Embed Size (px)

Citation preview

EquityImpactsofFeeSystemstoSupportZeroEmissionVehicleSalesinCalifornia

June2016 AResearchReportfromtheNationalCenterforSustainableTransportation

LewFulton,UniversityofCalifornia,Davis

JulieSchiffman,UniversityofCalifornia,Davis

GilTal,UniversityofCalifornia,Davis

i

AbouttheNationalCenterforSustainableTransportationTheNationalCenterforSustainableTransportationisaconsortiumofleadinguniversitiescommittedtoadvancinganenvironmentallysustainabletransportationsystemthroughcutting-edgeresearch,directpolicyengagement,andeducationofourfutureleaders.Consortiummembersinclude:UniversityofCalifornia,Davis;UniversityofCalifornia,Riverside;UniversityofSouthernCalifornia;CaliforniaStateUniversity,LongBeach;GeorgiaInstituteofTechnology;andUniversityofVermont.Moreinformationcanbefoundat:ncst.ucdavis.edu.U.S.DepartmentofTransportation(USDOT)DisclaimerThecontentsofthisreportreflecttheviewsoftheauthors,whoareresponsibleforthefactsandtheaccuracyoftheinformationpresentedherein.ThisdocumentisdisseminatedunderthesponsorshipoftheUnitedStatesDepartmentofTransportation’sUniversityTransportationCentersprogram,intheinterestofinformationexchange.TheU.S.Governmentassumesnoliabilityforthecontentsorusethereof.AcknowledgmentsThisstudywasfundedbyagrantfromtheNationalCenterforSustainableTransportation(NCST),supportedbyUSDOTthroughtheUniversityTransportationCentersprogram.TheauthorswouldliketothanktheNCSTandUSDOTfortheirsupportofuniversity-basedresearchintransportation,andespeciallyforthefundingprovidedinsupportofthisproject.WewouldalsoliketothankreviewersfromtheCaliforniaAirResourcesBoardandvariousothercompaniesandnon-governmentalorganizations.

ii

EquityImpactsofFeeSystemstoSupportZeroEmissionVehicleSalesinCalifornia

ANationalCenterforSustainableTransportationResearchReport

June2016

LewFulton,UniversityofCalifornia,Davis

JulieSchiffman,UniversityofCalifornia,Davis

GilTal,UniversityofCalifornia,Davis

iii

[pageleftintentionallyblank]

iv

TABLEOFCONTENTSEXECUTIVESUMMARY....................................................................................................................v

Introduction...................................................................................................................................3

ABriefReviewofRelevantLiterature............................................................................................4

CurrentCaliforniaPolicy................................................................................................................6

AnalysisApproach..........................................................................................................................7

AnalysisofAlternativeFeeStructures.........................................................................................17

Results..........................................................................................................................................19

SummaryofFindingsandPolicyImplications..............................................................................23

Lookingtoward2025...................................................................................................................24

PotentialFutureResearch............................................................................................................26

References...................................................................................................................................27

v

EquityImpactsofFeeSystemstoSupportZeroEmissionVehicleSalesinCalifornia

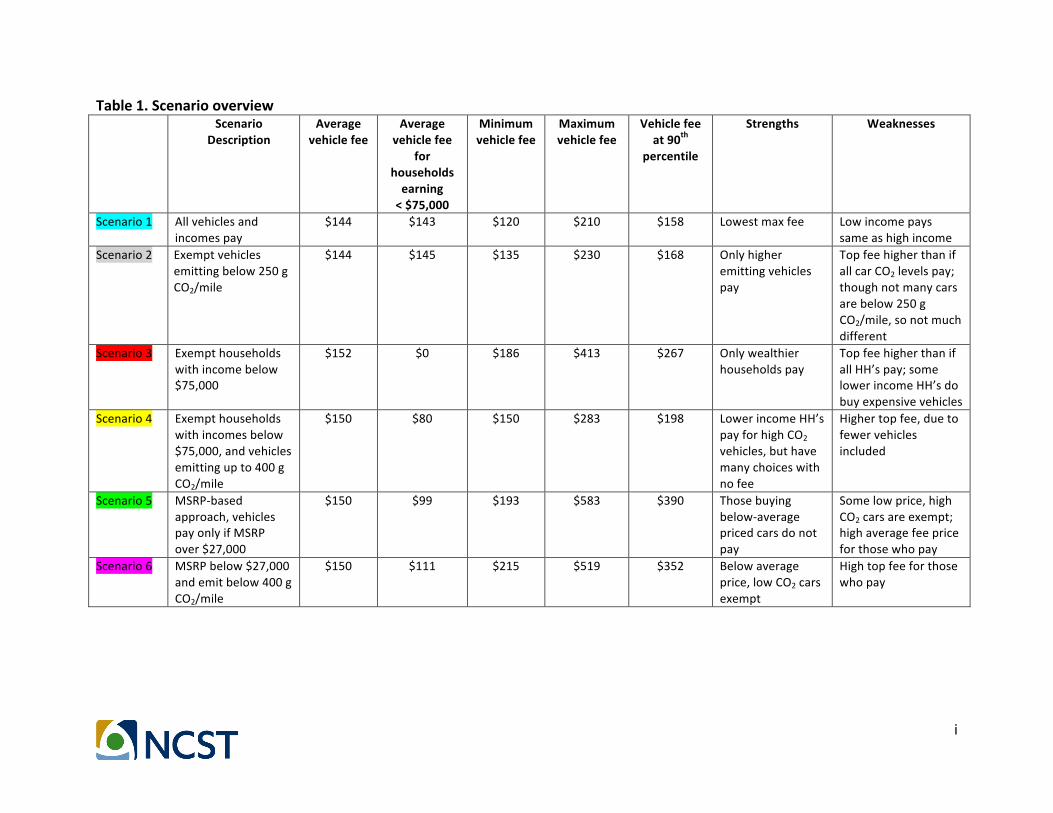

EXECUTIVESUMMARYToacceleratethemarketintroductionofzero-emissionvehicles(ZEVs,includingbatteryelectricandfuelcellelectricvehicles)andtransitionalZEVs(TZEV,includingplug-inhybridvehicles),customerincentivesandsubsidiesmaybeneededformanyyears—untiltheadditionalcosttomanufacturethesevehiclesdecreasesconsiderably.Currently,Californiaprovides$5,000forthepurchaseoflightdutyfuelcellvehicles,$2,500forbatteryelectricvehicles,and$1,500forplug-inhybridelectricvehicles,aspartofitsCleanVehicleRebateProject(CVRP-2,2015),currentlyfundedfromrevenuescollectedbythecarboncapandtradeprogram,aswellasmotorvehiclefees.InFY2015-2016,thestateallocated$75millionforrebatesundertheprogram,whichwasnotsufficienttocovertheCVRPpayments.Thisreportpresentsanalysisresultsofpotentialdesignsoffeesystemsforthepurchaseofnew(non-ZEV)vehiclesthatcouldhelpfundCalifornia’sCVRP.DifferentCO2-basedfeestructureswereconsidered,andthepotentialincidenceofthesefeesacrosshouseholdgroupswithdifferentincomelevelswasestimated.Thestudyassessesdifferentfeestructuresforthegivenrebateprogram,butitdoesnotconsideralternativerebatesystems(onlytheexistingCVRPsystem),sotheterm“feebate”isnotused,butrather“vehiclefees”todescribethescenarios.Inthescenarios,eachincomegrouphasbeenrelatedtothetypicalCalifornianumberandtypesofnewlight-dutyvehiclespurchased,includingaverageCO2emissionsofthesenewvehicles,tothefeestheywouldpay(individuallyandasincomegroups)underthedifferentfeestructures.The2010-2012CaliforniaHouseholdTravelSurveydata(including2011-2012andlimited2013vehiclemodels)toexploretheserelationships,sotheyareatbestonlyindicativeofcurrentandfuturerelationships.Sixdifferentfeestructurepolicyscenariosweredevelopedthatapplyvariousvehiclefeesdependingona)theCO2emissionsofindividualnon-ZEVvehiclemodels,b)possibleadjustmentstofeespaidbylowerincomegroups,andc)possibleadjustmentoffeesbyMSRP.Allcasesrequirethesametotalrevenuetargetraisedviathesevehiclefees,sotheyrepresentsixalternativewaystoraiseasetlevelofrevenuestopayforCVRPrebates.Thesixfeestructurescenariosallappearcapableofraising$200millionperyear,whichisalevelthatshouldbesufficienttopayforCVRPrebatesforZEVs,atleastthrough2018.Thepresentedscenariosallincludea$100minimumfeeonthosevehicleschargedafee,withvaryingmaximumfeesdependingontheindividualscenarioassumptions.Forexample,Scenario1appliesfeestothepurchaseofallnew(non-ZEVorTZEV)vehicles,withfeesincreasinginproportiontoeachmodel’stestedfueleconomy(convertedtoCO2emissions).Usingthe$100minimumfeeforpurchasingthelowestCO2-emittingcarsresultsin

vi

$210high-endfeeforthehighestemittingcars,whichwhenmultipliedacrosssalesof1.5millionvehicles,reachesthe$200millionrevenuetarget.InScenario2,thefeewasonlyappliedtocarsemittingover250gCO2/mile;allcarsbelowthisemissionslevel(mostlyhybridcars)areexempt.Inthatcase,thehighestemittingcarsarechargedafeeof$230.Inyetanotherscenario,feeswereonlyappliedtohouseholdswithannualincomesabove$75,000;lowerincomelevelhouseholdsareexempt.Thisraisesthehigh-endfeeto$413.Inall,Table1summarizesdevelopmentofthesixscenariosandcomparesthemintermsoffeesassessedbyhouseholdincomegroup.

i

Table1.Scenariooverview Scenario

DescriptionAverage

vehiclefeeAverage

vehiclefeefor

householdsearning<$75,000

Minimumvehiclefee

Maximumvehiclefee

Vehiclefeeat90th

percentile

Strengths Weaknesses

Scenario1 Allvehiclesandincomespay

$144 $143 $120 $210 $158 Lowestmaxfee Lowincomepayssameashighincome

Scenario2 Exemptvehiclesemittingbelow250gCO2/mile

$144 $145 $135 $230 $168 Onlyhigheremittingvehiclespay

TopfeehigherthanifallcarCO2levelspay;thoughnotmanycarsarebelow250gCO2/mile,sonotmuchdifferent

Scenario3 Exempthouseholdswithincomebelow$75,000

$152 $0 $186 $413 $267 Onlywealthierhouseholdspay

TopfeehigherthanifallHH’spay;somelowerincomeHH’sdobuyexpensivevehicles

Scenario4 Exempthouseholdswithincomesbelow$75,000,andvehiclesemittingupto400gCO2/mile

$150 $80 $150 $283 $198 LowerincomeHH’spayforhighCO2

vehicles,buthavemanychoiceswithnofee

Highertopfee,duetofewervehiclesincluded

Scenario5 MSRP-basedapproach,vehiclespayonlyifMSRPover$27,000

$150 $99 $193 $583 $390 Thosebuyingbelow-averagepricedcarsdonotpay

Somelowprice,highCO2carsareexempt;highaveragefeepriceforthosewhopay

Scenario6 MSRPbelow$27,000andemitbelow400gCO2/mile

$150 $111 $215 $519 $352 Belowaverageprice,lowCO2carsexempt

Hightopfeeforthosewhopay

i

Mainanalysisinsights:• Forthosehouseholdsbuyingnewcars,boththeexpenditurelevelpercarandtheaverage

CO2emissionspercarincreasesubstantiallyfromlowertohigherincomehouseholds.Wealthierhouseholdsbuymanymorevehiclesemittingover400gCO2/mile,althoughtheyalsobuymorevehiclesbelow200gCO2/mile(suchastheToyotaPrius).

• TocoverCVRPcostsofupto$200millionperyear(asignificantamountmorethanwhatwasspentin2015,andwithintheexpectedrequirementsthrough2018)theimplementationofanaveragefee,ontheorderof$140pernon-ZEV/TZEVcarwillbeneeded.Alternatively,aflat0.5%taxonvehiclepricewouldalsoachievethis.

• ThefeefordifferenttypesofcarswithdifferentCO2levels,andaveragefeesfordifferentincomehouseholdsvariesconsiderablydependingonscenarioassumptions.

• Feestructuresthatexemptverylow-CO2emittingcarsdonotchangetherelativefeeincidenceondifferentincomehouseholdssignificantly.

• Acrossthesixscenarios,thefeepercarpurchasedcanbezeroformanyhouseholds,butcanreachnearly$600forhouseholdsbuyingveryhighCO2vehicles.Theaveragefeeperhouseholdbuyinganewcardoesnotriseabove$150,evenforthewealthiesthouseholds,withasmallerfeeforlowerincomehouseholdsinseveralscenarios.

• Feelevelswouldneedtoriseasthetargetrevenuegenerationexceeds$200millionperyear,whichmayoccurfrom2019onwardtosupporthigherZEV/TZEVsaleslevels.

• Exemptinghouseholdsthatearnlessthan$75,000peryearshiftstheaveragefeeforotherhouseholdsfromabout$150uptoover$200pervehicle.Combiningthe$75,000incomeexemptionwitharequirementthatvehicleCO2bebelow400gCO2/miletobeexemptedresultsinabouta$50averagefeeforthoselowerincomehouseholds(withsomepayingnothingandotherspayingmorethan$100percar).

• Exemptingvehiclespriced(MSRP)lessthan$16,000hasarelativelysmalleffect,butsettingtheexemptionatanMSRPof$27,000hasasignificanteffect,since55%ofallnewvehiclespurchasedwerebelowthisprice.Inthiscase,householdaveragefeesriseindirectproportiontoincome.Also,requiringvehiclestohavelessthan400gCO2/miledoesnotsubstantiallychangethisresult.

• Overallitappearspossibletoconstructvehiclefeesystemsthatraise$200millionwithfairlyequalimpactsacrosshouseholdsofdifferentincomelevels,orwithsignificantlygreaterimpactsonhigherincomehouseholds,dependingonthedesign.Theaveragefeepervehiclesoldwouldlikelybeunder$150andthehighestfeespervehiclecouldbekeptbelow$250,dependingondesign.

Lookingoutto2025• Theresultsinthisstudy,focusedonraising$200millionperyear,areatmostrelevantto

theCVRPthrough2018.Afterthatyearandwiththecurrentincentivelevels,itislikelythatasZEVandTZEVsalesriserapidly,ascouldtherequiredrebateexpenditures.Ifthisoccurred,onefactorthatcouldbecomemorerelevantistheconsumerresponsetohigherper-vehiclefees,suchasshiftstolowerCO2vehicles.

ii

• Inthisproject,suchpotentialshiftsinvehiclepurchasesasaresultofthesixproposedfeestructureswerenotassessed.ThehighestratioofvehiclefeetovehicleMSRPinanyscenarioconsideredhereisabout1.8%,withanaverageratioofabout0.5%.Thisisnotexpectedtotriggerasignificantshiftinvehiclepreferencesorpurchasepatterns.However,ifrevenuerequirementsriseandfeesriseaccordingly,analysisofpotentialpurchaseshiftsrelatedtofeestructurescouldbecomeanimportantconsideration.PurchaseshiftstendtohelpincreasethesalesofZEVsandTZEVssincetheywillreceiverebates,whileothervehicleswouldbeassessedfees.Futureresearchcouldconsiderthisdynamic.

• Asimplifiedprojectionofthefeestructuresto2025,assumingslowgrowthinLDVsales(reachingabout1.8millionin2025,butwithrisingZEVandTZEVsalesandmarketsharesasforeseenintheCaliforniaZEVmandate,causesanincreaseinaveragefeesuptoover$700by2025.Thisalsoreflectsadeclineinthenumberofvehiclesthatwouldbeassessedfees,since22%ofvehiclesinthatyearareassumedtobeZEVorTZEV.Thisestimateisa“ballpark”estimate,sincea)thestructureofsalesandthenumberofvehiclessoldmaychangedramaticallyby2025,andb)feesapproaching$1,000pervehiclemaytriggerpurchaseshiftsthatshouldbetakenintoaccount.Afullanalysislookingoutto2025wouldbemuchmorecomplexthanthisstudy,butwouldbeusefulfollow-onresearch.

PotentialFutureResearch

ThisprojecthasundertakenwhatcouldbecalledfirststepsofresearchininvestigatingpossiblefundingsystemsfortheCVRP.Follow-upresearchcouldincludeanumberofactivities,including:

• CreatingamoredetailedprojectionofCaliforniavehiclesalesto2025byhouseholdtype,incorporatingexpectedevolutionofincomeanddemographiccharacteristicsaswellaschangingvehicletechnologiesandpotentialreductionsinnewconventionalvehicleCO2levels.

• Alsofora2025projection,applyingmarketpurchaseresponsefunctionstochangesinvehicleprices,usinganappropriatevehiclemarketmodel.

• Investigationofotherrevenueraisingconceptsandtheirequityimpacts,suchasannualregistrationfeesacrossallownedvehicles(notjustnewones)orvehiclein-usefees(e.g.fuelpricing,roadpricingorVMTfees)thatcouldberelatedbothtoCO2emissionsandtoelectricv.non-electricdriving.

• Broadeningthegeographicscopeoftheworktoincludeotherstatesornationallevelanalysis(suchasanationalfeebate).

3

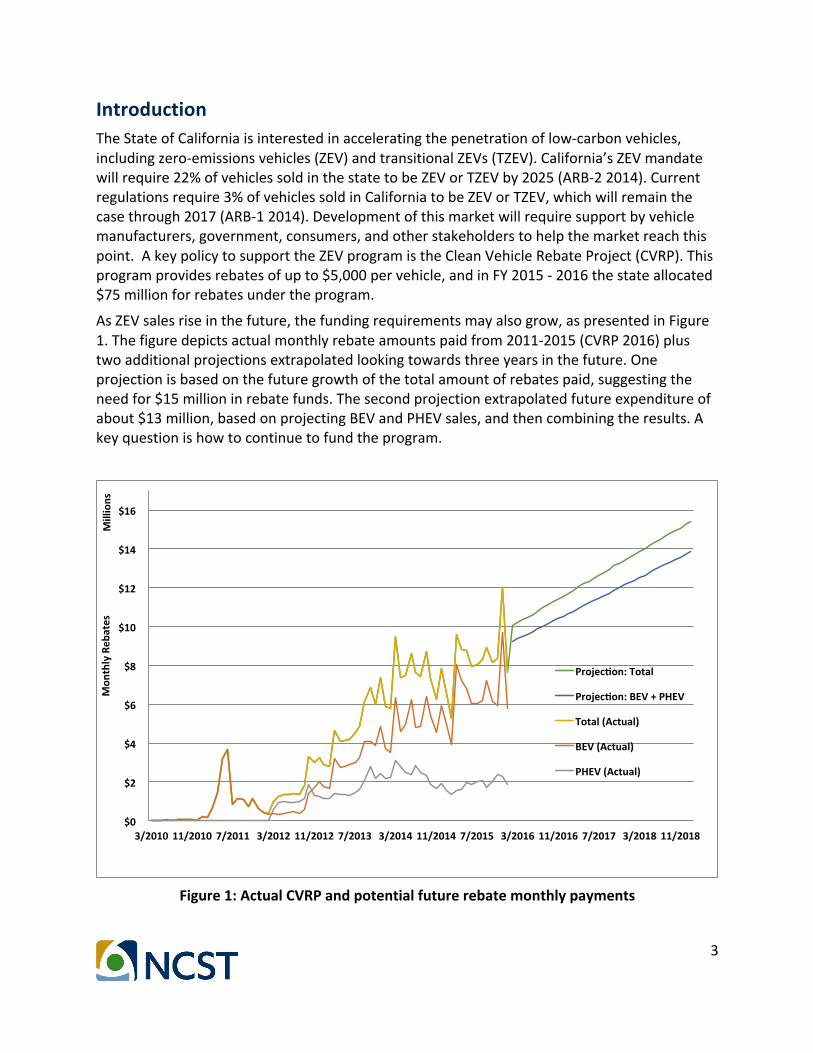

IntroductionTheStateofCaliforniaisinterestedinacceleratingthepenetrationoflow-carbonvehicles,includingzero-emissionsvehicles(ZEV)andtransitionalZEVs(TZEV).California’sZEVmandatewillrequire22%ofvehiclessoldinthestatetobeZEVorTZEVby2025(ARB-22014).Currentregulationsrequire3%ofvehiclessoldinCaliforniatobeZEVorTZEV,whichwillremainthecasethrough2017(ARB-12014).Developmentofthismarketwillrequiresupportbyvehiclemanufacturers,government,consumers,andotherstakeholderstohelpthemarketreachthispoint.AkeypolicytosupporttheZEVprogramistheCleanVehicleRebateProject(CVRP).Thisprogramprovidesrebatesofupto$5,000pervehicle,andinFY2015-2016thestateallocated$75millionforrebatesundertheprogram.

AsZEVsalesriseinthefuture,thefundingrequirementsmayalsogrow,aspresentedinFigure1.Thefiguredepictsactualmonthlyrebateamountspaidfrom2011-2015(CVRP2016)plustwoadditionalprojectionsextrapolatedlookingtowardsthreeyearsinthefuture.Oneprojectionisbasedonthefuturegrowthofthetotalamountofrebatespaid,suggestingtheneedfor$15millioninrebatefunds.Thesecondprojectionextrapolatedfutureexpenditureofabout$13million,basedonprojectingBEVandPHEVsales,andthencombiningtheresults.Akeyquestionishowtocontinuetofundtheprogram.

Figure1:ActualCVRPandpotentialfuturerebatemonthlypayments

!$0!!

!$2!!

!$4!!

!$6!!

!$8!!

!$10!!

!$12!!

!$14!!

!$16!!

3/2010! 11/2010! 7/2011! 3/2012! 11/2012! 7/2013! 3/2014! 11/2014! 7/2015! 3/2016! 11/2016! 7/2017! 3/2018! 11/2018!

Mon

thly!Reb

ates!

!Millions!

Projec>on:!Total!

Projec>on:!BEV!+!PHEV!

Total!(Actual)!

BEV!(Actual)!

PHEV!(Actual)!

4

Onepotentialmechanismtodothisisbyapplyingafeetothesalesofnon-ZEV/TZEVvehicles.Afeestructurecanbeapowerfulmechanism,sincethispolicyapproachcangenerateasustainablerevenuestreamtosupporttheneededincentivesandrelatedexpenses,andcanalsodirectlyencourageconsumerstobuyZEVsviathepricesignalstheyprovideinthemarketplace.Additionally,feestructureshavethepotentialtoaddressequityimplicationsconcerningpolicymakersaboutcurrentfederalandstateincentives,andthefundingsourcesoftheseincentives.ThisstudybuildsontheITS-Davisfeebatestudyconductedduring2008to2010(BunchandGreene,2010)byexploringfeestructurescenarioalternativesintermsoftheirimpactondifferenttypesofvehiclesandhouseholdsinCalifornia.Thisprojectfocusesonanear-termdistributionalimpactanalysisoftheincidenceofdifferentfeestructuresondifferenthouseholds(brokenoutbyincomegroups),withoutlookingatmorecomplexfeestructureissuessuchasvehiclemanufacturerresponsesorconsumerpurchaseresponses.Further,thedatausedinthisprojectfocusesontherecentnewcarmarket(basedon2011-2013data)andhowthedifferentfeestructureswouldimpactthismarket.(Amoreforwardlookinganalysis,withprojectionsofhouseholdincome,purchasepatternsandZEV-relatedfeesandrebatesoutto2025couldbeconsideredasafollow-onstudy.)Thisreportincludesabriefreviewofrecentresearchonfeebatesandvehiclefee-relatedpolicies(particularlytheBunchandGreene(2010)studythatincludedCaliforniainitsanalysis),areviewoftherelevantCaliforniapolicycontext,asnapshotofrecentCaliforniahouseholdcharacteristics(andincomedistributionalaspects),andananalysisofsixdifferenttypesofpotentialfeestructuresbasedonnewcarpurchasesthatappearcapableofraisingenoughrevenuetofundtheCVRP,atleastintheshorttermthrough2018.Finally,potentialextensionsofthisanalysisareidentified,includingmakingprojectionsto2025thatcouldbeundertakeninafollow-onproject.

ABriefReviewofRelevantLiteratureManystudieshaveassessedthepotentialforfeestructurestoimpactvehiclesales,energyuse,andCO2emissions.Somestudieshaveusedmodelingapproaches(e.g.BunchandGreene,2010)andsomehaveassessedexistingfeestructureprograms(mostlyinEurope).Thecurrentresearchonfeestructuresgenerallysuggeststhatfeesystemsprovidepowerfulincentivestovehiclepurchaserstoshifttomoreefficient,lowercarbonvehiclesandtovehiclemanufacturerstoproducesuchvehicles,asevidenceintheUnitedKingdom(Brand,etal,2011)andIreland(RoganandDennehy,etal,2011).BunchandGreeneprovideadetailedreviewintheirreport;therearealsoanumberofpapersonEuropeanfeestructuresystems.TheBunchandGreene(2010)studyisespeciallyrelevantforthecurrentprojectsinceitcoveredtheCaliforniaandU.S.light-dutyvehicle(LDV)market.Theirpaperusedfeebates,acombinationoffeesandrebatesbasedonvehicleemissions,anddeterminedthatarangeofdifferentfeebatescouldsignificantlyreducegreenhousegas(GHG)emissionsinCalifornia,with

5

othernetpositivesocietalbenefitssuchasreducedvehiclelifetimefuelcosts.However,implementingafeebatepolicyonlyinCaliforniawillcreateasystemthatlackstheleveragetochangetheproductionplansofmanufacturerssignificantly,aswellasthebuyinghabitsandpreferencesoftherestofthenation.Anation-widepolicyhasgreaterpotentialtoreduceCO2emissions.BunchandGreenealsofoundthatdesigningafeebateprogramtobearevenueneutralsystemischallengingsinceitinvolvespredictingpurchasingpatternswithperiodicadjustmentstothefeebate.TheydidnotlookspecificallyatfeebateprogramsinvolvingZEVsorthecurrentCVRPprogram,sincetheirstudywasundertakenpriortothecurrentCVRPprogram.RecentstudiesinSwedenandNorwayprovedbeneficialinaidingrebatesforlow-emittingvehicles.Europetendstofavorcompactvehicles.However,largervehiclestendtodominateSweden’sroads.This,alongwithaEuropeanUniondirectivestatingthattheaverageCO2emissionsfornewcarsmustbelessthan200gCO2/mileby2015and153gCO2/mileby2021(EuropeanCommission2015),hasmotivatedSwedentomakechanges.Sweden’sgoalistohaveafossilindependentcarfleetby2030andtobefossilfreeby2050.A2015Swedishstudy(Habibi,Hugosson,etal,2015)basedonthe2013carfleetlookedatfourdifferentfeestructures(referredtoasbonus-malus)andwaystoincorporateemissionsfeesasdifferenttaxes.Theirresultsshowthatconsumerswillnotchangepurchasingdecisionsbasedonafeeassessment,andwillcontinuetopurchasetheirvehicleofchoice.Swedenalsodidnotachievetheiremissionsgoals.However,thebonus-malusissuccessfulingeneratingenoughmoneytofundtherebateportion.ThestudysuggestsSwedenneedsadditionalpoliciesinordertoreachitstargetemissionsgoalsandfindwaystomotivateconsumerstopurchasecleanervehicles.Norwayfacessimilaremissionsproblemssinceitwitnessedanincreaseinpersonalvehiclesandvehiclemilestraveled.Duetotheseincreases,Norway’svehicleemissionsare30%higherthannumbersrecordedin1990.A2014studylookedatNorway’s2007vehicleregistrationtaxreform(Ciccone2014),whichaimstoreduceemissionsbydisincentivizinghighemittingvehicles.Norwaydoesnotmanufactureanycars,soitmustimplementpoliciesinordertobeeffectiveatreducingvehicleemissions.Norway’semissionstaxisattimeofpurchase,andismosteffectivebecausetheirconsumersaretypicallyswayedbyprice.Previoustaxeswerebasedonengine-size,buthavebeenupdatedtoreflectCO2emissions.Norway’sbonus-malusispoliticallyacceptablebecauseitsgoalisrevenueneutrality.In2007,theaveragecaremitted257gCO2/mile.Norwaysuccessfullyreducedemissionsofnewvehiclesby10gCO2/milewhenthepolicywasfirstenactedin2007.Researchersestimatethiswaspartiallyduetoa23%increaseinthemarketshareofdieselcarsanda12%decreaseinthemarketshareforhigh-emittingvehicles,aswellasimprovementsinfueleconomy.WhatisclearisthatwiththecurrentCVRPpurchaseincentiveprogramforZEVandTZEVvehicles,afeestructureoverlaidonthiscouldprovide:revenuestohelppayfortheexistingincentives,andastrongerincentiveforconsumerstoshifttheirpurchasestoloweremittingvehicleswithincentives(sincemorevehicleswouldalsohavefeesassociatedwiththeirpurchase).

6

AnelementmissinginBunchandGreene,aswellasotherstudies,isananalysisofthepotentialimpactofdifferentfeestructuresondifferenttypesofhouseholds(intermsofincome,purchasepatterns,orothercharacteristics).ThisprojectinvestigatesthisquestionandprovidesaninitialanalysisoffeestructuresintheCaliforniacontext,providingacontributionthatbuildsonthispreviouswork.

CurrentCaliforniaPolicyCaliforniahasarangeofcurrentpoliciesthatincentivizepurchasinglow-emittingpersonalvehicles.TheseincludetheCVRPandrelatedbillsAB118andSB1275,amongothers.ARB’sLowCarbonTransportationandAQIP(AirQualityImprovementProgram)fundtheCVRP,whichisthecurrentsourceforplug-invehiclerebates.ForFY2015-2016,theCaliforniaAirResourcesBoard(ARB)allocated$75millioninrebates,andhasalreadyrunoutoffunding.CVRPincentivesareasfollows:ZEVspoweredonlybyabattery(BEVs)andproducenotailpipeemissionsqualifyforarebateof$2,500,FuelCellElectricVehicles(FCEVs)receive$5,000,andPlug-inHybridElectricVehicles(PHEVs)receivea$1,500rebate.SenateBill1275,TheChargeAheadCaliforniaInitiative,aidslower-incomecarbuyersintheireffortstosupporttheenvironmentandpurchasecleanvehicles.ThebillplacesacaponthemaximumallowableannualhouseholdincomeeligiblefortheCVRP.IncomethresholdsbasedontaxreturnsrequireZEVrebateeligibilitybasedonsinglefilersearninglessthan$250,000,$340,000forheadofhouseholds,and$500,000forfilingjoint,whichwentintoeffectinMarch2016.HouseholdspurchasingFCEVsarenotsubjecttotheincomecapforthefirstthreeyearsofthebill.Additionally,thelawincreasestherebateamountforlower-incomehouseholdsby$1,500.Furthermore,SB1275givesauthoritytoARBtodecreaserebateamountsasnecessary,inordertocontinueincentivizingcleanvehiclepurchases.AstheZEVmarketgrows,ARBsuggeststherebateamountswilldiminish,thoughincentivizingpurchasesisimportanttoenticeconsumerstobuythesevehiclesinordertomeettheZEVmandaterequirements.ThevehicleincentiveamountsbytypeofvehicleandhouseholdincomeareshowninTable2.

7

Table2.SummaryofCVRPincentiveamountsunderSB1275

Source:ARB2015

AnalysisApproachThisfeestructureanalysisfocusesnotonfuturepotentialstructuresofrebatesundertheCVRPorrelatedprograms,butinsteadonpotentialfeesonnon-ZEV/TZEVsthatcouldbedeployedtocoverrebatecostsundertheCVRP.Thisstudyalsodoesnotestimatemarketresponsestothevariousfeestructuresconsidered,butfocusesonassessingandreportingtheincidenceoftheparticularfeestructuresondifferenttypesofcarsanddifferenthouseholdincomecategories.Thisanalysisisbasedonhistoricaldata.Noprojectionshavebeenmadeatthistime,thoughthatwouldbeanextphaseoftheanalysis.ThegoalistofirstunderstandthecurrentandrecentnatureofvehiclepurchasesacrossdifferenthouseholdincomesforpotentialCVRPcostsinthenextfewyears,beforelookingoutto2020andbeyond.Datausedforthisanalysiswascollectedfromthe2010-2012CaliforniaHouseholdTravelSurvey(CHTS).Therewere42,431householdswhocompletedthesurvey,dividedinto10incomegroups,andencompassingover70,000vehicles.Asubsetwascreatedbasedonnewvehiclepurchases,encompassingModelYear2011-2013vehicles.Some2013vehiclesareincludedinthissurveysincetheywereavailableforpurchaseattheendof2012.Thesubsetrepresentsabout13%ofallCHTShouseholds.NotmanyTZEVsandZEVsweresoldintheseyears.Asaresult,thestudyfocusesontherestofthevehiclemarket,andlooksatfeestructuresonthesenon-TZEVsandnon-ZEVsthatwouldraiseenoughrevenuetopayforalltherebatesactuallydistributedbytheCVRP.Itisestimatedtorequire$200million(arough

8

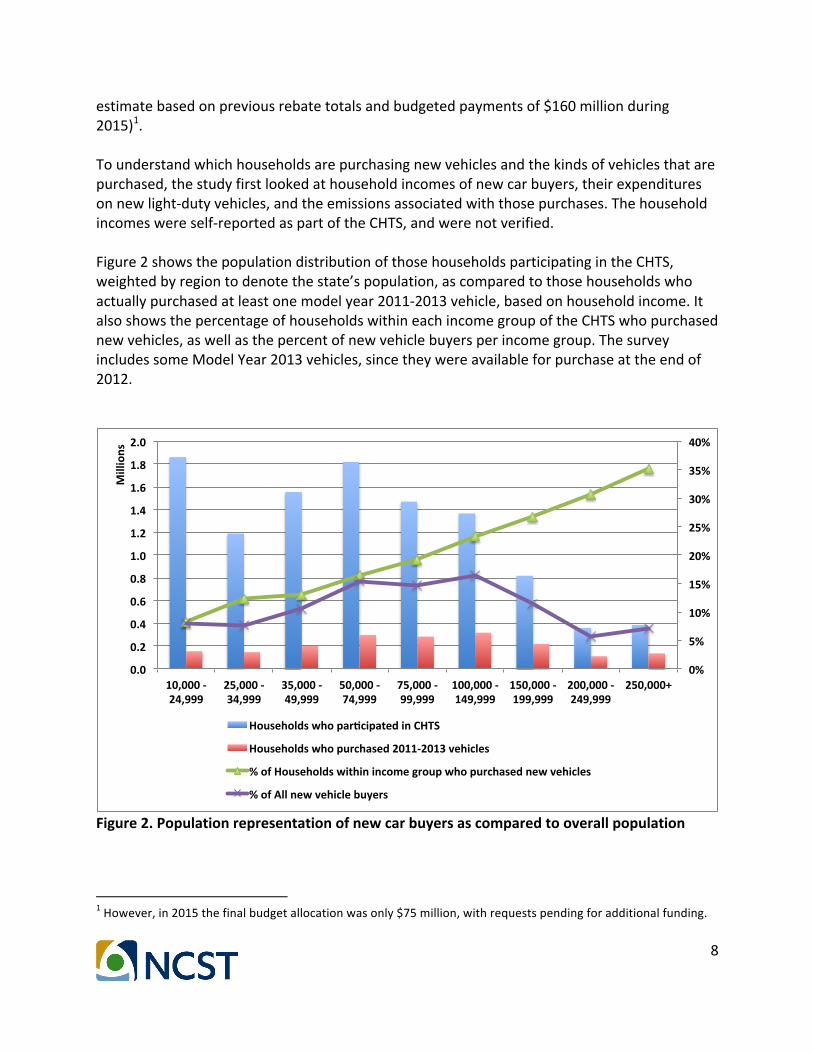

estimatebasedonpreviousrebatetotalsandbudgetedpaymentsof$160millionduring2015)1.Tounderstandwhichhouseholdsarepurchasingnewvehiclesandthekindsofvehiclesthatarepurchased,thestudyfirstlookedathouseholdincomesofnewcarbuyers,theirexpendituresonnewlight-dutyvehicles,andtheemissionsassociatedwiththosepurchases.Thehouseholdincomeswereself-reportedaspartoftheCHTS,andwerenotverified.Figure2showsthepopulationdistributionofthosehouseholdsparticipatingintheCHTS,weightedbyregiontodenotethestate’spopulation,ascomparedtothosehouseholdswhoactuallypurchasedatleastonemodelyear2011-2013vehicle,basedonhouseholdincome.ItalsoshowsthepercentageofhouseholdswithineachincomegroupoftheCHTSwhopurchasednewvehicles,aswellasthepercentofnewvehiclebuyersperincomegroup.ThesurveyincludessomeModelYear2013vehicles,sincetheywereavailableforpurchaseattheendof2012.

Figure2.Populationrepresentationofnewcarbuyersascomparedtooverallpopulation

1However,in2015thefinalbudgetallocationwasonly$75million,withrequestspendingforadditionalfunding.

0%#

5%#

10%#

15%#

20%#

25%#

30%#

35%#

40%#

0.0#

0.2#

0.4#

0.6#

0.8#

1.0#

1.2#

1.4#

1.6#

1.8#

2.0#

10,000#-#24,999#

25,000#-#34,999#

35,000#-#49,999#

50,000#-#74,999#

75,000#-#99,999#

100,000#-#149,999#

150,000#-#199,999#

200,000#-#249,999#

250,000+#

Millions#

Households#who#par@cipated#in#CHTS#

Households#who#purchased#2011-2013#vehicles#

%#of#Households#within#income#group#who#purchased#new#vehicles#

%#of#All#new#vehicle#buyers#

9

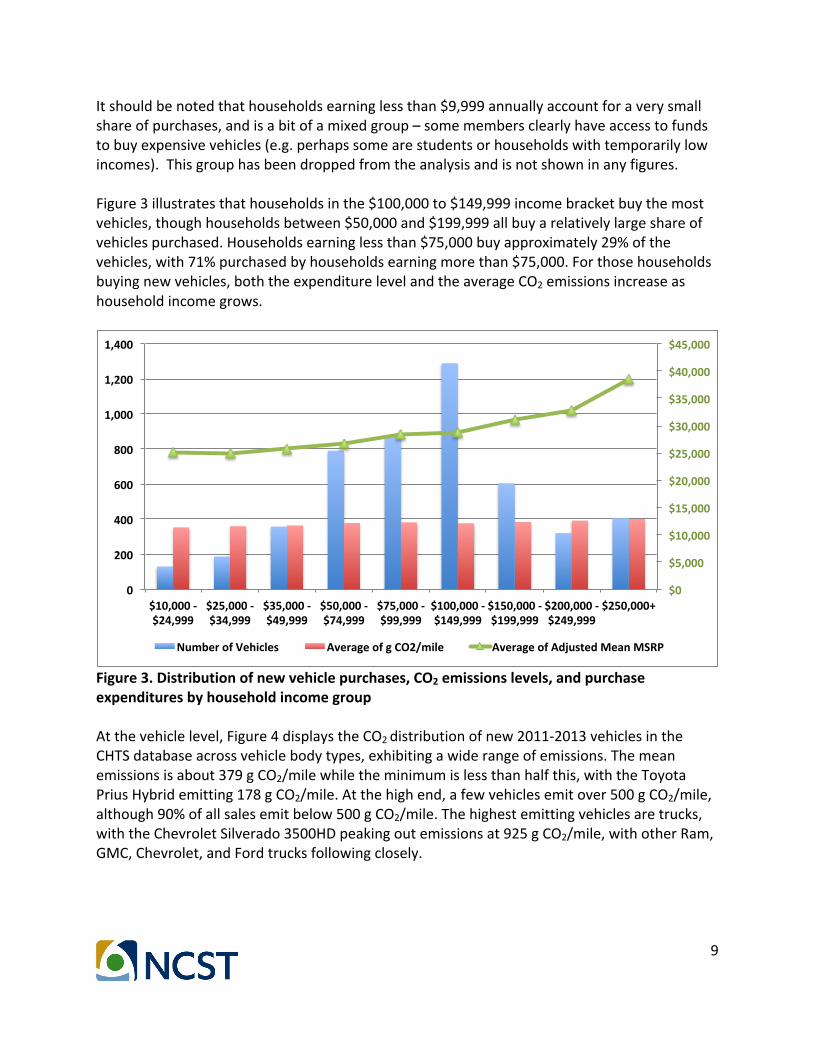

Itshouldbenotedthathouseholdsearninglessthan$9,999annuallyaccountforaverysmallshareofpurchases,andisabitofamixedgroup–somemembersclearlyhaveaccesstofundstobuyexpensivevehicles(e.g.perhapssomearestudentsorhouseholdswithtemporarilylowincomes).Thisgrouphasbeendroppedfromtheanalysisandisnotshowninanyfigures.Figure3illustratesthathouseholdsinthe$100,000to$149,999incomebracketbuythemostvehicles,thoughhouseholdsbetween$50,000and$199,999allbuyarelativelylargeshareofvehiclespurchased.Householdsearninglessthan$75,000buyapproximately29%ofthevehicles,with71%purchasedbyhouseholdsearningmorethan$75,000.Forthosehouseholdsbuyingnewvehicles,boththeexpenditurelevelandtheaverageCO2emissionsincreaseashouseholdincomegrows.

Figure3.Distributionofnewvehiclepurchases,CO2emissionslevels,andpurchaseexpendituresbyhouseholdincomegroupAtthevehiclelevel,Figure4displaystheCO2distributionofnew2011-2013vehiclesintheCHTSdatabaseacrossvehiclebodytypes,exhibitingawiderangeofemissions.Themeanemissionsisabout379gCO2/milewhiletheminimumislessthanhalfthis,withtheToyotaPriusHybridemitting178gCO2/mile.Atthehighend,afewvehiclesemitover500gCO2/mile,although90%ofallsalesemitbelow500gCO2/mile.Thehighestemittingvehiclesaretrucks,withtheChevroletSilverado3500HDpeakingoutemissionsat925gCO2/mile,withotherRam,GMC,Chevrolet,andFordtrucksfollowingclosely.

$0#

$5,000#

$10,000#

$15,000#

$20,000#

$25,000#

$30,000#

$35,000#

$40,000#

$45,000#

0#

200#

400#

600#

800#

1,000#

1,200#

1,400#

$10,000#,#$24,999#

$25,000#,#$34,999#

$35,000#,#$49,999#

$50,000#,#$74,999#

$75,000#,#$99,999#

$100,000#,#$149,999#

$150,000#,#$199,999#

$200,000#,#$249,999#

$250,000+#

Number#of#Vehicles# Average#of#g#CO2/mile# Average#of#Adjusted#Mean#MSRP#

10

Figure4.CO2characteristicsandweighteddistributionfornewcars,2011-2013Theexpenditureeffect,showninFigure5,presentstheshareofpurchasesbyvehicleprice(ManufacturerSuggestedRetailPrice,MSRP)acrossdifferenthouseholdincomegroups.Asincomeincreases,householdspurchasemoreexpensivevehicles.Edmunds.comdataaddedMSRPvalues,waslinkedtotheCHTSsurveybycomparingself-reportedvehiclecharacteristicstotheEdmundsinformation,andthenadjustedto2011dollars.

Figure5.DistributionofnewvehicleadjustedMSRPperannualhouseholdincome

0"

50,000"

100,000"

150,000"

200,000"

250,000"

300,000"

350,000"

400,000"

150)200"

200)250"

251)300"

301)350"

351)400"

401)450"

451)500"

501)550"

551)600"

601)650"

651)700"

701)750"

751)800"

801)850"

851)900"

901)950"

g"CO2/mile"

wagon"

van"

SUV"

sedan"

pick)up"

minivan"

hatchback"

coupe"

converHble"

0%#

10%#

20%#

30%#

40%#

50%#

60%#

70%#

80%#

90%#

100%#

10,000#.#24,999#

25,000#.#34,999#

35,000#.#49,999#

50,000#.#74,999#

75,000#.#99,999#

100,000#.#149,999#

150,000#.#199,999#

200,000#.#249,999#

250,000+# All#Households#

Annual#Household#Income#

$55,000+#

$40,000.$55,000#

$34,000.$40,000#

$27,000.$34,000#

$19,000.$27,000#

$16,000.$19,000#

<$16,000#

11

ThetotalMSRPexpenditureasapercentageoftotalhouseholdincomeisdisplayedinFigure6.Therelationshipbetweenvehicleexpenditurechangesdrasticallyasincomeincreases.Thelowerincomehouseholdsspendmorethantheirincomewhenpurchasingnewvehicles.Forthosehouseholdsearninglessthan$75,000,53%oftheirincomewasspentonanewvehicle,whereashouseholdsearningmorethan$75,000used21%oftheirincomeonanewvehicle.Thisalsoassumesthevehiclewaspaidforinitsentiretyattimeofpurchaseandignoresthepossibilityofvehiclefinancing.

Figure6.ShareofnewvehicleexpenditurebytotalincomeFigure7showsCO2emissionsdistributionfromnewvehicles,whichwereassignedtoeightdifferentemissionscategories.Thereisashiftfrommodelsinthe300-400gCO2/milerangeintothe400-500gCO2/milerange,ashouseholdincomeincreases,mostvisibleasincomegrowsabove$150,000.

0%#

20%#

40%#

60%#

80%#

100%#

120%#

140%#

160%#

10,000#*#24,999#

25,000#*#34,999#

35,000#*#49,999#

50,000#*#74,999#

75,000#*#99,999#

100,000#*#149,999#

150,000#*#199,999#

200,000#*#249,999#

250,000+#

Share#of#MSRP#per#Household#Income#Group#

12

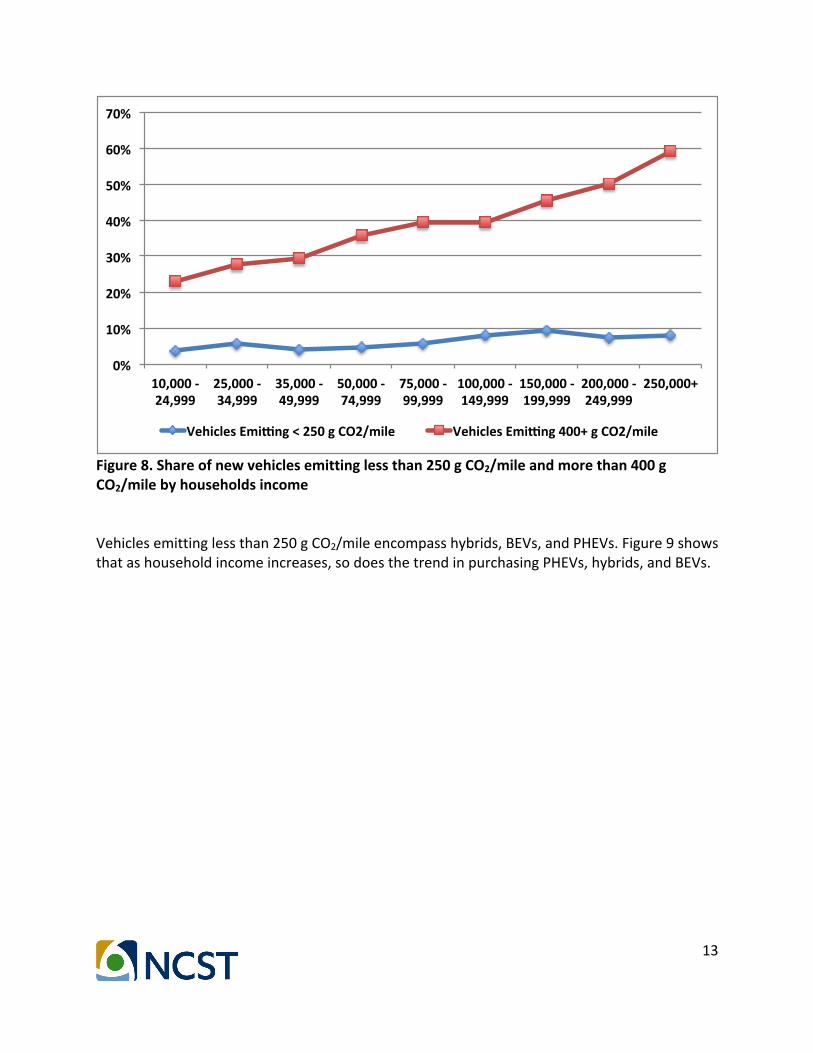

Figure7.DistributionofvehicleGHGemissions(gCO2/mile)perannualhouseholdincomeAlsonoticeable,inFigure8,aremodelsemittinglessthan250gCO2/mileperaremorecommoninthehigherincomehouseholds.Householdsearninglessthan$75,000purchase20%oftheselowemissionvehicles,withtheremaining80%purchasedbyhouseholdsearningmorethan$75,000.However,theneteffectonaverageCO2isrelativelyminor(asshowninFigure3),sincethenumberofhatchbacksandSUVsincreasedandpickuptrucksdecreaseinthehighestincomehouseholds.

0%#

10%#

20%#

30%#

40%#

50%#

60%#

70%#

80%#

90%#

100%#

10,000#.#24,999#

25,000#.#34,999#

35,000#.#49,999#

50,000#.#74,999#

75,000#.#99,999#

100,000#.#149,999#

150,000#.#199,999#

200,000#.#249,999#

250,000+# All#Households#

Annual#Household#Income#

500+#

450.500#

400.450#

350.400#

300.350#

250.300#

200.250#

<200#

13

Figure8.Shareofnewvehiclesemittinglessthan250gCO2/mileandmorethan400gCO2/milebyhouseholdsincomeVehiclesemittinglessthan250gCO2/mileencompasshybrids,BEVs,andPHEVs.Figure9showsthatashouseholdincomeincreases,sodoesthetrendinpurchasingPHEVs,hybrids,andBEVs.

0%#

10%#

20%#

30%#

40%#

50%#

60%#

70%#

10,000#,#24,999#

25,000#,#34,999#

35,000#,#49,999#

50,000#,#74,999#

75,000#,#99,999#

100,000#,#149,999#

150,000#,#199,999#

200,000#,#249,999#

250,000+#

Vehicles#Emi8ng#<#250#g#CO2/mile# Vehicles#Emi8ng#400+#g#CO2/mile#

14

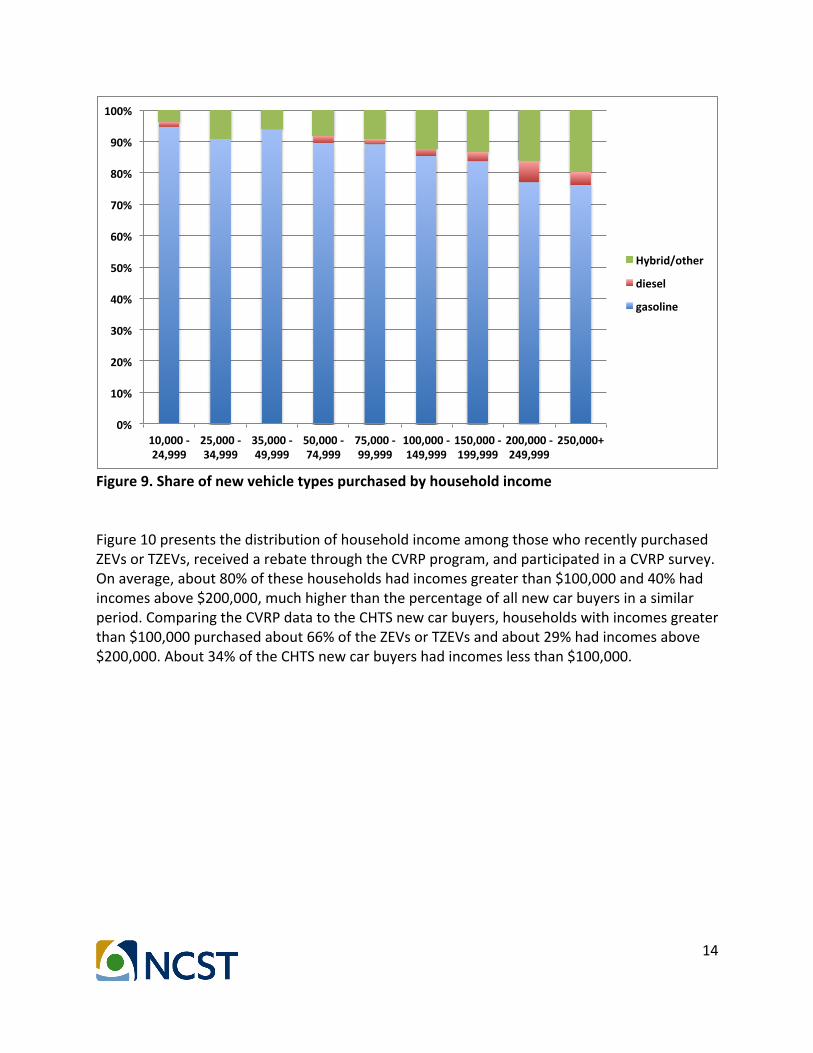

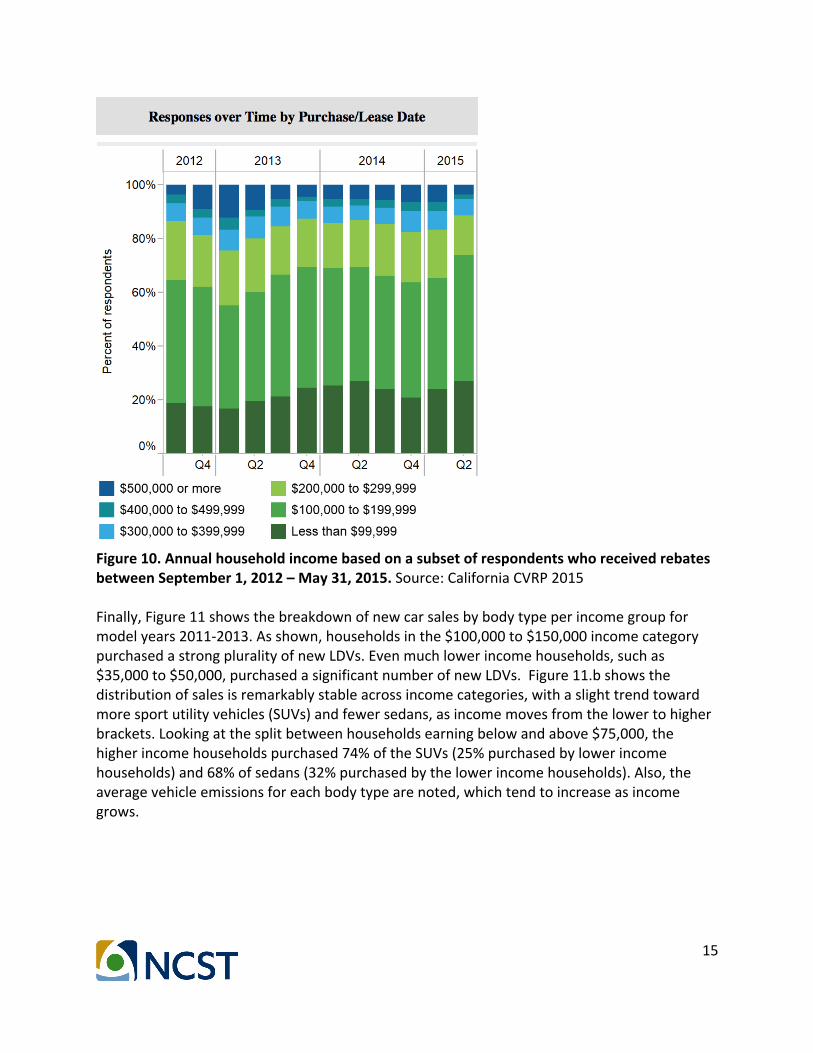

Figure9.ShareofnewvehicletypespurchasedbyhouseholdincomeFigure10presentsthedistributionofhouseholdincomeamongthosewhorecentlypurchasedZEVsorTZEVs,receivedarebatethroughtheCVRPprogram,andparticipatedinaCVRPsurvey.Onaverage,about80%ofthesehouseholdshadincomesgreaterthan$100,000and40%hadincomesabove$200,000,muchhigherthanthepercentageofallnewcarbuyersinasimilarperiod.ComparingtheCVRPdatatotheCHTSnewcarbuyers,householdswithincomesgreaterthan$100,000purchasedabout66%oftheZEVsorTZEVsandabout29%hadincomesabove$200,000.About34%oftheCHTSnewcarbuyershadincomeslessthan$100,000.

0%#

10%#

20%#

30%#

40%#

50%#

60%#

70%#

80%#

90%#

100%#

10,000#.#24,999#

25,000#.#34,999#

35,000#.#49,999#

50,000#.#74,999#

75,000#.#99,999#

100,000#.#149,999#

150,000#.#199,999#

200,000#.#249,999#

250,000+#

Hybrid/other#

diesel#

gasoline#

15

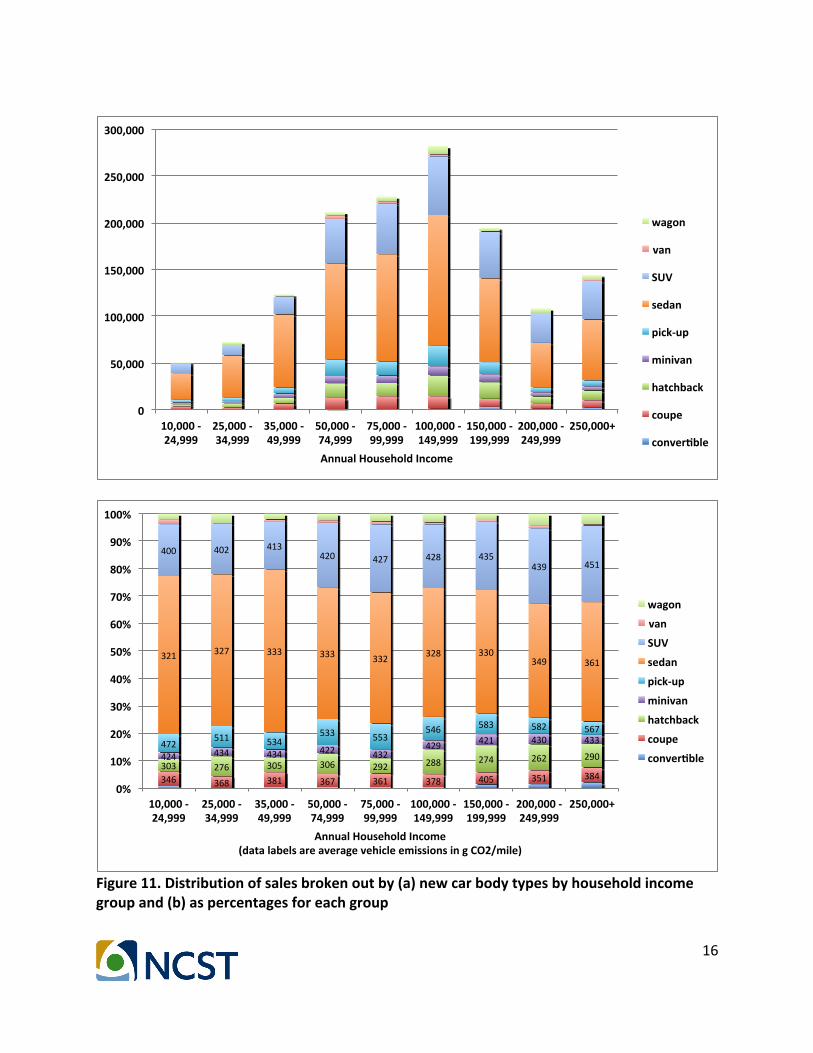

Figure10.AnnualhouseholdincomebasedonasubsetofrespondentswhoreceivedrebatesbetweenSeptember1,2012–May31,2015.Source:CaliforniaCVRP2015Finally,Figure11showsthebreakdownofnewcarsalesbybodytypeperincomegroupformodelyears2011-2013.Asshown,householdsinthe$100,000to$150,000incomecategorypurchasedastrongpluralityofnewLDVs.Evenmuchlowerincomehouseholds,suchas$35,000to$50,000,purchasedasignificantnumberofnewLDVs.Figure11.bshowsthedistributionofsalesisremarkablystableacrossincomecategories,withaslighttrendtowardmoresportutilityvehicles(SUVs)andfewersedans,asincomemovesfromthelowertohigherbrackets.Lookingatthesplitbetweenhouseholdsearningbelowandabove$75,000,thehigherincomehouseholdspurchased74%oftheSUVs(25%purchasedbylowerincomehouseholds)and68%ofsedans(32%purchasedbythelowerincomehouseholds).Also,theaveragevehicleemissionsforeachbodytypearenoted,whichtendtoincreaseasincomegrows.

16

Figure11.Distributionofsalesbrokenoutby(a)newcarbodytypesbyhouseholdincomegroupand(b)aspercentagesforeachgroup

0"

50,000"

100,000"

150,000"

200,000"

250,000"

300,000"

10,000"("24,999"

25,000"("34,999"

35,000"("49,999"

50,000"("74,999"

75,000"("99,999"

100,000"("149,999"

150,000"("199,999"

200,000"("249,999"

250,000+"

Annual"Household"Income"

wagon"

van"

SUV"

sedan"

pick(up"

minivan"

hatchback"

coupe"

converGble"

346$ 368$ 381$ 367$ 361$ 378$ 405$ 351$ 384$303$ 276$ 305$ 306$ 292$ 288$ 274$ 262$ 290$424$ 434$ 434$ 422$ 432$

429$ 421$ 430$ 433$472$511$ 534$

533$ 553$546$ 583$ 582$ 567$

321$ 327$ 333$ 333$ 332$ 328$ 330$349$ 361$

400$ 402$ 413$420$ 427$ 428$ 435$

439$ 451$

0%#

10%#

20%#

30%#

40%#

50%#

60%#

70%#

80%#

90%#

100%#

10,000#.#24,999#

25,000#.#34,999#

35,000#.#49,999#

50,000#.#74,999#

75,000#.#99,999#

100,000#.#149,999#

150,000#.#199,999#

200,000#.#249,999#

250,000+#

Annual#Household#Income#(data#labels#are#average#vehicle#emissions#in#g#CO2/mile)#

wagon#

van#

SUV#

sedan#

pick.up#

minivan#

hatchback#

coupe#

converOble#

17

AnalysisofAlternativeFeeStructuresAsdescribedabove,thedataanalyzedrepresentsvehiclesalesbetween2011and2013,andthecharacteristicsofthehouseholdsthatboughtthesevehicles.ThefundsgeneratedarebasedonthetotalpaidCVRPincentives.Varioustypesofvehiclefeestructuresweredevelopedtoexploretheimpactonequitywhileexcludinglowincomeorbelowaverage-pricedvehicles,basedonCO2emissions.Theanalysisobserveshowthesefeeswouldbedistributedacrosshouseholds,giventhehouseholdincomeandvehiclesalesdistributionsintheCHTS.Asimplecalculationrevealsthatifallnon-ZEVbuyerspaidthesamefee,thisfeewouldbeabout$140pervehicle.Buildingoffthissimplescenario,twobroadtypesofCO2-basedfeestructureswereexamined.Scenario1requiresallnon-ZEVpurchaserstopayafeedifferentiatedbyvehicleCO2.Scenario2exemptspurchasersofcarsemittingbelow250gCO2/milelevelfrompayinganyfee-effectivelya“donuthole”structuresincePHEVsreceivearebateundertheCVRP.Ahouseholdincomescenarioisalsoincludedintheanalysistotesttheeffectofexcludinglowerincomehouseholds,whereonlyhouseholdsearningmorethan$75,000peryearpayanyfeewhenbuyingacar(Scenario3).The$75,000annualincomethresholdwasselected,asitseparatedCHTSnewcarbuyersintoaboutequalhalves.Further,inScenario4,onlythosehouseholdsthatearnmorethan$75,000annuallyandpurchaseavehicleemittingmorethan400gCO2/milepayafee.Itwouldbedifficulttoaddincomeverificationtothefeeprocess,soMSRPscenariosarethesecondbestoptiontoreducetheburdenonlowerincomebuyers.InScenarios5and6,vehicleMSRPplayedaroleindeterminingwhichhouseholdspayafee.ThiswastoexaminewhetherexemptingvehicleswithMSRPlessthan$27,000wouldplacelessofaburdenonlowerincomehouseholds,andwhetherithasaneffectonfeespaidbyotherhouseholds.Thisthresholdwasestablishedbecauseitisbelow$29,000,theaverage-pricedvehicleinthedataset.Thecombinationofthesevariantscreatedsixseparatescenarios,asshowninTable3.Scenario4and6assessedallvehiclesemittingover400gCO2/mileafee,regardlessofincomeorMSRP.Thetypicalvehiclesexcludedbasedonemittinglessthan250gCO2/mileareamixtureofhybrids,someofwhicharetheHondaCivichybrid,ToyotaPrius,Smartfor2,amongothers.Commonvehiclesemittingover400gCO2/mileincludeminivans,SUVs,andpick-uptrucks.Thosecarsemittingover400gCO2/mileinclude76%ofthevehiclesforincomegroupsearningabove$75,000.

18

Table3.FeestructurescenariosconsideredScenarioDescription

CO2 Income MSRP

Scenario1 Allpay Allpay Allpay

Scenario2 Vehiclesemittinglessthan250gCO2/mileareexempt

---- ----

Scenario3 --- Exempthouseholdswithincomebelow$75,000

---

Scenario4 Vehiclesemittinglessthan400gCO2/mileareexempt

Exempthouseholdswithincomebelow$75,000

---

Scenario5 --- --- ExemptvehicleswithMSRPbelow$27,000

Scenario6 Vehiclesemittinglessthan400gCO2/mileareexempt

--- ExemptvehicleswithMSRPbelow$27,000

Inallscenarios,thegoalistogenerate$200millioninrevenuefortheCVRPrebates,withaminimumfeeof$100pernewvehicle,forthosevehiclesthatincurafee.The$200millionperyearshouldbesufficienttocoverCVRPcostsoverthenext3years,beforehighertotalrevenuestreamsmaybeneededasaresultofincreasedZEVsalesrequirements(whichwillbeaddressedinalaterphaseofthisanalysisthatlooksoutto2025).Theminimum$100pervehiclereflectstheideathatanyamountbelowthisismorenuisancethanusefulrevenuecollector.Inordertogeneratethetarget$200millionineachofthesixscenarios,themaximumfeepaidforthehighestCO2vehicleswasadjustedhigherorlower(thusaffectingtheslopeofthefeescheduleandthefeepaidforallcars)asneededtoachievethetargetedrevenue.TheCO2emissionsstartingfeeandtheincomelevelsofhouseholdsexemptfromthefeewerealsoadjustedupordowndependingonthescenario.Itisimportanttonoteatthistime,thatthepossibilitythefeeswillinanywayalterthechoicespeoplemakeofwhichvehicletopurchasewasnotconsidered.Excludingconsumerchoiceisamajorsimplification,sincetheapplicationofvehiclepurchasefeeswilllikelyaffectthecarmodelsthatpeoplepurchase.However,aswillbeseenbelow,thelevelsoffeenecessarytogeneratethetargetrevenuesconstitute0.5%ofthevehiclecost,andarelowenoughthatconsumerpurchaseshiftsinresponsearesmallandcanperhapsbeneglected.Athigherfees(neededforhigherrevenuetargetsandaslessnon-ZEV/TZEVvehiclesaresold),this

19

assumptionwillbecomemoreunrealistic.Thisissuewillbefurtherexploredinalaterphaseofstudy.

ResultsFigure12showsthemainresults,includingScenarios1and2,whereallhouseholdincomelevelsaresubjecttopayingafee,Scenarios3and4,whereincomeslevelsabove$75,000playaroleindeterminingwhichhouseholdspayanyfee,andScenarios5and6,whereMSRPabove$27,000playaroleindeterminingfees.Severalimplicationsoftheresultsareapparent.First,ifallhouseholdsaresubjecttopayandallnon-plug-invehicles(non-PEVs)aresubjecttoafee,anaveragefeeofaround$140perhouseholdisveryconstantacrosshouseholdincomegroups,becausetheaverageCO2

emissionsofthepurchasedvehiclespergroupissimilar.Thislowfeeistranslatedtoabout0.6%oftheyearlyincomeofa$25,000newcarbuyerto0.06%oftheyearlyincomeofa$250,000newcarbuyer.Exemptingvehicleswithemissionsbelow250gCO2/miledoesnotchangethisdistribution,astheshareofthosevehiclesislowforallincomegroups.ThisleadstoScenarios3and4.InScenario3,householdswithincomesbelow$75,000donotpay,andtheburdenshiftstohigherincomehouseholds.Theaveragefeesthosehouseholdspayingshiftstoover$200pervehicle.Scenario4alsohasthisincomethresholdandaddsanadditionalexemptionforvehiclesemittingbelow400gCO2/mile,resultinginabouta$50averagefeeforthoselowerincomehouseholds.Scenarios5and6bothareMSRP-focused.Scenario5exemptsvehicleswithMSRPbelow$27,000,whileScenario6addsanadditionalexemptionthatthosevehicleswithMSRPbelow$27,000mustalsoemitbelow400gCO2/mile.Thishasasignificanteffectsince55%ofthevehicleshaveanMSRPbelow$27,000.Thesescenariosmaybetterallocatetheburdenonthedifferentincomegroups,asthevehicleMSRPmaybeastrongerindicatorthanreportedincomeforthehouseholdeconomicsituation.AddingtheemissionsrequirementinScenario6doesnotdrasticallychangetheoutcome.Theaveragefeesperhouseholdtakeonalineareffect,withfeesincreasingasincomeincreases.

20

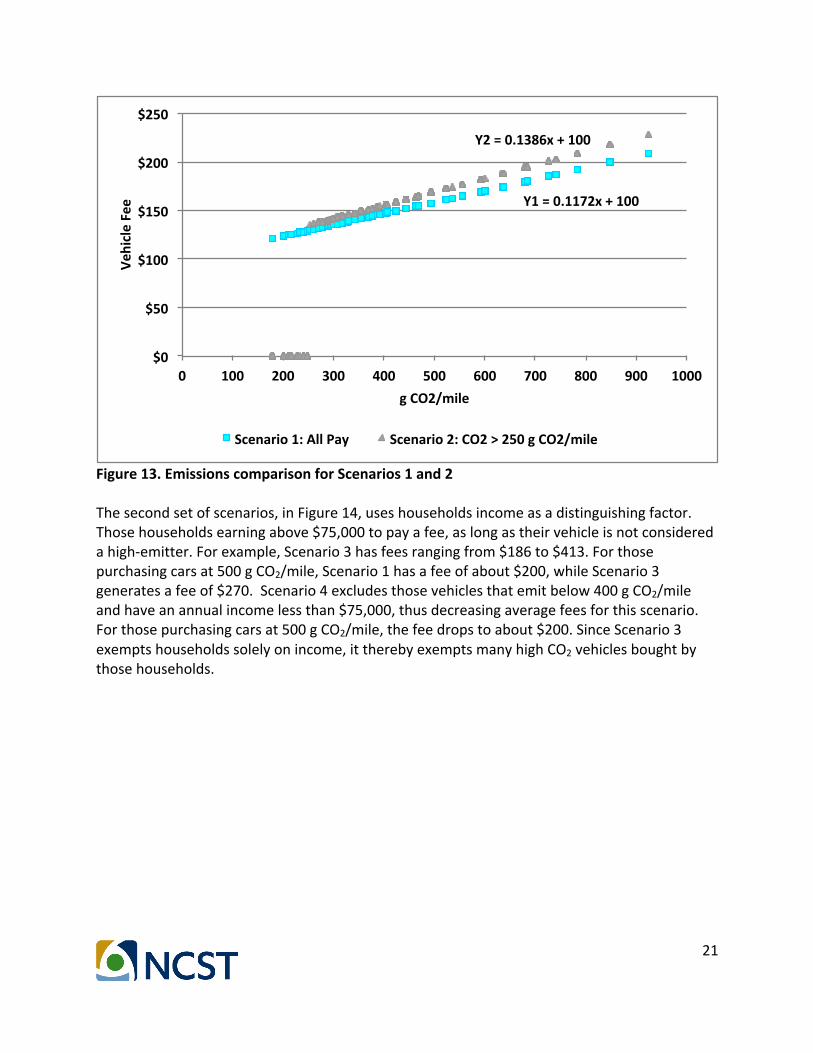

Figure12.AveragefeepervehicleperannualhouseholdincomeThefulldistributionoffeelevelsasafunctionofvehicleCO2levelsisshowninFigures13-15below.Figure13comparesScenario1,wherethefeestartsat177gCO2/mile(thebestnon-PHEV)toScenario2,wherethefeestartsat250gCO2/mile(exempting7%ofthenewvehicles).Withthefeestartingat177gCO2/mile,thefeeneedstorisetoabout$210forthehighestemittingvehiclesandthefeeneedstobeabout$160forthehighestemitters(500gCO2/mile)togeneratetheneeded$200million.Thustherevenuecanberaisedwith0.62%ofhouseholdspayingmorethan$200whenpurchasingavehicle.Withonlycarsaboveaminimumof250gCO2/milepayingafee,theupperlimitrisesfrom$208toabout$228andthefeeforcarsat500gCO2/mileisabout$170.

$0#

$50#

$100#

$150#

$200#

$250#

10,000#(#24,999#

25,000#(#34,999#

35,000#(#49,999#

50,000#(#74,999#

75,000#(#99,999#

100,000#(#149,999#

150,000#(#199,999#

200,000#(#249,999#

250,000+#

Average#Fee#pe

r#Veh

icle#

Annual#Household#Income#

Scenario#1:#All#Pay#

Scenario#2:#CO2#<#250#g#CO2/mile#exempt#

Scenario#3:#Income#<#$75k#exempt#

Scenario#4:#Income#<#$75k#and#CO2#<#400#g/mile#exempt##

Scenario#5:#Vehicles#MSRP#<#$27,000#exempt#

Scenario#6:#Vehicles#MSRP#<#$27,000#and#CO2#<#400#g/mile#exempt#

21

Figure13.EmissionscomparisonforScenarios1and2Thesecondsetofscenarios,inFigure14,useshouseholdsincomeasadistinguishingfactor.Thosehouseholdsearningabove$75,000topayafee,aslongastheirvehicleisnotconsideredahigh-emitter.Forexample,Scenario3hasfeesrangingfrom$186to$413.Forthosepurchasingcarsat500gCO2/mile,Scenario1hasafeeofabout$200,whileScenario3generatesafeeof$270.Scenario4excludesthosevehiclesthatemitbelow400gCO2/mileandhaveanannualincomelessthan$75,000,thusdecreasingaveragefeesforthisscenario.Forthosepurchasingcarsat500gCO2/mile,thefeedropstoabout$200.SinceScenario3exemptshouseholdssolelyonincome,ittherebyexemptsmanyhighCO2vehiclesboughtbythosehouseholds.

Y1#=#0.1172x#+#100#

Y2#=#0.1386x#+#100#

$0#

$50#

$100#

$150#

$200#

$250#

0# 100# 200# 300# 400# 500# 600# 700# 800# 900# 1000#

Vehicle#Fee#

g#CO2/mile#

Scenario#1:#All#Pay# Scenario#2:#CO2#>#250#g#CO2/mile#

22

Figure14.EmissionscomparisonforScenarios3and4,basedonannualhouseholdincomeAnalternativetoexemptinghouseholdsbasedonincomeisonebasedonvehicleMSRP.Thefinaltwoscenarios,Scenarios5and6(Figure15)useavehiclefeeexclusioniftheMSRPislessthan$27,000,representing55%ofthevehiclesintheCHTS.Scenario5onlylooksatprice,anditisevidentthatthisallowshigh-emittingvehiclestoavoidpayingafee.Therefore,arestrictioncanbeaddedtoalsoexemptvehiclesemittinglessthan400gCO2/milefrompayingafee,asdemonstratedinScenario6.Whenallvehiclescostingbelow$27,000areexempt,thehighestfeeonremainingvehiclesrisesto$583.Withanexemptionlimitatthe400gCO2/mile,themaximumfeedropsto$519.

Y3#=#0.3377x#+#100#

Y4#=#0.1978x#+#100#

$0#

$50#

$100#

$150#

$200#

$250#

$300#

$350#

$400#

$450#

0# 100# 200# 300# 400# 500# 600# 700# 800# 900# 1000#

Vehicle#Fee##

g#CO2/mile#

Scenario#3:#Income#>#$75k# Scenario#4:#CO2#>#400#g#CO2/mile#and#Income#>#$75k#

23

Figure15.EmissionscomparisonforScenarios5and6,basedonvehicleMSRPTable1showsasummaryofallsixscenarios,outliningtheaverageandtopvehiclefeesandashortdescriptionofstrengthsandweaknessesofeachapproach.Ofcourse,manymorecasesandscenarioscouldbecreated,buttheseprovidearoughideaofhowsomedifferent,andpotentiallyimportant,approachescompare.SummaryofFindingsandPolicyImplicationsTheforegoingalternativefeestructureanalysisforraising$200milliontopayfortheCVRPyieldsanumberofinsightsintermsoffeerequirements,impactsacrosshouseholds,andforpolicymakinginthisarea.Theseinclude:• Toraise$200millionwithavehiclefeesystem,theaveragefeewouldbealowpercentage

ofaveragevehiclepricesin2016(e.g.around$140outof$30,000+averagevehicleprice,lessthan0.5%).Italsoisnotasignificantshareofincomeformosthouseholdsthatbuyanewcar.

• ItshouldbepossibletocontinueincentivizingZEVandTZEVpurchasesundertheCVRPprogramwitharelativelysmall($140)averagefeeonnon-eligiblevehicles.

• ByfocusingthefeeonvehicleCO2emissions,thiscansendasignaltobuyersofthosevehiclesregardingtheCO2impactsoftheirpurchases.However,varyingfeestructuresbyhouseholdincomeorvehicleMSRPcanhaveasignificantimpactonthedistributionoffeesacrosshouseholdincomelevels.

Y5#=#0.5224x#+#100#

Y6#=#0.4533x#+#100#

$0#

$100#

$200#

$300#

$400#

$500#

$600#

$700#

0# 100# 200# 300# 400# 500# 600# 700# 800# 900# 1000#

Vehicle#Fee##

g#CO2/mile#

Scenario#5:#Vehicles#MSRP#<#$27,000#

Scenario#6:#Vehicles#MSRP#<#$27,000#and#CO2#<#400#g/mile#

24

• Excludingvehiclesemittingunder250gCO2/milehasasmallimpactontheaveragefeesforvehiclesemittingabove250gCO2/mile,butmaybeanimportantelementtoofferconsumerssomezerofeeoptionsandhighlightwhichmodelsachievethis.

• Feestructuresmaycreatepricedifferentialsforthesamemodelvehicle,dependingontheengineconfiguration(gasolineorPHEV).Thiswasnotexploredinthisstudy.

• Forthoselowerincomehouseholdsbuyinganewcar,alargeshareoftheirincomeappearstobeneededforthis(neglectingfinancingoptionstospreadoutcostsovertime).Suchhouseholdsmaybequitesensitivetoincentiveschemesforpurchasingcleanervehicles.

• Anyincentivesorfeesystemsshouldincludethisinformationaspartofthecarwindowstickersoitisobviousattimeofsale.

• Inthefuture,therewillbelessnon-ZEV/TZEVvehiclessold,asZEV/TZEVsalesincrease,sothefeelevelspernon-ZEV/TZEVwillneedtoincrease(apartfromincreasingasthetotalnumbersofincentivizedvehiclesincreases).

• Asvehicletechnologiesadvance,fueleconomywillincreaseandCO2emissionswilldecrease.ThiswouldimpacttheCO2thresholdsindicatedinthisstudy.FeesthatautomaticallyadjustwiththeaverageCO2levelsofnewcarswillhelpmaintainrevenuestreams.

• Whenexcludingbyincome,asinScenario3,33%ofnewcarswithaverageMSRPof$25,500andaverageemissionsof367gCO2/mileareexemptfrompayingafee.

• ExcludinglessthanaverageMSRP,likeScenario5,allowsthehigherincomehouseholds,whichmakesup63%ofthisgroup(oraboutone-thirdofallnewcarbuyers),tobeexemptfrompayingafee,butreducespolicycomplicationsandmaybebettercorrelatedwithpurchasingpower.

• Assessingfeesonvehiclesemittingover400gCO2/milemaybeanimportantmessage,butmayaddadditionalburdenonhouseholdswhorequirebiggervehicles.Thisresearchdidnottakeintoaccountfamilysize.

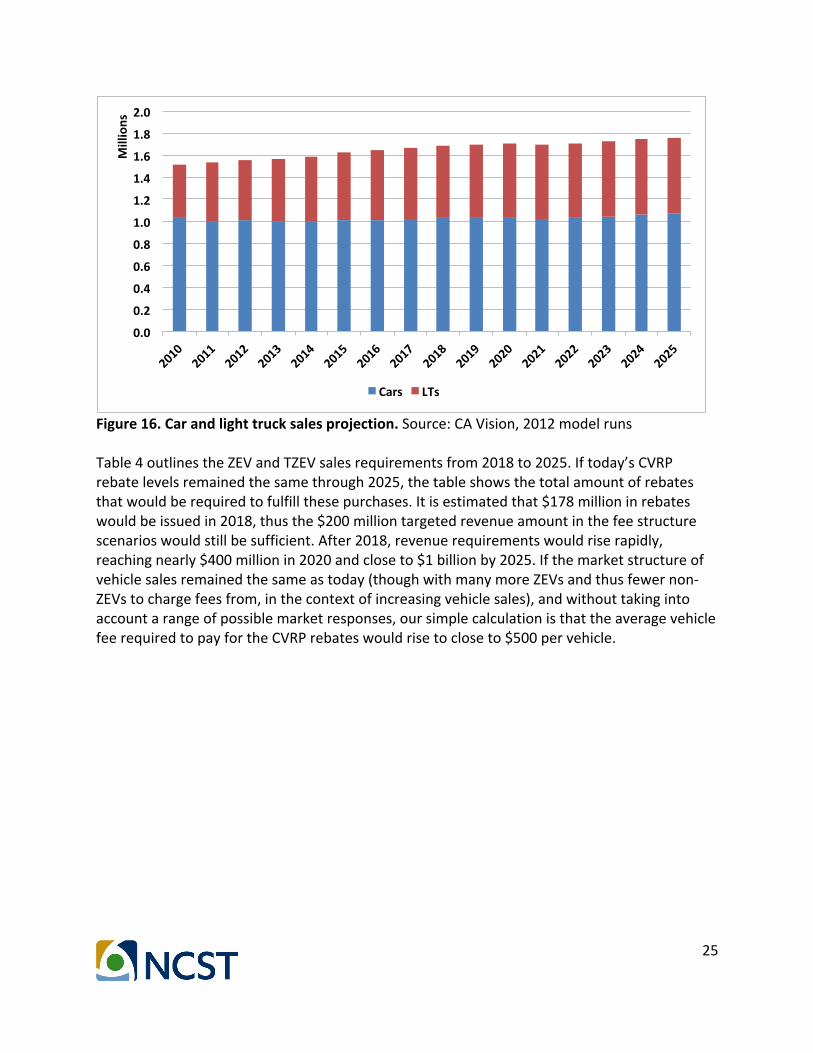

• Acombinationofsomescenariosmaybebetterthantheindividual6presented.Lookingtoward2025Althoughadetailedanalysisoffuturemarketevolution,incentiveexpendituresonZEVsandTZEVs,relatedrevenueneedsandpossiblefeestructuresarebeyondthescopeofthisreport,afewsimpleprojectionsandcalculationsareprovidedhere.Additionalresearchinthisarearepresentsanimportantpotentialfollow-upstudy.UsingARB’spreviousprojectionfromtheCaliforniaVision2012,basedonEMFAC(ARB’sEmissionsFactorsformobilesourcesdatabase),LDVsalesareprojectedtoincreasefromabout1.6millionin2015tonearly1.8millionin2025,anoverallincreaseof8%(comprisedofabouta7%increaseincarsalesand12%inlighttrucksales),asseeninFigure16.

25

Figure16.Carandlighttrucksalesprojection.Source:CAVision,2012modelrunsTable4outlinestheZEVandTZEVsalesrequirementsfrom2018to2025.Iftoday’sCVRPrebatelevelsremainedthesamethrough2025,thetableshowsthetotalamountofrebatesthatwouldberequiredtofulfillthesepurchases.Itisestimatedthat$178millioninrebateswouldbeissuedin2018,thusthe$200milliontargetedrevenueamountinthefeestructurescenarioswouldstillbesufficient.After2018,revenuerequirementswouldriserapidly,reachingnearly$400millionin2020andcloseto$1billionby2025.Ifthemarketstructureofvehiclesalesremainedthesameastoday(thoughwithmanymoreZEVsandthusfewernon-ZEVstochargefeesfrom,inthecontextofincreasingvehiclesales),andwithouttakingintoaccountarangeofpossiblemarketresponses,oursimplecalculationisthattheaveragevehiclefeerequiredtopayfortheCVRPrebateswouldrisetocloseto$500pervehicle.

0.0#

0.2#

0.4#

0.6#

0.8#

1.0#

1.2#

1.4#

1.6#

1.8#

2.0#

2010#

2011#

2012#

2013#

2014#

2015#

2016#

2017#

2018#

2019#

2020#

2021#

2022#

2023#

2024#

2025#

Millions#

Cars# LTs#

26

Table4.ProjectionofCVRPRebatesbasedonProgramtargetsandprojectedvehiclesales

ModelYears ZEVsRequiredProjectedLDV

sales(Vision2.0)(millions)

ZEVRebates(millions)

Averagefeepernon-ZEV

purchasedtopayforrebates

2018 2% 1.58 $79 $512019 4% 1.61 $161 $1042020 6% 1.62 $244 $1602021 8% 1.64 $327 $2172022 10% 1.66 $414 $2782023 12% 1.68 $503 $3412024 14% 1.70 $594 $4072025 15% 1.72 $644 $441

(Note:Totalrebatesbasedon$2,500pervehicleforZEVsthrough2025.)ResearchNextStepsPotentialFutureResearchThisprojecthasundertakenwhatcouldbecalledfirststepsofresearchininvestigatingpossiblefundingsystemsfortheCVRP.Follow-upresearchcouldincludeanumberofactivities,including:

1) CreatingamoredetailedprojectionofCaliforniavehiclesalesto2025byhouseholdtype,incomeand/ordemographiccharacteristics,andlinkingthisprojectiontotheZEVsalesrequirementsalongwithpotentialrequiredfundingforCVRP.ThisshouldalsotakeintoaccountchangingvehicletechnologiesandpotentialreductionsinnewconventionalvehicleCO2levels.Takingintoaccountsuchchangeswillenableabetterforward-lookinganalysisofdifferentfeestructures,inthecontextofrisingprogrambudgetneedsandchangingdemographicsandmarketenvironments.

2) Alsofora2025projection,applyingmarketpurchaseresponsefunctionstochangesinvehicleprices,suchasbyusingtheMA3Tmodel(amarketsimulationmodelcalledMarketAcceptanceofAdvancedAutomotiveTechnologies)oranothermodel.Asfeeandrebatelevelspervehiclerise,thelikelihoodofasignificantconsumerresponsewouldalsorise,andthusshouldnotbeneglected.Infact,consumerresponsetofeesandrebatescouldstrengthentheZEVprogrambyhelpingincreasedemandforZEVandTZEVsalesanddecreasingfundingrequirements,apotentiallyimportantdynamic.

3) Investigationofotherrevenueraisingconceptsandtheirequityimpacts,suchasin-usefees(e.g.VMTfees)thatcouldberelatedtoelectricv.non-electricdriving.

4) Broadeningthegeographicscopeoftheworktoincludeotherstatesornationallevelanalysis(suchasanationalfeebate).

27

ReferencesBrand,Christian,JillianAnable,andMartinoTran."Acceleratingthetransformationtoalowcarbonpassengertransportsystem:Theroleofcarpurchasetaxes,feebates,roadtaxesandscrappageincentivesintheUK."TransportationResearchPartA:PolicyandPractice49(2013):132-148.Bunch,DavidS.,andDavidL.Greene.Potentialdesign,implementation,andbenefitsofafeebateprogramfornewpassengervehiclesinCalifornia:interimstatementofresearchfindings.InstituteofTransportationStudies,UniversityofCalifornia,Davis,2010.CaliforniaAirResourcesBoard(ARB-1).July10,2014.Zero-emissionvehiclestandardsfor2009through2017modelyearpassengercars,light-dutytrucks,andmedium-dutyvehicles.www.arb.ca.gov/msprog/zevprog/zevregs/1962.1_Clean.pdf.AccessedMarch29,2016.CaliforniaAirResourcesBoard(ARB-2).July10,2014.Zero-emissionvehiclestandardsfor2018andsubsequentmodelyearpassengercars,light-dutytrucks,andmedium-dutyvehicles.www.arb.ca.gov/msprog/zevprog/zevregs/1962.2_clean.pdf.AccessedSeptember6,2015.CaliforniaAirResourcesBoard(ARB).June25,2015.Proposedfiscalyear2015-2016fundingplanforlowcarbontransportationinvestmentsandtheairqualityimprovementprogram.www.arb.ca.gov/msprog/aqip/fundplan/proposed_fy15-16_funding_plan.pdf.AccessedNovember1,2015.CaliforniaCleanVehicleRebateProject(CaliforniaCVRP-1).2015.EligibleVehicleRebates.https://cleanvehiclerebate.org/eng/eligible-vehicles.AccessedNovember1,2015.CaliforniaCleanVehicleRebateProject(CaliforniaCVRP-2).2015.EVconsumersurveydashboard.http://energycenter.org/clean-vehicle-rebate-project/survey-dashboard.AccessedNovember1,2015.CaliforniaCleanVehicleRebateProject(CaliforniaCVRP).2016.CVRPRebateStatisticshttps://cleanvehiclerebate.org/eng/rebate-statistics.AccessedApril12,2016.Ciccone,Alice.IsitallaboutCO2emissions?TheenvironmentaleffectsofataxreformfornewvehiclesinNorway.No.19/2014.Memorandum,DepartmentofEconomics,UniversityofOslo,2014.EuropeanCommission.2015.ReducingCO2emissionsfrompassengercars.http://ec.europa.eu/clima/policies/transport/vehicles/cars/index_en.htm.AccessedNovember1,2015.

28

Habibi,Shiva,MurielBeserHugosson,PiaSundbergh,andStaffanAlgers.Evaluationofbonus-malussystemsforreducingcarfleetCO2emissionsinSweden.No.2015:6.CTS-CentreforTransportStudiesStockholm(KTHandVTI),2015.Liu,Changzheng,ElizabethCooke,DavidGreene,andDavidBunch."Feebatesandfueleconomystandards:impactsonfueluseinlight-dutyvehiclesandgreenhousegasemissions."TransportationResearchRecord:JournaloftheTransportationResearchBoard2252(2011):23-30.Rogan,Fionn,EmerDennehy,HannahDaly,MartinHowley,andBrianP.Ó.Gallachóir."Impactsofanemissionbasedprivatecartaxationpolicy–firstyearex-postanalysis."TransportationResearchPartA:PolicyandPractice45,no.7(2011):583-597.