Embed Size (px)

Citation preview

Entrepreneurship: Owning Your Own Business

Focus Questions

What are four advantages of being an entrepreneur?

What are three forms of business organization?

What is a limited liability company (LLC)?

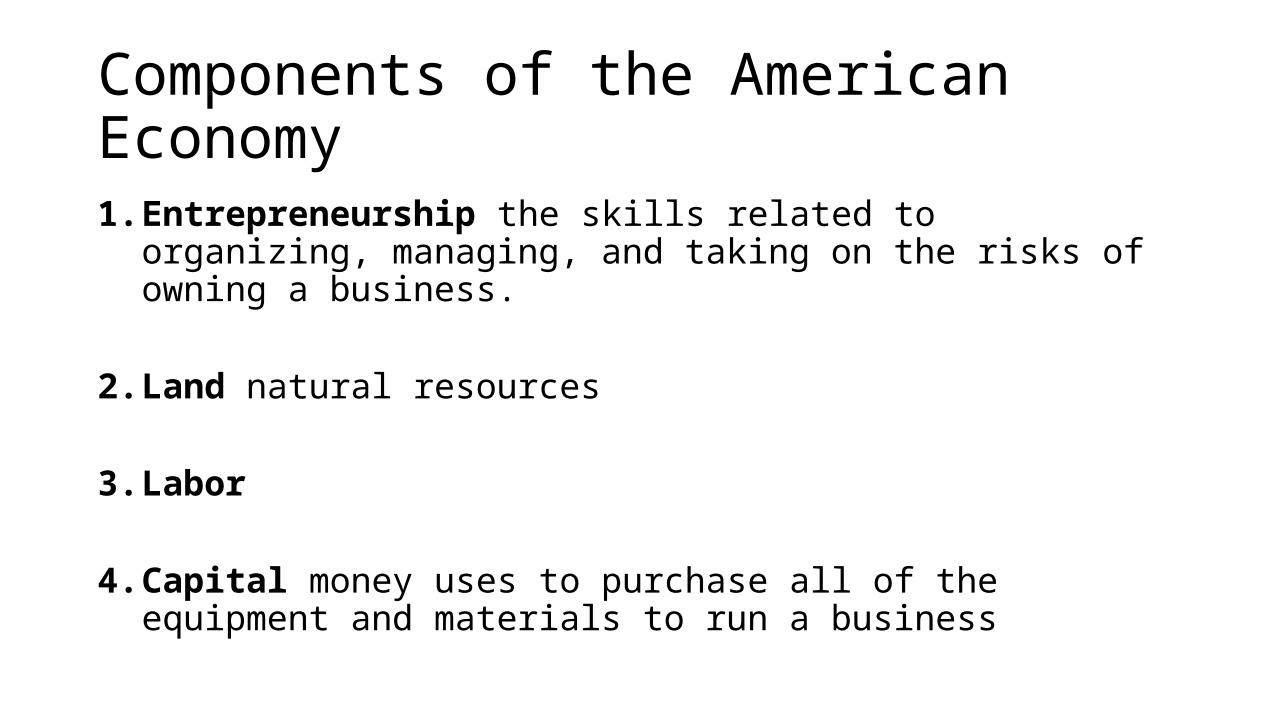

Components of the American Economy1. Entrepreneurship the skills related to organizing, managing, and

taking on the risks of owning a business.

2. Land natural resources

3. Labor

4. Capital money uses to purchase all of the equipment and materials to run a business

Entrepreneurs plan, organize, and manage their businesses, expecting to earn profits.

Advantages of Entrepreneurship

Being the boss and owning your company can be very satisfying

You can set your work hours You make all the decisionsFinancial securityYou can leave the business to children or others

Disadvantages

• Is there a big enough market?

• You need a business plan

• Not a nine to five job

• Great chance of failure

Do you have what it takes?

How well do you plan and organize?

How good are you making decisions?

How well do you get along with different personalities?

Do you have the physical and emotional stamina to run a business?

How will the business affect your family?

Are you willing to keep an open mind and keep on learning?

Do you have the passion to stick with it and make it work?

Types of Business Opportunities

• Take over a family business

• Purchase an existing business

• Start your own business

• Purchase a franchise

• A franchise is a legal contract that allows you to operate a business in the name of a recognized company

• The company is known as the franchisor

• Franchisee the person who operates a franchise

Forms of Business Organizations

Sole Proprietorship a business owned by one person

Simple tax form (Schedule C)

Pay both employee’s and employer’s portion of FICA and Medicare

Responsible for business related obligations

Partnerships

Partnerships a business co – owned by two or more individuals

General partners share assets, profits, liabilities (debts and obligations of the business), voting rights, and management responsibilities

Limited partners do not have voting rights and they are not held responsible for company liabilities beyond the amount of their investment

Silent partners invest in the company but have no say in its management

A partnership agreement defines the type of relationship and spells out the details

Advantages of Partnerships over Sole Proprietorship• Easier to raise capital

•More expertise and greater range of knowledge

• As easy to set up

• Costs, risks, and workload are shared

Disadvantages of Partnerships

• All general partners are liable for the debts and obligations

• Partners may disagree about management and operational procedures

• Partners may have different business goals or time frames

• Potential for personal disputes

Corporations

A legal entity that can own property, acquire debt, sue, and be sued

Stockholders and a board of directors own the corporation and control its business

Stockholders’ liability is limited to the amount of their investment

Ownership is transferred by buying or selling stock

A corporation may enter into contracts, obtain loans, and continue to exist even after its stockholders die or transfer their shares to others

Unless limited by its articles of incorporation (the primary rules governing the management of a corporation) or by state law, a corporation continues indefinitely

Limited Liability Company (LLC)

New type of corporate arrangement (not a true corporation)

Owners have limited personal liability for the debts and actions of the company

Steps in Forming a Corporation

File articles of incorporation with the state where you wish to incorporate

Write bylaws that govern its operation

Hold a meeting of the board of directors

Issue stock to stockholders

Finally a corporation has to meet standards of bookkeeping, maintain its own bank accounts, and the accounts of their employees