Embed Size (px)

Citation preview

1Private and Confidential

Equity market - way forward

AcePro Advisors Pvt. Ltd.Asset Management

2018

2Private and Confidential

Presentation Flowl

ABOUT US

GOVERNMENT’S BEHAVIOUR AHEAD OF ELECTIONS

WHAT HAS CHANGED

INDIAN EQUITY MARKET

SOME OTHER MACRO NUMBERS

FEEDBACK / Q&A

ACEPRO CONTRA SECTOR ROTATION STRATEGY

3Private and Confidential

About Us

AcePro Advisors Pvt Ltd. is a subsidiary of Sarthi Capital Advisors

Pvt Ltd., a part of Sarthi Group. Sarthi is committed to deliver

exceptional client service with operations in six service lines-

Investment Banking, Merchant Banking, Compliance Management,

Advisory services, Asset Management and NBFC with prime

business focus on SME segment. Sarthi provides solutions across

geographies to a wide range of clients enabling them to meet their

business, regulatory and financing objectives.

Key Strengths

Experience & Expertise

Networking

Comprehensive Offering

Personalized Approach

Result Oriented Approach

Research driven

Advisory

4Private and Confidential

Sarthi Capital Advisors- IPO Deal Track Record

5Private and Confidential

Sarthi Capital Advisors- IPO Deal Track Record

6Private and Confidential

Sarthi Capital Advisors- Best In The League….

7Private and Confidential

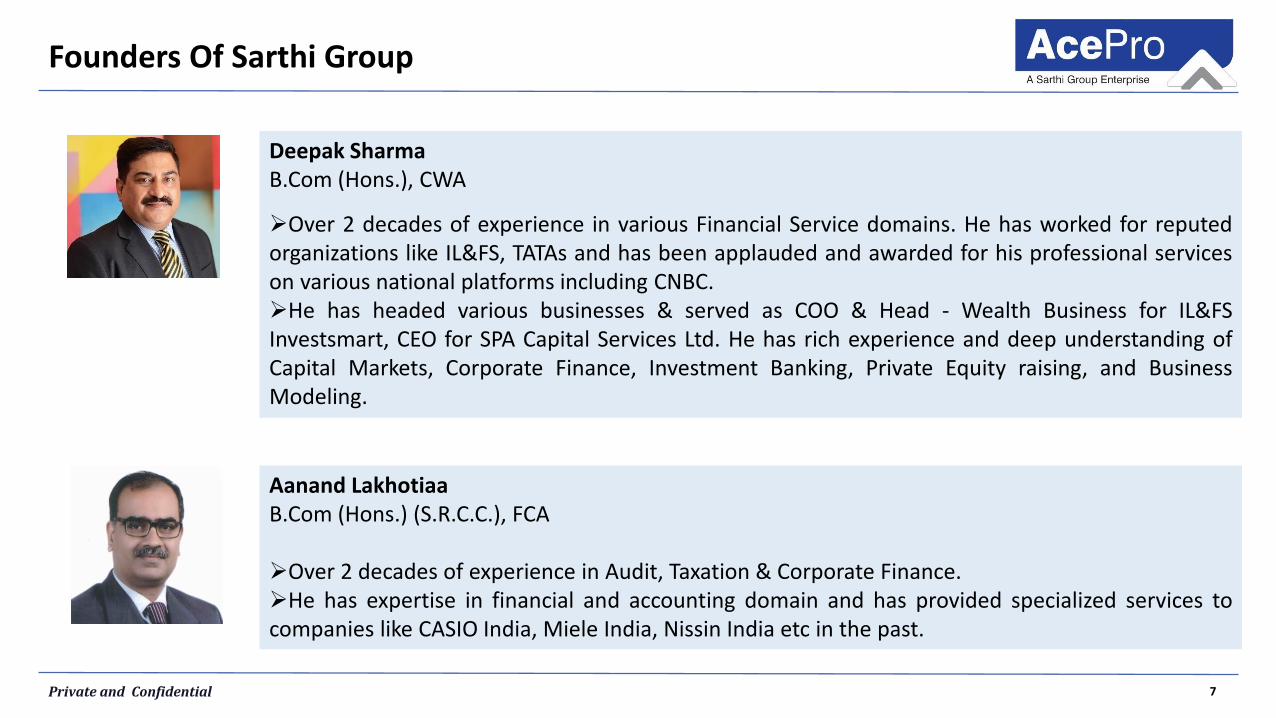

Founders Of Sarthi Group

Deepak SharmaB.Com (Hons.), CWA

Over 2 decades of experience in various Financial Service domains. He has worked for reputedorganizations like IL&FS, TATAs and has been applauded and awarded for his professional serviceson various national platforms including CNBC.He has headed various businesses & served as COO & Head - Wealth Business for IL&FSInvestsmart, CEO for SPA Capital Services Ltd. He has rich experience and deep understanding ofCapital Markets, Corporate Finance, Investment Banking, Private Equity raising, and BusinessModeling.

Aanand LakhotiaaB.Com (Hons.) (S.R.C.C.), FCA

Over 2 decades of experience in Audit, Taxation & Corporate Finance.He has expertise in financial and accounting domain and has provided specialized services tocompanies like CASIO India, Miele India, Nissin India etc in the past.

8Private and Confidential

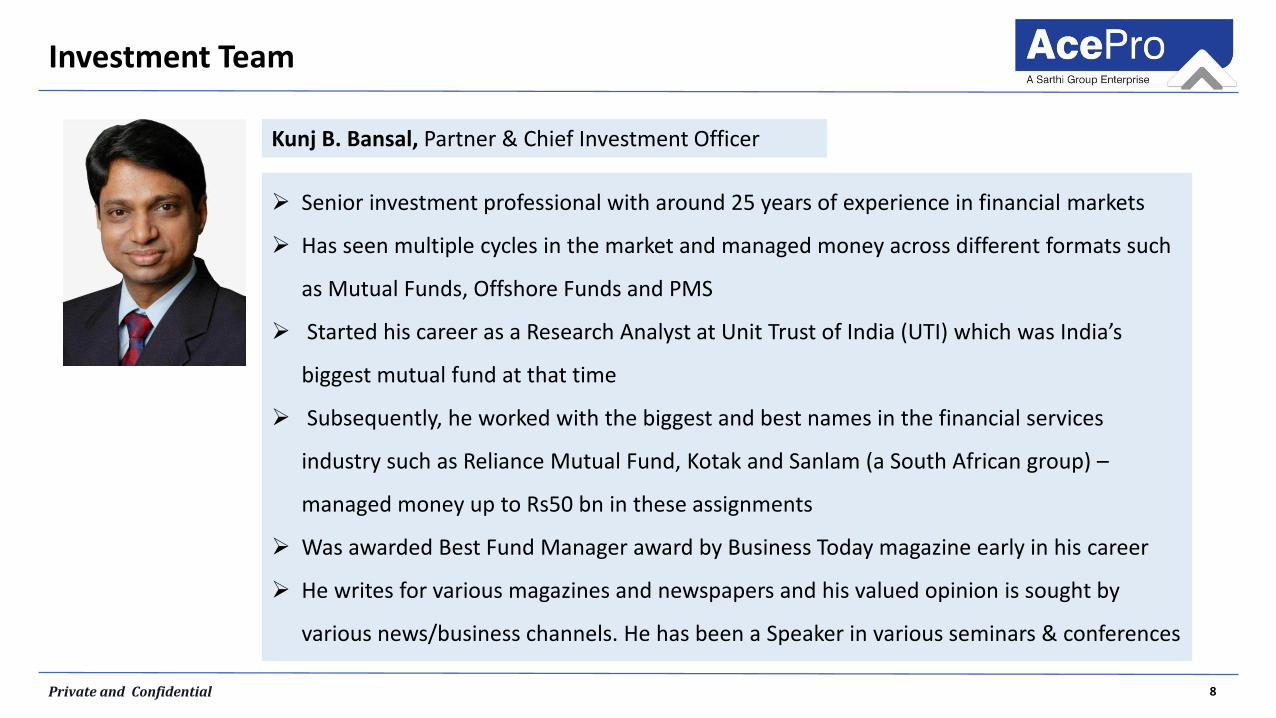

Senior investment professional with around 25 years of experience in financial markets

Has seen multiple cycles in the market and managed money across different formats such

as Mutual Funds, Offshore Funds and PMS

Started his career as a Research Analyst at Unit Trust of India (UTI) which was India’s

biggest mutual fund at that time

Subsequently, he worked with the biggest and best names in the financial services

industry such as Reliance Mutual Fund, Kotak and Sanlam (a South African group) –

managed money up to Rs50 bn in these assignments

Was awarded Best Fund Manager award by Business Today magazine early in his career

He writes for various magazines and newspapers and his valued opinion is sought by

various news/business channels. He has been a Speaker in various seminars & conferences

Kunj B. Bansal, Partner & Chief Investment Officer

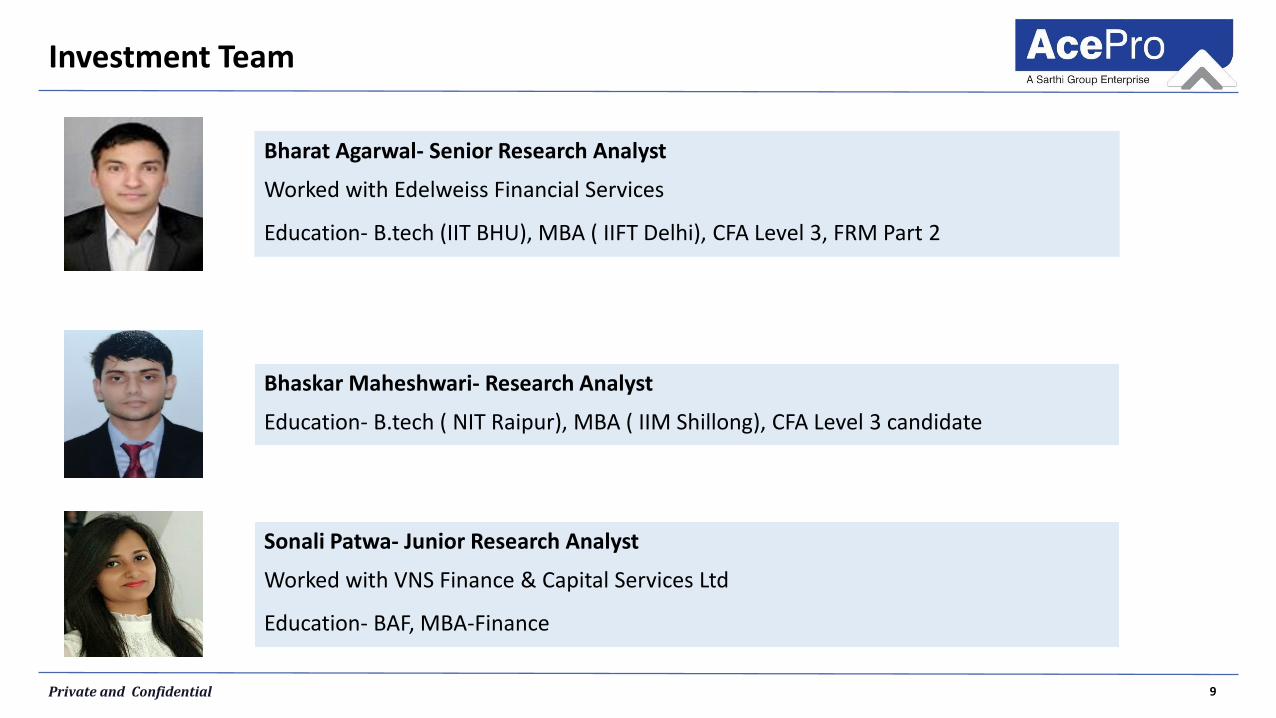

Investment Team

9Private and Confidential

Investment Team

Bhaskar Maheshwari- Research Analyst

Education- B.tech ( NIT Raipur), MBA ( IIM Shillong), CFA Level 3 candidate

Bharat Agarwal- Senior Research Analyst

Worked with Edelweiss Financial Services

Education- B.tech (IIT BHU), MBA ( IIFT Delhi), CFA Level 3, FRM Part 2

Sonali Patwa- Junior Research Analyst

Worked with VNS Finance & Capital Services Ltd

Education- BAF, MBA-Finance

10Private and Confidential

INDIAN EQUITY MARKET

11Private and Confidential

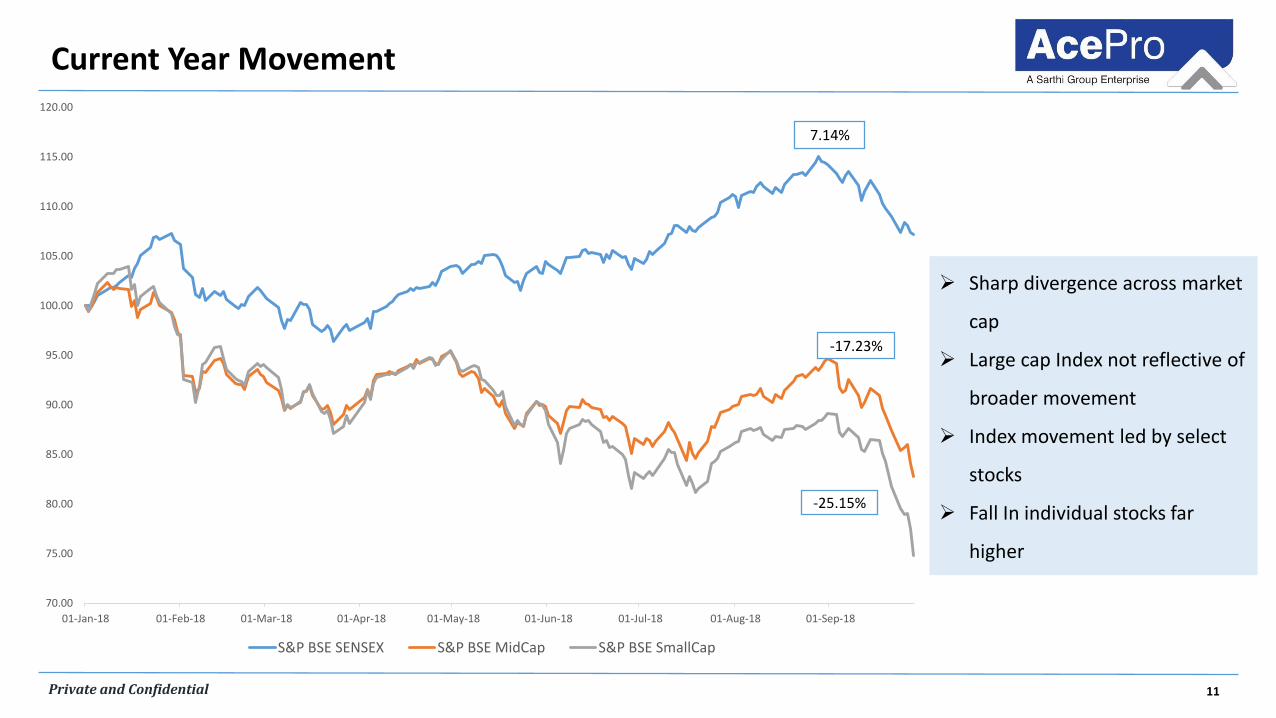

Current Year Movement

Sharp divergence across market

cap

Large cap Index not reflective of

broader movement

Index movement led by select

stocks

Fall In individual stocks far

higher

70.00

75.00

80.00

85.00

90.00

95.00

100.00

105.00

110.00

115.00

120.00

01-Jan-18 01-Feb-18 01-Mar-18 01-Apr-18 01-May-18 01-Jun-18 01-Jul-18 01-Aug-18 01-Sep-18

S&P BSE SENSEX S&P BSE MidCap S&P BSE SmallCap

7.14%

-17.23%

-25.15%

12Private and Confidential

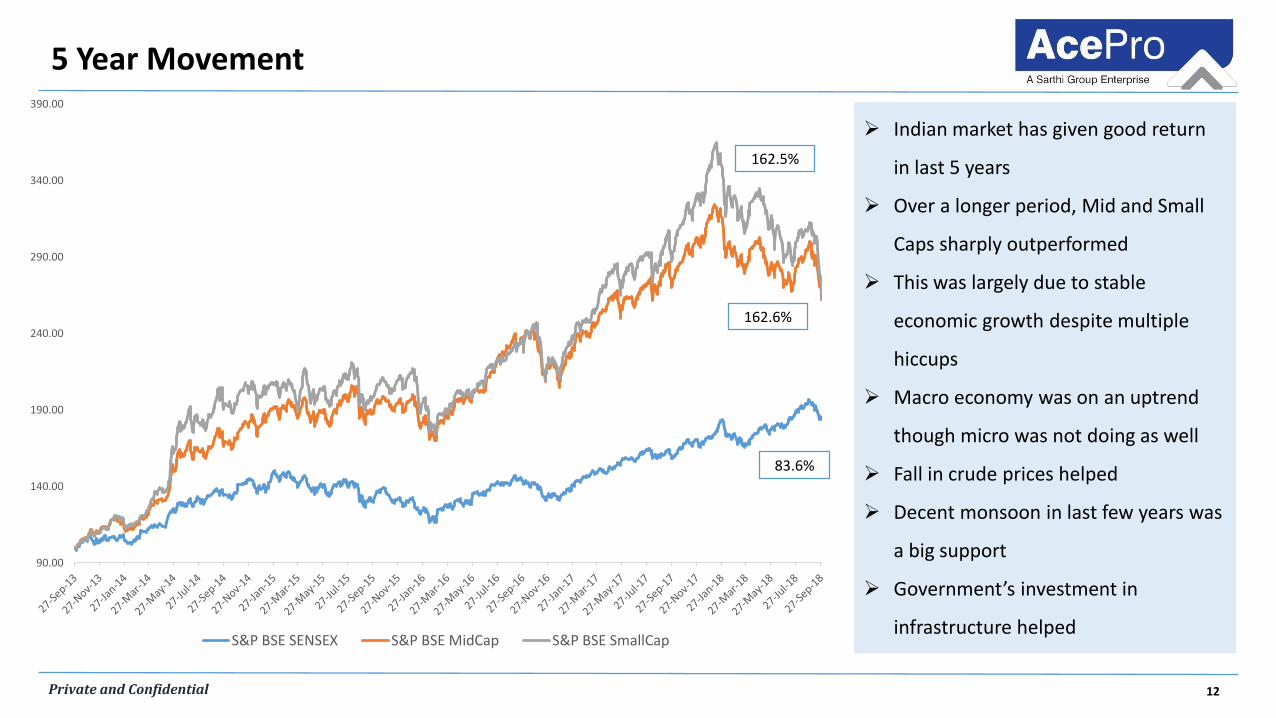

5 Year Movement

Indian market has given good return

in last 5 years

Over a longer period, Mid and Small

Caps sharply outperformed

This was largely due to stable

economic growth despite multiple

hiccups

Macro economy was on an uptrend

though micro was not doing as well

Fall in crude prices helped

Decent monsoon in last few years was

a big support

Government’s investment in

infrastructure helped

90.00

140.00

190.00

240.00

290.00

340.00

390.00

S&P BSE SENSEX S&P BSE MidCap S&P BSE SmallCap

83.6%

162.6%

162.5%

13Private and Confidential

Gainers & Losers

Contributors to SENSEX Journey from 29th Jan’18 (36000) to 28th Aug’18 (39000)

Top10 Gainers

Reliance Industries 37%

TCS 29%

M&M 28%

HUL 27%

Asian Paints 22%

Infosys 21%

Kotak Mahindra Bank 15%

ITC 13%

Indusind Bank 11%

Axis Bank 9%

Top10 Losers

Tata Motors -35%

Vedanta -33%

Tata Steel -21%

Bajaj Auto -20%

ONGC -15%

Bharti Airtel -15%

Adani Ports -11%

Hero Motocorp -11%

ICICI Bank -5%

Wipro -5%

14Private and Confidential

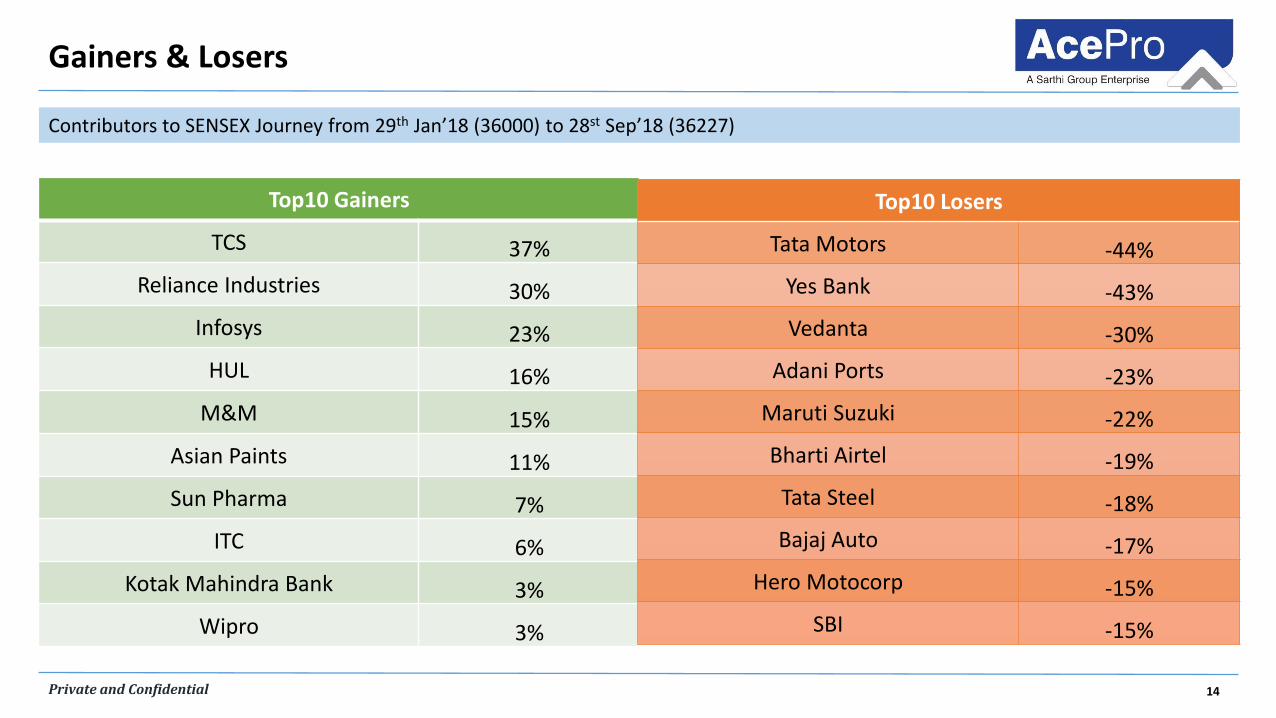

Gainers & Losers

Contributors to SENSEX Journey from 29th Jan’18 (36000) to 28st Sep’18 (36227)

Top10 Gainers

TCS 37%

Reliance Industries 30%

Infosys 23%

HUL 16%

M&M 15%

Asian Paints 11%

Sun Pharma 7%

ITC 6%

Kotak Mahindra Bank 3%

Wipro 3%

Top10 Losers

Tata Motors -44%

Yes Bank -43%

Vedanta -30%

Adani Ports -23%

Maruti Suzuki -22%

Bharti Airtel -19%

Tata Steel -18%

Bajaj Auto -17%

Hero Motocorp -15%

SBI -15%

15Private and Confidential

WHAT HAS CHANGED….?

16Private and Confidential

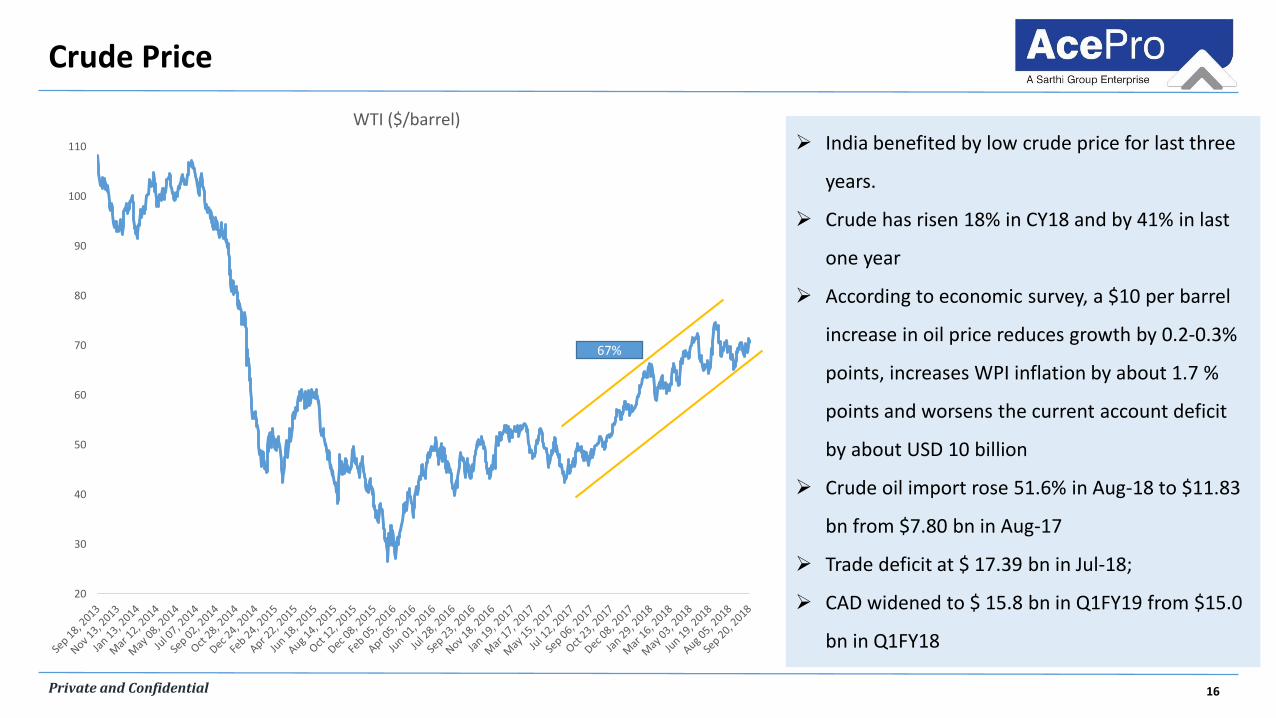

Crude Price

India benefited by low crude price for last three

years.

Crude has risen 18% in CY18 and by 41% in last

one year

According to economic survey, a $10 per barrel

increase in oil price reduces growth by 0.2-0.3%

points, increases WPI inflation by about 1.7 %

points and worsens the current account deficit

by about USD 10 billion

Crude oil import rose 51.6% in Aug-18 to $11.83

bn from $7.80 bn in Aug-17

Trade deficit at $ 17.39 bn in Jul-18;

CAD widened to $ 15.8 bn in Q1FY19 from $15.0

bn in Q1FY18

20

30

40

50

60

70

80

90

100

110

WTI ($/barrel)

67%

17Private and Confidential

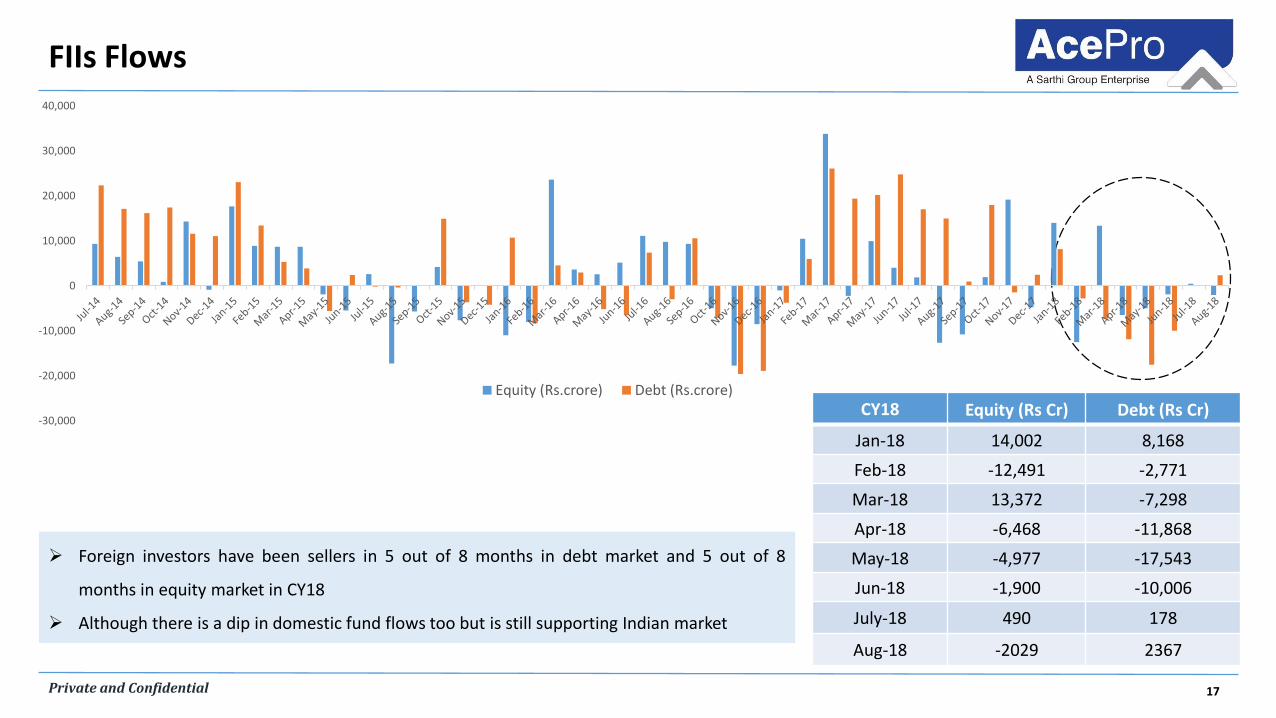

FIIs Flows

Foreign investors have been sellers in 5 out of 8 months in debt market and 5 out of 8

months in equity market in CY18

Although there is a dip in domestic fund flows too but is still supporting Indian market

-30,000

-20,000

-10,000

0

10,000

20,000

30,000

40,000

Equity (Rs.crore) Debt (Rs.crore)

CY18 Equity (Rs Cr) Debt (Rs Cr)

Jan-18 14,002 8,168

Feb-18 -12,491 -2,771

Mar-18 13,372 -7,298

Apr-18 -6,468 -11,868

May-18 -4,977 -17,543

Jun-18 -1,900 -10,006

July-18 490 178

Aug-18 -2029 2367

18Private and Confidential

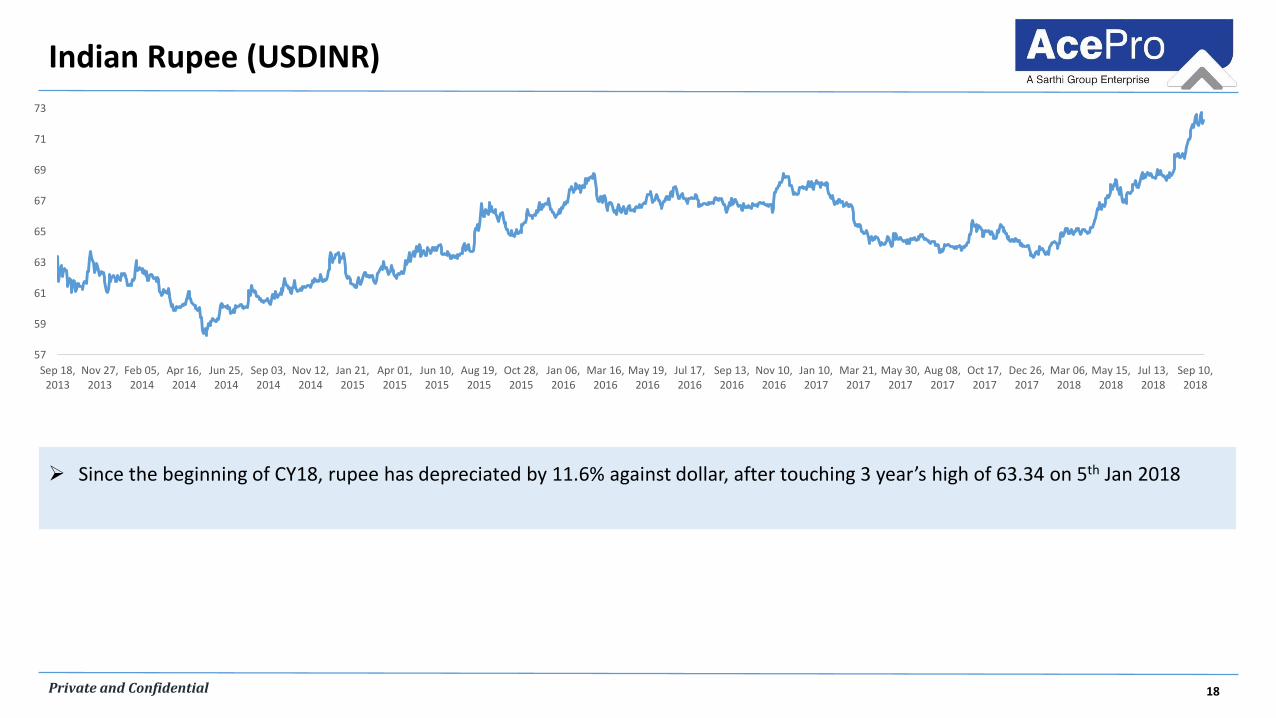

Indian Rupee (USDINR)

Since the beginning of CY18, rupee has depreciated by 11.6% against dollar, after touching 3 year’s high of 63.34 on 5th Jan 2018

57

59

61

63

65

67

69

71

73

Sep 18,2013

Nov 27,2013

Feb 05,2014

Apr 16,2014

Jun 25,2014

Sep 03,2014

Nov 12,2014

Jan 21,2015

Apr 01,2015

Jun 10,2015

Aug 19,2015

Oct 28,2015

Jan 06,2016

Mar 16,2016

May 19,2016

Jul 17,2016

Sep 13,2016

Nov 10,2016

Jan 10,2017

Mar 21,2017

May 30,2017

Aug 08,2017

Oct 17,2017

Dec 26,2017

Mar 06,2018

May 15,2018

Jul 13,2018

Sep 10,2018

19Private and Confidential

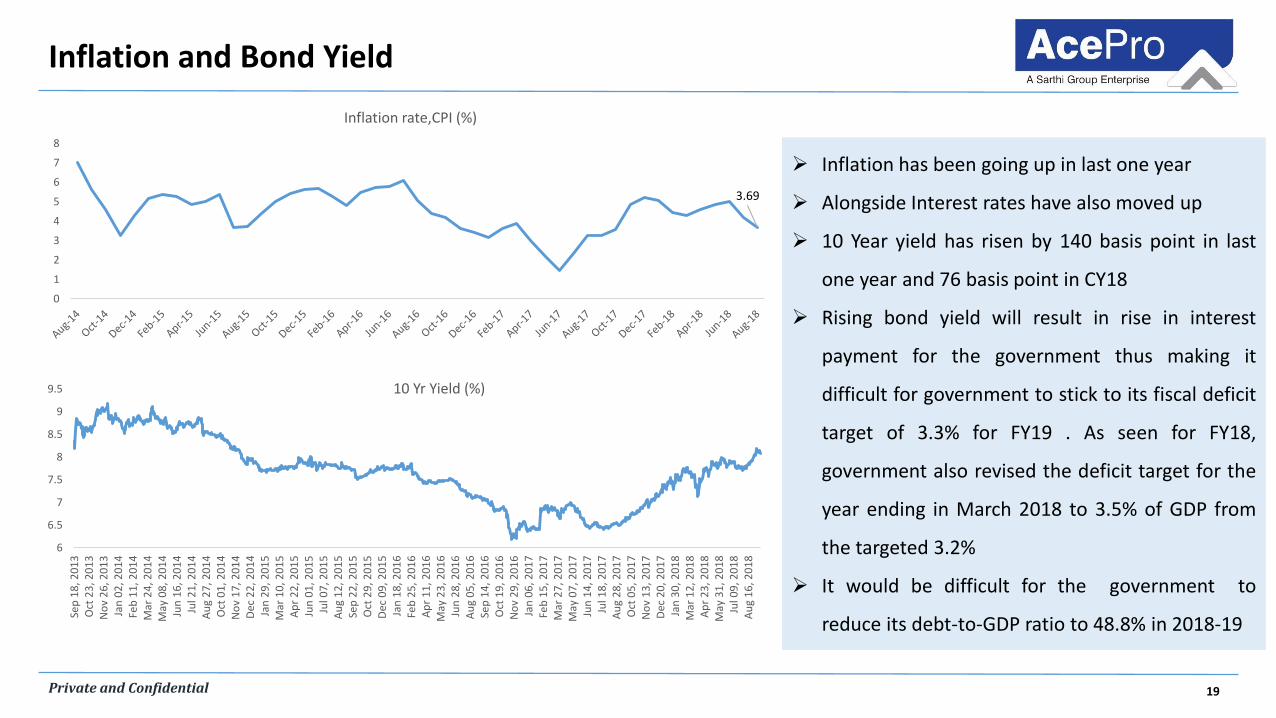

Inflation and Bond Yield

Inflation has been going up in last one year

Alongside Interest rates have also moved up

10 Year yield has risen by 140 basis point in last

one year and 76 basis point in CY18

Rising bond yield will result in rise in interest

payment for the government thus making it

difficult for government to stick to its fiscal deficit

target of 3.3% for FY19 . As seen for FY18,

government also revised the deficit target for the

year ending in March 2018 to 3.5% of GDP from

the targeted 3.2%

It would be difficult for the government to

reduce its debt-to-GDP ratio to 48.8% in 2018-19

6

6.5

7

7.5

8

8.5

9

9.5

Sep

18

, 20

13

Oct

23

, 20

13

No

v 2

6, 2

01

3Ja

n 0

2, 2

01

4Fe

b 1

1, 2

01

4M

ar 2

4, 2

01

4M

ay 0

8, 2

01

4Ju

n 1

6, 2

01

4Ju

l 21

, 20

14

Au

g 2

7, 2

01

4O

ct 0

1, 2

01

4N

ov

17

, 20

14

Dec

22

, 20

14

Jan

29

, 20

15

Mar

10

, 20

15

Ap

r 2

2, 2

01

5Ju

n 0

1, 2

01

5Ju

l 07

, 20

15

Au

g 1

2, 2

01

5Se

p 2

2, 2

01

5O

ct 2

9, 2

01

5D

ec 0

9, 2

01

5Ja

n 1

8, 2

01

6Fe

b 2

5, 2

01

6A

pr

11

, 20

16

May

23

, 20

16

Jun

28

, 20

16

Au

g 0

5, 2

01

6Se

p 1

4, 2

01

6O

ct 1

9, 2

01

6N

ov

29

, 20

16

Jan

06

, 20

17

Feb

15

, 20

17

Mar

27

, 20

17

May

07

, 20

17

Jun

14

, 20

17

Jul 1

8, 2

01

7A

ug

28

, 20

17

Oct

05

, 20

17

No

v 1

3, 2

01

7D

ec 2

0, 2

01

7Ja

n 3

0, 2

01

8M

ar 1

2, 2

01

8A

pr

23

, 20

18

May

31

, 20

18

Jul 0

9, 2

01

8A

ug

16

, 20

18

10 Yr Yield (%)

3.69

0

1

2

3

4

5

6

7

8

Inflation rate,CPI (%)

20Private and Confidential

State Of Macros

Interest Rate

The increase in inflation has already resulted in interest ratesmoving up which is likely to continue.

Spate of elections

Assembly elections are due in states of Rajasthan, Madhya Pradesh,Chhattisgarh and Mizoram in next few months to be followed bygeneral elections in 2019

Worsening Deficit/ Macroeconomic numbers

Historically, governments are known to spend aggressively ahead ofgeneral elections. This is likely to put pressure on fiscal deficit.

Trade War Impact

The global trade war initiated by the US and followed by othercountries has created uncertainty and needs to be monitored

Crude Price

The recent rise in crude price will increase the import burdenthus affecting the current account deficit. Indian currency hasalready witnessed sharp pressure due to this. Companiesdependent on crude derivatives for their raw materialrequirement will see increased manufacturing costs.

Global fund flows

Indian market has been witnessing an outflow of global funds.With US fed continuing its tightening monetary policy, futurefund flows will be a key monitorable

Higher inflation Rate/ MSP Hike

Government has sharply increased MSP for crops. This alongwith increased deficit and currency depreciation effects will leadto higher inflation which is already visible

21Private and Confidential

GOVERNMENT’S BEHAVIOUR AHEAD OF

ELECTIONS

22Private and Confidential

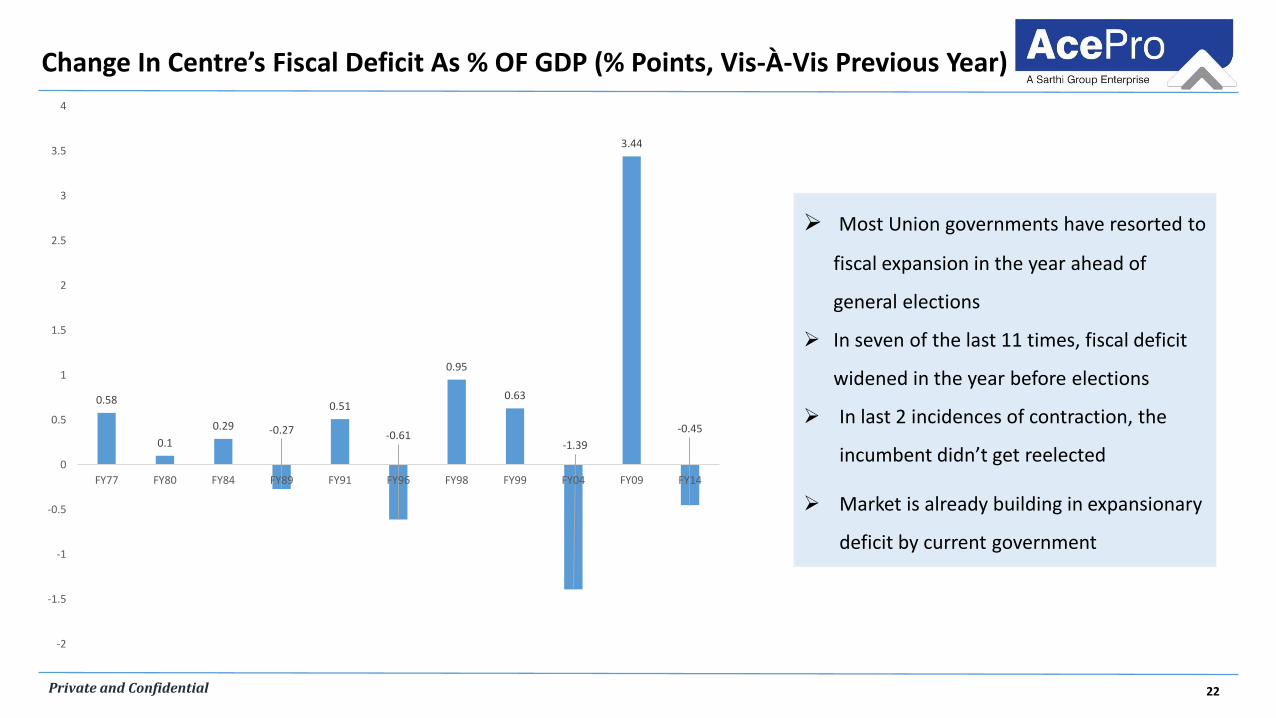

0.58

0.1

0.29 -0.27

0.51

-0.61

0.95

0.63

-1.39

3.44

-0.45

-2

-1.5

-1

-0.5

0

0.5

1

1.5

2

2.5

3

3.5

4

FY77 FY80 FY84 FY89 FY91 FY96 FY98 FY99 FY04 FY09 FY14

Most Union governments have resorted to

fiscal expansion in the year ahead of

general elections

In seven of the last 11 times, fiscal deficit

widened in the year before elections

In last 2 incidences of contraction, the

incumbent didn’t get reelected

Market is already building in expansionary

deficit by current government

Change In Centre’s Fiscal Deficit As % OF GDP (% Points, Vis-À-Vis Previous Year)

23Private and Confidential

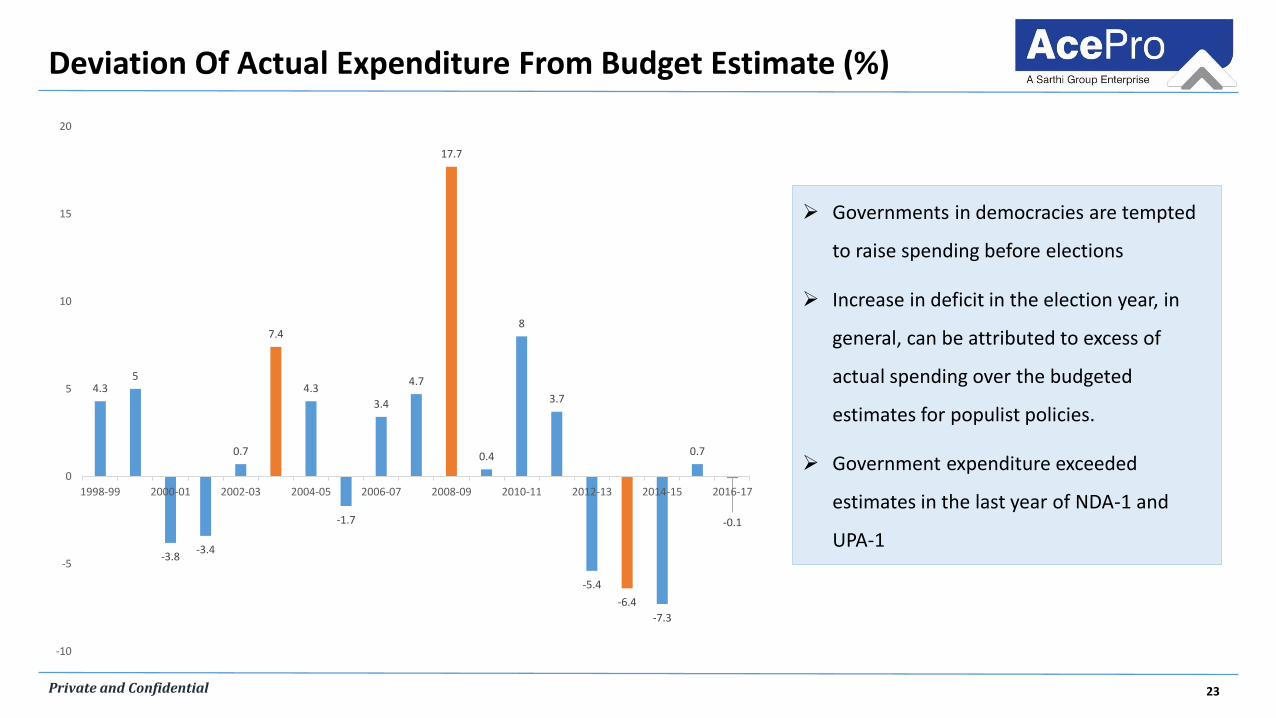

Deviation Of Actual Expenditure From Budget Estimate (%)

4.35

-3.8-3.4

0.7

7.4

4.3

-1.7

3.4

4.7

17.7

0.4

8

3.7

-5.4

-6.4

-7.3

0.7

-0.1

-10

-5

0

5

10

15

20

1998-99 2000-01 2002-03 2004-05 2006-07 2008-09 2010-11 2012-13 2014-15 2016-17

Governments in democracies are tempted

to raise spending before elections

Increase in deficit in the election year, in

general, can be attributed to excess of

actual spending over the budgeted

estimates for populist policies.

Government expenditure exceeded

estimates in the last year of NDA-1 and

UPA-1

24Private and Confidential

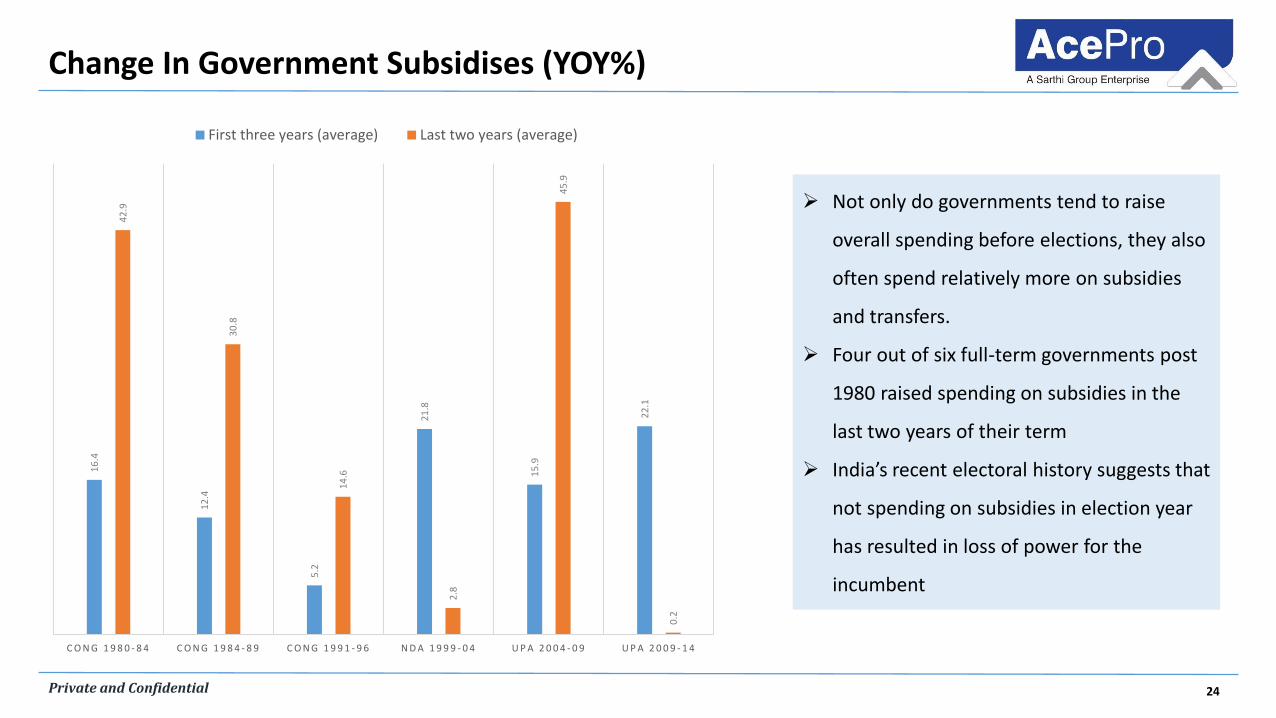

16

.4

12

.4

5.2

21

.8

15

.9

22

.1

42

.9

30

.8

14

.6

2.8

45

.9

0.2

C O N G 1 9 8 0 - 8 4 C O N G 1 9 8 4 - 8 9 C O N G 1 9 9 1 - 9 6 N D A 1 9 9 9 - 0 4 U P A 2 0 0 4 - 0 9 U P A 2 0 0 9 - 1 4

First three years (average) Last two years (average)

Not only do governments tend to raise

overall spending before elections, they also

often spend relatively more on subsidies

and transfers.

Four out of six full-term governments post

1980 raised spending on subsidies in the

last two years of their term

India’s recent electoral history suggests that

not spending on subsidies in election year

has resulted in loss of power for the

incumbent

Change In Government Subsidises (YOY%)

25Private and Confidential

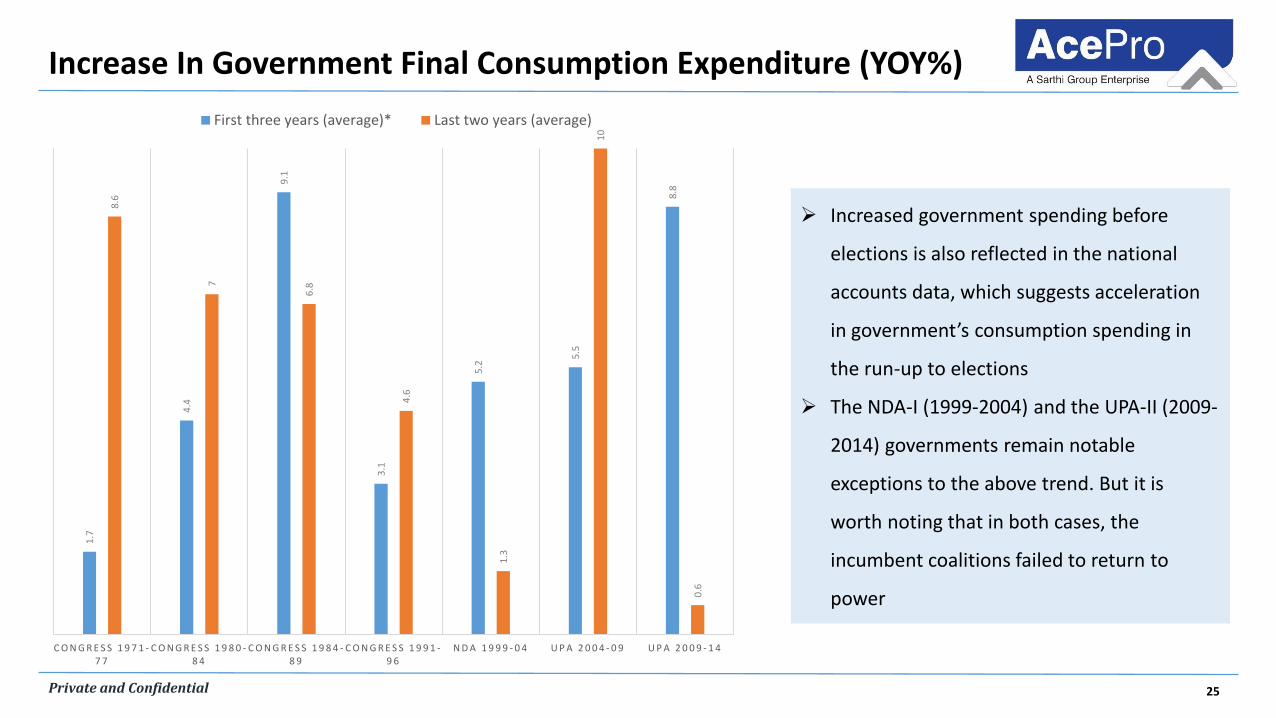

1.7

4.4

9.1

3.1

5.2

5.5

8.8

8.6

7

6.8

4.6

1.3

10

0.6

C O N G R E S S 1 9 7 1 -7 7

C O N G R E S S 1 9 8 0 -8 4

C O N G R E S S 1 9 8 4 -8 9

C O N G R E S S 1 9 9 1 -9 6

N D A 1 9 9 9 - 0 4 U P A 2 0 0 4 - 0 9 U P A 2 0 0 9 - 1 4

First three years (average)* Last two years (average)

Increase In Government Final Consumption Expenditure (YOY%)

Increased government spending before

elections is also reflected in the national

accounts data, which suggests acceleration

in government’s consumption spending in

the run-up to elections

The NDA-I (1999-2004) and the UPA-II (2009-

2014) governments remain notable

exceptions to the above trend. But it is

worth noting that in both cases, the

incumbent coalitions failed to return to

power

26Private and Confidential

SOME OTHER MACRO NUMBERS

27Private and Confidential

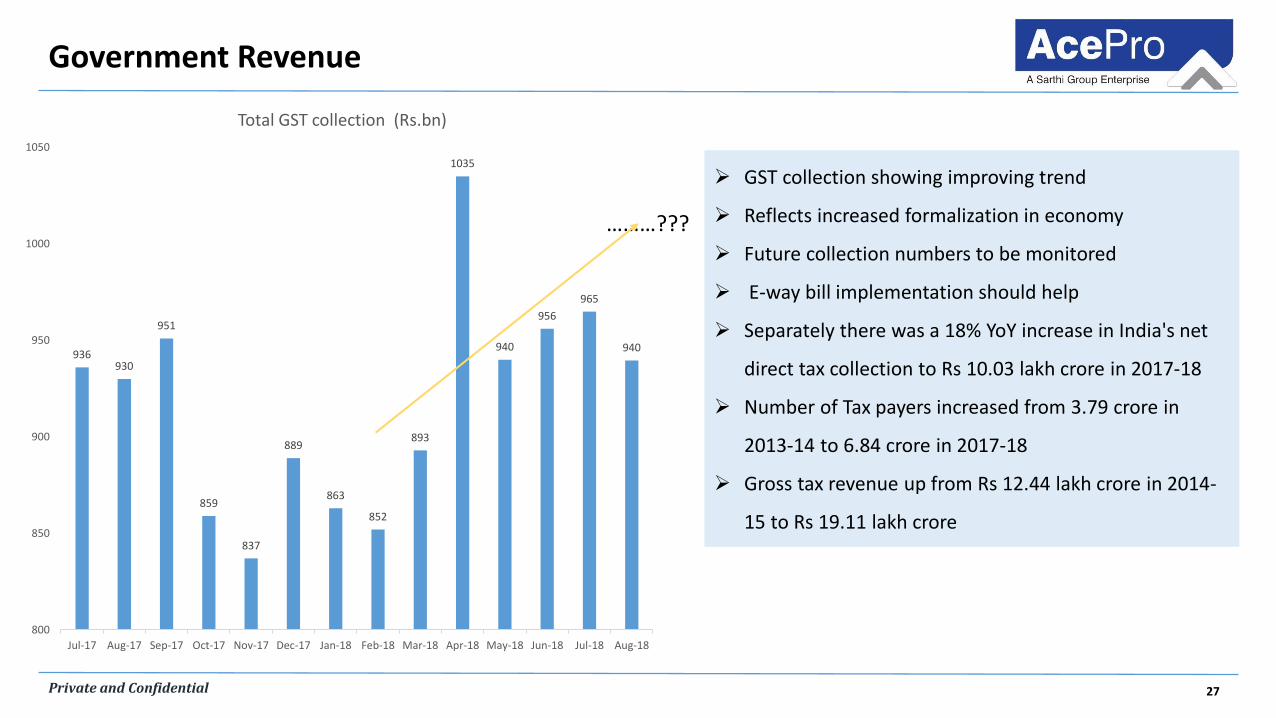

Government Revenue

GST collection showing improving trend

Reflects increased formalization in economy

Future collection numbers to be monitored

E-way bill implementation should help

Separately there was a 18% YoY increase in India's net

direct tax collection to Rs 10.03 lakh crore in 2017-18

Number of Tax payers increased from 3.79 crore in

2013-14 to 6.84 crore in 2017-18

Gross tax revenue up from Rs 12.44 lakh crore in 2014-

15 to Rs 19.11 lakh crore

………???

936930

951

859

837

889

863

852

893

1035

940

956

965

940

800

850

900

950

1000

1050

Jul-17 Aug-17 Sep-17 Oct-17 Nov-17 Dec-17 Jan-18 Feb-18 Mar-18 Apr-18 May-18 Jun-18 Jul-18 Aug-18

Total GST collection (Rs.bn)

28Private and Confidential

Infrastructure Activity

5013

5732

4250 4410

6061

8231

9829

4000

5500

7000

8500

10000

FY12 FY13 FY14 FY15 FY16 FY17 FY18

NH Constructed (in Km)

NH Constructed

12%

6491

1116 14383069 4368 4337

7396

3303

8004883

48215730

11934

9659

0

4000

8000

12000

16000

20000

FY12 FY13 FY14 FY15 FY16 FY17 FY18

NH Projects awarded (Km)

NHAI MORT and others

10%

Good growth in national highway projects awarded and highway construction in last few years

Proxy to infrastructure growth

Shows increase in investment by country

Has helped economic growth when private capex was low

Incremental Govt. spend over FY16-18 averaged Rs 5.3tn per annum vs. Rs 3.1tn per annum over the FY12-15 period adding ~1% to GDP

growth each year.

FY19 budget envisages a roads capital outlay of Rs. 1.21tn, a 10% increase over FY18

NHAI is slated to award 8,000kms of road projects in FY19

29Private and Confidential

Consumption Activity

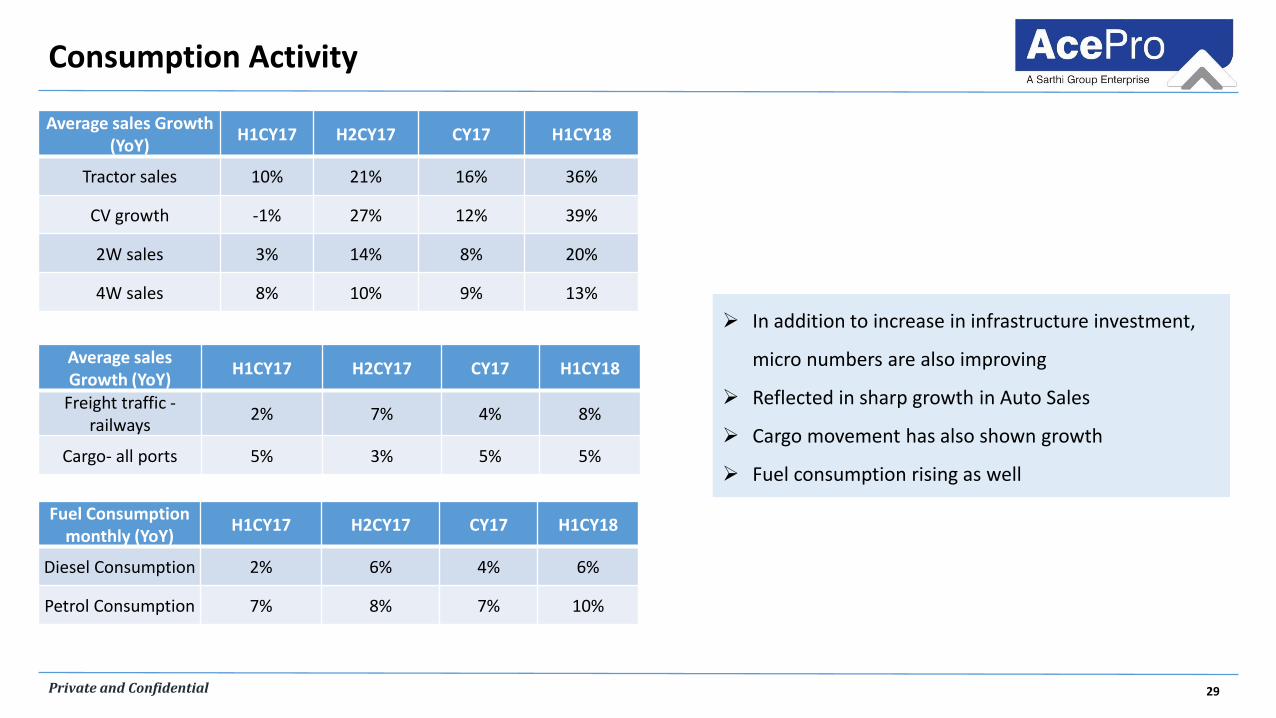

In addition to increase in infrastructure investment,

micro numbers are also improving

Reflected in sharp growth in Auto Sales

Cargo movement has also shown growth

Fuel consumption rising as well

Average sales Growth (YoY)

H1CY17 H2CY17 CY17 H1CY18

Tractor sales 10% 21% 16% 36%

CV growth -1% 27% 12% 39%

2W sales 3% 14% 8% 20%

4W sales 8% 10% 9% 13%

Average sales Growth (YoY)

H1CY17 H2CY17 CY17 H1CY18

Freight traffic -railways

2% 7% 4% 8%

Cargo- all ports 5% 3% 5% 5%

Fuel Consumption monthly (YoY)

H1CY17 H2CY17 CY17 H1CY18

Diesel Consumption 2% 6% 4% 6%

Petrol Consumption 7% 8% 7% 10%

30Private and Confidential

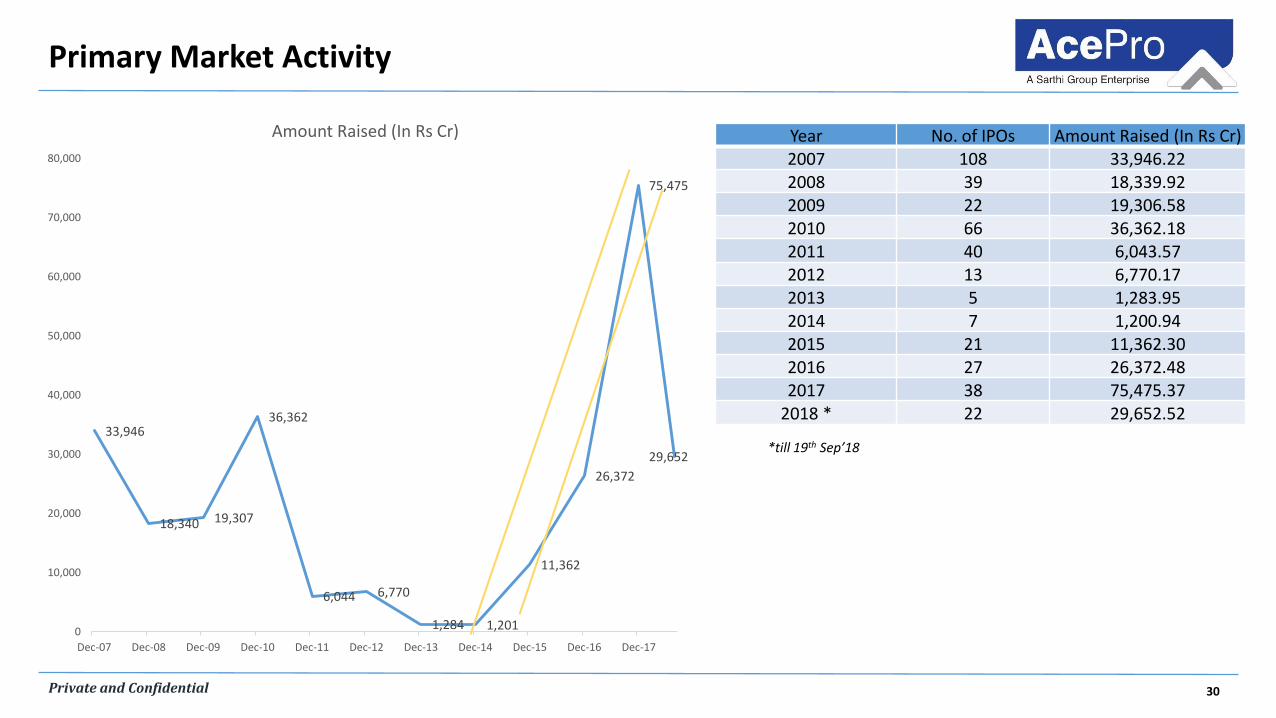

Primary Market Activity

Year No. of IPOs Amount Raised (In Rs Cr)2007 108 33,946.222008 39 18,339.922009 22 19,306.582010 66 36,362.182011 40 6,043.572012 13 6,770.172013 5 1,283.952014 7 1,200.942015 21 11,362.302016 27 26,372.482017 38 75,475.37

2018 * 22 29,652.52

*till 19th Sep’1833,946

18,340 19,307

36,362

6,044 6,770

1,284 1,201

11,362

26,372

75,475

29,652

0

10,000

20,000

30,000

40,000

50,000

60,000

70,000

80,000

Dec-07 Dec-08 Dec-09 Dec-10 Dec-11 Dec-12 Dec-13 Dec-14 Dec-15 Dec-16 Dec-17

Amount Raised (In Rs Cr)

31Private and Confidential

Way Forward

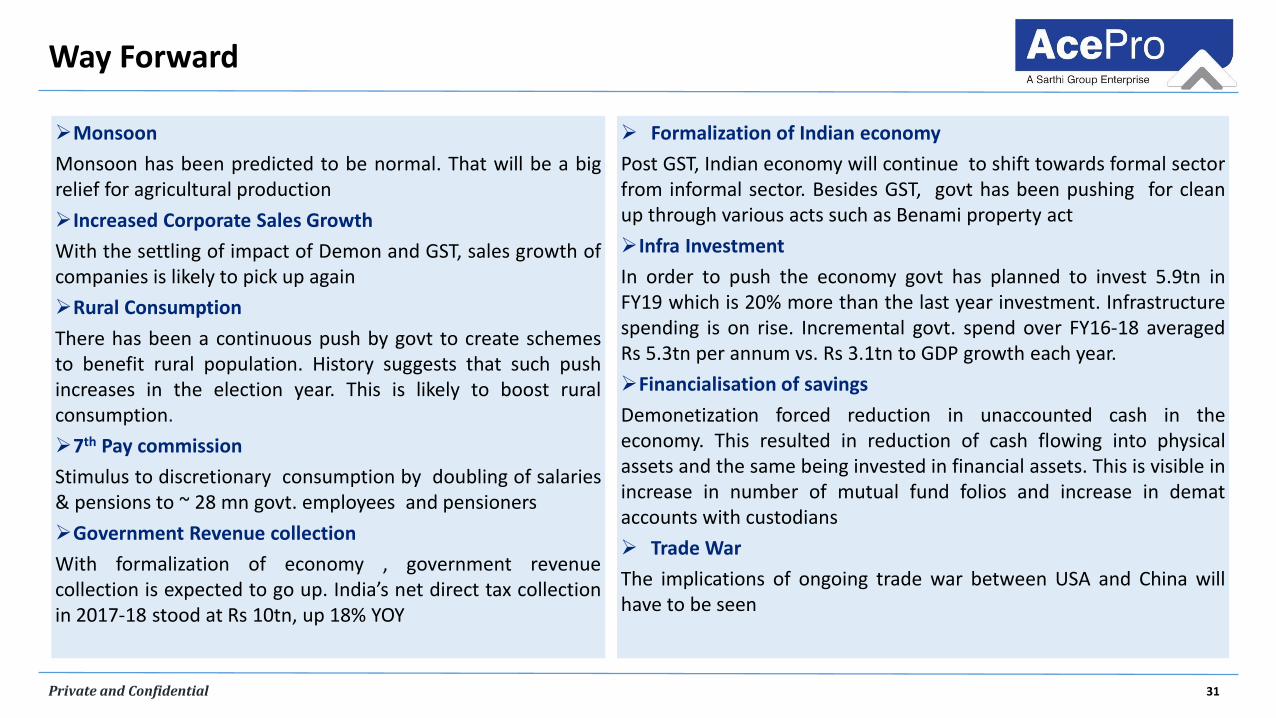

Formalization of Indian economy

Post GST, Indian economy will continue to shift towards formal sectorfrom informal sector. Besides GST, govt has been pushing for cleanup through various acts such as Benami property act

Infra Investment

In order to push the economy govt has planned to invest 5.9tn inFY19 which is 20% more than the last year investment. Infrastructurespending is on rise. Incremental govt. spend over FY16-18 averagedRs 5.3tn per annum vs. Rs 3.1tn to GDP growth each year.

Financialisation of savings

Demonetization forced reduction in unaccounted cash in theeconomy. This resulted in reduction of cash flowing into physicalassets and the same being invested in financial assets. This is visible inincrease in number of mutual fund folios and increase in demataccounts with custodians

Trade War

The implications of ongoing trade war between USA and China willhave to be seen

Monsoon

Monsoon has been predicted to be normal. That will be a bigrelief for agricultural production

Increased Corporate Sales Growth

With the settling of impact of Demon and GST, sales growth ofcompanies is likely to pick up again

Rural Consumption

There has been a continuous push by govt to create schemesto benefit rural population. History suggests that such pushincreases in the election year. This is likely to boost ruralconsumption.

7th Pay commission

Stimulus to discretionary consumption by doubling of salaries& pensions to ~ 28 mn govt. employees and pensioners

Government Revenue collection

With formalization of economy , government revenuecollection is expected to go up. India’s net direct tax collectionin 2017-18 stood at Rs 10tn, up 18% YOY

32Private and Confidential

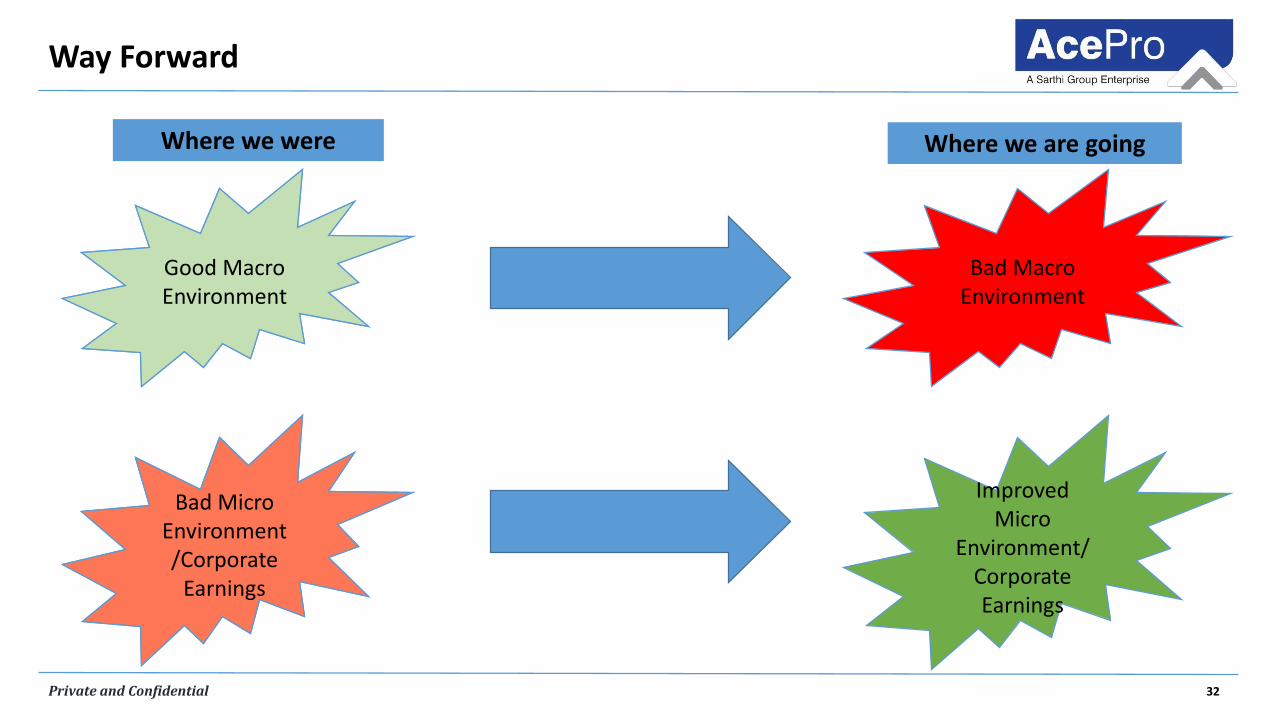

Way Forward

Good Macro Environment

Where we were

Bad Micro Environment/Corporate

Earnings

Good Macro Environment

Bad Macro Environment

Where we are going

Bad Micro Environment/Corporate

Earnings

Improved Micro

Environment/Corporate Earnings

33Private and Confidential

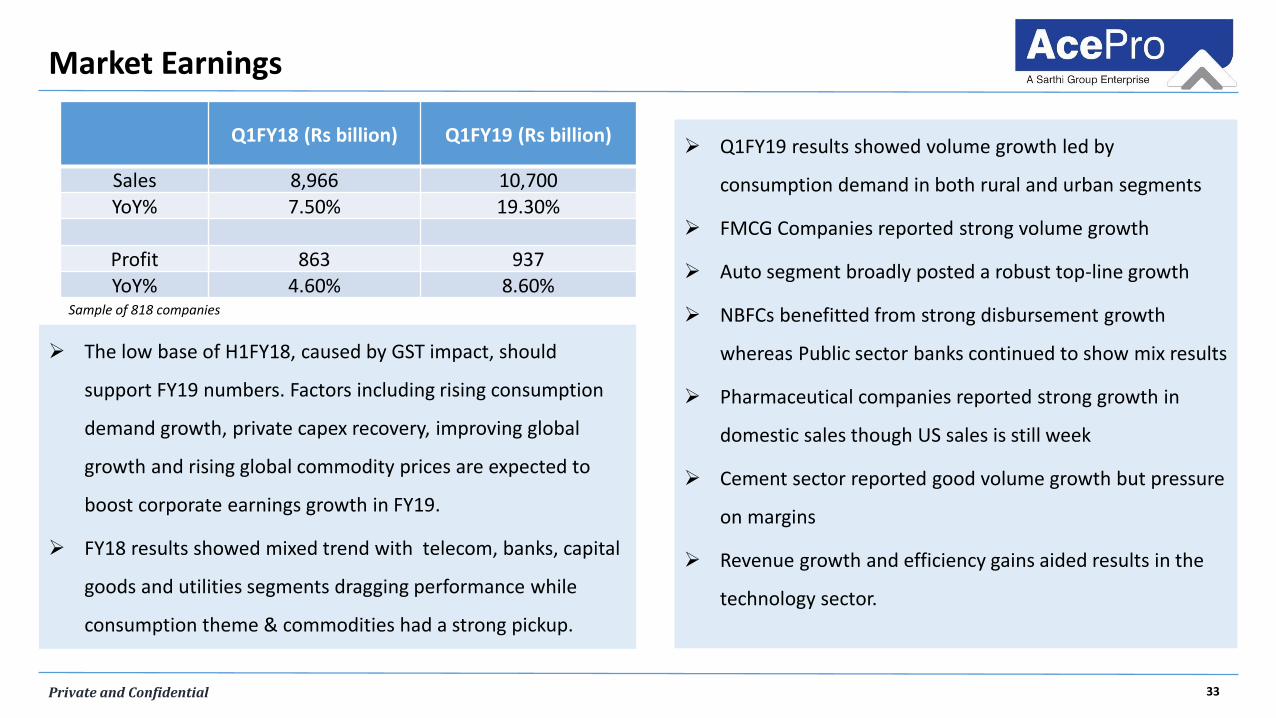

Market Earnings

Q1FY19 results showed volume growth led by

consumption demand in both rural and urban segments

FMCG Companies reported strong volume growth

Auto segment broadly posted a robust top-line growth

NBFCs benefitted from strong disbursement growth

whereas Public sector banks continued to show mix results

Pharmaceutical companies reported strong growth in

domestic sales though US sales is still week

Cement sector reported good volume growth but pressure

on margins

Revenue growth and efficiency gains aided results in the

technology sector.

The low base of H1FY18, caused by GST impact, should

support FY19 numbers. Factors including rising consumption

demand growth, private capex recovery, improving global

growth and rising global commodity prices are expected to

boost corporate earnings growth in FY19.

FY18 results showed mixed trend with telecom, banks, capital

goods and utilities segments dragging performance while

consumption theme & commodities had a strong pickup.

Q1FY18 (Rs billion) Q1FY19 (Rs billion)

Sales 8,966 10,700YoY% 7.50% 19.30%

Profit 863 937YoY% 4.60% 8.60%

Sample of 818 companies

34Private and Confidential

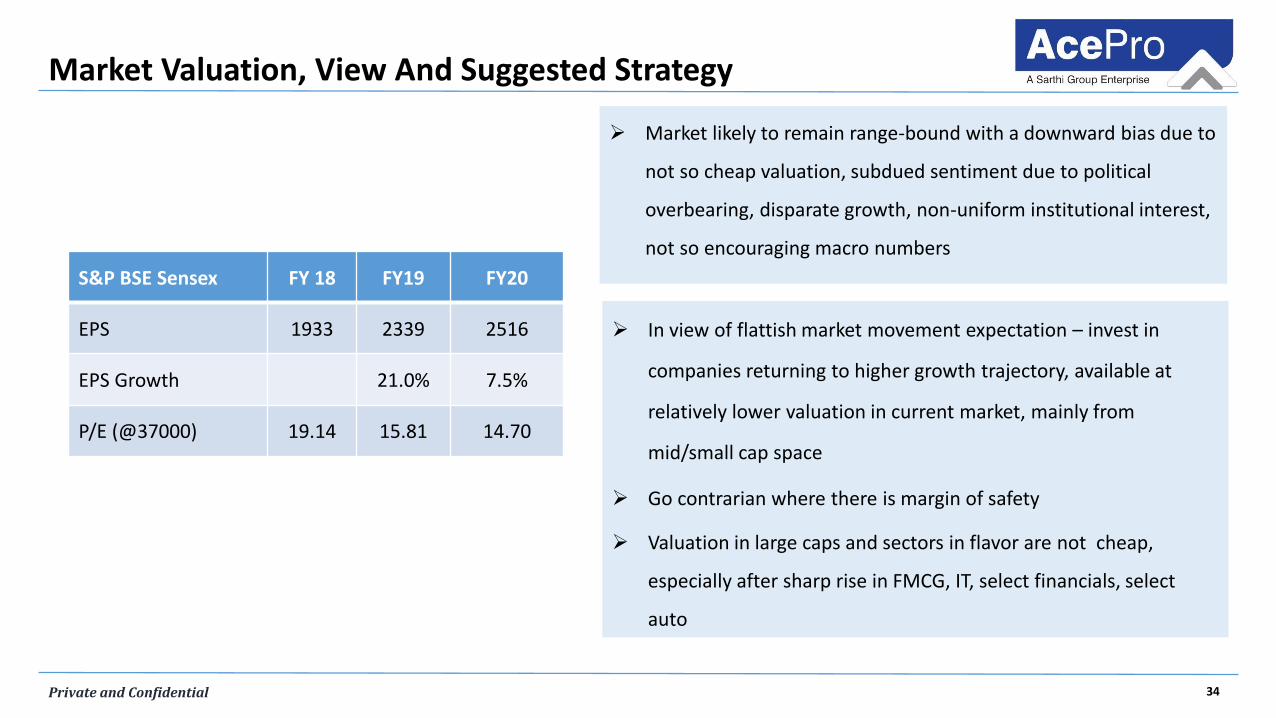

Market Valuation, View And Suggested Strategy

Market likely to remain range-bound with a downward bias due to

not so cheap valuation, subdued sentiment due to political

overbearing, disparate growth, non-uniform institutional interest,

not so encouraging macro numbers

In view of flattish market movement expectation – invest in

companies returning to higher growth trajectory, available at

relatively lower valuation in current market, mainly from

mid/small cap space

Go contrarian where there is margin of safety

Valuation in large caps and sectors in flavor are not cheap,

especially after sharp rise in FMCG, IT, select financials, select

auto

S&P BSE Sensex FY 18 FY19 FY20

EPS 1933 2339 2516

EPS Growth 21.0% 7.5%

P/E (@37000) 19.14 15.81 14.70

35Private and Confidential

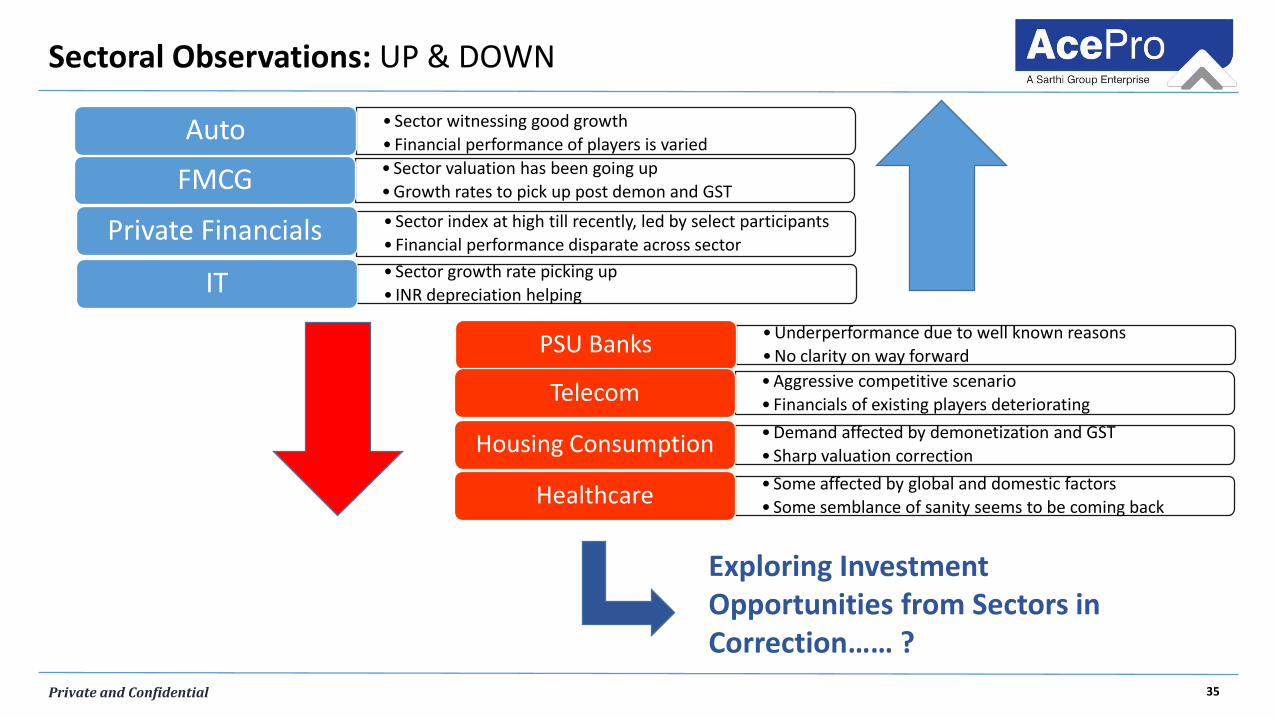

Sectoral Observations: UP & DOWN

Exploring Investment Opportunities from Sectors in Correction…… ?

• Sector witnessing good growth

• Financial performance of players is varied Auto

• Sector valuation has been going up

• Growth rates to pick up post demon and GSTFMCG• Sector index at high till recently, led by select participants

• Financial performance disparate across sectorPrivate Financials

• Sector growth rate picking up

• INR depreciation helping IT

• Underperformance due to well known reasons

• No clarity on way forwardPSU Banks

• Aggressive competitive scenario

• Financials of existing players deterioratingTelecom

• Demand affected by demonetization and GST

• Sharp valuation correctionHousing Consumption

• Some affected by global and domestic factors

• Some semblance of sanity seems to be coming backHealthcare

36Private and Confidential

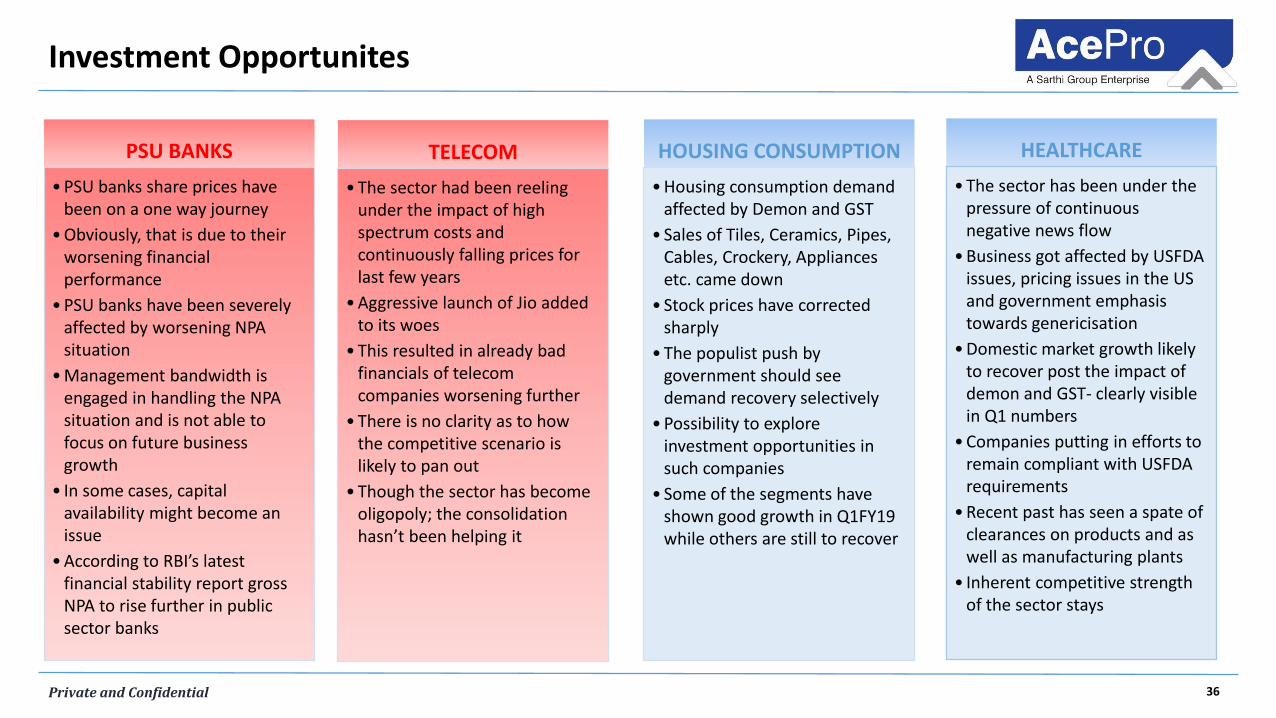

Investment Opportunites

TELECOM

• The sector had been reeling under the impact of high spectrum costs and continuously falling prices for last few years

• Aggressive launch of Jio added to its woes

• This resulted in already bad financials of telecom companies worsening further

• There is no clarity as to how the competitive scenario is likely to pan out

• Though the sector has become oligopoly; the consolidation hasn’t been helping it

HOUSING CONSUMPTION

• Housing consumption demand affected by Demon and GST

• Sales of Tiles, Ceramics, Pipes, Cables, Crockery, Appliances etc. came down

• Stock prices have corrected sharply

• The populist push by government should see demand recovery selectively

• Possibility to explore investment opportunities in such companies

• Some of the segments have shown good growth in Q1FY19 while others are still to recover

HEALTHCARE

• The sector has been under the pressure of continuous negative news flow

• Business got affected by USFDA issues, pricing issues in the US and government emphasis towards genericisation

• Domestic market growth likely to recover post the impact of demon and GST- clearly visible in Q1 numbers

• Companies putting in efforts to remain compliant with USFDA requirements

• Recent past has seen a spate of clearances on products and as well as manufacturing plants

• Inherent competitive strength of the sector stays

PSU BANKS

• PSU banks share prices have been on a one way journey

• Obviously, that is due to their worsening financial performance

• PSU banks have been severely affected by worsening NPA situation

• Management bandwidth is engaged in handling the NPA situation and is not able to focus on future business growth

• In some cases, capital availability might become an issue

• According to RBI’s latest financial stability report gross NPA to rise further in public sector banks

37Private and Confidential

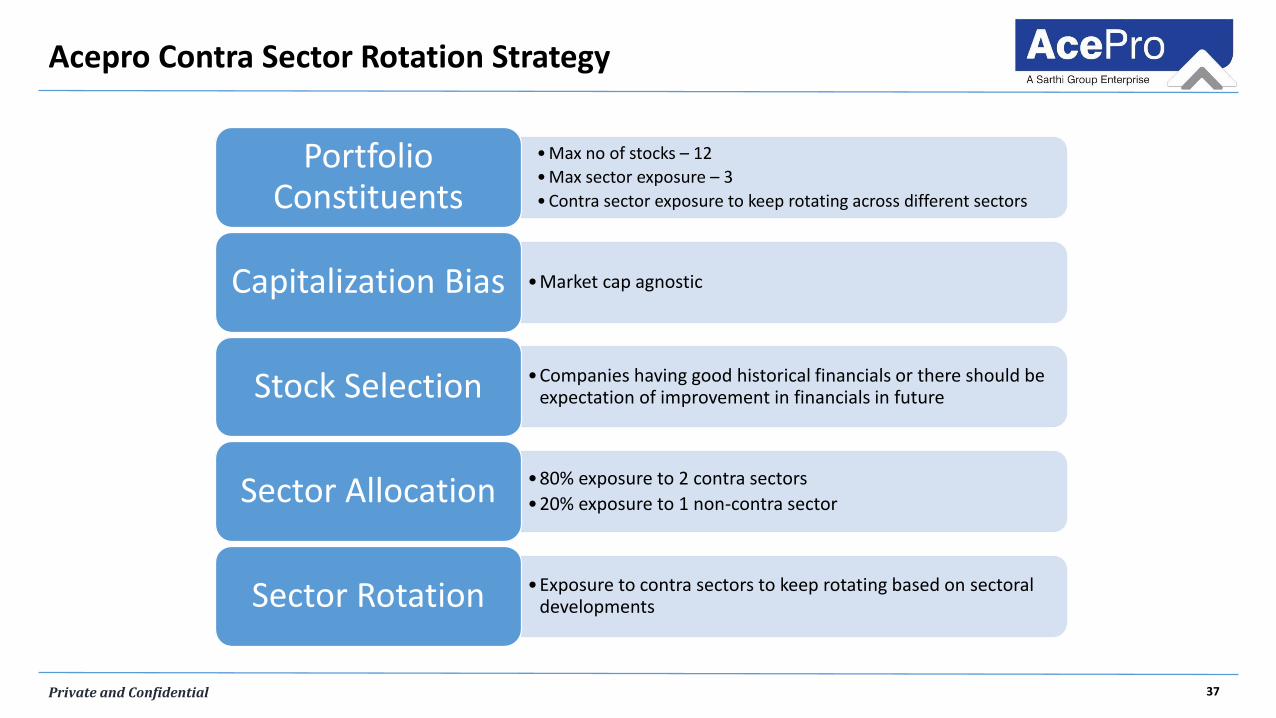

Acepro Contra Sector Rotation Strategy

• Max no of stocks – 12

• Max sector exposure – 3

• Contra sector exposure to keep rotating across different sectors

Portfolio Constituents

•Market cap agnosticCapitalization Bias

•Companies having good historical financials or there should be expectation of improvement in financials in futureStock Selection

•80% exposure to 2 contra sectors

•20% exposure to 1 non-contra sectorSector Allocation

•Exposure to contra sectors to keep rotating based on sectoraldevelopmentsSector Rotation

38Private and Confidential

FEEDBACK / Q&A

HAPPY TO HELP…

Corporate Headquarters:Mumbai401, 4th floor, Manek Plaza,

167,Vidya NagariMarg, Kalina,Santacruz(E), Mumbai-400 098Landline: (022) 26528671-72, Fax: (022) 26528673E-mail: [email protected]

Regional Office:New Delhi411, 4th Floor, Pratap Bhawan,5, Bahadurshah Zafar Marg,New Delhi – 110002Tel.: 011-23739425-27, Fax: 011-23739424

DisclaimerAll data and information is provided for informational purposes only and is not intended for any factual use. Itshould not be considered as binding / statutory provisions. Neither AcePro Advisors nor any of its group company,directors, or employees shall be liable for any of the data or content provided for any actions taken in reliancethereon.

AcePro ADVISORS PRIVATE LIMITEDA Sarthi Group Enterprise

![Untitled-2 [] · FS 78 FS 68 , FOCUS ÉkJ ËFOCUS FS 78 FS 68 FS 68 , , , FS 68 Foundation FS 68 , FS 68 68 fi , FOCUS F-s 688 , , 68 , 688 FOCUS FS , FS 68 , , , 688 ,](https://img.pdfslide.us/doc/110x75/5b75f9b67f8b9a3b7e8b5e04/untitled-2-fs-78-fs-68-focus-ekj-efocus-fs-78-fs-68-fs-68-fs-68.jpg)