highest costs to healthcare systems around the globe.According to the World Cancer Report 2014, published by the World HealthOrganization (WHO), over 14 million new cases of cancer (excluding non-melanoma skin cancers) and over eight million cancer deaths occurredglobally in 2012.

A better understanding of cancer cell biology and the immune system hasled to the development of immuno-oncology, an approach that uses thebody's immune system to fight cancer. As well as significantly reducingthe burden of side effects, immuno-oncology treatment offers the hope ofmore durable responses to treatment than conventional therapy. Combinedsales of the two immuno-oncology drugs launched since September 2014are already annualizing at over USD 1 billion. These new treatments arenot a "cure," but do represent a material improvement in length andquality of life for many patients. Important progress is also being made inpersonalized cancer treatment, an area that could offer hope for a "cure"for cancer in certain circumstances.

Oncology is a growth-oriented theme, with little economic sensitivity toits fundamentals. Pharmaceutical companies with exposure to oncologytend to offer above-GDP earnings growth, high returns on capitaland growing dividends. Many new cancer therapeutics are beingdeveloped by smaller biotechnology companies with no earnings history;these companies' returns depend on successful clinical development orcommercial partnerships for their drugs. Hence, we emphasize a long-term investment horizon and diversification when investing in the oncologytheme.

Source: Fotolia

Selection list as of 14 August 2015

Most Preferred

Company Country Subsector

AbbVie US Pharma

AstraZeneca UK Pharma

BioMarin Pharmaceuticals US Biotech

Celgene Corporation US Biotech

Halozyme Therapeutics US Biotech

Incyte Corporation US Biotech

Medivation US Biotech

Merck & Co US Pharma

Pfizer US Pharma

Roche Switzerland Pharma

Source: UBS, FactSet

This is a copy of the Equity Preference List(EPL) "Oncology." As selections may change, werecommend visiting the UBS WM CIO portal (whichalso lists the analyst(s) responsible for the selectionsand the thematic benchmark), or contacting yourclient advisor for the latest update of this EPL.

Please note this theme has been renamed -for previous documents please see our reportsunder the title "Major advances in cancertherapeutics". Previous reports:

• Major advances in cancer therapeutics - update2, published 8 April 2015

• Major advances in cancer therapeutics - update,published 21 November 2014

• Major advances in cancer therapeutics,published 5 May 2014

This report has been prepared by UBS Switzerland AG. Please see important disclaimers and disclosures at the end of the document.

Introduction

Our oncology theme recommends companies that we believe are potentialwinners in the global cancer therapeutics market. We recommend exposureto the theme through a diversified portfolio of pharmaceutical andbiotechnology stocks. Given the length of time taken to develop newdrugs, a long-term investment horizon is needed.

Currently oncology currently represents a USD 100bn market, or around10% of the global pharmaceutical market, and has grown at an averageannual rate of 6% since 2009. We expect this to accelerate to 15% over2015-2020, with melanoma and lung cancer seeing 20%-plus growth.

In particular, we see a potential USD 25 billion market opportunity for thefirst wave of recently-launched immuno-oncology drugs. Melanoma andlung cancer, where the first such drugs have begun to receive approvals,could be worth USD 10 billion or more, while other cancer types for whichinitial data already exists, including kidney and head & neck cancers, couldadd another USD 15 billion opportunity.

These targeted treatments are changing the standard of care in melanomaand lung cancer. For example, melanoma progression-free survival hasimproved from just a few weeks using traditional chemotherapy to 11.5months using a combination of Bristol-Myers Squibb's immuno-oncologydrugs Opdivo and Yervoy. While not a cure, this represents a materialimprovement in the length and quality of life for patients with this hard-to-treat disease. Other technologies, such as personalized immunotherapy,may offer hope for effective cures for some patients, although this too issome years away.

Oncology is a growth-oriented theme, with little economic sensitivity toits fundamentals. Pharmaceutical companies with exposure to oncologytend to offer above-GDP earnings growth, high returns on capital andgrowing dividends. Many new cancer therapeutics are being developedby smaller biotechnology companies with no earnings history; these com-panies' returns depend on successful clinical development or commercialpartnerships for their drugs.

Investment risksA key risk in biotechnology and pharmaceutical investment is clinical failure.A new drug can fail at any point in clinical development, encounter reg-ulatory issues or fail in post-approval commerce. We therefore promotediversification when investing in this theme. Concerns over drug pricing arealso valid given that many of these new agents will likely be introduced atextremely high prices. However, truly novel therapeutics face limited com-petition and thus low price pressure.

From a macro perspective, the biotechnology sector is sensitive tochanges in risk attitude, in particular the availability of finance for devel-opment-stage companies, while the broader healthcare sector's perfor-mance has historically been negatively correlated to bond yields.

Report structureOver the next few pages we provide background on cancer, the oncologymarket, and the most exciting new technologies in development. Weinclude a more detailed discussion of recent developments in the field inthe appendices that follow.

Box 1: Private market investments in oncology, by

Cyril Demaria (analyst, UBS Switzerland AG)

Long-term investors willing to accept a certain level of

illiquidity can gain exposure to oncology through private

markets, specifically through early-stage venture capital

funds. Oncology venture investments clearly demonstrate

the potential for attractive returns as well as social

impact, with the objective of more effective and less

painful patient care through predictive medicine, inno-

vative means of treatment delivery and genomic therapies

and vaccines. Investment in this area is largely focused at

earlier stages of development, as larger corporations are

increasingly outsourcing exploration of such innovations

to start-up entities rather than developing them in house,

and only at later stages acquiring or partnering with those

with the most promising products. Few venture capital

managers are exclusively focused on oncology due to the

highly specialized knowledge required, instead focusing

more broadly on healthcare or biotechnology. Over the

past 12 years, 751 funds made at least one investment

in the oncology sector according to Pitchbook, while only

125 funds made 10 or more. Preqin only identifies three

managers focusing exclusively on this area.

Box 2: Link to sustainable investing

Investing in oncology therapeutics fits our sustainable

investing framework. Despite significant advances, cancer

remains a leading cause of death and generates among

the highest costs to healthcare systems around the globe.

As with many serious diseases, the economic burden of

cancer far exceeds the direct cost of treating the disease.

Investing in oncology could help to reduce this rising

cost to society. For more information about the UBS

Sustainable Investing framework, please see our report

"Adding value(s) to investing" published in March 2015.

Equity markets

UBS CIO WM 14 August 2015 2

Oncology basics

Cancer is a leading cause of death and generates among the highest coststo healthcare systems around the globe. According to the World CancerReport 2014, published by the World Health Organization (WHO), over14 million new cases of cancer (excluding non-melanoma skin cancers)and over eight million cancer deaths occurred globally in 2012. The WHOfurther estimated the annual global financial cost of cancer at USD 1.16trillion in 2010, with the cost and occurrence expected to rise steadily giventhe ever aging population worldwide.

Cancer starts when cells, for genetic, environmental (e.g., sun exposure),life-style (smoking, diet) or even unknown factors, become abnormal andgrow out of control. Some cancers, like leukemias and lymphomas, affectthe blood stream and blood-forming organs, while other cancers invadenormal tissues and can spread throughout the body.

The most common types of cancer in men are lung, prostate, colorectal andstomach cancer, and in women breast, colorectal, lung and cervical (Fig. 1),although less severe forms of skin cancer would dominate if also taken intoaccount. These cancers, along with blood-borne cancers like leukemia andlymphoma, are among the largest therapeutic markets for pharmaceuticaland biotechnology companies today.

There are over 100 forms of cancer, each with its own biological andlife-altering characteristics. Treatment often requires multiple rounds ofvarious combination therapies — surgery, chemotherapy, immunotherapy,targeted drug therapy, etc. — to modify disease progression, which com-monly means increasing life expectancy by a matter of months.

Given the complexity of the disease, it is unlikely that we will ever finda "golden bullet" that cures cancer. However, scientific progress in bothdiagnosis and treatment has led to a better outlook for cancer patients overthe past few decades. According to the American Cancer Society, the 5-yearsurvival rate for all cancers diagnosed between 2004 to 2010 increased to68%, up from 49% in 1975 to 1977. While there are some notable successstories, such as prostate and breast cancer, survival rates for some hard-to-treat cancers remain low. Five-year relative survival rates for lung cancer are18%, compared to 12% 40 years ago, while pancreatic cancer five-yearsurvival is just 7% for patients diagnosed between 2004-10, as comparedto 3% for patients diagnosed between 1975-1977. Clearly, the need fornew and better treatments for these cancer types is as great as ever.

Fig. 1: Cancer in the US: Incidence, prevalenceand five-year survival ratesA) Incidence - new cancer cases in 2015

-

50,000

100,000

150,000

200,000

250,000

Bre

ast

Lung

Pros

tate

Col

orec

tal

Sto

mac

h

Blad

der

Mel

ano

ma

No

n-H

odgk

in

Thyr

oid

Kid

ney/

Ren

al

End

omet

rial

Leuk

emia

Panc

reas

Mye

lom

a

Ova

rian

Cer

vica

l

B) Prevalence - patients living with cancer

-

500,000

1,000,000

1,500,000

2,000,000

2,500,000

3,000,000

Bre

ast

Pro

stat

e

Co

lore

ctal

Mel

ano

ma

Endo

met

rial

Thyr

oid

Blad

der

No

n-H

odgk

in

Lung

Kid

ney/

Ren

al

Leuk

emia

Cer

vica

l

Ova

rian

Mye

lom

a

Sto

mac

h

Panc

reas

C) Five-year survival rates

0%

20%

40%

60%

80%

100%

Pros

tate

Thyr

oid

Mel

anom

a

Brea

st

Endo

met

rial

Blad

der

Kid

ney/

Rena

l

Non

-Hod

gkin

Cer

vica

l

Col

orec

tal

Leuk

emia

Mye

lom

a

Ova

rian

Stom

ach

Lung

Panc

reas

Note: Incidence - number of new cases estimated in 2015; Prevalence -cumulative number of patients alive with the disease based on 2012 dataSource: National Cancer Institute, SEER database, UBS

Equity markets

UBS CIO WM 14 August 2015 3

New cancer treatments

Much of the recent excitement in cancer treatment stems from advancesin the field of T-cell mediated immunotherapies. These include checkpointinhibitors and related immuno-oncology drugs, as well as personalizedtreatment options including CAR-T therapy and cell therapy. We explorethese treatment options in more detail below.

Cancer treatment evolved slowly until the last two decadesIn ancient times, as is common today, many cancers are first treated byattempting to remove malignant tumors surgically (Fig. 2). The result,however, can be temporary as the tumor often grows back. For thisreason, there is a pervasive belief that cancer cannot be cured; however,there are many more cancer treatment options beyond surgery. In the late19th century, radiation (x-rays) was discovered and subsequently used incancer treatment. Also in the 19th century, the effect of specific hormoneson certain cancers was discovered, establishing the groundwork for themodern use of hormone therapy that took off in the 20th century. DuringWorld War II, the impact of particular chemicals on cancer was observed,which translated into the development of the first chemotherapies.

These treatment options — surgery, radiation, hormone therapy andchemotherapy — remain prevalent today, but much more effective treat-ments, with better survival outcomes and improved quality of life, havecome to the fore. During the second half of the 20th century, the under-standing of the immune system and the biology of cancer advanced signif-icantly and led to what we now call immunotherapy. Initially this includedbiotechnological development of substances like interferons, interleukins,and other cytokines aimed at boosting a patient's immune system.

Around the turn of the millennium, this approach was followed by thedevelopment of techniques that identified specific tumor targets and aimedantibodies at these tumors, thereby hindering tumor growth. These so-called recombinant monoclonal antibodies are now used routinely in cancertherapy, often in combination with older cancer therapies, and have led tobetter survival rates and improved quality of life.

T-cell mediated immuno-oncologyMore recently, a better understanding of cancer cell biology and theimmune system has led to the development of immuno-oncology, anapproach that uses the body's immune system to fight cancer. As wellas significantly reducing the burden of side effects, immuno-oncologytreatment offers the hope of more durable responses to treatment thanconventional therapy. So far, results in lung cancer and melanoma haveconfirmed a survival benefit compared to previous treatments, but it is stilltoo early to determine just how durable the responses to treatment will bein the real world.

The first classes of immuno-oncology drugs to reach the market are knownas checkpoint inhibitors. These drugs are designed to block the cancer'sability to defend itself from attack by the patient's immune system. Specif-ically, Bristol-Myers Squibb's Yervoy (a CTLA-4 inhibitor) was approvedto treat melanoma in 2011, and two PD-1 inhibitors have more recentlyreached the market (Bristol's Opdivo approved for melanoma in December2014 and lung cancer in March 2015, and Merck & Co's Keytruda approvedfor melanoma in September 2014). Combined, sales of these two drugsare already annualizing at over USD 1 billion.

Fig. 2: The evolution of cancer treatmentSeveral advances beyond traditional cancertreatment

Ancient times

Surgery

1900'sRadiation

1940's

Hormone therapy

1950's

Chemotherapy

2000'sImmunotherapy: recombinant monoclonal antibodies

Since2013

T-cell mediated immunotherapy: Checkpoint inhibitors

Targeted therapies

Next?Personalized immunotherapy: CAR-T

Source: UBS

Fig. 3: The hope for immuno-oncologyLong, durable responses could transform survivalrates

Source. Credit Suisse, UBS. Note: for illustration only, not based on actualdata

Equity markets

UBS CIO WM 14 August 2015 4

These drugs are rapidly establishing themselves as the standard of care inmelanoma and lung cancer, and generating widespread interest with bothphysicians and investors due to:

• An impressive impact on survival in lung cancers and melanoma.For example, melanoma progression-free survival has improved fromtypically just a few weeks with traditional chemotherapy, to 2.9months with Yervoy, 6.9 months with Opdivo, and more recently 11.5months using Opdivo and Yervoy in combination.

• A significantly improved safety profile compared to traditionalchemotherapy.

• The wide breadth of tumor types potentially amenable totreatment including renal carcinoma, hepatocellular carcinoma, headand neck cancer, Hodgkin's lymphoma, as well as ovarian, bladder andstomach cancer, and the hard-to-treat triple-negative breast cancer.

Following presentation of early data at the recent American Society ofClinical Oncology meeting in June 2015, we expect large-scale clinical trialsof these and other immuno-oncology drugs in a wide variety of indicationsto be published over the next 1-3 years, substantially de-risking market esti-mates of the drugs' sales. (See Appendix 1 for a more detailed discussionof how checkpoint inhibitors are revolutionizing lung cancer treatment.)

It is important to note that these drugs still only represent the first waveof immuno-oncology products, however, with an alphabet soup of newapproaches at earlier stages of development including IDO inhibitors,OX-40, CD137, anti-GITR, anti-KIR and other mechanisms of action. Theseand other drugs are also likely to be explored in combination with thecheckpoint inhibitors.

However, despite the impressive improvement in survival seen so far withcheckpoint inhibitors, these treatments do not yet represent a “cure” forcancer. One area of development that could offer such a hope, admittedlyonly in limited circumstances, is the development of personalized cellularimmunotherapy including CAR-T treatment and T-cell receptors.

CAR-T and novel personalized therapiesNew developments in T-cell engineering technology hold out the promise ofpersonalized cellular immunotherapy, i.e. using a patient’s immune cells toattack cancer. One such approach, chimeric antigen receptor T-cells (CAR-T), has shown remarkable but early evidence of efficacy in leukemia andmay have applications in solid tumors.

CAR-T treatment combines the cytotoxic (i.e. cell-killing) ability of T-cells(a type of white blood cell responsible for fighting infections) with the tar-geted nature of monoclonal antibodies. Treatment involves a three-stepprocess (Fig. 4):

1. T-cells are removed from the body

2. The T-cells are engineered to recognize the relevant cancer target

3. Engineered T-cells (CAR-T's) are reintroduced to the patient where theymultiply and attack the targeted cancer cells

Novartis could be the first to market with a CAR-T therapy: its CAR-Tproduct CTL019 produced complete remissions in 27 out of 30 leukemiapatients in a Phase 2 trial, with 78% of patients still alive after six months.

Fig. 4: CAR-T involves a three-step processKey steps in treatment

Source: Kepler Cheuvreux, UBS

Equity markets

UBS CIO WM 14 August 2015 5

These data are promising, but still early stage, and a number of issuesneed to be resolved before CAR-T therapy becomes a commercial reality.We expect safety profile to be a key challenge, particularly in solid tumorindications, due to the significant impact of CAR-T treatment on thepatient's immune system. Additionally, the nature of CAR-T treatment alsointroduces technical hurdles in manufacturing, notably consistency andsecurity of supply, since each treatment is unique to a single patient. Never-theless, if these challenges can be overcome, the potential for personalizedimmunotherapies is great, in our view.

Alternative approachesIn addition to the personalized (or "autologous") approach describedabove, a number of companies are investigating “off-the-shelf” methodsthat do not need to be personalized:

• Universal chimeric antigen receptors (UCAR-T’s) are derived froma healthy donor’s T-cells, and engineered in such a way that they canbe used to treat any patient. Pfizer is exploring this process with Frenchbiotech Cellectis. UCAR-T’s would have the benefit of scalability andfaster treatment compared to the autologous approach.

• Bispecific T-cell engagers (BiTE) are antibodies that bind to both aspecific tumor cell and a T-cell, to direct the patient’s immune systemto the cancer. Amgen’s Blyncyto (blinatumomab), approved to treatacute lymphoblastic leukemia, is an example of BiTE technology. Thusfar, data in ALL suggest that CAR-T has higher efficacy than the BiTEapproach, albeit at the cost of much worse side effects.

• Biotech company Kite Pharma is developing engineered T-cellreceptors (TCR’s) capable of targeting antigens inside, as well as onthe surface of, tumor cells. This method could potentially be useful intreating solid tumors.

• Antibody-coupled T-cell receptors (ACTR’s) are re-engineered T-cells designed to be used alongside monoclonal antibodies.

In the following appendices, we describe in more detail the current state ofplay in lung cancer (see Appendix 1), where the new checkpoint inhibitorsare fast becoming standard of care, and outline important recent develop-ments in other cancer types (see Appendix 2). In Appendix 3, we list a widerange of cancer therapeutics in development, while Appendix 4 providesdefinitions of terms and acronyms used in this report.

Equity markets

UBS CIO WM 14 August 2015 6

Appendix 1: Immuno-oncology could revo-lutionize lung cancer treatment

Lung cancer is one of the largest markets in oncology and a major focus fordevelopment of immuno-oncology (IO) drugs. The National Cancer Institute(NCI) estimates there will be 221,200 new cases of lung cancer in the US in2015, the second-highest cancer incidence in the US. Non-small cell lungcancer (NSCLC) comprises 85% of lung cancer cases, out of which 70% ofNSCLC cases are the non-squamous histology. Small cell lung cancer (SCLC)and mesothelioma (related to asbestos) make up the remainder of cases(Fig. 5).

Since the approval of Bristol-Myers Squibb’s (Bristol-Myers) Opdivo forsecond-line lung cancer in March 2015, immuno-oncology has rapidlyestablished itself as the standard of care in second-line lung cancer. Weexpect Bristol-Myers to remain the leader in the second-line setting, givenits competitive clinical data and first-to-market status, although we seeMerck & Co (Merck) as catching up and think the market underestimatesthe potential for Keytruda in this setting, especially with Keytruda’s moreconvenient dosing regimen.

While the initial development of IO drugs in lung cancer has concentratedon later lines of therapy, ultimately the majority of the market will be infirst-line disease. Here our initial assessment is that Roche has the earlyadvantage with its chemotherapy combination strategy. However, much isstill to be proven in the data.

Second-line treatment: monotherapy and combinationsThus far, Bristol-Myers’ Opdivo is the only PD-1 or PD-L1 therapy approvedfor lung cancer, having received FDA approval in March 2015 and Europeanapproval in July for previously-treated squamous NSCLC. We expect Bristol-Myers to file the drug imminently for the larger non-squamous indication,which could see it approved during 2H15. However, Merck has alreadyfiled Keytruda in this indication and should receive approval in October2015. Clinically, we view the two drugs as having minimal differentiation,although Keytruda has a more favorable dosing regimen (every three weeksversus every other week with Opdivo).

Roche looks up to a year behind with its PD-L1 atezolizumab, which islikely to be filed in early 2016 and approved in 2H16. AstraZeneca’s PD-L1durvalumab monotherapy data have disappointed and the company lookslate-to-market with an undifferentiated product in this setting. Merck KGaAand Pfizer’s PD-L1 avelumab looks even later and less differentiated.

However, while Bristol-Myers has generally had poor results with PD-1+ CTLA-4 combination (Opdivo + Yervoy), AstraZeneca appears to havesolved the difficulty of finding a suitable dose for its equivalent combinationof durvalumab + tremelimumab in third-line lung cancer, showing a 27%overall response rate in third-line patients treated with the combination.This may give AstraZeneca an option to bring the drug to market earlierthan 2017.

Fig. 5: Lung cancer incidence by typePercent of new cases

Non-squamous

NSCLC60%Squamous

NSCLC25%

SCLC andmesothelioma

15%

Source: UBS. Note: NSCLC - non-small cell lung cancer; SCLC - small celllung cancer

Identifying patients using biomarkersEmerging data suggests that, in most cancer types except squamousNSCLC, patients whose tumors express a high level of PD-L1 are morelikely to benefit from treatment with checkpoint inhibitors. This raises thequestion whether all NSCLC patients should be treated with PD-1’s/PD-

Equity markets

UBS CIO WM 14 August 2015 7

L1’s or if non-squamous patients should be tested for PD-L1 status priorto treatment. So far, opinions from doctors in the field appear to favorBristol-Myers' “treat all comers” approach, at least in the less cost-con-scious US market. However, as alternative PD-1’s/PD-L1’s come to market,and companion diagnostics are improved and require less invasive biopsies,we would expect to see greater use of PD-L1 status in the treatment algo-rithm. This is likely to be especially true in the price-sensitive Europeanmarket, where government payers may not be prepared to spend nearlyUSD 100,000 for a course of treatment without some indication of its likelysuccess. In the meantime, the jury is out.

Moving into first-line diseaseUltimately the largest commercial opportunity is likely to be treating first-line NSCLC. Being first to market and establishing a drug as standard of caresignificantly raises the bar for approval of other therapies. Also, patientsfor whom initial treatment with a PD-1 or PD-L1 regimen is ineffective areunlikely to receive a similar drug in the second-line setting, in our view. Thiswill potentially decrease the size of the second-line market once PD-1/PD-L1’s move into first-line treatment. Our initial assessment is that Roche ispotentially in the lead here, based on superior efficacy when used in com-bination with chemotherapy, although all companies’ studies are relativelyearly-stage and a full assessment is not yet possible.

As in second-line disease, there are also differences in developmentstrategies in the first-line NSCLC setting. Roche, which has shown the mostpromising data so far, is concentrating on chemotherapy combinations.By contrast Bristol-Myers is pursuing both monotherapy and combinationstudies with its CTLA-4 drug Yervoy. AstraZeneca is also progressing witha CTLA-4 combination, using its own tremelimumab, although its primaryfocus appears to be on PD-L1 negative patients, an otherwise under-servedmarket niche.

Early data from Roche show a 67% response rate across all comers in first-line NSCLC when used in combination with chemotherapy. These results areunprecedented compared to historical response rates for chemotherapy inthe 30% range and a response rate of 43% across all lung cancer patientsfor Merck's Keytruda when used in combination with chemotherapy. Theyalso compare favorably with chemo combination data from Bristol-Myers,which has been relatively poor thus far, suggesting that PD-L1’s work betterin combination with chemotherapy than PD-1’s.

We expect data from Roche’s three phase 3 trials (all comers, using dif-ferent chemo combinations) in first-line NSCLC to become available in2017. In addition, Roche is running two phase 3 trials with atezolizumabmonotherapy (in PD-L1 positive patients), which could allow it to positionthe drug in elderly patients not suitable for chemotherapy, although thesedata are unlikely to be available before 2018. Merck, which is expected tobegin similar phase 3 Keytruda and chemo combination trials soon, appearsto be running behind Roche.

While Bristol-Myers is launching a large phase 3 program in first-lineNSCLC, it will not include a chemotherapy combination, although it willinclude a combination with Yervoy. Given the previous data for this combi-nation, we are somewhat cautious on the outcome at present.

Equity markets

UBS CIO WM 14 August 2015 8

Appendix 2: Recent developments in clas-sical oncology, targeted and other treat-ments

Beyond the progress in new immunotherapies described above, many com-panies are still making important developments in classical oncology (hor-monal, chemotherapy and targeted antibodies). New drugs are in clinicaltrials across a range of tumor types that could contribute to longer survivaltimes, or better quality of life, for patients. This area remains a significantopportunity for pharmaceutical and biotechnology companies. Below weoutline some key recent developments, organized by tumor type.

Breast cancer

Breast cancer is the most commonly diagnosed cancer in women, with theNational Cancer Institute estimating 231,800 new cases will occur in theUS in 2015. Breast cancer is classified and treated based on the presence orabsence of hormone receptors (estrogen or progesterone receptor positiveor negative) and whether tumor cells over-express the HER2-neu receptor.Hormone receptor positive tumors represent around two thirds of breastcancer cases, HER2-positive but hormone receptor negative cases accountfor 10-15%, and the remainder are known as triple negative breast cancer(Fig. 6). This type of cancer is particularly difficult to treat.

Puma adjuvant data good in HER2+/HR+ patientsPuma presented two-year extended adjuvant (post-surgery) data in HER2-positive (HER2+) breast cancer patients at ASCO. The phase 3 ExteNETtrial showed a bigger absolute benefit in HER2+ patients who were alsohormone receptor-positive (HR+); however, the HR-negative subset was dis-appointing, as were lymph node negative patients. Overall we think thedata reinforce that the effect was driven by the HR+ patients, which pro-vides a USD 1.5-2.0 bn opportunity for the drug. Still, the three-year follow-up ExteNET data, expected to be released late this year, will be criticalto the market opportunity in adjuvant. Regardless, we believe neratinib isapprovable on the two-year data, most likely in 2016.

Puma neoadjuvant data expected this yearThe NSABP (National Surgical Adjuvant Breast and Bowel Project) is con-ducting the FB-7 neratinib neoadjuvant (presurgery) trial, with toplineexpected at any time (although already delayed) and detailed data expectedlate in the year. While this trial is not controlled or conducted by Puma, theoutcome will be important to neratinib sales. We believe that FB-7 coulddemonstrate that neratinib (in combination with Taxol) could prove to bebetter than Roche's Herceptin or Perjeta combination in the neoadjuvantsetting; another major opportunity for Puma.

Pfizer's Ibrance off to a strong start in ER+/HER2- breast cancerPfizer's Ibrance, a first-in-class CDK 4/6 inhibitor for the treatment of ER+/HER2- breast cancer, has shown a relatively rapid sales ramp. More recentdata has demonstrated that adding Ibrance to the current standard of caremore than doubled the time to disease progression (9.2 months vs 3.8months) We await long-term Ibrance trials to evaluate its overall survival(OS) benefit and ultimate potential, but place the preliminary potential ofCDK-4/6 agents in excess of USD 10bn after 2020.

Fig. 6: Breast cancer incidence by typePercent of new cases

HR positive,HER2 negative

43%

HR positive,HER2 positive

22%

HER2 positive,HR negative

15%

Triple negative20%

Source: UBS. Note: HR - hormone receptor; HER2 - HER2-neu receptor

Equity markets

UBS CIO WM 14 August 2015 9

Eli Lilly and Novartis also have CDK 4/6 drug candidates, both in phase 3,with possible market introductions in 2017. While these competing drugsare clearly a threat to Ibrance, the post-menopausal ER+/HER2– advancedbreast cancer opportunity is large. It is still too early to determine theultimate winner in the CDK 4/6 inhibitor class.

Medivation's Xtandi works in triple-negative breast cancer (TNBC)Medivation's anti-androgen Xtandi, which has exceptionally high potentialin prostate cancer (see below), has now also demonstrated early successin TNBC, an extremely hard-to-treat cancer. Xtandi's clinical benefit ratewas 35% in early studies, although very few (6-8%) had a complete orpartial response; still, most of these patients demonstrated stable diseaseover a 24-month period, which is better than other therapies. With addi-tional studies, regulatory approval for this indication is possible by 2017.

Leukemia and lymphomas

Leukemia, lymphoma and myeloma (discussed below) are cancers of theblood and plasma cells. Leukemias are tumors in circulating blood, whilelymphomas are tumors of the lymph nodes. There are a number of dif-ferent types of each, with varying treatment and prognosis. The NationalCancer Institute estimates there will be approximately 54,000 new casesof leukemia in the US in 2015. The most common subtype is chronic lym-phocytic leukemia (CLL) which, while generally not curable, has relativelyhigh survival rates with most patients living longer than 10 years post-diagnosis. The majority of lymphoma cases are non-Hodgkin's lymphoma(NHL), with an estimated 71,850 new cases in the US in 2015. NHL canbe further broken down into diffuse large B-cell lymphoma (DLBCL), fol-licular lymphoma (FL) and mantel cell lymphoma (MCL), with DLBCL themost common.

Abbvie is building a fortress in leukemia/lymphoma therapiesInfinity's PI3K inhibitor (duvelisib), partnered with AbbVie, has demon-strated excellent early efficacy in chronic lymphocytic leukemia (CLL) andhas potential in other leukemias and lymphomas. Its early data are atleast comparable to Gilead's Zydelig and AbbVie's Btk inhibitor Imbruvica(recently acquired through AbbVie's Pharmacyclics acquisition). To date,Imbruvica has demonstrated the highest single-agent efficacy in CLL andwill likely be approved for front-line CLL within two years. Furthermore,potential combination with AbbVie's own venetoclax (ABT-199) and/or duvelisib could completely change treatment paradigms for variousleukemias and lymphomas later this decade.

Celgene's Revlimid is moving beyond myelomaCelgene, together with its partner Roche, has recently demonstrated thata surrogate endpoint (complete response at 30 months) could be accu-rately used to predict progression-free survival (PFS) in first-line follicularlymphoma (FL; a type of non-Hodgkin lymphoma) instead of conductingthe protracted studies otherwise necessary to prove PFS in this form oflymphoma. If the FDA accepts this endpoint, Revlimid (in combinationwith Roche's Rituxan) could be on the market for FL much sooner (dataexpected in 2017) and the R-squared combination could become the newstandard of care in FL, just like other Revlimid combinations in myelomatoday. Celgene also recently announced a collaboration with AstraZenecato develop Astra's PD-L1 in hematological cancers.

Equity markets

UBS CIO WM 14 August 2015 10

Multiple myeloma

Multiple myeloma is a cancer of the plasma cells, where the cells interferewith the production of normal blood cells in the bone marrow. There will bean estimated 26,850 new cases of myeloma in the US in 2015, accordingto the National Cancer Institute. Treatment advances have improved theprognosis for myeloma patients, but the five-year relative survival rate is stillthe lowest of the major hematologic cancer groups at 47%.

Amgen's Kyprolis added to relapsed myeloma regimenAmgen's Kyprolis has demonstrated perhaps the best efficacy (based onprogression free survival) compared to all other phase 3 relapsed myelomatrials, and some have even suggested that Kyprolis, together with Celgene'sRevlimid and old-line drug dexamethasone (together known as KRd), is nowthe new "standard of care" for relapsed myeloma. Further, recent phase2 study results with KRd given in front-line myeloma (with stem cell trans-plant) suggest that the addition of Kyprolis could ultimately translate intobetter survival outcomes in the front-line setting; a large potential oppor-tunity for Amgen. However, the drug's side effect—higher cardiac, hyper-tension and dyspnea (labored breathing) events—and its required twice-weekly dosing could limit its use.

New myeloma therapeutics on the horizonWhile Celgene's Revlimid is still the backbone of nearly all drug regimensfor myeloma, there are a number of new drugs beyond Kyprolis in thelater stage of development in combination with Revlimid for this life-threat-ening condition. AbbVie and Bristol-Myers' CS1 antibody (elotuzumab)has shown early data that is comparable to Kyprolis, with better dosing(once a week vs. twice a week; both IV formulations). Physicians are alsoencouraged by the potential of new CD38 antibody agents, with Johnson& Johnson (J&J)/Genmab's daratumumab in the lead: phase 3 relapsed-refractory myeloma studies are expected to complete in 2017. Also, Takedahas recently reported good results in a phase 3 trial for its proteasomeinhibitor (ixazomib), a follow-on to its drug Velcade (marketed by J&J inthe US).

Prostate cancer

The National Cancer Institute estimates there will be 220,800 new cases ofprostate cancer in the US in 2015, making it the highest incidence canceramong men. Survival rates are generally high due to improved diagnosis,but the outlook for late-stage prostate cancer remains poor with a 28%five-year survival rate for patients whose cancer has spread beyond nearbylymph nodes (the so-called M1 category).

Medivation's Xtandi is the one to watch in prostate cancerIn January, Medivation announced results of its eagerly anticipatedTERRAIN study of anti-androgen Xtandi in pre-chemotherapy M1 prostatecancer patients. Xtandi showed a nearly three-fold improvement in pro-gression-free survival (PFS) compared to old-line drug Casodex (15.7months vs 5.8 months). Then in April, Medivation announced that itsSTRIVE study showed even more impressive PFS results in comparison toCasodex (19.4 months vs 5.7 months) in M0 patients (ie. those for whomcancer has not spread beyond lymph nodes) or M1 patients. This opens upa major market opportunity for Xtandi.

Equity markets

UBS CIO WM 14 August 2015 11

At Xtandi's current price and Casodex's current duration of treatment (sixmonths), conversion of Casodex prescriptions to Xtandi would translateinto US sales of about USD 4bn a year. If the average duration doubledto about 12 months, then full conversion of current Casodex prescriptionscould translate into sales of USD 8bn/year.

Ovarian cancer

The National Cancer Institute estimates that approximately 21,300 womenwill be diagnosed with ovarian cancer in the US in 2015. Ovarian cancer isdifficult to treat with five-year survival rates of around 46%.

New drugs advance in ovarian cancer developmentAs noted above, early studies with Merck KGaA/Pfizer's PD-L1 (avelumab)and Merck & Co's PD-1 (Keytruda) both demonstrated an 11% overallresponse rate in late-stage patients; a low but nevertheless impressive resultgiven the difficult-to-treat patient set. In addition to these developments,PARP inhibitors are also advancing. Clovis recently presented results of twophase 2 studies showing fairly high response rates with its PARP (rucaparib)in ovarian cancer patients with BRCA mutations and in BRCA-like patients.Clovis has a leading position within PARP development, with Tesaro also inthe later stages of development with its PARP (niraparib), for which phase3 data in germline negative BRCA ovarian cancer is expected by year end,while a phase 3 in BRCA-positive breast cancer is ongoing. AbbVie's veli-parib and BioMarin's BMN-673 are other PARP inhibitors in development.AstraZeneca's PARP (Lynparza) is already on the market for BRCA-mutatedovarian cancer.

ImmunoGen's ADC also delivered early signs of efficacy. ImmunoGen'santibody drug conjugate (ADC), which combines a folate receptor alpha(FRα) targeting monoclonal antibody with chemotherapy agent DM4,showed good, but very early data in FRα-positive ovarian cancer. While earlydata are encouraging, we look to additional updates in ovarian cancer, notexpected until ASCO 2016 (June 2016), to better frame the overall clinicalprofile of this ADC.

Pancreatic cancer

Pancreatic cancer is one of the most difficult to treat and has the lowestsurvival rate (7% five-year relative survival) of major cancers. The NationalCancer Institute estimates approximately 49,000 new cases of pancreaticcancer will be diagnosed in the US in 2015.

Halozyme's PEGPH20 holds promise in pancreatic cancerPEGPH20 is a pegylated enzyme (which prolongs circulation time) thatbreaks down the protective "halo" (hyaluranan) surrounding certain cancercells and permits greater effectiveness of cancer therapeutics. In an interimphase 2 study, Halozyme's drug showed good overall response rates(73% of patients or 52% using more conservative measures), which couldtranslate into a survival benefit. While cardiovascular events are a con-cerning side effect, recent data showed a lower rate of events after a studyprotocol change. In 2016, Halozyme expects to reveal completed phase2 results and initiate phase 3. Though market approval may not occuruntil 2018, clinical success for PEGPH20 would be highly promising forHalozyme.

Equity markets

UBS CIO WM 14 August 2015 12

Appendix 3: Major cancer treatments in developmentSome of the promising pharmaceuticals and biologics for oncology in development currently

Cancer area Treatment approach Company Molecule Clinical status

Immuno-oncology PD-1 inhibitors Merck & Co. Keytruda (pembrolizumab)Mktd (2L melanoma)/P3 (lung,head/neck, gastric, CRC, others)

Bristol-Myers Squibb Opidivo (nivolumab)Mktd (2L melanoma, NSCLC)/P3(renal, Hodkins, gastric others)

AstraZeneca AMP-514/MEDI0680 P1PD-L1 inhibitors Roche atezolizumab (MPDL-3280) P3 (lung, bladder, others)

AstraZeneca durvalumab (MEDI4736)P3 (lung, bladder, gastric, pancreaticcancer, head/neck

Merck KGaA/Pfizer avelumab (MSB0010718C) P2 (lung, ovarian)Bristol-Myers Squibb BMS-936559 P1

CTLA-4 inhibitors Bristol-Myers Squibb Yervoy (ipilimumab)Mktd (melanoma)/P3 (lung); Alsodeveloping with PD-1s

AstraZeneca tremelimumabP3 (lung, melanoma, and incombination with PD-L1)

Checkpoint inhibs-Other Bristol-Myers Squibb anti-KIR, Anti-LAG3 P2Roche RG7155 (CSF1R) P2Various companies Anti-GITR, Anti-OX40, P1

PF-2566 (CD-137), TGF-ßR2CSF1R mAB

IDO modulator Incyte IDO modulator P2CAR-T therapy Novartis, Juno/Celgene, Various hemotologic and P1/2

Kite/Amgen, Bellicum, solid tumors beingbluebird (w/Celgene for MM) investigated

Ziopharm/Intrexon

Cancer vaccines Bavarian Nordic Prostvac P3 (prostate cancer)Roche/Immatics IMA942 P1

Inovio INO-5150, Immatics P1

Leukemias, lymphomas CD20 ant ibodies Roche Rituxan (rituximab)Mktd (various lymphomas,leukemias, other)

Roche Gazyva Mktd (CLL)/P3 (NHL)Novartis Arzerra Mktd (CLL)/P3 (NHL)

Btk inhibitors AbbVie /J&J Imbruvica (ibrutinib)Mktd (CLL, MCL, WM)/P3 (NHL, solidtumors, RA)

Celgene CC292 P2Ono ONO-4059 P1

PI3K inhibitors Gilead Sciences Zydelig (idelalisib) Mktd (CLL, iNHL)/P3 (NHL)Bayer copanlisib P3 NHL

Infinity/AbbVie duvelisibP2 (relapsed/refractory iNHL, CLL,others)

Bcl-2 Inhibitor AbbVie/Roche venetoclax (ABT-199) P3 (CLL, NHL)CD19 ant ibodies (BiTE) Amgen Blincyto (blinatumomab) Mktd (relapsed/refractory ALL)

Sanofi SAR3419 P2BCR-Abl (TKI) inhibitor Novartis Gleevec Mktd (Ph+ CML, GIST)

Novartis Tasigna Mktd (Ph+ CML)Bristol-Myers Squibb Sprycel Mktd (Ph+ CML, Ph+ ALL)Ariad Iclusig Mktd (CML, Ph+ ALL)

CD40 ant ibody Roche Anti-CD40 P2 (NHL-DLBCL)

CD137 ant ibody Pfizer Anti-CD137 P2 (relapsed/refractory NHL)

Mult iple myeloma (MM) IM iDs (immunomodulatory Celgene Revlimid (lenalidomide)Mktd (multiple myeloma, MDS)/P3(NHL)

drug) Celgene Pomalyst (pomalidomide)Mktd (relapsed/refractory multiplemyeloma)

Proteasome inhibitor Takeda/J&J Velcade (bortezomib)Mktd (relapsed/refractory multiplemyeloma)

Amgen/Onyx Kyprolis (carfilzomib)Mktd (relapsed/refractory multiplemyeloma)

Takeda ixazomib (MLN-9708) P3 (multiple myeloma)CD38 ant ibodies J&J/Genmab daratumumab P3 (multiple myeloma)

Sanofi SAR650984 P3 (multiple myeloma)Celgene MOR202 P3 (multiple myeloma)

CS1 ant ibody AbbVie/Bristol-Myers elotuzumab P3 (multiple myeloma)

(T-cell mediated treatmentfor numerous cancers,

including lung, melanoma,bladder, head & neck,kidney/renal, others)

Source: UBS

Equity markets

UBS CIO WM 14 August 2015 13

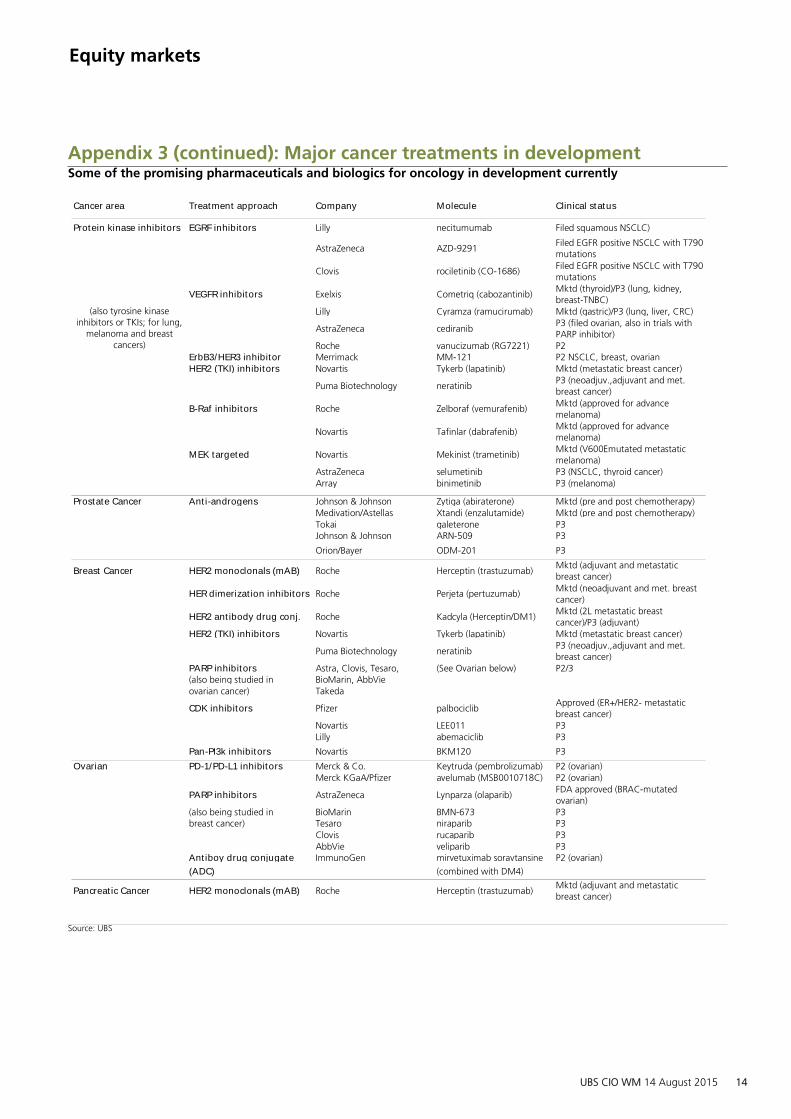

Appendix 3 (continued): Major cancer treatments in developmentSome of the promising pharmaceuticals and biologics for oncology in development currently

Cancer area Treatment approach Company Molecule Clinical status

Protein kinase inhibitors EGRF inhibitors Lilly necitumumab Filed squamous NSCLC)

AstraZeneca AZD-9291Filed EGFR positive NSCLC with T790mutations

Clovis rociletinib (CO-1686)Filed EGFR positive NSCLC with T790mutations

VEGFR inhibitors Exelxis Cometriq (cabozantinib)Mktd (thyroid)/P3 (lung, kidney,breast-TNBC)

Lilly Cyramza (ramucirumab) Mktd (gastric)/P3 (lung, liver, CRC)

AstraZeneca cediranibP3 (filed ovarian, also in trials withPARP inhibitor)

Roche vanucizumab (RG7221) P2ErbB3/HER3 inhibitor Merrimack MM-121 P2 NSCLC, breast, ovarianHER2 (TKI) inhibitors Novartis Tykerb (lapatinib) Mktd (metastatic breast cancer)

Puma Biotechnology neratinibP3 (neoadjuv.,adjuvant and met.breast cancer)

B-Raf inhibitors Roche Zelboraf (vemurafenib)Mktd (approved for advancemelanoma)

Novartis Tafinlar (dabrafenib)Mktd (approved for advancemelanoma)

MEK targeted Novartis Mekinist (trametinib)Mktd (V600Emutated metastaticmelanoma)

AstraZeneca selumetinib P3 (NSCLC, thyroid cancer)Array binimetinib P3 (melanoma)

Prostate Cancer Ant i-androgens Johnson & Johnson Zytiga (abiraterone) Mktd (pre and post chemotherapy)Medivation/Astellas Xtandi (enzalutamide) Mktd (pre and post chemotherapy)Tokai galeterone P3Johnson & Johnson ARN-509 P3

Orion/Bayer ODM-201 P3

Breast Cancer HER2 monoclonals (mAB) Roche Herceptin (trastuzumab)Mktd (adjuvant and metastaticbreast cancer)

HER dimerizat ion inhibitors Roche Perjeta (pertuzumab)Mktd (neoadjuvant and met. breastcancer)

HER2 ant ibody drug conj. Roche Kadcyla (Herceptin/DM1)Mktd (2L metastatic breastcancer)/P3 (adjuvant)

HER2 (TKI) inhibitors Novartis Tykerb (lapatinib) Mktd (metastatic breast cancer)

Puma Biotechnology neratinibP3 (neoadjuv.,adjuvant and met.breast cancer)

PARP inhibitors Astra, Clovis, Tesaro, (See Ovarian below) P2/3(also being studied in BioMarin, AbbVieovarian cancer) Takeda

CDK inhibitors Pfizer palbociclibApproved (ER+/HER2- metastaticbreast cancer)

Novartis LEE011 P3Lilly abemaciclib P3

Pan-PI3k inhibitors Novartis BKM120 P3

Ovarian PD-1/PD-L1 inhibitors Merck & Co. Keytruda (pembrolizumab) P2 (ovarian)Merck KGaA/Pfizer avelumab (MSB0010718C) P2 (ovarian)

PARP inhibitors AstraZeneca Lynparza (olaparib)FDA approved (BRAC-mutatedovarian)

(also being studied in BioMarin BMN-673 P3breast cancer) Tesaro niraparib P3

Clovis rucaparib P3AbbVie veliparib P3

Ant iboy drug conjugate ImmunoGen mirvetuximab soravtansine P2 (ovarian)

(ADC) (combined with DM4)

Pancreat ic Cancer HER2 monoclonals (mAB) Roche Herceptin (trastuzumab)Mktd (adjuvant and metastaticbreast cancer)

(also tyrosine kinaseinhibitors or TKIs; for lung,

melanoma and breastcancers)

Source: UBS

Equity markets

UBS CIO WM 14 August 2015 14

Appendix 4: Cancer therapeutic terms and acronymsDefinitions of terms and acronyms used in this report

Clinical t rial assessmentCR Complete response -disappearance of all signs of cancer; also called complete remission

DFS Disease-free survival - length of time after treatment ends that patients survive without signs of that cancer

ORR Objective or overall response rate - percent of patients with a measurable response; CR plus PR

OS Overall survival - percentage of patients in treatment group still alive for a defined period after treatment

MRD Minimal residual disease - no signs or symptoms of disease after treatment; commonly used in leukemia treatment

PFS Progression-free survival - length of time during and after treatment a patient lives without disease worsening

PR Partial response - decrease in the size of a tumor or in the extent of cancer; also called partial remission

Lymphomas Blood cell tumors in lymph nodes that develop from lymphocytes (certain white blood cells)DLBCL Diffuse large B cell lymphoma; the most common type of NHL in adults

HL Hodgkin lymphoma; presence of Reed Sternberg cells (RS cells); different treatment from NHL

MCL An aggressive B-cell non-Hodgkin lymphoma that usually occurs in adults

MM Multiple myeloma; cancer of plasma cell (B-cell), a white blood cell normally responsible for producing antibodies

NHL Non-Hodgkin Lymphoma; over 30 distinct types; can be aggressive or indolent

iNHL Indolent non-Hodgkin lymphoma; slow-growing NHL

Leukemias Blood cell tumors in circulating blood; bone marrow leading to abnormal blood cells (lymphocytes and myeloid cell

ALL Acute lymphocytic leukemia; the most common leukemia in children

AML Acute myeloid leukemia; occurs mainly in adults

CLL Chronic lymphocytic leukemia; most often affects adults over age 55

CML Chronic myeloid leukemia; occurs mainly in adults

Breast cancer There are numerous types of breast cancer, simplified here by general treatment categoriesBRCA BRCA1 and BRCA2 genes suppress cell growth; mutations increase risk of breast, ovarian and other cancers

ER+ Estrogen receptor positive breast cancer

ER- Estrogen receptor negative breast cancer

HER2+ Human epidermal receptor positive breast cancer

HER2- Human epidermal receptor negative breast cancer

Triple negative Progesterone negative, ER- and HER2- breast cancer

Lung cancerMesothelioma Cancer affecting the lining of the chest or abdomen; exposure to asbestos particles in the air increases risk

NSCLC Non-small cell lung cancer; relatively insensitive to chemotherapy

SCLC Small cell lung cancer; a highly malignant form, usually sensitive to chemotherapy

Prostate cancer A cancer in the prostate, a gland in the male reproductive systemmCRPC Metastatic castrate resistant prostate cancer; an advanced stage of the disease

PSA Prostate specific antigen; an enzyme secreted by the prostate; often elevated in men with prostate cancer

Other cancers ment ionedCRC Colorectal cancer (cancer of the colon or rectum)

Melanoma A form of skin cancer that begins in melanocytes (cells that make the pigment melanin)

RRC Renal cell carcinoma; kidney cancer

SCCHN Squamous cell carcinoma of the head and neck

UBC Urothelial bladder cancer

General terms1st -line therapy The first treatment given for a disease; also called induction therapy or primary treatment

2nd-line therapy The treatment given after first-line therapy no longer works

3rd-line therapy Treatment given after both first-line therapy and second-line therapy no longer work

adjuvant Post-operative; given with initial treatment after surgery

metastat ic The spread of cancer from one part of the body to another

monotherapy The use of a single drug or other treatment to treat a disease

neo-adjuvant Pre-operative; to reduce size or extent of cancer prior to surgery

squamous cell A skin or organ surface or lining cell

Source: UBS

Equity markets

UBS CIO WM 14 August 2015 15

AppendixIf you require information on UBS Chief Investment Office WM and its research products, please contact the mailbox [email protected] (please note that e-mail communication is unsecured) or contact your client advisor for assistance.

Disclosures (14 August 2015)AbbVie 8, 13, 14, Amgen Inc. 5, 8, 10, 11, 12, 13, 14, 17; Ariad Pharmaceuticals 13, Array Biopharma 13, AstraZeneca 11, 12,13, BioMarin Pharmaceuticals 13, Bristol-Myers Squibb 3, 5, 6, 8, 11, 12, 13, 14, Celgene Corporation 6, 8, 13, 14, Cellectis SASponsored ADR 13, Clovis Oncology 13, Exelixis, Inc. 13, Gilead Sciences 2, 13, Halozyme Therapeutics, Inc. 13, ImmunoGen 4,13, Incyte Corporation 13, Infinity Pharmaceuticals Inc 13, Intrexon 13, Johnson & Johnson 5, 6, 11, 12, 13, 14, Juno therapeutics13, Kite Pharma 13, Lilly (Eli) & Co. 5, 6, 8, 10, 11, 12, 13, 14, 17; Medivation 13, Merck & Co. 6, 8, 10, 11, 12, 13, 14, 15,Merrimack 13, Novartis 1, 5, 9, 10, 13, 15, 16, 17; Pfizer Inc. 6, 7, 11, 12, 13, 14, Puma Biotechnolgy, Inc. 13, Roche 10, 15, 16,Sanofi 13, Tesaro 13, Tokai 13, Ziopharm Oncology 13,

1. UBS AG, its affiliates or subsidiaries beneficially owned 1% or more of a class of this company's common equity securities as oflast month's end (or the prior month's end if this report is dated less than 10 days after the most recent month's end).2. A U.S.-based global equity strategist, a member of his team, or one of their household members has a long common stockposition in Gilead Sciences Inc.3. A U.S.-based global equity strategist, a member of his team, or one of their household members has a long common stockposition in Bristol-Myers Squibb.4. A U.S.-based global equity strategist, a member of his team, or one of their household members has a long common stockposition in ImmunoGen Inc.5. This company/entity is, or within the past 12 months has been, a client of UBS Securities LLC, and investment banking servicesare being, or have been, provided.6. This company/entity is, or within the past 12 months has been, a client of UBS Securities LLC, and non-investment bankingsecurities-related services are being, or have been, provided.7. A U.S.-based global equity strategist, a member of his team, or one of their household members has a long common stockposition in Pfizer Inc.8. This company/entity is, or within the past 12 months has been, a client of UBS Securities LLC, and non-securities services arebeing, or have been, provided.9. UBS AG is acting as agent in regard to Novartis AG's announced share buyback programme.10. UBS AG, its affiliates or subsidiaries expect to receive or intend to seek compensation for investment banking services fromthis company/entity within the next three months.11. This company/entity is, or within the past 12 months has been, a client of UBS Financial Services Inc, and non-investmentbanking securities-related services are being, or have been, provided.12. Within the past 12 months, UBS Financial Services Inc has received compensation for products and services other thaninvestment banking services from this company.13. UBS Securities LLC makes a market in the securities and/or ADRs of this company.14. Within the past 12 months, UBS Securities LLC has received compensation for products and services other than investmentbanking services from this company/entity.15. The equity analyst covering this company, a member of his or her team, or one of their household members has a long commonstock position in this company.16. UBS AG, its affiliates or subsidiaries held other significant financial interests in this company/entity as of last month's end (orthe prior month's end if this report is dated less than 10 working days after the most recent month's end).17. UBS AG, its affiliates or subsidiaries has acted as manager/co-manager in the underwriting or placement of securities of thiscompany/entity or one of its affiliates within the past 12 months.

Equity markets

UBS CIO WM 14 August 2015 16

Appendix

Equity selection system:Analysts provide three equity selections (Most Preferred, Neutral View, Least Preferred).

Most preferred:Taking into consideration the stock's rating as well as other factors relevant for portfolio management (e.g. risk, diversification),analysts expect the stock to contribute positively to the overall performance of the relevant Equity Preference List (EPL) in the next12 months, i.e. to outperform versus the thematic benchmark.Neutral view:Analysts expect the stock to neither contribute positively nor negatively to the performance of the relevant EPL, i.e. to perform inline with the thematic benchmark in the next 12 months.Least preferred:Taking into consideration the stock's rating as well as other factors relevant for portfolio management (e.g. risk, diversification),analysts expect the stock to contribute positively to the relevant EPL in the next 12 months, i.e. to underperform versus the thematicbenchmark, which results in a positive contribution to the EPL.SuspendedIssuing an analyst's research on a company can be restricted due to legal, regulatory, contractual or best business practiceobligations, which are normally caused by UBS Investment Bank’s participation in an investment banking transaction involving thecompany concerned.Equity Selections: An assessment versus a benchmarkEquity selections in Equity Preference Lists are relative assessments versus a sector/industry, country/regional or thematic benchmark.In the case of sectors/industries and countries/regions, the respective global MSCI benchmarks are used. For thematic research,analysts select a benchmark most representative of the investment idea. The chosen benchmark is disclosed on the front page ofeach Equity Preferences List and is also used to measure the performance of the individual analyst. Stocks can be selected for severalEquity Preference Lists (EPLs). To keep the lists consistent, a stock can only be selected in either Most Preferred or Least Preferredlists, but not both simultaneously. As benchmarks differ between lists, stocks need not be included on every list to which theycould theoretically be added. UBS‘s selection methodology advises investors on how to profit from a specific investment theme/sector/region. Whenever CIO has an investment view on an entire sector/industry or country/region over a 3–12 month horizon,we state our preference relative to global equity markets by using the terms Overweight, Neutral and Underweight. UBS's selectionmethodology shows private clients how to best invest if they would like to profit from a specific investment theme.

Current UBS global rating distribution (as of last month-end)

Buy 44.16% (29.70%*) . . .Neutral 40.55% (33.33%*) . . .Sell 13.06% (18.42%*) . . .Suspended 2.06% (83.33%*) . . .Discontinued 0.17% (0.00%*) . . .

Equity markets

UBS CIO WM 14 August 2015 17

Appendix

Rating history table (last 12 months)

Release date Company name Equity Preference List Current select ion Previous select ion

Nov 10 2014 Bristol-Myers Squibb Healthcare Not Listed Most Preferred

Apr 24 2015 Johnson & Johnson Healthcare Not Listed Most Preferred

Sep 18 2014 Novartis Healthcare Not Listed Most Preferred

Sep 18 2014 Roche Healthcare Most Preferred Not Listed

Feb 09 2015 Sanofi Eurozone Not Listed Least Preferred

Source: UBS

Terms and AbbreviationsTerm / Abbreviation Description / Definition Term / Abbreviation Description / Definition1H, 2H, etc. or 1H11,2H11, etc.

First half, second half, etc. or first half 2011,second half 2011, etc.

A actual i.e. 2010A

bn Billion COM Common sharesE expected i.e. 2011E GDP Gross domestic productNAV Net asset value p.a. Per annum (per year)Shares o/s Shares outstanding UP Underperform: The stock is expected to

underperform the sector benchmarkCIO UBS WM Chief Investment Office x multiple / multiplicator

Disclaimer

UBS Chief Investment Office WM's investment views are prepared and published by Wealth Management and Retail & Corporate or Wealth Management Americas,Business Divisions of UBS AG (regulated by FINMA in Switzerland), its subsidiary or affiliate ("UBS"). In certain countries UBS AG is referred to as UBS SA. This material isfor your information only and is not intended as an offer, or a solicitation of an offer, to buy or sell any investment or other specific product. Certain services and productsare subject to legal restrictions and cannot be offered worldwide on an unrestricted basis and/or may not be eligible for sale to all investors. All information and opinionsexpressed in this material were obtained from sources believed to be reliable and in good faith, but no representation or warranty, express or implied, is made as to itsaccuracy or completeness (other than disclosures relating to UBS). All information and opinions as well as any prices indicated are current as of the date of this report,and are subject to change without notice. The market prices provided in performance charts and tables are closing prices on the respective principal stock exchange.The analysis contained herein is based on numerous assumptions. Different assumptions could result in materially different results. Opinions expressed herein may differor be contrary to those expressed by other business areas or divisions of UBS, as a result of using different assumptions and/or criteria. UBS and any of its directors oremployees may be entitled at any time to hold long or short positions in investment instruments referred to herein, carry out transactions involving relevant investmentinstruments in the capacity of principal or agent, or provide any other services or have officers, who serve as directors, either to/for the issuer, the investment instrumentitself or to/for any company commercially or financially affiliated to such issuers. At any time, investment decisions (including whether to buy, sell or hold securities)made by UBS and its employees may differ from or be contrary to the opinions expressed in UBS research publications. Some investments may not be readily realizablesince the market in the securities is illiquid and therefore valuing the investment and identifying the risk to which you are exposed may be difficult to quantify. UBSrelies on information barriers to control the flow of information contained in one or more areas within UBS, into other areas, units, divisions or affiliates of UBS. Futuresand options trading is considered risky. Past performance of an investment is no guarantee for its future performance. Additional information will be made availableupon request. Some investments may be subject to sudden and large falls in value and on realization you may receive back less than you invested or may be requiredto pay more. Changes in foreign exchange rates may have an adverse effect on the price, value or income of an investment. The compensation of the analyst(s) whoprepared this report is determined exclusively by research management and senior management (not including investment banking). Analyst compensation is not basedon investment banking revenues, however, compensation may relate to the revenues of UBS Wealth Management and Retail & Corporate as a whole, which includesinvestment banking, sales and trading services. The analyst(s) responsible for the preparation of this report may interact with trading desk personnel, sales personneland other constituencies for the purpose of gathering, synthesizing and interpreting market information. Tax treatment depends on the individual circumstances andmay be subject to change in the future. UBS does not provide legal or tax advice and makes no representations as to the tax treatment of assets or the investmentreturns thereon both in general or with reference to specific client's circumstances and needs. We are of necessity unable to take into account the particular investmentobjectives, financial situation and needs of our individual clients and we would recommend that you take financial and/or tax advice as to the implications (includingtax) of investing in any of the products mentioned herein. For structured financial instruments and funds the sales prospectus is legally binding. If you are interested youmay attain a copy via UBS. This material may not be reproduced or copies circulated without prior authority of UBS. UBS expressly prohibits the distribution and transferof this material to third parties for any reason. UBS accepts no liability whatsoever for any claims or lawsuits from any third parties arising from the use or distributionof this material. This report is for distribution only under such circumstances as may be permitted by applicable law. In developing the Chief Investment Office (CIO)economic forecasts, CIO economists worked in collaboration with economists employed by UBS Investment Research. Forecasts and estimates are current only as ofthe date of this publication and may change without notice. For information on the ways in which UBS CIO WM manages conflicts and maintains independence of itsinvestment views and publication offering, and research and rating methodologies, please visit www.ubs.com/research. Additional information on the relevant authorsof this publication and other CIO publication(s) referenced in this report; and copies of any past reports on this topic; are available upon request from your client advisor.External Asset Managers / External Financial Consultants: In case this research or publication is provided to an External Asset Manager or an External FinancialConsultant, UBS expressly prohibits that it is redistributed by the External Asset Manager or the External Financial Consultant and is made available to their clients and/or third parties. Australia: 1) Clients of UBS Wealth Management Australia Ltd: This notice is issued by UBS Wealth Management Australia Ltd ABN 50 005 311937 (Holder of Australian Financial Services Licence No. 231127): This Document is general in nature and does not constitute personal financial product advice. TheDocument does not take into account any person’s objectives, financial situation or needs, and a recipient should obtain advice from an independent financial adviserand consider any relevant offer or disclosure document prior to making any investment decisions. 2) Clients of UBS AG: This notice is issued by UBS AG ABN 47 088129 613 (Holder of Australian Financial Services Licence No 231087): This Document is issued and distributed by UBS AG. This is the case despite anything to the contraryin the Document. The Document is intended for use only by “Wholesale Clients” as defined in section 761G (“Wholesale Clients”) of the Corporations Act 2001 (Cth)(“Corporations Act”). In no circumstances may the Document be made available by UBS AG to a “Retail Client” as defined in section 761G of the Corporations Act.UBS AG’s research services are only available to Wholesale Clients. The Document is general information only and does not take into account any person’s investmentobjectives, financial and taxation situation or particular needs. Bahamas: This publication is distributed to private clients of UBS (Bahamas) Ltd and is not intended fordistribution to persons designated as a Bahamian citizen or resident under the Bahamas Exchange Control Regulations. Bahrain: UBS AG is a Swiss bank not licensed,supervised or regulated in Bahrain by the Central Bank of Bahrain and does not undertake banking or investment business activities in Bahrain. Therefore, Clients have noprotection under local banking and investment services laws and regulations. Belgium: This publication is not intended to constitute a public offering or a comparablesolicitation under Belgian law, but might be made available for information purposes to clients of UBS Belgium, branch of UBS (Luxembourg) SA, registered with theNational Bank of Belgian and authorized by the “Financial Services and Markets Authority", to which this publication has not been submitted for approval. Brazil:Prepared by UBS Brasil Administradora de Valores Mobiliários Ltda, entity regulated by Comissão de Valores Mobiliários ("CVM"). The views and opinions expressedin this report accurately reflect analyst's personal views about the subject securities and issuers. This report is only intended for Brazilian residents if such residents aredirectly purchasing or selling securities in the Brazil capital market through a local authorized institution. For investors residing in Brazil, Eligible Investors are consideredto be: (i) financial institutions, (ii) insurance firms and investment capital companies, (iii) supplementary pension entities, (iv) entities that hold financial investmentshigher than R$ 300.000 and that confirm the status of qualified investors in written, (v) investment funds, (vi) securities portfolio managers and securities consultantsduly authorized by CVM, regarding their own investments, and (vii) social security systems created by the Federal Government, States, and Municipalities. Canada:The information contained herein is not, and under no circumstances is to be construed as, a prospectus, an advertisement, a public offering, an offer to sell securities

Equity markets

UBS CIO WM 14 August 2015 18

Appendix

Disclaimer