Embed Size (px)

DESCRIPTION

EPRI Studies of IGCC Impacts – Emissions, Economics and Status. APPA New Generation Workshop August 1, 2007 Portland, Oregon Stu Dalton ([email protected]) Director, Generation. Other Wind Nuclear Coal Combustion Turbine Combined Cycle Retirements. 1999. 2001. 2003. 2005. 2007. - PowerPoint PPT Presentation

Citation preview

EPRI Studies of IGCC Impacts – Emissions, Economics and Status

APPA New Generation Workshop

August 1, 2007

Portland, Oregon

Stu Dalton ([email protected])Director, Generation

2© 2007 Electric Power Research Institute, Inc. All rights reserved.

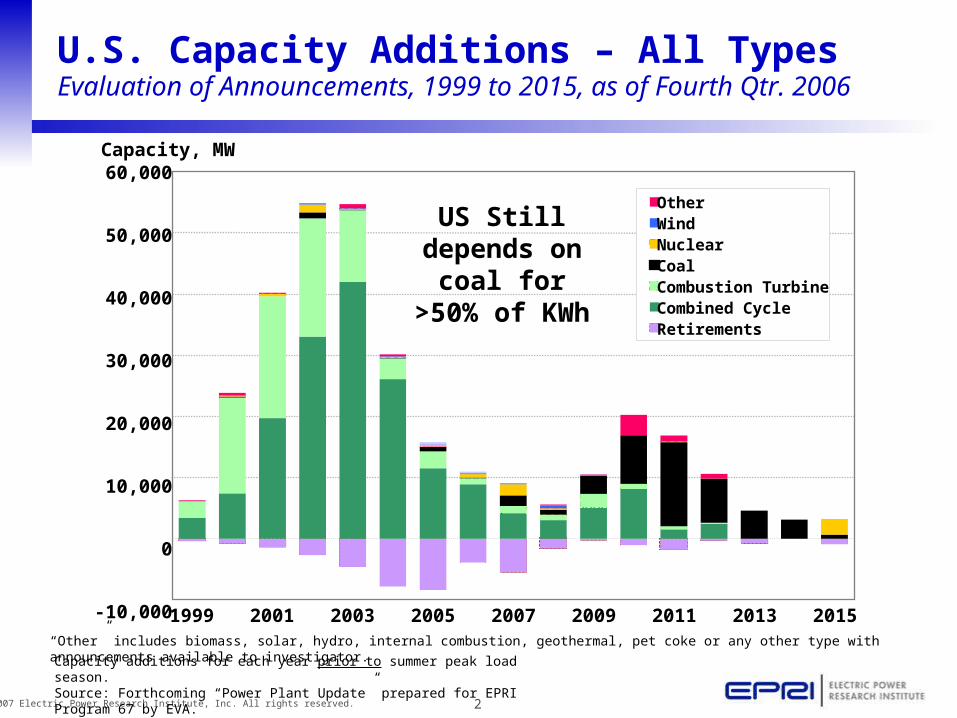

U.S. Capacity Additions – All TypesEvaluation of Announcements, 1999 to 2015, as of Fourth Qtr. 2006

OtherWindNuclearCoalCombustion TurbineCombined CycleRetirements

1999 2001 2003 2005 2007 2009 2011 2013 2015

60,000

50,000

40,000

30,000

20,000

10,000

0

-10,000

Capacity, MW

US Still depends on

coal for >50% of KWh

“Other” includes biomass, solar, hydro, internal combustion, geothermal, pet coke or any other type with announcements available to investigator.

Capacity additions for each year prior to summer peak load season.Source: Forthcoming “Power Plant Update” prepared for EPRI Program 67 by EVA.

3© 2007 Electric Power Research Institute, Inc. All rights reserved.

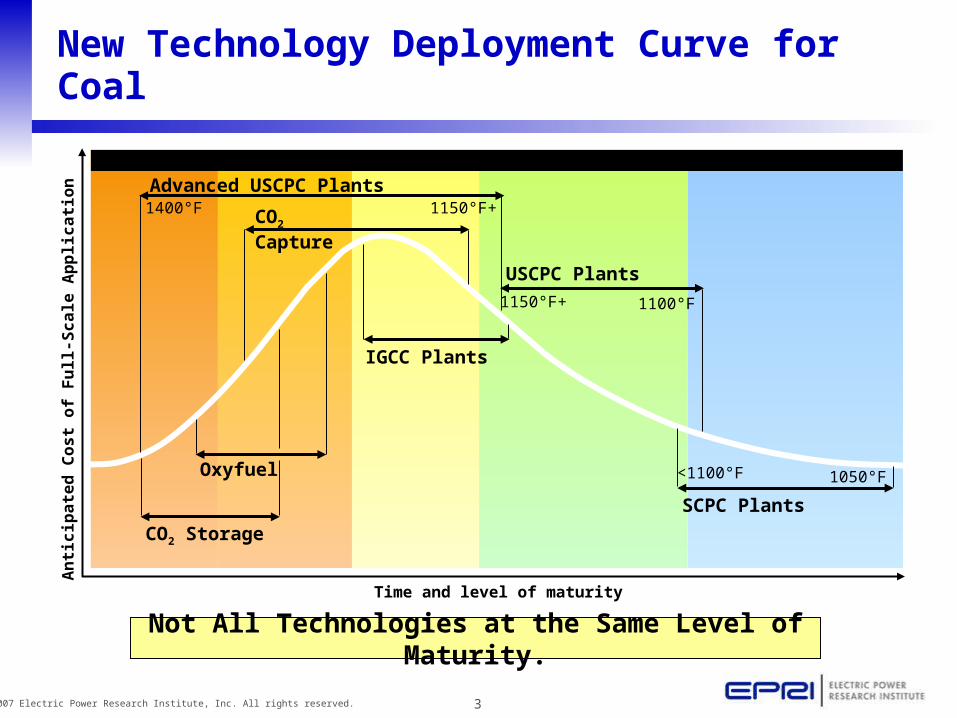

Research Development Demonstration Deployment Mature Technology

Time and level of maturity

An

tic

ipa

ted

Co

st

of

Fu

ll-S

ca

le A

pp

lic

ati

on

New Technology Deployment Curve for Coal

Not All Technologies at the Same Level of Maturity.

Oxyfuel

CO2 Storage

CO2 Capture

IGCC Plants

USCPC Plants

SCPC Plants

1150°F+ 1100°F

<1100°F 1050°F

Advanced USCPC Plants1150°F+1400°F

4© 2007 Electric Power Research Institute, Inc. All rights reserved.

No

n-

Re

gu

late

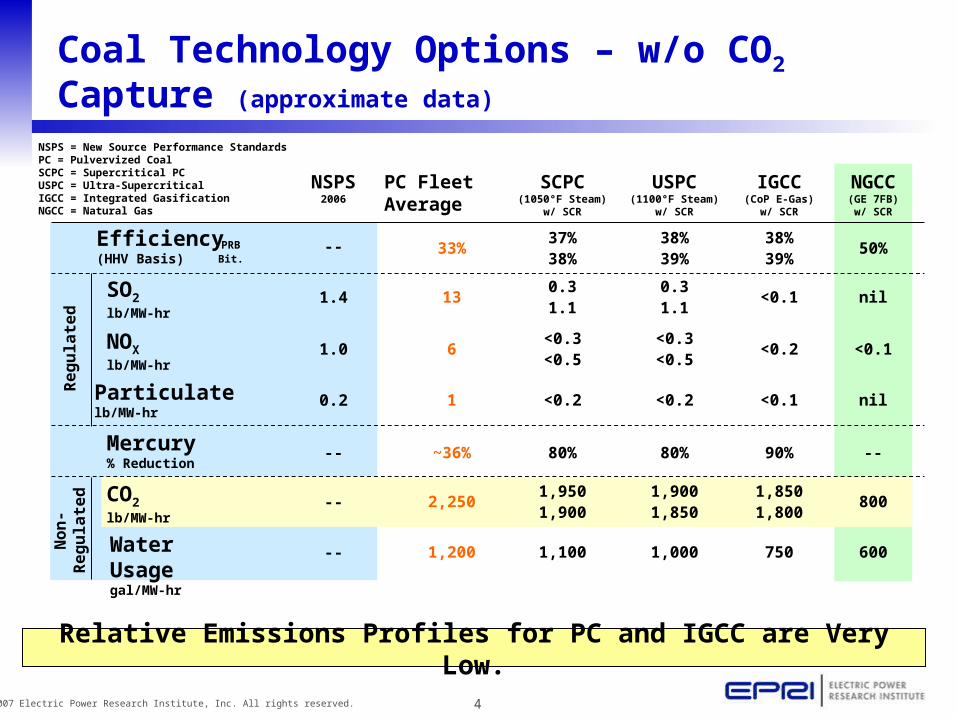

dCoal Technology Options – w/o CO2 Capture (approximate data)

PRBBit.

Water Usagegal/MW-hr

Mercury% Reduction

Re

gu

late

d

Efficiency(HHV Basis)

SO2lb/MW-hr

NOXlb/MW-hr

Particulatelb/MW-hr

CO2lb/MW-hr

Relative Emissions Profiles for PC and IGCC are Very Low.

PC FleetAverage

33%

13

6

1

2,250

~36%

1,200

IGCC(CoP E-Gas)

w/ SCR

38%39%

<0.1

<0.2

<0.1

1,8501,800

90%

750

USPC(1100°F Steam)

w/ SCR

38%39%

0.31.1

<0.3<0.5

<0.2

1,9001,850

80%

1,000

NGCC(GE 7FB)w/ SCR

50%

nil

<0.1

nil

800

--

600

SCPC(1050°F Steam)

w/ SCR

37%38%

0.31.1

<0.3<0.5

<0.2

1,9501,900

80%

1,100

NSPS = New Source Performance StandardsPC = Pulvervized CoalSCPC = Supercritical PCUSPC = Ultra-SupercriticalIGCC = Integrated GasificationNGCC = Natural Gas

NSPS2006

--

1.4

1.0

0.2

--

--

--

5© 2007 Electric Power Research Institute, Inc. All rights reserved.

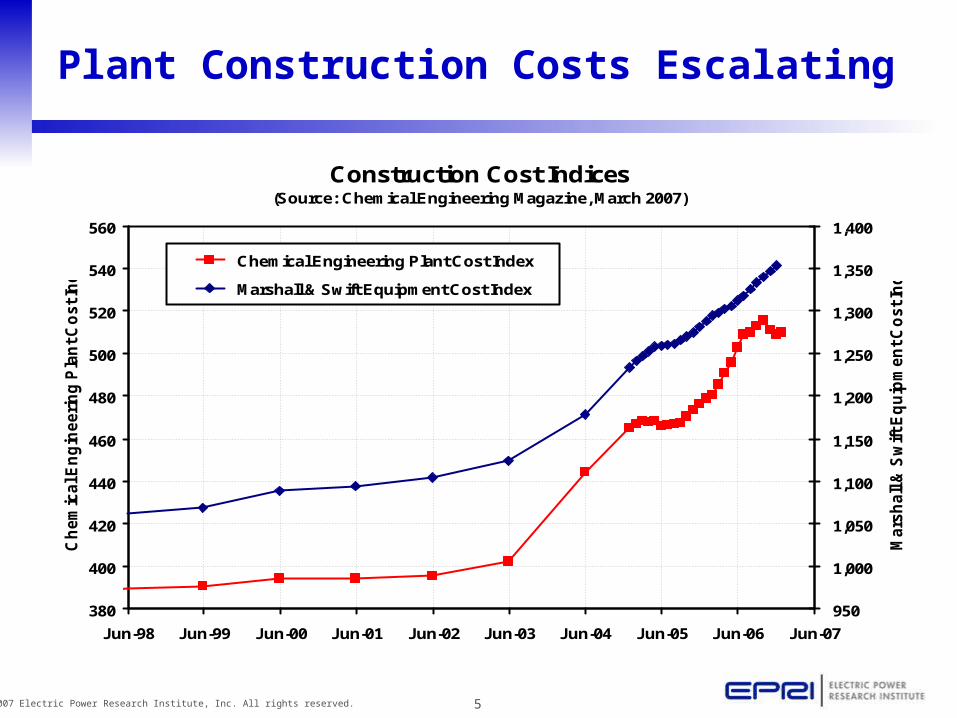

Plant Construction Costs Escalating

Construction Cost Indices(Source: Chemical Engineering Magazine, March 2007)

380

400

420

440

460

480

500

520

540

560

Jun-98 Jun-99 Jun-00 Jun-01 Jun-02 Jun-03 Jun-04 Jun-05 Jun-06 Jun-07

Ch

em

ical E

ng

ineeri

ng

Pla

nt C

ost In

dex

950

1,000

1,050

1,100

1,150

1,200

1,250

1,300

1,350

1,400

Mars

hall

& S

wift E

qu

ipm

en

t C

ost In

dex Chemical Engineering Plant Cost Index

Marshall & Swift Equipment Cost Index

6© 2007 Electric Power Research Institute, Inc. All rights reserved.

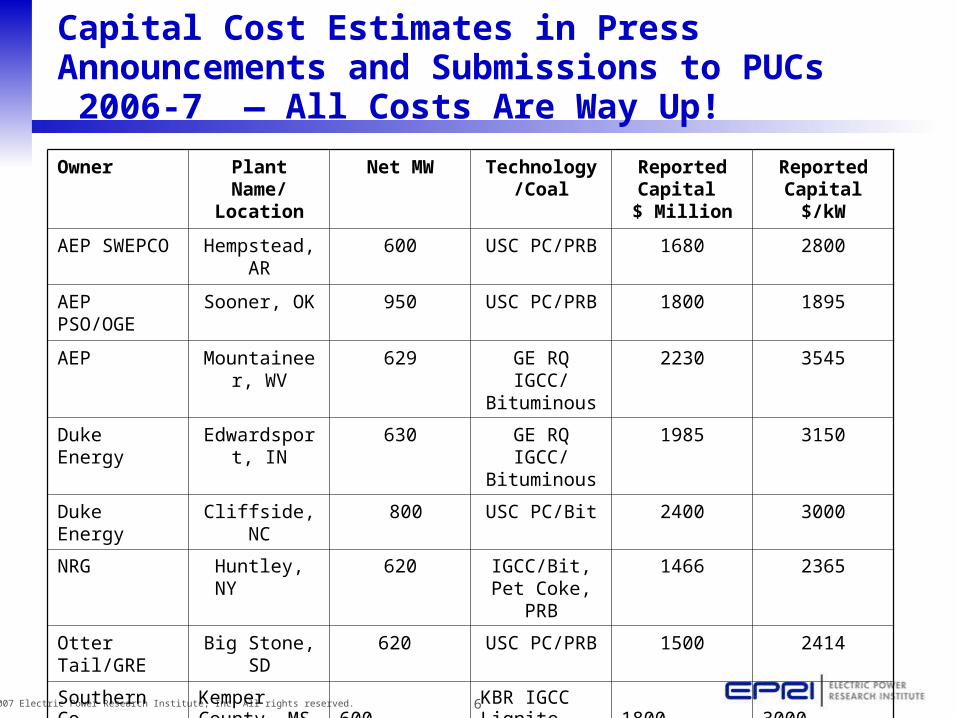

Capital Cost Estimates in Press Announcements and Submissions to PUCs 2006-7 — All Costs Are Way Up!

Owner Plant Name/ Location

Net MW Technology/Coal

Reported Capital $ Million

Reported Capital $/kW

AEP SWEPCO

Hempstead, AR

600 USC PC/PRB 1680 2800

AEP PSO/OGE

Sooner, OK 950 USC PC/PRB 1800 1895

AEP Mountaineer, WV

629 GE RQ IGCC/ Bituminous

2230 3545

Duke Energy Edwardsport, IN

630 GE RQ IGCC/ Bituminous

1985 3150

Duke Energy Cliffside, NC 800 USC PC/Bit 2400 3000

NRG Huntley, NY

620 IGCC/Bit, Pet Coke, PRB

1466 2365

Otter Tail/GRE

Big Stone, SD 620 USC PC/PRB 1500 2414

Southern Co Kemper County, MS

600 KBR IGCC Lignite

1800 3000

7© 2007 Electric Power Research Institute, Inc. All rights reserved.

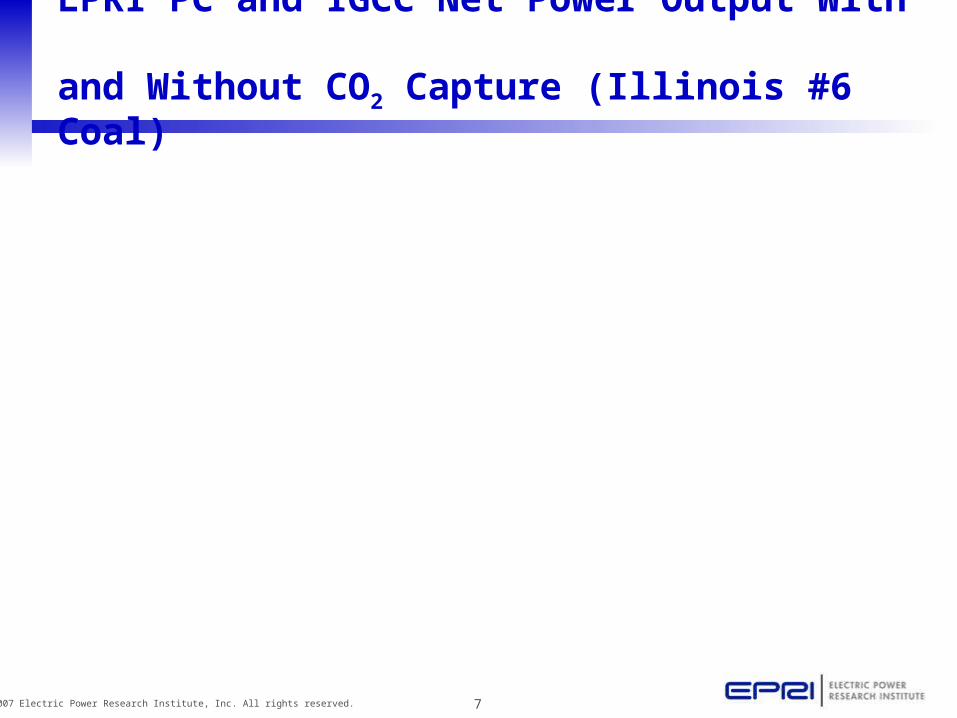

EPRI PC and IGCC Net Power Output With and Without CO2 Capture (Illinois #6 Coal)EPRI PC and IGCC Net Power Output

With and Without CO2 Capture (Illinois #6 Coal)

0

100

200

300

400

500

600

700

800

SupercriticalPC

GE RadiantQuench

GE TotalQuench

Shell GasQuench

E-Gas FSQ

Net

Po

wer

Ou

tpu

t, M

We

.

No Capture

Retrofit Capture

New Capture

8© 2007 Electric Power Research Institute, Inc. All rights reserved.

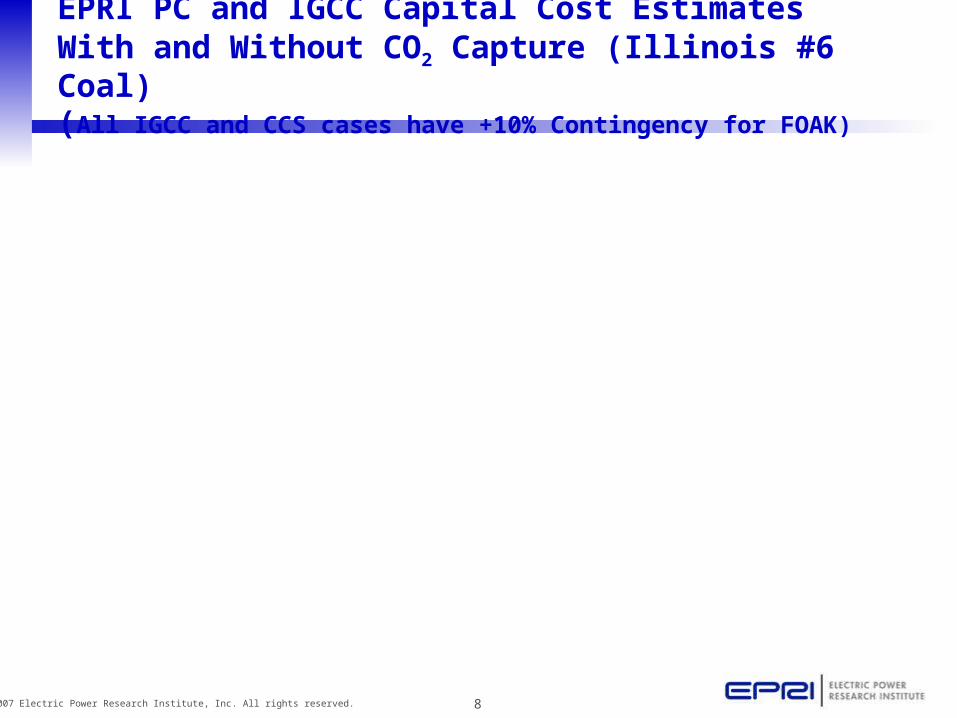

EPRI PC and IGCC Capital Cost EstimatesWith and Without CO2 Capture (Illinois #6 Coal)(All IGCC and CCS cases have +10% Contingency for FOAK)EPRI 600 MW (net) PC and IGCC Capital Cost Estimates

With and Without CO2 Capture (Illinois #6 Coal)

1,500

2,000

2,500

3,000

3,500

4,000

4,500

5,000

SupercriticalPC

GE RadiantQuench

GE TotalQuench

Shell GasQuench

E-Gas FSQ

To

tal

Cap

ital

Req

uir

emen

t, $

/kW

(20

06$)

.

No Capture

Retrofit Capture

New Capture

9© 2007 Electric Power Research Institute, Inc. All rights reserved.

EPRI PC and IGCC Cost of ElectricityWith and Without CO2 Capture (Illinois #6 Coal)(All IGCC and CCS cases have +10% TPC Contingency for FOAK)EPRI 600 MW (net) PC and IGCC Cost of Electricity

With and Without CO2 Capture (Illinois #6 Coal)

40

50

60

70

80

90

100

110

120

130

SupercriticalPC

GE RadiantQuench

GE TotalQuench

Shell GasQuench

E-Gas FSQ

30-Y

r le

veli

zed

CO

E,

$/M

Wh

(C

on

stan

t 20

06$)

.

No Capture

Retrofit Capture

New Capture

COE Includes $10/tonne for CO2 Transportation and Sequestration

10© 2007 Electric Power Research Institute, Inc. All rights reserved.

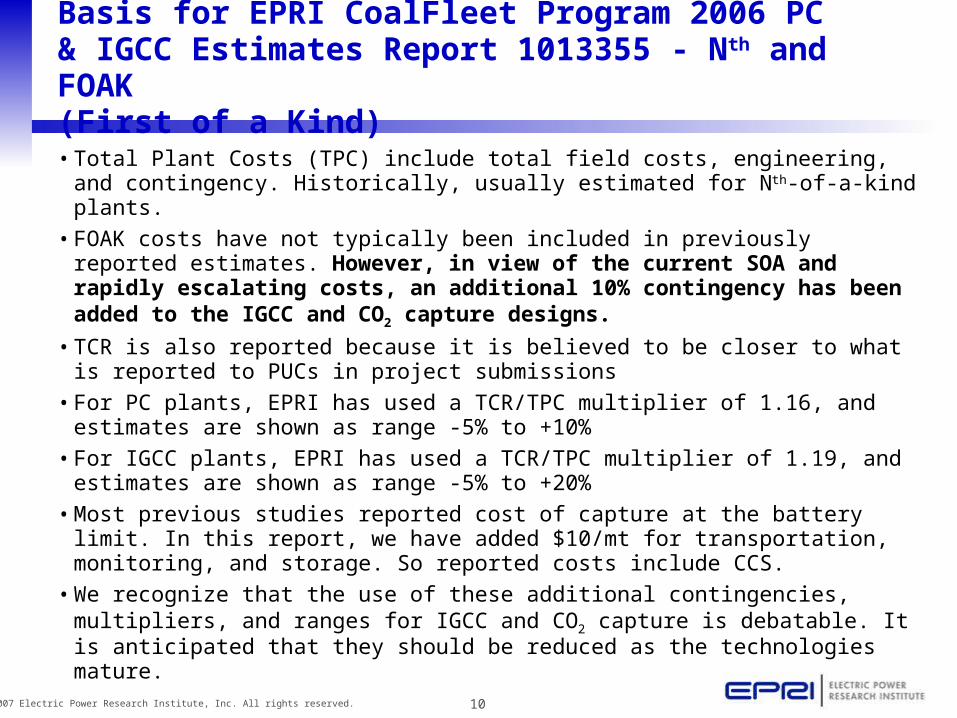

Basis for EPRI CoalFleet Program 2006 PC & IGCC Estimates Report 1013355 - Nth and FOAK (First of a Kind)

• Total Plant Costs (TPC) include total field costs, engineering, and contingency. Historically, usually estimated for Nth-of-a-kind plants.

• FOAK costs have not typically been included in previously reported estimates. However, in view of the current SOA and rapidly escalating costs, an additional 10% contingency has been added to the IGCC and CO2 capture designs.

• TCR is also reported because it is believed to be closer to what is reported to PUCs in project submissions

• For PC plants, EPRI has used a TCR/TPC multiplier of 1.16, and estimates are shown as range -5% to +10%

• For IGCC plants, EPRI has used a TCR/TPC multiplier of 1.19, and estimates are shown as range -5% to +20%

• Most previous studies reported cost of capture at the battery limit. In this report, we have added $10/mt for transportation, monitoring, and storage. So reported costs include CCS.

• We recognize that the use of these additional contingencies, multipliers, and ranges for IGCC and CO2 capture is debatable. It is anticipated that they should be reduced as the technologies mature.

11© 2007 Electric Power Research Institute, Inc. All rights reserved.

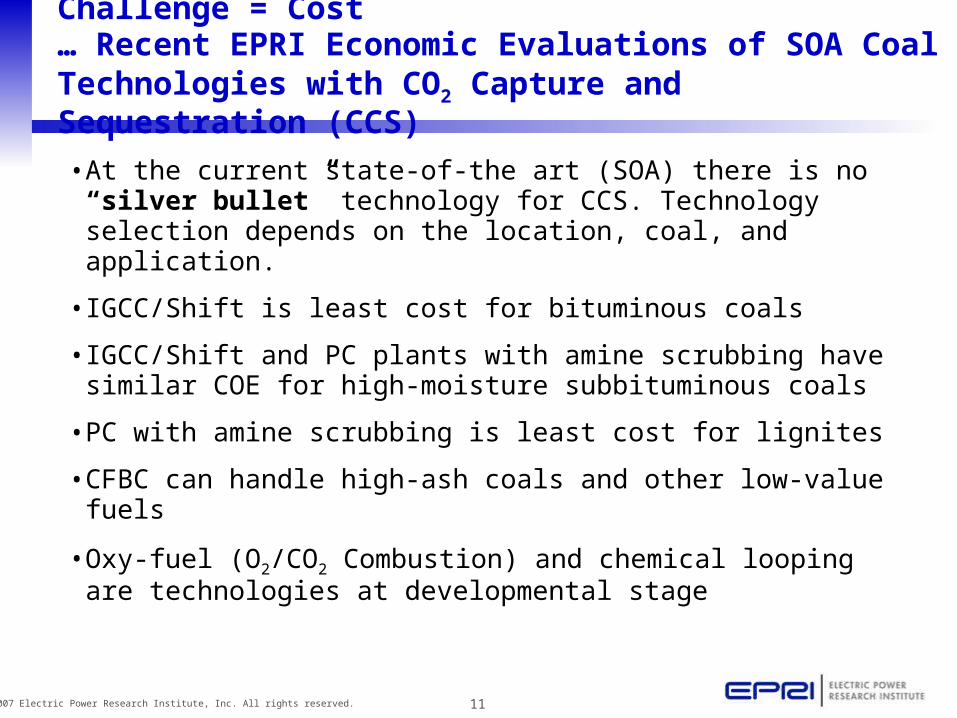

Challenge = Cost… Recent EPRI Economic Evaluations of SOA Coal Technologies with CO2 Capture and Sequestration (CCS)

• At the current state-of-the art (SOA) there is no “silver bullet” technology for CCS. Technology selection depends on the location, coal, and application.

• IGCC/Shift is least cost for bituminous coals

• IGCC/Shift and PC plants with amine scrubbing have similar COE for high-moisture subbituminous coals

• PC with amine scrubbing is least cost for lignites

• CFBC can handle high-ash coals and other low-value fuels

• Oxy-fuel (O2/CO2 Combustion) and chemical looping are technologies at developmental stage

12© 2007 Electric Power Research Institute, Inc. All rights reserved.

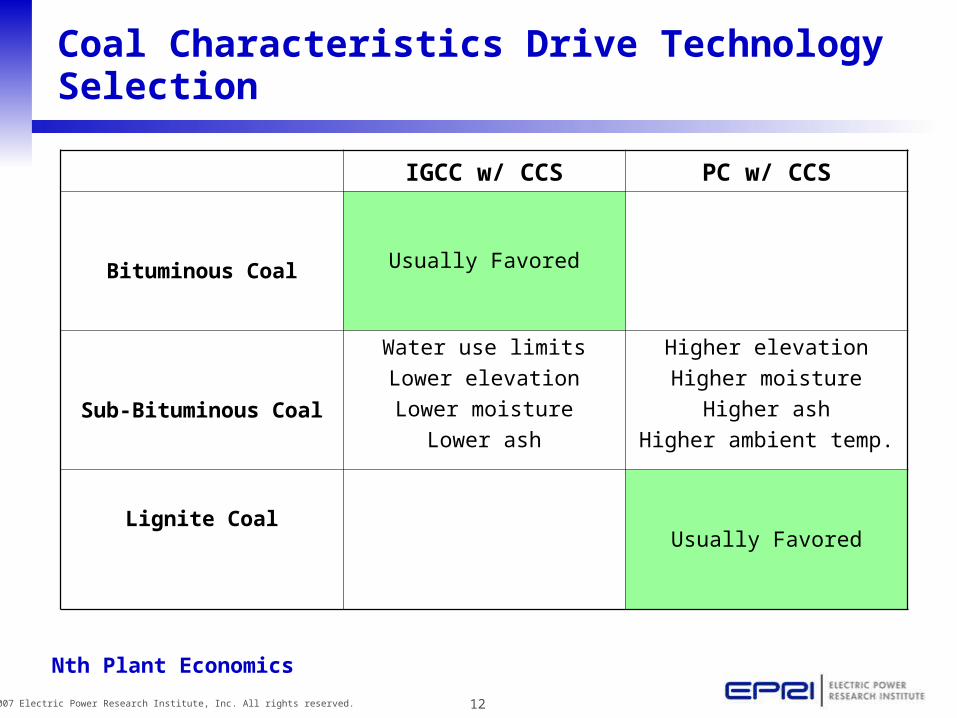

Coal Characteristics Drive Technology Selection

IGCC w/ CCS PC w/ CCS

Bituminous Coal Usually Favored

Sub-Bituminous Coal

Water use limits

Lower elevation

Lower moisture

Lower ash

Higher elevation

Higher moisture

Higher ash

Higher ambient temp.

Lignite CoalUsually Favored

Nth Plant Economics

13© 2007 Electric Power Research Institute, Inc. All rights reserved.

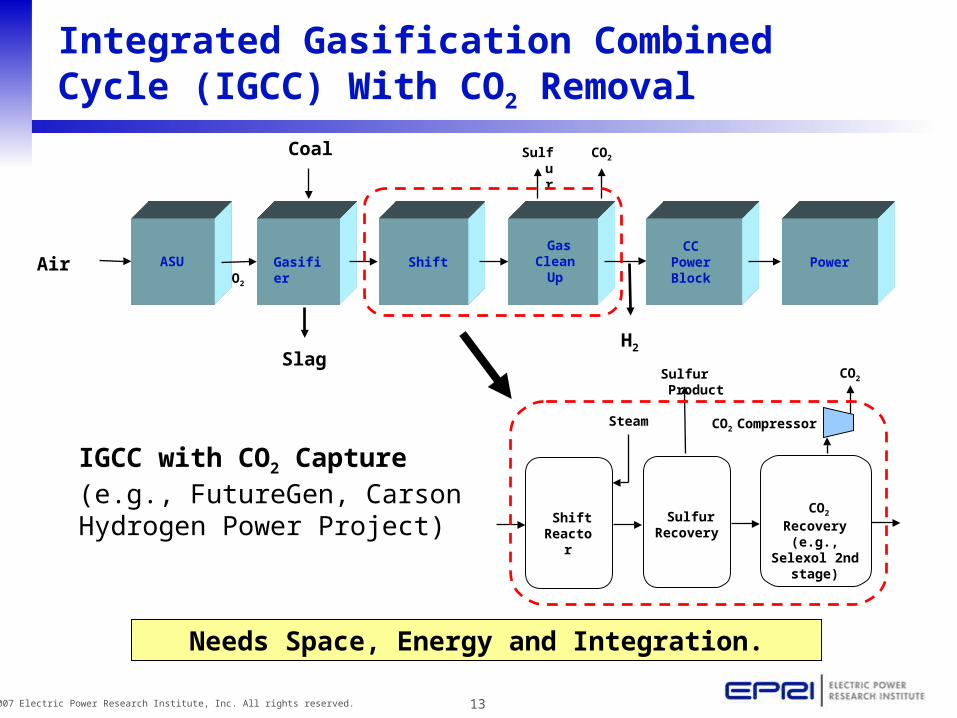

Integrated Gasification Combined Cycle (IGCC) With CO2 Removal

ASU Gasifier GasClean

Up

CCPowerBlock

Air

Sulfur

PowerO2

Coal

Slag

Shift

CO2

H2

ShiftReactor

SulfurRecovery

CO2

Recovery(e.g., Selexol 2nd stage)

Steam

Sulfur Product CO2

CO2 Compressor

IGCC with CO2 Capture(e.g., FutureGen, Carson Hydrogen Power Project)

Needs Space, Energy and Integration.

14© 2007 Electric Power Research Institute, Inc. All rights reserved.

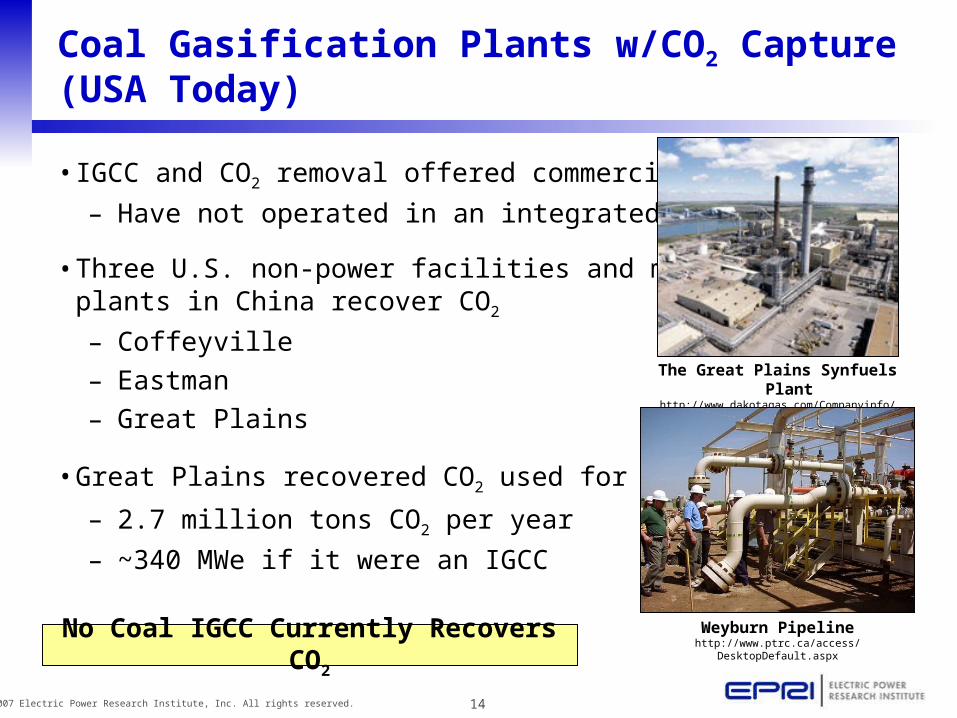

Coal Gasification Plants w/CO2 Capture (USA Today)

• IGCC and CO2 removal offered commercially:

– Have not operated in an integrated manner

• Three U.S. non-power facilities and many plants in China recover CO2

– Coffeyville

– Eastman

– Great Plains

• Great Plains recovered CO2 used for EOR:

– 2.7 million tons CO2 per year

– ~340 MWe if it were an IGCC

The Great Plains Synfuels Planthttp://www.dakotagas.com/Companyinfo/index.html

Weyburn Pipelinehttp://www.ptrc.ca/access/DesktopDefault.aspxNo Coal IGCC Currently Recovers CO2

15© 2007 Electric Power Research Institute, Inc. All rights reserved.

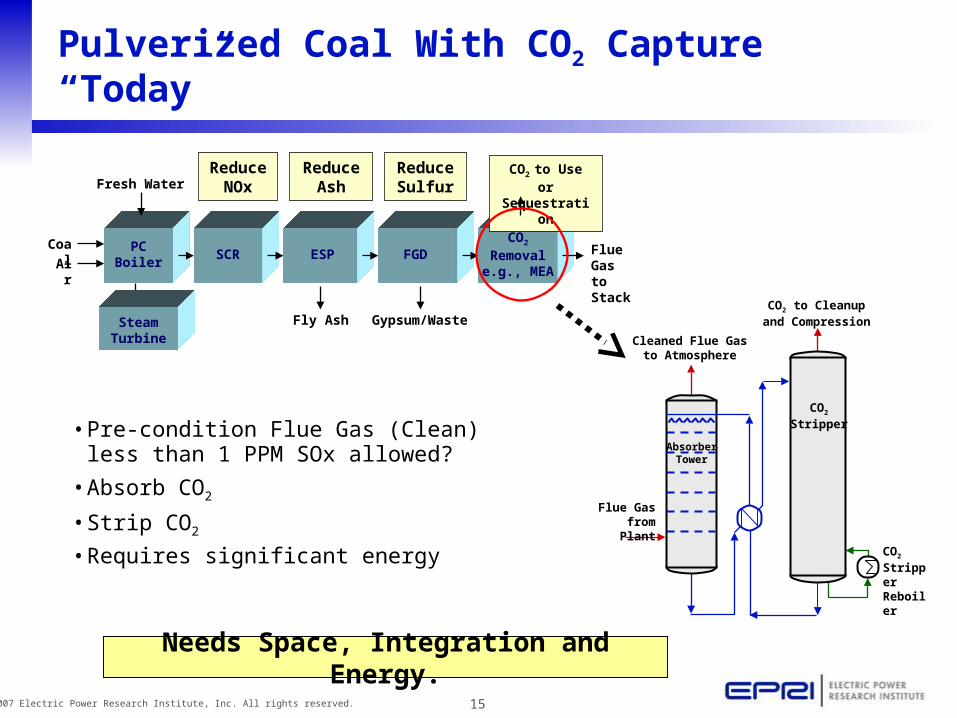

Pulverized Coal With CO2 Capture “Today”

Needs Space, Integration and Energy.

• Pre-condition Flue Gas (Clean) less than 1 PPM SOx allowed?

• Absorb CO2

• Strip CO2

• Requires significant energy

Fresh Water

PCBoiler

SCR

SteamTurbine

ESP FGDCO2

Removale.g., MEA

CO2 to Use or Sequestration

Flue Gasto Stack

Fly Ash Gypsum/Waste

Coal

Air

CO2 to Cleanupand Compression

Cleaned Flue Gas to Atmosphere

Absorber Tower

CO2 Stripper Reboiler

Flue Gas from Plant

CO2

Stripper

ReduceSulfur

ReduceAsh

ReduceNOx

16© 2007 Electric Power Research Institute, Inc. All rights reserved.

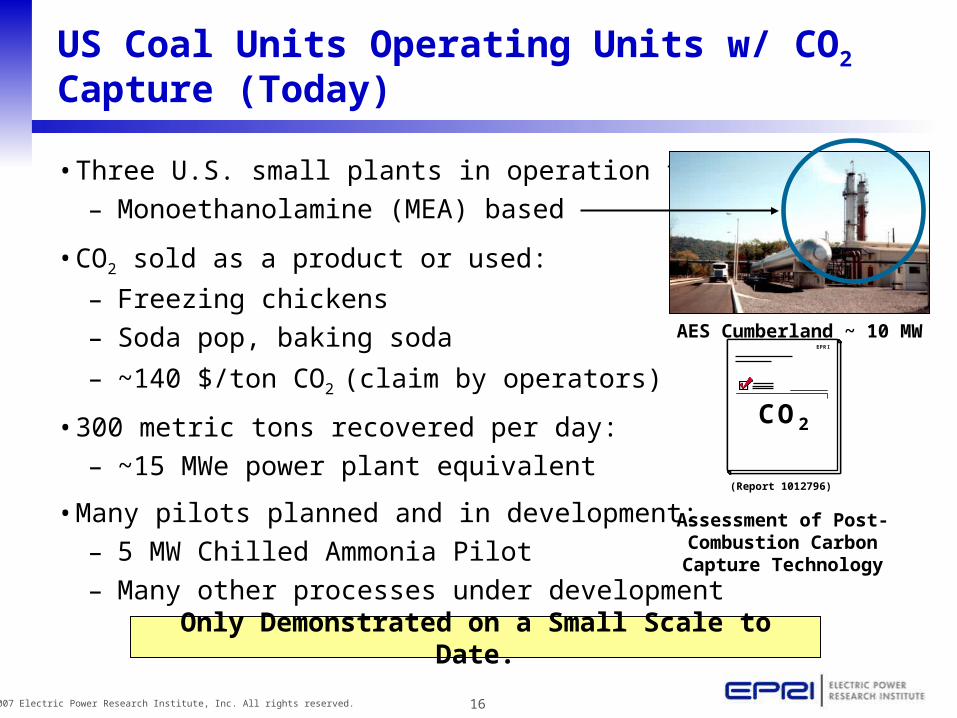

US Coal Units Operating Units w/ CO2 Capture (Today)

• Three U.S. small plants in operation today:

– Monoethanolamine (MEA) based

• CO2 sold as a product or used:

– Freezing chickens

– Soda pop, baking soda

– ~140 $/ton CO2 (claim by operators)

• 300 metric tons recovered per day:

– ~15 MWe power plant equivalent

• Many pilots planned and in development:

– 5 MW Chilled Ammonia Pilot

– Many other processes under development

AES Cumberland ~ 10 MW

Assessment of Post-Combustion Carbon Capture Technology

(Report 1012796)

Only Demonstrated on a Small Scale to Date.

EPRI

CO2

EPRIEPRIEPRI

CO2

17© 2007 Electric Power Research Institute, Inc. All rights reserved.

Challenge- Regulatory Uncertainty on CO2 Emissions

• Kyoto Signatory Countries post 2012. New G-8 Proposals

• New Motion in Australia, EU

• US proposed Federal legislation Intense in Washington – MANY bills

• US Regional Initiatives

– Western Regional Climate Action (WA,OR,CA,AZ, and NM). Western Governors Association (WGA)

– RGGI – East Coast Regional GHG Initiative (10 NE States)

– Powering the Plains (ND,SD,IA,MN,WI, Manitoba)

• California, Washington - others…

– New long term base load power or renewal (>5years) commitments shall have CO2 emissions no greater than NGCC (established as <1100 lbs/MWh ~ 500 kg/MWh).

• Liability of CO2 injection into geological formations? New questions with BP “Carson Hydrogen Power Project” project in California

18© 2007 Electric Power Research Institute, Inc. All rights reserved.

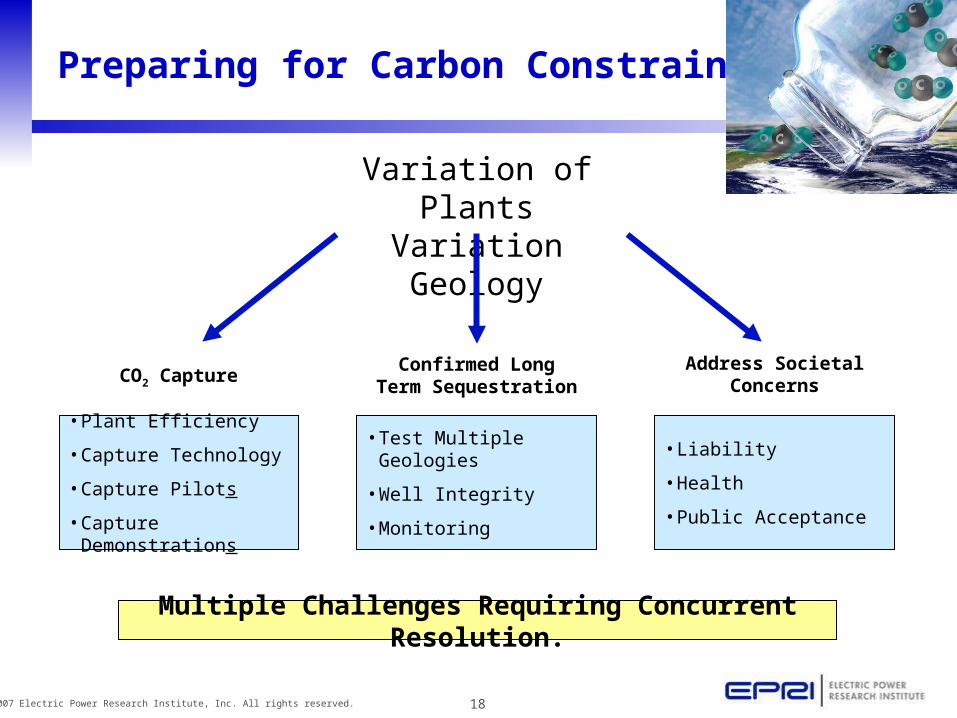

Preparing for Carbon Constraints

Variation of Plants Variation Geology

CO2 Capture

• Plant Efficiency

• Capture Technology

• Capture Pilots

• Capture Demonstrations

Confirmed Long Term Sequestration

• Test Multiple Geologies

• Well Integrity

• Monitoring

Address Societal Concerns

• Liability

• Health

• Public Acceptance

Multiple Challenges Requiring Concurrent Resolution.

19© 2007 Electric Power Research Institute, Inc. All rights reserved.

CoalFleet for Tomorrow is an International Collaboration on Clean Coal including CO2 Capture

• Participants from 5 continents , Asia, Australia, Europe, Africa, North America (2/3 of all coal fired in NA)

• Best design guides developed by industry for industry

• Power Producers, Suppliers, Rail, Coal, engineering firms, Governmental entities

• Many of the leading “early deployment” firms working with us to assure successful designs that meet the performance and operational goals

• New plants starting to look at designs for CO2 capture and integration

20© 2007 Electric Power Research Institute, Inc. All rights reserved.

CoalFleet Participants Span 5 Continents >60% of U.S. Coal-Based Generation, Large European Generators,Major OEMs (50 & 60 Hz) and EPCs, CEC, U.S. DOE

Doosan Heavy Industries (Korea) Duke Energy Corp. Dynegy EdF (France) Edison International Edison Mission Energy Endesa (Spain) ENEL (Italy) Entergy E.ON UK E.ON US ESKOM (South Africa) Exelon Corp. FPL GE Energy (USA) Golden Valley Electrical Assoc.

Alliant Energy Corp. Alstom Power Ameren Services Company American Electric Power Arkansas Electric Coop. Austin Energy Babcock & Wilcox Company Bechtel Corp. BP Alternative Energy International California Energy Commission ConocoPhillips Technology Consumers Energy CPS Energy CSX Transportation Dairyland Power Coop.

21© 2007 Electric Power Research Institute, Inc. All rights reserved.

CoalFleet Participants Span 5 Continents (cont’d)

Great River Energy Hoosier Energy Integrys Energy Group (WPS) Jacksonville Electric Authority Kansas City Power & Light Kellogg Brown & Root (KBR) Lincoln Electric System Midwest Generation Minnesota Power Mitsubishi Heavy Industries (MHI) Nebraska Public Power District New York Power Authority Oglethorpe Power PacifiCorp PNM Resources Portland General Electric

Pratt & Whitney Rocketdyne Richmond Power & Light Rio Tinto Salt River Project Siemens Southern California Edison Southern Company Stanwell Corporation TransCanada Pipelines Limited Tri-State G&T TVA TXU U.S. DOE (NETL) We Energies Wolverine Power Xcel Energy

22© 2007 Electric Power Research Institute, Inc. All rights reserved.

What’s Next – What’s Needed for Coal

• Acceleration of the Industry efforts worldwide in addition to governmental efforts – new pilots, demonstrations, initiatives

• Cost reductions and efficiency improvements for the underlying technology

• Three “strata” of certainty/understanding

– Political/siting, economic, technical

23© 2007 Electric Power Research Institute, Inc. All rights reserved.

Backup sides

24© 2007 Electric Power Research Institute, Inc. All rights reserved.

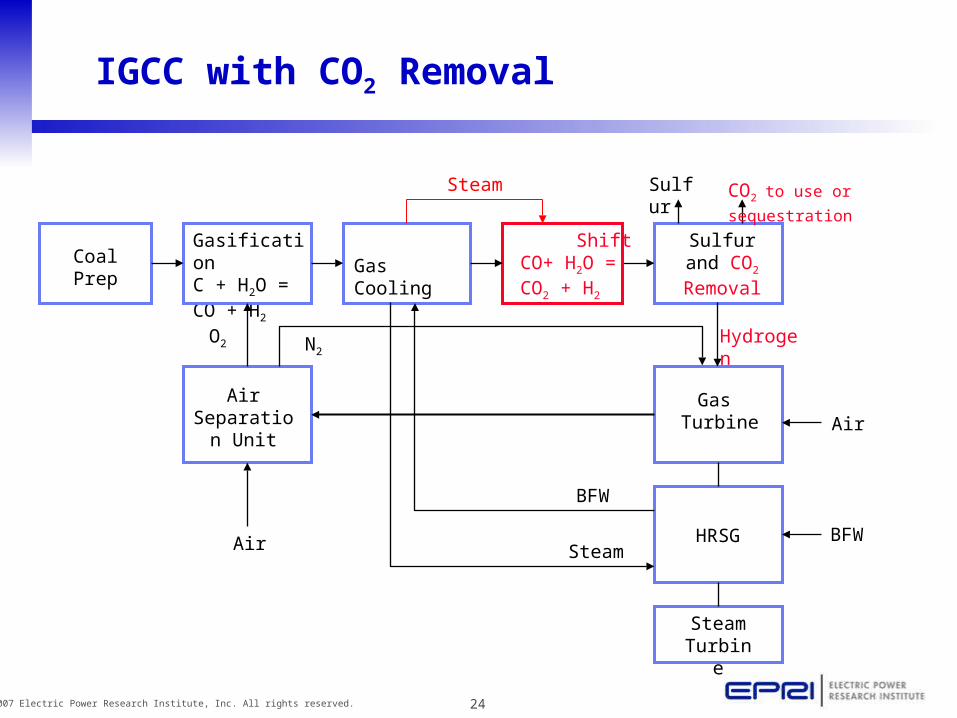

IGCC with CO2 Removal

O2 N2

Air

BFW

BFWSteam

Steam Turbine

HRSG

CoalPrep

Gas CoolingGasificationC + H2O = CO + H2

Sulfur and CO2

Removal

Air Separation

Unit

Gas Turbine

Air

Hydrogen

CO2 to use or sequestrationSulfur

ShiftCO+ H2O = CO2 + H2

Steam

25© 2007 Electric Power Research Institute, Inc. All rights reserved.

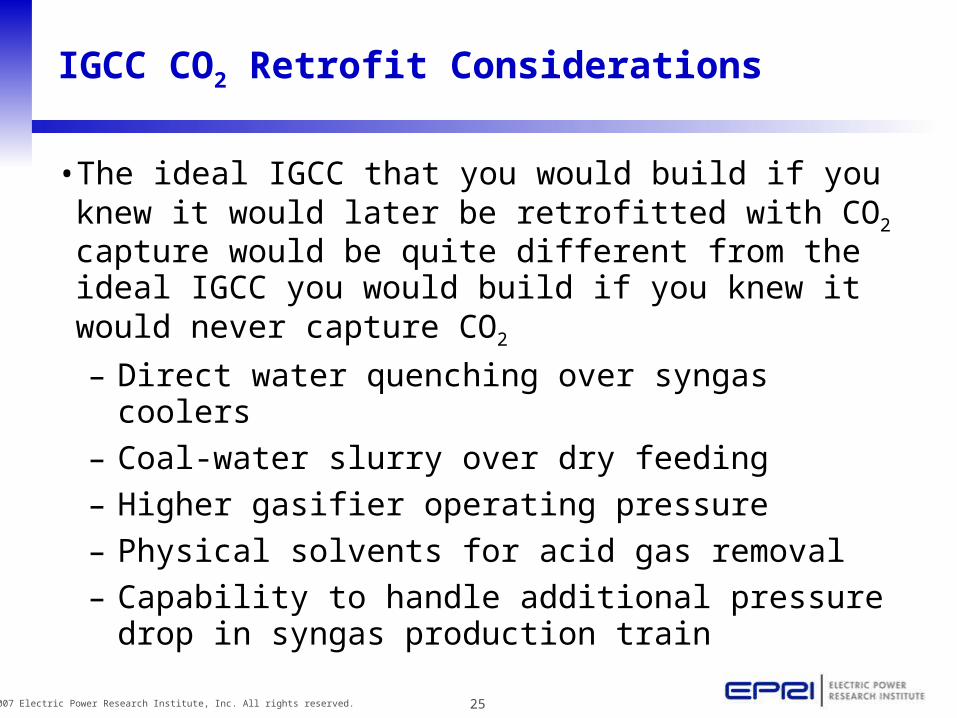

IGCC CO2 Retrofit Considerations

• The ideal IGCC that you would build if you knew it would later be retrofitted with CO2 capture would be quite different from the ideal IGCC you would build if you knew it would never capture CO2

– Direct water quenching over syngas coolers

– Coal-water slurry over dry feeding

– Higher gasifier operating pressure

– Physical solvents for acid gas removal

– Capability to handle additional pressure drop in syngas production train

26© 2007 Electric Power Research Institute, Inc. All rights reserved.

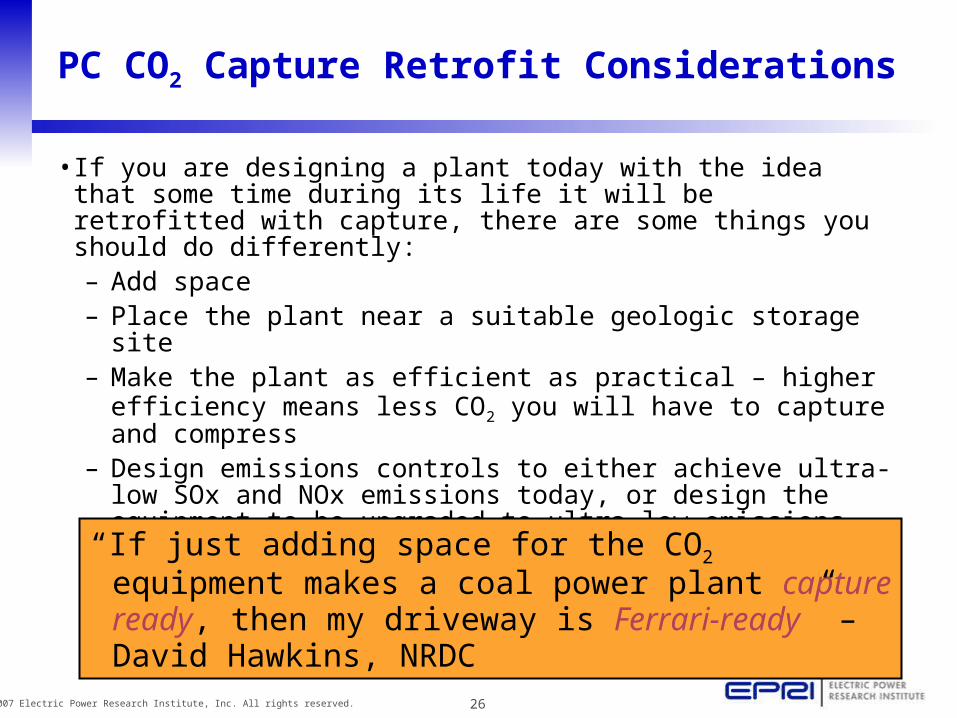

PC CO2 Capture Retrofit Considerations

• If you are designing a plant today with the idea that some time during its life it will be retrofitted with capture, there are some things you should do differently:– Add space – Place the plant near a suitable geologic storage site– Make the plant as efficient as practical – higher efficiency

means less CO2 you will have to capture and compress– Design emissions controls to either achieve ultra-low SOx

and NOx emissions today, or design the equipment to be upgraded to ultra-low emissions

– Design steam turbine to accommodate very large extraction of low pressure steam for solvent regeneration“If just adding space for the CO2 equipment makes a coal power plant capture ready, then my driveway is Ferrari-ready” – David Hawkins, NRDC

27© 2007 Electric Power Research Institute, Inc. All rights reserved.

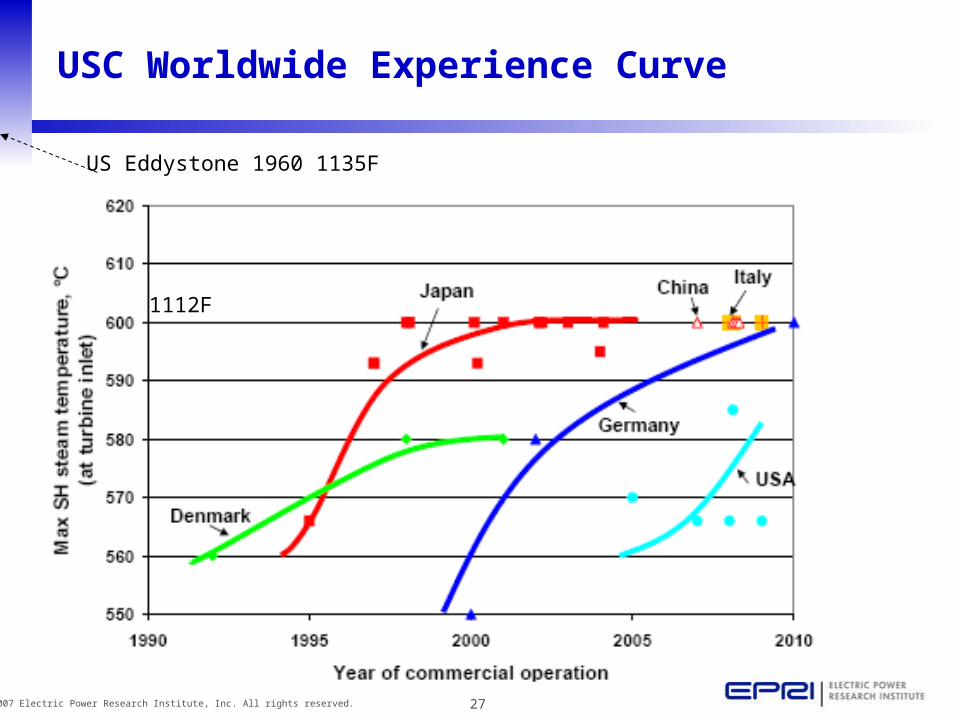

USC Worldwide Experience Curve

US Eddystone 1960 1135F

1112F

28© 2007 Electric Power Research Institute, Inc. All rights reserved.

Total Plant Cost ($/kW) Plant Net Efficiency (HHV Basis)

2005 2010 2015 2020 2025 2030

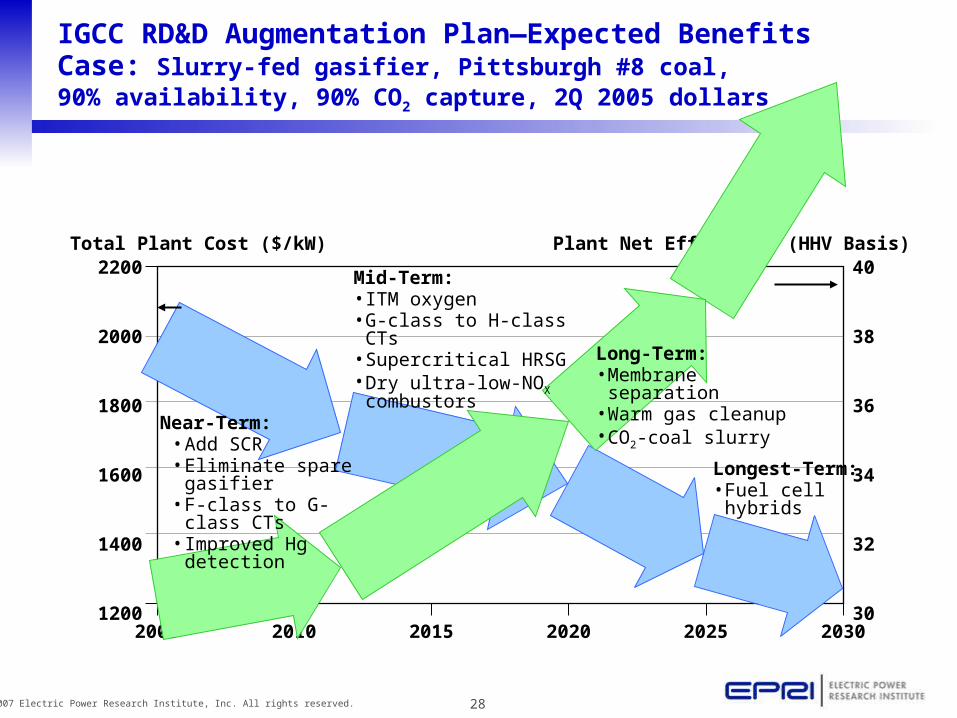

IGCC RD&D Augmentation Plan—Expected Benefits Case: Slurry-fed gasifier, Pittsburgh #8 coal, 90% availability, 90% CO2 capture, 2Q 2005 dollars

2200

2000

1800

1600

1400

1200

40

38

36

34

32

30

Long-Term:• Membrane separation• Warm gas cleanup• CO2-coal slurry

Mid-Term:• ITM oxygen• G-class to H-class CTs• Supercritical HRSG• Dry ultra-low-NOX

combustors

Longest-Term:• Fuel cell

hybrids

Near-Term:• Add SCR• Eliminate spare

gasifier• F-class to G-class CTs• Improved Hg detection

29© 2007 Electric Power Research Institute, Inc. All rights reserved.

Total Plant Cost ($/kW) Plant Net Efficiency (HHV Basis)

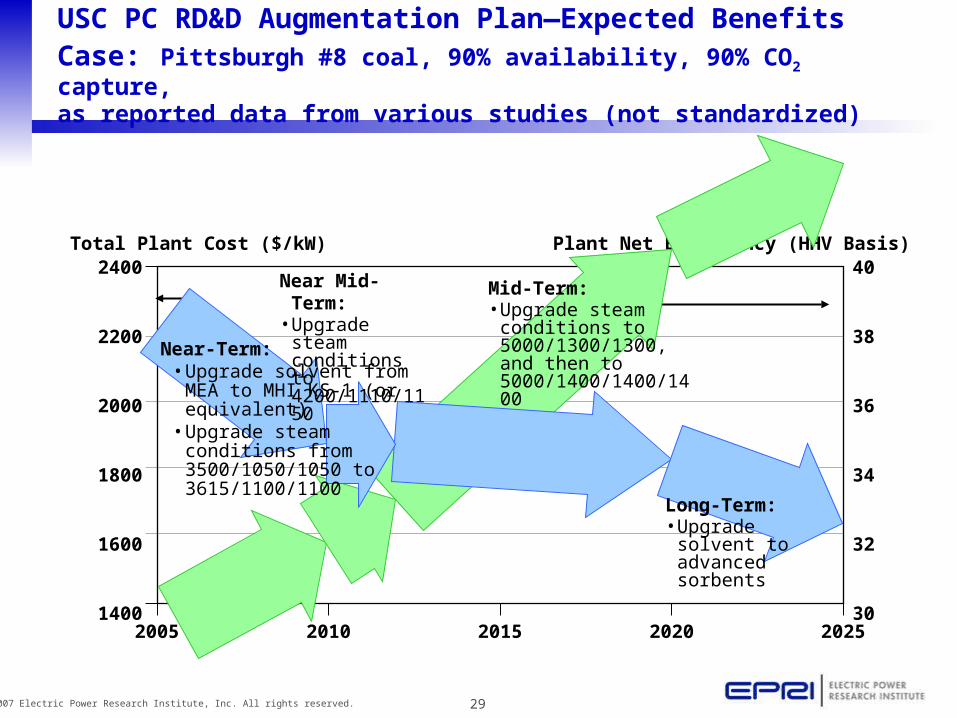

USC PC RD&D Augmentation Plan—Expected Benefits Case: Pittsburgh #8 coal, 90% availability, 90% CO2 capture, as reported data from various studies (not standardized)

2400

2200

2000

1800

1600

14002005 2010 2015 2020 2025

40

38

36

34

32

30

Near Mid-Term:• Upgrade steam

conditions to 4200/1110/1150

Mid-Term:• Upgrade steam

conditions to 5000/1300/1300, and then to 5000/1400/1400/1400

Near-Term:• Upgrade solvent from MEA

to MHI KS-1 (or equivalent)• Upgrade steam conditions

from 3500/1050/1050 to 3615/1100/1100

Long-Term:• Upgrade solvent

to advanced sorbents

30© 2007 Electric Power Research Institute, Inc. All rights reserved.

EPRI’s CoalFleet forTomorrow Program

• Build an industry-led program toaccelerate the deployment ofadvanced coal-based power plants;members now span five continents

• Employ “learning by doing” approach; generalize actual deployment projects (50 & 60 Hz) to create design guides

• Augment ongoing RD&D to speed marketintroduction of improved designs and materials

• Deliver benefits of standardization to IGCC (integration gasification combined cycle), USC PC (ultra-supercritical pulverized-coal), and SC CFBC (supercritical circulating fluidized-bed combustion)– Lower costs, especially with CO2 capture– High reliability– Near-zero SOX, NOX, and PM emissions– Shorter project schedule– Easier financing and insuring

Further information availableat www.epri.com/coalfleet