Embed Size (px)

Citation preview

���������������

In our view, Emaar is probably one of the most misunderstood and undervalued USD20bn

market-cap companies that we cover globally. The stock is stuck at its post-2006 market-

crash level, mostly because of selling by retail investors. However, with the share-for-land

swap issue becoming a distant memory, we think institutional involvement and improving

corporate communication should lead to a strong recovery.

Last year, the market was euphoric about Abu Dhabi names (Aldar, Sorouh) and nervous

about an oversupply of real estate in Dubai. In reality, the two markets are essentially one. But

while Aldar and Sorouh have yet to build a track record, Emaar is a global player. The reward

is comparable (we see a 100% potential return for Emaar, c.75% for Aldar), the risk is not.

Colliers’ estimates suggest deliveries are being pushed back and scaled down. We think

that means the current housing shortage is here to stay at least until 2010. A negative real

rate environment (-8%) should further support the property market. And with c50% of

housing controlled by the government, supply can be managed to match demand.

Emaar is no longer just a Dubai story. Even if the market were to melt down in Dubai and the

company cancelled all future projects and halted construction on unsold developments,

theoretically only AED8.5 would be taken off our target price and AED6.4 off our estimated

2008 NAV. We believe the stock is currently trading at our estimated floor NAV of AED11.3.

We believe most of the negative news that we can think of is already in the price. The

shares-for-land swap has been called off. The struggling US business has only a marginal

effect on our valuation (AED0.1 per share). Negative earnings revisions (margins to

bottom in Q2 2008, we estimate) should be over. The Indian IPO was postponed and a

lower-than-expected dividend payout has already been made.

The current price seems to ignore potential margin recovery and foreign subsidiaries. We value

Emaar at AED23, implying a potential total return of 102%. Our 2008e NAV of AED17.7 per

share is at a 23% discount to our DCF value. We initiate with an Overweight (V) rating.

Overweight (V)

Target price (AED) 23.00 Share price (AED) 11.30 Potential total return (%) 103.5

Dec 2007a 2008e 2009e

HSBC EPS 1.08 1.10 1.70 HSBC PE 10.5 10.3 6.7

Performance 1M 3M 12M

Absolute (%) -22.1 -18.7 -15.0 Relative^ (%) -17.3

Note: (V) = volatile (please see disclosure appendix)

20 February 2008

Walid Khalfallah* Analyst HSBC Bank Middle East Ltd +971 4 5077458 [email protected]

Majed Azzam* Analyst HSBC Bank Middle East Ltd +971 4 5077380 [email protected]

Ankur Khetawat* Associate, Bangalore

View HSBC Global Research at http://www.research.hsbc.com

*Employed by a non-US affiliate of HSBC Securities (USA) Inc, and is not registered/qualified pursuant to NYSE and/or NASD regulations

Issuer of report: HSBC Bank Middle East Ltd

Disclaimer & Disclosures This report must be read with the disclosures and the analyst certifications in the Disclosure appendix, and with the Disclaimer, which forms part of it

Real Estate Equity – United Arab Emirates

Company report

Enterprise value (AEDm) 65169 Free float (%) 68 Market cap (USDm) 18,742 Market cap (AEDm) 68,831

Source: HSBC

Index^ DUBAI FINL MKT IDX Index level 5707.32 RIC EMAR.DU Bloomberg EMAAR UH

Source: HSBC

Emaar Properties PJSC

Overlooked for much too long: initiating coverage with a target price of AED23 and an Overweight (V) rating

� One of the most misunderstood and undervalued USD20bn market-cap companies that we cover globally, in our view

� The stock is currently trading at a NAV which is pricing in what we believe to be an unlikely Dubai property crash

� We initiate coverage with an Overweight (V) rating and AED23 target price

2

Emaar Properties PJSC Real Estate 20 February 2008

��

����

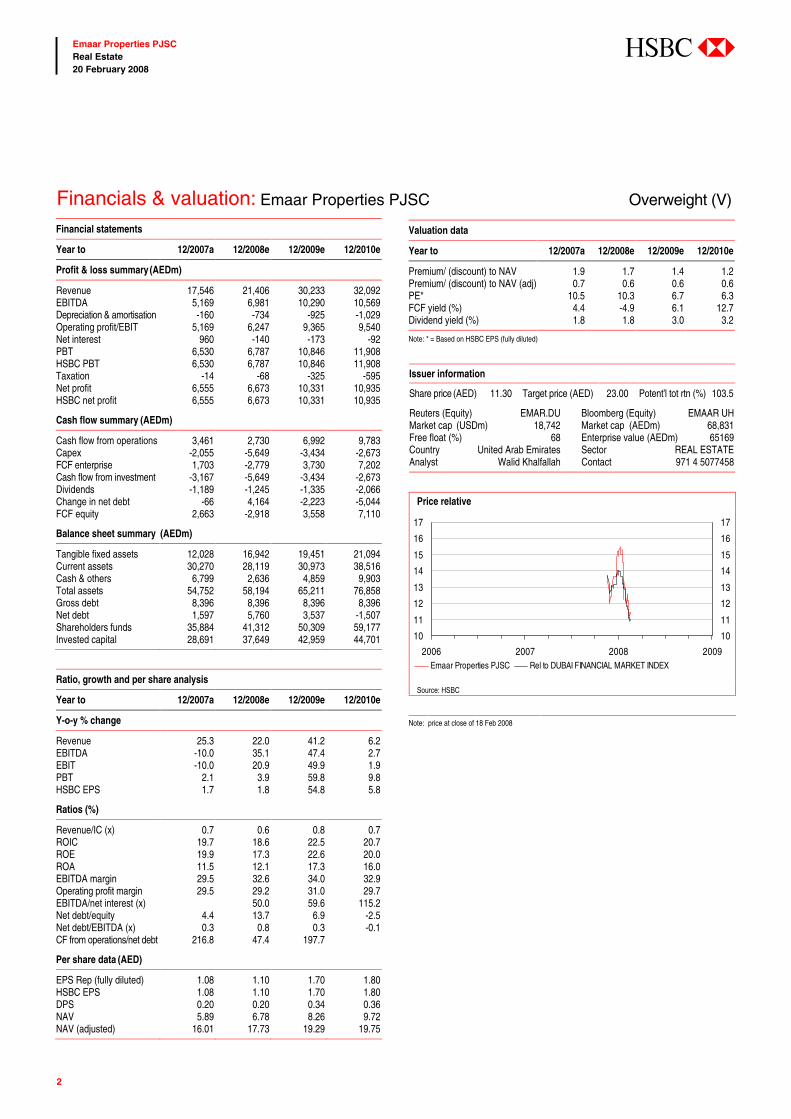

Financials & valuation: Emaar Properties PJSC Overweight (V) Financial statements

Year to 12/2007a 12/2008e 12/2009e 12/2010e

Profit & loss summary (AEDm)

Revenue 17,546 21,406 30,233 32,092 EBITDA 5,169 6,981 10,290 10,569 Depreciation & amortisation -160 -734 -925 -1,029 Operating profit/EBIT 5,169 6,247 9,365 9,540 Net interest 960 -140 -173 -92 PBT 6,530 6,787 10,846 11,908 HSBC PBT 6,530 6,787 10,846 11,908 Taxation -14 -68 -325 -595 Net profit 6,555 6,673 10,331 10,935 HSBC net profit 6,555 6,673 10,331 10,935

Cash flow summary (AEDm)

Cash flow from operations 3,461 2,730 6,992 9,783 Capex -2,055 -5,649 -3,434 -2,673 FCF enterprise 1,703 -2,779 3,730 7,202 Cash flow from investment -3,167 -5,649 -3,434 -2,673 Dividends -1,189 -1,245 -1,335 -2,066 Change in net debt -66 4,164 -2,223 -5,044 FCF equity 2,663 -2,918 3,558 7,110

Balance sheet summary (AEDm)

Tangible fixed assets 12,028 16,942 19,451 21,094 Current assets 30,270 28,119 30,973 38,516 Cash & others 6,799 2,636 4,859 9,903 Total assets 54,752 58,194 65,211 76,858 Gross debt 8,396 8,396 8,396 8,396 Net debt 1,597 5,760 3,537 -1,507 Shareholders funds 35,884 41,312 50,309 59,177 Invested capital 28,691 37,649 42,959 44,701

Ratio, growth and per share analysis

Year to 12/2007a 12/2008e 12/2009e 12/2010e

Y-o-y % change

Revenue 25.3 22.0 41.2 6.2 EBITDA -10.0 35.1 47.4 2.7 EBIT -10.0 20.9 49.9 1.9 PBT 2.1 3.9 59.8 9.8 HSBC EPS 1.7 1.8 54.8 5.8

Ratios (%)

Revenue/IC (x) 0.7 0.6 0.8 0.7 ROIC 19.7 18.6 22.5 20.7 ROE 19.9 17.3 22.6 20.0 ROA 11.5 12.1 17.3 16.0 EBITDA margin 29.5 32.6 34.0 32.9 Operating profit margin 29.5 29.2 31.0 29.7 EBITDA/net interest (x) 50.0 59.6 115.2 Net debt/equity 4.4 13.7 6.9 -2.5 Net debt/EBITDA (x) 0.3 0.8 0.3 -0.1 CF from operations/net debt 216.8 47.4 197.7

Per share data (AED)

EPS Rep (fully diluted) 1.08 1.10 1.70 1.80 HSBC EPS 1.08 1.10 1.70 1.80 DPS 0.20 0.20 0.34 0.36 NAV 5.89 6.78 8.26 9.72 NAV (adjusted) 16.01 17.73 19.29 19.75

Valuation data

Year to 12/2007a 12/2008e 12/2009e 12/2010e

Premium/ (discount) to NAV 1.9 1.7 1.4 1.2 Premium/ (discount) to NAV (adj) 0.7 0.6 0.6 0.6 PE* 10.5 10.3 6.7 6.3 FCF yield (%) 4.4 -4.9 6.1 12.7 Dividend yield (%) 1.8 1.8 3.0 3.2

Note: * = Based on HSBC EPS (fully diluted)

Issuer information

Share price (AED) 11.30 Target price (AED) 23.00 Potent’l tot rtn (%) 103.5

Reuters (Equity) EMAR.DU Bloomberg (Equity) EMAAR UH Market cap (USDm) 18,742 Market cap (AEDm) 68,831 Free float (%) 68 Enterprise value (AEDm) 65169 Country United Arab Emirates Sector REAL ESTATE Analyst Walid Khalfallah Contact 971 4 5077458

Price relative

10

11

12

13

14

15

16

17

2006 2007 2008 2009

10

11

12

13

14

15

16

17

Emaar Properties PJSC Rel to DUBAI FINANCIAL MARKET INDEX

Source: HSBC

Note: price at close of 18 Feb 2008

��

3

Emaar Properties PJSC Real Estate 20 February 2008

���

Value drivers Dubai remains the largest contributor

Value drivers: Dubai remains the largest contributor (AED)

0

5

10

15

20

25

Dubai Emerging Markets Developed Markets

Dubai R eal Es tate B us iness

B awadiAmlak15.9 India

Saudi Econ. CityEgyptMorocco

Other US7.0 0.1

Source: HSBC estimates

Emaar’s size and the extensive coverage of its story

lead us to focus on those areas that add the most

value. While the company has been expanding

overseas, as shown in the chart above, Dubai still

accounts for about 73% of its total value. It is the

main focus of this report, although other markets that

contribute significantly (particularly India, which

adds about AED2 per share) are also analyzed in

some detail.

We are grateful to Colliers International for providing the

industry data for our analysis. For further details please

contact Eamon Alashkar, Associate Director –

Consultancy Services (e-mail: ealashkar@colliers-

me.com, phone: +971 4 355 4177)

Dubai real estate business Shifting product mix impact on margins

Dubai business revenue breakdown (in AEDmn)

-

5,000

10,000

15,000

20,000

25,000

2006 2007 2008 2009 2010 2011 2012

Plot sales Unit sales R ental Hotel

40%

42%

44%

46%

48%

50%

52%

54%

56%

58%

60%

Margins

-

5,000

10,000

15,000

20,000

25,000

2006 2007 2008 2009 2010 2011 2012

Plot sales Unit sales R ental Hotel

40%

42%

44%

46%

48%

50%

52%

54%

56%

58%

60%

Margins

Source: Company data, HSBC estimates from 2008

Until 2006, plot sales accounted for more than

half of Emaar’s revenues. During those years, the

company recorded exceptionally high margins

(c60%), since the land was acquired for free. But

in 2007, Emaar entered a new stage, with more

revenues coming from unit sales and only 8%

from plot sales. Gross margins shrank to 48% (not

overall margin; see “Tying it all together,’’

below). We expect this trend to continue for the

Dubai business until rental income starts to

contribute more significantly, after which margins

should expand again (starting in 2009). In 2015,

we estimate, rental income will account for c30%

of Dubai revenues.

� Dubai remains the largest contributor to valuation …

� … however, other emerging markets are gaining significance

� Supply shortage in Dubai is here to stay

��

4

Emaar Properties PJSC Real Estate 20 February 2008

���

Emaar Dubai income statement (in AEDmn)

2007e 2008e 2009e 2010e

Revenue 14,055 16,064 21,132 18,801 Cost of revenue 7,339 8,968 11,144 10,170 Gross profit 6,716 7,096 9,988 8,632 Gross margin 48% 44% 47% 46% Associate Income* - - 75 213 Net Profit 6,173 5,810 8,070 7,031

Source: HSBC estimates

* Bawadi, UAQ Marina

Another year of delays

The widely anticipated oversupply in Dubai has

yet to materialize. Deliveries continue to be

pushed back and scaled down. Based on the latest

estimates by Colliers International, we forecast

the residential market in Dubai will remain

undersupplied at least until 2010.

Dubai residential cumulative demand/supply (in units)

0

50,000

100,000

150,000

200,000

250,000

300,000

2005 2006 2007 2008 2009 20102.6

2.7

2.8

2.9

3.0

3.1

3.2

3.3

3.4

3.5

Demand Dec. 2007 supply es t.Dec. 2006 supply es t. People per dwelling

Source: Colliers International, HSBC estimates from 2008

Emaar expects to deliver roughly 15,000 units

over the next three years. Of that, c10,000 (66%)

have been sold and 15% of revenues recognized.

Emaar uses the percentage of completion method,

in which revenues start to be recognized only

after 20% of construction is complete.

We estimate AED47bn of revenues in Dubai are

yet to be recognized.

Emaar Dubai residential developments (units)

-

5,000

10,000

15,000

20,000

25,000

30,000

Units revenue recognized Units sold Total units

Burj Dubai

Arabian Ranches

Dubai Marina

Emirates living

Emaar Towers

L’Ussailly UAQ Marina

JV with Bawadi

Source: Company data

Dubai secondary-market residential prices (in USD/m²)

Apr-07 Jan-08 Growth

International City 1,940 2,290 18% The Springs* 3,139 3,388 8% Arabian Ranches* 3,125 3,526 13% Jumeirah Lake Towers 2,647 3,690 39% Dubai Marina* 3,641 4,427 22% Jumeirah Beach Residences - 4,531 - The Greens* - 4,617 - Business Bay - 5,203 - Palm Jumeirah 4,455 5,331 20% Burj Dubai Development* 5,750 6,453 12% Emirates Hills* 7,936 Burj Dubai Tower* 11,790 18,456 57%

Source: Better Homes

* Emaar developments

In our model, for residential developments we

assume a net to gross area of 80%. Our price

assumptions range from a low of AED8,500 per

sq m for UAQ Marina and a high of AED23,000

per sq m for Burj Dubai Development. While

different developments might see varying price

movement (Burj Dubai Tower prices grew by

57% this year), for simplicity’s sake we apply a

uniform growth rate in line with our outlook for

the Dubai housing market – 14% followed by

10% until 2010.

��

5

Emaar Properties PJSC Real Estate 20 February 2008

���

Differentiation through branding

A recent survey conducted by Colliers within the

Dubai Marina area showed Emaar developments,

despite being priced at a premium, consistently

had above-average occupancy. We believe this is

a reflection of the company’s strong brand image

and commitment to after-sales services.

Office: Emaar’s exposure is limited

Emaar’s limited exposure to the office market

makes the segment dynamics almost irrelevant to

valuation. The company’s only office

developments are Burj Dubai Square and Emaar

Business Park.

Compared with other sectors, the office market in

Dubai is the tightest, with occupancy over 98%.

Taking just Dubai into account, it is still the most

at risk of oversupply. However, a large part of the

population of Sharjah and Ajman actually work in

Dubai; in our analysis we assume 50% and 30%

respectively. As such, the demand suggests the

market will reach equilibrium in 2009e.

Dubai office cumulative demand/supply (m²)

0

1,000,000

2,000,000

3,000,000

4,000,000

5,000,000

6,000,000

7,000,000

2006 2007 2008 2009 2010-

0.5

1.0

1.5

2.0

2.5

3.0

3.5

4.0

4.5

Demand SupplyDubai GLA/capita EUR GLA/capitaUS GLA/capita

Source: Colliers International, HSBC estimates from 2008

Dubai prime office rents by location

Rents in USD/m² p.a.

DIFC 1,100 SZR 985 Burj Dubai 600 Deira 570 TECOM 560 Garhoud 390

Source: Colliers International

Emaar Malls According to Colliers International, retail gross

leasable area (GLA) in Dubai is expected to triple,

from 1.4 million sq m in 2006 to 4.2 million sq m

by 2010. Emaar expects to supply about 0.5

million sq m, or c12%, by 2010 and 0.8 million sq

m by 2011. Dubai Mall will account for most of

that, with 0.35 million sq m of retail space.

Dubai cumulative retail demand/supply (m²)

0

500,000

1,000,000

1,500,000

2,000,000

2,500,000

3,000,000

3,500,000

4,000,000

4,500,000

2006 2007 2008 2009 20100.0

0.5

1.0

1.5

2.0

2.5

3.0

3.5

Demand Supply

Dubai GLA/capita EUR av. GLA/capitaUS av. GLA/capita Emaar Supply

0

500,000

1,000,000

1,500,000

2,000,000

2,500,000

3,000,000

3,500,000

4,000,000

4,500,000

2006 2007 2008 2009 20100.0

0.5

1.0

1.5

2.0

2.5

3.0

3.5

Demand Supply

Dubai GLA/capita EUR av. GLA/capitaUS av. GLA/capita Emaar SupplyEmaar Supply

Source: Colliers International, company data, HSBC estimates from 2008

While the city won’t be able to absorb all the new

supply by itself, Dubai has established itself as the

country’s retail hub and also caters to the nearby

emirates. If we look at the UAE as a whole, the

supply and demand numbers do not look too bad

in our view. Furthermore, we feel that given their

prime locations and branding, Emaar malls will

naturally cannibalize other, smaller malls.

Regional as well as international tourism is a big

part of demand, but it was excluded from our

analysis, which is based on the domestic

population only (GLA per capita). Retail tourism

in Dubai is substantial, given the influx of GCC

shoppers, especially during the Dubai Shopping

Festival, but it is difficult to quantify.

��

6

Emaar Properties PJSC Real Estate 20 February 2008

���

UAE cumulative retail demand/supply (m²)

0

1,000,000

2,000,000

3,000,000

4,000,000

5,000,000

6,000,000

7,000,000

8,000,000

9,000,000

2006 2007 2008 2009 2010

0.00

0.20

0.40

0.60

0.80

1.00

1.20

1.40

1.60

1.80

2.00

Demand SupplyUAE GLA/capita EUR av. GLA/capitaUS av. GLA/capita

Source: Colliers International, HSBC estimates from 2008

For both Dubai Mall and Marina Mall, we assume

an initial occupancy rate of 60%, which we

gradually increase to 90% by 2012e. We

conservatively assume a rental rate of AED3,200

per sq m per annum (below market average),

growing by 7% and 5% before stabilizing at 4%.

As the malls reach full capacity (2013), we

estimate they will contribute roughly AED2.2bn

of total Dubai revenue. Emaar Hospitality Group The Dubai Department of Tourism recently

revised its tourist target from 15 million by 2010

to 10 million. That has a significant impact on

hotel demand estimates, but in our view it will not

lead to an oversupply. We do expect a decline in

hotel occupancy rates from an average rate of

82% in 2006 to an average of 60% by 2009e, still

within globally acceptable levels.

However, five out of six of Emaar’s hotels are

located within the Burj Dubai development, which

is both a prime tourist destination (Armani Hotel,

Burj Dubai, Dubai Mall, etc.) and business centre

(between Business Bay and DIFC), so we feel that

occupancy should be higher. Additionally, the

various product offerings of ultra-luxury (Armani

Hotel), luxury (Burj Dubai Lake Hotel, Dubai

Mall Hotel, and the Palace) and four-star hotels

(Al Manzil and Qamardeen), should attract a

wider demographic. As a result, in our model we

assume 75% occupancy at full capacity.

Emaar Hospitality currently runs three hotels (625

rooms) and 318 serviced apartments in Dubai.

Three additional hotels (642 rooms) and 1,517

serviced apartments are under construction and

are expected by Emaar to be operational by 2008.

By 2010, we estimate the company will control a

c4% market share.

Dubai hotel cumulative demand/supply (in rooms)

0

10,000

20,000

30,000

40,000

50,000

60,000

70,000

80,000

90,000

2006 2007 2008 2009 20100%

10%

20%

30%

40%

50%

60%

70%

80%

90%

Demand Supply OccupancyEmaar Supply

0

10,000

20,000

30,000

40,000

50,000

60,000

70,000

80,000

90,000

2006 2007 2008 2009 20100%

10%

20%

30%

40%

50%

60%

70%

80%

90%

Demand Supply OccupancyEmaar Supply

Source: Colliers International, HSBC estimates from 2008

For hotels, we assume a 70% occupancy rate at

launch (2007 and 2008), rising to 75% the

following year. We assume an average room rate

of AED1,000 for four-star hotels (Al Manzil and

Qamardeen) and AED1,500 for five-star hotels

(The Palace Hotel, Dubai Mall Hotel, Burj Dubai

Lake Hotel). For Burj Dubai Armani Hotel we

assume AED2,000. We also assume a non-room

revenue (restaurants, bars, etc.) to room revenue

ratio of 40%, in line with global hospitality

standards.

Bawadi joint venture

We estimate Bawadi will contribute 6.5 million sq

m of land (valued at AED3.85bn) and Emaar will

contribute AED3.85bn in cash to fund the

construction work. Bawadi will progressively

transfer land rights as Emaar invests the

equivalent amount in construction.

��

7

Emaar Properties PJSC Real Estate 20 February 2008

���

Bawadi JV project overview

Total land area (in m²) 6,500,000 Total BUA 3,847,000 Density 59% Start date 2008 Completion date 2017 Residential units 18,000 Hotel & services apt. 6,350 Residential BUA 2,700,000 Commercial BUA 250,000 Retail BUA 297,000 Hotel & Services apt. BUA 600,000 NPV (in AEDmn) 4,873 Shares outstanding (in mn) 6,091 Value per share (in AED) 0.8 Emaar 50% (in AED) 0.4

Source: Company presentation, HSBC estimates

While the joint venture is not as lucrative for

Emaar as its other Dubai projects, since the land

was not acquired for free, it does add value. The

most obvious benefit to the company is the

replenishment of its quickly depleting land bank

in Dubai, which it increases by 38%, with no up-

front cash payment. If the land value remains

fixed at AED3.8bn, then Emaar would benefit

from land-price appreciation. If it is marked to

market in phases as rights are transferred, the

company’s margins may come under pressure.

Overall, Emaar expects an IRR of 15%,

significantly lower than its other projects.

Prices and rents still going strong Strong rental and price appreciation

Residential

Rent USD/m² p.a.

Price USD/m²

Yield

Q4 2006 319 3,371 9.5% Q4 2007 343 3,960 8.7% Growth 8% 17% Office Q4 2006 573 7,346 7.8% Q4 2007 692 9,227 7.5% Growth 21% 26% Retail Q4 2006 1,026 13,678 7.5% Q4 2007 1,233 16,440 7.5% Growth 20% 20% Hotel

Average Room rate in USD

RevPAR

Q4 2006 249 207 Q4 2007 296 255 Growth 19% 23%

Source: Colliers International, Deloitte HotelBenchmark survey

As the supply shortage widened, the property

market in Dubai saw strong rental and price

appreciation across all sectors in 2007. While

residential prices jumped 17%, rental rates only

grew by 8%, due to the government imposed 7%

rental cap, which resulted in a decline in yields

from 9.5% in 2006 to 8.7% last year. Overall, the

office market remains the most lucrative,

recording the strongest growth (26% in prices and

21% in rentals). The following chart highlights

our forecast of residential prices until 2010.Given

the tightness in the market, we still expect further

price and rental appreciation this year.

��

8

Emaar Properties PJSC Real Estate 20 February 2008

���

Dubai residential price forecasts

0

1,000

2,000

3,000

4,000

5,000

6,000

2007 2008 2009 20107.2%

7.4%

7.6%

7.8%

8.0%

8.2%

8.4%

8.6%

8.8%

Prices in USD/m² R ental yield

Source: HSBC estimates from 2008

On a relative basis, given the amount of wealth in

Dubai, prices are still cheap, in our view.

Residential price/sq m in USD (y-axis) vs. GDP/capita in USD (x-axis)

0

2,000

4,000

6,000

8,000

10,000

12,000

14,000

0 10,000 20,000 30,000 40,000 50,000 60,000

Cairo

B angkokWarsaw

B udapestPragueKiev

Shanghai

Dubai Abu Dhabi

MoscowR ome

Hong Kong

S ingapore

T okyoLondon

New Y ork

AmsterdamParis

B arcelona

Source: Colliers International, Jones Lang LaSalle, CB Richard Ellis, Pricewaterhouse, HSBC Research

Cost inflation: material costs not the full story

Going forward we expect some cost deceleration

Cost split 2007a 2008e 2009e 2010e

Labor costs 12% 25% 22% 15% 10% Cement 14% 3% -6% -4% -1% Steel 14% 33% 10% -4% -9% PEM&I* 60% 15% 15% 13% 12% Total dev. costs 100% 17% 13% 9% 7%

Source: Meed, HSBC estimates

* Plumbing, electro-mechanical, and interior finishing

While development costs are usually associated

with steel, cement, and labor, they apply more to

contractors, and only constitute about 40% of a

developer’s total costs. The remaining 60% relate

to plumbing, electro-mechanical and interior

finishing such as kitchens, bathrooms, cabinets

and tiles. Material and labor costs were more

pronounced last year, but PEM&I cost inflation

was broadly in line with overall inflation.

In our forecasts, we assume a 3% differential

between cost escalation and price appreciation.

Hence, for the next two years we are looking at

10% cost growth, followed by 8%, and then 5%,

mirroring long-term inflation.

Competitive landscape

Emaar’s two largest competitors in Dubai are

Nakheel and Dubai Holding, which are both

government-owned. Nakheel was mainly

commissioned to develop land-reclamation

projects (the three palm islands, The World, and

Dubai Water Front), although it has done some

land development (International City, Jumeirah

Lake Towers, etc.). Dubai Holding was mandated

to build knowledge hubs (Heathcare City, Media

City, Internet City, etc.) and amusement parks

(Dubai Land). Together, the three developers

control roughly 50% of the residential market.

Supply breakdown by developer (in units)

-

10,000

20,000

30,000

40,000

50,000

60,000

70,000

80,000

2008 2009 2010

Emaar Dubai Holding Nakheel Union Properties Other

Source: Colliers International

��

9

Emaar Properties PJSC Real Estate 20 February 2008

���

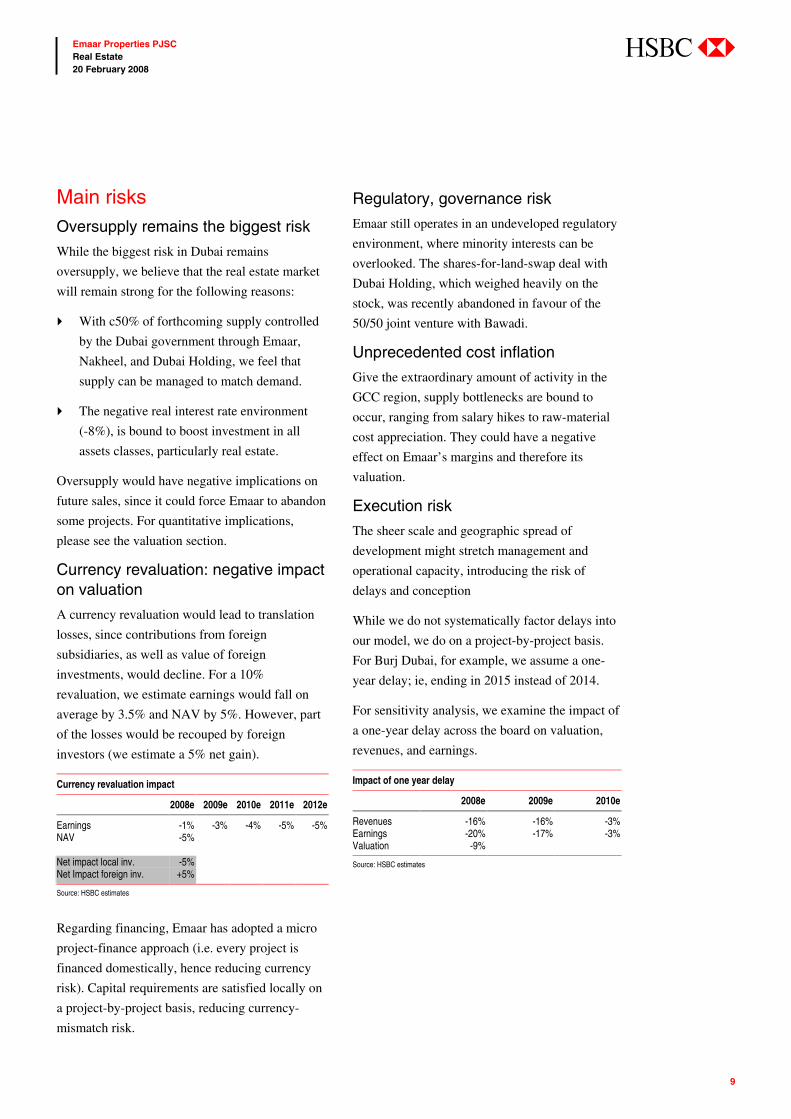

Main risks Oversupply remains the biggest risk

While the biggest risk in Dubai remains

oversupply, we believe that the real estate market

will remain strong for the following reasons:

� With c50% of forthcoming supply controlled

by the Dubai government through Emaar,

Nakheel, and Dubai Holding, we feel that

supply can be managed to match demand.

� The negative real interest rate environment

(-8%), is bound to boost investment in all

assets classes, particularly real estate.

Oversupply would have negative implications on

future sales, since it could force Emaar to abandon

some projects. For quantitative implications,

please see the valuation section.

Currency revaluation: negative impact on valuation

A currency revaluation would lead to translation

losses, since contributions from foreign

subsidiaries, as well as value of foreign

investments, would decline. For a 10%

revaluation, we estimate earnings would fall on

average by 3.5% and NAV by 5%. However, part

of the losses would be recouped by foreign

investors (we estimate a 5% net gain).

Currency revaluation impact

2008e 2009e 2010e 2011e 2012e

Earnings -1% -3% -4% -5% -5% NAV -5% Net impact local inv. -5% Net Impact foreign inv. +5%

Source: HSBC estimates

Regarding financing, Emaar has adopted a micro

project-finance approach (i.e. every project is

financed domestically, hence reducing currency

risk). Capital requirements are satisfied locally on

a project-by-project basis, reducing currency-

mismatch risk.

Regulatory, governance risk

Emaar still operates in an undeveloped regulatory

environment, where minority interests can be

overlooked. The shares-for-land-swap deal with

Dubai Holding, which weighed heavily on the

stock, was recently abandoned in favour of the

50/50 joint venture with Bawadi.

Unprecedented cost inflation

Give the extraordinary amount of activity in the

GCC region, supply bottlenecks are bound to

occur, ranging from salary hikes to raw-material

cost appreciation. They could have a negative

effect on Emaar’s margins and therefore its

valuation.

Execution risk

The sheer scale and geographic spread of

development might stretch management and

operational capacity, introducing the risk of

delays and conception

While we do not systematically factor delays into

our model, we do on a project-by-project basis.

For Burj Dubai, for example, we assume a one-

year delay; ie, ending in 2015 instead of 2014.

For sensitivity analysis, we examine the impact of

a one-year delay across the board on valuation,

revenues, and earnings.

Impact of one year delay

2008e 2009e 2010e

Revenues -16% -16% -3% Earnings -20% -17% -3% Valuation -9%

Source: HSBC estimates

��

10

Emaar Properties PJSC Real Estate 20 February 2008

���

Emaar MGF Land Ltd. Conservative valuation: 30% lower than IPO bottom range

Emaar MGF, key assumptions

BUA (in mn m²)

Av. Price (in USD/m²)

Av. cost (in USD/m²)

Av. Cap rate

Residential 28.1 1,168 367 Plots 12.3 299 27 Commercial 8.1 11* 489 10% Retail 1.5 18* 543 10% BUA

(in mn m²)

ARR Av. Cost

( USD/room)

Hotel 0.3 139 176,768 9%

Source: HSBC estimates

* Rentals

India valuation very conservative, below IPO lower range

-

100

200

300

400

500

600

- 10 20 30 40 50 60 70 80

Land area (in mn sq m)

EV/L

and

(in U

SD/s

q m

)

we value Emaar MGF at 30% discount to lower range

Unitech

DLF

Indiabulls

Parsv

HDIL

Sobha

IPO range

Source: Company data, Bloomberg, Emaar MGF prospectus

The chart above shows the key listed real estate

developers in India. We believe our valuation is

conservative, as it is below the IPO lower range

and the comparative best-fit line.

Third-largest land bank in India

EMLL’s has acquired a 50 million sq m land bank

in India, with c70% of the cost already paid, and

the rest to be paid over the next few years. The

land bank is a good mix of large and upcoming

markets in our view. The majority of the

company’s land bank is in north India (c87%).

Overall, Tier I and II cities account for 54% of the

land bank.

EMLL land bank breakdown

North million m² South million m²

Chail 0.07 Chennai 0.21 Dehradun 4.57 Coimbatore 1.07 Delhi 5.31 Hyderabad 2.06 Ghaziabad 1.53 Kochi 1.46 Gurgaon 11.36 Mangalore 0.30 Jaipur 1.68 Mysore 0.62 Jalandhar 0.96 Total 5.72 Lucknow 1.58 Ludhiana 1.40 West million m² Mohali 11.23 Aibaugh 0.10 Total 39.71 Goa 1.95 Indore 0.83 East million m² Pune 2.10 Kolkata 0.02 Total 4.99 Shillong 0.32 Total 0.35 Grand Total 50.77

Source: Company

EMLL plans to sell 24% of its land bank as plots

and 55% as residential units, greatly minimizing

its working-capital requirements. Residential

development is more capital-intensive, because of

the investment in initial infrastructure and a

deferred payment scheme. But we estimate they

will become cash positive at 50-55% of cost. Most

of the remaining land bank will be held as

investment properties, which are cash-intensive.

Business model: geared towards residential and plot sales

Residential sale 55% Plots sale 24% Commercial lease 10% Commercial sale 6% Retail lease 2% Retail sale 1% Hotel 1% SEZ 1%

Source: Company data, HSBC estimates

EMLL to capture 20% of premium housing market by 2011

Growing affluence and income levels have had a

cascading effect on demand for premium residential

space in India. Since this segment represents

EMLL’s target market, it is the most relevant. We

estimate that from 2006 to 2010 roughly 158 million

sq m (c1.6 million units) of additional premium

residential space will be needed.

��

11

Emaar Properties PJSC Real Estate 20 February 2008

���

Knight Frank estimates Grade A and B+

residential supply of 49 million sq m (c490,000

units) over the next three years in the top seven

locations in India to meet this demand. As the chart on the top of the next page shows,

there is a huge undersupply in the premium

residential market in India. We estimate by the

end of 2010 the shortage will reach c46 million sq

meters or roughly 460,000 units. Overall, EMLL

plans to develop 40 million sq m of premium

residential property. Out of the total BUA (built-

up area) 31% (12 million sq m) will be sold as

land plots and the rest developed as community

housing. We estimate that by 2011, EMLL will

account for roughly 20% of total premium

housing supply.

India cum. premium residential demand/supply (million m²)

0

10

20

30

40

50

60

70

80

90

100

2009 2010 2011 2012 2013

Demand T otal Supply Emaar Supply

0

10

20

30

40

50

60

70

80

90

100

2009 2010 2011 2012 2013

Demand T otal Supply Emaar Supply

Source: Knight Frank, HSBC estimates from 2009

* Our estimate of Emaar supply is based on major planned residential developments

Office: a play on the growing IT/ITES sector

The IT/ITES sector has been growing at a c25%

CAGR over the past 5 years and has been the

biggest demand driver for commercial space. The

industry currently employs c300,000 people every

year. We expect the sector to add 3 million jobs

over the next five years, which would support

demand for commercial space of c28 million sq m

over 2007-12. We estimate demand by the

commercial, non- IT/ITES segment to reach 30%

of total commercial space, which would translate

into total space demand of c37 million sq m over

2007-2012. Our estimates are in line with most

property consultants, who are expecting 37

million to 42 million sq m over the same period.

As the following chart shows, by 2012, we

estimate EMLL will account for c20% of total

office supply.

India cumulative office demand (million m²)

0

5

10

15

20

25

30

35

40

2008 2009 2010 2011 2012

Non IT Emaar SupplyIT/ITES

0

5

10

15

20

25

30

35

40

2008 2009 2010 2011 2012

Non IT Emaar SupplyIT/ITES

Source: Company, HSBC estimates from 2008

Retail: shift towards malls

While organized retail (malls, etc.) in India

currently accounts for only c5% of total retail

space, we estimate it will grow at a 35% CAGR to

reach a 15% market share by 2012. We expect the

market to demand c32 million sq m of organized

retail space over the next five years. This is in line

with the expansion plans of most large retail

companies. Furthermore, we expect the absorption

rate to reach 30 million by 2012, although some

micro markets are likely to face problems of

oversupply. In total, EMLL plans to develop

roughly 1.6 million sq m of retail GLA across

different cities, of which c1 million sq m are

expected by the company to be ready by 2011.

��

12

Emaar Properties PJSC Real Estate 20 February 2008

���

India cumulative organized retail demand (million m²)

0

5

10

15

20

25

30

35

2007 2008 2009 2010 2011 2012

Source: HSBC estimates from 2008

Hotel: occupancy to reach 80% this year

Strong growth in domestic and foreign passenger

travel has led to unprecedented demand for hotel

rooms in India, with occupancy levels expected

by us to reach c80% in 2008. According to

government estimates, foreign tourist arrivals in

India grew 11% in 2005 and 15% in 2006, 50% of

which were estimated to be business travellers.

We estimate this number will grow by 8% to 10%

annually over the next 10 years. EMLL plans to

develop roughly 5,000 hotel rooms spread across

different geographies. This will be done through a

multiple product offering within the hospitality

segment. The company intends to cater to all

market segments by offering luxury, five-star,

budget, economy, and serviced apartments.

India cumulative hotel demand/supply (in rooms)

0

5,000

10,000

15,000

20,000

25,000

30,000

35,000

40,000

45,000

2007 2008 2009 2010 201164%

66%

68%

70%

72%

74%

76%

78%

80%

Demand Supply OccupancyEmaar supply

0

5,000

10,000

15,000

20,000

25,000

30,000

35,000

40,000

45,000

2007 2008 2009 2010 201164%

66%

68%

70%

72%

74%

76%

78%

80%

Demand Supply OccupancyEmaar supply

Source: CRIS INFAC

Cairo real estate business Demographic growth and middle-class expansion to boost demand

Cairo price comparison (in USD per m²)

Villa Apartment

Emaar 1,900 1,770 OHD 2,500 - SODIC 1,500 900 TMG 1,360 600 SODIC/Solidere - 1,400

Source: Company data, HSBC Research

Based on TMG numbers, we know that the real

estate market is Cairo was very vibrant last year.

The company recorded strong price growth, with

average prices at Madinaty (which accounted for

65% of total sales) for villas and apartments

growing by 37% to EGP7,510 per sq m and 34%

to EGP3,205 per sq m respectively, beating our

forecast of EGP6,000 per sq m and EGP2,600 per

sq m. This was driven by strong economic growth

and negative real rates.

In Cairo, Emaar is developing four upscale

residential communities targeted at the high-

income segment (USD1,900 per sq m for villas at

a 40% premium to TMG , which targets the

middle to high income). The company expects to

deliver roughly 15,000 units by 2015, about 3% of

overall forthcoming premium residential supply.

So far, only 450 units have been launched, of

which 320 were sold.

��

13

Emaar Properties PJSC Real Estate 20 February 2008

���

We estimate that at the end of 2006, the number

of housing units catering to the middle-to-high

income segment in Cairo stood at around 1.1

million, or c24% of overall supply. We forecast

that supply in this segment will reach 1.6 million

units by 2015. We also estimate that over the

same period, an additional 565,190 housing units

will be required.

Forthcoming supply breakdown (in units)

-

10,000

20,000

30,000

40,000

50,000

60,000

70,000

80,000

90,000

2007 2008 2009 2010 2011 2012 2013 2014 2015

T MG Emaar Heliopolis Nas r City SODIC Other developers

Source: USAID, Companies data, HSBC estimates from 2008

Cairo residential demand/supply (in units)

-

100,000

200,000

300,000

400,000

500,000

600,000

2007 2009 2011 2013 20153.62

3.64

3.66

3.68

3.70

Demand Supply People per dwelling

Source: USAID, CAPMAS, Companies data, HSBC estimates from 2008

In our model, we conservatively assume an

average price of EGP7,000 per sq m, almost in

line with TMG despite Emaar’s developments

being much more upscale. For Cairo Gate lease,

we assume an average rental rate of (EGP1,866

per sq m p.a.). We estimate that by 2010, Egypt

will contribute roughly 10% of Emaar’s

total revenue.

Morocco Vacation homes and tourist resorts

Morocco planned developments

Emaar ownership

Sale units

Lease units

Value per share (AED)

Amelkis II 50% 310 - Amelkis III 50% 440 - Bahia Bay 50% 2,730 - Saphira 100% 16,500 7,300 Oukaeimeden 100% 3,500 1,250 Tinja 100% 2,950 840 Total 26,430 9,390 1.9

Source: Company presentation, HSBC estimates for value per share data

In Morocco, Emaar is developing luxury

beachfront, mountain, and golfing resort

communities, targeting vacation home buyers

and tourists (similar to the OHD model, Al Guna).

More than a third of the units will be leased out.

Three of the projects will be developed in

conjunction with ONA through a 50/50 JV.

The projects will span from 2005 to 2016. In total,

293 units have been sold in Amelkis II and Tinja,

out of 381 units released.

Based on company guidance (townhouses starting

at AED1.5m and villas at AED2.3m), in our

valuation, we assume an average price of

AED6,000 per sq m (MAD12,000) and an average

rental rate of AED350 per sq m p.a. (MAD735).

Given the large rental component, we estimate

that Morocco will account for c10% of revenues

by 2010 and 16% by 2011.

Emaar the Economic City If you build it, they will come

Emaar the Economic City mega-project, is part of

the kingdom’s drive to expand and diversify its

economy, create employment opportunities, and

attract foreign investment. The development is

ambitious and has been received with a fair

amount of scepticism.

��

14

Emaar Properties PJSC Real Estate 20 February 2008

���

According to our strategist, John Lomax, who

visited the site, EEC, the company responsible for

developing the site, was very bullish. However,

apparently the king also recently visited and was

disappointed by the lack of progress.

Nonetheless, plans are being accelerated, doubling

the number of residential units scheduled for

Phase 1. Half of the first-phase leases in the

industrial zone have already been sold.

Furthermore, there seems to have been some

initial confusion about who would provide the

infrastructure for King Abdullah Economic City.

That has now been clarified – the government will

not invest in infrastructure; it is down to the city

itself.

Emaar thought that development margins would

end up being the same as in Dubai. However, a

project on this scale does seem to have a lot of

scope for a loss of financial discipline. The rollout

of the city master plan also has a great deal of

scope for delays in our view.

Given the scale of the project, implementation is

necessary to gain market confidence. Some

speculative demand exists, but residents appear

cautious and unwilling to commit until progress

becomes clearer.

Emaar the Economic City masterplan

Residential apartments (units) 250,000 Residential villas (in units) 25,000 Central Business District (mn m²) 3.3 Hotel rooms 25,000 Industrial zone (mn m²) 63.5 Sea port (mn m²) 13.8 Education zone (Students) 45,000

Source: Company

At this juncture, we did not dive into the details,

and for the time being, we use EEC’s market cap

as an indication.

Other emerging markets 5% contribution to valuation

Emaar ownership

Sale units Lease units

Value per share (AED)

Saudi Arabia 0.4 Al Khobbar Lakes 61% 3,800 - Jeddah Gate 61% 1,899 264 Jordan 0.3 Dead Sea Dev. 37% 1,042 482 Syria 0.3 Eighth Gate 60% 1,012 1,338 Turkey 0.0 Tuscan Valley 60% 555 - Pakistan 0.1 Karachi 67% 5,388 - Islamabad 67% 4,535 - Total 1.1

Source: Company presentation, HSBC estimates t for value per share data

Other emerging markets are not at critical mass.

They add only AED1.1 per share to our target price

and contribute 14% of revenues at peak (2012e).

Developed markets John Laing Homes: value-dilutive

Emaar acquired John Laing Homes in 2006 at the

top of the US housing boom when valuations

were at their peak. At USD1.1bn, the acquisition

was expensive, we feel. Financially, John Laing

Homes is not value-additive; in fact, it is value-

dilutive. While the company was acquired at

cAED0.6 per share, according to our analysis,

given where we are in the cycle, it only adds

cAED0.1 per share. Furthermore, with a gross

margin of 6%, JLH is putting pressure on overall

margins (please refer to the ‘Tying it all together’

section below). Nonetheless, to be fair, the

acquisition has some intangible advantages,

mainly transfer of knowledge and expertise (the

current Emaar Dubai CEO, Richard Rodriguez,

joined from JLH). Regardless, in the larger

scheme of thing, its contribution to our valuation

is small.

��

15

Emaar Properties PJSC Real Estate 20 February 2008

���

Tying it all together Margins set to bottom out this year

Revenue breakdown and overall gross margin

0%

10%

20%

30%

40%

50%

60%

70%

80%

90%

100%

2006 2007 2008 2009 2010 2011

UAE USA Morocco Egypt KSA Rest

30%

35%

40%

45%

50%

55%

Margins

0%

10%

20%

30%

40%

50%

60%

70%

80%

90%

100%

2006 2007 2008 2009 2010 2011

UAE USA Morocco Egypt KSA Rest

30%

35%

40%

45%

50%

55%

Margins

Source: Company reports, HSBC estimates from 2008

We expect margins will bottom out in 2008 and

should progressively improve over the coming

years. Gross margins came under pressure in 2006

and 2007 as plot sales declined (at 90%, the

highest margins) and the US business was

included (6% gross margin). This was the main

reason behind the significant negative earnings

revision last year. However, increased

contributions from other emerging markets

(Egypt, Morocco, KSA, etc.) will mitigate the

struggling US business, in our view.

Revenue breakdown by mix and overall gross margin

0%

10%

20%

30%

40%

50%

60%

70%

80%

90%

100%

2006 2007 2008 2009 2010 2011

Plot sales Units sale Rental income Hotel

30%

35%

40%

45%

50%

55%

Margins

0%

10%

20%

30%

40%

50%

60%

70%

80%

90%

100%

2006 2007 2008 2009 2010 2011

Plot sales Units sale Rental income Hotel

30%

35%

40%

45%

50%

55%

Margins

Source: Company reports, HSBC estimates from 2008

In our view, also shifting product mix towards

investment properties, particularly in Dubai,

Morocco, and Syria, should further support

margin improvement. In Dubai, Dubai Mall,

Marina Mall and most hotels are scheduled for

completion at the end of 2008. In Morocco, the

company plans to lease out a third of total

residential units (9,390). We estimate that rental

income from Morocco will start to kick in by

early 2012. In Syria, 50% of residential units

(1,338) will be leased and will also start

contributing in 2012.

� Margins to bottom out in Q2 2008e and negative earnings revision

should be over

� Emerging markets to offset struggling US business

� Shifting mix towards investment properties to support margins

��

16

Emaar Properties PJSC Real Estate 20 February 2008

���

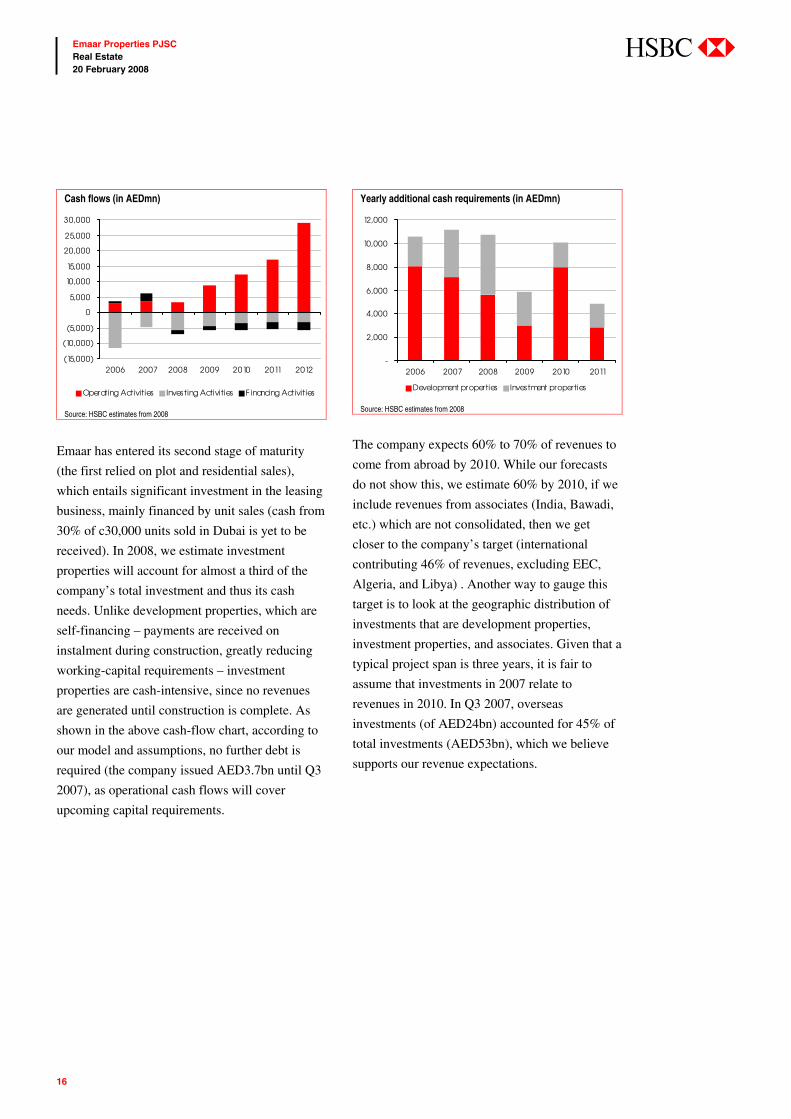

Cash flows (in AEDmn)

(15,000)

(10,000)

(5,000)

0

5,000

10,000

15,000

20,000

25,000

30,000

2006 2007 2008 2009 2010 2011 2012

Operating Activities Investing Activities F inancing Activities

Source: HSBC estimates from 2008

Emaar has entered its second stage of maturity

(the first relied on plot and residential sales),

which entails significant investment in the leasing

business, mainly financed by unit sales (cash from

30% of c30,000 units sold in Dubai is yet to be

received). In 2008, we estimate investment

properties will account for almost a third of the

company’s total investment and thus its cash

needs. Unlike development properties, which are

self-financing – payments are received on

instalment during construction, greatly reducing

working-capital requirements – investment

properties are cash-intensive, since no revenues

are generated until construction is complete. As

shown in the above cash-flow chart, according to

our model and assumptions, no further debt is

required (the company issued AED3.7bn until Q3

2007), as operational cash flows will cover

upcoming capital requirements.

Yearly additional cash requirements (in AEDmn)

-

2,000

4,000

6,000

8,000

10,000

12,000

2006 2007 2008 2009 2010 2011

Development properties Investment properties

Source: HSBC estimates from 2008

The company expects 60% to 70% of revenues to

come from abroad by 2010. While our forecasts

do not show this, we estimate 60% by 2010, if we

include revenues from associates (India, Bawadi,

etc.) which are not consolidated, then we get

closer to the company’s target (international

contributing 46% of revenues, excluding EEC,

Algeria, and Libya) . Another way to gauge this

target is to look at the geographic distribution of

investments that are development properties,

investment properties, and associates. Given that a

typical project span is three years, it is fair to

assume that investments in 2007 relate to

revenues in 2010. In Q3 2007, overseas

investments (of AED24bn) accounted for 45% of

total investments (AED53bn), which we believe

supports our revenue expectations.

��

17

Emaar Properties PJSC Real Estate 20 February 2008

���

Valuation

Value drivers: Dubai remains the largest contributor (AED per share)

0

5

10

15

20

25

Dubai Emerging Markets Developed Markets

Dubai R eal Es tate B us iness

B awadiAmlak15.9 India

Saudi Econ. CityEgyptMorocco

Other US7.0 0.1

Source: HSBC estimates

We use a DCF to value all projects where

development plans have been completed based on

built up areas. Hence projects such as Algeria and

Libya, although significant, are excluded. For

associates and subsidiaries, we use market cap

if available (EEC, Amlak) or net asset value

(Dubai Bank). Regarding MGF India, given the

IPO withdrawal, we apply a 30% discount to

the offering lower range (which was already

reduced twice).

DCF valuation (in AEDm)

Net Debt/ (Cash) 5,760.4 Total DCF value 123,631.4 Net DCF value 117,871.0 Total no of shares 6,091.2 Value per Share 19.4 KAEC 5,412.6 Emaar MGF 12,850.6 Dubai Bank 0.0 Amlak 3,456.0 Total value 21,719.2 No of shares 6,091.2 Value per share 3.6 Total value per share (AED) 23

Source: HSBC estimates

In our model, given Emaar’s geographic spread,

we use country-by-country discount rates and

effective tax rates.

WACC and tax assumptions

Country WACC Effective tax rate

UAE 9.4% 0% Saudi Arabia 9.5% 0% Egypt 14.4% 20% Morocco 11.0% 20% Turkey 18.0% 20% Syria 14.0% 20% Pakistan 16.5% 20% Jordan 12.5% 20% US 8.7% 30%

Source: HSBC estimates

� DCF value of AED23 implies a 100% potential return

� 2008e NAV at 25% discount to DCF, reflecting developer margin

� We estimate a floor NAV of AED11.3 if Dubai market were to

collapse

��

18

Emaar Properties PJSC Real Estate 20 February 2008

���

Valuation key assumptions

Residential 2007e 2008e 2009e 2010e 2011e 2012e 2013e 2014e 2015e Net to gross area 80% 80% 80% 80% 80% 80% 80% 80% 80% Dubai Prices in AED/m² min 11,000 12,540 13,794 14,484 15,208 15,968 16,767 17,605 18,485 Prices in AED/m² max 20,000 22,800 25,080 26,334 27,651 29,033 30,485 32,009 33,610 Growth rate 14% 10% 5% 5% 5% 5% 5% 5% Costs in AED/m² min 6,000 6,600 7,128 7,484 7,859 8,252 8,664 9,097 9,552 Costs in AED/m² max 8,000 8,800 9,504 9,979 10,478 11,002 11,552 12,130 12,736 Growth rate 10% 8% 5% 5% 5% 5% 5% 5% Morocco Prices in AED/m² min 5,214 5,996 6,776 7,521 8,123 8,772 9,299 9,857 10,349 Prices in AED/m² max 5,688 6,541 7,392 8,205 8,861 9,570 10,144 10,753 11,290 Growth rate 15% 13% 11% 8% 8% 6% 6% 5% Costs in AED/m² min 3,081 3,327 3,594 3,845 4,076 4,280 4,494 4,718 4,954 Growth rate 8% 8% 7% 6% 5% 5% 5% 5% Egypt Prices in AED/m² min 4,500 5,175 5,848 6,491 7,010 7,571 8,025 8,507 8,932 Prices in AED/m² max 7,500 8,625 9,746 10,818 11,684 12,619 13,376 14,178 14,887 Growth rate 15% 13% 11% 8% 8% 6% 6% 5% Costs in AED/m² min 2,250 2,430 2,624 2,808 2,977 3,125 3,282 3,446 3,618 Costs in AED/m² max 3,450 3,726 4,024 4,306 4,564 4,792 5,032 5,284 5,548 Growth rate 8% 8% 7% 6% 5% 5% 5% 5% Lease Business YR 1 YR 2 YR 3 YR 4 YR 5 YR 6 YR 7 YR 8 YR 9 Occupancy (60% at launch) 60% 70% 80% 90% 90% 90% 90% 90% 90% 2007 2008 2009 2010 2011 2012 2013 2014 2015 Dubai Rent in AED/m² p.a. min 2,940 3,146 3,303 3,435 3,573 3,716 3,864 4,019 4,179 Rent in AED/m² p.a. max 3,000 3,210 3,371 3,505 3,646 3,791 3,943 4,101 4,265 Growth rate 7% 5% 4% 4% 4% 4% 4% 4% Costs in AED/m² 5000 5400 5832 6240 6615 6945 7293 7657 8040 Growth rate 8% 8% 7% 6% 5% 5% 5% 5% Morocco Rent in AED/m² p.a. min 697 746 798 830 863 897 933 971 1,009 Rent in AED/m² p.a. max 722 772 826 859 894 929 967 1,005 1,045 Growth rate 7% 7% 4% 4% 4% 4% 4% 4% Costs in AED/m² 2,844 3,072 3,317 3,549 3,762 3,951 4,148 4,355 4,573 Growth rate 8% 8% 7% 6% 5% 5% 5% 5% Hotel 2007 2008 2009 2010 2011 2012 2013 2014 2015 Occupancy 75% 75% 75% 75% 75% 75% 75% 75% 75% NRR/ARR* 40% 40% 40% 40% 40% 40% 40% 40% 40% Dubai ARR in AED min 1,000 1,050 1,103 1,158 1,216 1,276 1,340 ARR in AED max 2,500 2,625 2,756 2,894 3,039 3,191 3,350 Growth rate 5% 5% 5% 5% 5% 5% Cost per room in AED min 1,000,000 1,000,000 1,080,000 1,166,400 1,248,048 1,322,931 1,389,077 1,458,531 1,531,458 Cost per room in AED max 2,000,000 2,160,000 2,332,800 2,496,096 2,645,862 2,778,155 2,917,063 3,062,916 3,216,062 Growth rate 8% 8% 7% 6% 5% 5% 5% 5% 2007 2008 2009 2010 2011 2012 2013 2014 2015 Selling & Marketing/Rev 5% 10% 11% 11% 11% 11% 11% 11% 11% G&A growth 10% 10% 10% 10% 10% 10% 10% 10% 10%

Source: HSBC estimates

��

19

Emaar Properties PJSC Real Estate 20 February 2008

���

Estimated floor NAV value of AED11.3 per share – if Dubai property market melts down

As we discussed earlier, we believe an oversupply

is unlikely. In this hypothetical scenario, we

analyse the impact on Emaar’s valuation of a real

estate market meltdown in Dubai. We assume that

the company would cancel all future projects

(L’Ussailly, Bawadi, and UAQ Marina, in total

56,000 units) and halt construction on current

projects that are being developed (Burj Dubai

roughly 9,000 units), except for those that have

already been sold. For lease projects (Dubai Mall,

Marina Mall, and office buildings) we assume a

drop in occupancy levels from 90% to 60% and a

20% decline in rental rates. For hotels (Al Manzil,

Qamardeen, The Palace, Burj Dubai Lake Hotel,

Dubai Mall Hotel, and Marina Mall Hotel) we

also assume a decline in occupancy to 60% from

75% and a 20% drop in room rates. This analysis

has two implications. First, it sets our estimated

floor NAV for this extreme scenario (-36%, NAV

2008 = AED11.3). Second, it illustrates the

impact on our DCF (-37%, TP = AED14.5).

2008e NAV at 23% discount to our DCF

NAV breakdown (AED per share)

0

2

4

6

8

10

12

14

16

18

20

2007 2008 2009

Adj. equity value* Associates Land Investment properties

Source: HSBC estimates

* Adj. for book value of Associates and IPs

Since Emaar’s land is not recognized on its books,

we value it at fair value using the residual method.

We assume a developer margin of 20% on

revenues and worked backwards to the value of

land based on prevailing market prices and costs.

We also marked to market the value of associates

and subsidiaries. Additionally, we revalued the

company’s investment property portfolio (malls,

offices and hotels), which is recognized at cost.

To value investment properties, we use a

capitalization rate of 7.4% (WACC – terminal

growth rate). To compute NOI (net operating

income), we apply a 75% margin for retail and

office, and 30% for hotels. On our estimates,

investment properties have a potential revaluation

of AED21bn to be released by 2010 (includes

lands pertaining to IPs). This is on top of

AED13bn already recognized on the balance sheet

at cost. Please note, Emaar so far has not reflected

any fair value gains.

Land valuation based on residual method (AED per sq m)

Burj Dubai 2007e

Average Price/m² (Net sellable area) 23,000 Average Price/m² (Gross BUA) 18,400 Development Cost/m² 9,000 Development Margin (20%)/m² 3,680 Average Land Price/m² 5,720

Source: HSBC estimates

Land value in AED/m

²

Burj Dubai 5,720 Other Dubai 2,600 Bawadi 1,680 UAQ Marina 260 UAE 2,784 Egypt 1,040 Morocco 548 KSA 760 Syria 740 Pakistan 260 Jordan 220 Turkey 292 Total 1,678 Weighted av. Emaar 2,700 Weighted av. Aldar 2,200

Source: HSBC estimates

��

20

Emaar Properties PJSC Real Estate 20 February 2008

���

While a typical developer margin is 15% (margin

on top of NAV), we derive a DCF value

(AED23), which is c30% higher than NAV

(AED17.7). We believe the difference is justified,

because our model implicitly includes price and

rental appreciation, while the static NAV

calculation does not. Furthermore, investment

properties are understated in our NAV calculation.

A project might be 90% complete, for example,

but it is still valued at cost under this

methodology. Indeed, if we were to apply a

percentage of completion to a project value, then

our NAV would increase considerably.

NAV to converge towards DCF value overtime

0

10

20

30

40

50

60

2008 2010 2012 2014 2016 2018 2020

NAV Value DCF Value

Source: HSBC estimates

As shown in the above chart, the NAV discount to

DCF will widen over the next two years before it

starts to converge. Since a DCF is the future value

of all projects discounted back, it will linearly

increase year on year by the discount rate.

However, NAV calculations do not capture profit

from future development projects as well as the

investment properties that will come on stream.

Once all land has been exhausted, and therefore

all that remains are investment properties

(reflected at fair value), the NAV and DCF will

converge. This is only a theoretical exercise, since

we believe Emaar is likely to replenish its land

bank, and hence continue development properties.

Comparative valuation Comparative valuation for real estate companies

is complicated by different accounting policies,

e.g. revenue recognition, (% of completion or

completed contract), or fair value adjustment

(land, investment properties, etc.). As such,

looking at P/E vs. growth (or EV/EBITDA) does

not provide a clear picture. The most indicative

would be P/B vs. ROE.

PE 2009e vs. EPS growth 2007-09e

0

5

10

15

20

25

30

0% 50% 100% 150%

Source: HSBC estimates

P/BV 2009 vs. ROE 2008e

Emaar Aldar

Sorouh

0.0

1.0

2.0

3.0

4.0

5.0

6.0

7.0

0% 10% 20% 30% 40% 50% 60%

TMG

Source: HSBC estimates

��

21

Emaar Properties PJSC Real Estate 20 February 2008

���

We initiate coverage with an Overweight (V) rating Under our research model, for stocks with a

volatility indicator, the Neutral band is 10

percentage points above and below the hurdle rate

for UAE stocks of 10.3%. Our target price of

AED23 provides total potential return of c100%,

above the Neutral band of our model; therefore,

we initiate coverage with an Overweight (V)

ratings.

Shareholder structure Shareholder structure

0%

20%

40%

60%

80%

100%

Dubai gov. 32%

Free float 68%

Nationals 76%

GCC 12%

Foreign 12%

Source: DFM

Comparative valuation

Peer Name

Reuters

Ticker

Country

Currency

Current Mkt Cap

(USDmn)

Current

Price

Target

Price

Rating

P/Book

PE

EV/

EBITDA

2008e 2009e 2008e 2009e 2008e 2009e Emaar Properties EMAR.DU UAE AED 18904 11.4 23 Overweight (V) 1.7 1.4 10.4 6.7 9.4 6.0 Aldar Properties ALDR.AD UAE AED 7022 11.3 20.3 Overweight (V) 2.2 1.5 12.2 6.2 56.2 10.8 Sorouh Real Estate SOR.AD UAE AED 6644 9.7 13.2 Overweight (V) 4.3 3.3 15.2 11.9 17.1 12.6 Echo Investment SA EPRS.WA POLAND PLN 1182 6.9 91.6 Overweight 1.4 0.9 6.0 2.3 6.4 3.1 GlobeTrade Centre GTCE.WA POLAND PLN 3378 37.6 15.7 Overweight (V) 1.3 0.7 3.6 1.7 33.4 13.0 Hammerson HMSO.L UNITED KINGDOM GBP 5942 10.5 7.6 Underweight 0.9 0.8 24.2 25.0 23.8 21.2 Land Securities Group LAND.L UNITED KINGDOM GBP 13884 15.3 15.6 Underweight 0.8 0.8 18.0 16.0 20.3 17.4 Nexity NEXI.PA FRANCE EUR 1411 29.8 73.0 Overweight 1.2 1.0 4.8 4.7 5.6 5.2 Orco Property Group ORCO.PR CZECH REPUBLIC CZK 844 1743.0 104.7 Neutral 0.8 0.8 6.8 6.4 60.6 209.2 Cyrela Braz Rlty CYRE3.SA BRAZIL BRL 5280 25.8 26.0 Neutral (V) 3.6 3.0 28.8 17.5 13.8 9.0 TMG TMGH.CA EGYPT EGP 4050 12.3 16.4 Overweight (V) 1.1 1.0 18.8 8.5 12.5 3.5 Gafisa SA GFSA3.SA BRAZIL BRL 2239 30.1 44.0 Overweight (V) 2.1 1.7 17.6 11.9 12.3 8.8 Sixth Of Oct. Dev OCDI.CA EGYPT EGP 1001 204.5 280.0 Overweight 3.2 2.8 36.0 24.3 36.6 46.9 DLF DLF.BO INDIA INR 36848 860.0 N/R N/R 5.6 4.0 15.0 11.6 12.5 10.3 Unitech UNTE.BO INDIA INR 16342 400.0 N/R N/R 10.3 6.2 21.1 13.0 14.7 9.8 Union Properties UPRO.DU UAE AED 3597 4.8 N/R N/R 2.3 1.6 18.3 3.9 29.6 4.6 Shimao Properties 0813.HK CHINA CNY 7450 17.6 N/R N/R 2.6 2.2 13.7 9.0 10.0 6.7 Agile Property 3383.HK CHINA CNY 5528 11.5 N/R N/R 3.8 2.9 13.2 9.8 9.9 7.4 Shui on Land 0272.HK CHINA HKD 4386 8.2 N/R N/R 1.9 1.7 17.8 13.7 14.6 12.3 Greentown China 3900.HK CHINA CNY 1951 10.0 N/R N/R 1.9 1.7 17.8 13.7 14.6 12.3

Source: Reuters, HSBC estimates

��

22

Emaar Properties PJSC Real Estate 20 February 2008

���

Aldar (ALDR.AD, AED20.30, Overweight (V)) Valuation

We value Aldar via a DCF as set out below.

Aldar DCF

Terminal Growth Rate 5.00% NPV: FCF 29,939.5 Net Debt/ (Cash) 1,469.9 Equity 28,469.6 Outstanding Shares 3,357 DCF Value (AED) 8.5 Value of Land (Al Yas Island) 23758.0 Value of Land (Al Raha Beach) 4257.0 Value of land (Mina Zayed 50% prob.) 11624.0 No of Shares 3357.3 Value of the Land (Per Share) 11.8 Total Value 20.3

Source: HSBC estimates

Company-specific risks

� Cost inflation: given the extraordinary

amount of activity in the GCC region, supply

bottlenecks are bound to occur, ranging from

salary hikes to raw material cost appreciation.

� Execution risk: the sheer scale of

development (AED184bn) will stretch

management and operational capacity, hence

introducing the risk of delays or even project

cancellation.

� Governance: Aldar is still operating in an

underdeveloped regulatory environment,

where minority interests can be overlooke

��

23

Emaar Properties PJSC Real Estate 20 February 2008

���

Emaar income statement (in AEDmn, except for per share data)

Year to December 2005a 2006a 2007a 2008e 2009e 2010e 2011e 2012e

Sale of Land 4,082.7 8,154.5 1,357.5 - - - - - Sale of Villas and Condominiums

4,153.1 5,240.7 16,188.5 19,961.7 27,142.1 27,619.6 28,999.1 40,579.6

Sale of Commercial Units - 410.9 - - - - - - Rental Income 125.6 199.4 - 997.2 2,371.8 2,694.6 3,306.3 4,415.3 Hotel Revenue - - - 447.4 718.6 1,778.1 1,864.8 1,955.8 Revenue 8,361.4 14,005.5 17,546.1 21,406.3 30,232.5 32,092.2 34,170.2 46,950.7 Cost of Land (1,604.0) (3,527.7) (163.5) - - - - - Cost of Villas & Condominiums

(1,963.5) (3,368.3) (10,477.0) (13,315.2) (17,816.3) (18,737.6) (19,166.6) (25,143.4)

Direct Rental Expenses (18.2) (12.8) - (99.7) (237.2) (269.5) (330.6) (441.5) Hotel Direct Costs - - - (246.1) (395.2) (977.9) (1,025.6) (1,075.7) (3,585.7) (7,039.4) (10,640.5) (13,661.0) (18,448.7) (19,985.0) (20,522.9) (26,660.6) % of sales 43% 50% 61% 64% 61% 62% 60% 57% Gross Profit 4,775.7 6,966.1 6,905.5 7,745.3 11,783.8 12,107.2 13,647.3 20,290.0 Margin 57% 50% 39% 36% 39% 38% 40% 43% Operating Expenses: SGA Expenses (1,021.8) (1,400.4) (2,119.0) (2,140.6) (3,325.6) (3,530.1) (3,758.7) (5,164.6) Other Operating Income 247.6 383.5 382.2 428.1 604.7 641.8 683.4 939.0 Other Income - - - 214.1 302.3 320.9 341.7 469.5 Other Operating Expenses (66.0) (207.0) - - - - - - Operating Expenses (840.2) (1,224.0) (1,736.8) (1,498.4) (2,418.6) (2,567.4) (2,733.6) (3,756.1) EBIT (incl Revaluation Gain) 3,935.5 5,742.1 5,168.7 6,246.9 9,365.2 9,539.8 10,913.7 16,534.0 Margin 47% 41% 29% 29% 31% 30% 32% 35% Net Financing cost 326.1 274.4 148.0 (139.5) (172.7) (91.7) 61.3 392.9 Other fin. Income/charges 122.5 253.3 811.6 - - - - - Associate Income 99.1 128.1 402.0 679.5 1,653.7 2,460.3 2,956.7 3,540.1 Gain on Disposal of Subsidiary

245.8 4.9 - - - - - -

Profit before Taxes 4,729.1 6,402.8 6,530.2 6,786.8 10,846.2 11,908.4 13,931.7 20,467.0 Income Taxes - -(47.1) (13.9) (67.9) (325.4) (595.4) (696.6) (1,023.3) Minority Shareholders’ Interest

2.2 15.4 (38.8) 46.2 189.4 377.9 609.1 920.7

Net Profit (Loss) 4,731.2 6,371.1 6,477.6 6,672.8 10,331.4 10,935.1 12,626.0 18,522.9 Margin 57% 46% 37% 31% 34% 34% 37% 39% Appropriation of Net Income Basic EPS 0.8 1.1 1.1 1.1 1.7 1.8 2.1 3.0 Number of shares 5,565.3 5,988.4 6,091.2 6,091.2 6,091.2 6,091.2 6,091.2 6,091.2 Fully Diluted EPS 0.8 1.1 1.1 1.1 1.7 1.8 2.1 3.0 Fully Diluted Shares 5,565.3 5,988.4 6,091.2 6,091.2 6,091.2 6,091.2 6,091.2 6,091.2

Source: Company reports, HSBC estimates

��

24

Emaar Properties PJSC Real Estate 20 February 2008

���

Emaar balance sheet (in AEDmn)

Year to December 2005a 2006a 2007a 2008e 2009e 2010e 2011e 2012e

Current Assets Cash and Cash Equivalents 10368.0 2329.3 6799.4 2635.5 4858.7 9902.9 19274.5 39626.3 Trade & Other Receivables 717.5 600.9 825.9 865.4 2156.8 330.4 165.2 0.0 Receivable from Project Finance 0.0 0.0 0.0 0.0 0.0 0.0 0.0 0.0 Development Properties 3025.8 11121.4 18269.0 20242.0 19582.1 23906.8 23071.5 17358.5 Development Work in Progress 0.0 0.0 0.0 0.0 0.0 0.0 0.0 0.0 Short term investment 2047.1 1518.6 1752.9 1752.9 1752.9 1752.9 1752.9 1752.9 Current Assets 18087 19129 30270 28119 30973 38516 46887 61360 Investments in Associates 3366.8 7043.5 8892.6 9572.1 11225.8 13686.1 16642.8 20182.8 Long Term Investments 1555.8 973.3 183.7 183.7 183.7 183.7 183.7 183.7 Long Term Assets/ Non Current 5317.9 8444.4 9492.2 10171.7 11825.4 14285.7 17242.3 20782.4 Intangible asset 0.0 2962.0 2962.0 2962.0 2962.0 2962.0 2962.0 2962.0 Hotels 0.0 0.0 0.0 1024.4 1895.4 1801.8 1712.9 1628.3 Property, Plant and Equipment 1875.6 4184.6 7109.2 7294.5 7470.7 7638.2 7797.4 7948.7 Investment Properties 6924.5 6970.5 4918.5 8623.3 10084.7 11654.2 13065.1 14442.0 Permanent 8800.1 14117.0 14989.7 19904.2 22412.8 24056.2 25537.3 26981.0 Total Assets 32204.7 41690.1 54751.8 58194.4 65211.4 76857.6 89666.5 109123.9 LIABILITIES Trade & Other Payables 5527.6 6265.4 8747.4 6997.9 5248.5 7891.1 9709.1 12251.7 Notes Payable 733.1 875.8 1005.2 723.7 304.0 60.8 3.6 0.0 Current Liabilities 6260.7 7141.3 9752.6 7721.7 5552.4 7951.9 9712.7 12251.7 Borrowing & long term debt 238.7 3992.2 8395.9 8395.9 8395.9 8395.9 8395.9 8395.9 Provision for employee services 9.0 12.0 16.3 16.3 16.3 16.3 16.3 16.3 Long Term Liabilities/Non current

247.7 4004.2 8412.3 8412.3 8412.3 8412.3 8412.3 8412.3

Minority Interest in Subsidiaries 135.4 565.9 702.6 748.7 938.2 1316.1 1925.2 2845.9 Paid - Up Capital 5780.2 6075.6 6091.2 6091.2 6091.2 6091.2 6091.2 6091.2 Statutory & Other Reserves 13922.7 14669.1 15197.7 15197.7 15197.7 15197.7 15197.7 15197.7 Retained Earnings 5862.5 9237.0 14596.9 20024.2 29021.0 37889.8 48328.8 64326.5 Shareholder’s Equity 25696.3 30544.7 36586.9 42060.4 51246.7 60493.4 71541.5 88459.9 Total Liabilities and Equity 32204.7 41690.1 54751.8 58194.4 65211.4 76857.6 89666.5 109123.9

Source: Company reports, HSBC estimates

��

25

Emaar Properties PJSC Real Estate 20 February 2008

���

Emaar cash flow statement (in AEDmn)

Year to December 2005a 2006a 2007a 2008e 2009e 2010e 2011e 2012e

Operating Activities: Net Profit before Minorities 4,729.1 6,355.7 3,266.9 6,719.0 10,520.8 11,313.0 13,235.1 19,443.6 Depreciation & amortization 99.0 118.0 77.2 734.2 925.2 1,029.3 1,105.8 1,179.8 Change in Working Capital 1,554.5 (3,491.2) (1,396.7) (4,043.3) (2,800.8) (98.8) 2,761.4 8,417.1 Interest Income & Exp - - - 139.5 172.7 91.7 (61.3) (392.9) Interest Recd - - - 175.3 79.2 160.2 313.1 644.8 Interest Paid - - - (314.8) (251.9) (251.9) (251.9) (251.9) Provision for employee end of service benefits

1.6 3.0 3.1 - - - - -

Net cash generated from operating activities

6,065.7 2,882.2 1,586.9 3,409.8 8,645.2 12,243.4 17,102.3 29,040.6

Investments activities: Capex (Excl Hotel Properties) (1,475.2) (2,501.4) (2,055.0) (4,598.3) (2,486.3) (2,672.7) (2,586.9) (2,623.5) Additions to Hotels Properties - - - (1,050.5) (947.5) - - - Additions to Investment Properties

(263.3) (183.7) - - - - - -

Associates (2,350.1) (3,387.9) (649.3) (679.5) (1,653.7) (2,460.3) (2,956.7) (3,540.1) Subsidiary (150.8) (4,223.4) (249.5) - - - - - Additions to Development WIP - - - - - - - - Acquisition/ sale of financial assets

(1,344.7) 152.8 623.0 - - - - -

Movement in >3 months bank deposits

(1,152.3) 252.2 (835.9) - - - - -

Net cash generated from investment activities

(6,736.5) (11,360.6) (3,166.6) (6,328.2) (5,087.5) (5,133.0) (5,543.6) (6,163.6)

Financing activities: Dividends paid (340.3) (2,355.2) (1,189.1) (1,245.5) (1,334.6) (2,066.3) (2,187.0) (2,525.2) Share issue 8,077.6 1,478.3 79.9 - - - - - Bank Borrowings Raised - 5,133.0 5,299.1 - - - - - Net Share Issuance Fee - - - - - - - - Borrowings Repaid (400.0) (3,567.0) (1,626.0) - - - - - Others 134.9 (5.2) 4.1 - - - - - -

- - - - - - - -

Net cash generated from financing activities

7,472.1 683.9 2,567.9 (1,245.5) (1,334.6) (2,066.3) (2,187.0) (2,525.2)

Net addition (deduction) in cash

6,801.4 (7,794.4) 988.1 (4,163.8) 2,223.2 5,044.2 9,371.6 20,351.8

Cash at beginning of fiscal year - - 6,799.4 6,799.4 2,635.6 4,858.7 9,902.9 19,274.5 Cash at end of fiscal year - - 7,787.5 2,635.6 4,858.7 9,902.9 19,274.5 39,626.4

Source: Company reports, HSBC estimates

��

26

Emaar Properties PJSC Real Estate 20 February 2008

���

��

27

Emaar Properties PJSC Real Estate 20 February 2008

���

Analyst certification The following analyst(s), who is(are) primarily responsible for this report, certifies(y) that the opinion(s) on the subject security(ies) or issuer(s) and any other views or forecasts expressed herein accurately reflect their personal view(s) and that no part of their compensation was, is or will be directly or indirectly related to the specific recommendation(s) or views contained in this research report: Walid Khalfallah and Majed Azzam

Important disclosures

Stock ratings and basis for financial analysis HSBC believes that investors utilise various disciplines and investment horizons when making investment decisions, which depend largely on individual circumstances such as the investor’s existing holdings, risk tolerance and other considerations. Given these differences, HSBC has two principal aims in its equity research: 1) to identify long-term investment opportunities based on particular themes or ideas that may affect the future earnings or cash flows of companies on a 12 month time horizon; and 2) from time to time to identify short-term investment opportunities that are derived from fundamental, quantitative, technical or event-driven techniques on a 0-3 month time horizon and which may differ from our long-term investment rating. HSBC has assigned ratings for its long-term investment opportunities as described below.

This report addresses only the long-term investment opportunities of the companies referred to in the report. As and when HSBC publishes a short-term trading idea the stocks to which these relate are identified on the website at www.hsbcnet.com/research. Details of these short-term investment opportunities can be found under the Reports section of this website.

HSBC believes an investor’s decision to buy or sell a stock should depend on individual circumstances such as the investor’s existing holdings and other considerations. Different securities firms use a variety of ratings terms as well as different rating systems to describe their recommendations. Investors should carefully read the definitions of the ratings used in each research report. In addition, because research reports contain more complete information concerning the analysts’ views, investors should carefully read the entire research report and should not infer its contents from the rating. In any case, ratings should not be used or relied on in isolation as investment advice.

Rating definitions for long-term investment opportunities

Stock ratings HSBC assigns ratings to its stocks in this sector on the following basis:

For each stock we set a required rate of return calculated from the risk free rate for that stock’s domestic, or as appropriate, regional market and the relevant equity risk premium established by our strategy team. The price target for a stock represents the value the analyst expects the stock to reach over our performance horizon. The performance horizon is 12 months. For a stock to be classified as Overweight, the implied return must exceed the required return by at least 5 percentage points over the next 12 months (or 10 percentage points for a stock classified as Volatile*). For a stock to be classified as Underweight, the stock must be expected to underperform its required return by at least 5 percentage points over the next 12 months (or 10 percentage points for a stock classified as Volatile*). Stocks between these bands are classified as Neutral.

Our ratings are re-calibrated against these bands at the time of any ’material change’ (initiation of coverage, change of volatility status or change in price target). Notwithstanding this, and although ratings are subject to ongoing management review, expected returns will be permitted to move outside the bands as a result of normal share price fluctuations without necessarily triggering a rating change.

��

28

Emaar Properties PJSC Real Estate 20 February 2008

���

*A stock will be classified as volatile if its historical volatility has exceeded 40%, if the stock has been listed for less than 12 months (unless it is in an industry or sector where volatility is low) or if the analyst expects significant volatility. However, stocks which we do not consider volatile may in fact also behave in such a way. Historical volatility is defined as the past month’s average of the daily 365-day moving average volatilities. In order to avoid misleadingly frequent changes in rating, however, volatility has to move 2.5 percentage points past the 40% benchmark in either direction for a stock’s status to change.

Prior to this, from 7 June 2005 HSBC applied a ratings structure which ranked the stocks according to their notional target price vs current market price and then categorised (approximately) the top 40% as Overweight, the next 40% as Neutral and the last 20% as Underweight. The performance horizon is 2 years. The notional target price was defined as the mid-point of the analysts’ valuation for a stock.

From 15 November 2004 to 7 June 2005, HSBC carried no ratings and concentrated on long-term thematic reports which identified themes and trends in industries, but did not make a conclusion as to the investment action that potential investors should take.

Prior to 15 November 2004, HSBC’s ratings system was based upon a two-stage recommendation structure: a combination of the analysts’ view on the stock relative to its sector and the sector call relative to the market, together giving a view on the stock relative to the market. The sector call was the responsibility of the strategy team, set in co-operation with the analysts. For other companies, HSBC showed a recommendation relative to the market. The performance horizon was 6-12 months. The target price was the level the stock should have traded at if the market accepted the analysts’ view of the stock.

Rating distribution for long-term investment opportunities

As of 19 February 2008, the distribution of all ratings published is as follows: Overweight (Buy) 55% (22% of these provided with Investment Banking Services)